Investment Strategy - SGKB · Photo: Roland Gerth. October 2017 Investment Strategy 1 Dear...

16

Investment Strategy Economy and Financial Markets October 2017

Transcript of Investment Strategy - SGKB · Photo: Roland Gerth. October 2017 Investment Strategy 1 Dear...

Investment StrategyEconomy and Financial MarketsOctober 2017

Contents

1 Editorial Champions of the euro in the ascendancy

2 Economy Euro: evolution preferable to revolution

4 Interest rates and yields ECB: End of bond purchase programme in sight

5 Equity markets Stormy times for reinsurers

6 Currencies Euro enjoying a confidence high

7 Commodities Harvey and Yellen: two key influences

8 Investment Strategy Equity markets enjoying a tailwind

9 Market overview Economic data and cycles Interest rates and currencies Equity and commodity markets Financial markets and forecasts

Impressum

IssuerSt.Galler Kantonalbank AG St.Leonhardstrasse 25 9001 St.GallenTel. +41 71 227 97 00 [email protected]

Analysts

Caroline Hilb (Economy, Investment Strategy)Patrick Häfeli, CFA (Interest rates and yields)Tobias Kistler, CFA (Equity markets)Daniel Wachter (Currencies, Commodities) Editorial deadline

September 20, 2017

Release

Monthly

Title Picture

Lake Powell Lone Rock, Utah, USAPhoto: Roland Gerth

October 2017 Investment Strategy 1

Dear investors,

The fact that the euro teetered on the edge of the abyss back in 2012 is gradually fading from people’s memories. Growth in the eurozone is accelerating, and is no longer restricted to the econo-mic engine that is Germany. The

Élysée Palace is occupied not by arch-opponent of the euro Marine Le Pen, but by Europe enthu-siast Emmanuel Macron. The single currency is once again in vogue in the foreign exchange markets, and has been strengthening against the US dollar in particular. This has allowed the champions of the euro at the highest levels of the EU to dream once again. Indeed, EU Com-mission President Juncker is keen to introduce the euro in all countries of the EU.

But the euro’s design flaws have not been elimi-nated. The structural imbalances that exist bet-ween the different countries of the eurozone are excessive, and have actually increased in recent years. Even when the euro was first conceived, the powers-that-be were aware that this pheno-menon posed a problem to the single currency area. For this reason, the Maastricht criteria we-re agreed in 1992, their purpose being to ensu-re the economic convergence of eurozone coun-tries.

25 years on, and the Maastricht criteria have lapsed into obscurity. Who can still recall that a debt ratio of less than 60% of GDP is a prerequi-site for being accepted as a euro country? How many finance ministers are truly mindful of the need to limit their budget deficit to 3% of GDP? Is anyone aware nowadays that the yield on the long-term bonds of a eurozone country may not exceed the average of the three most stable eu-rozone countries by more than 2%? These regu-lations were designed to ensure the economic

stability of eurozone countries, as well as the gradual harmonization of the various econo-mies’ productivity over time.

The eurozone must take advantage of the im-proved economic outlook and the current tran-quillity of the financial markets, and refocus its attentions on the Stability and Growth Pact. It must increase the pressure on the Maastricht vi-olators to press on with the necessary reforms. In return, the wider reform package could en-compass an increase in solidarity between euro-zone countries, as well as the shared financing of certain investment in the context of the Euro-pean financial budget. The next recession and the next financial crisis will surely come. By then, the entity that is the euro must have been strengthened to the point where its existence can no longer be called into question by the fi-nancial markets. Whether or not the ECB has the ability and the desire to rescue the euro for a se-cond time is an open question.

So the focus of the next few years should not be on bringing even more unsteady countries un-der the euro umbrella. Instead, the focus should be on making the existing eurozone more resili-ent in the face of a crisis. Among other things, this must also include creating the legal and po-litical prerequisites so that countries not suited to the euro can leave the single currency area – either voluntarily, or at the instigation of the EU itself.

Dr. Thomas Stucki

Chief Investment Officer

EditorialChampions of the euro in the ascendancy

140%

120%

100%

80%

60%

40%00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16

France Italy Germany Eurozone

Government debt in relation to GDP

Investment Strategy October 20172

EconomyEuro: evolution preferable to revolution

Some people love it, others only see its weak-nesses and reject it. Some would like to expand it, others insist on adherence to economic crite-ria. Nothing divides opinions quite like the eu-ro. And despite all the criticism, it continues to develop.

In a speech given in mid-September, EU Com-mission President Jean-Claude Juncker called for an expansion of the eurozone. This view was im-mediately contradicted by various European fi-nance ministers. Germany’s Finance Minister Wolfgang Schäuble pointed out the require-ments that must be met in order for a country to join the euro.

Transparent criteria – with flawsWhen Wolfgang Schäuble cited economic re-quirements, he was actually referring to the eurozone’s convergence criteria, better known as the Maastricht criteria. These criteria were laid down in February 1992 with a view to ensuring greater economic stability in the euro area through clear fiscal and monetary parame-ters, as well as driving forward the harmoniza-tion of eurozone productivity. On the positive side, these criteria ensure that the conditions of accession are both comprehensible and trans-parent. On the negative side, no one has ques-tioned how the criteria were arrived at, nor has there been much determination to ensure sus-tained adherence to them. The best-known rule stipulates that outstanding government debt must not exceed 60% of gross domestic pro-duct. The sister rule under this criterion relates to the annual budget deficit, which may not ex-ceed 3% of GDP. These criteria are also enshri-ned in the Stability and Growth Pact, which countries must comply with after joining the single currency area. Rather less well-known are three other criteria. Two of these have pro-ved relatively simple to meet, and remain so in the current environment. The first relates to ex-change rate stability. Specifically, an accession candidate must undertake to keep its currency within a narrow exchange rate bandwidth against the euro for at least two years prior to joining. The second concerns price stability: the inflation rate of an accession candidate may not be more than 1.5 percentage points above the

inflation rate of the three member states exhi-biting the greatest price stability. And the other criterion relates to the level of long-term inte-rest rates. Here too, the three most «price-sta-ble» member states of the eurozone are taken as the benchmark. Specifically, the rate of inte-rest of long-term government bonds must not be more than 2 percentage points higher than the average of the most price-stable member states. The strong rise in interest rates experi-enced by certain eurozone countries in the af-termath of the financial crisis, reflecting the higher risk premiums imposed by the bond markets, forced the European Central Bank (ECB) to intervene on a massive scale.

Eurozone wants to survive, so must enforce its own rulesThe idea behind the convergence criteria is posi-tive in principle. Full compliance with these crite-ria would result in harmonization quasi-automa-tically, supported by a large domestic market and a «one-size-fits-all» monetary policy. In rea-lity, however, the Maastricht criteria have proved to be insufficiently enforceable. Above all, the

Maastricht clause with design flaws

Source: Eurostat

Yields on 10-year government bonds7%

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17

6%

5%

4%

3%

2%

1%

0%

-1%

France Italy Germany

October 2017 Investment Strategy 3

Source: Bloomberg

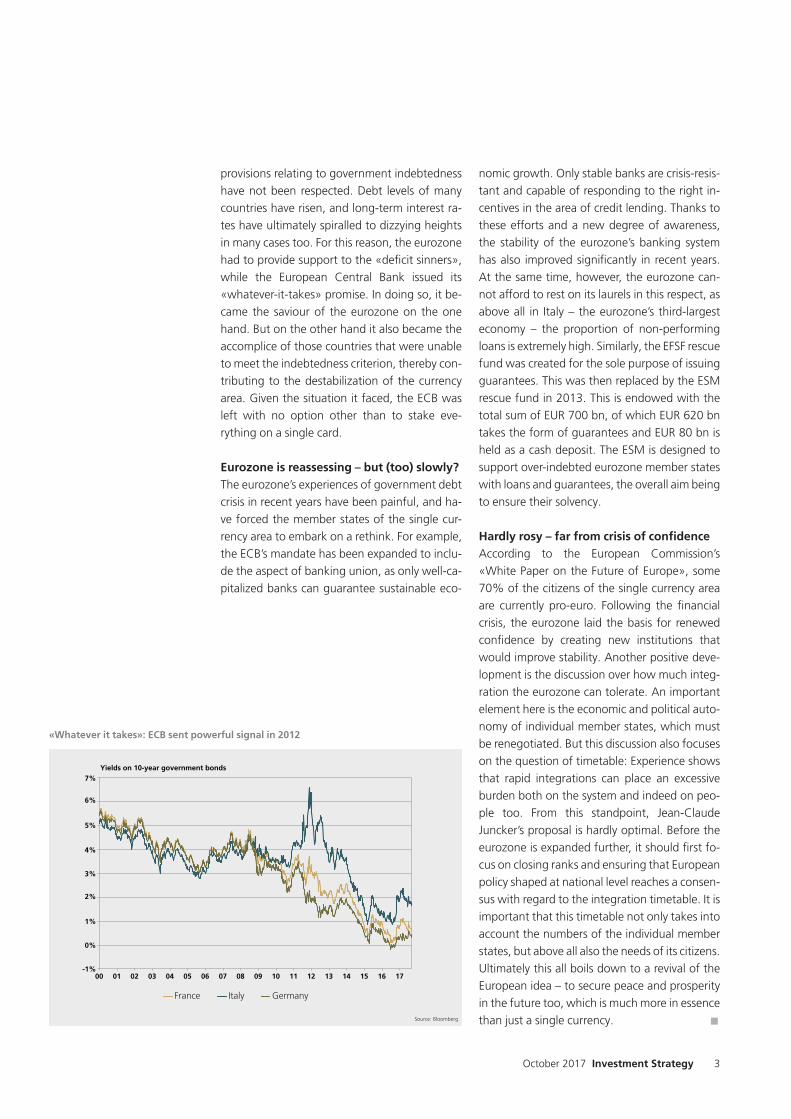

provisions relating to government indebtedness have not been respected. Debt levels of many countries have risen, and long-term interest ra-tes have ultimately spiralled to dizzying heights in many cases too. For this reason, the eurozone had to provide support to the «deficit sinners», while the European Central Bank issued its «whatever-it-takes» promise. In doing so, it be-came the saviour of the eurozone on the one hand. But on the other hand it also became the accomplice of those countries that were unable to meet the indebtedness criterion, thereby con-tributing to the destabilization of the currency area. Given the situation it faced, the ECB was left with no option other than to stake eve-rything on a single card.

Eurozone is reassessing – but (too) slowly?The eurozone’s experiences of government debt crisis in recent years have been painful, and ha-ve forced the member states of the single cur-rency area to embark on a rethink. For example, the ECB’s mandate has been expanded to inclu-de the aspect of banking union, as only well-ca-pitalized banks can guarantee sustainable eco-

nomic growth. Only stable banks are crisis-resis-tant and capable of responding to the right in-centives in the area of credit lending. Thanks to these efforts and a new degree of awareness, the stability of the eurozone’s banking system has also improved significantly in recent years. At the same time, however, the eurozone can-not afford to rest on its laurels in this respect, as above all in Italy – the eurozone’s third-largest economy – the proportion of non-performing loans is extremely high. Similarly, the EFSF rescue fund was created for the sole purpose of issuing guarantees. This was then replaced by the ESM rescue fund in 2013. This is endowed with the total sum of EUR 700 bn, of which EUR 620 bn takes the form of guarantees and EUR 80 bn is held as a cash deposit. The ESM is designed to support over-indebted eurozone member states with loans and guarantees, the overall aim being to ensure their solvency.

Hardly rosy – far from crisis of confidenceAccording to the European Commission’s «White Paper on the Future of Europe», some 70% of the citizens of the single currency area are currently pro-euro. Following the financial crisis, the eurozone laid the basis for renewed confidence by creating new institutions that would improve stability. Another positive deve-lopment is the discussion over how much integ-ration the eurozone can tolerate. An important element here is the economic and political auto-nomy of individual member states, which must be renegotiated. But this discussion also focuses on the question of timetable: Experience shows that rapid integrations can place an excessive burden both on the system and indeed on peo-ple too. From this standpoint, Jean-Claude Juncker’s proposal is hardly optimal. Before the eurozone is expanded further, it should first fo-cus on closing ranks and ensuring that European policy shaped at national level reaches a consen-sus with regard to the integration timetable. It is important that this timetable not only takes into account the numbers of the individual member states, but above all also the needs of its citizens. Ultimately this all boils down to a revival of the European idea – to secure peace and prosperity in the future too, which is much more in essence than just a single currency. n

«Whatever it takes»: ECB sent powerful signal in 2012

Billions

5‘000

4‘000

3‘000

2‘000

1‘000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 20170

Fed’s balance sheet (in USD) ECB's balance sheet (in EUR)

Investment Strategy October 20174

Interest rates and yieldsECB: End of bond purchase programme in sight

60 billion euros – the sum the European Central Bank has spent on bond purchases every month since March 2015 in order to strengthen the im-pact of its low-interest policy. The aim of this po-licy is/was to steer the European economy back onto a healthy growth trajectory following the financial and government debt crisis. This ob-jective now appears to be on the verge of being met.

Over the last two-and-a-half years, the Euro-pean Central bank has purchased bonds with a total value of more than EUR 2,200 billion, the-reby more than doubling the size of its balance sheet. Among other things, the increased de-mand for European government bonds trigge-red by this bond purchase programme has ensu-red that European bond yields have remained at record lows. And this despite the fact that the economic outlook for the eurozone has impro-ved significantly over the last two-and-a-half ye-ars. The favourable refinancing conditions enjo-yed by European companies are likely to have been a major contributory factor to this impro-vement.

The eurozone’s show of strengthThere has been a clear acceleration in economic growth in the eurozone since 2014. Indeed, at 2.3% in a year-on-year comparison, the Euro-pean economy has recently exhibited even stron-ger growth than its US counterpart. Admittedly, inflation is still only 1.5%, which is below the Eu-ropean Central Bank’s 2% target. Nonetheless, the trend of recent months is headed in the right direction. What’s more, unemployment has con-tinued to fall and is now back to 2009 levels – reason enough to consider bringing the bond purchase programme to an end in the near fu-ture.

Fed points the wayIt is likely that members of the European Central Bank’s Governing Council have been ruminating on this issue for a while now. The Council has su-rely already debated various ideas for curtailing its extraordinary measures. On the other side of the Atlantic, the US central bank has been provi-ding an object lesson in this regard: the Fed sca-led down its bond purchases back in 2014 and

has since raised its key interest rate by a quarter of a percentage point no less than four times.

Minimal repercussions thanks to circum-spect approachThe ECB’s existing bond purchase programme will be pursued unchanged until the end of this year at least. However, we are expecting ECB President Mario Draghi to provide information on the central bank’s policy going forward as early as October. We expect the European Cen-tral Bank to taper its monthly bond purchases to-wards zero at a sedate tempo in the first half of 2018. In much the same way as the Fed, the ECB will for now reinvest the interest and maturing capital from the bonds it has bought in recent years, thus maintaining a stable balance sheet. Thanks to this very circumspect approach, Euro-pean capital market yields will rise only slightly over the next few months. Moreover, key inte-rest rates in the Eurozone will remain at a very low level for the time being, as an initial rate hi-ke on the part of the European Central Bank is inconceivable before the bond purchase pro-gramme is brought to an end. This will not hap-pen before the second half of 2018. n

Source: Bloomberg

ECB more than doubles its balance sheet with bond purchases

200%

150%

100%

50%

0% 2012 2013 2014 2015 2016 2017

Price in CHF

MunichRe SwissRe SPI Index

Equity marketsStormy times for reinsurers

vered by reserves. However, the profitability of insurers in the core non-life business has been under pressure for a considerable while now. Claims relating to major natural catastrophes have actually been below average in recent ye-ars, resulting in a noticeable increase in equity capital throughout the industry. As a result of the lower burden of catastrophe claims, premi-ums have fallen. In some segments this business has been considered to be insufficiently profita-ble, prompting reinsurers to steer clear of new business. As a result, underwriting has taken a blow. Moreover, the risk of natural catastrophes is increasingly being passed on directly to institu-tional investors, which has meant competition for insurers and hence greater price pressure. Some 15% of natural catastrophe cover now takes the form of so-called «cat bonds» (catast-rophe bonds). In addition to these challenges, insurers are also struggling with meagre returns on capital investments owing to persistently low interest rates.

What next?In the medium term, the global shortfall in insu-rance cover – particularly in Asia – points to further growth for reinsurers going forward. For example, SwissRe estimates the insurance po-tential just for natural catastrophes that are not yet covered at USD 180 bn. In the short term, the major claim events of recent weeks will probab-ly result in only minor improvements in premi-ums and cover. It is likely that the competition to reinsurers from institutional investors will per-sist, which in turn spells oversupply. A rise in in-terest rates would be helpful here as it would create investment alternatives and improve the investment returns of insurers whose portfolios are skewed toward fixed income.

Attractive dividend plays Thanks to their robust capital bases, SwissRe and MunichRe have among the highest solvency ra-tios in their industry, amounting to more than double the minimum requirement. This means that the danger of dividends being slashed is low – even in years in which the claim burden is high. We therefore consider MunichRe and SwissRe to be attractive dividend plays for long-term-orien-ted investors. n

It is not just since the US was hit by devastating storms that the share prices of the world’s two largest reinsurers – MunichRe and SwissRe – ha-ve lagged behind the development of the equity market as a whole. Are there structural reasons behind their weak performance, or is this just a temporary nadir?

The hurricane season, which is characterized by extreme weather conditions in the North Atlan-tic and Caribbean from the start of June to the end of November, was predicted to be particu-larly severe this year. In particular, Hurricanes Harvey and Irma testified to the accuracy of this forecast, proving calamitous for the people who found themselves in their path. For the insu-rance industry, events of this kind result in signi-ficant claims. According to the latest estimates, Irma alone will trigger payments of between USD 20 bn and USD 40 bn. Over the last five ye-ars, catastrophe claims of this kind have cost the insurance industry between USD 37 bn and USD 80 bn per annum.

Structural pressure on premiumsFor reinsurers, claims that go beyond the risk budget can lead to a loss in excess of the sum co-

Source: Bloomberg

Short-lived weakness for reinsurers?

October 2017 Investment Strategy 5

130

2012 2013 2014 2015 2016 2017

120

110

100

90

Trade-weighted exchange rates (indexed, 2012=100)

US dollar Euro

Investment Strategy October 20176

CurrenciesEuro enjoying a confidence high

The euro has emerged from a politically eventful first half of the year in stronger shape. Europe’s electoral carousel came to an end with the elec-tions to Germany’s federal parliament on Sep-tember 24. Where the euro is concerned, the fo-cus will now switch to the direction of moneta-ry policy in particular.

At the start of the year, some observers were muttering that the euro could soon be worth less than a US dollar. Precisely the opposite has occurred. On the one hand, the dollar’s perfor-mance this year has been the weakest of the in-dustrial nations. On the other hand, the euro has been gaining in strength ever since the second quarter of 2017. At the end of August, the EUR/USD rate was back at 1.20 for the first time since January 2015, and was some 15% higher than its level at the start of the year. The euro has al-so strengthened against the Swiss franc, appre-ciating by 7% since April.

Political hurdles are diminishingIt is quite some time since the eurozone last ex-perienced the kind of economic strength it en-joys right now. Moreover, the elections are now over in the two largest eurozone countries, France and Germany. Angela Merkel is set to embark on a fourth term as Chancellor, even if the next government is unlikely to include its existing coalition partner, the SPD. Development has also been seen on the reform-side. However, reform is unlikely to pursue the path proposed by EU Commission President Jean-Claude Jun-ker, who has called for an expansion of the eu-rozone («euro for all»). As things stand, 19 of the EU’s 28 member states use the euro. The fu-ture of the eurozone is also likely to be increasin-gly influenced by anticipated German-French agreements. The two countries are at least put-ting on a show of unity to the outside world with regard to the eurozone’s need for reform.

ECB as new signal provider By contrast, where the immediate future is con-cerned, it is the monetary policy of the ECB that will set the direction for the euro. As the experi-ence of the dollar and the Fed have shown, when speculation grows in the run-up to a mo-netary policy reversal, this pushes up the value of

the corresponding currency. As the US central bank’s rate-hiking cycle is already at an advan-ced stage, the focus of the currency markets has shifted in recent weeks to the European Central Bank as the latest signal provider. The improved economic situation will prompt the ECB to re-consider its expansionary monetary policy, which will benefit the euro. After the September meeting of the Governing Council, ECB Presi-dent Draghi did not yet unveil any plans for ta-pering the existing bond purchase programme. However, we are expecting him to do so at the next meeting on 26 October.

Euro boosted by benign outlookThe combination of bright economic prospects and expectations of a less expansionary policy stance on the part of the ECB has not only boos-ted the euro’s spot rate, it has also triggered a sentiment trend reversal in the futures markets. The one-sided positioning in favour of the euro currently reflects heightened expectations. The euro’s movements over the next few months will be strongly shaped by this phenomenon. That said, it would be wrong to expect the ECB to set too brisk a tempo when it comes to the norma-lization of monetary policy – particularly as an overly rapid appreciation of the euro harbours risks in terms of inflationary and economic deve-lopment. n

Source: Bloomberg

Euro with tail wind

120

100

80

60

40

202012 2013 2014 2015 2016 2017

Price movements (indexed, 2012=100)

Oil (WTI, USD per barrel) Gold (USD per oz)

October 2017 Investment Strategy 7

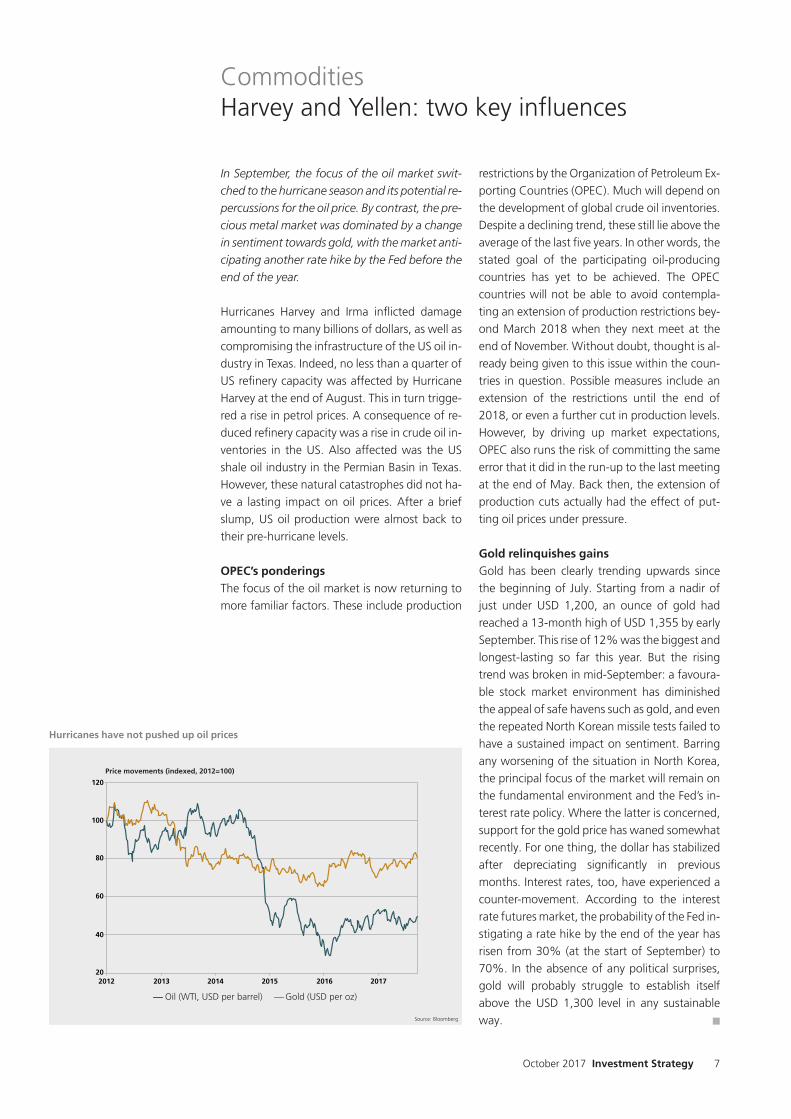

In September, the focus of the oil market swit-ched to the hurricane season and its potential re-percussions for the oil price. By contrast, the pre-cious metal market was dominated by a change in sentiment towards gold, with the market anti-cipating another rate hike by the Fed before the end of the year.

Hurricanes Harvey and Irma inflicted damage amounting to many billions of dollars, as well as compromising the infrastructure of the US oil in-dustry in Texas. Indeed, no less than a quarter of US refinery capacity was affected by Hurricane Harvey at the end of August. This in turn trigge-red a rise in petrol prices. A consequence of re-duced refinery capacity was a rise in crude oil in-ventories in the US. Also affected was the US shale oil industry in the Permian Basin in Texas. However, these natural catastrophes did not ha-ve a lasting impact on oil prices. After a brief slump, US oil production were almost back to their pre-hurricane levels.

OPEC’s ponderingsThe focus of the oil market is now returning to more familiar factors. These include production

restrictions by the Organization of Petroleum Ex-porting Countries (OPEC). Much will depend on the development of global crude oil inventories. Despite a declining trend, these still lie above the average of the last five years. In other words, the stated goal of the participating oil-producing countries has yet to be achieved. The OPEC countries will not be able to avoid contempla-ting an extension of production restrictions bey-ond March 2018 when they next meet at the end of November. Without doubt, thought is al-ready being given to this issue within the coun-tries in question. Possible measures include an extension of the restrictions until the end of 2018, or even a further cut in production levels. However, by driving up market expectations, OPEC also runs the risk of committing the same error that it did in the run-up to the last meeting at the end of May. Back then, the extension of production cuts actually had the effect of put-ting oil prices under pressure.

Gold relinquishes gains Gold has been clearly trending upwards since the beginning of July. Starting from a nadir of just under USD 1,200, an ounce of gold had reached a 13-month high of USD 1,355 by early September. This rise of 12% was the biggest and longest-lasting so far this year. But the rising trend was broken in mid-September: a favoura-ble stock market environment has diminished the appeal of safe havens such as gold, and even the repeated North Korean missile tests failed to have a sustained impact on sentiment. Barring any worsening of the situation in North Korea, the principal focus of the market will remain on the fundamental environment and the Fed’s in-terest rate policy. Where the latter is concerned, support for the gold price has waned somewhat recently. For one thing, the dollar has stabilized after depreciating significantly in previous months. Interest rates, too, have experienced a counter-movement. According to the interest rate futures market, the probability of the Fed in-stigating a rate hike by the end of the year has risen from 30% (at the start of September) to 70%. In the absence of any political surprises, gold will probably struggle to establish itself above the USD 1,300 level in any sustainable way. n

CommoditiesHarvey and Yellen: two key influences

Source: Bloomberg

Hurricanes have not pushed up oil prices

Investment Strategy October 20178

The mood in the financial markets is positive. On the one hand, the economic data look convin-cing. On the other, while stumbling blocks are evident, market participants are stepping non-chalantly around them. And last but not least, a number of market indicators point to a healthy background situation.

Where the economic indicators are concerned, the leading indicators are conspicuous for their persistently positive signals. These are pointing almost across the board to sound economic de-velopment over the next three to six months. The hard economic data are also looking good. In the eurozone in particular, these figures have regularly been exceeding expectations. Things look slightly different in the US, where the oc-casional figure has disappointed. All in all, how-ever, the economic indicators suggest the US economy is headed in the right direction and will continue to enjoy a solid recovery. The ar-ray of positive indicators also extends to com-panies’ earnings expectations. These are positi-ve not just for the US, but also for the eurozo-ne and Switzerland. The equity markets are therefore receiving positive stimuli both from the corporate side – in the form of positive cor-porate earnings prospects – and from the busi-ness cycle.

Market sends out positive signalsThe signals from the financial markets themsel-ves are also predominantly positive. They indica-te that equities will continue to reward investors as an asset class. The signals from the credit mar-ket are pointing also in this direction. Credit spreads are a measure of the risk situation in the credit markets. The wider the credit spreads, the greater the mistrust in the credit markets. And these spreads are currently at a historic low, i.e. extremely narrow. Is this justified? Interest rates remain extremely low globally, and would still be historically low even if they were to rise. Moreo-ver, as the economic outlook is promising, bond default rates are unlikely to increase over the next few months. In other words, the lights are set at green as far as the financial markets are concerned. The fact that cyclical currencies such as the euro are on the firm side strengthens this impression all the more.

Investment StrategyEquity markets enjoying a tailwind

Investment strategy

A look at the spoilersEven if the fundamentals look good for equities, we still see a number of potential warning lights. The current geopolitical situation remains a good case in point. The sabre-rattling between the US and North Korea is getting out of hand not just verbally, but also in the real world. Both parties are testing their boundaries. This inclu-des missile tests, but also open threats on the part of US President Trump in front of the UN General Assembly. Up until now, however, the financial markets have barely reacted, or have simply switched their attention back to day-to-day business. The next steps in US monetary po-licy are also under scrutiny. A clearly positive as-pect here is the circumspect and transparent ap-proach taken by the Fed. It is aware of the pow-er of verbal intervention, and has been playing this card in an exemplary manner.

Conclusion: We have decided to increase the equity weighting in view of the positive economic and earnings prospects. We are setting the un-derweight positioning in the US back to neutral and increasing the allocation to Switzerland. n

liquidity

bonds

convertible bonds

equities

Switzerland

Eurozone

North America

Asia Pazific (ex. Japan)

Emerging Markets

alternative investments

commodities

others

– – – Neutral + ++

Source: own graph

October 2017 Investment Strategy 9

Market overviewEconomic data and cycles Data as of 20 September 2017; Source: Bloomberg, Graphics: own illustration

Economic trend in industrialized countries

Switzerland USA Eurozone Germany

Switzerland 0.4 % 0.4 % 0.5 % 0.5% 3.2 % 3.2% 55.6 61.2

USA 2.0 % 2.2 % 1.9 % 1.9 % 4.3 % 4.4 % 54.9 58.8

Eurozone 2.0% 2.3% 1.4 % 1.5% 9.2 % 9.1 % 57.0 57.4

Germany 3.2% 0.8 % 1.5% 1.8% 5.7 % 5.7 % 59.5 59.3

GD

P qo

q, a

nnua

lized

,

prev

ious

qua

rter

GD

P qo

q, a

nnua

lized

,

curr

ent

Ass

essm

ent

Infl

atio

n ra

te y

oy,

prev

ious

qua

rter

Infl

atio

n ra

te y

oy,

curr

ent

Ass

essm

ent

Une

mpl

oym

ent

rate

,

prev

ious

qua

rter

Une

mpl

oym

ent

rate

,

curr

ent

Ass

essm

ent

PMI,

prev

ious

qua

rter

PMI,

curr

ent

Ass

essm

ent

Macro scenarion Switzerland: PMI survey figures signal a positive trend. We are expecting stimuli

for the export economy from the strong euro in particular.n USA: The US economy is performing well, but the recovery is coming to an end.n Eurozone: Economic development in the eurozone is robust and will continue to

improve.n Germany: The outlook is still very good, but the actual figures are less positive.

We are optimistic, but will be keeping a close watch on developments.

Economic trend in emerging markets

China India Brazil Russia

GD

P yo

y,

prev

ious

qua

rter

GD

P yo

y, c

urre

ntA

sses

smen

tIn

flat

ion

rate

yoy

, pr

evio

us q

uart

erIn

flat

ion

rate

yoy

, cu

rren

t

Ass

essm

ent

Une

mpl

oym

ent

rate

,

prev

ious

qua

rter

Une

mpl

oym

ent

rate

,

curr

ent

Ass

essm

ent

PMI,

prev

ious

mon

thPM

I, cu

rren

t

Ass

essm

ent

China 6.9 % 6.9 % 1.5% 1.8 % 4.0 % 4.0% 51.1 51.6

India 5.6% 5.6%

2.2% 3.4 % – – 47.9 51.2

Brazil –0.4 % 0.3% 3.6% 2.5% 7.5 % 8.2 % 50.0 50.9

Russia 0.5% 2.5 % 4.1% 3.3 % 5.2 % 4.9% 53.4 54.2

Macro scenarion China: China’s growth is in stability mode in anticipation of this autumn’s

People’s Congress. Decision-makers are keen to avoid creating unnecessary uncertainty in the run-up to the event.

n India: India’s economic development continues to look promising. The govern-ment led by President Modi is unifying the country and providing it with fresh perspectives.

n Brazil: Brazil has finally emerged from its prolonged crisis. But despite this country’s catch-up potential, euphoria would be misplaced. The corruption alle-gations against President Temer are proving an obstacle to necessary reforms.

n Russia: Russia has bottomed out. The economic situation is showing signs of im-provement.

positive assessment neutral assessment negative assessment

positive assessment neutral assessment negative assessment

Recovery

Recession

Boom

Downturn

Recovery

Recession

Boom

Downturn

Investment Strategy October 201710

Interest rates and currenciesData as of 20 September 2017; Source: Bloomberg, Graphics: own illustration

Switzerland: Attention is still focusing on the strong franc despite its recent fall in value. Inflation remains low.Outlook: The SNB is sticking to negative interest rates and will actively intervene in the currency market.

Eurozone: Inflation has edged up slightly, but remains low. Positive expectations on the economy.Outlook: Key interest rates set to stay low for now. The ex-pected announcement of the end of the bond-buying pro-gramme will probably come before the end of the year.

USA: The domestic economy points to rate rises, but inflatio-nary pressure is only picking up slowly.Outlook: The Fed will continue to raise interest rates – one more hike by the end of the year. It will begin the process of downsizing its balance sheet in October 2017.

Switzerland: Negative interest rates, low inflation and de-mand for bonds are keeping interest rates low.Outlook: Interest rates to rise slightly in medium term in step with eurozone.

Eurozone: Economic recovery is becoming tangible. Expect a «tapering» announcement before 2017 is out. The first ECB rate hike will make it on to the agenda in the second half of 2018.Outlook: The debate over the ECB’s first rate hike will push up interest rates next year.

USA: Positive economic prospects. Wage pressure firming slowly. Other interest rate hikes will follow.Outlook: Rising medium-term yields due to rate-hiking cycle and reduction in the size of the Fed’s balance sheet.

EUR/USD: There has been a broad-based improvement in the economic outlook for the eurozone, and the euro is also gai-ning support from the debate over the ECB’s monetary policy.

USD/CHF: The currency market has grown accustomed to the Fed’s tighter monetary policy. The US administration’s unclear policies are clipping the dollar’s wings.

EUR/CHF: Market expectations of an adjustment to the ECB’s monetary policy, coupled with the brighter economic outlook are giving the euro a boost. The SNB will welcome a weaker Swiss franc, but will not be making any changes to its mone-tary policy.

Key interest rates for selected central banks

Capital markets: yields on individual 10-year government bonds

Currencies: rates for selected currency pairs

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

2012 2013 2014 2015 2016 2017 -1.0%

SNB ECB FED

-1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

2012 2013 2014 2015 2016 2017

Switzerland Germany USA

0.8

0.9

1.0

1.1

1.2

1.3

1.4

2012 2013 2014 2015 2016 2017

Euro in CHF US dollar in CHF Euro in US dollar

October 2017 Investment Strategy 11

Equity and commodity marketsData as of 20 September 2017; Source: Bloomberg, Graphics: own illustration

In general:n The stock markets remain robust.n The outlook for earnings is positive.n In Europe at least, uncertainties arising from political events

are receding into the background again.

Outlook:n The solid underlying trend looks set to be punctuated by

high share price volatility and negative phases.

In general:n Valuation ratios have increased during the course of the year.n Valuations are above the average for the last 10 years.

Outlook:n All markets show positive earnings growth.n Europe and the Emerging Markets currently have the stron-

gest forecast earnings growth.

Oil price: OPEC will also be reducing its production quota inthe second half of the year. This news is not sufficient to pushup the oil price.Outlook: High global inventories and a rebound in US oilproduction will prevent any substantial price rise for now.

Gold price: Tensions with North Korea and lower interest rates have brought gold back into fashion. The price per ounce reached a record high in September.Outlook: The demand for secure investments is supporting the gold price. On the other hand, the prospects of higher US interest rates combined with a moderate rise in inflation is limiting gold’s upside potential.

Equity markets for selected regions (indexed)

Valuations: estimated P/E ratio for selected regions and markets

Commodity markets: Price trend for oil and gold

75

100

125

150

175

200

225

250

2012 2013 2014 2015 2016 2017

SPI DAX S&P 500 Emerging Market Index

7

9

11

13

15

17

19

21

2012 2013 2014 2015 2016 2017

SPI P/Est DAX P/Est S&P 500 P/Est Emerging Market Index P/Est

20

40

60

80

100

120

1'000

1'200

1'400

1'600

1'800

2'000

2012 2013 2014 2015 2016 2017

Gold (USD per oz) Oil (WTI, USD per barrel)

Investment Strategy October 201712

Financial markets and forecastsClosing prices as of 20 September 2017; Source: Bloomberg; Forecast: SGKB

Key interest rates 12 Months ago 3 Months ago Current Forecast 3 Months

Forecast 12 Months

SNB –0.75 % –0.75 % –0.75 % –0.75 % –0.75 %

ECB 0.00 % 0.00 % 0.00 % 0.00 % 0.00 %

FED 0.25 % – 0.50 % 1.00% – 1.25 % 1.00 % – 1.25 % 1.25% – 1.50% 1.75 % – 2.00 %

Capital market yields 12 Months ago 3 Months ago Current Forecast band 3 Months

Forecast band12 Months

10-year Conf. –0.41% –0.15 % –0.05% –0.05 % – 0.15 % 0.30 % – 0.50 %

10-year German Bund 0.00% 0.27% 0.44% 0.55 % – 0.75 % 1.00 % – 1.20 %

10-year Treasury 1.65% 2.16 % 2.27% 2.40 % – 2.70 % 2.70 % – 3.00 %

Currencies 12 Months ago 3 Months ago Current Forecast band 3 Months

Forecast band12 Months

EUR/CHF 1.0898 1.0861 1.1536 1.10 – 1.15 1.07 – 1.12

USD/CHF 0.9739 0.9725 0.9698 0.92 – 0.97 0.93 – 0.98

EUR/USD 1.1189 1.1168 1.1892 1.16 – 1.21 1.12 – 1.17

Commodities 12 Months ago 3 Months ago Current Forecast band 3 Months

Forecast band12 Months

Oil (WTI, USD per barrel) 45 43 50 45 – 50 45 – 55

Gold (USD per oz) 1335 1246 1300 1200 – 1300 1200 – 1300

Equity markets YTD Valuation(est. P/E) Current Index Trend

last 3 MonthsTrend

last 12 Months

S&P500 (local currency) 13.7% 19.2 2508

EuroStoxx50 (local currency) 10.2% 15.1 3526

SMI (local currency) 14.3% 18.1 9096

MSCI Emerging Markets in USD 31.6% 13.9 1112

Disclaimer: The information contained on this Recommendation List and specifically the descriptions of individual securities constitute neither an offer to purchase the securities nor an invitation to engage in any other transactions. All of the information contained in this document has been carefully selected and obtained from sources that the Invest-ment Center of the St.Galler Cantonal Bank AG fundamentally believes to be reliable. Opinions or other representations conveyed in this document are subject to change without notice. No guarantee is assumed as to the accuracy or completeness of the information. St.Galler Cantonal Bank AG is regulated and supervised by Swiss Financial Market Super vision Authority FINMA, Einsteinstrasse 2, 3003 Berne, Switzerland, www.finma.ch.