Irish Water: Phase 1 Report - Minister for Housing ... · Irish Water: Phase 1 Report Page 2 of 148...

148

Irish Water: Phase 1 Report 2nd November 2011

Transcript of Irish Water: Phase 1 Report - Minister for Housing ... · Irish Water: Phase 1 Report Page 2 of 148...

Irish Water:Phase 1 Report

2nd November 2011

Irish Water: Phase 1 Report

Page 2 of 148

Private and ConfidentialMr. Mark GriffinAssistant SecretaryDepartment of Environment, Community and Local GovernmentCustom HouseDublin 1

2nd November 2011

Dear Mark,

In accordance with your instructions as confirmed in our contract dated 10th June2011, we now include our second interim report which reports uponrecommendations for the optimal organisational form for water services delivery inIreland.

We draw your attention to important comments regarding the scope and process ofour work set out immediately following this letter.

This is an interim report, which based on our review of information provided byDECLG ("Department") officials and local authorities, meetings with a range ofstakeholders agreed with the Department, our review of international experiencewith the establishment of structures to provide water services and the experienceof our team, recommends an organisational form for water services in Ireland. Ourfinal report will in addition, include issues associated with the implementation ofthe model, as selected by the Department for delivery of water services in Ireland.Our comments in this interim report are subject to amendment or withdrawal; ourdefinitive findings and conclusions will be those set out in the final report.

You may not make copies of this report available to other persons except for thepurpose of assessing the optimal structure for water services delivery in Ireland.We will not accept any duty of care, (whether in contract, tort (includingnegligence) or otherwise) to any person other than you, except under thearrangements described in the Contract between us.

Yours faithfully

Garrett CroninPartner

T: 01 7928807F: 01 7926766

Irish Water: Phase 1 Report

Page 3 of 148

Important Message

Important message to any person not authorised to have access to this report

Any person who is not an addressee of this report or who is not receiving this report directly from anaddressee for the purpose of assessing the optimal structure for water services delivery in Ireland is notauthorised to have access to this report.

Should any unauthorised person obtain access to this report, by reading this report such person acceptsand agrees to the following terms:

1. The reader of this report understands that the work performed by PricewaterhouseCoopers wasperformed in accordance with instructions provided by our addressee client and was performedexclusively for our addressee client's use.

2. The reader of this report acknowledges that this report was prepared at the direction of our addresseeclient and may not include all procedures deemed necessary for the purposes of the reader.

3. The reader agrees that PricewaterhouseCoopers, its partners, principals, employees and agents neitherowe nor accept any duty or responsibility to it, whether in contract or in tort (including withoutlimitation, negligence and breach of statutory duty), and shall not be liable in respect of any loss, damageor expense or whatsoever nature which is caused by any use the reader may choose to make of thisreport, or which is otherwise consequent upon the gaining of access to the report by the reader. Further,the reader agrees that this report is not to be referred to or quoted, in whole or in part, and not todistribute the report without PricewaterhouseCoopers' prior written consent.

Irish Water: Phase 1 Report

Page 4 of 148

Scope Process

Purpose of theStudy

To undertake an independent assessment of the transfer of responsibility for water services provision fromthe local authorities to a water utility and to recommend the most effective assignment of functions andstructural arrangements for delivering high quality competitively priced water services to customers(domestic and non-domestic) and for infrastructure provision; in particular to examine two principal formsof potential company structure (or variants of those forms) for Irish Water:

A water company which would be a self funding water utility in a regulated environment, responsible foroperation, maintenance and investment in all water services infrastructure, customer billing, charging;and

A company charged mainly with investment in the sector (strategic planning, delivery of projects of aregional/national priority, national metering programme) with local authorities operating as agents ofthe company, retaining their operational responsibilities and for delivery of smaller scale investment.

Scope of ourWork

This report covers phase 1 of the engagement and includes;

An assessment of current water and wastewater services in Ireland;

An overview of relevant models from other jurisdictions;

Recommendations on the optimal organisational form for water services delivery in Ireland;

Recommended target operating model, including financial and funding considerations;

Assessment of the potential role for an existing State agency;

Transition strategy; and

Legal considerations in the implementation of the recommendations.

ApproachAdopted

The approach to conducting Part I of the study has been to:

Assess the strengths and weaknesses of the current model for provision of water services in Ireland toidentify the challenges that would need to be addressed by a new model for water service delivery,without losing the positive aspects of the current model;

Review the Models for Water Service Provision Internationally to identify trends and lessons to belearned for water sector reform in Ireland;

Take Soundings from Stakeholders in the sector regarding the changes they feel would best deliverimproved services for Ireland and the implementation challenges for any new model;

Identify potential operating models for Irish Water and Evaluate those Models against a set ofEvaluation Criteria based on Policy Requirements for water reform in Ireland;

Describe the Recommended Operating Model and its financial, legal, organisational, staffing,environmental and other implications; and

Develop a High Level Transition Strategy designed to minimise the delay in achieving the benefitswhile managing the implementation risks of the recommended operating model.

Sources ofInformation

Information was received through:-

Consultation stakeholders (listed in Section 1), some of whom also made written submissions;

Information provided on request by the DECLG, the local authorities and the LGMA;

Publically available information;

Research on international best practice.

PwC have not audited or independently validated any of the information provided.

ManagementRepresentations

We have shown a draft of this report to the Department sponsors and to the extent that we considerappropriate, we have incorporated their comments in this report.

Irish Water: Phase 1 Report

PwC Page 5 of 148

Table of Contents1. Executive Summary ........................................................................................................................... 10

Background .................................................................................................................................................................................... 10

Purpose of the Study...................................................................................................................................................................... 10

Approach .........................................................................................................................................................................................11

Strengths and Weaknesses of the Current Model .........................................................................................................................11

International Experience............................................................................................................................................................... 13

Stakeholder Soundings .................................................................................................................................................................. 13

Operating Models Considered....................................................................................................................................................... 13

Operating Model Recommended for Irish Water......................................................................................................................... 15

Regulation ...................................................................................................................................................................................... 16

Potential Role for an Existing State Agency ................................................................................................................................. 16

Financial Analysis ...........................................................................................................................................................................17

Transition....................................................................................................................................................................................... 18

Next Steps ...................................................................................................................................................................................... 19

2. Introduction and Overview ................................................................................................................ 21

Background .................................................................................................................................................................................... 21

Objectives and Scope of the Study ................................................................................................................................................ 21

Policy Context ................................................................................................................................................................................22

Challenges Facing Water Provision in Ireland .............................................................................................................................23

Objectives of Reform Programme.................................................................................................................................................24

Consultation Process .....................................................................................................................................................................25

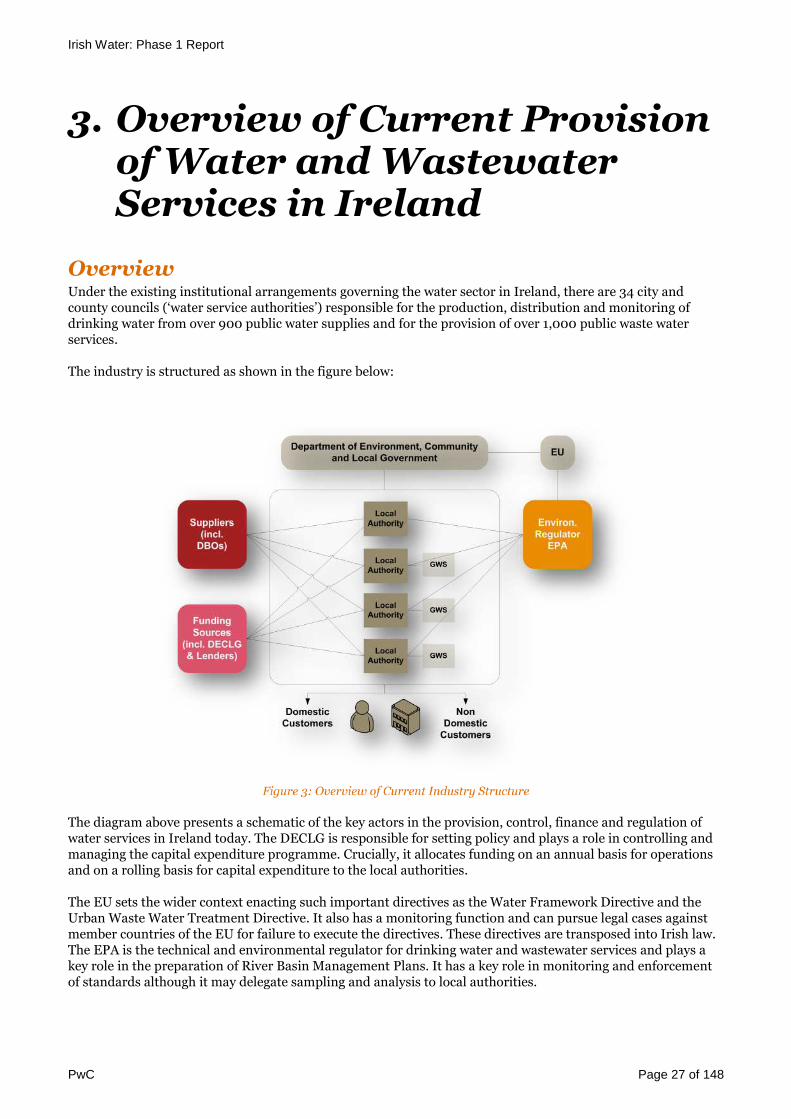

3. Overview of Current Provision of Water and Wastewater Services in Ireland.................................... 27

Overview......................................................................................................................................................................................... 27

Legislative Framework ..................................................................................................................................................................28

Economic and Funding Situation..................................................................................................................................................30

Regulation ......................................................................................................................................................................................32

Leadership and Coordination........................................................................................................................................................33

Operations...................................................................................................................................................................................... 35

Asset Management and Capital Programme ................................................................................................................................36

Customer Service and Billing ........................................................................................................................................................40

Finance ........................................................................................................................................................................................... 41

Staffing ...........................................................................................................................................................................................49

Marketing and Communications................................................................................................................................................... 51

MIS/IT............................................................................................................................................................................................52

Current Initiatives.......................................................................................................................................................................... 53

Indicators of Performance............................................................................................................................................................. 55

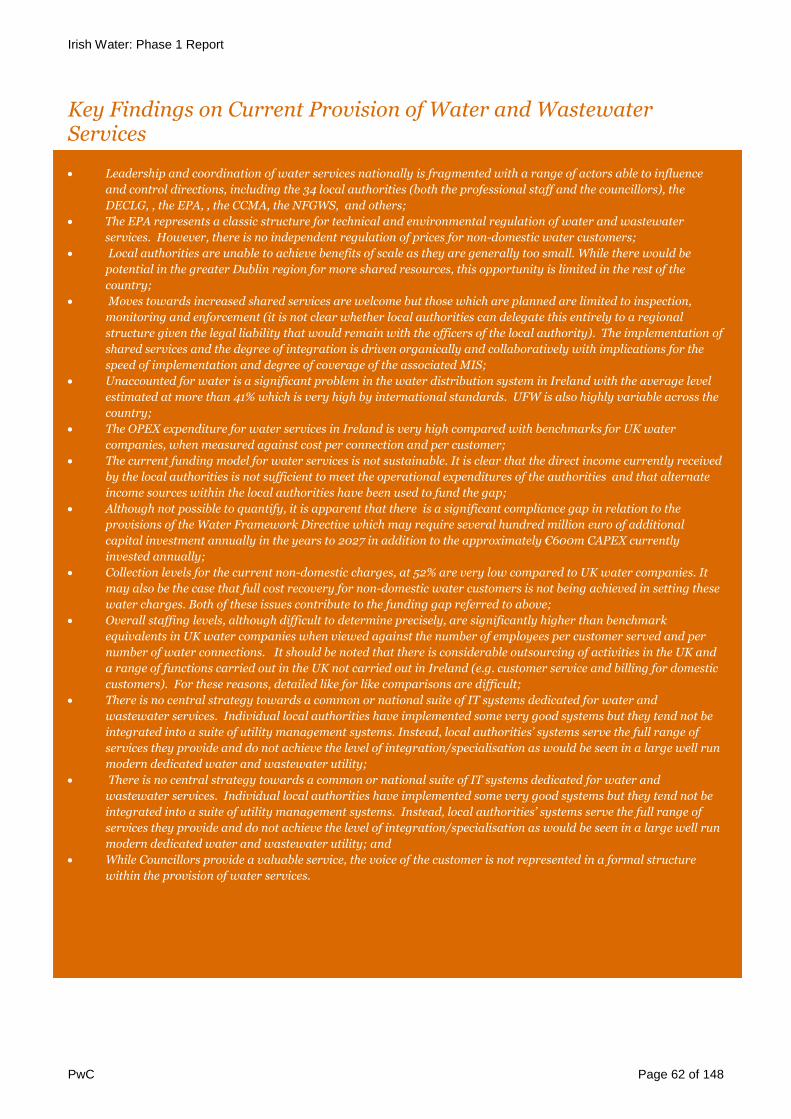

Summary Assessment of the Current Provision of Water and Wastewater Services ................................................................. 61

4. Overview of Relevant Models from other Jurisdictions ...................................................................... 67

Introduction ................................................................................................................................................................................... 67

Key Observations ...........................................................................................................................................................................68

Irish Water: Phase 1 Report

PwC Page 6 of 148

Implications for Irish Water.......................................................................................................................................................... 73

5. Options for Reform............................................................................................................................. 75

Overview of Options ...................................................................................................................................................................... 75

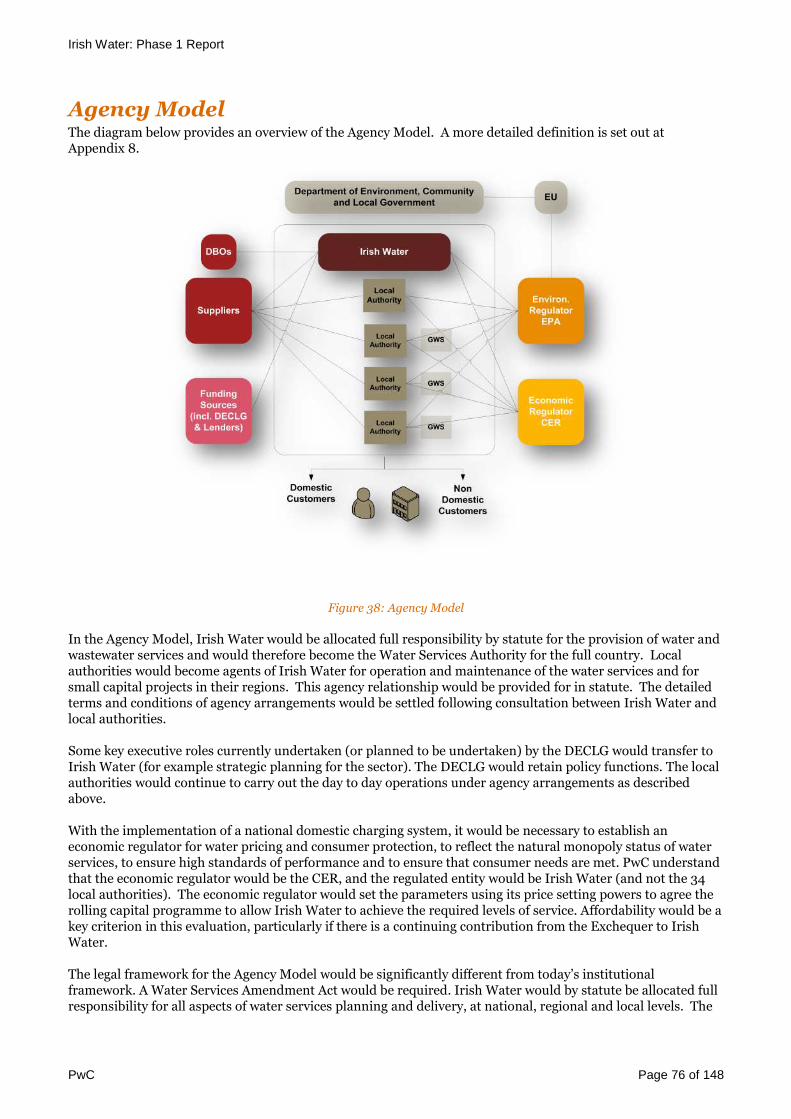

Agency Model................................................................................................................................................................................. 76

Public Utility Model ....................................................................................................................................................................... 79

Minimal Change Model .................................................................................................................................................................82

Intercommunal Model...................................................................................................................................................................84

Models Selected for Further Evaluation .......................................................................................................................................87

6. Evaluation Process.............................................................................................................................90

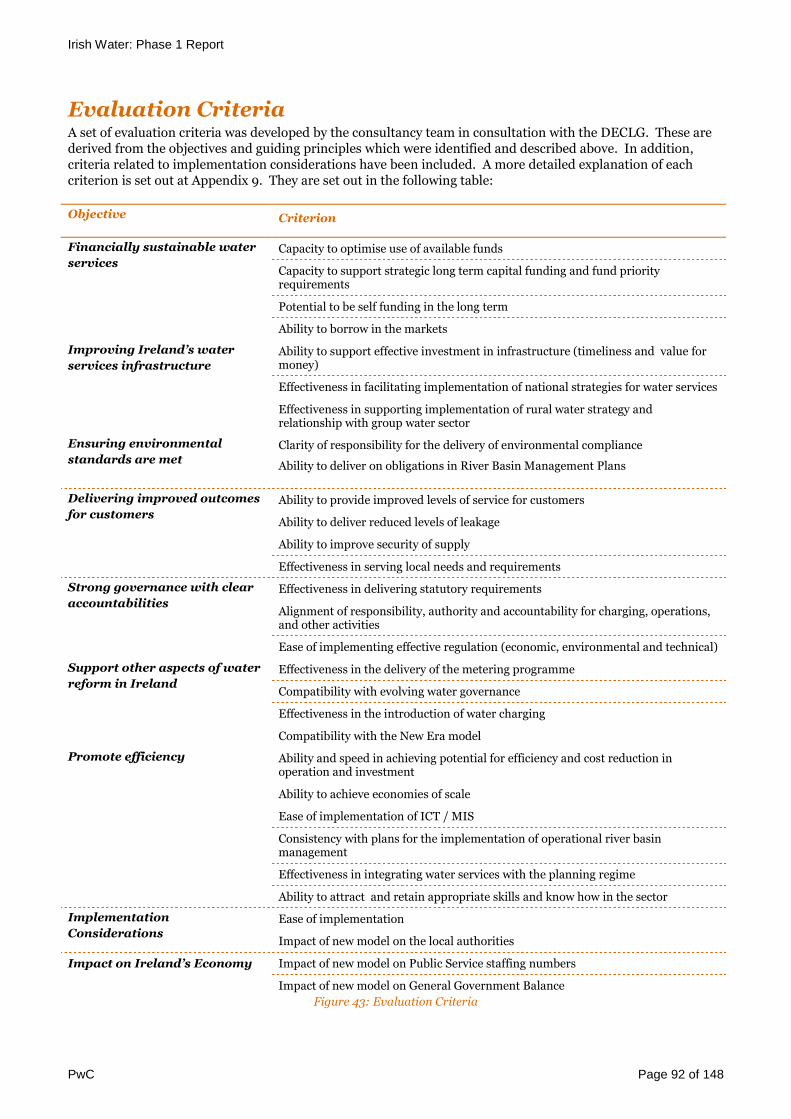

Objectives for Reform....................................................................................................................................................................90

Guiding Principles ......................................................................................................................................................................... 91

Evaluation Criteria.........................................................................................................................................................................92

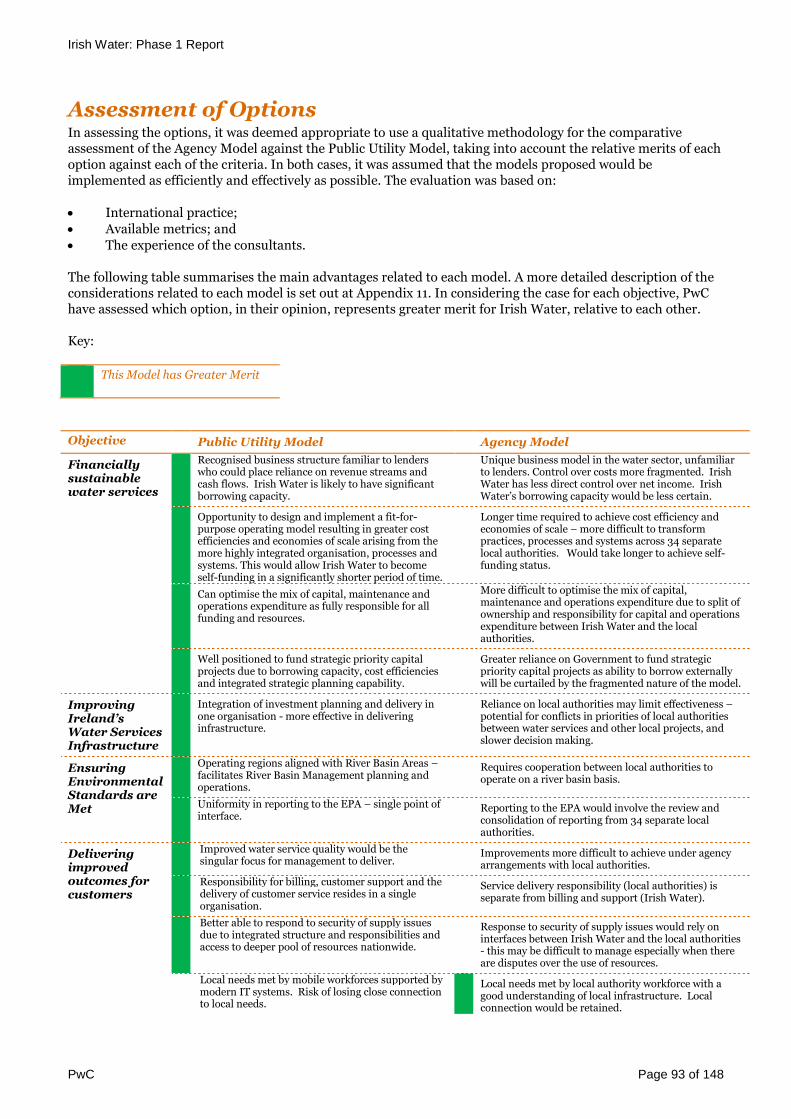

Assessment of Options...................................................................................................................................................................93

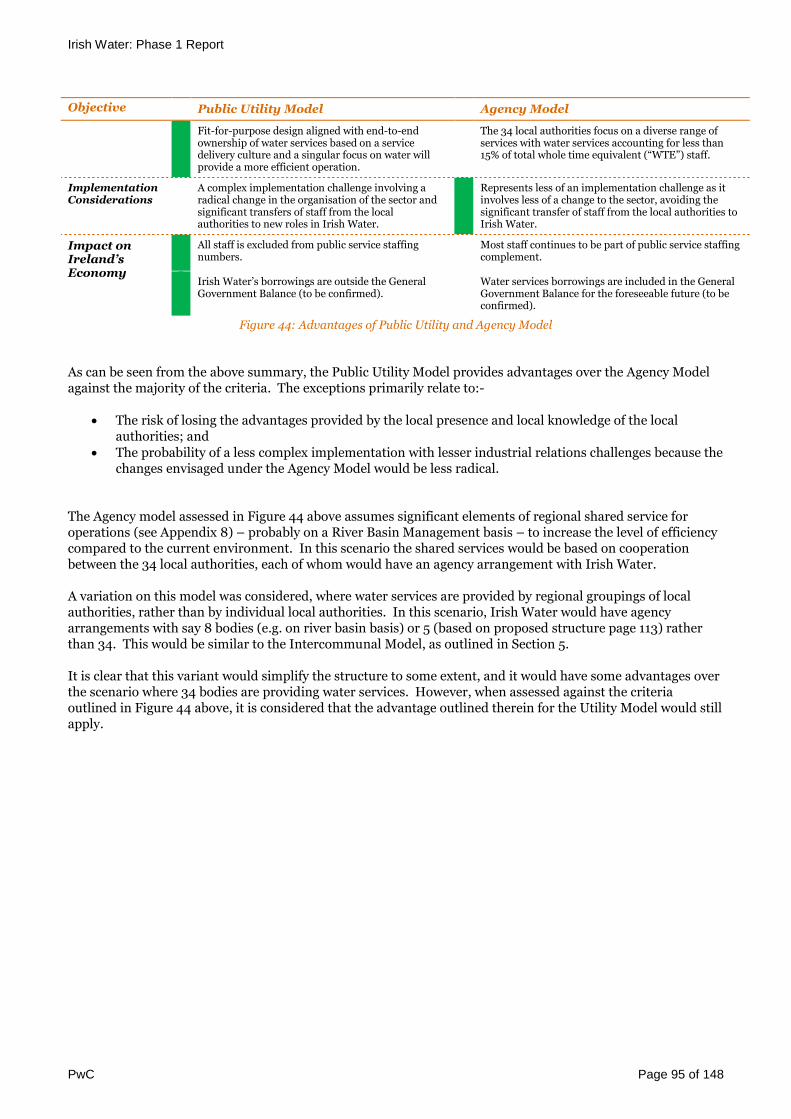

Conclusion on Assessment of Options ..........................................................................................................................................96

Recommended Option for Irish Water ......................................................................................................................................... 97

7. Assessment of Potential Role for an Existing State Agency .................................................................. 99

Irish Water Requirements .............................................................................................................................................................99

Relevant State Agencies.................................................................................................................................................................99

Use of an Existing State Agency ..................................................................................................................................................100

8. Recommended Target Operating Model ........................................................................................... 106

Legal and Institutional Framework ............................................................................................................................................ 106

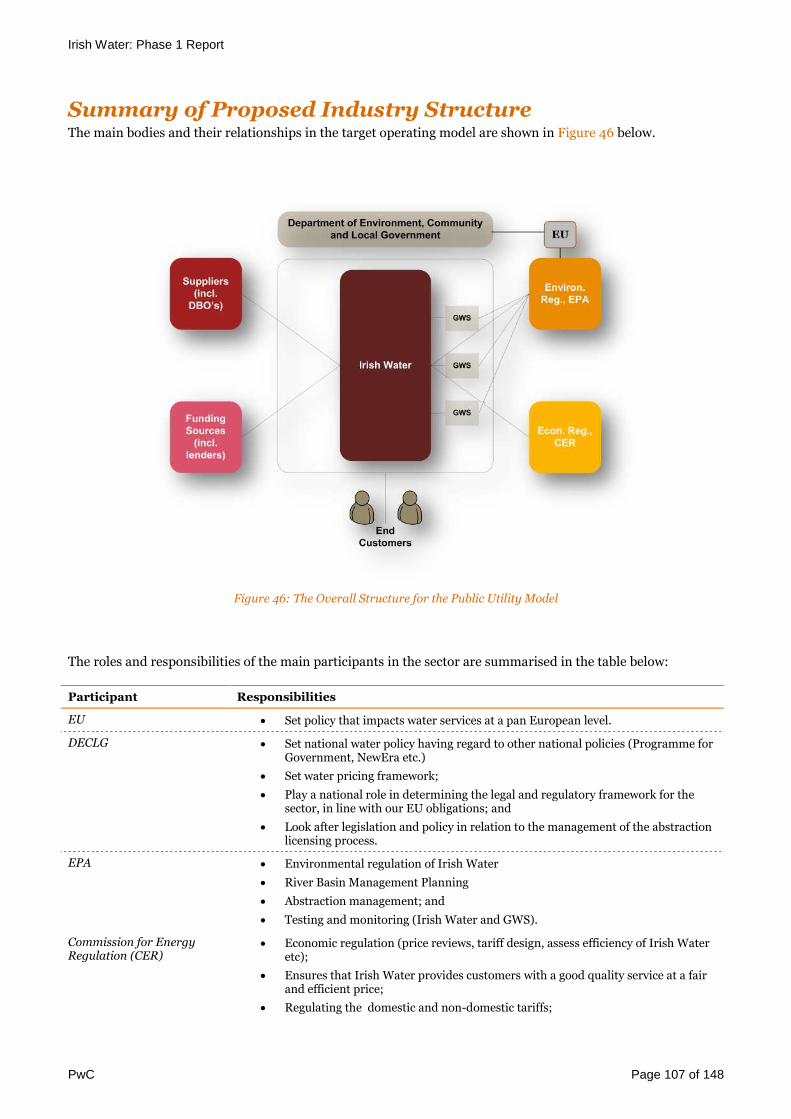

Summary of Proposed Industry Structure.................................................................................................................................. 107

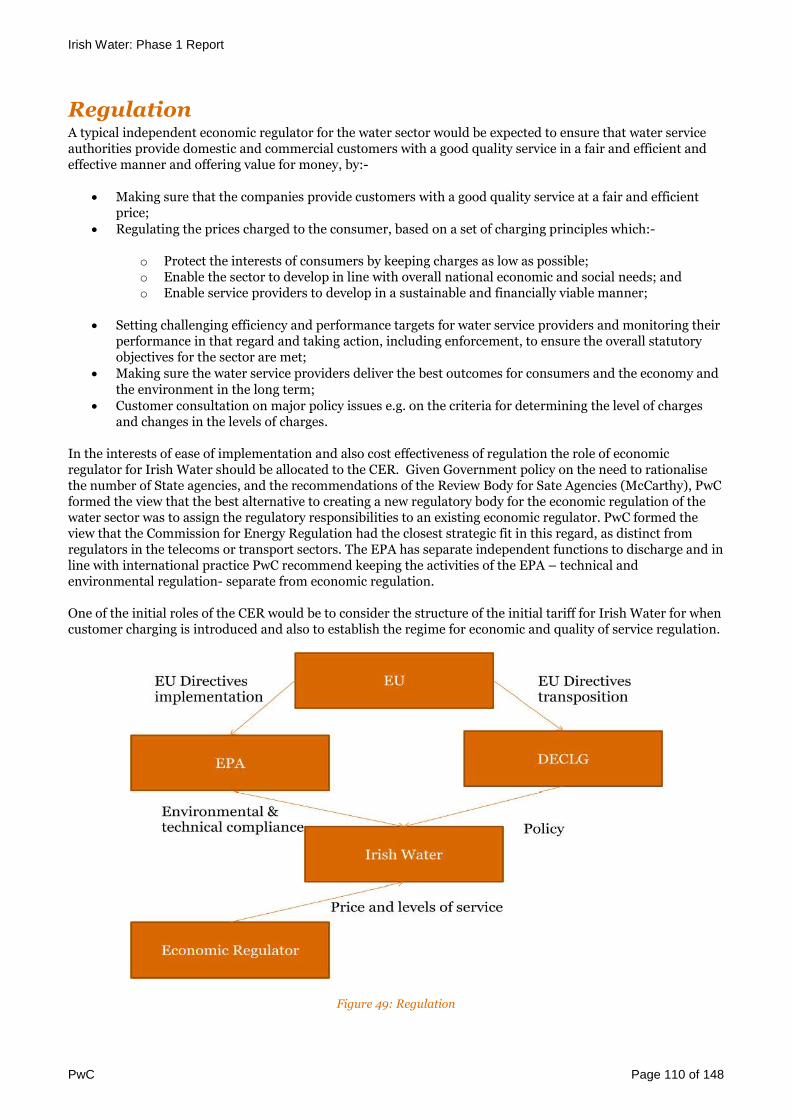

Regulation .....................................................................................................................................................................................110

Leadership and Coordination....................................................................................................................................................... 111

Operations.....................................................................................................................................................................................112

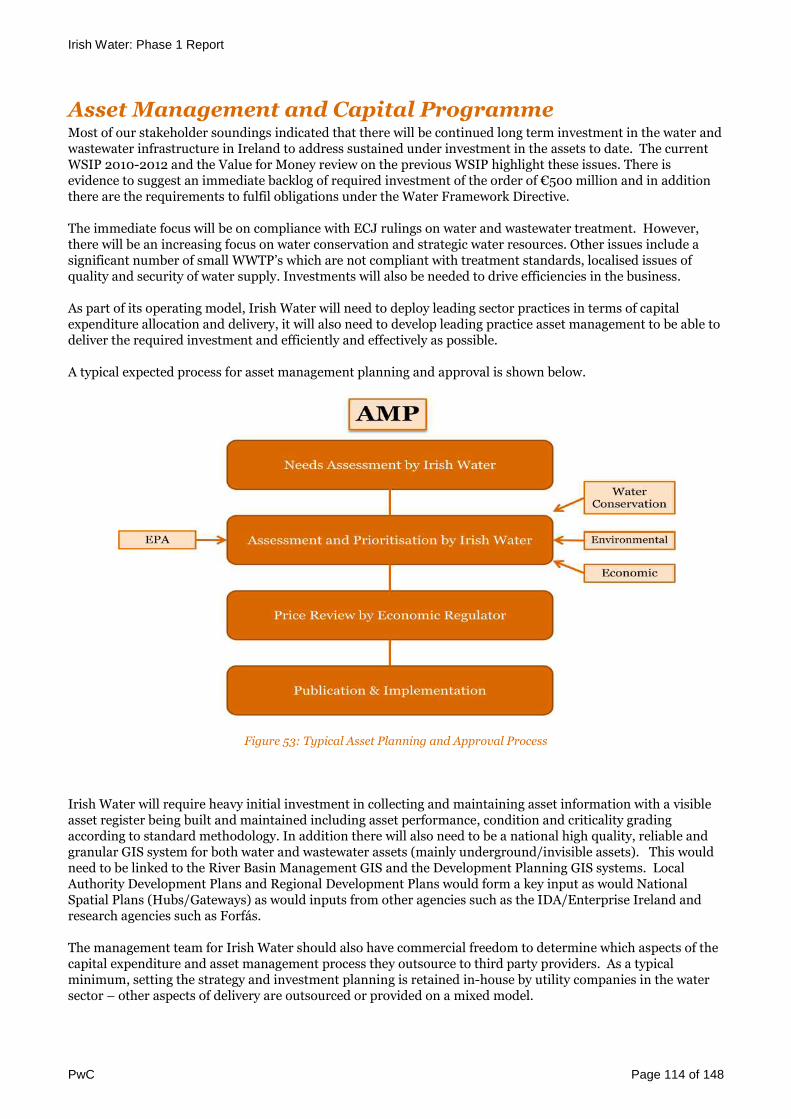

Asset Management and Capital Programme ...............................................................................................................................114

Customer Service and Billing .......................................................................................................................................................115

Funding Requirements and Financial Arrangements.................................................................................................................116

Staffing ..........................................................................................................................................................................................119

Marketing and Communications................................................................................................................................................. 120

MIS/IT.......................................................................................................................................................................................... 120

Integration into Regional and Local Planning.............................................................................................................................121

The Role of Competition in the Provision of Water Services ..................................................................................................... 122

Annex 1 to Section 8 - Detailed Financial Workings ...............................................................................124

9. Transition Strategy...........................................................................................................................139

10.Implementation Considerations - Legal ............................................................................................145

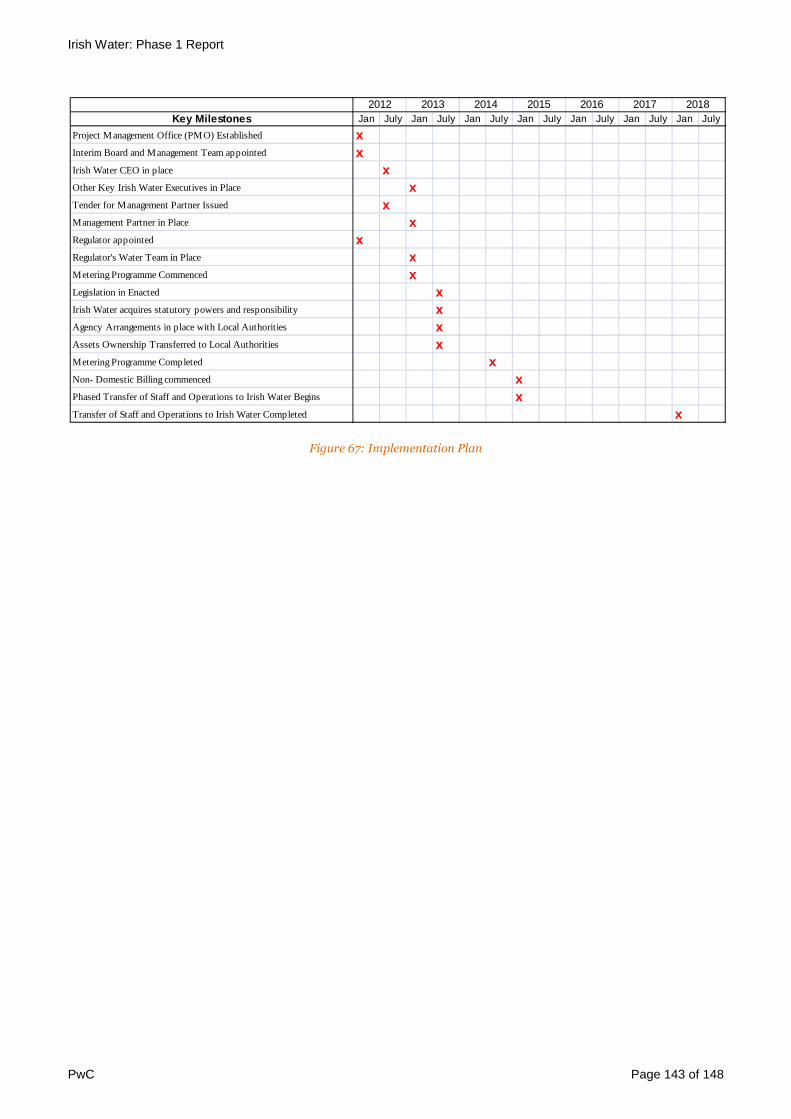

Figure 1: Phased Transition Strategy.......................................................................................................................................... 18

Irish Water: Phase 1 Report

PwC Page 7 of 148

Figure 2: Participants in Consultation Process...........................................................................................................................25

Figure 3: Overview of Current Industry Structure..................................................................................................................... 27

Figure 4 : Funding sources for water sector operating expenditure in Ireland (Source – Unaudited Annual Financial

Statements 2010)........................................................................................................................................................................... 31

Figure 5 : Funding sources for water sector capital expenditure in Ireland (Source – Unaudited Annual Financial

Statements 2010)...........................................................................................................................................................................32

Figure 6: NDP Expenditure Trend €ms 2000 – 2009 (Source VFM Study).............................................................................32

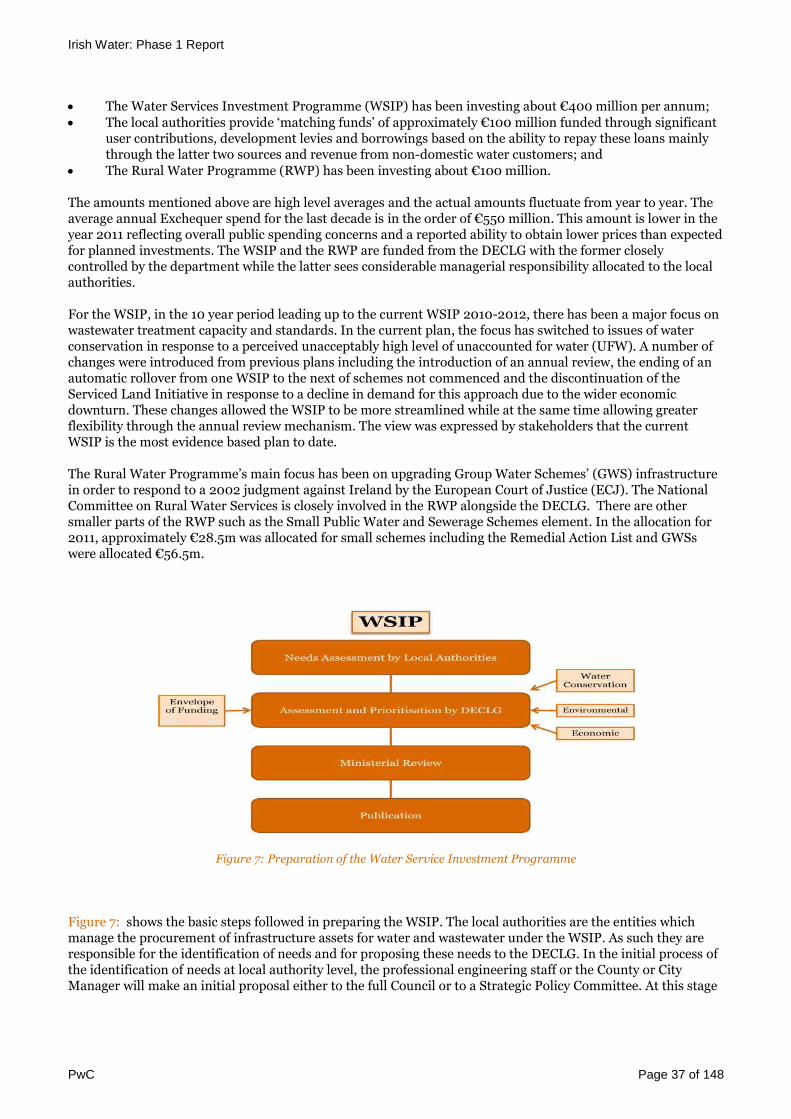

Figure 7: Preparation of the Water Service Investment Programme ....................................................................................... 37

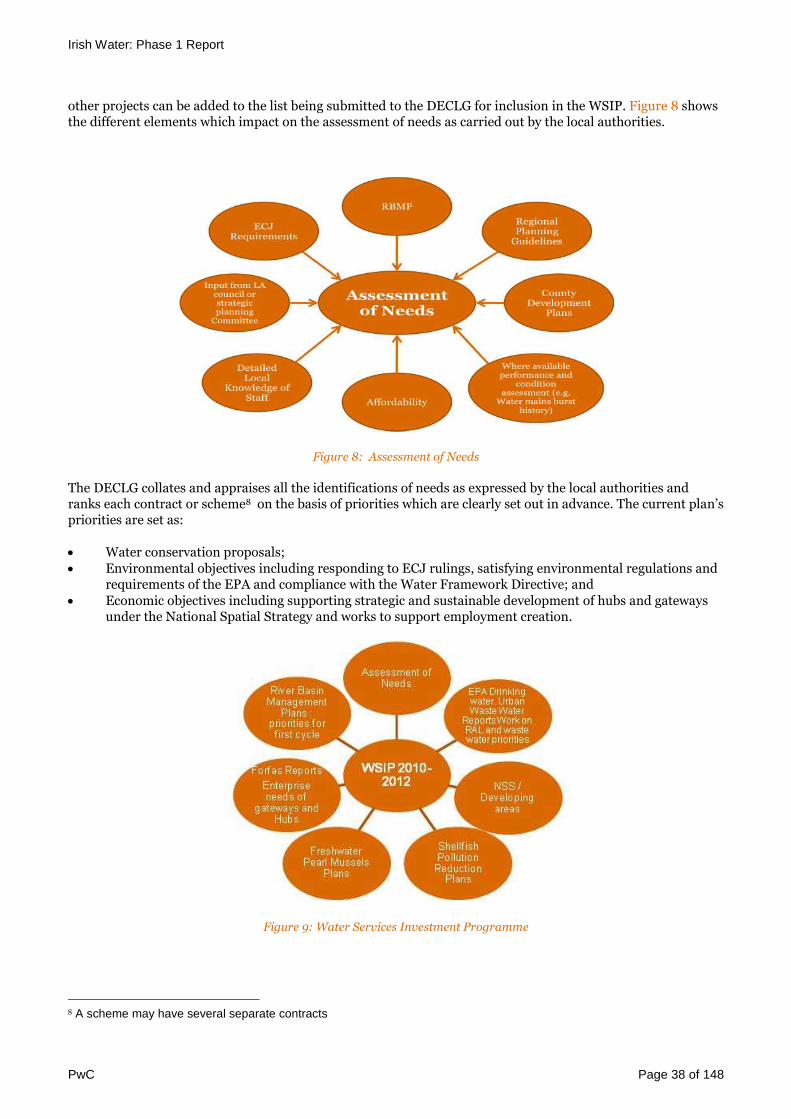

Figure 8: Assessment of Needs ....................................................................................................................................................38

Figure 9: Water Services Investment Programme .....................................................................................................................38

Figure 10: Basic Project Steps ......................................................................................................................................................39

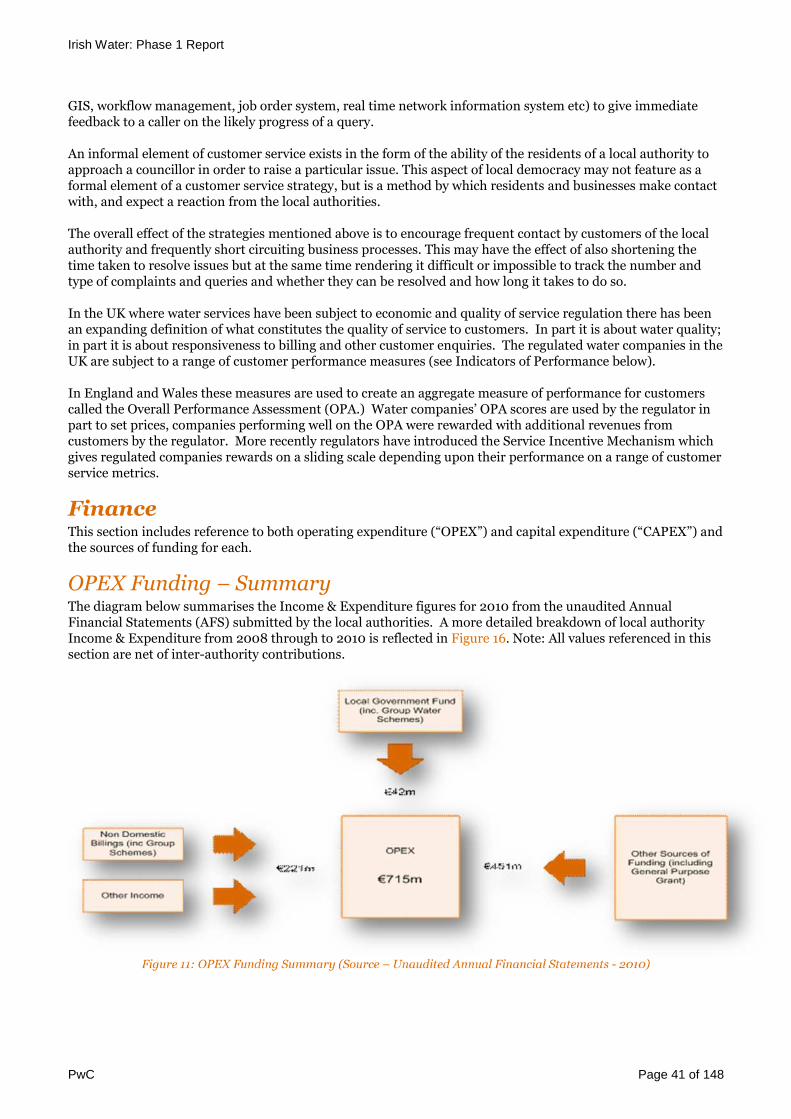

Figure 11: OPEX Funding Summary (Source – Unaudited Annual Financial Statements - 2010) ......................................... 41

Figure 12: Direct Income to Fund OPEX €m (2008 – 2010 Actuals plus 2011 Budget)...........................................................42

Figure 13: Commercial Collection Rates (2010)..........................................................................................................................43

Figure 14: Breakdown of OPEX Expenditure for 2010...............................................................................................................43

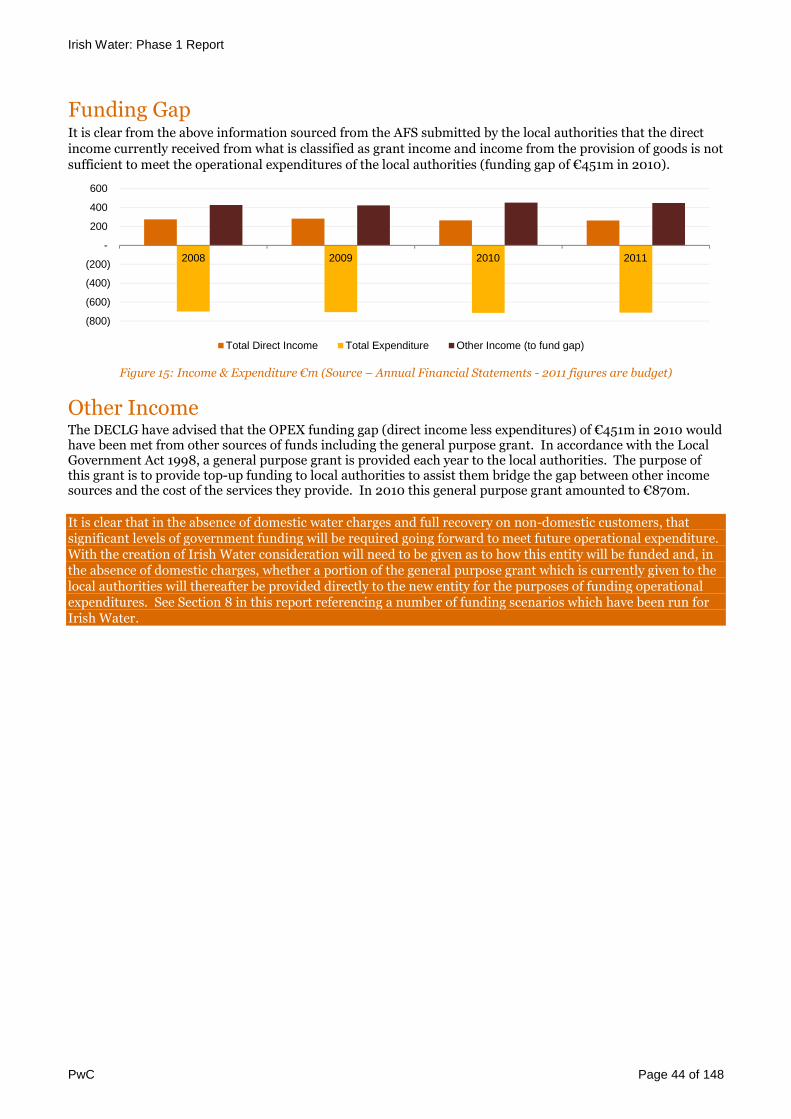

Figure 15: Income & Expenditure €m (Source – Annual Financial Statements - 2011 figures are budget) ...........................44

Figure 16: Income & Expenditure (2008 – 2010) .......................................................................................................................45

Figure 17: CAPEX Funding-Overview (2010) .............................................................................................................................46

Figure 18: CAPEX Movement €m (2010) ....................................................................................................................................46

Figure 19: Percentage breakdown of CAPEX funding (exc. opening and closing balances but including transfers)............ 47

Figure 20: NDP Expenditure Trends €m (2000 – 2009)........................................................................................................... 47

Figure 21: WTE’s engaged in Water and Waste Water Services ............................................................................................... 51

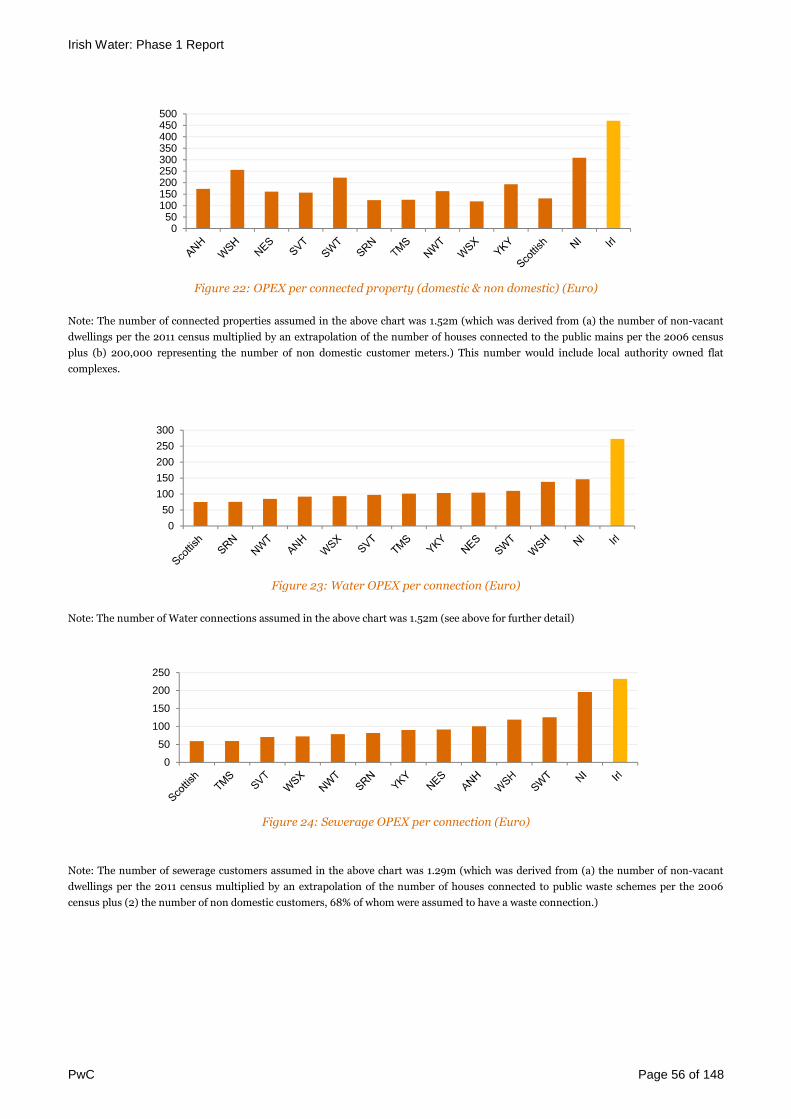

Figure 22: OPEX per connected property (domestic & non domestic) (Euro)..........................................................................56

Figure 23: Water OPEX per connection (Euro) ..........................................................................................................................56

Figure 24: Sewerage OPEX per connection (Euro) ....................................................................................................................56

Figure 25: Commercial Collection Rates in Irl (2010)................................................................................................................ 57

Figure 26: Collection Rates........................................................................................................................................................... 57

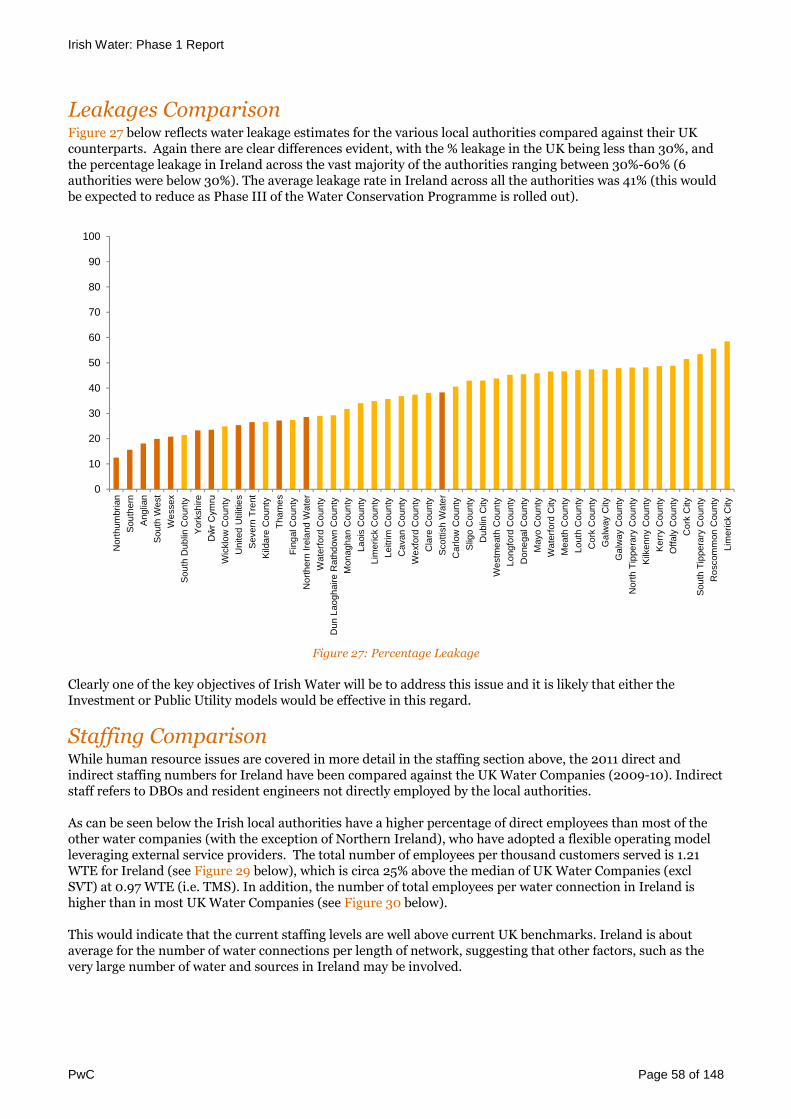

Figure 27: Percentage Leakage....................................................................................................................................................58

Figure 28: Number of Direct & Indirect Staff (exc. SVT) ...........................................................................................................59

Figure 29: Total Employees per thousand customers served (exc. SVT) ..................................................................................59

Figure 30: Total number of direct and indirect employees per thousand water connections (domestic plus non- domestic)

(exc. SVT) .......................................................................................................................................................................................59

Figure 31: km water pipe per thousand water connection.........................................................................................................60

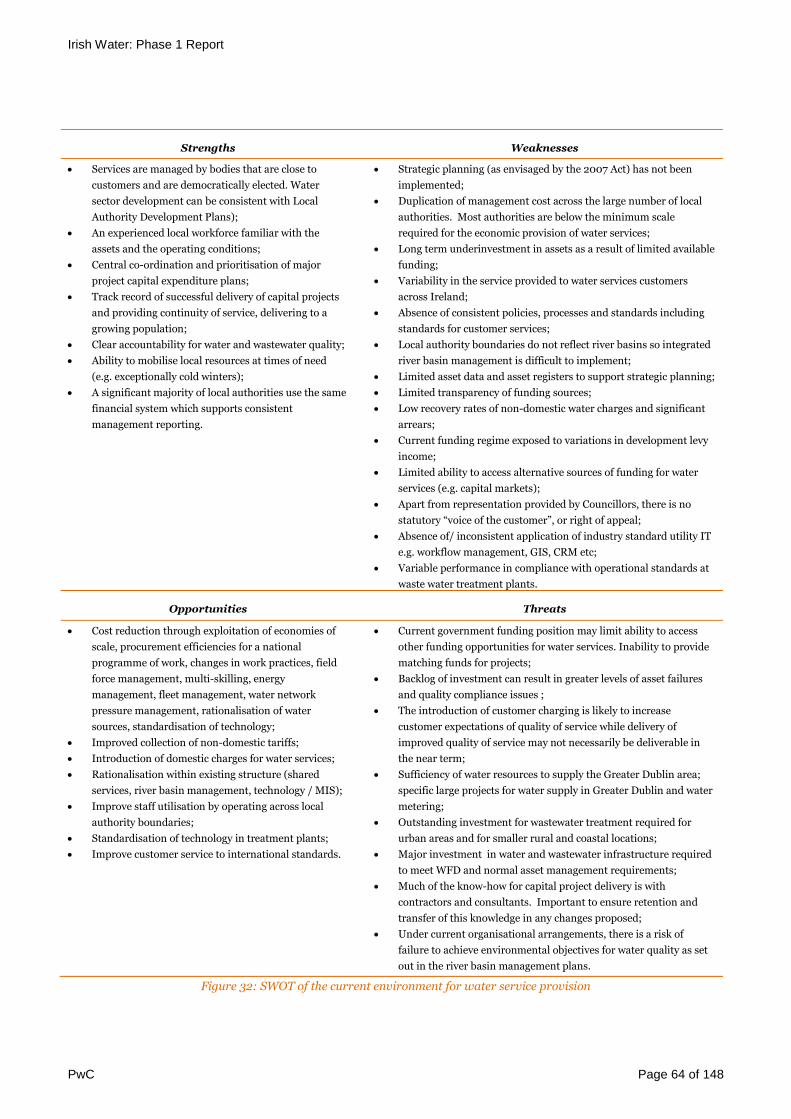

Figure 32: SWOT of the current environment for water service provision ..............................................................................64

Figure 33: Countries chosen as international comparators for Irish Water ............................................................................68

Figure 34: Water undertakings in England and Wales 1956 to 1970........................................................................................69

Figure 35: Trends in operating costs for the England and Wales water companies ................................................................71

Figure 36: England and Wales water companies, overall performance assessment .............................................................. 72

Figure 37: Agency and Public Utility Models ............................................................................................................................. 75

Figure 38: Agency Model.............................................................................................................................................................. 76

Figure 39: Public Utility Model .................................................................................................................................................... 79

Figure 40: Minimal Change Model..............................................................................................................................................82

Figure 41: Intercommunal Model ................................................................................................................................................84

Figure 42: Agency and Public Utility Models – Summary Comparison ...................................................................................88

Figure 43: Evaluation Criteria.....................................................................................................................................................92

Figure 44: Advantages of Public Utility and Agency Model ......................................................................................................95

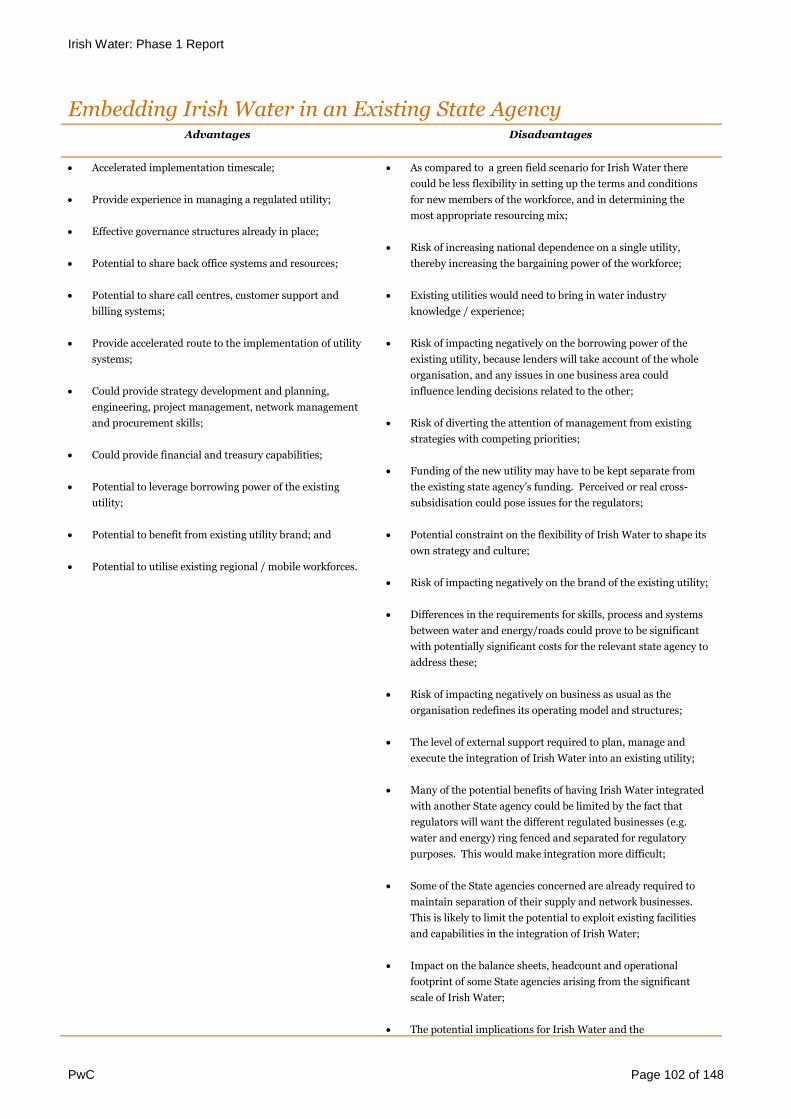

Figure 45: Embedding Irish Water in an Existing State Agency............................................................................................. 103

Figure 46: The Overall Structure for the Public Utility Model................................................................................................. 107

Figure 47: Water Services: Key Roles and Responsibilities ..................................................................................................... 109

Figure 48: Other bodies: key roles and responsibilities ........................................................................................................... 109

Figure 49: Regulation ..................................................................................................................................................................110

Figure 50: Typical Organisation Chart for a Water Utility...................................................................................................... 111

Figure 51: River Basins of Ireland .............................................................................................................................................112

Figure 52: Operations Services ...................................................................................................................................................113

Figure 53: Typical Asset Planning and Approval Process ........................................................................................................114

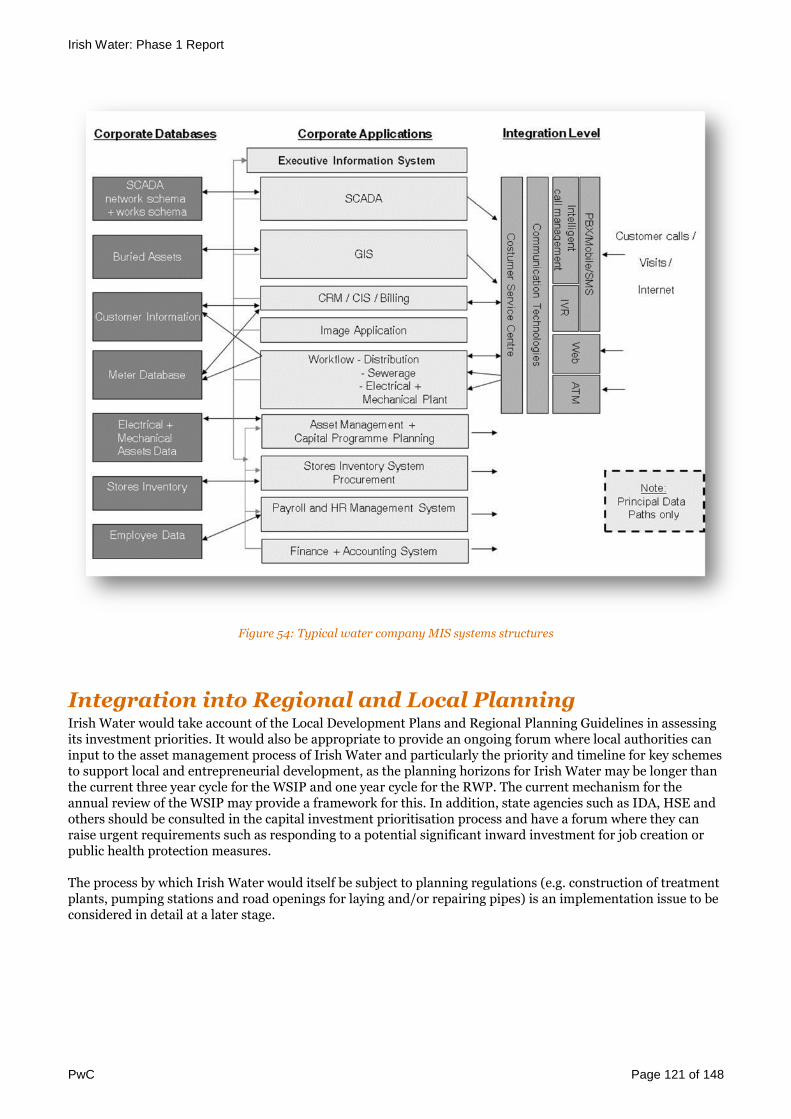

Figure 54: Typical water company MIS systems structures ....................................................................................................121

Figure 55: Funding Requirement per annum (Euro) ............................................................................................................... 125

Figure 56: Non Domestic Charges (2014 – 2030) adjusted for bad debts (Euro Excl. VAT)................................................. 126

Figure 57: Domestic Charges (2014 – 2030) including and excluding a free allowance (Euro Excl. VAT) ......................... 126

Irish Water: Phase 1 Report

PwC Page 8 of 148

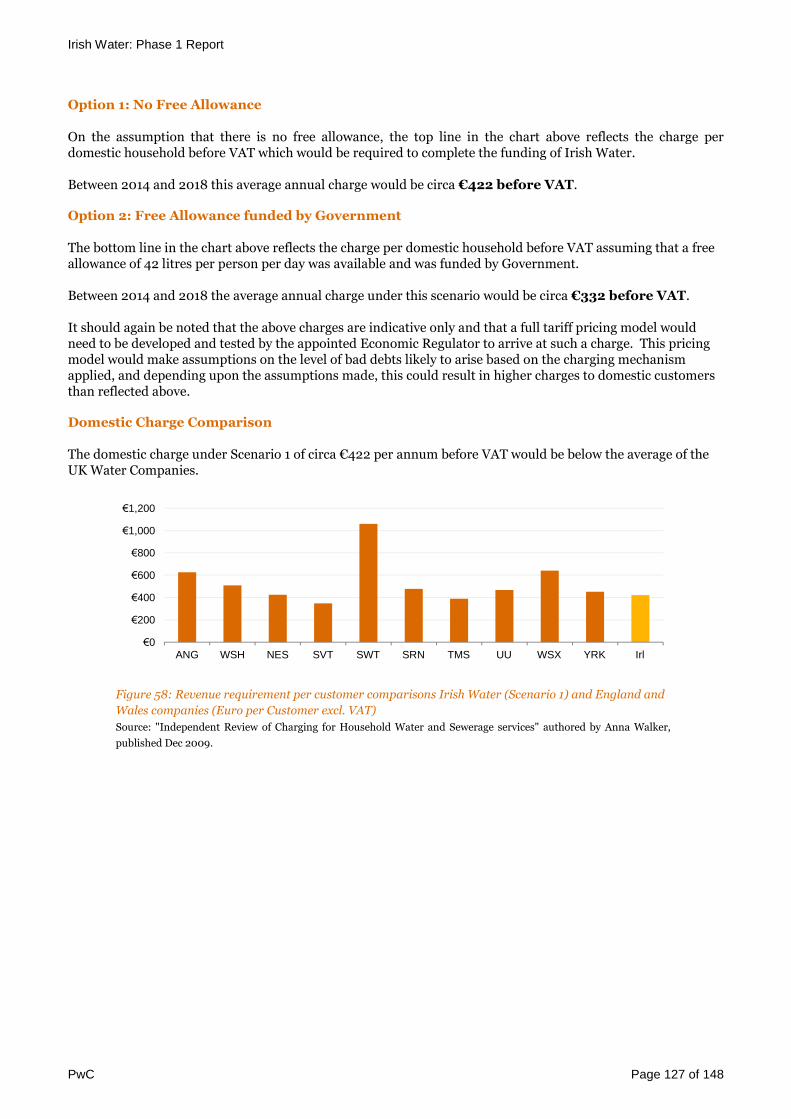

Figure 58: Revenue requirement per customer comparisons Irish Water (Scenario 1) and England and Wales companies

(Euro per Customer excl. VAT)....................................................................................................................................................127

Figure 59: Scenario 1: Sales as a % of Operating Costs (2014 – 2030)................................................................................... 129

Figure 60: Funding Requirement per annum (Euro)................................................................................................................131

Figure 61: Non Domestic Charges (2014 – 2030) adjusted for bad debts .............................................................................. 132

Figure 62: Domestic Charges (2014 – 2030) (Euro Excl. VAT) ............................................................................................... 132

Figure 63: Scenario 2: Sales as a % of Operating Costs (2014 – 2030) .................................................................................. 134

Figure 64: Funding Requirement per annum (Euro) ............................................................................................................... 135

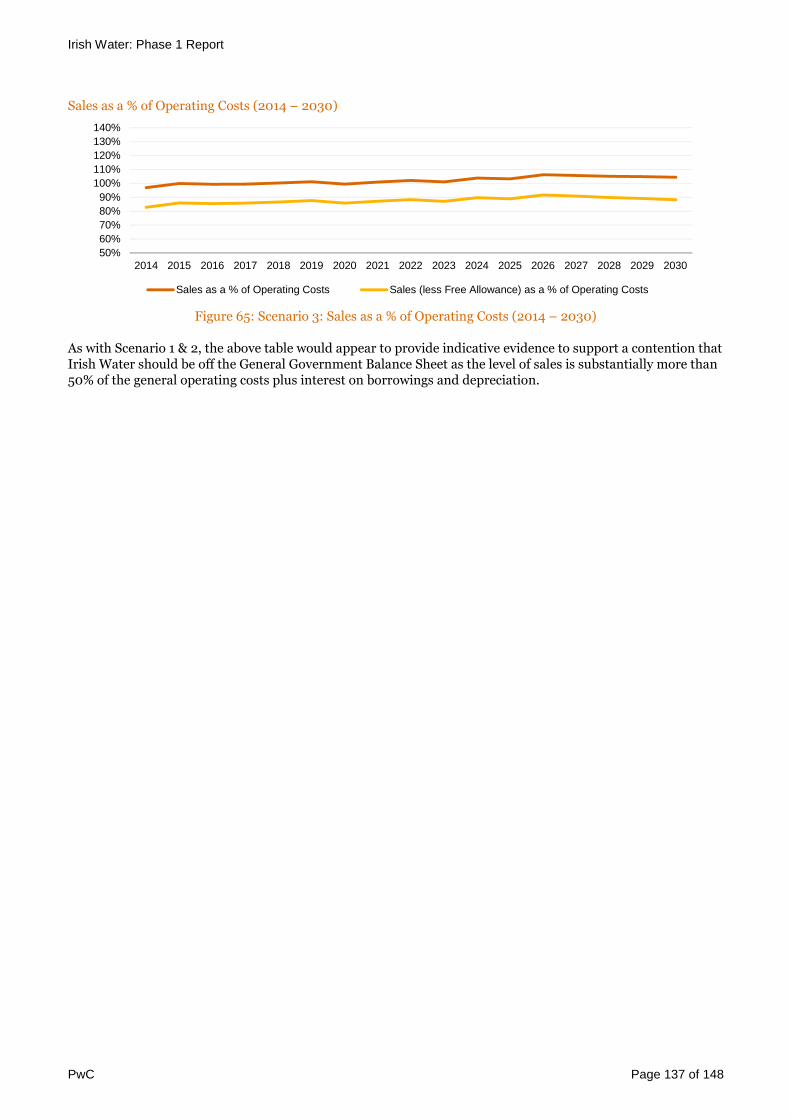

Figure 65: Scenario 3: Sales as a % of Operating Costs (2014 – 2030) ...................................................................................137

Figure 66: Phased Approach ...................................................................................................................................................... 139

Figure 67: Implementation Plan ................................................................................................................................................ 143

Irish Water: Phase 1 Report

PwC Page 9 of 148

1. Executive Summary

Irish Water: Phase 1 Report

PwC Page 10 of 148

1. Executive Summary

BackgroundThe delivery of high quality water and waste water services and the need to meet ever-increasing demands forwater, while ensuring security of supply and responsiveness to the needs of commercial and domesticconsumers, poses a significant challenge to the State.

Water and wastewater services cost approximately €1.2bn per annum, of which around €1bn is funded by theGovernment, with other sources, including non-domestic water charges, contributing just over €200m.

There has been a substantial and historic under-investment in water and wastewater services in Ireland andwhile there has been significant investment in the last decade, a recent review carried out by Department ofEnvironment, Community and Local Government (“DECLG”) indicates that there is still a substantial backlogof capital investment. With an ageing and poor quality infrastructure in some areas, substantial investmentwill be required to bring the standard of the water network up to the needs of a modern economy.

The Water Framework Directive (WFD) is a key initiative aimed at improving water quality throughout the EU.It applies to rivers, lakes, groundwater, and coastal waters. The Directive requires an integrated approach tomanaging water quality on a river basin basis; with the aim of maintaining and improving water quality. Fullcompliance with the Water Framework Directive has not been costed but is likely to run to several billion euroover the period to 2027.

Given the wider economic context in which Ireland finds itself, sourcing funds to meet all of these requirementswill be a difficult challenge.

It is against this background that this study has been commissioned.

Purpose of the StudyCurrently, 34 city and county councils are responsible for the production, distribution and monitoring ofdrinking water and for the provision of public waste water services in the Republic of Ireland. In the context ofrecent Government announcements concerning the creation of Irish Water, PwC was selected by the DECLG to:

a) Undertake an independent assessment of the transfer of responsibility for water services provision from thelocal authorities to a water utility;

b) Recommend the most effective assignment of functions and structural arrangements for delivering highquality competitively priced water services to customers (domestic and non-domestic) and forinfrastructure provision.

In particular the study was required to examine two principal forms of potential company structure (or variantsof those forms) for Irish Water:

A water company which would be a self funding water utility in a regulated environment, responsible foroperation, maintenance and investment in all water services infrastructure, customer billing, charging(the Public Utility Model); and

A company charged mainly with investment in the sector (strategic planning, delivery of projects of aregional/national priority, national metering programme) with local authorities operating as agents ofthe company, retaining their operational responsibilities and for delivery of smaller scale investment (theAgency Model).

A privatised water utility is outside the scope for consideration.

Irish Water: Phase 1 Report

PwC Page 11 of 148

This report is the outcome of Part I of the study which was concerned with recommending the optimalorganisational form for water services delivery in Ireland. Part II will focus on the detailed implementationissues involved in the creation of a new company in line with the recommendations made in Part I, subject totheir being accepted.

ApproachThe approach to conducting Part I of the study has been to:

1. Assess the strengths and weaknesses of the current model for provision of waterservices in Ireland to identify the challenges that would need to be addressed by a new modelfor water service delivery, without losing the positive aspects of the current model;

2. Review the Models for Water Service Provision Internationally to identify trends andlessons to be learned for water sector reform in Ireland;

3. Take Soundings from Stakeholders in the sector regarding the changes they feel would bestdeliver improved services for Ireland and the implementation challenges for any new model;

4. Identify potential operating models for Irish Water and Evaluate those Models against a setof Evaluation Criteria based on Policy Requirements for water reform in Ireland;

5. Describe the Recommended Operating Model and its financial, legal, organisational,staffing, environmental and other implications; and

6. Develop a High Level Transition Strategy designed to minimise the delay in achieving thebenefits while managing the implementation risks of the recommended operating model.

Strengths and Weaknesses of the Current ModelA SWOT analysis was developed for the current provision of water services in Ireland. The key conclusionswere that:-

The current model for water service provision has been operating under significant constraints. Ourstudy indicates that low levels of funding and an inability to access alternative sources of funding in thepast have resulted in a backlog of investment and maintenance in the water services infrastructure.Nevertheless, significant positive views of the current model came across very clearly in discussions withthe various stakeholders, in particular:-

o The value of having a local body accountable to the local community for the provision of waterservices;

o The operational effectiveness of the current locally based maintenance teams with water engineerswho “know their assets” and the associated asset maintenance regimes;

o The ability to draw on the wider resources of the local authorities in times of great need for waterservices, such as occurred during the cold weather events in the last two winters.

Efficiency levels do not compare well against international benchmarks. Some of the key metricsinclude:-

o Operating expenditure per connection is more than twice the average of UK water companies;o The level of “Unaccounted for Water” (largely due to leakage) at 41% is very high against

international benchmarks (although this would be expected to reduce as Phase III of the WaterConservation Programme is rolled out);

o Staffing levels are higher than comparable UK water companies on an employee per populationserved basis;

o The collection level for non-domestic water charges which averages 52% in 2010 is particularlylow.

Irish Water: Phase 1 Report

PwC Page 12 of 148

Ireland is about average for the number of water connections per length of network, suggesting thatpopulation dispersal is not a major factor in the benchmarks mentioned above. Other factors, such as thevery large number of water and wastewater plants in Ireland may be involved. One way or another, thesecomparisons would indicate that there are significant opportunities to increase efficiency and reducecosts over time once Irish Water is established.

Income currently received by the local authorities from the provision of goods and services from thirdparties and from Local Government Funding, for operational expenditure in relation to the provision ofwater services is not sufficient to meet their needs. It was estimated that there was a funding gap of€451.2m in 2010 which was met from other sources of funds including the general purpose grantreceived by the local authorities from DECLG;

The dependence on the Exchequer for Capital funding has in the past constrained investment in thesector. While approximately €600m is provided annually in capital investment, it is estimated that thereis currently a backlog of approximately €500m for essential projects. This figure is derived from DECLGdata on schemes in local authority needs assessment not included in the Water Services InvestmentProgramme 2010-2012. According to the Department and other stakeholders, this still leaves asignificant compliance gap in relation to the provisions of the EU Water Framework Directive which mayrequire several hundred million euro of further capital investment annually in the years to 2027;

The study concluded that many of the issues identified above arise from a combination of factors including:-

Fragmented leadership and coordination with a range of stakeholders able to influence and controldirections; including the 34 local authorities, the DECLG, the EPA, the CCMA the NFGWS and others;

Difficulty in exploiting economies of scale, particularly as the water service is organised on the basis ofcounty boundaries;

Relative difficulty in implementing policies and projects of national importance; An ageing and poor quality network; and Historical underinvestment in the water service.

The structures required to deliver an efficient and effective water service in Ireland, operating under theconstraints of available funding are not in place. The fragmented nature of the current model result insignificant levels of duplication across the 34 local authorities with limited sharing of resource, cooperation onstrategic initiatives or coordinated operational planning in place. The introduction of customer charges willcreate the need for increased levels of regulatory management, which under the current model will result infurther duplication of support structures.

Overall, it is our assessment that the current local authority based service provision model is highly unlikely toachieve the efficiencies and quality of service that have been achieved internationally in the water sectorthrough amalgamations. The local authorities have investigated opportunities for co-ordinated action.However the likely efficiencies suggested are small compared with the nearly 40% reduction in operating costsseen in Scotland post amalgamation. Fragmented local authority-based provision will perpetuate themanagement of sub scale water providers, inability to secure large scale procurement efficiencies and the abilityto deliver efficiency through planning field work over a larger customer base/geographical area.

A self-funding water service will require significant levels of external funding. Optimal external funding isbased on the ‘investment grade’ of individual companies, which is driven by the size of the organisation, thefocus and experience of the management team, the stability and efficiency of back office and frontlineoperational execution and for regulated entities, the ability to comply efficiently and effectively with economicand environmental regulatory requirements. In addition, since the level of external funding available isnormally based on earnings, the extent to which operating costs are reduced through the rationalisation,consolidation and simplification of the delivery model increases the level of borrowings available to thecompany.

Consequently, the ability to optimise the level of external funding is best achieved by a single water company,with authority to centrally manage the delivery of water services in Ireland.

Irish Water: Phase 1 Report

PwC Page 13 of 148

International ExperienceWe have reviewed relevant models for water service provision in a number of countries, including Scotland,England, Wales, Northern Ireland, Germany, France, Netherlands, South Africa, Australia, and Bulgaria werereviewed.

Our review pointed to fragmentation in the provision of water services in particular in continental Europe.However, the fragmented nature of water service provision is being addressed in most countries either by theamalgamation of municipal water services, the creation of utilities or the use of intercommunal structures (seebelow). Creation of larger bodies for the provision of water services, often outside of municipal control, is a keytrend in the industry.

Our research demonstrated that most of the models identified are based on the Public Utility Model. Thereis little evidence of arrangements similar to the Agency Model being used in the water sector. Anotherapproach found to be in common use is the Intercommunal Model, where several municipalities jointly setup a company to which they delegate the provision of water services.

Our research identified very few examples of the combination of water services provision with otherinfrastructure provision (e.g. roads) or utility services (such as gas or electricity). Multi-utility companies whichwere created in the UK a number of years ago were broken up in recent years to allow management teams tofocus on specific activities e.g. water or electricity. The research indicates that investors have tended to valuethe focussed single utility model more highly than the multi-utility model.

Where single function utilities have been created, the evidence indicates that there has been good performancein terms of cost reduction and improvement to the quality of service provided to customers. Theseimprovements have been driven in part by regulation that has focussed on economic efficiency, environmentalpreservation and ensuring good outcomes for customers.

Stakeholder SoundingsPwC met with a wide range of stakeholders in the sector to obtain a cross section of views on the current waterservice and on potential future models for the water sector. These included representatives of local authoritycouncillors and management, professional bodies, representatives of employers and of the unions, regulators,semi-state utilities and relevant government departments and agencies (see Section 2). A number of theseorganisations also made formal submissions to the PwC team.

A number of key messages were consistent across the stakeholder groups consulted. These included:-

The need for increased efficiency and value for money in the sector; The desirability of moving to a River Basin structure for managing water services; The need for improved water quality and greater security of supply in the coming years; The importance of obtaining increased funding to meet the increasing demands of customers; The benefits of transferring responsibility for water services to a single state agency; and The need to retain the local skills, knowledge and responsiveness in any new model for the delivery of

water services;

All of the information and views provided by stakeholders were taken into account in the analysis conducted bythe PwC team.

Operating Models ConsideredIn line with the Terms of Reference, two primary models were considered – these were termed the PublicUtility Model and the Agency Model. In addition, two possible variant models were identified – these weretermed the Minimal Change Model and Intercommunal Model. The models are summarised below:-

The Public Utility Model: Under the Public Utility Model, Irish Water would be a Public Utility andwould become the water services authority and the single point of contact for all customers. It would be asingle integrated commercial Semi-state body corporate operating on a regional structure delivering all

Irish Water: Phase 1 Report

PwC Page 14 of 148

water services currently provided by the local authorities, and most of those currently provided by theDECLG (with the exception of policy and legislation). The regions would be structured around riverbasins rather than local authority boundaries. Irish Water would own the entire infrastructure for waterservices including all assets, liabilities, income and expenditure. All water service staff would beemployed by Irish Water. BGE and ESB represent similar examples of this model in Ireland.

In this scenario, local authorities would no longer have a function in the provision of water andwastewater services.

The Agency Model: Under the Agency Model, a new state agency, Irish Water would be allocated fullresponsibility by statute for the provision of water and wastewater services and would therefore becomethe Water Services Authority for the full country. Similar to the Public Utility Model, Irish Water wouldown the entire infrastructure for water services including all assets, liabilities, income and expenditure.Irish Water would also take over most of the responsibilities of the DECLG, and undertake large capitalprojects and projects of national importance (including metering and domestic charging).

In this scenario, local authorities (or groupings of local authorities) would be designated by statute asagents of Irish Water for operation and maintenance of the water services and for small capitalprojects in their regions. They would operate under the control of Irish Water on the basis of agencyarrangements under which they would be paid by Irish Water for services provided. Staff required foroperation and maintenance would continue to be employed by the local authorities.

The Minimal Change Model: The Minimal Change Model would envisage retaining the localauthorities as the Water Service Authorities. Irish Water would take over certain executive functions ofthe DECLG, including responsibility for large capital projects and projects of national importance. Inthis scenario, the operation and maintenance of the water service (and therefore the bulk of the existingpersonnel) would remain with the local authorities. Ownership of the assets would be retained by thelocal authorities, and they would continue to be financially responsible for the operation andmaintenance of water services in their respective regions. Improvements in efficiency would be achievedthrough local authorities cooperating to achieve economies of scale.

The Intercommunal Model: This approach, as outlined above, has been adopted in several parts ofEurope. In this scenario, local authorities would retain the basic obligation to provide water services butwould agglomerate to achieve economies of scale by setting up intercommunal companies to which theywould delegate responsibility for the operation and maintenance of water services. In Ireland, this wouldinvolve three or more separate water companies each serving a different region.

Evaluation MethodologyPwC deemed it appropriate to use a qualitative methodology for the comparative assessment of the alternativemodels, taking into account the relative merits of each option against a set of evaluation criteria developed by usand reviewed with the DECLG and the stakeholder group referenced above. The criteria took into account themain objectives of the water services reform programme, which were identified as:-

Creation of a financially sustainable water service: Improving Ireland’s water services infrastructure; Ensuring environmental standards are met; Delivering improved outcomes for customers; Ensuring strong governance with clear accountabilities; Supporting other aspects of water reform in Ireland; and Promoting efficiency in water services.

The evaluation was carried out with reference to international practice, and based on the available metrics andon the experience of the consultants. The views expressed by stakeholders were also taken into consideration.

Irish Water: Phase 1 Report

PwC Page 15 of 148

Operating Model Recommended for Irish WaterOur study recommends the Public Utility Model as the most appropriate operating model for the provision ofwater services in Ireland in the future. Under this model, Irish Water would be a Public Utility with fullresponsibility for the water cycle from abstraction to waste water treatment and sludge disposal.

The key factors leading to this conclusion are:-

The scope to design, build and implement a fit-for-purpose focussed utility which is subject to regulationand is proven to achieve greater efficiencies and economies of scale in the provision of water servicesthan any of the alternative models.

Irish Water will operate under one single coherent integrated organisation structure (as against 34separate organisations today), with clear lines of accountability, authority and responsibility and afocused and experienced management team to facilitate timely decision making and efficient andeffective consistent delivery;

The Public Utility model is the most attractive proposition to lenders and is understood by investors wholend to the water sector in other countries. Its capacity to borrow on the international markets would bea key factor in enabling the company become financially sustainable;

This model will also have the effect of reducing and ultimately eliminating the burden on the Exchequerto provide capital and current funding to the water sector, with consequent positive impact on the State’sGDP /Debt ratio;

Under the Public Utility Model, Public Service staff numbers would be reduced with the transfer of staffto a new commercial semi-state agency. Based on comparative benchmarks (see Section 3), it isenvisaged that the total number of employees required for Irish Water when fully operational (i.e. from2018) would be significantly lower than the approximately 4,300 involved in water services today. Thiswould result from designing a fit-for-purpose operating model, eliminating existing duplication ofactivity. consolidating work locations and creating centres of expertise, driving synergies throughnational/regional management of service delivery, leveraging technology to automate activity andremotely manage operations, rationalising roles and responsibilities of staff and leveraging the flexibilityof external expertise;

The Public Utility will also be the most effective model for delivery of national strategies and managingissues across local authority boundaries. This will make the organisation better able to respond tosecurity of supply issues as it will be able to plan water resources at a national level;

The Public Utility will be best positioned to introduce and manage nationwide customer charges andcustomer service provision from a single location; and

Irish Water as a Public Utility will be a single entity for the economic and environmental regulators toregulate, being of a similar scale to compare/benchmark against UK water companies to assess efficiencyand quality of service. The Public Utility Model will be best placed to more efficiently and effectivelymonitor, manage and report compliance with regulatory requirements.

Transferring responsibility for water services from the local authorities to a new model as described willfacilitate the achievement of critical mass, economies of scale and a simplified operating model, which are notpossible under the existing fragmented institutional framework. Other benefits of the approach recommendedinclude:-

Facilitating greater efficiency and effectiveness in asset management and capital programme executionand in managing the supply chain to optimise value for money. Effective strategic planning on a nationaland regional basis will be of particular importance for the water metering programme and for regionalwater resource planning;

Enabling more efficient use of water resources;

Irish Water: Phase 1 Report

PwC Page 16 of 148

Optimising the use of water and wastewater treatment facilities; Facilitating increased standardisation of technology, modern procurement methods and increased

purchasing power; Supporting the implementation of the Water Framework Directive and best international practice in river

basin management; Enabling more effective use of field operatives; Facilitating reduction in overheads through consolidation of head office functions; Reducing reliance on consultants, with increased in house core skills due to scale; Facilitating economies of scale in billing and collection; Introducing 21st century operating practices throughout the country, as well as integrated best-in-class

ICT and management information systems; and Presenting opportunities not otherwise available to staff dedicated to water services. Increased

specialisation will provide routes for career development and training as well as enhancing jobsatisfaction.

Irish Water will face challenges in achieving the benefits as set out above but there are recent examples ofsimilar successes following consolidation in Scotland and England. In the period from 1994 to 2001, operatingcosts for water services in England and Wales were reduced from c£3.15bn to c2.65bn representing a decreaseof 3% per annum. In Scotland, efficiencies of around 40% were achieved over the period from 2002 to 2006.

It is recognised that retention of the local touch which local authorities can offer today, including liaison withGroup Water Schemes, will be an important element of implementation as will be the ability to respond flexiblyin times of urgent need such as happened in recent cold snaps.

RegulationPwC have recommended that the Environmental Protection Agency would be the environmental and technicalregulator for Irish Water, and that it would also become the regulator for Group Water Schemes, a rolecurrently played by the local authorities.

It is recommended that the role of the Commission for Energy Regulation (CER) be expanded to include waterregulation, as this role would fit well with its existing responsibilities for regulating energy utilities. In this rolethe CER, in cooperation with the National Consumer Agency would be responsible for protecting the interestsof the consumer.

Potential Role for an Existing State AgencyIn the establishment of Irish Water, there is a clear opportunity to establish a new fit-for-purpose organisation,based on international best practice and structured to deliver an efficient and effective service to domestic andnon-domestic customers. The single Water Utility Model is recognised in capital markets as an investmentgrade structure, with funding packages tailored specifically for this purpose. Precedence points to theefficiencies that have been delivered in relation to the operating costs of standalone water utilities in the UK asoutlined above, and to the improvement in the quality of service provided to customers.

Alternatively, it may be possible to leverage the structure, expertise and governance of an existing State agency,and clearly there is some merit in considering this. This approach may provide some marginal acceleration ofthe implementation timescale, but would not in our view significantly shorten it, since the critical path will bedetermined by the preparation of essential legislation, the lengthy and complex implementation programme,and by the speed of the transfer of assets, staff and responsibilities from local authorities to the new utility.

Few examples of multi-utilities exist internationally on this scale. Experience indicates that multi-utilitymodels have not been successful due to the need to maintain management focus. In the cases of Welsh Waterand United Utilities (England), the water utility was initially integrated with the electricity utility but wassubsequently separated out into individual utilities due to difficulties in managing multi-utility companies andthe limited opportunity for operational synergies where water and electricity operations needed to be ring-fenced for regulatory purposes. They were broken up by investors and management to allow a focus on theprovision of a single service.

Irish Water: Phase 1 Report

PwC Page 17 of 148

Whilst our analysis has indicated that there would be a number of potential advantages in embedding IrishWater in an existing State agency (see page 102), in our view these are outweighed by the disadvantages, inparticular:

The potential impact on the borrowing power of both Irish Water and the existing State agency; The constraints on integration and sharing imposed by the requirement to ring-fence the water service

from other regulated businesses, and the requirement to maintain separation of the networks and supplybusinesses in some of the existing State agencies;

The need for a fully focused management team to drive through the establishment of Irish Water over thenext six years, managing the transition of activities from 34 local authorities to Irish Water,implementing water charges, and managing an evolving regulatory regime;

The potential implications for Irish Water and the ESOP/ESOT’s of existing Semi States on the transferin of water assets;

The uncertainty surrounding the future ownership of the state agencies concerned following recentGovernment considerations to sell some State assets; and

The international experience indicating the likelihood of failure to achieve significant synergies andefficiencies due mainly to the constraints imposed by the separation of the different regulated activities.

Consequently, on balance, PwC see no compelling reason to assign responsibility for water services provision toanother State agency. Based on the analysis conducted, PwC concluded that, unless the above issues could besatisfactorily addressed, Irish Water should be established as a separate company in its own right.

A number of State agencies could, however, be suitable candidates, either on their own or in partnership withthe private sector, to provide outsourced services to Irish Water. PwC has recommended that Irish Waterprocures a management partner through a competitive tendering process as soon as possible after January2012. The role of a management partner would be to support the:

Set up and management of the new organisation; National initiatives to be undertaken (e.g. billing, metering); and Design and management of the transition to a fully operational utility.

It is envisaged that a number of State agencies could be suitable candidates for this role, either on their own orin partnership with the private sector. However, PwC expect that public procurement considerations willdictate that the partner would have to be selected through a public tendering process open to the private sectoras well as the State agencies.

Financial AnalysisFor the Public Utility Model PwC undertook a high level assessment of what the financial position for thebusiness might be and in particular the likely funding requirements. A number of scenarios were run on thesenumbers, with varying assumptions in relation to Government subvention, the level of external funding and thecharges to be applied. The detailed workings behind each scenario are set out in Annex 1 to Section 8. Threeillustrative scenarios are described below:-

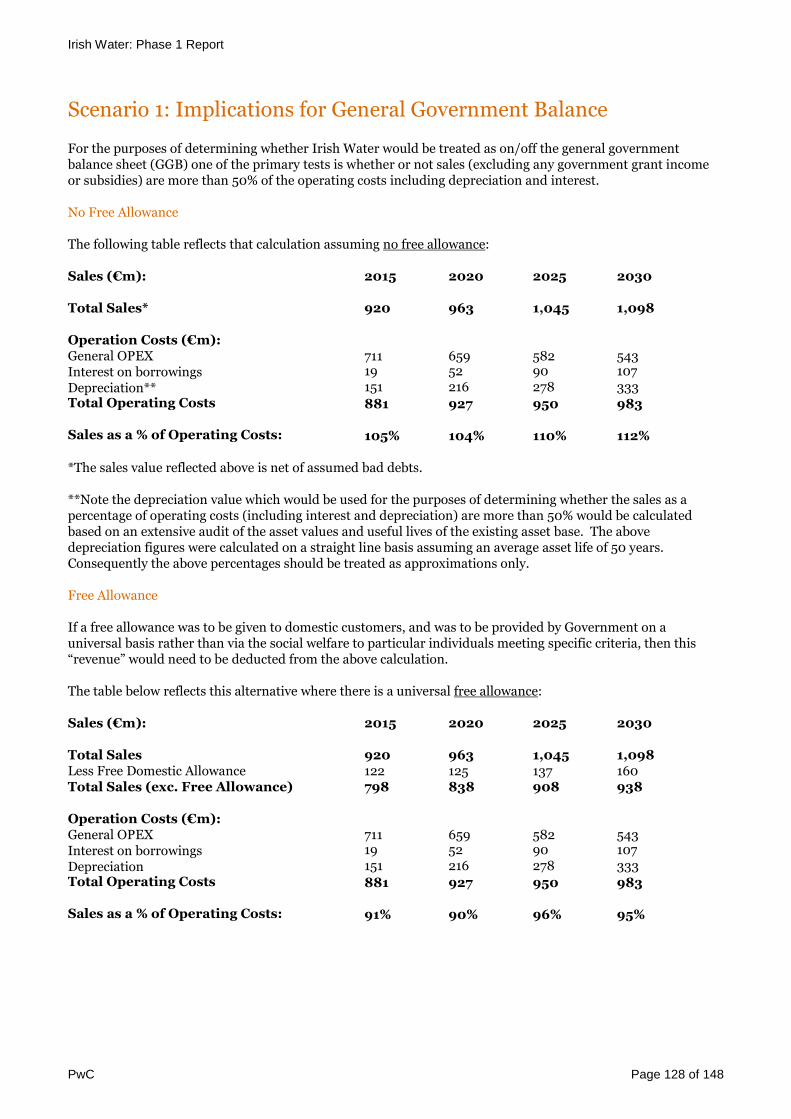

Scenario 1: This scenario is based on the assumption that Government funding will cease after 2022. Inthis situation, the net annual funding requirement from domestic and non-domestic customer charges(after taking into account bad debt assumptions) is c. €920m in 2015, increasing to c. €963m by 2020.Government funding of €2.1bn would be required for the period from 2015 to 2022;

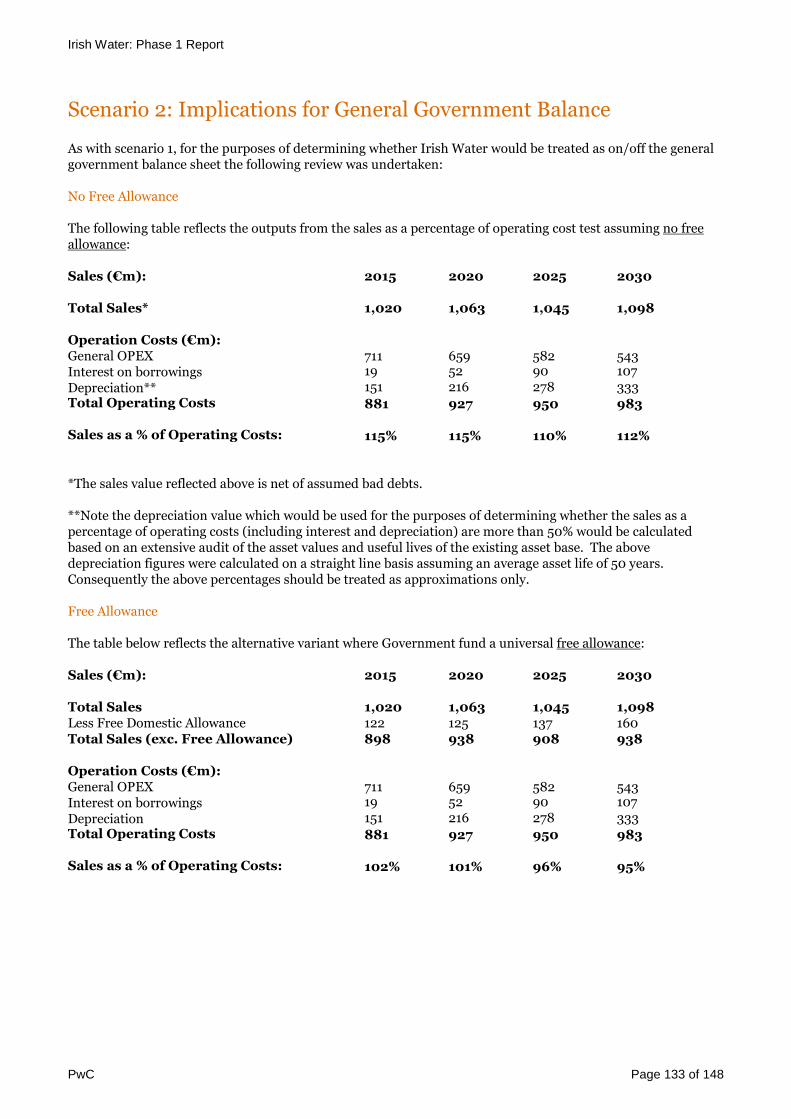

Scenario 2: This scenario is based on the assumption that Government funding will cease after 2018. Inthis situation, the net annual funding requirement from domestic and non-domestic customer charges(after bad debts) would be higher at c. €1,020m in 2015, increasing to c €1,063m by 2020. Governmentfunding would amount to €900m for the period.

Scenario 3: This scenario, assumes a fixed domestic charge in the mid-range of UK water companycharges for the period through to 2030. In this situation, the funding from domestic and non-domesticcustomers (after bad debts) is c. €880m in 2015, increasing to c. €923m by 2020. As domestic charges

Irish Water: Phase 1 Report

PwC Page 18 of 148

could not be flexed to offset changes in funding requirements or assumptions around bad debts in thisscenario, Government funding of c. €3.1bn would be required in the period through to 2030.

If a Free Allowance along the lines of that outlined in recent Government policy statements were to beintroduced, the cost of this Free Allowance in 2015 would be €122m, thus reducing total funding required fromdomestic and non-domestic customers by between 12% and 13%. This €122m would have to be funded byGovernment.

The financial analysis undertaken indicates that, in the scenarios explored, subject to certain assumptions, IrishWater could become a self-financing utility as early as 2018, depending on how quickly Government wishes tocease funding and on the level of water charges imposed. Our analysis indicated that in the scenarios explored,Irish Water could achieve a borrowing capacity of up to €2.9bn by 2030.

A key factor in evaluating the merits of the new operating model is the possibility that the borrowings of IrishWater could be outside the General Government Balance (GGB). We conducted an analysis on each of thescenarios outlined above and, subject to confirmation by the CSO / Eurostat, it would appear that adetermination could be made that Irish Water’s borrowings would be deemed to be outside the GGB.

TransitionA phased transition strategy has been proposed which would commence on 1st January 2012 and see completionof the transfer of responsibilities for water service from the local authorities to Irish Water by the end of 2017.The phased approach is recommended over a ‘Big Bang’ approach, as it allows Irish Water design, build andimplement a ‘fit for purpose’ organisation structure to deliver water services without the constraints of theexisting local authority model. It also allows Irish Water control the development of water services during thetransition period through agency arrangements with the local authorities. Consequently, it is most likely todeliver efficiencies earlier, reduce the risk of failure and maintain security of supply throughout the transitionperiod. This is illustrated in Figure 1 below.

Figure 1: Phased Transition Strategy

It is envisaged that passing the required legislation will take up to 18 months, during which time interimarrangements will need to be put in place within the DECLG to design and implement the new organisationalstructures, and the Irish Water CEO and Senior Executive Team will be selected. From that point (July 2013),local authorities would be appointed as agents of Irish Water with responsibility for operational andmaintenance services for a period of up to 5 years. This transition period would allow Irish Water to build itsown capabilities and determine the most appropriate resourcing mix of permanent staff, contract staff andvarious types of outsourcing arrangements.

Commencing in January 2015, Irish Water would take over the water operations of the local authorities on aphased basis. The pace of transition of operations, and the unwinding of interim agency arrangements, wouldbe determined by Irish Water management, in consultation with the DECLG and local authority management.It is envisaged that this transition would be completed by the end of 2017 at the latest.

This phased approach to transition would allow Irish Water to set up and develop organically as a new utilitywith its own culture, structure and resourcing, taking on board the resources and skills it requires from the local

Irish Water: Phase 1 Report

PwC Page 19 of 148

authorities in a planned and manageable way while ensuring the retention of valuable local knowledge. It isdesigned to minimise the delay in achieving the benefits while effectively managing the implementation risks.

To ensure a smooth and speedy transition, it is recommended that a Management Partner for Irish Watershould be procured through a competitive tendering process. The partner could be in place by January 2013.The partner organisation should be experienced in managing utilities and in particular within the waterindustry. It is anticipated that the partner would provide an interim management team, comprising primarilysecond line management resources to support the Irish Water Executive Team in managing Irish Water for aperiod of up to 5 years from January 2013.

Next StepsOn approval of the recommended operating model and transition strategy for Irish Water, Part II of the studywill focus on the detailed implementation issues involved in the creation of a new company, and on the issuesthat would arise from the consolidation of water services provision from the local authorities to Irish Water.

To achieve the timescales outlined above, it would be important to commence the detailed planning andpreparation as soon as possible but no later than the first quarter of 2012. It is recommended that aProgramme Management Office would be set up within the DECLG to manage and coordinate this process assoon as is practicable.

Irish Water: Phase 1 Report

PwC Page 20 of 148

2.Introduction andOverview

Irish Water: Phase 1 Report

PwC Page 21 of 148

2. Introduction and Overview

Background

Currently, 34 city and county councils are responsible for the production, distribution and monitoring ofdrinking water from over 900 public water supplies and for the provision of public waste water services.Investment by the 34 city and county councils in water services is guided by the River Basin ManagementPlanning process completed in 2010 and priorities are set out in the Department of Environment Communityand Local Government’s Water Services Investment Programme 2010 – 2012. The councils are also responsiblefor the supervision of any group and private water supplies in their areas and for the carrying out of variouswater-related inspection and enforcement activities. The Environmental Protection Agency continues to havestatutory responsibility for the supervision of the quality of water and waste water services.

The Programme of Financial Support for Ireland agreed between the Government and the EU/IMF requires,inter alia, that by the end of 2011, the Government will have undertaken an independent assessment of thetransfer of responsibility for water services provision from the local authorities to a water utility. In theProgramme for National Recovery, 2011-2016, the Government signalled its intention to create a new Statecompany to take over key water/waste water functions from the 34 existing local authorities. The programmeenvisages that:

“Irish Water will supervise and accelerate the planned investments needed to upgrade the State’sinefficient and leaking water network. The objective is to install water meters in every household inIreland and move to a charging system that is based on use above the free allowance. Thus, IrishWater would become a major State monopoly requiring separate independent regulation to promoteefficiency and competitiveness in the consumer interest and the general economic interest.”

The programme also contains commitments in relation to the NewERA plan under which streamlinedrestructured semi-States will make significant additional investments, over and above current plans, over thenext four years in “next generation” infrastructures including water. These investments – and theaccompanying semi-state restructuring process – will be financed and pro-actively managed by a New Economyand Recovery Authority (New ERA), which will absorb the National Pension Reserve Commission.

Against the backdrop of the EU/IMF agreement and the Government decision to establish Irish Water, PwCwas commissioned to carry out an independent assessment of the transfer of responsibility for water servicesprovision from the local authorities to a water utility.

This is an Interim Report on the assessment carried out. The purpose of this report is to provide a broadindication of the role and functions that Irish Water should have and the rationale for assigning these functionsto the company.

The Final Report will outline additional detailed information regarding implementation and transitionalarrangement issues.

Objectives and Scope of the StudyThe objectives of the study, as outlined in the Terms of Reference from the Department of the Environment,Community and Local Government are as follows:

a) To undertake an independent assessment of the transfer of responsibility for water services provision fromthe local authorities to a water utility

b) To recommend the most effective assignment of functions and structural arrangements for delivering highquality competitively priced water services to customers (domestic and non-domestic) and forinfrastructure provision.

Irish Water: Phase 1 Report

PwC Page 22 of 148

The scope of the study includes water and waste water. It is required to address the legal framework andfinancial and economic dimensions as well as organisational issues, having regard to international experienceand relevant examples of best practice.

The study is required to examine two principal forms of potential company structure for Irish Water:

A water company which would be a self funding water utility in a regulated environment, responsible foroperation, maintenance and investment in all water services infrastructure, customer billing, charging;and

A company charged mainly with investment in the sector (strategic planning, delivery of projects of aregional/national priority, national metering programme) with local authorities operating as agents ofthe company, retaining their operational responsibilities and for the delivery of smaller scale investment.

The terms of reference require that the study contrast these organisational forms, or variants thereof, withcurrent arrangements across a number of parameters e.g. governance, value for money, financial viability,statutory compliance, efficiency, level of service, cost to consumers, infrastructure investment, leakage rates etc.The study is also to consider the possibility/desirability of assigning responsibility for water services provision,or part thereof, to an existing state agency.

A copy of the Terms of Reference for the project is contained in Appendix 1.

Policy ContextThe study has taken due account of Government policies in the area of water services. The key policies include:

Commitments in the Programme for Government in relation to the water sector in Ireland such as:-

o The establishment of a new State body Irish Water,o A fair and efficient funding model for charging for domestic water,o The installation of water meters in every household in Ireland, ando A move to a charging system that is based ‘on use above a free allowance’.

The Programme for Government also provides that Irish Water, a new State company, will take over thewater investment maintenance programmes of the 34 existing local authorities. It will supervise andaccelerate the planned investments needed to upgrade the State’s inefficient and leaking water networkwhich has proved so unreliable during the recent harsh weather conditions.

The report of the Local Government Efficiency Group which was published in July 2010 and which, inaddition to general recommendation on achieving greater costs and efficiencies in the Local Governmentsector, made a number of specific recommendations in relation to the water sector, including that anenhanced regional office approach be developed at river basin level for infrastructure delivery andimplementation of the River Basin Management Plans.

The National Development Plan, 2007-2013, ‘Transforming Ireland’, which sets down current nationalpriorities for investment in national physical infrastructure, including the Water Services InvestmentProgramme and the Rural Water Programme. A new National Development Plan is expected to bepublished shortly which will set out new national priorities for infrastructural development, includingwater.

The Programme of Financial Support for Ireland agreed between the Government and the EU/IMF inDecember 2010;

The report of the Review Group on State Assets and Liabilities; and

Other relevant policies on pay and staff numbers.

Appendix 2 contains a high level description of the relevant policies referred to above.

Irish Water: Phase 1 Report

PwC Page 23 of 148

Challenges Facing Water Provision in IrelandIn the period since the year 2000 there has been very substantial progress in a number of areas in the provisionof water and wastewater services in Ireland. Between 2000 and 2010, the Exchequer has invested almost€5.2bn in the Water Services Investment Programme and the Rural Water Programme. Approximately twothirds of this was to address a substantial compliance gap under the Urban Waste Water Treatment Directive.In the period 2000-2009 there has been an increase of 3.7 million population equivalent in secondarywastewater treatment capacity and of one million population equivalent in water treatment capacity.

In recent years the Rural Water Programme has invested approximately €100 million per annum to effectimprovements in the quality of water supplied in rural areas, particularly for Group Water Schemes in responseto a European Court of Justice judgement in 2002. As a result, many of the Group Water Schemes have seensubstantial improvements in water quality and a professionalization of the management of those schemesthrough the introduction of Design, Build, Operate contracts, sometimes on a bundled basis.