Investor Presentations2.q4cdn.com/.../Investor-Presentation-Updated_2017-9-12.pdfability to recruit...

28

September 2017 Investor Presentation

Transcript of Investor Presentations2.q4cdn.com/.../Investor-Presentation-Updated_2017-9-12.pdfability to recruit...

September 2017

Investor Presentation

2

Forward-Looking Statements

This presentation includes “forward-looking statements” within the meaning of the “safe harbor” provisions of the United States Private Securities Litigation Reform Act

of 1995. Forward-looking statements may be identified by the use of words such as “believe,” “intend,” “expect,” “estimate,” “plan,” “outlook,” “project” and other

similar words and expressions that predict or indicate future events or trends that are not statements of historical matters. These forward-looking statements include

statements regarding the Company’s optimism for agent recruitment, investment, acquisitions (including the integration of regional acquisitions), Motto Mortgage, and

improving housing conditions; the factors working to continue the Company’s momentum; the Company’s channels for long-term organic growth; the productivity of the

agent network; the focus on growing the highest quality real estate network in the world; and consistent execution of the Company’s plan and continued success; as well

as other statements regarding the Company’s strategic and operational plans and business models. Forward-looking statements should not be read as a guarantee of

future performance or results, and will not necessarily be accurate indications of the times at, or by, which such performance or results will be achieved. Forward-looking

statements are based on information available at the time those statements are made and/or management’s good faith belief as of that time with respect to future events,

and are subject to risks and uncertainties that could cause actual performance or results to differ materially from those expressed in or suggested by the forward-looking

statements. Such risks and uncertainties include, without limitation, (1) changes in business and economic activity in general, (2) changes in the real estate market,

including changes due to interest rates and availability of financing, (3) the Company’s ability to attract and retain quality franchisees, (4) the Company’s franchisees’

ability to recruit and retain real estate agents and mortgage loan originators, (5) changes in laws and regulations that may affect the Company’s business or the real

estate market, (6) failure to maintain, protect and enhance the RE/MAX and Motto Mortgage brands, (7) fluctuations in foreign currency exchange rates, as well as those

risks and uncertainties described in the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations”

in the most recent Annual Report on Form 10-K filed and Quarterly Report on Form 10-Q with the Securities and Exchange Commission (“SEC”) and similar disclosures

in subsequent periodic and current reports filed with the SEC, which are available on the investor relations page of the Company’s website at www.remax.com and on the

SEC website at www.sec.gov. Readers are cautioned not to place undue reliance on forward-looking statements, which speak only as of the date on which they are

made. Except as required by law, the Company does not intend, and undertakes no duty, to update this information to reflect future events or circumstances.

3

Why Invest in RE/MAX Today?

Organic Growth Catalysts Return of Capital

Shareholder Return Driven By

Stable recurring revenue

High margin & Strong

Free Cash Flow

Driven by:

1) Agent growth

2) Franchise sales

3) Motto Mortgage

4) Steadily improving

housing market

Independent region

acquisitions

Reinvest in the business

Other acquisitions within

our core competencies of

franchising and real

estate

Committed to returning

capital through dividend

payments over time

Dividend metrics:

– ~30% of FCF in 20161

– ~1.2% current yield2

FCF Fuels Catalysts and Return of Capital to Create Shareholder Value

1Free Cash Flow (“FCF”) = Operating Cash Flow – Capital Expenditures; $18M 2016 quarterly dividend payments / $60M 2016 FCF = 30%; see Appendix for reconciliationof Non-GAAP measures2Yield based on regular quarterly dividend of $0.18 and a stock price of $61.00 per share as of September 11, 2017

4

Unique product or service offering

Brand name and market share

Training and productivity tools

Group purchasing power

Hallmarks of a Successful Franchise Business

Key Success Factors of

FranchisorsSuccessful Franchisors

5

RE/MAX is a Premium Franchisor

Nobody sells more Real Estate than

RE/MAX1

100% franchised business, delivering

the full economic benefits of the model

Dual-brand franchisor, focused on our

core businesses

Among the best-in-class franchisor

operating margins

1As measured by residential transaction sides

6

Owned & operated by brokerage

30-40% of commission goes to broker

Commission rate typically determined

by brokerage, not agent

Lack of autonomy within brokerage

Marketing dictated by brokerage

100% franchised

Recommended 95% agent commission

Ability for agent to set commission

rates with sellers in many cases

Entrepreneurially driven agents

Multiple support channels: brand,

marketing & training

Revenue Driven by Commission Revenue Driven by Agent Count

Unique and Effective Agent-Centric RE/MAX Model

Traditional Brokerage The RE/MAX Model

7

Transactions Per

Agent

(Large brokerages only)1

U.S. Residential

Transaction Sides2

Brand Awareness

(unaided) 3

Countries and

Territories

Offices

Worldwide

Agents

Worldwide

17.2 1 million+ 27.6% 100+ 7,343 111,915

6.8 977,603 7.3% 16 800 154,979

8.4 727,415 14.2% 49 3,000 88,400

8.2 420,184 19.7% 77 7,300 110,800

8.2 128,812 1.1% 31 2,300 37,900

6.5 111,950 2.1% 66 850 20,300

6.9 70,980 0.6% 3 300 10,900

9.2 Not Released 4.3% 1 1,240 42,747

RE/MAX Agents at Large Brokerages on Average Outsell Competing Agents More Than 2 to 1

Ranking RE/MAX vs. Other National Real Estate Franchise Brands

Realogy Brand

Data is full-year or as of year-end 2016, as applicable. Except as noted, Coldwell Banker, Century 21, ERA, Sotheby’s and Better Homes and Gardens data is as reported by RealogyCorporation on SEC Form 10-K, Annual Report for 2016; Keller Williams, and Berkshire Hathaway HomeServices data is from company websites and industry reports1Transaction sides per agent calculated by RE/MAX based on 2017 REAL Trends 500 data, citing 2016 transaction sides for the 1,705 largest participating U.S. brokerages. ColdwellBanker includes NRT. Berkshire does not include HomeServices of America.²Keller Williams reports all transaction sides and does not itemize U.S. residential transactions.³MMR Strategy Group study of unaided awareness among buyers, sellers, and those planning to buy or sell; asked, when they think of real estate brands, which ones come to mind?

8

Among Highest Franchisor Adjusted EBITDA Margins1,2

57% 54%

27%

20%17%

15%12%

10%

Franchisors Real Estate Brokerages

1Adjusted EBITDA and Adjusted EBITDA margin are Non-GAAP measures. See appendix for definitions and reconciliations of RE/MAX Non-GAAP measures.

Other companies may calculate this measure differently so these measures may not be comparable. This chart is for illustrative purposes only. Calculations

use financial statements from company public filings.2Choice Hotels and Domino’s do not report Adjusted EBITDA therefore EBITDA has been used for the calculation of the margin

Full-year 2016

9

54%

18%

27%

Unmatched Global Footprint

June 30, 2017

Canada21,053 Agents

Outside the U.S.

and Canada31,968 Agents

U.S.63,249 Agents

RE/MAX Regional or Franchise Presence

RE/MAX Global Footprint Agents by Geography

The RE/MAX brand spans over 100 countries and territories

June 30, 2017

10

87,47689,008

93,228

98,010

104,826

111,915

116,270

2011 2012 2013 2014 2015 2016 Q2 2017

Global Agent Network Growing

+28,794 from 2011

through Q2 2017

Strongest full-year

agent gain in 2016

since 2006

Consistent organic

agent count growth for

the last five years

Total Network Agent Count

11

Motto Mortgage is a mortgage brokerage franchisor

Franchises will be independently owned and operated

Motto Mortgage is not a lender and will not underwrite loans

Offers potential homebuyers the opportunity to find both real estate agents and

independent Motto Mortgage loan originators in offices in one location

Motto Mortgage loan originators will access a variety of quality loan options from

multiple leading wholesalers

Ward Morrison will lead Motto Mortgage with an operational team which will scale as

Motto grows

Motto Mortgage franchises will ultimately be available for purchase by select

qualified brokerage owners in the real estate industry outside of RE/MAX

Motto Mortgage Fact Sheet

12

Motto Mortgage UpdateFocused on Enabling the Success of Initial Group of Franchisees

▪ Initial group of franchisees are

operational

▪ Focused on enabling success of

initial franchisees, who should

serve as concept validators

▪ Major marketing events

scheduled for the second half of

2017

Revenue ramp timeline: it should take ~14-17 months after a sale

for a franchisee to ramp to paying the full set of monthly fees

Operational update Financial Update

▪ Expect to sell tens of franchises

in 2017

▪ Expect 2017 Motto revenue in

the low single-digit millions of

dollars

▪ Expect 2017 Motto expenses to

exceed related revenue resulting

in a net investment

13

Reacquiring Independent Regions Increases Revenue Per Agent by ~$1,700

64% of Agents in the U.S. & Canada are in

Company-owned Regions1

Washington

Oregon

Idaho

Montana

California

Hawaii

ColoradoUtah

Wyoming

SouthDakota

NorthDakota

Texas

Pennsylvania

Delaware

Florida

North Carolina

South Carolina

BritishColumbia

Alberta

Saskatchewan

Manitoba

Yukon

U.S./Canada Overview1

Company-owned Regions

– 18 regions

– 54,145 agents

Independent Regions

– 10 regions

– 30,157 agents

Average Annual Revenue per

Agent

– Company-owned regions:

~$2,500

– Independent regions:

~$800

Company-owned Regions

Independent Regions

Nevada

Arizona New Mexico

Maryland

Virginia

WestVirginia

Missouri

Illinois

Ohio

Northwest

TerritoriesNunavut

1Agent counts are as of June 30, 2017 and average revenue to RE/MAX, LLC per agent is for the year ended December 31, 2016

New York

Alaska

New Jersey

Georgia

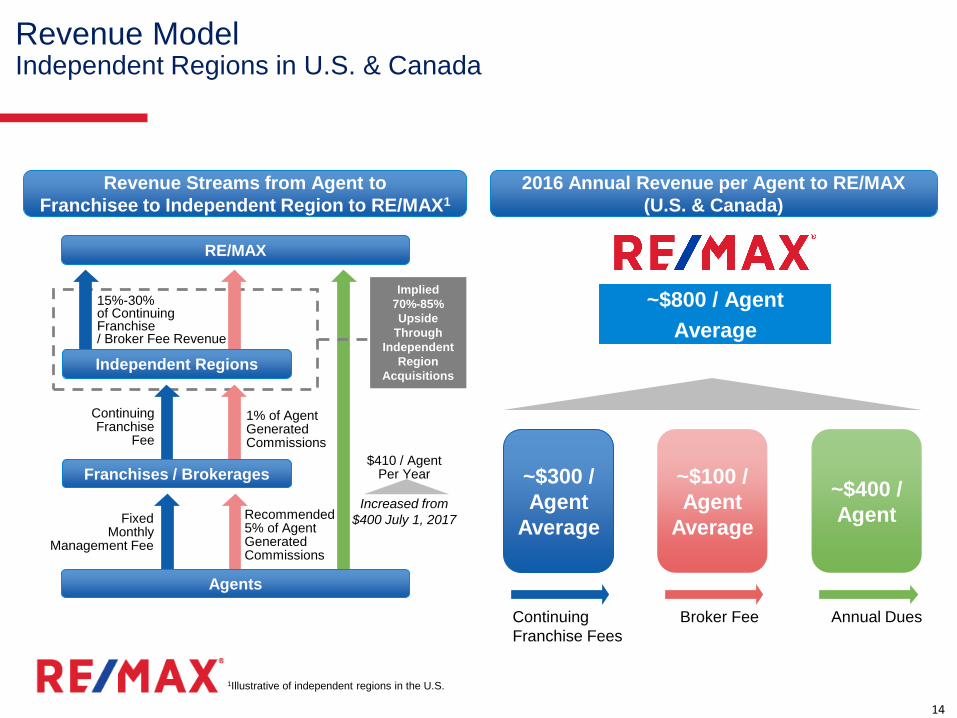

14

Agents

RE/MAX

Franchises / Brokerages

Independent Regions

$410 / AgentPer Year

Recommended5% of AgentGeneratedCommissions

Fixed Monthly

Management Fee

ContinuingFranchise

Fee

1% of Agent GeneratedCommissions

15%-30%of Continuing Franchise / Broker Fee Revenue

Implied

70%-85%

Upside

Through

Independent

Region

Acquisitions

~$300 /

Agent

Average

~$100 /

Agent

Average

~$400 /

Agent

Revenue Model Independent Regions in U.S. & Canada

~$800 / Agent

Average

Revenue Streams from Agent to

Franchisee to Independent Region to RE/MAX1

2016 Annual Revenue per Agent to RE/MAX

(U.S. & Canada)

Annual DuesBroker FeeContinuing

Franchise Fees

1Illustrative of independent regions in the U.S.

Increased from

$400 July 1, 2017

15

~$2,500 / Agent

Average

Revenue ModelCompany-owned Regions in U.S. & Canada

~$1,400 /

Agent

Average

~$700 /

Agent

Average

~$400 /

Agent

RE/MAX

Franchises / Brokerages

$410 / AgentPer Year

Recommended5% of AgentGeneratedCommissions

$128 / Agent Per Month

1% of Agent GeneratedCommissions

Agents

Revenue Streams from Agent to

Franchisee to RE/MAX1

2016 Annual Revenue per Agent to RE/MAX

(U.S. & Canada)

Annual DuesBroker FeeContinuing

Franchise Fees

Increased from

$123 July 1, 2016

Fixed Monthly

Management Fee

1Illustrative of company-owned regions in the U.S.

Increased from

$400 July 1, 2017

16

46%

21%

14%

19%

83%

13%

4%

Revenue by Stream and Geographic AreaGrowing Recurring Revenue Base

Revenue Streams Revenue by Geographic Area

U.S.

Canada

Outside the U.S.

and Canada

Recurring fees and dues (i.e. Continuing

Franchise Fees and Annual Dues) accounted for

65% of revenue in 2016

~96% of 2016 revenue

was generated in the U.S.

and Canada

Franchise Sales & Other

Franchise Revenue

Broker Fees

Annual Dues

Continuing

Franchise Fees

17

$43$49 $53

2014 2015 2016

$80

$90$95

2014 2015 2016

1Adjusted EBITDA and Adjusted Net Income are Non-GAAP measures. See appendix for definitions and reconciliations of Non-GAAP measures.

Annual Financial PerformanceGenerating High Margins

$171$177 $176

2014 2015 2016

Revenue Adjusted EBITDA1 Adjusted Net Income1

47%

($M) ($M) ($M)

Stable, High Adjusted

EBITDA Margins51% 54%

18

$1.8 $2.4 $2.4 $2.4 $2.4

2017 2018 2019 2020 2021 Thereafter

Maturities of Debt1 Balance Sheet

▪ Credit facility of $235.0 million plus $10.0 million

revolving credit facility

▪ Covenant light deal

▪ Variable Rate: LIBOR + 275bps with 0.75% floor

▪ $229.9 million in term loans1 and no revolving

loans outstanding

▪ Cash balance of $70.3 million on June 30, 2017

▪ Total Debt / Adjusted EBITDA of 2.3x2

▪ Net Debt / Adjusted EBITDA of 1.6x3

$222.7

Low Leverage to Support Strategy

1Net of unamortized debt discount and debt issuance costs2Based on twelve months ended June 30, 2017, Adjusted EBITDA of $100.1M and total debt of $229.9M, net of unamortized debt discount and debt issuance costs3Based on twelve months ended June 30, 2017, Adjusted EBITDA of $100.1M and net debt of $159.6M, net of unamortized debt discount, debt issuance costs and

cash balance at June 30, 2017

19

1Free Cash Flow = Operating Cash Flow – Capital Expenditures2Free Cash Flow after Distributions to RIHI = Free Cash Flow – Tax and other discretionary non-dividend distributions paid to RIHI to enable RIHI to satisfy its

income tax obligations3Unencumbered Cash Generated = Free Cash Flow after Distributions to RIHI – Quarterly debt principal payments – Annual excess cash flow payment on debt, see Appendix for reconciliation of Non-GAAP measures

$64$60

$50

$35

Operating CashFlow

Free CashFlow

Free CashFlow after

Distributionsto RIHI

UnencumberedCash Generated

Full-Year 2016

Acquire independent regions

Reinvest in the business

Other acquisitions

Return of capital

1

2

3

4

1

2

3

63% 37%As % of

Adj. EBITDA

Capital Allocation Priorities

52%

$’s in Millions

Cash Flow Generation Fuels Capital Allocation Strategy

Strong Annual Adjusted EBITDA Conversion to FCF

20

Leading Real Estate Franchisor

#1 Real Estate Franchise Brand1 with Unmatched

Global Footprint

Highly Productive Network of More Than 115,000

Agents

Agent-Centric Model is Different and Better

Stable, Recurring Fee-Based Revenue Model with Strong

Margins and Cash Flow

100% Franchised Business

Multiple Drivers of Shareholder Value Creation

1Source: MMR Strategy Group survey of unaided brand awareness in the U.S. and Canada

Each Office Independently Owned and Operated. 17_191524

22

200

250

300

350

400

450

500

550

600

650

Positive Forecasts for 2016 & 2017Gradual Expansion of the Housing Market Continues

1Source: NAR (National Association of Realtors) – Existing Home Sales, numbers presented are not seasonally adjusted; June 2013 through June 20172Source: NAR (National Association of Realtors) – U.S. Economic Outlook, July 20173Source: Fannie Mae – Economic and Strategic Research – Housing Forecast, July 20174Source: NAHB (National Association of Home Builders) – Housing and Interest Rate Forecast June 2017

Monthly Existing Home Sales1 (Thousands) Annual Existing Home Sales2,3 (M)

Housing Starts - Single Family3,4 (Thousands)Home Price Appreciation2,3 (YoY)

5.3

5.5

5.65.7

5.3

5.5

5.6

5.8

2015 2016 2017e 2018e

Fannie Mae NAR

5.9%6.2%

5.8%

4.7%

6.8%

5.1% 5.1%

3.5%

2015 2016 2017e 2018e

Fannie Mae NAR

713 782

831

945

713 784

855

961

2015 2016 2017e 2018e

Fannie Mae NAHB

23

Mortgage Finance ForecastsPurchase Originations Expected to Grow, Rates to Rise Slowly

1Source: Mortgage Bankers Association – MBA Mortgage Finance Forecast July 2017

Loan Originations1 Mortgage & Interest Rates1

3.6%4.2%

4.9%5.3%

1.8%

2.5%3.0%

3.5%

2016 2017e 2018e 2019e

30-Year Fixed 10-Year Treasury

$990

$1,089$1,178

$1,245

$901

$538

$410 $395

2016 2017e 2018e 2019e

Purchase Refinance

24

(Unaudited) (Amounts in thousands)

RE/MAX Holdings, Inc. Adjusted EBITDA Reconciliation to Net Income (Reflects RE/MAX Holdings with 100% ownership of RMCO, LLC)

Net income $ 47,810 $ 51,350 $ 43,979

Depreciation and amortization 16,094 15,124 15,316

Interest expense 8,596 10,413 9,295

Interest income (160) (178) (313)

Provision for income taxes 15,273 12,030 9,948

Gain on sale or disposition of assets and sublease (1) (171) (3,650) (340)

Loss on early extinguishment of debt and debt modif ication expense (2) 2,893 94 178

Equity-based compensation expense 2,330 1,453 2,002

Public offering related expenses (3) 193 1,097 —

Acquisition related expenses (4) 1,899 2,750 313

Adjusted EBITDA (5) $ 94,757 $ 90,483 $ 80,378

Adjusted EBITDA margin (5) 53.7 % 51.2 % 47.0 %

2014

Year Ended December 31,

2016 2015

(1) Represents gains on the sale or disposition of assets as well as the gains on the sublease of a portion of the Company’s corporate headquarters office building.

(2) Represents losses incurred on early extinguishment of debt on the Company’s credit facility for each full-year period presented as well as costs associated with the

refinancing of the Company’s credit facility during the year ended December 31, 2016.

(3) Represents costs incurred for compliance services performed in connection with the issuance of shares of Class A common stock as a result of the RIHI, Inc. (“RIHI”)

redemption of 5,175,000 common units in RMCO during the fourth quarter of 2015 (the “Secondary Offering”).

(4) Acquisition-related expenses include fees incurred in connection with the Company’s acquisitions of certain assets of HBN, Inc. (“HBN”) and Tails, Inc. (“Tails”) in October

2013, the acquisition of six Independent Regions (New York, Alaska, New Jersey, Georgia, Kentucky/Tennessee and Southern Ohio, collectively, the (“2016 Acquired

Regions”) and the acquisition of Full House Mortgage Connection, Inc., now known as Motto Mortgage (“Motto”). Costs include legal, accounting and advisory fees as well

as consulting fees for integration services.

(5) Non-GAAP measure. See the end of this presentation for definitions of Non-GAAP measures.

25

(Unaudited) (Amounts in thousands)

RE/MAX Holdings, Inc. Adjusted Net Income and Adjusted EPS Reconciliation to Net Income (Reflects RE/MAX Holdings with 100% ownership of RMCO, LLC)

Net income $ 47,810 $ 51,350 $ 43,979

Amortization of franchise agreements 14,590 13,566 13,566

Provision for income taxes 15,273 12,030 9,948

Add-backs:

Gain on sale or disposition of assets and sublease (1) (171) (3,650) (340)

Loss on early extinguishment of debt and debt modif ication expense (2) 2,893 94 178

Equity-based compensation 2,330 1,453 2,002

Public offering related expenses (3) 193 1,097 —

Acquisition related expenses (4) 1,899 2,750 313

Adjusted pre-tax net income 84,817 78,690 69,646

Less: Provision for income taxes at 38% (32,230) (29,902) (26,465)

Adjusted net income (5) $ 52,587 $ 48,788 $ 43,181

Total basic pro forma shares outstanding 30,188,341 29,925,446 29,345,764

Total diluted pro forma shares outstanding 30,237,368 30,083,609 29,976,577

Adjusted net income basic earnings per share (5) $ 1.74 $ 1.63 $ 1.47

Adjusted net income diluted earnings per share (5) $ 1.74 $ 1.62 $ 1.44

2016 2015 2014

Year Ended December 31,

(1) Represents gains on the sale or disposition of assets as well as the gains on the sublease of a portion of the Company’s corporate headquarters office building.

(2) Represents losses incurred on early extinguishment of debt on the Company’s credit facility for each full-year period presented as well as costs associated with the

refinancing of the Company’s credit facility during the year ended December 31, 2016.

(3) Represents costs incurred for compliance services performed in connection with the Secondary Offering.

(4) Acquisition-related expenses include fees incurred in connection with the Company’s acquisitions of certain assets of HBN and Tails in October 2013, the 2016 Acquired

Regions and the acquisition of Motto. Costs include legal, accounting and advisory fees as well as consulting fees for integration services.

(5) Non-GAAP measure. See the end of this presentation for definitions of Non-GAAP measures.

26

RE/MAX Holdings, Inc. Free Cash Flow and Unencumbered Cash Generation

(1) Non-GAAP measure. See the end of this presentation for definitions of non-GAAP measures.

Cash flow from operations $ 64,379 $ 77,358

Less: Capital expenditures (4,395) (3,546)

Free cash flow (1) 59,984 73,812

Free cash flow 59,984 73,812

Less: Tax and Other non-dividend discretionary distributions to RIHI (10,391) (7,358)

Free cash flow after tax and non-dividend discretionary distributions to RIHI (1) 49,593 66,454

Free cash flow after tax and non-dividend discretionary distributions to RIHI 49,593 66,454

Less: Quarterly debt principal payments (2,081) (2,080)

Less: Annual excess cash flow (ECF) payment (12,727) (7,320)

Unencumbered cash generated (1) $ 34,785 $ 57,054

Summary

Cash flow from operations $ 64,379 $ 77,358

Free cash flow $ 59,984 $ 73,812

Free cash flow after tax and non-dividend discretionary distributions to RIHI $ 49,593 $ 66,454

Unencumbered cash generated $ 34,785 $ 57,054

Adjusted EBITDA $ 94,647 $ 91,401

Free cash flow as % of Adjusted EBITDA 63.4% 80.8%

Free cash flow less distributions to RIHI as % of Adjusted EBITDA 52.4% 72.7%

Unencumbered cash generated as % of Adjusted EBITDA 36.8% 62.4%

Year Ended December 31,

2016 2015

27

Non-GAAP Financial Measures

The SEC has adopted rules to regulate the use in filings with the SEC and in public disclosures of financial measures that are not in accordance with U.S. GAAP, such as Adjusted EBITDA

and the ratios related thereto, Adjusted net income, Adjusted basic and diluted earnings per share (Adjusted EPS) and Free cash flow. These measures are derived on the basis of

methodologies other than in accordance with U.S. GAAP.

The Company calculates Adjusted EBITDA as EBITDA (consolidated net income before depreciation and amortization, interest expense, interest income and the provision for income taxes,

each of which is presented in the unaudited condensed consolidated financial statements included in the Quarterly Report on Form 10-Q), adjusted for the impact of the following items that

are either non-cash or the Company does not consider representative of its ongoing operating performance: loss or gain on sale or disposition of assets and sublease, loss on early

extinguishment of debt, professional fees and certain expenses incurred in connection with the Secondary Offering, acquisition-related expenses and equity-based compensation expense.

Adjusted EBITDA margin represents Adjusted EBITDA as a percentage of revenue.

During the first quarter of 2017, the Company revised its definitions of Adjusted EBITDA and Adjusted EBITDA margin to better reflect the performance of the business and comply with SEC

guidance. The Company now adjusts for equity-based compensation expense and no longer adjusts for straight-line rent expense and severance-related expenses. Adjusted EBITDA and

Adjusted EBITDA margin were revised in prior periods to reflect this change for consistency in presentation.

Because Adjusted EBITDA and Adjusted EBITDA margin omit certain non-cash items and other non-recurring cash charges or other items, the Company believes that each measure is less

susceptible to variances that affect its operating performance resulting from depreciation, amortization and other non-cash and non-recurring cash charges or other items. The Company

presents Adjusted EBITDA and the related Adjusted EBITDA margin because the Company believes they are useful as supplemental measures in evaluating the performance of its operating

businesses and provides greater transparency into the Company’s results of operations. The Company’s management uses Adjusted EBITDA and Adjusted EBITDA margin as factors in

evaluating the performance of the business.

Adjusted EBITDA and Adjusted EBITDA margin have limitations as analytical tools, and you should not consider these measures in isolation or as a substitute for analyzing the Company’s

results as reported under U.S. GAAP. Some of these limitations are:

• these measures do not reflect changes in, or cash requirements for, the Company’s working capital needs;

• these measures do not reflect the Company’s interest expense, or the cash requirements necessary to service interest or principal payments on its debt;

• these measures do not reflect the Company’s income tax expense or the cash requirements to pay its taxes;

• these measures do not reflect the cash requirements to pay dividends to stockholders of the Company’s Class A common stock and tax and other cash distributions to its non-controlling

unitholders;

• these measures do not reflect the cash requirements to pay RIHI Inc. and Oberndorf pursuant to the tax receivable agreements;

• although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often require replacement in the future, and these measures do not reflect

any cash requirements for such replacements;

• although equity-based compensation is a non-cash charge, the issuance of equity-based awards may have a dilutive impact on earnings per share; and

• other companies may calculate these measures differently so similarly named measures may not be comparable.

The Company’s Adjusted EBITDA margin guidance does not include certain charges and costs. The adjustments to EBITDA margin in future periods are generally expected to be similar to

the kinds of charges and costs excluded from Adjusted EBITDA margin in prior quarters, such as gain on sale or disposition of assets and sublease and acquisition related expenses, among

others. The exclusion of these charges and costs in future periods will have a significant impact on the Company’s Adjusted EBITDA margin. The Company is not able to provide a

reconciliation of the Company’s Non-GAAP financial guidance to the corresponding U.S. GAAP measures without unreasonable effort because of the uncertainty and variability of the nature

and amount of these future charges and costs.

28

Adjusted net income is calculated as Net income attributable to RE/MAX Holdings, assuming the full exchange of all outstanding non-controlling interests for shares of Class A common

stock as of the beginning of the period (and the related increase to the provision for income taxes after such exchange), plus primarily non-cash items and other items that management does

not consider to be useful in assessing the Company’s operating performance (e.g., amortization of acquired intangible assets, gain on sale or disposition of assets and sub-lease, loss on

early debt extinguishment, public-offering related expenses, acquisition-related expenses and equity-based compensation expense).

Adjusted basic and diluted earnings per share (Adjusted EPS) are calculated as Adjusted net income (as defined above) divided by pro forma (assuming the full exchange of all

outstanding non-controlling interests) basic and diluted weighted average shares, as applicable.

When used in conjunction with GAAP financial measures, Adjusted net income and Adjusted EPS are supplemental measures of operating performance that management believes are

useful measures to evaluate the Company’s performance relative to the performance of its competitors as well as performance period over period. By assuming the full exchange of all

outstanding non-controlling interests, management believes these measures:

• facilitate comparisons with other companies that do not have a low effective tax rate driven by a non-controlling interest on a pass-through entity;

• facilitate period over period comparisons because they eliminate the effect of changes in Net income attributable to RE/MAX Holdings, Inc. driven by increases in its ownership of RMCO,

LLC, which are unrelated to the Company’s operating performance; and

• eliminate primarily non-cash and other items that management does not consider to be useful in assessing the Company’s operating performance.

Free cash flow is calculated as cash flows from operations less capital expenditures, both as reported under GAAP, and quantifies how much cash a company has to pursue opportunities

that enhance shareholder value. The Company believes free cash flow is useful to investors as a supplemental measure as it calculates the cash flow available for working capital needs, re-

investment opportunities, potential independent region and strategic acquisitions, dividend payments or other strategic uses of cash.

Free cash flow after tax and non-dividend distributions to RIHI is calculated as free cash flow less tax and other non-dividend distributions paid to RIHI (the non-controlling interest

holder) to enable RIHI to satisfy its income tax obligations. Similar payments would be made by the Company directly to federal and state taxing authorities as a component of the Company’s

consolidated provision for income taxes if a full exchange of non-controlling interests occurred in the future. As a result and given the significance of the Company’s ongoing tax and non-

dividend distribution obligations to its non-controlling interest, free cash flow after tax and non-dividend distributions, when used in conjunction with GAAP financial measures, provides a

meaningful view of cash flow available to the Company to pursue opportunities that enhance shareholder value.

Unencumbered cash generated is calculated as free cash flow after tax and non-dividend distributions to RIHI less quarterly debt principal payments less annual excess cash flow payment

on debt, as applicable. Given the significance of the Company’s excess cash flow payment on debt, when applicable, unencumbered cash generated, when used in conjunction with GAAP

financial measures, provides a meaningful view of the cash flow available to the Company to pursue opportunities that enhance shareholder value after considering its debt service

obligations.

Non-GAAP Financial Measures (continued)