Investor Presentation January - 2017 - South Indian Bank Investor... · looking...

57

Experience Next Generation Banking Investor Presentation January - 2017

Transcript of Investor Presentation January - 2017 - South Indian Bank Investor... · looking...

Experience Next Generation Banking

Investor PresentationJanuary - 2017

2

Safe Harbor

No representation or warranty, express or implied is made as to, and no relianceshould be placed on, the fairness, accuracy, completeness or correctness of suchinformation or opinions contained herein. The information contained in thispresentation is only current as of its date. Certain statements made in thispresentation may not be based on historical information or facts and may be “forwardlooking statements”, including those relating to the Company’s general business plansand strategy, its future financial condition and growth prospects, and futuredevelopments in its industry and its competitive and regulatory environment. Actualresults may differ materially from these forward-looking statements due to a numberof factors, including future changes or developments in the Company’s business, itscompetitive environment and political, economic, legal and social conditions in India.This communication is for general information purpose only, without regard tospecific objectives, financial situations and needs of any particular person. Thispresentation does not constitute an offer or invitation to purchase or subscribe forany shares in the Company and neither any part of it shall form the basis of or berelied upon in connection with any contract or commitment whatsoever. TheCompany may alter, modify or otherwise change in any manner the content of thispresentation, without obligation to notify any person of such revision or changes. Thispresentation can not be copied and/or disseminated in any manner.

3

Contents

About Us

Q3 FY17 Highlights

Performance Matrix

Next Generation Bank

An Inflection Point

Business Strategy

4

Q3 FY17 Highlights

5

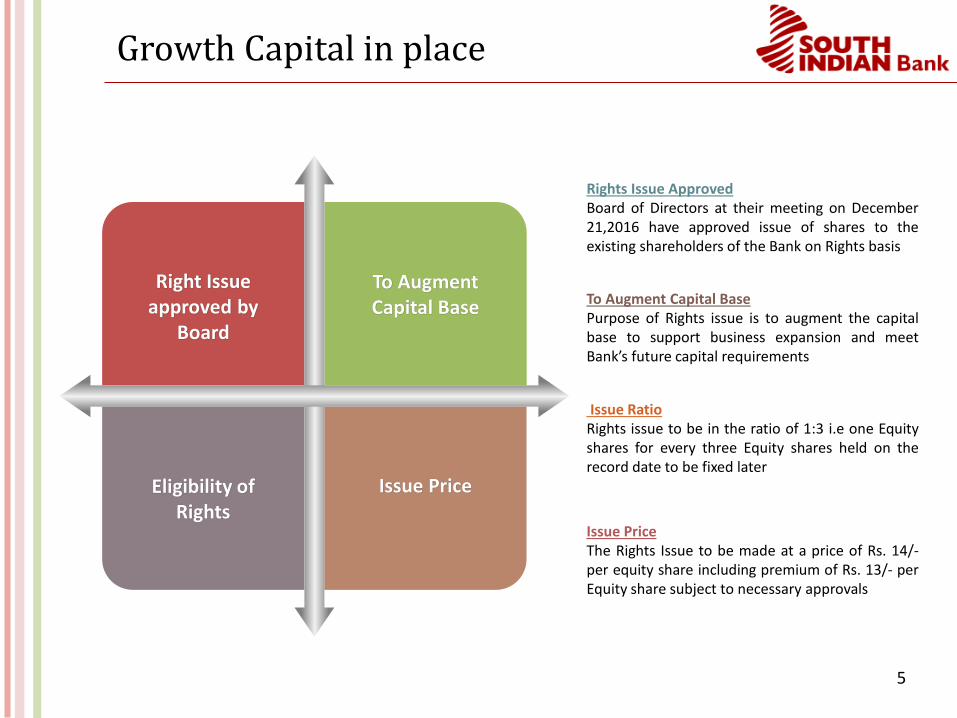

Growth Capital in place

Right Issue approved by

Board

To Augment Capital Base

Eligibility of Rights

Issue Price

Rights Issue ApprovedBoard of Directors at their meeting on December21,2016 have approved issue of shares to theexisting shareholders of the Bank on Rights basis

Issue RatioRights issue to be in the ratio of 1:3 i.e one Equityshares for every three Equity shares held on therecord date to be fixed later

Issue PriceThe Rights Issue to be made at a price of Rs. 14/-per equity share including premium of Rs. 13/- perEquity share subject to necessary approvals

To Augment Capital BasePurpose of Rights issue is to augment the capitalbase to support business expansion and meetBank’s future capital requirements

6

Representative Office in Dubai, UAE

01

02

03

RBI Approval Received foropening RepresentativeOffice in Dubai, UAE

Representative office is inaddition to extensivearrangements with leadingexchange houses

Representative office willboost NRI Banking effortsfor the Bank and expandNRI Customer base

7

Key Performance Highlights- Q3 FY17

Rs in Crores Q3 FY17 Q3 FY16 Growth

PPOP 377 263 43.3%

EBIDTA 17 41 26%Deposits 63,595 53,441 19.0%

Advances 45,234 40,601 11.4%

CASA 16,486 12,307 34.0%

PAT 111.4 101.6 9.6%

8

UPI Integration – Ahead of the Curve

SIB M-Pay is one of the first Mobile Banking Applications to be powered with UPI Service

9

Recent Awards

South Indian Bank receives the FIEO Export Excellence Award 2014-15 in the Best Financial Institution Category (Southern Region) from Smt. Nirmala Sitharaman, Hon’ble Minister of State

(Independent Charge) for Commerce & Industry, Govt of India

10

Business Strategy

11

Our Strategy…

• Focus on retail loan products

• Efficient branches for faster processing of loans

• Continuous training of work force

• Invest in Brand Building

Expand Retail

Business

• Cluster based approach in industry hubs

• Sole Banker to SMEs for all banking needs

• Dedicated vertical to penetrate SME banking

Strengthen SME Base

• Strategy & Road map in place to increase CASA funds

• Centralized processes allowing branches to focus on garnering low cost funds

Improve CASA

• Granulize loan portfolio to spread out risk

• Cautious approach on large corporate lending

• Special recovery cell for monitoring non performing and restructured assets

Enhance Asset

Quality

• Focus on increasing banking services for SME, Retail & NRI clients

• Enhance treasury capabilities & increase branch strength

• Expand PoS & ATM Network

Improve share of

other Income

12

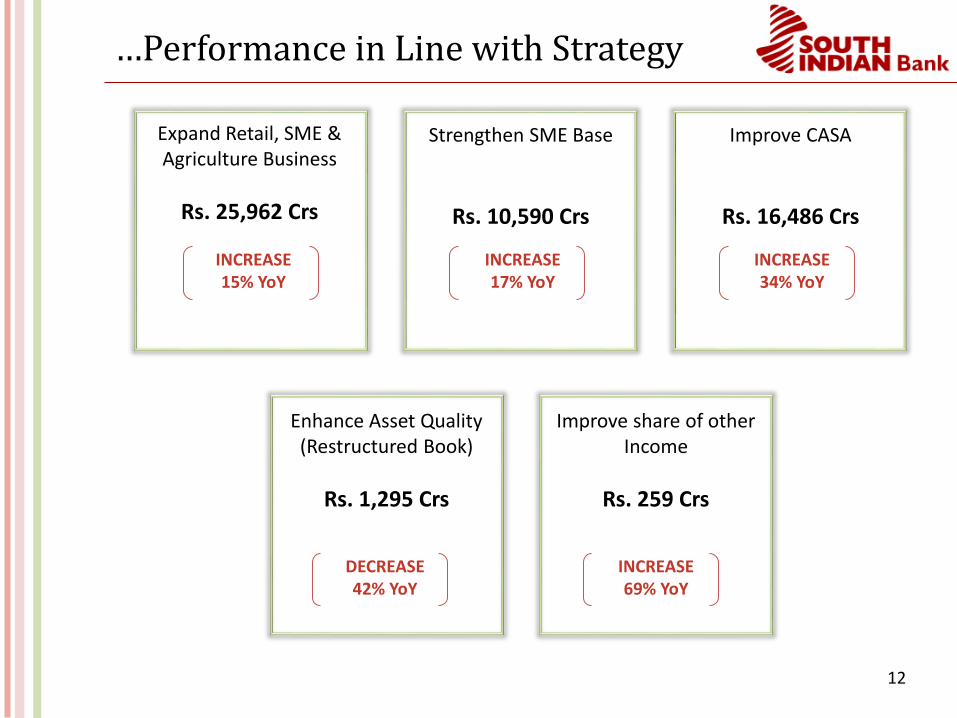

…Performance in Line with Strategy

INCREASE15% YoY

Expand Retail, SME & Agriculture Business

Rs. 25,962 Crs

Strengthen SME Base

Rs. 10,590 Crs

Improve CASA

Rs. 16,486 Crs

Enhance Asset Quality(Restructured Book)

Rs. 1,295 Crs

Improve share of other Income

Rs. 259 Crs

INCREASE17% YoY

INCREASE34% YoY

DECREASE42% YoY

INCREASE69% YoY

13

Shall continue to focus on Core Strengths

01 Increase …

CASA

02 Retail Business …

More Products

03 SME Business …

Sole Banker

04 Improve

NIM

05 Increase…

Fee Income

06 Sustainable…

Asset Quality

RetailRelationships

SMERelationships

14

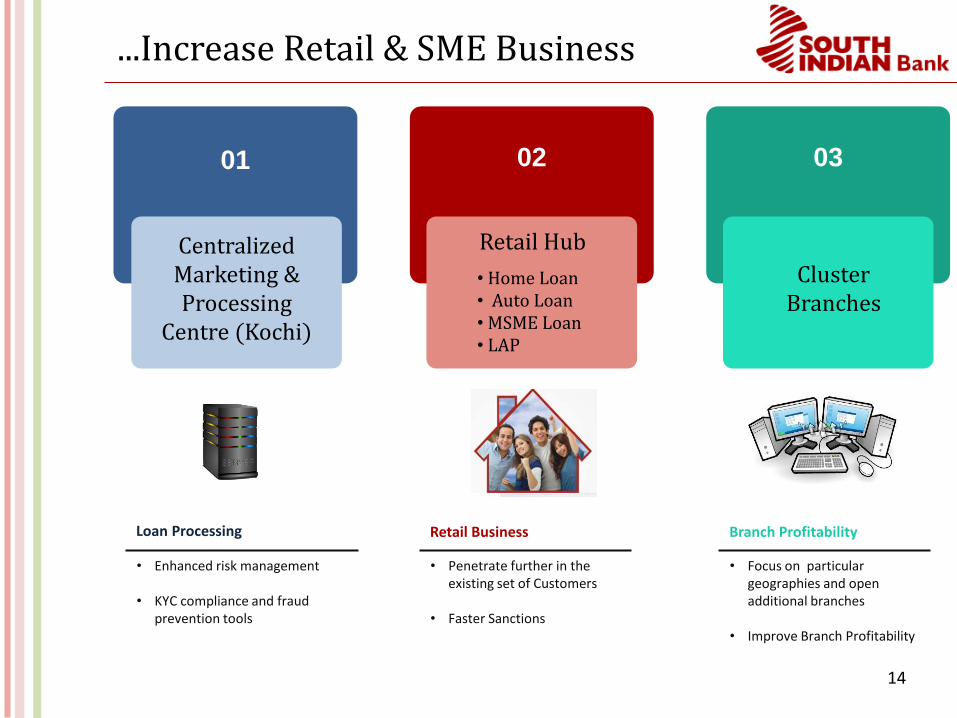

...Increase Retail & SME Business

• Enhanced risk management

• KYC compliance and fraud prevention tools

Loan Processing

• Penetrate further in the existing set of Customers

• Faster Sanctions

Retail Business

• Focus on particular geographies and open additional branches

• Improve Branch Profitability

Branch Profitability

Centralized Marketing & Processing

Centre (Kochi)

01 02 03

Retail Hub

• Home Loan• Auto Loan• MSME Loan• LAP

Cluster Branches

15

…by focus on Housing Loans in Retail

2,499 2,614 2,677 2,756

1,455 1,371 1,417 1,432

1,501 1,564 1,510 1,535

1,9982,521 2,410 2,446

872

973 9251,0941,057

1,049 1,0631,094

2,828

1,290

1,606

2,622

909

1,154

10,358 10,409

Jun-16

10,002

Mar-16 Dec-16Sep-16

9,382

Dec-15

10,093

Retail Breakup

Others

HousingLAD* Manufacturing

Service & Traders Gold

Housing: Key Initiatives

• Retail hub in Kochi to increase focus on housing finance

• Two more hubs to be set up – one in South India and one in North India

• Branch staff being given specific training to market mortgage loans

• Marketing initiative through TVCs

• Tailor made products for different segments

Oct to Dec 2016

• Housing Loans Sanctioned : 807 Nos.

• Amount of Housing Loans Sanctioned – 182 Crs

Rs Crs

*LAD = Loan against deposits

16

…becoming a Banker of Choice to SMEs

Loan Book by Geography – Q3 FY17

• Dedicated DGM appointed to ensure focus and better coordination with regions

• Focused ‘Green Channel’ branches to drive faster loan growth to SMEs

• Target to become banker of choice to SMEs thereby getting other business as well –liabilities, vehicle finance, etc.

• Ongoing training (in-house as well as external)

SME Highlights

Average SME Loan / Account

16.1015.7615.5615.3315.26

Jun-16Dec-15 Sep-16 Dec-16Mar-16

Kerala43%

South (Ex-Kerala)

34%

Rest of India23%

Rs Lakhs

17

…with the help of our Branch Network

Branch Location*No of

Branches

Kerala 455

South India (Ex-Kerala) 245

Rest of India 140

Total 840

Total Branch Network

Total ATM Network

840834822794738688

FY13FY12 9M FY17FY16FY15FY14

+4.1%

1,3131,2871,200

1,000800

663

FY12 FY13 9M FY17FY16FY14 FY15

+14.6%

*Map for illustration purpose only

18

… and our Experienced Employees

Total Employees: 6,983*

3% 5%

37%

31%

24%

< 1 Year 1-2 Years 2-5 Years

5-10 Years > 10 Years

Employee Addition

41

32 53

Sep-16Jun-16 Dec-16 Closing

6,983

Mar-16Dec-15

7,048

*Employees include full-time officers and clerks.

19

Performance Matrix

20

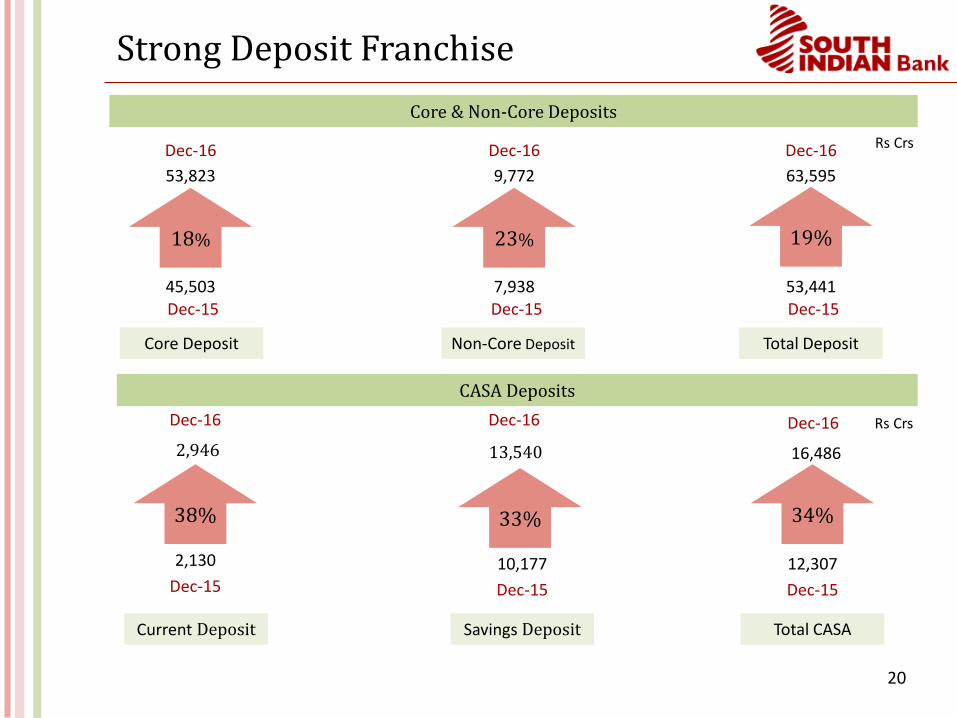

Strong Deposit Franchise

Core & Non-Core Deposits

CASA Deposits

18%

Core Deposit Non-Core Deposit Total Deposit

Dec-16 Dec-16

Dec-15 Dec-1545,503

53,823

53,441

63,595

19%

Current Deposit Savings Deposit Total CASA

Dec-16 Dec-16 Dec-16

Dec-15 Dec-15 Dec-15

2,130 10,177

13,540

12,307

16,486

38% 33% 34%

2,946

Rs Crs

Rs Crs

23%

Dec-16

Dec-157,938

9,772

21

Core Deposits Growing...

Breakup of Deposits

7,930 9,203 9,205 10,215 9,693

10,177 10,476 11,267 11,299 13,540

33,20434,059

35,23036,279

37,415

2,946

Dec-16Sep-16Jun-16

2,187 2,399

60,19257,889

Mar-16

53,441

2,130 1,983

55,721

Dec-15

63,595

Term Others*CurrentSavings

CASA Deposit

12,3072,130

Dec-15 Dec-16

10,177

16,486

13,540

2,946

+34%

Term Deposits

37,41533,204

Dec-15

+13%

Dec-16

Rs Crs Rs Crs

SavingsCurrent

Rs Crs

*Others includes: Bulk, Certificates of Deposits

22

NRI Deposits Growing…

23.0 22.4

23.2 22.8

25.9

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

CASA NRI Deposits

16,31715,476

15,02514,303

13,566

Mar-16Dec-15 Jun-16 Dec-16Sep-16

+20%

In (%)Rs Crs

23

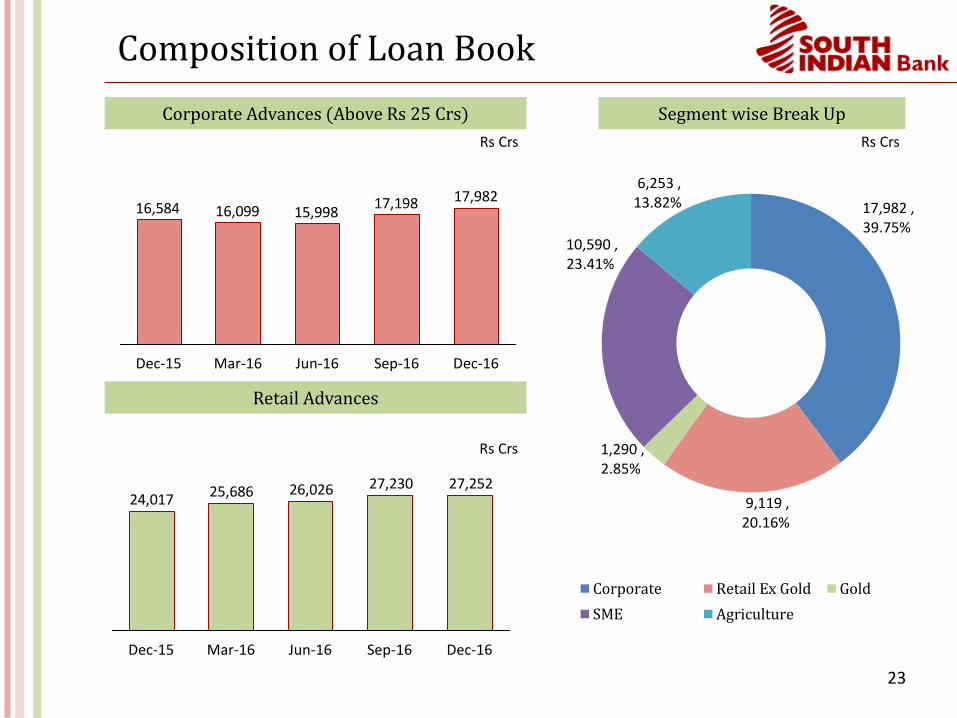

17,982 , 39.75%

9,119 , 20.16%

1,290 , 2.85%

10,590 , 23.41%

6,253 , 13.82%

Corporate Retail Ex Gold Gold

SME Agriculture

Composition of Loan Book

27,25227,23026,02625,68624,017

Dec-16Dec-15 Jun-16Mar-16 Sep-16

Segment wise Break UpCorporate Advances (Above Rs 25 Crs)

Rs Crs Rs Crs

17,98217,19815,99816,09916,584

Sep-16Mar-16Dec-15 Jun-16 Dec-16

Retail Advances

Rs Crs

24

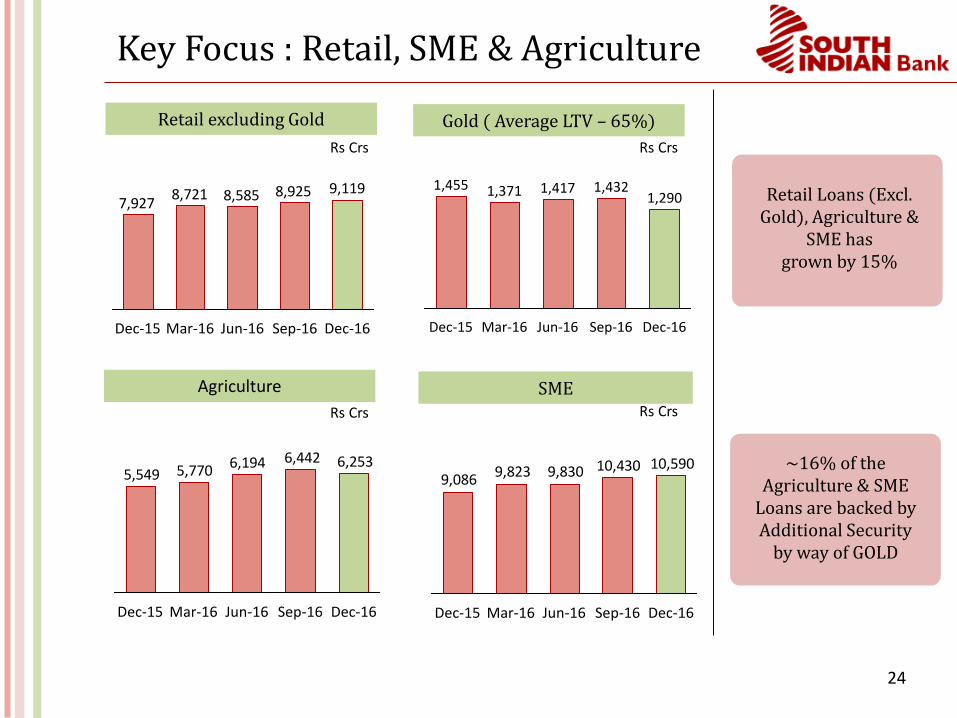

Key Focus : Retail, SME & Agriculture

Retail excluding Gold Gold ( Average LTV – 65%)

SMEAgriculture

8,9258,5858,7217,927

9,119

Dec-16Sep-16Jun-16Mar-16Dec-15

1,4321,3711,455

Mar-16

1,417

Dec-15 Dec-16Sep-16Jun-16

1,290

10,4309,8309,8239,08610,590

Dec-16Sep-16Jun-16Mar-16Dec-15

6,4426,1945,7705,5496,253

Sep-16 Dec-16Mar-16 Jun-16Dec-15

~16% of the Agriculture & SME

Loans are backed byAdditional Security

by way of GOLD

Retail Loans (Excl. Gold), Agriculture &

SME has grown by 15%

Rs Crs

Rs Crs

Rs Crs

Rs Crs

25

Advances growing across Regions

14,983 15,680 15,994 17,092 17,548

13,17813,556 13,315

13,923 14,054

12,44012,549 12,715

13,413 13,632

44,428

Dec-16Sep-16

40,60142,02441,785

Dec-15 Mar-16

45,234

Jun-16

South Ex- KeralaRest of India Kerala

Rs Crs

26

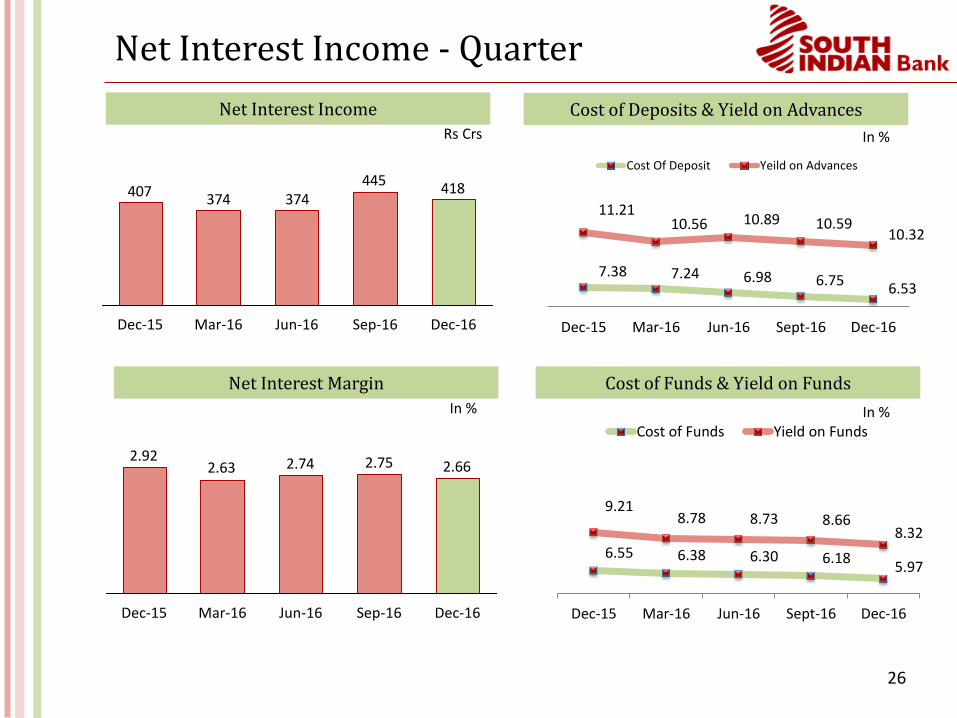

Net Interest Income - Quarter

Net Interest Income

418445

374374407

Sep-16Mar-16 Jun-16Dec-15 Dec-16

Cost of Deposits & Yield on Advances

Net Interest Margin

2.662.752.742.632.92

Sep-16Jun-16 Dec-16Mar-16Dec-15

Cost of Funds & Yield on Funds

Rs Crs

In %

In %

6.55 6.38 6.30 6.185.97

9.218.78 8.73 8.66

8.32

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Cost of Funds Yield on FundsIn %

7.38 7.24 6.98 6.75 6.53

11.21 10.56 10.89 10.59

10.32

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Cost Of Deposit Yeild on Advances

27

Net Interest Income - Cumulative

Net Interest Income

1,236

819

374

1,510

1,135

Dec-16Sep-16Jun-16Mar-16Dec-15

7.58 7.526.98 6.86 6.75

11.3611.18 10.89 10.73

10.59

Dec-15 Mar -16 Jun -16 Sept -16 Dec -16

Cost of Deposits Yield on Advances

Cost of Deposits & Yield on Advances

Net Interest Margin

2.722.752.742.732.76

Sep-16Dec-15 Mar-16 Dec-16Jun-16

Cost of Funds & Yield on Funds

Rs Crs

In %

In %

6.77 6.69 6.30 6.32 6.20

9.29 9.18 8.73 8.80 8.63

Dec-15 Mar -16 Jun -16 Sept-16 Dec-16

Cost of Funds Yield on FundsIn %

28

Improving Operating Efficiency

56.60 56.62

52.5751.08

48.53

Dec-15 Mar -16 Jun -16 Sept -16 Dec -16

C/I Ratio

Business per Employee Business per Branch

13.513.213.012.011.9

Dec-15 Dec-16Jun-16Mar-16 Sep-16

119117115108108

Mar-16 Dec-16Dec-15 Jun-16 Sep-16

Employee Additions

-75

-41-32

3 5

Dec-15 Mar -16 Jun -16 Sept -16 Dec -16

In %

Rs Crs Rs Crs

29

Sustainable Other Income

…Sustainable : Transaction Fees + Technology

23 23 25 26

44 52 54 48

22

45

Dec-16

74

Jun-16 Sep-16Mar-16

7976

Dec-15

67 67

Total Other Income led by ….

TechnologyTransaction Fees

Investment Book as on Dec-16

Rs Crs Rs Crs

50 57 5123

30

1271314

57

5102422

Dec-16Jun-16 Sep-16

16

8

Mar-16Dec-15

OtherForex Profit on Sale of Investments

Profit on Sale of Investments, Forex & Others

Rs Crs

259

146173

139153

Dec-15 Jun-16Mar-16 Sep-16 Dec-16

Details Rs. Crs M Duration

HTM 13,492 5.61

AFS 4,161 4.38

HFT 1 -

Total 17,654 5.36

30

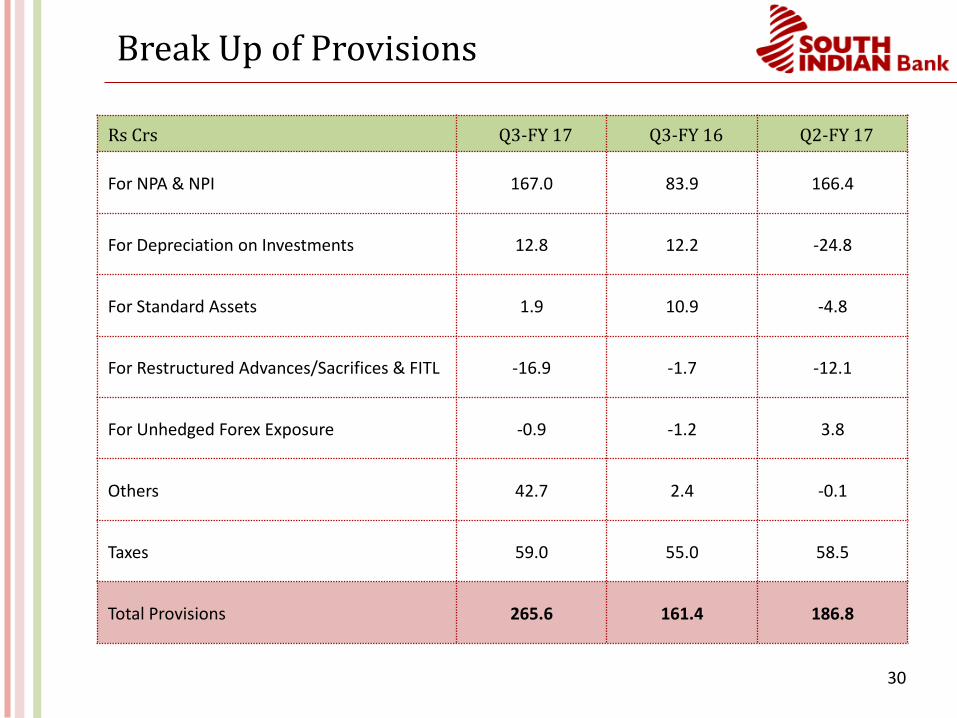

Break Up of Provisions

Rs Crs Q3-FY 17 Q3-FY 16 Q2-FY 17

For NPA & NPI 167.0 83.9 166.4

For Depreciation on Investments 12.8 12.2 -24.8

For Standard Assets 1.9 10.9 -4.8

For Restructured Advances/Sacrifices & FITL -16.9 -1.7 -12.1

For Unhedged Forex Exposure -0.9 -1.2 3.8

Others 42.7 2.4 -0.1

Taxes 59.0 55.0 58.5

Total Provisions 265.6 161.4 186.8

31

Non Performing Assets

Net NPA

1.80%

2.89% 2.89% 2.77%2.52%

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Gross NPA

2.75%

3.77% 3.96% 3.96% 3.98%

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Net NPA MovementGross NPA Movement

Rs Crs Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Opening 892 1,108 1,562 1,651 1,745

Additions 367 845 125 226 197

Deductions 151 391 36 132 155

Closing 1,108 1,562 1,651 1,745 1,787

Rs Crs Dec-15 Mar-16 Jun-16 Sept -16 Dec -16

Opening 550 716 1,185 1,192 1,206

Additions 311 664 105 135 125

Deductions 145 195 98 121 216

Closing 716 1,185 1,192 1,206 1,116

32

Restructured Advances Breakup

Restructured Assets Break-up

949 945761

642

306

443 442

532653

2,236

1,930

Dec-16Sep-16

1,293 1,2951,387

Mar-16

1,392

Jun-16Dec-15

Restructured Standard Advance

Restructured NPA

Sector Standard Restructure – Q3FY17

17%

49%

34%

Power DiscomsConstruction EPCOthers

Rs Crs

*Other includes IT, Bullion, etc.

Government’s Uday Scheme

targeted towards power Discomsbenefiting SIB

Benefits of Udaygetting reflected in Restructured

Book

UDAY Scheme to Benefit

33

Restructured Standard Advance

Restructured Standard Asset BookRs Crs

113 0 0

411 0 0

237 1 0

DISCOMS

OpeningIncrease in

Existing Balance

Uday – SDLInvestments

Construction EPC

Others

0

-98

-16

Slippages to NPA

761 1 0Total -114

111

313

218

Closing Balance

642

0

0

0

Fresh Addition

0

-2

0

-4

Decrease in Balance

-6

34

Movement in Restructured Accounts

Movement in Restructured Accounts

1,2951,293

Upgradation in Standard

Category

ClosingClosure incl

write-off

Dec. in Balance

6

Inc. in Balance

20

Opening Fresh Additions

00 12

Shift of focus from Large Corporate

toSMEs

Defocusing from Power & Infra Sectors

Special Recovery Cell &

Asset Monitoring Cell

Rs Crs

35

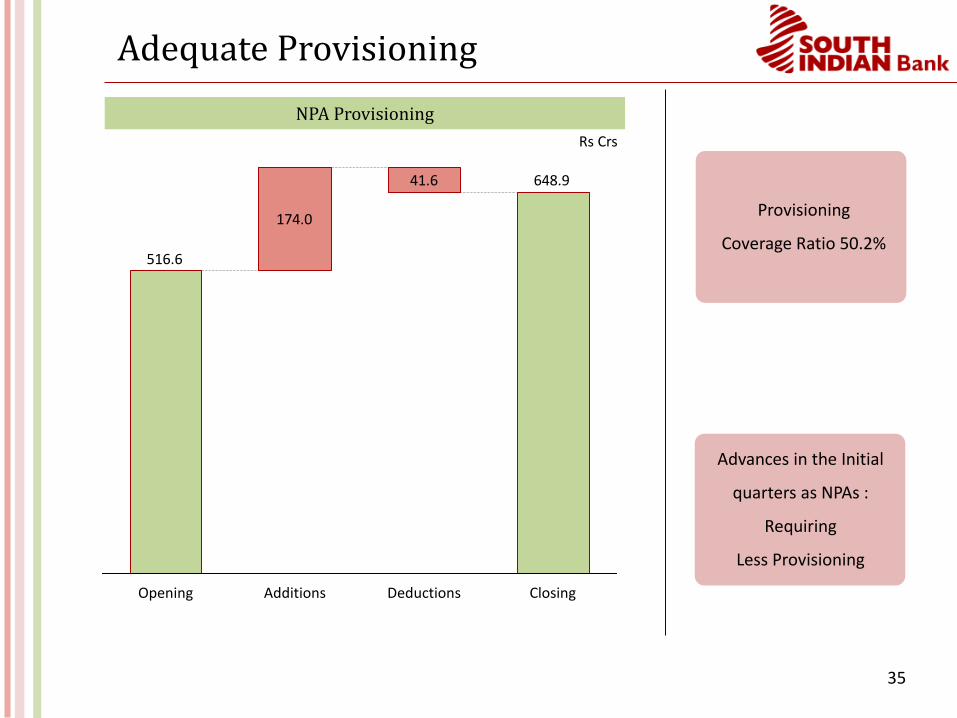

Adequate Provisioning

NPA Provisioning

174.0

516.6

648.941.6

DeductionsAdditions ClosingOpening

Provisioning

Coverage Ratio 50.2%

Advances in the Initial

quarters as NPAs :

Requiring

Less Provisioning

Rs Crs

36

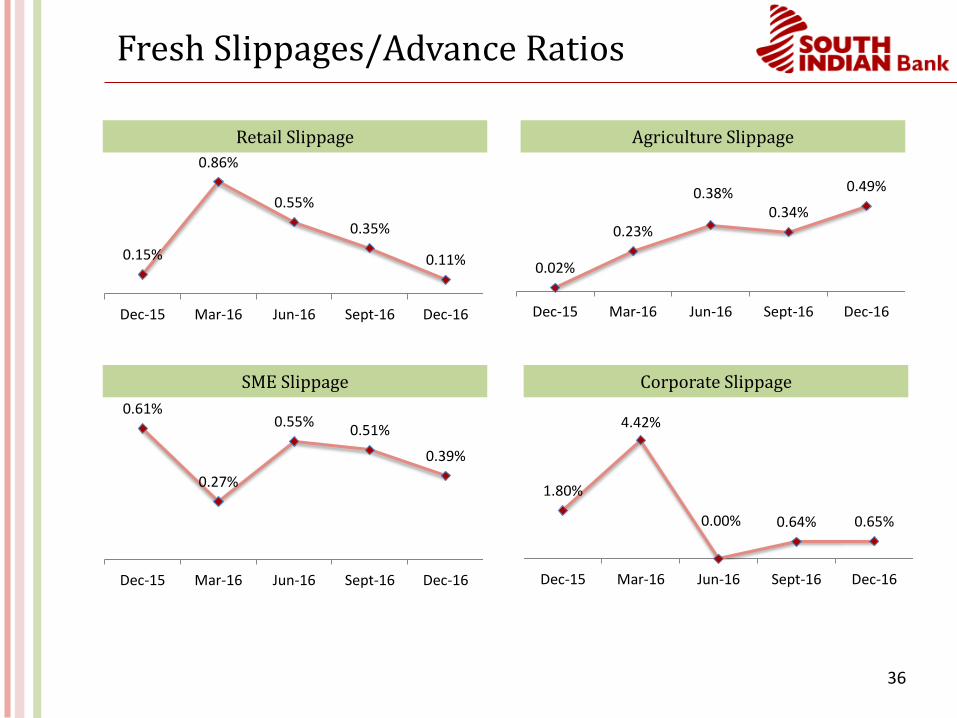

Fresh Slippages/Advance Ratios

SME Slippage

Retail Slippage

Corporate Slippage

0.15%

0.86%

0.55%

0.35%

0.11%

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

Agriculture Slippage

0.02%

0.23%

0.38%0.34%

0.49%

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

0.61%

0.27%

0.55%0.51%

0.39%

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

1.80%

4.42%

0.00% 0.64% 0.65%

Dec-15 Mar-16 Jun-16 Sept-16 Dec-16

37

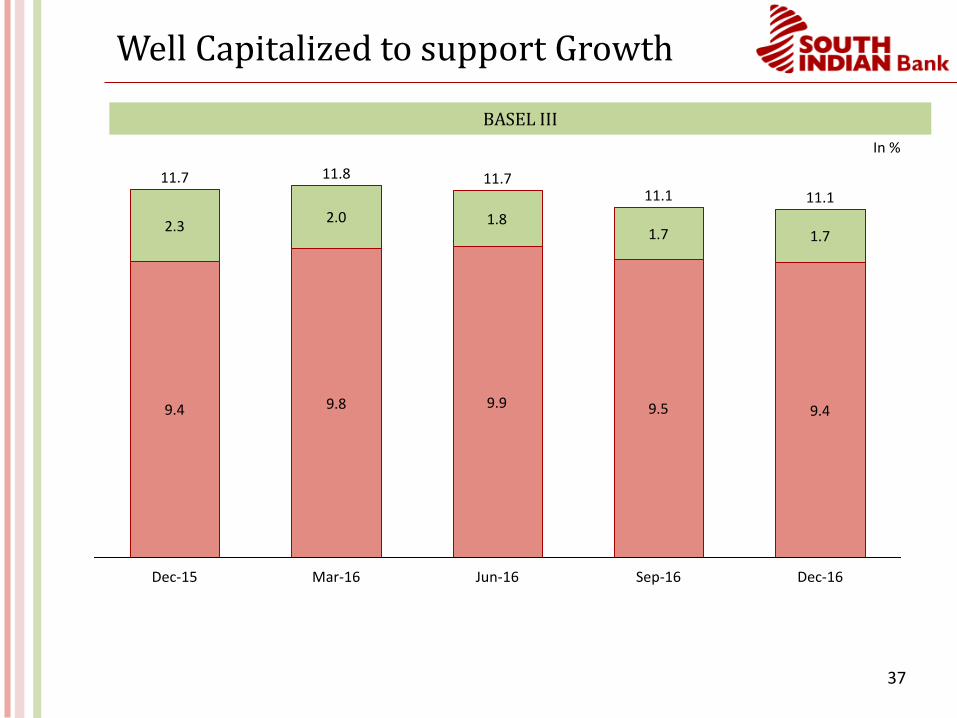

Well Capitalized to support Growth

BASEL III

9.4 9.8 9.9 9.5

2.32.0 1.8

1.7

9.4

1.7

Dec-15

11.811.711.1

Dec-16Sep-16Mar-16

11.7

Jun-16

11.1

In %

38

Balance Sheet Overview- Q3 FY17

Rs Crs Q3-FY 17 Q3-FY 16 Y-o-Y (%) Q2-FY 17 Q-o-Q (%)

Capital & Liabilities 71,446 60,269 18.55% 67,054 6.55%

Capital 135 135 0.12% 135 0.08%

Reserves and Surplus 4,141 3,715 11.48% 4,027 2.85%

Deposits 63,595 53,441 19.00% 60,192 5.65%

Borrowings 2,205 1,665 32.45% 1,499 47.13%

Other Liabilities & Provisions 1,369 1,312 4.34% 1,201 14.00%

Assets 71,446 60,269 18.55% 67,054 6.55%

Cash & Balances with RBI 3,576 2,367 51.10% 2,832 26.28%

Balances with Banks 1,420 249 471.30% 404 251.18%

Investments 17,576 13,259 32.56% 15,777 11.40%

Advances 44,256 39,909 10.89% 43,548 1.63%

Fixed Assets 595 485 22.51% 598 -0.57%

Other Assets 4,023 4,000 0.59% 3,894 3.32%

Business (Advances + Deposits) 107,850 93,350 15.53% 103,740 3.96%

Current Accounts 2,946 2,130 38.32% 2,399 22.83%

Savings Accounts 13,540 10,177 33.04% 11,299 19.83%

CASA Ratio 25.92% 23.03% 289 bps 22.76% 317 bps

39

Profit & Loss Overview- Q3 FY17

Rs Crs Q3-FY17 Q3-FY 16 Y-o-Y (%) Q2-FY17 Q-o-Q (%)

Net Interest Income 417.52 406.72 2.66% 445.18 -6.21%

Other Income 258.51 153.32 68.61% 145.90 77.18%

Total Income 676.03 560.04 20.71% 591.08 14.37%

Operating Expenses 299.06 296.97 0.70% 293.74 1.81%

Operating Profit 376.97 263.07 43.30% 297.34 26.78%

Provisions (Ex-Tax) & Contingencies

206.63 106.39 94.22% 128.33 61.01%

Profit Before Tax 170.34 156.68 8.72% 169.01 0.79%

Provision for Tax 58.96 55.05 7.10% 58.49 0.80%

Profit After Tax 111.38 101.63 9.59% 110.52 0.78%

40

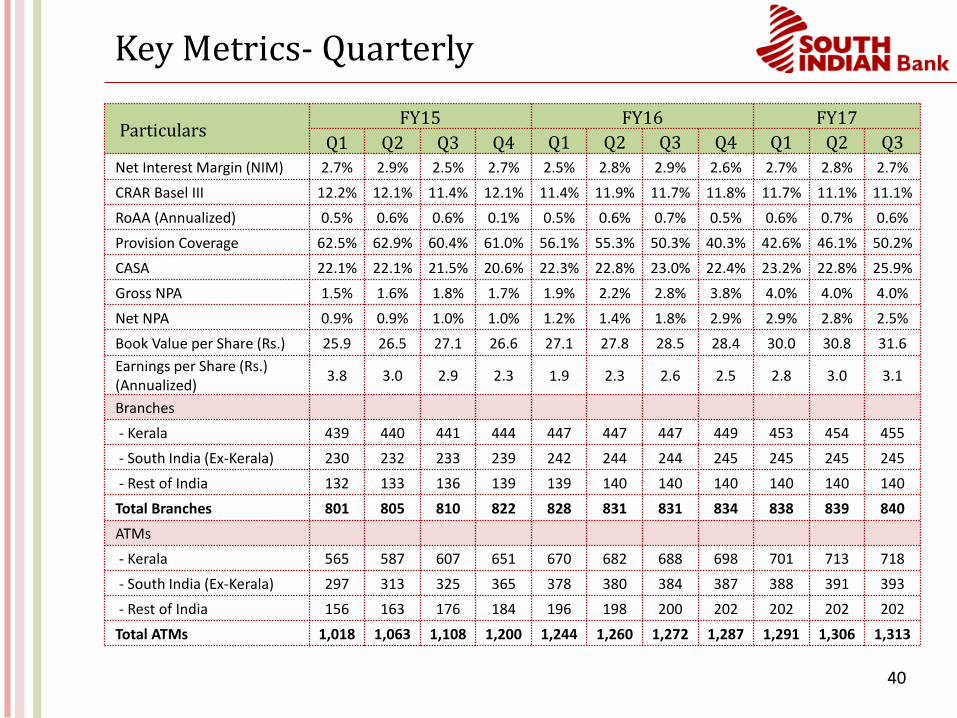

Key Metrics- Quarterly

Particulars FY15 FY16 FY17

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

Net Interest Margin (NIM) 2.7% 2.9% 2.5% 2.7% 2.5% 2.8% 2.9% 2.6% 2.7% 2.8% 2.7%

CRAR Basel III 12.2% 12.1% 11.4% 12.1% 11.4% 11.9% 11.7% 11.8% 11.7% 11.1% 11.1%

RoAA (Annualized) 0.5% 0.6% 0.6% 0.1% 0.5% 0.6% 0.7% 0.5% 0.6% 0.7% 0.6%

Provision Coverage 62.5% 62.9% 60.4% 61.0% 56.1% 55.3% 50.3% 40.3% 42.6% 46.1% 50.2%

CASA 22.1% 22.1% 21.5% 20.6% 22.3% 22.8% 23.0% 22.4% 23.2% 22.8% 25.9%

Gross NPA 1.5% 1.6% 1.8% 1.7% 1.9% 2.2% 2.8% 3.8% 4.0% 4.0% 4.0%

Net NPA 0.9% 0.9% 1.0% 1.0% 1.2% 1.4% 1.8% 2.9% 2.9% 2.8% 2.5%

Book Value per Share (Rs.) 25.9 26.5 27.1 26.6 27.1 27.8 28.5 28.4 30.0 30.8 31.6

Earnings per Share (Rs.) (Annualized)

3.8 3.0 2.9 2.3 1.9 2.3 2.6 2.5 2.8 3.0 3.1

Branches

- Kerala 439 440 441 444 447 447 447 449 453 454 455

- South India (Ex-Kerala) 230 232 233 239 242 244 244 245 245 245 245

- Rest of India 132 133 136 139 139 140 140 140 140 140 140

Total Branches 801 805 810 822 828 831 831 834 838 839 840

ATMs

- Kerala 565 587 607 651 670 682 688 698 701 713 718

- South India (Ex-Kerala) 297 313 325 365 378 380 384 387 388 391 393

- Rest of India 156 163 176 184 196 198 200 202 202 202 202

Total ATMs 1,018 1,063 1,108 1,200 1,244 1,260 1,272 1,287 1,291 1,306 1,313

41

Next Generation Bank

42

Present across Customer Touch Points

Mobile Banking Mobile Banking

Point of SaleInternet Banking

ATMs

1,313 ATMs across India

Branches

840 Branches & 45 Extension Counters

Traditional & Alternate Channels

43

Technology Initiatives

SIB Mirror is a mobile-led platform with instant account access, balance retrieval, immediate fund transfers, all account intimations, and much more

SIB-er Net is a suite of comprehensive internet banking services positioning SIB as a technology-driven bank offering superior services to retail customers

Retail branches now interconnected with single-window service and providing real-time online, real-time transactions to customers

SIB offers Visa, MasterCard, and RuPay debit cards with online access to users for secure domestic and international transactions

Centralized Processing Center allows enhanced risk management and customer creation with complete KYC compliance and fraud prevention tools

SIB has offered new initiatives such as Co-branded Credit Cards with SBI and is amongst the 1st to introduce M-Pay a mobile banking application powered with UPI Service

44

Personal Banking: Technology Banking

Active Internet Users

133 134 141 157

175

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

Mobile Transaction Volume

Internet Transaction Volume Internet Transaction Value

Mobile Transaction Value

785663611591

1,254

Dec-16Dec-15 Sep-16Mar-16 Jun-16

3,2933,054

2,5512,5152,385

Dec-16Sep-16Dec-15 Jun-16Mar-16

1,175

913

748670

507

Dec-16Sep-16Jun-16Mar-16Dec-15

599

350

233170

124

Sep-16 Dec-16Dec-15 Jun-16Mar-16

(000)’s (000)’s

(000)’s

Rs Crs

Rs Crs

45

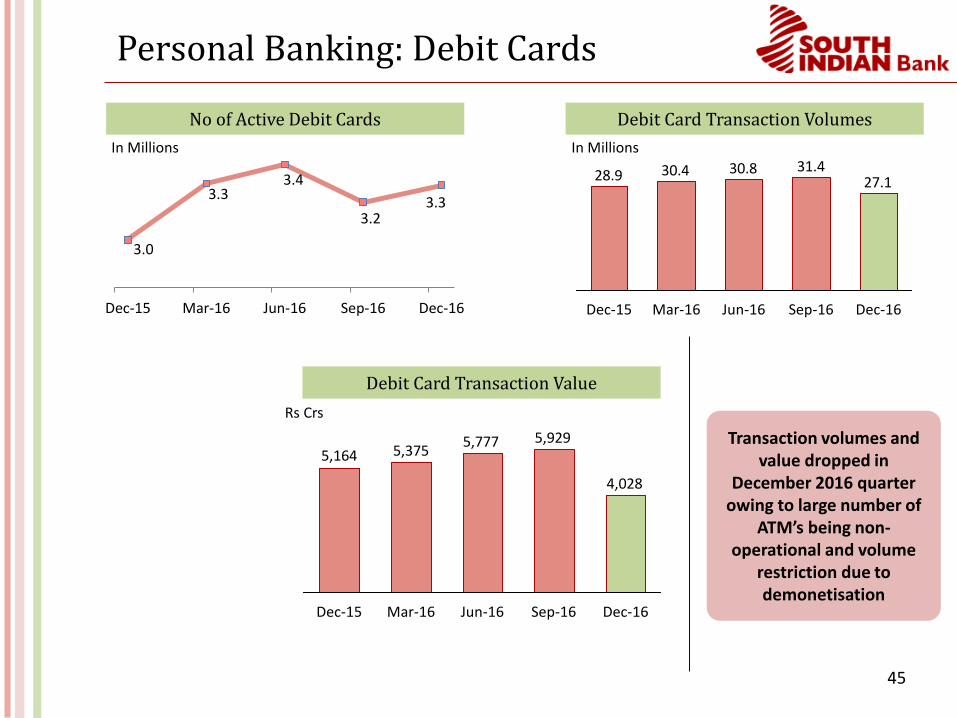

Personal Banking: Debit Cards

3.0

3.3 3.4

3.2 3.3

Dec-15 Mar-16 Jun-16 Sep-16 Dec-16

No of Active Debit Cards Debit Card Transaction Volumes

Debit Card Transaction Value

27.131.430.830.428.9

Jun-16Mar-16 Sep-16Dec-15 Dec-16

4,028

5,9295,7775,3755,164

Mar-16 Jun-16Dec-15 Sep-16 Dec-16

In Millions In Millions

Rs Crs

Transaction volumes and value dropped in

December 2016 quarter owing to large number of

ATM’s being non-operational and volume

restriction due to demonetisation

46

An Inflection Point

47

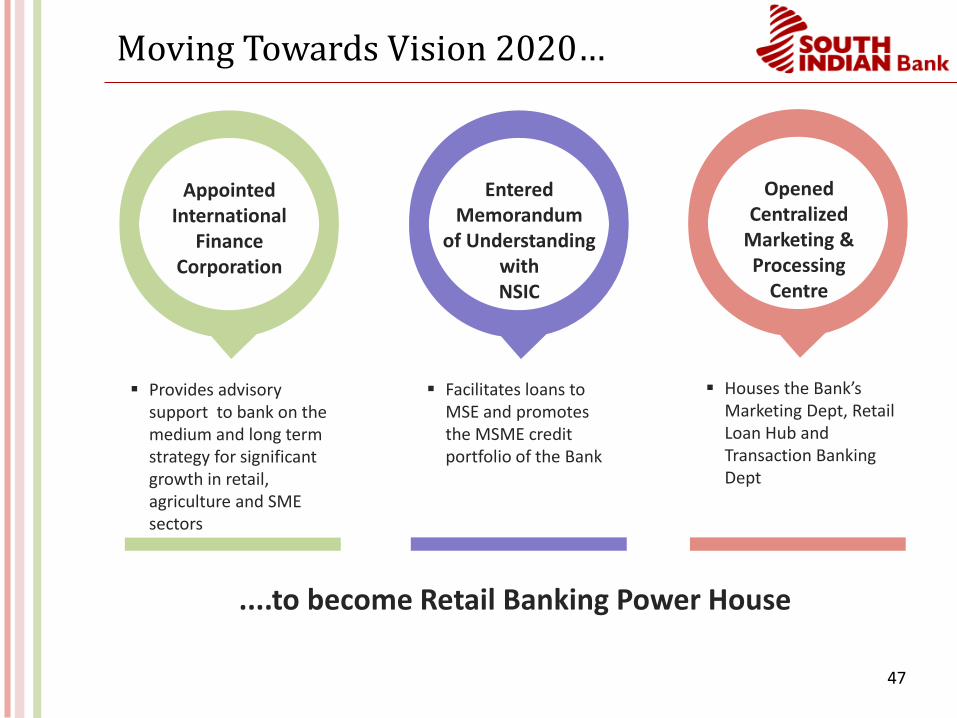

Moving Towards Vision 2020…

Provides advisory support to bank on the medium and long term strategy for significant growth in retail, agriculture and SME sectors

Appointed International

Finance Corporation

Facilitates loans to MSE and promotes the MSME credit portfolio of the Bank

Entered Memorandum

of Understanding with NSIC

Houses the Bank’s Marketing Dept, Retail Loan Hub and Transaction Banking Dept

Opened Centralized

Marketing & Processing

Centre

....to become Retail Banking Power House

48

About Us

49

Milestones

FIRST among the private sector banks in Kerala to

become a scheduled bank in 1946 under the RBI Act

FIRST bank in the private sector in India to open a

Currency Chest on behalf of the RBI in April 1992

FIRST private sector bank to open a NRI branch in

November 1992

FIRST bank in the private sector to start Industrial Finance

Branch in March 1993

FIRST among the private sector banks in Kerala to open an "Overseas Branch" to cater

exclusively to the export and import business in June 1993

FIRST bank in Kerala to develop an in-house, a fully integrated branch automation software in addition to

the in-house partial automation solution operational since 1992

The FIRST Kerala based bank to implement Core Banking System

50

Expansion over a Decade

Branch Network

140121

245263

449

56

FY16FY06

440

~2X

834

Kerala South Ex-Kerala Others (Rest of India)

ATM Network

698

202

387

66

1,287

144

40

~9x

FY16FY06

38

51

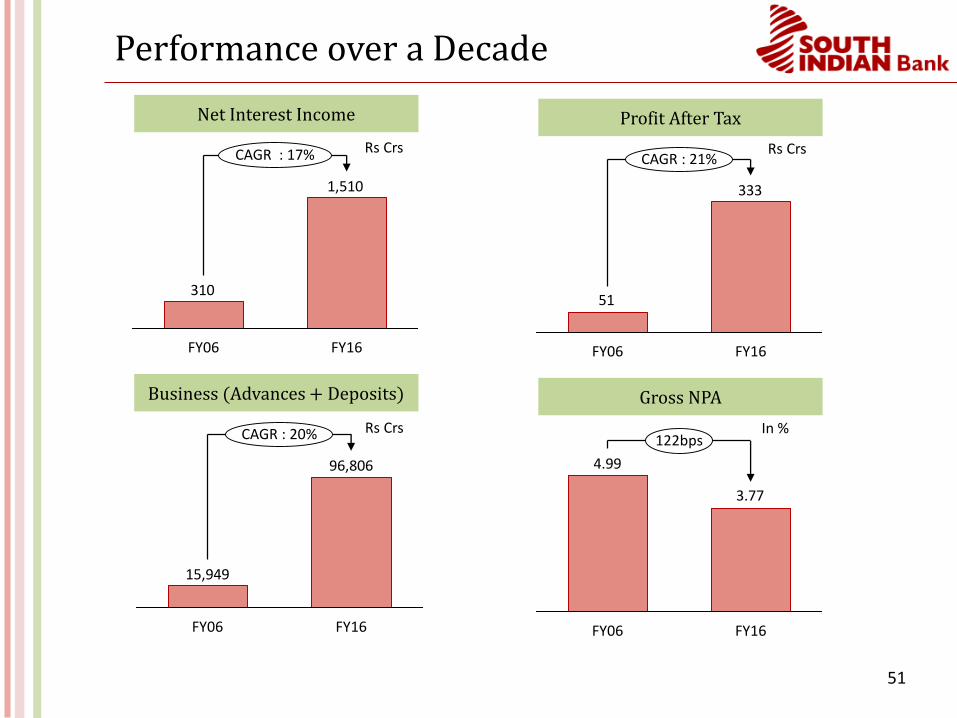

Performance over a Decade

1,510

310

CAGR : 17%

FY16FY06

Net Interest Income

96,806

15,949

FY06 FY16

CAGR : 20%

Business (Advances + Deposits)

333

51

FY06 FY16

CAGR : 21%

Profit After Tax

3.77

4.99

FY06

122bps

FY16

Gross NPA

Rs Crs Rs Crs

Rs Crs In %

52

Leadership Team

Mr. V. G Mathew , MD & CEO

Post Graduate in Physics and CAIIB with over 37 years of experience

Joined SIB in January, 2014 as Executive Vice President and appointed as MD & CEO in October, 2014

Significant experience in Retail & Corporate Credit, Technology and Risk Management

Joined SBI as a probationary officer in the Ahmadabad Circle in 1978 and was Chief General Manager before joining SIB

The major assignments handled by Mr. Mathew in SBI are

Dy. General Manager (IT Networking Project)

Dy. General Manager and Branch Head, (Overseas Branch, Bangalore)

General Manager, (Corporate Accounts Group-Mumbai Branch)

Chief General Manager (Risk Management)

Chief General Manager (Corporate Accounts Group)

He has served on various committees at Corporate Center of SBI such as Wholesale Banking Credit Committee,

Investment Committee, Corporate Centre Credit Committee and was a Director on the Board of SBI Macquarie

Infrastructure Trustee (P) Limited

53

Leadership Team

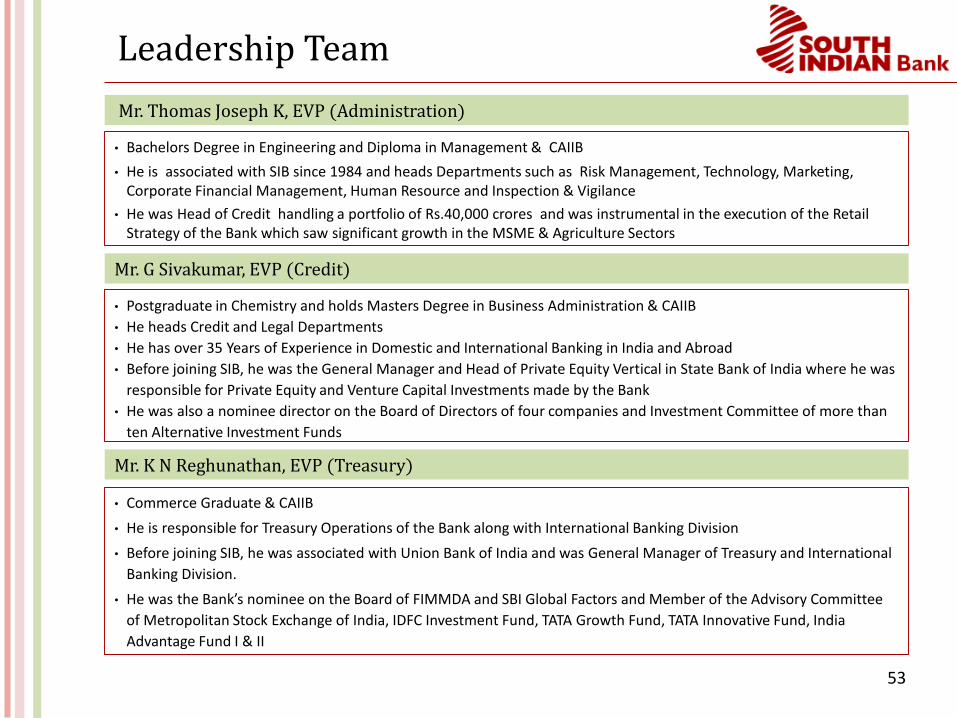

Mr. Thomas Joseph K, EVP (Administration)

• Bachelors Degree in Engineering and Diploma in Management & CAIIB

• He is associated with SIB since 1984 and heads Departments such as Risk Management, Technology, Marketing, Corporate Financial Management, Human Resource and Inspection & Vigilance

• He was Head of Credit handling a portfolio of Rs.40,000 crores and was instrumental in the execution of the Retail Strategy of the Bank which saw significant growth in the MSME & Agriculture Sectors

Mr. G Sivakumar, EVP (Credit)

• Postgraduate in Chemistry and holds Masters Degree in Business Administration & CAIIB

• He heads Credit and Legal Departments

• He has over 35 Years of Experience in Domestic and International Banking in India and Abroad

• Before joining SIB, he was the General Manager and Head of Private Equity Vertical in State Bank of India where he was

responsible for Private Equity and Venture Capital Investments made by the Bank

• He was also a nominee director on the Board of Directors of four companies and Investment Committee of more than

ten Alternative Investment Funds

Mr. K N Reghunathan, EVP (Treasury)

• Commerce Graduate & CAIIB

• He is responsible for Treasury Operations of the Bank along with International Banking Division

• Before joining SIB, he was associated with Union Bank of India and was General Manager of Treasury and International

Banking Division.

• He was the Bank’s nominee on the Board of FIMMDA and SBI Global Factors and Member of the Advisory Committee

of Metropolitan Stock Exchange of India, IDFC Investment Fund, TATA Growth Fund, TATA Innovative Fund, India

Advantage Fund I & II

54

Management Team

Mr. John Thomas, Senior General Manager (Business Development Department)

• Bachelors Degree in Science, MBA and CAIIB

Mr. Raphael T.J., Senior General Manager (Marketing & Information Technology)

• Bachelors Degree in Commerce, Masters in EXIM,

Diploma in Financial Management and CAIIB

• Bachelors Degree in Arts & Masters Degree in Business

Administration and CAIIB

Mr. Anto George T., General Manager (Delhi Regional Office)

• Bachelors Degree in Arts & Post Graduate Diploma in

Computer Application, Certification in RDBMS & Oracle

8i and JAIIB

Mr. Bobby James , Senior General Manager (Inspection & Vigilance)

• Bachelors Degree in Commerce, C.A. (Inter) and JAIIB

Mr. Benoy Varghese, Senior General Manager(Credit Department)

Mr. Paul V.L., General Manager (Administration)

• Masters Degree in Arts and Post Graduate Diploma in

Personnel Management & JAIIB

55

Management Team

Mr. C.P. Gireesh, Chief Financial Officer

• Bachelors Degree in Mathematics

• Fellow member of the Institute of Chartered Accountants of India and Certified Associate of the Indian Institute of

Banking & Finance

Mr. Jacob EA, Chief Compliance Officer

• Bachelors Degree in Science & CAIIB - I

Mr. Jimmy Mathew, Company Secretary

• Bachelors Degree in Commerce, Associate Member of

Institute of Company Secretary of India and Institute of

Cost & Management Accountants of India. Also a

Certified Associate of the Indian Institute of Banking &

Finance

56

Awards & Recognition

SIB wins prize in IDRBT Banking Application Contest

SIB wins Master Card Innovation Award

SIB wins ‘Social Banking Excellence Award instituted by ASSOCHAM”

57

Company: Investor Relations Advisors:

The South Indian Bank Ltd.CIN – L65191KL1929PLC001017Mr. C. P. Gireesh, [email protected]

www.southindianbank.com

Strategic Growth Advisors Pvt. Ltd.CIN - U74140MH2010PTC204285Ms. Payal Dave / Mr. Shogun [email protected] / [email protected]+91 98199 16314 / +91 77383 77756www.sgapl.net

For further information, please contact: