Investment Promotion and Enterprise Development Bulletin ...s3.amazonaws.com/zanran_storage/ · B....

124

Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific No. 1 ECONOMIC AND SOCIAL COMMISSION FOR ASIA AND THE PACIFIC UNITED NATIONS

Transcript of Investment Promotion and Enterprise Development Bulletin ...s3.amazonaws.com/zanran_storage/ · B....

Investment Promotion andEnterprise Development Bulletin

for Asia and the Pacific

No. 1

ECONOMIC AND SOCIAL COMMISSION FOR ASIA AND THE PACIFIC

UNITED NATIONS

UNITED NATIONSNew York, 2003

Investment Promotion andEnterprise Development Bulletin

for Asia and the Pacific

No. 1

ESCAP works towards reducing povertyand managing globalization

ECONOMIC AND SOCIAL COMMISSION FOR ASIA AND THE PACIFIC

The Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific is publishedannually by the Economic and Social Commission for Asia and the Pacific.

Any uncredited article or information in this Bulletin may be copied, summarized or translated into anylanguage provided that acknowledgement of its use is made and a copy of the publication in which it appears issent to the Editor. However, permission must be received from the original author before use may be made of anyarticle, picture, drawing, cartoon or other account for which credit is specifically given.

The designations employed and the presentation of the material in this publication do not imply theexpression of any opinion whatsoever on the part of the Secretariat of the United Nations concerning the legalstatus of any country, territory, city or area, or of its authorities, or concerning the delimitation of its frontiers orboundaries.

On 1 July 1997, Hong Kong became Hong Kong, China. Mention of “Hong Kong” in the text refers to adate prior to 1 July 1997.

The opinions, figures and estimates set forth in this publication are the responsibility of the author, andshould not necessarily be considered as reflecting the views or carrying the endorsement of the United Nations.Mention of firm names and commercial products does not imply the endorsement of the United Nations.

Short articles and viewpoints on industrial development issues from readers are welcome. The editorreserves the right to edit and publish manuscripts in accordance with the editorial requirements of this publication.

All correspondence should be addressed to:

ChiefTrade and Investment DivisionEconomic and Social Commission for Asia and the Pacific (ESCAP)United Nations Building, Rajdamnern Nok AvenueBangkok 10200, Thailand

ST/ESCAP/2259

UNITED NATIONS PUBLICATION

Sales No. E.03.II.F.36

Copyright © United Nations 2003

ISBN: 92-1-120176-4 ISSN: 0252-4481

ii

iii

CONTENTS

Page

Abbreviations ....................................................................................................................................... vi

Explanatory notes .............................................................................................................................. viii

I. STRENGTHENING THE COMPETITIVENESS OF SMALL ANDMEDIUM ENTERPRISES IN THE GLOBALIZATION PROCESS:PROSPECTS AND CHALLENGES .................................................................................... 1

– Bhavani P. Dhungana

A. Globalization: challenges and prospects for small and medium enterprisesin Asia and the Pacific ............................................................................................................ 1

B. Industrial dynamism, economic prosperity and economic crisis: liberalization,globalization and private sector-led industrial growth ........................................................... 4

C. Role of SMEs in the development process: some country experiences ................................. 11

D. Promoting the competitiveness of SMEs within the ongoing processof globalization ........................................................................................................................ 16

E. Conclusions and recommendations ......................................................................................... 22

II. PROMOTING RESOURCE-BASED EXPORT-ORIENTED SMEsIN ASIA AND THE PACIFIC ............................................................................................... 33

– Tarun Das

A. Introduction ............................................................................................................................. 33

B. Resource-based and agro-based industries: sector’s main characteristics .............................. 33

C. Rationale for development and contribution of agro-based and resource-basedindustries to poverty alleviation .............................................................................................. 39

D. Economic policies and strategies for development of agro-based andresource-based industries ........................................................................................................ 49

E. Role of the World Trade Organization for the development of agro-based andresource-based industries ........................................................................................................ 60

F. Conclusions and recommendations ......................................................................................... 63

iv

CONTENTS (continued)

Page

III. ISSUES AND STRATEGIES FOR THE TRANSFER AND ADOPTION OFPROSPECTIVE TECHNOLOGIES BY SMEs AND SMALL GROWERSFOR PROCESSING OF HORTICULTURAL PRODUCE INDEVELOPING ASIAN COUNTRIES ................................................................................. 77

– K. Lakshminarayanan

A. Introduction ............................................................................................................................. 77

B. Technology gaps ...................................................................................................................... 82

C. Problems and prospects in technology transfer ...................................................................... 85

D. Technology management issues .............................................................................................. 87

E. Conclusions ............................................................................................................................. 90

IV. REPORT OF THE EXPERT GROUP MEETING ON PROMOTINGRESOURCE-BASED EXPORT-ORIENTED SMEs FOR POVERTYALLEVIATION IN ASIA AND THE PACIFIC ............................................................... 93

– ESCAP secretariat

A. Regional overview of the status of the resource-based export-oriented SMEsand their impacts on poverty alleviation in Asia and the Pacific .......................................... 93

B. Evolving model of programmes for enhancing the competitiveness of SMEs,and issues and strategies for the transfer and adoption of prospective technologiesfor processing horticultural produce ....................................................................................... 95

C. Country experiences ................................................................................................................ 95

D. Recommendations ................................................................................................................... 97

V. FOREIGN DIRECT INVESTMENT: DETERMINANTS, TRENDSIN FLOWS AND PROMOTION POLICIES .................................................................... 99

– Joong-Wan Cho

A. Globalization and foreign direct investment ........................................................................... 99

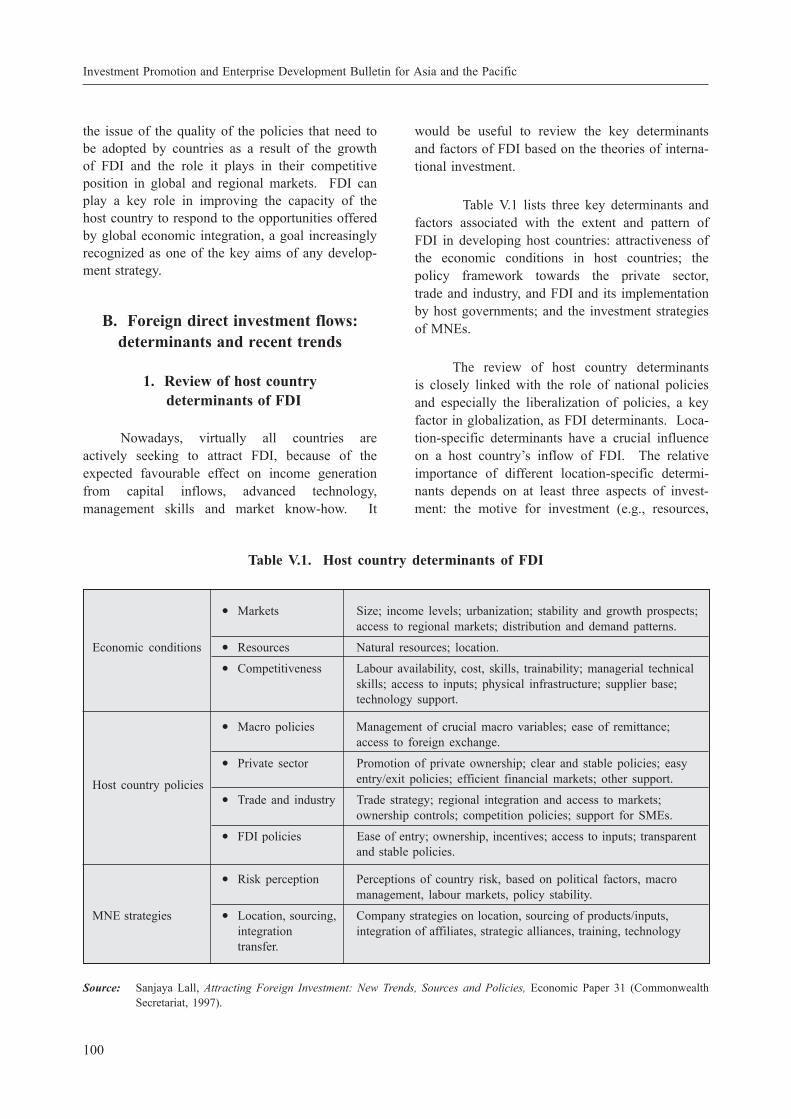

B. Foreign direct investment flows: determinants and recent trends .......................................... 100

C. Host country FDI promotion policy trends ............................................................................. 104

D. FDI by small and medium enterprises .................................................................................... 108

E. Conclusions and implications for regional action and cooperation ....................................... 110

v

LIST OF TABLES

Page

I.1. Real GDP of selected Asian and Pacific economies ...................................................................... 5

I.2. Selected economies of the ESCAP region: rates of economic growth and inflation,2000-2004 ........................................................................................................................................ 6

II.1. Growth rate and share of MVA in selected Asian countries, 1980-2000 ...................................... 34

II.2. Employment by economic activity in selected Asian economies ................................................... 35

II.3. Share of females in total employment by branches in selected Asian countries ........................... 36

II.4. Value added per employee in selected Asian countries .................................................................. 37

II.5. Average annual growth of manufacturing in selected Asian economies, 1990-1999 .................... 41

II.6. Distribution of employment and value added among the manufacturing sectors .......................... 43

II.7. Tax policies in selected Asian economies in 1990 and 2000 ........................................................ 53

II.8. Science and technology development in selected Asian economies .............................................. 56

V.1. Host country determinants of FDI .................................................................................................. 100

V.2. FDI inflows by region, 1997-2001 .................................................................................................. 102

V.3. FDI inflows to the Asian and Pacific region, 1997-2001 ............................................................... 103

LIST OF BOXES

II.1. WTO and market access ................................................................................................................. 61

II.2. Uruguay Round: principal commitment on agriculture .................................................................. 62

II.3. Agreement on Textiles and Clothing (ATC) ................................................................................... 63

vi

ABBREVIATIONS

ADB Asian Development Bank

AFTA ASEAN Free Trade Area

APCAEM Asian and Pacific Centre for Agricultural Engineering and Machinery

APCTT Asian and Pacific Centre for Transfer of Technology

APEC Asia Pacific Economic Cooperation (currently comprises 21 countries/areas includingAustralia; Brunei Darussalam; Canada; Chile; China; Hong Kong, China; Indonesia;Japan; Malaysia; Mexico; New Zealand; Papua New Guinea; Peru; the Philippines; theRepublic of Korea; the Russian Federation; Singapore; Taiwan Province of China;Thailand; and the United States of America).

ASEAN Association of Southeast Asian Nations (comprises Brunei Darussalam, Indonesia,Malaysia, the Philippines, Singapore, Thailand, Viet Nam, the Lao People’s DemocraticRepublic, Myanmar and Cambodia).

ASEAN-4 Comprises Indonesia, Malaysia, the Philippines and Thailand

ATC Agreement on Textiles and Clothing

BITs bilateral investment treaties

CGPRT Regional Coordination Centre for Research and Development of Coarse Grains, Pulses,Roots and Tuber Crops in the Humid Tropics of Asia and the Pacific

DLC letter of credit

ECDC economic cooperation among developing countries

ESCAP Economic and Social Commission for Asia and the Pacific

ESTs environmentally sound technologies

EU European Union

FAO Food and Agriculture Organization of the United Nations

FDI foreign direct investment

FIAS Foreign Investment Advisory Service

FTZ free trade zone

GATT General Agreement on Tariffs and Trade

ICT information and communication technology

IPR intellectual property rights

ISO International Organization for Standardization

ISO 9000 international standards for quality management systems

ISO 14000 international standards for environmental management systems

vii

ABBREVIATIONS (continued)

IT information technology

LDCs least developed countries

M&As mergers and acquisitions

MFA Multifibre Arrangement

MFIs microfinance institutions

MFN most-favoured nation

MNCs multinational corporations

MNEs multinational enterprises

MVA manufacturing value added

n.e.c. not elsewhere classified

NGOs non-governmental organizations

NIEs newly industrializing economies

NIPAs national investment promotion agencies

NTEs new technology enterprises

NTMs non-tariff measures

OECD Organisation for Economic Cooperation and Development (comprises Australia, Austria,Belgium, Canada, the Czech Republic, Denmark, Finland, France, Germany, Greece,Hungary, Iceland, Ireland, Italy, Japan, Luxembourg, Mexico, the Netherlands, NewZealand, Norway, Poland, Portugal, the Republic of Korea, Spain, Sweden, Switzerland,Turkey, the United Kingdom of Great Britain and Northern Ireland, and the UnitedStates of America).

ODA official development assistance

QRs quantitative restrictions

R&D research and development

S&T science and technology

SAARC South Asian Association for Regional Cooperation (comprises Bangladesh, Bhutan,India, Maldives, Nepal, Pakistan and Sri Lanka)

SBA Small Business Administration

SCMs subsidies and countervailing measures

SIDBI Small Industries Development Bank of India

SMBA Small and Medium Business Administration

SMEs small and medium-sized enterprises

viii

ABBREVIATIONS (continued)

SMIPC Small and Medium Industry Promotion Corporation

SSI small-scale industry

SSTC State Science and Technology Commission

T&C textiles and clothing

TBT technical barriers to trade

TCDC technical cooperation among developing countries

TNCs transnational corporations

TRIMs trade-related investment measures

TRIPs trade-related intellectual property rights

UNCTAD United Nations Conference on Trade and Development

UNIDO United Nations Industrial Development Organization

USSR Union of Soviet Socialist Republics (also known as the Soviet Union for short, consistedof Russia and surrounding countries that today make up Armenia, Azerbaijan, Belarus,Estonia, Georgia, Kazakhstan, Kyrgyzstan, Latvia, Lithuania, the Republic of Moldova,the Russian Federation, Tajikistan, Turkmenistan, Ukraine and Uzbekistan)

VERs voluntary export restraints

WTO World Trade Organization

EXPLANATORY NOTES

M$ = ringgitRs = Indian rupeeUS$ = United States dollars

A. Globalization: challengesand prospects for small and mediumenterprises in Asia and the Pacific

The Asian and Pacific region – a fast-growing, dynamic part of the developing world –has sustained its vibrancy and impressive growth,despite the unexpected setbacks during the latterhalf of the 1990s. The dynamism and vibrancy ofthe economies and the economic crisis of 1997-1998 are both cited as the results of the fast paceof liberalization and the globalization process.Opinions are divided and experts have differentviews on these issues. However, globalization,which is generally defined as the “shrinkage ofeconomic distances (i.e., the costs of doing busi-ness) between nations”, when one analyses thetrends in production and trade or finance andcapital flows among countries in the region as wellas global terms,1 has ushered in new opportunitiesand challenges especially for small and medium-sized enterprises (SMEs). Globalization has alsoresulted in the integration of economies and hasprompted a rapid increase in the movement ofproducts, capital and labour across borders. It isincreasingly realized that globalization offers clearadvantages as it contributes to the maximizationof economic efficiencies, including the efficientutilization and allocation of resources, such asnatural resources, labour and capital on a globalscale, resulting in a sharp increase in global outputand growth.

It is becoming increasingly clear that theglobalization of production and trade has led to arising trade-GDP (gross domestic product) ratioand has also resulted in the fragmentation of theproduction process into its subcomponent parts,which in turn are distributed across countries onthe basis of comparative and competitive advan-tages. Developing countries have also benefitedsignificantly from increased flows of capital andother forms of finance. However, globalizationalso has disadvantages, particularly as nationalGovernments in many countries display a lackof political will and/or competence to adjustaccordingly to the process of globalization. It isalso observed by some people that globalizationis a process mainly pushed by the developed worldto unsustainable levels, and has placed manydeveloping countries in rather unstable situations,disregarding the nature and appropriateness ofdeveloping countries’ national policy frameworksand other limitations. This is the subject of furtheranalysis requiring concerted efforts by nationalGovernments to seek new policy options. Never-theless, the international community has aresponsibility to institute mechanisms to manageglobalization2 well to the advantage of all coun-tries while as mentioned earlier national Govern-ments would have a responsibility to formulate andimplement policies to adjust their economiessmoothly and efficiently to benefit from the

* Chief, Investment and Enterprise Development Section,Trade and Investment Division, Economic and SocialCommission for Asia and the Pacific.

1 Ramkishen S. Rajan, “Economic globalization and Asia:trade, finance and taxation”, ASEAN Economic Bulletin,vol. 18, No. 1 (January 2001), pp. 1-11.

2 In view of the needs and priorities expressed by theGovernments of Asia and the Pacific, the United NationsEconomic and Social Commission for Asia and thePacific adopted a new programme structure with“Managing globalization” as one of the main themes at itsfifty-eighth session, held in May 2002. The Commissionhas also established a Subcommittee on InternationalTrade and Investment to focus on globalization issues.

I. STRENGTHENING THE COMPETITIVENESS OF SMALL ANDMEDIUM ENTERPRISES IN THE GLOBALIZATION PROCESS:

PROSPECTS AND CHALLENGES

Bhavani P. Dhungana*

1

Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific

globalization process, especially if SMEs are tobe promoted and sustained in this new economicenvironment.

As pointed out earlier, it is becoming obvi-ous that globalization is driven by a variety offactors, such as the accelerated growth of interna-tional trade and foreign direct investment (FDI),and rapid development in information technology,further facilitated by the global flow of informationas a result of the rapid spread of Internet use,which have far-reaching implications for SMEs.In particular, the advances in information andcommunication technology have driven down thecosts of international transactions and exchangesand enabled the creation of the global financialsystem. In turn, these interdependent and mutuallyreinforcing global flows of products, technology,information and capital are pushing globalizationfurther, making the whole process evolve at anaccelerated pace. However, with the advent ofglobalization, growth has become somewhat vola-tile, as recently demonstrated in Asian countries,imposing additional costs in terms of reconcilinggrowth and social development on the onehand and sustainability of development on theother.3 This aspect is to be especially noted whenexamining the implications of globalization forSMEs.

Nevertheless, globalization will lead to amore liberalized and market-oriented economicprocess. As past experience has demonstrated,it will expedite growth and spread technologymore rapidly, especially information technology.

A recent study by the World Bank has alsoanalysed the critical effect of globalization oninequality and poverty. The study identified agroup of developing countries that are participatingeffectively in the globalization process and found apositive relationship between globalization andpoverty reduction. For example, China, India andseveral other large countries are part of this groupand well over half of the population of the deve-loping world lives in these globalizing economies.The post-1980 globalizers have seen largeincreases in trade with significant declines intariffs over the past 20 years. Their growth rateshave accelerated from the 1970s to the 1980s andfurther accelerated in the 1990s. The post-1980globalizers are catching up with the rich countries,while the rest of the developing world, whichhas not been part of the globalization process, isfalling farther behind. The study also analyseshow general these patterns are and finds a strongpositive effect of trade on growth after controllingfor changes in other policies and addressingendogeneity with internal instruments. Finally, thestudy examines the effects of trade on the poor.Since there is little systematic evidence of arelationship between changes in trade volumes (orany other globalization measure considered) andchanges in the income share of the poorest, theincrease in growth rates that accompaniesexpanded trade leads to proportionate increasesin the incomes of the poor. The evidence fromindividual cases and from cross-country analysissupports the view that globalization leads to fastergrowth and poverty reduction in poor countries.4As mentioned earlier, the globalization process willalso bring various volatilities in the economy withgreater risks in the areas of capital and financialflows as well as in currency exchange arrange-ments. It is therefore urgent that certain concretemeasures be taken to safeguard SMEs and makethem sustainable. Furthermore, it should be noted

3 Several international organizations have focused theiractivities on assisting countries in dealing with variousissues of globalization processes. See World Bank, WorldDevelopment Report 2001/2002; ESCAP, Economic andSocial Survey of Asia and the Pacific 2002: EconomicProspects: Preparing for Recovery (ST/ESCAP/2144);and Asian Development Bank, Asian DevelopmentOutlook 2002. Also refer Byron G. Auguste, “What’s sonew about globalization?”, New Perspectives Quarterly,1 January 1998; to illustrate the decline in costs of inter-national transactions, he notes that since 1945 averageocean freight charges have fallen by 50 per cent, airtransport costs by 90 per cent and trans-atlantic telephonecharges by 99 per cent. See also International MonetaryFund, World Economic Outlook, May 1997.

4 For further details see, David Dollar and Aart Kraay,“Trade growth and poverty”, World Bank Policy ResearchWorking Paper 2615. See also United Kingdom of GreatBritain and Northern Ireland, “Eliminating world poverty:making globalisation work for the poor”, White Paperon International Development (available at <http://www.globalisation.gov.uk>).

2

that smaller firms have traditionally focused ondomestic markets and many will continue to relyheavily on local assets and markets. At the sametime, SMEs will be increasingly globalized. About25 per cent of manufacturing SMEs are nowinternationally competitive but this share shouldincrease rapidly. At present, SMEs contributebetween 25 and 35 per cent of world manufacturedexports and account for a smaller but growingshare of FDI. They are becoming more involvedin international strategic alliances and jointventures both among themselves and together withthe larger multinationals. More generally, network-ing allows SMEs to combine the advantages ofsmall scale, e.g., flexibility, and the economies ofscale and scope provided by firm groups.5 It isalso essential that some new and innovativemeasures be taken to improve their competitive-ness in the globally integrated and highly competi-tive economy. Furthermore, since SMEs accountfor the majority of the firms in a country and havethe largest share in employment and since the 2billion urban population throughout the world willincrease in the next decade, it is therefore essentialthat urban SMEs be promoted as major providersof employment. SMEs are also important to growout of a stage-dominated economy characterizedby government subsidy and control and, becauseof their independence and sheer numbers, SMEsrepresent a constituency of good policy andgovernance in many developing countries of theAsian and Pacific region.

In a recent United Nations Industrial Deve-lopment Organization (UNIDO) forum on “Fight-ing marginalization through sustainable industrialdevelopment: challenges and opportunities in aglobalizing world”, the experts, while addressingthe role of investment, technology and trade inpromoting industrial and economic development ina globalizing world, emphasized that technologyand liberalization were the prime forces drivingglobalization. Technological innovation ratherthan capital accumulation was seen as the mainsource of long-term sustainable growth and it was

urged that in order to overcome the threat ofmarginalization, developing countries be enabledto mobilize the key ingredients of productivity-based growth, namely, information, knowledge,skills and technology, by drawing on internationaltrade, capital/investment and technology flows. Onthe subject of global norms and standards inthe context of development, it was agreed thatdeveloping countries were to be provided with thecapacity to participate more fully in internationaltrade agreements and environmental conventions.The forum had also highlighted the critical role ofdevelopment agencies in guiding productivity-based growth in the developing world and promot-ing “workable” globalization. These necessitiesare even more forcefully reinforced when one triesto strengthen the role of SMEs in developing coun-tries to enable them to be the forceful agents inpromoting the integration of industrial activities atthe regional and global levels.

Therefore, this paper has tried to analyseand suggest measures as to what strategies canbe adopted to enhance the development of SMEsin the context of the ongoing process of globali-zation. There are many ways to approach thedevelopment of SMEs, but the paper has focusedon the various ways and means to enhance theexport capabilities of SMEs, in promoting coopera-tion and networking of SMEs to play importantroles in regional/global markets, in improvingvarious measures for the provision of businessservices for SME competitiveness and in promot-ing good management and efficient overall govern-ance, including the provision of a legal frameworkto manage globalization for the benefit andefficiency of SMEs. At the end, a set of urgentmeasures to promote the competitiveness of SMEsis presented.

Before the analysis actually focuses on thespecific issues of SMEs and competitiveness, it isrelevant to present some analysis of the recenteconomic and industrial trends and situation ofAsian and Pacific developing countries, followedby a section on the role of SMEs in selectedcountries of the region, so that coherent andconsistent policy issues for SME development andways to improve their competitiveness can beanalysed.

5 Organisation for Economic Cooperation and Develop-ment, OECD Small and Medium Enterprise Outlook(Paris, OECD, 2000).

I. Strengthening the Competitiveness of SMEs in the Globalization Process: Prospects and Challenges

3

Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific

B. Industrial dynamism,economic prosperity and economic

crisis: liberalization, globalization andprivate sector-led industrial growth

1. Recent economic growth

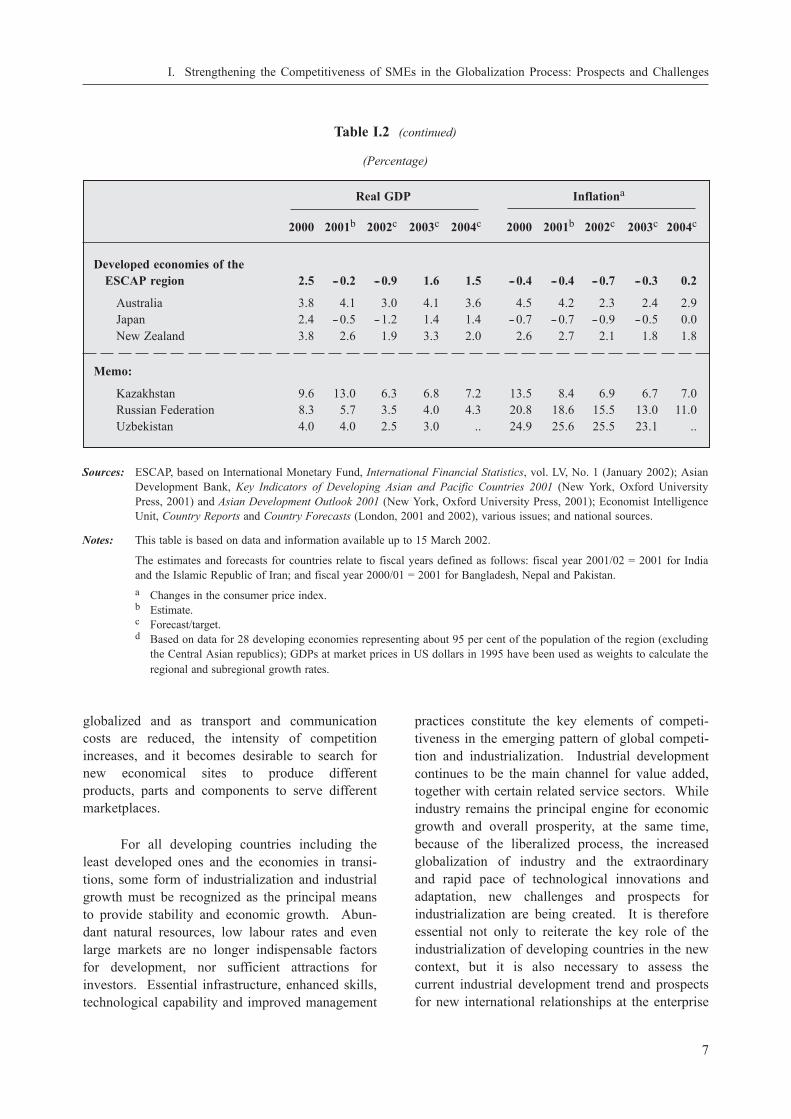

The Asian and Pacific developing regionhas frequently been termed one of the mostdynamic parts of the global economy. However,these economies again registered a decline inGDP growth in 2001 to 3.1 per cent as comparedwith 7.0 per cent in 2000.6 Several economiesregistered a decline in their growth rate (see tablesI.1 and I.2). There was also a slowdown in theglobal GDP growth rate. The slowdown wasparticularly evident in the information and commu-nication technology sector and in economies witha preponderance of ICT-related manufacturingactivities and with high trade-to-GDP ratios, as inEast and South-East Asia, were most affected bythe slowdown. While some economies andsubregions remained relatively immune initially,the dramatic suddenness of the global slowdownand its intensity slowed GDP growth in theseeconomies and subregions as well. The events of11 September 2001 aggravated the slowdownthrough a loss of business and consumer confi-dence.

It should be noted that since March 2002,signs of a global and regional upturn were beingseen. On balance, evidence of a gentle recoveryin both the global and regional economies wasbecoming discernible. The majority of the ESCAPeconomies were expected to exceed their 2001GDP growth rates in 2002 (see table I.2). Abenign inflationary environment and comfortableexternal positions indicated that most economies inthe region had considerable leeway to compensatefor the loss of external demand through domesticstimulus measures.7

Thus, the Asia-Pacific region is quite resil-ient and is able to cope with economic problemsmuch more quickly. In general, it managed totrigger a process of unprecedented economicgrowth led by industry (in particular manufactur-ing) among a selected few developing countriesowing to a combination of appropriate policies anda conducive international economic environmentduring the last three decades despite catching upwith the crisis in 1997. The aggregate GDPgrowth of the Asia-Pacific region (excludingChina) grew by an annual average of 7 per centduring the period 1980-1996 but contracted byover 4 per cent in 1998 after growing 5.6 per centin 1997. Conducive national policies aimed atsuccessful integration of national economies intothe world economy certainly played a fundamentalrole in explaining East Asia’s success stories.Only during the last three years of the 1990s, hadit become obvious that major adjustments at boththe national and international levels were necessaryto manage the globalization process to the benefitof all.

In the coming years, the Asian and Pacificregion in general is expected to continue achievinghigher growth rates, depending on the degree ofdevelopment in the United States and Japaneseeconomies. Thus, a regional economic recoveryin 2003 is essentially predicated on a significantimprovement in the external environment, sup-ported by appropriate domestic policy measures.However, the pace of economic performance ingeneral and industrial growth in particular in somedeveloping economies of the region could remainunsatisfactory. The least developed countries andthe economies in transition could achieve onlymarginal growth. Many such poorer economiescould stagnate and remain poor, unless majoreconomic and industrial transformations arebrought about at the regional and global levels,promoting the integration of those economies. It istherefore essential that the production system atthe regional and global levels be diversified, anddispersed and the production process fragmented,so that not only efficiencies and cost-effectivenessare achieved, but also the disadvantaged group ofcountries could somehow find niches in regionaland global production and create jobs and incomesin their respective economies. It should be notedthat as production becomes more and more

6 Asian Development Bank, Asian Development Outlook2002 (New York, Oxford University Press, 2002), p. 4.

7 “Summary of the economic and social survey of Asia andthe Pacific, 2002” (E/2002/18), 15 April 2002, p. 1.

4

Table I.1. Real GDP of selected Asian and Pacific economies

(Annual percentage change)

10-yearaverage

1982-1991 1992 1993 1994 1995 1996 1997 1998 1999

Asiaa

Bangladesh 4.8 4.3 4.5 4.8 5.0 5.3 5.0 5.2 3.89Bhutan 4.4 5.0 5.1 6.9 6.0 5.7 4.6 6.5 5.26Cambodia 4.8 7.5 7.0 7.7 7.0 1.0 1.0 4.97 4.0China 14.2 13.5 12.6 10.5 9.6 8.8 7.8 7.1 8.0Fiji 4.8 3.5 4.2 2.4 3.3 3.6 4.0 4.5 4.95Hong Kong, China 6.3 6.1 5.4 3.9 4.5 5.0 --5.1 3.06 10.05India 4.2 5.0 6.7 7.6 7.1 4.7 6.3 6.55 6.37Indonesia 7.2 7.3 7.5 8.2 8.0 4.5 --13.0 0.85 4.77Kiribati --1.6 0.8 7.2 6.5 2.6 3.3 6.1 2.5 2.0Lao People’s Democratic Republic 7.0 5.9 8.1 7.1 6.9 6.5 5.0 5.0 5.7Malaysia 8.9 9.9 9.2 9.8 10.0 7.3 --7.4 5.81 8.54Maldives 6.3 6.2 6.6 7.2 6.5 6.2 6.0 8.55 7.58Marshall Islands 0.1 5.4 2.7 --1.9 --13.1 --5.3 --4.3 --1.8 –Micronesia, Federated States of --1.2 5.7 --0.9 1.3 --0.5 --3.8 --2.8 --2.0 –Myanmar 9.7 5.9 6.8 7.2 7.0 7.0 7.0 10.92 5.46Nepal 4.1 3.8 8.2 3.5 5.3 5.0 3.0 3.94 5.99Pakistan 7.8 1.9 3.9 4.1 4.9 1.0 2.6 4.33 5.09Papua New Guinea 11.8 16.6 1.9 --2.6 2.9 --2.4 1.4 3.15 --1.21Philippines 0.3 2.1 4.4 4.8 5.8 5.2 --0.6 3.32 3.95Republic of Korea 5.4 5.5 8.3 8.9 6.8 5.0 --6.7 10.89 8.81Samoa 4.1 1.7 --0.1 6.8 6.1 1.6 1.2 2.5 3.5Singapore 6.5 12.7 11.4 8.0 7.5 8.4 0.4 5.86 9.89Solomon Islands 9.5 2.0 5.4 10.5 3.5 --2.3 0.5 --0.5 --1.0Sri Lanka 4.3 6.9 5.6 5.5 3.8 6.4 4.7 4.3 6.0Taiwan Province of China 6.8 6.3 6.5 6.0 5.7 6.8 4.7 5.42 5.98Thailand 8.1 8.4 9.0 8.9 5.9 --1.7 --10.2 4.22 4.31Tonga 0.3 3.7 5.0 4.8 --1.4 --4.4 --1.5 – 1.5Vanuatu --0.7 4.5 1.3 2.3 0.4 0.6 6.0 --2.5 3.97Viet Nam 8.6 8.1 8.8 9.5 9.3 8.2 3.5 4.2 5.5

Central Asia

Armenia --52.6 --14.1 5.4 6.9 5.9 3.3 7.2 3.3 6.0Azerbaijan --22.7 --23.1 --19.7 --11.8 1.3 5.8 10.0 7.4 10.27Georgia --44.9 --29.3 --10.4 2.6 10.5 10.7 2.9 2.9 1.5Kazakhstan --5.3 --9.2 --12.6 --8.2 0.5 1.7 --1.9 2.8 9.44Kyrgyzstan --13.9 --15.5 --19.8 --5.8 7.1 9.9 2.1 3.6 5.04Mongolia --9.5 --3.0 2.3 6.3 2.4 4.0 3.5 3.2 2.98Russian Federation --19.4 --10.4 --11.6 --4.2 --3.4 0.9 --4.9 3.2 7.5Tajikistan --28.9 --11.1 --21.4 --12.5 --4.4 1.7 5.3 3.7 8.3Turkmenistan --5.3 --10.0 --17.3 --7.2 --6.7 --11.3 5.0 16.0 17.6Uzbekistan --11.1 --2.3 --4.2 --0.9 1.6 2.5 4.3 4.4 4.0

Source: IMF, World Economic Outlook 2000, Statistical Appendix. Available at <www.imf.org/external/pubs/ft/weo/2001/01/data/growth_a.csv>.a Excluding Central Asian economies.

I. Strengthening the Competitiveness of SMEs in the Globalization Process: Prospects and Challenges

5

Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific

Table I.2. Selected economies of the ESCAP region: rates of economicgrowth and inflation, 2000-2004

(Percentage)

Real GDP Inflationa

2000 2001b 2002c 2003c 2004c 2000 2001b 2002c 2003c 2004c

Developing economies of theESCAP regiond 7.0 3.1 4.2 5.4 5.9 2.1 3.1 3.0 3.4 3.6

South and South-West Asiac 4.5 4.6 5.5 6.0 6.6 6.1 6.9 7.3 6.7 6.3

Bangladesh 5.9 6.0 4.3 .. .. 3.4 1.6 4.0 .. ..India 4.0 5.4 6.0 6.3 7.0 3.7 4.2 5.0 5.0 4.5Islamic Republic of Iran 5.9 5.5 6.5 6.5 6.0 12.6 12.0 14.0 14.0 11.5Nepal 6.4 5.9 5.0 6.0 6.5 3.5 2.4 4.5 5.0 5.0Pakistan 3.9 2.6 4.0 4.7 5.2 3.6 4.7 5.0 5.0 5.0Sri Lanka 6.0 0.9 3.3 5.5 5.9 6.2 13.0 9.0 7.5 6.6Turkey 7.1 --8.4 2.0 4.4 4.1 54.9 65.0 51.2 43.0 34.9

South-East Asia 6.5 1.8 3.2 4.4 4.6 2.3 5.0 4.3 3.9 3.9

Cambodia 5.4 5.3 4.5 6.3 6.0 --0.8 --0.6 3.0 5.0 5.0Indonesia 4.8 3.3 3.8 4.9 4.6 3.7 11.1 9.8 6.3 5.3Lao People’s Democratic

Republic 5.7 6.4 5.0 .. .. 25.1 9.0 12.0 15.0 ..Malaysia 8.3 0.4 3.2 5.1 6.1 1.6 1.5 1.6 3.4 4.0Myanmar 13.6 5.0 5.1 5.9 .. --0.1 9.6 .. .. ..Philippines 4.3 3.4 4.0 3.4 4.0 4.4 6.3 5.7 5.3 5.0Singapore 9.9 --2.0 2.0 5.8 5.7 1.4 1.0 0.8 1.5 1.7Thailand 4.4 1.5 2.5 2.5 3.5 1.6 1.6 1.8 2.5 3.1Viet Nam 6.8 6.8 6.1 6.8 7.3 --1.7 --0.1 2.0 3.8 7.6

East and North-East Asia 8.0 3.2 4.3 5.7 6.2 0.8 1.1 1.2 2.1 2.7

China 8.0 7.3 7.0 7.5 7.6 0.4 0.7 1.1 2.2 2.5Hong Kong, China 10.5 --2.0 1.0 6.0 6.3 --3.8 --1.6 --1.0 2.5 4.0Mongolia 1.1 1.4 4.0 5.0 6.0 11.8 8.8 6.0 5.0 5.0Republic of Korea 8.8 3.0 3.9 4.6 5.0 2.3 3.2 2.8 2.6 3.4Taiwan Province of China 5.9 --2.2 1.7 4.0 5.4 1.3 0.0 0.0 1.0 1.5Pacific island economies --1.0 --1.2 2.7 2.7 2.5 7.1 7.2 8.2 7.1 5.9Cook Islands 3.2 3.2 3.3 .. .. 2.0 1.0 1.0 .. ..Fiji --2.8 1.5 5.0 4.0 3.0 3.0 2.3 2.5 3.0 3.0Papua New Guinea --0.8 --3.3 1.2 1.8 2.1 10.0 10.3 12.0 10.0 8.0Samoa 7.3 6.5 4.8 4.3 4.1 1.0 1.5 2.0 2.0 2.0Solomon Islands --14.5 --7.0 5.5 3.0 2.0 6.0 8.0 10.0 6.0 5.0Tonga 6.1 3.0 2.5 2.9 3.0 7.0 8.0 3.0 3.0 3.0Vanuatu 4.0 2.0 3.0 3.5 3.5 4.1 3.0 2.0 2.5 2.5

(Continued)

6

Table I.2 (continued)

(Percentage)

Real GDP Inflationa

2000 2001b 2002c 2003c 2004c 2000 2001b 2002c 2003c 2004c

Developed economies of theESCAP region 2.5 --0.2 --0.9 1.6 1.5 --0.4 --0.4 --0.7 --0.3 0.2

Australia 3.8 4.1 3.0 4.1 3.6 4.5 4.2 2.3 2.4 2.9Japan 2.4 --0.5 --1.2 1.4 1.4 --0.7 --0.7 --0.9 --0.5 0.0New Zealand 3.8 2.6 1.9 3.3 2.0 2.6 2.7 2.1 1.8 1.8

Memo:

Kazakhstan 9.6 13.0 6.3 6.8 7.2 13.5 8.4 6.9 6.7 7.0Russian Federation 8.3 5.7 3.5 4.0 4.3 20.8 18.6 15.5 13.0 11.0Uzbekistan 4.0 4.0 2.5 3.0 .. 24.9 25.6 25.5 23.1 ..

Sources: ESCAP, based on International Monetary Fund, International Financial Statistics, vol. LV, No. 1 (January 2002); AsianDevelopment Bank, Key Indicators of Developing Asian and Pacific Countries 2001 (New York, Oxford UniversityPress, 2001) and Asian Development Outlook 2001 (New York, Oxford University Press, 2001); Economist IntelligenceUnit, Country Reports and Country Forecasts (London, 2001 and 2002), various issues; and national sources.

Notes: This table is based on data and information available up to 15 March 2002.

The estimates and forecasts for countries relate to fiscal years defined as follows: fiscal year 2001/02 = 2001 for Indiaand the Islamic Republic of Iran; and fiscal year 2000/01 = 2001 for Bangladesh, Nepal and Pakistan.a Changes in the consumer price index.b Estimate.c Forecast/target.d Based on data for 28 developing economies representing about 95 per cent of the population of the region (excluding

the Central Asian republics); GDPs at market prices in US dollars in 1995 have been used as weights to calculate theregional and subregional growth rates.

globalized and as transport and communicationcosts are reduced, the intensity of competitionincreases, and it becomes desirable to search fornew economical sites to produce differentproducts, parts and components to serve differentmarketplaces.

For all developing countries including theleast developed ones and the economies in transi-tions, some form of industrialization and industrialgrowth must be recognized as the principal meansto provide stability and economic growth. Abun-dant natural resources, low labour rates and evenlarge markets are no longer indispensable factorsfor development, nor sufficient attractions forinvestors. Essential infrastructure, enhanced skills,technological capability and improved management

practices constitute the key elements of competi-tiveness in the emerging pattern of global competi-tion and industrialization. Industrial developmentcontinues to be the main channel for value added,together with certain related service sectors. Whileindustry remains the principal engine for economicgrowth and overall prosperity, at the same time,because of the liberalized process, the increasedglobalization of industry and the extraordinaryand rapid pace of technological innovations andadaptation, new challenges and prospects forindustrialization are being created. It is thereforeessential not only to reiterate the key role of theindustrialization of developing countries in the newcontext, but it is also necessary to assess thecurrent industrial development trend and prospectsfor new international relationships at the enterprise

I. Strengthening the Competitiveness of SMEs in the Globalization Process: Prospects and Challenges

7

Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific

and institutional levels. As a result, industrialgrowth in developing countries is likely to becomeincreasingly complex and difficult during thecoming years. Furthermore, in developing coun-tries of the region, major institutional changes andnew strategies and mechanisms will be required forthe successful integration of developing countriesinto the mainstream of international trade, invest-ment and technological flows. Industrial policyreforms and the role of government will needmajor changes and adjustments to ensure thatmarket shortcomings are adequately adjusted andcorrected through appropriate policy interventionsto improve long-term economic performanceand ensure that economies can be truly part ofthe mainstream of global trade and investment.Countries must increasingly assume a leading rolein enhancing both domestic and international com-petitiveness and the increased export orientation oflocal enterprises. At the same time, the growingcomplexity of industrialization in the light ofglobal economic developments highlights the needfor specialized institutional support at the interna-tional level to provide a range of technical servicesfor accelerated industrialization and technologicalprocess in developing countries.8

2. Liberalization and globalizationprocess and SMEs

Thus, it has to be underscored that theprocess of globalization and liberalization hasassisted individual firms in operating acrossnational boundaries in Asian and Pacific countries,affecting thereby the whole process of industrialdevelopment in different economies. Increasinglyit is being realized that the opening of globalmarkets through trade liberalization is not onlymaking it easier for firms to extend their opera-tions beyond national boundaries but also provid-ing greater potential for expansion and growth.But all countries are not benefiting, as this will

require competitive capacity and additional re-sources for investment, in addition to technologicaland marketing linkages to promote rapidly chang-ing and high-quality products and services. This iswhere the importance of international and globalproduction networks lies. It is very essential thatall countries and economies be somehow linkedand integrated into such production networks sothat sustainable regional and global productionstructures could be created for everyone to playmutually beneficial economic roles.

Furthermore, as a result of globalizationfactors, the world has witnessed unprecedentedgrowth in output and trade over recent decades.World output grew by an annual average of 2.7 percent during 1981-1990 and 3.5 per cent in 1996and 1997, before the crisis reduced growth to 1.9per cent in 1998. However, it increased to 3.8 percent in 2000, but fell to 1.3 per cent in 2001.9World trade has grown at about twice the rate, at4.5 per cent on average during 1981-1990 andabout 7.0 per cent during 1991-1997 with a growthrate of 10.5 per cent in 1994 largely owing tosustained trade liberalization. World trade volumegrew by 12.4 per cent in 2000, but declined to -0.2per cent in 2001.10 In 2002 the world tradevolume is expected to increase by 2.5 per cent.Average tariffs in industrial countries fell from 40per cent in 1946 to about 5 per cent in 1990. Bythe early 1990s, world exports (adjusted forinflation) were nearly 10 times higher than 40years earlier.11 Even in 1998, world trade grew attwice the rate of growth in world output.12 In2003 world trade is expected to grow by 6.6 percent in comparison with the world output growthof 4.0 per cent in that year.13 Global FDI flowsrose from US$ 24 billion in 1990 to US$ 120billion in 1999. For many developing countries,private capital flows have largely replaced official

8 Bhavani P. Dhungana, “Economic integration and indus-trial production networking: Asia’s prospects andchallenges in 21st century”, paper presented at the Work-shop on the Emerging Economic Map of Asia: RegionalProduction Restructuring, Asian Integration and Sustain-able Development, Bangkok, 1-2 August 2001, p. 5.

9 UNCTAD, Trade and Development Report 2002, p. 5.

10 World Bank, Global Economic Prospects and the Deve-loping Countries 2002, p. 3.

11 International Herald Tribune, 4 January 2000.

12 United Nations, World Economic and Social Survey 1999.

13 International Monetary Fund, World Economic Outlook,April 2002, p. 6.

8

capital flows. In 1990, official capital providedhalf the loans and credits to 29 major developingcountries (including India, China and the Republicof Korea in Asia). By 1999 private flows totalledabout US$ 136 billion to these countries comparedwith only US$ 22 billion in government capitalflows.14

As indicated above, the Asian and Pacificregion also witnessed rapid economic growthduring the 1980s and 1990s as a result of globali-zation factors in combination with conducivenational policies. To a large extent, this economicgrowth was triggered by the impressive growth ofthe industrial sector, in particular manufacturing,especially after the switch from import substitutionto export promotion as the main developmentstrategy adopted by most East Asian economies.This policy has proved tremendously successful asjudged by the rapid export growth of selectedAsian countries.

A rise in the share of manufactured exportsand imports as a share of total merchandise tradewould be consistent with rapid growth in manu-facturing value added. Manufactured exports haveindeed shown a steadily increasing share of totalmerchandise exports with very large increases ineach ASEAN country and increases amongSAARC countries as well.15

Indonesia had a spectacular rise in manu-factured exports as a share of total merchandiseexports from just 2 per cent in 1980 to over 50 percent in 1995 and 1996. Manufactured exports hadbecome dominant in the exports of Malaysia (76per cent), Singapore (84 per cent), Thailand (73per cent), India (74 per cent), Nepal (99 per cent)and Pakistan (84 per cent) by the mid-1990s.Shares of manufactured imports had also risen

perceptibly in every case in ASEAN, but manu-factured goods shares in imports fluctuated inSouth Asia. Imports of manufactured goods inmuch of South Asia were subjected to high tariffsand several types of controls.

However, in general there has been adramatic shift in the pattern of developing countrytrade, with a shift away from dependence oncommodity exports to much greater reliance onmanufactures and services and the greatly in-creased importance of exports to other developingcountries. While national-level policy initiativesremain the principal focus of trade policy reforms,developing countries have become increasinglyinvolved in regional and multilateral trade negotia-tions. The multilateral system has made substan-tial adjustments to the increased importance ofdeveloping countries, but reforms in governanceand a sharper distinction between positive andnegative approaches to integration seem likely tobe needed. Furthermore, between 1980 and 1985manufactured exports and imports grew slowly inASEAN (with the exception of Indonesia, wheremanufactured exports rose rapidly from a verysmall base between 1980 and 1985). The slowgrowth during the first half of the 1980s reflectsthe period of economic recession in the region.Import growth was sharply negative in thecrisis-ridden Philippines in 1980-1985. Notably,there was a dramatic recovery of growth of manu-factured imports and exports in the Philippinesonce the economic and political situation had beenstabilized after 1986. In South Asia manufacturedimports grew very slowly in Bangladesh, Pakistanand Sri Lanka during 1980-1985, but have shownhigher growth since then. In Nepal, manufacturedimports decelerated after 1985 and growth becamenegative between 1990 and 1995. Growth inimports of manufactured goods fluctuated in India.The performance of manufactured exports ofIndia after 1990 was quite good compared with1980-1985. Nepal steadily increased its exportsof manufactured goods. The performance ofPakistan’s manufactured exports fluctuated. SriLanka had fairly strong growth in manufacturedexports during the 1980s.

Indeed, it is now widely recognized that themaintenance of an open liberalized domesticeconomy was decisive in explaining the growth of

14 Institute of International Finance, as quoted in Inter-national Herald Tribune, 4 January 2000. Private capitalflows comprise bank loans, bond financing, equityinvestments in local stock markets and foreign directinvestment.

15 Export Competitiveness and Sustained EconomicRecovery, Studies in Trade and Investment No. 46,(ST/ESCAP/2150), pp. 38-39.

I. Strengthening the Competitiveness of SMEs in the Globalization Process: Prospects and Challenges

9

Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific

East Asia and other successful developing coun-tries. It not only allowed for large inflows of FDIbut also for the rapid export growth generated to alarge extent by foreign-invested companies. Eastand South-East Asia have been the leading destina-tion among developing countries for global FDIflows. FDI inflows have been particularly high inthose countries, which also witnessed large exportgrowth. It is evident that those countries whichfailed to open their economies and adopt an exportpromotion strategy also failed to reap the benefitsof the globalization process. Globalization, inter-preted as constituting growing opportunities forworld trade and investment, after all enabled coun-tries with an export promotion strategy to actuallyincrease their exports. Without globalization, indi-vidual countries, including developed countries,would have continued their protectionist policies,so common in the direct aftermath of theglobal depression of the 1930s, and would haveprevented East Asian and other developing coun-tries from increasing their exports at such highrates.

The latest success story in Asia with respectto export growth has been China since the countrystarted to liberalize its economy in the early 1980s.China is a very large economy in terms of absolutesize of production and trade. China has provedattractive to foreign investors as a result of itsrapid economic growth, large size, abundance oflow-cost labour and increasing trade orientation.Recent studies have found that Chinese manu-facturing industries and firms have proven to beformidable competitors with ASEAN counterpartsin both the United States and Japan. The exportshares of China in labour-intensive manufacturesrose sharply in the 1990s in both the United Statesand Japan and had an undeniable impact on themarket share of ASEAN. China devalued the yuantwice in 1990 and 1994 and strengthened itscompetitiveness vis-à-vis the ASEAN countries asthey by and large pegged their currencies to UnitedStates dollar, which appreciated strongly againstthe yen and most other major currencies in 1995and 1996. The sharp currency realignments in1997 and 1998, coupled with China’s pledge toavoid competitive devaluation, had eroded thiscompetitive advantage, however. It is also note-worthy that China, like most of South-East Asia

(the Philippines being the exception), experiencedan export slowdown in 1996. Thus, China is notable to avoid cyclical swings in export markets anymore than other Asian economies. South Asianindustries and firms may also have experiencedsome competitive pressure from China, particularlyin markets for labour-intensive manufactures suchas textiles, apparel, footwear and leather goods,toys and other miscellaneous manufactures. None-theless, trade with China also appears to havebeen expanding rapidly in the case of Indiabetween 1991 and 1997, with exports and importsboth expanding impressively. China maintains amerchandise trade surplus with the SAARC region.Both SAARC and ASEAN members have aninterest in the terms and conditions of China’saccession to the World Trade Organization (WTO)and may wish to consider commercial benefits andcosts in that context.

The growing trend of intraregional trade andinvestment is in fact a reflection at the regionallevel of global trends, which are pushed byglobalization. However, as globalization is likelyto continue at an accelerated pace, the implicationsfor industrial development and restructuring inline with the requirements of globalization arewide-ranging and include both opportunities andchallenges. That having been said, it should benoted, especially in the context of promotingSMEs, that a critical long-term policy challengewhich the ESCAP region will face is how tomanage globalization, extend the duration of thecurrent recovery and broaden its reach so thatthe poor can benefit from economic growth. Muchwill depend on creating new sources of growthby increasing the region’s export competitiveness,especially of exports by SMEs, while maintainingfinancial stability in increasingly open and inter-dependent economies.

This is the critical issue on which thecompetitiveness of SMEs will depend and attemptswill be made to seek answers to the followingquestions:

(a) What are the policy reforms that willensure that the region can sustain the internationalcompetitiveness of SMEs in a globalizing worldeconomy?

10

(b) How can the productivity andefficiency of SMEs be boosted? What institutionaland infrastructural factors are necessary forimproving the efficiency of SMEs?

(c) What are the implications of thecurrency exchange rate crisis for the long-termstability and export competitiveness of SMEs?

(d) What are the implications of regiona-lism and multilateralism for the survival and com-petitiveness of SMEs?

(e) What economy-wide integrated policyissues are important for the promotion of SMEsand their competitiveness at the internationalmarket?

C. Role of SMEs in the developmentprocess: some country experiences

1. General observations

SMEs all over the world have played afundamental role in promoting economic and in-dustrial production. In particular, SMEs providethe necessary foundations for sustained growth andrising incomes in the less developed and transi-tional economies. Sustained and healthy growth ofthe SME sector in weaker economies is obviouslynecessary, as it is difficult to imagine raisingoverall living standards and social peace in thoseeconomies without SME development. In general,SMEs provide the bulk of the entrepreneurs andemployment in those economies and they aremostly in the private sector. The development ofthe SMEs and their linkages with larger enterpriseshave also played a significant role in the highlysuccessful business practices of the verticallyintegrated Japanese “keiretsu” financial-industrialgroups during most of the post-war period. Simi-lar linkages appear to have been important inrecent successes of “township and village enter-prises” (TVE) in China. Another quite differentsynergistic relationship, based on both horizontaland vertical linkages, is represented by the kindof local cooperative/competitive development com-mon for a long time in Europe and North America,but only recently dignified with the titles of

“industrial district” and “cluster”.16 However, theSME sector in many developing countries hasusually been neglected and discriminated against interms of access to government attention, access tofinance, management and marketing expertise andtechnology, as compared with large enterprises.This has been particularly so in the economies intransition, where the large-scale State sector hadassumed the major role in economic and industrialdevelopment. Private sector development in theeconomies in transition and in the least developedcountries should, therefore, start by strengtheningand promoting SMEs as to allow these enterprisesto grow into medium- to large-scale enterprisesand enable them to take over the functions of thepreviously State-owned enterprises.

Although there are variations in theproliferation of SMEs and their contributions tothe economy, in recent decades there have beensome efforts to improve the conditions for SMEpromotion in the Asian and Pacific region.Policies have been adopted and attempts made toimprove the institutional facilities for their func-tioning. However, it also has to be noted that inthe Asian and Pacific region SMEs comprise awide range of plant sizes and technologies, bothacross and within countries, covering three broadtiers of activities. At the top, there is the modernSME sector, often closely linked with large enter-prises as subcontractors and producing modernconsumer and manufacturing products such asmetal goods, paints, processed foods, plastic goodsand wood products. These types of enterprisesgenerally use more modern technology andare located nearer to cities and ports with well-developed infrastructure facilities. In addition,urbanization and localization tend to facilitate thegrowth of the modern SME sector. At the otherextreme can be found the traditional SME sector,consisting of artisans, workshops, household unitsand craft industries and other industries, which arenormally found in rural areas. Enterprises operat-ing in this segment of the SME spectrum usually

16 Robert McIntyre, The Role of Small and MediumEnterprises in Transition: Growth and Entrepreneurship,Research for Action No. 49 (United Nations University,World Institute for Development Economics Research[WIDER], December 2001), p. 5.

11

I. Strengthening the Competitiveness of SMEs in the Globalization Process: Prospects and Challenges

Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific

employ rudimentary implements and rely on localmarkets for the supply of raw materials and thesale of the final products. Here, the agrariannature of the economy and fragmented markets,low technology and weak infrastructure favourlabour-intensive manufacturing at the householdlevel. Between these two sets of SMEs arethe agro-based industries, most often found insemi-urban areas, which utilize agricultural rawmaterials as major production inputs but maydepend on distant markets to sell their products.These types of SMEs, clustering around townshipsand population centres, have a great potential inmeeting some of the urgent needs of developingcountries, especially those with weaker economies.

In most less developed economies andeconomies in transition in the Asian and Pacificregion, the bulk of the industrial labour force isengaged in small- and medium-scale enterprises.Small-scale and cottage industries in LDCs usuallyemploy around 80 per cent of the entire industrialworkforce of the country. This sector also makes avaluable contribution to the industrial value addedof the economy. However, most of the valueadded, varying from around 40 to 70 per cent,routinely originates from only a few industries,usually food and beverages, jewellery and gems,leather and leather products, jute and jute products,textiles, furniture, wood products and handicrafts,indicating the narrow base of the SMEs in theeconomy. In the more advanced economies, SMEsare found in a wide array of industries.

2. Selected country experiences

SMEs in Bangladesh have contributedsignificantly to manufacturing growth and employ-ment creation. There are around 27,000 medium-sized enterprises and around 150,000 small-scaleenterprises in the country. At present, 80 per centof manufacturing establishments are SMEs,accounting for 80 per cent of the labour force and50 per cent of the output of the sector and 5 percent of GDP. SMEs provide vital linkages tolarger enterprises, particularly in the high-growthexport sector, and also form part of the corebusiness activities in both rural and urban areas.The garments industry contributed to SME deve-lopment through orders for accessories, packaging

materials, etc., while the footwear industry in-creased subcontracts to SMEs. In addition, agro-processing and poultry have recently emerged asimportant activities for the development of SMEs.Over the past decades, SMEs have contributedsignificantly to fostering labour-intensive growthand reducing poverty. Their production processesare often marked by outdated technologies. SMEsin general cannot offer the requisite collateral andmeet the transaction costs for obtaining access toinstitutional credit. SMEs also find it relativelymore difficult to access key infrastructure, includ-ing electricity and gas. The policy environment isnot conducive to the growth of SMEs. They aresubject to the same procedural rigours of registra-tion, taxation, credit disbursement, export andimport as large enterprises, thus adding high coststo their operations.

In India, small-scale industries (SSIs)account for 95 per cent of the country’s industrialunits, 40 per cent of industrial output, 80 per centof employment in the industrial sector, 35 per centof value added by the manufacturing sector, 40 percent of total exports and 7 per cent of net domesticproduct.

In Pakistan, the SME sector employs about80 per cent of the industrial labour force andmakes up about 60 per cent of the manufacturingsector. However, the contribution of SMEs toGDP is only 15 per cent.

In Indonesia, before the 1997 economiccrisis, almost two thirds of small business were inthe agricultural sector, over 17 per cent in trading(including restaurants and hotels), over 7 per centin processing industries, 5 per cent in the servicesector, 2.5 per cent in consultancy and 4 per centin other sectors. Thus, although SMEs account formore than 90 per cent of the total number ofcompanies in Indonesia, their share in the Indone-sian economy is very insignificant, as 80 per centof GDP is produced by large corporations.

SMEs constitute a large portion ofThailand’s national economy as they account for70 per cent of employment in the industrial sectorand 4.7 per cent of total manufacturing valueadded. About 98 per cent of establishments in the

12

manufacturing sector in Thailand are SMEs,17

which are scattered in both the Bangkok Metro-politan area and regional areas. The main indus-tries which are dominated by SMEs in Thailandinclude metal and steel, plastic products, rubberand garments. The competitiveness of SMEs isthus a crucial component of the national competi-tiveness agenda. The SME Promotion Act wasenacted in February 2000. The SME PromotionCommittee, chaired by the Prime Minister, and theOffice of Small and Medium Sized EnterprisePromotion, have been established to promotethe development of SMEs. The SME PromotionFund has also been established with seed moneyfrom the Government and other private sources.The Fund can be used for lending to SMEsor groups of SMEs and for funding projectsof government departments, other governmentagencies, State enterprises and private sector or-ganizations as approved under the SME PromotionAction Plan.

Concerted efforts are being made to supportSMEs through: (a) strengthening of technologicaland management capabilities; (b) developing skillsand knowledge; (c) enhancing market accessibility;(d) strengthening of the financial support system;(e) establishing a conducive business environment;(f) commercialization and incubation programmes;and (g) developing networks and clusters.18

Additional work is needed on SMEs, given theirpotential for job creation.

SMEs in Malaysia, defined as companieshaving paid-up capital of less than M$ 25 millionwith not more than 150 full-time employees, areprimarily involved in the manufacturing, engineer-ing and printing areas. SMEs contributed almost30 per cent of total output, 17.6 per cent of value

added and 17.5 per cent of employment in themanufacturing sector in 1995. Figures for thatyear show that only 20 per cent of SMEs areinvolved in exports. Currently more than 80 percent of total manufacturing firms in Malaysia areSMEs. Malaysian Industrial Development FinanceBerhad, which covers the manufacturing sector,provides 60 per cent of its coverage to SMEs.

In the Philippines, SMEs accounted for99 per cent of all enterprises, 45 per cent ofemployment and 28 per cent of value added in themanufacturing sector in the mid-1990s.

Singapore has no statistics for SMEs, but itis estimated that SMEs account for over 40 percent of manufacturing production and over 25 percent of value added in manufacturing.

In the Republic of Korea, SMEs accountedfor 70 per cent of employment, 46 per cent ofgross output and 47 per cent of value added in1997. Since the mid-1990s, SME policies in theRepublic of Korea have focused on fosteringcompetitive SMEs, accelerating the shift towards amore sophisticated and value-added industrialstructure through automation- and information-based processes and providing assistance for tech-nology development and quality improvement.SMEs have been encouraged to form cooperativeties with large companies and enhance their marketcompetitiveness at home and abroad. Short-termpolicies have focused on ensuring stability forSMEs in, for example, access to financing, particu-larly in the wake of the financial crisis. In addi-tion, sanctions against unfair transaction practicesbetween large companies and SMEs have beenstrengthened, and support for SME technologydevelopment projects has been increased. SMEpolicies also place emphasis on promoting exports.The Small and Medium Business Administration(SMBA) was established in 1996 as the centralsupport organization to assist SMEs. SMBA has11 regional offices throughout the country, workingin cooperation with related organizations suchas the Small and Medium Industry PromotionCorporation (SMIPC), Korea Federation of SmallBusiness (KFSB), Korea Credit Guarantee Fund(KCGF) and Korea Technology Credit GuaranteeFund (KOTEC).

17 Korea Trade-Investment Promotion Agency (KOTRA),A Strategy for Internationalization of SMEs in the Asia-Pacific Region: Lessons from the Empirical Study onKorean and Other APEC Member Countries (October1999), pp. 116-117.

18 Research Institute for Development and Finance, JapanBank for International Cooperation (JBIC), Issues ofSustainable Development in Asian Countries: Focusedon SMIs in Thailand, JBIC Research Paper No. 8-1(January 2001), pp. 9-12.

13

I. Strengthening the Competitiveness of SMEs in the Globalization Process: Prospects and Challenges

Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific

In China, the Government has not adopteda comprehensive SME policy yet. However, theState Economic and Trade Commission has deve-loped policies to support SMEs’ managementcontrol, financing and technology developmentsince it established its Small and Medium Enter-prises Department in 1998. In March 1999, theNational People’s Congress recommended morereforms and restructuring of SMEs and recentlygovernment circles have started to use the termSME more frequently. It is known that measuresto support SMEs, especially in financing andpreferential tax policies, have been implementedactively. The large State-owned corporations’difficult management situation has prompted theChinese Government to implement a promotionpolicy for SMEs. Currently there are no accuratestatistics on SME exports; however, it is roughlyestimated that 60 per cent of total exports fromChina come from the SME sector. The main areathat the Chinese Government is focusing on topromote SMEs is financial support, which includesrelieving SME debt through policy adjustmentsand providing credit and preferential tax treatmentto SMEs. Especially to provide credit loans toSMEs, the Government encouraged banks toexpand loans to SMEs by establishing a depart-ment that deals with SME credit loans exclusively.

3. SMEs and export promotion

In developing economies of the ESCAPregion, SMEs are now exporting a wide variety ofproducts and continue to play a crucial role ingenerating and diversifying exports. Although thedeveloping countries’ exports are mostly labour-intensive, as economies of the region are undergo-ing industrial restructuring of varying kinds withemphasis on the private sector as the engine ofgrowth, the importance of SMEs in exports hastaken on a new dimension. In particular, SMEsplay a significant role in the first or early phaseof an export-oriented industrialization strategy bysupplying low-cost labour-intensive products suchas textiles and garments, leather goods and otherconsumer products. Again, as SMEs begin tomodernize, they have been active in producinglight engineering goods such as forgings, castings,diesel engines, simple machinery, machine tools,domestic appliances and construction hardware.

Electronics is in a different category, beingknowledge-intensive but requiring little capital andinfrastructure; it provides a valuable opportunityfor a new breed of young entrepreneurs, techni-cally and professionally qualified, to make theirmark. In countries such as the Republic of Korea,China, India, the Philippines, Thailand and Indone-sia, this sector is proving to be highly productiveespecially for exports from the SME sector. At themargin, imports of SMEs also tend to be lesscapital-intensive than those of large enterprises.This pattern of exports and imports not onlygenerates additional employment, but also has apositive impact on the trade balance. In all thenewly industrialized economies (NIEs), the export-oriented development strategy made a significantcontribution and in that context SMEs had amajor role to play. Even after Japan and AsianNIEs reached an advanced stage of development,SMEs in their economies continued to play acritical role in the export of manufacturedproducts, especially in those that are technology-and skill-intensive such as computers and software,and specialized parts and components for themachinery, transport and aircraft industries. Whilepromoting the ESCAP region’s export competitive-ness of SMEs entails creating new sources ofproductivity growth in the SME sector withstability and further trade liberalization and greaterflow of information, the contribution of SMEs todirect exports is considerable in most economies ofthe region. This contribution is even higher ifindirect exports are included. Statistics are usuallyonly available to limited extents for direct exportsand once again, the picture varies across countriesin the region. In India, SMEs account for about 35per cent of total exports. Since SMEs in Indonesiado not play a very significant role, only less than 5per cent of SMEs are involved in exports but thisfigure is much higher when indirect exports areincluded in terms of export items, textiles, fabrics,garments and agro-based products. In recent yearsexports of jewellery products from SMEs haveincreased rapidly in Indonesia. In Malaysia, SMEexports make up about 20 per cent of total exports.In Pakistan, SMEs exports account for about 80per cent of total exports of manufactured products.In the Philippines, some 90 per cent of exportersfall into the category of SMEs and their contribu-tion to exports is estimated at around 20 per cent.

14

In the Republic of Korea, SMEs accounted for41.8 per cent of exports in 1996. Main exportitems include electric and electronic products,machinery, other household goods and plasticitems. In China, textiles and light industry haveemerged as SME-dominated export sectors. Thesetwo sectors now account for over one third each ofthe total exports of China. In Japan, althoughSMEs occupy a very important place, in terms ofexports, they are not significant. SMEs play a veryimportant role in the exports of Taiwan Province ofChina. In Singapore, as companies are focusingon direct or indirect export of goods through multi-national corporations, the ratio of exports fromSMEs is not high.

Other developing countries trying to repeatthe success of the NIEs face vastly differentexternal market conditions. In particular, theproduct structure of SMEs would have to changein line with changes in external demand. Sinceexternal demand is shifting to human capital andinformation-intensive products, the SMEs of theAsian NIEs are better placed than SMEs in othercountries of the region to respond to this change.The newcomers, particularly countries eager torepeat the success of the NIEs, may find that theirSMEs are less favourably placed. They are likelyto encounter increased competition from otherSMEs from outside the region. In addition, thehigh cost of some capital goods and exchange ratevolatility add to their difficulties.

SMEs make a valuable contribution assubcontractors to large enterprises, which oftentend to be transnational corporations (TNCs).They produce parts and components for largeenterprises on a contractual basis, using localresources and skills. In terms of economic fluctua-tions, they act as “shock absorbers” for the largeenterprises, adjusting their own employment andproduction levels to reflect changes in demandand supply conditions. In these ways, they add tothe flexibility and viability not only of the largeenterprise sector but also of the entire economy.While the importance of such linkages is recog-nized, the actual existence and utilization of thevast potential to forge and strengthen such linkageshave remained limited and therefore requireincreased government attention.

4. SMEs and foreign direct investment

Although information on FDI by SMEs isdifficult to obtain, in some cases it is obvious thatSMEs are playing an increasingly important role inFDI, especially from the more advanced develop-ing countries. However, not all countries collectcomprehensive data on SME-related FDI. Excep-tions in this regard are Japan and the Republic ofKorea. However, there is no survey to identifyinward or outward FDI by SMEs. Nevertheless, inthe Republic of Korea, investment abroad by smallbusinesses amounted to 65.7 per cent of totaloutward investment in 1996 or US$ 3,968 million.In 1996 small and medium-sized TNCs accountedfor 55 per cent of new foreign affiliates byJapanese firms.19 In Thailand, 46 per cent of theapproximately 2,500 Japanese firms operatingin the country are SMEs.20 In 1997 the UnitedNations Conference on Trade and Development(UNCTAD) undertook a questionnaire survey andanalysed the problems and obstacles facing invest-ment by SMEs. This is the only comprehensiveanalysis on the subject.21

On the basis of the above analysis, itappears that SMEs are quite important in theircontribution to overall development in countries ofAsia and the Pacific. They have also increasinglybecome involved in the globalization process,which has clearly created opportunities. Interna-tionalization of SMEs has opened up new opportu-nities for growth within the domestic economythrough employment promotion, entrepreneurshipdevelopment and exports. However, globalizationalso has its costs and has affected SMEs somewhatnegatively, in particular when one looks at it withreference to the recent Asian crisis. Some suchimplications of the globalization process for SMEsare presented in the following section of this study.

19 UNCTAD, World Investment Report 1999: ForeignDirect Investment and the Challenge to Development(United Nations publication, Sales No. E.99.II.D.3).UNCTAD defines SMEs as firms with 300-500 workers.

20 According to the Board of Investment in Thailand,Bangkok Post, 3 March 2000.

21 UNCTAD, Handbook on Foreign Direct Investment bySmall and Medium-sized Enterprises: Lessons from Asia(United Nations publication, Sales No. E.97.II.D.4).

I. Strengthening the Competitiveness of SMEs in the Globalization Process: Prospects and Challenges

15

Investment Promotion and Enterprise Development Bulletin for Asia and the Pacific

D. Promoting the competitivenessof SMEs within the ongoing process

of globalization

The analysis and information provided inthe earlier sections of this study have pointed outthat globalization and its various aspects haveimpacted in different ways on the SMEs, whichhas not been positive all the time. Furthermore, inmost of the developed countries, SMEs enjoyedthe support of the Government in terms ofappropriate legislation for the provision of credit,technical support and other incentive measures andbuilt-up their capacity to deal with the adverseimpacts of globalization. However, in developingcountries, SMEs enjoy only limited support fromgovernment for the same types of facilities. Inaddition to the problems that the SMEs have toface in developing countries, new challenges haveunfolded as a result of the globalization process.SMEs of developing countries, particularly smallmanufacturing firms, are facing serious challengesdue to new developments at the regional andglobal levels, leading to severe competition indomestic as well as international markets. Someof these challenges are presented below.

1. Trade liberalization and multilateralagreements

While SMEs in Asia and the Pacific willmainly benefit in the long run from trade liberali-zation within the region, the various provisions ofregional and multilateral agreements including theUruguay Round agreements have led to substantialtariff cuts in developed countries, changing thestructure of export markets, especially for productswhich are important to SMEs. For instance,above-average cuts involve seven product groups,which together account for over 70 per cent ofindustrialized countries’ imports: metals; mineralproducts and precious stones; electrical machinery;wood, pulp, paper and furniture; non-electricalmachinery, chemicals and photographic supplies;and other manufactured articles, all of which aresectors in which SMEs are direct producers orsuppliers. However, not only SMEs in Asia andthe Pacific will benefit, but SMEs from other

regions will as well, which will intensify the levelof competition among SMEs globally for exportsto developed countries. Moreover, high tariffs aremaintained in developed countries on productswhich are also important to SMEs, such as textilesand garments, rubber, leather, footwear and travelgoods. It is also to be noted that regionaleconomic groupings are gaining power and arechanging the patterns of international trade.

For those countries with a less developedeconomy and industrial sector, including the LDCsin South and South-East Asia, their commitmentsunder the regional and multilateral agreementswill provide both opportunities and challenges, inparticular for SMEs. While opportunities liemainly in the necessity to upgrade national capa-bilities and the performance of both public andprivate enterprises forced by international competi-tion, challenges include mobilizing the necessaryfinancing, political commitment and skills to do so.While trade liberalization provides major opportu-nities for SMEs to increase their exports, a majorchallenge will be to improve their competitivenessnot only for exports but also at home as SMEshave to compete with imports and larger inflows ofFDI, including foreign investment from otherSMEs.