INVENTORY Accounting ASW Summer 2005. Two Inventory Issues Manufacturing accounting –what if you...

22

INVENTORY Accounting ASW Summer 2005

-

date post

19-Dec-2015 -

Category

Documents

-

view

216 -

download

0

Transcript of INVENTORY Accounting ASW Summer 2005. Two Inventory Issues Manufacturing accounting –what if you...

INVENTORY

Accounting ASW

Summer 2005

Two Inventory Issues

• Manufacturing accounting– what if you make inventory rather than buying?

• Inventory cost flow assumptions– how do you know which units you sold?

Manufacturing Accounting

• How do we value inventory/CGS for a manufacturing firm?

• Should include all costs of acquiring the product and making it ready for sale

Overview of Manufacturing Firm

• Period costs

- Selling, general and administrative, etc.

• Production costs

Period Costs

• Examples - corporate headquarters - marketing, advertising - finance, interest - research and development

• Generate period costs charged to expense - just as in a merchandising firm

Product Costs

• Identify all relevant costs of “acquiring”– Direct labor

• labor costs which can be linked to specific product

• typically costs of employees working directly on that product

• assigned based on actual labor used

• Direct materials

– materials costs which can be linked to products

– typically major components of the product

– assigned based on actual materials used

• Overhead--can’t be linked to products– indirect labor

• e.g., janitorial, supervisor

– indirect materials• e.g., supplies, small components

– overhead• e.g., depr., rent, utilities on production facilities

– allocate based on “drivers”• e.g., direct labor, direct materials

Are these product or period costs?Cutting-machine operatorFactory janitorFactory payroll clerksFactory superintendentGeneral office secretaryGuards at the factory gateInspectors in a factoryFactory maintenance workersFactory security guardsGeneral office clerksPresident of the firmSales managerRaw materials receiving room workersSweepers who clean a retail storeTraveling salespersons

Physical flow

• Raw materials into warehouse

• Materials and labor on plant floor

• Finished product to warehouse

• Shipped out when sold

Cost allocation

• Cost of materials inputs into raw material inventory when acquired

• Cost of materials, labor & overhead into work in process inventory as produced

• Total cost incurred into finished goods inventory when completed

• Total cost into cost of goods sold at sale

DIRECT COSTSWages Payable (Dir. Labor)

Raw Mat. Inv. (Dir. Materials)

Inc. Statement

Sales WIP Inv. FG Inv.

- CGS

GMOVERHEAD - SG&A

Wages Payable NI (Indir. Labor)

Accum. Depr. (Depreciation)

S, G & A ExpenseSalaries Pay.

(SG&A Exp.)

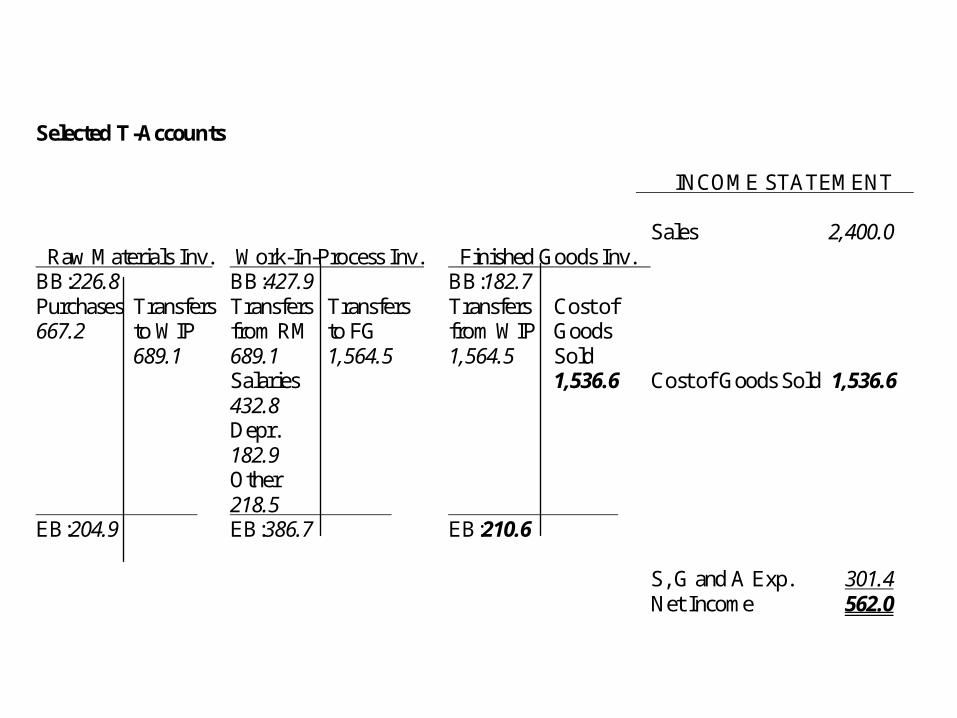

Journal Entries—Problem 7.36 Raw Materials Inventory (B/S-A) 667.2 Cash (B/S-A) 667.2 Acquire raw materials Work-in-Process Inventory (B/S-A) 689.1 Raw Materials Inventory (B/S-A) 689.1 Place raw materials in production Work-in-Process Inventory (B/S-A) 432.8 Selling, Gen’l and Admin. Exp. (I/S-E) 112.0 Cash (B/S-A) 544.8 Pay salaries, part for production and part for S,G&A Work-in-Process Inventory (B/S-A) 182.9 Selling, Gen’l and Admin. Exp. (I/S-E) 99.6 Accumulated Depreciation (B/S-CA) 282.5 Record depreciation, split between production and S,G&A Work-in-Process Inventory (B/S-A) 218.5 Selling, Gen’l and Admin. Exp. (I/S-E) 89.8 Cash (B/S-A) 308.3 Pay other costs, part for production and part for S,G&A Finished Goods Inventory (B/S-A) 1,564.5 Work-in-Process Inventory (B/S-A) 1,564.5 Complete production of a portion of the work in progress Accounts Receivable (B/S-A) 2,400.0 Sales Revenue (I/S-R) 2,400.0 Sell a portion of the completed units Cost of Goods Sold (I/S-E) 1,536.6 Finished Goods Inventory (B/S-A) 1,536.6 Record cost of units sold

Selected T-Accounts INCOME STATEMENT Sales 2,400.0 Raw Materials Inv. Work-In-Process Inv. Finished Goods Inv. BB:226.8 BB:427.9 BB:182.7 Purchases Transfers Transfers Transfers Transfers Cost of 667.2 to WIP from RM to FG from WIP Goods 689.1 689.1 1,564.5 1,564.5 Sold Salaries 1,536.6 Cost of Goods Sold 1,536.6 432.8 Depr. 182.9 Other 218.5 EB:204.9 EB:386.7 EB:210.6 S, G and A Exp. 301.4 Net Income 562.0

Inventory Accounting

Inventory xx

Cash xx

Cost of Goods Sold xx

Inventory xx

Issue: How do you know which inventory you sold?

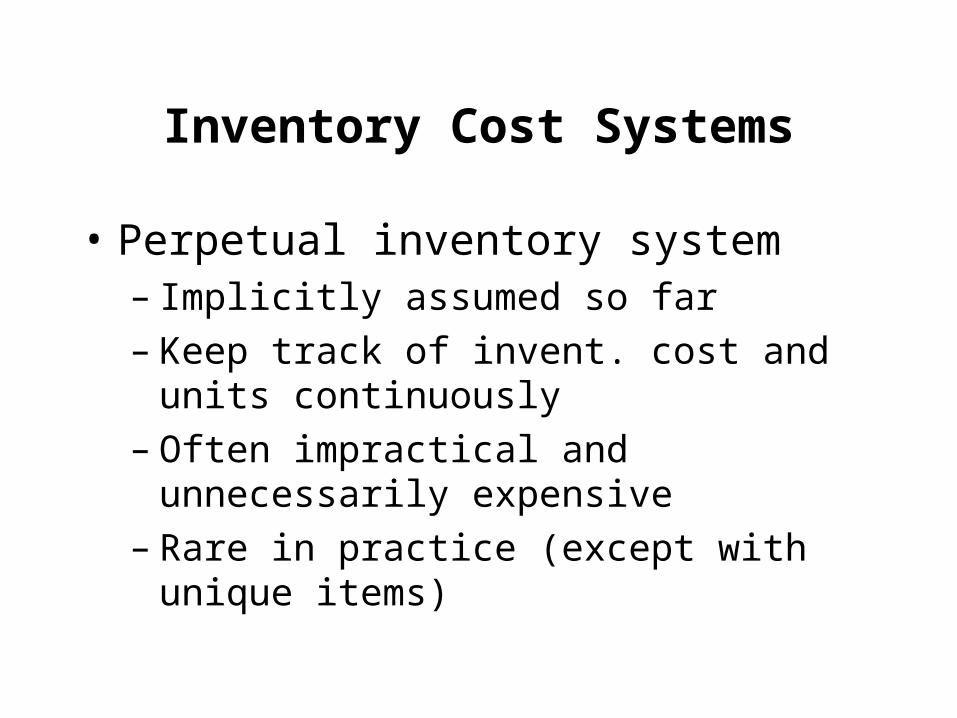

Inventory Cost Systems

• Perpetual inventory system– Implicitly assumed so far– Keep track of invent. cost and units continuously– Often impractical and unnecessarily expensive– Rare in practice (except with unique items)

• Periodic inventory system

– keeps track of beginning inventory & purchases

– uses ending balance in inventory to infer cost of goods sold

– most common approach

Inventory Equations• Problem 7.29

Beg. Inv. + Purchases = Cost of Goods Available for Sale

$0 + $24,384 = $24,384

0 Units + 10,700 units = 10,700 units available

CGAS - Ending Inventory = Cost of Goods Sold

$24,384 - Ending Inventory = Cost of Goods Sold

10,700 - 3,500 = 7,200 units sold• How to infer what products were sold?

- only important if prices are changing

- typically make an assumption

Ways to measure cost flows

• Specific identification - identify specific item being sold - accurately measures cost - cumbersome and expensive

• Cost flow assumption - need not mirror actual flows - all three are common in practice

Cost flow assumptions

• First In, First Out (FIFO)

– assumes first ones purchased were first sold

– generally matches costs and unit flows

– high net income and inventory balances if prices are increasing

• Last In, First Out (LIFO)– assumes last ones purchased were first sold– poor matching of costs and unit flows– low net income and inventory balances if prices are

increasing– required in US for financial reporting if used for tax– rare outside the US– exception to general rule that financial reporting

does not need to match tax

• Weighted average

– assumes inventory sold was purchased at average cost

– generally good matching of costs and unit flows

– net income and inventory balances between LIFO and FIFO (most similar to FIFO)