INVESTING IN MARITIME INDONESIA - Mare Forum · Investing in Maritime Indonesia 2 Total area + 1.9...

28

INVESTING IN MARITIME INDONESIA BANI M MULIA

-

Upload

truongminh -

Category

Documents

-

view

216 -

download

0

Transcript of INVESTING IN MARITIME INDONESIA - Mare Forum · Investing in Maritime Indonesia 2 Total area + 1.9...

INVESTING IN MARITIME INDONESIA

BANI M MULIA

2 Investing in Maritime Indonesia

Total area + 1.9 milllion sq km. 2/3 is covered by

water

95,181 km of sea line 4th longest in the world after

Canada, USA and Russia

Approx 17, 480 islands separated by sea

Archipelago

Growing conomy

Sea Transportation

3 Indonesia

Fourth largest population in the world : 241

million

Substantial natural resources

6.5% economic growth in 2011.

GDP per capita is predicted to reach USD 4,140

in 2013

4

Sources : McKinsey

Jakarta-based Routes

BELAWAN

PADANG BATAM

PANJANG

JAKARTA

SURABAYA

PONTIANAK

SEMARANG

BANJARMASIN

SAMARINDA

TARAKAN

BONTANG BITUNG

`` GORONTALO PANTOLOAN

KENDARI

MAKASAR

TERNATE

AMBON

MANOKWARI

SORONG

MERAUKE

KUPANG

BENETTE BENOA

BIAK

PEKANBARU

PERAWANG

PALEMBANG

JAYAPURA BENGKULU

BALIKPAPAN

Surabaya-based Routes

BELAWAN

PADANG

PERAWANG

BATAM

PANJANG

JAKARTA

SURABAYA

PONTIANAK

SAMPIT

SAMARINDA

TARAKAN

BONTANG

`` GORONTAL

O PANTOLOAN

TERNATE

AMBON

MANOKWARI

SORONG JAYAPURA

MERAUKE

KUPANG

BIAK

DILI

TIMIKA

KENDARI

MAKASAR

LUWU

K

TOLI-

TOLI

TOBELO

BATULICIN

KUMAI

BALIKPAPAN

BANJARMASIN

BITUNG BERAU

NUNUKAN

TUAL

FAK-FAK

KAIMANA

SERUI

NABIRE

LEMBAR MAUMERE

BENOA

Container Throughput Jakarta & Surabaya Based

DESCRIPTION 2010 2011 2012

JKT BASED 810,086 906,292 1,066,037

SUB BASED 652,905 758,553 784,405

TOTAL 1,462,991 1,664,845 1,850,442

(in TEUs)

Sources : Samudera Internal Data

9 Pendulum Nusantara

Belawan

Batam

Jakarta

Surabaya

Sorong

Makassar

Source : Ministry of Transportation Republic of Indonesia

KALIBARU TERMINAL DEVELOPMENT PLAN

JAKARTA

Descriptions Stage I

(2011–2013)

Stage II

(2013–2016)

Stage III

(2016–2019)

INFRASTRUCTURE - WHARF (Draft -18m LWS)

- BACK UP AREA

- CAPACITY

1.000 m’

60 ha

1.5 Million TEU

1.200 m’

108 ha

1.8 Million TEU

1.500 m’

90 ha

2.2 Million TEU

EQUIPMENTS

- Quay Container Crane

- Rubber Tired Gantry Cr

- Head Truck

- Chassis

- Reefer

10 units

30 units

62 units

70 units

200 units

12 units

40 units

83 units

90 units

200 units

15 units

46 units

104 units

110 units

200 units

Current terminal capacity

5.8 mio teus

PORT DEVELOPMENT TO SUPPORT PENDULUM NUSANTARA

TANJUNG EMAS

TELUK LAMONG TANJUNG PRIOK

BELAWAN

12

Palaran Container Terminal

Samarinda

• BOT contract 50 years concession

• Wharf 270 meter.

• Draft 6 meter.

• Capacity of 200,000 TEUs per year (phase 1)

• Provided with :

• 2 Unit CC 40 ton

• 5 Unit RTGC

• Start Operation : end of 2009

158 174 193 220 242 266 293

322 354 379 406

434 464

497 522 548

-

100

200

300

400

500

600

700

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Tho

usa

nd

s

TPK Palaran Volume Projection (in TEUs)

CY existing CY existing + extension Existing+extension+ TPK 2

TPK 1+ext 1+ TPK 2+ext 2 Volume

Container Volume Projection – TPK Palaran

Existing Capacity

Add Capacity by CY Extension

Add Capacity by TPK-2

Add Capacity by CY Extention 2

Confidential & proprietary of PT. Samudera Indonesia Tbk

TPK PALARA

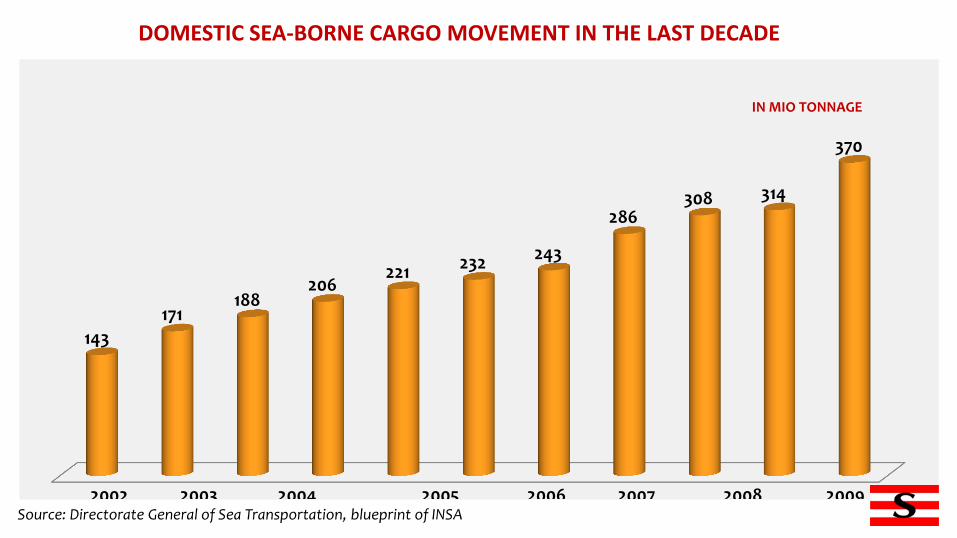

143

171 188

206 221 232 243

286 308 314

370

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

IN MIO TONNAGE

DOMESTIC SEA-BORNE CARGO MOVEMENT IN THE LAST DECADE

Source: Directorate General of Sea Transportation, blueprint of INSA

DOMESTIC SEA-BORNE CARGO MOVEMENT IN THE LAST DECADE

Source: Directorate General of Sea Transportation, blueprint of INSA

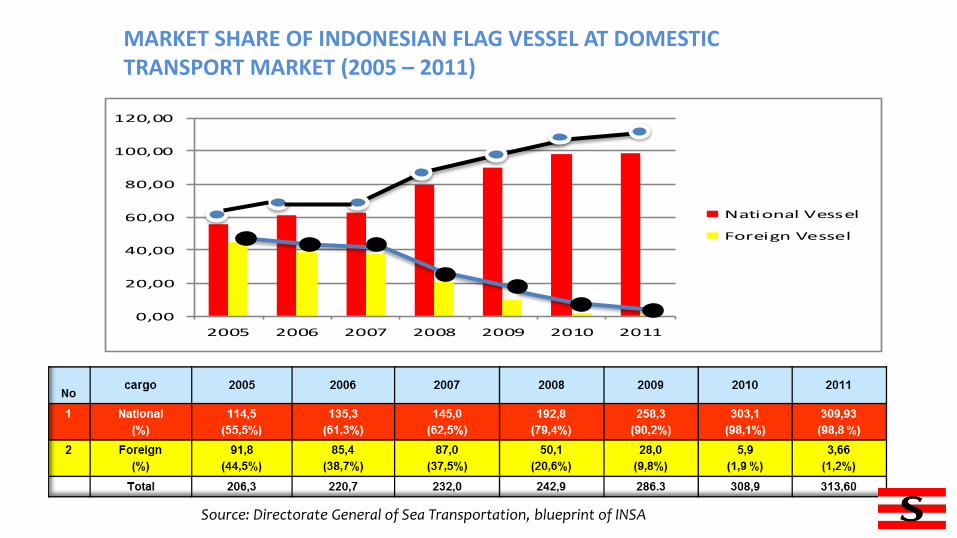

MARKET SHARE OF INDONESIAN FLAG VESSEL AT DOMESTIC TRANSPORT MARKET (2005 – 2011)

Source: Directorate General of Sea Transportation, blueprint of INSA

0,00

20,00

40,00

60,00

80,00

100,00

120,00

2005 2006 2007 2008 2009 2010 2011

National Vessel

Foreign Vessel

MARKET SHARE OF INDONESIAN FLAG VESSEL AT EXPORT-IMPORT

Source: Directorate General of Sea Transportation, blueprint of INSA

No Cargo 2006 2007 2008 2009 2010

1 National

(%)

29,4

(5,7%)

31,4

(5,9%)

38,2

(7,1%)

49,3

(9,0%)

51,2

(9,0%)

2 Foreign

(%)

485,8

(94,3%)

500,5

(94,1%)

498,2

(92,9)

501,7

(91,0)

516,1

(91,0)

Total 515,2 541,0 536,4 551,0 567,2

INDONESIAN SEA-BORNE CARGO MOVEMENT SOON TO HIT NEW RECORD

TOTAL Indonesian Sea-Borne Cargo

Will soon to reach

1 Billion Tonnage in 2—3 years ahead , with potential Freight business

turnover to reach

US$25 Billion. Indonesian Shipping Industry will have to be prepared

to grab opportunities arising from this

• Number of vessels as per 31st October 2012 are 11.628 units (16,08 mio GT) • Number of vessels as per 31st March 2005 are 6.041 unit (5,67 mio GT) • Therefore there increasing number of vessel 5.587 units (92%) with total tonnage

10.41 mio GT (184%)

31st March 2005 31st Oct 2012

No. of Ships 6.041 11.628

0

1.500

3.000

4.500

6.000

7.500

9.000

10.500

12.000

13.500

Un

it V

esse

l

5.587 units (92 %)

11.628

6.041

NUMBER OF INDONESIAN FLAG VESSELS

> 16 mio GT

11.628 vessels

> 19 mio DWT

Indonesian Economic Overview

1989

(306)

1999

(747)

2009

(1.064)

2011

(1.168)

2013

(1.293)

THE GROWTH OF INSA MEMBERS

2.150

2.200

2.250

2.300

2.350

2.400

2.450

2.500

2.273

2.655

382 unit (16,8%)

• Based on Shipping Licenses (SIUPAL and SIOPSUS) issued by Sea Com DG - Ministry of Transport, Republic of Indonesia, the number of shipping companies in Indonesia as per October 2012 is 2.655 units

2010 2012

THE GROWTH OF SHIPPING COMPANIES

NATIONAL SHIPPING COMPANIES LISTED IN IDX

Number of national shipping companies listed in the Indonesian Stock Exchange increased 320 % from 5 companies in 2000 to 21 companies in 2013 (including those consolidated in respectives holding companies)

0

2

4

6

8

10

12

14

16

18

7

21

5

Units

2000 2005 2013

No Company ID Activity Registered

1 PT Berlian Laju Tanker Tbk BLTA Transport - Marine 26-Mar-90

2 PT Rig Tenders Indonesia Tbk RIGS Transport - Marine 26-Mar-90

3 PT AKR Corporindo Tbk AKRA Distribution/Wholesale Sep-94

4 PT Mitra Internasional Resources MIRA Transport - Marine 30-Jan-97

5 PT Samudera Indonesia Tbk SMDR Transport - Marine 05-Jul-99

6 PT Tanah Laut Tbk INDX Infrastructure, Utilities and Transport

17-Mei-01

7 PT Arpeni Pratama Ocean Line Tbk APOL Transport - Marine 22-Jun-05

8 PT Ancora Indonesia Resources Tbk OKAS Petrochemicals 29-Mar-06

9 PT Radiant Utama Interinsco Tbk RUIS Oil Comp-Explor&Prodtn 12-Jul-06

10 PT Humpuss Intermoda Trans Tbk HITS Transport - Marine 15-Des-07

11 PT Elnusa Tbk ELSA Oil-Field Services 06-Feb-08

12 PT Trada Maritime Tbk TRAM Transport - Marine 10-Sep-08

13 PT Pelayaran Tempuran Emas Tbk TMAS Transport - Marine 31-Des-09

14 PT Wintarmar Offshore Marine Tbk WINS Transport - Marine 29-Nop-10

15 PT Mitrabahtera Segara Sejati Tbk MBSS Transport - Marine 06-Apr-11

16 PT Buana Listya Tama Tbk BULL Transport - Marine 23-Mei-11

17 PT Indo Straits Tbk PTIS Transport - Marine 12-Jul-11

18 PT ABM Investama Tbk ABMM Diversified Operations 06-Des-11

19 PT Pelayaran Nelly Dwi Putri Tbk NELY Transport - Marine 10-Nop-12

20 PT Pelayaran Nasional Bina Guna Raya Tbk BRRM Transport - Marine 09-Jan-13

21 PT Trans Power Marine Tbk TPMA Transport - Marine 20-Feb-13

List of Shipping Companies Listed in IDX

OPPORTUNITY FOR SHIPYARD INDUSTRY

• Number of shipyards in Indonesia is approx 250 shipyards, local shipyard capacity for docking and repair is approx 12 mio DWT

• Given such fact, the capacity of shipyards in Indonesia is still under the amount of 19,5 mio DWT Indonesian vessel (current condition)

• There’s an opportunity for shipyard industry to grow in order to support demand from Indonesian shipping industry

Current issue • On 27th February 2013, Indonesia Ministry of Trade signed

MoU with several industry Associations : – INSA (Indonesia National Shipowners' Association),

– Apindo (Employers' Association of Indonesia),

– ALFI/INFA (Indonesian Forwarders' Association),

– Indonesia Eximbank

• The MoU is related to the conversion the term of delivery from FOB to CIF for export activities

• The Aim is to boost Indonesian export. It will also have a direct impact to shipping industry, as it will encourage Indonesian investors to invest more on shipping sector

THANK YOU