Issue22 November 2012 - Bridgepoint Capital

40

THE POINT Intelligent investing in Europe from Bridgepoint Issue 22 | November 2012 bridgepoint.eu Hitting home Why it pays businesses to take the local approach More for less Sustainability in the age of austerity Tuning in to tomorrow The art of predicting the future Join theparty Be part of the social network

Transcript of Issue22 November 2012 - Bridgepoint Capital

THE POINT

Intelligent investing in Europefrom Bridgepoint

Issue 22 | November 2012

bridgepoint.eu

Hitting homeWhy it pays businesses totake the local approach

More for lessSustainability in the age of austerity

Tuning in to tomorrowThe art of predicting the future

Join thepartyBe part of the social network

CONTENTS

15BUSINESS TRENDS

The local touchBusiness in the community:recognising the benefits of localism

9MARKET INSIGHT

Social pressureHow to succeed on social networks

19IN MY OPINION

The future is out thereMagnus Lindkvist on predictivepitfalls and how to avoid them

24IN THE SPOTLIGHT

Easing the squeezeAmid all the talk about ‘the squeezed middle’,discounters and niche brands are still doing well. Why?

2INS & OUTS

Bridgepoint investmentsand exits across Europe

5TALKING POINT

Green and meanDoes sustainability still resonate when times are hard?

28FACE TO FACE

Great chemistryDr Martin Wienkenhöver, CEO of CABB, enjoys the hands-on challenge of running the speciality chemicals business

32MANAGEMENT FOCUS

Big business is watching youMaking the most of internet innovation

36LAST WORD

Growing old gracefully The cult of youth can be taken too far. Agnès Poirierinvestigates

1

FOREWORD

They say that invisible threads are the strongest ties. With more than half ofthe world’s adults now said to be using social networks, a mind-bogglinglevel of penetration by any measure, it’s clear those threads are becomingever stronger. And such is their pull, that no business or brand can afford toignore them. The problem for many of us in business is that we can’t evenbegin to understand social media: the goalposts constantly change as well asthe audiences that these networks are designed to target. In our analysis ofthe phenomenon, ‘Social pressure’ on page 9, we show why social media ishere to stay, what current best practice is and why it is no longer thepreserve of the individual but increasingly of businesses, large and small. Just as businesses are waking up to the benefits of social networking, so too are theyrealising that the appeal to the consumer of localism, the need to feel part of acommunity, is on the rise. For years, business has adopted a centralised approach tomanagement, but as we show in ‘The local touch’ (page 15), decentralisation in favour ofmore blatant local community engagement is a growing serious alternative, in either theway goods are sourced or services marketed.In a similar vein, many companies are demonstrating remarkable fleetness of foot andflexibility in competing for every euro spent by the consumer. ‘Easing the squeeze’ (page24) identifies the type of initiatives many businesses are adopting across Europe in amarket characterised by rising prices and falling incomes. We also ask, in the light ofsuch economic constraints, whether it is right that sustainability should remain on thecorporate and governmental agenda when some argue that there are more pressingpriorities. In ‘Green and mean’ (page 5), we see how CSR is adapting to a changed worldof greater austerity. If it’s true that ‘Any fool can know – the point is to understand’, then web developers maybe stealing a march on us all. Of course, we’ve known for some time that the internet canglean personal information on all of us, but what is being done with that information (‘Bigbusiness is watching you’, page 32) is much more fascinating and sometimes alarming.Find out how companies use that information to influence how and what they offer theircustomers and the prices that they charge.Finally, our regular ‘Ins & Outs’ section (page 2) provides details of two new Bridgepointinvestments: Compagnie du Ponant, the French luxury cruise company specialising inthe polar cruise market, and BigHand, a UK voice productivity software business. Thereis also an update on recent realisations within the Bridgepoint portfolio. Let us know ifthere are any other topics relevant to the performance of business in Europe that youbelieve we should write about, and please enjoy the read n

November 2012Issue 22

Published by Bladonmore (Europe) Ltd

EditorJoanne Hart

DesignBagshawe Associates UK LLP

Reproduction, copying or extracting by any means ofthe whole or part of this publication must not be undertaken without the written permission of the publishers.

The views expressed in The Point are not necessarilythose of Bridgepoint.

www.bridgepoint.eu

THE POINT

William Jacksonis managing partner of Bridgepoint

The pull of the unseen

2

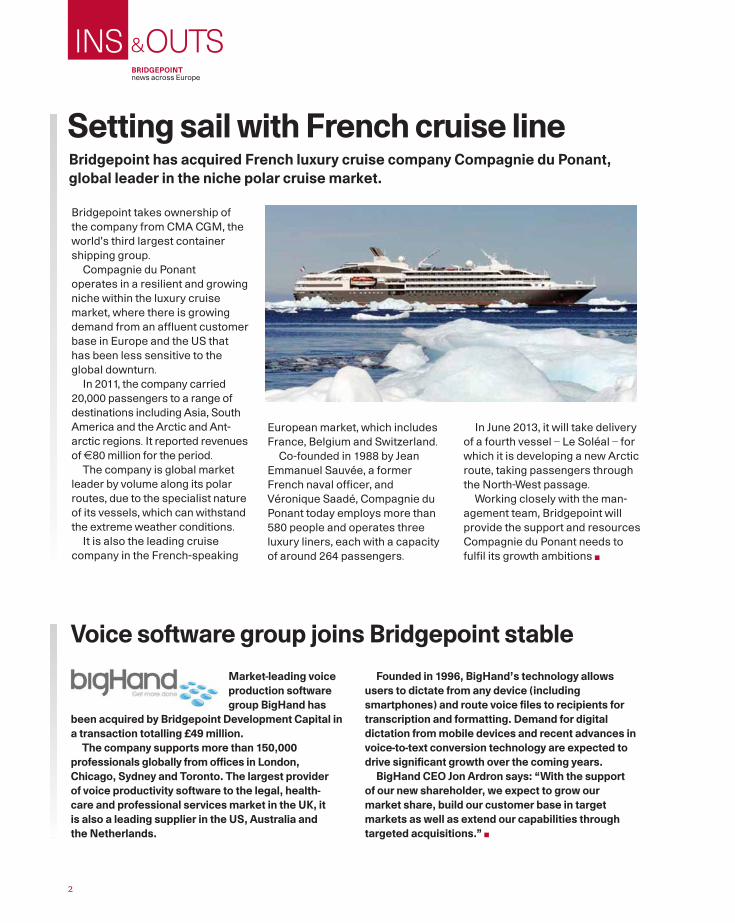

INS &OUTSBRIDGEPOINTnews across Europe

Bridgepoint takes ownership ofthe company from CMA CGM, theworld’s third largest containershipping group. Compagnie du Ponant

operates in a resilient and growingniche within the luxury cruisemarket, where there is growingdemand from an affluent customerbase in Europe and the US thathas been less sensitive to theglobal downturn. In 2011, the company carried

20,000 passengers to a range ofdestinations including Asia, SouthAmerica and the Arctic and Ant-arctic regions. It reported revenuesof €80 million for the period.The company is global market

leader by volume along its polarroutes, due to the specialist natureof its vessels, which can withstandthe extreme weather conditions. It is also the leading cruise

company in the French-speaking

European market, which includesFrance, Belgium and Switzerland.Co-founded in 1988 by Jean

Emmanuel Sauvée, a formerFrench naval officer, andVéronique Saadé, Compagnie duPonant today employs more than580 people and operates threeluxury liners, each with a capacityof around 264 passengers.

In June 2013, it will take deliveryof a fourth vessel – Le Soléal – forwhich it is developing a new Arcticroute, taking passengers throughthe North-West passage.Working closely with the man-

agement team, Bridgepoint willprovide the support and resourcesCompagnie du Ponant needs tofulfil its growth ambitions n

Setting sail with French cruise lineBridgepoint has acquired French luxury cruise company Compagnie du Ponant,global leader in the niche polar cruise market.

Voice software group joins Bridgepoint stableMarket-leading voiceproduction softwaregroup BigHand has

been acquired by Bridgepoint Development Capital ina transaction totalling £49 million.The company supports more than 150,000

professionals globally from offices in London,Chicago, Sydney and Toronto. The largest provider of voice productivity software to the legal, health-care and professional services market in the UK, it is also a leading supplier in the US, Australia and the Netherlands.

Founded in 1996, BigHand’s technology allowsusers to dictate from any device (includingsmartphones) and route voice files to recipients fortranscription and formatting. Demand for digitaldictation from mobile devices and recent advances invoice-to-text conversion technology are expected todrive significant growth over the coming years. BigHand CEO Jon Ardron says: “With the support

of our new shareholder, we expect to grow our market share, build our customer base in targetmarkets as well as extend our capabilities throughtargeted acquisitions.” n

3

Symington’s, the manufacturerof iconic brands such asCampbell’s and Crosse &Blackwell, has been sold byBridgepoint after five years ofsubstantial growth.The Leeds-based company is

one of Britain’s longest-established food manufacturersand has been acquired byIntermediate Capital Group in amanagement buyout.

The value of the deal was notdisclosed but Bridgepoint hasmade a healthy return on its investment in the 185-year-oldcompany.Over five years, Bridgepoint

helped Symington’s increase itstotal number of product lines from550 to 930. Chicken Tonight,Ragu and The Food Doctor rangewere just some of the brandsadded to the company’sportfolio during this time n

Bridgepoint exits Afflelou

Convenience food-maker sold

Germany-baseddrug manufac-turer AenovaGroup has been

sold by Bridgepoint after aseven-year investment, duringwhich the company experiencedtransformational growth. Formed in 2008 following the

merger of two previous Bridge-point acquisitions, Swiss Capsand Dragenopharm, Aenova hasbecome one of Europe’s leading

contract development andmanufacturing businesses,developing vitamins, supple-ments and pharma products.Post-merger, a new manage-

ment team was appointed andmore than €50 million wasinvested in new products andresearch and development.Efficiency measures alsoreduced the number of manufac-turing sites from nine to six n

Drugs group sold aftertransformational change

Motorcyclechampionshipsjoin forces

Bridgepoint hasappointed ChristianStreiff, former CEO ofPSA Peugeot Citroën,to its advisory board.Streiff has held

leadership positions at several majorEuropean businesses. He wasexecutive chairman of Airbus anddeputy CEO of Saint Gobain andserved on the boards of Faurecia andContinental. He is currently a non-executive director of ThyssenKrupp,Finmeccanica and Crédit Agricole. William Jackson, managing partner

at Bridgepoint, says: “Christian is oneof the leading European industrialistsof his generation. His extensiveknowledge of a number of industrieswill provide us and our portfoliocompanies with important commer-cial and strategic insight.” n

Bridgepoint has sold eyewear retail chain AlainAfflelou, following a six-year investment in thecompany. The largest optical franchisor inEurope, Afflelou has a network of nearly 1,100stores across France, Spain, Portugal, Belgium,Luxembourg, Switzerland, Morocco, Lebanon and

Ivory Coast. Attractive products, promotional offersand investment in marketing have helped the company enjoysubstantial growth and created a brand with 98 per cent awarenessin its core French market. Last year, sales reached €800 million n

Two of the world’s biggestmotorcycle racing events, MotoGPand World SBK, are to be integratedunder a single umbrella organisation. Bridgepoint already owns Dorna,

which runs MotoGP, and recentlyacquired sports marketing agencyInfront Sports & Media, which isresponsible for World SBK. The twoworld-leading racing events will beintegrated within the Dorna Sportsgroup but managed separately.As part of the reorganisation,

Infront becomes marketing partnerand global adviser to both champ-ionships, which should providesubstantial marketing and commer-cial benefits n

European industrialiston board

5

Talking point

Green andmeanSaving the planet was a laudable aim whencash was in plentiful supply and consumersfelt good. But is sustainability still centrestage after four years of austerity?

icture the scene. It is June1992 and the sun is shiningon Rio de Janeiro’s Ipanema

beach as President George H.W.Bush arrives by helicopter for amilestone environmental summitthat will set the green agenda forthe next 20 years.

The former US President wasjust one of 109 heads of state whoattended the Brazilian EarthSummit. As the politicians signeda groundbreaking deal to save theplanet, Hollywood star Jane Fondarubbed shoulders with Brazilianfootball legend Pelé.

While the Rio 1992 deal focusedon global issues of carbonreduction and biodiversity, itturbocharged a host of localmovements that brought

watchwords such as social respon-sibility and sustainability into theliving rooms of Europe, leavingconsumer-facing businessesscrambling to establish their green credentials.

Fast forward to 2012, anddespite a seismic change in theworld’s views on sustainability, theguest list for Rio Mark II was notquite so glittering.

President Hollande of Franceput in an appearance, but neitherthe UK nor Germany sent top-level delegates and PresidentObama and the film stars stayedfirmly at home.

Unsurprisingly, the successorevent yielded little more thanplans to make plans. Four years on from the credit crisis, it seems as if the West has neitherthe will, nor the cash, to fight forthe environment.

Even the most socially respon-sible Western Europeanbusinesses – which are facing theworst peacetime recession since

the Great Depression – havebeen privately questioningtheir commitment to thecause at a time when cash isextremely tight.

Organic dropSales of organic food, oncea byword for commitmentto sustainability, have beensteadily falling for the pastfew years in Britain, one ofthe organic movement’smost developed markets.

According to the SoilAssociation, the body that

certifies food as organic, UK salesof organically produced foodpeaked at £2.1 billion in 2008, justas Britain’s banks were collapsing.In 2011, sales dropped by 3.7 percent to £1.67 billion, the thirdconsecutive year of falls.

Jim Murphy, editorial director at the Future Foundation, atrendspotting think tank thatadvises European businesses onsustainability, says batteredconsumers increasingly believecharity begins at home andretailers are responding to their concerns.

“This is a very substantial issuefor us. We have plenty ofcustomers – supermarkets, forexample – who have a big stake insustainability and who have madelarge investments in corporatesocial responsibility and carbonreduction,” he says.

A Future Foundation survey ofconsumers’ views on environ-mental issues found thepercentage of British consumerswho believe they should actpersonally to help the environ-ment fell from 60 per cent in 2009to 50 per cent this year, withnegative online responses – whichare viewed as a more honestrepresentation of opinion thanface-to-face surveys – growingeven faster.

But Murphy emphasises thatbecause Britain is a maturemarket, any drop in the UK will befrom a high base. “There isresilience to public opinion. Onceratcheted up, it cannot easily beput back in the box,” he says.

P

UK sales of organically produced food peaked at £2.1 billionin 2008. In 2011, sales dropped to £1.67 billion, the thirdconsecutive year of falls”

‘‘

6

7

Dan Crossley, an adviser atbusiness sustainability consultancyForum for the Future, believes thatsustainability is still on the agendabut that it has to be handled differently in the current climate.

“Retailers have been forced towork harder to sell environment-ally sound produce in a difficultmarket. Sustainability might havefallen down consumers’ list ofpriorities, but this means retailershave shifted the way they sellthings. They have to show thatsomething is cheap as well assustainable,” he says.

With money tight, consumersare inevitably prioritising theirspending. But even within organicfood, there are exceptions to theslump. Global sales of organic foodgrew by 8 per cent last year aswealthy consumers in emergingmarkets started to turn on tosustainability.

Within the UK, demand forhigher-value produce, such aslamb and chicken, continued toincrease, while sales of organicbaby food soared by 6.6 per cent,suggesting the last thing yummymummies will cut back on is theirchildren’s wellbeing.

Outside the straight organicmarket, certain establishedsustainable products continue tosell well, thanks to backing fromhigh-street retailers.

“Fairtrade goods have really heldup. Over the last few years, we’veseen Fairtrade increase 30-fold. It’snow an established brand with 80-90 per cent recognition andbecause it has made its caseretailers are still cross-subsidisingits products,” says Crossley.

Michelle Gallant, engagementand events manager at Business in the Community, a business-ledcharity that promotes sociallyresponsible practices, agrees thereis a more cost-conscious focus tosustainability but asserts that com-panies still believe it is important.

“Businesses that want to bearound in 50 years’ time arerealising they need to adapt inorder to address some of thechallenging issues of our time –from resource scarcity toincreasing population,” she says.

CSR plans unchangedDespite the difficult climate, twohigh-profile pan-Europeanretailers, Marks & Spencer and

Kingfisher, have pushed aheadwith long-planned environmentaland corporate social responsibility projects.

Marks & Spencer, a Britishretailer with a modest footprintacross Continental Europe, isfocusing on growth in emergingmarkets. But despite the retailer’sexpansionary focus on lessenvironmentally sensitive markets,it is the first major British chain tobecome fully ‘carbon-neutral’under Plan A, a scheme to combatclimate change, reduce waste, usesustainable raw materials andtrade ethically.

The retailer launched thescheme in 2007 and reaffirmed itscommitment to a carbon-neutralpolicy this year.

Meanwhile Kingfisher, whichowns the UK’s B&Q, France’s BricoDépôt chain and Castorama, whichhas stores in France, Russia andPoland, has adopted a broader “netpositive” strategy and stuck by it.

The home improvementretailer's chief executive IanCheshire has personally alliedhimself to the scheme, whichpromises a combination of socially responsible initiativesincluding the use of sustainabletimber, a reduction in energyconsumption as well as invest-ment in local communities.

The plus point of austerity Proponents of the sustainabilityagenda argue that austerity couldactually have a positive influenceon both companies and consumersbecause it encourages customersto be more careful about costs.

“Economic depression is insome ways very good for theenvironment, given the reductionof industrial waste and energyconsumption,” says Murphy.

8

“Our research has consistently demonstrated that acompany that is managing its community impact ismore efficient and better at coping with challenges,”adds Gallant.

Crossley points to a cost-conscious reduction infood waste as a counterbalance to consumers’reduced spending on organic goods.

Action group Love Food Hate Waste saysconsumers in the UK throw away 7.2 million tonnesof food and drink every year, at a cost of £12 billion.But in the last two years the body believes theheadline percentage of food thrown away has fallenfrom 33 per cent to 25 per cent as cash-strappedconsumers organise their fridges better.

In Southern Europe, where consumershave been particularly hard hit by theglobal economic downturn, the urgeto conserve cash by consumingless has been the strongest of all.

“We are seeing a refocus on areas where efficiency dovetails with green issues. In a way,countries like Greece and Spain have to be even morefocused on efficiencies because they are struggling economically,” says Murphy.

Crossley says the pan-European picture is verymixed, with long-established commitments to foodquality providing a buffer to spending cuts in nationssuch as France.

“Countries like France and Italy are starting from ahigher base. But the green agenda is by no means justa UK phenomenon. Companies like Ikea andCarrefour have really committed to it and they aredoing more, not less. Scandinavia, in particular, leadsthe way on issues like renewable energy andpackaging,” he says.

Commentators point to global developments suchas the rise of online shopping as the biggest ongoingdriver of green spending and social responsibility inEurope. “There is lots of efficiency and thereforesustainability implied by that,” says Crossley.

In addition, a number of recent trends are drivingefficiency. “A really big development is towardsproduct service systems, which is where you get

access to an itemwithout actuallyhaving to own it,” saysMurphy. He points toclothes libraries and carclubs such as Zipcar andStreetcar as examples of

this movement.The point about these

services is that they not onlysuit the sustainability agenda; they are

also cheaper than traditional alternatives. As Gallantexplains: “There is no reason why corporate socialresponsibility should ‘cost’ consumers more. On thecontrary, companies are increasingly recognising thebusiness benefits of sustainability.”

Other commentators agree. They acknowledge thesevere short-term financial pressures on consumersbut believe the public’s commitment to environmentaland social issues can overcome these challenges.

“For those who never understood what sustainability means, it might have dropped off theagenda. But for those who embraced it, it’s moreimportant than ever. Now though, it’s about makingsustainability pay,” says Crossley.

And Murphy argues: “This is crunch time forretailers who have made serious commitments to CSR and environmentalism. Is anyone going to getpayback now for introducing more programmes of thissort? I think not. But will companies be criticisedpublicly for abandoning them once they’ve startedthem? Yes, absolutely.”

In other words, it is too late to put the genie of Rio1992 back in the bottle. These days, however, it is juston a budget n

Austerity could actually have apositive influence on bothcompanies and consumersbecause it encourages customersto be more careful about costs”

‘‘

Market insight

he Arab Spring in 2011 was awatershed moment for socialmedia. Over the course of a

few months, Twitter and Facebookbecame the focal point for arevolution that would eventuallytopple three oppressive regimesand shift the balance of power in aregion for good.

As the world watched andwaited, one thought must surelyhave rattled around boardroomslike a ball bearing in a biscuit tin: if social networks have the powerto galvanise nations, what couldthey do for our brand and ourbottom line?

Latest figures show that 62 percent of the world’s adults usesocial networks, spending a

massive 22 per cent of their onlinetime scouring channels such asFacebook, Twitter and Pinterest.Fuelled by the rapid uptake ofsmartphones, more people thanever are constantly connected,driving a growing demand forinstant interaction with friends,colleagues and businesses.

Digital footfall in numbersThe numbers are mind-boggling.Facebook now has more than 950 million active users worldwide– even if, by its own admission, 83 million of these users arepotentially false.

Twitter is hot on Mark Zucker-berg’s heels too, with 140 millionsigned-up users and the Twitter-

sphere tipped to hit 250 million bythe end of 2012.

One thing is clear: empoweredconsumers are here, and they arehere to stay in volumes it is nowimpossible to ignore. What’s more,these consumers are no longerjust sharing what they ate forbreakfast, they are increasinglyadopting social tools to investigateproducts, engage with brands andspend money.

According to industry blogThesocialskinny.com, social sitesare becoming an increasinglyimportant part of the purchasingjourney, with 40 per cent ofTwitter users regularly searchingfor products and 12 per centmaking a purchase because of

T

Some people swear by it. Others do not begin tounderstand it. But it can create heroes and villains,wreak havoc with corporate reputations and it ishere to stay. Social networking is a growing forceworldwide, but what does that mean for businessesand brands?

9

pressureSocial

information found on the socialnetworking site.

Facebook is no different, with60 per cent of users happy to postabout products or services in theirtimeline in order to secure a dealor discount.

The power of this digital footfallis forcing every business to asksoul-searching questions. Do weneed to engage these people? If so,how? Can we afford it? How dowe maximise the opportunitiesand minimise the risks? What canwe expect to get from it and, mostimportantly, what is our measurefor success?

“Any brand worth its salt istrying to figure out how to

engage and activateconsumers via socialmedia,” says ChristianVollmer, a partner with

global consulting firm Booz &Company, which conducted astudy of 117 leading companies’attitudes to social media in 2011.

“Those that are not focused onbuilding capabilities in this areaare, at their peril, ignoring one ofthe most important globaldevelopments in media, marketingand technology today.”

The view that doing nothing isnot an option is supported byRuth Mortimer, editor of MarketingWeek, the UK’s leading marketingindustry publication.

“I think it’s necessary for allcompanies to monitor social mediaand work out how to interact withit. I’m not sure it is alwaysnecessary for every company to behighly active on every area ofsocial media (for example, atechnical medical suppliesmanufacturer may have little tooffer on Pinterest), but it isimportant to monitor what is

being said andrespond whereappropriate. If youdon’t monitor socialmedia, you will neverknow what’s beingsaid about yourbrand,” she says.

Consumer-ledchangeOne view on this new

reality is that brandsno longer have the choice.

Consumers and employeesare already making thatdecision on their behalf.

“The nature of moderncommunications means

every company already has

a social media ‘presence’ via theactivities of staff on LinkedIn andFacebook as well as a brandfootprint made up of mentionsacross Twitter, Tumblr, blogs andcomments,” argues AnthonyCooper, managing director ofPearlfinders, a business researchcompany that quizzed more than5,000 marketers worldwide aboutsocial media usage.

“The real decision all companiesmust make is what resources tocommit to managing this presence.The minimum any company mustdo is to ensure visibility andunderstanding of the socialchannels through which its clientsvoice their opinions,” he adds.

Some companies are yet to bepersuaded by this logic, however.“Even though there is a cleardigital evolution, there are stillcompanies that are not convincedthat they have to go with thatevolution,” says Professor StevenVan Belleghem, partner at onlineresearch agency InSites Consulting.

“The risk for these companies is that they will miss out on an important target group in theirmarket. It is time for them toobserve, facilitate and join these conversations.”

During its research, Booz &Company found that the businesses already deemed to be excelling in the social space, such as Burberry, Diageo andNike, had evolved three newcapabilities to drive their success:community management, contentdevelopment and the tools for real-time analytics.

Vollmer compares effectivecommunity management to being

62%Sixty-two per cent of the world’s

adults use social networks, spendinga massive 22 per cent of their onlinetime scouring channels such asFacebook, Twitter and Pinterest”

‘‘

10

11

a good host at a party.“Brands can’tjust invite fansin; they haveto listen andreward their behaviour with aresponsive, interesting, valuableand attentive social experience.They have to do all this in realtime while reinforcing the brand’spositioning, the unique brandvoice and the company’s businessobjectives,” he says.

According to Matt Park, head ofsocial media at PR agency RedConsultancy, two other brandswhich have understood this earlyon are mobile network O2 andfruit smoothie pioneer Innocent.

“Both do great work – theybehave like their consumers do onsocial media, with an impressivelightness of touch combined withan appropriate level of brandmessaging that never feelsintrusive. Good and bad newstravel fast across social media, and the conversation is always on,”he says.

“Companies that are quick torecognise this are leading thepack. O2’s Twitter responses toconsumer complaints during arecent network outage are a greatexample of how a forward-thinking company can use socialmedia to turn a serious negativeinto a positive.”

Building a connectionWhile community and crisismanagement are accepted as anecessity, the challenge forcompanies seeking to reach newconsumers and push their brand

message further is different. The ability to create authentic, engaging and shareable content or“messages” is key; the kind of con-tent, Vollmer claims, that “buildsan active connection between abrand and its fan community”.

“The most compelling storiesare told by brands that use theinherent properties of social mediato do something they cannot do inother media,” says Ajaz Ahmed,founder and chairman of AKQA,one of the world’s leading digitaladvertising agencies.

“With Twitter, that meansimmediacy. With Facebook, itmeans making a creative, inspiringand useful contribution to thecommunity.”

An excellent example of this isHeinz’s “Get Well Soon” Facebookcampaign. Heinz was able tomonitor status updates and pickout people who said they werefeeling unwell. The food companyresponded by sending out personal-ised cans of soup on Facebook,tapping into the nostalgia aroundthe brand and using social mediato personalise the products.

Burberry is another brand thatappears to have worked out howto add value via unique content. In2011 it streamed a live video feedof its spring/summer andautumn/winter shows, sharingthis exclusive content withmillions of fans and interestedconsumers on Facebook and

YouTube. It alsopremiered anadvert for itsfragrance Body onBurberry.com andYouTube – not on TV. This activity hasseriously reduced thefashion brand’s depend-ence on traditional media,especially print.

“Burberry has committedto being the first ‘digital end-to-end’ company and CEOAngela Ahrendts recognises theneed to be totally connected witheveryone who touches the brand,”says David Cushman, co-founderof social media consultancy 90:10 Group.

Ahrendts herself is blunt. “Ifyou’re not [‘totally connected’] Idon’t know what your businessmodel is going to be in five years,”she says. Burberry’s social strategies have been credited witha 10 per cent rise in same-storesales, so the figures seem to backher up. For many companies,however, proving social campaignsoffer good returns on investmentremains a significant challenge.

“A lot of social media experi-ments and campaigns fail. There’sno getting away from that,” admitsCushman. “They are often ill-conceived, developed without theinvolvement of those for whomthey are intended or any formaladvance evidence-gathering.

Heinz’s “Get Well Soon”campaign picked out people whosaid they were feeling unwell andsent out personalised cans ofsoup on Facebook”‘‘

12

They’re built for broadcast on theassumption that social media willsimply be a free ride.

“In most cases, the boardroomonly looks at the numbers. I’veseen organisations pay hundredsof thousands of pounds toagencies who, for example, wantto make a YouTube competitionwhen the evidence in that nicheor sector suggests customerswon’t join in. When something likethat results in a handful of entriesand very low quality, it’s nowonder boardrooms ask questions.

“But senior teams should notgive up on social media. It’s thedoorway to a powerful newrelationship with customers, butyou have to shift the emphasisfrom yet another medium throughwhich to do stuff to customers toone in which they can join withand do stuff with customers,”says Cushman.

Best plan of action

So how cancompanies guarantee maximumreturn on investment and avoidthe pitfalls? First, it is vital not toslip blindly into the superficial “we do it because the CEO wantsit” approach.

“A common mistake is commit-ting significant budgets to socialmedia initiatives before theaudience is there – a promotionalcampaign using Twitter, forexample, will only pay off if youhave a strong follower communityto start with. Another thing tostay away from is using socialmedia in a way that’s overtly self-promotional – brands’ activityinstead needs to strike a balancebetween being confident and

engaging, yet low-key and partici-patory in tone,” says Cooper.

Another oft-repeated error isfailing to be clear about who ownssocial media output and ensuringthere is sufficient resource to do it properly.

“One of the main pitfalls isassuming that social media issomething that can be owned by ajunior member of the team. It’sessential that it is included in thefull communications structure andmarketing mix and should neverbe left to an individual who doesn’thave the position to push itthrough into other areas of themarketing or PR department. Onits own, social media is oftenweak; as part of the largercommunications strategy, it isincredibly powerful,” says SarahScales, co-founder of PR agency Brands2Life.

Companies also need to knowfrom the outset what they aretrying to achieve and recognisethat simply having a large numberof ‘likes’ on Facebook or followerson Twitter does not necessarilyequate to a successful strategy.

“Social media marketing shouldbe aligned with the business’soverall marketing and communications objectives,”advises Eva Keogan, head ofinnovation at reputation manage-ment firm Fishburn Hedges.

Organisations pay hundreds of thousandsof pounds to agencies who, for example,want to make a YouTube competition whenthe evidence in that sector suggestscustomers won’t join in. When somethinglike that results in a handful of entries andvery low quality, it’s no wonderboardrooms ask questions”

‘‘

Benefits include better marketand customer knowledge;accelerated and moresuccessful innovation; moreastute evidence-based decisionmaking; raised levels of trust –and customer and employeeloyalty and satisfaction”

‘‘

“Metrics should be kept simpleand should be set out during thetesting phase of the social mediastrategy. Many companies look attheir competitors and seek parityor beyond as a way of measuringsuccess, while some look toincrease brand reputation andoverall sentiment towards theircompany and brands. They shouldall be thinking about volume,reach, engagement and conversionand should order these accordingto their key objectives,” she adds.

Great rewardsGet the approach to social mediaright and the rewards can besignificant. Benefits include bettermarket and customer knowledge;accelerated and more successfulinnovation; more astute evidence-based decision-making; raisedlevels of trust – and customer andemployee loyalty and satisfaction.

“The benefits of getting it rightin social media are the same asany marketing channel,” saysMortimer. “Brands that get it rightfind better engagement with theirconsumers, new opportunities forbusiness and new customers. Butlike most things, social media isonly one channel and it is probablybest used in conjunction withother communication or customerservice methods.”

One thing is certain: theconstant flux and change in socialmedia means the goalposts willmove as new platforms such asInstagram, Pinterest andFoursquare take hold. But, even asthe rules change, companies needto remain engaged. Otherwise,they risk being left behind n

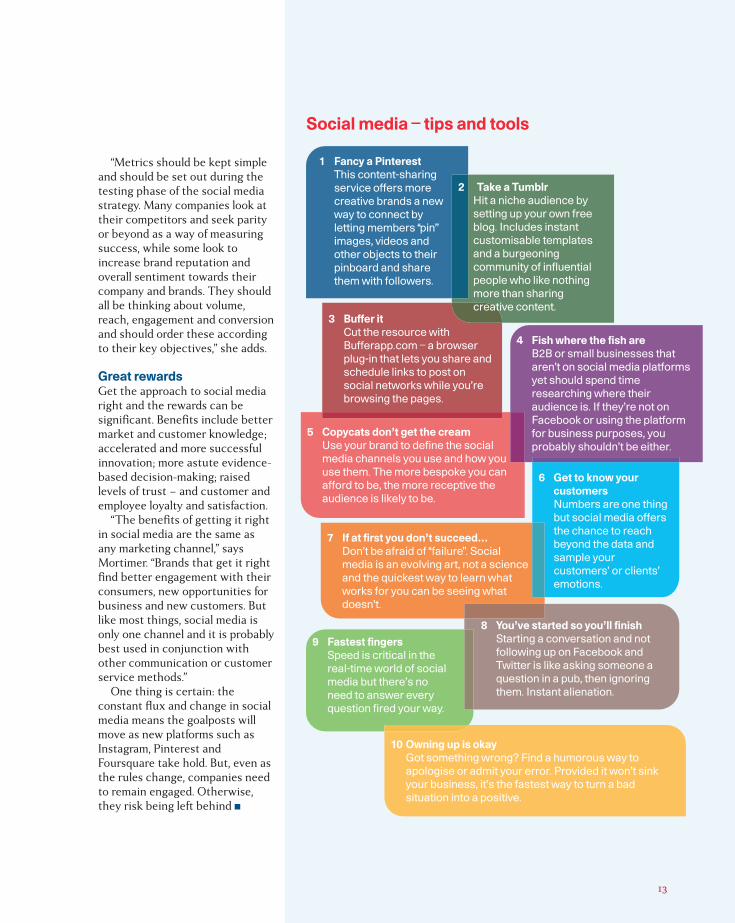

Social media – tips and tools

9 Fastest fingersSpeed is critical in thereal-time world of socialmedia but there’s noneed to answer everyquestion fired your way.

3 Buffer itCut the resource withBufferapp.com – a browserplug-in that lets you share andschedule links to post onsocial networks while you’rebrowsing the pages.

10 Owning up is okayGot something wrong? Find a humorous way toapologise or admit your error. Provided it won’t sinkyour business, it’s the fastest way to turn a badsituation into a positive.

6 Get to know yourcustomersNumbers are one thingbut social media offersthe chance to reachbeyond the data andsample yourcustomers’ or clients’emotions.

4 Fish where the fish areB2B or small businesses thataren’t on social media platformsyet should spend timeresearching where theiraudience is. If they’re not onFacebook or using the platformfor business purposes, youprobably shouldn’t be either.

5 Copycats don’t get the creamUse your brand to define the socialmedia channels you use and how youuse them. The more bespoke you canafford to be, the more receptive theaudience is likely to be.

7 If at first you don’t succeed…Don’t be afraid of “failure”. Socialmedia is an evolving art, not a scienceand the quickest way to learn whatworks for you can be seeing whatdoesn’t.

8 You’ve started so you’ll finishStarting a conversation and notfollowing up on Facebook andTwitter is like asking someone aquestion in a pub, then ignoringthem. Instant alienation.

1 Fancy a PinterestThis content-sharingservice offers morecreative brands a newway to connect byletting members “pin”images, videos andother objects to theirpinboard and sharethem with followers.

2 Take a TumblrHit a niche audience bysetting up your own freeblog. Includes instantcustomisable templatesand a burgeoningcommunity of influentialpeople who like nothingmore than sharingcreative content.

13

14

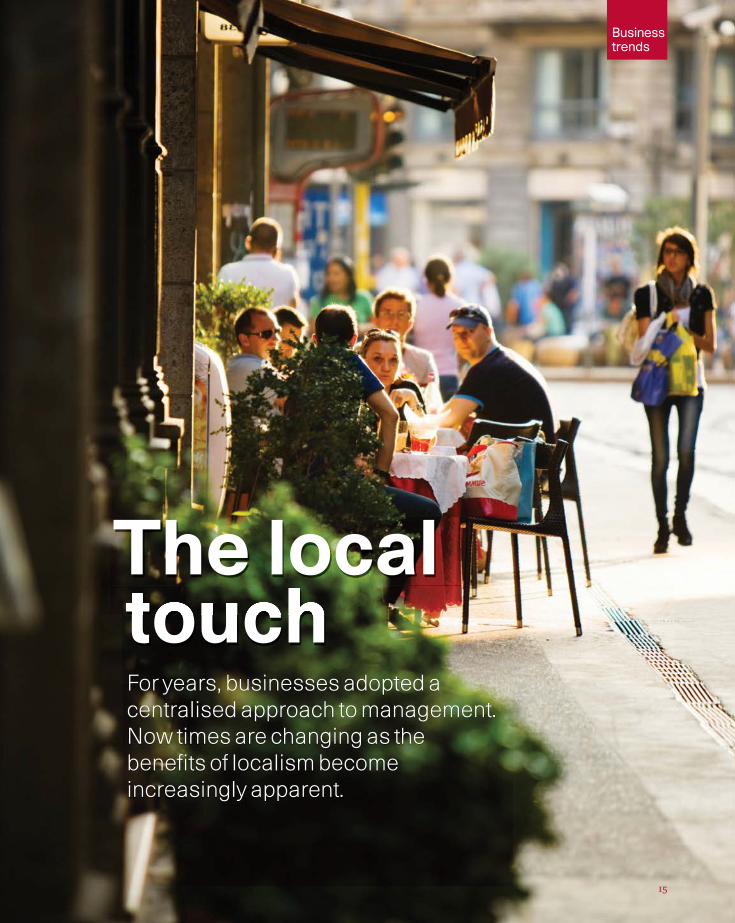

Businesstrends

15

touchThe local For years, businesses adopted acentralised approach to management.Now times are changing as thebenefits of localism becomeincreasingly apparent.

ocalism used to bealmost a bywordfor amateur. Fordecades, consumer-facing companiesstrove to deliverbrand consistencyand uniformity

through centralisation and top-down management. Now, however,the retail industry is waking up tothe very real benefits thatlocalism can bring. As consumerschafe against the uniformity oftoday’s high streets, businessesare starting to recognise that amore local approach can wincustomers and generate income.

“Localism has become a lotmore important,” says NeilSaunders, retail analyst atresearch group Columino. “Theidea that you set a commonstandard at the centre of a retailorganisation and roll it out to allthe stores needs to be temperedwith some sensitivity. Nationalchains have to come to terms withthis or risk a consumer backlash.”

The rest of Europe is signifi-cantly ahead of the UK in thisrespect, in part because the retailsectors in Italy and France, forexample, are far more fragmentedthan in the UK.

“There is a much more concen-trated retail environment inBritain,” says Saunders. “AlthoughFrance and Italy do have big

players, there are many moreindependent retailers and a prolif-eration of local store groups.”

Certain retailers are nowstarting to adopt a more Europeanapproach. Companies such asWaitrose, part of the John LewisPartnership, try to source locally,and John Lewis has recentlythrown open spare rooms in itsdepartment stores for use by localcharities and health and artsgroups. Announcing the initiativeearlier this year, John Lewis man-aging director Andy Street said:“We’d like our shops to become aplace where the community ishappy to spend time, for use as agenuine resource.”

Saunders agrees. “Opening upthe stores is a very good way tosay to the local community, ‘We’rehere for more than just selling youstuff; we’re part of you.’ Retailersare recognising that this is theway to go.”

Vive la différenceThis change in mindset is drivenat least in part by customers, whohave become increasingly dissatisfied with supersized,uniform high-street chains. Tesco,the world’s third-largest retailer, isconstantly criticised for killing offlocal retailers. News of a newTesco store opening can sparklocal protests and other largechains experience similar attacks.

Following fierce local opposition,Costa Coffee, for example, hasabandoned plans to open a branchin the small Devon town ofTotnes, which prides itself on athriving high street packed withindependent retailers.

The sheer size of Tesco makesit harder to pursue a localapproach, but the group iscertainly demonstrating a willing-ness to try with its latestdiversification into the boomingcoffee-shop market.

The retail giant is launching achain of “artisan” coffee shops –but is not doing so under its ownname. Instead, it has taken a 49per cent stake in the newbusiness, Harris and Hoole,named after two coffee-housewits featured in Samuel Pepys’sdiary. The H&H shops will be runas local businesses by Tesco’spartners in the venture; they willdisplay no sign of the supermarketgroup’s involvement and will bepromoted as family-run.

Tesco is clearly trying hard tomove away from the anonymous,identikit approach to the highstreet but in Spain, Spanishfashion chain Zara has provedthat large, successful retailers canstill have serious local credentials.Unlike its fashion rivals, whichsource most of their productsfrom Asia and Africa, Zaraproduces around half its clothes

L

16

in local factories in Spain andPortugal and another 25 per centin the rest of Europe. By keepingclose to its main markets, Zara,owned by Inditex, has been ableto capitalise on fashion trends and is renowned for being able totake an item from a designer’sdrawing pad to the shop floor inlittle more than a fortnight.Retailers that source from Asiasimply cannot compete on speed,allowing the Spanish chain to take full advantage of ficklefashion trends.

Another retail giant, Amazon, isalso tapping into the localismtrend. Having successfullylaunched a similar service in theUS last year, it has just launchedAmazonLocal in London, a dealswebsite offering discounts onlocal services and productsranging from spa days to flyinglessons and meals out. Customersare targeted with deals from localretailers and London has beendivided into six areas: Central,North, East, West, Southeast andSouthwest. Initially available onlyin London, the aim is to roll outAmazonLocal across the UK andmaybe further afield thereafter.

There are many kinds oflocalism across Europe, from theburgeoning farmers’ marketsmovement to the growing numberof hyper-local news websites andlocal bloggers.

The rise of local currencyIn Germany, monetary localism ison the rise, with a proliferation ofmicro-currencies throughout theregions, such as the Chiemgauercurrency in Bavaria. It started lifenine years ago as a school projectand has grown into the world’smost successful alternativecurrency, with a turnover of morethan €5 million a year.

Christian Gelleri wanted apractical way to teach his studentsabout money, so he got them todesign their own vouchers for useby local shoppers and traders. TheChiemgauer is pegged to the eurobut its value depreciates by 2 percent every three months, whichencourages people to spend itmore quickly. It’s estimated thatthe Chiemgauer circulates almost three times faster than theeuro, which boosts trade and thelocal economy. More than 600traders in the region now acceptthe currency.

In Britain, the Brixton poundwas launched three years ago aspart of an effort to boost the localeconomy – thenotes changehands in the sameway as sterlingbut, as they arenot validelsewhere, thecash stays withinthe neighbourhood.

Similar schemes exist elsewherein Britain – the Totnes pound, theStroud pound and the Lewespound. None has been assuccessful as the Chiemgauer butthis may reflect Britain’scentralised approach to govern-ment, which has proved a drag onmany local initiatives in recentyears.

“Britain has one of the mostcentralised tax and spendingsystems in the developed world –well under 20 per cent of localauthorities’ revenue is raisedlocally compared with an averageof over 60 per cent across Britain’sG7 competitors,” says formerTreasury economist MikeDenham, a research fellow at theTaxpayers’ Alliance.

Raising more money locallywould give far greater power tolocal authorities and would bringhuge savings, he believes, asauthorities would then be able toshape things for the local market.“There needs to be a closer linkbetween those who pay and thosewho benefit,” he suggests.

Unlike its fashion rivals, which source mostof their products from Asia and Africa, Zaraproduces around half its clothes in localfactories in Spain and Portugal and another25 per cent in the rest of Europe”

‘‘

17

1818

Transfer of power David Boyle of the NewEconomics Foundation sayslocalism will never be trulyeffective unless there is a transferof economic as well as politicalpower. Britain lags well behind therest of Europe in terms of localbanking, with only 170 local banksper one million people in the UK,compared with 960 in France and520 in Germany.

“Localism is about power. It’snot enough just to get close to thecustomers. How much of thefinancial crisis was driven bytarget numbers? That is a tool ofcentralisation – managers justdon’t think about anything else.Where are the skills of bankmanagers? They don’t manage anymore and banks are not banks anymore – they are conglomeratesrun by risk software. Without localknowledge, they are flying blind,”says Boyle.

Now, however, change is afoot.Large clearing banks are trying toregain a more local approach tocustomers while newcomers, suchas Metro Bank, are makinglocalism a priority. The first newbank to open its doors on theBritish high street in more than acentury, Metro prides itself onbeing different.

Customers areoffered a traditionalface-to-face servicewith no need to bookappointments; branches areknown as “stores” to highlight thecommitment to customer serviceand they open early and close late,seven days a week, again inimitation of successful retailers.

Derek Granville, local managerat Metro’s flagship store inLondon’s Holborn district,explains: “The word local is in mytitle, and there’s a reason for that.When I worked for other banks, Ijust felt like a number. It wasgetting more and more restrictiveas banks centralised everything.They got further and further awayfrom what’s right for the customer,for the community, and that’s whatneeds to be reversed.”

Metro stores are large so thebank can offer space to the localcommunity for events and exhibi-tions. And, unlike other banks,Metro employees do not havesales targets – they havecustomer service targets instead,and that includes volunteering inthe community. Metro managersalso have a high degree ofautonomy so they can makedecisions based on local ratherthan centralised parameters.

Boyle believes this is animportant, and overdue, develop-ment. “Small businesses are cryingout for finance and decentralisingdecision-making would make areal difference,” he says. “Europe isnot without its problems but atleast they have banks with localknowledge and are prepared toback local enterprises. That’s ahuge advantage for theireconomies.”

Localism is still a relatively smallmovement but momentum isgrowing. As internet purchasessoar, consumers, perhapsironically, seek a contrast from theanonymity of the web. They wantto feel part of their community.They want to buy products andservices from people who knowthem. They want face-to-facecontact and recognition. Thosebusinesses that can and dorespond are most likely to benefitover the coming years n

In Bavaria, the Chiemgauer alternativecurrency circulates almost three times fasterthan the euro, which boosts trade and thelocal economy. More than 600 traders in theregion now accept the currency”

‘‘

The future is out there

In myopinion

Predicting the future is not easy – but it’s abusiness necessity. Magnus Lindkvist

explains how companies can avoid predictivepitfalls and best position themselves for the

years ahead.

19

20

n this turbulent age, it has become fashionableto claim that we cannot predict the future – theworld is too complex, interconnected and

volatile to make any meaningful prophecies aboutwhat lies ahead. However, political leadership, life-altering decisions and, above all, running a businessrequire us to make bets on what we think will happenbeyond tomorrow.

Besides, the notion that nothing can be predictedsimply isn’t true. From tennis ball trajectories todemographic shifts, we have quite a good idea of what the future will look like. What is clear, however,is that many ‘predictioneers’ make common mistakeswhen they try to anticipate the road ahead. More specifically, there are five common fallacies andpitfalls that interfere with the way we see the future.

1. The narrative trapThe future is often told as a story, one that simplifiesa complex reality and makes us see the present in newways and ask new questions. Good storytellingrequires a captivating narrative and this presents thefirst stumbling block because a cluttered, contradic-

tive reality doesn’t obey narrative simplicity. We tend to make the future a moral tale where the

things we have created take their revenge – think ofthe number of erroneous doomsday scenarios such asY2K, which sounded frightening but turned out to beuntrue. Businesses are also prone to adoptingnarratives that sound great (“We intend to be theGoogle of B2B services”) but have little relationship toreal-world costs and revenue flows. Conversely, manythings that didn’t work in theory or focus groups –such as Wikipedia or Red Bull – turned out to befantastic in practice.

2. Reducing the futureWhen we use the phrase “the future”, it’s easy to over-simplify. People make bold claims like “the future ofmedia is about three things: digital, social and mobile”.Simplifications are seductive because they reducecomplexity but when it comes to describing thefuture, diversity – not convergence – is the rule. Thenumbers of musical genres, TV channels and businessmodels, for example, have exploded in scope andvariety over the past decades.

When we position the future as a zero sum game – where either East or West, fossil fuels orrenewables, IOS or Android, will win it all – we fail totake co-existence into account. Vinyl records, forexample, have been the one of the fastest-growingmusical formats in the past decade, despite the digital revolution.

3. Add-on futureWe tend to use the present as a base line whenthinking about the future. Now is the norm and whatlies ahead will merely be variations of now. The futurewill therefore be about things such as flying cars,humanoid robots, megacities and more extremevariations of technologies that already exist.

Similarly, we think the problems that we worryabout – from climate change to the euro crisis – willalso be what our grandchildren will wrestle with. Sowe limit our thoughts to what we can relate to todaybecause we cannot relate to the unseen, the abstractor the not-yet-invented. To quote Karl Popper: “Wecannot know what we will know in the future becauseif we could, we would know it now.”

4. Blinded by historyA sage once said: “Forget the past and lose an eye.Dwell on it and lose both eyes.” We frequently use thepast to guide us into the future – think economistsand management consultants – yet maps of the pastcan be misleading. The internet is not just a new kindof telegraph; future wars will not be reiterations ofWorld War II; Lady Gaga is more than just a NewMadonna; and so on. Think of how many investments

I

Historical analogies make peoplesound smart but close our eyes toreal progress – where theimpossible all of a sudden becomes possible”

‘‘

went awry because the industry structure seemed tohave something in common with something we hadseen before yet turned out to have nothing incommon with the past.

Historical analogies make people sound smart butclose our eyes to real progress – where the impossibleall of a sudden becomes possible. If history alwaysrepeated itself, we would have a global outbreak ofbubonic plague every decade.

5. The future as a fixed destinationThe future isn’t a place. In fact, there is no such thing as the future – there are only futures. However,we often hear statements about what lies ahead as ifit is out there, waiting for us to arrive. Morealarmingly, people seem to feel entitled to the futurethese days. Technological marvels and innovationswill arrive by themselves and all we need to do is sitback and enjoy the ride. Instead of becoming amotivator, the future incapacitates.

We need to change the way that people approachthe coming decades. The future is neither a place nor a set date. It’s a state of mind that we should useto inspire ourselves and others into action; to findthe courage to experiment with new solutions;to open our minds to what might come and,of equal importance, what should fall bythe wayside.

The past few years have frightened manycompanies into survival mode, where all they focus onis the present and how to run it more efficiently. Theycompete but they don’t create. Fear is the biggestenemy of progress and to break out from the prison ofthe present, we should revisit three important strandsof business DNA. The first is experimentation, themother of all inventions. From pharmaceuticals andutilities to high-tech and retail, it was often random –even life-threatening – tinkering that built today’sbusiness powerhouses. Secondly, experiments oftenfail but instead of ridiculing failures, we should recycle them.

The future rarely arrives when it should. Think ofCharles Babbage’s computing machine in the mid-1800s. He conceived a computer a century before itcould be built. Failures are often the right idea withthe wrong ingredients or timing. We should learn fromthem and recycle them.

Patience mig

ht just be capitalis

m’s

missing in

gredient”

‘‘

21

22

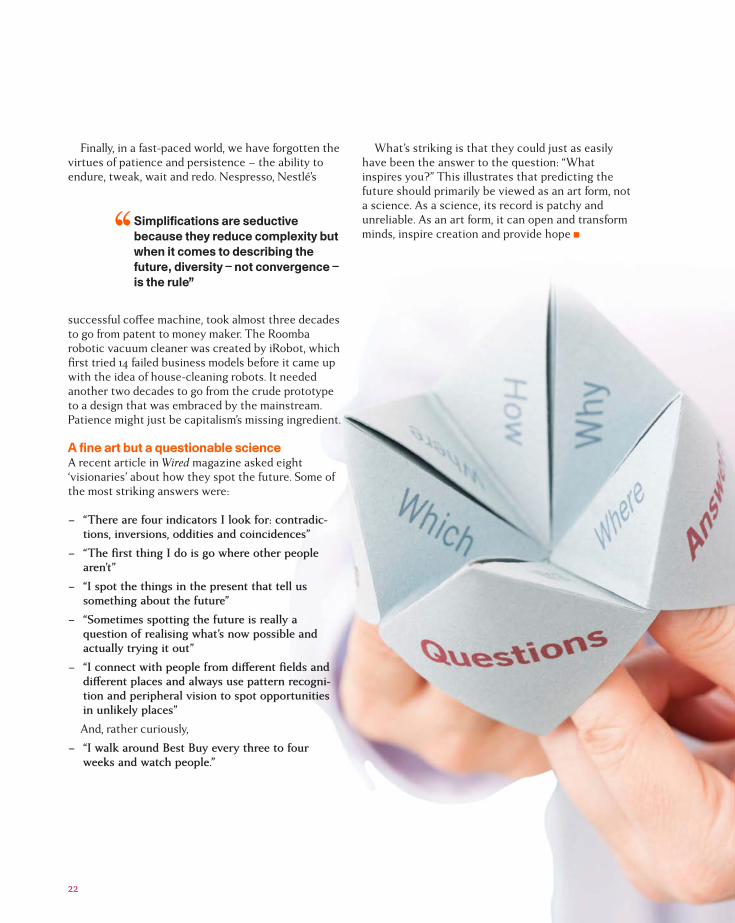

Finally, in a fast-paced world, we have forgotten thevirtues of patience and persistence – the ability toendure, tweak, wait and redo. Nespresso, Nestlé’s

successful coffee machine, took almost three decadesto go from patent to money maker. The Roombarobotic vacuum cleaner was created by iRobot, whichfirst tried 14 failed business models before it came upwith the idea of house-cleaning robots. It neededanother two decades to go from the crude prototypeto a design that was embraced by the mainstream.Patience might just be capitalism’s missing ingredient.

A fine art but a questionable scienceA recent article in Wired magazine asked eight ‘visionaries’ about how they spot the future. Some ofthe most striking answers were:

– “There are four indicators I look for: contradic-tions, inversions, oddities and coincidences”

– “The first thing I do is go where other peoplearen’t”

– “I spot the things in the present that tell ussomething about the future”

– “Sometimes spotting the future is really aquestion of realising what’s now possible andactually trying it out”

– “I connect with people from different fields anddifferent places and always use pattern recogni-tion and peripheral vision to spot opportunitiesin unlikely places”And, rather curiously,

– “I walk around Best Buy every three to fourweeks and watch people.”

What’s striking is that they could just as easilyhave been the answer to the question: “Whatinspires you?” This illustrates that predicting thefuture should primarily be viewed as an art form, nota science. As a science, its record is patchy andunreliable. As an art form, it can open and transformminds, inspire creation and provide hope n

Simplifications are seductivebecause they reduce complexity butwhen it comes to describing thefuture, diversity – not convergence –is the rule”

‘‘

In the spotlight

Rising prices and falling incomes have dealt a heavy blow to companies andconsumers across Europe. But pockets of opportunity remain for nimble andquick-thinking businesses.

Easing the squeeze

24

ancy making a sausage? Youdo? It’s your lucky day. Forjust £8.99, you can buy

everything you need to craft a finebatch of bangers: a piping bag,seasoning, and, of course, 13 feet of “casing”. Cramming mincedmeat into a few metres of beefsleeve may not be a universallyappealing concept, but it doeshave its fans. Just ask UK retailerLakeland. The kitchen-gadgetmaker this summer launched itssausage-making kit range to targeta growing part of the population,the “squeezed middle”.

Increasingly, working familiesare stuck in a pincer betweenfrozen or barely rising wages andthe soaring cost of everydaybasics, such as food, electricityand petrol. Disposable incomes areshrinking, and with respitenowhere in sight, Lakeland hasseen a dramatic shift in buyingpatterns as families eschew nightsout and eat in instead.

Lakeland is just one of manycompanies scrambling to adjust tothe new reality. Indeed, four yearsafter the collapse of LehmanBrothers started the inexorableslide into the economic mire,executives no longer view currentconditions as a blip. And thehardest-hit part of the populationis the middle – the backbone ofthe consumer economy.

In the UK, for example, dispos-able incomes for the middle fifth ofBritish households shrank by 4.3per cent between 2009 and 2011, adecrease of about £1,100 per home.As Andy Clarke, president andCEO of Asda, which is part of theworld’s largest retailer Walmart,explained recently: “In real termsUK families have less cash in theirpockets than they did a year ago –

and when you take a two-yearview it’s clear we’re facing thelongest consecutive decline indisposable income since the 1920s.”

The same picture can be seenacross Europe. Spain and Greeceare grappling with youthunemployment rates of more than50 per cent, while even inGermany, allegedly the engine of asputtering Europe, the jobless tallyrose in August for the fifthstraight month.

Flexible approachFor businesses trying to thrive insuch a market, prospects can seemvery bleak. But the key to successappears to be flexibility because,when money is tight, buyers arechoosier about how they spend it.

Take gyms – an expense thatvery much falls in the nice-to-havecategory. When itis a choicebetween aweekend shop atthe grocery storeand another £100in monthlymembership dues,the gym moreoften than notloses out. Some prominent chainshave been wiped out but othersare flourishing. The Gym Group, aprivate business founded in Britainfour years ago, has grown to nearly30 sites and plans to top 150within five years. Its secret issimple. Rather than insisting onlong-term membership contractsthat big chains prefer – and manycustomers loathe – The GymGroup offers month-to-monthdeals for as little as £11. Suddenly,the gym doesn’t feel like an extravagance – and membership is growing.

Retailer Majestic Wine has alsorevamped its offer to assuagecustomers who find themselvesless well off than before recessionstruck. Initially, the company wassavaged by the downturn – itsprofits halved in 2009, comparedto the previous year. So the groupcut its minimum-buying require-ment from a dozen bottles to six.The results have been dramatic. InJune the company revealed £23.2million in annual pre-tax profits,three times the low point it hitjust three years before.

Neither The Gym Group norMajestic was particularly revolu-tionary. But both benefited fromchanging their business models ina timely fashion – adapting to amarket that has fundamentallyshifted. A sluggish response canbe deadly: Majestic’s two big rivals,

Oddbins and Threshers, bothcollapsed as the economicdownturn took hold.

Others would do well to learnfrom their mistakes becauseeconomic winds do not look to bechanging anytime soon. Govern-ments across Europe areattempting to stimulate theireconomies but most schemes haveproved to be damp squibs becausethey coincide with austeritymeasures that in one way oranother eat into disposableincomes. And, to make mattersworse, the cost of essentials is

F

Rather than insisting on long-term member-ship contracts that big chains prefer – andmany customers loathe – the Gym Groupoffers month-to-month deals for as little as£11. Suddenly the gym doesn’t feel like anextravagance – and membership is growing”

‘‘

25

continuing to rise. Householdenergy bills have doubled in thelast five years. A catastrophicdrought in America has drivencorn and soya prices to levels lastseen in 2008 and the oil price ishovering at around twice its levelfive years ago.

Discount dealsBut there are pockets of opportu-nity amid the gloom. Discounters,for example, used to be below theradar of middle-income earners.Now they have stepped in toprovide an alternative for hard-uphouseholds. Poundland, theemporium where everything froma tent to toilet cleaner costs £1,has been one of Europe’s biggestsuccess stories. The retailerrecently opened its 400th storeand has seen weekly customernumbers soar to four million – ajump of 500,000over last year.Annual profitshave leaptby a quarter.

The contrast with Tesco,Europe’s second-biggest retailerafter Carrefour, could not be morestark. This year, the supermarketgiant reported its first drop inBritish profits in two decades,largely because it was too slowto recognise the changingstresses on its customers. It is atestament to just how profoundthose changes are that Tesco,once synonymous with lowprices, is being undersold andout-serviced by rivals.

Like Aldi. The Germandiscounter has, for sometime, been the fastest-growing supermarket groupin the UK. Its combination ofrock-bottom prices,broadened product range,and a migration to high-income areas it would havepreviously overlooked haswidened its appeal.

Rock-bottom prices aren’t theonly way to get ahead. In hardtimes, escapism sells.Ambassador Theatre Group, Britain’s biggesttheatre chain, recently reported a 70 per centincrease in annual operating profit”

‘‘

26

The group has also benefitedunexpectedly from other factors atwork on the squeezed middle.Clive Black, analyst at investmentfirm Shore Capital, explains: “Thehigh cost of fuel influencedconsumer behaviour and encour-aged a lot more local and smallstore shopping. With its circa10,000 square foot outlets, Aldi’sstores have been at the right placeat the right time.”

The situation is similar acrossthe EU. Metro, the Germanretailing giant, announced a fresh round of job cuts in July assales slowed. Car manufacturerssuch as Opel, meanwhile, havedipped back into the reducedhours working system known as“Kurzarbeit”, which allowscompanies to cut hours while the government pays part of the difference.

It is not always so easy tochange the rules. Spain wasrocked by widespread protestsearlier this year after the govern-ment passed labour reforms tomake it easier and cheaper to layoff workers. But winners andlosers are emerging. El CorteIngles, the high-end departmentstore that traces its roots back tothe 1930s and is seen as abarometer for the wider economy,unveiled a sharp drop in 2011 sales.Discounters Dia and Mercadonastepped into the void. Both havereported big sales jumps.

Escape routesRock-bottom prices aren’t the onlyway to get ahead. In hard times,escapism sells. AmbassadorTheatre Group, Britain’s biggesttheatre chain, recently reported a70 per cent increase in annualoperating profit thanks to hitssuch as Dirty Dancing and Ghostthe Musical. It is true that thecompany discounts tickets, buteven the cheapest are still dearerthan a typical trip to the cinema.The most expensive can run to£100 or more.

And for those who find itdifficult to separate the massesfrom their cash in Europe, Chinaprovides at least some relief. BigEuropean brands such as HugoBoss, Hermes and Christian Diorare booming, thanks to soaringsales in the middle kingdom.Erwan Rambourg, analyst atHSBC, says: “In the late 1990s, theluxury industry (and we were partof it back then) coveted China buthad barely scratched the surfaceof its potential. Today, Chineseconsumption dominates thesector’s global sales.”

The web has proved anotherefficient way to cope. Next, theUK fashion chain, recentlyunveiled a drop in annual like-for-like sales but the company has

spent time and money building upits online offering. The result is asite that is intuitive and genuinelyconvenient – rather than justbeing a web version of the shopfloor that some companies settlefor. Customers have respondedand internet sales are increasing atdouble-digit rates.

Jon Copestake, analyst from theEconomist Intelligence Unit, says:“Next’s results reflect the exacttrends underpinning the retailmarket at present. The chain hasseen declining like-for-like salesand weak growth in its bricks-and-mortar operations but benefitsstrongly from a multi-channelapproach, which has seen adouble-digit growth in online and catalogue sales. Offeringdelivery or store collection fromonline channels has fitted into aflexible, consumer-friendlyapproach to services.”

Whether it is building up a webpresence or overhauling long-heldpractices to cater for a changedmarket, there are ways to tap intoseams of opportunity. It seemsclear, however, that the era when arising tide lifted all boats is unlikelyto return for a good few years.Perhaps it is time to brush up onthose sausage-making skills n

El Corte Ingles, the high-end department store that tracesits roots back to the 1930s and is seen as a barometer forthe wider economy, unveiled a sharp drop in 2011 sales.Discounters Dia and Mercadona stepped into the void.Both have reported big sales jumps”

‘‘

27

Face to face

Dr Martin Wienkenhöver is CEO of CABB, an industrial chemicals companyheadquartered outside Cologne. A chemist by training, Wienkenhöver hasspent more than two decades in the sector. But his career could have beenradically different.

28

29

The chief executive of Germany-based industrialchemicals manufacturer CABB intended to play thetrumpet professionally when he left school, butrethought his future after a conversation with hisforthright trumpet teacher.

“My teacher told me you should not make yourhobby into a profession, which was a gentle way ofsaying I was not good enough,” says Wienkenhöver.

“He said to me: ‘I work at the weekend when otherpeople are enjoying themselves instead of being withmy family, and the rest of the week I give lessons tochildren who don’t really want to come. Do you wantthat?’ I thought to myself: you should listen whensomeone tells you something like that. I neverregretted it.”

Foregoing a glamorous life as a star trumpet player,Wienkenhöver took the sensible option and acquireda doctorate in chemistry from the University ofMünster, Germany.

He later joined the dyestuffs division of Bayer as ahands-on production chemist, eventually rising to theboard of Bayer Chemicals. In 2005 Wienkenhöverhelped to spin off that business, which subsequentlyfloated on the Deutsche Borse under the name ofLanxess. The job was the perfect preparation for lifeat CABB, a speciality chemicals business created bymerging the non-core subsidiaries of severalcorporate giants.

Wienkenhöver joined the business in 2010, andsoon after his arrival he oversaw the sale of thebusiness to Bridgepoint in a classic buy-and-buildprivate equity deal.

“At the time I was 54 years old and I’d been in thechemical industry for 20-plus years. I thought it was agood challenge to take on,” he says.

Careful husbandryThe CABB production facility in ChemieparkKnapsack near Cologne is about as far removed as itis possible to be from the louche, smoke-filled jazzbar a young Martin Wienkenhöver might havedreamed of. Sited on a sprawling industrial park, theplant produces CABB’s mainstay, monochloroacetic

acid, an industrial chemical used by manufacturers tomake everything from agrochemicals to make-up.

Wienkenhöver spends most of his time at an officeat CABB’s corporate headquarters more than 200kilometres away in Sulzbach near Frankfurt. The longhours that he works leave him little time for trumpetpractice but he insists that despite appearances,there is art in chemistry.

“I have always really liked natural sciences and therelation to theory. You have to memorise a lot, butthere’s also this craftsmanship part,” he says.

“If, for example, you have to build a 20 metre-highcolumn made out of glass pieces and make sure itdoesn’t crack, even when it heats up and expands,there is real craftsmanship in that. And I was always ahandyman; I learned from my father.”

CABB certainly requires careful husbandry. Theemphasis across the group – which has its heart inGermany and Switzerland, but stretches from Finlandto India – is on safely managing the productionprocess and paying close attention to detail tooptimise performance and productivity.

“As a technical manager in one of our factories, firstyou would look at our mid-term production plan.There’s a whole bunch of logistics to be taken care of.The utilitieshave to bethere to heatand cool theequipment. Allthe ingredientshave to bethere. Thesafety has to betaken care ofand that has togo through the whole process,” says Wienkenhöver.

“Then there’s the other part, where you arepermanently thinking: what can we do better than weare doing now? What can we do to reduce thereaction time? Or change the sequence to utilise theexisting equipment to get more tonnes, which meansmore sales and greater returns.”

n another life Dr Martin Wienkenhöverwould have been a professionaltrumpet player. I

The CABB production facility inChemiepark Knapsack nearCologne is about as far removedas it is possible to be from thelouche, smoke-filled jazz bar ayoung Martin Wienkenhövermight have dreamed of”

‘‘

30

From his office, Wienkenhöver manages all theseissues at a macro level.

“We are looking for opportunities to buy extracapacity because the customers want much morethan we can make. There is no such thing as sparecapacity here – we have to increase our research toget more tonnes out of what we have got.”

Shortly after Bridgepoint’s investment in April 2011,CABB bought KemFine, a custom manufacturingbusiness that added industrial outsourcing foragrochemical and other clients to the company’sroster. The acquisition plugged a key gap in the groupby providing large-capacity batch reactors.

“The technology toolbox was widened and thecustomer relationships expanded. KemFine wasfocusing on big reactors and multi-step operations, sothe business filled the middle piece of a jigsawpuzzle,” says Wienkenhöver.

Hands-on jobCABB has just 1,000 staff compared with more than120,000 at Bayer, but Wienkenhöver says he wasattracted by the challenge of a hands-on job at asmaller business.

“CABB was basically three pieces, which all areunwanted orphans from bigcorporations that are nowintegrated into one consistent business. Allthree were grosslyundermanaged,” he says.

“We are always shootingto make this asset better. In a big corporation, youdoubt sometimes you are working for the same goal.”

CABB now operates two divisions – a bulkmanufacturing division that makes specialitychemicals including monochloroacetic acid andchlorine for a range of industries and a custommanufacturing division that allows other manufac-turers, particularly in agrochemicals, to outsourceparts of their production chain.

Each unit has a distinct geographical and salesstrategy. Custom manufacturing is based in Switzer-land and Finland, where there is a highly educatedworkforce and strong intellectual property laws.

“IP is a critical issue for our customers on thecustom manufacturing side,” says Wienkenhöver.

“They are very worried about us taking production to Asia. They want control and they are saying veryclearly they want our capacity to remain in Europe.Anyway, we are better and more cost-effective than many Asian competitors – our competitor is the customer.”

The bulk speciality chemicals business has no suchIP constraints, so production in emerging marketsmakes sound commercial sense. CABB is alreadyoperating in India and Wienkenhöver is looking toexpand into China too.

Working long days at CABB and living apart fromhis wife during the week, Wienkenhöver is proud that the company’s profit margins are already higherthan any of the businesses that sold off theirunwanted divisions. “The business had a turnover ofaround €310 million when Bridgepoint took over. Wewant to take turnover up to between €600 and €700million,” he says.

Expansion will be by way of organic growth andfurther acquisitions where the opportunity arises.Profit growth, meanwhile, will come from constantlystreamlining and improving operations and the supply chain.

One thing cash will not be wasted on is what herefers to as “corporateoverhead”. With 1,000 staff, fiveplants and four sales offices,CABB employs just 15 people inits corporate headquarters.

“We don’t have many peoplehere to do things. Here, if youwant something done, you do it

yourself,” he says. After a career spent in huge German corporations,

he admits working with private equity has been asteep learning curve.

“It’s about direct management. They absolutely relyon our technical skills, knowledge of the business andknowledge of the customers. But on the other side,we are fortunate to have Bridgepoint’s experience offinancing, banking and regulations. It’s a give-and-take situation but the combination is great,” he says.

Leisure timeAt the weekend Wienkenhöver retreats to his housein Leverkusen, a town close to Cologne, to spend timewith his wife and four children and watch Bayer

The business had a turnover ofaround €310 million whenBridgepoint took over. We wantto take turnover up to between€600 and €700 million”

‘‘

31

Leverkusen, the football club where he is a seasonticket holder.

A poor performance by Leverkusen last seasonmeans there has been no need to take time off forChampions League games this year. But he compen-sates by spending moretime with his children,only one of whom stilllives at home.

“They are all grownup now. One of our sonsis a commercial pilot buthe will soon move toStuttgart and my wife and I will be on our own. Butthe kids are still enjoying Hotel Mum, bringing theirclothes on Friday, getting them ironed and raiding ourfridges,” he says.

Ultimately, Bridgepoint will exit CABB. There are nofirm plans to sell right now but flotation or a tradesale are obvious options.

“A flotation is one possibility. You have to be acertain size to float. The window of opportunity hasto be there, but obviously that would be an attractiveproposition,” says Wienkenhöver.

“Another exit would be a strategic buyer like achemical conglomerate.You could combine theseoperations with existingbusinesses and realisesome synergies. The thirdpossibility is foreigninvestors, Asians –Chinese and Japanese –

or Americans.”With the children nearly gone, the CABB boss is

looking forward to taking it a little easier in years to come.

“I’ll be over 60 soon,” he says. “It will be time to havesome fun n

Name: Dr Martin Wienkenhöver Age: 56Born: Tecklenburg, Germany

EducationDoctorate in natural science (in organicchemistry)

First jobsDevelopment chemist at Bayer,Germany (Dyestuff Divison in 1985)

FamilyMarried with four children

CarBMW 730d

HobbiesTime with the family; trumpet-playing;Bayer Leverkusen season ticketholder; literature; BMW motorcycle(R1200C)

Long-term ambitionDevelop CABB towards successful IPO

Biggest professional achievement Turnaround of distressed chemicalbusinesses

Biggest regretLack of time spent with our childrenwhen they were little

With 1,000 staff, five plants and four salesoffices, CABB employs just 15 people in itscorporate headquarters. We don’t havemany people here to do things. Here, if youwant something done, you do it yourself”

‘‘

Management focus

businessBig

The internet’sunparallelled ability toglean personalinformation is widelyknown. But somecompanies now usethese insights toinfluence both whatthey offer to customersand the prices thatthey charge.

is watching you

32

hen George Orwell wrote his novel 1984,computer technology was almost certainlynot at the top of his mind. But the iconic

novel, with its dystopian images of Big Brother andthe Thought Police, may have foretold the futuremore accurately than most of us care to believe.

Indeed, it may come as a surprise to all but themost tech-savvy web users that Big Brother – or atleast big business – really is keeping tabs on youevery time you venture on to the internet, pay at acheckout counter with a credit card or use yoursmartphone to send a tweet or find directions.

Concern about tracking has fuelled lively debateabout the right of individuals to keep at least some oftheir personal information private. But whether welike it or not, the ability to log and – in most cases –track site visitors has been baked into the mechanicsof the web pretty much since it first began to have animpact in the early 1990s.

Tools to spyWeb developers have long had access to free softwaretools such as AWStats which analyse website trafficand can, for example, tell site administrators the IP(internet protocol) address of a visitor, which countrythey came from, which pages they looked at, howmuch time they spent on a site, and what browserthey were using.

Other free analytics software provides informationon many other aspects of web traffic and websitemarketing. Google Analytics, for example, not onlyenables companies to measure sales and websiteconversions (or customers), but also provides themwith information about how visitors use their sitesand how they arrived on the sites.

There is a wide range of fee-basedanalytic and statistical software too,that companies can use to analysevisitors and model their behaviour.They can also track advertisingcampaigns and invest in fraud analysis,highlighting traffic that may be false.

While these tools may ultimatelyenable companies to deliver useful andrelevant information, the collection,analysis and reporting of user data

without users’ permission or knowledge have madesome tools highly controversial, particularly thosethat rely on so-called third-party cookies that can beshared between websites.

Cookies are small bits of code sent from a websiteand stored on a user’s computer in their web browser.They were developed early on to notify websiteowners when a particular visitor returned to their siteand to recall user information, such as their user preferences or which pages they have visited inthe past.

Most of the time they make online life easier andare essential for the smooth operation of the internet.But cookies and other techniques are also used tobuild up and store anonymous profiles of websitevisitors and their preferences, in order to send moretargeted adverts.

Google account holders can check out how old thecompany thinks they are, whether they are male orfemale, and their interests, by accessing the AdPreferences page. If you think it has made anymistakes, you can correct this information.