INVESTING IN ICAP - NEX · • ICAP is committed to a truly hybrid model based on - Combined voice...

89

INVESTING IN ICAP Michael Spencer

Transcript of INVESTING IN ICAP - NEX · • ICAP is committed to a truly hybrid model based on - Combined voice...

INVESTING IN ICAPMichael Spencer

2

INTRODUCTION

• The world’s largest voice and electronicinterdealer broker

• Daily average transaction volume in excessof $550 billion, 40% of which is electronic

• 2800 staff operating from 21 officesworldwide

• One of the UK’s 130 largest quotedcompanies. A FTSE 250 company with amarket capitalisation of circa £1.4bn(US$2.3bn)

• The Total Shareholder Return since themerger (Sept 99) up to the close on23 Sept 03 has been 463%

INT

RO

DU

CT

ION

3

IDB SERVICE

• Wholesale intermediary

• Anonymity/execution/liquidity/information

• No principal trading

• Where settlement systems areestablished, operates as “matchedprincipal”

• In markets where credit risk existsbetween counter parties, “name give up”

• Similar to an exchange

INT

RO

DU

CT

ION

4

HYBRID CLARIFICATION

• Many different definitions

• ICAP is committed to a truly hybridmodel based on- Combined voice and electronic liquidity

- Customers choice of either voice orelectronic deal execution

5

INDUSTRY DEVELOPMENTS

• Rapid consolidation of previously fragmentedindustry driven by:

- Impact of the Euro- Merger of customers- Increasing impact of technology- The emergence of e-broking- Weakness of some balance sheets- Operational leverage and economies of scale

• Continued belief that further consolidation will resultin the emergence of 2 or 3 global interdealerbrokers with a small number of niche players

INT

RO

DU

CT

ION

6

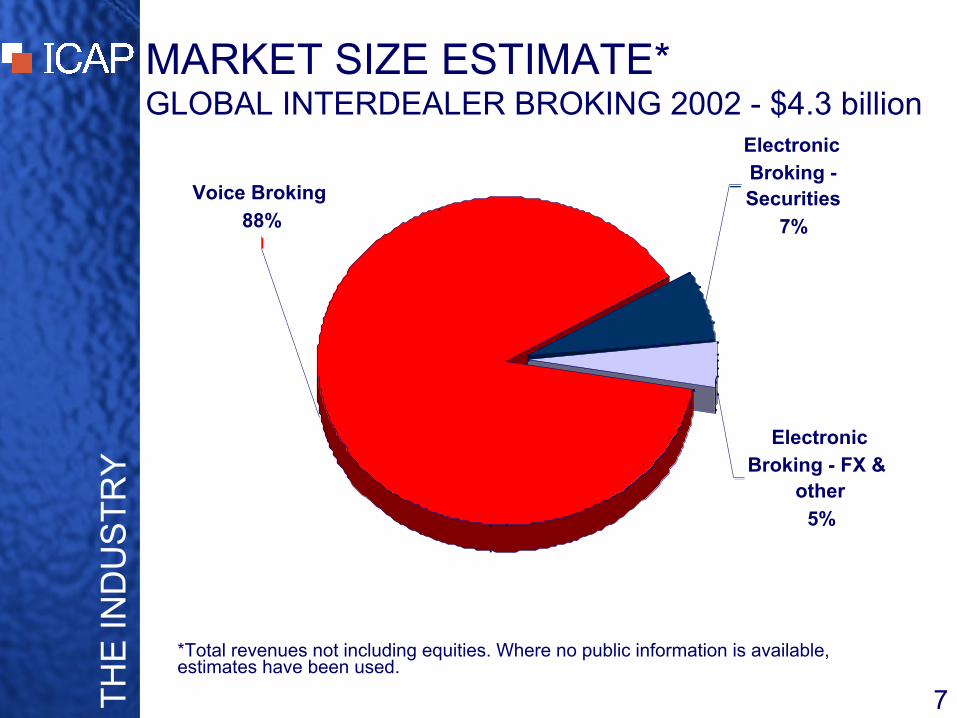

MARKET SIZE ESTIMATE*GLOBAL INTERDEALER BROKING 2002 - $4.3 billion

ICAP plus BrokerTec

Collins Stewart Tullett

Tradition

Other Voice brokers

Prebon

Cantor/Espeed

GFI

Other Electronic brokers

Other Energy brokers

* Total revenues not including equities. Where no public information is available,estimates have been used.

TH

E IN

DU

ST

RY

7

MARKET SIZE ESTIMATE*GLOBAL INTERDEALER BROKING 2002 - $4.3 billion

Electronic

Broking - FX & other

5%

Electronic

Broking - Securities

7%

Voice Broking

88%

*Total revenues not including equities. Where no public information is available,estimates have been used.

TH

E IN

DU

ST

RY

8

INTERNATIONAL BONDS AND NOTESAMOUNTS OUTSTANDING (US$ billions)

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Source: BIS

DR

IVE

RS

FO

R G

RO

WT

H

9

MARKET GROWTHINTEREST RATE SWAPS OUTSTANDING (US$ trillions)

0

10

20

30

40

50

60

70

80

Dec-90Dec-91Dec-92Dec-93Dec-94Dec-95Dec-96Dec-97Dec-98Dec-99Dec-00Dec-01Dec-02

Source: BIS

DR

IVE

RS

FO

R G

RO

WT

H

10

ELECTRONIC BROKING VOLUMESALL PRODUCTS (average $ billion/day)

0

50

100

150

200

250

1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03 2Q03

ICAP/ETC

MTS Group

BrokerTec

eSpeed

Sources: BrokerTec, ICAP, estimates from eSpeed and MTS websites - counting only trades executed electronically

ELE

CT

RO

NIC

BR

OK

ING

INVESTING IN ICAPSteve McDermott

12

AMERICAS

• American operations- 35+% of ICAP’s global profit

- 116% profit growth for the region

between 2002 and 2003

- Growth has been both organic and

through acquisitions

- The larger ICAP acquisitions have

been in North America.

BU

SIN

ES

S A

NA

LY

SIS

13

AMERICAS

• The merger between Garban and theIntercapital Group.

- Garban brought a leading Americanpresence

- Intercapital a leading Europeanpresence

- The combination created the world’slargest interdealer broker.

BA

CK

GR

OU

ND

14

AMERICAS

• 9/11 was another key—albeit tragic—eventin our evolution

- We were based in the World Trade Center

- Had market leading positions in a number ofproducts

- And, in the midst of developing and rolling outE-initiatives

- Suddenly we were dispersed, and conductingbusiness with nothing more than pads, pencilsand outside phone lines

BA

CK

GR

OU

ND

15

AMERICAS

• Background- We survived and succeeded.

- In the two years since the attacks onthe Trade Center we have achievedgrowth in every measurable way.

BA

CK

GR

OU

ND

16

AMERICAS

• Background- In the past 18 months, we have completed

three major acquisitions

• First Brokers in April 2002 expanded

• APB (now ICAP Energy) in October 2002

• BrokerTec in May 2003

- Headcount in all US operations is 1170

- New North American headquarters is a stateof the art facility, which can be expanded.

BA

CK

GR

OU

ND

17

AMERICAN MANAGEMENT

• Ron Purpora is CEO of our Securitiesbusiness in North America. Thisincludes products such as:

- US Treasury products- U.S. Repo agreements- U.S Mortgages- U.S. Agencies- U.S. Corporates- Credit Derivatives- Equity NYSE floor business

INT

RO

DU

CT

ION

S

18

AMERICAN MANAGEMENT

• Doug Rhoten, CEO, Garban CapitalMarkets. Doug is responsible for

- Money Markets

- Spot and Forward Foreign Exchange

- Emerging Market Derivatives

- Derivatives, including options andInterest Rate Swaps

- Energy

INT

RO

DU

CT

ION

S

19

AMERICAN MANAGEMENT

• Hal Hinkle, Global CEO, ICAPElectronic Broking Division and FormerCEO of BrokerTec

- Hal joined as part of the acquisition

- In addition to the BrokerTec system,Hal is responsible for our ETC productand several other system and electronicinitiatives.

INT

RO

DU

CT

ION

S

INVESTING IN ICAPRon Purpora

21

AMERICAN SECURITIES MARKETS

• Core Divisions• Treasury Products

• Mortgage Securities

• Federal Agency Issues

• Corporate Products including– Corporate Bonds

– Emerging Markets

– Credit Derivatives

– Equity and related

INT

RO

DU

CT

ION

22

AMERICAN SECURITIES MARKETS

• 350 Brokers servicing

• Voice and Electronic Capabilities

• Market leading positions in all coredivisions

• 67% revenue increase from fiscal 2001to fiscal 2003

INT

RO

DU

CT

ION

23

OVERVIEW – RECENT EVENTS

• Cemented dominance in CorporateBonds with First Brokers purchase

• Expanded Credit Derivatives group

• Rolled out new technologies to exploitSTP capabilities across products

• Historically strong performancesrelated to overall growth in FixedIncome arena

OV

ER

VIE

W

24

TREASURIES - HYBRID BROKING

41%

44%

11%1% 3%

ICAP-BTEC

E-Speed

TTL

Maxcor

Hill

Source: Federal Reserve Bank of New York Data, ICAP estimates

MA

RK

ET

S

Estimated Market Share – US Treasury Trading

25

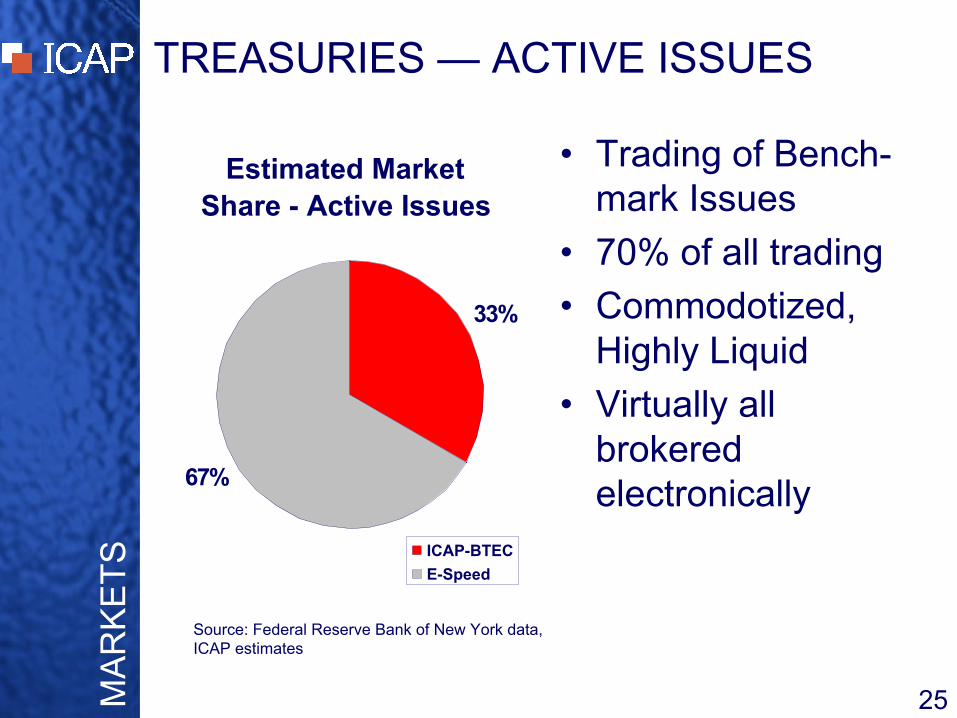

TREASURIES — ACTIVE ISSUES

Estimated Market Share - Active Issues

33%

67%

ICAP-BTEC

E-Speed

• Trading of Bench-mark Issues

• 70% of all trading

• Commodotized,Highly Liquid

• Virtually allbrokeredelectronically

Source: Federal Reserve Bank of New York data,ICAP estimates

MA

RK

ET

S

26

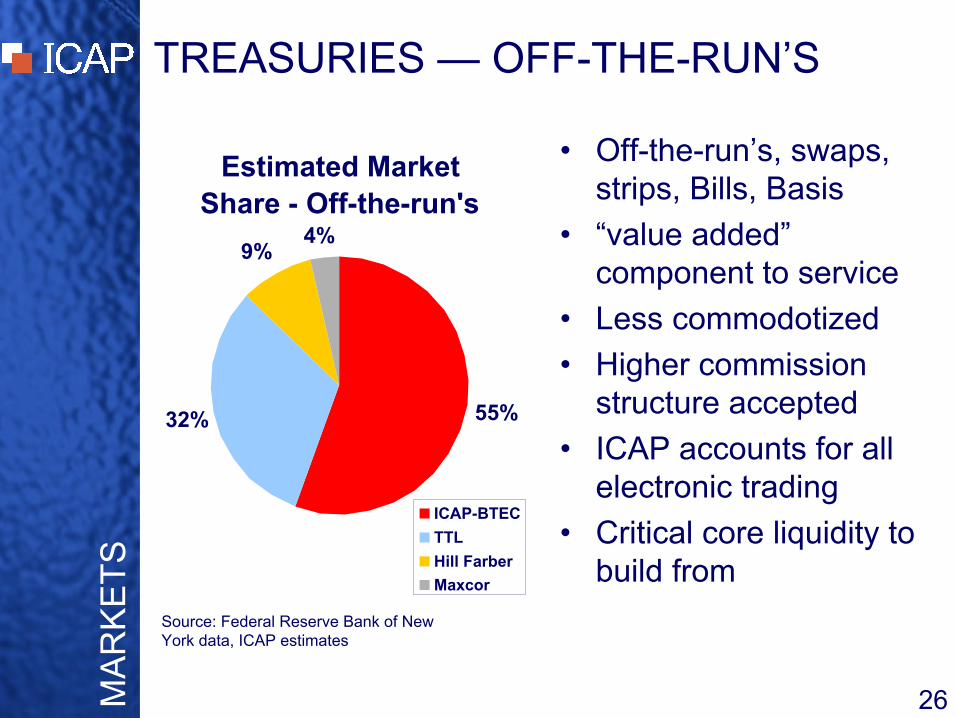

TREASURIES — OFF-THE-RUN’S

Estimated Market Share - Off-the-run's

55%32%

9%4%

ICAP-BTEC

TTL

Hill Farber

Maxcor

• Off-the-run’s, swaps,strips, Bills, Basis

• “value added”component to service

• Less commodotized

• Higher commissionstructure accepted

• ICAP accounts for allelectronic trading

• Critical core liquidity tobuild from

Source: Federal Reserve Bank of NewYork data, ICAP estimates

MA

RK

ET

S

27

Average Daily Volume US Treasury Securities

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003

source: Federal Reserve Bank of New York

TREASURIES - PERFORMANCEM

AR

KE

TS

28

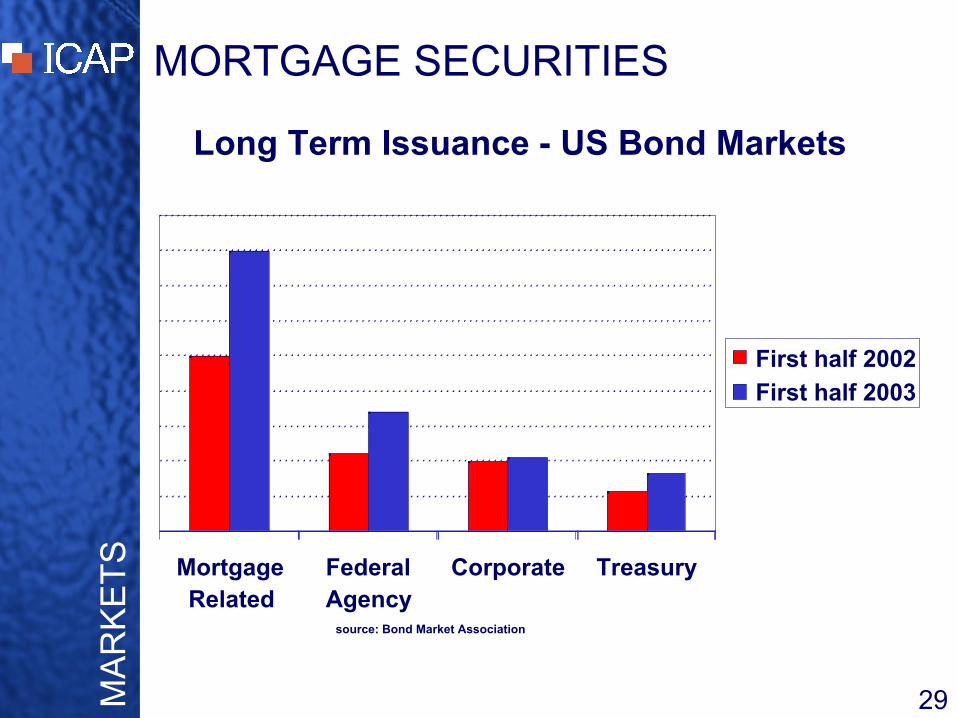

MORTGAGE SECURITIES

• ICAP has strongest presence acrossproduct base- TBA Collateral market

- Specified Pools

- Collateralized Mortgage Obligations

- ARM’s, ABS and Commercials

• 36 Brokers servicing these products

• Strong operating margin

MA

RK

ET

S

29

MORTGAGE SECURITIES

MortgageRelated

FederalAgency

Corporate Treasury

source: Bond Market Association

First half 2002

First half 2003

MA

RK

ET

SLong Term Issuance - US Bond Markets

30

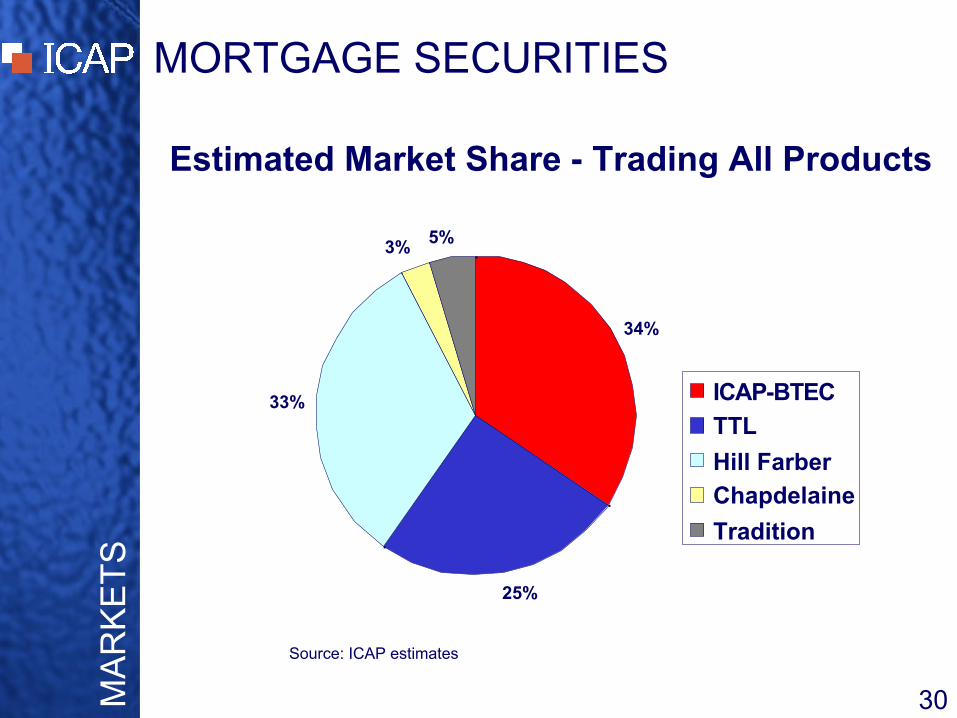

MORTGAGE SECURITIES

34%

25%

33%

3%5%

ICAP-BTEC

TTL

Hill Farber

Chapdelaine

Tradition

Source: ICAP estimates

MA

RK

ET

SEstimated Market Share - Trading All Products

31

MORTGAGE SECURITIES

• Electronic participation

• Trading volumes up strongly- Explosion in refinancing activity

- Unprecedented market volatility

• Offer full suite of mortgage products

MA

RK

ET

S

32

AGENCY ISSUES

• Government Sponsored Enterprises –FNMA and FHLMC-Notes and bonds

-Callables

• Staff of 30 brokers offering screen-based voice execution

• ICAP is by far the leading broker-Voice capabilities

-Electronic capabilities

MA

RK

ET

S

33

AGENCY ISSUES

71%

23%

5% 1%

ICAP-BTEC

TTL

Maxcor

Tradition

Source: Federal Reserve Bank of New York data, ICAP estimates

MA

RK

ET

S

Estimated Market Share – Agency Trading

34

CORPORATE PRODUCTS

• With Acquisition of First Brokersestablished dominance in this sector

• Traded in a voice environment

• Staff of 176 Brokers

• High technology deployment- Straight Through Processing Initiatives

- Regulatory Requirements

- Market data dissemination

MA

RK

ET

S

35

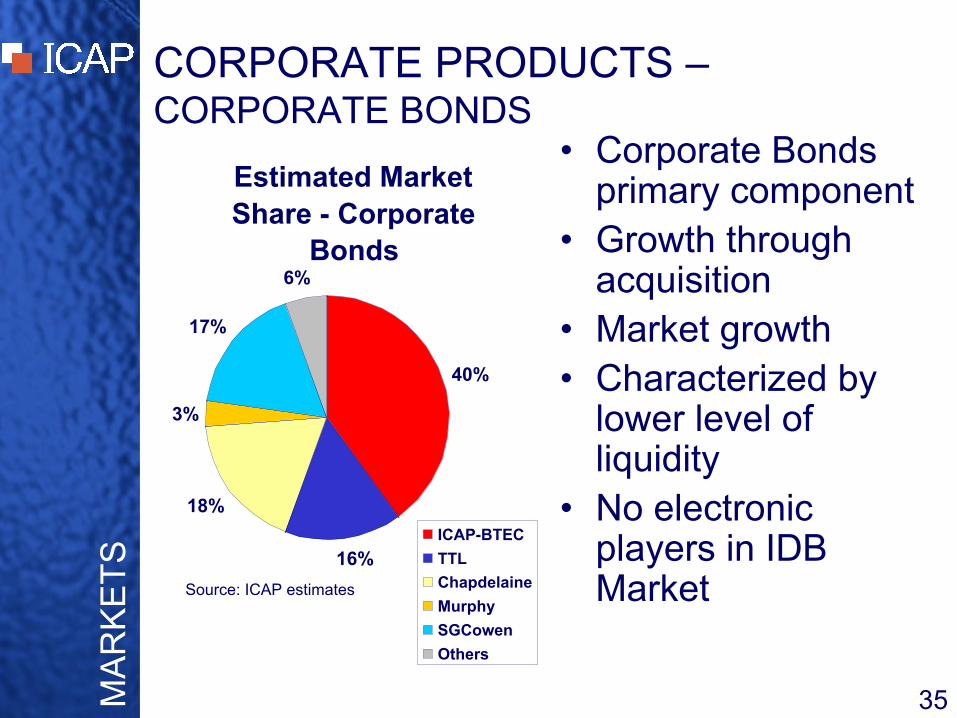

CORPORATE PRODUCTS –CORPORATE BONDS

Estimated Market Share - Corporate

Bonds

40%

16%

18%

3%

17%

6%

ICAP-BTEC

TTL

Chapdelaine

Murphy

SGCowen

Others

• Corporate Bondsprimary component

• Growth throughacquisition

• Market growth• Characterized by

lower level ofliquidity

• No electronicplayers in IDBMarketSource: ICAP estimates

MA

RK

ET

S

36

CORPORATE PRODUCTSMARKET EXTENSION

• Developments-Credit Derivatives

• High growth area +275% year on year

• Rapidly attained a top position

• Strong Margins

-Equities• Direct Access Unit

• NYSE seat holder

• Equity Derivatives

• Institutional Equity Brokerage

MA

RK

ET

S

37

MARKET BREADTH

• Treasury Products• A Market leader - +40% share

• Hybrid brokerage

• Agency Issues• Dominant share in voice and electronic brokerage

• 70% market share

• Mortgage Securities• Market leader - +30% share

• Full suite of mortgage products

• Corporate Products• Dominant broker of corporate bonds

• 40% market share

SU

MM

AR

Y

INVESTING IN ICAPDoug Rhoten

39

CAPITAL MARKETS INTRODUCTION

• Money Market• Foreign Exchange

- Spot- Forwards- NDF’s

• Derivatives• Canadian Products• Emerging Market Derivatives• Repurchase Agreements• Energy• Latin America

INT

RO

DU

CT

ION

40

VOTED TOP BROKER IN…

Source: Risk Magazine; Global Derivatives Rankings, September 2003

Short-Dated IRS Exotic Interest Rate ProductsUS Dollar Volatility/Variance SwapsJapanese Yen Constant Maturity - US DollarEuro Bermudan/American - EuroSterling (jointly with Prebon) Bermudan/American - US Dollar

QuantosIRS 2-10 years Inflation Swaps - Eurozone US Dollar Inflation Swaps - North AmericaJapanese YenEuro Cross Currency Swaps

Sterling Euro/US Dollar (jointly with Tullett)Euro/Japense Yen

IRS 10 years + Sterling/US DollarUS Dollar Euro/SterlingEuro US Dollar/Swiss France (jointly with Tullett)Sterling Dollar/Norwegian Krone (jointly with Tullett)Canadian DollarAustralian Dollar Overnight Index Swaps

US DollarInterest Rate Caps/Floors EuroUS Dollar Danish KroneEuroSterling Repo

Canadian Dollar US DollarAustralian Dollar Euro

SterlingInterest Rate Swaptions Canadian Dollar

EuroSterling FRA's

Canadian Dollar EuroAustralian Dollar Japanese YenNorwegian Krone Danish Krone

41Source: Risk Magazine; Global Derivatives Rankings, September 2003

ICAP:Credit Derivatives Currency Forwards Vanilla Default Swaps US Dollar/Canadian DollarInvestment Grade Asia US Dollar/Danish KroneHigh Yield AsiaEmerging Markets - East Europe

TFS-ICAP:Vanilla Currency Options Exotic Currency Options Euro/US Dollar Euro/US Dollar BarrierEuro/Japanese Yen US Dollar/Yen BarrierUS Dollar/Swiss Franc Sterling/US Dollar BarrierUS Dollar/Canadian Dollar (jointly with GFI) Other BarrierUS Dollar/Australian Dollar Binary/DigitalUS Dollar/Swedish Krona HybridsUS Dollar/Danish Krone Long-datedUS Dollar/Emerging Mkts Europe Average RateUS Dollar/Emerging Mkts Americas

VOTED TOP BROKER IN…

42

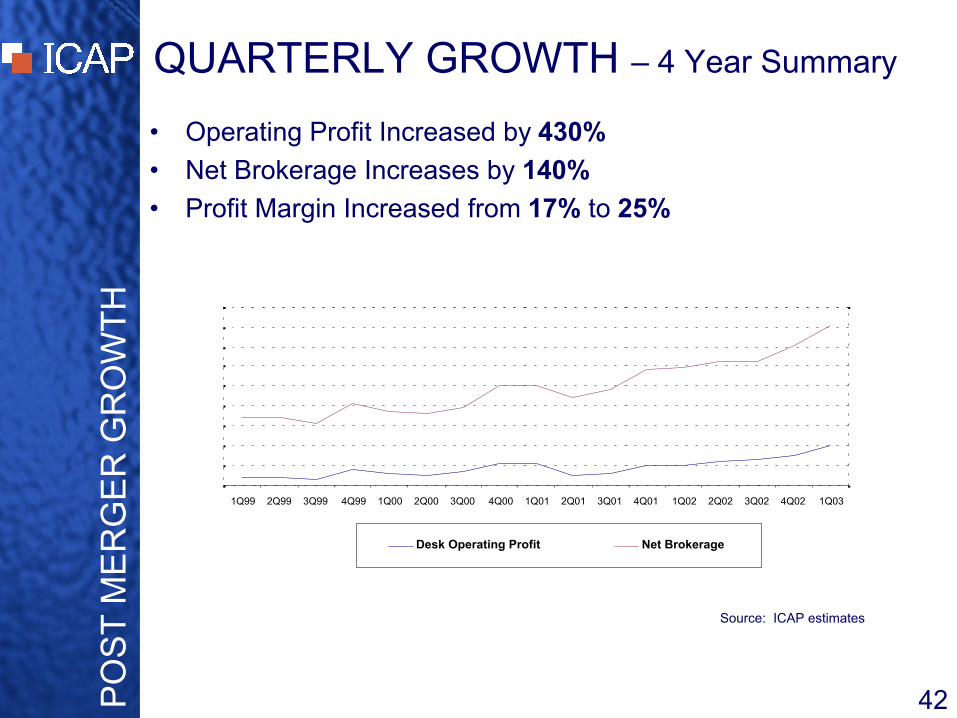

QUARTERLY GROWTH – 4 Year Summary

1Q99 2Q99 3Q99 4Q99 1Q00 2Q00 3Q00 4Q00 1Q01 2Q01 3Q01 4Q01 1Q02 2Q02 3Q02 4Q02 1Q03

Desk Operating Profit Net Brokerage

• Operating Profit Increased by 430%

• Net Brokerage Increases by 140%

• Profit Margin Increased from 17% to 25%

PO

ST

ME

RG

ER

GR

OW

TH

Source: ICAP estimates

43

OTC BUSINESS MODEL

• Premiere Brokers

• Production Management

• Build and Consolidate Voice Liquidity

• Integrate Technology

• Create Indices and Distribute Data

• Pursue Partnerships With IndustryLeaders

44

MANAGEMENT

• Flat Management Structure

• Unmatched Product Knowledge

• Long Term Tenure

• Broker Loyalty

• Customer-centric Approach

OT

C B

US

INE

SS

MO

DE

L

45

BUILD VERBAL LIQUIDITY

• Market Share Goal: 35%

• Product Specialization

• Continued Expansion

• Customers Help Drive Process

OT

C B

US

INE

SS

MO

DE

L

46

COMPLEMENTARY TECHNOLOGY

• Pre-trade pricing and analytics

• Straight Through Processing

• Electronic trading capabilities

OT

C B

US

INE

SS

MO

DE

L

47

CREATING INDICES

• 19900 Telerate

• ISDA Swapfix

• Fed Funds (Telerate page 5)

• SwapPX

• GovPX

OT

C B

US

INE

SS

MO

DE

L

48

PARTNERSHIPS

• STP- Swapswire- Financial Oxygen

• Expansion- Mexican, Chilean, Peruvian & ColumbianStock Exchanges- GovPX- Shorcan

• Market Practices- ISDA Swapfix

OT

C B

US

INE

SS

MO

DE

L

49

OTC BUSINESS MODEL

• Production Management

• Build and Consolidate Voice Liquidity

• Integrate Technology

• Create Indices and Distribute Data

• Pursue Partnerships With IndustryLeaders

50

$ INTEREST RATE DERIVATIVES• Market Share – 40%

- Rank #1

• Benchmark Index- Telerate 19900- SwapPX- ISDA Swapfix

• Technology- FRACross- Swapswire STP- CAS- Datatec- I-Swap

• Partnership- Swapswire- ISDA- NumeriX- Tri-Optima- GovPX

Prebon15%

Tullett25%

ICAP40%

Others20%

MA

RK

ET

SH

AR

E &

OV

ER

VIE

W

51

MONEY MARKET

• Market Share – 35%- Rank #1

• Technology- Bank Oxygen

• Benchmark Index- Telerate page 5

• Partnership- Financial Oxygen(Chase & BOA)

MA

RK

ET

SH

AR

E &

OV

ER

VIE

WEurobrokers

15%

Prebon20%

Tradition22%

ICAP35%

Tullett8%

52

REPURCHASE AGREEMENTS

• Market Share – 54%- Rank #1- $750+ Billion per day

turnover

• Technology- BrokerTec/ETC

• “Franchise” approach- Extend capital and

technologyinfrastructure

• 3 Voice BrokerageDesks

MA

RK

ET

SH

AR

E &

OV

ER

VIE

W

TTL7%

Tradition7%

Maxcor7%

Prebon

25%

ICAP-

BTEC54%

53

FOREIGN EXCHANGE – VOICE MARKET

ICAP32%

Prebon32%

Tullett16%

Tradition20%

ICAP45%

Prebon30%

GFI20%

Other5%

Tullett30%

ICAP70%

MA

RK

ET

SH

AR

E &

OV

ER

VIE

W

ForwardsNDF’s

Spot

54

MEXICO JOINT VENTURE

• Merger- SIF/Garban

• Technology- Datatec

- Sipo

- Bursatec

• Latin American Expansion- Chile

- Columbia

- Dominican Republic

- Peru

55

ENERGY

Prebon13%

Others31%

ICAP21%

Amerex24%

GFI11%

Prebon16%

Amerex20%

Others35%

ICAP16%

ICE13%

MA

RK

ET

SH

AR

E &

OV

ER

VIE

W

• APB Energy Acquisition- October 2002

• Technology- Datatec/ETC

• Benchmark Index- Under NDA

• Partnership- TBD

Natural GasElectricity

56

EMERGING MARKET DERIVATIVES

ICAP30%

GFI23%

Prebon23%

Local Brokers

24%

• Market Share – 30%- Rank #1

• Technology- Datatec

- CAS

- Kalahari

- Mavis

• Partnership- TBD

MA

RK

ET

SH

AR

E &

OV

ER

VIE

W

57

OTC CANADIAN PRODUCTS

• Market Share – 40%- Rank #1

• Technology- Datatec

- CAS

- BrokerTec/ETC

• Benchmark Index- Telerate 19900

• Partnership- Shorcan

Prebon15%

Tradition22%

ICAP40%

Other5%

Tullett18%

MA

RK

ET

SH

AR

E &

OV

ER

VIE

W

58

OTHER INITIATIVES

• Wembley Asset Management

• Wrightson

• Pari-mutual Derivatives

• Mortgage Prepayments

• Whole Loan Broking

• Broader Energy Market

INIT

IAT

IVE

S

59

CLOSING

What differentiates us from ourcompetitors-Highest Quality Brokers

-Production Management

-Specialized Structure

-Constant Customer Contact

-Leverage Complimentary Technologies

-Customer Responsiveness

-Commitment to Growth

INVESTING IN ICAPICAP E-Broking / E-Markets

Hal Hinkle

OVERVIEW

• Overview-BrokerTec

-ICAP E-Broking• Product Comparison• Cross Connect• Revenue Commitment Agreements• Hybrid Brokering

• 3 year old global platform

• 184 Customers worldwide

• Executed 6.8 million sides

• Executed $94.1 trillion in single count volume

• 99+% STP

WHAT IS BROKERTEC? -SNAPSHOT

+

WHAT IS ICAP E-BROKING? – BEFOREMERGER

•3.

•E-Markets

•PlatformProvider

•2.

•VoiceSupport +

Development

•1.

•HybridCustomer

Broker

•Pure Customer

•E-Broking

•99+ % Central Clearing

•(fully electronic)

ETCBTEC US / EU

•Third PartyProvisions

•VoiceSupport andDevelopment

Voice - Third Party

WHAT IS ICAP E-BROKING? – AFTERMERGER

Customer E-Broking

US EU and Asia

PRIMARY ELECTRONIC COMPETITORS

EU

Wholesale

US / EU

Retail

Global

Wholesale andRetail

Global

WholesaleFootprint

Request ForQuote

UST

Money Markets

TradeWeb MTSESPDBTEC

MatchingMatchingMatchingPlatform

Euro-Govs

Italian RepoUST

UST

US Repo

US Agencies

US Repo

PrincipalProduct

WHO IS THE ELECTRONICCOMPETITION?

400 connections1,400+700+184Customers

8

$28.2 trillion

US: 14.5 hours

Europe: 8.5hours

TradeWeb MTSESPDBTEC

100+319115Total Employees

$94.4 million$76.8 millionTotal Expenses(2002)

$60 million – est.$126 million$97.3 millionTotal Revenue(2002) 2

13 systems1226Total Products

40 trillion

$47.8 trillion(fully electronic)

$77.8 trillion(total electronic)

$81.7 trillion

(fully electronic)Total Volume 1

Cash: 10 hours

Repo: 11.5 hours23 hours23 hours

Operating Hours

2 ESPD’s 2002 revenues exclude a one-time business interruption insurance gain. Expenses exclude non-cashbusiness partner activities.

1 BTec and ESPD as of 06/03; TradeWeb – public statement 7/7/03; MTS– company estimates as of 6/03.

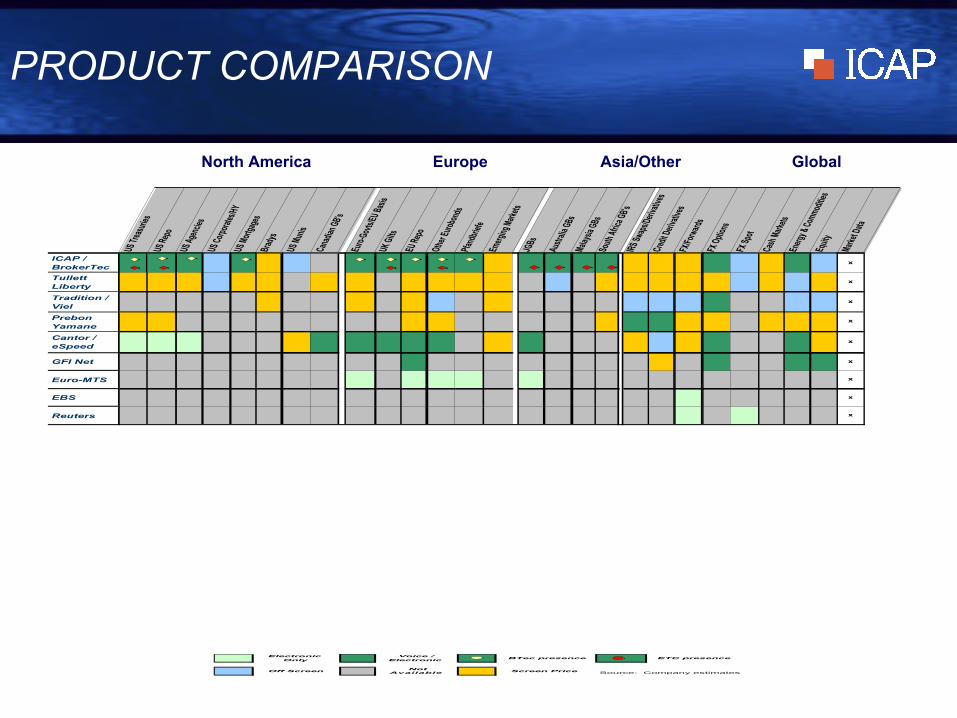

North America Europe Asia/Other Global

PRODUCT COMPARISONUS

Trea

surie

sUS

Repo

US Ag

encie

sUS

Corpo

rates

/HYUS

Mort

gage

sBr

adys

US M

unis

Cana

dian G

B's

Euro-

Govts

/EU Ba

sisUK

Gilts

EU Re

po

Othe

r Euro

bond

sPfa

ndbri

efeEm

erging

Mark

etsJG

Bs

Austr

alia G

BsMa

laysia

GBs

South

Afric

a GB's

IRS Sw

aps/D

eriva

tives

Cred

it Deri

vativ

esFX

/Forw

ards

FX O

ption

s

FX Sp

ot

Cash

Mark

etsEn

ergy &

Commod

ities

Equit

y

Marke

t Data

ICAP / BrokerTec

x

Tullett Liberty

x

Tradition / Viel

x

Prebon Yamane

x

Cantor / eSpeed

x

GFI Net x

Euro-MTS x

EBS x

Reuters x

Electronic Only

Voice / Electronic

BTec presence ETC presence

Off Screen Not

Available Screen Price Source: Company estimates

PRODUCT COMPARISON – NORTHAMERICA

North America

US

T

US

Rep

o

US

Age

ncie

s

US

Cor

ps/H

Y

US

Mor

tgag

es

Bra

dys

US

Mun

is

Can

adia

n G

B's

ICAP / BrokerTec

Cantor / eSpeed

Euro-MTS

Electronic Only

Voice / Electronic

BTec presence ETC presence

Off Screen Not

AvailableScreen Price Source: Company estimates

PRODUCT COMPARISON – EUROPE

Europe

Eur

o-G

ovs/

EU

Bas

is

UK

Gilt

s

EU

Rep

o

Oth

er E

urob

onds

Pfa

ndbr

iefe

Em

ergi

ng M

arke

ts

ICAP / BrokerTec

Cantor / eSpeed

Euro-MTS

Electronic Only

Voice / Electronic

BTec presence ETC presence

Off Screen Not

AvailableScreen Price Source: Company estimates

PRODUCT COMPARISON– ASIA / OTHER / GLOBAL

Asia/Other GlobalJG

Bs

Austr

alia G

Bs

Malay

sia G

Bs

South

Afric

a GB's

IRS Sw

aps/D

eriva

tives

Cred

it Deri

vative

s

FX/Fo

rward

s

FX O

ption

s

FX Sp

ot

Cash

Mark

ets

Energ

y / Co

mmod

ities

Equit

y

Marke

t Data

ICAP / BrokerTec

x

Cantor / eSpeed

x

Euro-MTS x

Electronic Only

Voice / Electronic

BTec presence ETC presence

Off Screen Not

AvailableScreen Price Source: Company estimates

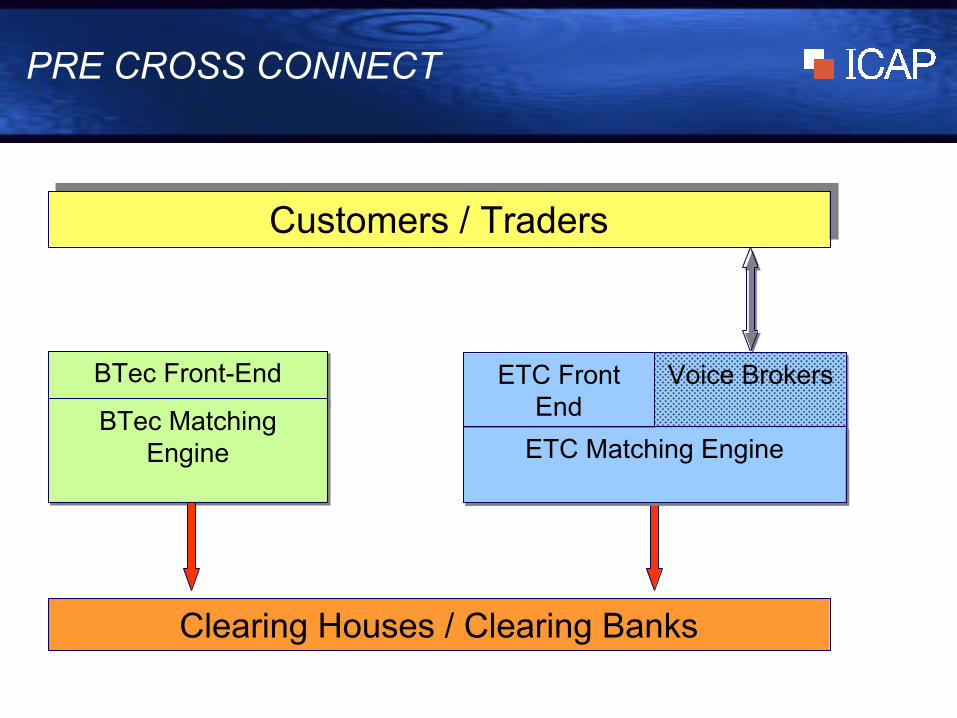

PRE CROSS CONNECT

Customers / TradersCustomers / Traders

BTec Front-EndBTec Front-End

BTec MatchingEngine

BTec MatchingEngine

ETC FrontEnd

ETC FrontEnd

Clearing Houses / Clearing BanksClearing Houses / Clearing Banks

Voice BrokersVoice Brokers

ETC Matching EngineETC Matching Engine

CROSS CONNECT

Customers / TradersCustomers / Traders

BTec Front-EndBTec Front-End

BTec MatchingEngine

BTec MatchingEngine

ETC Front

End

ETC Front

End

Clearing Houses / Clearing BanksClearing Houses / Clearing Banks

Voice

Brokers

Voice

Brokers

ETC MatchingEngine

ETC MatchingEngine

• 13 RCA Customers

• 8 Customers at $4 million floor / $5.5 millioncap

• Started June 2003

• Expect to Use “Cumulative” Accounting

REVENUE COMMISSION AGREEMENTS

HYBRID BROKING

• Voice and/or electronic access to a common pool ofliquidity

• Give customers choice between-Value-added voice support-Efficient and economical electronic option

• Provide incentives to existing voice desks to buildbalance between voice and electronic support

HYBRID BUSINESS APPROACH

• Team Manage Construction of Hybrid Business –Product Specific

• Use Flexible Broker Incentives/Transfers

• Balance Customer – Broker Transparency Needs

• Build Relationship Team from Best Voice andElectronic Coverage

CURRENT AGENDA

• Continue Implementing Cross Connect Technology

• Extend Hybrid Business Model

• Rationalize Technology and Operations

• Relocate Offices – July to December 2003

• Consolidate Corporate Administration and

Infrastructure

INVESTING IN ICAPJim Pettigrew

79

REVENUE GROWTH

0

200

400

600

800

2001 2002 2003

Headline CAGR 19%

Ex-acquisitions CAGR 10%

£m

FIN

AN

CE

80

INCREASING OPERATING MARGINS

10

12

14

16

18

20

2001 2002 2003

%

14%

15%

17%

FIN

AN

CE

81

MARGINS BY SEGMENTS

Year ended Year ended

31/03/03

31/03/02

Activity Securities broking 14% 11%

Derivatives and money broking 18% 20%

Geographic region

Americas 12% 8%

Europe 20% 19%

Asia Pacific 6% 11%

Note: Operating profit margin is profit before interest and exceptional items but after goodwill amortisation for the Group’s continuing operations.

FIN

AN

CE

82

COST CONTROL DISCIPLINE

Broker Rem.

T&E

Telecoms

Other

Overheads

Profit*0

10

20

30

40

50

60

70

80

90

100

2002 2003

Fixed Variable

Classification as a % of turnover Broker remuneration variable/fixed

* Group operating profit.

%of total broker remuneration

%

54464

1517

FIN

AN

CE

83

EPS AND DIVIDEND GROWTH

0

20

40

60

80

100

2001 2002 2003

Pence PerShare

EPS adjusted(excludesgoodwill andexceptionals).

Dividend pershare.

49.4p

77.3p

30p

20p

58.0p

24p

FIN

AN

CE

84

EFFICIENT PROFIT/CASHCONVERSION

0

20

40

60

80

100

120

140

2002 2003

* Before goodwill amortisation and exceptional items.

£m

103%

125%

Group operatingprofit*.

Cash inflowfrom operatingactivities.

FIN

AN

CE

85

CASHFLOW Year ended

31/03/03 £’m

Operating Profit 113 Depreciation 16

Working Capital 13

142

Net Capex (16)

Associates, JVs, interest and Other 6

Taxation (36)

96

Dividends (27)

Acquisitions/Investments (36)

Exceptional Items (14)

Change in Net Cas h and Investments 19

FIN

AN

CE

86

BALANCE SHEET (EXTRACT)

Year ended Year ended

31/03/03 £’m

31/03/02 £’m

Net Assets 263 196

Net Cash & Investments 185 166

FIN

AN

CE

87

THE 2003/2004 FINANCIAL YEAR

“The financial priorities for theforthcoming year are to integratesatisfactorily the BrokerTecacquisition and to increase our profitmargins through a combination ofgrowth in market share and effectivecost control. We plan to achieve thisagainst a continuing background ofstrong cash managementdisciplines.”

CFO report in ICAP’s 2003 Annual Report

FIN

AN

CE

INVESTING IN ICAPMichael Spencer

89

STRATEGY• Consolidation in the interdealer broking industry

continues in both the voice and electronic markets.

• Growth from building market share organically and,where appropriate, through selective acquisition

• Developing and delivering technology to makecross market trading possible. ICAP’s liquidity in abroad range of benchmark derivative and cashmarkets provide a significant competitive advantage

• Enlarging ICAP’s available market making it moreeconomic for banks to trade through us than direct

• Integration between ICAP’s networks and systemsand our customers’ networks and systems createsa pipeline for our products and services. Otherbrokers will find this is difficult and slow to replicate

OU

TLO

OK

90

• A unique combination: the world’s leading voiceand electronic broker

• Continue growing market share (both voice andelectronic) organically and through selectiveacquisition

• Further integration of BrokerTec with roll out of

Cross Connect

• Uncertainty in the global financial markets is likely

to continue and trading can be expected to remain

active.

OUTLOOKO

UT

LOO

K