![Database of StateDatabase of State Incentives forIncentives for ...€¦ · e:] Renewable Energy Energy Efficiency Select Incentive Type: Search by Incentive Type Select the database](https://static.fdocuments.us/doc/165x107/5f831940c58eab702e4e8486/database-of-statedatabase-of-state-incentives-forincentives-for-e-renewable.jpg)

Investments with Incentive Certificate - ey.comFILE/Investments_with_Incentive_Certificate.pdf · 2...

32

Investments with Incentive Certificate 2017

-

Upload

hoangthien -

Category

Documents

-

view

222 -

download

0

Transcript of Investments with Incentive Certificate - ey.comFILE/Investments_with_Incentive_Certificate.pdf · 2...

Investmentswith IncentiveCertificate2017

2 |

Table of ContentsA. Scope of application of incentives and supports ..........................4 1. Basis of incentive practice .......................................................4 2. Eligible persons and entities ....................................................4 3. Investments eligible for incentives and supports .......................5 4. Investments that will be incentivized under certain conditions ...6B. Regional classification, large-scale and strategic investments .....7 1. Purpose and limits of regional classification ..............................7 2. Regions in investment incentive practice ..................................7 3 Incentives and supports provided in the scope of regional incentive practice ....................................................................8 4. Support of investments with different incentive elements by project ....................................................................................8 5. Investmentsubjectseligibleforincentivesinİstanbul,Ankara, İzmirandBursa .................................................................... 11 6. Large-scale investments ....................................................... 15 7. Incentives and supports provided for large-scale investments . 15 8. Investments included in the scope of strategic investments .... 16 9. Incentives and supports provided for strategic investments .... 16 10. Primary investment subjects ................................................ 16 11.IncentivesProvidedUnderAttractionCentersProgramme ..... 17 12.Caseswhereinvestmentscanbenefitfromthesupports available to the lower region ................................................. 18 13. Minimum amount limitation defined for investments .............. 18 14. Limitations regarding intangible fixed assets ......................... 18 15. Incentives related to R&D and environment investments ........ 18C. Obtaining incentive certificate for investments ........................ 19 1. The authority for application for the incentive certificate ....... 19 2. Applicationsthatcanbefiledtolocalauthorities ................... 19 3. Documents required for the application for incentive certificate . 19 4. Expenditures not included in the scope of incentive certificate 20 5. Starting date of investment .................................................. 20 6. Investments that can be made under incentive certificate ...... 21 7. Amendmentsinthelistsofmachinesand started the attachment of the incentive certificate ................. 21 8. Extension of the period specified in the incentive certificates . 21 9. Force majeure and emergency cases ..................................... 21 10.Changeofinvestmentsubjectaftertheinvestmenthasstarted .....21 11. Move of investments to other regions.................................... 22 12. Sale or transfer of the machines and equipment within the scope of incentive certificate ........................................... 22 13. Sale or transfer of investment goods which have not completed 5 years .......................................................... 22 14. Sanctions to be imposed in case of unauthorized sales ........... 22 15. Sanctions to be imposed on those acting in conflict with the provisions of investment support and incentive practices ....... 22 16.Applicationofnewincentivelegislationtoformerinvestments .. 22D. Incentive application in financial leasing transactions.............. 23 1. Maximum amount limitation for investments conducted through financial leasing ...................................................... 23 2. CustomstaxandVATexemptionforthemachineryand equipment procured through financial leasing ....................... 23 3. Liability in case of the transfer of the machinery and equipment subject to financial leasing ............................ 23 4. Use of the machinery and equipment subject to the financial leasing transaction for another investment .............. 23 5. Tansfer transactions of the machinery and equipment subject to financial leasing .................................................... 23E. Incentive and support elements ............................................... 24 I. Customs tax exemption, VAT exemption and VAT refund ..... 24 1. Requirements of benefiting from the customs tax exemptionandVATexemption ............................................. 24 2. InvestmentsthatcanbenefitfromVATrefund ....................... 24 3. Goods that can be imported under the scope of customs tax exemption ...................................................................... 24 4. Limitations on benefiting from the customs tax exemption ..... 24 5. Customstaxexemptionspecificallygrantedtoautomobile and engine manufacture investments .................................... 24 6. The application in machinery and equipment imports realized after the incentive certificate application date ....................... 25 7. Inappropriate imported machinery and equipment from technical or qualitative aspects ..................................... 25 8. Actionstobetakenifimportationhasstartedbuthasnot been completed until the end of investment period ................ 25 9. Importation of used machinery and equipment under the scope of the incentive certificate ..................................... 25

10. Importation of used complete facilities from free zones .......... 25 11.Valueaddedtaxtreatmentoftheimportedmachineryand equipment ........................................................................... 25 II. Interest support ................................................................. 26 1. Requirements of benefiting from the interest support ............ 26 2. Advantagesofferedtoinvestorsinthescopeofinterestsupport .. 26 3. Regional distinction in strategic investments and R&D and environmental investments................................................... 26 4. Applicationofinterestsupportforinvestmentstobe carried out through financial leasing ..................................... 26 5. Maximum amount of the interest support .............................. 26 6. Interest support payments in strategic investments ............... 26 7. Interest support for foreign exchange loans ........................... 26 8. Utilization of interest support stated in incentive certificates .. 26 9. “Intermediary institution” in interest support application ....... 26 10. Investments where interest support is not applicable ............. 27 11.Sanctionstobeappliediftheinterests,principalmoneyor dividends of the loans are not paid ........................................ 27 12.Applicationofinterestsupportiftheinvestmentistransferred .. 27 13. Sanctions to be applied if the loan is used for another purpose .. 27 III. Support on insurance premium employer’s share ............... 27 1. Scope of the insurance premium employer’s share support .... 27 2. Main requirement of benefiting from the insurance premium employer’s share support ..................................................... 28 3. Sanctions to be applied if the premiums are paid with delay ... 28 4. Beginning date of the insurance premium employer’s share support ............................................................................... 28 5. Scope of the application of insurance premium employer’s share support in shipbuilding investments ............................. 28 6. Utilization of insurance premium employer’s share for workersemployedbysub-employers ..................................... 28 7. Utilization of support by the transferee if the investment is transferred ....................................................................... 28 IV. Insurance premium support ............................................... 28 1. Scope of insurance premium support .................................... 28 2. Main requirement of benefiting from insurance premium suppor ................................................................................. 28 3. Sanctions to be applied if the premiums are paid with delay ... 28 4. Beginning date of insurance premium support ....................... 28 5. Utilizationofthissupportforworkersemployedby sub-employers ..................................................................... 29 6. Utilization of the support in case of the transfer of investment ... 29 V. Income withholding tax support ......................................... 29 1. Scope of income withholding tax support .............................. 29 2. Sanctions to be applied if the investment is not completed oriftheincentivecertificateisrevoked ................................. 29 3. Utilization of the support in case of the transfer of investment ... 29 VI. Reduced corporate tax application ..................................... 29 1. Reduced corporate tax application ........................................ 29 2. Gains of investors which can benefit from the reduced tax rate .. 29 3. Taxpayers and investments excluded from the reduced corporate tax application ...................................................... 29 4. Investments that can benefit from the tax reduction .............. 29 5. Expenditures that cannot benefit from the reduced tax application ........................................................................... 30 6. Beginning date of reduced tax application ............................. 30 7. Limitations on the reduced tax rate application ...................... 30 8. Investment contribution amount and investment contribution rate .................................................................. 30 9. Applicableinvestmentcontributionratesandcorporatetax reduction rates .................................................................... 30 10. Investment contribution rates and corporate tax reduction rates applicable to strategic investments ................ 30 11.Applicationofreducedtaxrateinadvancetaxperiods ........... 30 12. Sanctions to be applied if the requirements for benefiting from the reduced rate are violated ........................ 30 13. Investment allowance carried forward to following periods ..... 30 14.Applicationofreducedcorporatetaxincaseof the transfer of investment .................................................... 30 15. Determination of the profit subject to reduced corporate tax in expansionary investments ........................................... 31 16. “Revaluated amount” and “fixed asset amount” .................... 31 VII. Allocation of investment location ....................................... 31 VIII. Other tax incentives ......................................................... 31

| 3

Investments with Incentive Certificate

Introduction

On6April2012,theGovernmenthasannouncedthenewincentivepackagewiththemain objective of directing savings to investmentswith high added value, increasingproductionandemployment,encouragingregional,large-scaleandstrategicinvestmentswith high technology and research & development content that will increase international competitivepower, increasinginternationaldirectinvestments,eliminatingdifferencesin regional development and supporting investments of clustering end environmental protection and research and development activities in line with the objectives set forth in development plans and annual programs.

The announcementsmade in this incentive package have been implemented by the“Decree on State Incentives in Investments” numbered 2012/3305, promulgated inthe Official Gazette dated 19 June 2012. Having entered into force on the date of its promulgation, theDecreemainly contains provisions on the incentives and supportsprovided to the investments made under incentive certificates and on the requirements fortheapplicationofsuch incentives.CouncilofMinistersDecreespromulgated lateronvariousdateshavemadecertainamendmentstotheCouncilofMinistersDecreeno.2012/3305.

We have prepared this study titled Investments with Incentive Certificate in order to provide an overview of incentives and supports pursuant to the “Decrees on State Incentives in Investments” and “Communiqués on the Implementation of theDecreeon State Incentives in Investments” promulgated in relation with these decrees and to respondtopotentialquestionsintheframeworkofbasicprinciples.

Aswecannotaddressall issues includedwithinthe legislation inthisstudy, investorsshouldnotexpecttofindanswertoalloftheirquestionshere.Wewould liketonotehere that the statements of the Ministry of Economy and Ministry of Finance should be followed regarding the hesitations arising in the practice. We hope that our study will be beneficial for the entrepreneurs having new investment plans.

Yourssincerely,

EYTurkey

This study titled “Investments with Incentive Certificate” has been prepared by EY profes-sionals in order to give general information to entrepreneurs on incentive and support elements specifiedwithinthescopeofCouncilofMinistersDecreeno.2012/3305(Decree)bytakingintoaccount the related provisions of tax and incentive legislation effective as of 5 February 2017. EYandKuzeyYeminliMaliMüşavirlikveBağımsızDenetimA.Ş.cannotbeheldresponsibleforthe information and explanations included in this study. Since our tax legislation is amended frequentlyandcanbeinterpretedfromdifferentperspectives,werecommendseekingprofes-sionalassistancefromtheexpertsbeforetakingactioninanyissue.

4 |

❱ 1. Basis of incentive practice

ThebasisofthepracticeisCouncilofMinistersDecreeno.2012/3305onStateIncentivesinInvestments,whichbecameeffectiveon19June2012whenitwaspromulgatedintheOfficialGazette(CMDorDecree).TheDecreeincludesprovisionsonincentiveandsupport elements to be granted by the State to the investments with incentive certificate. Procedures and principles on the application of this Decree were determined with the “CommuniquéontheImplementationoftheDecreeonStateIncentivesinInvestments”no.2012/3305,promulgatedintheOfficialGazettedated20July2012.

However,variousamendmentshavebeenmadeinthisDecreeno.2012/3305bythefollowingCouncilofMinistersDecrees:

• Decreeno.2012/3802,promulgatedintheOfficialGazettedated13.10.2012,• Decreeno.2013/4288,promulgatedintheOfficialGazettedated15.02.2013,• Decreeno.2013/4763,promulgatedintheOfficialGazettedated30.05.2013,• Decreeno.2014/6058,promulgatedintheOfficialGazettedated09.05.2014,• Decreeno.2014/6588,promulgatedintheOfficialGazettedated06.08.2014,• Decreeno.2014/7273,promulgatedintheOfficialGazettedated05.03.2015,• Decreeno.2015/7496,promulgatedintheOfficialGazettedated08.04.2015,• Decreeno.2015/8050,promulgatedintheOfficialGazettedated27.08.2015,• Decreeno.2015/8216,promulgatedintheOfficialGazettedated19.11.2015,• Decreeno.2016/9139,promulgatedintheOfficialGazettedated05.10.2016,• Decreeno.2016/9495,promulgatedintheOfficialGazettedated26.11.2016and• Decree no. 2017/9917 promulgated in the Official Gazette dated 22.02.2017

Communiquéno.2012/1on the Implementation of theDecreeonState Incentives inInvestments,whichbecameeffectiveuponitspromulgationintheOfficialGazettedated20 June 2012, has determined the principles for the application of the Decree no.2012/3305.Thiscommuniquéhasalsorepealed theCommuniquéno.2009/1on theImplementationoftheDecreeonStateIncentivesinInvestments,whichwaspromulgatedintheOfficialGazettedated28July2009.Furthermore,variousamendmentshavebeenmadeintheCommuniquéno.2012/1bytheCommuniquéno.2014/1promulgatedinthe Official Gazette dated 10.04.2014, Communiqué no. 2014/2 promulgated in theOfficial Gazette dated 08.05.2014, and Communiqué no. 2014/3 promulgated in theOfficialGazettedated25.09.2014.Furthermore,amendmentshadbeenmadeonArticle32/AofCorporatkeTaxLawthroughtheCorporateTaxGeneralCommuniqueseriesno.10publishedintheOfficialGazettedated5August2016.

“LawontheAmendmentstotheLawontheCollectionofPublicReceivablesandCertainOtherLaws”no.6322,promulgatedintheOfficialGazettedated15June2012and“LawontheAmendmentstotheTurkeyRetirementFundLawandCertainLawsandDecrees”no.6770,promulgated in theOfficialGazettedated15June2012havechanged theprovisions and added new provisions in relevant laws with respect to the incentives and supports under the legislation in question.

❱ 2. Eligible persons and entities

Real persons, ordinary partnerships, equity companies, cooperatives, associations,businesspartnerships,publicinstitutionsandorganizations(generalandspecialbudgetedinstitutionsandorganizations,specialprovincialadministrations,municipalitiesandstate-owned enterprises and institutions and organizations having shares at a rate higher than 50%inthecapitalsoftheseinstitutions)andfoundationsandprofessionalassociationsinthenatureofpublicinstitutionandTurkishbranchesofforeigncompaniescanbenefitfromtheregulation,providedthattheyobtaintheincentivecertificate.

Applicationsonincentivecertificatemadeforlegalentitieswithincompleteincorporationprocedures are not processed.

A. Scope of application of incentives and supports

| 5

Investments with Incentive Certificate

❱ 3. Investments eligible for incentives and supports

Investments ineligible to benefit from the incentives and supportsarespecifiedinAnnex4attachedtotheDecree.Evenifthe investments listed below fulfill all other conditions specified intheDecree,theystillcannotbenefitanyoftheincentiveandsupport elements mentioned in the Decree.

a. Agriculture and agricultural industry

1. Flour,semolina(excludingpastaproductionandintegratedsemolinainvestmentsandcornsemolina),fodder(excludingfishmeal, fish oil, fish feed and fodder productionwithinintegratedanimalhusbandryproduction),cornstarchandstarch-based sugar (excluding investments on exclusivelycrystalfructoseproductionfromstarchmilk)

2. Enterprisesrenderingfoodservice(catering).

3. Sugar cube.

4. Greenhouse investments under 5 decare.

5. Crop production (excluding greenhouse cultivation above5 decare,mushroom cultivation and cultivation of foragecropswithinintegratedanimalhusbandryinvestments).

6. Animalhusbandryinvestmentsexcludingintegratedanimalhusbandry investments to be incentivized within the scope of regional investments and animal husbandry investments to be supported conditionally.

7. Milk processing investments of and under a productioncapacity of 5 tons/day.

b. Production, energy and mining investments

1. Brick and roof tile manufacturing investments excludinginvestments of modernization.

2. Unginned cotton processing investments.

3. Yarn and weaving investments (except wool yarninvestments,yarninvestmentsoverTL15Million,weavinginvestments over TL 5 Million, and investments for theproduction of smart and multifunctional textile, carpet,tufting,enweavedandunknottedfabricandsack)excludinginvestments of modernization.

4. Naturalgasbasedelectricproductioninvestments(Exceptfor completely new and expansionary investments licensed by the Energy Market Regulatory Authority before19/6/2012 and modernization investments aiming to reducespecificfuelconsumptionat leastby15%)(Decreeno.2015/7496Art.9)

5. Mining investments based on royalty contracts (mininginvestments made on public mine fields on basis of the contracts entered into with state institutions and organizations or their direct subsidiaries are not considered withinthisscope).

6. Investments for the manufacturing of iron and steel products containedinAnnex5(however,facilitiesfulfillingallofthecriteria below for these manufacturing subjects may only benefitfromthegeneralincentivesystem).

a. The total share of one or more than one legal entities or state institutions and organizations within the shareholding structure must not be equal to or more than 25%.

b. No other body can be holder of more than 25% of the capital.

c. The number of employees must be less than 250 persons per year.

d. The annual net sales income must not exceed the TurkishLiraequivalentof50MillionEuroorthefinancialbalancesheetvaluemustnotexceedtheTurkishLiraequivalent of 43 Million Euro

These criteria may also apply for the documents issued according totheDecreeoftheCouncilofMinistersNo.2009/15199)

7. Investments for synthetic fiber and synthetic yarn manufacturing using extrusion method except the investmentsofmodernization(however,suchmodernizationinvestments and investments for synthetic fiber and synthetic yarn manufacturing with extrusion method made bythebusinessesthatmeetallthecriteriainArticle7canonlybesupportedfromthegeneralinvestmentsystem).

c. Service sector

1. Educational investments excluding pre-school education,elementary education, secondary education, high school,college, university, higher education and technical andprofessional education; and investments for educating adults(suchascourses,privateteachinginstitutions),

2. Polyclinic, consulting room and shared consulting roominvestments.

3. Tourism accommodation facilities excluding hotels with tourism investment/operation certificates (including thosethat hold business license as a hotel business under the latestregulations),boutiquehotels,holidayvillages,specialrest areas and mountain resorts.

4. Press and media investments excluding national daily newspaper printing services, television and radiobroadcasting, and printing, press house and packaginginvestments.

5. Cinematheaterinvestments.

6. Residential construction and contracting services investments.

7. Bus, tow truck and trailer investments for passenger andcargo transportation (Except investments undertaken bymunicipalities).

8. Investments for wholesale and retail trade including hypermarket, trade center, shopping center and car parkinvestments.

9. Land vehicles maintenance and service station investments.

10. Petroleumproduct(includingLPG)distributioninvestments,fuel station investments.

11. Highway recreation facilities investments.

6 |

12. Restaurants, cafeterias, entertainment venues, dailyexcursionfacilities,thermalcurefacilities,wellnesscenters,swimming pools.

13. Yacht import investments.

14. Vehicleleasinginvestments.

15. Carpetwashinginvestments.

16. Realestaterentingandbusinessactivities(exceptsoftware,R&D activities, data base activities, data processing,technical testing and analysis, packaging activities, andshows,exhibitionsandcongressactivities).

17. Excluding leasing activities, investments of financialintermediaries.

18. Investments of cold store the closed area of which is less than 500 m2.

19. Completelynewandexpansioninvestmentsofshipbuildingyards.

❱ 4. Investments that will be incentivized under certain conditions UnderAnnex4attachedtotheDecree,someinvestmentscanbenefit from the incentives and supports, provided that theymeet certain conditions. These investments and the related conditions are presented below.

a. Agriculture and agricultural industry

1. Minimum 150 cattle in integrated dairy cattle investments.

2. Minimum 150 cattle in integrated meat cattle investments.

3.Minimum150cattle/periodinintegratedstockcattlebreeding(meat/dairy)investments.

4. 100.000 pieces/period in integrated poultry investments.

5.1.000 ovine (sheep/goat)/period in integrated ovineinvestmentsformeatanddairy(stockincluded).

are compulsory.

b. Manufacturing industry

1. Total number of machines-systems in investments of flatbed knittingmustbeminimum60.

2.An incentive certificate is issued only for completely newinvestments in ready-mixed concrete investments with a minimum capacity of 100 m3/hour and above.

c. Service sector

1. Investment incentive certificates can be issued for integrated logistics investments having a covered area of at least 10,000m2,wherewarehousing, handling-packagingand automation services are offered together with customs andinsuranceservicesinoneormorethanonelocations,provided that the L2 certificate obtained from the Ministry of Transportation,MaritimeandCommunicationissubmitteduntil the end of the incentive period. Such incentive certificates cannot include vehicles for cargo transportation.

2. For pipe-line transportation as well as filling and storage facilityinvestmentsforpetroleumandnaturalgasproducts,an investment incentive certificate can be issued only for expendituresforfixedplant,excludingdistributionvehiclesand gas cylinders.

3. Forculturalinvestments,aninvestmentincentivecertificatecan be issued on basis of the culture investment certificate to be obtained from theMinistry ofCulture andTourism.However, except units exclusively built for this purpose,unitssuchasfoodandbeverage,sports,entertainmentandsales units are not covered within this scope.

4. Tourism investments such as entertainment center and theme parks without accommodation can be granted aninvestment incentive certificate provided that they possess a tourism certificate to be obtained from the Ministry of CultureandTourism.However,exceptunitsexclusivelybuiltforthispurpose,unitssuchasfoodandbeverage,sports,entertainment and sales units are not covered within this scope.

5. Investment incentive certificates can be issued for fair,congress,exhibitionandculturalcenterinvestmentswhichpossessaCultureorTourismCertificatetobeobtainedfromtheMinistryofCultureandTourism.Forfairandexhibitioncentersminimumcoveredareamustbeatleast5,000m2 excludingparkinglot.Minimumrequirednumberofseatsis1,000forcongresscenters,and2,500forculturalcenters.

6. Minimum fixed investment amount of TRY 10 Million is required for sports facility investments.

7. Forairportgroundhandlingservicesinvestments,vehiclesthat do not enter into city traffic but used only in the apron can be included within the context of investment incentive certificate. Passenger cars cannot be included within the scope of the project.

8. For aircrafts to be procured in airway services and/or cargo transportation investments, it is required that passengeraircrafts must have minimum 50 seats per unit and cargo aircraftsmusthaveminimum30,000kgofcargocapacity.Investment incentive certificates cannot be issued for investments aiming at general purpose and air taxi services except for the investments whose field of activity is exclusively airway services and/or cargo transportation.

9. Investment goods used by the ones who get the service in servicesinvestmentsinwhichthetelecommunication,radio,televisionanddata signals transmittedvia satellite, radio,cableetc.arecombinedinasinglepackageandofferedtothe end consumers cannot benefit from the support items.

10. Investmentsofpublicinstitutions,municipalities,provincialspecialadministrations,unions,cooperativesetc.relatedtotheir field of operation will be evaluated on project basis and may be assigned an investment incentive certificate.

11. Each crane should have minimum 100 tons of lifting capacity for investments only aiming at crane services. The import of second hand cranes under 500 tons lifting capacity is not allowed.

12. Minimum fixed investment amount of TL 2 Million is required for laundry washing and drying investments.

13. The yacht length should be minimum 24 meters in order to obtain an incentive certificate for yacht building investments.

| 7

Investments with Incentive Certificate

❱ 1. Purpose and limits of regional classification

UnderCouncilofMinistersDecreeno.2002/4720,StatisticalClassificationofRegionalUnitshasbeenperformedacrossthecountrytocollectanddevelopregionalstatistics,toconductsocio-economic analysis of regions, to determine the framework of regional politics and tocreate comparable statistical database in compliance with European Union Regional Statistics System.UndertheDecree,provinceshavebeendividedinto6groupsaccordingtotheirsocio-economic development levels. Provinces divided into 6 groups in the scope of statistical regional classification are provided in tables below.

❱ 2. Regions in investment incentive practice

Region 1 Region 2 Region 3 Region 4 Region 5 Region 6

Ankara Adana Balıkesir Afyonkarahisar Adıyaman Ağrı

Antalya Aydın Bilecik Amasya Aksaray Ardahan

Bursa Bolu Burdur Artvin Bayburt Batman

Eskişehir

Çanakkale(excluding

Bozcaada and Gökçeada)

Gaziantep Bartın Çankırı Bingöl

İstanbul Denizli Karabük Çorum Erzurum Bitlis

İzmir Edirne Karaman Düzce Giresun Diyarbakır

Kocaeli Isparta Manisa Elazığ Gümüşhane Hakkari

Muğla Kayseri Mersin Erzincan Kahramanmaraş Iğdır

Kırklareli Samsun Hatay Kilis Kars

Konya Trabzon Kastamonu Niğde Mardin

Sakarya Uşak Kırıkkale Ordu Muş

Tekirdağ Zonguldak Kırşehir Osmaniye Siirt

Yalova Kütahya Sinop Şanlıurfa

Malatya Tokat Şırnak

Nevşehir Tunceli Van

Rize Yozgat

Çanakkale(excluding

Bozcaada and Gökçeada)

Sivas

B. Regional classification, large-scale and strategic investments

8 |

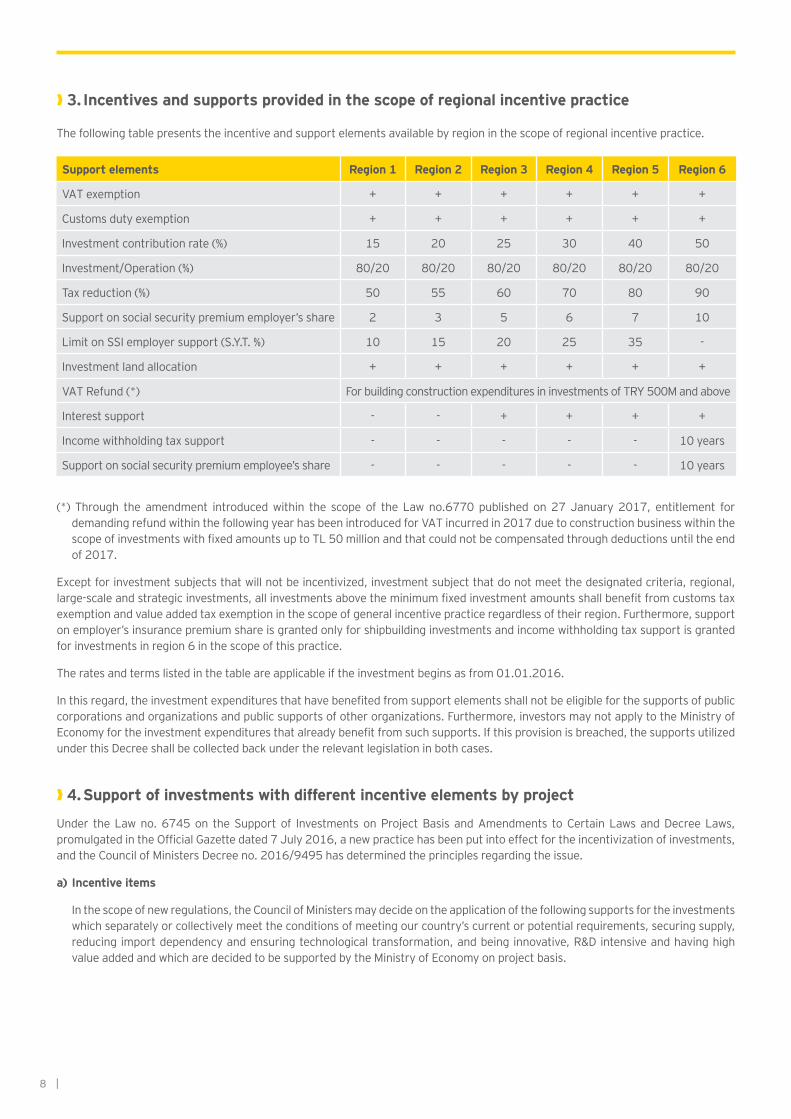

❱ 3. Incentives and supports provided in the scope of regional incentive practice

The following table presents the incentive and support elements available by region in the scope of regional incentive practice.

Support elements Region 1 Region 2 Region 3 Region 4 Region 5 Region 6

VATexemption + + + + + +

Customsdutyexemption + + + + + +

Investmentcontributionrate(%) 15 20 25 30 40 50

Investment/Operation(%) 80/20 80/20 80/20 80/20 80/20 80/20

Taxreduction(%) 50 55 60 70 80 90

Support on social security premium employer’s share 2 3 5 6 7 10

LimitonSSIemployersupport(S.Y.T.%) 10 15 20 25 35 -

Investment land allocation + + + + + +

VATRefund(*) For building construction expenditures in investments of TRY 500M and above

Interest support - - + + + +

Income withholding tax support - - - - - 10 years

Support on social security premium employee’s share - - - - - 10 years

(*) Through the amendment introducedwithin the scope of the Lawno.6770published on27January2017, entitlement fordemandingrefundwithinthefollowingyearhasbeenintroducedforVATincurredin2017duetoconstructionbusinesswithinthescope of investments with fixed amounts up to TL 50 million and that could not be compensated through deductions until the end of 2017.

Exceptforinvestmentsubjectsthatwillnotbeincentivized,investmentsubjectthatdonotmeetthedesignatedcriteria,regional,large-scaleandstrategicinvestments,allinvestmentsabovetheminimumfixedinvestmentamountsshallbenefitfromcustomstaxexemptionandvalueaddedtaxexemptioninthescopeofgeneralincentivepracticeregardlessoftheirregion.Furthermore,supporton employer’s insurance premium share is granted only for shipbuilding investments and income withholding tax support is granted for investments in region 6 in the scope of this practice.

The rates and terms listed in the table are applicable if the investment begins as from 01.01.2016.

Inthisregard,theinvestmentexpendituresthathavebenefitedfromsupportelementsshallnotbeeligibleforthesupportsofpubliccorporationsandorganizationsandpublicsupportsofotherorganizations.Furthermore,investorsmaynotapplytotheMinistryofEconomyfortheinvestmentexpendituresthatalreadybenefitfromsuchsupports.Ifthisprovisionisbreached,thesupportsutilizedunderthisDecreeshallbecollectedbackundertherelevantlegislationinbothcases.

❱ 4. Support of investments with different incentive elements by project

Under theLawno.6745on theSupportof InvestmentsonProjectBasisandAmendments toCertainLawsandDecreeLaws,promulgatedintheOfficialGazettedated7July2016,anewpracticehasbeenputintoeffectfortheincentivizationofinvestments,andtheCouncilofMinistersDecreeno.2016/9495hasdeterminedtheprinciplesregardingtheissue.

a) Incentive items

Inthescopeofnewregulations,theCouncilofMinistersmaydecideontheapplicationofthefollowingsupportsfortheinvestmentswhichseparatelyorcollectivelymeettheconditionsofmeetingourcountry’scurrentorpotentialrequirements,securingsupply,reducingimportdependencyandensuringtechnologicaltransformation,andbeinginnovative,R&Dintensiveandhavinghighvalue added and which are decided to be supported by the Ministry of Economy on project basis.

| 9

Investments with Incentive Certificate

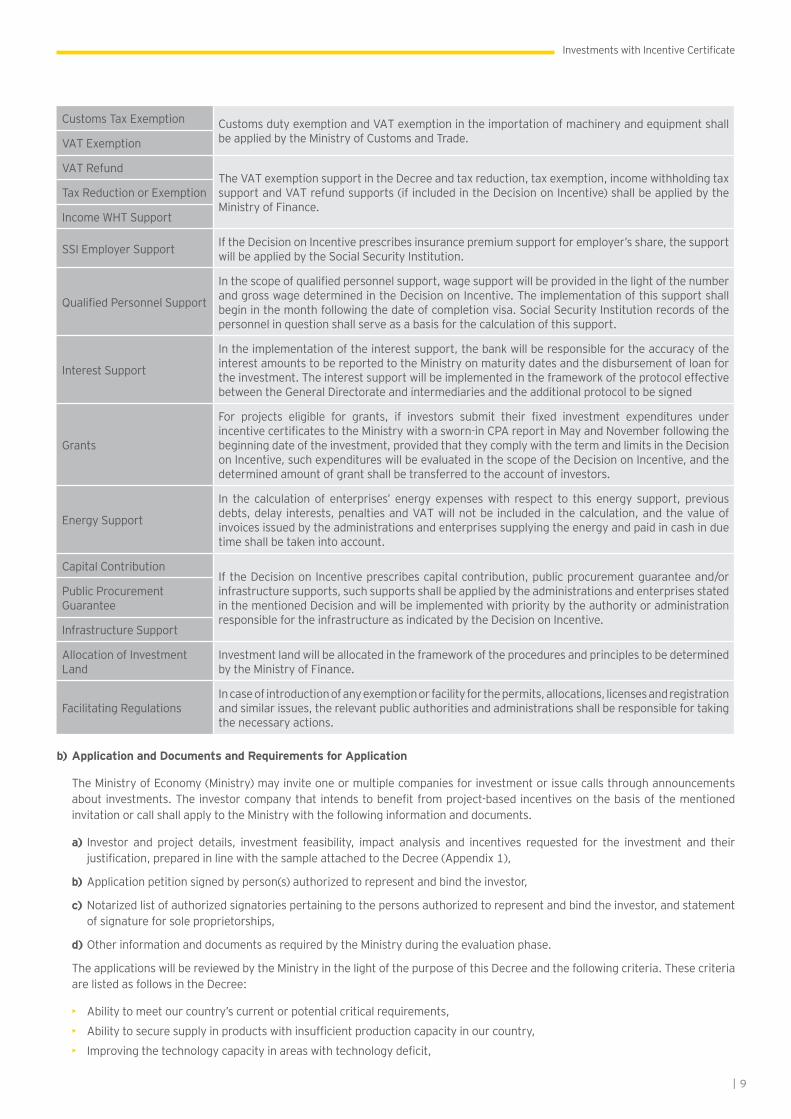

CustomsTaxExemption CustomsdutyexemptionandVATexemptionintheimportationofmachineryandequipmentshallbeappliedbytheMinistryofCustomsandTrade.VATExemption

VATRefundTheVATexemptionsupportintheDecreeandtaxreduction,taxexemption,incomewithholdingtaxsupportandVATrefundsupports(ifincludedintheDecisiononIncentive)shallbeappliedbytheMinistry of Finance.

Tax Reduction or Exemption

Income WHT Support

SSI Employer Support IftheDecisiononIncentiveprescribesinsurancepremiumsupportforemployer’sshare,thesupportwill be applied by the Social Security Institution.

Qualified Personnel Support

Inthescopeofqualifiedpersonnelsupport,wagesupportwillbeprovidedinthelightofthenumberand gross wage determined in the Decision on Incentive. The implementation of this support shall begin in the month following the date of completion visa. Social Security Institution records of the personnel in question shall serve as a basis for the calculation of this support.

Interest Support

Intheimplementationoftheinterestsupport,thebankwillberesponsiblefortheaccuracyoftheinterest amounts to be reported to the Ministry on maturity dates and the disbursement of loan for theinvestment.Theinterestsupportwillbeimplementedintheframeworkoftheprotocoleffectivebetween the General Directorate and intermediaries and the additional protocol to be signed

Grants

For projects eligible for grants, if investors submit their fixed investment expenditures underincentivecertificatestotheMinistrywithasworn-inCPAreportinMayandNovemberfollowingthebeginningdateoftheinvestment,providedthattheycomplywiththetermandlimitsintheDecisiononIncentive,suchexpenditureswillbeevaluatedinthescopeoftheDecisiononIncentive,andthedetermined amount of grant shall be transferred to the account of investors.

Energy Support

In thecalculationofenterprises’ energyexpenseswith respect to thisenergysupport,previousdebts,delayinterests,penaltiesandVATwillnotbeincludedinthecalculation,andthevalueofinvoices issued by the administrations and enterprises supplying the energy and paid in cash in due timeshallbetakenintoaccount.

CapitalContributionIftheDecisiononIncentiveprescribescapitalcontribution,publicprocurementguaranteeand/orinfrastructuresupports,suchsupportsshallbeappliedbytheadministrationsandenterprisesstatedin the mentioned Decision and will be implemented with priority by the authority or administration responsible for the infrastructure as indicated by the Decision on Incentive.

Public Procurement Guarantee

Infrastructure Support

AllocationofInvestmentLand

Investmentlandwillbeallocatedintheframeworkoftheproceduresandprinciplestobedeterminedby the Ministry of Finance.

Facilitating RegulationsIncaseofintroductionofanyexemptionorfacilityforthepermits,allocations,licensesandregistrationandsimilarissues,therelevantpublicauthoritiesandadministrationsshallberesponsiblefortakingthe necessary actions.

b) Application and Documents and Requirements for Application

TheMinistryofEconomy(Ministry)mayinviteoneormultiplecompaniesforinvestmentorissuecallsthroughannouncementsabout investments. The investor company that intends to benefit from project-based incentives on the basis of the mentioned invitation or call shall apply to the Ministry with the following information and documents.

a) Investor and project details, investment feasibility, impact analysis and incentives requested for the investment and theirjustification,preparedinlinewiththesampleattachedtotheDecree(Appendix1),

b)Applicationpetitionsignedbyperson(s)authorizedtorepresentandbindtheinvestor,

c) Notarizedlistofauthorizedsignatoriespertainingtothepersonsauthorizedtorepresentandbindtheinvestor,andstatementofsignatureforsoleproprietorships,

d) Other information and documents as required by the Ministry during the evaluation phase.

The applications will be reviewed by the Ministry in the light of the purpose of this Decree and the following criteria. These criteria arelistedasfollowsintheDecree:

• Abilitytomeetourcountry’scurrentorpotentialcriticalrequirements,

• Abilitytosecuresupplyinproductswithinsufficientproductioncapacityinourcountry,

• Improvingthetechnologycapacityinareaswithtechnologydeficit,

10 |

• Reducing import dependency in areas yielding foreign tradedeficit,

• Havingahighvalueadded,

• Ability to ensure production with new generationtechnologieswhicharenotmanufacturedinourcountry,

• Ability to offer competitive power to our country indifferentsectors,

• Ability to accelerate technological transformation in thesectors involved in transactions and to offer positive externalitytosuchsectors,

• BeinganinnovativeinvestmentbasedonR&D,

• Being an investment for the manufacturing of processed products with high added value to be made in sectors which negatively affect the current account balance and experienceshortageinrawmaterials,

• Beinganinvestmentinintegratedproductionwhichmakesuse of our country’s raw material potential.

c) Minimum investment scale and Promulgation of the Decision on Incentive

The minimum fixed investment amount must be 100 million US dollars for the evaluation of projects under the Decree.

The project(s) approved as a result of the evaluation shall bepresented to theCouncilofMinistersby theMinistry,and theDecision on Incentive shall be promulgated for the projects decidedtobesupportedbytheCouncilofMinisters.

This “Decision on Incentive” shall include the characteristics ofthe investmentsuchassubject,capacity,amountandtermof investment as determined by the Council of Ministers,commitments of the investor, incentives to be granted to theinvestment, institutions responsible for the application ofthe incentives and rates, terms and quantities relating to theincentives,andspecialrequirementssetforthfortheinvestment.

Ontheotherhand,applicationsthatarenotdeemedeligibleforincentive can be evaluated in the scope of the “Decree on State Incentives” upon the request of the investor. Therefore, theinvestments not deemed eligible for project-based investment supports may be entitled to benefit from incentives and supports under the Decree no. 2012/3305.

d) Incentive certificate, term of investment and completion visa

The Ministry shall issue an incentive certificate for the projects decidedtobesupportedbytheCouncilofMinistersonprojectbasis.

The beginning and ending dates of the investment shall be determined in the Decision on Incentive; the investments to be supported must be completed within the time specified in the DecisiononIncentive,includingextratimes.

The completion visa must be issued after the completion of the investment as a result of the expert review to be conducted by the committee that will consist of the personnel of the General Directorate of Incentive Implementation and Foreign Investment of the Ministry of Economy (General Directorate) and the

personnel assigned by other relevant ministries depending on the investment subject.

e) Explanation on the practice

It is stipulated in the Decree that the implementation of the support items foreseen in the incentive certificate by related publicauthoritiesandinstitutionsisobligatory,andtheMinistrymay delegate certain procedures concerning the implementation within the scope of this Decree to other public authorities and institutionswithintheframeworkofproceduresandprinciples.

The Decree further states that if the investment is not realized or the obligations serving as a basis for the use of project-based supportsarenot fulfilledand if it is requestedso, theprojectmay be evaluated in the scope of the provisions of the Decree on StateIncentivesinInvestments,whichiscurrentlyinforce,butit is stated that the supports benefited from under this Decree but not provided in the scope of Decree on State Incentives in Investments and the supports provided excessively shall be takenbackunderparagraphoneofarticle11oftheDecreetitled“Sanctions”.

f) Transfer of company shares and investment

The transfer of the investment will be subject to the Ministry’s permit andPrimeMinistry’s approval in the frameworkof thetime and conditions specified in the Decision on Incentive.

Ontheotherhand,ifthetransferofinvestmentisauthorized,thetransferee may benefit from the remaining portions of supports and the exceptions and exemptions provided that it fulfils the nature and commitments of the investment.

Except the case where the investor company sells its shares on Istanbul Stock Exchange through public offering, transfer ofshares before the completion of the investment shall also be subject to the Ministry’s authorization.

g) Sanctions

According to article 11 of the Decree, excluding the reasonsarising from public, the investor shall be responsible for nottimely realizing the investment. If the investor does not fulfil its liabilitiesundertheDecisiononIncentive,thetaxesnotaccruedon time due to

•Applicationofreducedcorporatetaxorexemption,and

•Incomewithholdingtaxincentive

shall be collected with delay interest without the application of anytaxlosspenalty,whereasothersupportswillbetakenbackunder the provisions of Law no. 6183.

Investment expenditures benefiting from the supports under this Decree shall not benefit from the supports of other public authorities and administrations. For investment expenditures that benefit or will benefit from the supports of other public authoritiesandadministrationsontheotherhand,noapplicationmay be filed to the Ministry to benefit from the supports covered by this Decree.

| 11

Investments with Incentive Certificate

Incaseofbreachofthisarticle,thesupportsenjoyedunderthisDecreeshallbetakenback.

h) Authorization, audit and roles of sworn-in certified public accountants

The Ministry of Economy has been authorized to do the following for the implementation of this Decree.

a)Determinetheproceduresandprinciplesforimplementation,

b) Take necessary measures in the light of macroeconomicpolicies and developments and introduce regulations accordingly,

c) Demandanykindofadditionalinformation,document,advice,permit, license etc. from relevant persons, administrationsandenterprises,

d) ExceptforthosespecifiedintheDecree,reviewandconcludespecialcases,provideadvice,conductnecessaryproceduresrelated to the incentive certificate in case of any force majeure and extraordinary events and resolve the disputes arising in practice,

e) Inspect whether the requirements in the incentive certificate areobservedandtakenecessarymeasuresdependingontheconclusions of audits.

Investors are obliged to submit the details of the fulfilment of their commitments related to the investment during the term of investment and operation and the amount of the support used by giving a sworn-in certified public accountant report every January and July during the time specified in the Decision on Incentive; these matters shall be followed up by the Ministry or the authorities and administrations to be assigned by the Ministry.

Another issue that must be substantiated with a sworn-incertified public accountant report is the projects that benefit from grants. For projects decided to be supported with grants undertheDecisionon Incentive, if investorssubmittheir fixedinvestment expenditures under incentive certificates to the Ministry with a sworn-in CPA report in May and Novemberfollowing the beginning date of the investment, provided thattheycomplywiththetermandlimitsintheDecisiononIncentive,such expenditures will be evaluated in the scope of the Decision on Incentive, and the determined amount of grant shall betransferred to the account of investors.

Authorities and administrations appointed for implementationin the Decision on Incentive shall be obliged to complete their duties in due time and notify the Ministry about the latest situation of the transactions every January until the conclusion of the incentives they are responsible for following the issuance of incentive certificate.

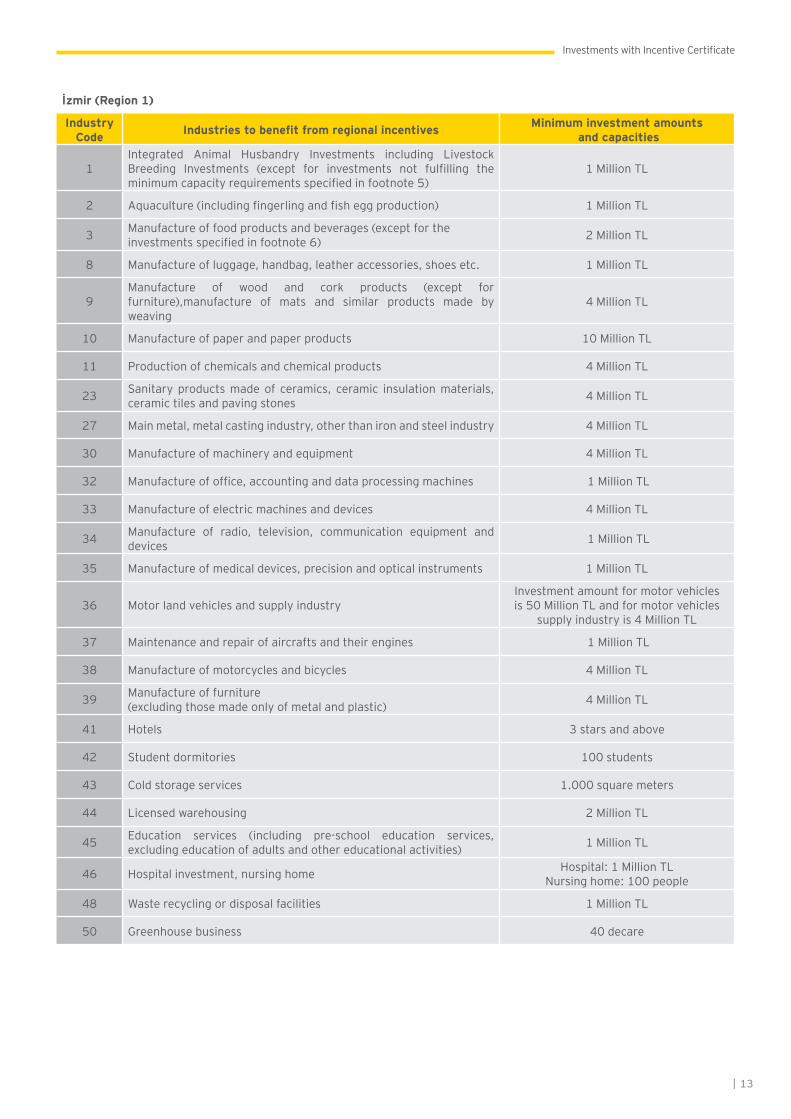

❱ 5. Investment subjects eligible for incentives in İstanbul, Ankara, İzmir and Bursa

It is stated in article 4 of the Decree that the investment subjects to benefit from regional incentives are demonstrated in the list 2-B attached to the Decree considering the investment potential and competitive power of each group of province shown above. In other words, not every investment is entitled to regionalincentives. List 2 attached to the Decree must be taken intoaccount in order to determine which investment subjects will benefit from incentives in the provinces grouped by region in the answerofquestion5.Sincethislististoolong,onlytheindustriesthat will benefit from incentives in 4 major provinces are included in our study.

Toserveasanexample,theinvestmentsubjectstobeincentivizedin İstanbul, Ankara, İzmir and Bursa within the scope of thisDecree are presented in the following tables.

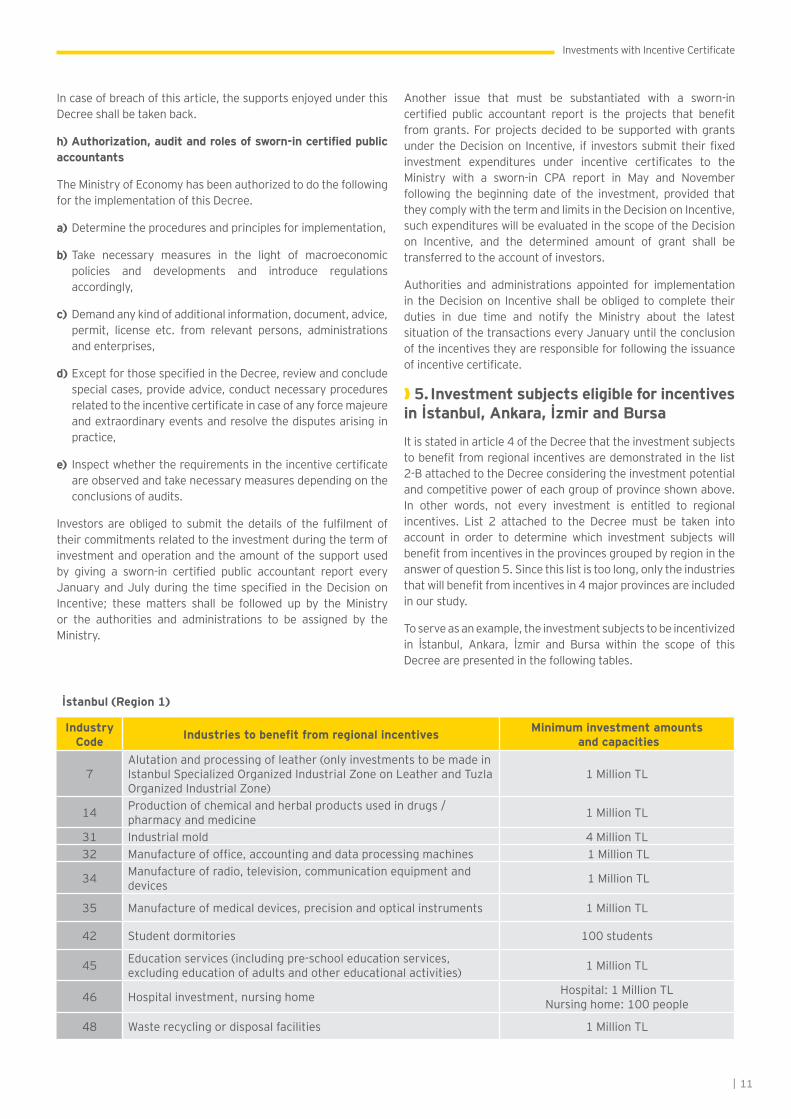

İstanbul (Region 1)

Industry Code Industries to benefit from regional incentives Minimum investment amounts

and capacities

7Alutationandprocessingofleather(onlyinvestmentstobemadeinIstanbul Specialized Organized Industrial Zone on Leather and Tuzla OrganizedIndustrialZone)

1 Million TL

14 Production of chemical and herbal products used in drugs / pharmacy and medicine 1 Million TL

31 Industrial mold 4 Million TL32 Manufactureofoffice,accountinganddataprocessingmachines 1 Million TL

34 Manufactureofradio,television,communicationequipmentanddevices 1 Million TL

35 Manufactureofmedicaldevices,precisionandopticalinstruments 1 Million TL

42 Student dormitories 100 students

45 Educationservices(includingpre-schooleducationservices,excludingeducationofadultsandothereducationalactivities) 1 Million TL

46 Hospitalinvestment,nursinghome Hospital:1MillionTLNursinghome:100people

48 Waste recycling or disposal facilities 1 Million TL

12 |

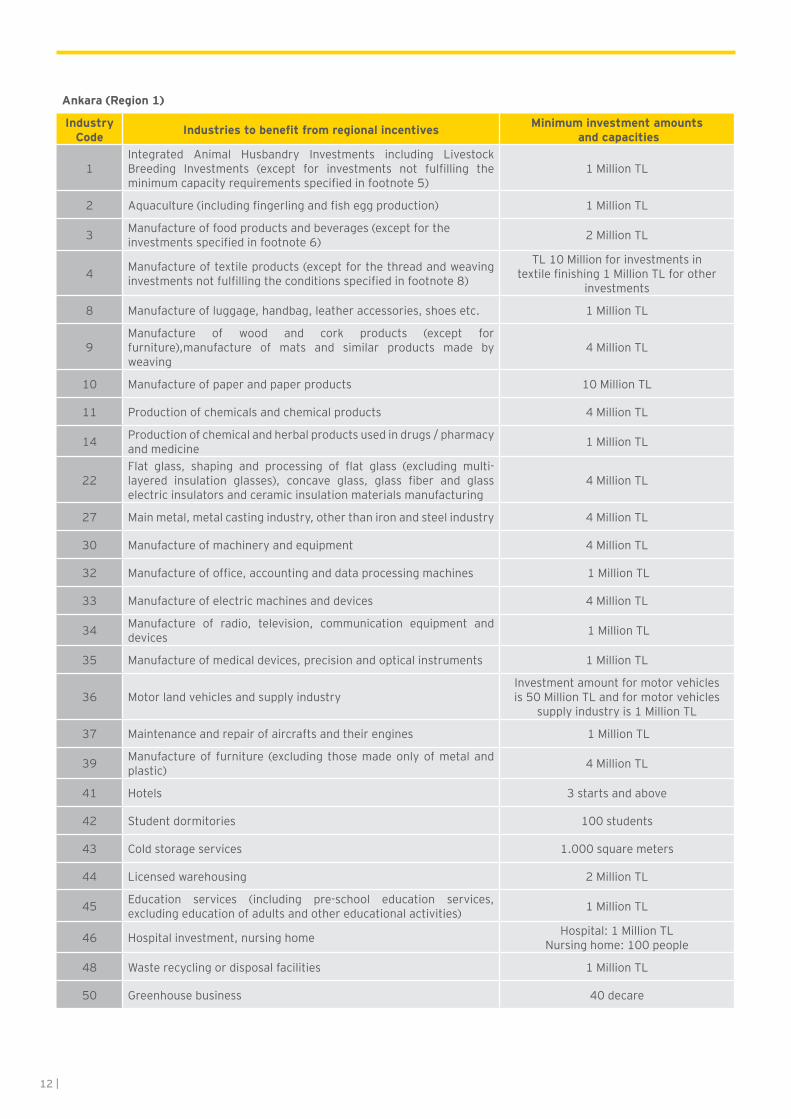

Ankara (Region 1)

Industry Code Industries to benefit from regional incentives Minimum investment amounts

and capacities

1Integrated Animal Husbandry Investments including LivestockBreeding Investments (except for investments not fulfilling theminimumcapacityrequirementsspecifiedinfootnote5)

1 Million TL

2 Aquaculture(includingfingerlingandfisheggproduction) 1 Million TL

3 Manufactureoffoodproductsandbeverages(exceptfortheinvestmentsspecifiedinfootnote6) 2 Million TL

4 Manufactureoftextileproducts(exceptforthethreadandweavinginvestmentsnotfulfillingtheconditionsspecifiedinfootnote8)

TL 10 Million for investments in textile finishing 1 Million TL for other

investments

8 Manufactureofluggage,handbag,leatheraccessories,shoesetc. 1 Million TL

9Manufacture of wood and cork products (except forfurniture),manufacture of mats and similar products made byweaving

4 Million TL

10 Manufacture of paper and paper products 10 Million TL

11 Production of chemicals and chemical products 4 Million TL

14 Production of chemical and herbal products used in drugs / pharmacy and medicine 1 Million TL

22Flat glass, shaping and processing of flat glass (excluding multi-layered insulation glasses), concave glass, glass fiber and glasselectric insulators and ceramic insulation materials manufacturing

4 Million TL

27 Mainmetal,metalcastingindustry,otherthanironandsteelindustry 4 Million TL

30 Manufacture of machinery and equipment 4 Million TL

32 Manufactureofoffice,accountinganddataprocessingmachines 1 Million TL

33 Manufacture of electric machines and devices 4 Million TL

34 Manufacture of radio, television, communication equipment anddevices 1 Million TL

35 Manufactureofmedicaldevices,precisionandopticalinstruments 1 Million TL

36 Motor land vehicles and supply industryInvestment amount for motor vehicles is 50 Million TL and for motor vehicles

supply industry is 1 Million TL

37 Maintenance and repair of aircrafts and their engines 1 Million TL

39 Manufactureof furniture (excluding thosemadeonlyofmetalandplastic) 4 Million TL

41 Hotels 3 starts and above

42 Student dormitories 100 students

43 Coldstorageservices 1.000 square meters

44 Licensed warehousing 2 Million TL

45 Education services (including pre-school education services,excludingeducationofadultsandothereducationalactivities) 1 Million TL

46 Hospitalinvestment,nursinghome Hospital:1MillionTLNursinghome:100people

48 Waste recycling or disposal facilities 1 Million TL

50 Greenhouse business 40 decare

| 13

Investments with Incentive Certificate

İzmir (Region 1)

Industry Code Industries to benefit from regional incentives Minimum investment amounts

and capacities

1Integrated Animal Husbandry Investments including LivestockBreeding Investments (except for investments not fulfilling theminimumcapacityrequirementsspecifiedinfootnote5)

1 Million TL

2 Aquaculture(includingfingerlingandfisheggproduction) 1 Million TL

3 Manufactureoffoodproductsandbeverages(exceptfortheinvestmentsspecifiedinfootnote6) 2 Million TL

8 Manufactureofluggage,handbag,leatheraccessories,shoesetc. 1 Million TL

9Manufacture of wood and cork products (except forfurniture),manufacture of mats and similar products made byweaving

4 Million TL

10 Manufacture of paper and paper products 10 Million TL

11 Production of chemicals and chemical products 4 Million TL

23 Sanitaryproductsmadeof ceramics, ceramic insulationmaterials,ceramic tiles and paving stones 4 Million TL

27 Mainmetal,metalcastingindustry,otherthanironandsteelindustry 4 Million TL

30 Manufacture of machinery and equipment 4 Million TL

32 Manufactureofoffice,accountinganddataprocessingmachines 1 Million TL

33 Manufacture of electric machines and devices 4 Million TL

34 Manufacture of radio, television, communication equipment anddevices 1 Million TL

35 Manufactureofmedicaldevices,precisionandopticalinstruments 1 Million TL

36 Motor land vehicles and supply industryInvestment amount for motor vehicles is 50 Million TL and for motor vehicles

supply industry is 4 Million TL

37 Maintenance and repair of aircrafts and their engines 1 Million TL

38 Manufacture of motorcycles and bicycles 4 Million TL

39 Manufacture of furniture (excludingthosemadeonlyofmetalandplastic) 4 Million TL

41 Hotels 3 stars and above

42 Student dormitories 100 students

43 Coldstorageservices 1.000 square meters

44 Licensed warehousing 2 Million TL

45 Education services (including pre-school education services,excludingeducationofadultsandothereducationalactivities) 1 Million TL

46 Hospitalinvestment,nursinghome Hospital:1MillionTLNursinghome:100people

48 Waste recycling or disposal facilities 1 Million TL

50 Greenhouse business 40 decare

14 |

Bursa (Region 1)

Industry Code Industries to benefit from regional incentives Minimum investment amounts

and capacities

1Integrated Animal Husbandry Investments including LivestockBreeding Investments (except for investments not fulfilling theminimumcapacityrequirementsspecifiedinfootnote5)

1 Million TL

2 Aquaculture(includingfingerlingandfisheggproduction) 1 Million TL

3 Manufactureoffoodproductsandbeverages(exceptfortheinvestmentsspecifiedinfootnote6) 2 Million TL

4 Manufactureoftextileproducts(exceptforthethreadandweavinginvestmentsnotfulfillingtheconditionsspecifiedinfootnote8)

TL 10 Million for investments in textile finishing 2 Million TL for other

investments

9Manufacture of wood and cork products (except forfurniture),manufacture of mats and similar products made byweaving

4 Million TL

10 Manufacture of paper and paper products 10 Million TL

11 Production of chemicals and chemical products 4 Million TL

14 Production of chemical and herbal products used in drugs / pharmacy and medicine 1 Million TL

20

Manufacture of non-metallic mineral products (excluding tiles andbricksandbuildingmaterialsmadeofbakedclay,cement,concreteproducts for construction, ready-mixed concrete, mortar, multi-layeredinsulationglasses)

4 Million TL

27 Mainmetal,metalcastingindustry,otherthanironandsteelindustry 4 Million TL

30 Manufacture of machinery and equipment 4 Million TL

32 Manufactureofoffice,accountinganddataprocessingmachines 1 Million TL

33 Manufacture of electric machines and devices 4 Million TL

34 Manufacture of radio, television, communication equipment anddevices 1 Million TL

35 Manufactureofmedicaldevices,precisionandopticalinstruments 1 Million TL

36 Motor land vehicles and supply industryInvestment amount for motor vehicles is

50 Million TL and for motor vehicles supply industry is 4 Million TL

39 Manufacture of furniture (excludingthosemadeonlyofmetalandplastic) 4 Million TL

41 Hotels 3 stars and above

42 Student dormitories 100 students

43 Coldstorageservices 1.000 square meters

44 Licensed warehousing 2 Million TL

45 Education services (including pre-school education services,excludingeducationofadultsandothereducationalactivities) 1 Million TL

46 Hospitalinvestment,nursinghome Hospital:1MillionTLNursinghome:100people

47 Smart multifunctional technical textile 1 Million TL

48 Waste recycling or disposal facilities 1 Million TL

50 Greenhouse business 50 Million TL

FootnotesstatedinAnnex2/aregardingtheDecreeshouldbetakenintoaccount.

| 15

Investments with Incentive Certificate

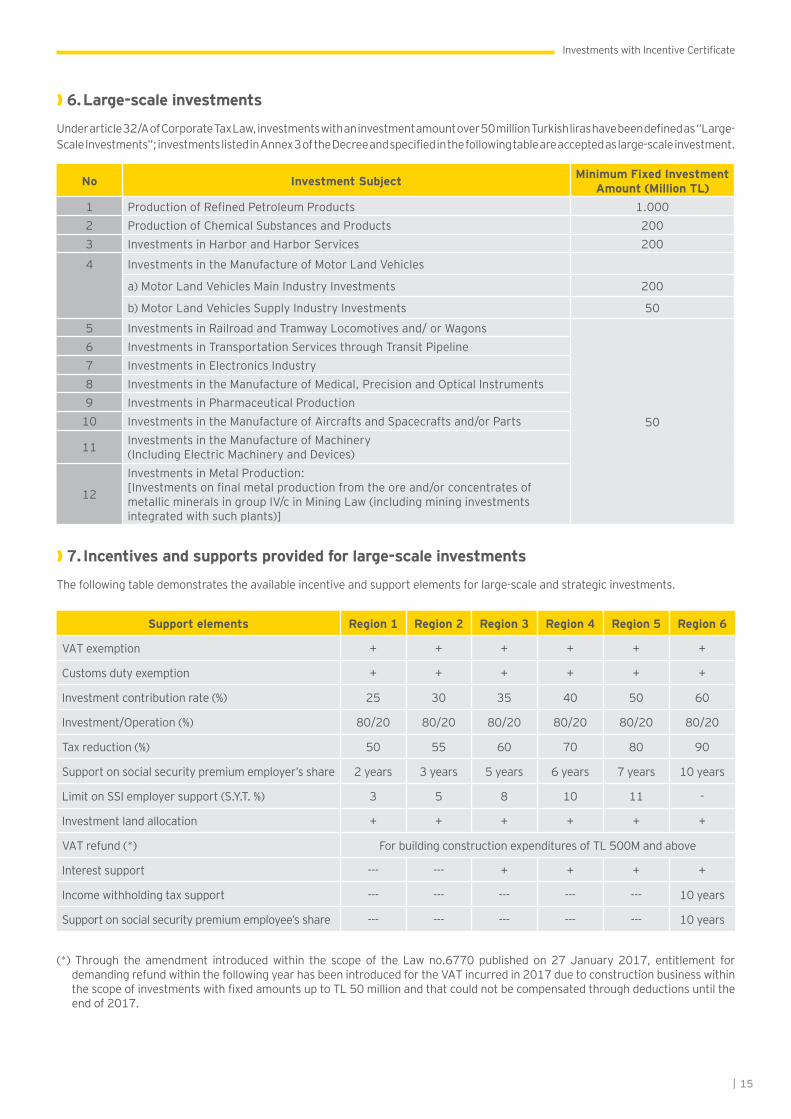

❱ 6. Large-scale investments

Underarticle32/AofCorporateTaxLaw,investmentswithaninvestmentamountover50millionTurkishlirashavebeendefinedas“Large-ScaleInvestments”;investmentslistedinAnnex3oftheDecreeandspecifiedinthefollowingtableareacceptedaslarge-scaleinvestment.

No Investment Subject Minimum Fixed Investment Amount (Million TL)

1 Production of Refined Petroleum Products 1.0002 ProductionofChemicalSubstancesandProducts 2003 Investments in Harbor and Harbor Services 200

4 InvestmentsintheManufactureofMotorLandVehicles

a)MotorLandVehiclesMainIndustryInvestments 200

b)MotorLandVehiclesSupplyIndustryInvestments 50

5 Investments in Railroad and Tramway Locomotives and/ or Wagons

50

6 Investments in Transportation Services through Transit Pipeline7 Investments in Electronics Industry 8 InvestmentsintheManufactureofMedical,PrecisionandOpticalInstruments9 Investments in Pharmaceutical Production

10 InvestmentsintheManufactureofAircraftsandSpacecraftsand/orParts

11 Investments in the Manufacture of Machinery (IncludingElectricMachineryandDevices)

12

InvestmentsinMetalProduction:[Investments on final metal production from the ore and/or concentrates of metallicmineralsingroupIV/cinMiningLaw(includingmininginvestmentsintegratedwithsuchplants)]

❱ 7. Incentives and supports provided for large-scale investments

The following table demonstrates the available incentive and support elements for large-scale and strategic investments.

Support elements Region 1 Region 2 Region 3 Region 4 Region 5 Region 6

VATexemption + + + + + +

Customsdutyexemption + + + + + +

Investmentcontributionrate(%) 25 30 35 40 50 60

Investment/Operation(%) 80/20 80/20 80/20 80/20 80/20 80/20

Taxreduction(%) 50 55 60 70 80 90

Support on social security premium employer’s share 2 years 3 years 5 years 6 years 7 years 10 years

LimitonSSIemployersupport(S.Y.T.%) 3 5 8 10 11 -

Investment land allocation + + + + + +

VATrefund(*) For building construction expenditures of TL 500M and above

Interest support --- --- + + + +

Income withholding tax support --- --- --- --- --- 10 years

Support on social security premium employee’s share --- --- --- --- --- 10 years

(*) Through the amendment introducedwithin the scope of the Lawno.6770published on27January2017, entitlement fordemandingrefundwithinthefollowingyearhasbeenintroducedfortheVATincurredin2017duetoconstructionbusinesswithinthe scope of investments with fixed amounts up to TL 50 million and that could not be compensated through deductions until the end of 2017.

16 |

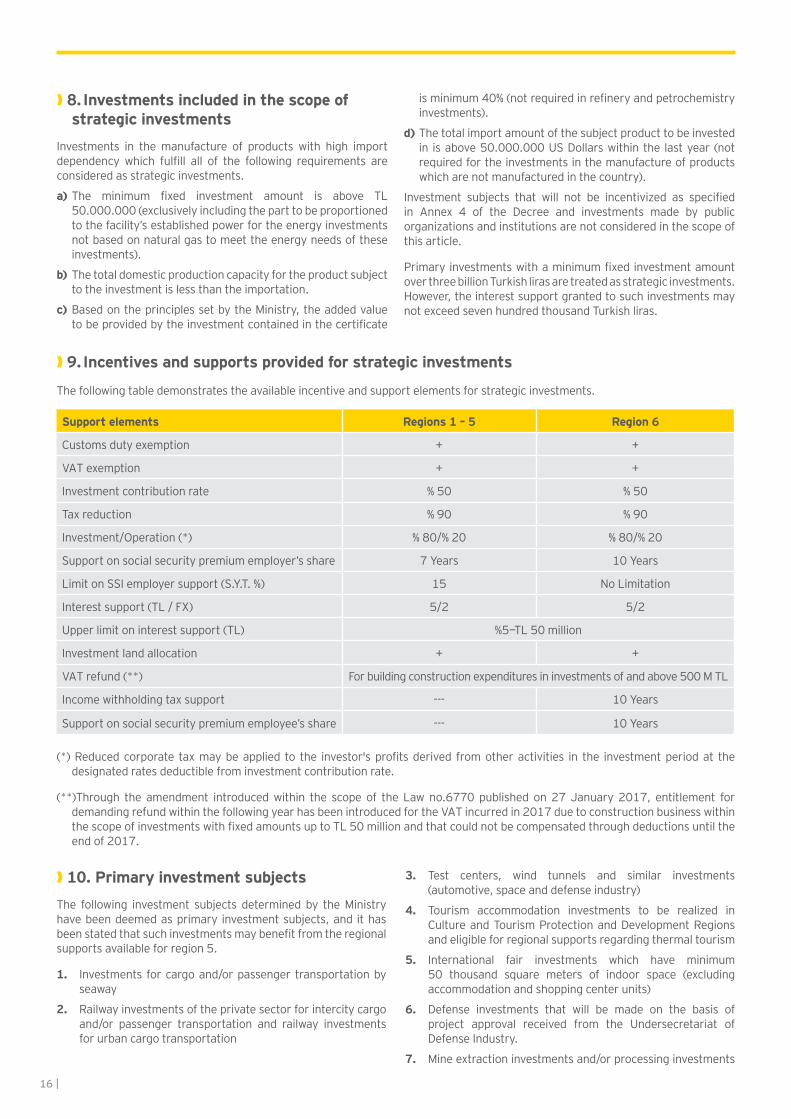

❱ 8. Investments included in the scope of strategic investments

Investments in the manufacture of products with high import dependency which fulfill all of the following requirements are considered as strategic investments.

a) The minimum fixed investment amount is above TL 50.000.000(exclusivelyincludingtheparttobeproportionedto the facility’s established power for the energy investments not based on natural gas to meet the energy needs of these investments).

b) The total domestic production capacity for the product subject to the investment is less than the importation.

c) BasedontheprinciplessetbytheMinistry,theaddedvalueto be provided by the investment contained in the certificate

isminimum40%(notrequiredinrefineryandpetrochemistryinvestments).

d) The total import amount of the subject product to be invested in isabove50.000.000USDollarswithinthelastyear(notrequired for the investments in the manufacture of products whicharenotmanufacturedinthecountry).

Investment subjects that will not be incentivized as specified in Annex 4 of the Decree and investments made by publicorganizations and institutions are not considered in the scope of this article.

Primary investments with a minimum fixed investment amount overthreebillionTurkishlirasaretreatedasstrategicinvestments.However,theinterestsupportgrantedtosuchinvestmentsmaynotexceedsevenhundredthousandTurkishliras.

❱ 9. Incentives and supports provided for strategic investments

The following table demonstrates the available incentive and support elements for strategic investments.

Support elements Regions 1 – 5 Region 6

Customsdutyexemption + +

VATexemption + +

Investment contribution rate % 50 % 50

Tax reduction % 90 % 90

Investment/Operation(*) % 80/% 20 % 80/% 20

Support on social security premium employer’s share 7 Years 10 Years

LimitonSSIemployersupport(S.Y.T.%) 15 No Limitation

Interestsupport(TL/FX) 5/2 5/2

Upperlimitoninterestsupport(TL) %5—TL 50 million

Investment land allocation + +

VATrefund(**) For building construction expenditures in investments of and above 500 M TL

Income withholding tax support --- 10 Years

Support on social security premium employee’s share --- 10 Years

(*)Reducedcorporate taxmaybeapplied to the investor'sprofitsderived fromotheractivities in the investmentperiodat thedesignated rates deductible from investment contribution rate.

(**)Through the amendment introducedwithin the scopeof theLawno.6770publishedon27January2017, entitlement fordemandingrefundwithinthefollowingyearhasbeenintroducedfortheVATincurredin2017duetoconstructionbusinesswithinthe scope of investments with fixed amounts up to TL 50 million and that could not be compensated through deductions until the end of 2017.

❱ 10. Primary investment subjectsThe following investment subjects determined by the Ministry havebeendeemedasprimary investmentsubjects,andithasbeen stated that such investments may benefit from the regional supports available for region 5.

1. Investments for cargo and/or passenger transportation by seaway

2. Railway investments of the private sector for intercity cargo and/or passenger transportation and railway investments for urban cargo transportation

3. Test centers, wind tunnels and similar investments(automotive,spaceanddefenseindustry)

4. Tourism accommodation investments to be realized in CultureandTourismProtectionandDevelopmentRegionsand eligible for regional supports regarding thermal tourism

5. International fair investments which have minimum 50 thousand square meters of indoor space (excludingaccommodationandshoppingcenterunits)

6. Defense investments that will be made on the basis of project approval received from the Undersecretariat of Defense Industry.

7. Mine extraction investments and/or processing investments

| 17

Investments with Incentive Certificate

(excluding group I minerals as described in the MiningLaw No. 3213 dated 4/6/1985 and crushed stones and extractionand/orprocessinginvestmentsinIstanbul)

8. Nursery and day care centers and pre-school, primary,secondary and high school education investments of the private sector

9. Investments regarding the manufacturing of products or parts that are developed as a result of R&D projects supported by the Ministry of Science, Industry andTechnology, by the Scientific and Technological ResearchCouncil of Turkey (TUBITAK) and by Small and MediumEnterprisesDevelopmentOrganization(KOSGEB)

10. Motor investments with a minimum amount of TL 75 million and investments with a minimum amount of TL 300 million which will be realized in the land motor vehicles main industry, as well as investments for motor engine parts,transmission components/parts and automotive electronics with a minimum amount of TL 20 million

11. Electricity production investments where the mines under the group 4-b of the 2nd article of the Mining Law no. 3213 are used as input in accordance with a valid mining operation license and permission issued by the Ministry of Energy and Natural Resources

12. Except for the "Investments Not Subject to Incentive" in Annex-4,onthebasisoftheprojectapprovalgrantedbytheMinistryofEnergyandNaturalResources, investmentsonenergy efficiency which will be made in existing production industry plants having an annual energy consumption of at least500TEP(tonsofequivalentpetroleum),whichsaveatleast 20% energy depending on the current status and have an investment turnover period of maximum 5 years

13. Based on waste heat, investments on energy productionthroughrecoveringwasteheatinaplant(exceptforenergyproductionplantsbasedonnaturalgas)

14. Liquefiednaturalgas(LNG) investmentsandundergroundnatural gas storage investments with a minimum amount of TL 50 million

15. Investments on carbon fiber production or production of compositematerialmadeofcarbonfiber,providedthatitisconducted together with carbon fiber production

16. Investments on the manufacture of products classified in high-technology industry according to the technological intensity definition of the Organization for Economic CooperationandDevelopment(OECD)(US97Code:2423,30,32,33and353) (Chemicalandherbalproductsusedin pharmacy and medicine, office, accounting and dataprocessing machines, radio, television, communicationequipment and devices, medical devices, precision andopticaldevicesandcounters,airandspacecrafts)

17. Mineral exploration investments to be made in licensed fields by investors holding a valid Exploration License or CertificateissuedundertheMiningLaw

18. Investments for the manufacture of turbine and generator for renewable energy investments and manufacture of blades used in wind power generation

19. Integrated investments for aluminium flat products manufacturing through direct chill slab casting and hot rolling methods.

20. Licensed warehousing investments

21. Nuclear energy investments

Iftheseinvestmentsaremadeinregion6,theycanbenefitfromthe supports available to the region where they are located.

Forthosewithafixedinvestmentamountof1billionTurkishlirasandabovefromprimaryinvestments,taxreductionsupportshallbe applied by adding 10 points to the investment contribution rate effective in Region 5.

❱ 11. Incentives Provided Under Attraction Centers Programme The provinces existingwithin the scope of Attraction CentersProgramme and additional incentive advantages concerning the investments to be performed in those provinces have been identified through the Decision on Procedures and Principles for the Implementation of Attraction Centers Programme no.2016/9596 published in the Official Gazette dated 11 January 2017.

In that direction, supports identified concerning the relatedinvestment types for the 6th region will be provided to the regional, large scaled and strategical investments to beperformed in organized industrial sites of 4th and 5th region provinceswithinthescopeofAttractionCentersProgrammeandorganized industrial sites in Kilis.

Regional, large scaled and strategical investments to beperformed within organized industrial sites in Adıyaman,Bayburt, Elazığ, Erzurum, Erzincan, Gümüşhane,Malatya andTunceli and the organized industrial sites in Kilis would also be benefitting of the supports identified for the 6th region under samerates,amounts,periodsandterms,withinthescopetheimplementation.

Ontheotherhand,theDecisiononProceduresandPrinciplesfortheImplementationofAttractionCentersProgrammeindicatesthat investors would be benefitting of the supports provided below within the context of facility relocation supports;

• Cashsupportforrelocation,

• Incentivesupports,

• Supports for the allocation of investment location within the scope of investment and manufacturing aid package andbusinessloanswithloweredinterest,

• Forthenew investments,advisorysupportand interest-freeinvestment loan support within the context of investment and manufacturingaidpackage.

Pursuant to the “Production Facility Relocation Support Package” within the scope of Attraction Centers Programme,investments considered as appropriate for being supported by theDevelopmentBankwouldbebenefittingofthosesupportswithin the context of the Decision on the conditions provided below. Pertaining to that;

1. In case additional investment hasn’t been made on the facility relocated in the provinces within the scope of Programme or despite investment was made if the minimum fixed investment amount and the terms for minimum capacity were not met;

a) Facilities relocated within the 4th and 5th region provinces pursuant to the Programme will be benefitting of the employer’s national insurance contribution support due to the period and amounts applicable for the region of relocation.

18 |

b) Facilities relocated within 6th region provinces will be benefitting of the employer’s national insurance contribution support, insurance premium support andincome tax witholding support as long as the period applicablefortheaforementionedregion,

2. If the relocation within the provinces under the Programme was performed and the additional investment’s minimum fixedinvestmentamountandtermsofcapacityweremet,therelocated facility will be benefitting of the supports indicated inthepreviousarticle(a)whiletheadditionalinvestmentwillbe benefitting of customs duty exemption, VAT exemptionand reduced tax in addition to those supports.

On the other hand, the call centers and data centers to beestablished in the Illumination Centers Program have theopportunity to benefit from the regional incentives of the region they have established without regard to any minimum investment requirement.

❱ 12. Cases where investments can benefit from the supports available to the lower regionLarge-scale investments or investments with incentive certificate in the scope of regional incentives may benefit from the supports at rates and in terms available to the lower region in terms of tax reduction and the support on SSI employer’s share. If the investmentismadeinanOrganizedIndustrialZone(OIZ)ortheinvestment is realized by an investor who has at least five real person or legal entity partners in the same sector and provides integration to the field of the common activity.

If the investment is in region6, theemployer’ssharesupportshall be applied by adding two years to the effective period of the support and the tax discount support shall be applied by adding five points to the investment contribution rate effective in the Region.

Under the regulation introduced by the Council of MinistersDecree no. 2016/9139 promulgated in the Official Gazette dated5October2016,investmentsinmanufacturingindustrymade in Industrial Zones are also entitled to benefit from the incentivesavailabletothelowerregion.Accordingly,large-scaleinvestments or investments for which incentive certificates are issued in the scope of regional incentive practices may benefit from such incentives at the rates and times available to the lower region in terms of tax reduction and insurance premium employer’s share if the investment is made in the Industrial Zone.

Council ofMinister Decree no. 2016/9139 also states that ifthe investments on the manufacture of products included in the medium-hightechnologyindustryclassaccordingtotheOECDtechnology intensity scale definedunderAppendix-6 attachedtothesameDecreearemade inregions1,2and3excludingIstanbul,theyshallbenefitfromtheregionalincentivesappliedinregion4,whereastheyshallbenefitfromtheincentivesavailabletotheirownregioniftheyaremadeinregions4,5or6.Theminimum fixed investment amount relating to such investments is1millionTLinregions1and2,and500thousandTLinotherregions.

Within the scope of the amendments introduced through the CouncilofMinistersDecisionno.2017/9917published in theOfficialGazettedated22February2017,thesupportsidentified

concerning the related investment types for the 6th region will be provided to the regional, large scaled and strategicalinvestments to be performed in organized industrial sites of 4th and5thregionprovinceswithinthescopeofAttractionCentersProgrammeandorganizedindustrialsitesinKilis.Inthatcontext,

Regional, large scaled and strategical investments to beperformed within organized industrial sites in Adıyaman,Bayburt, Elazığ, Erzurum, Erzincan, Gümüşhane,Malatya andTunceli and the organized industrial sites in Kilis would also be benefitting of the supports identified for the 6th region under samerates,amounts,periodsandterms,withinthescopetheimplementation being subjected to.

❱ 13. Minimum amount limitation defined for investmentsFortheavailabilityofsupportsunderthegeneralincentivesystem,the minimum fixed investment amount must be 1.000.000 TL in investments in regions 1 and 2 and 500.000 TL in investments inregions3,4,5and6.However,large-scaleinvestmentsandregional investments must fulfil the requirement of minimum fixed investment amount and/or minimum capacity requirement specifiedinthelistsintheannexesoftheDecree(Annex2andAnnex3).

Requirement of minimum fixed investment amount and investment completion visa shall not be applicable for incentive certificates issued in the name of public institutions and corporations.

❱ 14. Limitations regarding intangible fixed assetsTherateofintangiblefixedassetssuchasbrand,license,know-how etc. accepted as investment expenditure in the scope of incentive certificate may not exceed 50% of the total fixed investment amount registered in the incentive certificate.

❱ 15. Incentives related to R&D and environment investments Regardless of region, research and development (R&D) andenvironmental investments can benefit from VAT exemption,customs duty exemption and interest support. Such investments shall also be eligible for income withholding tax and social security premium support if they are realized in region 6.

Furthermore, investments on the manufacture of productsdeveloped as a result of R&D projects supported by the Ministry of Science,IndustryandTechnologycanbenefitfromtheincentivesof region 5 as primary investments. If such investments are madeinregion6,theycanbenefitfromthesupportsavailableto this region.

| 19

Investments with Incentive Certificate

❱ 1. The authority for application for the incentive certificateApplicationsforincentivecertificatemustbefiledtotheMinistryofEconomy.Ontheotherhand,fortheinvestmentssubjecttoregionalincentiveswhosefixedinvestmentamountdoesnotexceed10millionTL,applicationscanbefiledtothelocalunitsoftheplace of investment.

❱ 2. Applications that can be filed to local authoritiesFirms can choose to apply to the local authorities located in the place of investment forthe following investments subject to general incentive practices with a maximum fixed investmentamountof10MillionTurkishLiras.

US 97 CODEof the Industry Investment subjects

15 Food and beverage production

17

Productionoftextileproducts(Excludingwoolthread,onlymodernization investments in preparation and spinning of textile fiber;andexcludingcarpet,tufting,unwovenandunknittedclothandsags,onlymodernizationinvestmentsintextileindustry)

18 Production of clothing

19 Alutationandprocessingofleather

20 Productionofwoodproducts(excludingfurniture);productionofmatsandsimilarknittedproducts

21 Production of paper and paper products

23 Production of refined petroleum products and nuclear fuel (excludingmininginvestments)

24 Production of chemical substances and products

25 Production of plastic and rubber products

26 Production of non-metallic other mineral products

27 Mainmetalindustry(excluding2710ironandsteelmainindustry)

28 Metal goods industry

29 Production of non-classified machines and equipment

30 Productionofoffice,accountinganddataprocessingmachinery

31 Production of non-classified electric machines and equipment

32 Productionofradio,television,communicationequipmentanddevices

33 Productionofmedicaldevices,precisionandopticaldevicesandcounters

34 Productionofmotorlandvehicle,trailerandsemi-trailer

35 Productionofothertransportationvehicles(excludingshipandyachtconstructioninvestments)

36 Production of furniture; other non-classified production

Investmentsinproductpackagingservices

Service and infrastructure investments municipalities and special provincial administrations

❱ 3. Documents required for the application for incentive certificate a) Letter of application signed by those authorized to represent and bind the investor

C. Obtaining incentive certificate for investments

20 |

b) Notarized circular of signature of those authorized to represent and bind the investor; statement of signature for public corporations and private companies and real persons.

c) Letter of commitment and investment information form,whichisincludedintheattachmentoftheCommuniquéno.2012/1 on Decree no. 3305 and which will be signed and sealed on each page by those authorized to represent and bind the investor; lists of machinery and equipment.

d) In theapplications tobemadeto theMinistryofEconomy,the receipt substantiating that TL 400 was deposited in theaccountof theMinistry’sCirculatingCapitalEnterprise;if the application is made to local authorities, the receiptsubstantiating that TL 100 of the abovementioned amount was deposited in the account of the relevant local authority and the receipt substantiating that the remaining amount was depositedintheaccountoftheMinistry’sCirculatingCapitalEnterprise. TL 10.000 must be paid in the applications to be made to the Ministry for the importation of used complete facilities in the scope of investment incentive certificate.

e) Original of the Turkish Trade Registry Gazette or TurkishTradesmen and Craftsmen Registry Gazette, whichdemonstrate the company’s current status in terms of shareholding structure, capital amountandbusiness,or itscopy certified by notary public or registry authority.

f) Excluding the applications filed by public organizations and corporations, the letter to be received from the relevantdepartments of Social Security Institution substantiating that the company does not have any premium or administrative finepayabletoSocialSecurityInstitutioninTurkeyaccordingto the Social Insurances and General Health Insurance Law no. 5510 or these fines have been postponed and/or divided into installations or have been structured and this structuring has not been interrupted or the printout with barcode to be derived from the Institution’s electronic information communication medium.

g) Investments for the manufacture of turbine and generator for renewable energy investments and manufacture of bladesusedinwindpowergeneration,theDecisionreceivedfrom the Ministry of Environment and Urbanization and/or Letter on the Decision for investment subjects that require an “Environmental Impact Assessment Positive Decision”or“NoRequirementforEnvironmentalImpactAssessment”under the provisions of the Regulation on Environmental Impact Assessment promulgated in the Official Gazettedated 3/10/2013 and numbered 28784. Before applying for incentivecertificate,theinformationanddocumentsspecifiedintheannexofthecommuniquéwhichneedtobeobtainedfrom other public corporations and institutions under the relevant legislation depending on the characteristics of the investment.

h) Resolution of Ministry of Environment and Forestry and/or Letter regarding the Resolution on investment subjects for which“EnvironmentalImpactAssessmentApprovalDecisionor Decision stating that Environmental Impact Assessmentis not required” included only in the attached lists of EnvironmentalImpactAssessmentRegulationwithreferencetotheEnvironmentCodeno2872isrequired.

i) Feasibility report containing the information, documents,accounts and schedules substantiating that all criteria under

article 10 have been fulfilled in addition to the industrial,financial and technical analyses regarding the investment subject with respect to strategic investments.

j) Other information and documents that might be requested by the General Directorate depending on the industry and size of the investment or incentive practices.

❱ 4. Expenditures not included in the scope of incentive certificate 1. Investment expenditures incurred before the date of

application shall not be considered in the scope of incentive certificate.

2. The following shall not be considered under incentive certificate;