Investor's Guide to the New Zealand Beverages Industry 2017 · THE INVESTOR’S GUIDE TO THE NEW...

98

THE INVESTOR’S GUIDE TO THE NEW ZEALAND BEVERAGES INDUSTRY 2017 Part of the New Zealand Food & Beverage Information Project FINAL REPORT; v1.02; June 2017

Transcript of Investor's Guide to the New Zealand Beverages Industry 2017 · THE INVESTOR’S GUIDE TO THE NEW...

THE INVESTOR’S GUIDE TO THE NEW ZEALAND BEVERAGES INDUSTRY 2017 Part of the New Zealand Food & Beverage Information Project

FINAL REPORT; v1.02; June 2017

STEERING & GUIDANCE

This project would not have been possible without the strong guidance of ourSteering Committee. In particular, we would like to thank Andrew McCallumof MBIE for his tireless energy in keeping this project on track, while at thesame time pushing us forward.

Draft versions of parts of this document were distributed to key firms forcomment, addition or correction. This was done in the form of emails andphone calls. We thank those who helped us in this process for their time andeffort. We also thank those who provided their photos.

We are grateful for all of the input we have received, but the report is oursand any errors are our own.

Finally, we acknowledge the support of the Ministry of Business, Innovationand Employment (MBIE), New Zealand Trade and Enterprise (NZTE) and theMinistry of Primary Industries (MPI). It is their funding that has made thisreport possible.

CONSTRAINTS & INHERENT LIMITATIONS

This work was commissioned by the Ministry of Business, Innovation andEmployment (MBIE) and prepared by Coriolis. This work is based onsecondary market research, analysis of information available or provided toCoriolis by our client, and a range of interviews with industry participants andindustry experts. Coriolis have not independently verified this informationand make no representation or warranty, express or implied, that suchinformation is accurate or complete.

The report is dated June 2017 and Coriolis accepts no liability for, and has notundertaken work in respect of, any event subsequent to that date, which mayaffect the report.

Key global trade data analysed in all sections of the F&B Information projectare calculated and displayed in US$. This is done for a range of reasons:

- It is the currency most used in international trade- It allows for cross country comparisons (e.g. vs. Denmark)- It removes the impact of NZD exchange rate variability- It is more comprehensible to non-NZ audiences (e.g. foreign investors)- It is the currency in which the United Nations collects and tabulates

global trade data

Anyone should feel free to call the authors if any of the material cannot beunderstood or accessed. We always welcome opportunities to discuss ourresearch with our readers and users.

Projected market information, analyses and conclusions contained herein arebased (unless sourced otherwise) on the information described above and onCoriolis’ judgment, and should not be construed as definitive forecasts orguarantees of future performance or results. Neither Coriolis nor its officers,directors, shareholders, employees or agents accept any responsibility orliability with respect to this document.

Coriolis wishes to draw your attention to the following limitations of theCoriolis report “New Zealand Beverages Industry 2017“ (the Coriolis Report)including any accompanying presentation, appendices and commentary (theCoriolis Commentary):

a. Coriolis has not been asked to independently verify or audit theinformation or material provided to it by, or on behalf of the Client, or any ofthe parties involved in the project;

b. the information contained in the Coriolis Report and any CoriolisCommentary has been compiled from information and material supplied bythird party sources and publicly available information which may (in part) beinaccurate or incomplete;

c. Coriolis makes no representation, warranty or guarantee, whether expressor implied, as to the quality, accuracy, reliability, currency or completeness ofthe information provided in the Coriolis Report and any Coriolis Commentary,or that reasonable care has been taken in compiling or preparing them;

d. the analysis contained in the Coriolis Report and any Coriolis Commentaryare subject to the key assumptions, further qualifications and limitationsincluded in the Coriolis Report and Coriolis Commentary, and are subject tosignificant uncertainties and contingencies, some of which, if not all, areoutside the control of Coriolis; and

e. any Coriolis Commentary accompanying the Coriolis Report is an integralpart of interpreting the Coriolis Report. Consideration of the Coriolis Reportwill be incomplete if it is reviewed in the absence of the Coriolis Commentaryand Coriolis conclusions may be misinterpreted if the Coriolis Report isreviewed in absence of the Coriolis Commentary.

Coriolis is not responsible or liable in any way for any loss or damageincurred by any person or entity relying on the information in, and theRecipient unconditionally and irrevocably releases Coriolis from liability forloss or damage of any kind whatsoever arising from, the Coriolis Report orCoriolis Commentary including without limitation judgments, opinions,hypothesis, views, forecasts or any other outputs therein and anyinterpretation, opinion or conclusion that the Recipient may form as a resultof examining the Coriolis Report or Coriolis Commentary.

The Coriolis Report and any Coriolis Commentary may not be relied upon bythe Recipient, and any use of, or reliance on that material is entirely at theirown risk. Coriolis shall have no liability for any loss or damage arising out ofany such use.

Unless otherwise noted, all photos used in this discussion document wereprovided by the New Zealand Story resource (www.nzstory.govt.nz),purchased by Coriolis from a range of stock photography providers (asdocumented where required), or are low resolution, complete product/brandfor illustrative purposes used under fair dealing/fair use for both “researchand study” and “review and criticism”. Our usage of them complies with NewZealand law or their various license agreements.

Cover image: Shutterstock (XiXinXing)

Where appropriate, this document is Copyright © 2017 Coriolis and MBIE.However, please feel welcome to use, refer to and cite this research.

Market Overview

Context & Conclusions

Production Categories Growth & Innovation

01 02 03 04INTRO

TABLE OF CONTENTS

Firms Performance

05

Pages 3-10 Pages 11-24 Pages 25-39 Pages 40-49 Pages 50-64 Pages 65+

+ Purpose

+ Situation summary

+ Drivers of success

+ Investment opportunities

+ SWOT

+ Supply chain

+ Global situation

+ Consumption

+ Import demand

+ Export supply

+ Key markets

+ Market growth

+ Wine

+ Beer

+ Juice

+ Alcoholic Spirits

+ Water

+ Production

+ Regional activity

+ Key inputs

+ Growth upside

+ Overview

+ Category Segmentation

+ Exports by product

+ Horizons for growth

+ Emerging export stars

+ Mega-trends driving change

+ Innovation & new products

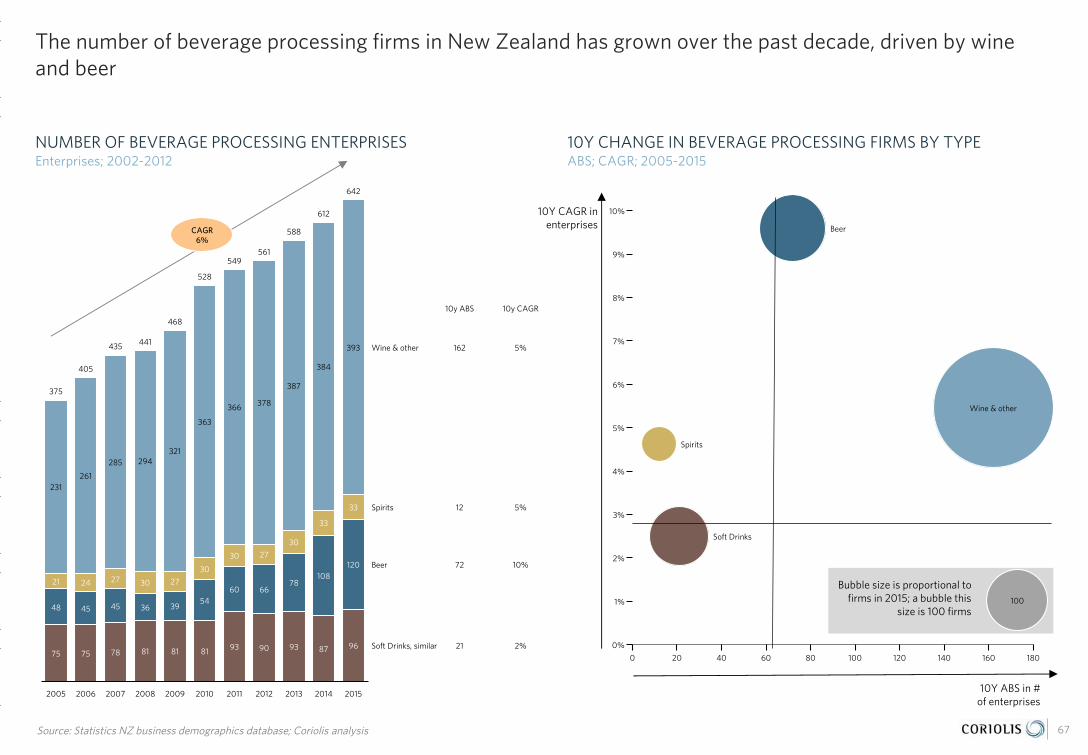

+ Enterprises

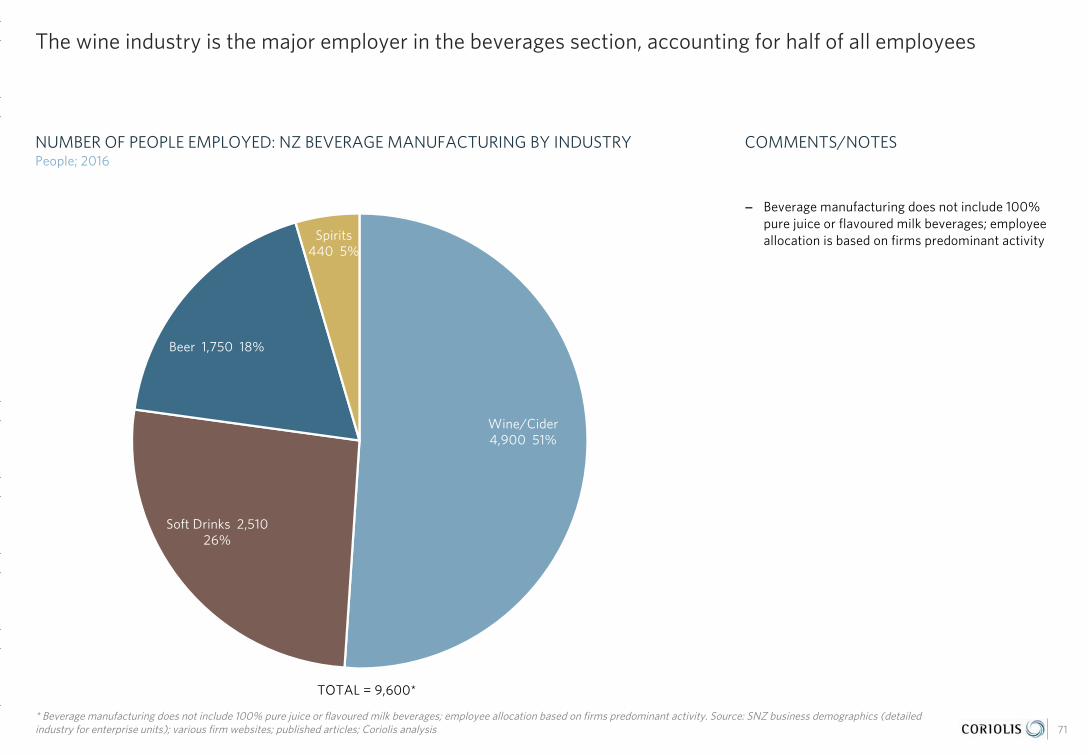

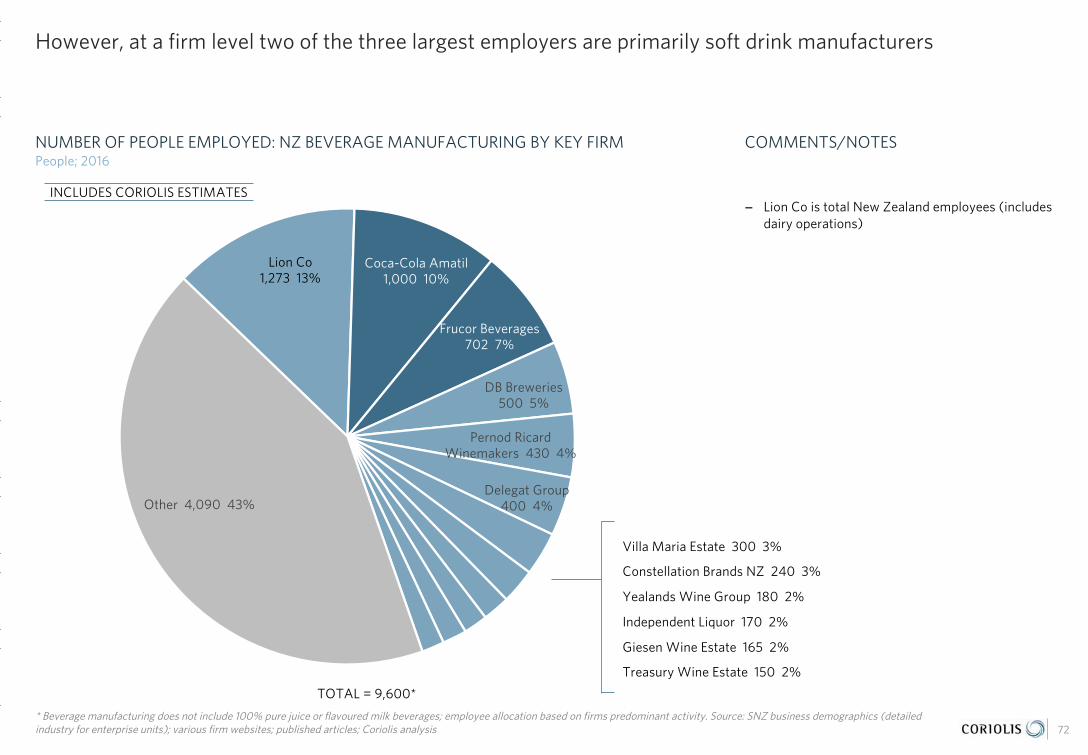

+ Employment

+ Turnover

+ Ownership

+ Foreign investors

+ Acquisitions

+ Investment

+ Rebranding

+ Leadership

+ Firm Profiles

PURPOSE Why did the New Zealand government undertake this project?

4

The project presents a comprehensive, business-focused overview of the total New Zealand food and beverage industry.

The project pulls together the available information on the food and beverage industry into one place, in a form which is familiar and useful to business. The reports contain analysis and interpretation of trends and opportunities to materially assist with business strategy and government policy.

The information will be of vital use to businesses, investors, government, and research institutions as the industry expands and diversifies. This industry view will be very useful to government, enabling better dialogue and the opportunity to address issues collectively.

– As support for raising capital

– As a base of market intelligence to enable business to be much more targeted in their own market research

– Reviewing and informing offshore market development (including export and investment) strategies

– Assisting in identifying areas of innovation and R&D for the future

– Identifying strategic partners and collaborators

– Enabling a company to benchmark performance with that of its competitors

– Monitoring industry activity

– Gaining a better understanding of their own industry sector

– Identifying internal capability needs or external inputs

While the government collects large amounts of industry data, little of this has an investor or industry-driven perspective.

This information will provide much greater insight into the industry, which is useful for a range of policy developments, from regulatory frameworks to investment in science and skills and facilitating access to international markets.

In particular, a single source of factual information will enable government agencies to better coordinate their efforts across the system and be more responsive to addressing industry issues.

All project resources are available online at:

www.foodandbeverage.govt.nz

What is the purpose of the project? What benefit will this bring to businesses? How will government use the reports?

SITUATION SUMMARY: WINE The New Zealand wine industry has shown rapid growth driven by Marlborough Sauvignon Blanc; some diversification into new varieties and new regions is occurring

5

NEW ZEALAND WINE

The New Zealand wine industry has achievedspectacular growth over the last 40 years, going fromNZ£51 in exports in 1960 to NZ$1.6b in 2016. TodayNew Zealand competes successfully with major wineproducers, both old world (e.g. France, Germany) andnew (e.g. Australia). New Zealand has achieved anoverall premium price position in–market on par withFrance (which has been producing wine for ~2,000years).

International success to date has been built almostexclusively on Marlborough Sauvignon Blanc whichhas become a “must-have” wine for major wineplayers. However good Marlborough wine area isnow almost all used. This may be a good thing asMarlborough now has almost as much area in grapesas Burgundy.

Emergent secondary regions are 20 years behindMarlborough in terms of development. Hawkes Bay,Waipara and Central Otago stand out as the next bestprospects. However, other than HawkesBay/Gimblett Gravels Syrah and Central Otago PinotNoir most regions have yet to find “their” wine andthe experience of Europe suggest this could takesome time.

Wine production is a fast growing industry for NewZealand, with a number of firms, ranging from verylarge to very small. Many large wineries are now

foreign owned and on-going acquisitions areoccurring. As a result foreign ownership now plays abig part in the wine industry, and these global firmswith their global sales resources and reach, provide apath-to-market for introducing global consumers toNew Zealand wines.

That being said, there is a substantial group ofsuccessful medium sized New Zealand ownedwineries that, in many ways, are the key force drivingindustry quality and innovation forward (e.g. lightwine development).

COMPETITORS

New Zealand wine competes directly with that fromother premium temperate climate countries,particularly France, Germany, cooler parts of the US(e.g. Oregon) and Chile.

CONSUMERS/MARKETS

Global oversupply has been ongoing, pushing downprices. These falling prices have impacted NewZealand wines.

At the same time wine consumption is declining inmany EU markets (France, Italy, Spain) for social,lifestyle and economic reasons. These twin forces,

falling consumption and falling prices, have in turntriggered a decrease in global wine area andproduction, particularly in the three largest wineproducers (France, Italy & Spain). On-going changesto EU subsidy systems have accelerated the process.

New Zealand’s success to date in wine has beenprimarily in the Anglo-Saxon four (USA, Canada, UK& AU). Luckily these markets have had stable-to-increasing consumption. However, it would be in theinterest of New Zealand producers to develop newmarkets to reduce this concentrated reliance on thesemarkets.

China is a rapidly emerging growth market for globalwine and is now the fourth largest wine importingcountry in the world by value. China is now NewZealand’s sixth wine export destination and growing.

Available in-market data suggests - at a high level -that the growth of New Zealand wine is at theexpense of French wines (i.e. the two are closesubstitutes for consumers).

Source: Coriolis; interviews

SITUATION SUMMARY: OTHER BEVERAGES Outside wine, the New Zealand beverage sector is primarily focused on production for domestic consumption; however, exports are growing strongly for many products

6

SPIRITS

Prior to 2000 there is a wide range of small spiritventures, producing small scale niche spirits for thedomestic market. At the same time IndependentLiquor launched RTD2 spirit beverages primarily fordomestic consumption and export to Australia.

Everything changed with the launch, rapid growth andfinancial success of 42 Below which created globalawareness of New Zealand as a super-premiumspirits provider. In the wake of 42 Below a largenumber of new firms have entered the industry with awide range of products and brands.

Independent Liquor, recently purchased by Asahi, isthe largest player in spirits. Independent initiallydeveloped its business around flavoured RTD drinks,however it is diversifying into other alcoholicbeverages. The two main brewers also produce andpack spirits, as well as distribute imported productsand brands.

There are a range of other smaller firms in spiritsachieving strong growth and the sector is wellpositioned for further growth (see related project2012 Spirits Opportunity report).

BEER

Globally, mainstream beer brewing has beendominated by large companies mainly leveraging

scale, point-of-purchase control and distributioneconomics. New Zealand’s three mainstreambrewers focused on domestic consumption are: DBBreweries (Heineken), Lion (Kirin) and Independent(Asahi).

This situation is changing rapidly with the emergenceof a burgeoning craft brewing scene. New Zealandnow has a range of smaller/micro breweries, risingwith the growth of craft beer. Leaders in this spaceinclude Moa Brewing, McCashin’s, Harrington’s andmany other smaller, innovative firms.

New Zealand is a currently a minor beer exporter1,and imports more beer than it exports. However, beerexports have surged in the last few years. Thecountry is known for its specialty hops and both usesthese domestically and exports them.

SOFT-DRINKS/FLAVOURED BEVERAGES

Non-alcoholic beverages are relatively consolidatedacross two international companies that primarilymanufacture for domestic consumption:

− Coca-Cola Amatil, Australian-listed Asia-Pacificlicensee of Coca-Cola;

− Frucor, former Apple & Pear Marketing Board juicebusiness, now a division of Suntory (Japan); makerof V energy drink and the Pepsi licensee in NewZealand.

Smaller innovators emerging outside core soft-drinks.Organic-producer Phoenix (Charlie’s/TBDC) ownedby Asahi.

A large range of premium adult beverages are gainingtraction across multiple channels.

JUICE

New Zealand exports apple and kiwifruit juice,primarily as a secondary product of the fresh fruitindustry. However New Zealand imports +20% morejuice than it exports and domestic fruit productioncost structures suggest a premium/niche strategy.

WATER

New Zealand has excellent theoretical potential toproduce and export premium bottled water. Anumber of brands and companies have moved intothis premium space (e.g. One, Antipodes and Palaeo).However, to date, little of this potential has beenrealised.

1. RTD = ready-to-drink; 2. Mexico, for example, exports 80x as much beer as New Zealand; NZ currently exports about as much beer as the Dominican Republic

DRIVERS OF SUCCESS New Zealand’s success in beverages has three key drivers

Source: photo credit (NZStory and images under license from shutterstock.com) 7

- Temperate climate similar to Italy or France

- Temperature extremes moderated by surrounding ocean

- Isolated location protected by natural barriers

Low production cost

IDEAL CLIMATE & SOILS EFFICIENT PEOPLE & SYSTEMS LOCATION & MARKETS

Trusted byconsumers

High share in key products

- Innovative New World wine producer that burst onto the global wine scene in the 1980’s

- Industry highly focused on export success

- Large pool of skilled people

- Strong systems and support networks

- Well-organised, cohesive industry

- Excellent proximity to East & South-East Asian markets

- CER agreement with Australia

- NZ was the first developed country to sign a free trade deal with China (2008)

INVESTMENT OPPORTUNITIES Beverages are a major opportunity for investors; wine has shown rapid growth; opportunities exist in second tier wine regions, cider, premium spirits and other beverages

8

WINE

New Zealand Sauvignon Blanc wine is now a “must-have” component of the portfolio for major globalwine companies. Three of the top five US winecompanies and three of the largest European alcoholicbeverage companies are active in New Zealand. Inaddition, three of the top five Australian winecompanies are in New Zealand.

There are some opportunities for further investmentin Marlborough. However, geographical constraintsplace limitations on further growth in Marlborough.

Large wine firms are either foreign owned by globalmajors or committed NZ family owners (i.e. Delegatand Villa Maria both have committed owners).Opportunities exist for new investment in next tierdown of firms (e.g. Giesen, Allan Scott, etc.).However these firms are looking for smart investmentwhich gives them access to a global salesforce and aroute to market.

Investors with transferrable skills or those looking tounlock hidden value should investigate emergentsecondary regions (i.e. “the next Marlborough”).

SPIRITS

New Zealand has clear potential in premium alcoholicbeverages, building, in part, on New Zealand

positioning in premium wine. Peer group countries(e.g. UK, Sweden) suggest strong future growthpossible. However, there are limited entry vehicles.At this point in the life cycle, opportunities exist forstart-ups into the space. Greenfields entry by globalplayer with a strong transferrable skill set also suits.

CIDER

New Zealand is a major apple producer and exporter.Recently the cider industry in New Zealand hasexperienced strong growth, both for domesticconsumption and export. Exports have shown stronggrowth over the past decade, primarily to Australia.While there are a large number of producers, mostexport volume is produced by the two main brewers(Heineken/DB & Kirin/Lion).

BEER

New Zealand produces hops and barley and has~150+ years of beer brewing experience. After a longperiod of flat exports, beer exports have recentlystarted growing. However to date limited demand forNew Zealand beer has been developed in marketsbeyond Australia. Microbreweries are small andgrowing, but most currently have a domestic focus.However, Moa Breweries has listed on the NZX and ismaking an export push.

Future export success by New Zealand beer will

require a unique or more differentiated product (aswas the case with wine).

SOFT DRINKS

In soft drinks, while both Frucor/V andTBDC/Charlie’s/Phoenix are attractive, but both arenow Japanese owned. A range of smaller firms exist.

WATER

There are potential opportunities in exporting bottledwater. However, at this late point in the global life-cycle, meaningful success will require global bestpractice marketing (cf. Lynda Rae Resnick/FijiWater). Best fit would be for investor withtransferrable capability.

SWOT ANALYSIS The New Zealand beverage industry is well positioned for further growth, but pressures will continue

STRENGTHS WEAKNESSES

- Islands in the middle of the South Pacific that have the area of Italy, but with only the population of Singapore; therefore relatively unspoilt

- Strong and growing success in premium/super-premium wine

- Achieves a strong price premium for wine in key markets (similar to France)

- New Zealand Sauvignon Blanc now a “must have” for global wine companies

- Growth in market share in key markets (e.g. USA)

- Innovative and quality-focused producers (e.g. Chia+Kawa)

- Closer shipping distances to Asia compared to European competitors

- Demonstrated capabilities in beverage production

- On-going growth and success of Frucor/V, and Charlies/Phoenix in non-alcoholic drinks category

- Emergent success in spirits (e.g. Stolen)

- Large number of small producers with limited economies of scale

- High debt levels of many small and medium sized producers

- Highly dependant on four countries (AU, UK, USA and Canada)

- Increasing exports of bulk wine

- Lack strong super-premium heritage brands as demanded by brand and status conscious Asian consumers

- No deep cultural unique “spirits” associated with New Zealand

- Long shipping distance to traditional western markets

- Unlike traditional sectors, no major ($1b+) New Zealand owned champion growing and driving New Zealand brand position in beer, wine or other beverages

- Limited culture of super-premium branding or positioning (e.g. relative to France)

- Not a major producer of many base ingredients of typical beverages (e.g. oranges)

OPPORTUNITIES ISSUES/THREATS/RISKS

- Continued income growth in Asian markets

- Rapidly growing demand for premium alcoholic beverages in Asia

- Low share in Europe (two thirds of global wine consumption) outside British Isles

- Joint in-market activity spreading cost of marketing

- Strong and growing demand in Asia for premium fortified wines/wine based spirits (e.g. cognac)

- Reduction of global “wine ocean” supporting higher prices

- Leverage success of New Zealand wine industry; build on awareness of New Zealand in wider premium beverages segments

- Wide range of New Zealand unique plants available as flavouring (e.g. 42 Below Manuka honey)

- Ongoing consolidation of the industry

- Difficult finding good distributors to gain access into key markets

- Continued growth of bulk wine trade reducing the value of wine

- Continued growth of retail brands/store brands in wine

- Limited opportunity shipping “water” around the world if it isn’t a premium product

- Changing consumer sentiment or government policy

- Failure to achieve large scale export traction outside wine

- Hollowing out of management skills in New Zealand industry due to foreign ownership (relative to Denmark or Holland for example)

9

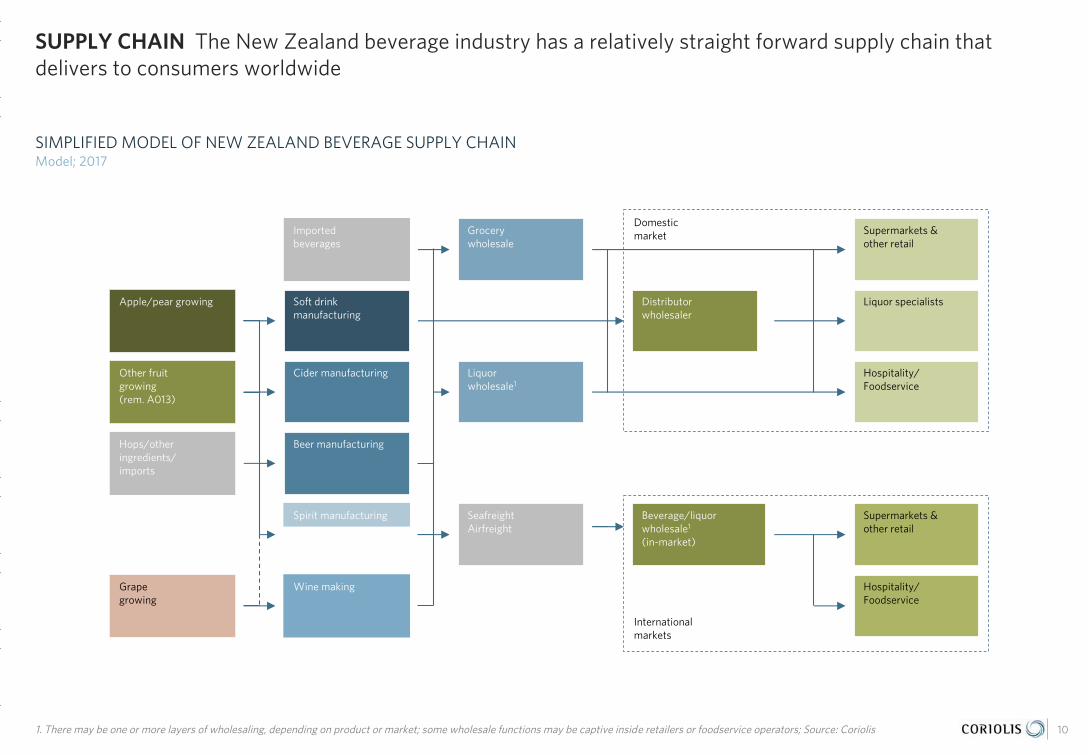

SUPPLY CHAIN The New Zealand beverage industry has a relatively straight forward supply chain that delivers to consumers worldwide

1. There may be one or more layers of wholesaling, depending on product or market; some wholesale functions may be captive inside retailers or foodservice operators; Source: Coriolis

SIMPLIFIED MODEL OF NEW ZEALAND BEVERAGE SUPPLY CHAINModel; 2017

10

Soft drink manufacturing

Liquor wholesale1

SeafreightAirfreight

Liquor specialists

Hospitality/ Foodservice

Beverage/liquorwholesale1

(in-market)

Supermarkets & other retail

Internationalmarkets

Domesticmarket

Distributorwholesaler

Other fruit growing(rem. A013)

Apple/pear growing

Grape growing

Wine making

Beer manufacturing

Hospitality/ Foodservice

Supermarkets & other retail

Spirit manufacturing

Hops/other ingredients/ imports

Grocerywholesale

Imported beverages

Cider manufacturing

Global Market Overview

+ Consumption

+ Global trade

+ Import demand

+ Export supply

+ Key markets

+ Market growth

01

New Zealand has a strong position in the growing global beverages trade

PRODUCTION

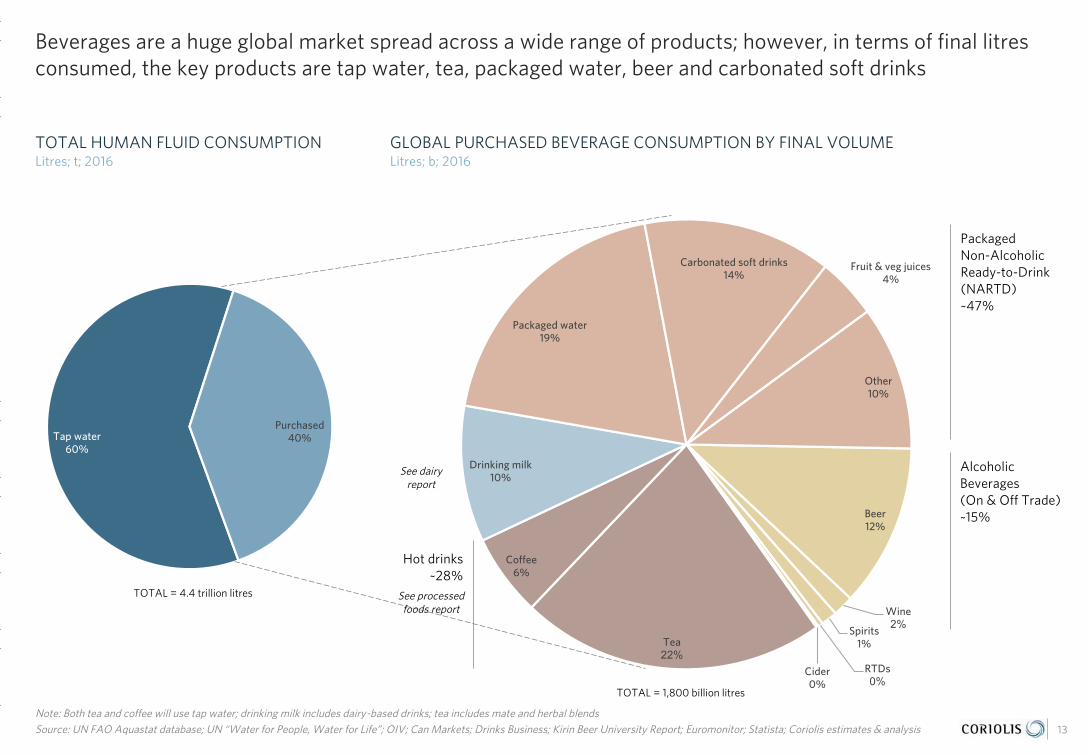

- Beverages are a huge global market spread across a wide range of products

- In terms of final litres consumed, the key products are tap water, tea, packaged water, beer and carbonated soft drinks

GLOBAL TRADE

- Global cross-border beverage trade volumes are growing (5.6% CAGR) with moderate price gains across the cycle leading to export value growth

DEMAND: PRODUCT CATEGORIES

- Total global cross-border beverage trade is spread across a wide range of products, though bottled wine ($22.7b), beer ($12.7b), Whiskeys ($10.9b) and wider soft drinks ($17.5) stand out for size

- “Other flavoured beverages,” gin, “other alcoholic spirits,” soft drinks, beer and mineral water stand out for global growth over the past five years

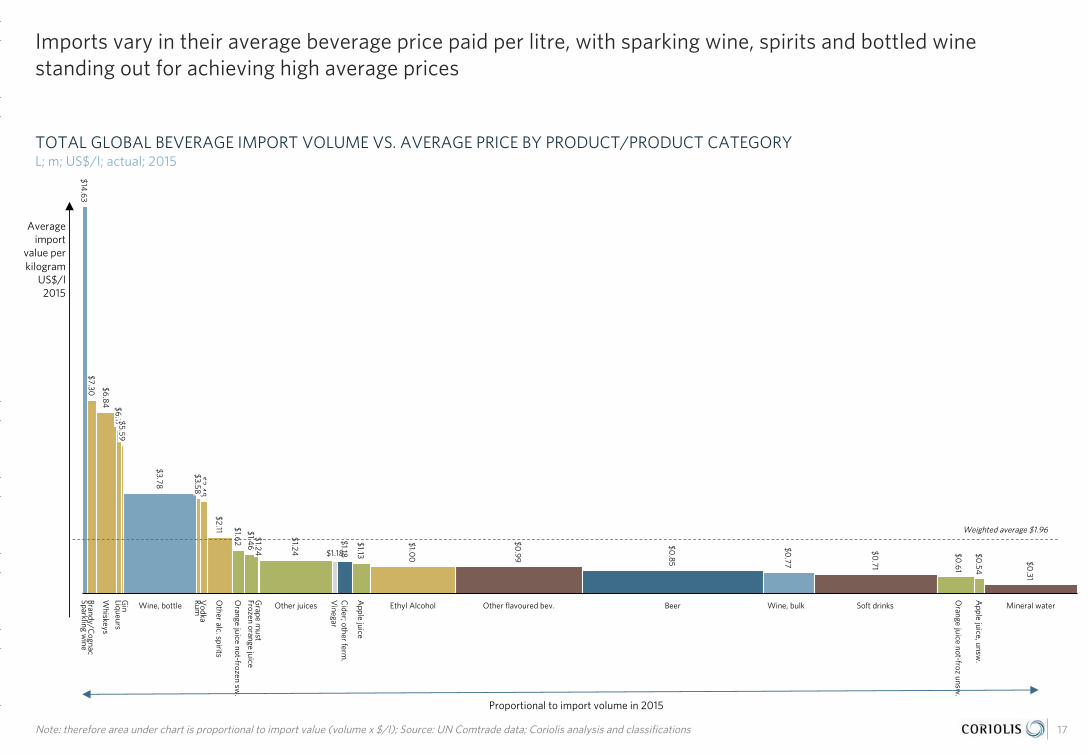

- Imports vary in their average beverage price paid per litre, with sparking wine, spirits and bottled wine standing out for achieving high average prices

DEMAND: IMPORT MARKETS

- Total global cross-border demand for beverages was US$116b in 2015; Europe (including inter-EU) is the single largest market, followed by E/SE Asia ($20.5b) and the US ($20.3b)

- China, various other E/SE Asian countries and the USA stand out for beverage import market growth

- Markets vary in average beverage import price, with Japan, China, much of E/SE Asia and the USA standing out as high value markets

SUPPLY: EXPORTERS

- On the supply side, Europe (including inter-EU) dominates the global beverage trade followed by the US; overall New Zealand is a strong second-tier supplier

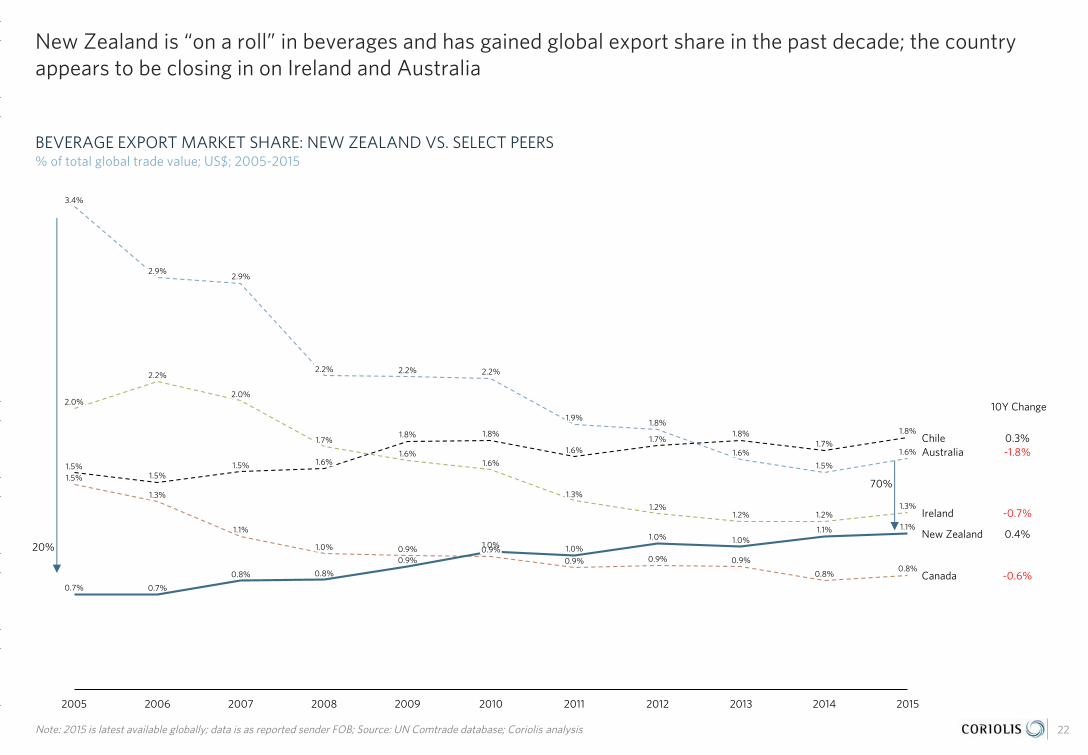

- New Zealand in “on a roll” in beverages and has gained global export share in the past decade; the country appears to be closing in on Ireland and Australia

- New Zealand achieved a solid growth performance in beverage exports over the past five years, beating Europe and Australia in rate of growth

- The average export price received for beverages varies among countries, with New Zealand outperforming almost all competitors, including France

12

Beverages are a huge global market spread across a wide range of products; however, in terms of final litres consumed, the key products are tap water, tea, packaged water, beer and carbonated soft drinks

Tap water60%

Purchased40%

Beer12%

Wine2%

Spirits1%

RTDs0%

Cider0%

Tea22%

Coffee6%

Drinking milk10%

Packaged water19%

Carbonated soft drinks14%

Fruit & veg juices4%

Other10%

13

Note: Both tea and coffee will use tap water; drinking milk includes dairy-based drinks; tea includes mate and herbal blendsSource: UN FAO Aquastat database; UN “Water for People, Water for Life”; OIV; Can Markets; Drinks Business; Kirin Beer University Report; Euromonitor; Statista; Coriolis estimates & analysis

TOTAL HUMAN FLUID CONSUMPTIONLitres; t; 2016

GLOBAL PURCHASED BEVERAGE CONSUMPTION BY FINAL VOLUMELitres; b; 2016

TOTAL = 4.4 trillion litres

TOTAL = 1,800 billion litres

PackagedNon-AlcoholicReady-to-Drink (NARTD)~47%

AlcoholicBeverages(On & Off Trade)~15%

See dairy report

See processed foods report

Hot drinks~28%

Global cross-border beverage trade volumes are growing (5.6% CAGR) with moderate price gains across the cycle leading to export value growth

-

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0

200

5

200

6

200

7

200

8

200

9

2010

2011

2012

2013

2014

2015

14Note: data excludes “other [bulk] water” is as reported sender FOB; Source: UN FAO database; Coriolis classification and analysis

GLOBAL EXPORT VOLUMEL; b; 2005-2015

AVERAGE GLOBAL EXPORT PRICEUS$/l; actual; 2005-2015

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

$1.80

200

5

200

6

200

7

200

8

200

9

2010

2011

2012

2013

2014

2015

GLOBAL EXPORT VALUEUS$; b; 2005-2015

$0

$20

$40

$60

$80

$100

$120

$140

200

5

200

6

200

7

200

8

200

9

2010

2011

2012

2013

2014

2015

X =

10y CAGR4.2% 10y CAGR

1.3%10y CAGR

5.6%

Total global cross-border beverage trade is spread across a wide range of products, though bottled wine ($22.7b), beer ($12.7b), Whiskeys ($10.9b) and wider soft drinks ($17.5) stand out for size

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

TOTAL GLOBAL BEVERAGE IMPORT VALUE BY PRODUCT OR PRODUCT CATEGORYUS$; b; FOB; 2015

15

Total = $116.2

Wine SpiritsBeer

Juices

Vinegar

Water

Soft Drinks

Ethyl Alcohol$7.0

$14.7$14.1 $35.2 $17.5$31.8

$0.6

$2.4

Apple juice$1.7

Orange juice not-frozen unsweetened$1.9

Wine, bulk$3.2

Vodka$2.2

Grape must$0.1

Beer$12.7

Wine, bottle$22.7

Other juices$7.4

Orange juice not-frozen sweetened$1.7

Cider; other fermented$1.4

Apple juice, unsweetened$0.4

Soft drinks$7.2

Frozen orange juice$1.7

Brandy/Cognac$6.1

Rum$1.0

Other flavoured beverages$10.3

Mineral w

ater$2.4

Liqueurs$2.9

Sparkling wine$5.8

Other alc. Spirits$4.3

Whiskeys$10.9

Gin$0.9

Bubble size is proportional to beverage import value in 2015; a bubble this size is US$3b

“Other flavoured beverages,” gin, “other alcoholic spirits,” soft drinks, beer and mineral water stand out for global import growth over the past five years

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

5Y IMPORT GROWTH MATRIX: 5Y VOLUME VS. 5Y CAGR VALUE VS. VALUE 2015 BY PRODUCT L; b; % of US$; US$b; FOB; 2010 vs. 2015

16

5%

10%

2.501.501.000.50 2.00 3.00

0%

4.00-4%

-0.50-1.00 3.500.00

Other flavoured beverages

$3

Vinegar

Mineral water

Whiskeys

Brandy/Cognac

Rum

Vodka

Liqueurs

Grape must

Wine, bottle

Cider; other fermented

Beer

Sparkling wine

Wine, bulk

Frozen orange juice

Orange juice not-frozen unsweetened

Orange juice not-frozen sweetened

Soft drinks

Other juices Ethyl Alcohol

Gin

Other alc. Spirits

Apple juice, unsweetened

Apple juice

5Y Change in volume (l; b) of beverages imported; 10-15

5Y CAGR value

US$; 10-15

Imports vary in their average beverage price paid per litre, with sparking wine, spirits and bottled wine standing out for achieving high average prices

Note: therefore area under chart is proportional to import value (volume x $/l); Source: UN Comtrade data; Coriolis analysis and classifications

TOTAL GLOBAL BEVERAGE IMPORT VOLUME VS. AVERAGE PRICE BY PRODUCT/PRODUCT CATEGORYL; m; US$/l; actual; 2015

17

Wine, bottle Wine, bulk

Apple juice, unsw

.

Orange juice not-frozen sw

.

Rum

Grape m

ust

Sparkling wine

Cider; other ferm

.

Whiskeys

Ethyl Alcohol

Brandy/Cognac

Soft drinks

Vinegar

Liqueurs

Mineral waterBeer

Other alc. spirits

Gin Other flavoured bev.

Apple juice

Orange juice not-froz unsw

.

Vodka

Frozen orange juice

Other juices

$0.71

$14.63

$0.61

$1.46

$3.48

$1.00

$6.17

$0.31

$1.18

$0.85

$1.13

$1.18

$3.58

$7.30

$0.54

$1.62 $1.24 $0.77

$5.59

$0.99

$2.11

$3.78

$1.24

$6.84

Proportional to import volume in 2015

Average import

value per kilogram

US$/l2015

Weighted average $1.96

Total global cross-border demand for beverages was US$116b in 2015; Europe (including inter-EU) is the single largest market, followed by E/SE Asia ($20.5b) and the USA ($20.3b)

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

GLOBAL BEVERAGE IMPORT VALUE BY RECEIVING COUNTRY/REGIONUS$; b; FOB; 2015

18

Total = $116.2

EuropeAmericasAustralasia

NA

/ME/C

A

E/SE AsiaS Asia

SS Africa

$31.0

SS Africa

$3.2

$53.0

Germany$8.0

Other E Asia$1.6

$2.5

Belgium$3.9

Other Europe$19.5

France$4.9

United Kingdom$8.7

$20.5

Russia$1.5

Belarus$0.2

Panama$0.5

United A

rab Emirates

$1.1

$4.4$3.2 $1.6

Other Americas$2.9

Mexico$1.1

India$0

.5

South Korea$1.4

Japan$3.2

Canada$5.3

Singapore$2.2

Other N

A/M

E/CA

$3.3

Thailand$0.6

Malaysia$0.7

Brazil$0.8

Other S A

sia$1.1

Netherlands$5.8

USA$20.3

Vietnam$1.8

Other SE Asia$2.0

Other Pacific

$0.3

Hong Kong SAR$2.6

Australia$1.9

Turkey$0.5

China$4.4

NZ

$0.3

Bubble size is proportional to beverage import value in 2015; a bubble this size is US$3b

China, various other E/SE Asian countries and the United States stand out for beverage import market growth

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

5Y IMPORT GROWTH MATRIX: 5Y VOLUME VS. 5Y CAGR VALUE VS. VALUE 2015 BY RECEIVING COUNTRY/REGIONL; b; % of US$; US$b; FOB; 2010 vs. 2015

19

2.5 3.0-0.5 1.51.00.50.0 2.0

5%

0%

10%

18%

15%

-5%

Japan

South Korea

Other SE Asia

Other E Asia

$3

Hong Kong SAR

China

Other Americas

UK

Panama

FranceGermany

Netherlands

Other Pacific

Australia

NZ

USA

Mexico

Brazil

Canada

Belgium

Vietnam

Other NA/ME/CA

India

Other S Asia

SingaporeMalaysia

Thailand

Belarus

Russia

Other Europe

United Arab EmiratesTurkey

SS Africa

5Y Change in import volume (l;b) of beverages imported; 10-15

5Y CAGR import

value US$; 10-

15

Markets vary in average beverage import price paid, with Japan, China, much of E/SE Asia and the USA standing out as high value markets

Note: therefore area under chart is proportional to import value (volume x $/l); Source: UN Comtrade data; Coriolis analysis and classifications

GLOBAL BEVERAGE IMPORT VOLUME VS. AVERAGE IMPORT PRICE BY KEY MARKETL; b; US$/l; actual; 2015

20

Panama

Mexico

UK

NZ

Other A

mericas

SS Africa

Belgium

Other SE A

sia

Australia

Other Pacific

South Korea

Netherlands

India

Other N

A/M

E/CA

Singapore

Other Europe

Japan

Thailand

China

Turkey

Other E A

siaM

alaysia

France

Vietnam

UA

E

Russia

Canada

Germany

Other S A

sia

Brazil

USA

Hong K

ong SAR

Belarus

$1.16

$1.19

$1.17

$1.94

$1.08

$2.12

$1.50

$2.63

$4.03

$3.59

$4.40

$1.65

$1.22

$2.48$2.29

$1.18$1.10

$1.64

$1.17

$0.87

$0.58

$2.22

$1.05

$0.99

$1.16

$1.98$1.87

$2.83

$2.07

$0.81

$1.50

$1.84$1.68

Proportional to import volume in 2015

Average import

value per kilogram

US$/l; 2015

Weighted average $1.42

On the supply side, Europe (including inter-EU) dominates the global beverage trade followed by the United States; overall New Zealand is a strong second-tier supplier

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

TOTAL GLOBAL BEVERAGE EXPORT VALUE BY SENDING COUNTRY/REGIONUS$; b; FOB; 2015

21

Total = $116.2

EuropeAmericasAustralasia

NA

/ME/C

A

E/SE Asia

S Asia

SS Africa

Other Americas$1.3

Argentina$1.3

$74.2$3.3

Hong Kong SAR$1.3

$22.2

France$16.5

$2.0

Netherlands$6.6

Guatemala$0.3

Russia$0.5

Chile$2.1

$12.1

$1.8

Belarus$0.1

$0.8

United Kingdom$10.0

Other S A

sia$0

.4

China$2.1

Canada$0.9

USA$8.6

Brazil$3.1

Thailand$2.0

Singapore$2.8

Turkey$0.5

Other E Asia$3.8

Other Pacific

$0.1

Germany$6.6

Other Europe$24.6

India$0

.3

Italy$8.9

Australia$1.9

Mexico$4.7

New

Zealand

$1.3

New Zealand is “on a roll” in beverages and has gained global export share in the past decade; the country appears to be closing in on Ireland and Australia

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

BEVERAGE EXPORT MARKET SHARE: NEW ZEALAND VS. SELECT PEERS% of total global trade value; US$; 2005-2015

22

2013

Australia

20152014

New Zealand

2005 2006 2007

10Y Change

Ireland

Chile

2008 2011 20122010

Canada

2009

2.2%

2.0%2.0%

-1.8%

0.4%

1.3%

0.3%

-0.6%

-0.7%1.2%

1.6%1.6%

1.7%

1.2%1.2%

1.3%

1.0% 0.9%

1.1%

1.5%

1.3%

0.9%

0.8%0.8%

0.9%0.9% 0.9%

0.8%

0.9%

0.8%

0.7% 0.7%

1.0%

1.1% 1.1%

1.0%1.0%

1.0%

2.2% 2.2%

2.9%

3.4%

2.9%

2.2%

1.5%

1.6%1.6%

1.9%1.8%

1.6%

1.8%

1.5%1.5%1.5%

1.8%1.7%

1.8%1.8%

1.6%1.7%

20%

70%

Bubble size is proportional to beverage export value in 2015; a bubble this size is US$3b

New Zealand achieved a solid growth performance in beverage exports over the past five years, beating both Europe and Australia in rate of growth

Note: 2015 is latest available globally; data is as reported sender FOB; Source: UN Comtrade database; Coriolis analysis

5Y EXPORT GROWTH MATRIX: 5Y VOLUME VS. 5Y CAGR VALUE VS. VALUE 2015 BY EXPORTING COUNTRY/REGIONL; b; % of US$; US$b; FOB; 2010 vs. 2015

23

-2%

3.0-0.5 0.0 4.02.5

-4%

3.5

10%

1.5

8%

12%

16%

1.0

14%

2.0

4%

0%

2%

0.5

6%

$3

SS Africa

France

Germany

Other Americas

Other Europe

Netherlands

United Kingdom

USA

Australia

New Zealand

Brazil

Argentina

Guatemala

Chile

Hong Kong SAR

China

Singapore

Mexico

Canada

Italy

NA/ME/CA

Russia

Turkey

India

Other E Asia

Thailand

Other S Asia

5Y Change in export volume (l; b) of beverages imported; 10-15

5Y CAGR export

value US$; 10-15

The average export price received for beverages varies among countries, with New Zealand outperforming almost all competitors, including France

Note: therefore area under chart is proportional to import value (volume x $/l); Source: UN Comtrade data; Coriolis analysis and classifications

TOTAL GLOBAL BEVERAGE EXPORT VOLUME VS. AVERAGE EXPORT PRICE BY KEY MARKETL; m; US$/l; actual; 2015

24

France

China

Singapore

Other Pacific

Brazil

Australia

Other A

mericas

Belarus

Canada

Chile

Netherlands

Turkey

India

Argentina

Other S A

sia

Thailand

Other Europe

Guatem

ala

Hong K

ong SAR

Other E A

sia

Germ

any

United K

ingdom

Russia

New

Zealand

Mexico

SS Africa

NA

/ME/C

A

Italy

USA

$0.96

$6.29

$0.4

6

$1.57

$1.24

$0.82

$2.03

$0.71

$2.85

$0.53

$1.13

$1.08

$1.35

$2.06

$1.33

$0.65

$0.81

$1.60

$1.54

$0.97

$0.4

7

$6.07

$1.11

$0.4

3

$1.74 $1.55

$2.24

$3.55

Proportional to export volume in 2015

Average export

value per kilogram

US$/l2015

Weighted average $1.96

High valuere-export

Whisky & Spirits

New Zealand Production

+ Wine

+ Beer

+ Juice

+ Alcoholic Spirits

+ Water

+ Production

+ Regional activity

+ Key inputs

+ Growth upside 02

New Zealand can continue to to grow beverage production for the foreseeable future

WINE PRODUCTIONNew Zealand is a rapidly emerging New World wine region with significant capacity for future growth and no major production challenges

- Wine is New Zealand’s largest beverage export- New Zealand grape area and wine production has grown

dramatically over the past twenty years in response to growing global demand for New Zealand wine

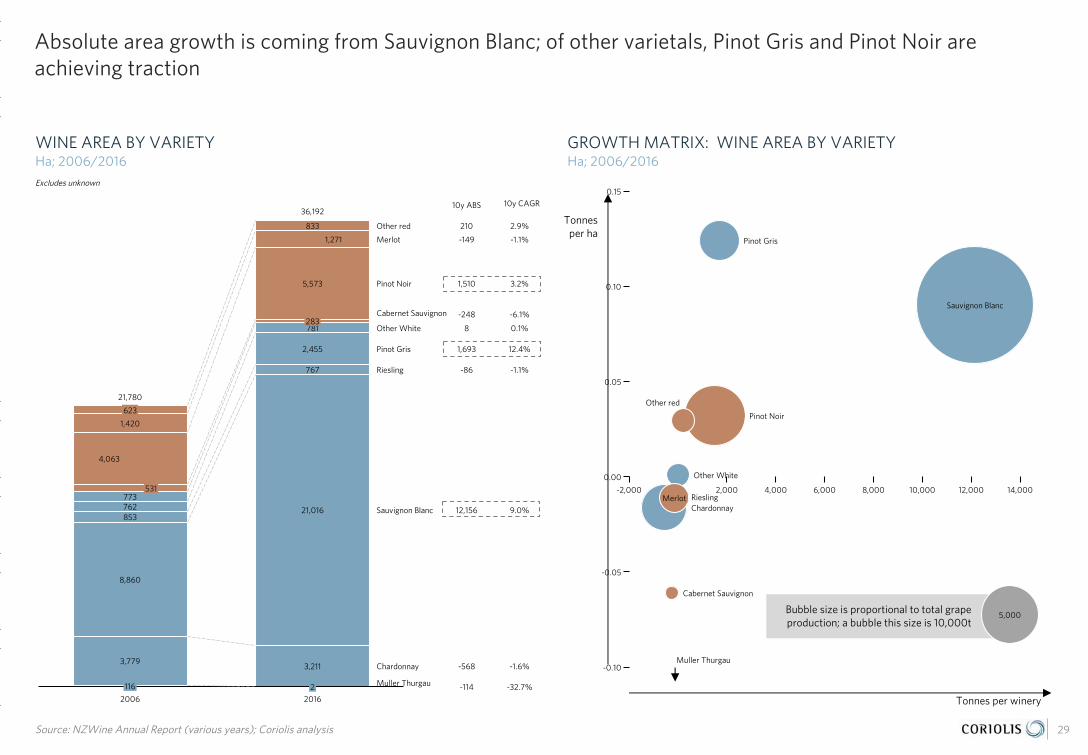

- Absolute area growth is coming from Sauvignon Blanc; of other varietals, Pinot Gris and Pinot Noir are achieving traction

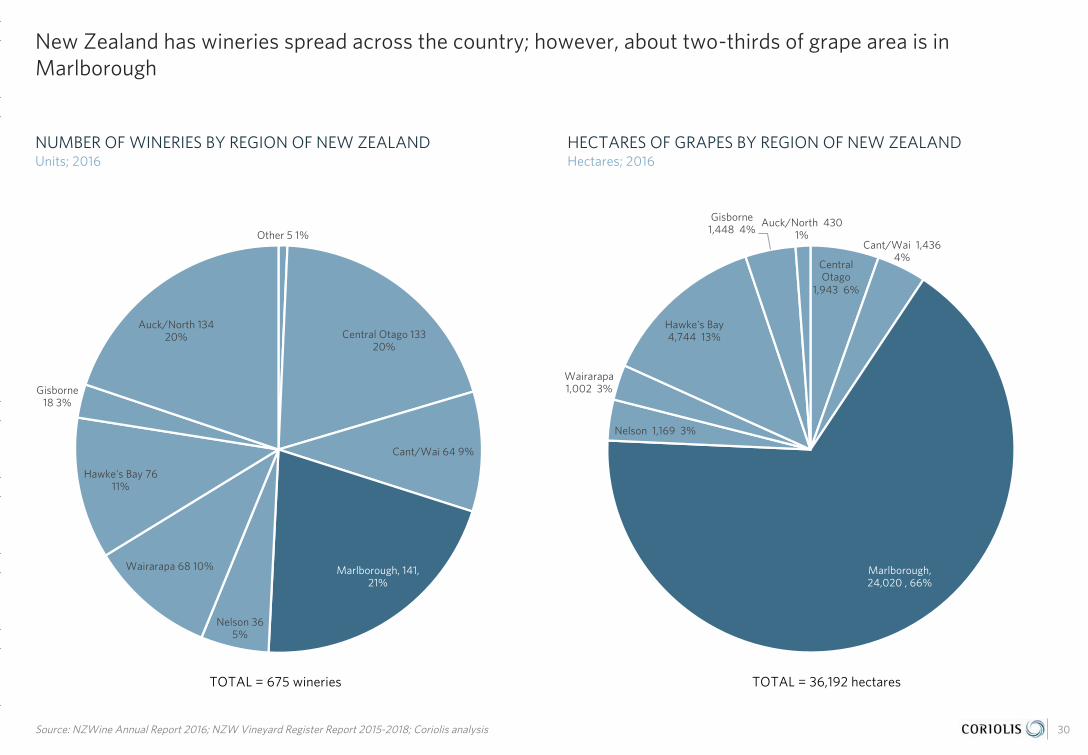

- New Zealand has wineries spread across the country; however, about two-thirds of grape area is in Marlborough

- As the largest, most mature region, Marlborough leads in terms of both (1) tonnes per winery and (2) tonnes per hectare

- While Marlborough is clearly the leading region, a number of the smaller regions are growing, particularly recognised red producers Hawke’s Bay (Syrah), Canterbury/Waipara (Pinot Noir), and Central Otago (Pinot Noir)

- Peer group performance suggests New Zealand has significant potential capacity to increase wine area over the mid-to-long run

OTHER BEVERAGE PRODUCTIONNew Zealand can and does produce a range of other beverages beyond wine, again with few limitations on potential production volumes

- New Zealand produces significant volumes of both key beer ingredients (hops and barley); beer production trending down in recent years reflecting the market movement to “less but better quality”

- New Zealand is a major global producer and exporter of apples and kiwifruit, as well as developing and pioneering a wide range of new varieties and species

- New Zealand has significant quantities of raw materials available to produce alcoholic spirits

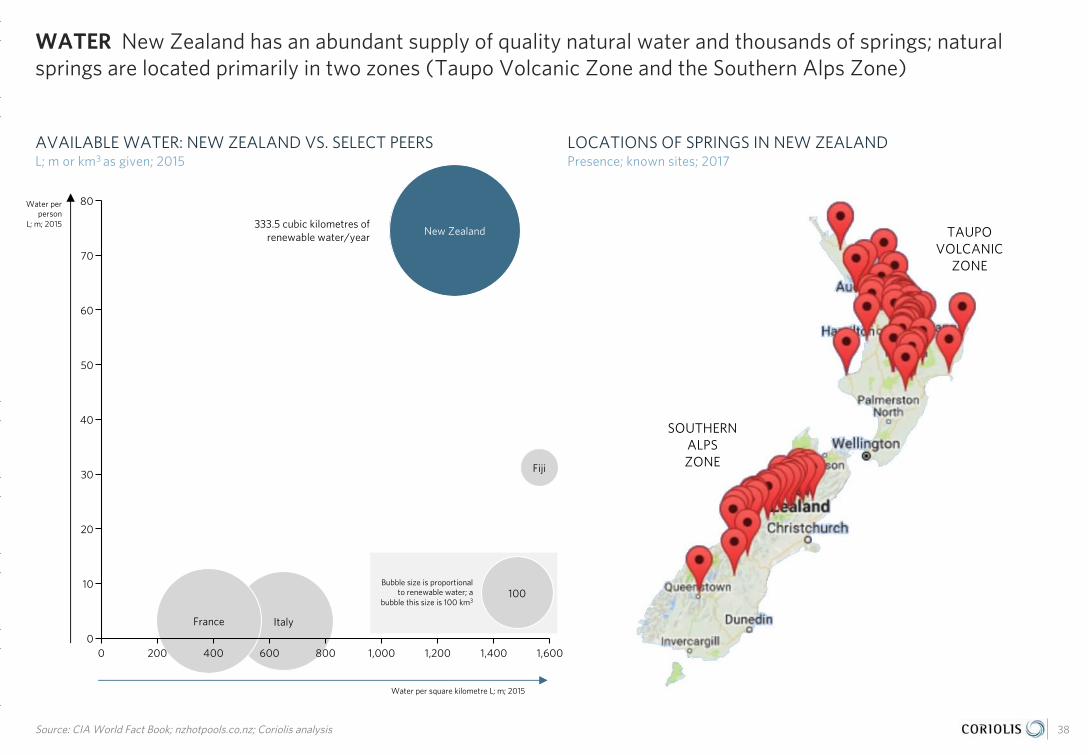

- New Zealand has an abundant supply of quality natural water and thousands of springs; natural springs are located primarily in two zones (Taupo Volcanic Zone and the Southern Alps Zone)

- Due to its unique history, New Zealand has a range of unique or signature ingredients and flavours suitable for use in beverages

26

New Zealand is a rapidly emerging New World wine region with significant capacity for future growth with no major impediments or capacity constraints

27

WINEOTHER

BEVERAGES

WINE PRODUCTION New Zealand grape area and wine production has grown dramatically over the past twenty years in response to growing global demand for New Zealand wine

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

1961196319651967196919711973197519771979198119831985198719891991199319951997199920

01

200

320

05

200

720

09

2011

2013

2015

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

1961196319651967196919711973197519771979198119831985198719891991199319951997199920

01

200

320

05

200

720

09

2011

2013

2015

28

NEW ZEALAND GRAPE AREAHectares; 1977-2016

NEW ZEALAND WINE PRODUCTIONL; m; 1977-2016

NEW ZEALAND GRAPE PRODUCTIONTonnes crushed; 1977-2016

Source: MAF/MPI; NZWine Annual Report ; UN FAO FAOSTAT database; Coriolis analysis

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

500,000

1961196319651967196919711973197519771979198119831985198719891991199319951997199920

01

200

320

05

200

720

09

2011

2013

2015

Low year

Bubble size is proportional to total grape production; a bubble this size is 10,000t

Absolute area growth is coming from Sauvignon Blanc; of other varietals, Pinot Gris and Pinot Noir are achieving traction

29Source: NZWine Annual Report (various years); Coriolis analysis

WINE AREA BY VARIETYHa; 2006/2016

GROWTH MATRIX: WINE AREA BY VARIETYHa; 2006/2016

2,000 4,000

0.05

-2,000

0.15

0

0.10

12,000

-0.05

-0.10

14,000

0.00

6,000 10,0008,000Riesling

5,000

Muller Thurgau

Chardonnay

Pinot Gris

Merlot

Pinot Noir

Other red

Sauvignon Blanc

Cabernet Sauvignon

Other White

Tonnes per ha

Tonnes per winery

Chardonnay

Riesling

10y ABS

Muller Thurgau

Other red

2006

Pinot Noir

Pinot Gris

Cabernet Sauvignon

Other White

Merlot

Sauvignon Blanc

2016

10y CAGR

-1.1%

12.4%

-1.6%

-32.7%

9.0%

0.1%

2.9%

21,780

36,192

-6.1%

3.2%

-1.1%

210

781

773

2,455

531

5,573

4,063

283

3,779

2116

3,211

762 21,016

8,860

1,420

1,693

-86

12,156

8

-149

1,510

-248

767

853

1,271

623

-568

-114

833

Excludes unknown

New Zealand has wineries spread across the country; however, about two-thirds of grape area is in Marlborough

Other 5 1%

Central Otago 13320%

Cant/Wai 64 9%

Marlborough, 141, 21%

Nelson 365%

Wairarapa 68 10%

Hawke's Bay 7611%

Gisborne18 3%

Auck/North 13420%

30Source: NZWine Annual Report 2016; NZW Vineyard Register Report 2015-2018; Coriolis analysis

NUMBER OF WINERIES BY REGION OF NEW ZEALANDUnits; 2016

HECTARES OF GRAPES BY REGION OF NEW ZEALANDHectares; 2016

Central Otago

1,943 6%

Cant/Wai 1,436 4%

Marlborough, 24,020 , 66%

Nelson 1,169 3%

Wairarapa1,002 3%

Hawke's Bay4,744 13%

Gisborne 1,448 4%

Auck/North 430 1%

TOTAL = 675 wineries TOTAL = 36,192 hectares

As the largest, most mature region, Marlborough leads in terms of both (1) tonnes per winery and (2) tonnes per hectare

31Source: NZWine Annual Report 2016; NZW Vineyard Register Report 2015-2018; Coriolis analysis

NZ: NUMBER OF WINERIES VS. TONNES PER WINERYUnits; t/unit; 2016

NZ: REGIONAL AREA VS. TONNES PER HECTAREHectares; tonnes/hectare; 2016

Canterbury

Gisborne

Haw

kes Bay

Nelson

Auckland

Waikato

Northland

Wairarapa

Otago

Marlborough

12 6 269

279

565

2,293

88

6

74

190

Canterbury

Gisborne

Haw

kes Bay

Nelson

Wairarapa

Waikato

Auckland

Otago

Northland

Marlborough

5.0

3.61.1

1.4

8.6

9.1

13.5

11.0

4.7

8.5

# of wineries

Tonnes/winery

Area in grapes

Tonnes/hectare

Bubble size is proportional to total grape production; a bubble this size is 10,000t

While Marlborough is clearly the leading region, a number of the smaller regions are growing, particularly those recognised red producers Hawke’s Bay (Syrah), Canterbury/Waipara (Pinot Noir), and Central Otago (Pinot Noir)

32Source: NZW Annual Reports various years; NZW Vineyard Register Report various years; Coriolis analysis

GRAPES CRUSHED IN VINTAGE BY REGIONT; 2006/2011/2016

PRODUCTION MATRIX: T/WINERY VS. T/HA VS. TOTALT; 2015/16

500

10

0

15

0 1,000 2,000 2,500

5

1,500

Auck/North

Nelson

Gisborne

Marlborough

10,000

Hawkes Bay

Wairarapa

Canterbury

Otago

Tonnes per ha

Tonnes per winery

Central OtagoOther

10y CAGR

Wairarapa

GisborneAuck/North

Hawke's Bay

10y ABS

2011

Nelson

2016

Marlborough

2006

Cant/Waipara

9,671

-2,105

2,041

4,565

4,405

9,119

209,854

357 50.7%

7.1%

14.8%

420,356

324,592

182,886

2.6%

-1.2%-2.7%

11.0%

6.0%5.3%

323,290

244,893

15,944

14,450

18,049

9,4853,051

5,623

42,958

35,533

33,287

113,436

10,028

7,854

1,814

36349

3,008

-437

5,049

3,598

7,1044,612

12,170

1,377

1,626

69,177

Peer group performance suggests New Zealand has significant potential capacity to increase wine area over the mid-to-long run

Source: OIV; NZ Winegrowers; CIA World Fact Book; Coriolis analysis

GROWTH MATRIX OF WINE AREA: % TOTAL AREA VS. M2/PERSON VS. TOTAL WINE AREA% of hectares; hectares/person; hectares; 2015 or 2016

33

1.5%

250

2.0%

200

0.0% 2.5%1.0%

100

50

150

0.5%0

Portugal

Romania

Italy

Spain

100,000

France

Greece

Austria

New Zealand

Bulgaria

Germany

Hungary

Wine area/person

m2

2015

Wine area as a percent of total land area; % of km2; 2015

Bubble size is proportional to total wine areaA bubble this size is 100,000 hectares

New Zealand can and does produce a wide range of other beverages beyond wine with few limitations on potential production volumes

34

WINEOTHER

BEVERAGES

BEER PRODUCTION New Zealand produces significant volumes of both key beer ingredients (hops and barley); beer production trending down in recent years reflecting the market movement to “less but better quality”

0

100

200

300

400

500

600

700

800

900

1,000

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

200

1

200

3

200

5

200

7

200

9

2011

2013

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

1961196319651967196919711973197519771979198119831985198719891991199319951997199920

01

200

320

05

200

720

09

2011

2013

35

NEW ZEALAND HOP PRODUCTIONTonnes; 1977-2014

NEW ZEALAND BEER PRODUCTIONTonnes; 1961-2014

NEW ZEALAND BARLEY PRODUCTIONTonnes; 1961-2015

Source: MAF/MPI; UN FAO FAOSTAT database; Coriolis analysis

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

1961196319651967196919711973197519771979198119831985198719891991199319951997199920

01

200

320

05

200

720

09

2011

2013

Ongoing shift to “less but better quality”

FRUIT FOR JUICE & CIDER New Zealand is a major global producer and exporter of apples and kiwifruit, as well as developing and pioneering a range of new varieties and species

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1961196319651967196919711973197519771979198119831985198719891991199319951997199920

01

200

320

05

200

720

09

2011

2013

AAPPPPLLEESS KKIIWWIIFFRRUUIITT OOTTHHEERR FFRRUUIITT

Granny Smith*

Splendour

Gala

Royal Gala

Braeburn

Jazz

Envy

Pacific Rose

Pacific Beauty

Pacific Queen

Smitten

Maxie

Sweetie

Hayward

(dominant global)

Bruno

Alison

EnzaGreen

EnzaGold

Zespri Gold

Zespri Sungold

Zespri SweetGreen

KiwiKiss

Feijoa

Tamarillo

Passionfruit

Kiwiberries

Kiwano

Blueberries

(various cultivars)

Blackcurrants

(various cultivars)

36* Appeared in Australia but was developed/improved in New Zealand; Source: MAF/MPI; UN FAO FAOSTAT database; Coriolis analysis

NEW ZEALAND FRUIT PRODUCTIONTonnes; 1961-2014

EXAMPLES OF FRUIT DEVELOPED OR PIONEERED IN NZSelect examples; 2017

Apples

Kiwifruit

Other fruit

Wine grapes

ALCOHOLIC SPIRITS INPUTS New Zealand has significant quantities of raw materials available to produce alcoholic spirits

0

5,000

10,000

15,000

20,000

25,000

1961

1963

1965

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

200

1

200

3

200

5

200

7

200

9

2011

2013

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1961

1964

1967

1970

1973

1976

1979

1982

1985

1988

1991

1994

1997

200

0

200

3

200

6

200

9

2012

2015

37

NEW ZEALAND WHEY PRODUCTIONTonnes; 1977-2014

NEW ZEALAND GRAIN PRODUCTIONTonnes; 1961-2016

NEW ZEALAND SUGAR REFINING PRODUCTION & IMPORTSTonnes; 1961-2014

Source: MAF/MPI; Statistics NZ; UN FAO FAOSTAT database; Coriolis analysis

0

50,000

100,000

150,000

200,000

250,000

300,000

1961196319651967196919711973197519771979198119831985198719891991199319951997199920

01

200

320

05

200

720

09

2011

2013

Total whey, including whey processed into alcohol

NZ Refined

Imported

Wheat

Corn

Barley

Other grains

WATER New Zealand has an abundant supply of quality natural water and thousands of springs; natural springs are located primarily in two zones (Taupo Volcanic Zone and the Southern Alps Zone)

38Source: CIA World Fact Book; nzhotpools.co.nz; Coriolis analysis

AVAILABLE WATER: NEW ZEALAND VS. SELECT PEERSL; m or km3 as given; 2015

LOCATIONS OF SPRINGS IN NEW ZEALANDPresence; known sites; 2017

20

30

1,6000

10

70

80

60

40

50

800 1,000 1,2000 200 400 600 1,400

New Zealand

Fiji

100

France Italy

Bubble size is proportional to renewable water; a

bubble this size is 100 km3

Water per person

L; m; 2015

Water per square kilometre L; m; 2015

TAUPOVOLCANIC

ZONE

SOUTHERN ALPSZONE

333.5 cubic kilometres of renewable water/year

UNIQUE FLAVOURS Due to its unique history, New Zealand has a range of unique or signature ingredients and flavours suitable for use in beverages

39

ManukaHoney

Kawakawa(Unique native

plant)

Feijoa

Kiwifruit

GoldKiwifruit

Titoki

New ZealandCategory Performance

+ Overview

+ Category Segmentation

+ Exports by product

03

New Zealand has a strong position in wine and is emerging across a wide range of other beverages

41

- New Zealand has a strong beverages platform and produces all six major categories of beverages; New Zealand has real strength in wine and is growing and emerging in other categories

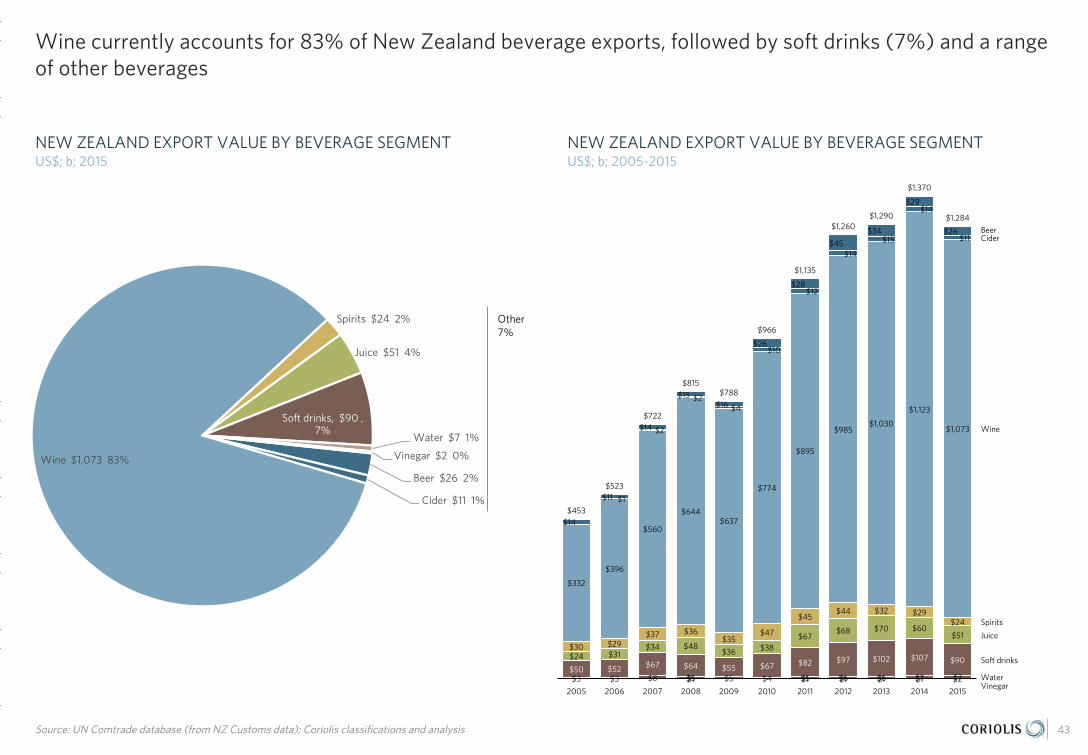

- Wine currently accounts for 83% of New Zealand beverage exports, followed by soft drinks (7%) and a range of other minor beverages

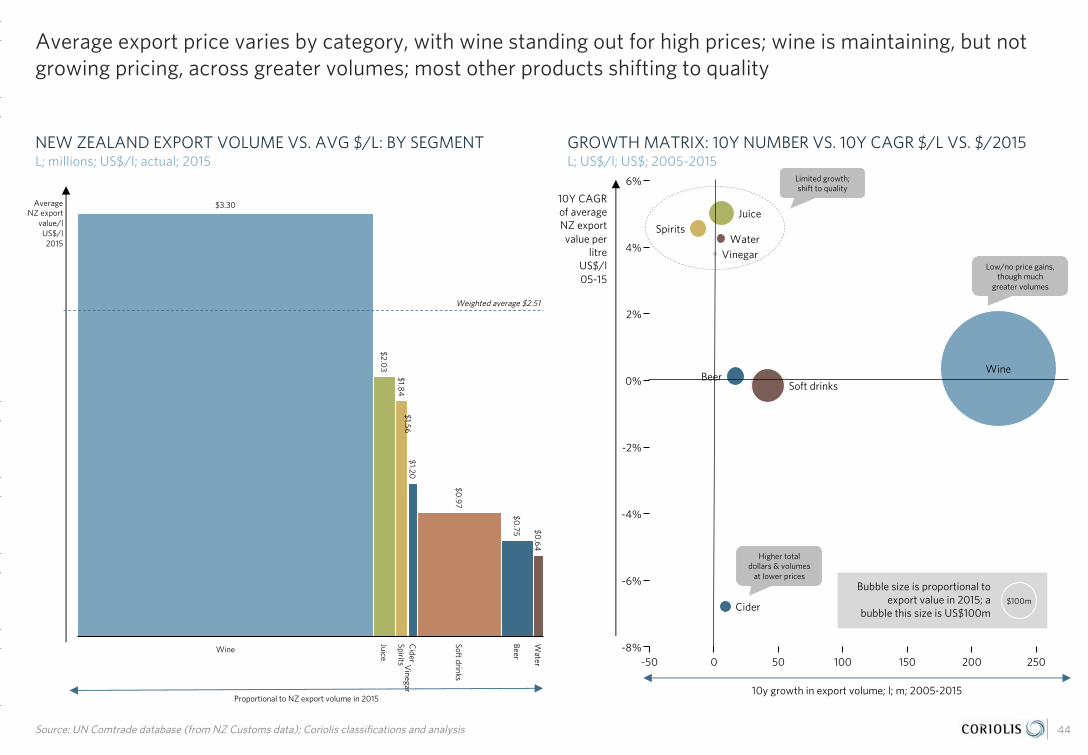

- Average export price varies by category, with wine standing out for high prices; wine is maintaining, but not growing pricing, across greater volumes; most other products shifting to quality

- New Zealand is growing its share of the global wine trade, but only maintaining share across most other beverages; cider appears to have stalled after solid growth (needs to transition beyond Australia)

- New Zealand has rapidly growing wine exports on the back of Marlborough Sauvignon Blanc, which is now a “must have” varietal across most major markets; Pinot Noir also achieving growing recognition

- New Zealand has had growing volumes of beer and cider exports, driven by increased interest in authentic, craft & premium; cider, in particular, appears well positioned for growth beyond Australia

- New Zealand has a fast evolving alcoholic spirits industry that is seeking its “signature” spirit in a large and growing global market

- New Zealand non-alcoholic beverages growing well, driven by juices and other flavoured beverages; Australia still the largest market, but E/SE Asia emerging (particularly Japan and China)

OVERVIEW BY CATEGORY

New Zealand has a strong beverages platform and produces all six major categories of beverages; New Zealand has real strength in wine and is growing and emerging in other categories

42

- New Zealand Sauvignon Blanc “owns” the category and is now a “must have”

- Refreshing/summer afternoon positioning to females (vs. reds)

- Emerging in Pinot Noir and other reds

- Strong growth for 30+ years

- Strong and growing market share across Anglo markets

- Growing rapidly in Asia

- Attracting global brand leaders (e.g. LVMH Moët Hennessy Louis Vuitton)

- Well regarded globally for the quality of its hops

- Benefiting from global shift to craft/specialty

- Leveraging long-term NZ strength in hops and apples

- Growth coming from global multinationals (e.g. Kirin, Heineken, Asahi) and local innovators

- Cider, in particular, stands out as having clear leverage and good long term growth prospects

- Sector in early stages of growth curve

- Emerging sector driven by strong marketing and unique products

- Rapid innovation underway

- Still seeking “unique” position beyond “me-too” spirits

- Huge hypothetical potential for growth

- Strong fundamentals

- Wide range of pioneers

- Second generation firms with strong products presentation and marketing (e.g. Antipodes) doing well

- Premium new comers Palaeo and OnePure

#1 Global Sauvignon Blanc

Focused on Australia

Focused on Australia

Emerging rapidly

- Building on New Zealand’s strength in export fruit, particularly in apples and kiwifruit

- Pioneer of a range of new fruits and fruit varieties

- No real leverage to date of existing strong fruit brands (e.g. Zespri, Jazz, Pacific Rose)

- Early pioneer in energy drinks (“V”)

- Growing strongly in a “post-CSD” environment [Carbonated Soft Drinks]

- Good fit with “Brand NZ” and existing strengths in select fruits

- Strong traction in “natural” positioned carbonated juices

Regionally strong in specific products

Focused on Australia

HIGH-LEVEL CATEGORIES

- Wine, bottles- Sparkling wine- Bulk wine

- Beer - Whisky/Whiskey- Vodka- Gin

- Bottled water- Other water (e.g. bulk)

- Apple juice- Kiwifruit/other juices

- Soft drinks- Other flavoured beverages

EXAMPLE PRODUCTS UNDER THESE CATEGORIES

WINE SOFT DRINKS WATERBEER/CIDER SPIRITS JUICES

Wine currently accounts for 83% of New Zealand beverage exports, followed by soft drinks (7%) and a range of other beverages

43Source: UN Comtrade database (from NZ Customs data); Coriolis classifications and analysis

NEW ZEALAND EXPORT VALUE BY BEVERAGE SEGMENTUS$; b; 2015

NEW ZEALAND EXPORT VALUE BY BEVERAGE SEGMENTUS$; b; 2005-2015

Beer $26 2%

Cider $11 1%

Wine $1,073 83%

Spirits $24 2%

Juice $51 4%

Soft drinks, $90 , 7%

Water $7 1%

Vinegar $2 0%

Cider

20132007 2012

Spirits

Beer

2008

Soft drinks

2014 20152006

Water

2010

Wine

Juice

20112005 2009Vinegar

$8

$1,370

$1$3

$453

$2

$90

$3

$1,284

$7

$722

$966

$1 $6

$815

$1 $1

$788

$7

$1,290

$523

$5$5 $1$6

$1,135

$5$4

$1,260

$24

$11

$34$31

$14

$12

$14

$15

$70$68 $51$60

$36$48

$67$38

$26

$16

$45

$28

$11

$14

$15

$14

$2

$2

$10

$4

$29

$34

$1

$26

$1,073

$1,123

$52$50

$895

$774

$1,030$985

$97$82$107$102

$64$67 $67$55

$47$35

$44$45

$29$30

$36$37

$560

$396

$637$644

$29$32

$332

$24

Other7%

Average export price varies by category, with wine standing out for high prices; wine is maintaining, but not growing pricing, across greater volumes; most other products shifting to quality

44Source: UN Comtrade database (from NZ Customs data); Coriolis classifications and analysis

NEW ZEALAND EXPORT VOLUME VS. AVG $/L: BY SEGMENTL; millions; US$/l; actual; 2015

GROWTH MATRIX: 10Y NUMBER VS. 10Y CAGR $/L VS. $/2015L; US$/l; US$; 2005-2015

Bubble size is proportional to export value in 2015; a

bubble this size is US$100m

Cider

Wine

Vinegar

Beer

Water

Soft drinks

Spirits

Juice

$0.75 $0

.64

$1.84$1.56

$2.03

$3.30

$0.97

$1.20

Proportional to NZ export volume in 2015

Average NZ export

value/lUS$/l2015

Weighted average $2.51

15010050

0%

-2%

2%

6%

4%

250200-8%

-4%

-6%

-50 0

Juice

Beer

$100mCider

WaterVinegar

Spirits

Wine

Soft drinks

10Y CAGR of average NZ export value per

litreUS$/l 05-15

10y growth in export volume; l; m; 2005-2015

Higher total dollars & volumes

at lower prices

Limited growth; shift to quality

Low/no price gains, though much

greater volumes

New Zealand is growing its share of the global wine trade, but only maintaining share across most other beverages; cider appears to have stalled after solid growth (needs to transition beyond Australia)

45Source: UN Comtrade database (from NZ Customs data); Coriolis classifications and analysis

NEW ZEALAND SHARE OF WORLD EXPORT VALUE BY CATEGORYUS$; % of US$; 2015

NEW ZEALAND SHARE OF WORLD EXPORT VALUE BY CATEGORY% of US$; 2005-2015

Vinegar

Wine

Cider

Beer SpiritsJuice

Water

Soft drinks

0.2%

0.1%

0.3%

0.8%

0.5%

3.4%

0.3%

0.3%

Proportional to total global export value in 2015

NZ share of total global

trade; % of $;

2015

Soft drinks

Juice

2012

Water

Beer

20152013 201420112007 2008 20092005 2006

Wine

2010

Cider

Spirits

0.5% 0.5%

0.4%

0.2%

0.6%0.5%

0.6%

0.3%

0.6%

0.3%

0.1% 0.1%

0.2%0.2%

0.3%0.3% 0.3%

0.2%0.1% 0.2%

0.2%0.1% 0.1%

0.3%0.3%

0.2%0.1%

0.9%

0.2%0.1%

0.8%

0.1%0.1%

1.0%

0.1%0.1%

1.0%

0.1%0.1%

2.7%

3.0%

2.0%

2.5%

2.8%

2.2%

3.4%

1.6%

0.2%

3.0%

3.2%

1.8%

0.1%

0.3%

0.0%

0.6%

0.4%

0.1%

0.4%0.4%

0.2%

0.4%0.5%

0.2%

0.6%

0.4%

0.3%0.2%

0.4%

0.9%

0.3%

0.9%

0.3%

0.4%

0.2%0.3% 0.3%

0.2%

Wine, bulk

2010

10Y ABS

2005

10Y CAGR

Sparkling wine

2015

Wine, bottle +$565

$1,073-$14

$332

$774

+$190

$299

$685

$864

$8$84

$198 38%

11%

-8%

$25

$4

$11

WINE New Zealand has rapidly grown wine exports on the back of Marlborough Sauvignon Blanc, which is now a “must have” varietal across most major markets; Pinot Noir also achieving growing recognition

46Source: UN Comtrade database; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis classifications and analysis

NZ WINE EXPORT VALUEUS$m; 2005-2015

SHARE OF NZ WINE GRAPE AREA BY VARIETAL% of ha; 1992-2016

AGGREGATE GLOBAL EXPORT GROWTHUS$b; 2005-2015

EXAMPLE PRODUCTS: SAINT CLAIR2017

CAGR12%

$15.1

$1.8$3.6 $3.0

$22.7

$3.2

$5.8 $6.1

Wine, bottle Wine, bulk Sparkling wine Brandy/Cognac

CAGR4%

05 15

CAGR5%CAGR

6%

CAGR8%

200

1

2010

1993

Merlot

200

6

200

0

2015

Sauvignon Blanc

Pinot Noir20

09

Pinot GrisRiesling

200

4

200

3

2014

200

2

1992

200

5

Other red

Muller Thurgau1998Chardonnay

1996

200

7

2012

1997

Other White

2013

1999

2016

200

8Cabernet Sauvignon

1994

2011

1995

18%15%

15%15% 15%

18%

15%

19%

15%

17%16% 16%

19%16% 16%

3%3% 2%

4%2%3% 3%3% 2%

4%4% 4%2% 2%

4%4% 3%3% 3%3%4%4% 4% 2%3% 2%3% 3% 2% 2%3%

6%6% 8%7%4%4% 6%5% 5% 5%6% 4% 4%4%8% 8%8% 7%8%

30%34%28%

25% 25%

36% 53% 53%50%41% 43%

24%

9%

14%

10%9% 10%

15% 23% 24%20%15% 17%

4% 4%5%5% 5%

4%4%

3%4%

4% 4%5%

57% 57%58%53% 58% 58%

5% 5%5%5% 5%

0% 0%1%1% 1% 0% 0% 0%0%0% 0%2%

16% 12%18%22%20%

10%3% 2%4%8% 6%

19% 17%21%26% 23%

16%12% 9%12%14% 13%

29%

22% 23%22%

0% 0%

24%

29%29%28%

26%26%

3%

9% 8%9%9% 10% 8%

6% 5%7%

8% 7%

10%

2% 2%3%

4% 3%

2% 1% 2%2%1% 1%

8% 7%7%

1%

6%8%

11%13%

10%8% 8%

1%

2%2%

2%4% 3%

2% 1% 1%1%2% 2%

1% 1%1%1% 1%

2%3% 5%

2%2% 2%0%

2% 2%2%3% 3% 2%

0% 0%0%

2%0%

10% 9%10%13% 12% 8%4% 4%5%

6% 5%14%

5% 7%6%5% 5% 7%

15% 15%7%7% 7%

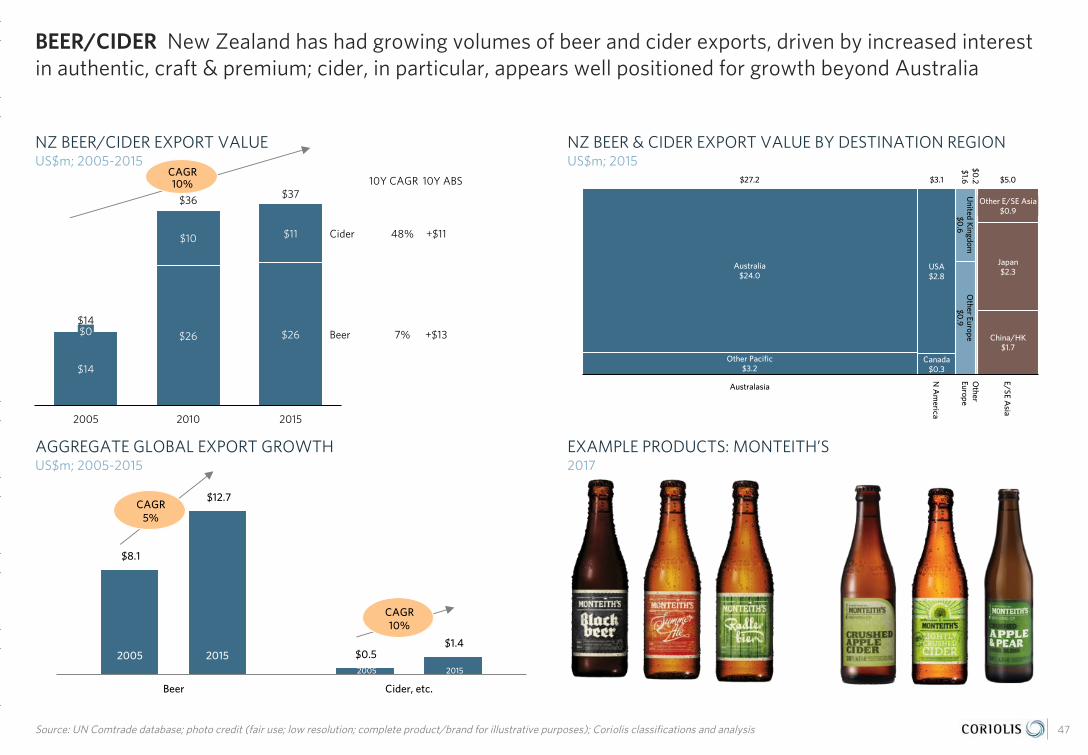

BEER/CIDER New Zealand has had growing volumes of beer and cider exports, driven by increased interest in authentic, craft & premium; cider, in particular, appears well positioned for growth beyond Australia

47Source: UN Comtrade database; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis classifications and analysis

NZ BEER/CIDER EXPORT VALUEUS$m; 2005-2015

NZ BEER & CIDER EXPORT VALUE BY DESTINATION REGIONUS$m; 2015

AGGREGATE GLOBAL EXPORT GROWTHUS$m; 2005-2015

EXAMPLE PRODUCTS: MONTEITH’S2017

$8.1

$0.5

$12.7

$1.4

Beer Cider, etc.

CAGR5%

2005 20152005 2015

CAGR10%

Europe

N A

merica

Other

Australasia

E/SE Asia

$3.1

$1.6 $5.0

$0.2

Canada$0.3

United K

ingdom$0

.6O

ther Europe$0

.9

Australia$24.0

Other Pacific$3.2

USA$2.8

China/HK$1.7

$27.2

Japan$2.3

Other E/SE Asia$0.9

10Y ABS

2005 2010 2015

10Y CAGR

Cider

Beer

$37$36

$14

$26 $26$0

$11 48%

7% +$13$14

$10 +$11

CAGR10%

SPIRITS New Zealand has a rapidly evolving alcoholic spirits industry that is seeking its “signature” spirit in a large and growing global market

$0.6 $1.0 $1.9 $3.8 $3.5

$7.5 $9.6 $10.4

$16.2

$22.3

$35.2

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

48Source: UN Comtrade database; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis classifications and analysis

NZ SELECT ALCOHOLIC SPIRITS EXPORT VALUEUS$m; 2005-2015

GLOBAL ALCOHOLIC SPIRITS EXPORT VALUEUS$b; 1965-2015

NZ INDUSTRY STRATEGIC DIRECTIONModel; 2017

EXAMPLE PRODUCTS: SIMPLY PURE NZ2017

CAGR9%

RTDBeverages

Made elsewherebottled in NZ

Conventionalspirits made in

NZ

Conventional spirits made in

NZ with NZ flavours

New Zealand unique spirits

10Y ABS

20152010

10Y CAGR

2005

Liqueurs

GinRum

Whiskeys

Vodka

RTD/Other alc. Spirits

-$0

+$4-$2

-$0

$47

$24

-$5

$26

+$1

$1

$1

$1

$1

$1

$1

$7

$3$1

$6

$7

$3

$3

-12%16%

7%

-2%

-3%

-5%$0

$1$19 $14

$28

NARTD* New Zealand non-alcoholic beverages growing well, driven by juices and other flavoured beverages; Australia still the largest market, but E/SE Asia emerging (particularly Japan and China)

49

* NARTD = Non-alcoholic ready-to-drink (industry term)Source: UN Comtrade database; photo credit (fair use; low resolution; complete product/brand for illustrative purposes); Coriolis classifications and analysis

NZ NARTD EXPORT VALUE BY TYPEUS$; m; 2005-2015

NZ NARTD EXPORT VALUE BY DESTINATIONUS$; m; 2015

$8,764 $8,390

$1,751

$14,715

$17,528

$2,402

Juice Soft drinks Water

AGGREGATE GLOBAL EXPORT GROWTHUS$m; 2005-2015

EXAMPLE PRODUCTS: KARMA COLA Co.2015

CAGR5%

2005 2015

CAGR3%

CAGR8%

Other unsweetened Other flavoured carbonated

2005

10Y ABS10Y CAGR

Mineral water

Other juices

Apple juice

2015

Other flavoured bev.

Soft drinks

2010

$149

+$3

11%-14% -$35

+$5

$77

+$24

+$75

$110

$6$35

$80

$10

$24

$14$14

$10$17 2%

$7

30%

13%

$4

$57

$45

$3

$10CAGR

7%

Other

Australasia

N A

merica

E/SE Asia

$41.4$16.8 $3.5

USA$16.0

Australia$83.7

Other Pacific$9.0

Canada$0.8

China/HK$11.6

$92.7

Other E/SE Asia$11.8

Japan$18.0

New ZealandGrowth & Innovation

+ Horizons for growth

+ Emerging export stars

+ Mega-trends driving change

+ Innovation & new products 04

New Zealand firms continue to develop a range of innovative new beverage products

51

THREE HORIZONS OF GROWTH

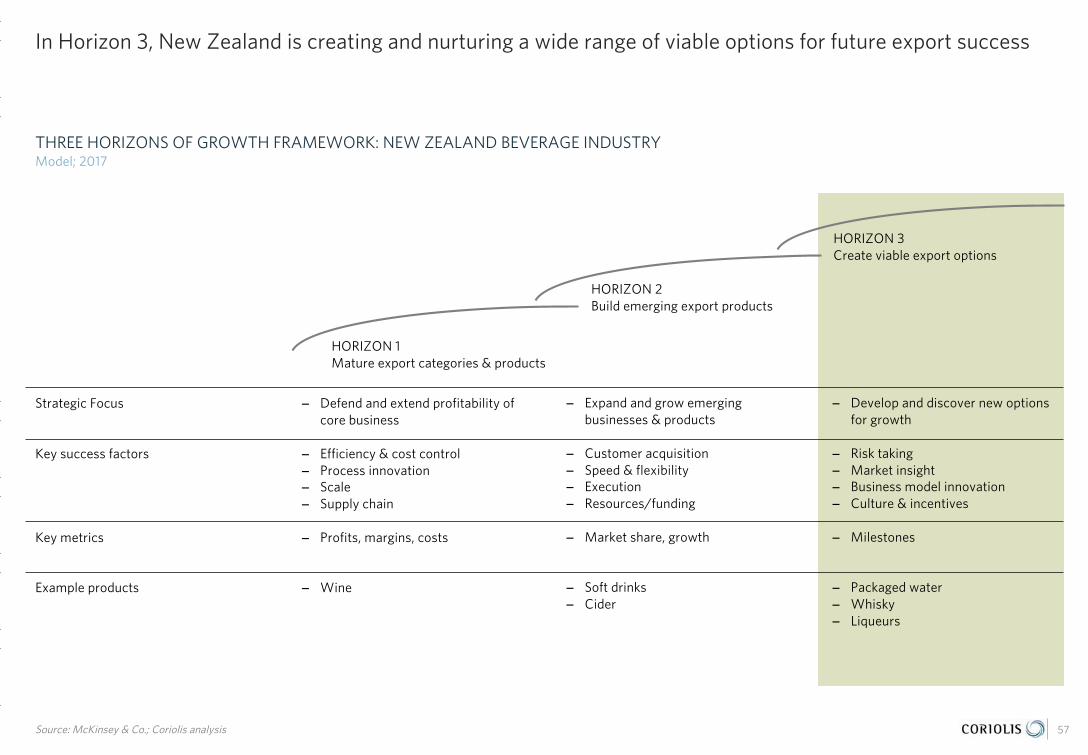

- Beyond its mature core export products (Horizon 1), New Zealand has both a strong range of emerging export stars (Horizon 2) and continues to innovate and produce new, viable export options (Horizon 3)

HORIZON 2: EMERGING EXPORT STARS

- In Horizon 2, New Zealand is building a range of emerging export products

- Two beverage products emerge as “growth stars” – cider and other flavoured beverages – from an evaluation of ten years of product-level trade growth

- Cider exports are growing and the product leverages New Zealand’s strengths in apples and other fruit; performance of peers suggest stronger growth is possible in this rapidly developing category

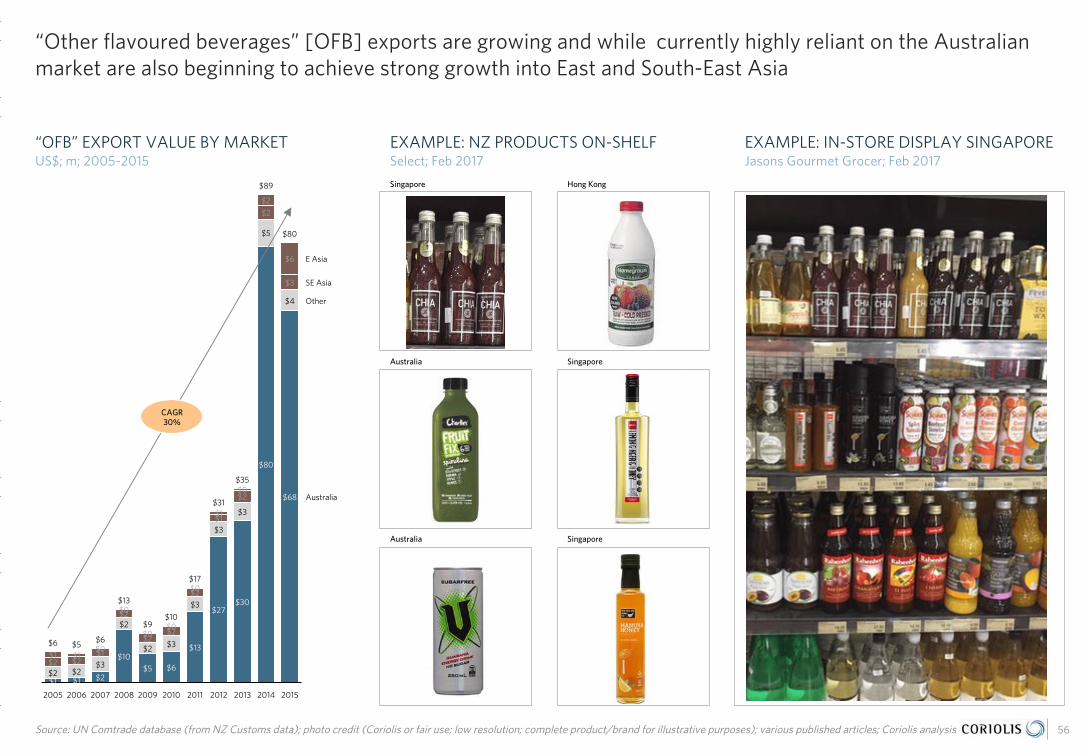

- “Other flavoured beverages” [OFB] exports are growing and while currently highly reliant on the Australian market are also beginning to achieve strong growth into East and South-East Asia

HORIZON 3: NEW, VIABLE OPTIONS

- In Horizon 3, New Zealand is creating and nurturing a wide range of viable options for future export success

- Four broad global consumer mega-trends are driving growth and new product development in the food & beverage industry

- New Zealand beverage products succeeding on-shelf in export markets are aligned with these trends

- These trends drive new product development, through (1) packaging, (2) product, (3) category and (4) channel innovation; success, however, often comes down to implementation and execution

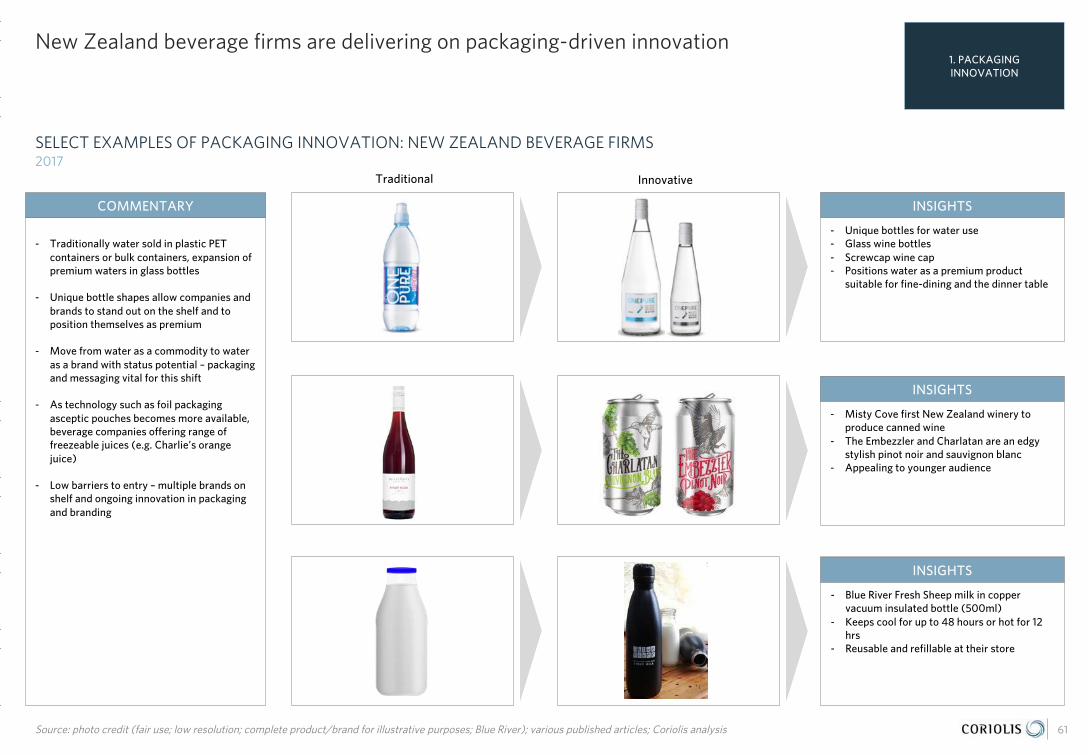

- New Zealand beverage firms are delivering on ppaacckkaaggiinngg-driven innovation

- New Zealand beverage firms are delivering on pprroodduucctt-driven innovation

- New Zealand beverage firms are delivering on ccaatteeggoorryy and cchhaannnneellinnovation

Beyond its mature core (Horizon 1) export products, New Zealand has both a strong range of emerging export stars (Horizon 2) and continues to innovate and produce new, viable export options (Horizon 3)

Source: McKinsey & Co.; Coriolis analysis

THREE HORIZONS OF GROWTH FRAMEWORK: NEW ZEALAND BEVERAGE INDUSTRYModel; 2017

52

− Defend and extend profitability of core business

− Efficiency & cost control− Process innovation− Scale− Supply chain

− Profits, margins, costs

− Wine

HORIZON 1Mature export categories & products

HORIZON 2Build emerging export products

HORIZON 3Create viable export options

Strategic Focus

Key success factors

Key metrics

Example products

− Expand and grow emerging businesses & products

− Customer acquisition− Speed & flexibility− Execution− Resources/funding

− Market share, growth

− Soft drinks− Cider

− Develop and discover new options for growth

− Risk taking− Market insight− Business model innovation− Culture & incentives

− Milestones

− Packaged water− Whisky− Liqueurs

FOCUS OF THIS SECTION

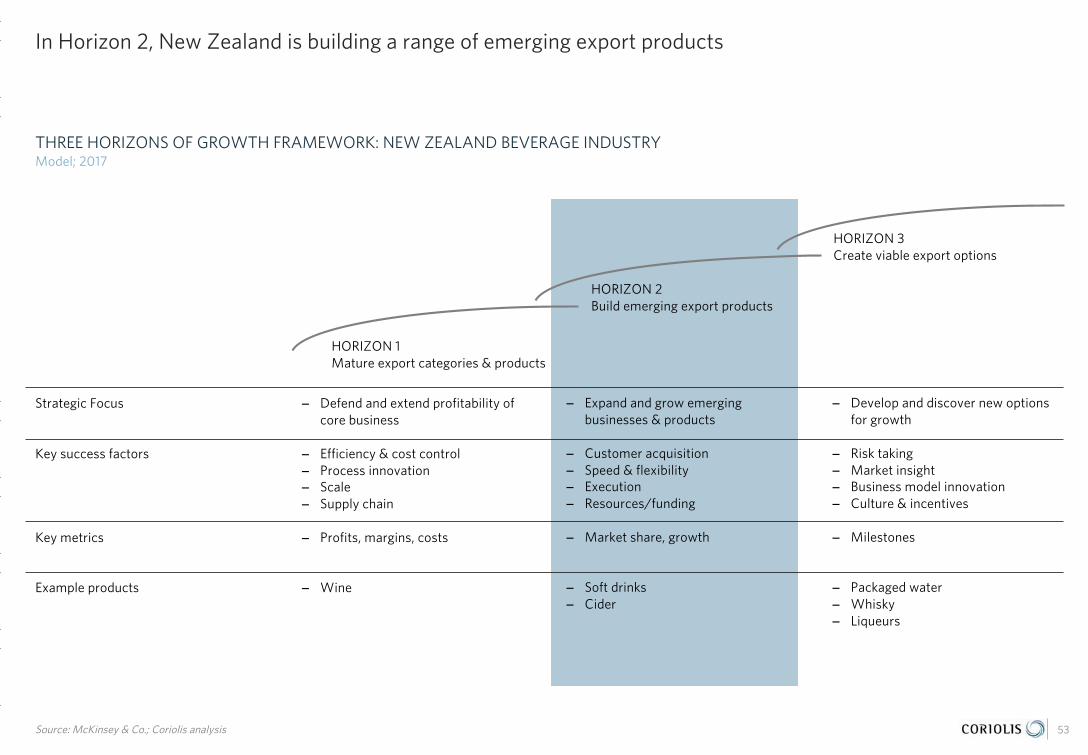

In Horizon 2, New Zealand is building a range of emerging export products

Source: McKinsey & Co.; Coriolis analysis

THREE HORIZONS OF GROWTH FRAMEWORK: NEW ZEALAND BEVERAGE INDUSTRYModel; 2017

53

Strategic Focus

Key success factors

Key metrics

Example products

HORIZON 1Mature export categories & products

HORIZON 2Build emerging export products

HORIZON 3Create viable export options

− Defend and extend profitability of core business

− Efficiency & cost control− Process innovation− Scale− Supply chain

− Profits, margins, costs

− Wine

− Expand and grow emerging businesses & products

− Customer acquisition− Speed & flexibility− Execution− Resources/funding

− Market share, growth

− Soft drinks− Cider

− Develop and discover new options for growth

− Risk taking− Market insight− Business model innovation− Culture & incentives

− Milestones

− Packaged water− Whisky− Liqueurs

Bubble size is proportional to export value in 2015; a bubble this size is

US$1b

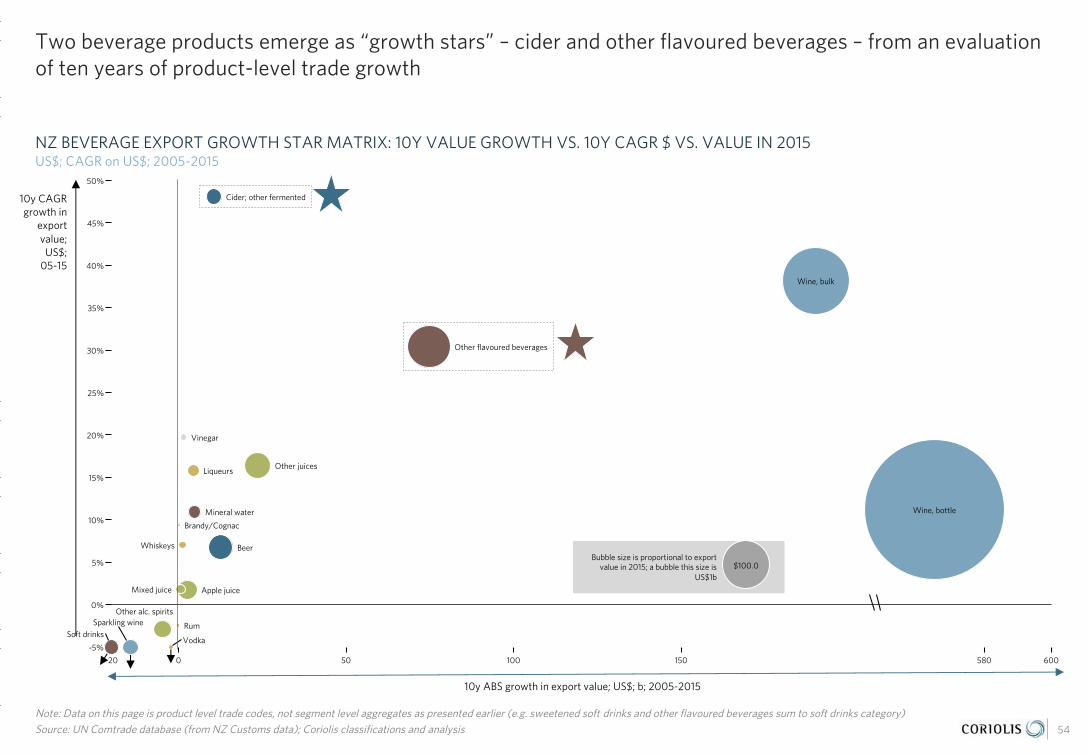

Two beverage products emerge as “growth stars” – cider and other flavoured beverages – from an evaluation of ten years of product-level trade growth

Note: Data on this page is product level trade codes, not segment level aggregates as presented earlier (e.g. sweetened soft drinks and other flavoured beverages sum to soft drinks category) Source: UN Comtrade database (from NZ Customs data); Coriolis classifications and analysis

NZ BEVERAGE EXPORT GROWTH STAR MATRIX: 10Y VALUE GROWTH VS. 10Y CAGR $ VS. VALUE IN 2015US$; CAGR on US$; 2005-2015

54

-20

5%

0

0%

100 580150

-5%

50 600

30%

25%

20%

35%

50%

45%

40%

15%

10%

$100.0

Liqueurs

Whiskeys

Other alc. spirits

Vodka

Wine, bulk

Wine, bottle

Cider; other fermented

Brandy/Cognac

Sparkling wineSoft drinks

Rum

Beer

Vinegar

Mineral water

Mixed juice Apple juice

Other flavoured beverages

Other juices

10y ABS growth in export value; US$; b; 2005-2015

10y CAGR growth in

export value;

US$; 05-15

Cider exports are growing and the product leverages New Zealand’s strengths in apples and other fruit; performance of peers suggest stronger growth is possible in this rapidly developing category