Investor Presentation Q2 2015 Results - zonebourse.com A/S... · Investor Presentation Q2 2015...

24

Investor Presentation Q2 2015 Results 27 August 2015

Transcript of Investor Presentation Q2 2015 Results - zonebourse.com A/S... · Investor Presentation Q2 2015...

Investor PresentationQ2 2015 Results

27 August 2015

Forward-looking statements

2

This presentation contains forward-looking statements, including, but not limited to, the statements and expectations contained in the “Outlook” section of this presentation. Statements herein, other than statements of historical fact, regarding future events or prospects, are forward-looking statements. The words ‘‘may’’, “will”, “should”, ‘‘expect’’, ‘‘anticipate’’, ‘‘believe’’, ‘‘estimate’’, ‘‘plan’’, "predict," ‘‘intend’ or variations of these words, as well as other statements regarding matters that are not historical fact or regarding future events or prospects, constitute forward-looking statements. ISS has based these forward-looking statements on its current views with respect to future events and financial performance. These views involve a number of risks and uncertainties, which could cause actual results to differ materially from those predicted in the forward-looking statements and from the past performance of ISS. Although ISS believes that the estimates and projections reflected in the forward-looking statements are reasonable, they may prove materially incorrect, and actual results may materially differ, e.g. as the result of risks related to the facility service industry in general or ISS in particular including those described in the Annual Report 2014 of ISS A/S and other information made available by ISS.

As a result, you should not rely on these forward-looking statements. ISS undertakes no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except to the extent required by law.

The Annual Report 2014 of ISS A/S is available at the Group’s website, www.issworld.com.

Agenda

3

• Highlights• Highlights

• Regional Performance• Regional Performance

• Financial Results• Financial Results

• Organisational Structure• Organisational Structure

• Outlook• Outlook

• Q&A• Q&A

REMINDERCapital Markets’ Day

17 September 2015London

12.30 – 17.00 (UK)

All enquiries to Martin Kjær Hansen ([email protected])

Highlights

5

Business Highlights Q2 2015

6

Operating Performance

Integrated Facility Services (IFS)

Emerging Markets

Strategic Initiatives

• Strategic initiatives progressing according to plans• Positive effect on margins continuing• Phase III of procurement initiative being launched• Integration of GS Hall on-track, insourcing of previously sub-contracted services has begun• Change in organisational structure to facilitate alignment across the group and boost customer focus

• Organic growth of 8% and an operating margin of 6.1% (unchanged year-on-year)• Represents 25% of group revenue

• Strong growth in IFS (+10% in local currency) which now represents 33% of group revenue• Significant IFS contract start-ups: Huawei (China) and UBS (UK)• Major IFS contract expansions: Danske Bank (Nordic, Eastern Europe) and DSB (Denmark)• Notable IFS contract win: Huashan Hospital (China), Healthcare segment (UK)

• Global Corporate Clients (GCC) revenues +13% in local currency• Start-up of significant Cleaning contract with major financial services customer

• Strong organic growth• Improved operating margin, despite operational challenges in the Netherlands and Brazil• Solid LTM cash conversion• Significantly improved net result

Key IFS Contracts Launched in Q2 2015

7

Future potential • Longer-term potential given scale of Huawei in China and internationally

• Seamless mobilisation thus far• Scope to deliver additional servces• 5 Broadgate will be a showcase building in London and hence

affords ISS the potential to demonstrate our delivery of transformational IFS

Why ISS?

• ISS demonstrated a deep understanding of Huawei’s needs• Customised service offering, delivering Hong Kong service

standards in mainland China• Initial support from ISS Hong Kong with service levels maintained by

local team thereafter

• ISS solution sharply focused on supporting UBS in attracting and retaining employees while enhancing their well-being

• High emphasis placed on transformation, sustainability, safety and security, technology and innovation

Scope

• 3-year contract, starting April 2015• Cleaning, Security, Office Support, Customer Service and Facility

Management provided at a residential campus for up to 3,300 Huawei employees

• c. 320 ISS employees (incl. 36 Hong Kong residents in Year 1)

• 5-year contract• Technical services, Energy management, Cleaning, Waste

management, Pest control, Security, Real Estate services, Client services

• 1.5m sq ft of property (incl. 5 Broadgate), c. 400 ISS employees

Background• Huawei seeking to attract and retain talented employees by

providing comfortable and enjoyable working and living conditions• ISS’ international brand and reputation – together with its leading

position in the Hong Kong market – helped forge the relationship

• UBS seeking a flexible, productive, world class office facilityachieving the highest standards of sustainability

• ISS’ relationship with UBS in Switzerland had illustrated our abilityto deliver ahead of customer expectations

Financial Highlights Q2 2015

8

1. Resilient Organic Growth

Organic growth was 4.8% in Q2 2015 vs. 3.1% in Q1 2015• Western Europe impacted by large contract

launches and selective demand for non-portfolio services (Switzerland and UK)

• Continued strong growth in emerging marketsand the Pacific

• Continued strong growth in IFS• Macroeconomic conditions in certain European

countries remain challenging

3. Strong Cash Conversion(2)2. Improved Operating Margin(1)

Organic Growth (%) Cash Conversion (LTM)LTM Operating Margin (LTM)

0%

1%

2%

3%

4%

5%

6%

7%

Q22011

Q22012

Q22013

Q22014

Q22015

Organic Growth (Q) Organic Growth (LTM)

5.0%5.1%5.2%5.3%5.4%5.5%5.6%5.7%5.8%5.9%6.0%

Q22011

Q22012

Q22013

Q22014

Q22015

Operating Margin (LTM)

Operating margin was 5.3% in Q2 2015 vs. 5.2% in Q2 2014• Positive margin progression across most

regions• Strategic initiatives to improve profitability and

competitiveness continue to progressaccording to plan

• Operational challenges in the Netherlands and Brazil

LTM cash conversion was 99% in Q2 2015 vs. 97% in Q1 2015• Ensuring a strong cash performance remains a

key priortity• Result reflects our efforts to ensure timely

payment for work performed

0%

20%

40%

60%

80%

100%

120%

Q22011

Q22012

Q22013

Q22014

Q22015

Cash Conversion (LTM)

Three key financial priorities

Regional Performance

9

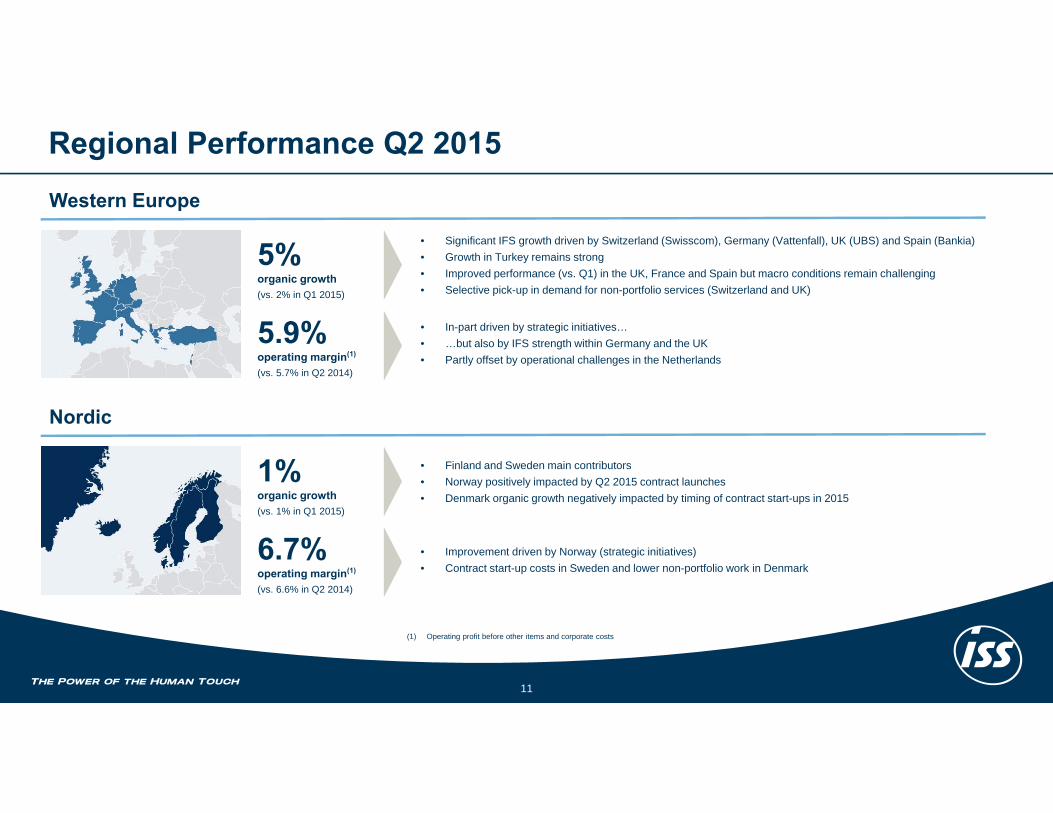

Regional Performance Q2 2015

10

Developed Markets Emerging Markets(1)

75%of Group revenue

43%of Group employees

4%organic growth(vs. 2% in Q1 2015)

6.0%operating margin(2)

(vs. 5.7% in Q2 2014)

25%of Group revenue

57%of Group employees

8%organic growth(vs. 7% in Q1 2015)

6.1%operating margin(2)

(vs. 6.1% in Q2 2014)

(1) Emerging Markets comprise Asia, Eastern Europe, Latin America, Israel, South Africa and Turkey(2) Operating profit before other items and corporate costs

Regional Performance Q2 2015

11

Western Europe

5%organic growth(vs. 2% in Q1 2015)

5.9%operating margin(1)

(vs. 5.7% in Q2 2014)

• Significant IFS growth driven by Switzerland (Swisscom), Germany (Vattenfall), UK (UBS) and Spain (Bankia)• Growth in Turkey remains strong• Improved performance (vs. Q1) in the UK, France and Spain but macro conditions remain challenging• Selective pick-up in demand for non-portfolio services (Switzerland and UK)

• In-part driven by strategic initiatives…• …but also by IFS strength within Germany and the UK• Partly offset by operational challenges in the Netherlands

Nordic

1%organic growth(vs. 1% in Q1 2015)

6.7%operating margin(1)

(vs. 6.6% in Q2 2014)

• Finland and Sweden main contributors• Norway positively impacted by Q2 2015 contract launches• Denmark organic growth negatively impacted by timing of contract start-ups in 2015

• Improvement driven by Norway (strategic initiatives)• Contract start-up costs in Sweden and lower non-portfolio work in Denmark

(1) Operating profit before other items and corporate costs

Regional Performance Q2 2015

12

Asia

10%organic growth(vs. 8% in Q1 2015)

7.0%operating margin(1)

(vs. 7.0% in Q2 2014)

• Double-digit organic growth in India, Indonesia, China and Thailand• Hong Kong returns to growth due to contract start-ups• Strong performance from Global Corporate Client contracts in Singapore

• Operational improvements in Hong Kong and cost savings in India

Latin America

4%organic growth(vs. 6% in Q1 2015)

4.9%operating margin(1)

(vs. 4.7% in Q2 2014)

• Higher demand for non-portfolio services in Chile• Price increases in Argentina• Contract losses in Brazil and Mexico with no significant contract start-ups

• Improved performance in Mexico and Chile• Margin declines in Brazil due to contract losses, scope reductions and cost increases

(1) Operating profit before other items and corporate costs

Regional Performance Q2 2015

13

Pacific

8%organic growth(vs. 10% in Q1 2015)

North America

Eastern Europe

• Strong performance across the board but notably within IFS and the aviation segment

• Growth driven by remote site resource segment in Australia• Year-on-year growth in Aviation has slowed versus Q1

4.9%operating margin(1)

(vs. 4.1% in Q2 2014)

1%organic growth(vs. -2% in Q1 2015)

• Restructuring initiatives have yielded an improved operational performance• Positive impact from IFS and higher demand for non-portfolio services

• Returned to positive organic growth in Q2• Higher demand for portfolio and non-portfolio services from Global Corporate Clients• Negative impact from contract exits and losses in 2014 and 2015

4.2%operating margin(1)

(vs. 3.2% in Q2 2014)

4%organic growth(vs. 1% in Q1 2015)

• Contract scope reductions in Romania and the Czech Republic, contract start-up costs and contract losses in Poland

• Driven by contract wins in Poland and Slovenia and higher demand for non-portfolio services in Slovakia• Negatively impacted by Czech Republic (contract loss in Financial Services, lower-than-expected volume developments elsewhere)

6.3%operating margin(1)

(vs. 7.3% in Q2 2014)

(1) Operating profit before other items and corporate costs

Financial Results

14

16,000

16,500

17,000

17,500

18,000

18,500

19,000

19,500

20,000

20,500

21,000

Q2 2014 Divestments/acquisition

Currency Organic Q2 2015

Revenue Bridge

15

(1%)

DKK million

Q2 2015 revenue growth of 9.8%

Note net currency impact due primarily to GBP, CHF, and USD

6%

4.8% 20,206

18,397

5.7

5.5

5.5

5.5

5.6

5.40

5.45

5.50

5.55

5.60

5.65

5.70

5.75

Q211 Q411 Q212 Q412 Q213 Q413 Q214 Q414 Q215

Operating Profit(1)

16

LTM Operating margin (%)

(1) Operating profit before other items

DKK million Q2 2015 Q2 2014 Δ H1 2015 H1 2014 Δ

Operating profi t(1) 1,067 956 +111 1,910 1,741 +169

Operating margin(1) 5.3% 5.2% +8 bps 4.9% 4.8% +10 bps

7 consecutive quarters of LTM margin improvement

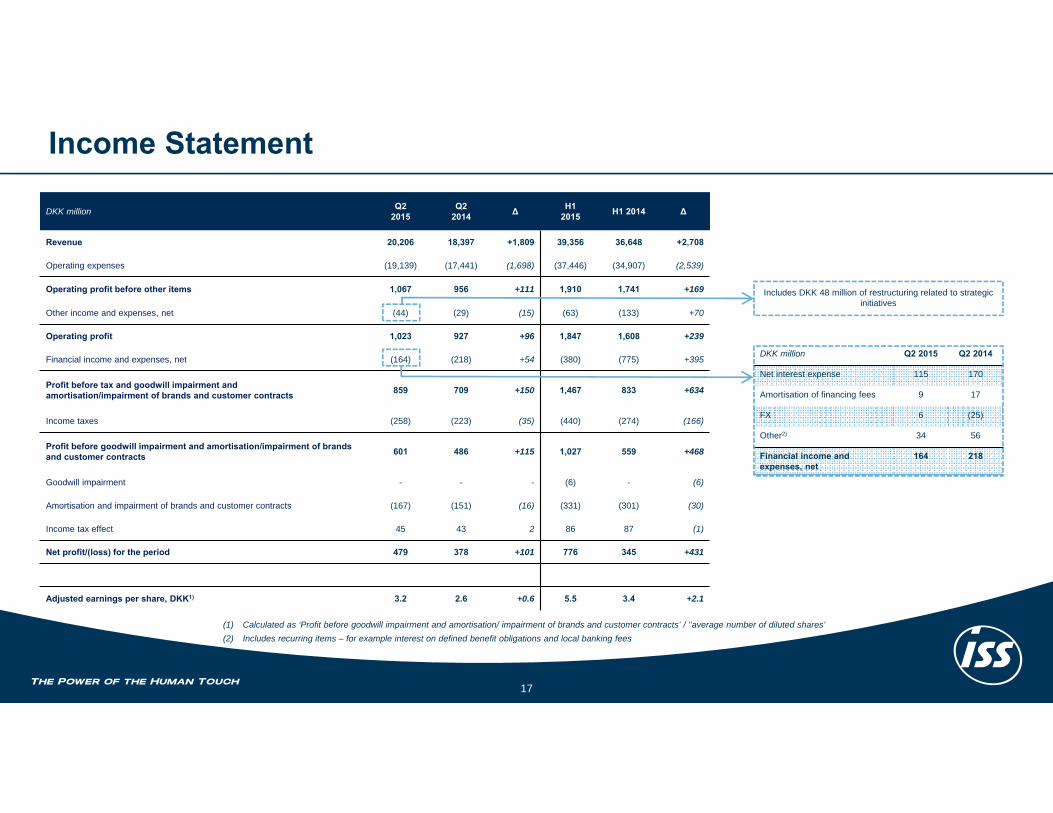

Income Statement

17

DKK million Q2 2015

Q2 2014 ∆ H1

2015 H1 2014 ∆

Revenue 20,206 18,397 +1,809 39,356 36,648 +2,708

Operating expenses (19,139) (17,441) (1,698) (37,446) (34,907) (2,539)

Operating profit before other items 1,067 956 +111 1,910 1,741 +169

Other income and expenses, net (44) (29) (15) (63) (133) +70

Operating profit 1,023 927 +96 1,847 1,608 +239

Financial income and expenses, net (164) (218) +54 (380) (775) +395

Profit before tax and goodwill impairment andamortisation/impairment of brands and customer contracts 859 709 +150 1,467 833 +634

Income taxes (258) (223) (35) (440) (274) (166)

Profit before goodwill impairment and amortisation/impairment of brands and customer contracts 601 486 +115 1,027 559 +468

Goodwill impairment - - - (6) - (6)

Amortisation and impairment of brands and customer contracts (167) (151) (16) (331) (301) (30)

Income tax effect 45 43 2 86 87 (1)

Net profit/(loss) for the period 479 378 +101 776 345 +431

Adjusted earnings per share, DKK1) 3.2 2.6 +0.6 5.5 3.4 +2.1

DKK million Q2 2015 Q2 2014

Net interest expense 115 170

Amortisation of financing fees 9 17

FX 6 (25)

Other2) 34 56

Financial income and expenses, net

164 218

Includes DKK 48 million of restructuring related to strategic initiatives

(1) Calculated as ‘Profit before goodwill impairment and amortisation/ impairment of brands and customer contracts’ / ‘’average number of diluted shares’(2) Includes recurring items – for example interest on defined benefit obligations and local banking fees

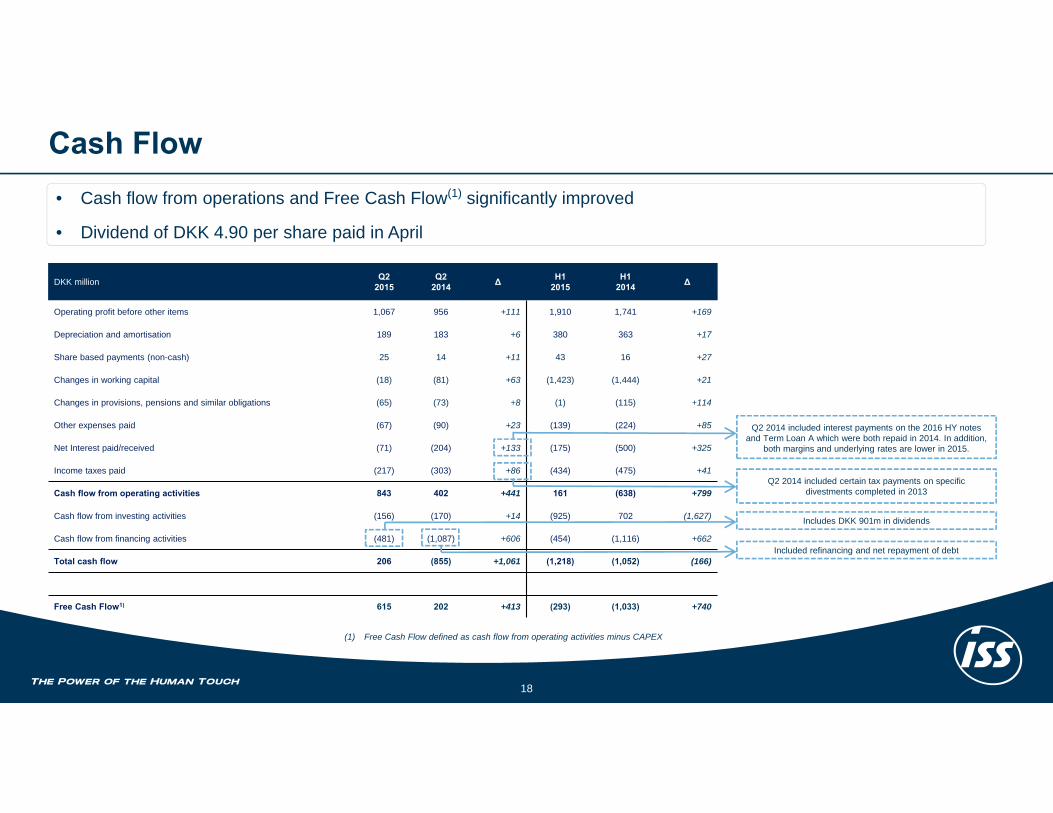

Cash Flow

18

DKK million Q22015

Q2 2014 ∆ H1

2015H1

2014 ∆

Operating profit before other items 1,067 956 +111 1,910 1,741 +169

Depreciation and amortisation 189 183 +6 380 363 +17

Share based payments (non-cash) 25 14 +11 43 16 +27

Changes in working capital (18) (81) +63 (1,423) (1,444) +21

Changes in provisions, pensions and similar obligations (65) (73) +8 (1) (115) +114

Other expenses paid (67) (90) +23 (139) (224) +85

Net Interest paid/received (71) (204) +133 (175) (500) +325

Income taxes paid (217) (303) +86 (434) (475) +41

Cash flow from operating activities 843 402 +441 161 (638) +799

Cash flow from investing activities (156) (170) +14 (925) 702 (1,627)

Cash flow from financing activities (481) (1,087) +606 (454) (1,116) +662

Total cash flow 206 (855) +1,061 (1,218) (1,052) (166)

Free Cash Flow1) 615 202 +413 (293) (1,033) +740

Q2 2014 included interest payments on the 2016 HY notes and Term Loan A which were both repaid in 2014. In addition,

both margins and underlying rates are lower in 2015.

Q2 2014 included certain tax payments on specific divestments completed in 2013

Includes DKK 901m in dividends

Included refinancing and net repayment of debt

• Cash flow from operations and Free Cash Flow(1) significantly improved

• Dividend of DKK 4.90 per share paid in April

(1) Free Cash Flow defined as cash flow from operating activities minus CAPEX

6.0

4.9 5.0 4.5

3.2

2.6 2.9

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Q112 Q312 Q113 Q313 Q114 Q314 Q115

Net debt (DKKm) Leverage

Leverage

19

Net debt and leverage(1)

(1) Net debt / Pro forma adjusted EBITDA (LTM)

DKK million Q2 2015 Q2 2014 Δ Q2 2015 Q4 2014 Δ

Net debt 14,668 15,278 ‐610 14,668 12,647 +2.021

Leverage(1) 2.9 3.2 ‐0.3 2.9 2.6 +0.3

Organisational Structure

20

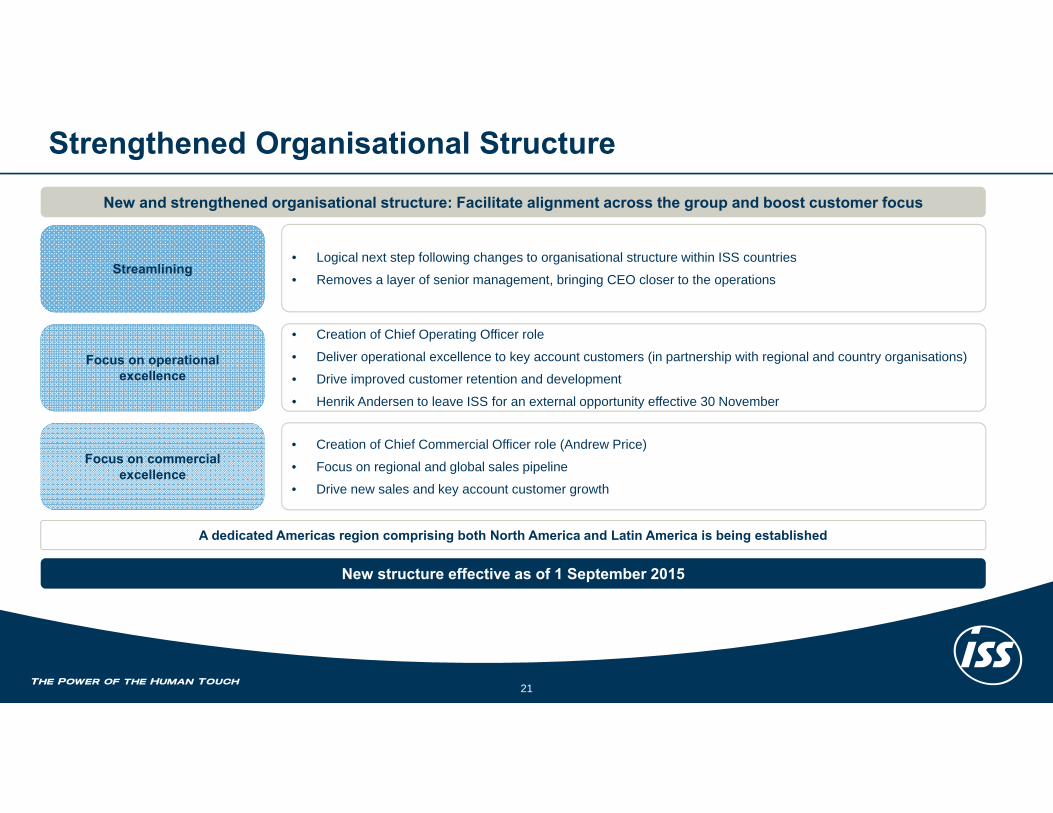

Strengthened Organisational Structure

21

New and strengthened organisational structure: Facilitate alignment across the group and boost customer focus

New structure effective as of 1 September 2015

Streamlining

Focus on operationalexcellence

Focus on commercialexcellence

• Creation of Chief Operating Officer role

• Deliver operational excellence to key account customers (in partnership with regional and country organisations)

• Drive improved customer retention and development

• Henrik Andersen to leave ISS for an external opportunity effective 30 November

• Creation of Chief Commercial Officer role (Andrew Price)

• Focus on regional and global sales pipeline

• Drive new sales and key account customer growth

• Logical next step following changes to organisational structure within ISS countries

• Removes a layer of senior management, bringing CEO closer to the operations

A dedicated Americas region comprising both North America and Latin America is being established

Outlook

22

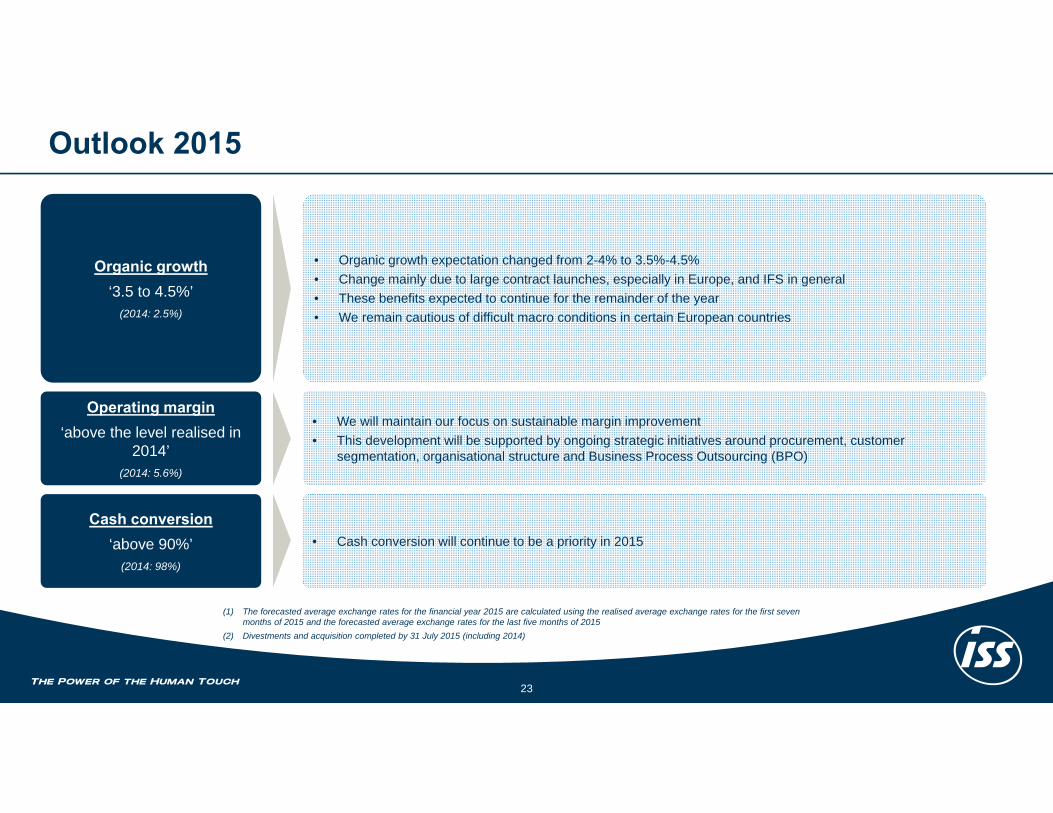

Outlook 2015

23

Operating margin‘above the level realised in

2014’(2014: 5.6%)

Cash conversion‘above 90%’

(2014: 98%)

• Cash conversion will continue to be a priority in 2015

• We will maintain our focus on sustainable margin improvement• This development will be supported by ongoing strategic initiatives around procurement, customer

segmentation, organisational structure and Business Process Outsourcing (BPO)

Organic growth‘3.5 to 4.5%’

(2014: 2.5%)

• Organic growth expectation changed from 2-4% to 3.5%-4.5%• Change mainly due to large contract launches, especially in Europe, and IFS in general• These benefits expected to continue for the remainder of the year• We remain cautious of difficult macro conditions in certain European countries

(1) The forecasted average exchange rates for the financial year 2015 are calculated using the realised average exchange rates for the first sevenmonths of 2015 and the forecasted average exchange rates for the last five months of 2015

(2) Divestments and acquisition completed by 31 July 2015 (including 2014)

Q&A

24