Issued on 24 July 2012 Responses due by 18 … · Issued on 24 July 2012 Prior to finalising the...

40

Market Consultation Issued on 24 July 2012 Responses due by 18 September 2012

-

Upload

trinhxuyen -

Category

Documents

-

view

215 -

download

0

Transcript of Issued on 24 July 2012 Responses due by 18 … · Issued on 24 July 2012 Prior to finalising the...

Market ConsultationIssued on 24 July 2012Responses due by 18 September 2012

CREFC EuropeMarket Principles for Issuing European CMBS 2.0

Market ConsultationIssued on24 July 2012

Prior to finalising the Market Principles for Issuing European CMBS 2.0, CREFC Europe and the CMBS 2.0 Committee are seekingcomments in relation to the document.

We encourage and welcome comments from all market participants and request that all comments be submitted on or before18 September 2012.

How to Submit Comments:To help process and review comments efficiently, we will only accept responses by our online response form. Online response form islocated at http://www.crefc.org/eucmbs20/

Comments received will be reviewed and will not be made publicly available.

Thank you,

CREFC Europe

Introduction .............................................................................2

The CMBS 2.0 Committee ......................................................2

Background for the Committee................................................2

Approach.................................................................................2

Best Practice Principles ...........................................................4

Part 1: Disclosure ....................................................................4

Part 2: Revenue Extraction: Excess Spread Monetisation ........8

Part 3: Investor Identification and Investor Forum ....................10

Part 4: Servicing, Transaction Counterparties and ControllingParty Rights .................................................................11

Part 5: Transaction Structural Features ....................................15

Part 6: Restructuring Issues.....................................................19

Part 7: Voting Issues................................................................21

Appendix 1 ..............................................................................22

Appendix 2 ..............................................................................23

Appendix 3 ..............................................................................27

Appendix 4 ..............................................................................33

Appendix 5 ..............................................................................35

cont

ents

This document (and its contents) contains only general information and is provided forinformation purposes only. This document (and its contents) does not constitute aninvitation or offer to buy or sell any investment or an official confirmation of anytransaction. None of CRE Finance Council Europe nor any of the participant firmsnamed herein nor any of its members nor any of its employees or officers are, by meansof this document (and its contents) or otherwise, rendering or providing (or could bedeemed to be rendering or providing) investment, legal, tax, accounting or otherprofessional advice or services. This document (and its contents) is not a substitute forsuch advice or services, nor should this document (and its contents) be used (and it isnot intended to be so used) as a basis for any investment decision or action orotherwise. Before making any investment decision or action or otherwise, you shouldconsult a qualified professional adviser. None of CRE Finance Council Europe, nor anyof the participant firms named herein nor any of its members nor any of its employeesor officers shall be responsible for any loss or liability whatsoever sustained or incurredby any person relating to the use of any information contained in this document or whootherwise relies on this document or its contents.

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

2

The CMBS 2.0 CommitteeThe Commercial Real Estate FinanceCouncil (CREFC) Europe established theCMBS 2.0 Committee to explore bestpractice principles for CMBS transactionswith the goal of improving confidence inthe European CMBS industry. It is thebelief of CREFC that improvedconfidence by market participants inCMBS structures will encourage thefurther development of the CMBS marketin Europe, which in turn will assist withthe immediate need for capital for realestate transactions. The Committee hastaken into account the views of a cross-section of both historical and activeparticipants in the real estate capitalmarkets, and the group comprises seniorrepresentatives from issuing banks,investors, loan servicers, financialadvisers, borrowers, trustees, lawyersand other industry experts. Consensuswas not reached on all issues and assuch the principles reflect the majorityview of participants. CREFC would like tothank everyone that participated for theirvaluable time and contribution to theprocess. A list of certain participatingfirms and organisations is attached asAppendix 1.

Background for theCommitteeGiven the size of the commercial realestate funding gap facing the Europeanreal estate markets over the next fewyears and, to date, the limited availability ofalternative funding sources, the capitalmarkets are an essential source of capitalfor the real estate industry. However,macro-economic and broader marketissues aside, successful issuance of futuretransactions will be dependent upon thevarious market participants havingconfidence in, and a proper understandingof, CMBS structures and the roles of therelevant transaction counterparties.

The recent crisis has exposed some ofthe weaknesses in historical CMBS

transaction structures, the direction andcoordination of the various transactioncounterparties and the availability ofappropriate levels of information. Thereare also a number of positive structuralfeatures which have been identified andthese should be more widelyimplemented in future transactions.

In response to this background, theCMBS 2.0 Committee has produced aset of best practice principles in relationto some of the key features of CMBS.These areas include:

n Disclosure (including pre-issuancedisclosure, post-issuance disclosure,investor reporting and investor notices);

n Revenue Extraction in the form ofexcess spread monetisation(including Class X Note structures);

n Investor Identification and InvestorForum;

n The role of servicers, special servicersand other transaction counterparties(including trustees and cashmanagers); and

n CMBS structural features (includingcontrolling party rights, votingprovisions, liquidity facilities andsynthetic securitisations);

Approach The principles assume a certain degreeof existing knowledge and experience ofCMBS structures. They do not seek toincorporate all aspects of CMBSstructuring but instead focus on areasof particular importance that havereceived the attention of variousindustry participants with the purpose ofcreating market consensus in light ofrecent experience.

Each market participant approachesCMBS transactions from their ownperspective and the purpose of theseprinciples is to provide a balancedapproach to specific issues in order toprovide for the broadest marketparticipation. The principles are onlysuggestions of best practice and it willultimately be a matter for marketparticipants to decide whether or not toendorse them by applying them to theirtransactions. In certain instances theprinciples refer to a range of optionsrather than a preferred option. Again, inthese instances the participants shouldnegotiate the right option for theirtransaction and fully reflect that option byway of disclosure and in the pricing ofthe transaction. The European CMBSmarket benefits from a variety of realestate asset classes, deal types and

IntroductionBy Nassar Hussain, Chair of the CMBS 2.0 Committee

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

3

jurisdictions and the principles will needto be adapted accordingly.

The principles make reference, in certaininstances, to the requirements of certainCentral Banks such as the Bank ofEngland for sterling denominatedtransactions and the European CentralBank for euro denominated transactionsin relation to their respective eligibilitycollateral frameworks (e.g. the Bank ofEngland CMBS Transaction OverviewTemplate). The ratings criteria ormethodology to be applied by the ratingagencies to new CMBS transactionscontinues to evolve. The potential ratingsimpact of any of the principles will needto be evaluated separately on atransaction by transaction basis with therelevant rating agencies.

The CMBS 2.0 Committee has tried notto overlap with the supplementary workcarried out by other CREFC Committees,

including the Lender, Servicer,Inter-Creditor, Hedging, Loan DueDiligence and E-IRP Committees. Thefocus has been on matters purely relatedto transaction structures, transactioncounterparties and disclosure ofappropriate levels of information. Theseprinciples do not cover matters relating toloan or property underwriting,assessment of credit risk or due diligencestandards or processes. Additionally, theprinciples do not endeavour to anticipatethe form of interest rate structure orduration and related changes that newCMBS investors may require as this willevolve over time.

The CMBS 2.0 Committee’s principlestake into consideration the current marketenvironment and shall be revisedperiodically through updates and theissuance of appendices to address newtopics as industry best practices continueto evolve.

CREFC will also operate an ongoingCMBS 2.0 Principles Comments Sectionon the CREFC Europe Website so thatindustry participants can continue toprovide feedback and receive updateson Principles.

These principles supplement andcompliment laws and regulationsapplicable to the issue of securities suchas CMBS as well as the rules of anyapplicable stock exchange. Issuers andarrangers of CMBS transactions shouldtake their own advice on such matters toensure that their CMBS transactionscomply with the same.

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

4

Part 1: Disclosure1.1 Introduction

The purpose of this section is toencourage improved levels of pre- andpost-issuance disclosure andtransparency and to generate industryefficiencies. The guidelines in thissection seek to:

n Promote the consistency of corereporting and uniformity of minimuminformation levels in European CMBStransactions in order to create ahigher standard for reporting and abetter means of comparing CMBStransactions; and

n Reduce the time required by marketparticipants to reconcile reporting andthe time information providers arerequired to respond to follow-upqueries from investors.

Investors should be satisfied thatdisclosure matters are adequatelyaddressed in the documentation at thetime of issuance.

In addition to the disclosure principles setforth in this section, there are specific itemsof disclosure set out in each of the othersections contained in these principles.

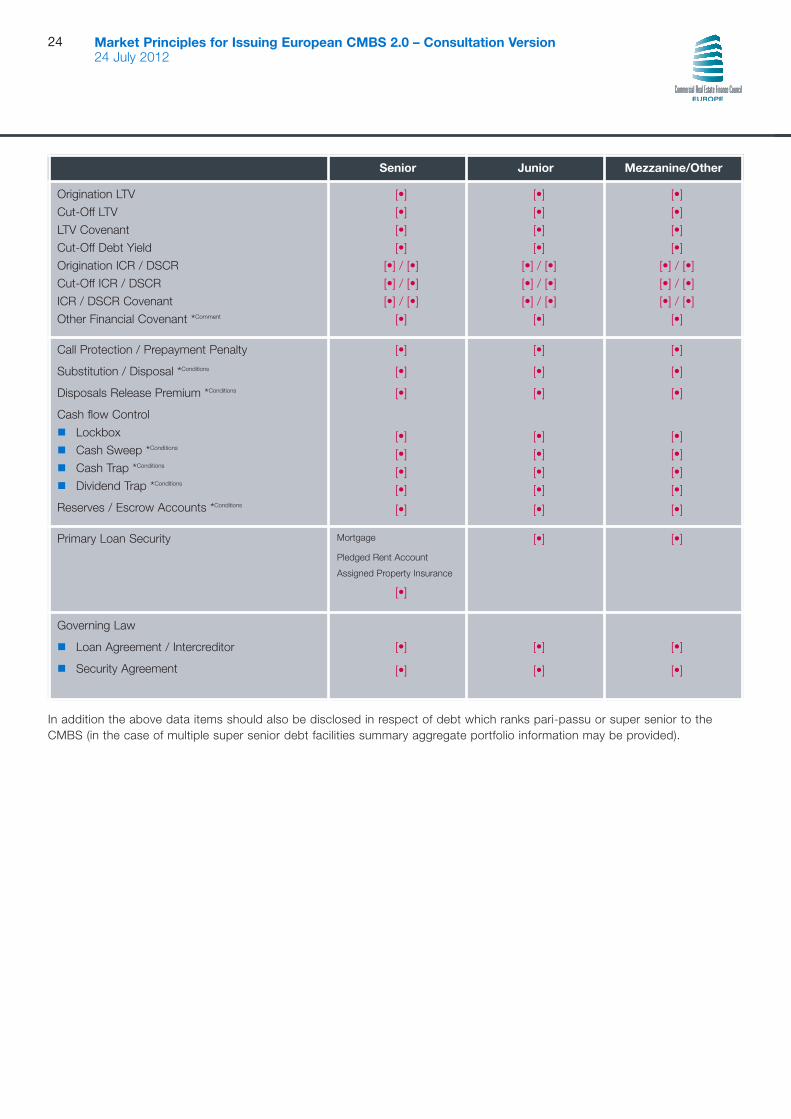

1.2 Offering Circular Disclosuren In transactions with a single loan or

for any loans constituting more than5% of the total assets, there shouldbe detailed loan level disclosure in theOffering Circular and, whereapplicable, disclosure of any borrowerlevel hedging.

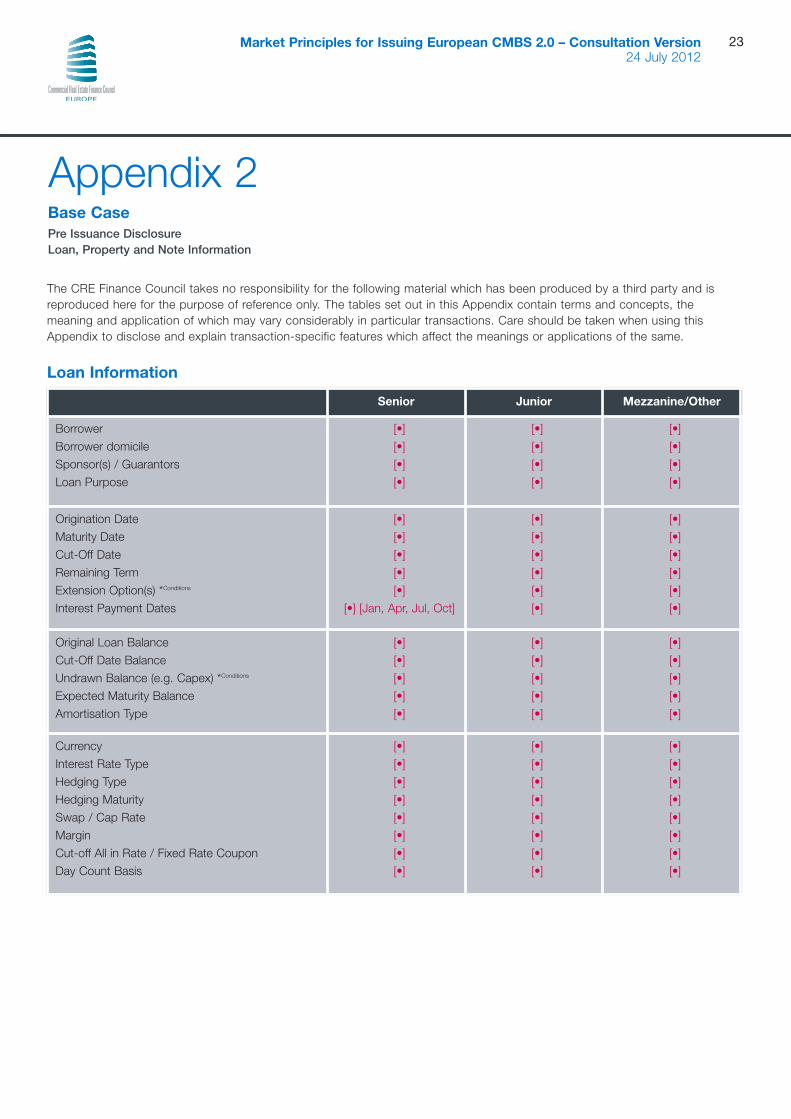

n In order to improve transparency andfacilitate comparison betweentransactions, information in respect ofthe loan(s), underlying property andnotes should be presented in astandardised format (the “BaseCase”). Summary tables should beused in the Offering Circular todisplay the Base Case in the form setout in Appendix 2.

n The Offering Circular should contain atransaction overview similar to orbased on the Bank of England’s

CMBS overview template (AFME/ESFversion for UK stand-alonetransactions), which is available at:http://www.crefc.org/eucmbs20/ butappropriately adapted on atransaction by transaction basis.

n Any transactions which incorporaterevenue extraction through excessspread monetisation (including class Xnotes) or otherwise (as set out inmore detail in Section 2.2) shouldinclude a separate section in theOffering Circular providing full detailsof such extraction.

n Conflicts of interest that are known toexist or are likely to or will exist in thefuture (e.g. on completion of thetransaction) at each level of thestructure should be clearly and fullydisclosed in the Offering Circular(including conflicts relating tonoteholders, junior and mezzaninelenders, the hedging provider, therevenue extraction holder, theservicer/special servicer and thetrustee), clearly specifying whichparties could be involved and how thepotential conflict of interest couldimpact investors. Appropriateprovision should be made in therelevant documentation so that if aconflict of interest arises in relation toa transaction counterparty after thedate of the Offering Circular it can bedisclosed in the periodicalinvestor reporting.

n If possible, information on the identityof the borrower and the ultimatesponsor(s) holding at least [10]% ofthe equity should be disclosed in theOffering Circular. This excludes limitedpartners in a fund managed by areputable and established investmentmanager. The purpose of the financingshould be disclosed (whetheracquisition or refinancing) togetherwith the amount of outstanding equityof each sponsor that remains at risk.However, these guidelinesacknowledge that the ability to makecertain of these disclosures will restwith the relevant sponsor, who may

have its own reasons for not wantingsuch detailed disclosure to be made inthe Offering Circular.

n The existence and amount of anyjunior debt (including B notes,mezzanine loans or othersubordinated loans or PIK typeinstruments), pari-passu debt andsuper-senior debt should bedisclosed in the Offering Circular.Further, all rights of such holders ofadditional debt should be disclosed inthe Offering Circular to the extent thatsuch rights relate to modifications,waivers or enforcement of thesecuritised debt setting out the rightsof the holders of such junior debt,whether the rights are entrenched(including consent rights, purchaseoptions, cure rights, enforcementrights, amendment rights). Also, thesecurity attached to such other debtshould also be disclosed.

n The Base Case and ongoing reporting(as described below) should specifywhether reported income is gross ornet (and what deductions are madebetween gross and net).

n The CMBS 2.0 Committee will workwith market participants in order toproduce and publish a base set ofbest practice representations andwarranties in the near future. The formof any representations and warrantiesshould be detailed and objective. Anydisclosure or exception to arepresentation and warranty shouldbe set out immediately below thespecific representation and warranty.For conduit and true sale transactionsthere should be detailed disclosure inthe Offering Circular of all therepresentations and warrantiescontained in the loan sale agreement.For all transactions there should bedetailed disclosure in the OfferingCircular of all the representations andwarranties relating to (i) disclosure ofall material information,accuracy/omissions of informationetc. to noteholders and (ii) generalmatters including due incorporation,

Best Practice Principles

authority, valid and binding obligationsand insolvency.

n The Offering Circular should disclosethe identity and key information inrespect of the transactioncounterparties including the business,experience, financial standing andownership of the key transactionparties including the servicer, specialservicer, trustee and cash manager. Inrelation to the servicer and specialservicer, there should be disclosureon their experience in relation to theloans and collateral (and the countryin which the collateral is located)which form part of the CMBS and theability of the servicer or specialservicer to implement potential work-out strategies with or without consent(e.g. restructuring, enforcement, saleof loan). There should also bedisclosure on the servicerreplacement mechanism and thecircumstances in which serviceradvances (if any) will be provided.

n The Offering Circular should disclosethe fees payable to such transactioncounterparties. CREFC is consciousof the potential sensitivity to thevarious transaction parties ofdisclosing such fees and, therefore, itwould be acceptable in respect ofonly the ordinary, annual fees of thetransaction parties (other than theservicer and special servicer) to onlydisclose an aggregated amount thatrepresents the total, annualcompensation for all of thetransaction parties.

n The Offering Circular should alsodisclose who receives the benefit ofany material ancillary cash flows suchas loan prepayment penalties, loanconsent fees, loan default interest orgains on hedge terminations.

1.3 Transaction Documents n All CMBS level transaction documents

(including the servicing agreements)should be made publicly availablethrough the issuer or the trustee inelectronic format on an investor

reporting website maintained by aparty to the transaction, a third partywebsite or both. The location of thewebsite should be disclosed in theOffering Circular and in each quarterlyinvestor report.

n In relation to loan documentation, thelevel of public disclosure will, to someextent, be determined by marketforces and reflect a balance betweenthe borrower’s need for privacy andthe note investors’ need to be able toevaluate the credit quality of thenotes. However, it is recommendedthat loan level documents which dealwith cash flows and security, whichhave a significant impact on theCMBS (e.g. the loan agreement,intercreditor agreement and hedgeagreements) should be madeavailable (in particular, there may bevariations for transactions with asingle loan or with large loans in thepool). In the absence of any of theabove documents being madepublicly available, the summaries inthe Offering Circular should bedetailed and should include allmaterial information

n Detailed disclosure of the hedginginstruments used should be madeand such disclosure should include,but should not be limited to, thefollowing information:

• The type of instruments andexplanation of the hedgingstructure;

• Borrower level or issuer level;

• The ranking(s) in the paymentwaterfall (both pre and postacceleration);

• Details of who the hedgingcounterparty is and any rights thatthey may have (including votingrights and the ability to terminatethe instrument);

• The notional profile of theinstrument;

• Payment dates including, inparticular, the maturity date;

• Whether the liquidity facility/serviceradvances are available to meethedging payments;

• Quarterly reporting of the mark-to-market valuation of the hedge bythe hedge counterparty toinvestors (through the investorreporting of the servicer or cashmanager, as the case may be);

• How changes in swap rates mayimpact the level of the mark tomarket valuation; and

• Ongoing disclosure of how muchcollateral under a credit supportannex has been posted atany time.

Any material amendments to the profile,other than partial terminations as a resultof partial redemptions, should bedisclosed as and when they occur.

In the absence of the underlying hedgedocumentation, (including the schedule,confirmations and any credit supportannex) being made publicly available, thesummaries in the Offering Circular shouldbe detailed and should include allmaterial information.

1.4 Investor Reporting, Data andCash flow Model

n Investor Reporting – The OfferingCircular should contain information onthe content, dates of availability,access (including any restrictions onaccess (such as registration of detailsor certification of interest)) and cost (ifany) of investor reporting and whichtransaction counterparty will beresponsible for each element of theinvestor reporting (e.g. servicer/specialservicer for loan and collateralinformation and cash manager fornote level information). The pro-formaform of the investor report should bedisclosed at the time of the noteissuance. A list of the recommendedinformation/data requirements forinvestor reporting is attached asAppendix 3. The investor reportshould be made publicly available in asuitable electronic format (.pdf, .xls or

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

5

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

6

.csv file) on a reporting websitemaintained by an agent of the issueror on a third party website or both.

n Provision of Data – The OfferingCircular should contain information onthe content, dates of availability, access(including any restrictions on access(such as registration of details orcertification of interest) and cost (if any)of transaction data in the form/templateof CREFC Europe’s Investor ReportingPackage® (E-IRP®). The most recentversion of E-IRP is v2.0 contains theLoan Setup File; Loan Periodic File;Property File; and Bond File and isavailable at:http://www.crefc.org/Global/CMSA-Europe/Resources/E-IRP/European_Investor_Reporting_Package. The E-IRP is currently incompliance with the latest requirementsof the European Central Bank and theBank of England. The populatedversion should be made available in asuitable electronic format (.xls or .csvfile) on a reporting website maintainedby an agent of the issuer or a thirdparty website or both.

n The data used to compile the loaninformation in the Base Case is in thesame form as the E-IRP Loan SetupFile and should be made available atthe outset to appropriate transactioncounterparties including the servicer,to assist in their ongoing reporting. Allservicer quarterly reports and relevant

interim RIS notices issued on behalfof the servicer should be easilyreferable to the Base Case.

n Issuer Waterfall Cash flowModel – The Offering Circular shouldcontain information on the content,dates of availability, access (includingany restrictions on access (such asregistration of details or certification ofinterest)) and cost (if any) of an issuerwaterfall cash flow model in order thatinvestors can project future note levelcash flows until the notes are repaid.The model may be provided in avariety of formats (e.g. website-hosted, downloadable program orspreadsheet) but should enableinvestors to input key variables usinga recognisable spreadsheet format(e.g. .csv, .xls or .xlsx) and investorsshould be able to retain or record theresults. The form of cash flow modelshould contain the information andfunctionality outlined in Appendix 4and should at the outset encompassrelevant transaction features includingprovision for liquidity facility or serviceradvances, hedging structure andtransaction triggers impactingthe waterfall.

n The arranger of the CMBS issuanceshould arrange for such cash flowmodel to be provided directly orindirectly (through a delegated cashflow model provider) to the market atissuance and to the extent the base

transaction structure changes thearranger should update it at therelevant time.

n The quarterly investor reportingshould contain any relevant inputs forthe cash flow model which reflect thecurrent status of the transaction suchas note balances, note margins,loan/loan portfolio balance, currentliquidity facility drawing amount,balances of issuer level accounts andledgers, fixed inputs required tocalculate aggregate issuer costs andexpenses etc. and details of anytriggers that have been activated ordeactivated. Certain assumptioninputs required to operate the cashflow model to project future cashflows to the maturity or ultimaterepayment date of the notes shouldbe determined and entered by theinvestor. Details of the appropriateinputs are contained in Appendix 4.

n In addition, on an optional basis andat an appropriate cost, the arrangeror delegated cash flow modelprovider may provide to investors:

(i) An integrated or separate modelto project loan portfolio cash flowswhich incorporates the coupons,hedging structure, balances,maturity/extensions, scheduledamortisation, prepayments etc.The outputs of such model shouldbe capable of being used directlyas inputs into the issuer waterfallcash flow model; and

(ii) An integrated or separate modelto calculate the price of the notesbased on the note cash flowsproduced by the issuer waterfallcash flow model and a discountmargin determined and input bythe investor (or vice versa using aprice to determine the discountmargin of the notes).

n All information made available to theinvestors at primary issuance shouldalso be accessible by secondarymarket investors on the investorreporting website for the life of thetransaction (including investor reportsand investor marketing presentations).

n Each of the updated investorreporting, data (E-IRP files) and cashflow model should be made availablefree of charge within 14 days of anote interest payment date.

1.5 RIS Noticesn RIS notices should be published as

soon as reasonably possible upon theservicer or cash manager (as the casemay be) becoming aware of a“Notifiable Event”. The servicer or cashmanager should notify the issuer of theNotifiable Event and (if appropriate)prepare the draft form of RIS and theissuer should then be responsible forissuing the RIS Notice on a promptbasis. A suggested list of NotifiableEvents is set out in Appendix 5.

n The publication of certain information inan RIS notice may be delayed for thereasons specified in section 1.9 below.

n Further detail on the Notifiable Eventmay be incorporated into thequarterly report when and whereappropriate, provided that all materialinformation has been disclosed in therelevant RIS notice.

n The filing requirements for an RISnotice will vary based upon thelocation of listing and issue for anyCMBS transaction.

n RIS notices should be distributedsimultaneously via the clearingsystems and any other methodrequired in the “Notices” condition inthe Offering Circular.

n In addition to the publication requiredby law for any RIS notices, otherinformation websites such as areporting website maintained by anagent to the issuer or a third partywebsite or both should be usedtogether with electronic messagingsystems such as Bloomberg (whenand where appropriate).

1.6 Borrower Reportingn In order to permit the transaction

counterparties to comply with theirdisclosure obligations as outlinedabove, the underlying loandocumentation should contain theappropriate information undertakingson the borrower and any other

relevant obligors to provide theinformation and data in a mannerconsistent with the timing, nature andformat of such reporting requirementsof such transaction counterparties. Astandardised form of borrowerreporting should be encouragedacross European CMBS transactions.The CREFC is working on appropriateborrower level reporting templates.

n Information and data provided by theborrower in its regular reportingshould be in a format that can beused in the loan level reportsprepared by the servicer (i.e. in anelectronic and downloadable format).

n Borrowers should be required toprovide information within a timeframethat enables servicers to preparereports with adequate time prior tothe note interest payment dates andin accordance with the principles setout in section 1.4.

n If borrowers have not agreed tocomplete certain basic fields, or haveagreed to provide enhancedreporting, or have not agreed toreport by the usual reporting dates,this should be disclosed so thatinvestors’ expectations as to ongoingdisclosure can be managed.

1.7 Valuations and PropertyInspections

n Pre-issuance: Recent valuationsdated up to six months prior to theissuance date should be madeavailable to investors. If the originalvaluation is more than six monthsold, a bring-down desk-top valuationshould also be provided to investorsin each case by the arranger.

n Post-issuance: Any valuationcompleted post-issuance should beprovided to investors by the serviceror special servicer.

n All valuations should be electronicformat copies of the full valuationreport or desk-top report (asappropriate), sanitised to reflect anyexceptions provided for in section 1.9.

n The servicer/special servicer shouldundertake appropriate periodicalproperty inspections usingappropriately experience staff. Anyrelevant material findings during a

property inspection should bedisclosed in the next quarterlyinvestor report or, if relevant, as aNotifiable Event.

1.8 Disclosure of and Reliance onDue Diligence Reports

n All material due diligence reports(including valuations, structuralsurveys, reports on title,environmental reports, legal opinionsetc.) should provide for reliance anddisclosure in a manner appropriatefor a CMBS transaction. In particular:

(i) Reliance should be provided toeach finance party under the facilityagreement as well as to any trusteewith respect to any securitiesissued by any such finance party inconnection with a securitisation ofthe loan or any part thereof.

(ii) Disclosure should clearly beavailable to:

• All successors and assignsof the addressees tothe report;

• Their agents and advisors;

• Their affiliates, employees,officers, directors, agents;

• Any actual or prospectivepurchaser, transferee orassignee of, or participant in,the facility;

• Any servicer or specialservicer of the facility;

• Any actual or prospectiveinvestor (including its agentsand advisers) in any securitiesissued in connection with anysecuritisation of the facility;

• Any rating agencies (actuallyor prospectively) rating suchsecurities issued inconnection with anysecuritisation of the facilityand their respective advisers;

• Any trustee of any financeparty; and

• Where disclosure is requiredby law, court order, regulation,public authority or in respectof legal proceedings.

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

7

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

8

n In addition, the terms of due diligencereports should permit the report or areference to the report (and themethodologies and results on whichthe same is based) being included orquoted or otherwise summarised inany information memorandum,offering circular, private placementmemorandum, registration statement,prospectus or term sheet as may berequired to comply with anyapplicable laws, regulations or officialguidelines relating to the issuance ofany securitisation of the facility or forany investor or potential investor to bein compliance with any applicable law,regulation or requirements of anygovernmental, banking, taxation orsimilar body relating to maintaining aninvestment in, or the regulatory capitaltreatment of, any securities issued insuch securitisation.

1.9 Exceptions to Ongoing DueDiligence DisclosureRequirements

n Specific items of disclosure may bedelayed, withheld or redacted if:

• There is a legitimate reason underthe Market Abuse Directive orapplicable law (e.g. for bankingconfidentiality/data protectionreasons), to withhold theinformation and

• Where either:

• The release of informationwould prejudice ongoingcommercially sensitivenegotiations by the borrower(e.g. sale, lease renewal orregearing or rent reviewnegotiations) which in thereasonable opinion of theservicer would be materiallyprejudicial to noteholders; or

• Where the servicer, specialservicer or other transactionparty has received suchinformation pursuant to aconfidentiality or othersimilar agreement.

n The information should be releasedpromptly as soon as the legitimatereason or confidentiality nolonger applies.

Part 2: Revenue Extraction:Use of Excess SpreadMonetisation (IncludingClass X Notes) and OtherMechanisms 2.1 Introductionn A CMBS transaction is typically

structured so that the aggregateinterest that accrues on the loansexceeds the aggregate amount ofinterest that accrues on the CMBSnotes. This excess amount iscommonly referred to as the“Excess Spread”.

n Many CMBS transactions providerevenue for the originating orarranging bank through theextraction or sale of at least a portionof this Excess Spread (“RevenueExtraction”). Sometimes part of theRevenue Extraction is utilised torecover certain upfront transactioncosts of the CMBS transaction.

n Revenue Extraction can be structuredand defined in various ways includingclass X notes, deferred consideration,residual interest or retained interest.Revenue Extraction structures can besimple such as a skim on the loanmargin or more complicated as withClass X Note structures. However,these structures may have additionalimplications such as the shortfall ofnote interest due to extraneousexpenses not otherwise covered byExcess Spread.

n Revenue Extraction structurestypically allocate to the beneficiaryeither:

(i) An amount equal to the excess ofall interest earned on theunderlying loan or pool of loansover the costs of the CMBStransaction (these costs wouldtypically include the interestpayable on the CMBS notes andsome level of expenses for theCMBS transaction); or

(ii) A proportion of the loan marginoutside the CMBS structure(resulting in the loan marginpayable to the issuer beingreduced accordingly).

n A summary example of a Class XNote formula is set forth below:

“Class X Interest Amount” for anyperiod is equal to Loan Interestminus Bond Costs, with

“Loan Interest” for any period isequal to interest that has accrued orshould have accrued on the loan forsuch period at its margin; and

“Bond Costs” for any period isequal to the aggregate of: (a) certainspecified costs of the CMBStransaction; and (b) the aggregate ofinterest accrued on the notes at theirrespective margins.

n Other forms of Revenue Extractioncan be calculated in a number ofdifferent ways, which can includethe following:

• Two-Waterfall Structure: Allprincipal and all interest above athreshold amount are depositedinto a collection account, whichis then distributed to payexpenses, interest and principalon the CMBS notes. A thresholdamount of interest is thenretained as an excess amount ofinterest and paid to the RevenueExtraction holder. Typically, thisamount is stripped from the loanoutside of the CMBS structure.

• Single Waterfall Structure: Allamounts collected on the loan aredeposited into a collectionaccount which is distributed in aspecified priority to pay expenses,interest, principal and the RevenueExtraction from a single waterfall.

2.2 Revenue Extraction Disclosure n The Offering Circular should contain

clear and concise disclosure thatsets forth the existence and nature ofany Revenue Extraction structure,how it is calculated and whether it isto be retained by the originatingbank, servicer/special servicer or theborrower or their affiliates.

n This disclosure should be maderegardless of whether the RevenueExtraction is stripped from withinthe CMBS structure or outside ofthe CMBS structure at the loan levelor otherwise.

n Further, the disclosure in the OfferingCircular should provide the following:

(i) Expenses: There should be cleardetails as to which expenses willor will not be effectively absorbedby the Revenue Extraction. Thisshould result in a clear list ofitems that will be deducted or notdeducted in the calculation forthe Revenue Extraction fromthe cash flow.

(ii) Conflicts of Interest: There shouldbe clear disclosure as to anyconflicts of interest with respectto the Revenue Extraction atissuance, including, in particular,as to whether the servicer/specialservicer or any of its affiliates orthe borrower was the owner ofthe Revenue Extraction.

(iii) Priority of Payments: Thereshould be precise disclosure asto what payments are made tothe Revenue Extraction, oreffectively paid, senior orsubordinate to payments due onthe other CMBS notes.

(iv) Liquidity Facility/ServicerAdvances: There should be cleardisclosure as to whether theliquidity facility drawings orservicer advances can be used tosupport Revenue Extraction.

n The ongoing noteholder reporting forany CMBS transaction should clearly

set forth the full breakdown of thevarious components of thecalculation for the RevenueExtraction and provide preciseamounts for its various components,such as the available cash flow,expenses and other components ofsuch calculation.

2.3 Structural Recommendations The Revenue Extraction should clearlybe structured to take into accountthe following:

n Default Rate Interest: The RevenueExtraction should not increase in itscalculated payment solely as a resultof interest accruing at the defaultrate. The portion of the calculation ofsuch amounts that relate to theamount of interest earned on themortgage loan(s) should be limited tothe interest accrued at its standardrate (and exclude any interest thataccrues at the default rate).

n Modified Interest: The RevenueExtraction should not increase in itscalculated payment solely as aresult of an increase in margin thatis the result of any restructuring ofthe loan. Again, the portion of thecalculation of such amounts thatrelate to the amount of interestearned on the mortgage loan(s)should be limited to the interestaccrued at its original interest rate(and exclude any increase in interest

or margin that occurs after the initialissuance of the CMBS transactionto the extent that any such increaseis the result of a subsequentmodification or restructuring of themortgage loan(s)).

n Maturity Date: The Revenue Extractionshould not be entitled to receive anyportion of interest earned on amortgage loan after its original statedmaturity (or its extended maturity date,solely to the extent that suchextension is a result of application ofan extension option that is containedin the original mortgage loandocumentation at the time of the initialissuance of the CMBS transaction).

n Loan Default: The impact of a loandefault on Revenue Extraction shouldbe determined on a transaction bytransaction basis and be fullydisclosed and the CMBS issuancepriced accordingly. Various optionscan be considered from the RevenueExtraction no longer being entitled toreceive interest on specified defaultsof a loan or such defaults having noimpact until a loss on the loan iscrystallised and then the RevenueExtraction is adjusted accordingly asappropriate based on that loss.

To the extent that the CMBS transactionreceives any excess amounts on anymortgage loan as a result of the items setforth above, such excess amounts shouldonly be paid to the Revenue Extractionafter all of the CMBS notes (other thanany notes forming part of the RevenueExtraction) have been repaid in full. In themeantime these excess amounts can beapplied in a number of different ways tobe determined on a transaction bytransaction basis including:

n Paydown of the most senior noteseach quarter;

n Payment of a shortfall of any intereston the notes, for example, prior toand where a liquidity facility advanceor service advance would have beenapplicable (until all the collateral issold and then applied to cover anyshortfall of interest on the notes); or

n The build-up of a reserve fund whichcan be applied to cover principallosses on the notes.

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

9

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

10

Any surplus residual cash amounts thatmay exist after all the CMBS notes(other than any notes forming part of theRevenue Extraction) have been paid infull as a result of the application of theseexcess amounts may be used for theRevenue Extraction.

Part 3: Investor Identificationand Investor Forum3.1 IntroductionThe clearing systems should beencouraged to devise and implement amore efficient mechanism for noteholdersto be identified so that interested partiesmay communicate with them in relationto their holdings. Pending theintroduction of such a mechanism, anoteholder forum (the “Forum”) shouldbe encouraged on a transaction bytransaction basis as an interim measureto facilitate the identification of andcommunications between noteholders.The participating noteholders would beprimarily responsible for the operation ofany meetings and subsequent actionsundertaken by the Forum.

3.2 Identification n A “Forum Coordinator” should be

appointed in connection with theissuance of the CMBS notes. TheForum Coordinator will have thoseresponsibilities set forth in thissection. The Forum Coordinatorshould be an entity with experienceof interacting with and/orrepresenting noteholders or theyshould be the party that managesthe relevant investor reportingwebsite (as described below),typically the cash manager.

n On the issue date of eachtransaction, the lead manager(s)should provide the ForumCoordinator with a list of the initialinvestors which would form the basisof the Forum.

n Noteholders should be invited toidentify themselves to the ForumCoordinator. Only the ForumCoordinator could use thisinformation to contact noteholdersfor the purposes of the Forum.

Noteholders should be made awarethat if they do not identifythemselves, they will not be able toreceive notices through the Forumand will instead have to rely onmethods such as RIS notices, theclearing systems and Bloomberg.

n In order to prevent any conflicts ofinterests, the Forum Coordinator willbe prohibited from taking on anyadvisory or other role relating to theCMBS transaction (other than purelyadministrative service functions suchas cash manager or calculation agent).

n Borrowers, lenders and transactioncounterparties and their affiliatesshould (promptly upon becomingaware) disclose to the ForumCoordinator holdings of notes inexcess of [three] per cent. of thePrincipal Amount Outstanding of anyclass. This information would only bemade available to the ForumCoordinator, the cash manager andtrustee and excludes holdings heldwithin other internal teams that areappropriately Chinese-walled such assecondary trading desks.

n The Offering Circular should containfull descriptions of the mechanismfor the appointment andresponsibilities of the ForumCoordinator (both in the riskfactors/investment considerationssection and in the terms andconditions of the notes) and explainthat there can be no assurance ofthe completeness or accuracy of theinformation maintained by the ForumCoordinator. The Offering Circularshould also attempt to identify risksto noteholders of participating or notparticipating in the Forum.

3.3 Website n The investor reporting website1 for

each transaction should require eachperson logging-on to certify whetherthey are a noteholder. All parties thatidentify themselves as a noteholdershould be requested to:

(i) Provide one or more emailaddresses at which they canbe contacted;

(ii) Either (a) certify that they are notaffiliated to the borrower or anyother noteholder or lender in thetransaction or (b) disclose thefact that they are affiliated to theborrower or a noteholder orlender but operate withappropriate Chinese walls inplace; and

(iii) Specify which class or classes ofnotes they hold (but not theamount of their holding).

Any noteholder who validlycompletes this certification will beconsidered a member of the Forumfor the transaction.

n Any noteholder not logging on to theinvestor reporting website for anagreed period of time will be sent anotice by email by the ForumCoordinator stating that unless theylog on within two weeks they will beremoved from the records and ceaseto be a member of the Forum.

3.4 Communications n All notices to noteholders from any

transaction party will be sent throughthe Forum in addition to any othermeans of communication required inthe terms and conditions of the notes.

n Subject to meeting the requirementsfor the form of the notice, anynoteholder that is a member of theForum or any transaction party(including the issuer, cash manager,trustee, servicer and specialservicer) will have the right torequest the Forum Coordinator tosend a notice on its behalf to theother members of the Forum. TheForum Coordinator should beobliged to send notices as quicklyas is practically possible.

n The Forum Coordinator should postsuch notices to the website andsend them by email to the Forummembers (or to Forum membersholding particular classes of notes)as well as through the othercommunication methodssanctioned by the transaction inquestion. Notices should also be

1 Where the website for a particular transaction is not capable of being used in this way, alternative arrangements should be made

forwarded to the issuer forpublication on the RIS system ofthe stock exchange on which thenotes are listed.

n Such notices should1:

(i) Have a short title which shouldseek to explain the subjectmatter of the notice;

(ii) Advise noteholders that they maysuffer losses (and the ForumCoordinator, cash manager, trustee,servicer and special servicer will notbe responsible for the same) if theyignore such notices;

(iii) Invite other Forum members toattend a meeting, conference callor website with appropriatedetails of the same;

(iv) Set out a short description of thepurpose of the same;

(v) Confirm that any discussionswith other noteholders willcommence with confirmation bythe party initiating thediscussions (or their advisers) asto whether any “price sensitiveinformation” is expected to bedisclosed and any proposedmechanism for “cleansing” thesame following which anynoteholders not wishing toreceive such information will begiven the opportunity to retirefrom the discussion;

(vi) Contain a warning to noteholdersparticipating in the discussionsthat they will be responsible forany “price sensitive information”they may disclose to any othernoteholders;

(vii) Be in such format or formats asare compatible with systemsmaintained by the stock exchangeon which the notes are listed andthe relevant clearing systems; and

(viii) In all other aspects comply withthe International CentralSecurities Depository standards.

n No notice may contain a statementof opinion on the CMBStransaction, any transaction partiesor otherwise. The ForumCoordinator will be instructed not todisseminate any notice containing astatement of opinion.

n Once the notice has been sent, theForum Coordinator will have nofurther role in relation to the subjectmatter of the notice (unlessrequested by noteholders and if theForum Coordinator is willing to do so)and it will be for the relevantnoteholders to make the necessaryarrangements.

n Prior to a meeting or conferencecall being held, any participatingnoteholder holding at least [10]% ofall the notes or the relevant class,as the case may be, may ask theForum Coordinator to request proofof holdings from the otherparticipating noteholders to ensurethey hold a position in theunderlying transaction. The ForumCoordinator will not be required todisclose the note amount or whichclass of notes any participatingnoteholder owns.

3.5 Protective Provisions n Forum Coordinators should be given

the benefit of protective provisionsrelieving them from any responsibilityfor the accuracy or completeness ofinformation provided to it for thepurposes of the Forum by anyperson, the contents of any suchnotice or the failure of any notice toreach any noteholder.

n Forum Coordinators will not beresponsible for the release of anyprice sensitive information byparticipating noteholders orresponsible for cleansing any suchprice sensitive information.

n Forum Coordinators should beentitled to charge an agreed fee fortheir work in establishing andmaintaining Forums.

Part 4: Servicing,Transaction Counterpartiesand Controlling Party Rights4.1 Servicer and Special Servicer

Considerations

4.1.1 Servicing Standardn The servicing standard should include

a duty to maximise recoveries at theloan level on a present value basistaking into account the interests ofthe CMBS noteholders (or all thelenders if they also service junior debt)as a collective whole as opposed toany individual tranche (other thantaking into account subordination).

n The interests of the RevenueExtraction holders should not beconsidered when analysing themaximisation of recoveries.

n The servicer and special servicershould have consistent principles forthe evaluation of any discount rate tobe applied for any PV calculation.

n The calculation of the maximisation ofrecoveries should take into accountany swap termination payments thatreduce or increase the level ofrecoveries but should not include theimpact of liquidity facility drawings,servicer advances, sequential paymenttriggers or similar note level mechanics.

n Whilst the servicer or special servicerneed not take into account suchnote level facilities or mechanisms indetermining and applying theirstrategy under the servicingstandard, they should be open tohearing representations fromnoteholders on the impact of theservicer’s proposed strategy on notelevel facilities or mechanisms.

4.1.2 Appointment, Function and Feesof Primary and Special Servicer

n A special servicer should always beappointed on the closing date andshould become active, automatically,upon the occurrence of prescribedtransfer events (“Servicing TransferEvents”). A Servicing Transfer Event

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

11

1 Care will be needed to ensure that the content is not price sensitive, defamatory or otherwise problematic. The Forum Coordinator will have the right to decline to send outany notice the content of which it determines (in its sole discretion) to be problematic

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

12

would typically occur when there is afailure to pay, insolvency event,enforcement or other material default.

n Depending on the nature of thetransaction, careful considerationshould be given to which defaults orother conditions should result in aServicing Transfer Event (for instancea breach of an ICR covenant may bea Servicing Transfer Event, a breachof an LTV covenant may not be aServicing Transfer Event but an LTVbeyond 90% may be a ServicingTransfer Event).

n The respective roles of the servicerand the special servicer should beclearly defined so there is noambiguity or overlap. Primary servicingand special servicing can be assignedto the same firm if the documentsallow for the replacement of thespecial servicer by the ControllingParty or Replacing Noteholders (asdefined in section 4.2.2 below).

n The remuneration of theservicer/special servicer should bedesigned to ensure that it alwaysacts in the interests of lenders andthe amount and basis of calculationsof such fees should always beadequately disclosed at the outset ofa transaction. All details with respectto the fees payable to the specialservicer, including liquidation andworkout fees should be negotiatedon a deal by deal basis taking intoaccount factors such as the size ofthe loan and the complexity, natureand jurisdictions of the assets.

n Any special servicer appointed by theControlling Party or ReplacingNoteholders should be required torepresent prior to its appointment that ithas not offered any inducement orother incentives to any ReplacingNoteholder, the Controlling Party or anytransaction counterparty or theiradvisers involved in the appointment ortheir representatives.

n For agented CMBS transactions itwould be preferable to have anindependent third party servicer andspecial servicer appointed ordesignated as part of the structure atthe outset.

4.1.3 Ability of Servicer/SpecialServicer to Raise Capital forEssential Capex or Opex

n The servicer/special servicer shouldhave the ability, subject to certaincontrols, limitations and caps, toraise additional capital (where it isnot already provided for in theliquidity facility or through a serviceradvance facility) to fund costs andexpenses necessary to improve orpreserve the value of the underlyingproperty (e.g. payment of propertyprotection expenses, buildingsinsurance, capex to reposition aproperty) or short term opex to avoidinsolvency in less creditor friendlyjurisdictions. There should be clearand detailed disclosure in the offeringcircular of the relevant provisions.

n Such ability to raise capital should be:

(i) Subject to the application of theservicing standard;

(ii) Based on analysis that clearlydemonstrates on a PV basis thatthe use and cost of the additionalcapital will improve recoverylevels by an amount whichexceeds the aggregate amountand cost of the additional capitalby at least [1.25x];

(iii) On arm’s length and marketterms after an appropriatebidding process;

(iv) Have an appropriate securitystructure; and

(v) Be subject to non-petitionlanguage where appropriate.

n The servicer should determine that itwould be in the better interests ofthe issuer, as either lender or ownerof any interest in any REO property,that such amounts were raised asopposed to such amounts not beingraised, taking into account therelevant circumstances, which willinclude, but not be limited to, therelated risks that the issuer would beexposed to if such amounts were notraised and whether any suchamounts would ultimately berecoverable from the obligors of therelated loan.

n Where it can be appropriatelystructured into the transaction at theoutset the Servicer should use themost efficient form of capital inaccordance with the servicingstandard (e.g. super senior debt,mezzanine or equity) available at thetime in relation to cost, terms andranking of repayment and return.

4.2 Controlling Party, Replacementof the Special Servicer andOther Rights

4.2.1 Determination of the ControllingParty

n Typically, a “Controlling Party” isappointed with respect to each loanin a CMBS transaction.

n The Controlling Party for a particularloan typically has certain rights, mostnotably the ability to appoint anoperating adviser, the ability toreplace the special servicer and haveconsultation rights in relation toamendments for such loan.

n Depending upon the particular loan,the Controlling Party might beanother lender (other than the issuerof the CMBS transaction) or anoteholder in the CMBS.

n If a lender, the Controlling Party istypically the holder of the most juniorloan which has a principal amountoutstanding at some specified level(typically 25% of original principalamount). It is typical for loan levelControlling Parties to have some orall of their rights subject to a ControlValuation Event (see below).

n If the Controlling Party is the portionof the loan which has beensecuritised, control is typically heldby the most subordinate class ofnotes (known as the “ControllingClass”). However, the ControllingClass may change upon a controlvaluation event.

n The calculation of which party is thecontrolling party should always bedynamic and based on:

(i) A specified valuation process; and

(ii) The principal amount outstandingof the relevant tranche whether

reduced due to amortisation,pre-payment or write-offs.

n Whilst precise definitions need tobe drafted on a transaction bytransaction basis, the following bestpractice principles shouldbe considered:

• The Controlling Class should bethe most junior ranking class ofnotes then outstanding which hasa principal amount outstanding ofat least [25%] of its principalamount outstanding at originationand which is not subject to aControl Valuation Event

• A Control Valuation Eventshould relate to the currentprincipal amount outstandingversus the current value of theproperties and is deemed to haveoccurred in respect of a particulartranche of the notes or the loan,as applicable, if:

(i) The sum of the currentprincipal amount outstandingof the relevant class or loanand all junior ranking classesor loans

LESS

(ii) The sum of any ValuationReduction Amounts and(without duplication) anylosses realised with respect toany enforcement of security inrespect of the relatedproperties is less than 25% ofthe current principal amountoutstanding of the relevantclass or loan

• A Valuation Reduction Amountequals;

(i) The outstanding principalbalance of the loan

LESS

(ii) The excess of

(a) 90% of the most recentvaluation (net of any priorsecurity interests butincluding all reserves andsimilar amounts whichcan be used to pay theloan) above

(b) The sum of all unpaidinterest on the loan, anyprior ranking fees andexpenses (including duebut unpaid ground rentsand insurance)

4.2.2 Controlling Class, Replacementof Special Servicer andReplacing Noteholders

n The concept of a Controlling Class isappropriate but it is important thatthe rights of the Controlling Class arereflective of its junior position and donot unduly empower the holder(s) ofa single tranche of debt.

n Accordingly, while the ControllingClass should benefit fromconsultation rights, a transactionshould consider (based on theimpact on demand for junior notesand loans) if the right to replace thespecial servicer should be vestedsolely in the Controlling Class orassigned more broadly to a widergroup or class of noteholders (the“Replacing Noteholders”).

n Several options have been proposedto define which noteholders shouldconstitute the ReplacingNoteholders. Prevailing marketconditions and the specifictransaction structure shoulddetermine which approach is used.

Potential options are as follows:

(a) A majority of the Controlling Classhas positive appointment rightsbut other classes, as defined byone of the options below, have a‘negative’ veto right:

(i) A majority of all classes(including out of the moneyclasses), in aggregate; or

(ii) A majority of all in-the-moneyClasses, in aggregate;

(b) The Controlling Class and anyrepresentative grouping ofnoteholders ([10]% of all notes)has nomination rights to putforward a candidate for the roleof special servicer. Multipleclasses (determined according tooptions (i) and (ii) above) thenvote on the basis of proposalsfrom the candidates. Options fora voting process with multiplecandidates could be:

(i) Simple majority, with aControlling Class ‘castingvote’ in case of insufficientquorum or failed vote;

(ii) Simple majority with decliningquorum, eventually with theControlling Class holding a‘casting vote’; or

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

13

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

14

(iii) Quorum plus “AlternativeVote” mechanism to deal withlack of outright majority.

n The above concepts relate to therights of the Controlling Class ofNoteholders. To the extent the loanincludes a junior loan that is not part ofthe securitisation, the rights of theControlling Party should be consideredin line with these principles.

n If any borrower or equity sponsors orany (actual or prospective)transaction counterparty (in particulara special servicer) or their affiliatesacquire or otherwise control loans ornotes which have Controlling Partyor Controlling Class rights, therelevant holder of the loan or notesshould be restricted from exercisingany such rights.

n Cost of the relevant transactioncounterparties incurred in replacingthe special servicer should be borneby the new special servicer or theExcess Spread.

4.2.3 Conditions for Replacing aSpecial Servicer

n With respect to the replacement ofthe special servicer by the ControlParty or Replacing Noteholders, thetransaction documents shouldprovide for the following:

• No Elective Actions byOutgoing Special Servicer

The replaced special servicershould not have the ability toprevent or limit the transfer to thenew special servicer, on the basisthat all specified conditions fortermination and replacementhave been met. In particular:

(i) the outgoing special servicershould not have any right tonegotiate any furtherindemnities in connection withits termination andreplacement; and

(ii) the elective or votingprocedure along with thesatisfaction of the otherreplacement conditionsshould be sufficient action toterminate the rights and

obligations of the outgoingspecial servicer

• No New Servicing Agreement

(i) The new, replacement specialservicer should not berequired to execute a newservicing agreement. Instead,the process for accession bythe new special servicer tothe existing servicingagreement should be simpleand straightforward (forexample, by way of anaccession deed executedsolely by the replacementspecial servicer).

(ii) Documents should be draftedin a manner to permit asimple accession (e.g., therepresentations andwarranties should be draftedto permit repetition by anysuccessor special servicerand not drafted specifically forthe initial special servicer).

• No Conditions That Could beUtilised to Prevent Transfer byOutgoing Special Servicer

(i) Any conditions to be met bythe replacement specialservicer should be objective

4.2.4 Clarity around the appointmentand role of the Operating Advisor

n With respect to any transaction inwhich an operating advisor can beappointed by any class ofnoteholders, the transactiondocuments should clearly provide forthe following:

(i) The documents should permit theappointment of the operatingadviser without the requirementof a full bondholder meeting. Awritten resolution will beacceptable, provided that such awritten resolution does notrequire a 100 per cent.bondholder vote (although aquorum of 50 per cent. and avote of 75 per cent of suchquorum would be permissible);

(ii) If the appointment of theoperating adviser is to occur by

way of a written resolution ofnoteholders, the voting procedureshould permit the possibility ofonly one bondholder voting,provided such bondholder meetsa minimum holding threshold;

(iii) The transaction documentsshould clearly provide that theoperating adviser will not be heldresponsible to any party for itsactions taken as operatingadvisor, provided that theservicing agreement alsoprovides for a “servicing standardoverride” with respect to anydirection or consultation providedby the operating advisor to eitherthe servicer or special servicer;

(iv) There should not be anyrequirement for the operatingadvisor to accede to any of thetransaction documents in order forit to exercise any of its rights; and

(v) The documents should clearlyprovide that, if the operatingadvisor is not appointed or if theoperating advisor does notprovide any direction orconsultation to the servicer orspecial servicer, that theservicer/special servicer can takeany action consistent with theservicing standard without regardto any requirement toconsult/receive direction from theoperating advisor.

4.3 Replacement of TransactionParties with a Pure ServiceFunction

n If requested by more than 10% ofnoteholders in aggregate, a noteholdervote can take place to replace certaintransaction parties without cause(including the primary servicer, thecash manager, forum coordinator, thenote trustee and if appropriatemechanisms are put in place, thesecurity trustee). A resolution toreplace a transaction party may bepassed if approved by more than[50%] of each tranche of notes.

• No Elective Actions byOutgoing TransactionCounterparty

The replaced transactioncounterparty should not have theability to prevent or limit thetransfer to the new transactioncounterparty, on the basis that allspecified conditions fortermination and replacementhave been met. In particular:

(i) The outgoing transactioncounterparty should not haveany right to negotiate anyfurther indemnities inconnection with its terminationand replacement; and

(ii) The elective or votingprocedure along with thesatisfaction of the otherreplacement conditionsshould be sufficient action toterminate the rights andobligations of the outgoingtransaction counterparty

• No New Agreements

(i) If possible, the newreplacement transactioncounterparty should not berequired to execute a newagreement. Instead, theprocess for accession by thenew transaction counterpartyto the existing agreementshould be simple and straightforward (for example, by way ofan accession deed executedsolely by the replacementtransaction counterparty).

(ii) Documents should be draftedin a manner to permit asimple accession (e.g., therepresentations andwarranties should be draftedto permit repetition by anysuccessor transactioncounterparty and not draftedspecifically for the initialtransaction counterparty).

• No Conditions That Could beUtilised to Prevent Transfer byOutgoing TransactionCounterparty

Any conditions to be met by thereplacement transactioncounterparty should be clearand objective

4.4 Replacement of TransactionParties with a Credit Function

n Transaction documents should detailthe process for replacing parties (e.g.bank account provider, swapcounterparty, etc.) if they aredowngraded or become insolvent.This should also include clearreference for who needs to managethe process and which other partiesneed to provide approval.

4.5 Fees, Costs and Expenses ofTransaction Counterparties

n The Offering Circular should detailthe fees payable to any transactioncounterparty to the transaction andany ability to vary these fees orrequest additional fees on an ad-hocbasis. Ongoing investor reportingshould promptly detail any additionalfees invoiced by any transactioncounterparty to the transaction withsome brief narrative on the natureand the purpose of the workcompleted for the additional fees.

n The fees payable to any professionaladvisers out of transaction cash flowsby any of the transactioncounterparties including legal,financial, property/valuation orhedging should be promptlydisclosed on an aggregated basis foreach transaction counterparty in theongoing quarterly investor reportingwith some brief narrative on thenature and the purpose of the advice.The primary purpose of anyprofessional advice should be tosupport such transaction party withrespect to its obligations under thetransaction (but for the avoidance ofdoubt should not be primarilyfocussed on liability issues fortransaction counterparties).

n Transaction counterparties shouldavoid appointing affiliated entities toprovide services to the transactionincluding financial, property/valuation,agency, LPA receivership andasset/property management unlessthey are suitably qualified andcompetitively priced. If any affiliatedentities are utilised, full disclosure ofthis should be made together with allfees being received by the transactioncounterparty and the affiliates.

4.6 Trustee Considerations4.6.1 Action to be Taken by the Trustee n The role of the trustee should be

limited to oversight of mechanicalprocesses and passive monitoring ofprescribed objective criteria. Any suchprocesses should be clearly laid outand defined to limit any ambiguity.Trustees should generally not berequired to exercise any discretion, butwhere trustees are asked to exerciseany discretion then the trustees shouldhave the ability to obtain appropriateexpert advice including legal,accounting, financial or property adviceat a reasonable cost which is chargedto the transaction. The trustee shouldplace primary reliance on the use ofthe expert advice to make anydetermination and rely on the standardmarket liability terms of professionaladvisers rather than seeking additionalindemnities in addition to the standarddeal level senior ranking indemnityalready provided.

n The documentation should establish atthe outset, whether any role of thetrustee allows the trustee to requestadditional indemnification (and fromwhom). A trustee should only bepermitted to withhold exercisingdiscretion in the absence of anindemnification where both the relianceon expert professional advice and thestandard deal indemnity are clearlyinsufficient in relation to the level of anypotential claim they may face.

Part 5: TransactionStructural Features5.1 Principal Payments – Definitions

and Sequential Triggers n The Offering Circular should include

full disclosure of how different typesof principal receipts should beallocated in all scenarios includingapplication of both the allocated loanamounts and release premiumswhether due to property sales orproperty refinancings.

n The transaction documents shouldensure that the party responsible fordetermining the allocation receives allinformation required in order todetermine how to treat the allocationof the relevant principal.

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

15

Market Principles for Issuing European CMBS 2.0 – Consultation Version24 July 2012

16

n In general, preference should begiven for simple waterfalls with alimited numbers of determinationsand triggers.

n Sequential payment triggers shouldbe based on the percentage (basedon the principal balance) of loanswhich have cumulatively entered andremain in special servicing (asopposed to separately defining thedifferent types of loan defaults thatwould apply). Loans which aresubject to the following scenariosshould typically be included towardsthe sequential trigger threshold:

(i) Loans that are subject to amaterial payment default afterany applicable grace or cureperiod; and

(ii) Loans that reach their originalmaturity date (unless an extension isspecifically provided for andpermitted in the original loandocumentation), regardless ofwhether a standstill or extension isagreed by all of the parties.

n The Offering Circular for atransaction should include a detaileddescription of the sequentialpayment trigger calculation. Inparticular, the Offering Circularshould disclose whether thesequential payment trigger has theability to “switch back”, or if once thesequential payment trigger has beenbreached, it is not subject to apossible cure.

n The responsibility for calculating,checking and reporting on thesequential payment trigger should beclearly allocated to a single party(either the servicer or cash manager)and reported to noteholders on aregular basis. If the sequentialpayment trigger is directly linked tothe definition of Servicing TransferEvent, it is suggested that theservicer undertakes the role of eitherdetermining whether a sequentialpayment trigger has occurred orproviding appropriate notification tothe cash manager. The servicer willnot be responsible for making anypayment calculations at note level.

5.2 Interest Shortfalls on Notesn Where an available funds cap applies

to particular tranches of notes, thistypically results in a shortfall ofinterest on those notes due to thelevel or order of prepayments of theunderlying loans. In such situations,there should be clear disclosure ofwhich classes of notes are potentiallyimpacted, whether the shortfall willever be recoverable (e.g. use ofdefault interest) or reversible, thelevel of prepayments required tocause a shortfall and theidentification of which loans (shouldthey prepay early) are most likely tocause the shortfall.

n There should also be disclosure ofany structural reasons why a shortfallof interest may occur on classes ofnotes such as the occurrence of asequential trigger event which maylead to an increased risk of non-payment of interest on junior notesdue to the weighted average cost ofthe notes increasing as the principalbalance of the senior notes reduceover time but the loan marginremains the same.

5.3 Liquidity Facilities n An appropriate mechanism should be

considered which restricts theamount that can be drawn from theliquidity facility to pay interest oncertain notes if there has been adecline in the collateralperformance/value. This may beconsidered appropriate sincepayments to notes that have beenvalued-out create a liability rankingsenior to all of the notes, for thebenefit of valued out junior noteswhich may in certain circumstancesincrease or cause a shortfall to seniornoteholders. The specific triggerlevels or structure can be determinedon a transaction by transaction basiswith due consideration to any ratingsimpact but may include:

(i) The liquidity facility may not beavailable to pay interest shortfallson any notes that have beenvalued out in accordance with thedefinition of Control ValuationEvent set out above (but basedon value alone and not due to the

principal amount outstandingbeing less than [25]%);

(ii) The liquidity facility may not beavailable to pay interest shortfallson any notes where on the basisof a calculation of estimatedrecovery proceeds from time totime they will suffer a principalloss of at least [90]% of theirprincipal amount outstanding;

(iii) The liquidity facility may not beavailable to pay interest shortfallson any notes that have beenwritten down (actually ornotionally) as a result of an actualloss suffered; or

(iv) If a Control Valuation Event orother event referred to above nolonger applies then liquidity maybe drawn again to pay interestshortfalls on notes there werevalued out including accrued butunpaid interest from previousinterest payment dates.

n The above restriction of paymentsonly applies to proceeds from theliquidity facility. In other words, if theloans pay sufficient interest, all ofthe notes should receiveinterest payments.

n Repayment of any principal amountoutstanding on the liquidity facilityshould be repaid from both principaland interest collections, rather thansolely from interest collections(subject to managing any mismatchbetween loan and note principalbalances and between loan/note andhedge notional principal balances).

n Provided appropriate mechanisms arein place to restrict the amount that canbe drawn from a liquidity facility basedon collateral performance/value themaximum principal amount availableunder the liquidity facility on eachpayment date from time to time shouldbe equal to the lower of the agreedamount as at the closing date and anagreed percentage of the aggregateprincipal amount outstanding of thenotes subject to a floor.

n The liquidity facility should beavailable to make payments of seniorexpenses, any interest rate swaps

(whether at borrower or issuer level),certain tax payments, propertyprotection expenses and certaintypes of essential capital expenditureor essential corporate expenditure toavoid insolvency.

n The procedure for renewing theliquidity facility should be clearly laidout in the documentation with clearresponsibility allocated to a singletransaction counterparty (typically thecash manager) to deal with therenewal process.

n The relevant provisions above wouldalso be applicable to serviceradvance facilities.

5.4 Hedging n In general, the instruments used

should be appropriate for the term,payment profile and structure ofthe transaction.

n To the extent possible under therelevant governing law, ensure thatpayments to the swap counterpartyare properly subordinated in the caseof a default by the swapcounterparty or a termination eventthat is the result of a downgrade ofthe swap counterparty.

n To the extent that the maturity date ofany hedging arrangements extendsbeyond loan maturity, considerationshould be given to including thehedging termination costs in thecalculation of any LTV or ControlValuation Event calculations.

n There should be full disclosure of thehedging details and structurepursuant to the principles in 1.3.

5.5 Note Maturity The CMBS transaction documentsshould contain adequate provisions toaddress what will happen if the notesare not repaid at their maturity date.The precise provision should bedetermined on a transaction bytransaction basis, but potentialsolutions may include the following;

(i) Note Maturity Plan: If a loan remainsoutstanding twelve months prior to thefinal maturity date of the CMBS notes,the special servicer should be charged

with providing various options fornoteholders to consider, includinganalysis of the optimum method ofenforcement and which type ofinsolvency procedure to use. Thetransaction will set forth how any suchproposed plan can be approved.

(ii) Appoint a Receiver/AdministrativeReceiver/Administrator (orequivalent insolvencypractitioner): If no option proposedby the special servicer receivesapproval by the requisite number ofnoteholders, the note trustee for theCMBS should be deemed to bedirected by the noteholders toappoint the relevant insolvencypractitioner based on the analysis ofthe special servicer, or, if none, itsown professional advisers, in orderto realise the secured assets of theissuer at such time as the securityfor the CMBS becomes enforceablein accordance with its terms. Thenote trustee should have no liabilityif, having used its reasonableendeavours, it is unable to find aperson who is willing to beappointed as insolvency practitionerwithout additional recourse back tothe note trustee.

5.6 Cash Management Considerations

5.6.1 Time Lag between Loan andNote IPD

n A balance should be struck betweenminimising basis swap costs andensuring that the time lag betweenthe loan IPD and note IPD is longenough to ensure the smoothrunning of the transaction cashflows. Suitable time periods (to bedetermined by the originating banktogether with the relevant transactioncounterparties) should be built inbetween the various key dates(calculation, drawdown of facilities,report production, payment dates,etc.) to avoid causing defaults inpayments and delivery of informationto noteholders.

5.6.2 Fee Netting Offn No party should perform any

netting off or similar arrangementoutside of the prescribed waterfalls

or the parameters of thetransaction documents.

5.6.3 Cure Periodsn Consideration should be given to

structuring and documenting anycure periods so that they do notoverlap with potential triggers ordefaults or that there is clarity on theimpact where they do overlap.

5.7 Asset and Property Management n An asset manager and a property

manager should be appointed withrespect to any property that securesa loan in a CMBS transaction. Suchmanagers should be reputable firmswith relevant experience inmanaging properties of a similarnature. The terms of theirappointments should be set out inseparate agreements and suchterms should be in line with marketstandards, particularly in relation tofees and the duties of the parties.