Investing Report - AgFunder · PDF fileAGTECH INVESTING REPORT 2015 ... most complete picture...

34

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 2 AgTech Investing Report MID YEAR REPORT 2015

Transcript of Investing Report - AgFunder · PDF fileAGTECH INVESTING REPORT 2015 ... most complete picture...

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 2

AgTechInvesting ReportM I D Y E A R R E P O R T 2 0 1 5

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

AGTECH INVESTING REPORT 2015

INTRODUCTION

We’re midway through 2015 and agtech investment has already hit $2.06B, just shy of the record-breaking $2.36B invested in all of 2014. Momentum continues to keep pace with roughly $1B invested in each quarter so far this year. We revised our Q1 numbers to $1.08B over 129 deals, from the $1.04B we reported in April 2015. Q2 posted 99 deals totaling $971M which we expect to revise upward as additional funding data trickles in. We know we’re still not discovering all deals in the sector, so we’ll continue to expand our sources to make the report as extensive as possible. High profile deals from Khosla, Google Ventures, and Andreessen have shone the spotlight on this sector, and this recognition is trickling down throughout the U.S. and the globe as new centers of innovation are emerging. The industry is also very much tied to the public sector, and we’re seeing an equal amount of support and some dollars coming in from public sources, which are not reflected in this report. There’s no question that technology will be the future of agriculture. The real question is just how quickly we will get there. In the past, agriculture revolutions have moved more slowly, but these fundings, together with technology adoption rates, are helping to propel the current agtech revolution forward to meet the goals of more food, better food, and sustainable food systems. We look forward to seeing what happens in the second half of the year.

AgFunder is an online equity

crowdfunding platform for

agriculture technology. We

help Accredited and

Institutional Investors

discover & invest in

developing technologies to

transform the agriculture

industry.

Learn more @

www.agfunder.com

Authors: Melissa Tilney, Rob Leclerc.

Design: Simona Barta Still on our mission to feed 10B by 2050! Rob Leclerc, AgFunder CEO

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

Data SourcesData was collected from a wide variety of sources to reflect the most complete picture of fundings in this area. Our sources included: CrunchBase, press releases, articles, U.S. Securities and Exchange filings, and direct sources. Data LimitationsBecause the U.S. Securities and Exchange Commission (SEC) requires companies to publicly file their financings with the SEC, there may be many more non-U.S. companies that receive financing, but which are absent from our analysis.

Undisclosed FinancingsSome of the financings in our data set have undisclosed financings that cannot be determined through SEC filings or direct sources. We were often able to obtain financing figures from the companies themselves, but they requested that we did not disclose exact figures. We excluded undisclosed financings when we computed averages and median values.

Multiple FinancingsSeveral companies closed multiple financings. While

CrunchBase data was generally accurate, there were instances where CrunchBase data double counted financings on a cumulative raise. When multiple financings represented rolling closes from the same round, we compounded all smaller financings into the largest so as to not inflate the total number of deals.

4

Sources

SOURCES

CrunchBase was an important supplementary data source for this report, which helped to capture a much more complete picture of the funding landscape. Special thanks to Tim Li and the CrunchBase team for their support and assistance.

Special Acknowledgement

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 5

ScopeThis report encompasses financings of technology companies within the global agriculture value chain. The agriculture sector is one of the largest and most important sectors of the economy, representing nearly 8.5% of Global GDP. However, this size comes with tremendous diversity. The sector is centered on cultivation of plants, animals, and other living organisms for food, materials, biofuels, chemicals, and medicinals. It also encompasses the rest of the agriculture value chain, including inputs, storage, processing, packaging, transportation, infrastructure, finance, health, and safety, as well as marketing and retail services that connect these products to consumers. Drawing the line between AgTech and consumer technologies is not easy. While restaurant-to-customer food delivery may technically fall within the agriculture value chain, we ultimately felt that these services were unlikely to have a disruptive effect on other areas of the agriculture value chain, therefore, we excluded these companies from our analysis. In contrast, we included grocery delivery services. Unlike restaurant delivery, grocery delivery services have a significant opportunity to disrupt the entire supply chain that sits between the farmer and the consumer. For clarity we grouped Food Ecommerce and

Farm 2 Consumer (F2C) marketplaces separately. Similarly, there’s a fine line between food technologies and food products, so the inclusion of food technology companies was limited to companies that had a potential impact on the rest of the agriculture value chain. Companies like Hampton Creek and Beyond Meat are all developing technologies that could have significant impact on the use of animals in agriculture, so these types of companies were included. For other technologies, such as drones, sensors, and biotech, in which application spans a number of sectors, we only included those companies that self identified agriculture as a key market. Tagging and CategorizationTo help categorize companies, we generated a set of 30 keywords and tagged each company’s description when it contained the keyword. We then manually curated the list to ensure that keywords were properly applied. Using the tags, description for each company, and seeing a sufficient concentration of investment or deal volume, we then assigned each company to a category to capture groups of companies that shared similar tags, and which were relevant either by number of deals or by total funding.

Methods

METHODS

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 6

MID-YEAR REVIEW

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 7

280 Unique Investors

228 Deals

$2.06B Invested

MIDYEAR OVERVIEW 2015

Image:AgriLifeToday/Flickr

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 8

1. Agtech investment is climbingComing off the heels of a record-breaking 2014, investment continued its upward trajectory this year. Halfway through 2015, investment stands at $2.06B; just $300M shy of last year’s total of $2.36B. There’s a lot of momentum in the market, and we expect investment to keep pace for the remainder of the year. Fundamentally, when we speak with growers and industry experts, there’s a consensus that agtech is here to stay. Precision agriculture, alternative farming methods, updated supply chains, sustainable proteins – all of these will become integral to farming in the future. The industry, however, is still in its infancy and money is flowing in to promote development. New investors continue to enter the sector, with 280 unique investors in the first half of 2015 versus 271 for all of 2014. The uptick in investors entering the sector is driving up the price and size of rounds, but average investment size is still behind industry venture averages. Although there will be the winners and losers among this group of companies receiving funds, the substantial size of the $6T industry means that this recent

influx of capital represents only a fraction of what’s possible. 2. Precision Ag1 continues to attract capitalPrecision agriculture’s ultimate goal is to enable farmers to analyze and adjust almost every aspect of their operation. Last year, $276M was invested into precision agriculture solutions. Midway through this year, that number has almost reached $400M. Large investments were made in satellite imagery company Planet Labs ($118M), which recently bought RapidEye and signed a data agreement with ag-retailer Wilbur-Ellis. Drone makers DJI ($75M), 3D Robotics ($64M) and Pulse AeroSpace ($23M) also saw new investment following the FAA’s Feburary announcement of rules governing commercial drone use. Following these deals, 2015 has already seen a healthy pipeline of precision ag deals with 22 Seed deals and 20 Series A deals. Venture capitalists have been keen to invest in this area because many solutions are based in software and big data – something VCs understand - and there’s potential for scale with broad adoption. We have seen early exits in this subsector because Monsanto (Climate Corp) is not afraid to open its wallet, and other VC-backed players have pursued aggressive acquisition strategies that are familiar in other VC sectors.

Five themes from AgTech fundings for Q1 & Q2 2015:

THEMES

1. Precision Ag mostly encompasses the companies in the categories: Decision Support Technologies, Drones & Robotics, and Smart Equipment & Hardware

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 9

3. Water tech one of the big winnersWater-focused technologies have taken center stage so far this year. This is especially the case in California where the state is entering its fourth year of a historic drought, creating major concern for its $40B+ farming industry. For a long time, everyone thought we would have enough water to last indefinitely. Now, however, with increasing stresses from population growth and climate change, it’s quickly become apparent that water is a scarce resource that needs to be managed more carefully. In the first half of 2015, $525M was invested in water technologies. Israeli drip irrigation provider Netafim accounted for the majority of that total with it’s $500M debt financing in Q1, while smaller startups like CropX ($9M), Hortau ($5M), and PowWow Energy ($3M) are just getting off the ground. Water desalination, which carries a high energy cost, is even gaining traction. Although water investment is key to the future, the long-term question will be whether investment continues at the same pace when the drought eases.

4. Old guard vs. new guard What started largely as investment by agriculture-specific funds and industry players, has now become more mainstream. When we look at Series B and C rounds, we are seeing sizes more inline with the tech VC market. In Q1 and Q2, for example, the median funding size was $4.3M for Series A, $11M for Series B, and $20M for a Series C. We have seen a gap in seed fundings. The median deal size for a seed stage deal was just $250,000, which is smaller than other industries, and points to a potential need for more money coming in at the earlier stage.

5. Food ecommerceFood ecommerce has massive potential to reshape the food value chain and get consumers closer to the point of production. These businesses are bringing much needed innovation to the supply chain. Large, later stage investments were made in companies like BlueApron ($135M), Munchery ($85M), Sprig ($45M) and NatureBox ($30). We observed an increasing number of international me-too companies crop up, like Indian grocery delivery services PepperTap ($11.2M) and Grofers ($35M). We’ll be looking at this space to see whether there are flame outs and whether the margins support long term growth in the sector.

Five themes from AgTech fundings for Q1 & Q2 2015 (cont.):

THEMES

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

$0.4 $0.5 $0.5

$0.9

$2.4

$4.1

2010 2011 2012 2013 2014 2015

10

Investment in agtech prior to

2012 was largely flat, hovering

around $500M annually. That

began to change in 2013, with

investment jumping 75% year-

over-year driven by early

moving cleantech VCs entering

the market. And, after Climate

Corp’s $1B exit at the end of

2013, investors and money

flowed into the sector in record

numbers in 2014. Now 2015

could eclipse that.

(Note: Historic 2010-2013 data is from

the Cleantech Group. Our data

collection methodologies differ so data

should be interpreted directionally.)

AgTech Investment 2010-2015 (annualized)

DEAL ACTIVITY BY QUARTER

Financing | $Billions

$4.1

Data Sources: 2010-2013 CleanTech Group; 2014-2015 CrunchBase & AgFunder

Annualized Financing

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 11

Quarterly investment saw a step-

change in Q4 2014. This level kept

pace in 2015 with over $1B

invested in each quarter.

As with Q4 2014, a handful of

deals drove top line numbers. In

Q1, the Israeli drip irrigation

company Netafim accounted for

approximately 50% of the total

dollars. In Q2, six deals (largely

food ecommerce) accounted for

nearly 50% of deals.

One important difference is that

deal volume year-to-date is much

higher than 2014, reflecting the

fact that more companies are

receiving early-stage funding.

Deal Volume and Amount by Quarter

DEAL ACTIVITY BY QUARTER

Deal Volume

Financing | $Millions

$467$416

$509

$969 $1,084 $971

55

78

67

64

129

99

2014-Q1 2014-Q2 2014-Q3 2014-Q4 2015-Q1 2015-Q2

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 12

DEALS BY SUBSECTOR

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 13

Food Ecommerce (27%) and Water

Technologies (26%) were the big winners

in H1. Later stage investment in Food

Ecommerce contributed heavily to this

number, while Water Tech’s Netafim

financing was the main reason we saw

such a pop in this category.

In the first half of the year, we saw a pull-

back in investment into BioEnergy and

Crop & Soil Tech (Biotech), both of which

represent the last generation of agtech.

However, we also saw a pullback in

investment into sensors and devices. This

may be attributed to the fact that there’s

only so many sensors required on a farm,

placing more importance on creating

services and products that manipulate

the data derived from the sensors

AgTech Subsector Breakdown

DEALS BY SUBSECTOR

% of Total Investment Dollars

27%

26%10%

9%

8%

6%

5%

2%1%1%

6%

Food Ecommerce

Water

Drones & Robotics

Decision Support Technology

Bioenergy

Soil & Crop Technology

Biomaterials & Biochemicals

Sustainable Protein

Cannabis

Food Storage

Miscellaneous

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 14

Food Ecommerce was the largest

sector in both sheer volume and

size of deals. This subsector spiked

because first generation

companies, like Blue Apron and

Munchery, are now later stage and

emerging me-too players are

joining the sector.

Precision agriculture, which spans

drones, decision support, and

select investment in smart

equipment, was the next largest

subsector, boasting the largest

volumes among all others.

While small in total deal amount,

cannabis experienced ample new

early stage activity.

Deal Volume and Amount by Subsector

DEALS BY SUBSECTOR

Financing | $Millions

# Deals

34

12

24

25

13

18

16

4

17

4

9

7

6

9

7

4

19

$551

$525

$201

$179

$166

$114

$92

$40

$39

$29

$20

$19

$19

$18

$6

$5

$32

Food Ecommerce

Water

Drones & Robotics

Decision Support Technology

Bioenergy

Soil & Crop Technology

Biomaterials & Biochemicals

Sustainable Protein

Cannabis

Food Storage

Animal Nutrition & Health

Waste Mitigation

Farm-to-Consumer (F2C)

Smart Equipment & Hardware

Indoor Agriculture

Food Safety & Traceability

Miscellaneous

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 15

The average deal size for the first

half of 2015 was $9.2M, which is

slightly lower than last year’s

$9.7M. This is noticeably below the

venture capital industry’s overall

average, which was approximately

$17M for H1.1 Agtech is still an

immature sector with a large

number of companies in Seed and

Series A.

During the first half of 2015, a

number of categories, like indoor

farming and sustainable protein,

haven’t had the big later stage

fundings that we saw in 2014.

Average Deal Size

DEALS BY SUBSECTOR

Financing | $Millions

1. Mattermark Q2 2015 – U.S. Venture Capital Activity Analysis. Note: Mattermark data is U.S. only.

$52.5

$18.4

$13.8

$10.6

$10.0

$8.9

$7.2

$7.1

$6.6

$3.8

$3.6

$3.2

$3.0

$2.5

$1.7

$.9

$1.9

Water

Food Ecommerce

Bioenergy

Drones & Robotics

Sustainable Protein

Decision Support Technology

Food Storage

Soil & Crop Technology

Biomaterials & Biochemicals

Smart Equipment & Hardware

Farm-to-Consumer (F2C)

Waste Mitigation

Cannabis

Animal Nutrition

Food Safety & Traceability

Indoor Agriculture

Miscellaneous

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 16

Median deal size paints a good

portrait of what’s happening in the

sector so far this year: for all but 3

categories, the median was under

$5M.

Sustainable protein is worth

highlighting because, despite having

only 4 companies receiving funding,

companies in the sector are showing

strong follow-on investment.

Food ecommerce has a strong

pipeline and continues to see later

stage deals. But newer technology

subsectors, like drones, decision

support, and smart equipment had

small median deal sizes. Many

companies haven’t been around long

enough to move faster.

Median Deal Size

DEALS BY SUBSECTOR

Financing | $Millions

$10.0

$10.0

$8.0

$3.0

$3.0

$3.0

$2.8

$2.5

$2.5

$2.0

$2.0

$1.8

$1.7

$1.3

$.9

$.7

$.8

Sustainable Protein

Bioenergy

Food Ecommerce

Farm-to-Consumer (F2C)

Food Storage

Decision Support Technology

Biomaterials & Biochemicals

Drones & Robotics

Soil & Crop Technology

Water

Animal Nutrition

Waste Mitigation

Food Safety & Traceability

Smart Equipment

Cannabis

Indoor Agriculture

Miscellaneous

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

$135

$85

$70

$45

$35

$30

$25

$20

$16

$14

Blue Apron

Munchery

Fruitday

Sprig

Grofers

NatureBox

Mathem

Beequick

Green Chef

Shopwings

17

The race is on to take over food

delivery. Many of these companies

have similar business models, and

we’re curious to see whether the

industry can sustain the onslaught

of startups and whether the

companies can sustain themselves.

There is a clear trend toward

replicating successful US models

overseas as quickly as possible.

Indian grocery delivery PepperTap

is a good example of this. The

company raised a $1.2M seed

round in March and successfully

raised $10M only one month later

in April, then announcing that

they’re raising a $60M round in the

middle of June.

Spotlight on Food Ecommerce: Top 10 Deals

SPOTLIGHT PRECISION AGRICULTURE

Financing | $Millions

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 18

Drone technologies continue to be

hot despite some concerns about

their promise for application in ag.

Farmer’s Business Network was

the winner in terms of the big data

software play, and Planet Labs’

satellite imagery excited some big

name VCs in its Q1 Series C round.

Precision ag faces an upward

battle because the sector is still in

its first generation. As a result, we

are taking a close look at

distribution numbers from these

players.

Spotlight on Precision Agriculture: Top 15 Deals

SPOTLIGHT PRECISION AGRICULTURE

Financing | $Millions

$118

$75

$50

$21

$15

$15

$14

$11

$9

$9

$8

$7

$5

$5

Planet Labs

DJI

3D Robotics

Pulse Aerospace

Illumitex

Farmers Business Network

3D Robotics

Clearpath Robotics

DroneDeploy

Orbital Insight

Intelescope Solutions

Intermap Technologies

OmniEarth

Skycatch

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 19

DEALS BY STAGE

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 20

Seed stage deals accounted for

approximately 45% of deal volume,

while Series A filled roughly 30% of

total deal volume.

Series A deal activity reflected a

departure from 2014 (and typical

VC stats) because the total amount

raised exceeded other series. The

total has already surpassed the

2014 total of $419M. This is a

leading indicator that companies

are moving from seed to Series A

successfully.

Deal Amount and Volume by Stage

DEALS BY STAGE

Deal Volume

Financing | $Millions

$43

$430

$293

$421

$234

$635101

71

1815

11

12

Seed A B C D Late/Other

1. Mattermark Traction Report 2014. Note: Date is U.S. only and covers the time period from Oct. 1, 2013-Sept. 30, 2014.

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 21

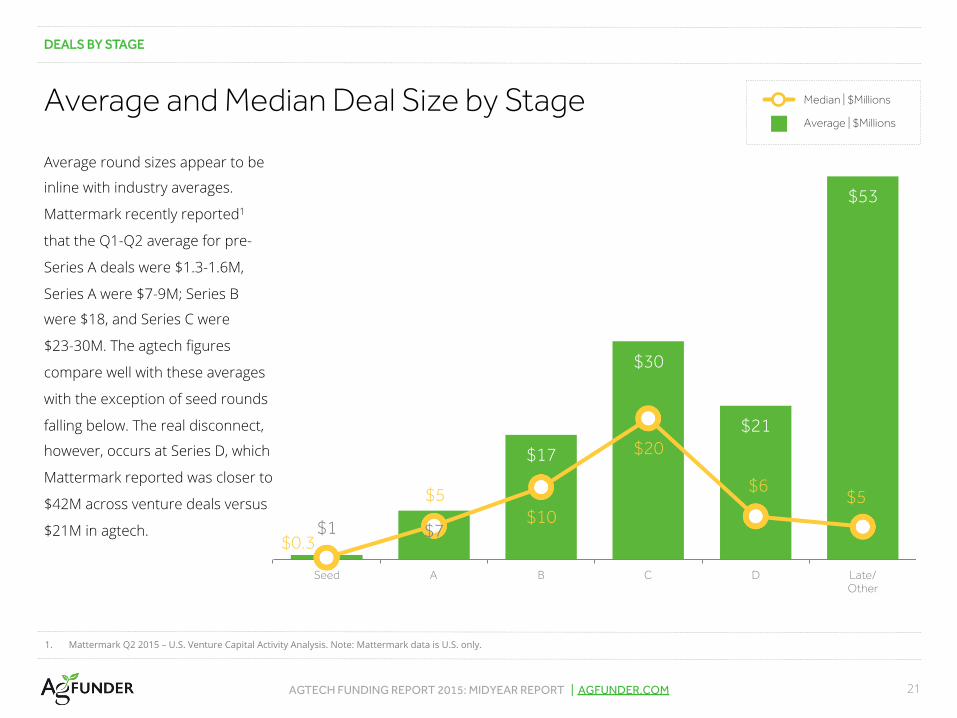

Average round sizes appear to be

inline with industry averages.

Mattermark recently reported1

that the Q1-Q2 average for pre-

Series A deals were $1.3-1.6M,

Series A were $7-9M; Series B

were $18, and Series C were

$23-30M. The agtech figures

compare well with these averages

with the exception of seed rounds

falling below. The real disconnect,

however, occurs at Series D, which

Mattermark reported was closer to

$42M across venture deals versus

$21M in agtech.

Average and Median Deal Size by Stage

DEALS BY STAGE

Median | $Millions

Average | $Millions

$1 $7

$17

$30

$21

$53

$0.3

$5$10

$20

$6$5

Seed A B C D Late/Other

1. Mattermark Q2 2015 – U.S. Venture Capital Activity Analysis. Note: Mattermark data is U.S. only.

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 22

Seed deal volume dropped by half

between Q1 and Q2. At the same

time, average deal size remained

relatively flat: $535k in Q1 versus

$630k in Q2. We’ll monitor this

early stage funding to see whether

this is a temporary dip or a larger

trend in agtech starts.

Otherwise, investment volume in

other stages stacked up similarly

from Q1 to Q2.

Q1 vs. Q2 2015 Deal Volume

DEALS BY STAGE

Q1 Deal Volume

Q2 Deal Volume

66

34

96

95

3537

9 9 2 7

Seed A B C D Late/Other

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 23

Top seed deals through the

midyear represent a diverse range

of sectors. The top five deals hail

from five different categories.

Some of the recent winners, such

as drone and precision ag

companies, are absent from the

list. Food ecommerce, however, is

well-represented, making up 20%

of companies on the list with

Chicory, Thirstie, Yumist, and Farm

Hill.

Top 20 Seed Deals

DEALS BY STAGE

Financing | $Millions

$3.0

$2.4

$2.1

$2.0

$2.0

$1.9

$1.8

$1.3

$1.2

$1.1

$1.0

$1.0

$1.0

$1.0

$1.0

$.9

$.8

$.7

$.7

$.6

PowWow Energy

Exosect

GrubMarket

DroneView Technologies

Back to the Roots

Biosyntia

HeatGenie

XpertSea Solutions

Chicory

Thirstie

Yumist

Farm Hill

Provivi

Eden Shield

Revolution Fuels

Edenworks

Microbial Solutions

Family Fish Farms Network

GrocerKey

Biopipe Global AG

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

$42

$21

$20

$20

$17

$16

$15

$14

$11

$10

$10

$10

$10

$10

$9

$9

$9

$9

$8

$

Zymergen

Pulse Aerospace

Rosa Labs

Soylent

Minnesota Medical Solutions

Green Chef

Godavari

Shopwings

Clearpath Robotics

Eaze

Roadrunnr

PepperTap

ZopNow

Phagelux

DroneDeploy

Ginkgo Bioworks

CropX

Orbital Insight

SeQuent Scientific

Nutresia

24

Biotech startup Zymergen

captured the outsized Series A

deal this year. It jumped from a

$2M seed in 2013 to its $42M

round in June. Looks like it’s taking

a page from Impossible Foods,

which raised a $75M Series A last

year.

Winners in Series A funding

included drones (Pulse Aerospace,

Clearpath Robotics, DroneDeploy),

sustainable protein (Rosa Labs,

Soylent), and Food eCommerce

(Govardi, Shopwings, Roadrunnr,

PepperTap, ZopNow).

Top 20 Series A Deals

DEALS BY STAGE

Financing | $Millions

Undisclosed

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 25

DEALS BY GEOGRAPHY

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

$1028

$510

$155

$111

$85

$35

$27

$24

$23

$22

United States

Israel

China

India

United Kingdom

Canada

Sweden

France

Germany

Switzerland

26

Companies located in the U.S.

continue to dominate when it

comes to receiving funding,

reporting roughly $1B in funding

during Q1 and Q2. Israel came in

second, primarily due to a large

boost it received from a single

funding (Netafim).

China sits at number 3 with total

fundings of $155M, which came

from three deals: DJI, Fruitday and

Phagelux.

Noticeably absent from the top 10

most funded countries is Australia,

which has a large ag industry but

we’re not seeing muhc agtech

activity from there.

Top 10 Countries Receiving Funding

DEALS BY GEOGRAPHY

Financing | $Millions

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

Top 20 U.S. Venture Capital Deals

27

DEALS BY GEOGRAPHY

Financing | $Millions

The top 20 U.S. venture capital

deals in agtech spanned nearly

every sector, with most of the top

deals going to grocery delivery,

sustainable protein, and drones.

The top two deals belong to Blue

Apron ($135M) and Munchery

($85M), both major players in the

food delivery service game.

The third and fourth largest deals

also broached the $50M mark,

with $70M from satellite giant

Planet Labs and $66M from

Arcadia Biosciences.

$135

$85

$70

$66

$50

$45

$42

$40

$30

$25

$23

$22

$21

$20

$20

$17

$16

$16

$15

$15

Blue Apron

Munchery

Planet Labs

Arcadia Biosciences

3D Robotics

Sprig

Zymergen

Joule Unlimited

NatureBox

Planet Labs

Planet Labs

Nomacorc

Pulse Aerospace

Rosa Labs

Soylent Corporation

Minnesota Medical Solutions

EdeniQ

Green Chef

Illumitex

Farmers Business Network

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 28

California-based companies again

dominated agtech investment in

the first half of 2015 with 44 deals,

compared to 68 deals for all of

2014 with a heavy focus on

software-based agtech (drones,

robotics, sensors, big-data, etc.)

and food eCommerce. California

accounted for 31% of all deals in

the U.S. (-6% decrease from 2014).

Colorado, despite ranking 22nd in

population size, continues to see a

significant number of investments

in agtech ranking fourth in number

of investments (9) behind

California (44,) New York (12), and

Massachusetts (10). One-third of

CO companies were in weed-tech.

U.S. Investment: Number of Deals by State

DEALS BY GEOGRAPHY

44

Deals Funded

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 29

Within the U.S., California

continues to dominate the field,

capturing 57% of all U.S. venture

capital deals (+11% increase from

2014). Surprisingly, New York takes

second place with $152M in

financings. This may be due to the

state’s host of food delivery

companies and food-centric tech

companies. Encompassing a

majority of the biotech industry,

Massachusetts came in third with

$68M, which we expect to increase

throughout the year and into 2016.

With the exception of a few states

like Nebraska, many farm-intensive

Midwestern states are absent from

this list.

U.S. Investment: Dollar Value of Deals by State

DEALS BY GEOGRAPHY

Financing | $Millions

$583

$152

$68

$31

$27

$26

$21

$20

$16

$16

$11

$8

$7

$7

$5

$5

$5

$5

$4

$2

California

New York

Massachusetts

North Carolina

Texas

Colorado

Kansas

Missouri

Illinios

Nebraska

Washington

Connecticut

Maryland

Michigan

Minnesota

Virginia

New Mexico

Oregan

Wisconsin

Georgia

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 30

INVESTOR ACTIVITY

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

242

27 7 3 1

x1 x2 x3 x4 x7

31

AgTech had 280 unique investors

in the first half of 2015, surpassing

the 271 unique investors in 2014.

Looking at the deal flow of

investors so far this year, none of

the most active investors (3+ deals)

in 2014 have done more than 3

deals so far this year. In other

words, all of the 3+ investors are

new. This might simply be a timing

issue, but it highlights a new crop

of investors coming to the table.

Sequoia jumped out ahead of

other investors, but a closer look at

their investments shows they are

long on food ecommerce.

Number of Deals by Investors

INVESTOR ACTIVITY

#AgTech Investments Added to Portfolio in 2015

#Investors

Num

ber o

f Inv

esto

rs

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

Grofers$35M Series B

Planet Labs$70M Series C

Holganix$100k Seed

Planet Labs$70M Series C

Planet Labs$70M Series C

Beequick$20M Series B

Zymergen$42M Series A

TerViva$100k Seed

Zymergen$42M Series A

Zymergen$42M Series A

PepperTap$10M Series A

Ginko Bioworks$9M Series A

Solapa4$100k Seed

EdeniQ$16M Series B

CropX$9M Series A

Grofers$10M Series A

DroneDeploy$9M Series A

AGERpoint$50k Seed

Roadrunnr$10M Series A

Orbital Insight$8.7M Series B

PepperTap$1.2M Seed

32

Investments by Top 10 Most Active Investors1

INVESTOR ACTIVITY

1. CapAgro wasn’t included in the list because deals are undisclosed.

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

DJI$75M Series B

Munchery$85M Series C

3D Robotics$64M Series C

Green Biologics$42M Series C

GrocerKey$690k Seed

ZopNow$10M Series A

Vicampo$4M Series A

ZopNow$10M Series A

Exosect$2.4M

GrocerKey$20k Seed

TeaBox$6 M Series A

Wine in BlackFunding Undisclosed

Inova Drone$120,000k Seed

Microbial Solutions$767k Seed

Bright Cellars$20k Seed

33

Investments by Top 10 Most Active Investors1 (cont.)

INVESTOR ACTIVITY

1. CapAgro wasn’t included in the list because deals are undisclosed.

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM

0 1 2 3 4 5 6 7

Sequoia CapitalData Collective

CapAgroThe Yield Lab

Draper Fisher Jurvetson (DFJ)Innovation Endeavors

Accel Partnerse.ventures

Qualcomm VenturesOxford Capital Partners

gener8torAME Cloud Ventures

Northgate CapitalTrue Ventures

Felicis VenturesLux Capital

SAIF PartnersSanDisk Ventures

WestSummit CapitalAtlantic Bridge

Tiger Global ManagementSofinnova Partners

Flagship VenturesSpace Angels Network

Kleiner Perkins Caufield & ByersAndreessen Horowitz

Google VenturesLerer Hippeau Ventures

Dragoneer Investment GroupOurCrowd

Union Square VenturesCultivation Capital

3wVenturesPassion Capital

BioGeneratorCherrystone Angel Group

Founder.orgNMotion

34

Investors with 2+ Deals

INVESTOR ACTIVITY

Between 2014 and 2015, one thing is

crystal clear. The diversity among

investors is increasing rapidly and

bringing more breadth and depth to

the sector’s ecosystem.

Today’s agtech investors include a

global cast with dedicated funds, tech

VC, accelerators, and some small-scale

investors. With many of these

investors making their debut

appearance on this list, we expect the

roster to increase by the end of the

year and well into 2016.

Number of Deals in H1 2015

AGTECH FUNDING REPORT 2015: MIDYEAR REPORT | AGFUNDER.COM 35

AgFunder is an online equity crowdfunding platform for agriculture.

We help Accredited and Institutional Investors discover & invest in developing

technologies to transform the agriculture industry.

See our list of live investments www.agfunder.com

Learn more @ www.agfunder.com Contact us @ [email protected]

Last updated July 30, 2015