Investing in Energy & Water...

36

Investing in Energy & Water Infrastructure Thursday 3 December 2015

-

Upload

nguyenquynh -

Category

Documents

-

view

217 -

download

1

Transcript of Investing in Energy & Water...

Investing in Energy & Water

Infrastructure

6.00pm Welcome: Imran Sheikh, Ingenious Clean Energy

6.10pm Introduction: Michael Sippitt, Forbury Investment Network

6.20pm Energy infrastructure – Tony Woods, Managing Consultant, Ricardo

6.40pm Water infrastructure – George Taylor, Chief Technology Officer, Isle Utilities

7.00pm Panel and Q&A, run by Clive Hall, Rushlight Events and augmented by:

Imran Sheikh, Ingenious Clean Energy

Stephen Plumb, Director of Water, Kier Group

8.00pm Networking

Investor Briefing on Energy

Infrastructure

Tony Woods

Managing Consultant

Thursday 3rd December 2015

4 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

• Ricardo Energy & Environment – Who we are

• Structure of the electricity industry in Great Britain and

Key Players

• Innovation in regulation – investment opportunities

• Challenges to networks

• What is a Smart Grid?

• Technical innovation mechanisms

• Where is the power sector going?

• Further Opportunities

• Risks

Overview

5 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

• A global, multi-industry consultancy for engineering, technology, project innovation and

strategy

• Revenue £258m

• Over 2,700 staff working in 21 offices worldwide

• Strategic acquisitions and business reorganisation; Vepro and Power Planning

Associates, Lloyd’s Register Rail and Cascade Consulting.

Ricardo PLC

6 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

• Internationally-renowned consultancy

• Heritage of world-leading scientific/technical capability

• Providing analysis and solutions for major environmental challenges

• Client base of international governments and businesses

• Headquartered at Harwell Science Park, near Oxford

• Over 450 scientists and technical staff

• Part of Ricardo PLC

Ricardo Energy & Environment

7 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

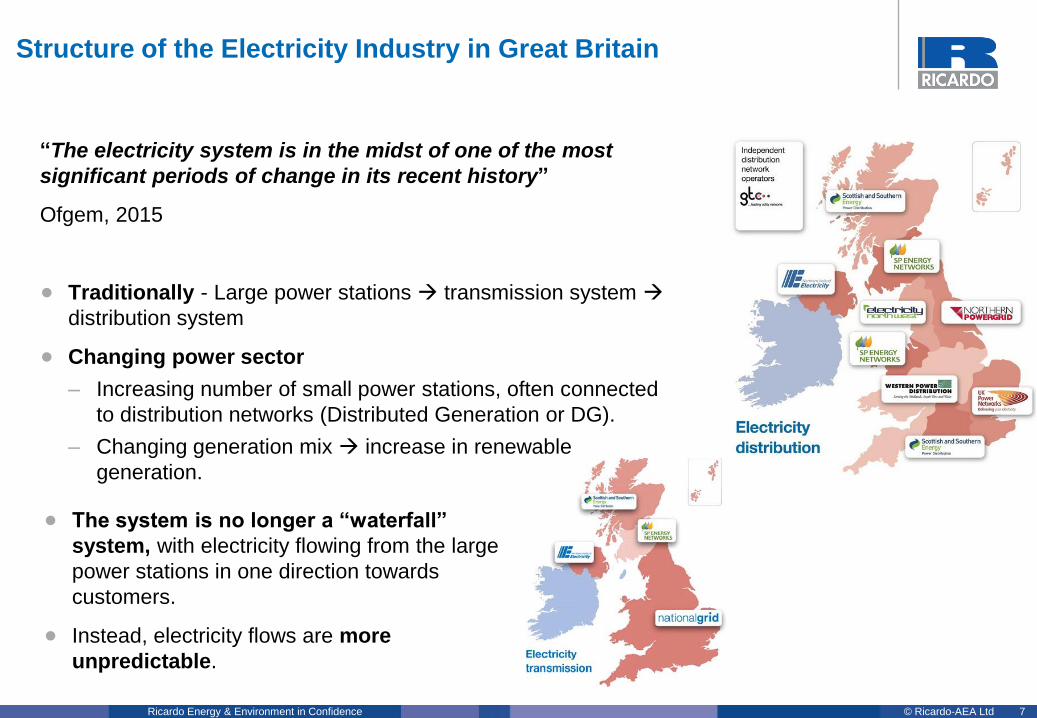

“The electricity system is in the midst of one of the most

significant periods of change in its recent history”

Ofgem, 2015

• Traditionally - Large power stations transmission system

distribution system

• Changing power sector

– Increasing number of small power stations, often connected

to distribution networks (Distributed Generation or DG).

– Changing generation mix increase in renewable

generation.

Structure of the Electricity Industry in Great Britain

• The system is no longer a “waterfall”

system, with electricity flowing from the large

power stations in one direction towards

customers.

• Instead, electricity flows are more

unpredictable.

8 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

Generators

8

Transmission Owners

Aggregators Distribution

Network

Operator

Retail

System

Operator

Key Industry Players

Regulator IDNO

9 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

Innovation in Regulation and Policy – leading to investment

opportunities

Feed in Tariffs (FITs), Renewables Obligation

Certificates (ROCs) and Contracts for Difference

(CfD)

Offshore Transmission Owners (OFTOs)

Image from: Transmission Capital Partners

Independent Distribution Network Operators

Competition in Transmission (CATO)

and Competition in Connections (Distribution)

10 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

Low Carbon Transition

Closure of large coal plants and

increased renewable generation

High uptake of Distributed

Generation in response to incentives

System Operator challenges –

Intermittency and Inertia

Electrification of heat and transport

(timeframe?)

Changing consumer demand – Electric Vehicles and Heat Pumps

Increased data from and visibility

of Low Voltage networks

Challenges to Electricity Networks

BIG DATA

LOWER

SYSTEM

INERTIA

INTERMITTENT

GENERATION

CHANGING

DEMAND

AND PROFILES

11 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

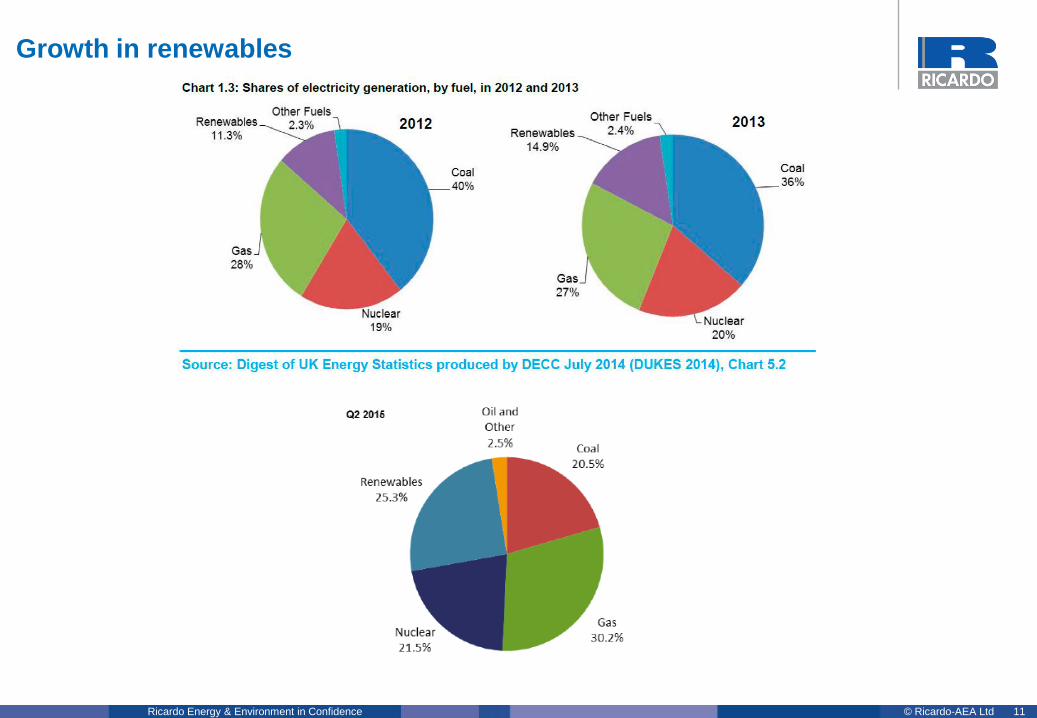

Growth in renewables

12 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

DECC: Digest of United Kingdom Energy Statistics (DUKES)

Contribution of renewable energy to electricity (TWh)

13 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

Low Carbon Transition

Closure of large coal plants and

increased renewable generation

High uptake of Distributed

Generation in response to incentives

System Operator challenges –

Intermittency and Inertia

Electrification of heat and transport

(timeframe?)

Changing consumer demand – Electric Vehicles and Heat Pumps

Increased data from and visibility

of Low Voltage networks

Challenges to Electricity Networks

BIG DATA

LOWER

SYSTEM

INERTIA

INTERMITTENT

GENERATION

CHANGING

DEMAND

AND PROFILES

14 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

What is a Smart Grid?

"Smart Grid" is today used as a marketing term, rather than a technical

definition. For this reason there is no well defined and commonly accepted

scope of what "smart" is and what it is not.

IEC (International

Electrotechnical Commission)

Integration of

Users

Themes:

Increased

monitoring and data

communication

A more active network -

and consumers

Maximise use of

existing assets

Increased

decentralised control

15 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

Network Operator incentives for innovation

• Low Carbon Networks Fund (LCNF) Tier 1 and Tier 2

• Network Innovation Competition (NIC) and Network Innovation Allowance (NIA)

– Gas and Electricity

– Transmission and Distribution

• Energy Systems Catapult – Initially funded by Innovate UK, to stimulate innovation

Technology Innovation Mechanisms

16 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

• New ways of addressing the need for network capacity

– Storage

– Demand Side Response and innovative tariffs

– Use of local generation

• Investment in infrastructure

– RIIO-ED1 and RIIO-T1 capital programmes

• Ofgem’s position paper on Flexibility

– DNO to DSO (Distribution Network Operator to Distribution System Operator)

– Clarifying the role of new market players – aggregators and storage providers

– Evolution of distribution charges (longer term)

• National Grid’s System Operability Framework 2015

– Development of new system services

– Increased co-ordination between transmission and distribution networks

– Increased flexibility from generating plant

Where is the power sector going?

17 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

• Innovation projects developing into business as usual solutions

– Active Network Management

– Power electronics for distribution

– Superconducting cables

• Emerging business models

– Storage providers

– Demand management as part of energy service contract

– Third party aggregators

• New system services required by National Grid System Operator, to access enhanced

capabilities from generation

– Enhanced Frequency Response procurement

– Review of provision of black start capability

Opportunities

Ofgem Position Paper: Making the electricity system more flexible and delivering

the benefits for consumers

“The energy sector is changing. Generation is becoming more distributed and variable, and

consumers are benefitting from new ways to monitor and manage their energy use. There are

opportunities for new business models and technologies to emerge, and for existing

businesses to develop, to deliver better services for consumers.”

18 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

• Political risks

– Changes to incentive mechanisms (Feed-in Tariff reductions, ROCs scheme closing

early for onshore wind)

– Climate change incentives – COP21

– Other policy developments (not supporting Carbon Capture and Storage (CCS),

desired increase in gas-fired power plants)

– Domestic gas and multi-vector interactions

• Consumer behaviour

– Rate of uptake of Low Carbon Technologies (Electric Vehicles and Heat Pumps)

– Willingness to participate in demand side response / realistic level of engagement

• Technical risks

– Developing and new technologies – e.g. Storage and Carbon Capture and Storage

(CCS)

– Developments in transport

Risks

19 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

• Significant changes in the power sector are resulting in challenges…and opportunities

• Infrastructure investment required in transmission and distribution networks…

– Competitively Appointed Transmission Owners (CATO), IDNOs, etc.

• …but investment in “copper” alone will not suffice

– New ways of addressing capacity challenges

– Innovation and Smart Grid projects – maximising the use of existing assets

– Emerging business models

– New system services required

Summary

20 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

Thank You

21 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

Appendix

22 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

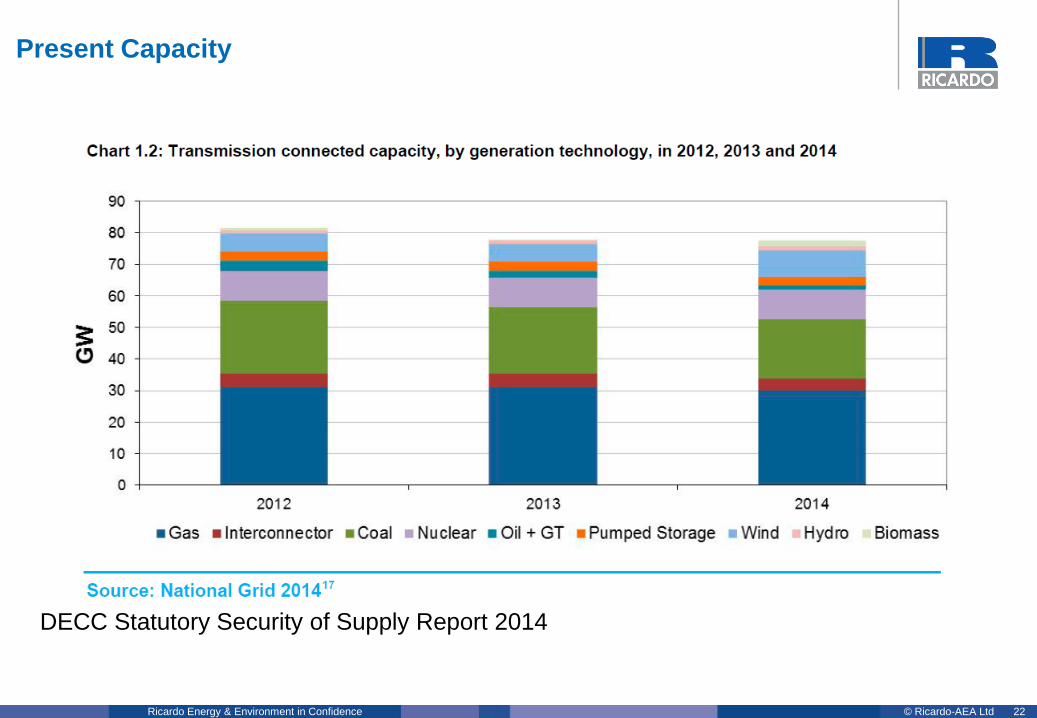

Present Capacity

DECC Statutory Security of Supply Report 2014

23 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

• As of end of March 2014, the UK had a total of around 77.6 GW of installed electricity

capacity connected directly to the transmission system, including available

interconnection capacity.

• In addition to transmission connected capacity, there is an estimated 11 GW of

electricity capacity connected directly to the distribution network also known as

‘embedded’ generation.

• GB also has the means to import from and export to other countries; the equivalent of

just under 4 GW of capacity can be transmitted to and from France, the Netherlands

and Ireland.

24 © Ricardo-AEA Ltd Ricardo Energy & Environment in Confidence

INVESTING IN ENERGY AND WATER INFRASTRUCTURE….

GEORGE TAYLOR CHIEF TECHNOLOGY OFFICER

25

Water Infrastructure….

Existing Infrastructure….

Decentralised – Wastewater, Water

Competition

Waste water

Clean Water

Future challenges…..

09/12/2015 isleutilities.com 26

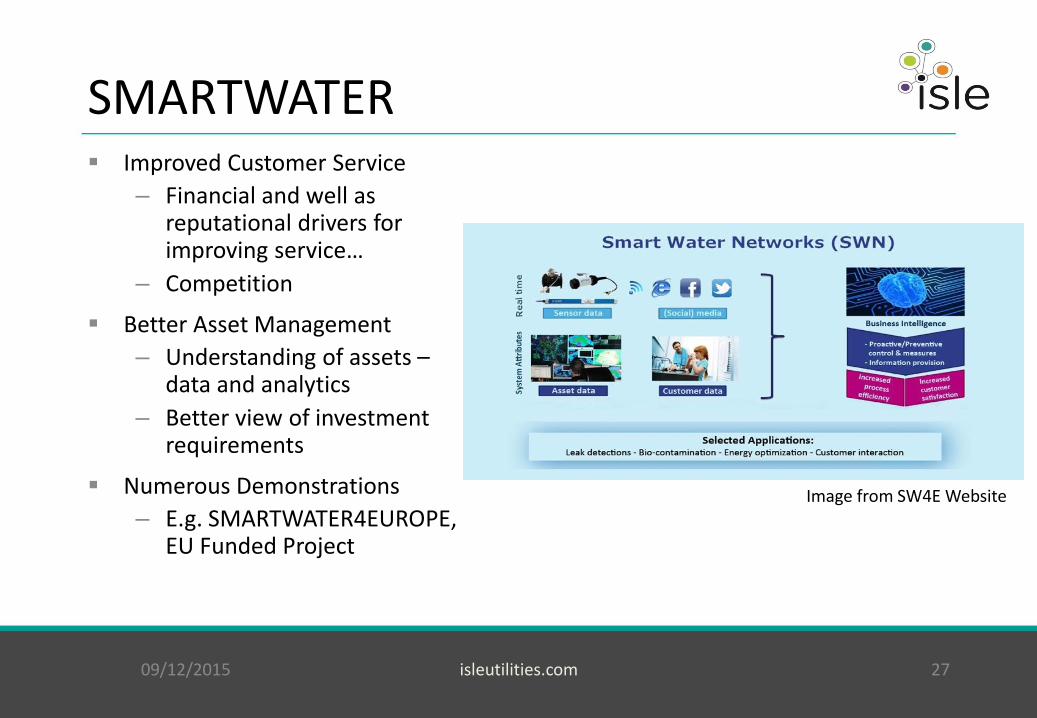

SMARTWATER Improved Customer Service

– Financial and well as reputational drivers for improving service…

– Competition

Better Asset Management

– Understanding of assets – data and analytics

– Better view of investment requirements

Numerous Demonstrations

– E.g. SMARTWATER4EUROPE, EU Funded Project

09/12/2015 isleutilities.com 27

Image from SW4E Website

Understanding condition….

416,000 kms of water main

369,000 kms of sewer

Current sewer replacement rates mean sewers have to last over 1000 years!

Good asset management requires that companies understand where and when to replace and the associated risks.

Improve resilience....

09/12/2015 isleutilities.com 28

But what if we don’t replace pipes?

Decentralisation

– Drinking Water - alternatives

– Waste Water - alternatives

09/12/2015 isleutilities.com 29

Competition….

Commercial Customer

– March 2017

Domestic Customer

– Could be in place by the end of this parliament

Upstream

– Could be in place by the end of this parliament…

09/12/2015 isleutilities.com 30

Wastewater – or Recycling….

Energy recovery

– Combined heat and power

– Thermal Hydrolosis (THP)

– Alternatives….

Nutrient recovery

– Phophorus – finite resource

Heat recovery (and cooling)

09/12/2015 isleutilities.com 31

Water – resources

Growth and climate change contributing to future supply demand deficits in part of the country…

– Water efficiency

– Metering

– Water trading

– Alternative sources – reuse, desalination, reservoirs, water transfer schemes

09/12/2015 isleutilities.com 32

UK Water Industry Research (UKWIR)

Three Big Questions….

How do we achieve zero leakage by 2050?

How can we achieve zero uncontrolled discharges from sewers by 2050?

How do we maintain 100% compliance with drinking water standards by 2050?

09/12/2015 isleutilities.com 33

WWT Innovation Conference 2015….

Managing and Monitoring SMART Networks

Technology game changers

– Nanotechnology – filters

– Robotics – inspection technologies

– Smart – phone applications

Energy from Waste

09/12/2015 isleutilities.com 34

Investing in Energy & Water Infrastructure

Q&As panel:

Tony Woods, Ricardo

George Taylor, Isle Utilities

Stephen Plumb, Kier Group

Imran Sheikh, Ingenious Clean Energy