ISAE 3402 - VUrORE · The ISAE 3402 framework is used to provide comfort to user entities and their...

66

Authors: A. Brugge MSc (PwC) and S.P.J. Vuong MSc (PwC) ISAE 3402 ISAE 3402 Additions for future operating effectiveness of controls

Transcript of ISAE 3402 - VUrORE · The ISAE 3402 framework is used to provide comfort to user entities and their...

........

Authors: A. Brugge MSc (PwC) and S.P.J. Vuong MSc (PwC)

ISAE 3402

ISAE 3402 Additions for future operating effectiveness of controls

I

Preface In one of our professional debates, we often discussed how the ISAE 3402 framework could be made more useful. A recurring subject was the limitation of information on the future operating effectiveness of controls. With this idea in mind, we noted in many discussions with colleagues and fellow students that this subject is easily recognizable and people were curious in finding the solution. After this, it seemed clear to us that this would become the subject of our thesis.

By writing this thesis, we would like to contribute to the profession of IT auditing and to NOREA. Within the period this thesis was written, we couldn’t create a completely approved and formalized framework to be used internationally. However, we believe this thesis will provide in the knowledge needed to make the first steps to enhance the current set of assurance frameworks (ISAE) to elaborate on the future operating effectiveness of controls in order to address the changing assurance needs.

We could not have written this thesis without the guidance and feedback of our supervisors René Matthijsse from VU University and Tom Ooms from PwC. We would also like to thank Arnold’s wife Maaike Brugge-Cobelens (who is pregnant at the time of writing) for her support and understanding.

October 2014

Arnold Brugge and Johnny Vuong

II

Executive summary To gain assurance about a process executed by a third party, independent auditors issue an opinion about the way a process is performed by the service providing organization, using for instance the International Standard on Assurance Engagements (ISAE) 3402. Different developments are discerned, such as continuous auditing and monitoring, with the focus on more insights in the continuity aspects of an organization. Currently, the ISAE 3402 framework does not encompass information about future operating effectiveness of controls and therefore, the continuity of controls. Given these changes, clients and auditors do not only need assurance of a process performed in the past, but also need more information about how the business and controls will operate in the future. This thesis investigates which additions should be made in the current ISAE 3402 approach to give the user of the ISAE 3402 the ability to report more insights in the future operating effectiveness of the controls at the service provider.

The ISAE 3402 framework is used to provide comfort to user entities and their auditors about the internal control components related to financial reporting of the service organization covering a specified period in which controls; designed and implemented, suitably designed throughout the specified period or as at a specified date and operated effectively throughout the specified period. This leads us to the most significant limitation of the ISAE 3402 framework within the context of this thesis research; the lack of information on future operating effectiveness of controls. The most important reasons why this absence of information is essential are effective operation of primary processes, more control over the processes (contributing to continuous monitoring) and transparency regarding continuity, as it is also a necessity within financial statement audits.

Based on the analysis of similar frameworks, such as ISAE 3000, combined with interviews with stakeholders, the following conceptual additions on the audit approach are suggested to contribute the future operating effectiveness of controls and are proven in practice by the use of case studies:

1) Select the right assurance framework to address the assurance need by choosing the ISAE 3000 framework or one of the SOC2/3 related frameworks. Maintain at least the scope of ISAE 3402 to cover the essential and obligatory assurance needs and expand this scope with the additional audit work to address the future operating effectiveness aspects.

2) Understanding the client and engagement by gaining an update of knowledge, and review the effects of changes regarding applicable industry and regulatory standards. Verify if an approach is implemented for establishing, implementing, operating, monitoring, reviewing, maintaining and improving an organization's internal control system and to verify if an Internal Audit function is established and actively involved in managing the achievement of control objectives related to the ISAE 3402 scope.

3) While execution of the audit, more attention is dedicated to the amount of Meta controls, monitoring the key controls and the amount of automated controls.

4) Ensure that the report covers subsequent events, a statement of the limitations of controls and the risk of projecting to future periods, a statement of direction by management.

III

Table of contents Preface ........................................................................................................... I

Executive summary ....................................................................................... II

Table of contents ......................................................................................... III

List of Figures ................................................................................................. V

List of Tables .................................................................................................. V

1 Introduction ............................................................................................. 1

1.1 Problem statement and decomposition ....................................................... 5

1.2 Research methodology ............................................................................. 5

1.3 Scope ..................................................................................................... 6

1.4 Relevance ............................................................................................... 6

1.5 Outline .................................................................................................... 7

2 The ISAE 3402 framework and its limitations .......................................... 8

2.1 Background ............................................................................................. 8

2.2 The scope of the ISAE 3402 framework ..................................................... 9

2.3 Objectives of the ISAE 3402 framework .................................................... 10

2.4 Usage of the ISAE 3402 framework in practice .......................................... 10

2.5 Limitations of the ISAE 3402 framework ................................................... 11

3 Analysis of the ISAE 3402 framework and other relevant frameworks .. 14

3.1 Elements within the 3402 framework ........................................................ 14

3.2 Analysis of frameworks similar to ISAE 3402 ............................................. 16

3.2.1 ISAE 3000 ........................................................................................ 17

3.2.2 ISO 27001 ....................................................................................... 18

3.2.3 SOC1, SOC2 and SOC3 ..................................................................... 18

3.2.4 PCI-DSS........................................................................................... 20

3.2.5 ISA 520 – Going Concern .................................................................. 21

4 Exploratory interviews and results ......................................................... 23

4.1 Interview approach ................................................................................. 23

4.2 Interview results ..................................................................................... 25

IV

4.3 Additions in the regular ISAE 3402 audit approach as derived from research 27

4.3.1 Choose the assurance framework to address the assurance need ......... 27

4.3.2 Planning and understanding the client ................................................ 27

4.3.3 Execution of the audit ....................................................................... 28

4.3.4 Reporting ......................................................................................... 28

5 Case study research ............................................................................... 29

5.1 Approach ............................................................................................... 29

5.2 Case study A .......................................................................................... 29

5.2.1 Context ........................................................................................... 29

5.2.2 Case study findings and analysis ........................................................ 30

5.2.3 Summary ......................................................................................... 35

5.3 Case study B .......................................................................................... 36

5.3.1 Context ........................................................................................... 36

5.3.2 Case study findings and analysis ........................................................ 37

5.3.3 Summary ......................................................................................... 42

5.4 Case research outcomes and analysis ....................................................... 43

6 Research question and conclusion ......................................................... 45

6.1 Research question ................................................................................... 45

6.2 Additions in the regular ISAE 3402 audit approach ..................................... 46

6.3 Limitations of this research ...................................................................... 47

6.4 Further research ..................................................................................... 48

7 Bibliography ........................................................................................... 49

Appendix ...................................................................................................... 51

A Exploratory interview: Domain Expert .......................................................... 51

B Exploratory interview: Service Provider ........................................................ 54

C Exploratory interview: Client of Service provider ........................................... 56

D Exploratory interview: External auditor ......................................................... 58

V

List of Figures Figure 1: Outline ................................................................................................. 7

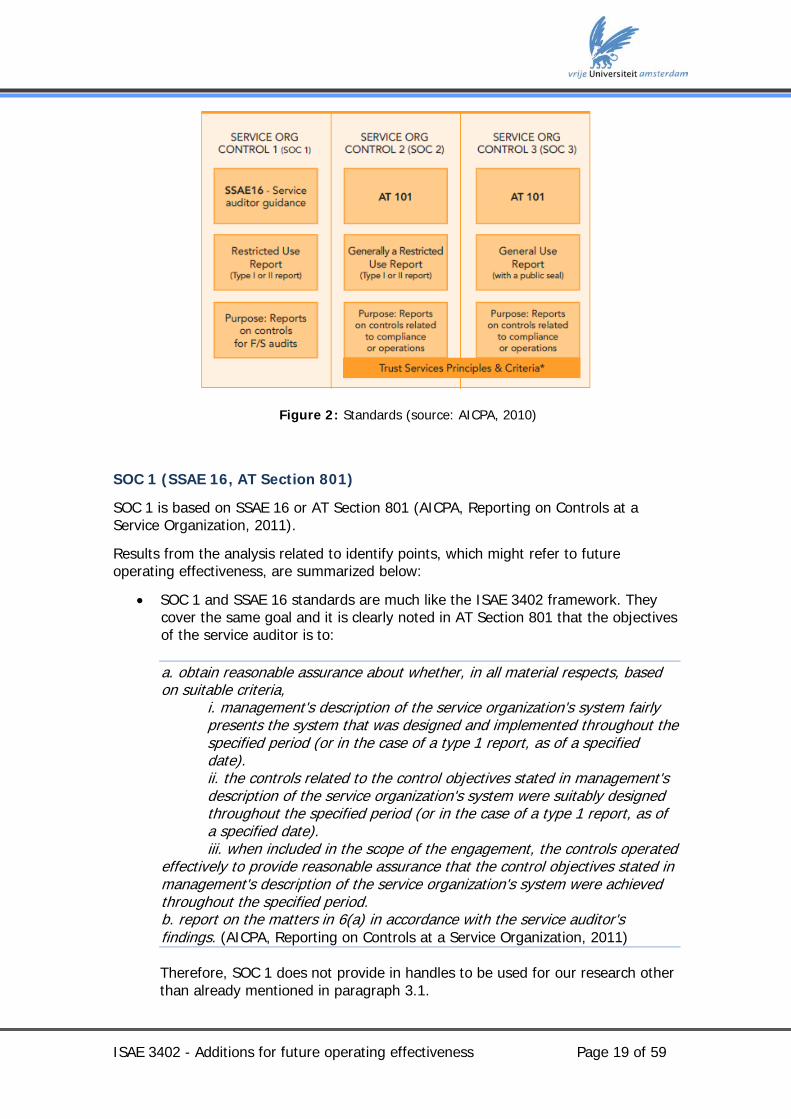

Figure 2: Standards (source: AICPA, 2010) ........................................................... 19

Figure 3: Meta controls ....................................................................................... 26

List of Tables Table 1: ISAE 3402 requirements analysis ............................................................. 14

Table 2: Case A analysis of additions .................................................................... 35

Table 3: Case B analysis of additions .................................................................... 42

ISAE 3402 - Additions for future operating effectiveness Page 1 of 59

1 Introduction Throughout the years, IT has become more and more Service-Oriented by which IT processes are outsourced to third parties. However, by outsourcing a process one does not outsource its accountability. To gain assurance about a process executed by a third party, independent auditors give an opinion about the way a process is performed by the service providing organization.

Until 2011, SAS70 was the reporting standard regarding service-providing organizations. The International Standard on Assurance Engagements (ISAE) developed by the International Auditing and Assurance Standards Board (IAASB) is a standard now used for an assurance opinion about the work performed by a Service Organization over a historic period in time, the successor of SAS70.

At the moment of writing, different developments are discerned such as Continuous auditing and monitoring. The developments are focussed on having more insight in the continuity aspects of an organization. For instance, regarding the annual financial statements reports, many discussions are held regarding the unavailability of continuity aspects of the audited organization in the annual financial statements report. The readers of the annual financial statements report, shareholders and other stakeholders, cannot form a grounded opinion and/or get insight in the future operating effectiveness of an organization as in the report the continuity aspects of an organization is not clearly explained (Mertens, Meliefste MSc, & Blij CFA, 2013). Especially with the current uncertainty in the economic developments, special attention is dedicated to the continuity of organizations. However, why is it important to look into aspects regarding continuity and future operating effectiveness? Before we look into depth why it is important to consider future operating effectiveness, allow us to first introduce our definition of future operating effectiveness.

Definition of future operating effectiveness

When we mention operating effectiveness, we refer to the effectiveness of the operation of a control. In nearly all audit standards, when performing an audit on the operating effectiveness of the controls (i.e. a Type II report), the historical information regarding the operation of the control are assessed and tested. This way the auditor gains reasonable assurance that the control has worked as it should be in a certain period in the past.

When we refer to the future operating effectiveness in this thesis, we mean the operating effectiveness of the specific control in the future. Based on the information acquired during the audit regarding the past and current operation of the control, a high-level opinion – with limited degree of assurance – on the future operation of the control can be formed. Future operating effectiveness is the operating effectiveness of the control in the future. By future, we mean any point in time after the audit has been performed.

With this definition being clear, the most important and relevant reasons why a stakeholder is interested in the future operating effectiveness of the key processes at a service organization are mentioned below.

ISAE 3402 - Additions for future operating effectiveness Page 2 of 59

Effective operation of primary processes

With the recent financial crisis, it is important for organizations to be more aware of the effectiveness of their processes and the related controls. This way, more or better goods and / or service can be delivered while saving costs. When (partly) outsourcing processes, it is of essence to have insight in the operating processes at the service organization. This way the user entity knows what processes are implemented at the service organization, and can use that to connect and improve their own processes. In the total value chain, more can be achieved in a more efficient matter (Holcomb & Hitt, 2007).

Nevertheless, with this integration of the user entity’s processes and the service organization’s processes, it is important to have information about whether the relevant processes at the service organization will continue to operate effectively in the near future. With this information, the user entity can anticipate its dependencies in their own primary processes.

When illustrating this perspective with an example; for a trading company it is essential to know how the logistic processes at a service providing logistics company operates. With this information, the user entity can connect their own processes to the ones of the logistics company and increase the total added value in the value chain. The trading company can now for instance inform their customer more accurate on the delivery times. With the acquired information on the operating effectiveness of the logistic company’s processes, the trading company can implement additional processes and / or controls to maintain their level of service quality when a calamity or exception occurs in the processes of the logistics company.

More control over the processes

As stated by (Roozendaal, 2011), stakeholders hold directors accountable regarding the reliability of (financial) processes, as governance becomes more and more important these days. Developments such as continuous monitoring and continuous audit become more relevant and can help organizations to map and accurately estimate the process risks. With the implementation of continuous monitoring and / or continuous auditing, it becomes possible to have insight in the operating effectiveness of the primary processes at all times, and therefore gain continuous assurance about the specific processes.

Continuous monitoring and auditing enables the organization to quickly relate the process output to the corresponding risk profile. This way the organization can instantly identify exceptions in the process output or changing risks and take corrective actions accordingly (Roozendaal, 2011).

As we have identified before in this thesis an increasing amount of organizations outsource (parts of) their processes to service organizations. In order of fulfilling the full potential of the benefits of continuous monitoring / auditing, it is of great importance to gain assurance on the processes at the service provider. An ISAE 3402 report gives assurance regarding the operating effectiveness of the controls of the service organization in the past period but it does not provide any information regarding the operating effectiveness in the near future. When relying on service organizations and willing to utilize the full potential of continuous monitoring, it is important to gain insight in the future operating effectiveness of the relevant process at the service provider.

ISAE 3402 - Additions for future operating effectiveness Page 3 of 59

With this information the process output can be more controlled, in a continuous assurance matter, and be corrected within the own (user entity’s) processes and controls if necessary. For example, a retail organization has outsourced its payment processes to a payment service provider (PSP). With continuous monitoring, the directors of the retail organization can monitor the most important processes related to sales and logistics. The payment process lies with the PSP, which provides not only information regarding the operating effectiveness of the payment process for the retail organization, but information on future operating processes as well. When the process impends to miss their process / control objective, the retail organization will know this soon enough to implement corrective measures and create their own workaround(s) to maintain their level of control and quality of its processes. Transparency regarding continuity also a necessity within financial statement audits

If we relate the need for information and transparency regarding continuity to the annual financial statements audit, the same can be concluded. Most financial statement audit reports lack a foundation or elaboration of the so-called “continuïteitsveronderstelling” (in English the assumption of continuity). Information regarding the continuity of a company is not transparent, implicit and / or spread across the report (Mertens, Meliefste MSc, & Blij CFA, 2013). For an outsider, the stakeholder it is hard to determine the continuity chances of an organization.

In order of fulfilling the information need regarding continuity (NBA, 2013), the accountant of the user entity needs to assess what processes are of key essence for the continuity of the organization. These key processes can be dependent on one or more service providers. Therefore, the accountant of the user entity needs insight in not only the operating effectiveness of the processes and controls at the service provider in the past, but in the future as well. This way the accountant of the user entity can include this information in his considerations regarding the assessment of the continuity of its auditee organization.

As you can imagine, a datacentre is very dependable on the controls and processes at the telecommunications company. When the controls at the telecommunications company are (partly) failing, this will have a significant impact on the continuity of the datacentre.

Additionally, with the control-based approach within the financial statement audits it is important to gain insight in the operating effectiveness of the controls in the service organization’s processes as these can affect the financial statements.

In practice, assessing the ISAE 3402 report on the service organization’s processes happens during the interim work of the audit. At this moment of the audit only an ISAE 3402 report of the previous year / period is available, in which it states that the controls in scope has or has not worked properly in the past period. This past period does not match with the time scope of the financial audit, in which we actually should conclude that limited assurance could be derived from the ISAE 3402 report.

ISAE 3402 - Additions for future operating effectiveness Page 4 of 59

For example, in the FY14 financial statements audit during the interim only ISAE 3402 FY13 reports are available, although as an accountant you would like assurance over the operating effectiveness of the controls in FY14, as these affects the financial statements of FY14. In some cases, the ISAE 3402 report over the period FY14 arrives at the very last moment of the financial statements audit, which is not an ideal situation.

It would be useful if the accountant of the user entity could gain more information about the continued effectively operating controls at the service organization, so he can anticipate on possible qualifiers (if present) in its audit approach for the financial statement audit.

We have defined future operating effectiveness as the operating effectiveness of the specific control in the future. Based on the information acquired during the audit regarding the past and current operation of the control, a high-level opinion – with limited degree of assurance – on the future operation of the control can be formed.

Goal

Based on the need for assurance going further than the past, this master thesis investigates which additions are needed to enhance the value of the current ISAE 3402 standard such that it is able to give insight about the operating effectiveness of a service organization in the near future.

The research goal of this thesis can be categorized as Understanding and “Guidance for Action: Design”. This thesis explains the characteristics of an ISAE 3402 audit. After the setting out the context of the ISAE 3402 standard, the ISAE 3402 standard is compared with other Assurance standards, in order to amplify the key differences and assess the added value and potential of the ISAE 3402 standard.

Once the current situation is defined, we focus on research to gain insight on how the current ISAE 3402 report is used and which information regarding the future operating effectiveness of the service organization is missing in the reports issued. Additionally we aim to gain insight in how the gap is overcome or accepted by the users of the ISAE 3402 report.

After the research performed to identify the need for information about the future operating effectiveness of a service organization, additions to a standard based on ISAE 3402 are proposed, which does not only provide assurance over the past operating effectiveness, but also provide information over the (near) future operating effectiveness of the controls at the service provider concerned. The concept additions to the regular audit approach are applied in two case studies as a proof of concept, to verify the added value.

As a result of this thesis research, not only an understanding of ISAE 3402 is provided but also additions are proposed for the ISAE 3402 approach. When these additions are performed in addition to (or integrated with) the current ISAE 3402 audit approach, the value of the ISAE 3402 audit will be enhanced, providing information about the operating effectiveness of a service organization in the near future.

ISAE 3402 - Additions for future operating effectiveness Page 5 of 59

1.1 Problem statement and decomposition Based on the context outlined in the paragraph above, the main question of this thesis is:

What additions should be made in the current ISAE 3402 audit approach to give the user of the ISAE 3402 report more assurance regarding the future

operating effectiveness of the service provider?

The main question can be decomposed in the following sub questions:

1) What are the main elements and characteristics of the current ISAE 3402 audit?

2) How is the current ISAE 3402 report used by stakeholders and what information is missing in the report regarding the future operating effectiveness of the service organization?

3) Which additions to the ISAE 3402 audit approach can be defined in order of assessing a service provider regarding the future operating effectiveness of controls?

1.2 Research methodology The method of this thesis research is a combination of literature study, case study and semi structured interviews with domain experts/ stakeholders regarding an ISAE 3402 audit.

To answer the sub questions, the following methods are used:

1) What are the main elements and characteristics of the current ISAE 3402 audit?

Literature study Using literature study we can build a solid base for the thesis research.

2) How is the current ISAE 3402 report used by stakeholders and what information is missing in the report regarding the future operating effectiveness of the service organization?

Semi-structured interviews The results from the literature study are then assessed with stakeholders who have experience in the execution and/or undergoing an ISAE 3402 audit. This is done by performing semi-structured interviews with the relevant stakeholders. The selected stakeholders are persons from an auditing firm, service provider (auditee), domain expert and a firm that uses the services of the auditee. With these four perspectives, adequate insight is acquired on the use and view of ISAE 3402 reports. The number of interviews and combination of different perspectives validates the output of the interviews.

3) Which additions to the ISAE 3402 audit approach can be proposed in order of assessing a service provider regarding the future operating effectiveness of the service organization?

ISAE 3402 - Additions for future operating effectiveness Page 6 of 59

Case studies The results of the thesis research are validated with two case studies and discussed with relevant stakeholders/domain experts to ensure validation.

1.3 Scope We limit our research to the standard ISAE 3402. This standard is chosen because it is widely used in the area of financial reporting. However, other standards might exist that are comparable to the ISAE 3402 standard.

Furthermore, we limit our research to perform two case studies in two different environments therefore resulting in a qualitative research.

1.4 Relevance The relevance of this research can be decomposed into two perspectives.

Firstly, currently the society requires special attention1 on the continuity of organizations. In the past years organizations encounter problems with continuity, which affect many other organizations up/ down the supply chain, employees, government and / or regular civilians. The society requires having more insight in the management of continuity risks in order of being able to anticipate on the possible consequences. In the modern world, many organizations work tightly with service providers to manage the whole process chain as efficient as possible. For this reason, it is of importance to be clear about the continuity of the operating effectiveness of the processes at the service provider related to the audittee organization, as this affects (partly) the continuity of the audittee organization. Assessing the need and implementation of continuity aspects in the ISAE 3402 standard helps to plot all the relevant continuity risks of an organization.

Secondly and partly related to the first described perspective, the current developments regarding continuous assurance, as stated in Spotlight (openly published company literature (Roozendaal, 2011), enables organizations to have more insight the effectiveness and efficiency of processes. This should include the processes that are (partly) outsourced to service providers. The current ISAE 3402 framework provides assurance based on historical information regarding the processes in scope. By adjusting the work performed it is possible give more insight in the operating effectiveness in the (near) future and therefore for the user organizations to include it in their monitoring processes in the light of continuous assurance.

1 http://www.accountancynieuws.nl/actueel/accountancymarkt/risicorapportage-in-jaarverslag-te-algemeen-voor.125662.lynkx

ISAE 3402 - Additions for future operating effectiveness Page 7 of 59

1.5 Outline This thesis is structured as described below. The previously described sub questions form broadly the structure of this thesis:

• Introduction, decomposition of the main question and its sub question with the description of the research methods

• Theoretical research regarding the ISAE 3402 standard, its limitations and the relevant developments regarding the stakeholders of the standard. Also analysis on similar frameworks on aspects that might point to future operating effectiveness

• Exploratory interview results and comparison with other relevant frameworks regarding the limitations noted

• Conceptual additions to the ISAE 3402 audit approach and case studies to proving the conceptual additions

• Conclusion with proposed additions to the regular audit approach to provide more information on future operating effectiveness

Chapter 3 Relevant

frameworks

Chapter 5

Validation by case study

Chapter 4 Practice (interviews)

Chapter 6 Conclusion

Chapter 1 Introduction

Figure 1: Outline

Chapter 2 ISAE 3402 framework

ISAE 3402 - Additions for future operating effectiveness Page 8 of 59

2 The ISAE 3402 framework and its limitations To gain a good understanding of the ISAE 3402 framework and its limitations, this chapter will first go into the background and the organization behind the standard. With the background in mind, the objectives and usage of the ISAE 3402 is elaborated. Based on this understanding, the limitations of the ISAE 3402 are explored and analysed. From the limitations this thesis research focuses particularly on the limitation of future operating effectiveness of controls, as in the last part of this chapter is described why this limitation is important.

2.1 Background Until 2011, Statement on Auditing Standards No. 70 (SAS 70) was the reporting standard regarding service-providing organizations. SAS 70 was a widely recognized American audit standard issued by the American Institute of Certified Public Accountants. SAS 70 provides guidance to service auditors when assessing the internal control of a service organization on behalf of a user organization. SAS 70 is applied in situations where outsourcing is in place. SAS 70 provides information on the service organization’s internal control on behalf of the user organization’s financial statement. SAS 70 is developed by accountants for accountants (Ewals, 2009). The scope of SAS 70 covers the integrity of financial reporting and may include specific controls determined by the client, who has engaged the service auditor.

A distinction in two types of SAS 70 can be made: type I and II (Ewals, 2009). A SAS 70 type I report states whether the service organization’s description of its controls are fairly presented and implemented on a certain date. A SAS 70 type II report provides the same information as a SAS 70 type I report and adds another part that reports on whether the controls that were tested were operating with sufficient effectiveness to provide reasonable assurance that the related control objectives were achieved during a specified period.

The main reason for the replacement of SAS70 was the need for an international standard. As SAS70 is an American standard, it complicates engagements that cross borders. There was a demand for a new single auditing standard that provides consistency to customers around the world. Global service organizations often issued assurance reports under various country specific standards, thereby creating more inconsistencies and confusion. Another reason was that SAS 70 did not maintain a risk based approach, its scope being limited to integrity of financial reports and management did not explicitly take the responsibility regarding internal control (Ernst & Young, 2009).

The International Standard on Assurance Engagements (ISAE), developed by the International Auditing and Assurance Standards Board (IAASB), is a standard now used for an assurance opinion about the work performed by a Service Organization over a historic period in time, the successor of SAS 70 mitigating the shortcomings noted above.

ISAE 3402 - Additions for future operating effectiveness Page 9 of 59

2.2 The scope of the ISAE 3402 framework To understand the scope of the ISAE 3402 framework, relevant scoping paragraphs of the framework are noted and analysed below.

Scope

According to the report issued by IFAC (IAASB, 2009).,

“The International Standard on Assurance Engagements (ISAE) deals with assurance engagements undertaken by a professional accountant in public practice to provide a report for use by user entities and their auditors on the controls at a service organization that provides a service to user entities that is likely to be relevant to user entities’ internal control as it relates to financial reporting.”

This means that the framework is used to provide comfort to user entities and their auditors about the internal control components related to financial reporting of the service organization.

“This ISAE applies only when the service organization is responsible for, or otherwise able to make an assertion about, the suitable design of controls. This ISAE does not deal with assurance engagements:

(a) To report only on whether controls at a service organization operated as described, or

(b) To report on controls at a service organization other than those related to a service that is likely to be relevant to user entities’ internal control as it relates to financial reporting (for example, controls that affect user entities’ production or quality control).

This ISAE, however, provides some guidance for such engagements carried out under ISAE 3000.” ( (IAASB, 2009)

This means that the framework only applies to controls related to financial reporting. Additionally, ISAE 3402 provides some guidance to a related framework ISAE 3000 but does not cover all.

“The performance of assurance engagements other than audits or reviews of historical financial information requires the service auditor to comply with ISAE 3000.” (IAASB, 2009)

Although our scope is set to the ISAE 3402 framework, because of the relation between both frameworks, a comparison between the two frameworks is included in chapter three to ensure that relevant information is encompassed in this research.

Based on the above, we consider the scope of the ISAE 3402 framework to be a framework used to provide comfort to user entities and their auditors about the internal control components related to financial reporting of the service organization relating to the ISAE 3000 framework, which covers internal control components other than audits or reviews of historical financial information.

ISAE 3402 - Additions for future operating effectiveness Page 10 of 59

2.3 Objectives of the ISAE 3402 framework According to (IAASB, 2009) the objectives of the service auditor are:

a) To obtain reasonable assurance about whether, in all material respects, based on suitable criteria:

(i) The service organization’s description of its system fairly presents the system as designed and implemented throughout the specified period (or in the case of a type 1 report, as at a specified date);

(ii) The controls related to the control objectives stated in the service organization’s description of its system were suitably designed throughout the specified period (or in the case of a type 1 report, as at a specified date);

(iii) Where included in the scope of the engagement, the controls operated effectively to provide reasonable assurance that the control objectives stated in the service organization’s description of its system were achieved throughout the specified period.

b) To report on the matters in (a) above in accordance with the service auditor’s findings

Based on the above, we consider the objectives of the ISAE 3402 framework to be:

A framework used to provide comfort to user entities and their auditors about the internal control components related to financial reporting of the service organization relating to the ISAE 3000 framework, which covers internal control components other than audits or reviews of historical financial information covering a specified period in which controls:

• Designed and implemented • Suitably designed throughout the specified period or as at a specified date • Operated effectively throughout the specified period

2.4 Usage of the ISAE 3402 framework in practice The ISAE 3402 framework is used in practice for different reasons than the intended purpose (refer to chapter 2.3. According to the interview with Domain Expert and (Leenders RA & Nagy RO, 2013), the following three reasons can be distinguished:

• Mandatory because of external requirements (law and regulations) • As a trigger to improve a company’s internal control framework • As a unique selling point to prove to their customers that they are in control

Depending on the reason, one is more eager to cover more processes and controls. Mainly, the ISAE 3402 is used as an auditor to auditor’s report (reason one of the above) to cover the risk of material misstatement in processes that are performed by the service organization.

ISAE 3402 - Additions for future operating effectiveness Page 11 of 59

When performing the audit of the annual financial statement of a company, the report as stated above is needed to cover all financial statement line items. As an auditor, the audit approach for the coming year relies on the ISAE 3402 audit report to be present for service organizations, especially, when this was to be true in the previous year. To help the auditor in the process of determining the audit approach, more insight in the quality of the service organization is needed to assume that a report without a qualified opinion can be issued the next year. Currently, this is not part of the ISAE 3402 framework and report. More details will be provided to this limitation in paragraph 2.5.

Regarding the second and third reason, the emphasis lies on proving or improving a company’s internal control system. Therefore, a company’s goal is to embed as many processes and controls as possible (within reasonableness).

The ISAE 3402 framework does however not support:

• All types of assurance • All objects of research • All types of scope • All periods of time

In practice, according to the interviewed domain expert, (Leenders RA & Nagy RO, 2013) and our own experiences, the ISAE 3402 framework is sometimes used to report on more than the framework was intended to provide. This leads us to the limitations of the ISAE 3402 framework in the next paragraph.

2.5 Limitations of the ISAE 3402 framework With the current use of the ISAE 3402 framework, we gain insight in the design of the controls in place at the service organization and whether controls operate effective over the period in scope.

However, there are limitations on the ISAE 3402 framework as we encountered during our audit work. From literature study and the interviews held the same limitations are observed.

From all the mentioned limitations in our daily work, interviews held and literature study, it comes down to the limitations as mentioned below in this paragraph, including the impact that these limitations have on the assessment of the external auditor and/or user entity.

Considering the use and appliance of the results of the ISAE 3402 audit in other audits as described in the previous chapter, we can observe several limitations in the framework. Out of these limitations, we look further into the relevance and importance of the limitations.

1) The ISAE 3402 framework requires a risk-based approach. Based on the risk management procedures of the service organization the most relevant controls are considered and included in the scope of the ISAE 3402 audit. These controls are the controls related to a service organization’s operations and compliance objectives, which is relevant to a user entity’s internal control as it related to financial reporting (IAASB, 2009). Defining which controls at a

ISAE 3402 - Additions for future operating effectiveness Page 12 of 59

service organization are likely to be relevant to user entities’ internal control is dependable on the defined control objectives and the suitability of the criteria as set by the service organization. This entails that the risk management procedures are adequately implemented. When not properly implemented, there is a risk that one or more relevant controls are not taken into account. For this reason, it is important to assess the controls in scope of a performed ISAE 3402 audit in order of adequately estimating the impact on the user entities’ internal control. The ISAE 3402 framework does dictate certain controls to be in scope.

2) An ISAE 3402 report describes whether the controls in design, implementation and operating effectiveness have met the related control objectives. However, this does not give information whether the controls will meet the related control objectives in the future (Buitendijk & van Gerner, 2011). The report only describes merely what controls have operated effectively and which ones encountered exceptions in the past period; it does not give any direct insight in the operating effectiveness of the controls in the (near) future.

3) The ISAE 3402 framework is not designed to cover all possible scope, types of assurance, objects of research and periods (please refer to point two above). For different (commercial) reasons, companies would like to fit as much as possible in the report which is in conflict with the original goal of the framework (Leung, 2011)

If we look into the limitations above, the limitation of not providing information about the reasonableness of the future operating effectiveness of the controls in scope is considered the most important one. Especially with the current need, in the light of the recent financial crisis, accounting scandals, for more transparency and control of one’s processes; we determined that organization require more insight the operation effectiveness of their internal controls, including the related controls at the service organization.

As described in detail in chapter one, the most important reasons why information on future operating effectiveness is relevant for the different stakeholders of the service provider can be summarized in three points:

• Effective operation of primary processes: as many processes are (partly) outsources, it is important to have insight in the operating processes at the service organization and its dependencies with one's own primary processes. With future operating effectiveness more can be said over the output of the outsource process (parts) over the upcoming period and therefore strengthen the control on the process output over time. This way the output of the primary processes remains controllable over time.

• More control over the processes: with the current development towards continuous monitoring, it enables organizations to relate the process output to the corresponding risk profile. This way the organization can instantly identify exceptions in the process output or changing risks and take corrective actions accordingly. To be able to be ahead of upcoming exceptions and/or risks, it is important to have insight in the future operating effectiveness of outsourced (parts of) processes.

ISAE 3402 - Additions for future operating effectiveness Page 13 of 59

• Transparency regarding continuity also a necessity within financial statement

audits: when a user organization is very dependable on a service provider, it is important to assess the future operating effectiveness of the controls. When these controls, mainly the ones that are important for the continuity of the user organization, are likely to (partly) fail the user organization can act timely upon to secure its continuity.

In the next chapter, we look into the conceptual additions to overcome the identified limitations.

ISAE 3402 - Additions for future operating effectiveness Page 14 of 59

3 Analysis of the ISAE 3402 framework and other relevant frameworks

In order to suggest additions to expand the scope of the regular ISAE 3402 audit approach, the framework itself is analysed, similar frameworks and other industry standards are reviewed on aspects, which might point to information on future operating effectiveness.

3.1 Elements w ithin the 3402 framework Because of the goal of the ISAE 3402 framework, there are no elements specified that support statements about future operating effectiveness of controls. However, keeping the concept of future operating effectiveness (from chapter one) in mind, we are able to define current elements that might be able to address the subject.

The framework consists of a list of requirements. Those requirements need to be addressed in the audit and or in the report. Based on our experience with ISAE 3402 assignments, we have indicated which requirements are likely to be useful to gain insight for future operating effectiveness of controls.

Table 1: ISAE 3402 requirements analysis

Requirements Likely to be usable

Unlikely to be usable

ISAE 3000 X

Ethical requirements X

Management and Those Charged with Governance X

Acceptance and Continuance X

Assessing the Suitability of the Criteria X

Materiality X

Obtaining an Understanding of the Service Organization’s System X

Obtaining Evidence Regarding the Description X

Obtaining Evidence Regarding Design of Controls X

Obtaining Evidence Regarding Operating Effectiveness of Controls X

The Work of an Internal Audit Function X

Written Representations X

Other Information X

Subsequent Events X

ISAE 3402 - Additions for future operating effectiveness Page 15 of 59

Requirements Likely to be usable

Unlikely to be usable

Documentation X

Preparing the Service Auditor’s Assurance Report X

Obtaining an Understanding of the Service Organization’s System

Regarding Obtaining an Understanding of the Service Organization’s System (IAASB, 2009), the following is defined:

“ 20. The service auditor shall obtain an understanding of the service organization’s system, including controls that are included in the scope of the engagement.”

In practice, using for instance PwC working papers PwC ISAE 3402 library, 2012 (PricewaterhouseCoopers, 2012), we gain an update of knowledge of, and review the effects of applicable industry and regulatory standards with a focus on significant changes affecting the current period or future periods. Therefore, this requirement already has insight in significant changes that would affect future periods. Based on this insight, it is likely that we can assess the impact on controls and their future operating effectiveness.

Obtain evidence

While performing procedures regarding Obtaining Evidence Regarding Design of Controls and Obtaining Evidence Regarding Operating Effectiveness of Controls, information is gathered from employee’s carrying out the day-to-day activities. This information might be relevant for next year’s audit, which will be documented in the working papers, but is not part of the final report due to the reporting period agreed upon.

Subsequent Events

Regarding Subsequent Events (IAASB, 2009), the following is defined:

“ 43. The service auditor shall inquire whether the service organization is aware of any events subsequent to the period covered by the service organization’s description of its system up to the date of the service auditor’s assurance report that could have a significant effect on the service auditor’s assurance report. If the service auditor is aware of such an event, and information about that event is not disclosed by the service organization, the service auditor shall disclose it in the service auditor’s assurance report.

As states above, Subsequent Events is part of the final stage before preparing the Service Auditor’s Assurance Report. These events cover the period between test work performed regarding the reporting period agreed upon to the moment that the report would be issued.

ISAE 3402 - Additions for future operating effectiveness Page 16 of 59

Preparing the Service Auditor’s Assurance Report

Regarding Preparing the Service Auditor’s Assurance Report (IAASB, 2009), the following is defined:

“j) A statement of the limitations of controls and, in the case of a type 2 report, of the risk of projecting to future periods any evaluation of the operating effectiveness of controls.”

Although the above might be seen as a limitation, the fact that the auditor needs to make a statement about the limitations might be usable for mentioning relevant information about future operating effectiveness of controls.

Bridge letter In practice, as is done for ADP, a so-called Bridge letter is issued based on inquiry with Management and those charged with governance. This is a solution to mitigate the limitation as set out in chapter one. However, inquiry is the lowest level of evidence (out of inquiry, observation, inspection and re-performance) and might not be sufficient using the current scope of the ISAE 3402 framework. The Bridge letter itself however might be usable to reflect on the proposed additions as set out in paragraph 5.1.

Based on the analysis performed in paragraph 3.1, the following items of the ISAE 3402 framework might contribute to elaborate on the future operating effectiveness of controls:

• Obtaining an Understanding of the Service Organization’s System • Obtain evidence • Subsequent Events • Preparing the Service Auditor’s Assurance Report • Bridge letter

3.2 Analysis of frameworks similar to ISAE 3402 In this sub chapter, several frameworks related and/or similar to ISAE 3402 are analysed. We look into the frameworks, identifying points in the current frameworks, which provide information on the future operating effectiveness within the organizations.

We expect these points to be not explicit regarding future operating effectiveness as we identified that the focus is very limited on this matter. Therefore, we are looking for starting points for gathering information on future operating effectiveness in the current frameworks. If we can incorporate these identified starting points in the ISAE 3402 audit, we are able to give more information on future operating effectiveness.

These identified points are summarized below.

ISAE 3402 - Additions for future operating effectiveness Page 17 of 59

3.2.1 ISAE 3000 A framework that is closely related to the ISAE 3402 framework is the ISAE 3000 framework (IAASB, 2008). “This International Standard on Assurance Engagements (ISAE) deals with assurance engagements other than audits or reviews of historical financial information, which are dealt with in International Standards on Auditing (ISAs) and International Standards on Review Engagements (ISREs), respectively.” When we examine the objective from a practitioner point of view: “6. In conducting an assurance engagement, the objectives of the practitioner are: (a) To obtain either reasonable assurance or limited assurance, as appropriate, about whether the subject matter information (that is, the reported outcome of the measurement or evaluation of the underlying subject matter) is free from material misstatement; (b) To express a conclusion regarding the outcome of the measurement or evaluation of the underlying subject matter through a written report that clearly conveys either reasonable or limited assurance and describes the basis for the conclusion; (Ref: Para. A1) and (c) To communicate further as required by relevant ISAEs.” Results from the analysis related to identify points, which might refer to future operating effectiveness, are summarized below:

• The objective defers from the ISAE 3402 standard leaving more room for professional judgment of the auditor.

When we examine the phase Preparing the Service Auditor’s Assurance Report:

“For example, in an assurance report related to the effectiveness of internal control, it may be appropriate to note that the historic evaluation of effectiveness is not relevant to future periods due to the risk that internal control may become inadequate because of changes in conditions, or that the degree of compliance with policies or procedures may deteriorate.” Results from the analysis related to identify points, which might refer to future operating effectiveness, are summarized below:

• Like the ISAE 3402 standard, ISAE 3000 states that a remark needs to be made in the report regarding future periods and effectiveness of controls.

ISAE 3402 - Additions for future operating effectiveness Page 18 of 59

3.2.2 ISO 27001 The standard describes itself as (British Standard Institute, 2005):

ISO 27001 certification is used by the service provider to show the outside world (i.e. their clients) that their information security is in control. Results from the analysis related to identify points, which might refer to future operating effectiveness, are summarized below:

• The standard refers to a comprehensive Information Security Management System (ISMS) in which changes to the ISMS is included in the standard. The standard takes into account that the ISMS and their supporting systems are subject to change over time. The standard adopts a process approach for establishing, implementing, operating, monitoring, reviewing, maintaining and improving an organization's ISMS. This approach is based on the “plan-do-check-act” (PDCA) model. Assessment of how the organization handles changes in ISMS, and therefore its processes/controls is useful in the light of future operating effectiveness.

If the controls are tested for a certain period of time, one wants to know whether the controls will work in the future and are limited affected by organizational and or process changes. If the user of the service provider is able to gain insight in the management regarding process and/or organization changes, more information can be gathered on the future operating effectiveness of the controls in scope. 3.2.3 SOC1, SOC2 and SOC3 Service Organization Controls (SOC) is a term used in US standards to refer to audit reports giving an attestation regarding controls at a company providing services (AICPA, Service Organization Controls, managing risks by obtaining a Service Auditor's Report, 2010).

SOC 1 engagements are performed in accordance with Statement on Standards for Attestation Engagements (SSAE) 16, Reporting on Controls at a Service Organization. SOC 1 reports focus solely on controls at a services organization that are likely to be relevant to an audit if a user entity’s financial statements. SOC 2 and 3 reports represent significant changes in service organization reporting approaches brought about as a result of several important changes.

“This International Standard has been prepared to provide a model for establishing, implementing, operating, monitoring, reviewing, maintaining and improving an Information Security Management System (ISMS). The adoption of an ISMS should be a strategic decision for an organization. The design and implementation of an organization’s ISMS is influenced by their needs and objectives, security requirements, the processes employed and the size and structure of the organization. These and their supporting systems are expected to change over time. It is expected that an ISMS implementation will be scaled in accordance with the needs of the organization, e.g. a simple situation requires a simple ISMS solution.”

ISAE 3402 - Additions for future operating effectiveness Page 19 of 59

SOC 1 (SSAE 16, AT Section 801)

SOC 1 is based on SSAE 16 or AT Section 801 (AICPA, Reporting on Controls at a Service Organization, 2011).

Results from the analysis related to identify points, which might refer to future operating effectiveness, are summarized below:

• SOC 1 and SSAE 16 standards are much like the ISAE 3402 framework. They cover the same goal and it is clearly noted in AT Section 801 that the objectives of the service auditor is to: a. obtain reasonable assurance about whether, in all material respects, based on suitable criteria,

i. management's description of the service organization's system fairly presents the system that was designed and implemented throughout the specified period (or in the case of a type 1 report, as of a specified date). ii. the controls related to the control objectives stated in management's description of the service organization's system were suitably designed throughout the specified period (or in the case of a type 1 report, as of a specified date). iii. when included in the scope of the engagement, the controls operated

effectively to provide reasonable assurance that the control objectives stated in management's description of the service organization's system were achieved throughout the specified period. b. report on the matters in 6(a) in accordance with the service auditor's findings. (AICPA, Reporting on Controls at a Service Organization, 2011)

Therefore, SOC 1 does not provide in handles to be used for our research other than already mentioned in paragraph 3.1.

Figure 2: Standards (source: AICPA, 2010)

ISAE 3402 - Additions for future operating effectiveness Page 20 of 59

SOC 2 and 3 (AT Section 101)

SOC 2 and 3 are based on AT Section 101 (AICPA, Attest Engagements, 2001) and Trusted Service Principles (AICPA, TRUST SERVICES PRINCIPLES AND CRITERIA, 2014). Important note is that SOC 1 / 2 / 3 are terms on which assurance frameworks can be related to, SOC 1 / 2 / 3 are no assurance frameworks. Furthermore, as noted in the mentioned source above SOC 2 / 3 requires that the audit approach should address, besides the objectives on the financial aspects, the obligated objectives of the Trust Service Principles as well.

Results from the analysis related to identify points, which might refer to future operating effectiveness, are summarized below:

• The AT section 101 does not support including remarks about future operating effectiveness of controls but does also not clearly state that the report should only cover historical data. Instead, the following is mentioned regarding the subject matter: Historical or prospective performance or condition. Therefore, it should be possible to report on future operating effectiveness of controls using SOC 2 or 3.

3.2.4 PCI-DSS The standard describes itself as:

This PCI-DSS framework is concerned with service providers, and therefore relevant in this thesis research for further analysis.

Results from the analysis related to identify points, which might refer to future operating effectiveness, are summarized below:

• In the scope of the PCI-DSS standard, there is no special attention on operating effectiveness of controls. However, the standard does mention that changes to the organizational structure should be appropriately addressed and mapped to the impact on PCI DSS scope and requirements. The periodic (audit) reviews should verify that the PCI DSS requirements continue to be in place at the organization. It does not mention that auditors should provide information on future organizational changes and its impact on the PCI DSS scope and requirements.

• In the standard itself, no references to future operating effectiveness are present.

“The Payment Card Industry Data Security Standard (PCI DSS) was developed to encourage and enhance cardholder data security and facilitate the broad adoption of consistent data security measures globally. PCI DSS provides a baseline of technical and operational requirements designed to protect cardholder data. PCI DSS applies to all entities involved in payment card processing—including merchants, processors, acquirers, issuers, and service providers, as well as all other entities that store, process or transmit cardholder data and/or sensitive authentication data” (PCI Security Standards Council, 2013).

ISAE 3402 - Additions for future operating effectiveness Page 21 of 59

3.2.5 ISA 520 – Going Concern As we understand from the International Standard on Auditing 520, as published on the IFAC website (IFAC, 2009) and described in the PwC audit guide (PricewaterhouseCoopers, 2014), this standard describes the auditor’s responsibilities in the audit (of financial statements) relating to management’s use of the going concern assumption (in the preparation of the financial statements).

Under the going concern assumption, an entity is viewed as continuing in business for the near future. This means that the results of the audit (in this case of the ISA 520 the general purpose financial statements) are prepared on a going concern base. In some of the financial reporting frameworks, require the management to make a specific assessment of the entity’s ability to continue as a going concern. The auditor’s responsibility is to obtain sufficient appropriate audit evidence about the appropriateness of management’s use of the going concern assumption.

Results from the analysis related to identify points, which might refer to future operating effectiveness, are summarized below:

• As the going concern is focused on the overall continuity of the business of the entity, we believe that we can use the same responsibility outlines, as described in the ISA 520, to enforce the auditor and management to assess the effect of current or near future developments within the entity on the (future) operating effectiveness of the entity’s controls. For instance, major IT system migrations or reorganizations can have an impact on the operating effectiveness of controls. With the responsibility, outlines similar to those in ISA 520, management and the auditor are required to assess the entity’s ability to maintain effectively operating controls.

Conclusion

Based on the analysis of the different frameworks above, we conclude that:

• The objective of ISAE 3000 defers from the ISAE 3402 standard leaving more room for professional judgment of the auditor and it states that a remark needs to be made in the report regarding future periods and effectiveness of controls.

• The ISO27001 standard refers to a comprehensive Information Security Management System (ISMS) in which changes to the ISMS is included in the standard. The standard adopts a process approach for establishing, implementing, operating, monitoring, reviewing, maintaining and improving an organization's ISMS. This approach is based on the “plan-do-check-act” (PDCA) model.

• The AT section 101 does not clearly state that the report should only cover historical data. Instead, the following is mentioned regarding the subject matter: Historical or prospective performance or condition. Therefore, it should be possible to report on future operating effectiveness of controls using SOC 2 or 3.

• PCI-DSS mentions that changes to the organizational structure should be appropriately addressed and mapped to the impact on the scope and requirements.

ISAE 3402 - Additions for future operating effectiveness Page 22 of 59

• The responsibility outlines, as described in the ISA 520, can be used to enforce

the auditor and management to assess the effect of current or near future developments within the entity on the (future) operating effectiveness of the entity’s controls.

ISAE 3402 - Additions for future operating effectiveness Page 23 of 59

4 Exploratory interviews and results In this chapter, additional research, on top of the literature research, is performed on the actual reality of the ISAE 3402 standard. To get a good overview of the practice, use and performing the ISAE 3402 audit in reality, we have chosen to perform semi-structured interviews with the stakeholders of the ISAE 3402 audits. The interviews serve an explanatory goal within this thesis research on the appliance of the ISAE 3402 in practice. In this way, we can combine and merge the research results from both the theory as the reality, in order of coming to a realistic approach on giving more information regarding future operating effectiveness within the ISAE 3402 reports.

4.1 Interview approach The interviews are held with the stakeholders involved with an ISAE 3402 audit. To gain a complete overview of the use and view of the ISAE 3402 reports, we have selected four perspectives from which we arranged the interviews.

1) External auditor, performing ISAE 3402 audits 2) Service provider organization, the auditee 3) Domain expert on the subject of ISAE 3402 4) User organization (the firm that relies on the services of the service provider. In

this case, a user organization with a reasonably sized internal audit department)

For the four different perspectives, we have selected the persons / organizations, which are significantly involved in ISAE 3402 and have a strong opinion on the standard and its developments. This way we want to acquire as much information from the interviewees as possible.

With these four perspectives, adequate insight is acquired on the use and view of ISAE 3402 reports. Insight in the practical use of the ISAE 3402 is gained, in which we can also detect the limitations of the framework in practice. Interviewees, from their perspectives, experience and knowledge share their ideas on possible additions/solutions – which can lead us to broaden or deepen our research.

The number of interviews and combination of different perspectives validates the output of the interviews. The interviews are semi-structured, and based both the results from the literature study within this thesis research as well as our knowledge and experience as external auditors performing the ISAE 3402 audits.

Below the interviewee’s and their role are summarized. From each interview we have summarized the points that we have discussed, this can be found in the appendix of this thesis. We have anonymized the interviewee’s names, the names are known with the thesis supervisors.

Interviewee’s

Service provider

A Controller working for a fast growing Payment Service Provider, ISAE 3402 audits are performed annually in his organization.

ISAE 3402 - Additions for future operating effectiveness Page 24 of 59

Client of a service provider

Involved in many client consultations to intermediate on behalf of the user organization with the service organization(s).

External Auditor

Involved in the execution of many ISAE 3402 engagements by the (Big 4) firm.

Domain expert

Involved in many (global) developments regarding SAS70 and ISAE 3402. Currently in discussion with NBA/NOREA on SOC2 audits.

Question structure

Per interviewee, we have defined open and closed questions. For each person / role, dependable on their role in relation to ISAE 3402 audits, we have additional questions. Both the general as the additional questions based on the interviewee’s role are summarized below. Please note that we have not walk through the questions on a sequential manner, as the questions function as a guide for the interviews, but are not exhaustive. In this way, the interviewees have enough space to bring their own opinions and suggestions for the framework.

Questions (general)

• Can you describe your professional role and background • How does your profession relate to the ISAE 3402 framework • What do you like and dislike about the ISAE 3402 framework • What is your view regarding the limitation of future operating effectiveness of

controls • What is your experience in practice related to the limitations • What would be regarded as added value to the report when issued without the

mentioned limitations • What would you suggest to add or change to mitigate the limitations

Questions (domain specific)

Service Provider

• Do you have the insight in your processes to assess operating effectiveness of control objectives over the coming year

• Which conditions needs to be addressed (e.g. technology, people and processes)

Auditor

• What is needed to use a ISAE 3402 more efficiently / effectively in your audit • How would you embed the suggested additions in the ISAE 3402 audit

approach Client of service provider

• Would it give you more assurance if a report is issued without the mentioned limitations

ISAE 3402 - Additions for future operating effectiveness Page 25 of 59

Domain expert

• Is it possible within the boundaries of the audit standard to mention future operating effectiveness in the report, if the information is available to the auditor

• Which developments do you see in the audit profession regarding third party assurance that would affect our object of research

4.2 Interview results The complete results of the interviews are part of the appendix. The most important results are documented below.

Choosing the right framework covering the need for assurance Both the Domain Expert as Client of the Service Provider mentioned in their interviews that the ISAE 3402 framework is sometimes stretched to cover more needs than originally intended. To some stakeholders, a Service Level Agreement and Reporting is sufficient to the need for assurance. Therefore, there is no need to use the ISAE 3402 framework for such assurance when other formats and frameworks are in place.

Based on our review of the ISAE 3402 framework, the SOC frameworks and the ISAE 3000 framework, the following additions are suggested:

• The ISAE 3000 framework covering the 3402 format enables the auditor to extend the scope of the audit beyond the limitations of 3402. The auditor can base its audit on the principles of the 3402 standard, but is not bound to its limitations.

• SOC 2/3 enables the auditor to extend the scope of SOC1 beyond its limitations (similar to the ISAE 3402 framework)

Organizational change management Both the Domain Expert and Service Provider indicated in their interviews that there is a need to continuously monitor organizational changes and its impact on the controls in scope of the ISAE 3402 audit. The PCI-DSS framework mentions this aspect as well. The Service Provider mentioned in the interview that an Internal Audit function which is actively involved in managing the achievement of control objectives, related to the ISAE 3402 scope, is highly recommended and might contribute to ensure future operating effectiveness of controls. The Domain Expert suggested in the interview that we should assess the change management processes over the changes in primary process to determine how the organization estimates the impact of process changes and its impact on the control objectives. Theses assessments can be part of the description of COSO elements, as pointed out by interviewed External Auditor. With the combined view of the controls framework and the COSO elements in place the user of the report can form its own opinion on the future operating effectiveness of the controls and/or the control organization in total.

Based on our review of the PCI-DSS framework and ISO 27001 and the performed interviews, the following additions are suggested:

ISAE 3402 - Additions for future operating effectiveness Page 26 of 59

• An approach is implemented for establishing, implementing, operating, monitoring, reviewing, maintaining and improving an organization's internal control system.

• An Internal Audit function is established and actively involved in managing the achievement of control objectives related to the ISAE 3402 scope.

• Both additions can be part of the COSO assessment in the existing audit approach and report.

Meta controls and automated controls During the interviews with the Domain Expert and the External Auditor mentioned that when a company’s internal control system is more mature, Meta controls covering regular controls are implemented that contribute to a more mature control environment. Meta controls can be defined as controls implemented to monitor the key controls. Therefore, it is more likely that controls in mature environment with Meta controls implemented will continue to operate effectively in the future. These Meta controls can be part of an organization wide quality management system.

Examples of monitoring controls include monitoring controls over key controls but can also controls regarding the reliability of Service Level Reports, which the service organization sends to their user organizations. This way the user organization gets reliable insight in the performance of the Service Provider during the year, even after the audit report has been issued. This can be regarded as form of information on “future operating effectiveness” of controls, as the audit report is older than the information provided by the Service Level Report. Important is that the KPI’s internally within the service organization are aligned with the KPI’s mentioned towards the user organization, on which the latter relies on. The Meta controls can be included in the controls framework, so the recent audit approach is not required to be changed.

With reliable periodic Service Level Reports, the user organization can better anticipate on possible failure of controls. As these controls are included in the controls framework, no special adjustment on the audit approach is required.

The same holds for automated controls, which are unlikely to operate ineffectively working except when the IT General Controls are found to be inadequate. These IT General controls can be part of an organization wide quality management system as well.

Based on the interviews, the following additions are suggested:

• The amount of automated controls as a percentage of the total control measures per control given the presence of reliable IT General Controls.

• Include Meta controls, such as monitoring controls over key controls and controls over reliability of Service Level Reporting in the controls framework.

Figure 3: Meta controls

C C

MC

ISAE 3402 - Additions for future operating effectiveness Page 27 of 59

Directive Report According to the interviewed Service Provider, a Directive Report by management is always part of the annual report of a company. Such a report is not part of a standard ISAE 3402 report in which only a management’s assertion is included and the system description. This report can be setup because of similar guidelines as described in ISA 520. This means that management is required to assess the impact of current of near future developments within the entity on the operational effectiveness of its controls.

Based on the interviews, the following additions are suggested:

• A statement of direction by management is required and should be part of the report to be issued. This means that management is required to assess the impact of current of near future developments within the entity on the operational effectiveness of its controls.

The conceptual additions to the regular ISAE 3402 audit approach as derived from the interviews held, combined with the results from the literature study are described in chapter 4.2

4.3 Additions in the regular ISAE 3402 audit approach as derived from research

The results from the literature study and the interviews held combined and analysed, we have derived the following suggestions and / or conceptual additions on providing more information on future operating effectiveness.

4.3.1 Choose the assurance framework to address the assurance need

1) ISAE 3000 framework covering the 3402 format enables the auditor to extend the scope of the audit beyond the limitations of 3402.

2) SOC 2/3 enables the auditor to extend the scope of SOC1 beyond its limitations (similar to the ISAE 3402 framework)

4.3.2 Planning and understanding the client 1) Gain an update of knowledge of, and review the effects of applicable industry

and regulatory standards with a focus on significant changes affecting the current period or future periods.

2) An approach is implemented for establishing, implementing, operating, monitoring, reviewing, maintaining and improving an organization's internal control system. This approach can be included in the current COSO assessments. Note the changes within the organization and its impact on the control framework.

3) An Internal Audit function is established and actively involved in managing the achievement of control objectives related to the ISAE 3402 scope. This information can be included in the current COSO assessments

ISAE 3402 - Additions for future operating effectiveness Page 28 of 59