Israel Discount Bank of New York

14

October 19, 2016 Israel Discount Bank of New York Analytical Contacts: M Scott Durant, Associate Director [email protected], (301) 969-3248 Joseph Scott, Managing Director [email protected], (646) 731-2438 Christopher Whalen, Senior Managing Director [email protected], (646) 731-2366 U.S. Financial Institutions Bank & BHC Surveillance Report

Transcript of Israel Discount Bank of New York

October 19, 2016

Israel Discount Bank of

New York

Analytical Contacts:

M Scott Durant, Associate Director

[email protected], (301) 969-3248

Joseph Scott, Managing Director

[email protected], (646) 731-2438

Christopher Whalen, Senior Managing Director

[email protected], (646) 731-2366

U.S. Financial Institutions

Bank & BHC Surveillance Report

Israel Discount Bank of New York Page 2 October 19, 2016

Table of Contents

Executive Summary ......................................................................................................... 3

Key Rating Drivers ........................................................................................................ 3

Financial Metrics ............................................................................................................ 4

Comparative Statistics ................................................................................................... 5

Rating Rationale............................................................................................................... 5

Key Quantitative Rating Determinants ............................................................................. 5

Liquidity .................................................................................................................... 6

Asset Quality ............................................................................................................. 7

Capital Adequacy ........................................................................................................ 8

Earnings .................................................................................................................... 8

Key Qualitative Rating Determinants ................................................................................ 9

Market Strategy ......................................................................................................... 9

Risk Management ..................................................................................................... 11

Liquidity Management ............................................................................................... 12

Economic and Regulatory Framework .......................................................................... 12

External Support ......................................................................................................... 12

Outlook ...................................................................................................................... 13

Drivers of Rating Change ........................................................................................... 13

Israel Discount Bank of New York Page 3 October 19, 2016

Executive Summary

Kroll Bond Rating Agency (KBRA) has affirmed the following ratings for Discount Bancorp, Inc.’s

subsidiary, New York, New York based Israel Discount Bank of New York (IDBNY or “the Bank”) based on

KBRA’s Global Bank and Bank Holding Company Rating Methodology published on February 19,

2016.

Ratings

Entity Type Rating Outlook Action

Israel Discount Bank of New York Deposit A- Stable Affirmed

Senior Unsecured Debt A- Stable Affirmed

Subordinated Debt BBB+ Stable Affirmed

Short-Term Debt K2 N/A Affirmed

Short-Term Deposit K2 N/A Affirmed

Discount Bancorp, Inc., a bank holding company incorporated in Delaware, owns 100% of Israel Discount

Bank of New York. Consolidated assets totaled approximately $9.2 billion with deposits of $7.2 billion as of

June 30, 2016. Chartered by the State of New York, IDBNY focuses on middle market commercial banking

activities and private banking for high net worth individuals. Discount Bancorp, Inc. is regulated by the

Federal Reserve.

The Bank’s strategy is to focus on domestic growth in select markets, while maintaining its international

private banking relationships. The Bank has branches in the New York Metropolitan Area, Los Angeles

Area, and Southern Florida. The Bank’s international network includes representative offices in Mexico,

Uruguay, Chile, Peru and Israel to service private banking customers. In late 2015, IDBNY successfully

closed a transaction to transfer all assets ($1.3 billion) and liabilities of Discount Bank Latin America

(DBLA), its Uruguayan retail bank, to ScotiaBank.

IDBNY, through its U.S. parent, Discount Bancorp, Inc., is wholly-owned by Israel Discount Bank Limited

(IDB Ltd.), a $56 billion banking group based in Tel Aviv, Israel. IDBNY is a key operating unit of IDB and

is considered strategically important to the group. IDBNY operates as a standalone bank without any

intercompany risk between it and the ultimate parent, IDB Ltd. IDBNY plans on upstreaming a portion of

net income to the Israeli parent bank subject to comfortably exceeding “well capitalized” U.S. regulatory

capital ratios.

Key Rating Drivers

The ratings for Israel Discount Bank of New York are supported by the Bank’s experienced management

team, strong asset quality metrics, ample liquidity and funding profile coupled with a stable depository

base, and strong capital position. However, these factors are counterbalanced by the Company’s below

average profitability, though improvement is noted over previous years, and reliance upon spread-derived

income. KBRA expects continued improvement in profitability over the medium term combined with a gradual increase in noninterest revenue.

The A- rating of Israel Discount Bank of New York generally maps to a short-term rating of K2 on KBRA’s

short-term rating scale. Consistent with KBRA’s notching guidelines, the assigned rating of BBB+ for

subordinated debt for the Bank is notched one rating below the senior Bank rating.

Israel Discount Bank of New York Page 4 October 19, 2016

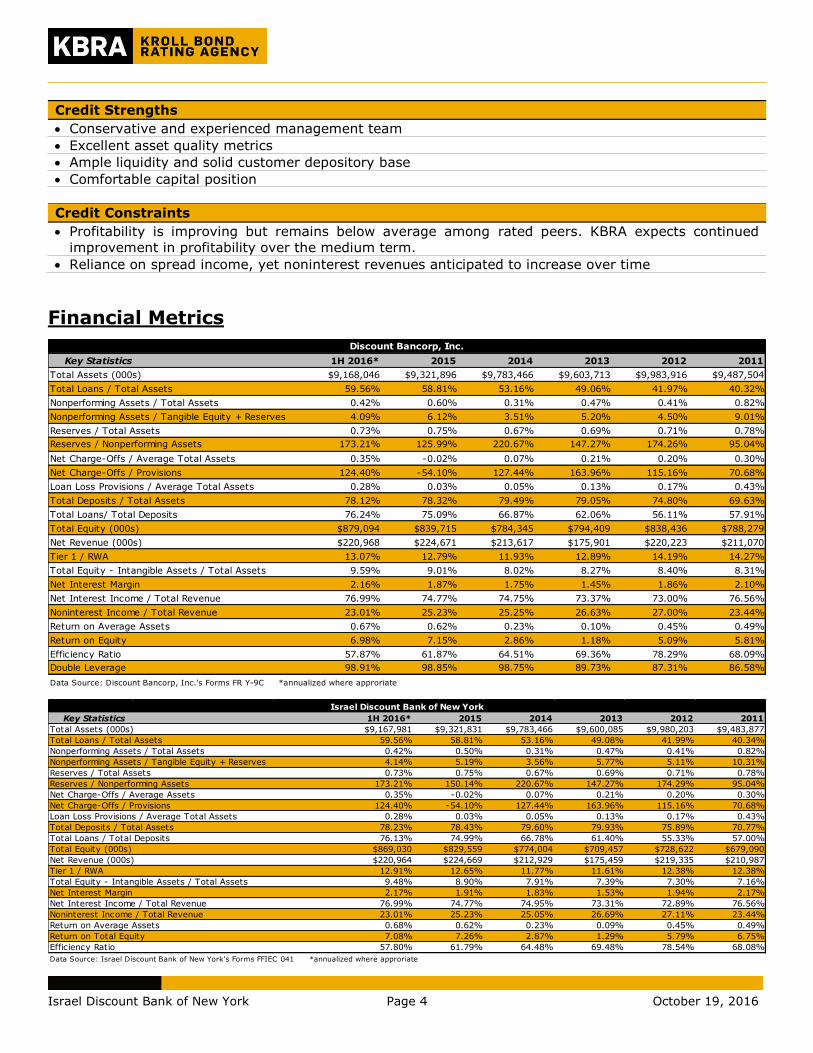

Credit Strengths

Conservative and experienced management team

Excellent asset quality metrics

Ample liquidity and solid customer depository base

Comfortable capital position

Credit Constraints

Profitability is improving but remains below average among rated peers. KBRA expects continued

improvement in profitability over the medium term.

Reliance on spread income, yet noninterest revenues anticipated to increase over time

Financial Metrics

Key Statistics 1H 2016* 2015 2014 2013 2012 2011

Total Assets (000s) $9,168,046 $9,321,896 $9,783,466 $9,603,713 $9,983,916 $9,487,504

Total Loans / Total Assets 59.56% 58.81% 53.16% 49.06% 41.97% 40.32%

Nonperforming Assets / Total Assets 0.42% 0.60% 0.31% 0.47% 0.41% 0.82%

Nonperforming Assets / Tangible Equity + Reserves 4.09% 6.12% 3.51% 5.20% 4.50% 9.01%

Reserves / Total Assets 0.73% 0.75% 0.67% 0.69% 0.71% 0.78%

Reserves / Nonperforming Assets 173.21% 125.99% 220.67% 147.27% 174.26% 95.04%

Net Charge-Offs / Average Total Assets 0.35% -0.02% 0.07% 0.21% 0.20% 0.30%

Net Charge-Offs / Provisions 124.40% -54.10% 127.44% 163.96% 115.16% 70.68%

Loan Loss Provisions / Average Total Assets 0.28% 0.03% 0.05% 0.13% 0.17% 0.43%

Total Deposits / Total Assets 78.12% 78.32% 79.49% 79.05% 74.80% 69.63%

Total Loans/ Total Deposits 76.24% 75.09% 66.87% 62.06% 56.11% 57.91%

Total Equity (000s) $879,094 $839,715 $784,345 $794,409 $838,436 $788,279

Net Revenue (000s) $220,968 $224,671 $213,617 $175,901 $220,223 $211,070

Tier 1 / RWA 13.07% 12.79% 11.93% 12.89% 14.19% 14.27%

Total Equity - Intangible Assets / Total Assets 9.59% 9.01% 8.02% 8.27% 8.40% 8.31%

Net Interest Margin 2.16% 1.87% 1.75% 1.45% 1.86% 2.10%

Net Interest Income / Total Revenue 76.99% 74.77% 74.75% 73.37% 73.00% 76.56%

Noninterest Income / Total Revenue 23.01% 25.23% 25.25% 26.63% 27.00% 23.44%

Return on Average Assets 0.67% 0.62% 0.23% 0.10% 0.45% 0.49%

Return on Equity 6.98% 7.15% 2.86% 1.18% 5.09% 5.81%

Efficiency Ratio 57.87% 61.87% 64.51% 69.36% 78.29% 68.09%

Double Leverage 98.91% 98.85% 98.75% 89.73% 87.31% 86.58%

Data Source: Discount Bancorp, Inc.'s Forms FR Y-9C *annualized where approriate

Discount Bancorp, Inc.

Key Statistics 1H 2016* 2015 2014 2013 2012 2011

$9,167,981 $9,321,831 $9,783,466 $9,600,085 $9,980,203 $9,483,877

59.56% 58.81% 53.16% 49.08% 41.99% 40.34%

0.42% 0.50% 0.31% 0.47% 0.41% 0.82%

4.14% 5.19% 3.56% 5.77% 5.11% 10.31%

0.73% 0.75% 0.67% 0.69% 0.71% 0.78%

173.21% 150.14% 220.67% 147.27% 174.29% 95.04%

0.35% -0.02% 0.07% 0.21% 0.20% 0.30%

124.40% -54.10% 127.44% 163.96% 115.16% 70.68%

0.28% 0.03% 0.05% 0.13% 0.17% 0.43%

78.23% 78.43% 79.60% 79.93% 75.89% 70.77%

76.13% 74.99% 66.78% 61.40% 55.33% 57.00%

$869,030 $829,559 $774,004 $709,457 $728,622 $679,090

$220,964 $224,669 $212,929 $175,459 $219,335 $210,987

12.91% 12.65% 11.77% 11.61% 12.38% 12.38%

9.48% 8.90% 7.91% 7.39% 7.30% 7.16%

2.17% 1.91% 1.83% 1.53% 1.94% 2.17%

76.99% 74.77% 74.95% 73.31% 72.89% 76.56%

23.01% 25.23% 25.05% 26.69% 27.11% 23.44%

0.68% 0.62% 0.23% 0.09% 0.45% 0.49%

7.08% 7.26% 2.87% 1.29% 5.79% 6.75%

57.80% 61.79% 64.48% 69.48% 78.54% 68.08%

Data Source: Israel Discount Bank of New York's Forms FFIEC 041 *annualized where approriate

Efficiency Ratio

Net Interest Margin

Net Interest Income / Total Revenue

Noninterest Income / Total Revenue

Return on Average Assets

Return on Total Equity

Israel Discount Bank of New York

Total Equity (000s)

Net Revenue (000s)

Tier 1 / RWA

Total Equity - Intangible Assets / Total Assets

Total Loans / Total Deposits

Total Assets (000s)

Total Loans / Total Assets

Nonperforming Assets / Total Assets

Nonperforming Assets / Tangible Equity + Reserves

Reserves / Total Assets

Reserves / Nonperforming Assets

Net Charge-Offs / Average Assets

Net Charge-Offs / Provisions

Loan Loss Provisions / Average Total Assets

Total Deposits / Total Assets

Israel Discount Bank of New York Page 5 October 19, 2016

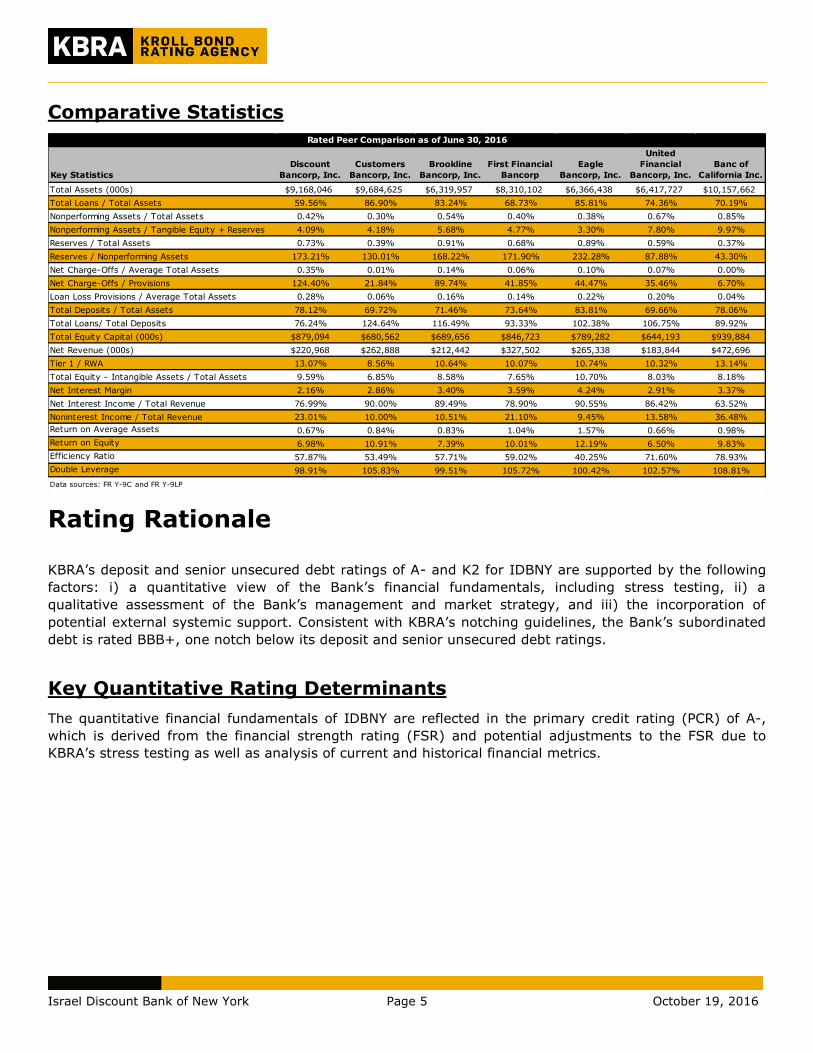

Comparative Statistics

Rating Rationale

KBRA’s deposit and senior unsecured debt ratings of A- and K2 for IDBNY are supported by the following

factors: i) a quantitative view of the Bank’s financial fundamentals, including stress testing, ii) a

qualitative assessment of the Bank’s management and market strategy, and iii) the incorporation of

potential external systemic support. Consistent with KBRA’s notching guidelines, the Bank’s subordinated

debt is rated BBB+, one notch below its deposit and senior unsecured debt ratings.

Key Quantitative Rating Determinants

The quantitative financial fundamentals of IDBNY are reflected in the primary credit rating (PCR) of A-,

which is derived from the financial strength rating (FSR) and potential adjustments to the FSR due to

KBRA’s stress testing as well as analysis of current and historical financial metrics.

Key Statistics

Discount

Bancorp, Inc.

Customers

Bancorp, Inc.

Brookline

Bancorp, Inc.

First Financial

Bancorp

Eagle

Bancorp, Inc.

United

Financial

Bancorp, Inc.

Banc of

California Inc.

Total Assets (000s) $9,168,046 $9,684,625 $6,319,957 $8,310,102 $6,366,438 $6,417,727 $10,157,662

Total Loans / Total Assets 59.56% 86.90% 83.24% 68.73% 85.81% 74.36% 70.19%

Nonperforming Assets / Total Assets 0.42% 0.30% 0.54% 0.40% 0.38% 0.67% 0.85%

Nonperforming Assets / Tangible Equity + Reserves 4.09% 4.18% 5.68% 4.77% 3.30% 7.80% 9.97%

Reserves / Total Assets 0.73% 0.39% 0.91% 0.68% 0.89% 0.59% 0.37%

Reserves / Nonperforming Assets 173.21% 130.01% 168.22% 171.90% 232.28% 87.88% 43.30%

Net Charge-Offs / Average Total Assets 0.35% 0.01% 0.14% 0.06% 0.10% 0.07% 0.00%

Net Charge-Offs / Provisions 124.40% 21.84% 89.74% 41.85% 44.47% 35.46% 6.70%

Loan Loss Provisions / Average Total Assets 0.28% 0.06% 0.16% 0.14% 0.22% 0.20% 0.04%

Total Deposits / Total Assets 78.12% 69.72% 71.46% 73.64% 83.81% 69.66% 78.06%

Total Loans/ Total Deposits 76.24% 124.64% 116.49% 93.33% 102.38% 106.75% 89.92%

Total Equity Capital (000s) $879,094 $680,562 $689,656 $846,723 $789,282 $644,193 $939,884

Net Revenue (000s) $220,968 $262,888 $212,442 $327,502 $265,338 $183,844 $472,696

Tier 1 / RWA 13.07% 8.56% 10.64% 10.07% 10.74% 10.32% 13.14%

Total Equity - Intangible Assets / Total Assets 9.59% 6.85% 8.58% 7.65% 10.70% 8.03% 8.18%

Net Interest Margin 2.16% 2.86% 3.40% 3.59% 4.24% 2.91% 3.37%

Net Interest Income / Total Revenue 76.99% 90.00% 89.49% 78.90% 90.55% 86.42% 63.52%

Noninterest Income / Total Revenue 23.01% 10.00% 10.51% 21.10% 9.45% 13.58% 36.48%

Return on Average Assets 0.67% 0.84% 0.83% 1.04% 1.57% 0.66% 0.98%

Return on Equity 6.98% 10.91% 7.39% 10.01% 12.19% 6.50% 9.83%

Efficiency Ratio 57.87% 53.49% 57.71% 59.02% 40.25% 71.60% 78.93%

Double Leverage 98.91% 105.83% 99.51% 105.72% 100.42% 102.57% 108.81%

Data sources: FR Y-9C and FR Y-9LP

Rated Peer Comparison as of June 30, 2016

Israel Discount Bank of New York Page 6 October 19, 2016

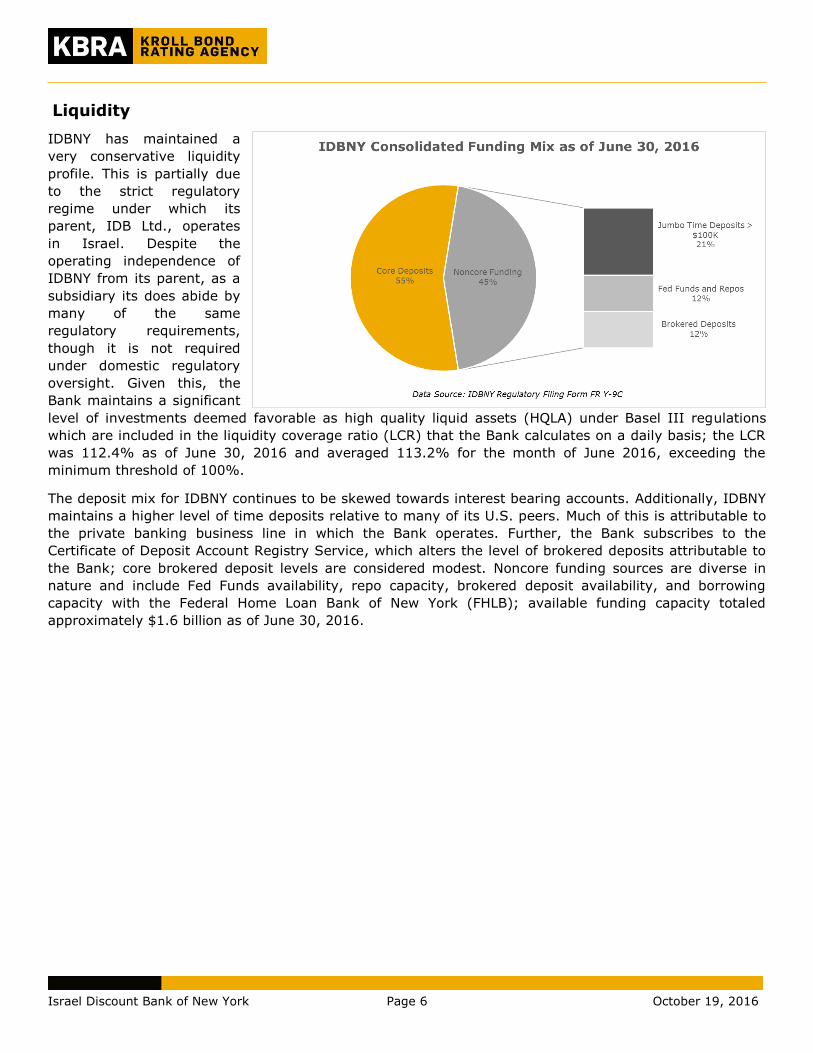

Liquidity

IDBNY has maintained a

very conservative liquidity

profile. This is partially due

to the strict regulatory

regime under which its

parent, IDB Ltd., operates

in Israel. Despite the

operating independence of

IDBNY from its parent, as a

subsidiary its does abide by

many of the same

regulatory requirements,

though it is not required

under domestic regulatory

oversight. Given this, the

Bank maintains a significant

level of investments deemed favorable as high quality liquid assets (HQLA) under Basel III regulations

which are included in the liquidity coverage ratio (LCR) that the Bank calculates on a daily basis; the LCR

was 112.4% as of June 30, 2016 and averaged 113.2% for the month of June 2016, exceeding the

minimum threshold of 100%.

The deposit mix for IDBNY continues to be skewed towards interest bearing accounts. Additionally, IDBNY

maintains a higher level of time deposits relative to many of its U.S. peers. Much of this is attributable to

the private banking business line in which the Bank operates. Further, the Bank subscribes to the

Certificate of Deposit Account Registry Service, which alters the level of brokered deposits attributable to

the Bank; core brokered deposit levels are considered modest. Noncore funding sources are diverse in

nature and include Fed Funds availability, repo capacity, brokered deposit availability, and borrowing

capacity with the Federal Home Loan Bank of New York (FHLB); available funding capacity totaled

approximately $1.6 billion as of June 30, 2016.

Israel Discount Bank of New York Page 7 October 19, 2016

As mentioned previously, the

investment securities portfolio

is mostly centered in

instruments that qualify for

favorable treatment in the

HQLA calculation. These

include U.S. Treasurys and

U.S. guaranteed agency

investments issued by the

Government National Mortgage

Association (GNMA). These two

investment categories account

for approximately 55% of the

total portfolio. Other

investments include those in

other agency mortgage-backed securities (MBS), state and local municipal bonds, and corporate bonds

holdings. Ninety-nine percent of the portfolio is investment grade-rated with seventy-eight percent rated

as AAA. The average duration for the $2.8 billion portfolio is 3.8 years which is in line with many peers.

Extension risk appears well contained with IDBNY management pursuing an investment strategy which

does not purchase investments above par values.

KBRA believes liquidity is conservatively managed. The Bank maintains an ample level of liquid assets

combined with a growing customer deposit base, particularly domestic deposits. Those deposits that are

derived internationally have historically been very stable. At 76% as of June 30, 2016, the loan to deposit

ratio for IDBNY compares well to the average of rated peers. At the Bank level, primary sources of

liquidity including liquid assets and estimated unused borrowing capacity totaled over $1.6 billion as of

mid-year 2016. This estimate is based on excess cash, FHLB of NY capacity, repo capacity, Fed Funds

availability, and brokered deposit availability. Liquid assets at the U.S. based holding company totaled

$9.5 million at mid-year 2016, with no liabilities.

Asset Quality

The Bank has seen slight

deterioration in its asset quality

metrics since year-end 2015,

though it still has comparatively

strong asset quality. The level

of nonperforming assets

relative to total assets and

charge-off experience remain

superior to respective peer

averages. Much of the increase

in nonperforming assets is

attributable to only a few

borrowers and only several

properties. Management has

indicated that the Bank

anticipates resolution on one of

the credits by year-end 2016. -10,000

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2Q1620152014201320122011

$ T

ho

usan

ds

Asset Quality Trends Israel Discount Bank of New York

Charge-offs

Provisions

Total NPAs

Israel Discount Bank of New York Page 8 October 19, 2016

As of mid-year 2016, the Texas ratio of just 4.09% compares favorably to the KBRA BBB+ rated average

of 6.43% for bank holding companies. IDBNY is a conservative credit underwriter with deep knowledge of

its customers and markets of operation. During the financial crisis and its aftermath, IDBNY’s level of

nonperforming assets and charge-off experience were considerably better than the track records of many

banks. Construction and development exposure remains relatively low with zero losses even during the

financial crisis.

Capital Adequacy

Capital ratios remain well above regulatory minimums to be considered well capitalized. The Tier 1 risk-

based capital ratio of 13.07% was above the KBRA BBB+ rated average of 11.14% for bank holding

companies and the ratio of tangible equity to assets was in line with peer averages. IDBNY’s economic

capital position is viewed even more positively, given the low risk nature of IDBNY’s asset mix,

conservative level of loan loss reserves and favorable charge-off experience. Double leverage was below

100% at June 30, 2016, indicating no reliance on debt at the U.S. based holding company to finance an

equity investment in IDBNY.

Earnings

Profitability as measured by return on assets (ROA) has remained below average among rated peers,

though it has steadily improved as expected by KBRA. In 2013 and 2014, reported profits were negatively

affected by various one-time expenses. In 2014, charges were taken related to the sale of the Bank’s

portfolio of trust preferred securities issued by other financial institutions. This sale was in response to

Basel III capital rules which punitively treat holdings of preferred investments in other financial

institutions. In addition, moderate charges were taken in late 2014 following the definitive agreement to

sell DBLA to ScotiaBank. Net income in 2015 rebounded substantially with return on average assets

(ROAA) increasing to 0.62% as the Bank returned to its core operation and without the inclusion of one-

time expenses.

Loan Type

Portfolio

Value ($000s)

Gross NPLs

($000s)

Percentage

Nonperforming

Construction & Development $181,585 $0 0.00%

Commercial Real Estate $1,655,131 $14,450 0.87%

Residential Mortgage $14,191 $0 0.00%

Commercial & Industrial $2,348,423 $3,628 0.15%

Consumer $112,614 $0 0.00%

Multi-Family Loans $65,390 $0 0.00%

Other $1,097,109 $20,647 1.88%

Leases $0 $0 0.00%

Total Loans $5,460,601 $38,725 0.71%

Source: FR Y-9C

Discount Bancorp, Inc. Portfolio Asset Quality - 2Q16

2Q16 2015 2014 2013 2012 2011

Tier 1 leverage ratio 9.54% 9.16% 8.13% 8.71% 8.96% 8.56%

Tier 1 risk-based capital ratio 13.07% 12.79% 11.93% 12.89% 14.19% 14.27%

Total risk-based capital ratio 14.09% 13.85% 12.94% 13.90% 15.39% 16.48%

Data Source: Discount Bancorp, Inc.'s Forms FR Y-9C

Regulatory Capital Ratios- Discount Bancorp, Inc.

2Q16 2015 2014 2013 2012 2011

Tier 1 leverage ratio 9.43% 9.06% 8.02% 7.85% 7.81% 7.43%

Tier 1 risk-based capital ratio 12.91% 12.65% 11.77% 11.61% 12.38% 12.38%

Total risk-based capital ratio 13.93% 13.71% 12.78% 12.62% 13.58% 14.59%

Data Source: Israel Discount Bank of New York's Forms FFIEC 041

Regulatory Capital Ratios- Israel Discount Bank of New York

Israel Discount Bank of New York Page 9 October 19, 2016

Profitability has continued to increase through the first half of 2016, reflecting moderate improvement in

net interest income, the net interest margin (NIM) and greater operating efficiency. A continued

improvement in profitability is expected in the second half of 2016 as these trends continue. The NIM and

overall profitability are still hampered by negative spreads generated on high cost term repo funding.

Particularly in 2017 and 2018, NIM is expected to benefit as a large portion of these repos mature.

Further, any move by the Federal Reserve to increase interest rates would benefit the Bank’s profitability

given the asset-sensitive nature of the balance sheet. Noninterest revenues have also been gradually

increasing and have remained a healthy percentage of the revenue mix at 24% of total revenues. KBRA

expects this trend to continue as management continues to build up the investment management

business.

Key Qualitative Rating Determinants

The qualitative aspects of IDBNY were assessed using a scoring model that focuses on four equally

weighted key factors: market strategy, risk management, liquidity management, and the economic and

regulatory framework. Overall, IDBNY scored in the strong category for qualitative factors using data

obtained from annual reports, earnings statements, management presentations, and regulatory reports.

The following describes KBRA’s qualitative assessment for the Company:

Market Strategy

Business Lines

As one of the first U.S. based foreign bank agencies, IDBNY has an extensive history, over 50 years, in

the New York market. The Bank’s network includes its main office in Manhattan, branches in Staten

Island, Brooklyn, and Short Hills, NJ, in addition to branches in Beverly Hills and downtown Los Angeles,

California; and Aventura, Florida. The Bank also maintains an offshore Grand Cayman Island branch; an

international banking facility at its main office in New York; and representative offices in Chile, Israel,

Mexico, Peru, and Uruguay. Securities brokerage activities are conducted through IDB Capital Corp., a

broker-dealer regulated by the Financial Industry Regulatory Authority and the Securities Exchange

Commission.

IDBNY provides private and commercial banking services to its U.S. and international customers. The

private banking division provides services to high net worth clients and includes a full range of investment

management, trust, brokerage, insurance as well as loans and depository services. Lending and other

credit activities include corporate lending, factoring, commercial real estate lending, asset based lending,

and trade finance. Additional services include cash management, foreign exchange, and interest rate

derivatives. IDBNY is a relationship focused bank with many long-standing customers both domestically

and internationally. Referrals from existing customers are the primary source of new business.

Management Profile and Strategy

The executive management team is very experienced with strong knowledge of customers, industries, and

markets in which IDBNY operates. Further, the management team averages 10 years of experience with

IDBNY, with many having previous experience at other large companies and financial institutions in the

New York market. IDBNY’s U.S. holding company, Discount Bancorp Inc., has its own board of directors

consisting of ten members including the CEO of IDBNY, three members from IDB Ltd. (the group CEO, the

head of the corporate division, and the head of the subsidiaries division), and six independent board

members. Independent board members have extensive financial sector experience.

Israel Discount Bank of New York Page 10 October 19, 2016

In late 2014, IDBNY signed an agreement to transfer all assets and liabilities of its Uruguayan retail bank

(assets: $1.3 billion) to ScotiaBank. This transaction was completed in the fourth quarter of 2015. In

2009, IDBNY established a domestic private banking enterprise which led to the opening of private

banking branches in Staten Island (2010), New Jersey (2013), and Brooklyn (2014). The Bank’s strategy

is to focus on achieving improved profitability through enhanced balance sheet and cost efficiencies as well

as domestic private banking and commercial loan growth, while maintaining and retaining its international

private banking relationships. To that end, IDBNY’s management has set specific strategic goals to be

achieved by 2021.

In pursuit of meeting these strategic goals, the Bank will focus on increasing the loan portfolio through

adding new teams and opening loan production offices, continuing to expand wealth management,

leveraging technology including customer relationship management tools, shrinking the relative size of the

investment portfolio, and expanding its customer base while increasing cross selling and product

opportunities with its existing clients.

The Bank continues to expand its investment management and trust business in an effort to improve its

product offerings and increase the proportion of fee income. Combined assets under management (AUM)

of global portfolio management and domestic investment management and trust is relatively small but

with sizeable growth potential over time given the Bank’s roster of high net worth customers. Combined

AUM grew in 2015 to reach approximately $536 million as of year-end. A key focus in this space has been

growth in assets managed for not-for-profit companies and endowments.

Revenue and Customer Profile

The revenue profile for IBDNY continues to be largely spread-reliant with approximately 76% of revenue

coming from net interest income. Noninterest revenue sources are diverse and include deposit service

charge income, fee income from investment banking and trust services, and trading revenue. Based upon

the longevity of many of the private banking relationships, IDBNY is able to command strong margins on

its investment and trust services. As the AUM base continues to grow, IBDNY expects to benefit from

these strong margins in terms of increased revenues. Of particular focus for growth in the commercial

portfolio are opportunities within the lower-tier middle market space; given the Bank’s relative size and

individualized and specialized approach to servicing and relationship management, IDBNY’s management

feels that the Bank has the capacity to successfully service this segment which has been essentially

abandoned by significantly larger competitors. Given the diversified nature of the commercial loan

portfolio with respect to industry, IDBNY has sufficient expertise to service a wide array of businesses and

industries.

Israel Discount Bank of New York Page 11 October 19, 2016

Overall, IDBNY scores average in market strategy.

Risk Management

KBRA considers IDBNY’s risk appetite to be conservative with a comparatively strong track record of loan

portfolio quality. Nonperforming assets remain at low levels with ample coverage by loan loss reserves.

IDBNY’s charge-off experience is favorable, reflecting conservative underwriting standards focused on

collateral strength combined with personal guarantees from customers typically with considerable financial

resources. For commercial real estate loans, average loan-to-value ratios are conservative (see below)

with solid debt service coverage. To limit interest rate risk, the Bank often employs fixed-to-floating swaps

for its commercial loan structures with Bank of Montreal serving as primary counterparty to the swap

transactions. The Bank also recent implemented new risk-adjusted return on equity (RAROE) tools to

better screen potential lending opportunities more efficiently and effectively.

Risk management practices and procedures are comprehensive. All credits require approval by

independent credit risk management. Approval levels factor in both the internal credit rating and amount

borrowed. All new credits over $10 million (approximately 1% of total regulatory capital) and existing

customers over $15 million require approval by the credit committee chaired by the CEO. Credit exposures

over $35 million (4% of total regulatory capital) require additional approval by the executive committee of

the board of directors. To further limit risk exposure to the Bank, loans exceeding $50 million are typically

participated out with other local institutions; IDNBY has approximately $1.4 billion in participation deals.

The Bank also employs an independent loan review department which typically reviews 40% of the loan

portfolio per year in addition to targeted industry reviews.

The credit portfolio is prudently monitored. Management reviews all watch list, criticized and classified

credits quarterly and conducts monthly meetings to discuss and implement strategies to reduce loans

warranting special attention and review all work-out credits. The chief risk officer leads weekly meetings

to discuss past dues and non-accruals, overdrafts, over lines, and over advances, as well as upcoming

annual credit reviews and line and loan maturities.

The risk management group performs a Dodd-Frank Act stress test (DFAST) compliant stress test

quarterly. In this test, IDBNY well exceeds minimum regulatory requirement in the severely adverse

scenario. Stress testing capabilities compare favorably to typical U.S. banks of IDBNY’s size.

Israel Discount Bank of New York Page 12 October 19, 2016

Overall, IDBNY scores strong in risk management for its favorable track record, comprehensive risk

oversight, corporate governance, and knowledge of customers and markets.

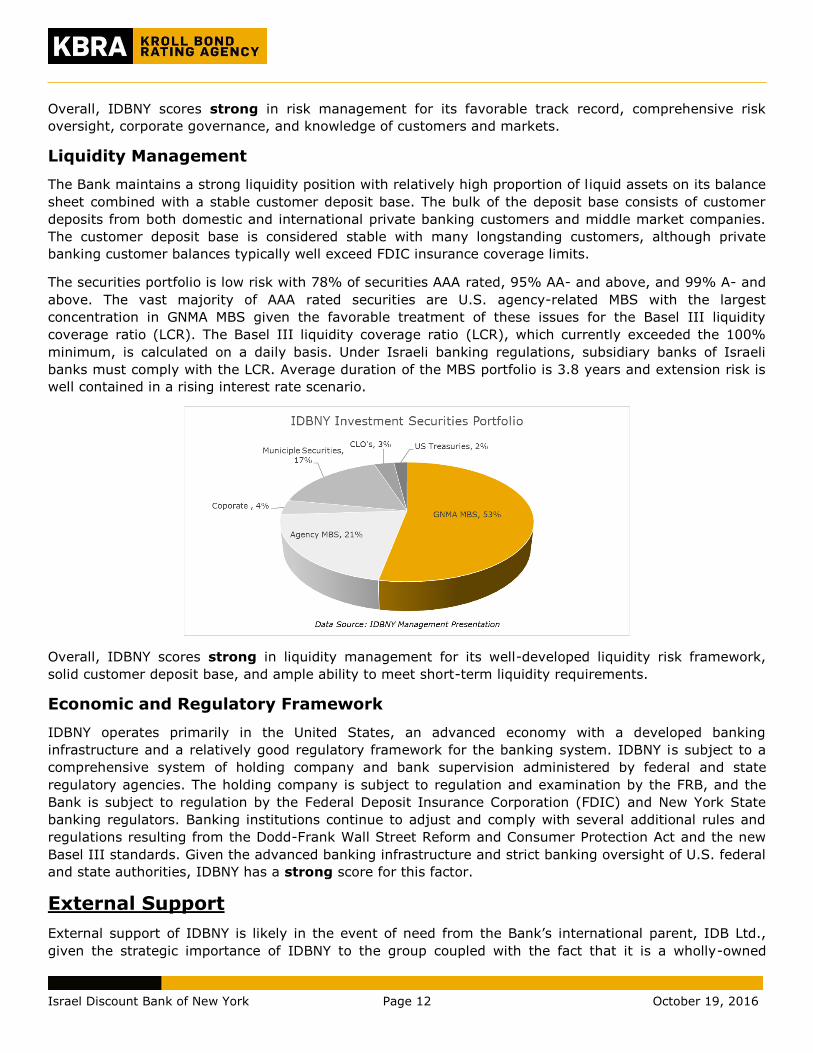

Liquidity Management

The Bank maintains a strong liquidity position with relatively high proportion of liquid assets on its balance

sheet combined with a stable customer deposit base. The bulk of the deposit base consists of customer

deposits from both domestic and international private banking customers and middle market companies.

The customer deposit base is considered stable with many longstanding customers, although private

banking customer balances typically well exceed FDIC insurance coverage limits.

The securities portfolio is low risk with 78% of securities AAA rated, 95% AA- and above, and 99% A- and

above. The vast majority of AAA rated securities are U.S. agency-related MBS with the largest

concentration in GNMA MBS given the favorable treatment of these issues for the Basel III liquidity

coverage ratio (LCR). The Basel III liquidity coverage ratio (LCR), which currently exceeded the 100%

minimum, is calculated on a daily basis. Under Israeli banking regulations, subsidiary banks of Israeli

banks must comply with the LCR. Average duration of the MBS portfolio is 3.8 years and extension risk is

well contained in a rising interest rate scenario.

Overall, IDBNY scores strong in liquidity management for its well-developed liquidity risk framework,

solid customer deposit base, and ample ability to meet short-term liquidity requirements.

Economic and Regulatory Framework

IDBNY operates primarily in the United States, an advanced economy with a developed banking

infrastructure and a relatively good regulatory framework for the banking system. IDBNY is subject to a

comprehensive system of holding company and bank supervision administered by federal and state

regulatory agencies. The holding company is subject to regulation and examination by the FRB, and the

Bank is subject to regulation by the Federal Deposit Insurance Corporation (FDIC) and New York State

banking regulators. Banking institutions continue to adjust and comply with several additional rules and

regulations resulting from the Dodd-Frank Wall Street Reform and Consumer Protection Act and the new

Basel III standards. Given the advanced banking infrastructure and strict banking oversight of U.S. federal

and state authorities, IDBNY has a strong score for this factor.

External Support

External support of IDBNY is likely in the event of need from the Bank’s international parent, IDB Ltd.,

given the strategic importance of IDBNY to the group coupled with the fact that it is a wholly-owned

Israel Discount Bank of New York Page 13 October 19, 2016

subsidiary. However, this support is not factored into ratings of IDBNY and its U.S. based holding

company, given their solid standalone financial condition coupled with uncertainty regarding the level of

support allowable by the parent under Israeli banking regulations.

Pursuant to the 2010 Dodd–Frank Act, U.S. regulators are in the process of creating a working resolution

regime for large banks so that their potential failure does not lead to a systemic crisis. However, KBRA

believes that for the foreseeable future, depositories such as the Bank and their uninsured depositors and

creditors will benefit from some degree of extraordinary systemic support. While we do not adjust the

rating to reflect this reality, the fact that the FDIC, when acting as a receiver of a bank, can pay uninsured

depositors and other creditors at its discretion creates the expectation of governmental support. 1

However, KBRA does not foresee any regulatory support being extended to the holding company level.

Outlook

The stable outlook for the long-term ratings reflects the resilience of IDBNY’s capital and earnings to

KBRA’s forward-looking economic stress scenarios.

Drivers of Rating Change

Rating Upgrade

The long-term ratings of the Bank and its U.S. parent share a stable outlook for the mid-term and in

KBRA’s view, a rating upgrade in the near future is not expected. A significant improvement in profitability

over time could lead to an upgrade if combined with the maintenance of favorable asset quality,

comfortable liquidity, and solid capital.

Rating Downgrade

As the Company’s ratings incorporate a certain degree of resilience based upon KBRA’s stress testing, a

rating downgrade in the near term is unlikely. Unexpected deterioration in asset quality or profitability

could lead to a downgrade. In addition, more aggressive lending or capital management could have

negative rating implications. The possibility of this occurring is considered remote given management’s

conservative financial and risk management practices.

1 Statement by Jeffrey M. Lacker, President, Federal Reserve Bank of Richmond before the Committee on Financial Services, U.S. House of Representatives, Washington, D.C., June 26, 2013.

Israel Discount Bank of New York Page 14 October 19, 2016

© Copyright 2016, Kroll Bond Rating Agency, Inc., and/or its licensors and affiliates (together, "KBRA”). All rights reserved. All

information contained herein is proprietary to KBRA and is protected by copyright and other intellectual property law, and none of

such information may be copied or otherwise reproduced, further transmitted, redistributed, repackaged or resold, in whole or in

part, by any person, without KBRA’s prior express written consent. Ratings are licensed by KBRA under these conditions.

Misappropriation or misuse of KBRA ratings may cause serious damage to KBRA for which money damages may not constitute a

sufficient remedy; KBRA shall have the right to obtain an injunction or other equitable relief in addition to any other remedies. The

statements contained in this report are based solely upon the opinions of KBRA and the data and information available to the authors

at the time of publication of this report. All information contained herein is obtained by KBRA from sources believed by it to be

accurate and reliable; however, KBRA ratings are provided “AS IS”. No warranty, express or implied, as to the accuracy, timeliness,

completeness, merchantability, or fitness for any particular purpose of any rating or other opinion or information is given or made by

KBRA. Under no circumstances shall KBRA have any liability resulting from the use of any such information, including without

limitation, for any indirect, special, consequential, incidental or compensatory damages whatsoever (including without limitation, loss

of profits, revenue or goodwill), even if KBRA is advised of the possibility of such damages. The credit ratings, if any, and analysis

constituting part of the information contained herein are, and must be construed solely as, statements of opinion and not statements

of fact or recommendations to purchase, sell or hold any securities. KBRA receives compensation for its rating activities from issuers,

insurers, guarantors and/or underwriters of debt securities for assigning ratings and from subscribers to its website.