Investor Briefing February 2015 NYSE:BMS - Bemis...

30

Investor Briefing February 2015 NYSE:BMS

-

Upload

duongkhuong -

Category

Documents

-

view

216 -

download

0

Transcript of Investor Briefing February 2015 NYSE:BMS - Bemis...

Investor Briefing February 2015

NYSE:BMS

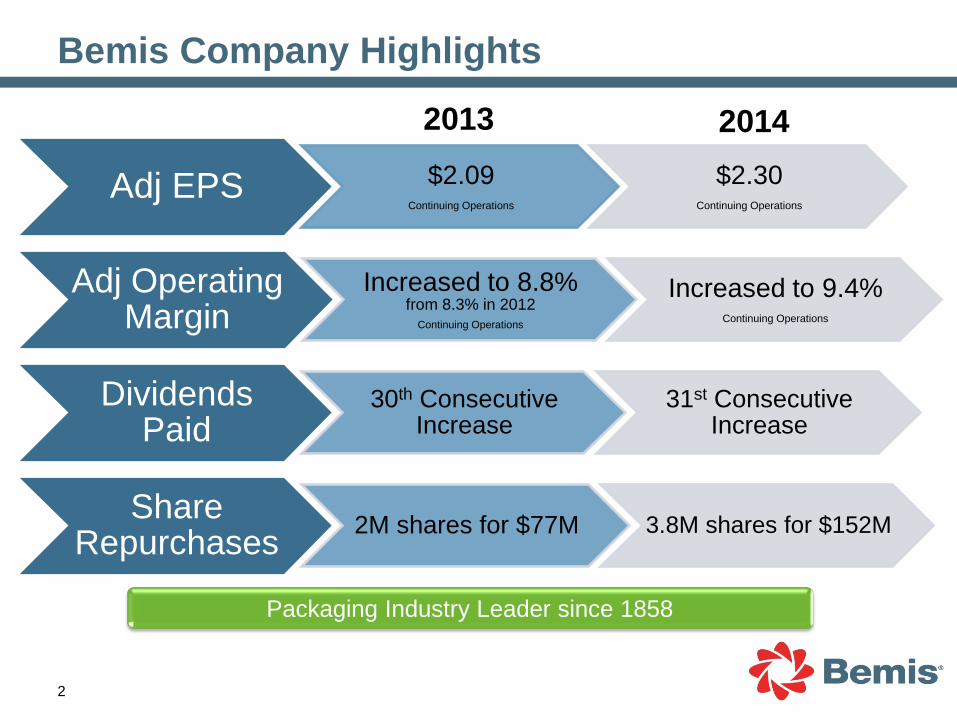

2

Adj EPS $2.09 Continuing Operations

$2.30 Continuing Operations

Adj Operating Margin

Increased to 8.8% from 8.3% in 2012

Continuing Operations

Increased to 9.4% Continuing Operations

Dividends Paid

30th Consecutive Increase

31st Consecutive Increase

Share Repurchases 2M shares for $77M 3.8M shares for $152M

2013 2014

Packaging Industry Leader since 1858

Bemis Company Highlights

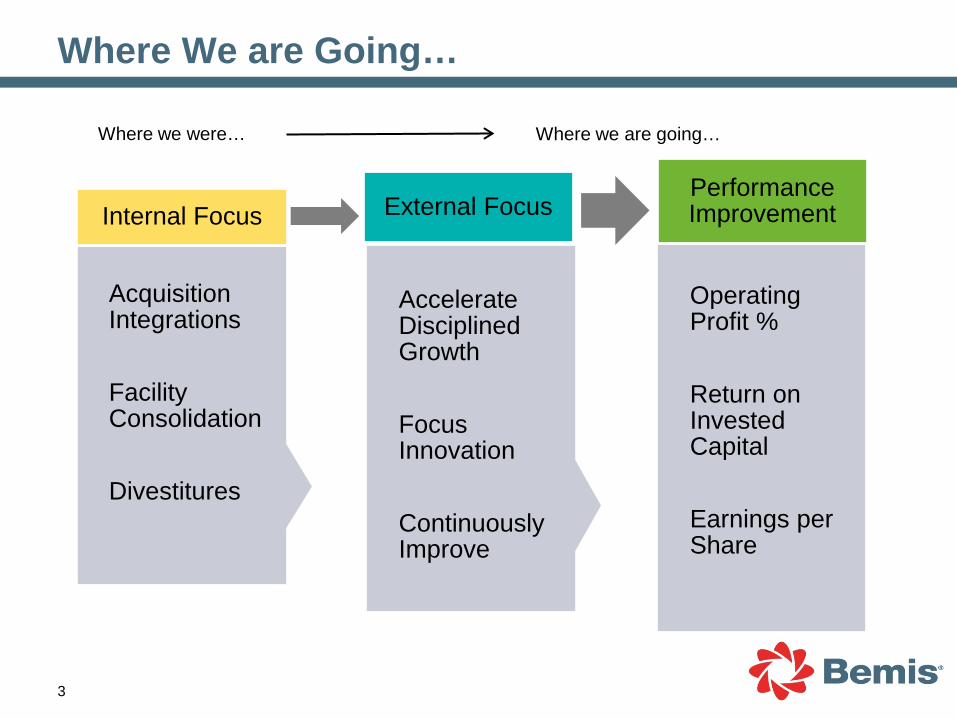

Where We are Going…

3

Operating Profit % Return on Invested Capital Earnings per Share

Performance Improvement

Accelerate Disciplined Growth Focus Innovation Continuously Improve

External Focus

Acquisition Integrations Facility Consolidation Divestitures

Internal Focus

Where we were… Where we are going…

4

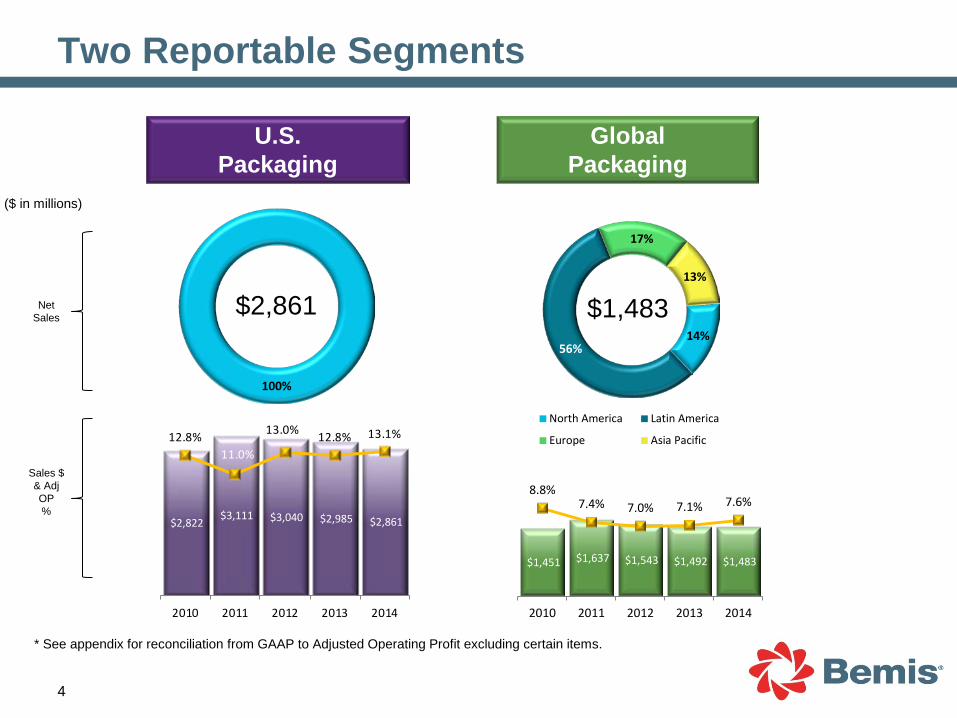

U.S. Packaging

Global Packaging

* See appendix for reconciliation from GAAP to Adjusted Operating Profit excluding certain items.

($ in millions)

$2,861 $1,483 Net Sales

Sales $ & Adj OP %

Two Reportable Segments

100%

14% 56%

17%

13%

North America Latin America

Europe Asia Pacific

$2,822 $3,111 $3,040 $2,985 $2,861

12.8%11.0%

13.0% 12.8% 13.1%

2010 2011 2012 2013 2014

$1,451 $1,637 $1,543 $1,492 $1,483

8.8% 7.4% 7.0% 7.1% 7.6%

2010 2011 2012 2013 2014

5

What’s Important:

• Shelf-life extension for perishable foods (meat, cheese, dairy, produce)

• Proprietary and patented film structures deliver convenience and sustainability features

• Extensive manufacturing scale support both national and regional brands

U.S. Packaging

0%

10%

20%

30%

Meat &Cheese

Dairy &Liquids

SpecialtyFood &Meals

Dry Foods BeverageWraps

Candy,Snacks &

Bakery

OtherNon-food

Health &Hygiene

Percent of 2014 Net Sales

6

What’s Important: • Expanding consumer markets in

Latin America and Asia • Sterility and quality are

paramount for medical applications

Global Packaging

0%

10%

20%

30%

Medical &Pharma

Dairy &Liquids

Meat &Cheese

Health &Hygiene

SpecialtyFood

BeverageWraps

Candy,Snacks &

Bakery

OtherNon-food

Percent of 2014 Net Sales

7

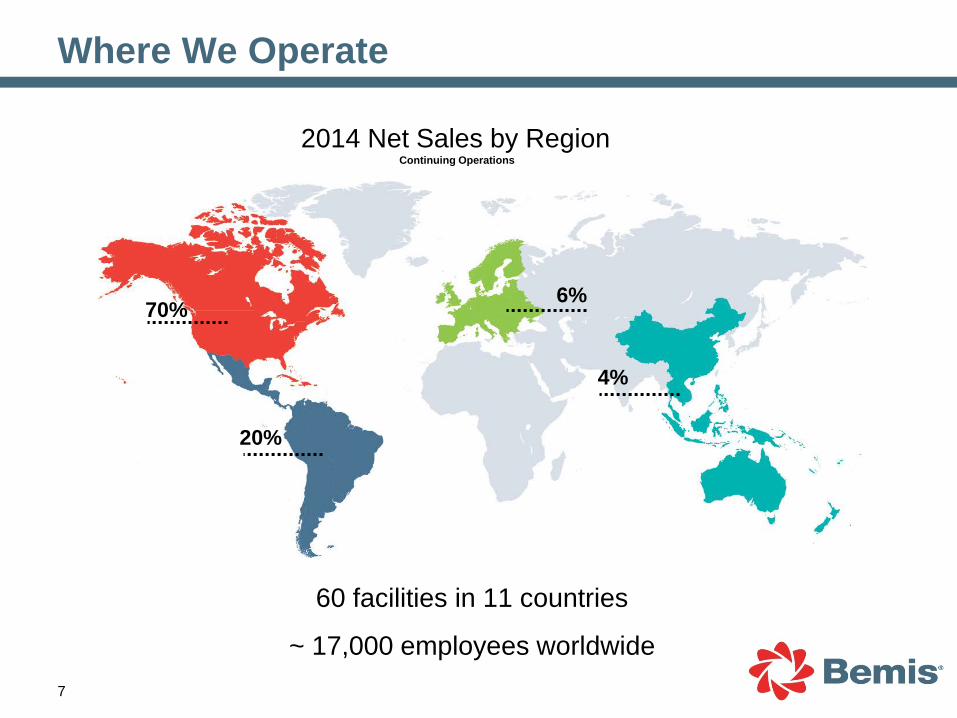

2014 Net Sales by Region Continuing Operations

Where We Operate

60 facilities in 11 countries

~ 17,000 employees worldwide

70% 6%

4%

20%

8

Why customers choose Bemis:

Reliable supply; quality product

Technology leader with differentiated product

Global breadth & scale

Longevity & financial stability

No customer represents more than 10% of Bemis sales

Who We Serve

Global Healthcare Packaging -Medical Device -Pharmaceutical

Packaging for Emerging

Economies

Our focus is differentiation that drives disciplined, profitable growth

Bemis will grow: • High-margin packaging solutions

• Where we have a competitive advantage • With a focus on profit

Accelerating Growth Globally

9

Increased consumer desire for freshness

and convenience

Growing demand for sustainable packaging solutions

Increased focus on

extending shelf life and

reducing waste

Accelerating Growth High-Barrier Packaging

10

Bemis technology creates the competitive advantage

11

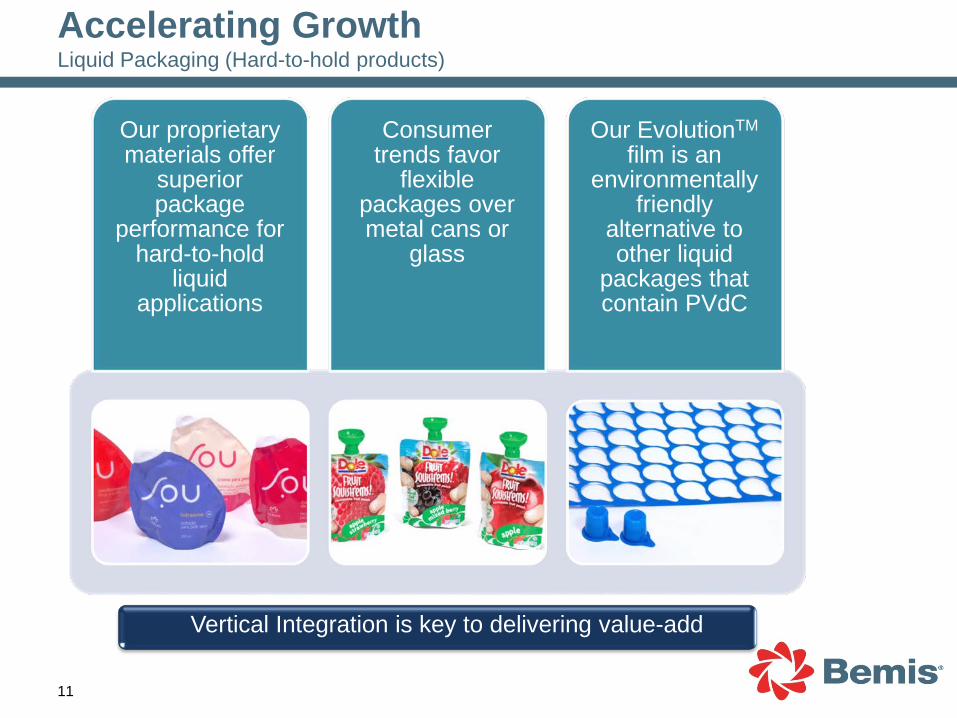

Our EvolutionTM film is an

environmentally friendly

alternative to other liquid

packages that contain PVdC

Consumer trends favor

flexible packages over metal cans or

glass

Our proprietary materials offer

superior package

performance for hard-to-hold

liquid applications

Accelerating Growth Liquid Packaging (Hard-to-hold products)

Vertical Integration is key to delivering value-add

12

Odor-absorbing Films for Poultry • Absorbs and confines poultry odors for an

extended period OvenRite™ Ovenable Films • Superior seal and form features • Consumer-convenience via EZ Open and self-venting

features

Flexible Stand-up Pouch for Vegetables

• Stand-up flexible pouch replaces the metal can packaging format • Provides savings to our customers

Barrel Pouch for Liquids • Stand-up flexible pouch replaces the bag in box

packaging format • Superior sealing technology withstands the harsh

distribution process

Technology Advantage

Vertical Integration creates a competitive advantage

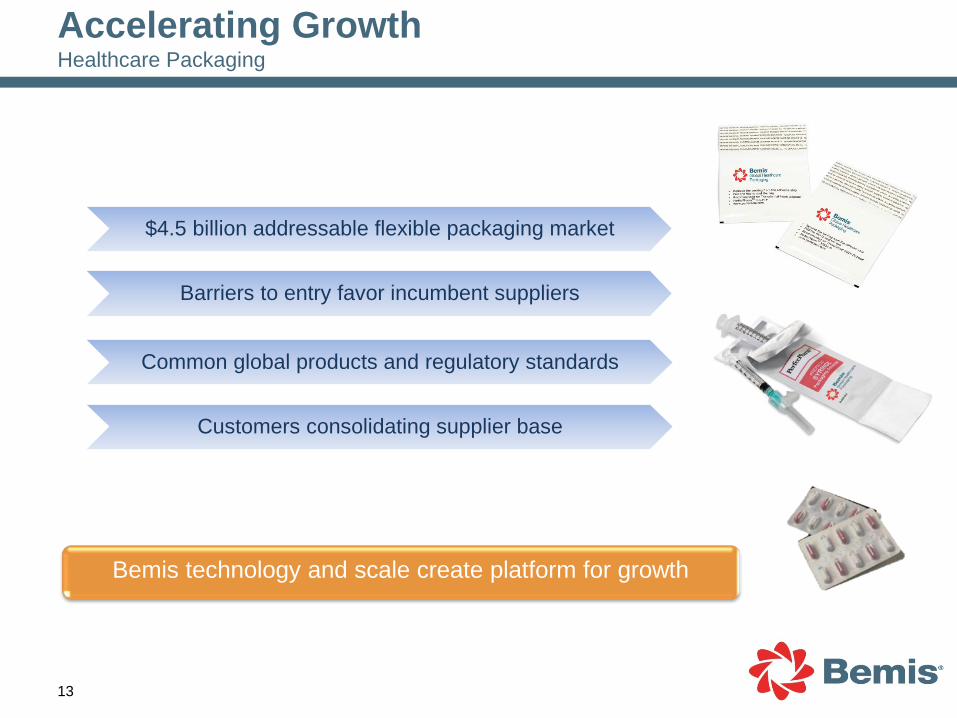

Bemis technology and scale create platform for growth

$4.5 billion addressable flexible packaging market

Barriers to entry favor incumbent suppliers

Common global products and regulatory standards

Customers consolidating supplier base

Accelerating Growth Healthcare Packaging

13

14

Emerging

Asian economies

coupled with Bemis

technology are a formula for success

*Source: EIU, Boston Consulting Group income database, BCG analysis

• Rapidly growing in China at 14% CAGR (2012 – 2020e)* Consumption

• 2020 affluent income population in China expected to be 4x current* Income Growth

• Evolving preferences & the need for shelf-stable food due to lack of refrigeration

Consumer Preferences

• Heightened consumer awareness and increased focus on safety & sterility Food Safety

Accelerating Growth in Emerging Economies – Asia-Pacific

15

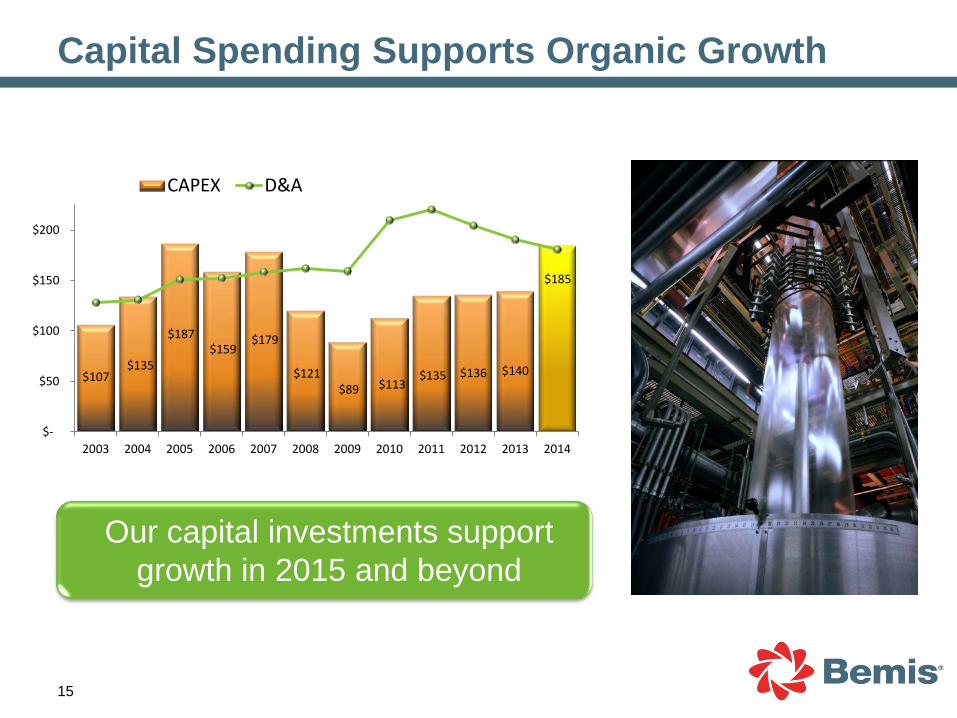

Capital investment in technologically advanced multi-layer extrusion

Our capital investments support growth in 2015 and beyond

Capital Spending Supports Organic Growth

$107 $135

$187 $159

$179

$121 $89 $113

$135 $136 $140

$-

$50

$100

$150

$200

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

CAPEX D&A

$185

16

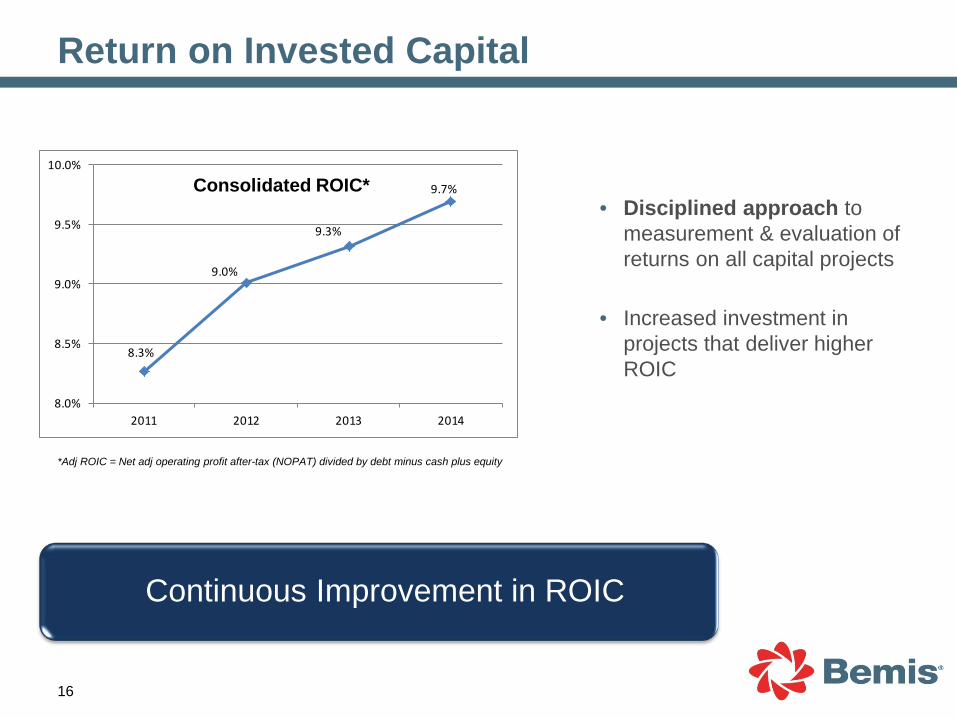

• Disciplined approach to measurement & evaluation of returns on all capital projects

• Increased investment in projects that deliver higher ROIC

*Adj ROIC = Net adj operating profit after-tax (NOPAT) divided by debt minus cash plus equity

Continuous Improvement in ROIC

Return on Invested Capital

8.3%

9.0%

9.3%

9.7%

8.0%

8.5%

9.0%

9.5%

10.0%

2011 2012 2013 2014

Consolidated ROIC*

17

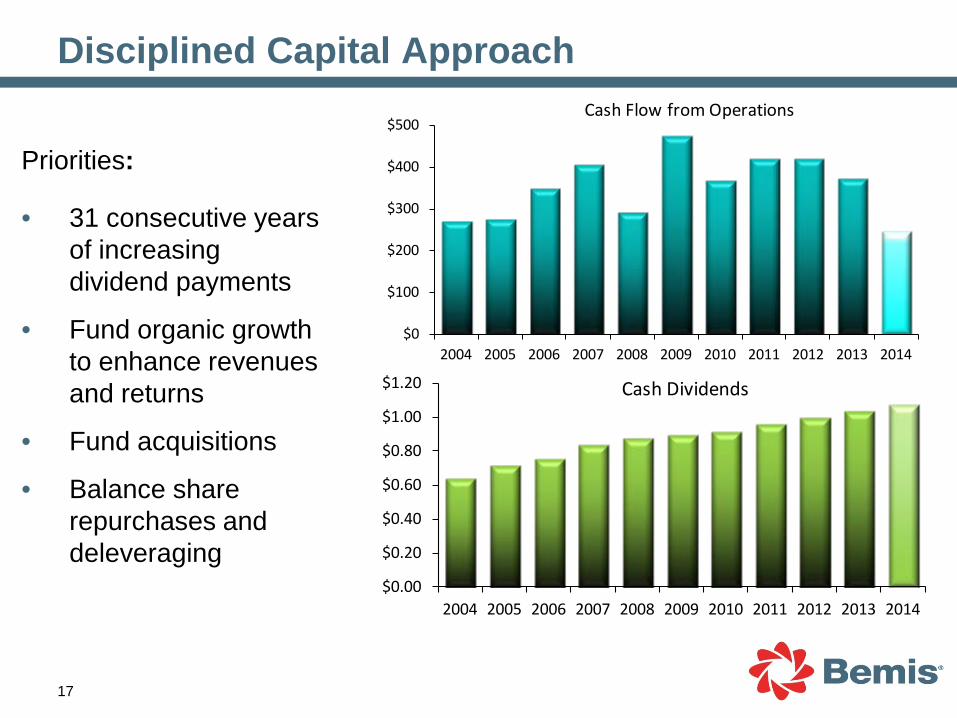

Priorities:

• 31 consecutive years of increasing dividend payments

• Fund organic growth to enhance revenues and returns

• Fund acquisitions

• Balance share repurchases and deleveraging

Disciplined Capital Approach

$0

$100

$200

$300

$400

$500

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Cash Flow from Operations

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Cash Dividends

18

Adjusted EPS guidance of $2.52 to $2.67 Continuing Operations

Capital expenditures of $185 to $200 million

Note: Guidance as of January 2015

2015 Financial Guidance

19

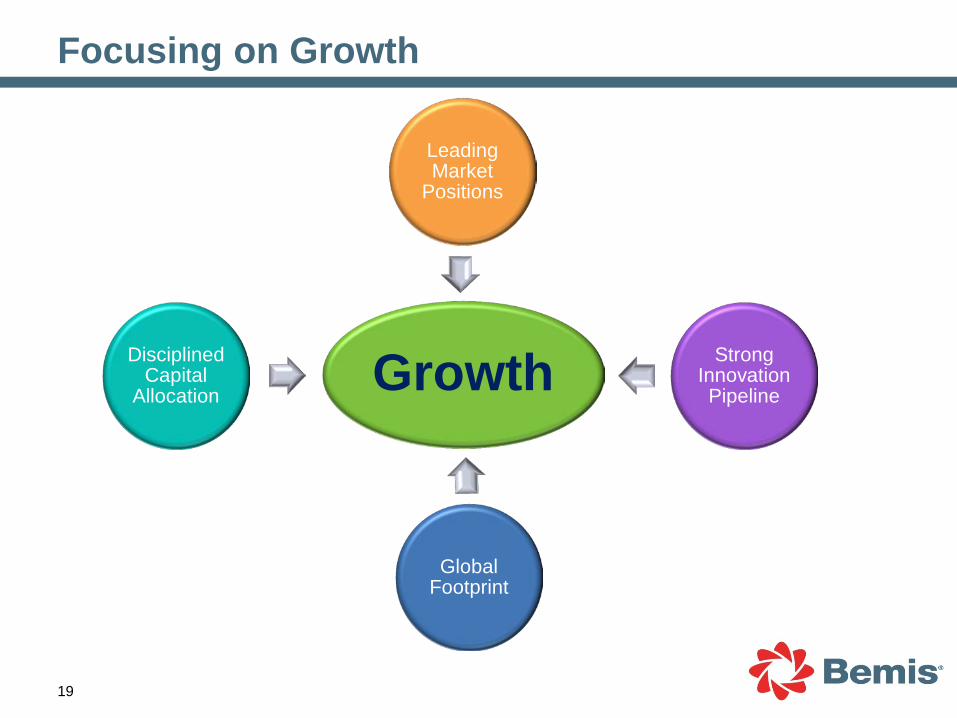

Growth

Leading Market

Positions

Strong Innovation Pipeline

Global Footprint

Disciplined Capital

Allocation

Focusing on Growth

20

This presentation includes forward-looking statements within the meaning of the Safe Harbor provisions

of the Securities Litigation Reform Act of 1995. Such statements include, but are not limited to,

statements relating to the expected future performance of the company and its objectives, expectations,

and intentions for the future. These forward-looking statements are based on the current beliefs and

expectations of Bemis Company’s management and are subject to risks and uncertainties. The forward-

looking statements speak only as of the date of this presentation, and Bemis Company does not

undertake to update such statements to reflect changes that occur after that date. There are a number of

factors that could cause actual results to differ from those set forth in the forward-looking statements.

These factors include, but are not limited to: general economic conditions, competitive conditions in our

markets, the cost and availability of raw materials, and our ability to pass these price changes on to our

customers. These and other risks, uncertainties, and assumptions are identified from time to time in our

filings with the Securities and Exchange Commission including our most recent Annual Report on form

10-K and our quarterly reports on Form 10-Q. Such reports are available on the website of the Securities

and Exchange Commission (www.sec.gov).

Safe Harbor Statement

22

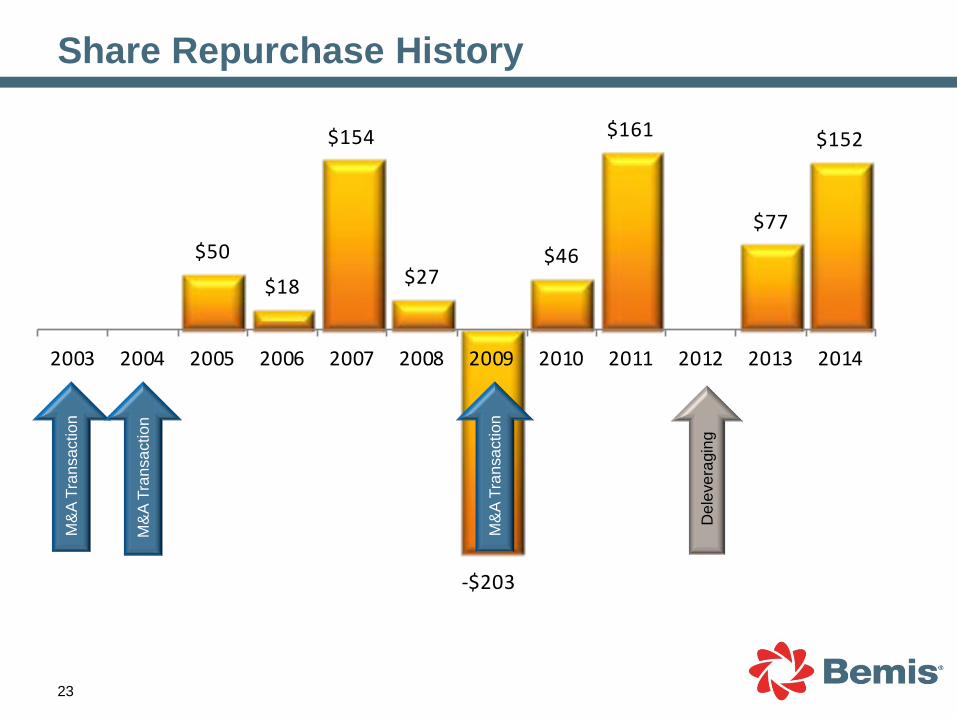

Completed the largest acquisition in company history of Alcan Food Americas for $1.2B

Completed facility consolidation, optimizing our manufacturing footprint with the closure of 9 plants

Acquired a film-based aseptic and bulk packaging manufacturer

Expanded footprint in Asia-Pacific with acquisitions in China of a converting operation in Dongguan and an extrusion platform in Foshan

Divested non-core businesses including thin gauge shrink film, Paper Packaging, and Pressure Sensitive Materials

Accomplishments 2010-2014

23

M&

A Tr

ansa

ctio

n

M&

A Tr

ansa

ctio

n

Share Repurchase History

$50

$18

$154

$27

-$203

$46

$161

$77

$152

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

M&

A Tr

ansa

ctio

n

Del

ever

agin

g

24

Economic Sustainability

Social Sustainability

Environmental Sustainability

• Delivering value to stakeholders

• Operating for the long-term with a sustainable business philosophy

• Contributing to the

economic stability of our communities

• Reducing food waste

• Developing

sustainable packaging solutions

• Minimizing

manufacturing waste

• Reducing our

impact on the planet

• Prioritizing employee safety

• Supporting programs that promote health and well-being in our communities

• Providing a positive workplace with opportunities for growth and success

Our Sustainability Commitment

25

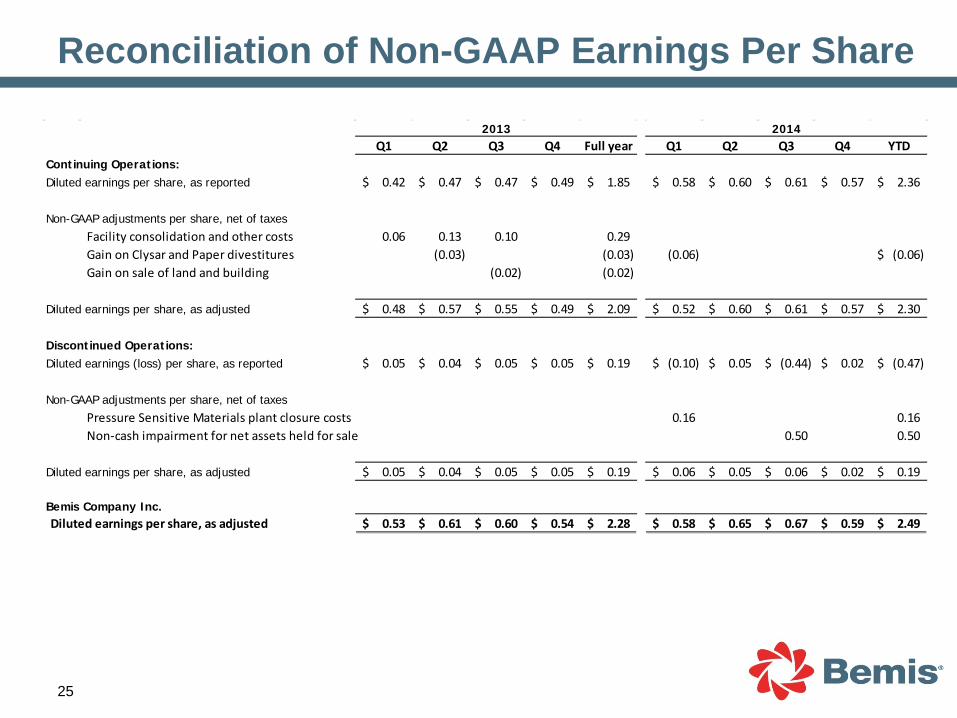

Reconciliation of Non-GAAP Earnings Per Share

Q1 Q2 Q3 Q4 Full year Q1 Q2 Q3 Q4 YTDContinuing Operations:Diluted earnings per share, as reported 0.42$ 0.47$ 0.47$ 0.49$ 1.85$ 0.58$ 0.60$ 0.61$ 0.57$ 2.36$

Non-GAAP adjustments per share, net of taxesFacility consolidation and other costs 0.06 0.13 0.10 0.29 Gain on Clysar and Paper divestitures (0.03) (0.03) (0.06) (0.06)$ Gain on sale of land and building (0.02) (0.02)

Diluted earnings per share, as adjusted 0.48$ 0.57$ 0.55$ 0.49$ 2.09$ 0.52$ 0.60$ 0.61$ 0.57$ 2.30$

Discontinued Operations:Diluted earnings (loss) per share, as reported 0.05$ 0.04$ 0.05$ 0.05$ 0.19$ (0.10)$ 0.05$ (0.44)$ 0.02$ (0.47)$

Non-GAAP adjustments per share, net of taxesPressure Sensitive Materials plant closure costs 0.16 0.16 Non-cash impairment for net assets held for sale 0.50 0.50

Diluted earnings per share, as adjusted 0.05$ 0.04$ 0.05$ 0.05$ 0.19$ 0.06$ 0.05$ 0.06$ 0.02$ 0.19$

Bemis Company Inc.Diluted earnings per share, as adjusted 0.53$ 0.61$ 0.60$ 0.54$ 2.28$ 0.58$ 0.65$ 0.67$ 0.59$ 2.49$

2013 2014

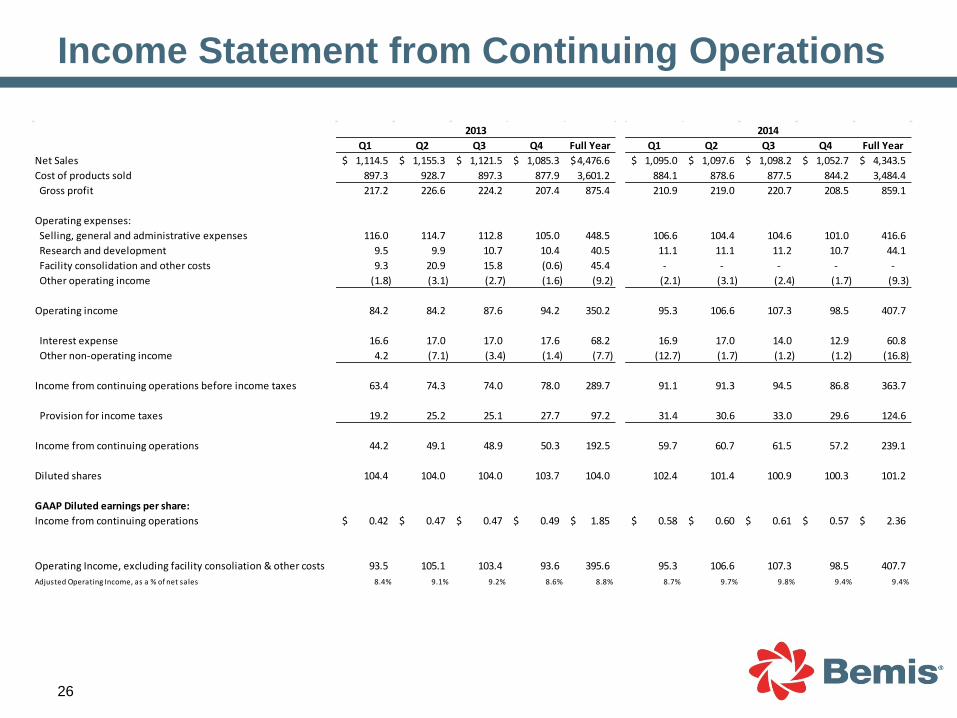

Income Statement from Continuing Operations

26

Q1 Q2 Q3 Q4 Full Year Q1 Q2 Q3 Q4 Full YearNet Sales 1,114.5$ 1,155.3$ 1,121.5$ 1,085.3$ 4,476.6$ 1,095.0$ 1,097.6$ 1,098.2$ 1,052.7$ 4,343.5$ Cost of products sold 897.3 928.7 897.3 877.9 3,601.2 884.1 878.6 877.5 844.2 3,484.4 Gross profit 217.2 226.6 224.2 207.4 875.4 210.9 219.0 220.7 208.5 859.1

Operating expenses: Selling, general and administrative expenses 116.0 114.7 112.8 105.0 448.5 106.6 104.4 104.6 101.0 416.6 Research and development 9.5 9.9 10.7 10.4 40.5 11.1 11.1 11.2 10.7 44.1 Facility consolidation and other costs 9.3 20.9 15.8 (0.6) 45.4 - - - - - Other operating income (1.8) (3.1) (2.7) (1.6) (9.2) (2.1) (3.1) (2.4) (1.7) (9.3)

Operating income 84.2 84.2 87.6 94.2 350.2 95.3 106.6 107.3 98.5 407.7

Interest expense 16.6 17.0 17.0 17.6 68.2 16.9 17.0 14.0 12.9 60.8 Other non-operating income 4.2 (7.1) (3.4) (1.4) (7.7) (12.7) (1.7) (1.2) (1.2) (16.8)

Income from continuing operations before income taxes 63.4 74.3 74.0 78.0 289.7 91.1 91.3 94.5 86.8 363.7 Provision for income taxes 19.2 25.2 25.1 27.7 97.2 31.4 30.6 33.0 29.6 124.6

Income from continuing operations 44.2 49.1 48.9 50.3 192.5 59.7 60.7 61.5 57.2 239.1

Diluted shares 104.4 104.0 104.0 103.7 104.0 102.4 101.4 100.9 100.3 101.2

GAAP Diluted earnings per share:Income from continuing operations 0.42$ 0.47$ 0.47$ 0.49$ 1.85$ 0.58$ 0.60$ 0.61$ 0.57$ 2.36$

Operating Income, excluding facility consoliation & other costs 93.5 105.1 103.4 93.6 395.6 95.3 106.6 107.3 98.5 407.7 Adjusted Operating Income, as a % of net sales 8.4% 9.1% 9.2% 8.6% 8.8% 8.7% 9.7% 9.8% 9.4% 9.4%

2013 2014

27

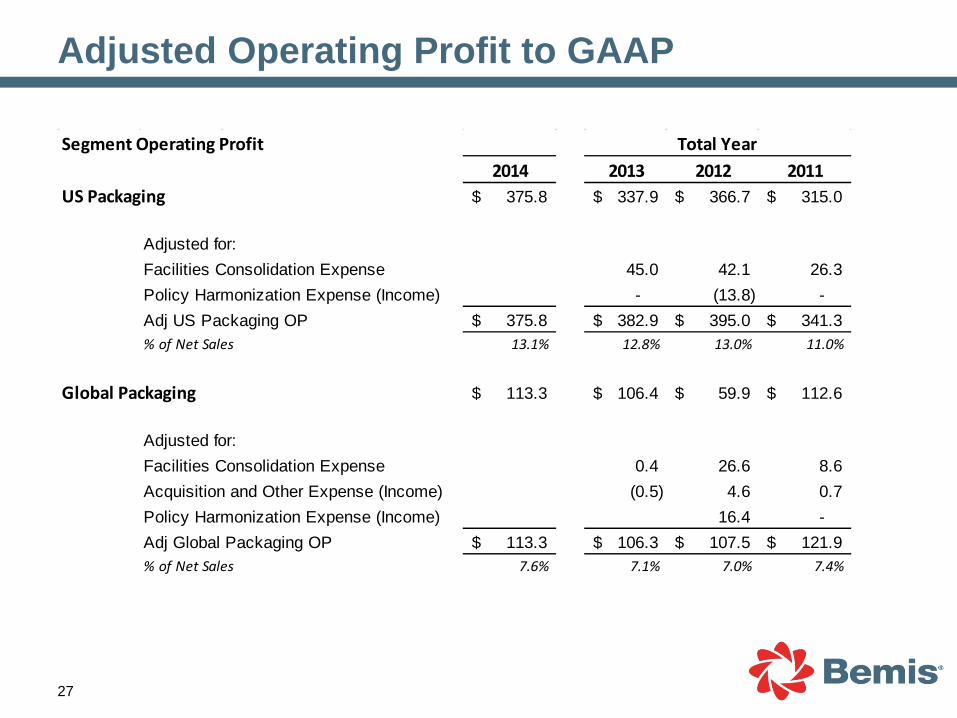

Adjusted Operating Profit to GAAP

Segment Operating Profit2014 2013 2012 2011

US Packaging 375.8$ 337.9$ 366.7$ 315.0$

Adjusted for:Facilities Consolidation Expense 45.0 42.1 26.3 Policy Harmonization Expense (Income) - (13.8) - Adj US Packaging OP 375.8$ 382.9$ 395.0$ 341.3$ % of Net Sales 13.1% 12.8% 13.0% 11.0%

Global Packaging 113.3$ 106.4$ 59.9$ 112.6$

Adjusted for:Facilities Consolidation Expense 0.4 26.6 8.6 Acquisition and Other Expense (Income) (0.5) 4.6 0.7 Policy Harmonization Expense (Income) 16.4 - Adj Global Packaging OP 113.3$ 106.3$ 107.5$ 121.9$ % of Net Sales 7.6% 7.1% 7.0% 7.4%

Total Year

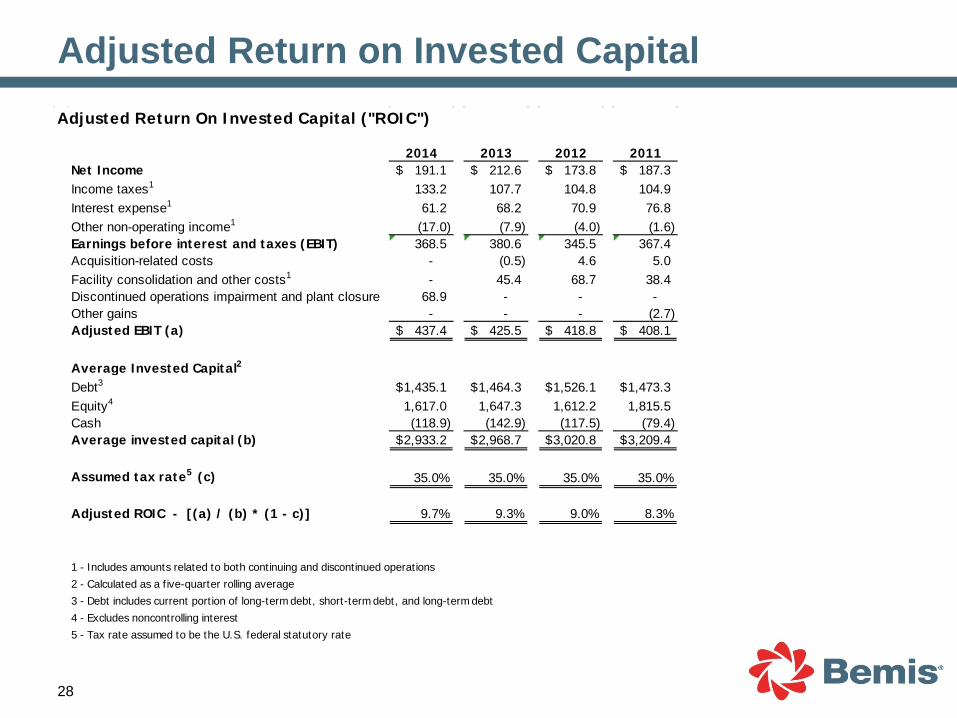

Adjusted Return on Invested Capital

28

Adjusted Return On Invested Capital ("ROIC")

2014 2013 2012 2011Net Income 191.1$ 212.6$ 173.8$ 187.3$ Income taxes1 133.2 107.7 104.8 104.9 Interest expense1 61.2 68.2 70.9 76.8 Other non-operating income1 (17.0) (7.9) (4.0) (1.6) Earnings before interest and taxes (EBIT) 368.5 380.6 345.5 367.4 Acquisition-related costs - (0.5) 4.6 5.0 Facility consolidation and other costs1 - 45.4 68.7 38.4 Discontinued operations impairment and plant closure 68.9 - - - Other gains - - - (2.7) Adjusted EBIT (a) 437.4$ 425.5$ 418.8$ 408.1$

Average Invested Capital2

Debt3 1,435.1$ 1,464.3$ 1,526.1$ 1,473.3$ Equity4 1,617.0 1,647.3 1,612.2 1,815.5 Cash (118.9) (142.9) (117.5) (79.4) Average invested capital (b) 2,933.2$ 2,968.7$ 3,020.8$ 3,209.4$

Assumed tax rate5 (c) 35.0% 35.0% 35.0% 35.0%

Adjusted ROIC - [(a) / (b) * (1 - c)] 9.7% 9.3% 9.0% 8.3%

1 - Includes amounts related to both continuing and discontinued operations2 - Calculated as a five-quarter rolling average3 - Debt includes current portion of long-term debt, short-term debt, and long-term debt4 - Excludes noncontrolling interest5 - Tax rate assumed to be the U.S. federal statutory rate

29

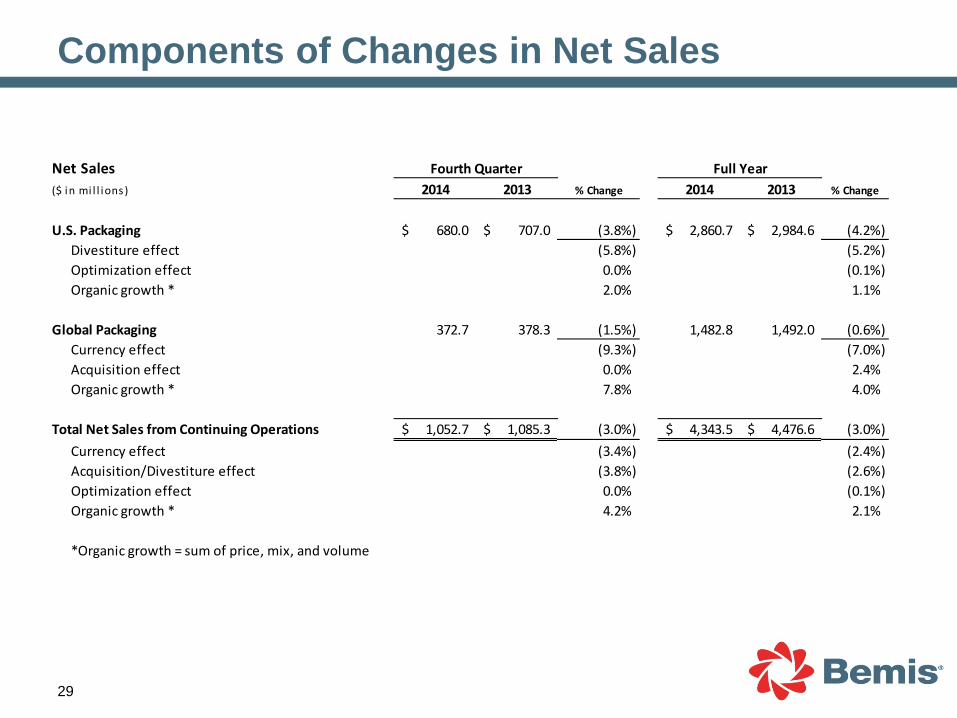

Components of Changes in Net Sales

Net Sales($ in mi l l ions) 2014 2013 % Change 2014 2013 % Change

U.S. Packaging 680.0$ 707.0$ (3.8%) 2,860.7$ 2,984.6$ (4.2%)Divestiture effect (5.8%) (5.2%)Optimization effect 0.0% (0.1%)Organic growth * 2.0% 1.1%

Global Packaging 372.7 378.3 (1.5%) 1,482.8 1,492.0 (0.6%)Currency effect (9.3%) (7.0%)Acquisition effect 0.0% 2.4%Organic growth * 7.8% 4.0%

Total Net Sales from Continuing Operations 1,052.7$ 1,085.3$ (3.0%) 4,343.5$ 4,476.6$ (3.0%)Currency effect (3.4%) (2.4%)Acquisition/Divestiture effect (3.8%) (2.6%)Optimization effect 0.0% (0.1%)Organic growth * 4.2% 2.1%

*Organic growth = sum of price, mix, and volume

Fourth Quarter Full Year

30