Investor Presentation - parauco.com · - 1 - 1 investor presentation february 2017 contacts sarah...

38

Investor Presentation FEBRUARY 2017 CONTACTS SARAH INMON (HEAD OF INVESTOR RELATIONS) | EDUARDO PEREZ MARCHANT (CORPORATE FINANCE MANAGER) TEL: (562) 22990510 | EMAIL: [email protected]

Transcript of Investor Presentation - parauco.com · - 1 - 1 investor presentation february 2017 contacts sarah...

- 1 -

1

Investor PresentationFEBRUARY 2017

CONTACTS

SARAH INMON (HEAD OF INVESTOR RELATIONS) | EDUARDO PEREZ MARCHANT (CORPORATE FINANCE MANAGER)

TEL: (562) 22990510 | EMAIL: [email protected]

- 2 -

2

disclaimer

2

This document has been prepared by Parque Arauco for the purpose of providing general infor-

mation about the Company. The Company assumes no responsibility for, or makes any represen-

tation or warranty, express or implied, with respect to, the accuracy, adequacy or completeness

of the information contained herein. The Company expressly disclaims any liability based on such

information, errors therein or omissions therefrom.

This presentation includes certain statements, estimates and forecasts provided by the Company

with respect to it’s anticipated future performance and involves significant elements or subjec-

tive judgment and analysis that may or may not prove to be accurate or correct. There can be no

assurance that these statements, estimates and forecasts will be attained and actual outcomes

and results may differ materially from what is estimated or forecast herein.

The information contained herein has been prepared to assist interested parties in making their

own evaluation of the company and does not purport to be all - inclusive or to contain all the infor-

mation that a potential counterparty may desire. In all cases, interested parties should conduct

their own independent investigation and analysis of the Company. Interested parties can only

rely on the result of their own investigation and the representations and warranties made in any

definitive agreement that may be executed.

- 3 -

3

INTRODUCTION

OUR OPERATIONS

INVESTMENT HIGHLIGHTS

FUTURE DEVELOPMENTS

Source: Parque Arauco(1) Does not include Marina Arauco nor Mall Center Curicó (2) Revenues from January 2016- December 2016. Exchange rate: US$= CLP 676.74(3) Source: Bloomberg

parque arauco OPERATIONAL METRICS BY COUNTRY

OPERATIONAL METRICS BY FORMAT

Shareholder structure (December 2016)

46.5% Chile

62.1% Chile

Colombia14.6%

Colombia7.0%

Peru30.9%

Peru38.9%

Parque Arauco is the third largest shopping center operator in Chile , the second largest Peru, and the fourth largest in Colombia.

Total GLA (m2)1 454,000 380,000 143,000 977,000

Owned GLA 383,108 270,000 124,775 777,883

Revenues 2016 (US$MM)2 147 73 17 237

# of Operations 26 18 3 46

TOTAL GLA1

977,000 m2

TOTALREVENUES2

US$MM 237

INTRODUCTION

Parque Arauco at a glance

MARKET CAP3

US$MM 2,020

24% Foreign

investment Funds

22% Local brokers

2% Local Mutual

Funds

5% Others

26% Controlling Group

5% Said Yarur Family

3% Abumohor Family

13% Local pension Funds

Indicator/ Country CHILE PERU COLOMBIA TOTAL

Daily Traded Volume 2016: US$MM 1.885.5%

Regional

Outlet5.2%

Strip center4.0%

Neighborhood5.3%

TOTAL REVENUES2

US$MM 23779.9%

Regional

Outlet6.2%

Strip center4.0%

Neighborhood9.9%

TOTAL GLA1

977,000 m2

- 5 -

5

INTRODUCTION

In the last five years Parque Arauco has doubled GLA, revenues

and EBITDA

GLA(1) m2

Revenues(1) US$ MM EBITDA(1) US$ MM

+2.0X

+1.9X +1.8X

Source: Parque Arauco. Exchange Rate: US$= 676,74(1) Does not include Marina Arauco nor Mall Center Curicó nor Mall Costa Pacífico in Coronel.

1982 Parque Arauco Kennedy opens as first shopping center in Chile1993 Arauco Maipu inaugurates in Santiago1995 Parque Arauco S.A. IPO1997 Inauguration of Marina Arauco in Viña del Mar, Chile2006 Parque Arauco expands into Peru with the purchase of a 45% stake in MegaPlaza Norte in Lima2008 Parque Arauco acquires Arauco Estación in Santiago, Chile2010 Parque Arauco opens first mall in Colombia, Parque Arboleda in Pereira2011 Capital increase for US$145 MM2012 Parque Arauco enters outlet format in Chile by acquiring Arauco Premium Outlet Buenaventura2014 Capital increase for US$182 MM2015 Purchase of minority shareholders in Colombia and Peru2016 Capital increase for US$100 MM

2011 2012 2013 20152014 2016

479,200 559,700693,100

728,500 818,500947,000

2011 2012 2013 20152014 2016

127 137158

185 215237

2011 2012 2013 20152014 2016

91 96109

126 148163

6

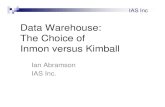

9%

Real Cap Rate(1) Real WACC (2) Spread Over Real WACC

6%

3%

Source: Parque Arauco (1) Real caprate is the yield on cost rate averaged by amount invested and considers the following properties: Arauco Express Calama, Arauco Express Ciudad Empresarial I, Arauco Express Colón, Arauco Express Huechuraba, Arauco Express Irarrázaval, Arauco Express Las Brujas, Arauco Express Luis Pasteur, Arauco Express Manuel Montt, Arauco Express Palmares, Arauco Premium Outlet Buenaventura, Arauco Premium Outlet Curauma, Arauco Premium Outlet San Pedro, Arauco Premium Outlet Coqumbo, Arauco Quilicura, MegaPlaza Chimbote, MegaPlaza Express Villa El Salvador, MegaPlaza Express Chincha, InOutlet Faucett, Viamix Chorrillos, Viamix Las Malvinas, InOutlet Premium Lurín, MegaPlaza Cañete, MegaPlaza Express Barranca, MegaPlaza Pisco, El Quinde Cajamarca, El Quinde Ica, Plaza Jesús María, Parque Caracolí.(2) Weighted Average Cost of Capital

INTRODUCTION

The spread over the cost of capital of our last projects is

approximately 3%

- 7 -

7

Total Return1, last 15 yearsAnnualized, local currency

Total Return1, last 5 yearsAnnualized, local currency

INTRODUCTION

Total Return

Parque Arauco’s value creation is proven by the fact that it has had one of the highest “Total

Return” of the real estate sector in the last years

Kepl

ierr

e

Keplierre

Gen

eral

Gro

wth

General Growth

Sim

on

Simon

S&P

500

S&P 500

Ham

mer

son

HammersonIgua

tem

i

Uni

bail

Mac

eric

h

Macerich

Fibr

a U

no

Fala

bella

Falabella

Parq

ue A

rauc

o

Parque Arauco

Mul

tipla

n

Taub

man

Taubman

Intu

Intu

Intu

Alia

nsce

BR M

alls

IPSA IPSA

Cenc

osud

17%18%

18%

18%

16%

13%

13%

10%

9%

8%

7%

3%

11%

14%

7%

16%

10%

13%

3%

16%

10%

14%

4%

15%

8%

12%

1%-7%

Source: Bloomberg(1) Total return includes dividends as of December 31,2016.

-2%

INTRODUCTION

Revenue type and contract duration

CONTRACT LENGTH (BASED ON º/º OF revenues)

FIXED VS VARIABLE RENTAL REVENUES as of December 30, 2016

41%

10%

10%

39% 100%

‹2 YEARS 2-3 YEARS 3-4 YEARS ›4 YEARS TOTAL

Variable Revenues15%

85% Fixed Revenues

OUR RENTAL REVENUES ARE DERIVED PRIMARILY FROM FIXED CONTRACTS AND ARE PROTECTED AGAINST INFLATION

39º/º OF OUR CONTRACTS HAVE A DURATION OF MORE THAN 4 YEARS AND THE AVERAGE LENGTH IS 6.5 YEARS

Other Revenues15%

85% Rental Revenues

- 9 -

9

INTRODUCTION

OUR OPERATIONS

INVESTMENT HIGHLIGHTS

FUTURE DEVELOPMENTS

- 10 -

10

MEGAPLAZA NORTE - PERÚ

LARCOMAR - PERÚ

LA COLINA- COLOMBIA

PARQUE ARAUCO KENNEDY - CHILE ARAUCO MAIPÚ - CHILE

ARAUCO ESTACIÓN - CHILE

OUR OPERATIONS

PortfolioParque Arauco has iconic and dominant shopping centers in Chile, Peru and Colombia

- 11 -

11

OUR OPERATIONS

Portfolio

Parque arauco is concentrated in Santiago and Lima, which makes the company a “market specialist” in these cities

Source: Parque Arauco(1) Santiago represents 90% of the NOI of Chile and Lima represents 65% of the NOI of Peru.NOI: Net Operating Income: Ingresos ordinarios + Costo de ventas + Gastos de Administración - Depreciación y Amortización + NOI Empresas relacionadas

San Antonio

Chillán

Concepción

Maipú

Kennedy

Buenaventura Outlet

Estación Central

Quilicura

Santiago

Antofagasta

Coquimbo

Lima

Cañete

Arequipa

Pisco

Villa El SalvadorVilla Chorrillos

Larcomar

MegaPlaza Norte

InOutlet Faucett

Cajamarca

InOutlet PremiumLurín

Plaza Jesús María

SANTIAGO1: 58% DEL NOI DE PARQUE ARAUCO LIMA1: 19% DEL NOI DE PARQUE ARAUCO

- 12 -

12

OUR OPERATIONS

Portfolio

Parque Arauco has 6 regional shopping centers, 4 outlets and 14 strip centers in Chile. the average age of the portfolio is 17 years.

Parque Arauco Kennedy 113,500 100% 113,500 98.6% 1982

Arauco Maipú 73,500 100% 73,500 99.0% 1993

Arauco Chillán 32,000 100% 32,000 100.0% 2007

Arauco Estación 66,500 83% 55,195 97.4% 2008

Arauco San Antonio 28,500 51% 14,535 94.2% 2009

Arauco Express 33,000 53% 17,378 84.9% 2012

Arauco Premium Outlets(1) 45,000 100% 45,000 92.4% 2012

Arauco Quilicura 32,000 100% 32,000 99.8% 2013

Mall Costa Pacífico 30,000 100% 30,000 N/A 2017

Total Chile 454,000 84% 413,108 96.7%

Year of

incorporationOccupancy% OwnershipGLA (m2)

Owned GLA (m2)

Source: Parque Arauco(1) Arauco Premium Outlet has four outlets located in Santiago, Concepción, Coquimbo and Curauma. (2) Arauco Express has 14 Stripcenters in Chile: 11 strip centers in Santiago, 1 in Viña del Mar, 1 in Calama, and 1 in Antofagasta.

San Antonio

Chillán

Concepción

Maipú

Kennedy

Buenaventura Outlet

Estación Central

Quilicura

Santiago

Chile

Antofagasta

Coquimbo

- 13 -

13

OUR OPERATIONS

Portfolio

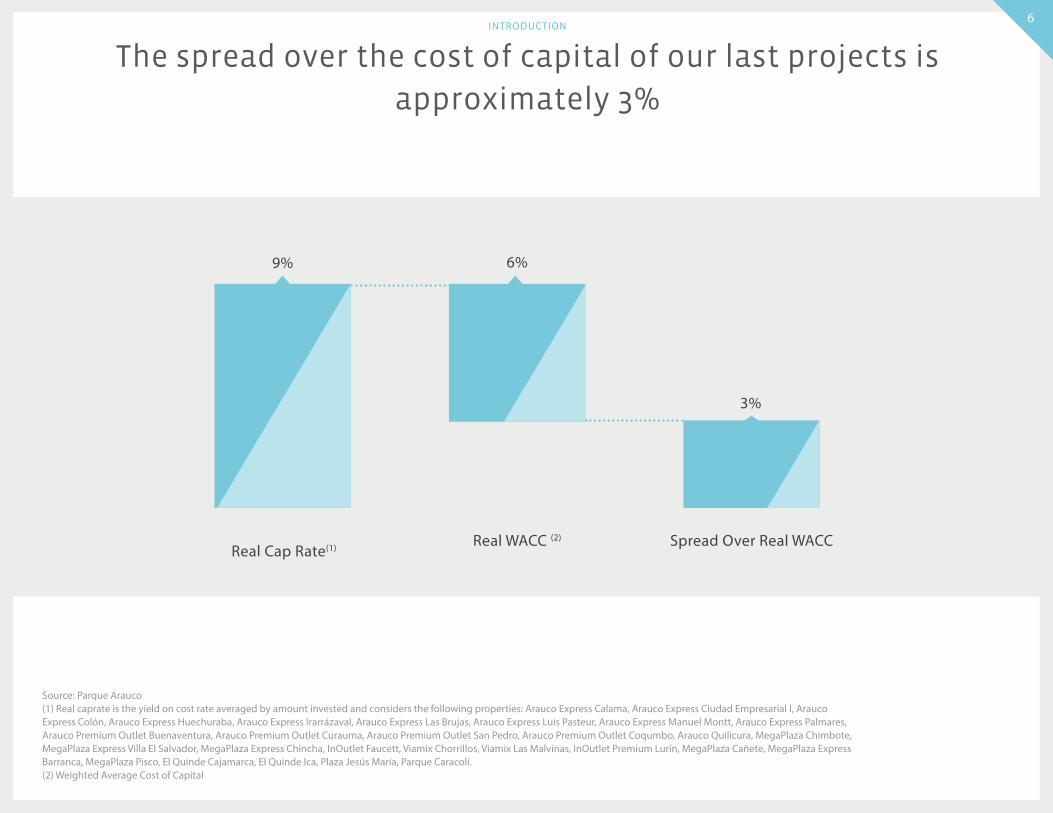

In Peru in the company has 6 regional shopping centers and 8 neighborhood shopping centers, 2 outlets and 2 strip centers. The average age of the portfolio is 5 years.

perú

MegaPlaza Norte 110,000 50% 55,000 98.9% 2006

MegaPlaza Express Villa Chorrillos 8,000 50% 4,000 96.6% 2009

Larcomar 26,500 100% 26,500 92.7% 2010

Parque Lambramani 29,500 100% 29,500 88.0% 2010

MegaPlaza Chimbote 28,000 50% 14,000 95.5% 2012

MegaPlaza Express Villa El Salvador 9,500 50% 4,750 98.3% 2012

MegaPlaza Express Chincha 9,000 50% 4,500 76.1% 2013

InOutlet and Viamix(2) 22,500 100% 22,500 68.7% 2013

MegaPlaza Cañete 16,500 50% 8,250 98.0% 2013

MegaPlaza Express Barranca 10,000 50% 5,000 98.8% 2013

MegaPlaza Pisco 14,500 50% 7,250 95.3% 2015

El Quinde Cajamarca 30,500 100% 30,500 92.8% 2015

El Quinde Ica 36,500 100% 36,500 96.5% 2015

Plaza Jesús María 14,500 100% 14,500 75.6% 2016

MegaPlaza Jaén 14,500 50% 7,250 82.7% 2016

Total Perú 380,000 71% 270,000 92.6%

Year of

incorporationOccupancy% Ownership1GLA (m2)

Owned GLA (m2)

Source: Parque Arauco(1)Only parnter in Peru is Grupo Wiese, which includes MegaPlaza formats (50%).(2) InOutlet and Viamix includes two premium outlet malls in Lima and two strip centers in Lima.

Ica

Lima

Cañete

Arequipa

Pisco

Villa El Salvador

Villa ChorrillosLarcomar

MegaPlaza Norte

InOutlet Faucett

Cajamarca

InOutlet Premium Lurín

Plaza Jesús María

- 14 -

14

OUR OPERATIONS

Portfolio

Parque Arauco has 3 regional shopping centers in Colombia and the average age of the portfolio is 3 years

COLOMBIA

Parque Arboleda 40,500 55% 22,275 95.7% 2010

Parque Caracoli 38,500 100% 38,500 88.4% 2013

Parque La Colina 64,000 100% 64,000 N/A 2016

Total Colombia 143,000 87% 124,775 91.6%

Bucamaranga

Pereira

Year of

incorporationOccupancy % OwnershipGLA (m2)

Owned GLA (m2)

Source: Parque Arauco

Bogotá

- 15 -

15

INTRODUCTION

OUR OPERATIONS

INVESTMENT HIGHLIGHTS

FUTURE DEVELOPMENTS

- 16 -

16

1.Strong results in a challenging macroeconomic environment.

2.Stable and diversified revenues

4.Solid corporate governance and increased concern with

sustainability

6.Important growth

opportunities.

3.Strong commercial relationships with local and global businesses.

5.Conservative debt

structure and outstanding financial performance.

investment highlights

- 17 -

17

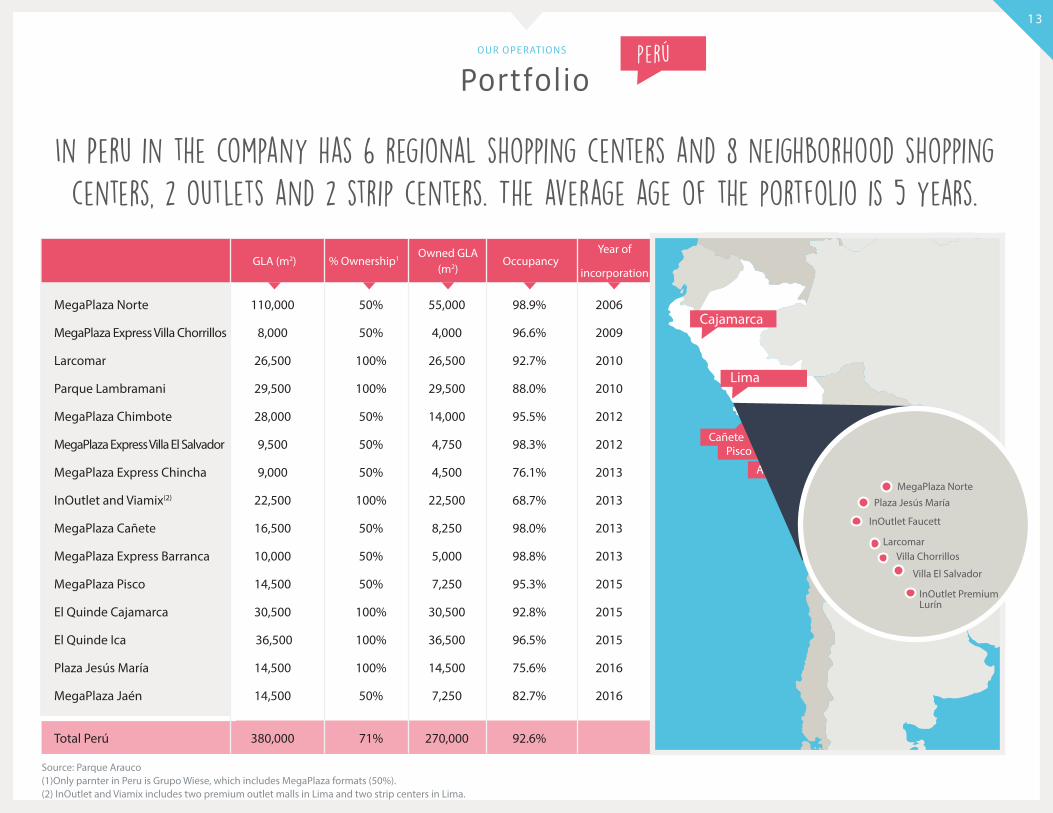

STRONG RESULTS IN A CHALLENGING MACROECONOMIC ENVIRONMENT

Positive but weaker macroeconomic outlook and attractive

industry dynamicsParque Arauco is positioned in countries with strong macroeconomic

prospects

GDP Growth

Chile2015

2.3%

2016

1.6%

2017f

2.2%

Peru2015

3.3%

2016

3.9%

2017f

4.5%

Colombia2015

3.3%

2016

2.5%

2017f

2.8%

Retail Sales Growth

Chile2014

7.4%

2015

6.0%

2016

4.9%

Peru2014

8.2%

2015

4.9%

2016

7.6%

Colombia2014

5.9%

2015

7.1%

2016

7.2%

Population (Millions)

Chile2014

17.8

2015

18.0

2016

18.2

Peru2014

30.8

2015

31.1

2016

31.5

Colombia2014

47.7

2015

48.2

2016

48.7GDP Per Capita, PPP

Chile2014

23,025

2015

23,507

2016

23,969

Peru2014

12,124

2015

12,518

2016

13,019

Colombia2014

13,430

2015

13,836

2016

14,161 Av. Latam:15,078

Av. Latam:41.7

Source: GDP Growth, Population and GDP Per Capita: International Monetary Fund, Consumption: Euromonitor.

- 18 -

18

STRONG RESULTS IN A CHALLENGING MACROECONOMIC ENVIRONMENT

Results have been positive in all three countries

1Q1

Chile

Tenant sales2 Revenues2 NOI2

PERU

COLOMBIA

940,4881,024,996

+9.0%

2,577,2022,749,836

+6.7%

349,727 376,439

+7.6%

91,47999,417

217,877

244,318

+12.1%

40,61444,446

+9.4%

80,80288,850

+10.0%

163,124189,124

+16.4%

29,080 33,346

+14.7%

(1) GLA in Chile does not include Mall Costa Pacífico.(2) Chile in MMCLP, Peru in MSoles and Colombia in MMCOP. (2) Not including overhead expenses (Corporate headquarters, regional Services Center, Chile Division, Peru Division and Colombia Division)

2015

409,500 424,000

+3.5%

GLA1

337,500 380,000

+12.6%

71,500143,000

+100.0%

+8.7%

2016 2015 2016 2015 2016 2015 2016

2015 2016 2015 2016 2015 2016 2015 2016

2015 2016 2015 2016 2015 2016 2015 2016

- 19 -

19

Strong Same Store Growth and a Healthy Occupancy Cost

1) Peru’s Same Store Sales and Same Store Rent in 4Q16 do not include Larcomar due to contingencies.

CHILE SAME STORE SALES / CH %

3Q16

7.2

4Q15

5.5

1Q16

7.7

2Q16

4.1

4Q16

2.6

PERU SAME STORE SALES1 / CH %

3Q16

2.0

4Q15

2.2

1Q16

6.8

2Q16

1.6

4Q16

0.4

COLOMBIA SAME STORE SALES / CH %

3Q16

5.7

4Q15

8.6

1Q16

11.5

2Q16

9.2

4Q16

8.3

CHILE SAME STORE RENT / CH %

3Q16

6.2

4Q15

6.8

1Q16

5.8

2Q16

4.3

4Q16

2.7

PERU SAME STORE RENT1 / CH %

3Q16

5.8

4Q15

3.0

1Q16

9.3

2Q16

3.8

4Q16

4.6

COLOMBIA SAME STORE RENT / CH %

3Q16

5.3

4Q15

12.5

1Q16

11.2

2Q16

8.4

4Q16

5.5

CHILE OCCUPANCY COST

4Q15

10.1%

4Q16

10.0%54%

Others

46%Anchor Stores

PERU OCCUPANCY COST

4Q15

7.2%

4Q16

6.7%

36%Others

64%Anchor Stores

COLOMBIA OCCUPANCY COST

4Q15

9.6%

4Q16

9.2%

69%Others

31%Anchor Stores

STABLE AND DIVERSIFIED REVENUES

- 20 -

20

socio-economic level diversification (º/º revenues)

Country level diversification (º/º revenues) Format level Diversification (º/º revenues)

42

48 10 100

Medium to HighIncome: Includes

ABC1 and C2 in Chile, A and B in Peru and 6, 5 and 4 in Colombia

Medium Income:Includes C3 and D in

Chile, C and D in Peru and 3 in

Colombia

Medium to LowIncome: Includes

E in Chile and Peru and 2 and 1 in

Colombia

Source: Parque Arauco. Based on socio-economic composition of community in which malls are located.

62.1% Chile

7.0% Colombia

30.9% Peru

STABLE AND DIVERSIFIED REVENUES

Parque Arauco diversifies its market risks at a

country, format, and socio-economic level

85.5% Regional

Outlet5.2%

Strip center4.0%

Neighborhood5.3%

- 21 -

21

STABLE AND DIVERSIFIED REVENUES

With a 39% market share in Chile, Parque Arauco

is the market leader in the outlet format in the Andean region

Arauco Premium Outlet Curauma, Chile InOutlet Faucett, Perú

Arauco Premium Outlet Buenaventura, Chile Arauco Premium Outlet Concepción, Chile

InOutlet Premium Outlet Lurin, Perú Arauco Premium Outlet Coquimbo, Chile

Outlets currently in our portfolio

Keys to the Premium Outlet Format

(1) LocationLocated near main cities

(2) BrandsPremium name-brands

(3) DiscountsMore than 30% discount

- 22 -

22

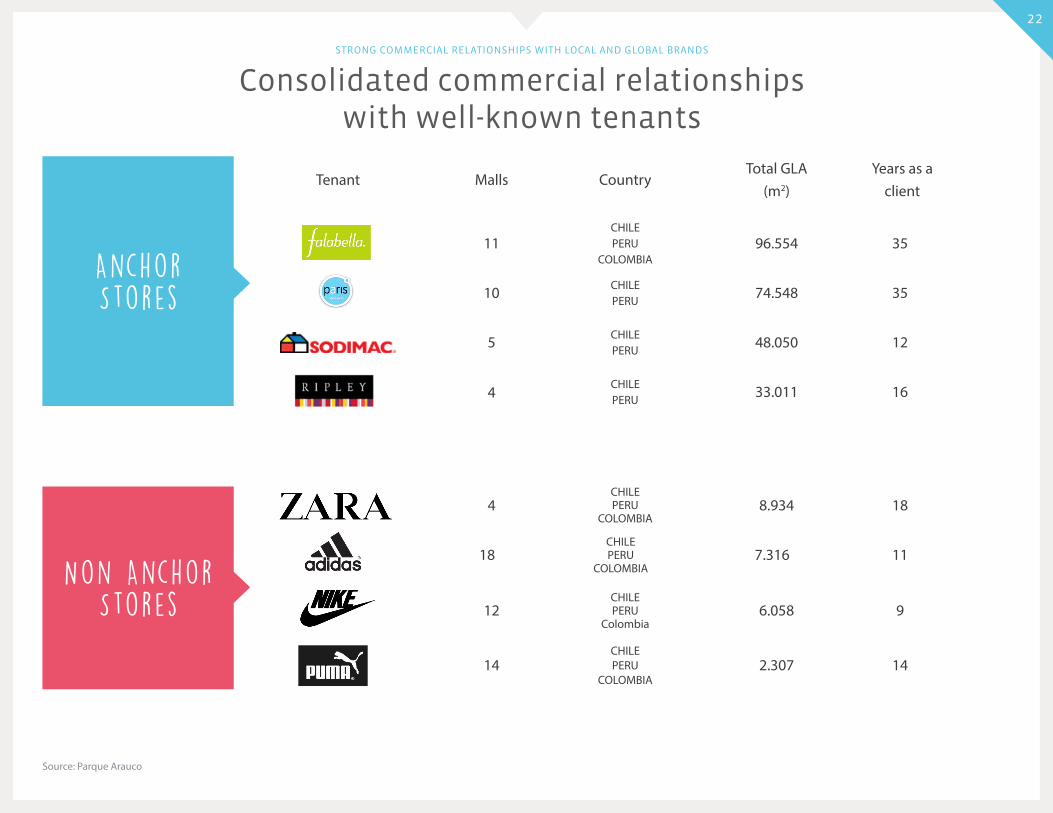

Anchor Stores

Non AnchorStores

Tenant Malls

11

4

10

5

12

Years as a client

35

16

35

12

9

Total GLA(m2)

96.554

33.011

74.548

48.050

6.058

Country

CHILEPERU

COLOMBIA

CHILEPERU

CHILEPERU

CHILEPERU

CHILEPERU

Colombia

18 117.316CHILEPERU

COLOMBIA

4 188.934CHILEPERU

COLOMBIA

14 142.307CHILEPERU

COLOMBIA

Source: Parque Arauco

STRONG COMMERCIAL RELATIONSHIPS WITH LOCAL AND GLOBAL BRANDS

Consolidated commercial relationships with well-known tenants

- 23 -

23

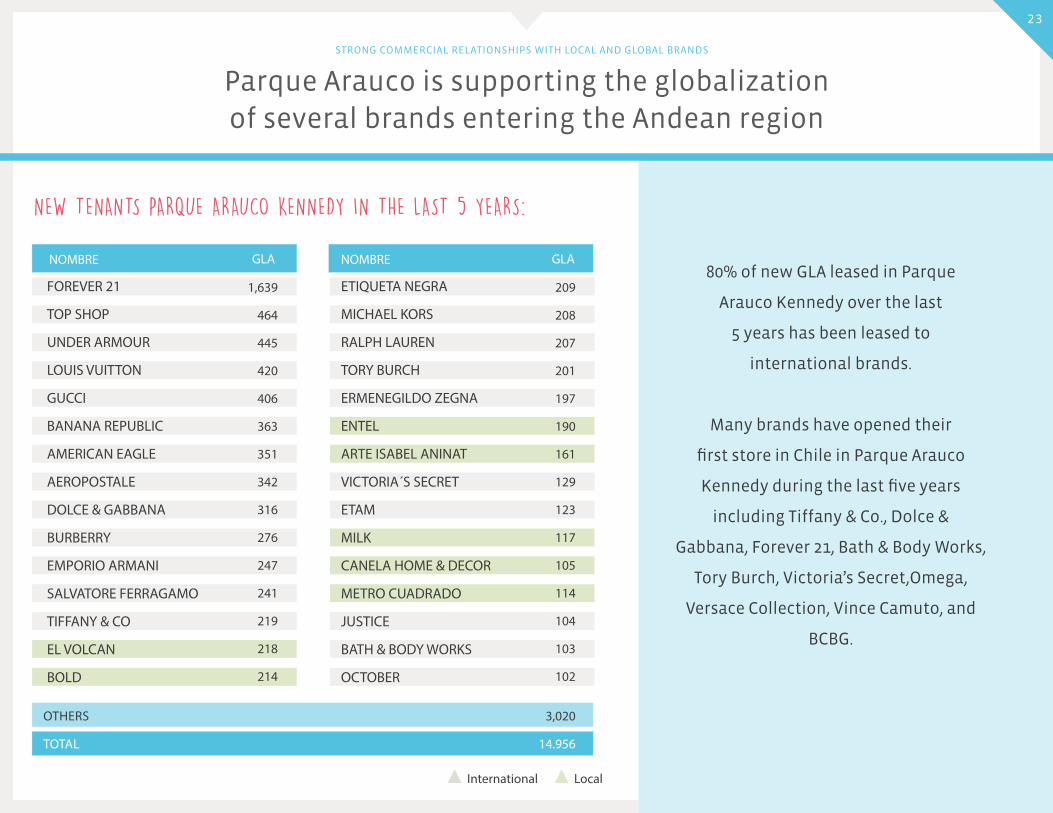

NEW TENANTS PARQUE ARAUCO KENNEDY IN THE LAST 5 YEARS:

80% of new GLA leased in Parque

Arauco Kennedy over the last

5 years has been leased to

international brands.

Many brands have opened their

first store in Chile in Parque Arauco

Kennedy during the last five years

including Tiffany & Co., Dolce &

Gabbana, Forever 21, Bath & Body Works,

Tory Burch, Victoria’s Secret,Omega,

Versace Collection, Vince Camuto, and

BCBG.

OTHERS

TOTAL

3,020

14.956

GLA GLANOMBRE NOMBRE

FOREVER 21

TOP SHOP

UNDER ARMOUR

LOUIS VUITTON

GUCCI

BANANA REPUBLIC

AMERICAN EAGLE

AEROPOSTALE

DOLCE & GABBANA

BURBERRY

EMPORIO ARMANI

SALVATORE FERRAGAMO

TIFFANY & CO

EL VOLCAN

BOLD

ETIQUETA NEGRA

MICHAEL KORS

RALPH LAUREN

TORY BURCH

ERMENEGILDO ZEGNA

ENTEL

ARTE ISABEL ANINAT

VICTORIA´S SECRET

ETAM

MILK

CANELA HOME & DECOR

METRO CUADRADO

JUSTICE

BATH & BODY WORKS

OCTOBER

1,639

464

445

420

406

363

351

342

316

276

247

241

219

218

214

209

208

207

201

197

190

161

129

123

117

105

114

104

103

102

STRONG COMMERCIAL RELATIONSHIPS WITH LOCAL AND GLOBAL BRANDS

Parque Arauco is supporting the globalization of several brands entering the Andean region

International Local

- 24 -

24

workplace Recognition

Investor Relations recognition

Management recognition

Sustainability REcognition

Best Capital Markets Strategy: Andes in 2016.

In 2016, Parque Arauco is part of the Dow Jones Emerging Market Sustainability Index. We are

the first Latin American real estate company to be part of this prestigious index.

Best Investor Relations Department for Mid-Size companies according to

Santander and Revista Capital in 2016.

Source: Parque Arauco

SOLID CORPORATE GOVERNANCE AND INCREASED CONCERN WITH SUSTAINABILITY

Parque Arauco has received important recognitions from local and

international organizations

Parque Arauco was recognized by Great Place to Work in Chile and

Peru in 2016.

- 25 -

25

Source: Parque Arauco

SOLID CORPORATE GOVERNANCE AND INCREASED CONCERN WITH SUSTAINABILITY

In the last year we have continued advancing on our sustainability strategy

ESG workstreams

soc ial

• Communication with neighboring communities: Community relations strategy advancement

• Cultural activities: Hosting cultural activities in our malls

• Social spaces: Providing spaces to social organizations

• Donations: Definition of corporate donation policy

Envi ronment

• Baseline measurement: Environmental assessment and definition of baseline carbon emissions in Chile, Peru and Colombia

• Sustainable Construction: Sustainable building criteria applied in InOutlet Lurín in Peru and Parque La Colina in Colombia

• Environmentally friendly operation: Environmental experts visited assets in Chile, Peru and Colombia, providing a diagnostic report and improvement recommendations

Corporate governance

• Talent attraction: Attract and retain talent through working conditions

• Risk management: Creation of a risk executive committee to identify, evaluate and manage risks

• Ethical behavior: Important ethical behavior campaign, including virtual games with ethical dilemmas in Chile, Peru and Colombia

- 26 -

26

2011 2012 2013 20152014 3Q16

0.87x0.78x

0.89x0.81x

1.15x 1.18x

< 1.40x

2011 2012 2013 20152014 2016

3.84x3.42x

3.89x

3.31x 3.33x3.04x

2011

2011

2012

2012

2013

2013

2015

2015

2014

2014

3Q16

2016

0.41x

3.34x

0.43x

3.85x

0.59x

5.00x

0.47x

4.25x

0.76x

5.87x

0.72x

5.88x

Liabilities / Equity

ebitda/financial expenses

Net Financial Debt / Equity

net financial debt/EBITDA

< 1.50x

> 2.50x

CONSERVATIVE DEBT STRUCTURE AND OUTSTANDING FINANCIAL PERFORMANCE

Parque Arauco’s policy is to finance projects with 50% debt

and 50% equity, and is comfortably within all its covenants

- 27 -

27

DEC. 2014

Summary of debt by currency

Liability amortization profile and duration2

116

2535

106

168

94

922

196

25-36months

13-24months

0-3months

49-60months

7-12months

11-20years

37-48months

4-6months

6-10years

21-35years

0

95

23

138

88

300

158

6

74

186

25-36months

13-24months

0-3months

49-60months

7-12months

11-20years

37-48months

4-6months

6-10years

21-35years

128

5.0 years 1

6.7 years 1

DECEMBER 2014 (US$MM)

DECEMBER 2016 (US$MM)

IMPROVEMENT IN LOCAL DEBT RATINGFitch: AA- Feller: AA- ICR:AA-

BBB- BBB BBB+ A- AA-A AAA+ AA+

Source: Parque Arauco(1) Average age(2) Does not include accrued interests and the exchange rate is at the close of December 31, 2016.

54%UF

7% CLP

16% PEN

14% USD

CONSERVATIVE DEBT STRUCTURE AND OUTSTANDING FINANCIAL PERFORMANCE

During the last 24 months, the Company has improved its debt rating, eliminated debt in Dollars, and considerably

increased the duration of its liabilities

9% COP

Summary of debt rates

96% Fixed

4% Variable

93% Fixed

7% Variable DEC.

2016DEC.2014

DEC. 2016

68%UF

5% CLP

16% PEN

11% COP

- 28 -

28

ONSERVATIVE DEBT STRUCTURE AND OUTSTANDING FINANCIAL PERFORMANCE

The cost of debt has decreased importantly in the past 5 years

The cost of debt of Parque Arauco has decreased 160 points from 4.1% to 2.5%

The spread five years ago had collateral agreements, while the current spread is unsecured

with no collateral.

Date: 12-12-2014Base: 1.66%Spread: 1.74%Duration: 14.3

Date: 04-17-2015Base: 1.62%Spread: 1.68%Duration: 14.77

Source: Risk America

Date: 10-12-2016Base: 1.46%Spread: 1.02%Duration: 12.71

Generic long-term bond issued by Parque Arauco in Chile

- 29 -

29

IMPORTANT GROWTH OPPORTUNITIES

Parque Arauco has 0.9 million m2 and a 2% market participation in Latin American and a 8% market participation in the Andean

Region.

MEXICOGLA: 17.4 million m2

38% of total

ANDEAN REGIONGLA: 11.3 million m2

25% of total

ARGENTINAGLA: 2.1 million m2

5% of total

BRAZILGLA: 14.7 million de m2

32% of total

Source: Prepared using information published by the International Council of Shopping Centers (ICSC)., and Parque Arauco analysis

LATIN AMERICAGLA: 45.5 million m2

Indicator

Total GLA (th)GLA Parque Arauco (th)Market ShareRank

CHILE

3,60042412%#3

PERU

2,10038018%#2

COLOMBIA

5,6001433%#4

- 30 -

30

IMPORTANT GROWTH OPPORTUNITIES

Parque Arauco participates in markets with a growing retail market

GDP Per Person vs. GLA per 1,000 inhabitants1

GLA

per

1,0

00 h

abit

ants

GLA

per

1,0

00 h

abit

ants

Canada

USA

France

Italy

Spain

Chile

Chile

Argentina

Brazil

Brazil

Mexico

Mexico

Colombia

Colombia

South Africa

South Africa

2,500

2,000

1,500

1,000

500

-

500

400

300

200

100

-10,000 20,000 30,000 40,000

Peru

Peru

Portugal

Portugal

GDP per person, PPP (log scale)

GDP per person, PPP

Argentina

AT Kearney GRDI1 window of opportunity

Opening Peaking Maturing Closing

Chile

Mexico

Brasil

PeruColombia

5,000 50,000

(1) Global Retail Development Index

(1) Source: International Council of Shopping Centers, World Bank

- 31 -

31

IMPORTANT GROWTH OPPORTUNITIES

Parque Arauco’s growth has come from greenfield projects and M&A

Total GLA

in 2006

194,745

55,651

83,70824,595

91,62527,676

80,242

132,85837,400

90,000

947,000

Total GLA

in 2007

Total GLA

in 2010

Total GLA

in 2014

Total GLA

in 2008

Total GLA

in 2011

Total GLA

in 2015

Total GLA

in 2009

Total GLA

in 2013

Total GLA

in 2012

New GLA

in 2016

Greenfields650,643 m2

M&A296,357 m2

Greenfield M&A

69%

31%

Total GLA2016

128,500

- 32 -

32

INTRODUCTION

OUR OPERATIONS

INVESTMENT HIGHLIGHTS

FUTURE DEVELOPMENTS

- 33 -

33

New Projects Country

Country

Format

Format

Estimated Opening Date

Estimated Opening Date

Total Investment in local currency1

Total Investment in local currency1

Total InvestmentUSDMM2

Total InvestmentUSDMM2

Owned GLAm2

Owned GLAm2

% Ownership

% Ownership

Total GLA m2

Total GLAm2expansions

1) Projects in Chile in UF, in Peru in ThPEN and in Colombia in MCOP 2) Exchange rate as of December 31, 2016: 226,347.1 CLP/UF, 669.5 CLP/USD, 3,00.3 COP/USD, 3.4 PEN/USD. 2) In addition to the 11,000 m2, this expansion includes a 401 room Hilton by Hilton Hotel and largest hotel convention center in Santiago.

Parque Angamos

MegaPlaza Villa El Salvador II

MegaPlaza Express Huaral

Various Projects SCP

Viamix Colonial

Arauco Premium Outlet Bogotá

Subtotal

Chile

Peru

Peru

Peru

Peru

Colombia

Chile

Colombia

Chile

Peru

Peru

Peru

Chile

Peru

Peru

Chile

Chile

Chile

Peru

Peru

Peru

Chile

Peru

Colombia

55%

50%

50%

100%

100%

100%

100%

100%

53%

100%

50%

50%

53%

50%

N/A

N/A

100%

53%

50%

100%

100%

100%

100%

100%

1H18

2H17

1Q17

2H18

1Q17

1H17

1Q17

4Q16

4Q16

4Q16

4Q16

2Q16

2Q16

2Q16

2Q16

2Q16

1Q16

1Q16

1Q16

1Q16

1Q16

2H21

2H17

2H17

886,000

36,000

38,000

180,000

25,000

78,000

1,520,000

672,000

320,000

9,500

53,000

38,000

319,000

47,000

28,600

2,137,500

309,000

115,000

9,000

76,000

53,500

5,355,000

39,500

17,500

Neighborhood

Neighborhood

Neighborhood

Neighborhood

Strip Center

Outlet

Regional

Regional

Strip Center

Strip Center

Regional

Regional

Strip Center

Neighborhood

N/A

N/A

Outlet

Strip Center

Regional

Outlet

Neighborhood

Regional / Hotel

Regional

Hotel

6,050

5,500

8,250

19,500

3,000

13,000

55,300

30,000

64,00

3,160

1,500

4,750

3,750

2,370

7,250

4,620

N/A

6,000

1,843

1,250

8,500

14,000

149.372

11,000

N/A

N/A

11,000

11,000

11,000

16,500

19,500

3,000

13,000

74,000

30,000

64,000

6,000

1,500

9,500

7,500

4,500

14,500

N/A

N/A

6,000

3,500

2,500

8,500

14,000

173,000

11,000

N/A

N/A

11,000

35

11

11

54

7

26

144

60

224

13

3

16

11

13

14

9

84

12

5

3

23

16

506

211

12

6

229

Total

Remaining investment as of December 31, 2016

215,672258,000 879

311

Parque Arauco Kennedy Expansion2

Renovación Parque Lambramani

Hotel Bucaramanga

Subtotal

Mall Costa Pacífico

Parque La Colina

Arauco Express Antofagasta

Viamix Chorrillos Expansion

MegaPlaza Norte Libertadores Expansion

Megaplaza Norte Cine Conquistadores Expansion

Arauco Express Ciudad Empresarial II

MegaPlaza Express Jaen

MegaPlaza Chimbote Minority Interest

Inmobiliaria Viña del Mar Minority Interest

Arauco Premium Outlet Coquimbo

Arauco Express Recoleta

MegaPlaza Chimbote Expansion

InOutlet Premium Lurín

Plaza Jesús María

Subtotal

Parque Arauco has announced projects that will add 228,000 m2 of GLA over the next few years

and will require an investment of US$ 819 million.

Future Developments 2016 and Onwards

Type

projects incorporated in 2016 Country Format Oeening DateTotal Investment in local currency1

Total Investment USDMM1

Owned GLA m2% OwnershipTotal GLA

m2Type

Type

Greenfield

Greenfield

Greenfield

Greenfield

Greenfield

Greenfield

Acquisition

Greenfield

Greenfield

Expansion

Expansion

Expansion

Greenfield

Greenfield

Minority Interest

Minority Interest

Greenfield

Greenfield

Expansion

Greenfield

Acquisition

Expansion

Renovation

Expansion

- 34 -

34

Parque La Colina was inaugurated in December 2016

Committed brands:

- 35 -

35

We announced a new expansion of Parque Arauco Kennedy

Project Details:

Investment: 5,355,000 UF5-star hotel: Hilton by HiltonRooms: 401Convention center: 3,000 m2

Parking spots: 700Additional GLA: 11,000 m2

- The project will have the first five star Hilton hotel in Chile, a convention center, as well as the incorporation of new stores and more parking.

- The five star Hilton hotel will have 401 rooms, two restaurants, three bars, two pools, a gym and an executive lounge. It will have the largest hotel convention center in the country, with the possibility of hosting over 2,800 people.

- The expansion will include a new flagship Falabella store with almost 25,000 m2 of GLA. This store will occupy the first four floors of the expansion.

Hotel Operator:

- 36 -

36

M2 % OwnershipTotal Cost

(Local Currency)1

Total Cost

(USD MM)nameQuilicura

Buenaventura

Chicureo

Los Andes

Others in Chile

Total Chile

Parque El Golf - San Isidro

Chimbote

Talara

Ica

Chiclayo

Others MegaPlaza

Total Peru

Neiva

Valledupar

Barranquilla

Total Colombia

Total

25,486

115,864

47,614

39,254

55,567

293,785

14,790

42,657

30,675

12,643

6,608

211,417

318,790

49,537

46,000

56,166

151,703

754,278

78,000

455,000

206,000

117,000

445,000

1,301,000

109,000

18,000

9,400

13,500

6,300

115,000

271,200

18,000

30,000

76,000

124,000

3

18

8

5

17

51

32

5

3

4

2

34

81

6

10

25

41

171

100%

100%

100%

100%

100%

100%

70%

100%

100%

100%

100%

50%

65%

100%

100%

100%

100%

86%

The company also has a valuable landbank which will serve as the base for future development.

Landbank

1) Landbank in Chile in UF, in Peru in ThPEN and in Colombia in MCOP

- 37 -

37

Adjusted FFO Margin - AFFO / revenues

AFFO -Adjusted Funds From Operations: Net Profit - Depreciation & Amortization - Other Income/expenses - Share of Profit (Loss) of Associates Accounted - Foreign Exchange Differences - Income (Loss) for indexed assets and liabilities - Gains (losses) from the difference between the previous book value and the fair value of financial assets - Deferred tax+ Associates accounted Adjusted FFO

Controlling Adjusted FFO -AFFO attributable to the shareholders of the company

Controlling FFO -FFO attributable to the shareholders of the company

EBITDA - Earnings Before Income Tax Depreciation and Amortization: Revenues + Cost of Sales + Administration Expenses - Depreciation and Amortization

EBITDA margin -EBITDA divided by revenues

EPS -Earnings Per Share: Net income attributable to the equity holders of the company/weighted average number of shares outstanding

FFO -Funds From Operations: Net Profit - Depreciation & Amortization - Share of Profit (Loss) of Associates Accounted + Associates Accounted FFO

GLA -Gross Leasable Area. Equivalent to the sum of all the areas available for lease

Green Field Projects - Organic development of new shopping centers

Landbank -Land held by the company for future development

LTM -Refers to information from the last twelve months

Monthly Revenues / m2 -Monthly revenues divided by GLA

weighted by average occupancy for the period

Monthly Sales/m2 -Monthly tenant sales divided by GLA weighted by average occupancy for the period

Neighborhood Mall -A shopping mall with a GLA between 6,000 and 20,000 m2

Net income margin -Net profit / revenues

NOI -Net Operating Income: Revenues + Cost of Sales + Administration Expenses - Depreciation & Amortization + Associates accounted NOI

Occupancy -GLA paying rent divided by total GLA

Occupancy cost -Minimum rent, plus variable rent, plus common expenses, plus a promotion fund that the tenants pay Parque Arauco divided by the sales of the tenant.

Owned GLA -Total GLA weighted by Parque Arauco’s interest in the mall

Pipeline -Greenfield and expansion projects under development

Premium Outlet - Shopping center located outside of the city offering name brand clothing and goods for a reduced price

Regional Mall - A shopping mall with a GLA over 20,000 m2.

SSR -Same Store Rent: Percentage change in rent collected from tenants that paid rent in both of the periods compared

SSS -Same Store Sales: Percentage change in sales from tenants that reported sales in both of the periods compared

Strip Center -A shopping center with a GLA less than 6,000 m2

Tenant Sales Tenant sales of the consolidated assets

UF -Unidad de Fomento: A chilean currency unit indexed according to inflation daily

37

Glossary

- 38 -

38

![[db tech showcase Tokyo 2015] DATA WAREHOUSE BASICS by Wiliiam Inmon](https://static.fdocuments.us/doc/165x107/588681ba1a28ab962a8b6ea9/db-tech-showcase-tokyo-2015-data-warehouse-basics-by-wiliiam-inmon.jpg)