Investment Climate in Kerala - IBEF · A good investment climate provides ... † Governance and...

26

www.ibef.org Investment Climate in Kerala

Transcript of Investment Climate in Kerala - IBEF · A good investment climate provides ... † Governance and...

������������

Investment Climate in

Kerala

������������

KERALA PAGE 3

Table of Contents

Executive Summary .................................................................................................................. 4

Kerala - Select Indicators ........................................................................................................ 5

Economic Overview of the State .......................................................................................... 6

Kerala’s economic performance ............................................................................................ 6

People - Economic prosperity .............................................................................................. 6

Industrial performance ............................................................................................................. 7

Investments................................................................................................................................. 7

Kerala’s contribution in India’s exports ................................................................................ 8

Labour Force .............................................................................................................................. 9

Infrastructure .........................................................................................................................10

Industrial infrastructure .........................................................................................................10

Educational Infrastructure .....................................................................................................12

Physical Infrastructure ............................................................................................................12

Key Nodal Agencies ................................................................................................................15

Policy Framework ...................................................................................................................16

Key industries and players in Kerala ...................................................................................18

Handloom and Powerloom Industry ..................................................................................19

Sericulture ................................................................................................................................19

Mining ........................................................................................................................................20

Tourism ......................................................................................................................................20

Food Processing Industry ......................................................................................................21

Electronics ................................................................................................................................21

Information Technology .........................................................................................................21

Doing Business in Kerala .......................................................................................................23

Contact Information ...............................................................................................................24

Appendix ...................................................................................................................................24

A report by ICRA for IBEF

‘Investment climate’ is a broad concept, encompassing all the factors affecting business decisions, including profi tability and where to locate plants and other units. A good investment climate provides opportunities and incentives for fi rms to invest productively and create jobs, thus playing a key role in ensuring sustained growth and poverty reduction.

Factors infl uencing investment climate include: • Availability and ease of use of factor inputs such as land and

labour;• Availability of adequate physical and social infrastructure,

such as power, telecom, urban infrastructure, water supply, hospitals, and educational institutions;

• Governance and regulatory framework in terms of rules and regulations governing entry, operation, and exit of fi rms, sta-bility in regulation, integrity of public services, law and order and investment facilitation; and

• Provision of incentives and access to credit.

Kerala is a very popular tourist destination in the world and is known as one of the ’10 paradises on Earth’ for its natural beauty, greenery, tranquility and rich cultural heritage. A combi-nation of picturesque sceneries, friendly people and rich culture make Kerala an ideal holiday destination for people looking for a spectacular mix of beauty, tradition and history.

Agriculture and fi shing continue to be the dominant source of livelihood in the state. Kerala is the largest producer of coconut, rubber, coir and pepper. The state is also the leading producer of a variety of spices, cashew, coffee and tea. Besides agriculture and fi shing, the services sector also plays a major role in Kerala’s economy. The growth in tourism and IT has enabled the services

sector to record a compound annual growth rate (CAGR) of 12 per cent since 1999-00.

Kerala is a leading state in terms of infrastructure penetration. It has the highest per capita density of roadways in the country, three international airports, a large port at Kochi, three interme-diate ports and 17 small ports. It is one of the only two Indian states to have two submarine cable landings. The Kerala State Industrial Development Corporation Ltd acts as a nodal agency for foreign and domestic investments in Kerala, providing com-prehensive support for investors.

The state ranks high on social, educational and health indica-tors. It has the highest literacy rate in the country at 90.9 per cent and sex ratio of 1,058 women per 1,000 men. Low infant mortality rate and high life expectancy are positive health indica-tors in the state. The state has the highest density of science and technology personnel in India.

Kerala is strongly engaged in nurturing its manufacturing sector and has proposed measures to help businesses seek technology upgradation and process improvements. The IT policy seeks to establish Kerala as a global IT services hub. Several steps have been proposed by the state government to improve labour relations and make governance streamlined, transparent and investor-friendly. The excellent infrastructure facilities, policy framework and the availability of skilled manpower have en-hanced the state’s reputation as an IT/ ITES destination. There are several opportunities in the biotech sector that are yet to be utilised. In order to promote the core competence sectors of Kerala, dedicated sector-specifi c industrial parks are being set up across the state.

Executive Summary

Regulatory Framework

Investment Climate of a State

Resources/InputPhysical &

Social Infrastructure

Incentives to Industry

KERALA PAGE 5

Industrial Area Boards have also been set up in various indus-trial areas of the state for clearance of the projects. An offi cer not below the rank of district collector is the chairman of each

board, while the Designated Authority of the industrial area is the convenor.

IndustryKey industries Coir, agro-based, textiles, seafood, chemicals, IT/ ITES, tourism

Capital Thiruvananthapuram

Land and ClimateGeographical Area (sq km)

38,863

Climate Winter (December to February)Summer (February to May)South West Monsoon (May to June) North East Monsoon (October to December)

Average Rainfall in 2004 (in mm)

2900

Number of districts 14

Number of taluks (as per 2001 Census)

63

Number of revenue divisions (as per 2001 Census)

21

Number of rural blocks (as per 2001 Census)

152

Number of villages (as per 2001 Census)

1467

People

Main religion Hinduism, Islam, Christianity

State Language Malayalam

Population (in million) (2001-Census)

31.8

Share of urban population 25.97%

State’s share in India’s population

3.1%

Population density (per sq km)

819

Growth in population be-tween 1991 and 2001

9.42%

Sex ratio (females per 1000 males)

1058

Literacy rate 90.9%

Birth rate (per thousand persons)

15.2

Death rate (per thousand persons)

6.1

Infant mortality rate (per thousand live births)

12

Human Development Index All India ranked one

(Source: UNDP Human Development Report 2004)

Key Industries in Kerala

Handlooms and Power looms

Rubber

Bamboo

Coir

Khadi and Village

Sericulture

Seafood and other marine products

Cashew

Beedi

Mining

Tourism

Food Processing

Spices and Spice extracts

The state of Kerala covers an area of 38,863 sq km (1.18 per cent of India’s landmass) and is identifi ed as one of the world’s 25 biodiversity hotspots. It has a 580-km-long coastline. Geo-graphically, Kerala can be divided into three climatically distinct regions: the eastern highlands (rugged and cool mountainous terrain), the central midlands (rolling hills), and the western lowlands (coastal plains).

With a gross domestic product of $26.4 billion, Kerala is among the well-performing states in India and holds an important posi-tion on the industrial front. The state’s share in India’s popula-tion is 3.1 per cent, while it contributes 2.6 per cent to the workforce. Between January 1999 and December 2005, Foreign Direct Investment (FDI) approved in the state was $270.4 mil-lion in 184 projects, which constituted 1.26 per cent of the total FDI approvals in the country.

About 50 per cent of the population depends on agriculture, characterized predominantly by cash crops. Kerala is a major producer of coconut, rubber, pepper, cardamom, ginger, banana, cocoa, cashew, arecanut, coffee and tea. Spices like nutmeg, cinna-mon and cloves are also cultivated. Rice and tapioca are impor-tant food crops. On a national scale, 92 per cent of the rubber, 70 per cent of coconut, 60 per cent of tapioca and almost 100 per cent of lemon grass oil is produced from the state. Agri-culture in Kerala has the distinction of having the highest gross income per net cropped area.

Kerala’s economic performance

The gross state domestic product (GSDP) of Kerala stood at $26.44 billion in 2005-06, with an impressive CAGR of 10.25 per cent from 1999-00 onwards, when GSDP stood at $14.72 bil-lion. This growth has been driven by all three sectors – primary (comprising agriculture and livestock, forestry and logging, fi sh-ing, mining and quarrying), secondary (comprising manufacturing, construction and electricity, gas and water supply) and tertiary (comprising trade, hotels and restaurants, transport, storage and communication, fi nancial services, real estate and related services, public administration and other services). The tertiary sector, in particular, has shown signifi cant increase in contribu-tion over the years.

Within the primary sector, mining and quarrying registered a growth rate of 12.7 per cent in 2005-06 over the previous year, followed by agriculture and allied activities, which registered a growth of nine per cent in 2005-06. The secondary sector is dominated by manufacturing, in particular food processing, chemicals and fertiliser and construction. Construction regis-tered the highest growth of 17 per cent in 2005-06 within the

secondary sector.

In the tertiary sector, travel and tourism is an important eco-nomic driver. It contributes 13 per cent to the GSDP and grew at 14.5 per cent in 2005-06.

People - Economic prosperity

The per capita income in Kerala is amongst the highest in the country. Having grown from $416.3 in 1999-00 to $618.9 in 2004-05, it is higher than the all-India per capita income of $514.2. The percentage of population in Kerala below the poverty line was 3.6 in 2004-05, as compared to the all-India percentage of 19.34.

Economic Overview of the State

2800

Source: Economic Survey of Kerala, 2005-06

Kerala’s GSDP (US$ billion)

0 400 800 1200 1600 2000 32002400

CAGR10.25%

14721999-00

14942000-01

16112001-02

21972003-04

23682004-05

18922002-03

26442005-06

1999-00

2005-06

Percentage distribution of GSDP

n Primary Sector n Secondary Sector n Tertiary Sector

Source: Economic Survey of Kerala, 2005-06

24.9% 21.2%

7.32% 10.07

53.9%

15.6% 61.0%23.4%

13.78%CAGR

0 5 10 15 20 25 30 35 40 45 50 55

Distribution of Households by Income (%)

Source: The Market Skyline of India 2006 by Indicus Analytics

n Kerala n India

Urban

>US$ 6667

US$ 3331-6667

US$ 1668-3330

<US$ 1667 12.1

13.726.1

50.439

29.622.7

6.4

KERALA PAGE 7

The annual income of households is also an important indicator of the economic prosperity of people in the state. A compari-son of distribution of households by various income categories in Kerala vis-à-vis the all-India fi gures shows that the share of households in higher income categories in Kerala is more. This holds true for urban as well as rural households. For example, 29.6 per cent of Kerala’s urban households and 14.1 per cent of rural households, fi gure in the highest income category of $6,667 and above, as compared to only 22.7 per cent and 4.6 per cent, respectively, for all-India. Likewise, 50.4 per cent of Kerala’s urban households fi gure in the income category of $3,331-6,667, as compared to 39.0 per cent of all-India urban households. In rural areas, 53.0 per cent of Kerala’s households fi gure in this income category, as compared to only 16.8 per cent of all-India rural households.

Another factor that points towards the economic well-being of the people is the ownership of physical assets like vehicles and consumer electronics. Assets like four-wheelers, two-wheelers and television sets are indicators of consumer aspirations. A comparison of asset ownership by households indicates a higher ownership of these assets in Kerala vis-à-vis all-India, except in

the case of two-wheelers. For example, fi ve per cent of Kerala’s households own a four-wheeler as compared to the all-India percentage of four. Similarly, 51 per cent of Kerala’s households own a television, as against an all-India fi gure of 41 per cent.

Industrial performance

The state has signifi cant industrial potential because of good infrastructure facilities like power, transport system, airports, ports and availability of rare minerals. Traditional industries are handlooms, cashew, coir and handicrafts. Other important indus-tries are rubber, tea, ceramics, electric and electronic appliances, telephone cables, transformers, bricks and tiles, drugs and chemi-cals, general engineering, plywood splints and veneers, beedi and cigar, soaps, oils, fertiliser and khadi and village industry prod-ucts. A number of manufacturing units have also come up for production of precision instruments, machine tools, petroleum and petroleum products, paints, pulp paper, newsprint, glass and non-ferrous metals.

There are 727 large and medium industrial undertakings in Kerala. Out of these, 590 units are in the private sector. The small-scale sector contributes to 40 per cent of industrial pro-duction and 35 per cent of exports from the state. There were 193,302 SSI units, with an investment of $1.3 billion and provid-ing employment of 710,508 persons, towards the end of March 2006.

Sector-specifi c clusters of industrial units are being promoted with the assistance of fi nancial institutions and skill development facilitated through common facility centres and training institu-tions. The state government has short-listed a few thrust sectors where intensive cluster development will be focused during the initial phase. Sixty clusters have been identifi ed, of which 32 have been developed and approved under the Cluster Development Programme.

Investments

The state leads in attracting investment in the country. Accord-ing to estimates by the Centre for Monitoring Indian Economy (CMIE), as of the quarter-ended June 2007, outstanding in-vestment was $19.4 billion. The state reported a total of 332 projects, out of which 207 were under implementation at the end of the quarter-ended June 2007. The services sector at-tracted the highest investment at $9.9 billion, up by 6.8 per cent as compared to the April-June quarter of 2006. The manufactur-ing sector was the next highest, with 61 outstanding projects amounting to $5 billion. Out of this, 19 projects were under implementation.

Four-wheelers

Source: The Market Skyline of India 2006 by Indicus Analytics

2%

4%All- India

Percentage of households with

0 1 2 3 4 5 6

Kerala

Two-wheelers

Source: The Market Skyline of India 2006 by Indicus Analytics

17%

18%All- India

Percentage of households with

0 2 4 6 8 10 12 14 16 18

Kerala

Television

Source: The Market Skyline of India 2006 by Indicus Analytics

51%

41%All- India

Percentage of households with

Kerala

0 10 20 30 40 50 60

The Karikayam Hydel Project under Ayyappa Hydro Power Ltd was the largest project announced during the quarter in terms of cost. The other important projects taken up were the Rubber Processing Project in Kochi under Kerala State Co-operative Marketing Federation and an Air Cargo Complex Project in Ko-zhikode, announced by the Kerala State Industrial Development Corporation. The High-tech City project, undertaken by Sobha Developers, the Titanium Sponge Manufacturing Facility Project and the Kannur Airport Project are some other notable projects.

FDI of $279.4 million relating to 184 projects – which consti-tutes 1.26 per cent of the total FDI approved in India - was approved in Kerala, between January 1999 and December 2005.

Some major upcoming investments in the state are as follows:

• Worbus Capital Resource, a global marketing consultancy, intends to bring about $180 million worth of investments in gross transaction volume in varied sectors such as software, knowledge process outsourcing and electronics industry.

• US Software, a provider of end-to-end IT services for Fortune 500 companies, has charted a mega expansion plan by building a huge campus adjacent to the Technopark. The campus, to be spread across 36 acres, would house 12,000 employees.

• Infosys Technologies Ltd plans to invest $73 million to set up a campus in Thiruvananthapuram. The development centre would have a seating capacity of 8,000.

• Steel and Industrial Forgings Ltd has planned the expansion and modernisation of its unit at Athani near Thrissur with an estimated investment of $3.2 million. According to the com-pany, after completion of the expansion, the unit’s capacity will go up from 5,040 tonnes to 6,640 tonnes, and produc-tion from 2,922 tonnes to 4,522 tonnes.

• Hindustan Paper Corporation Ltd, a state-owned company, is planning capacity expansion and upgradation of its units in Assam and Kerala. The project is expected to be completed by 2009. It has earmarked $171.2 million for expansion in Kerala.

• The Hong Kong-based J. B. Group has expressed interest in developing an IT Park in Kochi. It will cover an area of 7 mil-lion sq ft, of which 5 million sq ft will be for the IT and ITES sectors. The remaining space will be used for residential ac-commodation, hotels and other amenities. According to the group, the proposed park will attract investments of $357.1 million and will create direct and indirect employment for over a million people.

• Kuwait-based KGA Group plans to invest $130 million in three luxury hotels in Kerala.

Kerala’s contribution in India’s exports

There has been a positive growth on the export front, except for coffee, cotton garments and piece goods.

Exports of key products from Kerala

During 2005 06, the volume of exports of marine products from Kerala was 97,311 tonnes, an 18 per cent share of the overall marine products export from India. In 2005-06, Kerala’s share in the country’s coir exports was 93 per cent, cashew kernels 65 per cent, spices 38 per cent, coffee 55 per cent and tea 26 per cent.

Item 2004-05(USD million)

2005-06(USD million)

Marine products 256.2 275.6

Spices 172.4 191.6

Software 143.8 161.3

Coir and coir products 89.6 105.1

Fruits and vegetables 87.4 93.3

Tea 81.9 92.2

Source: Economic Review of Kerala 2005-06

Breakup of investments by sector

Source: CMIE

n Services n Manufacturing n Electricity n Construction

n Irrigation n Mining

55%

19%

14%

10%

1%1%

KERALA PAGE 9

The total value of exports from Kochi port increased from $1.77 billion in 2004-05 to $2.23 billion in 2005-06, an increase of 26 per cent.

Labour Force

As per Census 2001, of the total population of 31.8 million, 10.3 million comprised the workforce, which is 2.6 per cent of India’s total workforce. There are 8.2 million main workers and 2.1 mil-lion marginal workers.

An important feature of the state’s economy, which distinguishes it from the rest of the country, is the net outward migration of labour force particularly to the Gulf countries, and the huge infl ow of remittances. A recent study by the Centre for De-velopment Studies (CDS), Thiruvananthapuram, and the Indian Institute of Management (IIM), Kozhikode, shows that in 2003, remittances from the Gulf was as high as 22 per cent of the state’s net domestic product. Moreover, almost 25 per cent of the male labour force is working in the Gulf. Migration to other countries and to different states within the country is also sub-stantially high.

S. No. Industry Number of Persons Employed as of 2006

1 Agriculture and Allied Industries 83,203

2 Mining and

Quarrying

21,138

3 Manufacturing 213,661

4 Construction 27,356

5 Electricity, Gas, Water & Sanitary

Services

21,490

6 Trade, Restaurants & Hotels 27,462

7 Transport, Storage & Communication

101,644

8 Financing, Insurance, Real Estate & Business Services

82,201

9 Community, Social & Personal Services

523,375

Total 1,101,530

Source: Directorate of Employment and Training

Industrial infrastructure

The industrial infrastructure of Kerala consists of industrial parks, townships, special economic zones (SEZs), industrial es-tates and industrial growth centres (IGCs).

IGCs are a joint industrial infrastructure development project of the Government of India and the Government of Kerala aimed at the development of industrially backward districts. There are four IGCs located at Kannur, Kozhikode, Malappuram and Alap-puzha. A total 1,108.8-acre area of has been acquired for these IGCs, of which 90 acres have already been allocated to industri-alists.

Industrial Parks: The Small Industries Development Corpora-tion (SIDCO) runs 17 major industrial estates throughout the state. Kerala Industrial Infrastructure Development Corporation (KINFRA), the premier industrial infrastructure development agency of the state, has 17 industrial parks in various sectors, with 150 operating units with an annual turnover of $222.2 mil-lion.

KINFRA’s major activities in 2005-06 included:

• Construction of an animation building with 100,000 sq ft to provide studio space for animation companies;

• Expansion of KINFRA International Apparel Park, Thiru-vananthapuram, under the Apparel Parks for Exports Scheme (APES) of the Ministry of Textiles, Government of India;

• Development of an Agro Food Business Incubation Centre in the KINFRA Food Processing Park at Kakkancherry;

• Development of a 50-acre Biotechnology Park at Kala-massery with private sector participation that will have a Technology Incubation Centre, Pilot Plant, and other facilities in built-up modules, in addition to the basic infrastructure facilities;

• Establishment of a Biotechnology Incubation Centre (BTIC) in the Biotechnology Park, Kochi, which would house com-mon equipment and instrument facilities like green house and hardening facilities, tissue culture facilities, analytical and quality control laboratories, extraction facilities for plant-based value added materials and bio informatics and a patent facilitation centre;

• Development of an 85-acre Integrated Infrastructure Devel-opment Centre & Food Processing Park at Enadimanagalam in Adoor, with fi nancial assistance from the Government of India for developing specifi c infrastructure facilities;

• Setting up of a 126-acre Textile Centre at Taliparambu with fi nancial assistance under the Textile Centre Infrastructure Development (TCID) scheme of the Government of India,

for improving infrastructure facilities for textile manufactur-ing and modernising processing technology in the state.

A total of 105 units have commenced production and are functioning in the various industrial parks of KINFRA with an investment of $43.6 million.

TechnoparkThe Technopark at Thiruvananthapuram, a facility with 1.5 million sq ft built-up space, offers reliable power supply and excellent support facilities such as conference rooms and convention centres. Technopark is the fi rst CMM Level 4 ICT Park. It is now acquiring another 100 acres of land at Attipra, Kazhakootam, for further expansion of the campus (Phase III), and 500 acres for the creation of a Knowledge City with private participa-tion (Phase IV). As on 31st March 2006, the Government had invested $26.3 million to build Technopark.

InfoparkThe Infopark at Kochi is an ideal destination for ITES compa-nies due to its proximity to submarine optical cables. It offers regulated power supply, excellent telecom facilities and support functions such as convention centres and seminar halls. The total land available with the Infopark is 96.9 acres. As on 1st Septem-ber 2006, 32 companies had invested $22.4 million in Infopark and accounted for exports of $15.9 million.

Infrastructure in Kerala

KERALA PAGE 11

Projects on the anvil in Kerala

Special Economic Zones

Kochi is the only city in India to have three SEZs. These include the Electronic Park at Kalamassery, Cochin SEZ and a port-based SEZ. Eleven new SEZs have been approved in the state. In nine out of the 11 approved SEZs, the state and central govern-ment agencies are the developers. Of the 11 SEZs, six are IT/ ITES-based SEZs, one each in food processing, biotechnology and electronics and two are port-based SEZs. While the Val-larpadam SEZ consists mainly of the Container Transshipment Terminal and related infrastructure, the Puthuvypeen SEZ will comprise an LNG Terminal. Two SEZs have been approved in principle, for development by Smart City Infrastructure Pvt Ltd and Sutherland Global Services Pvt Ltd.

Apart from these SEZs, Technopark is planning to have two more SEZs on a 240-hectare area. KSIDC is planning to have four SEZs covering a total area of 2,200 hectares. It is also plan-ning to convert three of the existing industrial growth centres at Kozhikode, Kannur and Malappuram into sector-specifi c SEZs.

Project LocationCost

(USD million)Promoter Current Status

Petrochemical Complex Kasargode 1,904.8 GAIL MoU signed. Pre feasibility study completed

NTPC - Expansion Kayamkulam 1,809.5 NTPC Tender for supply of fuel (LNG) completed

Kochi Refi neries Ltd - Expansion

Cochin 619.0 KRL

LNG Terminal Cochin 547.6 PETRONET LNG

Board of Petronet LNG has cleared the proposal. Land allotted by Cochin Port Trust

International Container Trans shipment Terminal

Cochin 504.3 Dubai Port Interna-tional

MoU signed. Clearance obtained from Central Govern-ment

Free trade and ware-housing Zone

Cochin 476.2 Cochin port Trust/ IL&FS/ KSIDC

Feasibility report underway, being prepared by IL&FS

Vizhinjam Container Terminal

Trivandrum 476.2 -N.A- Tendering process is on

Gas pipe line laying Cochin 381.0 GAIL Agreement signed with 14 anchor customers for supply-ing LNG

Smart City Cochin 357.1 Dubai In-ternet City

Discussions with Government underway

Single Buoy Mooring Cochin 171.4 Kochi Re-fi neries Ltd

Tendering process over and fi nalisation of the imple-menter underway

International Ship repair facility.

Cochin 75.0 Cochin Port Trust

Pre feasibility report under preparation

International Bunkering Terminal

CochinPuthuvypeen

47.6 Cochin Port Trust

RFP issued under license system

Italian Fashion City Cochin 35.7 Libertie Group Italy

Mou signed. Concession package to be offered being worked out

International cruise terminal

Cochin 13.1 NA Tender process underway

Source: www.ksidc.org

List of notifi ed SEZs after the SEZ Act came into force, as on 29th August 2007

Educational Infrastructure

The literacy rate in Kerala, at 90.9 per cent as compared to the all-India average of 65.4 per cent, is the highest in India. Kerala’s male literacy rate at 94.2 per cent and female literacy rate at 87.9 per cent, favour comparably with the corresponding na-tional fi gures of 75.85 per cent and 54.16 per cent, respectively.

The state’s expenditure on education increased by 5.7 per cent in 2004-05, and the estimated expenditure in 2005-06 showed an 18.6 per cent increase.

The state’s higher education system comprises seven universities and two deemed universities.

There has been a remarkable increase in the number of engi-neering colleges in Kerala in recent years, especially in the num-ber of private self-fi nancing colleges. Vocational Higher Second-ary Education was introduced to ensure maximum employment opportunities.

Medical & Health care facilities

Kerala is reputed for its high quality health care infrastructure and renowned medical personnel, some of whom are guest faculty at leading medical schools. Kerala enjoys India’s highest life expectancy and lowest infant mortality and birth rates in the country. Facilities for Homoeopathy and Ayurveda are equally

reputed. There are 2,696 government institutions engaged in the three systems of medicine. Kerala has a vast health infrastruc-ture network, including 961 primary health centres and 5,094 sub centres.

The state has entered the third or fi nal phase of demographic transition, characterised by low death rate and declining birth rate leading to a slowdown in the population growth rate. Its health indicators show that the health status is more advanced than the all-India averages and is even comparable with devel-oped countries.

Infrastructure for savings and borrowings

As of 31st March 2007, the banking sector in Kerala had deposits of $21.2 billion and a credit of $13.5 billion. There were 3,553 bank branches, of which 350 were rural, 2,375 were semi-urban and 828 were urban branches. The state reported a credit-deposit ratio of 61.7 per cent in March 2006, up from 55.9 per cent in March 2005.

Physical Infrastructure

TransportKerala’s infrastructure in terms of rail, road and transport net-work is good. Virtually all of its villages are connected by road.

RoadKerala has eight National Highways (NHs), several State High-ways (SHs) and a good network of district roads. It is the fi rst state to have 100 per cent road access to remote villages. The total road length in Kerala in 2005-06 was 160,944 km. Road density in the state was 414 km per 100 sq km, way above the national average of 74.9 km.

Name of the developer

Location Type Area (hectares)

Infopark Kakkanad, Ernakulam

IT/ITES 30.76

Cochin Port Trust Puthuvypeen, Ernakulam District

Port Based 285.84

Cochin Port Trust Vallapadom, Mulavukadu/Fort Kochi Village, Ernakulam District

Port Based 115.25

Electronic Technology Park

Trivandrum IT/ITES 12.55

M/S Electronics Technology Park

Trivandrum IT/ITES 34.5

M/S Kerala Industrial Infrastructure Development Corporation

Trivandrum Animation & Gaming 10.12

KINFRA Kakkancherry, near Calicut

Food Processing 12.52

KINFRA Cochin Electronics Industries

12.14

Source: www.sezindia.nic.in

Kerala All-India

Birth rate* 15.2 24.8

Death rate* 6.1 8.1

Infant Mortality rate** 12.0 63 .0

*Per thousand persons

**Per thousand live births

Life expectancy at birth (years)

Male 71.7 64.1

Female 75.0 65.4

Total Fertility rate (Per woman)

1.99 3.30

Comparison of Health Indicators

Source: Indiabusiness.nic.in

KERALA PAGE 13

Civil AviationKerala has three airports – Thiruvananthapuram, Kochi (Nedum-bassery) and Kozhikode, of which the fi rst two are international airports. While Thiruvananthapuram and Kozhikode airports are owned by the Government of India, the one at Kochi is owned by the Cochin International Airport Ltd. (CIAL), a company set up with public private participation. Traffi c at the three airports has been growing steadily due to increased tourist arrivals as well as travel by a large number of Keralites working in the Gulf and other countries. During 2005-06, 43,394 fl ights (17,839 do-mestic and 25,555 international) were operated from the three airports.

PortsKerala, with a 585-km-long coastline, has a major port at Cochin, three intermediate ports and 14 minor ports. Cochin port is ISO 9001-2000 certifi ed.

Major port projects in Kerala

RailwaysThe state has a good railway network, with the Thiruvanan-thapuram division ranking second in number of passengers and passenger earnings. The division carries 165,000 passengers daily, operating 47 express/ mail trains and 59 passenger trains. The Konkan Railway has enhanced connectivity to Mumbai and Pune. The state has a total railway route of 1,148 km and covers 13 sectors. It has 1,053.86 km of broad gauge lines and 94.14 km of metre gauge lines.

Power

The growth of power sector in Kerala during the last two decades has been remarkable, especially in the area of hydro-power. The state’s power infrastructure consists of 30 power-generating stations, which include 24 hydel, fi ve thermal and one wind. The Kerala State Electricity Board has an installed capacity of 2087.23 MW of its own, with another 570.02 MW contrib-uted by the National Thermal Power Corporation (NTPC) and private sector producers, taking the total installed capacity in the state to 2,657.25 MW.

The Government of India has launched the Rajiv Gandhi Grameen Vidhyuteekaran Yojana (RGGVY) for the electrifi ca-tion of 3,578 habitations in 930 villages covering 14 districts of Kerala. The government has sanctioned $49.3 million to imple-ment the scheme in the fi rst phase, covering seven districts - Kasargod, Kannur, Wayanad, Kozhikode, Malappuram, Idukki, and Palakkad.

In January 2007, total power generation in Kerala was 845.89 million kwh, up from 602.76 million kwh a year ago. Account-ing for 72.2 per cent of the total power generation in the state, hydropower generation totalled 610.73 million kwh. Thermal power generation escalated to 235.16 million kwh in January 2007, from a meagre 5.46 million kwh in the previous year.

Trends in power infrastructure in Kerala

NameCost (In USD million)

Status Location

Kannur Airport Project 221.4 Proposed Moorkhanparambu

Cochin International Airport Project 71.4 Proposed Nedumbassery

Thiruvananthapuram Airport Terminal Bldg. Project

58.6 Proposed Thiruvananthapuram

Kozhikode Airport Project 22.6 Under Implementation

Kozhikode

Nedumbassery-Cochin Airport Expansion Project

10.7 Announcement Nedumbassery

Aircraft Maintenance Hangar Project 4.8 Proposed Cochin

Total of the above 389.5

Total Investment 389.5

Source: Monthly Review of states of India, CMIE March Report 2007

NameCost(In USD million)

Status Location

Kochi Shipyard Project 7.1 Announcement Kochi

Boat Train Pier Jetty Expansion Project 1.2 Announcement Kochi

Andhakaranazhi Fishing Harbour Project Proposed Andhakaranazhi

Marine Drive Boat Jetty Project Proposed Kochi

Total of the above 8.3

Total Investment 8.3

Source: Monthly Review of states of India, CMIE March Report 2007

Particulars/Year 2004 20052006(up to

31.08.2006)

Installed capacity (MW) 2,617 2,641 2,657

Annual sales (MU) 9,384 10,270 5,896

Per capita consumption (kWh) 400 427 444

EHT lines (circuit kilometres) 9,924 10,178 10,248

Sub Stations (numbers) 251 269* 272

HT lines (circuit kilometres) 33,618 34,680 35,152

LT lines (circuit kilometres) 207,711 215,152 217,784

Source: KSEB* Includes one 400 KV Pallippuram sub station of Power Grid Corporation of India Limited

Major power projects in Kerala

Kerala has implemented several reforms in the power sector:• All the 1.5 million households to be electrifi ed by effecting

service connection to 0.5 million households per year. • Energy audit to reduce system losses by metering all 11 KW

and above feeders completed;• 100 per cent metering of all consumers completed;• MIS cell with headquarters at Thiruvananthapuram and two

regional offi ces at Ernakulam & Kozhikode functioning;• Action for reducing expenditure and increasing revenue col-

lection expedited;

• Computerised billing and customer service centres at sec-tions set up;

• Anti Power Theft (APT) activities intensifi ed and APT wing reorganised. APT ordinance promulgated by Government of Kerala;

• Renovation and modernisation works of Pallivasal, Sengulam and Panniar completed;

• Renovation works of Neriamangalum hydel generating sta-tions nearing completion;

• Introduced Availability Based Tariff (ABT) in southern region with effect from 1st January 2003; Kerala is strictly following grid regulations;

• The Government of Kerala issued its captive power policy on small hydro projects in January 2003

Telecom and ITKerala Circle had 1.75 million mobile connections as on 30th September 2006, of which 1.34 million were pre-paid and 411,360 were post-paid. The state has about 365 post offi ces, 140 telegraph offi ces and 1,223 telephone exchanges.

It has a well-developed telecommunications infrastructure with a high tele-density. All the telephone exchanges in the state are connected to STD/ ISD network and 98 per cent are connected to the National Internet Backbone (NIB) by optical fi bre cables. Kerala is one of the best-networked states in the country in terms of telecom and datacom. The state’s tele-density is double the national average and all the telephone exchanges are digital. VSNL’s International Communication Gateway, with two high-speed submarine cable landings (SEA-ME-WE-3 and SAFE) offer-ing 15 Gbps bandwidth, is located in Kochi. This gateway cur-rently handles more than two thirds of the country’s data traffi c. Optical fi bre connectivity up to the grass-root level makes high quality, reliable bandwidth available in any part of Kerala.

Major telecommunication projects in Kerala

The IT infrastructure of the state consists of a State Information Backbone, which links the Data Centre at Thiruvananthapuram. Networking operating centres at Kochi and Kozhikode have been set up as part of the State Information Infrastructure. The

Name CapacityCost (In USD Million)

Status Location

Kayamkulam Expansion Power project

1950 Mw 1571.4 Proposed Kayamkulam

Chimmeni Power Project 500 Mw 357.1 Proposed Chimmeni

Kannur Power Project 513 Mw 350.2 Proposed Azhikal

Karapara-Kuriarkutty Hydel Power Project

84 Mw 131.0 Announce-ment

Kerala

Athirappally Hydel Power Project

160 Mw 98.1 Proposed Athirappally

Kuttiyadi Hydel Power Project II

100 Mw 95.2 Under Implemen-

tation

Kuttiyadi

Pathrakadavu hydro Power project

70 Mw 58.8 Announce-ment

Pathrakkadavu

Kasargod Diesel Power Project

61 Mw 52.9 Under Implemen-

tation

Kasaragod

Thottiyar Hydel power Project

70 Mw 49.3 Proposed Thottiyar

Captive Power Project 50 Mw 47.6 Announce-ment

Kannur

Mankulam Hydroelectric Project

40 Mw 42.9 Announce-ment

I dukki

Neriamangalam Hydel Power Project

25 Mw 23.8 Under Implemen-

tation

Kerala

Alupuram Captive power project

30 Mw 23.8 Announce-ment

Alupuram

Karikayam Hydel Project 15 Mw 17.9 Announce-ment

Chittar

Barapole-Muttannur Trans-mission Project

17.6 Announce-ment

Barapole/Mut-tannur

Coal Based Captive Power Project

20 Mw 16.7 Announce-ment

Udyogmandal

Barapole Hydel power project

21 Mw 15.5 Proposed Barapole

Pothangod-Kattakada Trans-mission Project

24 km 5.7 Under Implemen-

tation

Kattakada/Po-thangod

Chembukkadavu Hydel Power Project Stage I

7 Mw 5.2 Under Implemen-

tation

Chembukkadvu

Captive Hydel Power Project

4.8 Announce-ment

Thiruvanan-thapuram

Total investment 2985.5

Source: Monthly Review of States of India, CMIE – March 2007Name

Cost(In USD Million)

Status Location

Kerala Cellular Service Project

24.8 Under Implementation Kerala

Technology Habitat Project

Proposed Cochin

Total of the above 24.8

Total Investment 24.8

Source: Monthly Review of States of India, CMIE – March 2007

KERALA PAGE 15

rural connectivity infrastructure based on wireless technology in Malappuram district is considered to be the biggest IP-based outdoor network in the world.

Key Nodal Agencies

The government introduced the Single Window Clearance System in 2000, to expedite various clearances required for new industrial projects. A fi nal clearance for all new projects, either approval or rejection, is given within a specifi c period from the date of submission of application. This has been made a statutory requirement under the Kerala State Single Window Clearance Boards and Industrial Township Area Development Act 1999.

Single Window Clearance Structure

District Level Boards have been constituted for issue of clear-ances required by small-scale industries. The district collector of the respective district is the chairman and general manager of the District Level Board. The District Industries Centre (DIC) is the convener for such Boards.

A State Level Board, headed by the chief secretary, has been constituted. The Board issues clearances within 45 days to me-dium and large-scale industries. Kerala State Industrial Develop-ment Corporation is the single contact point and convener of the State Board.

Industrial Area Boards have also been set up in the various industrial areas of the state for clearance of the projects. An of-fi cer not below the rank of district collector is the chairman of each Board, with the Designated Authority of the Industrial Area as the convener.

The State Level Board takes 45 days, the District Level Board 60 days, and the Industrial Area Board 30 days for issue of clear-ances. A Common Application Form has been formulated, which an entrepreneur needs to submit at a single point only.

Kerala State Industrial Development Corporation Ltd. (KSIDC)

Established in July 1961 to nurture the medium and large-scale industrial sector in the state, KSIDC acts as a promotional agen-cy for the development of physical and social infrastructure in the state. A nodal agency for foreign and domestic investments in Kerala, KSIDC provides comprehensive support for investors. The incentive schemes are processed, and constant interaction between the government and industrial sector is facilitated by

KSIDC so that timely and appropriate support is given to the industry. Kerala Venture Capital Fund Pvt Ltd (KVCF), formed in association with Kerala Financial Corporation (KFC) and Small Industries Development Bank of India (SIDBI), is dedicated to investing in higher-end sectors like information technology and biotechnology.

KSIDC has facilitated investments in some mega proj-ects that include:• USD 1.6 billion port-based SEZ project; • USD 555.6 million LNG Terminal, USD 1.6 billion petro-

chemical complex; • USD 1.6 billion NTPC expansion and USD 100 million city

gas distribution project; • Gem and Jewellery Park near Kochi International Airport.

Kerala Industrial Infrastructure Development Corpora-tion (KINFRA)

KINFRA aims at developing infrastructure to promote industrial growth. It offers single window clearance facilities.

KINFRA has 17 industrial parks in various sectors comprising 150 operating units with an annual turnover of $222.2 million, providing employment to 5,000 persons. Each park offers com-prehensive infrastructure and support services.

Kerala Industrial and Technical Consultancy Organisa-tion (KITCO)

KITCO is involved in various activities such as rendering con-sultancy services, particularly in the fi elds of detailed engineer-ing and human resources development. Other activities include special studies, valuation of assets and energy audit.

Directorate of Industries & Commerce (DIC)

DIC provides infrastructure facilities for the small-scale sector by acquiring land and transforming it into development areas/ plots with facilities like developed land, road, water supply, elec-tricity and necessary building infrastructure.

Small Industries Development Corporation

The Small Industries Development Corporation undertakes works on provision of infrastructure facilities for the small-scale sector through its major industrial estates and mini industrial estates.

Kerala Financial Corporation (KFC)

KFC provides term loan assistance up to a maximum of $50 million per unit for the corporate sector and $20 million for others to develop and promote small and medium-scale indus-trial units in the state. During 2004-05, KFC disbursed $854.8 million, of which $409.6 million was given to the SSI segment for 187 projects. Policy Framework

The State Government of Kerala has announced various invest-ment friendly policies and initiatives.

Industrial Policy 2007

The main aim of Industrial Policy 2007 is to convert Kerala into an investment friendly destination and achieve high economic growth. The main objectives of the policy are:• To convert Kerala into a favoured destination for manufac-

turing, agro processing, health services, knowledge-based industries and services;

• To enable growth, revival and diversifi cation of state level public enterprises;

• To strengthen and modernise traditional industries;• To accelerate the fast growing services and commerce sec-

tor;• To develop Kerala as a global centre of excellence with state-

of-the-art education and skill sets and preparing a pool of multi-skilled, technically competent individuals and organisa-tions;

• To create additional employment for 0.5 million persons in the manufacturing and service sectors;

• To sustain industrial and economic growth by facilitating ac-celerated fl ow of investment.

It has outlined a number of areas to meet the objectives of this policy. It focuses on encouraging public private partnership for providing industrial infrastructure and utilities, and revitalising handlooms and textile sector. The government also offers a spe-cial fi scal benefi ts package in deserving cases for existing large industries. Incentives are provided for investment in supporting facilities like pollution control and effl uent treatment facilities, up to 50 per cent of the cost subject to a maximum of $60,000, ap-plicable for industrial units as well as commercial establishments. Special incentives package/ facilities to mega investments with an outlay of $23.8 million and above are considered on a case-to-case basis.

IT Policy 2001-2005

The highlights of the IT policy of the state are:• To establish Kerala as a leading IT destination in the country

within the next fi ve years;• To provide a nurturing and enabling environment conducive

to the vigorous growth of the local IT industry;• To signifi cantly enhance direct and indirect employment

creation in the IT sector;• To attain a minimum growth level of 100 per cent every year

in IT;• To signifi cantly accelerate the levels of investment infl ows

including foreign capital into the hardware, software and ITES sectors;

• To aggressively promote the state as the destination of choice for emerging IT business opportunities including ITES, new media products and e-services;

• To develop Kochi as an international media and ICT hub;• To consolidate and expand Technopark, Thiruvananthapuram

as a leading software and HR centre in the region;• To provide the physical and institutional environment for

decentralised IT usage.

Under this policy, the Kerala Government has formulated a com-prehensive and unique package of incentives for the industry. To accelerate the process of private sector-led IT infrastructure development, the government shall, in association with reputed global IT park developers and consultants, announce a minimum set of standards for IT parks to qualify as ‘Parks Standard’-certi-fi ed.

Kochi will be promoted as an ICT hub where facilities offered will match the best available worldwide. A 200-acre Hi-tech Park will be developed there. An IT Corridor connecting the new international airport at Nedumbassery with the city will also be established as part of the larger proposed SEZ continuum.

E-governance is one of the focus areas of the Government of Kerala to bring about transparency, speed and correctness in governance. Computerisation is underway in a majority of government departments. The Motor Vehicles Department has implemented ‘Smart Move,’ a software that enables it to offer driving test on any working day and issue licence immediately on passing the test. It avoids scope of manipulation and helps in accurate tax and fee calculation. To streamline the working of all treasuries, an e-governance project called TRIM is being imple-mented. All activities from bill submission to payment can be done in a speedy manner. THOZHIL, a project of employment exchanges, provides for online renewal of registration, addition of experience certifi cate and search for vacancies. AKSHAYA, a

KERALA PAGE 17

universal e-literacy programme, piloted in Malappuram District during 2002-03, involves setting up of around 5,000 multi-purpose community technology centres called Akshaya Kendras across the state.

Considering the tremendous potential for the IT indus-try in the state, KSIDC has evolved a special fi nancial package to promote the sector.• New IT units are eligible for an investment subsidy of 20 per

cent of fi xed capital investment (includes land, buildings, plant & machinery, utilities and miscellaneous fi xed assets), subject to a maximum of $2.5 million;

• 75 per cent of the eligible subsidy is included in the means of fi nance as subsidy loans, to reduce the promoter’s minimum contribution in the project. The subsidy loan is given at the term loan rate, for a period of one year and is adjusted against subsidy released from the government;

• A Venture Capital Fund with a corpus of $4.4 million has been formed jointly by the Small Industries Development Bank of India (SIDBI), KSIDC and Kerala Financial Corpora-tion (KFC). IT units can avail of venture capital assistance from the fund.

Biotech Policy

The Biotechnology Policy for Kerala is designed to catal-yse the development and application of biotechnology in the state. The highlights include:• To enhance the value - with adequate assurance of quality -

of the state’s export-oriented resources such as spices and related plantation crops, sea food and marine resources;

• To upgrade productivity and evolve new application in rub-ber, coconut, tuber crops, and develop novel internationally competitive products;

• To ensure the sustainable and eco-friendly exploitation of the state’s forest, animal and marine wealth;

• To boost the state’s renowned healthcare practices of Ayurveda by synergising traditional knowledge with scientifi c validation and technical product profi ling and clinical data base;

• To develop recombinant DNA and other modern technolo-gies to combat major health hazards such as cancer, diabetes and cardio-vascular and other physiological disorders; to develop diagnostics and vaccines for overall healthcare as well as to protect the state’s agriculture, spice, plantation and forest crops, from biotic and abiotic stresses;

• To enhance the quality of the environment and promote sustainable development;

• To provide an ambience with a package of guidelines for fi nancial support and incentives, legal and labour reforms as

well as institutional autonomies needed for the healthy, ef-fi cient and competitive growth of biotechnology knowledge base and industry.

Tourism Policy

Kerala is one of India’s largest developed tourism destinations. International tourist arrivals rose to 350,000 in 2005 from 210,000 in 2004. Travel and tourism generates 7.7 per cent of GSDP and 6.2 per cent of total employment. Tourism receipts from foreign visitors add up to 14.3 per cent of the total ex-ports of the state.

Kerala was nominated as one of the three fi nalists at the WTTC (World Tourism Travel Council) ‘Tourism for Tomorrow’ awards in the destination category in 2005. World Tourism Organiza-tion (WTO) has selected Thenmala ecotourism project as one of the 64 best eco-friendly tourist destinations spread over 47 countries.

The Kerala Government has adopted several strategies to promote tourism:• Implementation of “Tourism Vision 2005” with focus on

sustainable development by conservation and preservation of heritage;

• Development of selected tourist destinations in a sustainable and eco-friendly manner;

• Development of basic infrastructure and ensuring cleanliness of tourist destinations and the safety and security of tourists;

• Development of specialised tourism – ecotourism, health tourism, rural tourism, adventure tourism, plantation tourism and back waters tourism as well as domestic pilgrimage tour-ism;

• To develop infrastructure through private public partnership with the government acting as a facilitator and catalyst;

• Continuation of extensive and aggressive marketing of Kerala at national and international markets as a unique tourism destination;

• Strengthening local tourism efforts initiated by local govern-ments;

• Human resource development in the state;• Formation of new tourism zones.

Labour Policy

The Labour Policy focuses on:• Fostering an enabling environment for rapid employment

generation through enhanced private and public investment, in order to achieve the goal of creating 1.5 million new jobs

in the coming fi ve years;• Retraining and rehabilitation of retrenched labour in closed

and sick units;• Improving working conditions, providing decent wages and

basic lifeline social security for workers, especially in the unorganised sector;

• Minimising adversarial labour relations and providing labour market security, employment security, work security, and income security for the working population.

Fiscal incentives offered by the Kerala Government

The fi scal incentives are applicable to all eligible companies op-erating in Kerala, other than those located in SEZs.

• Standard Investment Subsidy (SIS) – This has been fi xed at 30 per cent of fi xed capital investment subject to a limit of $30,000 for companies located in Thiruvananthapuram and Ernakulam districts. For companies located outside these districts, the applicable SIS will be 40 per cent of fi xed capital investment subject to a limit of $60,000.

• For IT units in Government IT Parks, there is an exemption from stamp duty and registration fees for executing lease/ sale agreement for land and built-up space as well as exemp-tion from entry tax for goods like machine equipment, capital goods and construction material procured for implementa-tion of infrastructure projects.

• For IT infrastructure developers in government IT Parks, there is an exemption from payment of stamp duty, registra-tion fee and transfer duty of land.

• Private IT Parks that meet a minimum set of standards shall be governed by the same set of industry enabling regulations that are applicable to government IT Parks, unless otherwise specifi ed by the Government. The Government will consti-tute a committee to decide on the minimum set of standards required by private IT Parks to qualify for certifi cation.

• An IT software unit that has its registered offi ce in Kerala and employs a minimum of 30 per cent of local workforce in its operations in the state shall be entitled to 7.5 per cent price preference on IT software solutions required by Kerala Government/ public sector units/ government bodies.

An IT hardware unit that has its registered offi ce in Kerala and employs a minimum of 30 per cent of local workforce in its Kerala operations shall be entitled to a 10 per cent price prefer-ence on IT hardware required by Kerala Government/ public sector units/ government bodies (provided the unit pays excise or it is ISO certifi ed, and otherwise compliant with the tender requirements).

Thrust areas for future focus

The following are the thrust areas for the Kerala Gov-ernment.

• Mega Industrial Parks: In order to make Kerala a destination of choice for investors, KINFRA will help to develop Mega Industrial Parks in select thrust sectors. Integrated Textile Parks at Palakkad and Mega Food Park at Wayanad are al-ready envisaged.

• Industrial Townships: Industrial Townships, which would be compact industrial areas providing necessary support to in-dustrial entrepreneurs and offering world class facilities, will be set up. The Palakkad Industrial Township Area Project and Knowledge Cities in Trivandrum, Ernakulam and Palakkad are being planned.

• SEZs: Product specifi c SEZs including service SEZs, with industry-specifi c infrastructure along with all basic and sup-porting facilities, will be encouraged in the state. KSIDC/ KINFRA will be setting up sector-specifi c SEZs at Kozhikode, Kannur, Kasargod and Malappuram. KSIDC shall take steps to set up a Free Trade and Ware Housing Zone (FTZ) at Kochi.

• Industrial Corridors: Three industrial corridors in the state, which would qualify as Commercial Districts, are proposed - IT & ITES Corridor from Kazhakuttom to Kovalam and from Kazakuttam to Kollam along NH Bypass; Biotechnology & Hitech Electronics Corridor along Seaport-Airport road at Kochi; and Food Processing and Textile corridor from Kanjik-ode to Walayar along the NH at Palakkad.

• Sector-specifi c Industrial Parks: Industrial Parks will be developed in certain select thrust sectors. Watercraft Park at Kochi and Print Village at Kochi are on the anvil. KSIDC shall facilitate setting up of a world-class Electronic Hub for at-tracting global leaders in electronic hardware and equipment, home appliances and semi conductor devices.

Key industries and players in Kerala

Kerala has a mix of industries – handloom, powerloom, rub-ber, bamboo, coir, khadi & village, sericulture, seafood and other marine products, cashew, beedi, mining, tourism, food processing, spices, electronics, and chemicals.

KERALA PAGE 19

Handloom and Powerloom Industry

The handloom sector in Kerala employs about 180,000 people and is next only to the coir industry among the traditional sectors in providing employment. It is concentrated in Thiru-vananthapuram and Kannur districts and in some parts of Kozhikode, Palakkad, Thrissur, Ernakulam, Kollam and Kasaragod districts. The co-operative sector dominates this industry, ac-counting for 94 per cent of looms. The major products include dhothies, furnishing material, grey saris and lungis. The Institute of Handloom and Textile Technology, Kannur, has been set up by the Kerala Government for the development of the handloom industry.

The National Institute of Fashion Technology, New Delhi, had identifi ed Kozhikode Handloom Cluster for a project on devel-opment of a Craft/ Textile cluster to be implemented as a special project under Swarna Jayanthi Gram Swarozgar Yojana. It was proposed by the Ministry of Rural Development, Government of India, with 75 per cent central assistance and 25 per cent state assistance. The Government of India has also approved the establishment of a Handloom Project Development Centre (HPDC) at Balaramapuram and $90,000 has been released for setting up of weaving, dyeing, printing and design development equipment.

Procurement and marketing of handloom fabrics is being under-taken by two state-level organisations – Kerala State Handloom Weavers Co-operative Society (Hantex) and Kerala State Hand-loom Development Corporation (Hanveev).

There are 3,800 powerlooms in the state, out of which 1,381 are in the co-operative sector. The looms are mostly in Kan-nur, Thrissur and Palakkad districts. There were 33 power loom co-operative societies, with 6,600 members, at the end of March 2005. In 2004-05, 6.2 million metres of cloth worth $1.7 million was produced.

Rubber Industry

Kerala has a large area under rubber plantation, of which 92 per cent is represented by small holdings. Its annual production of 370,000 tonnes of rubber accounts for over 90 per cent of India’s natural rubber. A network of intermediate rubber units engaged in rubber compounding and crumb rubber manufacture exists in the state.

Apollo Tyres Ltd

Apollo Tyres Ltd is one of India’s leading automobile tyre manu-facturers. With an annual turnover of $600 million, it has manu-facturing plants at Perambra and Kalamassery in Kerala, Vadodara in Gujarat and Pune in Maharashtra. The company is QS 9000 certifi ed and will be upgrading to TS1619 shortly.

Coir Industry

Kerala accounts for 95 per cent of total coir and coir products production in the country. The industry is labour-intensive and employs around 390,000 persons, of which 86 per cent are women. The Alappuzha district alone contributes around 90 per cent of the total coir produced in the state. Several ma-jor initiatives have been taken by the government to promote the coir industry. A Common Facility Service Centre is being implemented to help small-scale producers in the coir sector. Steps have been taken for setting up a National Coir Research and Management Institute to strengthen the R & D activities and to enable the industry to produce more value-added and new design products. Two Coir Parks have been set up at Alappuzha with a total investment of $5 million.

A High Tech Coir Park is to be implemented by the Centre for Development of Coir Technology (DOCT) Thiruvananthapuram, with the support of state, central and national fi nancing institu-tions at an estimated cost of $3.8 million. It will offer a meeting ground for scientists, technologists and entrepreneurs and is expected to open up possibilities to develop a wide range of eco-friendly products based on coconut fi bre.

Sericulture

Sericulture is an agro-¬based industry promoted as a subsidiary occupation in Kerala. The State Sericulture Cooperative Federa-tion (SERIFED) is the nodal agency for promoting sericulture activities. A cluster-based development, active involvement of local self-government and member societies and emphasis on post-cocoon technology sector are the three components of the sericulture development strategy during the Tenth Plan. Co-coon production added up to 92.08 MT in 2005¬-06, as against 77.61 MT in 2004-¬05.

Sea Food and other marine products

Kerala contributes nearly half of India’s marine fi sh landings of 250,000 tonnes. Sardines, shrimps, lobster, cuttlefi sh, squid and tuna, which have huge demand in the overseas markets, are

available in abundance. Ongoing technology upgradation in the export-oriented marine product sector points towards greater growth in the immediate future. Investment options exist in the areas of Individually Quick Frozen (IQF) Marine Products, freeze-dried marine products, shrimp/ crab extracts, shrimp/ fi sh feeds, shrimp feed ingredients and sushi shrimp.

Mining

Kerala occupies a unique position in the mineral map of India. Heavy mineral sands and china clay contribute more than 90 per cent of the total value of mineral production in the state.

Gold occurs in Kerala both as primary and placer depos-its. The known occurrences are mainly in Wayanad Nilambur regions. The largest bauxite deposit is in Nileswaram with a reserve of 5.32 million tonnes. A total reserve of 172 million tonnes of china clay has been estimated in the state. The coastal tract between Alappuzha and Aroor in Alap-puzha district contains extensive deposits of silica sand. Lignite, which was discovered recently, is the only fuel mineral in Kerala. A range of gemstones has been identifi ed in Thiru-vananthapuram and Kollam districts. Tile manufacturing units are concentrated mainly in the Feroke area of Kozhikode district, Thrissur Aluva area of Thrissur and Ernakulam districts, Chathannur of Kollam district and Amaravila of Thiruvanan-thapuram district.

Kerala’s annual production of China clay adds up to $66.7 mil-lion, about 35 per cent of the total value of production of minerals in the state, excluding atomic minerals. Paper coating clay from Thiruvananthapuram district has excellent export po-tential. There are 25 working china clay mines in the state, of which 17 are in Thiruvananthapuram, four in Kollam and two each in Kannur and Kasargod districts. Kerala contrib-utes 58 per cent of the total annual production of pro-cessed clay in the country. The total revenue of the mining and geology department was $5.2 million in 2005-06.

Kerala Minerals and Metals Ltd (KMML)

KMML is a pioneer in the fi eld of mineral sand industry in India and is a fully owned Kerala Government enterprise. It is the world’s fi rst fully integrated titanium dioxide plant. Since its inception, KMML has made a mark in the fi elds of mining, mineral processing and manufacturing. It has factories at Sanga-ramangalam and Kovilthottam, and is India’s only manufacturer of rutile grade titanium dioxide by chloride route. KMML also manufactures iron oxide bricks used for building purposes. The

production of these bricks from waste iron oxide is an in-house development. KMML’s titanium pigments are reputed for their high degree of gloss, tint retention capacities and ease of disper-sion. The company is ISO 9002 certifi ed.

Tourism

Kerala is one of the prime tourism economies of India, with the sector contributing 13 per cent to the state’s GDP. The total revenue (including direct and indirect) from tourism in 2005 was $1.7 billion. The Central Government has allotted $8.6 million as the fi rst installment of aid, out of the total sanctioned amount of $10.9 million, for 12 different tourism projects including devel-opment of beach tourism circuit and spice tourism circuit.

Kerala is also ranked as a tourism brand, listed amongst the 101 strongest brands in India by Super Brands India Pvt Ltd, and has been accorded the “Super Brand Status”, known as the ‘Oscar’ in the world of branding.

According to the World Travel and Tourism Council (WTTC), tourism arrivals in Kerala are expected to grow by 11.6 per cent per annum over the next decade (this is the highest growth in the world, surpassing Turkey’s 10.2 per cent and the all-India growth of 9.7 per cent). A record growth of 23.5 per cent is also expected in external account earnings from travel and tourism over the next 10 years (India’s estimates for this period are 14.3 per cent, while the world average is only 6.5 per cent)

The Kerala Tourism Department has initiated various projects for the development of basic infrastructure at tourist destina-tions, creation of new products and en-route facilities. Projects under implementation include:• Construction of houseboat terminals is being taken up at major backwater nodes such as Alappuzha, Kumarakom, Thanneermukkom, Chettuva, Vadikkal and Neeleswaram. The terminal at Kumarakom is ready and a second one is being built.• Tourism infrastructure and basic amenities are being developed along the Pamba-Kuttanad backwater cruise routes after detailed studies. Tourist resorts at Pallathuruthy, Nedumudi, Kotharathode and Vattakkayal are being developed.• Houseboats have been deployed at Neeleswaram, Parassinikkadavu, Kozhikode and Chettuva as part of extending backwater-based activities to the Malabar area. Valliyaparamba has been developed as a major backwater centre. Boat jetty complexes are being developed at Iringal, Azhhkal, Kotti and Ayit-tikadavu.

KERALA PAGE 21

Food Processing Industry

The Kerala Government has identifi ed the food processing industry as a thrust area for development. Kerala ranks number three in the country in terms of the number of licensed food processing units, after Maharashtra and Tamil Nadu. The state is richly endowed with resources and raw materials such as fruits and vegetables, vanilla, and freshwater and marine fi sh.

Kerala is known as the land of spices. Today, there is great demand for 26 Indian spices in different countries. Pepper is perhaps the world’s oldest known spice and is cultivated in over 158,000 hectares in Kerala, which accounts for 96 per cent of the total production in the country. There are a number of op-portunities available for investors in the spice sector.

Chemicals and Fertiliser industry

Kerala ranks ninth in the country in terms of installed capacity of production of chemicals, at 279,750 tonnes in 2005-06.

Fertilisers and Chemicals Travancore (FACT)

Fertilisers and Chemicals Travancore (FACT) is a prominent player in the industry. A Government of India enterprise, it has business interests in manufacturing and marketing of fertiliser, Caprolactum, engineering consultancy and fabrication of equip-ment. It has two manufacturing units at Udyogamandal and Cochin in Kerala.

Electronics

The Electronics Technology Park, Technopark, at Thiruvanan-thapuram, is attracting electronic manufacturers from across the world. Kerala scores in the availability of skilled and semi-skilled workers for the electronics industry. Investments have come in the area of computers and peripherals, industrial and process control equipment, automotive and medical electronics, tele-communications and fi bre optic terminal equipment, surveillance and security systems, banking automation, consumer electronic products, ASIC design, fabrication and packaging, chip/ ceramic components and hybrid micro circuits.

Prominent players in the electronics industry in the state are Traco Cable Company Ltd, and Transformers and Electricals Kerala Ltd.

Traco Cable Company Limited

Traco Cable Company, a premier state government company,

commenced operations in 1964, manufacturing high-quality electric cables and wires in technical collaboration with Kelsey Engineering Co Ltd, Canada. Since then Traco has been meeting the needs of public sector undertakings like Indian Railways and the electricity boards of various states for power and signalling cables.

Transformers and Electricals Kerala Ltd (TELK)

TELK was incorporated in 1963 following an agreement be-tween the Government of Kerala, Kerala State Industrial Devel-opment Corporation and Hitachi of Japan, to set up a full fl edged unit for designing and manufacturing extra high voltage electrical equipment. TELK ventured into the area of manufacturing high capacity transformers at a time when the nation relied mostly on imported equipment to meet its power transmission require-ments. Located at Angamally, near Kochi, the fi rst product rolled out from TELK’s manufacturing facility in 1966.

Information Technology

Kerala has all the major infrastructural facilities that are required for the growth of the IT sector. Kochi is fast emerging as a unique IT destination. It was ranked number two in a report by the National Association of Software and Services Companies (NASSCOM) on the country’s Super ITES destinations, and number three in a study of cities ideal to do business in. Kochi is directly connected by two submarine cables and satellite gateways.

The state has recorded major achievements in the IT sector:• Malappuram - India’s fi rst e-literate district;• Chamravattom - India’s fi rst e-literate village;• Vellanad and Talikkulam - India’s fi rst and second fully com-

puterised Grama Panchayats;• Akshaya wireless network in Malappuram - world’s biggest

IP-based network;• Palakkad - India’s fi rst fully computerised District Collector-

ate;• First state to use ‘Edusat’ for on-line learning solutions;• Information Kerala Mission – single-largest computerisation

programme for local bodies and deployment of software developed in an Indian language;

• First state to have Citizen’s Call Centre on government-related details;

• First Technology Park in India to achieve CMMI level 4.

Prominent players in the IT industry in the state are IBS Soft-ware Services, Softex Computer Consultants, GCI Enterprise

Solutions, Toonz Animation India Pvt Ltd, US Software, Seaview Support Systems and Suntech Business Solutions.

IBS Software Services

The IBS group is a leading software solutions provider to the global travel, transportation and logistics industry. IBS offers a range of software products that manage critical operations of major airlines, airports, oil and gas companies, seaports, cruise lines and tour operators world-wide. In addition, IBS offers services that include software development, business and tech-nology consulting, application maintenance and onsite software development services. Its development centre in Thiruvanan-thapuram operates from Technopark. Its facility at Cochin is based at Infopark.

Softex Computer Consultants

Softex Computer Consultants, based at Technopark, has entered into a long-term agreement with Siemens Worldwide, Germany. The products developed by Softex for General Packet Radio Service (GPRS), 3G cell phones and mobile devices, are globally marketed by Siemens.

GCI Enterprise Solutions

GCI is a SAP software partner, which has created a state-of-the-art information technology centre at the Technopark campus, enabling round-the-clock development services for clients. GCI also operates dedicated Offshore Development centres for major clients.

Toonz Animation India Pvt Ltd

Toonz, a major provider of animation to top US and European producers, is South Asia’s biggest animation studio. Founded in 1999, its client list includes Marvel, Hallmark, Paramount, Disney and Cartoon Network. Toonz is the preferred one-stop studio for entertainment majors in America, Europe and Asia. It has its corporate headquarters at the Technopark campus, with divi-sions in USA, Europe, Japan and Australia.

US Software

US Software is a wholly owned subsidiary of US Technology Resources, LLC, a California-based company operating through a hybrid global sourcing and delivery model. A leading provider of end-to-end global IT and BPO services to Fortune 500 com-panies, it has strong domain experience in strategic business sectors, including healthcare, entertainment, transportation and

logistics, banking, fi nance and insurance, retail and manufacturing. The company is located at Technopark.

Seaview Support Systems Pvt Ltd

Seaview Support System is a Technopark-based BPO, provid-ing back-offi ce services such as medical transcription, coding, billing, medical research transcription, legal transcription and consultancy. The company, incorporated in 1996, has over 270 transcriptionists and operators in the domain of medical BPO, legal transcription, business/ general transcription and medical research transcription.

KERALA PAGE 23

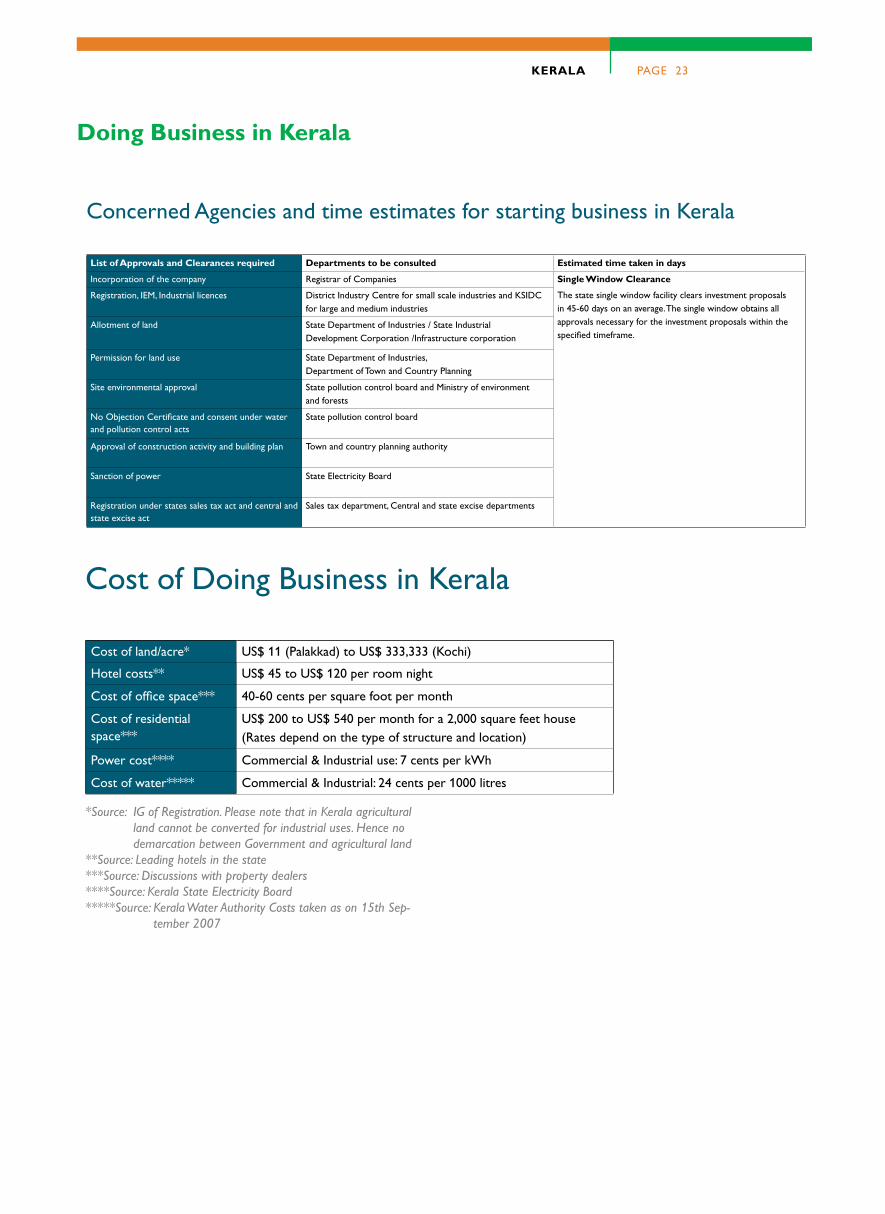

Doing Business in Kerala

Concerned Agencies and time estimates for starting business in Kerala

List of Approvals and Clearances required Departments to be consulted Estimated time taken in days

Incorporation of the company Registrar of Companies Single Window Clearance

The state single window facility clears investment proposals in 45-60 days on an average. The single window obtains all approvals necessary for the investment proposals within the specified timeframe.

Registration, IEM, Industrial licences District Industry Centre for small scale industries and KSIDC for large and medium industries

Allotment of land State Department of Industries / State Industrial Development Corporation /Infrastructure corporation

Permission for land use State Department of Industries,Department of Town and Country Planning

Site environmental approval State pollution control board and Ministry of environment and forests

No Objection Certificate and consent under water and pollution control acts

State pollution control board

Approval of construction activity and building plan Town and country planning authority

Sanction of power State Electricity Board

Registration under states sales tax act and central and state excise act

Sales tax department, Central and state excise departments

Cost of Doing Business in Kerala

Cost of land/acre* US$ 11 (Palakkad) to US$ 333,333 (Kochi)

Hotel costs** US$ 45 to US$ 120 per room night

Cost of office space*** 40-60 cents per square foot per month

Cost of residential space***

US$ 200 to US$ 540 per month for a 2,000 square feet house (Rates depend on the type of structure and location)

Power cost**** Commercial & Industrial use: 7 cents per kWh