Inventory Control & Determining Profitability · Inventory Control & Determining Profitability 2...

21

1 1 Dr. Charlie Hall Dr. Charlie Hall c- [email protected] [email protected] ellisonchair.tamu.edu ellisonchair.tamu.edu Inventory Control & Determining Profitability Inventory Control & Determining Profitability 2 Inventory control is seemingly a paradoxical oxymoron. • Paradox = a self‐contradictory and false proposition. It seems to be easy but its not! It seems to be easy but its not! • Oxymoron = a rhetorical figure in which incongruous or contradictory terms are combined. e.g. deafening silence, cruel e.g. deafening silence, cruel kindness, inventory kindness, inventory control control , etc. , etc.

Transcript of Inventory Control & Determining Profitability · Inventory Control & Determining Profitability 2...

1

1

Dr. Charlie HallDr. Charlie [email protected]@tamu.edu

ellisonchair.tamu.eduellisonchair.tamu.edu

Inventory Control & Determining ProfitabilityInventory Control & Determining Profitability

2

Inventory control is seemingly a paradoxical oxymoron.

• Paradox = a self‐contradictory and false proposition. It seems to be easy but its not!It seems to be easy but its not!

• Oxymoron = a rhetorical figure in which incongruous or contradictory terms are combined. e.g. deafening silence, cruel e.g. deafening silence, cruel kindness, inventory kindness, inventory controlcontrol, etc., etc.

2

3

The basic inventory problem…

•• ““How many ___ can I get by ____?How many ___ can I get by ____?””

• You need information fast! – To know if you can substitute something else

– Or to know when you will have the item.

• Sounds simple, but…

4

Inventory control is not the same for all types of firms!

• It is a complex activity unique to each green industry sector.– Nursery growers (container, field, PIP)

– Greenhouse growers (bench vs air space)

– Propagation

– Service firms

– Retail firms

3

5

Inventory control is not thesame for all sizes of firms!

• It is a complex activity unique to the size of the firm in each green industry sector.

– Hobbyists

– Mom & pop businesses (small)

– Medium‐sized non‐corporate firms

– Large corporate firms

complexity

6

Tracking inventory is rarelyan exact science.

• Plants die.

• Some grow too fast & too large and get cut back.

• Others grow too slow.

• Some simply don’t sell.

4

7

So why worry with it?

• Minimizes over‐ & under‐selling

• Basis for planning labor needs, work schedules, space requirements, and supplies needed.

• Calculating COGS and determining prices.

• Analyze impact of cultural practices on inventory turns.

8

DistributionAnd

OutboundLogistics

Production

PurchasedSupplies

andInboundLogistics

Sales andMarketing Service Profit

Margin

Product R&D, Technology, Systems Development

Human Resources Management

General Administration

SupportActivitiesand Costs

Managing inventory is pervasive throughout the value chain.

5

9

Managing inventory involves...

• Developing an accurate sales forecast.– Consumer trends ‐ Vendor managed inventory– Pre‐booked sales ‐ Production contracts

– Invasive species ‐ Niche differentiation

• Developing a production plan to make inventory available when & where customers want it.

10

Managing inventory involves...

• Building relationships with quality suppliers.

– JIT vs stockpiling

• Setting realistic inventory turnover objectives and computing the cost of carrying inventory.

6

11

Managing inventory involves...

• Using the most timely and accurate information system the business can afford to provide everyone with vital inventory information.

• Teaching employees how inventory control systems work so they can help manage inventory on a daily basis.

12

Types of inventory – based on stage of completion

• Raw materials inventory ‐ includes the cost of materials being held for future use.

• Work in process inventory ‐ includes the cost incurred for partially completed items, including costs of raw materials, labor, and other costs

• Finished goods inventory ‐ the accumulated costs of “goods” that are finished and ready for sale

7

13

Perpetual and periodic physical inventory systems

• Two main systems for keeping inventory records:– Perpetual inventory system ‐ keeps a running, continuous record of inventories on a day‐to‐day basis.

– Periodic physical inventory system ‐computed periodically by relying solely on physical counts without keeping day‐to‐day records of units sold or on hand.

14

Comparing accounting procedures for periodic and perpetual inventory systems

• Under the perpetual system, inventory amounts are updated each time an inventory transaction is processed.

• Under a periodic system, the inventory account does not change until the end of the accounting period.

– At that time, a physical inventory is taken to determine the amount of inventory on hand, and an adjusting entry is made to inventory.

8

15

Do not underestimate the need for accurate dumpage records!

• Key resource in possible litigation.

• Crop insurance necessity.

• Accuracy of perpetual inventory depends on it.

16

Methods of valuing inventory

• Cost method

• Lower of cost or market method

• Retail method

9

17

The value placed on inventory can have a significant effect on the net income of a company. Because net income is the basis of calculating federal income tax, accountants frequently must decide whether to value inventory to reflect higher net profit to entice investors or lower net profit to minimize income taxes.

Consider the effects on tax liability

18

Cross-docking? A sound theory but still in the “proving” stage.

• shifts the focus from "supply chain" to "demand chain"

• stock coming in has already been pre‐allocated against a replenishment order generated by a retailer in the supply chain

10

19

Photo courtesy of Rick Goff, Advanced Grower Solutions

20

RFID, bar code and scanner technology

11

21

The “tablet pc” in action

Photos courtesy of Rick Goff, Advanced Grower Solutions

22

The ideal software package???

• It used to be a paradoxical oxymoron. Butthings have improved – dramatically!

• Off‐the‐shelf vs. program your own?

• Refer to hbin.tamu.eduhbin.tamu.eduHorticultural Business Information Network

12

23

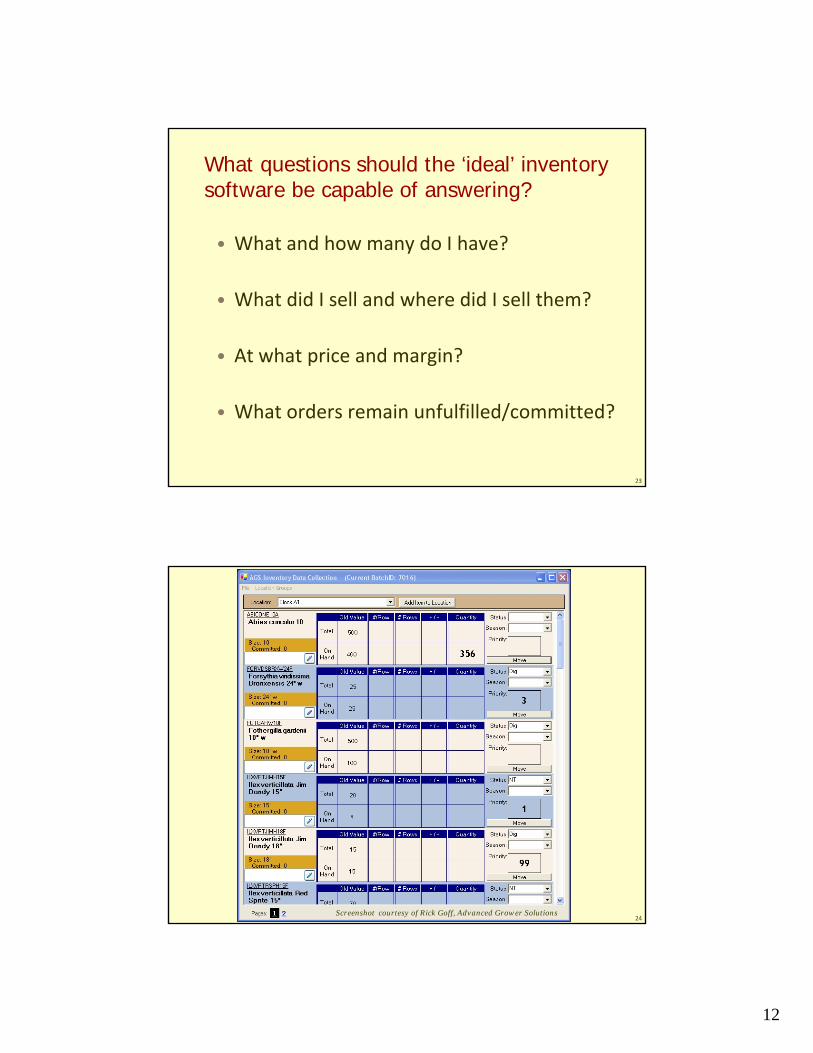

What questions should the ‘ideal’ inventory software be capable of answering?

• What and how many do I have?

• What did I sell and where did I sell them?

• At what price and margin?

• What orders remain unfulfilled/committed?

24Screenshot courtesy of Rick Goff, Advanced Grower Solutions

13

25

Making the transition…

• A NEW MODEL: Most vendors will offer transition services to get you “online.” A few are offering software as a service on a “subscription” basis (usually monthly).

• Costs (and capabilities) vary widely, so doing your homework is essential. Talk with peers, but recognize you are unique.

SAASSAAS

26

Remember…

• Many tend to invest in an inventory control software package for the wrong reason. They feel it will do the work for them!

• Information overload is a real possibility. Pare down the reports to the ones you will actually use!

14

27

Inventory Profitability Metrics

28

Inventory turnover analysis

• The most basic and fundamental tool for controlling your investment in inventory

• Assist you in deciding which items or categories need attention.

• Identifies items that take too long to sale.

15

29

Inventory turnover analysis, cont.

• Requires calculation of individual item sales.

• Points to items that have excessive, low, or the right amount of inventory.

• Carrying costs should be used as a factor when determining how much inventory you need to fulfill your customer order requirements.

30

Inventory turnover calculation

• IT = COGS ÷ Average Inventory

• An indication of the velocity with which dollars move through the business

• In WGNA study, typical growers sell out the equivalent of inventory value 0.6 times per year.

16

31

Inventory holding period calculation

• 365 ÷ Inventory turnover

• Shows how long it should take to sell off existing inventory. Cost of carrying inventory has to be weighed against lost profit of not having product ready to sell.

32

WNGA Cost of Doing Business Report –results by nursery type

17

33

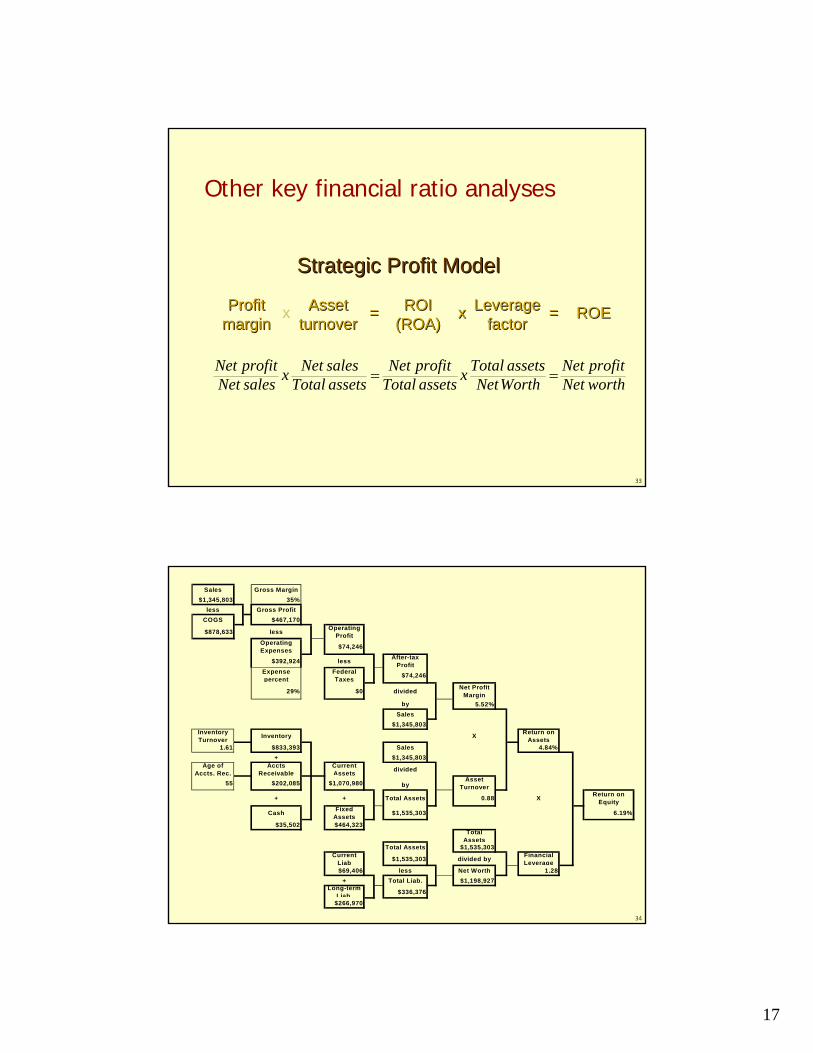

Other key financial ratio analyses

Net profitNet sales x Net sales

Total assetsNet profit

Total assets x Total assetsNetWorth

Net profitNet worth= =

Profit Profit marginmargin

Asset Asset turnoverturnover

ROI ROI (ROA)(ROA)

x == xx Leverage Leverage factorfactor == ROEROE

Strategic Profit ModelStrategic Profit Model

34

Sales Gross Margin$1,345,803 35%

less Gross ProfitCOGS $467,170

$878,633 less Operating Profit

Operating Expenses $74,246

$392,924 less After-tax Profit

Expense percent

Federal Taxes $74,246

29% $0 divided Net Profit Margin

by 5.52%Sales

$1,345,803Inventory Turnover Inventory X Return on

Assets1.61 $833,393 Sales 4.84%

+ $1,345,803Age of

Accts. Rec.Accts

ReceivableCurrent Assets divided

55 $202,085 $1,070,980 byAsset

Turnover

+ + Total Assets 0.88 X Return on Equity

Cash Fixed Assets $1,535,303 6.19%

$35,502 $464,323Total

AssetsTotal Assets $1,535,303

Current Liab $1,535,303 divided by Financial

Leverage$69,406 less Net Worth 1.28

+ Total Liab. $1,198,927Long-term

Liab. $336,376

$266,970

18

35

WNGA Cost of Doing Business Report –results by nursery type

36

WNGA Cost of Doing Business Report –results by size of firm

19

37

WNGA Cost of Doing Business Report –results by size of firm

38

WNGA Cost of Doing Business Report –results by size of firm

20

39

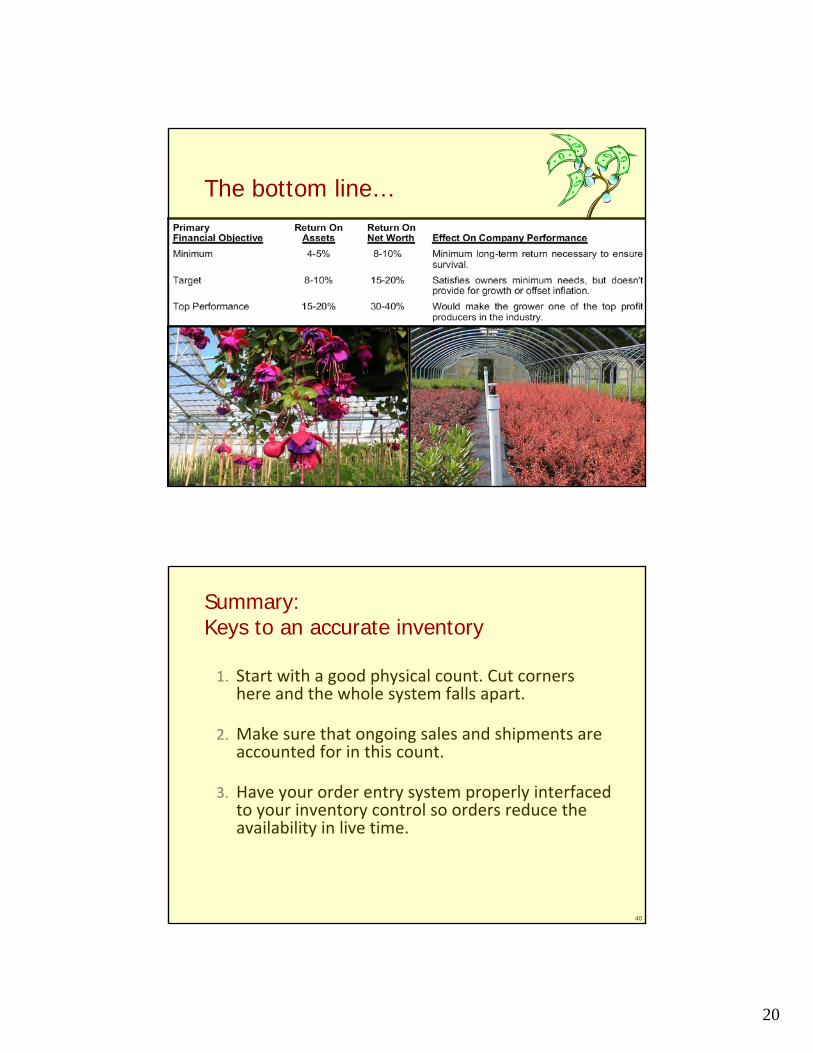

The bottom line…

40

Summary:Keys to an accurate inventory

1. Start with a good physical count. Cut corners here and the whole system falls apart.

2. Make sure that ongoing sales and shipments are accounted for in this count.

3. Have your order entry system properly interfaced to your inventory control so orders reduce the availability in live time.

21

41

Summary:Keys to an accurate inventory

4. Ensure that the invoice or shipping process is being performed in a timely manner so the “on hand” counts in the system reflect the reality out in the field.

5. Initiate the proper controls on your fulfillment teams so that inventory is being pulled from the correct locations.

6. Put measures in place to account for waste, shrinkage and inventory moves.

42

Questions?Questions?

Dr. Charlie HallDr. Charlie [email protected]@tamu.edu

ellisonchair.tamu.eduellisonchair.tamu.edu