INVESTMENT FUNDS FOR DEVELOPMENT PROGRAM …€¦ · · 2016-07-15• Private equity...

69

INVESTMENT FUNDS FOR DEVELOPMENT PROGRAM Fin4Dev Investment Funds Group December 2015 101598 Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized ed

Transcript of INVESTMENT FUNDS FOR DEVELOPMENT PROGRAM …€¦ · · 2016-07-15• Private equity...

INVESTMENT FUNDS FOR DEVELOPMENT

PROGRAM

Fin4Dev Investment Funds Group

December 2015

101598

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Outline

• Program development objective

• Intermediate outcomes

• Strategic relevance

• Program context/description

• Program risks

• Roles of clients and partners

• Dissemination and outreach strategy

1

Program development objective

The development objective of the Investment Funds for Development (IFD)

program is to enable EMDE governments and regional economic

communities to create the conditions to mobilize investment fund

resources for SMEs and infrastructure finance, with the objective to

contribute to the achievement of the SDGs of growth and employment

(SDG8), resilient infrastructure (SDG9), and climate adaptation and

mitigation (SDG13).

2

Intermediate outcomes

• Increase in penetration of private equity and venture capital assets under

management (AUM) invested in EMDEs by 10% by 2020

• Increase in private equity and debt funds AUM invested in infrastructure

in EMDEs by 10% by 2020

• Increase private equity and debt funds assets AUM invested in climate

mitigation and adaptation in EMDEs by 15% by 2020

3

Strategic relevance: Role of investment funds in SME

finance for growth and employment

• Young SMEs are primary source of job creation

• Young SMEs (less than 5 years) = 17% of employment 42% of job creation 22% of job

destruction (OECD)

• Positive correlation between entrepreneurship and job creation across Indian states (WB)

• Resource flows to young patenting firms stronger in countries with more developed

markets for seed and early-steage venture capital (OECD)

• Increasing access of young patenting firms to seed and venture capital is critical to support

innovation

• Private equity participation increases number of citations of patent by 30% (EVCA)

• Private equity backing improves operational performance of portfolio companies by 4.5%

to 8.5% (EVCA)

• Private equity participation improves productivity by 6.9% on average (EVCA)

4

Strategic relevance: Role of investment funds in SME

finance for growth and employment

Globally private equity funds assets under management (AUM) have grown rapidly over

the last 10 years, reaching US$ 3.8 trillion in 2014

5

298 377 407 402 409563

8061,011 1,075 1,067 993 1,007 941 1,074 1,144418 374 360 465 554

675

898

1,265 1,2041,413

1,7832,029

2,332

2,5462,644

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

Dec-0

0

Dec-0

1

Dec-0

2

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-1

1

Dec-1

2

Dec-1

3

Ju

n-1

4

Private Equity Assets under Management December 2004 - June 2014 (US$ billion)

Dry Powder Unrealized Value

Source: 2015 Preqin Global Private Equity Report

Strategic relevance: Role of investment funds in SME

finance for growth and employment

by type of fund, buyout funds are the leading asset class (37% of dry powder), followed

by real estate funds (17%), venture capital funds (11%), and infrastructure funds (9%)

6

0

200

400

600

800

1,000

1,200

1,400

Dec-03 Dec-04 Dec-05 Dec-06 Dec-07 Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Dec-14

Dry

Po

wd

er

($b

n)

Private Equity Dry Powder by Fund Type 2003 – 2014 (US$ billion)

Buyout Distressed Private Equity Growth

Infrastructure Mezzanine Real Estate

Source: 2015 Preqin Global Private Equity Report

Strategic relevance: Role of investment funds in SME

finance for growth and employment

Among exit strategies, trade sales represented 53% of exit transactions in Q4 2014,

followed by sales to general partners (31%) and IPOs (15%)

7

0

20

40

60

80

100

120

140

160

0

50

100

150

200

250

300

350

400

450

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

2006 2007 2008 2009 2010 2011 2012 2013 2014

Aggre

ga

te E

xit V

alu

e ($

bn

)N

o. o

f E

xits

Private Equity-Backed Exits by TypeQ1 2006 – Q4 2014

IPO Restructuring Sale to GP Trade Sale Aggregate Exit Value ($bn)

Source: 2015 Preqin Global Private Equity Report

Strategic relevance: Role of investment funds in SME

finance for growth and employment

The investor base of PE funds has undergone significant transformation over the last 6 years:

8

28%

13%

3%

8%7%

4%

6% 6%5%

4%

1% 2%

22%

13%

10%

6%

10%

6%

3%

12%

3%

5%

2% 3%

0%

5%

10%

15%

20%

25%

30%

Pu

blic

Pe

nsio

nF

unds

Fu

nd

of F

und

sM

ana

ge

rs

Hig

h-N

et-

Wo

rth

Indiv

idua

ls

En

do

wm

ent

Pla

ns

Priva

te S

ecto

rP

ensio

n F

un

ds

Fam

ily O

ffic

es

Fou

nd

atio

ns

Insura

nce

Co

mp

an

ies

Ba

nks &

Investm

ent

Ba

nks

Go

vern

me

nt

Ag

en

cie

s

Co

rpo

rate

Investo

rs

Sovere

ign

We

alth

Fu

nds

Pro

po

rtio

n o

f C

ap

ital C

om

mit

ted

Investor Type

Make-up of LPs in the Average Fund by LP Type (Capital Committed to Funds Closed in 2009-2014)

2009-2011

2012-2014

Source: 2015 Preqin Global Private Equity Report

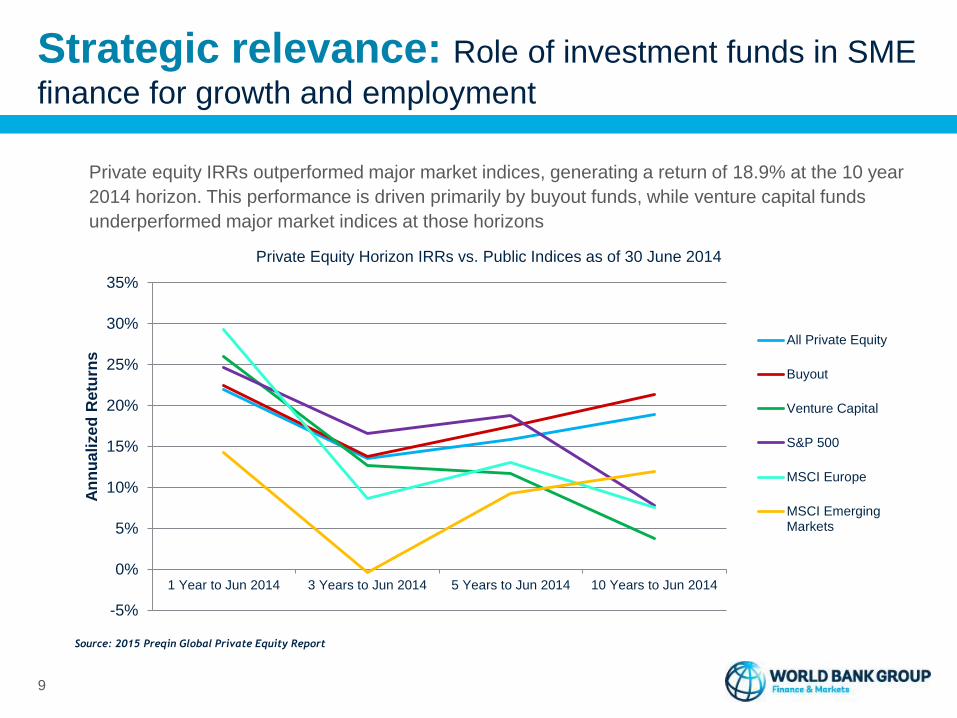

Strategic relevance: Role of investment funds in SME

finance for growth and employment

Private equity IRRs outperformed major market indices, generating a return of 18.9% at the 10 year

2014 horizon. This performance is driven primarily by buyout funds, while venture capital funds

underperformed major market indices at those horizons

9

-5%

0%

5%

10%

15%

20%

25%

30%

35%

1 Year to Jun 2014 3 Years to Jun 2014 5 Years to Jun 2014 10 Years to Jun 2014

An

nu

ali

ze

d R

etu

rns

Private Equity Horizon IRRs vs. Public Indices as of 30 June 2014

All Private Equity

Buyout

Venture Capital

S&P 500

MSCI Europe

MSCI EmergingMarkets

Source: 2015 Preqin Global Private Equity Report

Strategic relevance: Role of investment funds in SME

finance for growth and employment

Following the international financial crisis in 2008, private debt funds have emerged as a rapidly

increasing asset class

10

60

8691 94

141

108

23

3946

58

79

64

0

20

40

60

80

100

120

140

160

2009 2010 2011 2012 2013 2014

Year of Final Close

Annual Private Debt Fundraising 2009 - 2014

No. of Funds Closed

Aggregate CapitalRaised ($bn)

Source: 2015 Preqin Global Private Debt Report

Strategic relevance: Role of investment funds in SME

finance for growth and employment

Among private debt funds, mezzanine funds represent 42% of the total, followed by direct lending

funds (23%), and distressed debt funds (16%)

11

23%

16%

42%

15%

4%

Primary Strategy of Private Debt Fund Managers Established Since 2008

Direct Lending

Distressed Debt

Mezzanine

Special Situations

Venture Debt

Source: 2015 Preqin Global Private Debt Report

Strategic relevance: Role of investment funds in SME

finance for growth and employment

After reaching a peak of US$ 52 billion in 2008, venture capital fund raising dropped significantly

following the international financial crisis. Fundraising rebounded significantly in 2011, stagnated in

2012 and 2013, and increase significantly to US$ 46 billion in 2014

12

52.4

27.0 26.5

42.2

38.1

31.2

45.7

0.0

10.0

20.0

30.0

40.0

50.0

60.0

2008 2009 2010 2011 2012 2013 2014

Evolution of Venture Capital Fundraising, 2008 – 2014 (US$ billion)

Source: 2015 Preqin Global Private Equity Report

Strategic relevance: Role of investment funds in SME

finance for growth and employment

VC investments cover a wide range of sectors, including internet, software, health care and telecoms

13

27%22% 25% 23% 26% 29%

18%

14%

21%20%

20% 17%

18%

25%

16% 22% 15% 15%

12%9%

14% 10%15% 16%

8%8%

8% 9% 9% 7%2%

2%

3% 2% 3% 3%4% 9%3% 3% 3% 3%4% 2% 3% 4% 3% 3%3% 2% 2% 1% 2% 2%3% 3% 2% 3% 2% 2%

3% 3% 3% 3% 2% 3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

No. of Deals Aggregate DealValue

No. of Deals Aggregate DealValue

No. of Deals Aggregate DealValue

2012 2013 2014

Pro

po

rtio

n o

f To

tal

Proportion of Number and Aggregate Value of Venture Capital Deals by Industry 2012 – 2014

Internet Software & Related Healthcare Telecoms

Other IT Business Services Clean Technology Consumer Discretionary

Industrials Semiconductors & Electronics Other

Source: Preqin Global Private Equity Reports, 2014 & 2015

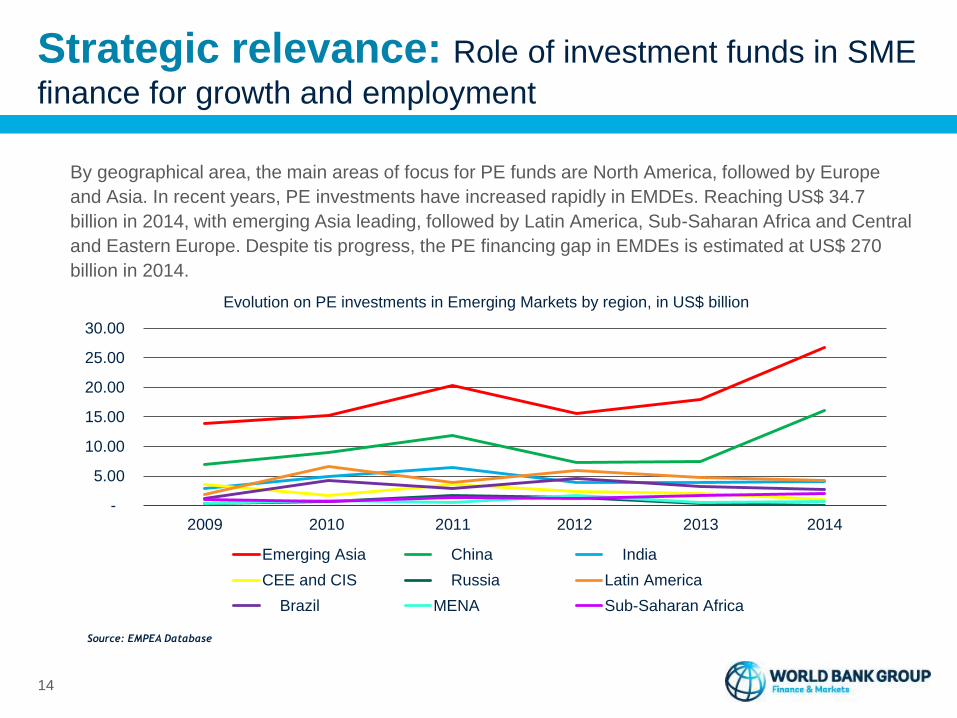

Strategic relevance: Role of investment funds in SME

finance for growth and employment

By geographical area, the main areas of focus for PE funds are North America, followed by Europe

and Asia. In recent years, PE investments have increased rapidly in EMDEs. Reaching US$ 34.7

billion in 2014, with emerging Asia leading, followed by Latin America, Sub-Saharan Africa and Central

and Eastern Europe. Despite tis progress, the PE financing gap in EMDEs is estimated at US$ 270

billion in 2014.

14

-

5.00

10.00

15.00

20.00

25.00

30.00

2009 2010 2011 2012 2013 2014

Evolution on PE investments in Emerging Markets by region, in US$ billion

Emerging Asia China India

CEE and CIS Russia Latin America

Brazil MENA Sub-Saharan Africa

Source: EMPEA Database

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

• Infrastructure investments have a positive impact on growth

• A 1% increase in physical infrastructure stocks temporarily raises GDP

growth by 1-2 percentage points

• Physical infrastructure in roads and telecoms facilitates spatial access

and information flows, raising labor productivity, boosting rural non-farm

incomes, and reducing the incidence of poverty in some geographical

area

• Electrification leads to rising female employment (South Africa)

• Better transportation systems and safer roads raise school attendance

• Increased access to electricity allows more time to study and the use of

computers

15

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

• Investments in large infrastructure required to achieve the SDGs are estimated at US$ 900 billion to US$ 1/6 trillion per year over the 2015-2030 period

• Investments in climate mitigation and adaptation are estimated at US$ 440 billion to US$ 780 billion per year over the same period

• Investments required to limit the rise in average global temperatures to no more than 2 degree Celsius are estimated to range from US$ 380 billion to US$680 billion over the period

• Investments in climate adaptation required to adapt to a 2 degree Celsius warmer world are estimated in the range of US$ 70 billion to 100 billion per year through 2050

•

16

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

• Energy production accounts for 2/3 of global greenhouse gas (GHG) emissions

• The full implementation of the Intended Nationally Determined Contributions (INDCs) will require the energy sector to invest $ 13.5 trillion in energy efficiency and low-carbon technologies over the 2015-2030 period

• About US$ 8.3 trillion are required to improve energy efficiency in

transport, buildings and industry sectors

• The remainder is required to decarbonize the energy sector

• However full implementation of the INDCs will lead to increase in average temperatures of 2.7 degree Celsius by 2100

• Additional investments required to limit increase to 2 degree Celsius

amount to US$ 3 trillion in energy efficiency, phasing-out least efficient

coal-fired power plants, and boosting investments in renewable-based

power generation technologies, passing-out fuel subsidies, and reducing

methane emissions from oil and gas production

17

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Cumulative world energy sector investment by scenario 2015-2030

18

Source: International Energy Agency, World Energy Outlook Special Briefing for COP21

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Adaptation costs vary significantly across climate scenarios

19

Source: WB EACC The economics of adaptation to climate change

Sector UNFCCC (2007)EACC Study Scenario

NCAR (wettest) CSIRO (driest)

Infrastructure 2-41 27.5 13

Coastal zones 5 28.5 27.6

Water supply and flood protection 9 14.4 19.7

Agriculture, forestry, fisheries 7 2.6* 2.5*

Human health 5 2 1.5

Extreme weather events - 6.7 6.4

Total 28-67 81.5 71.2

*Note that the costs of adaptation in the agriculture, forestry and fisheries sector have changed as compared to the estimates presented in the EACC Global Report (The Cost to Developing

Countries of Adapting to Climate Change:

New Methods and Estimates, WB 2010) in which these costs stood at $7.6Billion for the NCAR and $7.3Billion for the CSIRO scenarios. The current costs are estimated as the difference in

public spending in the scenario with climate change and adaptation as compared to the no climate change scenario, and use the same methodology as has been applied to the other sectors. In

WB 2010, the costs were incorrectly reported as reflecting the difference in public spending in the scenario with climate change and adaptation as compared to the scenario with climate change

but no adaptation. The difference lowers the EACC lower bound estimate of the global cost of adaptation from US$ 75 billion reported in WB 2010 to US$ 71.2 billion per year, rounded to

US$ 70 billion per year.

Note: NCAR is The National Centre for Atmospheric Research, and CSIRO is the Commonwealth Scientific and Industrial Research Climate.

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Adaptation costs are part of broader set of resilience investments to

be undertaken as part of comprehensive disaster risk management

(DRM) strategies

Resilience investments include:

Resilience infrastructure investments by governments• Flood protection structures

• Community shelters

• Improved water supply and drainage systems

• Rehabilitation and construction of resilient public buildings

• Rehabilitation and construction of resilient energy facilities and transport

systems

• Installation of more resilient wireless communications

20

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Resilience investment by enterprises

• Operational resilience (on site and through relocation)

• Development of resilience products and services value chains

production of resilient construction materials

collection, recycling and reuse of waste materials

design and installation of micro water harvesting systems

design and installation of household solar energy systems

design and delivery of disaster risk management services

21

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Resilience investments by communities

• Resilient community facilities

• Community-based flood protection systems

• Resilient food storage facilities

Resilience investments by households

• Resilient housing

• Solar energy

Many resilience investments raise the quality of assets to insurable levels

22

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Resilience investments yield triple dividend

• Avoid losses by saving lives, reducing infrastructure damages, and

reducing economic losses

• Unlock suppressed economic potential and stimulate economic

activity through

encouraging households to save and build assets

promoting entrepreneurship

stimulating firms to invest and innovate

• Yield co-benefits through

generating employment opportunities in environmental services

stimulating the development of value chains in protected areas

improving access to employment and services through improved resilience of transportation networks

23

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Significant part of large infrastructure investment for growth, climate mitigation and adaptation, and resilience will be undertaken on balance sheet by national and sub-national governments

Amount:

• large infrastructure U$ 398 billion to US$ 844 billion/year

(53%)

• climate mitigation and adaptation US$ 140 billion to US$

225 billion/year (28%)

Financing through sovereign and sub-sovereign borrowing (loans, bonds)

24

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Given fiscal constraints, remaining investments will need to be undertaken off-government balance sheet through PPP SPVs

Amount:

• large infrastructure US$ 291 billion to US$ 755 billion/year

(47%)

• climate mitigation and adaptation US$ 300 billion to US$

564 billion/year (72%)

Financing through PPP SPV equity (25%) and debt finance (75%)

25

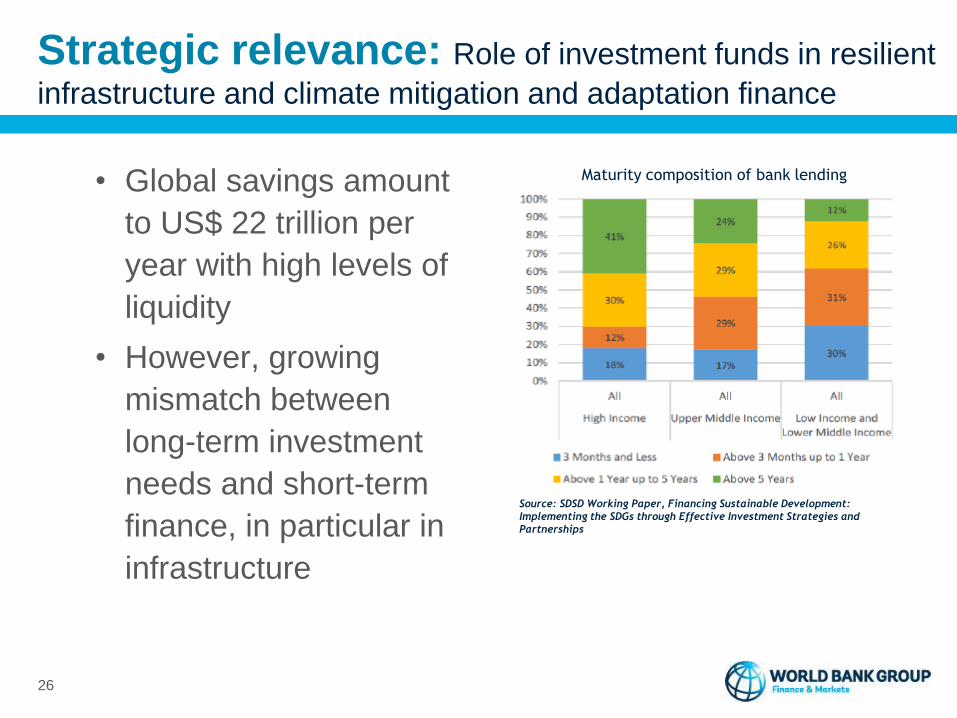

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

• Global savings amount

to US$ 22 trillion per

year with high levels of

liquidity

• However, growing

mismatch between

long-term investment

needs and short-term

finance, in particular in

infrastructure

26

Source: SDSD Working Paper, Financing Sustainable Development:

Implementing the SDGs through Effective Investment Strategies and

Partnerships

Maturity composition of bank lending

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

• Institutional investors hold US$ 79 trillion in AUM but have only 1 percent of their portfolio directly invested in infrastructure assets. The vast majority of these investments are concentrated in home countries

• Increasing investments by EMDE pension funds in infrastructure in recent years

Out of 33 pension funds reporting investments in infrastructure in 2013, 10 are from EMDEs

EMDE pension funds invested US$ 22.3 billion in infrastructure or 5.7% of total AUM in 2013, compared to 2.0% for listed debt/equity and 1.3% for unlisted equity

EMDE pension funds have also started to invest in infrastructure equity and debt funds

27

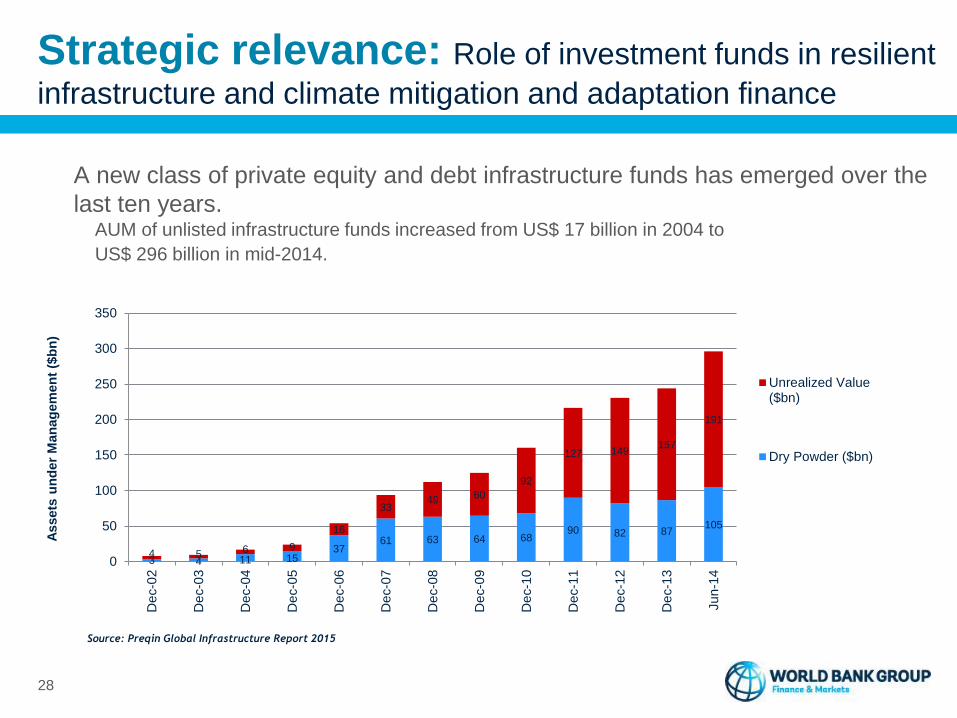

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

A new class of private equity and debt infrastructure funds has emerged over the

last ten years.AUM of unlisted infrastructure funds increased from US$ 17 billion in 2004 to

US$ 296 billion in mid-2014.

28

3 4 11 1537

61 63 64 6890 82 87

105

4 5 6 9

16

3349 60

92

127 149157

191

0

50

100

150

200

250

300

350

De

c-0

2

De

c-0

3

De

c-0

4

De

c-0

5

De

c-0

6

De

c-0

7

De

c-0

8

De

c-0

9

De

c-1

0

De

c-1

1

De

c-1

2

De

c-1

3

Jun-1

4

Assets

un

der

Man

ag

em

en

t ($

bn

)

Unrealized Value($bn)

Dry Powder ($bn)

Source: Preqin Global Infrastructure Report 2015

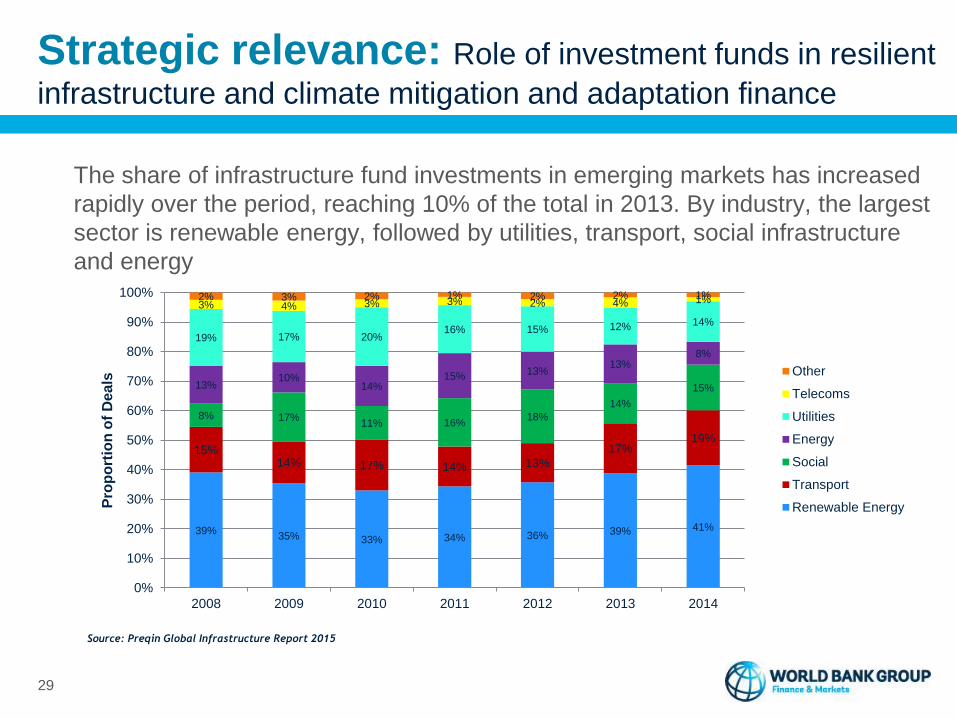

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

The share of infrastructure fund investments in emerging markets has increased

rapidly over the period, reaching 10% of the total in 2013. By industry, the largest

sector is renewable energy, followed by utilities, transport, social infrastructure

and energy

29

Source: Preqin Global Infrastructure Report 2015

39%35% 33% 34% 36% 39% 41%

15%14% 17% 14% 13%

17%19%

8% 17%11% 16%

18%

14%

15%13%10%

14%15% 13%

13%8%

19% 17% 20%16% 15% 12% 14%

3% 4% 3% 3% 2% 4% 1%2% 3% 2% 1% 2% 2% 1%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014

Pro

po

rtio

n o

f D

eals

Other

Telecoms

Utilities

Energy

Social

Transport

Renewable Energy

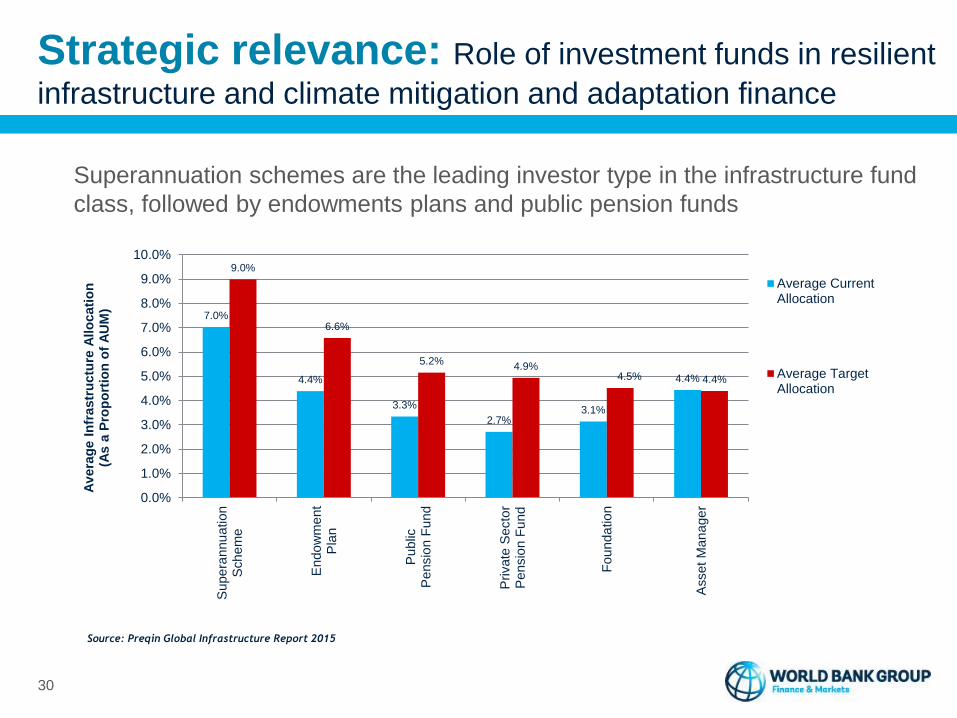

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Superannuation schemes are the leading investor type in the infrastructure fund

class, followed by endowments plans and public pension funds

30

Source: Preqin Global Infrastructure Report 2015

7.0%

4.4%

3.3%

2.7%3.1%

4.4%

9.0%

6.6%

5.2%4.9%

4.5% 4.4%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

10.0%

Supe

rannu

ation

Sch

em

e

Endo

wm

ent

Pla

n

Public

Pensio

n F

und

Private

Secto

rP

ensio

n F

und

Fo

unda

tio

n

Asset

Man

age

r

Av

era

ge I

nfr

astr

uctu

re A

llo

cati

on

(A

s a

Pro

po

rtio

n o

f A

UM

)

Average CurrentAllocation

Average TargetAllocation

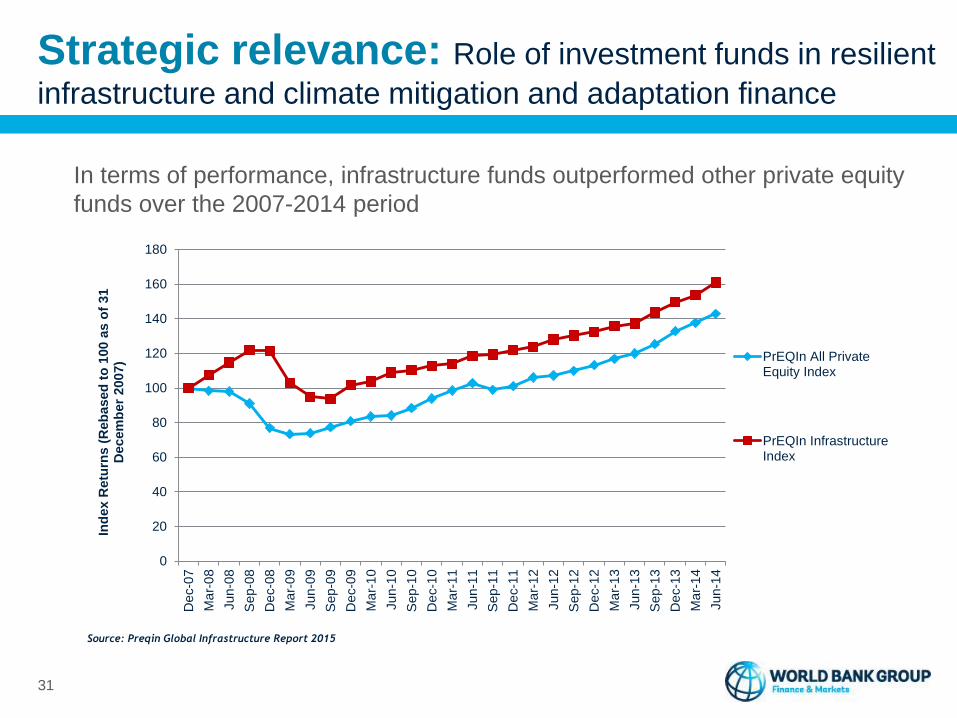

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

In terms of performance, infrastructure funds outperformed other private equity

funds over the 2007-2014 period

31

Source: Preqin Global Infrastructure Report 2015

0

20

40

60

80

100

120

140

160

180

De

c-0

7

Ma

r-0

8

Jun-0

8

Sep-0

8

De

c-0

8

Ma

r-0

9

Jun-0

9

Sep-0

9

De

c-0

9

Ma

r-1

0

Jun-1

0

Sep-1

0

De

c-1

0

Ma

r-1

1

Jun-1

1

Sep-1

1

De

c-1

1

Ma

r-1

2

Jun-1

2

Sep-1

2

De

c-1

2

Ma

r-1

3

Jun-1

3

Sep-1

3

De

c-1

3

Ma

r-1

4

Jun-1

4

Ind

ex R

etu

rns (

Reb

ased

to

100 a

s o

f 31

Decem

ber

2007) PrEQIn All Private

Equity Index

PrEQIn InfrastructureIndex

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Since 2009 infrastructure debt funds have emerged albeit from a low base. By

January 2015, there were 31 funds on the road seeking US$ 22.7 billion,

compared to 20 funds seeking US$ 15 billion in January 2014

32

Source: Preqin Global Infrastructure Report 2015

54

6

4

9

14

1716

20

31

1.82.6 3.3

0.41.9

5.9

8.09.7

15.0

22.7

0

5

10

15

20

25

30

35

Jan-06 Jan-07 Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15

No. of FundsRaising

Aggregate TargetCapital ($bn)

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

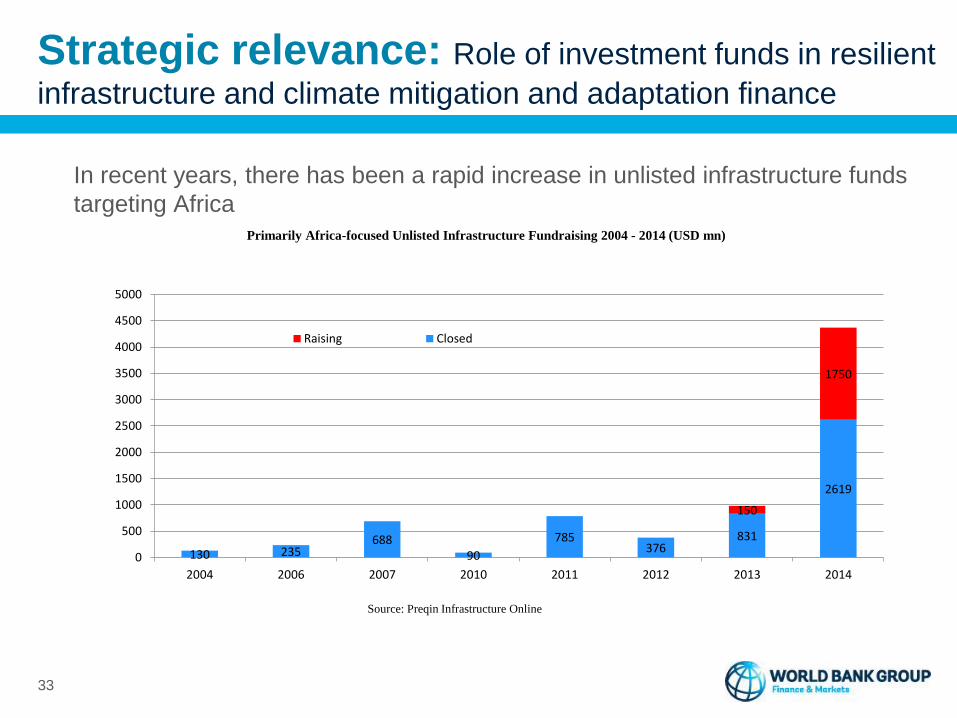

In recent years, there has been a rapid increase in unlisted infrastructure funds

targeting Africa

33

130 235688

90

785376

831

2619

150

1750

0

500

1000

1500

2000

2500

3000

3500

4000

4500

5000

2004 2006 2007 2010 2011 2012 2013 2014

Source: Preqin Infrastructure Online

Primarily Africa-focused Unlisted Infrastructure Fundraising 2004 - 2014 (USD mn)

Raising Closed

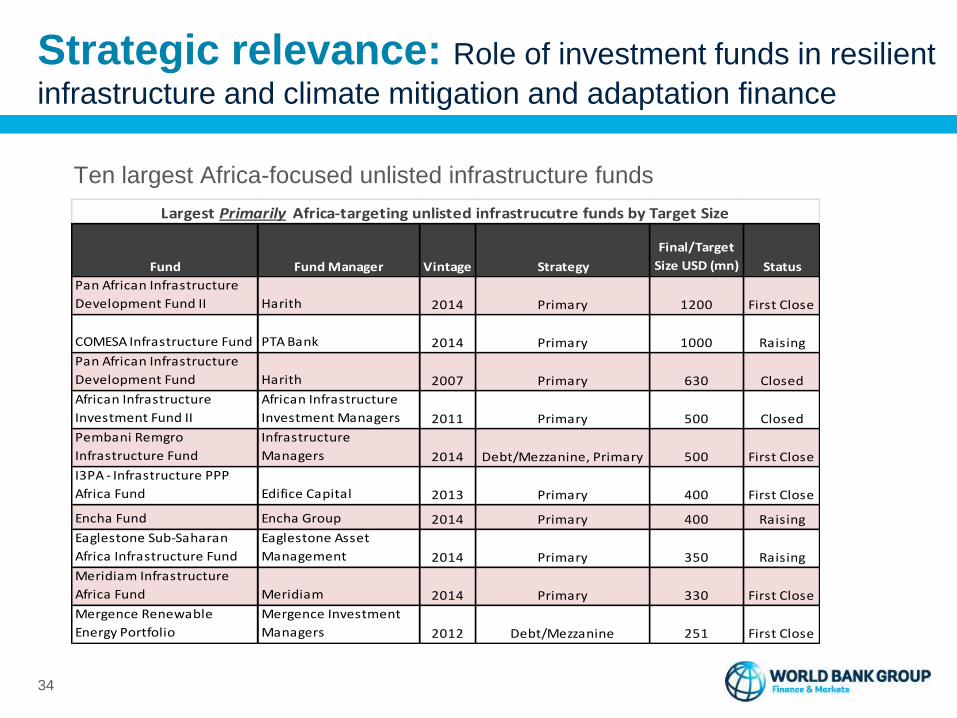

Strategic relevance: Role of investment funds in resilient

infrastructure and climate mitigation and adaptation finance

Ten largest Africa-focused unlisted infrastructure funds

34

Fund Fund Manager Vintage Strategy

Final/Target

Size USD (mn) Status

Pan African Infrastructure

Development Fund II Harith 2014 Primary 1200 First Close

COMESA Infrastructure Fund PTA Bank 2014 Primary 1000 Raising

Pan African Infrastructure

Development Fund Harith 2007 Primary 630 Closed

African Infrastructure

Investment Fund II

African Infrastructure

Investment Managers 2011 Primary 500 Closed

Pembani Remgro

Infrastructure Fund

Pembani Remgro

Infrastructure

Managers 2014 Debt/Mezzanine, Primary 500 First Close

I3PA - Infrastructure PPP

Africa Fund Edifice Capital 2013 Primary 400 First Close

Encha Fund Encha Group 2014 Primary 400 Raising

Eaglestone Sub-Saharan

Africa Infrastructure Fund

Eaglestone Asset

Management 2014 Primary 350 Raising

Meridiam Infrastructure

Africa Fund Meridiam 2014 Primary 330 First Close

Mergence Renewable

Energy Portfolio

Mergence Investment

Managers 2012 Debt/Mezzanine 251 First Close

Largest Primarily Africa-targeting unlisted infrastrucutre funds by Target Size

Program context/description

• Pillar 1: developing PE/VC ecosystem

• Pillar 2: developing framework for infrastructure PPPs

• Pillar 3: developing Strategic Investment Funds (SIFs) and

the domestic component of Sovereign Wealth Funds (SWFs)

35

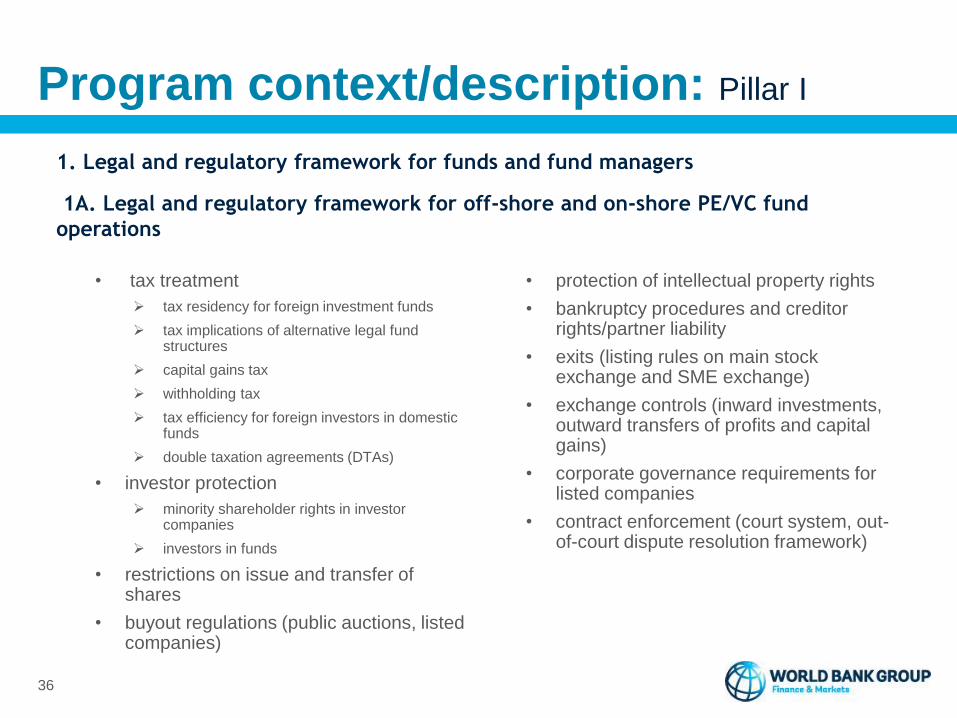

Program context/description: Pillar I

• tax treatment

tax residency for foreign investment funds

tax implications of alternative legal fund structures

capital gains tax

withholding tax

tax efficiency for foreign investors in domestic funds

double taxation agreements (DTAs)

• investor protection

minority shareholder rights in investor companies

investors in funds

• restrictions on issue and transfer of shares

• buyout regulations (public auctions, listed companies)

• protection of intellectual property rights

• bankruptcy procedures and creditor rights/partner liability

• exits (listing rules on main stock exchange and SME exchange)

• exchange controls (inward investments, outward transfers of profits and capital gains)

• corporate governance requirements for listed companies

• contract enforcement (court system, out-of-court dispute resolution framework)

36

1. Legal and regulatory framework for funds and fund managers

1A. Legal and regulatory framework for off-shore and on-shore PE/VC fund

operations

Program context/description: Pillar I

• fund legal structures (including fund

compartments)

• qualified assets

• qualified investors

• management company legal

structure

• qualification and disclosure of

persons who conduct the business

of the management company

• disclosure and resolution of conflicts

of interest

• delegation of core management

functions

• own funds

• asset valuation rules

• contents of fund prospectus

• disclosure to investors

• auditing and reporting

• depositary rules

• cooperation with the supervisory

agency

• penalties for non-compliance

37

1B: Legal and regulatory framework for domestic registration and supervision of

on-shore funds

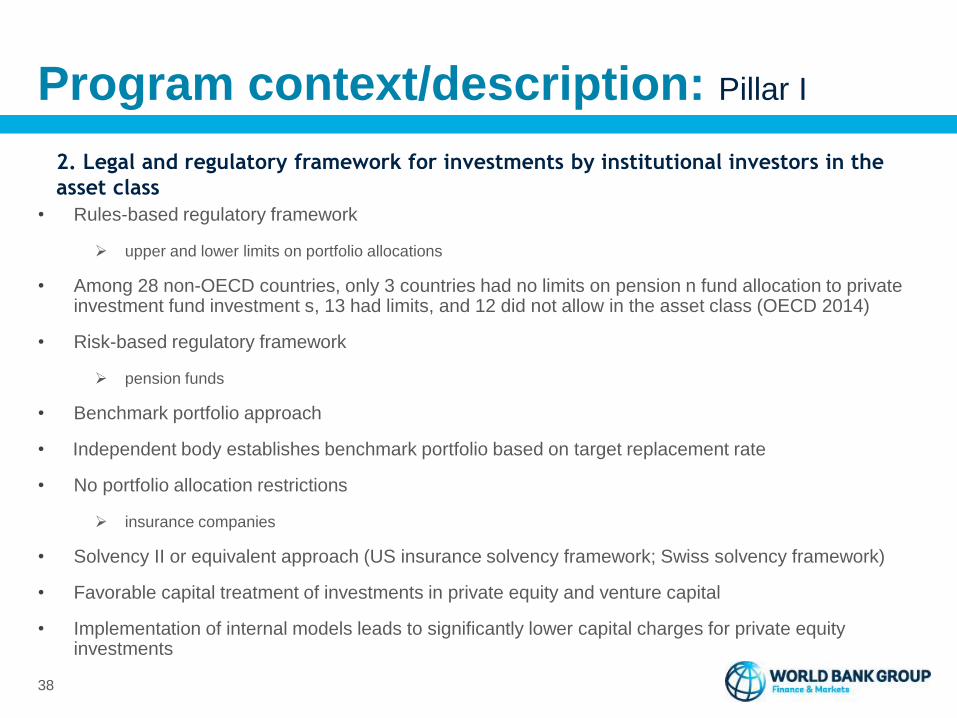

Program context/description: Pillar I

• Rules-based regulatory framework

upper and lower limits on portfolio allocations

• Among 28 non-OECD countries, only 3 countries had no limits on pension n fund allocation to private investment fund investment s, 13 had limits, and 12 did not allow in the asset class (OECD 2014)

• Risk-based regulatory framework

pension funds

• Benchmark portfolio approach

• Independent body establishes benchmark portfolio based on target replacement rate

• No portfolio allocation restrictions

insurance companies

• Solvency II or equivalent approach (US insurance solvency framework; Swiss solvency framework)

• Favorable capital treatment of investments in private equity and venture capital

• Implementation of internal models leads to significantly lower capital charges for private equity investments

38

2. Legal and regulatory framework for investments by institutional investors in the

asset class

Program context/description: Pillar I

• globally innovation is underfunded even in well-functioning markets due to

information asymmetries and appropriation risks

• problem exacerbated for new entrants and start-ups because they lack

track record to signal ability to investors and because they produce

intangible asset that does not constitute collateral

• in many EMDES, the lack of robust and continuous pipeline of promising

start-ups stalls development of strong angel investor community to back

innovative companies

• this in turn hampers development of stream of promising early-stage

companies in which venture capital funs can invest

Market failure can be addressed through balanced set of demand-side and supply-side

policies aimed at supporting development of angel investor and VC fund industry

39

3. Business enabling environment for PE/VC fund operations

Program context/description: Pillar I

Supply-side policies

• tax credits

• seed funds co investing with qualified angel investor groups

• technical assistance and training for angel investor groups (platform

set-up, group management, deal sourcing and due diligence,

investment tracking, entrepreneurship mentoring, follow-on financing

and exit management

40

Policies to support development of angel investor community

Program context/description: Pillar I

Demand-side policies

• entrepreneurship training

• support to development of business incubator and accelerators

incubator creation and management (strategy, positioning and long-term sustainability,

internal organization and governance)

incubation process (admission, incubation and exit mechanisms)

performance assessment (monitoring and evaluation, value-added of incubator in fostering

business development)

• resolution of coordination failures

linkages between university an private research centers and business incubators

linkages between business incubators and accelerators and angel investor groups.

41

Policies to support development of angel investor community

Program context/description: Pillar I

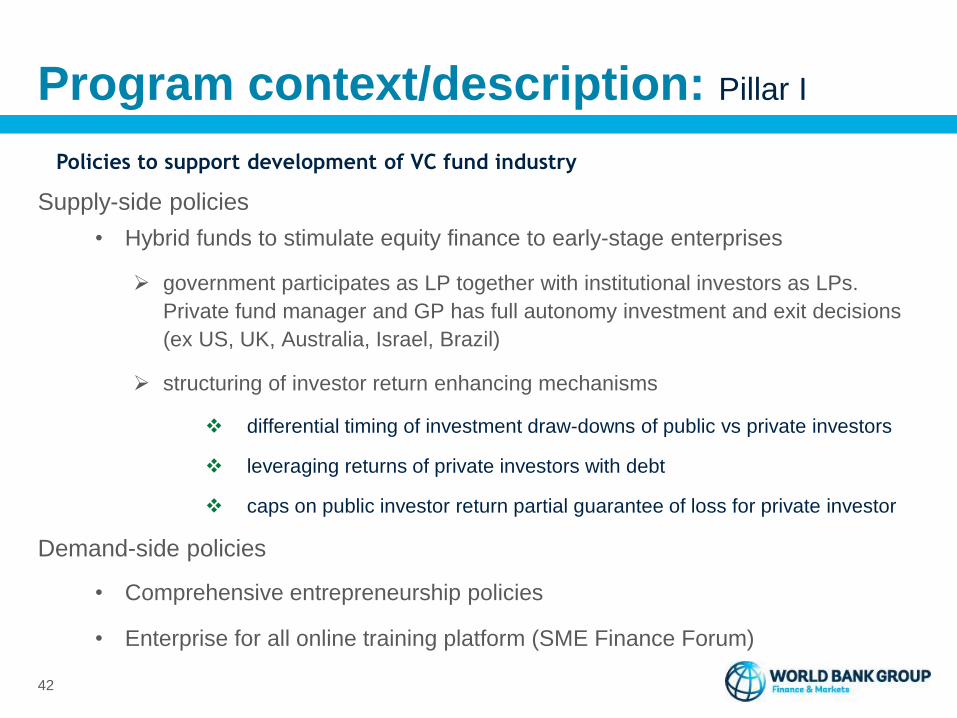

Supply-side policies

• Hybrid funds to stimulate equity finance to early-stage enterprises

government participates as LP together with institutional investors as LPs.

Private fund manager and GP has full autonomy investment and exit decisions

(ex US, UK, Australia, Israel, Brazil)

structuring of investor return enhancing mechanisms

differential timing of investment draw-downs of public vs private investors

leveraging returns of private investors with debt

caps on public investor return partial guarantee of loss for private investor

Demand-side policies

• Comprehensive entrepreneurship policies

• Enterprise for all online training platform (SME Finance Forum)

42

Policies to support development of VC fund industry

Program context/description: Pillar II

43

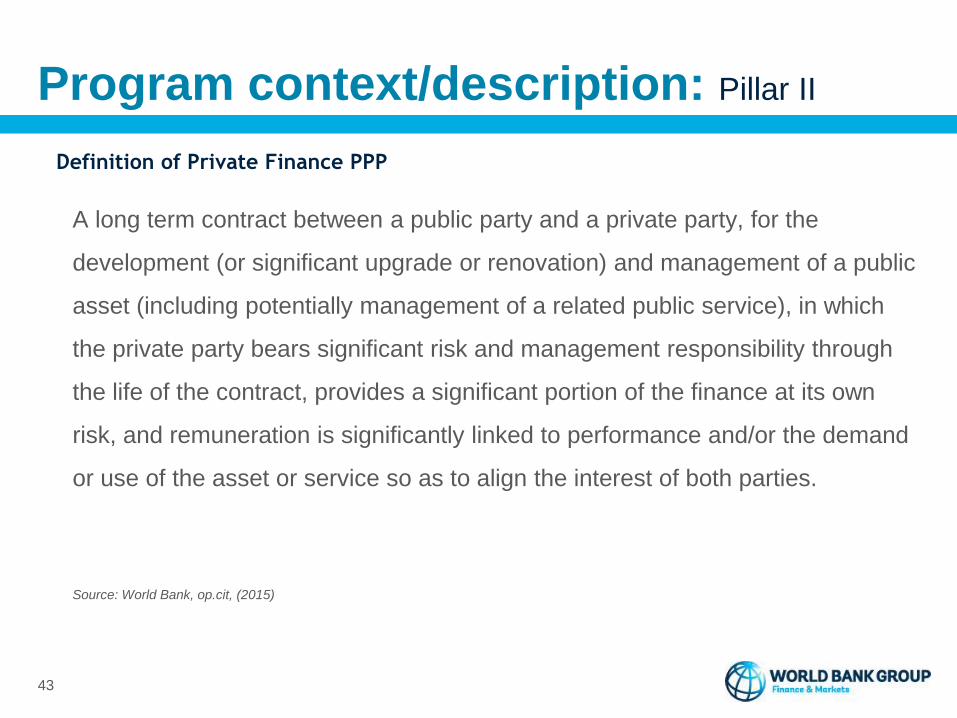

Definition of Private Finance PPP

A long term contract between a public party and a private party, for the

development (or significant upgrade or renovation) and management of a public

asset (including potentially management of a related public service), in which

the private party bears significant risk and management responsibility through

the life of the contract, provides a significant portion of the finance at its own

risk, and remuneration is significantly linked to performance and/or the demand

or use of the asset or service so as to align the interest of both parties.

Source: World Bank, op.cit, (2015)

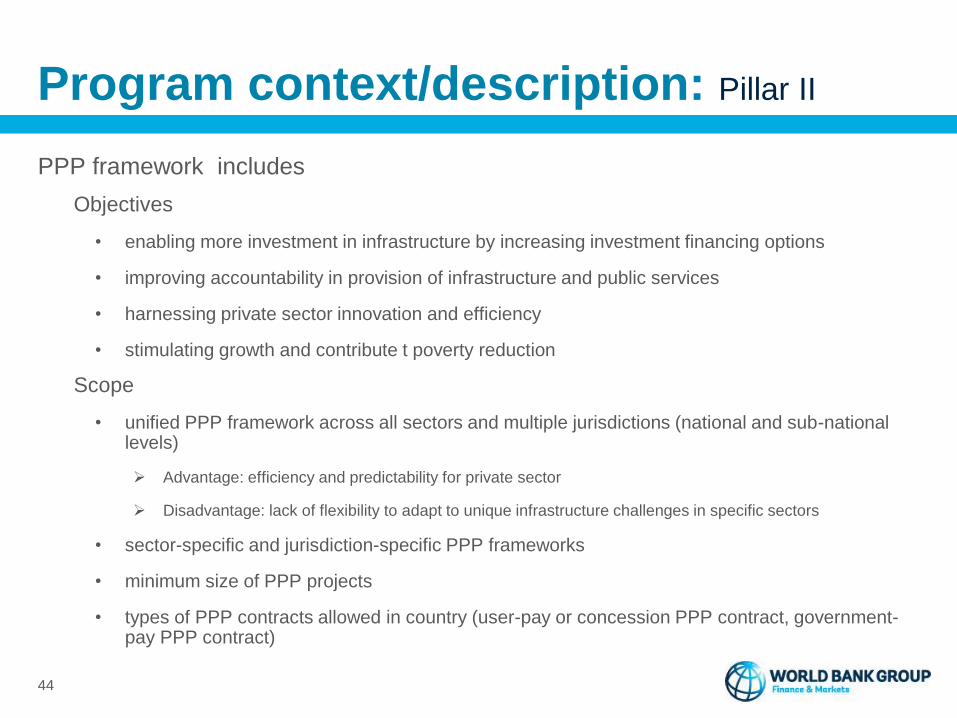

Program context/description: Pillar II

44

PPP framework includes

Objectives

• enabling more investment in infrastructure by increasing investment financing options

• improving accountability in provision of infrastructure and public services

• harnessing private sector innovation and efficiency

• stimulating growth and contribute t poverty reduction

Scope

• unified PPP framework across all sectors and multiple jurisdictions (national and sub-national levels)

Advantage: efficiency and predictability for private sector

Disadvantage: lack of flexibility to adapt to unique infrastructure challenges in specific sectors

• sector-specific and jurisdiction-specific PPP frameworks

• minimum size of PPP projects

• types of PPP contracts allowed in country (user-pay or concession PPP contract, government-pay PPP contract)

Program context/description: Pillar II

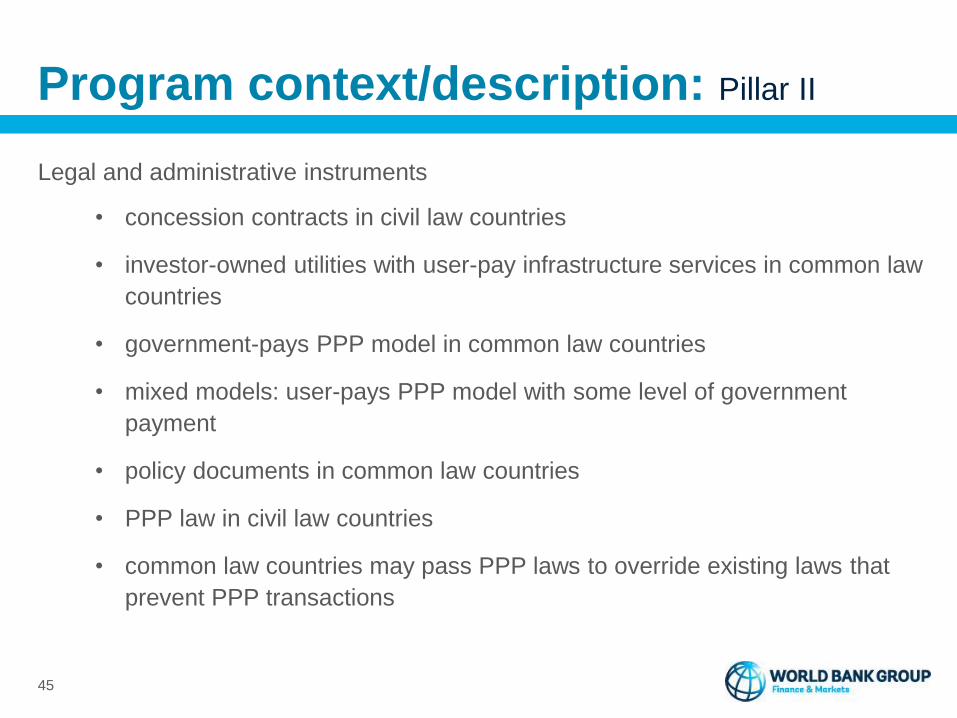

45

Legal and administrative instruments

• concession contracts in civil law countries

• investor-owned utilities with user-pay infrastructure services in common law

countries

• government-pays PPP model in common law countries

• mixed models: user-pays PPP model with some level of government

payment

• policy documents in common law countries

• PPP law in civil law countries

• common law countries may pass PPP laws to override existing laws that

prevent PPP transactions

Program context/description: Pillar II

46

PPP framework procedures and decision criteria

Project identification and preparation• Scoping of projects in the public investment program (central government and

sub-national entities) and SOE investment program for PPP suitability;

• Confirmation of fit with sectoral strategies

• Confirmation of fiscal responsibility

• Submission of project documentation for approval by relevant agencies

Project appraisal• Preparation of PPP business case incl economic, financial, fiscal, technical ESG

and legal feasibility

• Submission of project documentation for approval by relevant agencies

Program context/description: Pillar II

47

PPP framework procedures and decision criteria (cont.)

Structuring of procurement process and project contract• Preparation of risk matrix and allocation of risks• Development of risk management plans• Drafting of contracts• Submission of contracts for approval by relevant agencies• Development of procurement strategy• Submission of procurement strategy for approval by relevant procurement agency

Project tender and award• Marketing of PPP• Undertaking OI• Shortlisting of qualifying firms• Development of criteria for proposals• Selection of proposals based on VFM criterion• Reaching financial close and sign contract

Source: World Bank, op.cit. 2015

Program context/description: Pillar II

48

Cost of preparation of PPP projects is substantial: share of preparation cost in total

project cost varies from 2-3 % in middle-income countries and experience low-income

countries to5%-10% in new sectors in low-income countries

Source: Fay, op.cit. 2011

Program context/description: Pillar II

49

• Cost of preparation may act as binding constraint for development of PPP

transactions in many EMDES

• EMDE governments considering establishing infrastructure PPP venture funds

together with private institutional investors including private equity infrastructure

funds

funds responsible for managing all stages of preparation of PPP

transactions up to financial close

funds take equity and/or mezzanine stake in PPP project SPV

possible compartment of SIF

Program context/description: Pillar II

50

PPP framework needs to integrate procedures for management of unsolicited

proposals (USP)

• inclusion of USP in best and final offer round under two-stage bid

processes

• developer fee paid by government or winning bidder

• bid bonus for USP (Chile)

• USP has option to match winning bid and win contract (Swiss

challenge)

Program context/description: Pillar II

51

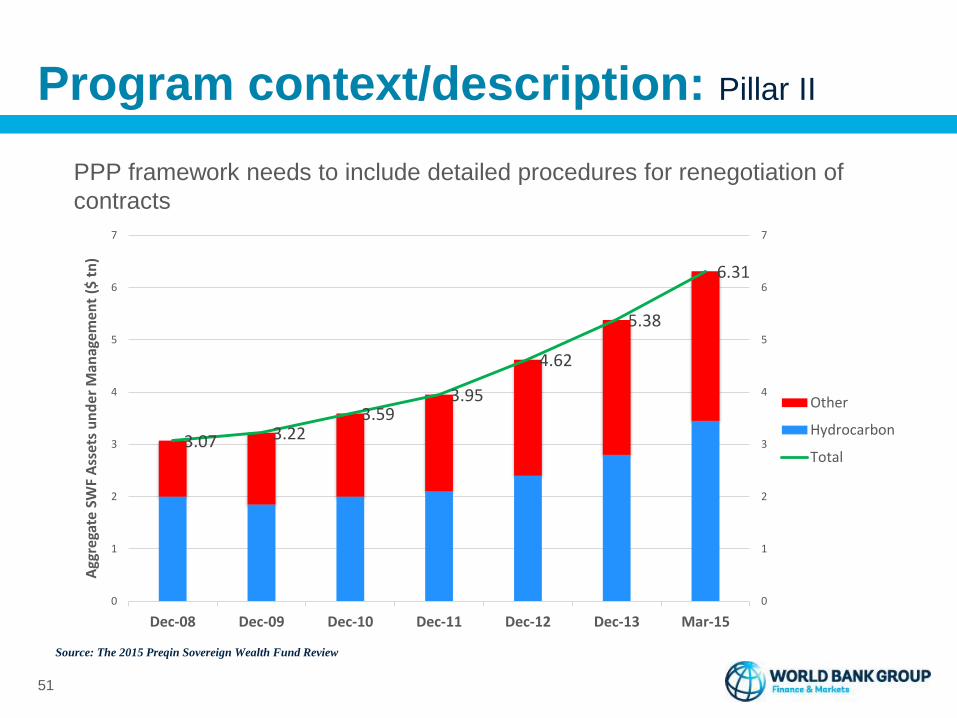

PPP framework needs to include detailed procedures for renegotiation of

contracts

3.07 3.223.59

3.95

4.62

5.38

6.31

0

1

2

3

4

5

6

7

0

1

2

3

4

5

6

7

Dec-08 Dec-09 Dec-10 Dec-11 Dec-12 Dec-13 Mar-15

Agg

rega

te S

WF

Ass

ets

un

der

Man

agem

ent

($ t

n)

Other

Hydrocarbon

Total

Source: The 2015 Preqin Sovereign Wealth Fund Review

Program context/description: Pillar III

52

Rationale for developing domestic investment component of SWFs

• Permanent income hypothesis-> countries should save enough of

revenues from non-renewable resources abroad to maintain

permanent income flow for indefinite future

• Dynamic stochastic general equilibrium (DSGE) model -> if returns

are higher at home than abroad, or if future generations can be

expected to be wealthier than current one, it may be optimal to save

less abroad and invest more at home now

Program context/description: Pillar III

53

• A number of SWFs have been established since the beginning of the 2000s with

the objective to undertake domestic investments in key sectors of the economy:

several SWFs in the Gulf, Samruk-Kazyna in Kazakhstand, Kazanah in Malaysia

• In the last four years, Nigeria and Angola have joined funds with domestic

investment function

• SWFs with a domestic investment function are being discussed in several

countries including Bangladesh, Kenya, Myanmar, Mongolia, Mozambique,

Sierra Leone, Tanzania, and Uganda, to be capitalized from revenues of oil and

mineral exports

Program context/description: Pillar III

54

• In parallel with increased allocation by oil or mineral-based SWFs to domestic

investment, a growing number of EMDEs are establishing Strategic Investment

Funds (SIFs) funded through fiscal surpluses, asset transfers and/or borrowing

• SIFs objective: to act as anchor investor for international and domestic

institutional investors, including private equity and debt funds, in domestic

projects, in particular for PPP infrastructure projects and SME funds

Program context/description: Pillar III

55

Challenges specific to SWFs

• SWFs are capitalized by inflows of foreign exchange from oil and mineral sales

• Key macroeconomic challenges:

exchange rate appreciation (Dutch disease)

macroeconomic volatility

• Need for coordination with overall monetary and fiscal policy

• Need for optimizing allocation of natural resource surpluses between foreign

savings and domestic investment

Program context/description: Pillar III

Legal and regulatory environment

• Legal and regulatory framework for private equity and debt funds operations (see above)

• Legal and regulatory framework for inward investment and outward repatriation of distributions and dividends

• Double taxation treaties (DTAs)

Governance structure

• clear separation between fund ownership and fund management functions

• investments through regulated investment equity and debt funds (infrastructure, SMEs)

• co-investments with private investors

• investments subject to double IRR/ERR trigger

• professional staff remunerated at market rates

• disclosure and reporting rules

56

Challenges common to domestic investment component of SWFs and SIFs

Program activities

57

• Manage a global focus point for investment professionals in the SWF/SIF and PE/VC space, through the Investment Funds CoP and its two open online platforms. Co-hosts for the two open platforms are, respectively, The Fletcher Network for Sovereign Wealth and Global Capital at Tufts University (SWF C4D platform), and the Emerging Markets Private Equity Association (EMPEA (PE/VC C4D platform).

• Jointly with TRE, manage the Sovereign Wealth Funds Secretariat, which functions as an internal one-stop shop for CMUs requiring support for SWF activities through the cross-GP Sovereign Wealth Fund Advisory Group.

• Developing global knowledge to directly support operations in the evolving field of SWF’s domestic investments, SIFs, and PE/VC funds, in particular:

Global review of SIFs

Guidelines for the design of SIFs

• Partnering with the International Forum of Sovereign Wealth Funds (ISWF) to further develop the Santiago Principles to include principles for domestic investment.

• In partnership with the GFDRR/DRFI Program and SURRGP, carry out a feasibility study for the establishment of a Global Infrastructure Resilience Fund (GRIF), with the objective of increasing commercial investment in climate resilient infrastructure and SMEs

Global engagements

Program activities

58

Global engagements

Engagement Partnerships Status LSI SDG

Investment Funds CoP EMPEA, Tufts University C - SDG8, SDG9

SWF Secretariat TRE C - SDG8, SDG9

Global review of SIFs PPIAF P - SDG8, SDG9

SIF design guidelines PPIAF P - SDG8, SDG9

Santiago principles for domestic

investments by SWFs

IFSWF P - SDG8, SDG9

GRIF GFDRR/DRFI

SURRGP

P GRIF TA and

financing

operation

SDG 8, SDG9,

SDG13

Program activities

59

At the sub-regional and country levels, the Investment Funds Group

team supports Regional FM GP and TC GP teams on three business

lines: (i) development of PE/VC ecosystems; (ii) development of SWFs

in LICs; and (iii) development of SIFs in low and middle-income

countries. In each business line, ongoing and planned country

engagements are selected on the basis of four fundamental criteria:

• Sub-regional/country demand through CMU

• Partnership across WBG (IFC, TRE, GPs, CCSAs)

• Partnership outside WBG (RAS, MDTFs, Multilateral TFs, Bilateral TFs,

etc..)

• Line of sight instrument (LSI) towards relevant SDG(s)

Sub-regional and country engagements

Program activities

60

Sub-regional and country engagements

Country Engagement Partnerships Stat LSI SDG

Croatia Innovation/VC Project EU TF C Innovation/VC Project 8

West Balkans PE/VC Development

Program

EU TF C PE/VC Development Program 8

Morocco Seed/VC Development

Project

IFC Funds Group C Seed/VC Development Project 8

Turkey PE/VC Market Analysis SIDA (CM deep

dive)

C SIF Project (TBD) 8,9,13

Bangladesh Prog. Approach

PE/VC Ecosystem Analysis

FIRST/ IFC SME

Ventures

C IPPF2 Project (P) 8,9,13

Ghana PE/VC Ecosystem

Analysis

C Fin Sector Development Project

(TBD)

8

Jamaica PE/VC Market Development

Program

IDB P Financial Inclusion Project (P) 8

DRC PE/VC Market Analysis FIRST/IFC SME

Ventures

P SIF Project (TBD) 8,9,13

Program activities

61

Sub-regional and country engagements

Country Engagement Partnerships Stat LSI SDG

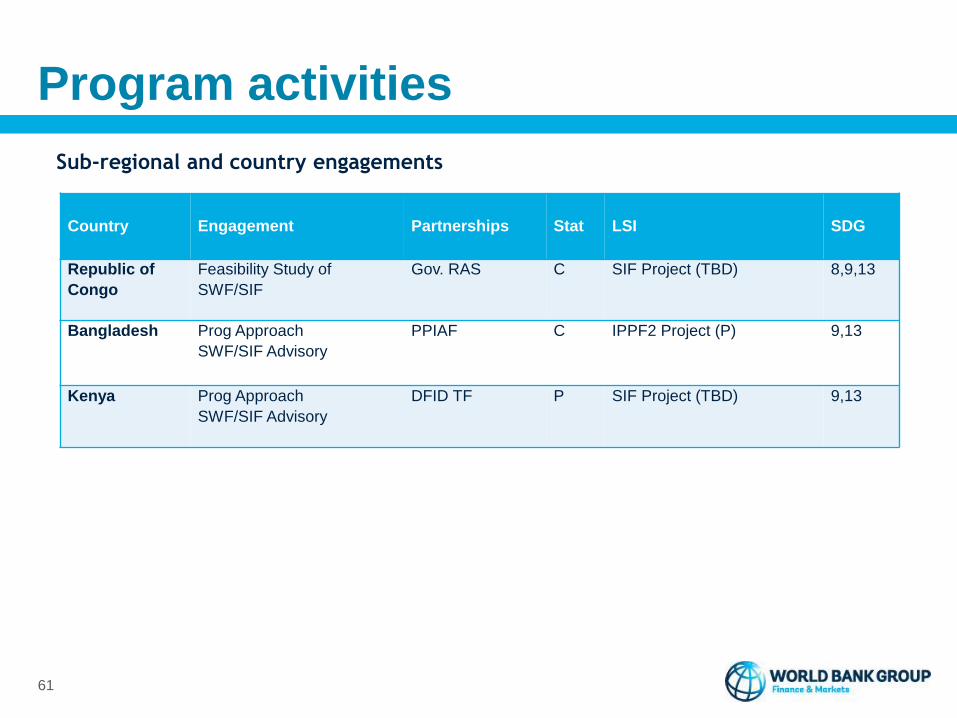

Republic of

Congo

Feasibility Study of

SWF/SIF

Gov. RAS C SIF Project (TBD) 8,9,13

Bangladesh Prog Approach

SWF/SIF Advisory

PPIAF C IPPF2 Project (P) 9,13

Kenya Prog Approach

SWF/SIF Advisory

DFID TF P SIF Project (TBD) 9,13

Program activities

62

Sub-regional and country engagements

Country Engagement Partnerships Stat LSI SDG

Caribbean Caribbean Diaspora

Initiative/Fund

CDB/DFID (P) C Carib Regional PPP Infra

Fund (TBD)

Carib SME Co-investment

Facility (TBD)

8,9,13

Morocco Morocco Investment Authority Gov RAS

(pilot)

C NA 8,9,13

Sénégal Support to Fund for Strategic

Investments (FONSIS)

PPIAF/FIRST C FONSIS Financing Project

(TBD)

8,9,13

Cameroon Support to SIF PPIAF P SIF Financing Project (TBD) 8,9,13

Côte d’Ivoire Support to Infra PPP Venture

Fund (I4PVF)

PPIAF P I4PVF Financing Project

(TBD)

8,19,13

Gabon Support to SIF PPIAF P SIF Financing Project (TBD) 8,9,13

Program risks

The key risk to the program is rapidly growing demand for advisory and project support in the investment funds space vs small size of core Investment Fund Group (IFG) team in Fin4Dev.

To mitigate this risk, the team is taking the following measures:

• Strengthen the core IFG team through partnerships with senior staff from

Governance GP (DA assignment) and Energy and Extractives GP (cross-support)

• Assign country engagement TTLship to Regional FMGP and TCGP colleagues and

retain TL and/or co-TTL role only in core IFG team

• Build cross-Group, cross-Practice and cross-CCSA task teams based on

engagement technical and operational scope in particular with IFC Funds Group/SME

Ventures, TRE, TCGP, SURRGP, Governance GP, Energy and Extractives GP, CC

CCSA and PPP CCSA

• Build strong cadre of senior consultant experts in PE/VC, SWF and SIF spaces to

contribute to specific advisory and operational engagements

63

Roles of clients and partners

At the global level, critical partnerships are:

• The Public-Private Infrastructure Advisory Facility (PPIAF), as multi-donor

forum for building ownership and for supporting the preparation of the global

review of SIFs and the preparation of guidelines for the design of SIFs.

• The International Forum of Sovereign Wealth Funds (ISWF), as

international standard setter for SWFs governance (Santiago Principles)

• The Emerging Markets Private Equity Association (EMPEA), as co-manager

of the PE/VC C4D platform

• The Fletcher Network for Sovereign Wealth and Global Capital (FNSWGC),

as co-manager of the SWF C4D platform

64

Roles of clients and partners

At the sub-regional and country level, critical partnerships are:

• The Global Fund for Disaster Reduction and Recovery (GFDRR), as multi-donor forum for

building ownership and funding mobilization for GRIF;

• The Public-Private Infrastructure Advisory Facility (PPIAF), as multi-donor forum for

building ownership and funding mobilization for the SIF business line

• The FIRST Initiative, as multi-donor forum for building ownership and funding mobilization

for the development of PE/VC legal and regulatory frameworks and reforms under the

PE/VC business line

• The European Union Commission, as partner and donor for PE/VC development programs

in EU candidate countries and in EU Eastern Partnership countries

• The UK Department for International Development (DFID), as partner and donor for the

proposed Caribbean Regional Infrastructure PPP Finance Fund (CRIP3F) and for the

Kenya SWF/SIF advisory

• The Caribbean Development Bank (CDB), as partner in the proposed CRIP3F and in the

proposed regional diaspora co-investment facility

65

Dissemination and outreach strategy

• The core of the dissemination and outreach strategy for the investment

fund for development program is the Investment Funds for Development

Community of Practice (CoP), and its two dedicated C4D platforms co-

managed and open to outside stakeholders in the investment funds

space (see Section IV.2.1 above).

• In addition, the IFG core team and regional engagement task team

leaders and team members will participate actively through speaking and

panel engagements in selected international forums and conferences, in

particular the IFSWF Annual Meeting, the EMPEA/IFC Annual

Conference, and the Fletcher Network Annual Infrastructure Forum.

66

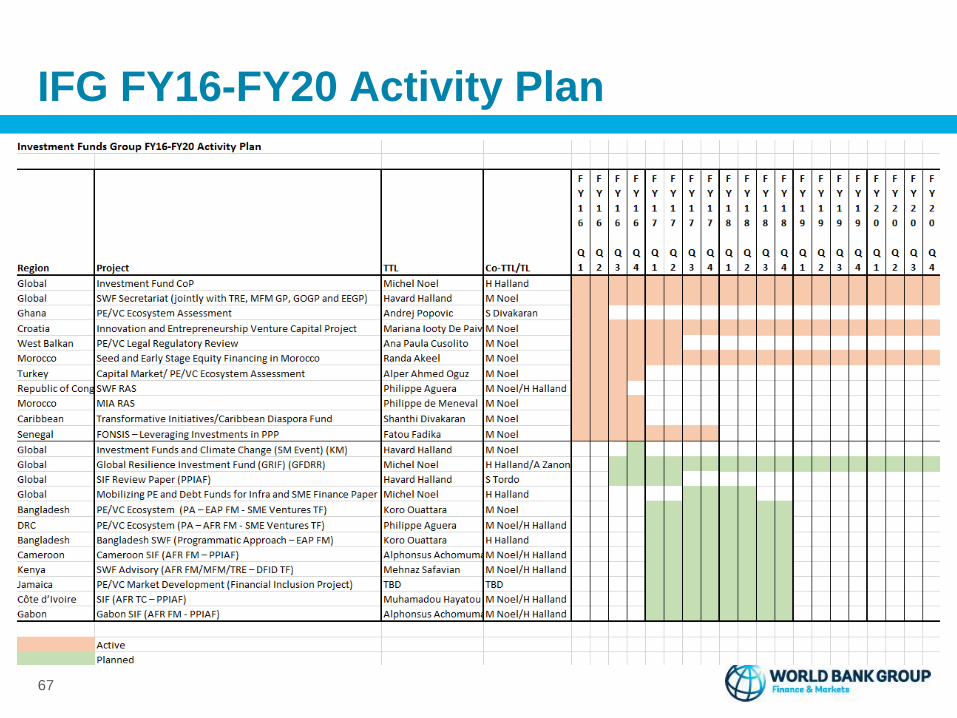

IFG FY16-FY20 Activity Plan

67

Investment Funds Group Team

68

Contact information:

Michel Noel

202-203-0874

Samuel Schneider

Consultant

Patrick J. McGinnis

Consultant

Sevara Atamuratova

Research Analyst

Shanthi Divakaran

Sr. Financial Sector Specialist

Michel Noel

Head

Thelma Ayamel

Program Assistant

Havard Halland

Sr. Economist

Honglin (Holly) Li

Learning Analyst

Jacob Owens

Consultant

![[PPT]PowerPoint Presentationc.ymcdn.com/.../Dublin_Presentation_1_-_B_M.pptx · Web viewSources: Euromonitor International, IMF, Asia Private Equity Review, EMPEA, EVCA and PitchBook.](https://static.fdocuments.us/doc/165x107/5b2684ad7f8b9a53228b4672/pptpowerpoint-web-viewsources-euromonitor-international-imf-asia-private.jpg)