Investor Presentation March, 2015 -...

49

MARCH, 2015

-

Upload

vuongtuyen -

Category

Documents

-

view

217 -

download

0

Transcript of Investor Presentation March, 2015 -...

MARCH, 2015

Market Leader in High-Yield Pre-Owned CV Financing

q Shriram Transport Finance Company Limited (STFC) is one of the largest asset financing NBFC specialised in pre-owned commercial vehicle financing.

q Strategically present in high yield - pre-owned CV financing with expertise in loan origination, valuation and collection

q Expanded product portfolio to include financing of tractors, small commercial vehicles, 3-wheelers, passenger commercial vehicles and construction equipment

q Large customer base in excess of 1.2 mn as of March 31, 2015

q Employee strength of approximately 16,160 including 9,658 product/credit executives as of March 31, 2015.

q Listed on the National Stock Exchange and Bombay Stock Exchange with a market capitalisation of over Rs. 250 bn as on March 31, 2015

q Foreign institutional investor holds more than 51 percent of the company equity.

4

Operating Revenue Break Up

FY 14 – Rs. 78.80 bn

Extensive Distribution Network Large Assets Under Management ( as on March, 2015)

q Total Assets Under Management (AUM)

● Pre-Owned CV: Approximately Rs. 537.42 bn

● New CV: Approximately Rs. 46.80 bn

● Others: Approximately Rs. 6.86 bn

q Pan-India presence through a network of

● 741 branch offices

● 776 rural centres

q Partnership with over 500 Private Financiers

FY15 – Rs. 86.37 bn

Corporate History

5

2009

2005-06

2002-04

1999

1984

1979

q Successfully placed Rs. 10 bn of NCD with domestic investors q Purchased hypothecation loan outstandings of commercial

vehicles and construction equipments of GE Capital Services India and GE Capital Financial Services (GE) aggregating to approximately Rs. 11 bn

q Merger of Shriram Investment Ltd. and Shriram Overseas Finance Ltd. With STFC ; PAT crosses Rs. 1,000 mn (2006)

q Investment from ChrysCapital (2005) and TPG (2006)

q Preferential Allotment to Citicorp Finance (India) in 2002 q Preferential Allotment to Axis Bank and Reliance Capital in 2004

q Tied up with Citicorp for CV financing under Portfolio Management Services (PMS) q The 1st securitization transaction by STFC

q Initial Public Offering

q STFC was established

AUM: Rs. 2.44 bn

AUM: Rs 591.08 bn As of March 31, 2015

1990 q Investment from Telco & Ashok Leylond

q Securitised Rs. 87.57 bn during FY 2010. q Successfully raised Rs. 5.84 bn through QIP with

domestic & international investors.

2010

Unique Business Model

6

CV Financing Business Model

Pre Owned (5-12 Years & 2-5 Years Old CVs) New

Lending yields 18-24% (5-12 years) Lending yields 15-16% (2-5 years)

Lending yields 14-16%

Target Segment q Small truck owners (less than 2-3 trucks) with underdeveloped banking habits

Performance q AUM of Rs. 537.42 bn at the end of FY15

q Existing customer base upgrading to new trucks

q AUM of Rs. 46.80 bn at the end of FY15

FY10 FY11 FY12 FY13 FY14 FY15

LCV 287,777 361,846 460,831 524,887 432,233 382,206

MHCV 244,944 323,059 348,701 268,263 200,618 232,755

Total 532,721 684,905 809,532 793,150 632,851 614,961

Vehicles sold during FY10-15

With a Strong Financial Track Record

29,078.5 32,261.4 34,536.1 36,679.6 41,129.4

0 3,000 6,000 9,000

12,000 15,000 18,000 21,000 24,000 27,000 30,000 33,000 36,000 39,000 42,000 45,000

2011 2012 2013 2014 2015

Net Interest Income

(Rs mn)

12,298.8 12,574.6

13,606.2

12,642.1 12,378.1

11,000

12,000

13,000

14,000

2011 2012 2013 2014 2015

Net Profit

(Rs mn)

54.49 55.59

59.98

55.72 54.56

48

54

60

66

2011 2012 2013 2014 2015

EPS

(Rs)

54,010.5 58,938.8 65,635.9

78,882.6 86,447.2

0 7,000

14,000 21,000 28,000 35,000 42,000 49,000 56,000 63,000 70,000 77,000 84,000 91,000

2011 2012 2013 2014 2015

Total Income

(Rs mn)

7

Driven by Fast Growth in AUM with Low NPAs

0.4% 0.4% 0.8%

0.8% 0.8%

2.6%

3.1% 3.2%

3.9% 3.8%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

FY'11 FY'12 FY'13 FY'14 FY'15

Net NPA Gross NPA

NPA Levels 198.7& 219.9&

314.5& 364.9&492.3&163.2& 182.3&

182.3& 166.3&98.8&

,50&10&70&

130&190&250&310&370&430&490&550&

2011& 2012& 2013& 2014& 2015&

Off,Books& On,Books&

AUM (Rs bn)

8

Strengths

10

1 Widespread Geographical Reach

2 Valuation Skills & Recovery/Collection Operation

3 Strong Balance Sheet

4 Strong Management Team

5 Organizational Structure: Credit Risk Focus

6 Strengthening Presence and Expanding Reach

11

Branch Locations Across India

States with STFC Presence

741 Branch Offices & 776 Rural Centres

Tie up with Appx. 500 Private Financiers

16,160 Employees including 9,658 Field Officers

Pan-India Presence

As on March 31, 2015

Regional Split of Branches

Geographical Reach & Proximity to the Customer

Valuation Skills & Recovery/Collection Operation: Leveraging on Relationships

12

q Valuation Skills: ● Considerable expertise in valuation

of pre-owned trucks

● Valuation skills is critical to succeed in this space given that the amount of loan, EMI and a truck operator’s ability to repay rests on the value of the truck

q Recovery/Collection Operation: ● Due to underdeveloped banking

habits of small truck operators, a large part of monthly collections is in the form of cash

● Compulsory monthly visits to borrowers by field officers help in managing large cash collections

● Continuous monitoring of disbursed loans

Field Officers Vast Customer Base

Knowledge & Relationship based Recovery Procedure

In-house Administered Loan Recovery

2 Knowledge driven valuation model

Experience in credit appraisal & recovery/collection operations has lead STFC to become one of the leading organized players in the sector

Vehicle Assessment 60%-70% Loan-to-Value

Ratio – Old CVs 75%-85% Loan to Value

Ratio – New CVs

Healthy Asset Quality

q Substituted formal credit evaluation tools, such as IT returns and bank statements, with personal understanding of the customers’ proposed business model

q Client and truck-wise exposure limits

13

Prudent Credit Norms NPA Levels

Reasons for Low Delinquency

q Asset backed lending with adequate cover

q Assets are easy to repossess with immediate liquidity

q Target segment generally operates on state highways and short distances, ferrying essential commodities

0.38% 0.44%

0.77% 0.83% 0.78%

2.64%

3.06% 3.20%

3.86% 3.79%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

4.5%

FY11 FY12 FY13 FY14 FY 15

Net NPA Gross NPA

3

Incentive Schemes

q Well-defined incentive plan for field officers to ensure low default rates

q Field officers are responsible for recovery of loans they originate

Around 80% coverage between Gross/Net NPA as on March, 2015

Has Attracted Strong Interest from Quality Investors

q Consistent track record and high growth potential has attracted reputed institutional and private equity investors to infuse growth capital

q Last fund raising : Allotted 11.658 mn equity shares at Rs. 500.80 per share to Qualified Institutional Buyers (QIB) for an aggregate sum of Rs. 5.84 bn resulting in a dilution of around 5.20% to 45 marquee global as well as domestic funds and insurers, which included 22 existing investors and the rest, new investors on January 28, 2010

q Capital Adequacy ratio as of March 31, 2015 : 20.52%

14 Large Investments by major Institutional and Private Equity Investors

Key Shareholders* Current Shareholding (Mn Shares) % age

Shriram Capital 59.10 26.05

Piramal Enterprises 22.60 9.96

Sanlam Life Insurance 6.76 2.98

Centaura Investments 4.49 1.98

Stiching Pension Fund 4.05 1.79

Small Cap World Fund 3.60 1.58

Ontario Teachers 2.82 1.24

Government of Singapore 2.52 1.11

Vanguard Emerging Market Stock Index Fund 2.34 1.03

Abudhabi Investment Authority 2.28 1.01

Merrill Lynch Capital Market Espana 2.27 1.00

Public & Others 114.05 50.27

Total 226.88 100.00

3

*As on March 31, 2015

Optimized Balance Sheet : Access to Low Cost Funds

q Strategic mix of retail deposits and institutional funding

q Average cost of funds declined over the years with increase in Bank/ Institutions liabilities

q Access to fixed rate long term loans of 3 - 5 years due to strong relationships with public, private sector, foreign banks and institutions

15

Borrowings

Securitization

q Securitization of loan book at regular intervals to fund new originations and maintain growth momentum.

q Securitized assets portfolio stands at Rs. 98.81 bn at the end of FY15

q Conservative recognition of income on account of amortization of securitization income over the tenor of the agreements

Funding Mix as % of Overall Liabilities

22% 21% 18% 20% 20%

78% 79% 82% 80% 80%

0%

20%

40%

60%

80%

100%

FY'11 FY'12 FY'13 FY'14 FY'15

Retail Banks/Institutions

Long term rating: AA+ from CARE & AA from CRISIL

Credit Ratings

Highest short term rating: A1+ from Fitch & A1+ from CRISIL

3

Strong Management Team

16

4 Umesh Revenkar CEO & Managing

Director

q Joined as an Executive Trainee in 1987 and looks after operations of the CV finance business

q Holds a degree in MBA Finance

Sanjay K Mundra Senior Vice President – Investor and Media

Relations

q Over 21 years experience in the finance Industry

q Joined in 2007, a qualified Company Secretary

Vinay Kelkar Deputy Managing

Director

q Over 32 years experience and 20 years of experience in finance industry

q Joined in 1995 and now heads the Compliance and Accounts function, a qualified Chartered Accountant & Cost Accountant

S. Sunder Executive Director – Accounts & Admn.

q Over 24 years experience in finance industry

q Joined in 1995 and now heads the Accounts and Administration function, a qualified Cost Accountant

Parag Sharma Executive Director &

CFO

q Over 24 years experience in finance industry

q Joined in 1995 and now heads the Finance function, a qualified Cost Accountant

Board of Directors

17

4

Subramanian Laksminarayanan

Chairman

q Member of Indian Administrative Services (IAS – retired) q Served at senior positions in the Ministry of Home Affairs, Ministry of Communication & IT etc.

R Sridhar Director

q Over two decades of experience in financial services sector, especially in commercial vehicle financing q Joined Shriram Group in 1985 and served as Managing Director from September, 2000 to March, 2012

q Holds directorship in other Shriram Group companies

q Fellow member of the Institute of Chartered Accountants of India

Amitabh Chaudhry Director

q Over two decades of experience in financial services, MBA from IIM Ahmedabad & B. Tech from BITS, Pilani q Holds directorship in HDFC Standard Life Insurance Co. Ltd. & HDFC pension management Co. Ltd.,

Manipal Global education Pvt. Ltd & Credila Financial Servies Private Limited

S. Sridhar Director

q Former Chairman & Managing Director of Central Bank of India, with nearly four decades of experience in commercial and development banking out of which 13 years were at the CEO/Board level.

q Currently, he serves as an Independent Director on the Boards of various companies, and also as a consultant to financial services companies.

Umesh Revenkar CEO & Managing

Director

q Joined as an Executive Trainee in 1987 and looks after operations of the CV finance business

q Holds a degree in MBA Finance

Board of Directors (Contd.)

18

4

Mrs Kishori Udeshi Director

q Holds degree in MA in Economics. First women Deputy Governor of RBI and also on the Board of SEBI, NABARD & EXIM Bank.

q Holds directorship in HSBC Asset Management (India) Pvt. Ltd., ION Exchange (India) Ltd., HALDYN Glass Ltd., Thomas Cook (India Ltd. And Elantas Beck India Ltd. Thomas Cook Insurance Services (India) Limited; and Shriram Automall India Limited etc.

Puneet Bhatia Director

q MD of TPG Capital and country Head – India for TPG’s Asian Business q Former Chief executive of the Private Equity Group for GE Capital India

q Holds a degree in Commerce and an MBA from IIM, Calcutta

Sumatiprasad M Bafna

Director

q Has extensive experience in the transportation business q He currently serves on the board of directors of Bafna Aviation Pvt. Ltd., Bafna Motors (Mumbai) Pvt. Ltd.,

Isuta Electronics (India) Ltd, Bafna Motors (Ratnagiri) Pvt Ltd, Kishore Transport Services Pvt. Ltd. etc.

Gerrit Lodewyk Van Heerde

Director

q Chief Financial Officer of Sanlam Emerging Markets q Has 22 years of experience in the financial services industry and has represented Sanlam at various other

boards.

Organizational Structure: Credit Risk Focus

19

National Product Heads Zonal Business Head Chief Operating Officer

Credit Admn

Regional Product Heads Regional Business Heads Regional Credit Risk Head

Credit Cell

Branch Heads Credit Risk Head Credit Cell

Product Executives

Zonal Credit Head

Clearly Demarcated Responsibilities

q Field Offices:

● Direct contact with customers for vehicle inspection & primary valuation, sales-lead generation, and collection & repossession in the case of default

q Branch Heads (741 Branches) :

● Deciding the credit worthiness of individuals and arranging the necessary documentation

● Each branch has ~15-20 employees, 8-10 field officers, 6-8 support staff

5

Strengthening Presence and Expanding Reach

20

6

Core Business q Leverage the large pan-India network to enhance reach in North & East India, particularly in large

CV hubs

q To increase market share in pre-owned CV market

Expanding the Pre-Owned CV Segment

q Introduce top-up products such as finance for tyres, working capital and engine replacement

Leveraging Private Financiers

q Build partnership with private financiers in the unorganized market to leverage their local knowledge to enhance market share

q Partnered with more than 500 private financiers as of March 31, 2015

Axis Bank co-branded credit

cards

q Tied up with Axis Bank to distribute credit cards to small truck owners

q Distributed over 3,70,000 credit cards as of March 31, 2015

Strengthening Presence and Expanding Reach (Contd.)

21

6

Freight Bill Discounting q Estimated market size of Rs. 60-70 bn with higher yields than the existing CV financing business.

Passenger Commercial

Vehicle Financing

q Estimated market size of Rs. 260 bn for FY15 backed by growth in population and an improving

road infrastructure

Tractor Financing q Market experiencing growth with increasing policy thrust on agricultural mechanization.

q The used tractor financing market is estimated at Rs. 310 bn in FY15

Construction Equipment Financing

q Market expected to reach over Rs. 400 bn in 2015 driven by huge infrastructure spending during the 11th 5-Year Plan estimated at approximately Rs. 20 tn

q This business would be through our 100% subsidiary Shriram Equipment Finance Company Ltd under an independent management which would focus on end-to-end equipment financing

Automall

q Platform to facilitate buyers and sellers to meet for sale of pre-owned CVs, where Shriram Automall, 100% subsidiary can earn commission fees through its advisory services and STFC will provide financing to the buyer

q Shriram Automall is creating a market for pre-owned trucks in organised and transparent manner and planning to create 50 – 60 such automall

STFCL

Increase Reach & Branding

New Innovative Products and

Tieups

Multiply Consolidated AUM over Rs 750 bn by

2016

Target to reach AUM over Rs 750 bn by FY16 6

Well Planed Strategy for Future Growth

22

Building Trust and Strengthening Relationship:

q Unparalleled physical auction model in the country.

q Opportunity for Sellers and Financial institutions to sell assets and realize the best value with bidding by 300 and more bidders in every auction.

q 50 Automalls in operation.

q Over 0.25 mn assets sold.

q Automalls in addition would be offering host of services like valuation, parking, financing etc.

23

q Touch Screen Kiosks are Virtual Truck Bazaars-Buy & Sell as per convenience.

q Facilitates Buyer and Sellers to purchase and sell vehicles at the Right price.

q Kiosks available in 500 branches across the length and breadth of the country.

q Over 0.25 mn transactions executed.

AutoMalls

Touch Screen Kiosks

These initiatives would help STFC gain the Trust of those associated with theTransport and Equipment Industry

6

Over 0.6 mn Customer Base

" Stable asset quality with Gross NPAs and the Net NPA at 3.79% & 0.78% respectively and the Net NPA in absolute

amount stands at Rs. 3,791.2 mn (Coverage ratio maintained around 80%)

" Employee strength decreased by 1,962 taking the total strength to 16,160 from 18,122 including 9,658 field executives.

Standalone Performance Review Q4 FY’14 Vs. Q4 FY’15

Total Income Net Interest Income* EPS

15.2%

Rs 23,123.2 mn Rs 10,853.6 mn

7.4%

Rs 13.96

Rs 20,068.4 mn Rs 9,205.2 mn Rs 13.00

*including Securitisation Income

Rs 3,167.3 mn

PAT

17.9%

Rs 2,949.6 mn

25

7.4%

Consolidated Performance Review Q4 FY’14 Vs. Q4 FY’15

Total Income Net Interest Income* EPS

12.6%

Rs 24,211.3 mn Rs 11,055.7 mn

73.3%

Rs 3.71

Rs 21,500.4 mn Rs 9,759.5 mn Rs 13.88

*including Securitisation Income

Rs 842.3 mn

PAT

13.3%

Rs 3,148.9 mn

73.3%

26

Rs 98.8 bn

Rs 166.3 bn

Off Books Assets

Rs 522.3 bn

30.9%

Rs 399.1 bn

On Books Assets

40.6%

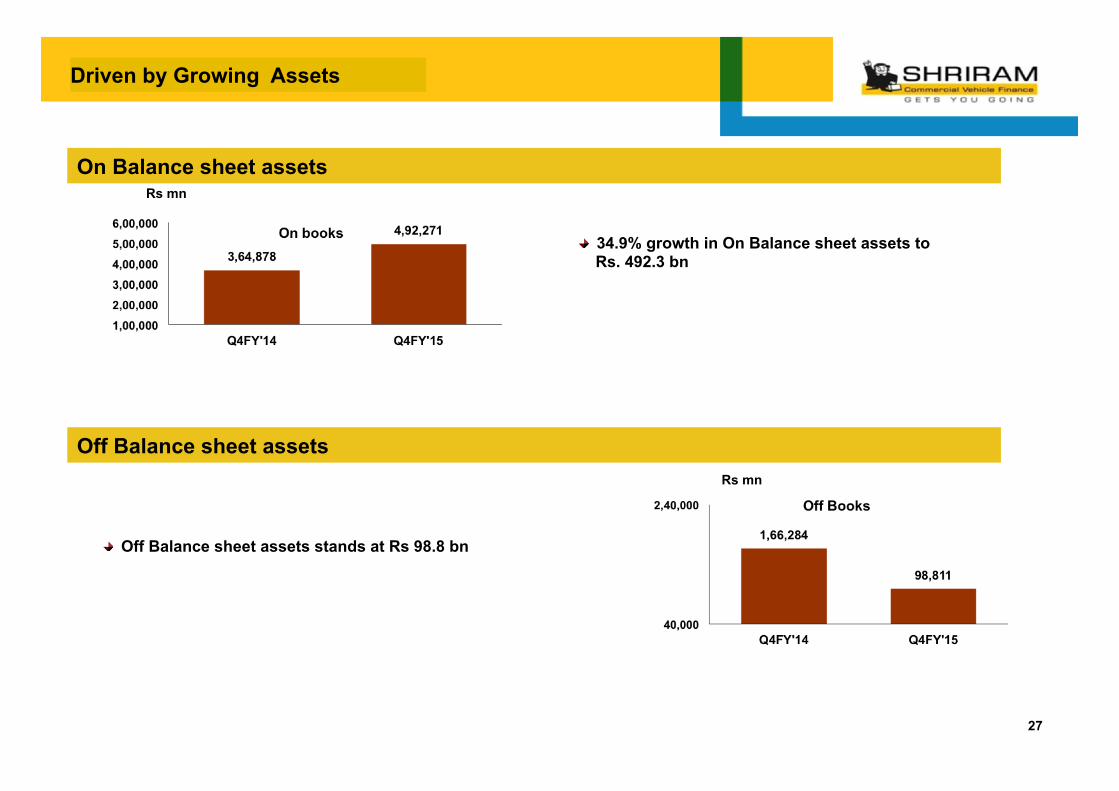

Driven by Growing Assets

On Balance sheet assets

" 34.9% growth in On Balance sheet assets to Rs. 492.3 bn

Off Balance sheet assets

" Off Balance sheet assets stands at Rs 98.8 bn

Rs mn

Rs mn

27

Driven by Growing Assets

Used CVs assets

" 15.4% growth in Used CVs to Rs 537.4 bn

New CVs assets

" New CVs stands at Rs 46.8 bn

Rs mn

Rs mn

28

29

AUM BREAK-UP

HCVs 42.3%

M&LCVs 27.0%

Passenger Vehicles 22.4%

Tractors 5.5%

Others 2.8%

Driven by Growing Assets

Supported by a Healthy Borrowing Profile

Borrowing Profile

Q4 FY’14 – Rs 359.2 bn Q4 FY’15 – Rs 442.8 bn

19.5%

80.5%

Retail Banks/Institutional

19.6%

80.4%

Retail Banks/Institutional

30

Modernization of trucking industry § Legislative pressure on banning trucks beyond 15 years is likely

to trigger replacement boom § Transport associations’ introduction of Voluntary Retirement

Scheme for old trucks with better financing options § Financing amount of Rs 1,078 bn to be triggered through

replacement demand for 1.35 mn new as well as pre-owned trucks

Sustained Growth Expected to Continue

§ CV Financing market size of Rs 1,900 bn § Shriram targets the largest market segment of pre-owned,

accounting for 43% of the total market volume § Market for second hand truck financing is under penetrated

with 65-70% of the market with private financiers who charge high interest rates

Shriram Target Segment

Market Potential

12+ Yrs Rs 180 bn

5-12 Yrs Rs 850 bn

0-4 Yrs Rs 870 bn

Truck Profile (7.5 mn)

0-4 Yrs 39%

5-12 Yrs 43%

Ø 12 Yrs 18%

Stricter emission norms expected to generate huge demand for 5-12 year old trucks Growing freight capacity § GDP growth rate driving incremental freight capacity which is estimated to increase at 1.25 times of GDP growth.

Exponential Growth in CV Financing

Only Organised Player in the Pre-owned CV Financing Market

32

Transport Logistic Model to Stay – hub & spoke

STFC will benefit from Exponential growth in the vehicles required for Last Mile Transport-SRTO

q Transport Industry maturing with the years.

q Distribution solution providers changing the dimension of Transportation.

q Rural and Semi Urban markets seeing higher growth rates across all products.

q Better Road network seeing light of the day.

q Competition and Emission standards driving manufacturer’s to launch Latest Technology International standard vehicles.

q Last mile Transport pushing demand for Cargo LCV’s.

33

Shareholding Structure as on March 31, 2015

No. of shares outstanding: 226.88mn

Promoter & Promoter Group 26.1%

FII 51.2%

MF/ Banks 4.2%

Public 6.2%

Other Corporate Bodies 12.1%

NRI/ OCBs 0.2%

35

Profit and Loss Statement

36

(Rs in mn) Profit & Loss Statement Q4 FY'14 Q1 FY'15 Q2 FY'15 Q3 FY'15 Q4 FY'15 YoY % QoQ % FY'14 FY'15 YoY % Interest Income 16,459.9 17,079.6 18,798.1 20,537.6 21,363.7 29.79% 4.02% 62,865.1 77,779.0 23.72% Interest expended 10,010.7 9,870.7 10,921.4 11,350.7 11,885.9 18.73% 4.72% 38,981.8 44,028.7 12.95% Net Interest Income 6,449.2 7,208.9 7,876.7 9,186.9 9,477.8 46.96% 3.17% 23,883.3 33,750.3 41.31% Income from Securi@sa@on 2,868.1 2,583.0 2,263.6 1,397.1 1,452.4 -‐49.36% 3.96% 13,367.7 7,696.1 -‐42.43% Less : Securi@sa@on expenses 112.1 116.0 68.0 56.4 76.6 -‐31.67% 35.82% 571.4 317.0 -‐44.52% Income from Securi@sa@on (Net) 2,756.0 2,467.0 2,195.6 1,340.7 1,375.8 -‐50.08% 2.62% 12,796.3 7,379.1 -‐42.33% Net Interest Income incl. SecurCsaCon Gain 9,205.2 9,675.9 10,072.3 10,527.6 10,853.6 17.91% 3.10% 36,679.6 41,129.4 12.13% Other fee based income 4.1 2.9 2.7 3.3 3.0 -‐26.83% -‐9.09% 21.9 11.9 -‐45.66% OperaCng Income 9,209.3 9,678.8 10,075.0 10,530.9 10,856.6 17.89% 3.09% 36,701.5 41,141.3 12.10% Opera@ng expenditure 2,466.8 2,514.7 2,575.1 2,701.7 2,991.1 21.25% 10.71% 9,560.9 10,782.6 12.78% Core OperaCng Profit 6,742.5 7,164.1 7,499.9 7,829.2 7,865.5 16.66% 0.46% 27,140.6 30,358.7 11.86% Other Income 157.4 233.5 160.6 143.6 157.1 -‐0.19% 9.40% 1,432.8 694.8 -‐51.51% OperaCng Profit 6,899.9 7,397.6 7,660.5 7,972.8 8,022.6 16.27% 0.62% 28,573.4 31,053.5 8.68% Provisions for Bad Debts 2,492.9 2,873.8 3,070.4 3,153.3 3,233.9 29.72% 2.56% 10,166.9 12,331.4 21.29% Provisions against Standard Assets (35.4) 91.9 83.9 115.5 6.9 -‐119.49% -‐94.03% 126.1 298.2 136.48% PBT 4,442.4 4,431.9 4,506.2 4,704.0 4,781.8 7.64% 1.65% 18,280.4 18,423.9 0.78% Tax 1,492.8 1,367.7 1,484.1 1,579.5 1,614.5 8.15% 2.22% 5,638.3 6,045.8 7.23% PAT 2,949.6 3,064.2 3,022.1 3,124.5 3,167.3 7.38% 1.37% 12,642.1 12,378.1 -‐2.09% EPS (Rs) 13.00 13.51 13.32 13.77 13.96 7.38% 1.38% 55.72 54.56 -‐2.08% Tier I CRAR % 17.69% 17.46% 17.09% 16.49% 16.40% -‐7.12% -‐0.36% 17.69% 16.40% -‐7.12% Tier II CRAR % 5.68% 5.43% 4.87% 4.58% 4.12% -‐27.29% -‐9.83% 5.68% 4.12% -‐27.24% Total CRAR % 23.37% 22.89% 21.96% 21.07% 20.52% -‐12.02% -‐2.42% 23.37% 20.52% -‐12.01% Book Value (Rs) 362.72 376.34 389.37 398.57 405.54 11.81% 1.75% 362.72 405.54 11.81%

Key RaCos (%) Q4 FY'14 Q1 FY'15 Q2 FY'15 Q3 FY'15 Q4 FY'15 YoY % QoQ % FY'14 FY'15 YoY % Return on Avg. Net Worth 14.43% 14.55% 13.85% 13.91% 13.83% -‐4.16% -‐0.58% 16.20% 14.03% -‐13.40% Return on Avg. Assets 2.38% 2.46% 2.31% 2.22% 2.17% -‐8.82% -‐2.25% 2.64% 2.28% -‐13.64% Interest Coverage Ra@o 1.95 2.02 1.94 1.95 1.93 -‐1.03% -‐1.03% 1.99 1.96 -‐1.51% NIM on AUM 6.46% 6.54% 6.60% 6.64% 6.67% 3.25% 0.45% 6.68% 6.61% -‐1.05%

Balance Sheet

37

(Rs in mn) Balance Sheet Q4 FY'14 Q1 FY'15 Q2 FY'15 Q3 FY'15 Q4 FY'15 YoY % QoQ % FY'14 FY'15 YoY % LiabiliCes Shareholder funds (a) Share capital 2,269.1 2,269.1 2,269.1 2,269.1 2,269.1 0.00% 0.00% 2,269.1 2,269.1 0.00% (b) Reserves and surplus 80,463.1 83,514.9 86,537.0 88,576.7 90,110.6 11.99% 1.73% 80,463.1 90,110.6 11.99% Non-‐current liabili4es (a) Long-‐term borrowings 2,27,120.9 2,25,020.6 2,71,118.9 2,96,139.0 3,15,707.6 39.00% 6.61% 2,27,120.9 3,15,707.6 39.00% (b) Other Long term liabili@es 9,687.1 8,988.9 8,348.8 7,904.0 9,713.4 0.27% 22.89% 9,687.1 9,713.4 0.27% (c) Long term provisions 12,717.4 13,342.2 14,125.7 14,989.0 15,865.0 24.75% 5.84% 12,717.4 15,865.0 24.75% Current liabili4es (a) Short-‐term borrowings 29,859.0 38,441.0 39,729.8 55,292.3 26,614.1 -‐10.87% -‐51.87% 29,859.0 26,614.1 -‐10.87% (b) Trade payables 4,739.6 4,770.5 4,455.7 9,965.7 11,596.9 144.68% 16.37% 4,739.6 11,596.9 144.68% (c) Other current liabili@es 1,22,562.9 1,19,804.1 1,12,321.1 1,04,345.6 1,17,416.4 -‐4.20% 12.53% 1,22,562.9 1,17,416.4 -‐4.20% (d) Short-‐term provisions 2,935.6 3,368.5 2,178.7 2,486.7 3,978.4 35.52% 59.99% 2,935.6 3,978.4 35.52% Total 4,92,354.7 4,99,519.8 5,41,084.8 5,81,968.1 5,93,271.5 20.50% 1.94% 4,92,354.7 5,93,271.5 20.50% Assets Non-‐current assets (a) Fixed assets (i) Tangible assets 990.2 972.1 1,003.2 975.1 994.5 0.43% 1.99% 990.2 994.5 0.43% (ii) Intangible assets 16.4 15.3 15.7 13.3 12.8 -‐21.95% -‐3.76% 16.4 12.8 -‐21.95% (b) Non-‐current investments 6,878.0 7,621.3 8,643.8 10,367.2 11,142.6 62.00% 7.48% 6,878.0 11,142.6 62.00% (c) Deferred tax assets (net) 2,511.6 2,426.0 2,491.8 2,580.1 2,564.8 2.12% -‐0.59% 2,511.6 2,564.8 2.12% (d) Long term loans and advances 2,21,003.7 2,46,556.7 2,70,700.2 3,01,710.3 3,08,228.7 39.47% 2.16% 2,21,003.7 3,08,228.7 39.47% (e) Other non-‐current assets 944.3 378.1 402.5 331.2 931.1 -‐1.40% 181.13% 944.3 931.1 -‐1.40% Current assets (a) Current investments 20,374.6 9,562.5 10,389.6 11,167.9 22,129.2 8.61% 98.15% 20,374.6 22,129.2 8.61% (b) Cash and bank balances 70,859.8 53,807.3 59,650.1 53,345.0 47,234.0 -‐33.34% -‐11.46% 70,859.8 47,234.0 -‐33.34% (c) Short-‐term loans and advances 1,67,976.0 1,77,352.3 1,86,889.1 2,00,695.1 1,99,409.4 18.71% -‐0.64% 1,67,976.0 1,99,409.4 18.71% (d) Other current assets 800.1 828.2 898.8 782.9 624.4 -‐21.96% -‐20.25% 800.1 624.4 -‐21.96% Total 4,92,354.7 4,99,519.8 5,41,084.8 5,81,968.1 5,93,271.5 20.50% 1.94% 4,92,354.7 5,93,271.5 20.50%

38

Details of Key Parameters (Profit & Loss Account)

ParCculars

Q4 Q1 Q2 Q3 Q4 % % Year ended Year ended %

FY 2013 14 FY 2014 15 FY 2014 15 FY 2014 15 FY 2014 15 YoY QoQ FY 2014 FY 2015 YoY

Interest Income mn 16,459.9 17,079.6 18,798.1 20,537.6 21,363.7 29.79% 4.02% 62,865.1 77,779.0 23.72%

SecuriCsaCon Income mn 2,756.0 2,467.0 2,195.6 1,340.7 1,375.8 -‐50.08% 2.62% 12,796.3 7,379.1 -‐42.33%

Total Interest Income mn 19,215.9 19,546.6 20,993.7 21,878.3 22,739.5 18.34% 3.94% 75,661.4 85,158.1 12.55%

Less : Interest Expenses mn 10,010.7 9,870.7 10,921.4 11,350.7 11,885.9 18.73% 4.72% 38,981.8 44,028.7 12.95%

Net Interest Income mn 9,205.2 9,675.9 10,072.3 10,527.6 10,853.6 17.91% 3.10% 36,679.6 41,129.4 12.13%

Other Income mn 161.5 236.4 163.3 146.9 160.1 -‐0.87% 8.99% 1,454.7 706.7 -‐51.42%

OperaCng Income mn 9,366.7 9,912.3 10,235.6 10,674.5 11,013.7 17.58% 3.18% 38,134.3 41,836.1 9.71%

Profit a]er Tax mn 2,949.6 3,064.2 3,022.1 3,124.5 3,167.3 7.38% 1.37% 12,642.1 12,378.1 -‐2.09%

Cost to Income RaCo % 24.87 23.06 22.32 23.42 25.01 0.56% 6.79% 24.15 23.48 -‐2.78%

EPS Rs. 13.00 13.51 13.32 13.77 13.96 7.38% 1.38% 55.72 54.56 -‐2.08%

ROA % 2.38% 2.46% 2.31% 2.22% 2.17% -‐8.82% -‐2.25% 2.64% 2.28% -‐13.64%

ROE % 14.43% 14.55% 13.85% 13.91% 13.83% -‐4.16% -‐0.58% 16.20% 14.03% -‐13.40%

NIM (on AUM) % 6.46% 6.54% 6.60% 6.64% 6.67% 3.25% 0.45% 6.68% 6.61% -‐1.05%

39

Details of Key Parameters (Balance Sheet)

ParCculars

Q4 Q1 Q2 Q3 Q4 % % Year ended Year ended %

FY 2013 14 FY 2014 15 FY 2014 15 FY 2014 15 FY 2014 15 YoY QoQ FY 2014 FY 2015 YoY

Asset under Management

-‐ On Books mn 3,64,877.6 4,05,062.8 4,41,331.1 4,90,064.7 4,92,271.4 34.91% 0.45% 3,64,877.6 4,92,271.4 34.91%

-‐ Off Books mn 1,66,284.3 1,38,733.4 1,14,270.2 80,770.5 98,811.4 -‐40.58% 22.34% 1,66,284.3 98,811.4 -‐40.58%

Total AUM mn 5,31,161.9 5,43,796.3 5,55,601.3 5,70,835.2 5,91,082.8 11.28% 3.55% 5,31,161.9 5,91,082.8 11.28%

SecuriCsaCon done mn 42,722 1,702 5,268 -‐ 37,844 -‐11.42% 0.00% 1,06,796 44,814 -‐58.04%

Gross NPA % 3.86% 3.74% 3.74% 3.59% 3.79% -‐1.81% 5.57% 3.86% 3.79% -‐1.81%

Net NPA % 0.83% 0.78% 0.80% 0.74% 0.78% -‐6.02% 5.41% 0.83% 0.78% -‐6.02%

Gross NPA mn 14,505.0 15,465.9 16,745.4 17,797.3 18,941.4 30.59% 6.43% 14,505.0 18,941.4 30.59%

Net NPA mn 3,029.1 3,134.9 3,491.9 3,561.2 3,791.2 25.16% 6.46% 3,029.1 3,791.2 25.16%

Coverage RaCo % 79.12% 79.73% 79.15% 79.99% 79.98% 1.10% -‐0.01% 79.12% 79.98% 1.10%

CRAR % 23.37% 22.89% 21.96% 21.07% 20.56% -‐12.01% -‐2.42% 23.37% 20.56% -‐12.01%

Book Value Rs. 362.72 376.34 389.37 398.57 405.54 11.81% 1.75% 362.72 405.54 11.81%

40

Subsidiary Information

1. Shriram Equipment Finance Company Limited. Assets under Finance - Rs. 29,985.8 mn in Q4 FY 15 (Rs. 34,183.9 mn in Q4 FY 14) PAT – Rs. (2,371.3) mn in Q4 FY 15 (Rs. 164.8 mn in Q4 FY 14)

2. Shriram Automall India Limited. - ONE STOP - Launched in more than 500 branches. - AUTOMALL – 50 Automall in operation.

3. Fees Income earned Rs. 212.4 mn in Q4 FY 15 (Rs. 197.6 mn in Q4 FY 14)

Profit and Loss Statement

41

Subsidiary - Shriram Equipment Finance Company Limited

Profit & Loss Statement Q4 FY'14 Q1 FY'15 Q2 FY'15 Q3 FY'15 Q4 FY'15 YoY % QoQ % FY'14 FY'15 YoY % Interest Income 1,320.9 1,261.8 1,393.4 1,280.3 888.7 -‐32.72% -‐30.59% 5,439.3 4,824.2 -‐11.31% Interest expended 766.6 751.4 746.8 741.6 686.6 -‐10.44% -‐7.42% 2,897.6 2,926.4 0.99% Net Interest Income 554.3 510.4 646.6 538.7 202.1 -‐63.54% -‐62.48% 2,541.7 1,897.8 -‐25.33% OperaCng Income 554.3 510.4 646.6 538.7 202.1 -‐63.54% -‐62.48% 2,541.7 1,897.8 -‐25.33% Opera@ng expenditure 165.0 153.0 168.4 184.3 216.5 31.24% 17.48% 584.2 722.2 23.62% Core OperaCng Profit 389.3 357.4 478.2 354.4 (14.4) -‐103.71% -‐104.07% 1,957.5 1,175.6 -‐39.94% Other Income 0.0 0.1 0.1 0.6 8.0 17708.53% 1356.43% 0.2 8.8 4897.86% OperaCng Profit 389.3 357.5 478.3 355.0 (6.4) -‐101.64% -‐101.80% 1,957.6 1,184.4 -‐39.50% Provisions for Bad Debts 141.0 278.5 367.4 248.7 2,357.5 1571.81% 847.74% 634.3 3,252.1 412.70% Provisions against Standard Assets (1.3) (1.4) (0.8) (3.3) (16.0) 1154.53% 387.10% 9.8 (21.5) -‐318.92% PBT 249.6 80.4 111.7 109.4 (2,347.9) -‐1040.73% -‐2245.64% 1,313.5 (2,046.2) -‐255.78% Tax 84.9 27.1 38.0 37.5 23.4 -‐72.40% -‐37.55% 445.2 126.0 -‐71.71% PAT 164.8 53.3 73.7 71.9 (2,371.3) -‐1538.74% -‐3396.99% 868.3 (2,172.2) -‐350.16% EPS (Rs) 16.47 5.33 7.36 7.19 -‐237.10 -‐1539.67% -‐3397.61% 86.81 -‐217.23 -‐350.25% Tier I CRAR % 14.21% 14.54% 14.82% 15.69% 9.93% -‐30.12% -‐36.71% 14.21% 9.93% -‐30.12% Tier II CRAR % 5.61% 5.68% 5.87% 6.11% 5.20% -‐7.43% -‐15.00% 5.61% 5.20% -‐7.43% Total CRAR % 19.82% 20.22% 20.69% 21.80% 15.12% -‐23.69% -‐30.62% 19.82% 15.12% -‐23.69% Book Value (Rs) 238.90 244.26 251.74 259.08 22.00 -‐90.79% -‐91.51% 238.90 22.00 -‐90.79%

Key RaCos (%) Q4 FY'14 Q1 FY'15 Q2 FY'15 Q3 FY'15 Q4 FY'15 YoY % QoQ % FY'14 FY'15 YoY % Return on Avg. Net Worth 13.71% 4.34% 5.92% 5.70% -‐242.88% -‐1871.29% -‐4363.81% 19.34% -‐46.08% -‐338.32% Return on Avg. Assets 1.88% 0.62% 0.83% 0.82% -‐29.61% -‐1673.56% -‐3728.50% 2.59% -‐6.32% -‐343.70% Interest Coverage Ra@o 1.72 1.68 1.87 1.73 1.31 -‐23.84% -‐24.28% 1.88 1.65 -‐12.02%

Balance Sheet

42

Subsidiary - Shriram Equipment Finance Company Limited

(Rs in mn) Balance Sheet Q4 FY'14 Q1 FY'15 Q2 FY'15 Q3 FY'15 Q4 FY'15 YoY % QoQ % FY'14 FY'15 YoY % I. EQUITY AND LIABILITIES (1) Shareholders' funds (a) Share capital 2,600.0 2,600.0 2,600.0 2,600.0 2,600.0 0.00% 0.00% 2,600.0 2,600.0 0.00% (b) Reserves and surplus 2,289.0 2,342.6 2,417.4 2,490.8 120.0 -‐94.76% -‐95.18% 2,289.0 120.0 -‐94.76% (2) Non-‐Current LiabiliCes (a) Long-‐term borrowings 13,915.1 12,279.9 13,680.5 13,721.0 12,848.2 -‐7.67% -‐6.36% 13,915.1 12,848.2 -‐7.67% (b) Other long term liabili@es 11.0 12.5 0.0 0.0 2.8 -‐74.71% 0.00% 11.0 2.8 -‐74.71% (c) Long term provisions 312.7 512.9 567.4 605.6 2,854.8 813.08% 371.36% 312.7 2,854.8 813.08% (3) Current LiabiliCes (a) Short-‐term borrowings 4,078.8 4,981.4 5,001.0 3,491.0 2,930.4 -‐28.16% -‐16.06% 4,078.8 2,930.4 -‐28.16% (b) Trade payables 509.7 749.3 882.3 347.6 444.3 -‐12.84% 27.81% 509.7 444.3 -‐12.84% (c) Other current liabili@es 10,895.5 11,169.8 11,720.9 10,539.8 8,579.3 -‐21.26% -‐18.60% 10,895.5 8,579.3 -‐21.26% (d) Short-‐term provisions 69.3 71.5 71.4 74.4 66.5 -‐4.03% -‐10.57% 69.3 66.5 -‐4.03% Total 34,681.1 34,719.9 36,940.9 33,870.2 30,446.3 -‐12.21% -‐10.11% 34,681.1 30,446.3 -‐12.21% II. ASSETS (1) Non-‐current assets (a) Fixed assets (I) Tangible assets 9.7 8.1 7.2 6.7 15.3 56.91% 128.97% 9.7 15.3 56.91% (ii) Intangible assets 1.0 0.9 0.9 0.8 0.7 -‐27.46% -‐8.54% 1.0 0.7 -‐27.46% (b) Deferred tax assets (net) 32.7 31.8 32.1 31.7 0.0 -‐100.00% -‐100.00% 32.7 0.0 -‐100.00% (c) Long term loans and advances 18,106.0 17,902.2 18,079.1 16,393.2 16,566.3 -‐8.50% 1.06% 18,106.0 16,566.3 -‐8.50% (2) Current assets (a) Cash and bank balances 304.1 494.7 2,668.6 985.0 170.0 -‐44.09% -‐82.74% 304.1 170.0 -‐44.09% (b) Short-‐term loans and advances 16,227.6 16,282.2 16,153.0 16,452.8 13,694.0 -‐15.61% -‐16.77% 16,227.6 13,694.0 -‐15.61% Total 34,681.1 34,719.9 36,940.9 33,870.2 30,446.3 -‐12.21% -‐10.11% 34,681.1 30,446.3 -‐12.21%

43

Subsidiary - Shriram Equipment Finance Company Limited Details of Key Parameters (Profit & Loss Account)

ParCculars

Q4 Q1 Q2 Q3 Q4 % % Year ended

Year ended %

FY 2013 14 FY 2014 15 FY 2014 15 FY 2014 15 FY 2014 15 YoY QoQ FY 2014 FY 2015 YoY

Interest Income mn 1,320.9 1261.8 1393.4 1,280.3 888.7 -‐32.72% -‐30.59% 5439.3 4824.2 -‐11.31%

Less : Interest Expenses mn 766.6 751.4 746.8 741.6 686.6 -‐10.44% -‐7.42% 2897.6 2926.4 0.99%

Net Interest Income mn 554.3 510.4 646.6 538.7 202.1 -‐63.54% -‐62.48% 2541.7 1897.8 -‐25.33%

Other Income mn 0.1 0.1 0.1 0.6 8.0 14477.98% 1356.43% 0.2 8.8 4897.86%

OperaCng Income mn 554.4 510.5 646.7 539.3 210.1 -‐62.09% -‐61.03% 2541.9 1906.6 -‐24.99%

Profit a]er Tax mn 164.8 53.3 73.7 71.9 -‐2,371.3 -‐1538.90% -‐3396.99% 868.3 -‐2172.2 -‐350.16%

Cost to Income RaCo % 29.76 29.97 26.04 34.18 103.04 246.22% 201.47% 22.98 37.88 64.81%

EPS Rs. 16.47 5.33 7.36 7.19 -‐237.10 -‐1539.59% -‐3397.63% 86.81 (217.23) -‐350.25%

ROA % 1.88 0.62 0.83 0.82 (29.61) -‐1673.56% -‐3728.50% 2.59 (6.32) -‐343.70%

ROE % 13.71 4.34 5.92 5.70 (242.88) -‐1871.29% -‐4363.81% 19.34 (46.08) -‐338.32%

44

Subsidiary - Shriram Equipment Finance Company Limited Details of Key Parameters (Balance Sheet)

ParCculars

Q4 Q1 Q2 Q3 Q4 % % Year ended Year ended %

FY 2013 14 FY 2014 15 FY 2014 15 FY 2014 15 FY 2014 15 YoY QoQ FY 2014 FY 2015 YoY

Asset under Management mn 34,183.9 33981.9 33921.7 32,576.6 29,985.8 -‐12.28% -‐7.95% 34183.9 29,985.8 -‐12.28%

Gross NPA % 1.30 2.31 2.59 2.94 15.68 1108.86% 434.12% 1.30 15.68 1108.86%

Net NPA % 0.53 0.95 1.07 1.22 6.94 1207.45% 466.97% 0.53 6.94 1207.45%

Gross NPA mn 449.8 789.1 881.5 961.2 4,718.5 948.96% 390.91% 449.8 4,718.5 948.96%

Net NPA mn 181.3 318.8 356.7 394.0 1,893.1 944.15% 380.51% 181.3 1,893.1 944.15%

Coverage RaCo % 59.70 59.60 59.53 59.01 59.88 0.31% 1.47% 59.70 59.88 0.31%

CRAR % 19.82 20.22 20.69 21.80 15.12 -‐23.69% -‐30.62% 19.82 15.12 -‐23.69%

Book Value Rs. 238.90 244.26 251.74 259.08 22.00 -‐90.79% -‐91.51% 238.90 22.00 -‐90.79%

Profit and Loss Statement

45

Subsidiary - Shriram Automall India Limited

(Rs. in Mn)

Particulars Q4 Q1 Q2 Q3 Q4

FY 14 FY 15 FY 15 FY 15 FY 15 FY 14 FY 15

Income Revenue from operations 212.69 154.77 152.72 171.40 218.96 744.62 697.85 Other income 0.94 1.00 0.64 1.33 3.34 19.84 6.32 Total 213.63 155.77 153.38 172.73 222.30 764.46 704.17 Expenditure Employees Benefit expense 64.76 61.22 70.30 73.58 76.26 272.19 281.35 Finance cost 0.11 0.50 0.19 0.03 0.80 0.41 1.53 Depreciation and amortisation 6.19 9.04 6.53 4.70 0.42 32.26 20.69 Other expenses 92.80 71.52 66.46 69.22 75.18 335.25 282.36 Total 163.86 142.28 143.48 147.53 152.66 640.11 585.93 Profit/(Loss) before taxation 49.77 13.49 9.90 25.20 69.64 124.36 118.24 Provision for taxation Current tax 15.76 5.50 4.26 8.91 21.42 46.98 40.10 Less: MAT credit entitlement - - - - - - - Deferred tax liability / (Asset) (0.52) (3.45) 0.85 0.01 1.87 (5.25) (0.71) Total tax expense / (income) 15.24 2.05 5.11 8.92 23.29 41.73 39.39 Profit/(Loss) after tax from continuing operations 34.53 11.44 4.79 16.28 46.35 82.63 78.85 Earnings/(Loss) per share Basic & Diluted (Rs.) 1.15 0.38 0.16 0.54 1.54 2.75 2.63 Nominal Value of Share (Rs.) 10.00 10.00 10.00 10.00 10.00 10.00 10.00

Balance Sheet

46

Subsidiary - Shriram Automall India Limited

(Rs in mn)

Particulars Q4 Q1 Q2 Q3 Q4

FY 14 FY 15 FY 15 FY 15 FY 15 FY 14 FY 15 I. EQUITY AND LIABILITIES (1) Shareholders' Funds (a) Share capital 300.00 300.00 300.00 300.00 300.00 300.00 300.00 (b) Reserves and Surplus 80.26 89.01 94.21 111.94 158.58 80.26 158.58 (2) Current Liabilities (a) Short-term borrowings 0.01 1.40 0.88 - 59.10 0.01 59.10 (b) Trade payables 286.73 239.25 248.67 290.25 254.45 286.74 254.45 (c) Other current liabilities 12.42 9.18 16.12 11.88 12.32 12.42 12.32 (d) Short-term provisions 11.42 11.59 11.58 13.16 24.22 11.42 24.22 Total 690.85 650.43 671.46 727.23 808.67 690.85 808.67 II. ASSETS (1) Non-current assets (a) Fixed assets (i) Tangible assets 526.76 518.42 518.61 516.54 517.94 526.76 517.94 (ii) Intangible assets 4.21 2.69 1.56 1.49 1.42 4.21 1.42 (b) Deferred tax assets 11.22 14.67 13.82 14.86 12.99 11.22 12.99 (c) Long term loans and advances 14.80 21.55 19.84 13.92 17.57 14.80 17.57 (2) Current assets (a) Trade receivables 82.34 9.76 30.31 17.47 29.89 82.34 29.89 (b) Cash and bank balances 20.47 49.22 56.46 131.42 207.76 20.47 207.76 (c) Short-term loans and advances 31.01 34.09 30.65 31.19 19.89 31.01 19.89 (d) Other assets 0.04 0.03 0.21 0.34 1.21 0.04 1.21 Total 690.85 650.43 671.46 727.23 808.67 690.85 808.67

Forward Looking Statement Certain statements in this document with words or phrases such as “will”, “should”, etc., and similar expressions or variation of these expressions or those concerning our future prospects are forward looking statements. Actual results may differ materially from those suggested by the forward looking statements due to a number of risks or uncertainties associated with the expectations. These risks and uncertainties include, but are not limited to, our ability to successfully implement our strategy and changes in government policies. The company may, from time to time, make additional written and oral forward looking statements, including statements contained in the company’s filings with the stock exchanges and our reports to shareholders. The company does not undertake to update any forward-looking statements that may be made from time to time by or on behalf of the company.

About Shriram Transport Finance Co. Ltd. Shriram Transport Finance Co Ltd. is the largest asset financing NBFC with Assets on Balance sheet of Rs. 49,227.14 crores and off Balance sheet assets of Rs. 9,881.14 crores. The company is a leader in organized financing of pre-owned trucks with strategic presence in 5-12 year old trucks. It has a pan-India presence with a network of 741 branches, and employs 16,160 employees including 9,658 field officers. The company has built a strong customer base of approx. 1.20 mn. Over the past 35 years, it has developed strong competencies in the areas of loan origination, valuation of pre-owned trucks and collection. It has a vertically integrated business model and offers a number of products which include: Pre-owned CV financing, New CV financing and other loans like accidental repair loans, tyre loans and working capital finance, etc. For more information please visit www.stfc.in

Contact Us

For any Investor Relations queries please contact

Sanjay K. Mundra Shriram Transport Finance Co. Ltd

Email: [email protected] Tel. No. +91-22-40959507

Thank You