Investing in Indonesia’s - EUIND - TCF · connect all of its islands from Sumatera to Papua in...

37

© 2015 by Indonesia Investment Coordinating Board (‘BKPM’). All rights reserved Investing in Indonesia’s seaports sector An overview of opportunities, capabilities and provisions Version: December 2015

Transcript of Investing in Indonesia’s - EUIND - TCF · connect all of its islands from Sumatera to Papua in...

© 2015 by Indonesia Investment Coordinating Board (‘BKPM’). All rights reserved

Investing in Indonesia’s

seaports sector

An overview of opportunities, capabilities and provisions

Version: December 2015

The Investment Coordinating Board of the Republic of Indonesia

2

Contents

An introduction 3

Why Indonesia? 4

Seaport sector overview 5

Market opportunities 6

Existing and future capabilities 23

Government provisions and support 31

Good reasons to invest in Indonesia’s seaport sector 37

The Investment Coordinating Board of the Republic of Indonesia

3

Introduction

The Government of Indonesia aims to establish a “maritime toll road” as part of its strategy to

connect all of its islands from Sumatera to Papua in order to improve logistics, reduce inflation

and create a greater impact on economic prospects for the Indonesian people.

The concept of a “maritime toll road” is to implement a sea transportation network across the

Indonesian archipelago by using large sea vessels from Belawan (Sumatera) right across to the

Eastern part of Indonesia in order to maximize economic connectivity.

This ambitious programme offers abundant opportunities for foreign investors.

Source: Badan Kordinasi Penanaman Modal

The Investment Coordinating Board of the Republic of Indonesia

4

Why Indonesia?GOVERNMENT PROVISIONS

& SUPPORT

Foreign seaport companies

which provide harbor facilities

can now have 95% ownership

(up from 49%).

Multimode of transportation

business is now open with up

to 49% foreign ownership. This

represents progress since it was

not previously open

The recently issued and

improved Presidential

Regulation No.38/2015

regarding PPP in infrastructure.

Sources: BKPM, CMEA

MARKET

OPPORTUNITIES

The Government of Indonesia

plans to build 24 new seaports,

270 ferry ports and 104 pioneer

vessels.

Efforts to increase fishery

products, improve fishery ports

and increase sea conservation

areas across the country.

65 locations for industrial

estates, 8 Special Economic Zones and 4 Free Trade Zones.

EXISTING & FUTURE

CAPABILITIES

Government will spend IDR 498

trillion on sea transportation.

State Owned Enterprises (SOEs)

will spend IDR 238.2 trillion for

this purpose and IDR 163.8

trillion will be sought from the

private sector from 2015-2019.

Currently there are 4 SOE port

operators in Indonesia : PT

Pelindo I-IV and private

operators in Indonesia. In total.

there are 10 port operators in

Indonesia.

Total passenger flows and

container flows are on the rise.

Source: CMEA, BKPM Sources: Ministry of Transportation

The Investment Coordinating Board of the Republic of Indonesia

5

Seaports Overview

According to the World

Bank, Indonesia ranks in

the middle among other

ASEAN countries with an

improvement from 2.94 to

3.08.

Indonesia currently has 44

seaports across the

country.

The Government of

Indonesia is to establish 24

new seaports from 2015-

2019 across the country.

The 24 new planned

seaports hows the serious

intention of the GoI in

advancing the maritime

toll road in the next five

years and connecting the

archipelago through an

ambitious logistics plan.

Source : Ministry of Transportation Source: Ministry of Transportation Source: World Bank

ASEAN’s Logistic

Performance Index

2010-2014

Current number of

seaports and future

plans

Number of airports

compared to seaports

Singapore: 4.00

Malaysia: 3.59

Thailand: 3.43

Indonesia: 3.08

The Philippines: 3.00 Current seaports (44) New seaports (24) Current airports: 39 Current seaports: 44

Market Opportunities

© 2014 by Indonesian Investment Coordinating Board. All rights reserved

SECTION DIVIDER SLIDE

SECTOR-RELEVANT IMAGE TO BE INSERTED

The Investment Coordinating Board of the Republic of Indonesia

7

World’s largest

archipelago country

17,000 islands

3,500 miles wide

Indonesian Seaport : The Push Factors

Indonesia is the world’s

17th largest GDP with US$

856 billion and a per

capita income of US$

3,587. Its trade activity is

getting stronger.

Indonesia’s vast size provides

huge maritime business

opportunities for foreign and

domestic investors in

Indonesia.

The Government has

pledged to improve logistics

within the country between

2015-2019.

The Government of

Indonesia is improving its

trade policies and pushing

exports to major economic

spots in Asia, Australia, North

America, Central America

and Middle East.

Indonesia features among the

locations with the world’s top 25

busiest seaports. Tanjung Priok

Port in Jakarta ranks 22nd globally

The traffic of goods between

Asia and North America and

North Europe had a total of 36

million TEUs in 2012.

Source: IMFSources: Bappenas Source: World Bank

Home to the world’s

22nd busiest seaport

in 2013 with volume

of 6.59 million TEUs.

The Investment Coordinating Board of the Republic of Indonesia

8

Sector Trends : Passengers for Sea Vessels

Passenger trends

7.63% Annual

Average

Growth

Source: BPS, Ministry of Transport

Year 2008 2009 2010 2011 2012 2013 2014

Number of

passengers

(million)

6.16 5.94 7.1 6.08 6.18 8.9 13.1

• Indonesians still use sea transport extensively, especially during holiday periods like religious

celebrations and school holidays. During holiday seasons many people use sea transportation

to go back to their home towns. Sea transport is still more affordable than flying.

• The figure went down in 2011 due to a restriction from Ministry of Tranport on old vessels

which were no longer seaworthy. The number of sea passengers has since recovered

however, with a significant increase in 2013-14

The Investment Coordinating Board of the Republic of Indonesia

9

Sector Trends : Cargo for Sea Vessels

Cargo trends

16.87% Average

Growth from 2011-2013

Source: BPS, Ministry of Transport

Year 2008 2009 2010 2011 2012 2013 2014

Number of

cargo in

million tons

162.5 146.9 109.3 156 176.1 225 216.7

• Transporting cargo by sea is still dominant in Indonesia due to low costs and the

ability of the vessels to reach distant islands across the archipelago.

• The figures have fluctuated due to fuel price fluctuations and several shipping

companies still choose airplanes for faster delivery to certain regions in Indonesia.

• Going forward, the outlook for sea cargo remains promising however.

The Investment Coordinating Board of the Republic of Indonesia

10

A Glimpse of Seaport Industry in Indonesia

Total Passengers in 2014:

13.1 million people

Total of cargo in 2014:

216.7 million tonnes

Main Ports in Indonesia:

Belawan, Tanjung Priok,

Tanjung Perak,

Makassar and

Balikpapan.

Port Operators in

Indonesia

Four State-Owned-

Company Port

Operators: Pelindo 1-4

and other private port

operators. Currently

there are a total of 10

port operators in

Indonesia.

Trade and

Movement of GoodsMain Ports in

The Country

Source: Ministry of Transport,

PT SMI

With the anticipated

consolidation of the AEC

moving into 2016 and

beyond, Indonesia will

experience a surge in

trade activties and

movement of people by

sea transportation.

The above major ports

cover the majority of

movement of goods and

people from the Western

part of the country into

the Eastern part of the

country.

Source: Ministry of Transport,

PT SMI

There are 4 State Owned

Company of port

operators in Indonesia

from Sabang to Merauke

and a total of 10 port

operators existing in the

country. Private

companies can operate

ports in Indonesia.

Source: Ministry of Transport,

PT SMI

The Investment Coordinating Board of the Republic of Indonesia

11

Infrastructure Ratings of Indonesian Ports & Infrastructure

Indonesia has improved its position in the Wold Economic Forum’s Global

Competitiveness Index, reaching number 38 in 2013-2014, an improvement from number

50 in 2012-2013. The overall Infrastructure sector has also increasing its rating from number

78 in 2012-2013 to number 61 in 2013-2014.

Indonesia’s port infrastructure rating has also improved considerably - from number 103 in

2011-12 to 89 in 2013-14.

Source: WEF Global Competitiveness Report 2011-2014

No. Year Indonesia Rating

1. 2011-2012 103/142

2. 2012-2013 104/144

3. 2013-2014 89/143

Country Ranking

Switzerland 1

Singapore 2

Finland 3

Germany 4

United States 5

Malaysia 24

Brunei 26

Thailand 37

Indonesia 38

Philippines 59

Vietnam 70

Global Competitiveness Index

Port Infrastructure rating

The Investment Coordinating Board of the Republic of Indonesia

12

MP3EI*- Master Plan for Economic Expansion in

Indonesia for Ports

• The projected investment for MP3EI is IDR 4,000 trillion and based on that amount 44%

(or IDR 1,774 trillion) will be allocated in infrastructure - 6% of which (IDR 117 trillion) will

be allocated to sea port development.

• In line with President Joko Widodo’s priority to develop areas outside Java, the

indication are that 46% of the total investment for port developments will be in

Sumatera and 35% for Kalimantan.

*MP3EI: Master Plan for Acceleration and Expansion of Indonesian Economic development

The Investment Coordinating Board of the Republic of Indonesia

13

Indonesia’s Main Ports

• Tanjung Priok Jakarta is the biggest and busiest port in Indonesia, Tanjung Priok’s capacity is

increasing gradually from 5.62 million TEUs in 2011 to 6.2 million TEUs (8.5% growth). During the past

10 years the container throughput in Tanjung Priok port has increased three times from 2.4 million

TEUs to 6.2 million TEUs.

• During the past five years, container throughput in Port Tanjung Perak grown 1.5 times from 1.5

million TEUs to 2.9 million TEUs close to the total capacity of 3.01 million TEUs.

• The Port of Belawan provides major facilities including: a liquid bulk terminal, dry bulk terminal,cargo load/unload container, passenger terminal, navigation services, space and warehousing

services within the port area. The Port of Belawan along with other ports in Sumatera will be

revitalized into international hubs.

• Container flow in Makassar Port reached 11.4 million tons in 2013 .

The Investment Coordinating Board of the Republic of Indonesia

14

Potential Seaport Project: New Tanjung Priok Port

.

.

.

.

Project profile: The construction of a new port - an extension of Indonesia's

busiest port, Tanjung Priok - is one of the biggest public projects currently in

development in Indonesia. The Tanjung Priok harbor in North Jakarta which

handles more than half of total goods that are exported from or imported to

Indonesia has however become overloaded over the years. The New Priok

project will bring Indonesia's port facilities on par with other world-class

ports

Projected value of investment:

Phase 1: US$ 2.47 billion, Phase 2: US$ 1.50 billion

Government contracting agency: Ministry of Transport & Pelindo II.

The Investment Coordinating Board of the Republic of Indonesia

15

Potential Seaport Project: New Tanjung Priok Port

.

.

.

.

When the whole project is

completed, Jakarta's

Tanjung Priok Port will

increase its annual capacity

from five million twenty-foot

equivalent units (TEU) of

containers to 18 million TEU

and will be able to facilitate

triple-E class container ships

(with a 18,000 TEU capacity)

in a 300 meter-wide two-

way sea lane.

Tanjung Priok was originally

designed to handle five

million TEU of container

traffic per year. In 2011,

however, container traffic in

this harbor reached 5.8 TEU,

indicating the necessity to

expand its infrastructure.

The Investment Coordinating Board of the Republic of Indonesia

16

Potential Seaport Project: Expansion of Cargo Terminal at

Belawan, North Sumatera

.

Project profile: The terminal will improve its capacity from the current 1.2 million TEUs to

2.2 million TEUs/year (or an 83% increase). It will involve the construction of a 350 m pier,

a causeway and stacking yard with a capacity of 400,000 TEUs. The harbor draft will also

be deepened to enable 5,000 TEU capacity vessels to enter the port. The Belawan port is

being envisioned to become the country’s main logistics gateway to compete with

neighboring Singapore and Johor Baru in Malaysia.

Projected value of investment: US$ 230 million

Government contracting agency: Ministry of Transport & Pelindo I.

The Investment Coordinating Board of the Republic of Indonesia

17

Potential Project: Development of Kuala Tanjung Port,

North Sumatera

.

Project profile: Once all the four stages are completed in 2019, the Kuala Tanjung Seaport will have

a 3.5 million ton of wet and one million ton of dry bulk capacity terminals, a 400,000 TEUs per year

container terminal, and a new 400-meter-long pier. The first stage of the Kuala Tanjung Seaport

project will be completed in 16 to 18 months with the development of a 400-meter-long pier, utilities

and equipment will be set up, and information technology installations will be made.

The second stage of the venture will include the development of a 10-hectare stacking yard and a

1,000-hectare industrial zone. While improving transshipment activities, such as loading and

unloading, from Kuala Tanjung to other ports in the world will be part of the third stage, the president

director explained that the fourth stage will include transforming Kuala Tanjung into a city port.

Projected value of investment: US$ 2 Billion.

Government contracting agency: Ministry of Transport & Pelindo I.

The Investment Coordinating Board of the Republic of Indonesia

18

Potential Project: Development of Tanjung Perak Port,

East Java

.

Project profile: The existing port of Tanjung Perak has been consistently operating over its

general cargo capacity of 3.57m tonnes per year, with volumes reaching more than 7m

tonnes in 2012. The first phase of the new Teluk Lamong terminal, which began

construction in 2010, will encompass a 500-sq-metre international yard, 450-sq-metre

domestic yard, a 10-ha dry bulk yard and a 15. 86-ha container storage yard. The

second phase of the project is planned to start in 2016 and is set to include development of a further 50 ha.

Projected value of investment: US$ 250 million.

Government contracting agency: Ministry of Transport & Pelindo III.

The Investment Coordinating Board of the Republic of Indonesia

19

Potential Project: Development of Bitung Port,North

Sulawesi

.

Project profile: Until the end of 2014, stevedoring traffic in Bitung Port has reached

200,000 TEUs or a 37.93-percent hike year on year. If vessel traffic from eastern Indonesia

increases the stevedoring will exceed 20% in this year. The existing Bitung container

yard utility rate has reached more than 80% so container traffic is too crowded. Ideally,

the container yard utility rate should be around 60%. The first phase of 65-meter berth

expansion has been conducted which will be followed by another 65-meter expansion project in this year.

Projected value of investment: US$ 500 million.

Government contracting agency: Ministry of Tranport & Pelindo IV.

The Investment Coordinating Board of the Republic of Indonesia

20

Potential Project: Development of Makassar, South Sulawesi

.

Project profile: According to the firm’s business plan, Pelindo IV will construct a port with

capacity for between 250,000 and 300,000 twenty-foot equivalent units (TEUs) in the first

phase to help support the existing Soekarno-Hatta Port in Makassar. The firm has

prepared a 106 hectare site for Makassar New Port’s container terminal and another 106

hectares for a multipurpose terminal. It has also prepared an 11.92 hectare area for

warehouse facilities and an industrial zone that will support logistics at the port, given

that Makassar is the logistics hub for transshipment in the east, along with East Java’s

Tanjung Perak Port. In the first phase, the port will be built with a draft of 14 meters and a

320 meter dockyard in order to allow large vessels, such as the Panamax and Post-

Panamax, to enter.

Projected value of investment: US$ 421.55m.

Government contracting agency: Ministry of Transport & Pelindo IV.

The Investment Coordinating Board of the Republic of Indonesia

21

Future Opportunity : Indonesia Shipping & Shipyard Industry

Fact: Indonesia has more than 100 commercial and small ports, many of which can only serve

quite small vessels on domestic runs and there are only a few which have container facilities. The country has a

shortage of large ports with capability to serve trans-oceanic ships and the result is Tanjung Priok port has been

burdened with the large number of Indonesia’s exports and imports (about 67%). The port is currently

handling 5 million TEUs a year compared to Singapore’s ability to serve more than 31 million TEU.

Indonesia is also facing increasing demand for domestic shipping. In 2005 the number of vessels was

6,041 and in 2013 the number had increased to12,536. The rising number of vessels has tripled the total volume

capacity from 5.67 million GT in 2005 to 17.89 million GT in 2013.

The country has 200 shipyards. It has a combined annual new-building capacity of 800,000 dead weight tonnes

(DWT) and maintenance capacity of 10 million DWT.

Opportunity: Batam-Bintan-Karimun FTZ is developing into a shipbuilding center. In shipping, while

Foreign ships are prohibited in the domestic shipping, a local presence or participation of local companies

allows investors to capitalize on the large demands of transporting people and goods across the world’s largest

archipelago.

Source: INSA, GBGinvestments

Existing and Future Capabilities

© 2014 by Indonesian Investment Coordinating Board. All rights reserved

SECTION DIVIDER SLIDE

SECTOR-RELEVANT IMAGE TO BE INSERTED

The Investment Coordinating Board of the Republic of Indonesia

23

Maritime Academy of Jakarta

http://www.stipjakarta.ac.id

Sekolah Tinggi Ilmu Pelayaran (Maritime Higher Education Institute) is

a state owned maritime institution administered under the Indonesian

Ministry of Transportation. It was founded in 1953, in the name of

Akademi Ilmu Pelayaran (Merchant Marine Academy) running a 3 - 4

year program of Diploma III (equal to Bachelor Degree) majoring in

Nautical and Technical Departments with Class III Certificate of

Competence.

Key universities and institutes

Business Maritime Academy at Semarang, Central Java www.akpelni.ac.id

It was founded in 1964 and offers Diploma III in maritime, vessel

engineering, port and merchant maritime. In 2001 the Academy

received ISO certification from QAS Limited Australia.

Maritime Academy of Yogyakartawww.akademimaritim.com

The academy provides D3 curriculum in merchant maritime and port

studies as well as working with private companies for apprenticeship

and job placements for its students and graduates.

The Investment Coordinating Board of the Republic of Indonesia

24

Established in 1960, PT Pelindo II was established in 1960. The

company was under the management of the Ministry of State

Owned Enterprise in 1998/1999. It manages 12 ports in 10

provinces (West Sumatera, Jambi, South Sumatera, Bengkulu,

Lampung, Bangka Belitung , Banten, DKI Jakarta, West Java and

West Kalimantan). It also owns and supervises The Jakarta

International Cargo Terminal at Tanjung Priok. The company’s

website is: www.indonesiaport.co.id. The company’s HQ is in

Jakarta.

Established in 1945, PT Pelindo I was under the Dutch

management until 1951. From 1960 it became a State Owned

Company (SOE) and is still under the mangement and supervision

of Ministry of State Owned Enterprises. This company manages

Nanngroe Aceh Darussalam, North Sumatera, Ria and Ria Islands.

The company’s website is: www.inaport1.co.id. The Headquarter’s

office is in Medan, North Sumatera.

Key State-Owned Enterprises (SOEs)

The Investment Coordinating Board of the Republic of Indonesia

25

Created in 1957, Pelindo IV is the main engine for the growth,

trade and development for eastern Indonesia. The company in

1960 was under the Government of Indonesia’s ownership,

previuosly from Dutch government. In 1992 the company became

a State Owned Company and is still under the management and

supervision of the Ministry of State Owned Companies. PT Pelindo

IV manages and owns ports in the eastern part of Indonesia such

as in East Kalimantan, North Sumatera, South Sumatera, Central

Sulawesi, West Sulawesi, Ambon and Papua. Its HQ is in Makassar,

South Sulawesi. The company’s official website is

www.inaport4.co.id

Key State-Owned Enterprises (SOEs)

PT Pelindo III was established in 1960 and in 1992 the company

was under the management of Ministry of State Owned

Company. It manages 43 ports in 7 provinces such as in East Java,

Central Java, South Kalimantan, Central Kalimantan, Bali, West

Nusa Tenggara, East Nusa Tenggara and other 7 subsidiaries. The

company’s website is: www.pelindo.co.id. Pelindo III’s

Headquarters is in Surabaya, East Java.

The Investment Coordinating Board of the Republic of Indonesia

26

Existing key foreign companies (1)

Website : www.vale.com

JICT covers a total of 100 hectares and is the largest container

terminal in Indonesia. JICT handles more than 2.2 million TEUs

(Twenty foot Equivalent Units) per year and is strategically located

at the industrial heartland of West Java.

JICT is owned by Hutchison Port Holdings (HPH), a subsidiary of the

multinational conglomerate Hutchison Whampoa Limited (HWL), is

the world's leading port investor, developer and operator.

From 2008-2013 JICT invested more than US$ 151 million for system

upgrading and increasing the capacity of its human resources.

Pelindo II’s cooperation with HPI in JICT has been conducted since

1999. Following the investment, stevedoring capacity in JICT

increased from 1.4 million TEUs to 3 million TEUs in 2013. JICT also

keeps increasing the investment to improve its service through the

implementation of new technology, human resources quality

improvement, and new equipment procurement. From 2008-2013,

the total investment disbursed by JICT reached USD 151 million.

In 2014, JICT announced an additional investment of USD 40 million.

The budget will be used for procuring equipment and building a

new entry gate – namely an automatic gate system (AGS)

connected with JORR which will be built in the port.

Website : www.jict.co.id

Vale has been managing 2 ports in

Indonesia and investing at those 2

ports as well.

Located in Balantang, a village in the

province of South Sulawesi, this port

has two different docking facilities with

a total capacity of 6,000 DWT. Vale’s

stake: 59.3% – operated in partnership

with Sumitomo and public investors.

Located in the village of Lampia, also

in South Sulawesi, this port has

mooring buoys that can

accommodate ships of up to 20,000

DWT, and a terminal that can service

tanker vessels of up to 2,000 DWT,

providing total capacity of 22,000

DWT. Vale’s stake: 59.3% – operated

in partnership with Sumitomo and

public investors

The Investment Coordinating Board of the Republic of Indonesia

27

Existing key foreign companies (2)

Website : www.tpkkoja.co.id

PT Pembangunan Perumahan

(PP) is a state-owned company

established in 1953. In 2010 the

company invested a 20% stake

or a IDR 4 trillion of value for the

expansion of Tanjug Priok port

phase 1.

Another investment of IDR 8.1

trillion was made in 2012 at

Tanjung Priok port showing that

Tanjung Priok port is expanding

and it meets the investment

appetite from the domestic

and foreign investors.

Website : www.pt-pp.com

The growth of Indonesia in early 1990s

has led to increase of export and

import activities through Tanjung Pirok

port. The existing two container

terminals were no longer able to

handle the massive volume of

containers.

In order to meet the steeply rising

demand form container handling

services, the state-own company, PT

Pelabuhan Indonesia II (Persero) in

cooperation with private company, PT

Hutchison Ports Indonesia, jointly

developed a completely new

terminal, the Koja Container Terminal

(Terminal Petikemas Koja – TPK KOJA)

These two companies have also

formed a Joint Operation (JO) to

handle the daily operations of

terminal. TPK Koja plans to invest US$

206 million in the next 6 years to

improve port handling efficiency.

The Investment Coordinating Board of the Republic of Indonesia

28

Asosiasi Logistik Indonesia was established in 2002, Indonesian Logistics Association.

ALI is a non profit organization for the Supply Chain & Logistics profession in

Indonesia. ALI is open to Indonesian citizens who work as practitioners,

academicians, regulation makers, or observers in the field of supply chain & logistics

management. ALI's membership is individual. ALI was opened to public membership

in January 2003. As per December 2009, total number of members registered

reached more than 3,000 professionals consisting of practitioners, academicians,

regulators, and those who have interest in this field. The practitioners came from

various industries, namely manufacturers, logistics providers, distributors, traders,retailers, Oil & Gas, and many more

Key Associations

Indonesia National Shipowner Association (INSA). INSA is a organization that is

tasked to enhance national shipping at both in Indonesia and other countries. It

has 57 members from ASEAN member countries, Asia and other international

organizations and countries which are interested to strengthen ties in trade and

shipping with Indonesia.

Web site: www.insa.or.id

Website : www.ali.web.id

Website : www.abupi.org

Indonesia Port Corporation / Asosiasi Badan Usaha Pelabuhan Indonesia (ABUPI)

or the Port Corporation Association is a forum for Indonesian businessmen/women

and also serves as the primary organization for corporation and

businessmen/women who are doing business in port: Port Corporation (BUP),

Special Terminal (TerSus) and Port for Internal Use (TUKS).

ABUPI was established with the objectives to support and assist government’s

endeavor to improve economic development in the Maritime sector as well as to

support and ease the members’ activities

The Investment Coordinating Board of the Republic of Indonesia

29

Benchmarking ASEAN-5

Labour Costs (US$)

by professionVietnam Indonesia Philippines Thailand Malaysia

Assistant Engineer 6,180 8,630 9,000 11,970 13,160

Chemical Engineer 39,150 37,050 36,490 53,800 51,940

Civil engineer 28,200 29,300 30,000 39,900 41,800

Engineering Manager 80,870 81,100 78,680 101,700 93,700

Industrial engineer 28,200 29,300 30,000 39,900 41,800

Secretary 3,920 4,680 6,340 7,930 9,900

1.14m 1.2m 1.22m

1.66m 1.73m

Vietnam Indonesia Philippines Thailand Malaysia

Labour Costs (US$)

The chart below presents the Financial Times’

analysis of the average total labour costs for

a engineering services operation. The costs are

based on a head count of 42 across 6 different

job functions (see the table below for the unit

cost per profession). The salary levels used in

these results are the average range base salary

levels for these locations.

Indonesia has the 2nd lowest total labour

costs at US$ 1.2m per annum.

Source: fDi Benchmark, a product of the Financial Times, June 2014

Government Provisions and Support

© 2014 by Indonesian Investment Coordinating Board. All rights reserved

SECTION DIVIDER SLIDE

SECTOR-RELEVANT IMAGE TO BE INSERTED

The Investment Coordinating Board of the Republic of Indonesia

31

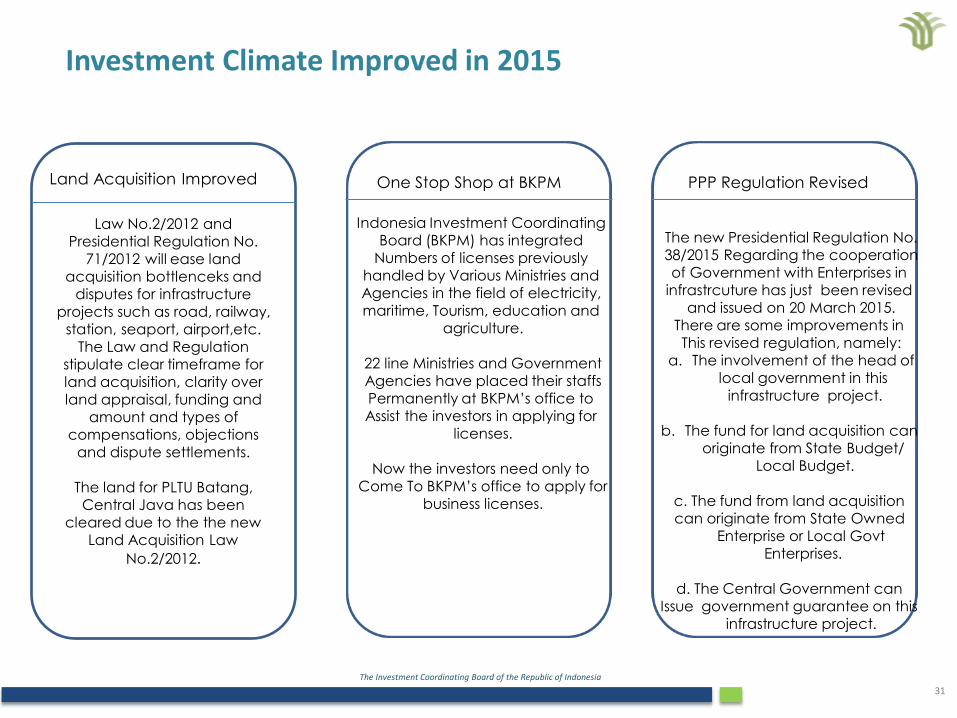

Investment Climate Improved in 2015

Law No.2/2012 and

Presidential Regulation No.

71/2012 will ease land

acquisition bottlenceks and

disputes for infrastructure

projects such as road, railway,

station, seaport, airport,etc.

The Law and Regulation

stipulate clear timeframe for

land acquisition, clarity over

land appraisal, funding and

amount and types of

compensations, objections

and dispute settlements.

The land for PLTU Batang,

Central Java has been

cleared due to the the new

Land Acquisition Law

No.2/2012.

Land Acquisition Improved One Stop Shop at BKPM PPP Regulation Revised

Indonesia Investment Coordinating

Board (BKPM) has integrated

Numbers of licenses previously

handled by Various Ministries and

Agencies in the field of electricity,

maritime, Tourism, education and

agriculture.

22 line Ministries and Government

Agencies have placed their staffs

Permanently at BKPM’s office to

Assist the investors in applying for

licenses.

Now the investors need only to

Come To BKPM’s office to apply for

business licenses.

The new Presidential Regulation No.

38/2015 Regarding the cooperation

of Government with Enterprises in

infrastrcuture has just been revised

and issued on 20 March 2015.

There are some improvements in

This revised regulation, namely:

a. The involvement of the head of

local government in this

infrastructure project.

b. The fund for land acquisition can

originate from State Budget/

Local Budget.

c. The fund from land acquisition

can originate from State Owned

Enterprise or Local Govt

Enterprises.

d. The Central Government can

Issue government guarantee on this

infrastructure project.

The Investment Coordinating Board of the Republic of Indonesia

32

Regulations in Indonesia Seaport

1. Law No 17/2008 on shipping has increased the scope for competition between ports by removing

the monopolies of the four state-woned Indonesian Port Corporations (IPC 1, IPC 2, IPC 3 and

IPC 4). The Law opens up the industry by allowing private port facility operators and port service

providers.

2. National Ports Master Plan establishes the Regulatory Framework and sets goals for Indonesian

port development until 2030, envisioning the construction of dozens of national ports and

hundreds of smaller feeder ports.

3. Presidential Decree No. 39/2014 on Negative Investment List, allows for foreign capital ownership

in the supply of port facilities- formerly capped at 49%- to reach a maximum of 95% within PPP

schemes during the concession period. This includes the supply of piers, buildings, container

and bulk terminals and Ro-Ro terminals. Outside of the PPP structure, the 49% cap on foreign

direct investment remains in place.

4. Government Regulation No.22/2011 allows exemptions from the cabotage principles with regards

to transportation services for the offshore oil and gas industry, where Indonesia still depends

heavily on global companies.

5. Law No. 2/2012 regarding land acquisition expedites the land procurement process thereby

removing what used to be a major stumbling block for PPP.

The Investment Coordinating Board of the Republic of Indonesia

33

Role of Private Sector and Government in Indonesia’s Seaports

InvestorDesign, engineering,

construction, commissioning

and procurement of seaport

Project in Indonesia.

Private Sector Government

Provide substantial financing

As well for the seaport

Project i.e expansion or

Development in Indonesia.

To support in land acquisition

and land access rights, thereby

alleviating what is arguably

the most daunting aspect for

private investors.

Government can also extend

to construction where deemed

Necessary. It can provide

Contingent guarantees to

mitigate low demand or

Unfavorable shifts in the political

environment.

The Investment Coordinating Board of the Republic of Indonesia

34

To assist in the acceleration of infrastructure development and

provision of infrastructure financing, the Government has created two

key institutions:

PT Indonesian Infrastructure Guarantee Fund

PT SMI (Sarana Multi Infrastruktur)

IIGF was established end 2009 as a Single Window in providing

guarantees for infrastructure projects Mandate: to provide guarantees for

Government Contracting Agencies’ (Ministry, Regional Government, SOE)

financial obligations under PPP Agreement for infrastructure projects with

Private Company. IIGF is 100% MoF owned SOE.

www.iigf.co.id

Financial support

PT SMI (Sarana Multi Infrastruktur), which is 100% owned by the Ministry

of Finance, provides mezzanine , equity financing,fund and guarantee for

infrastructure projects in rupiah.

www.ptsmi.co.id

The Investment Coordinating Board of the Republic of Indonesia

35

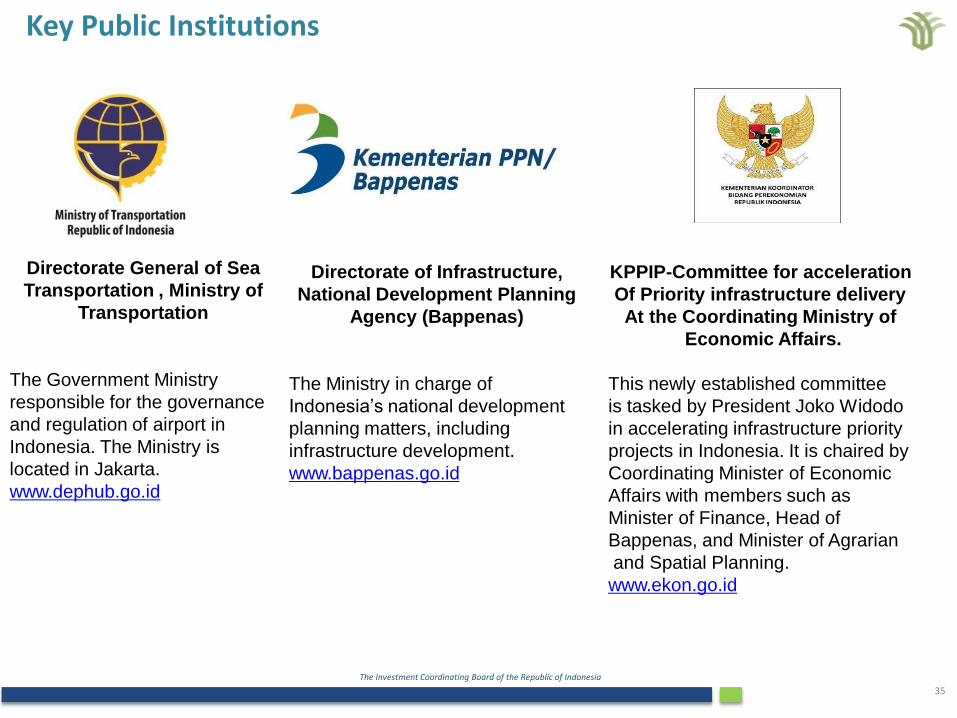

Key Public Institutions

Directorate General of Sea

Transportation , Ministry of

Transportation

The Government Ministry

responsible for the governance

and regulation of airport in

Indonesia. The Ministry is

located in Jakarta.

www.dephub.go.id

Directorate of Infrastructure,

National Development Planning

Agency (Bappenas)

The Ministry in charge of

Indonesia’s national development

planning matters, including

infrastructure development.

www.bappenas.go.id

KPPIP-Committee for acceleration

Of Priority infrastructure delivery

At the Coordinating Ministry of

Economic Affairs.

This newly established committee

is tasked by President Joko Widodo

in accelerating infrastructure priority

projects in Indonesia. It is chaired by

Coordinating Minister of Economic

Affairs with members such as

Minister of Finance, Head of

Bappenas, and Minister of Agrarian

and Spatial Planning.

www.ekon.go.id

The Investment Coordinating Board of the Republic of Indonesia

36

Six good reasons to invest in Indonesia’s seaport sector

A Government

committed to

supporting seaports

One of the priorities of the

Government of Indonesia

through Ministry of

transportation is for seaport

development

Large opportunities

across the entire

seaport supply chain

Ongoing and upcoming

projects covering feasibility

studies and construction to

improvement of seaport

facilities and services.

Large and various

sources of funding

(public and private)

Indonesian Government,

International development

banks, and fully private funds

are involved in seaport

projects (passenger and

freight)

Growing pool of

qualified labour in SE

Asia

Beyond having the largest

pool of workers, Indonesia has

the 2nd lowest labour costs for

engineering services in the

ASEAN-5

An ambitious seaport

development/revitalization

program worth more than

US$ 9 BillionTo develop and improve the

Indonesian ports. Plans

include grading the existing

airports and establish more

commercial and non-

commercial seaports.

A growing and

profitable sector

PT Pelindo I booked profit of

IDR 585 billion, PT Pelindo II

booked profit of IDR 2.1

trillion, Pelindo III booked profit

of IDR 1.2 trillion and Pelindo

IV booked IDR 530 billion in

2013.

Source: fDi Benchmark (Financial Times)

Invest in...

For further information, contact us at:

© 2015 by Indonesia Investment Coordinating Board (‘BKPM’). All rights reserved

This presentation has been developed with the

support of:

The European Union (EU) Desk at BKPM, part

of EU-Indonesia Trade Cooperation Facility

(TCF) projects.

Kantor Representatif EU DESK di

BADAN KOORDINASI PENANAMAN MODAL (BKPM)

REPUBLIK INDONESIA

Jl. Jend. Gatot Subroto No. 44, Jakarta 12190, Indonesia

P : +62 21 5274 803

W : www.bkpm.go.id

www.euind-tcf.com/eudesk/

BKPM international representative offices

(Investment Promotion Centre):