Introduction to Venture Capital - edXRWTHx+VC101x+1T2017+type@asset... · School of Business and...

17

School of Business and Economics TIME Research Area | Innovation & Entrepreneurship Group (WIN) Introduction to Venture Capital Week 2 Understanding the pre-investment phase

Transcript of Introduction to Venture Capital - edXRWTHx+VC101x+1T2017+type@asset... · School of Business and...

School of Business and Economics TIME Research Area | Innovation & Entrepreneurship Group (WIN)

Introduction to Venture Capital Week 2 Understanding the pre-investment phase

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

2 © Innovation & Entrepreneurship Group

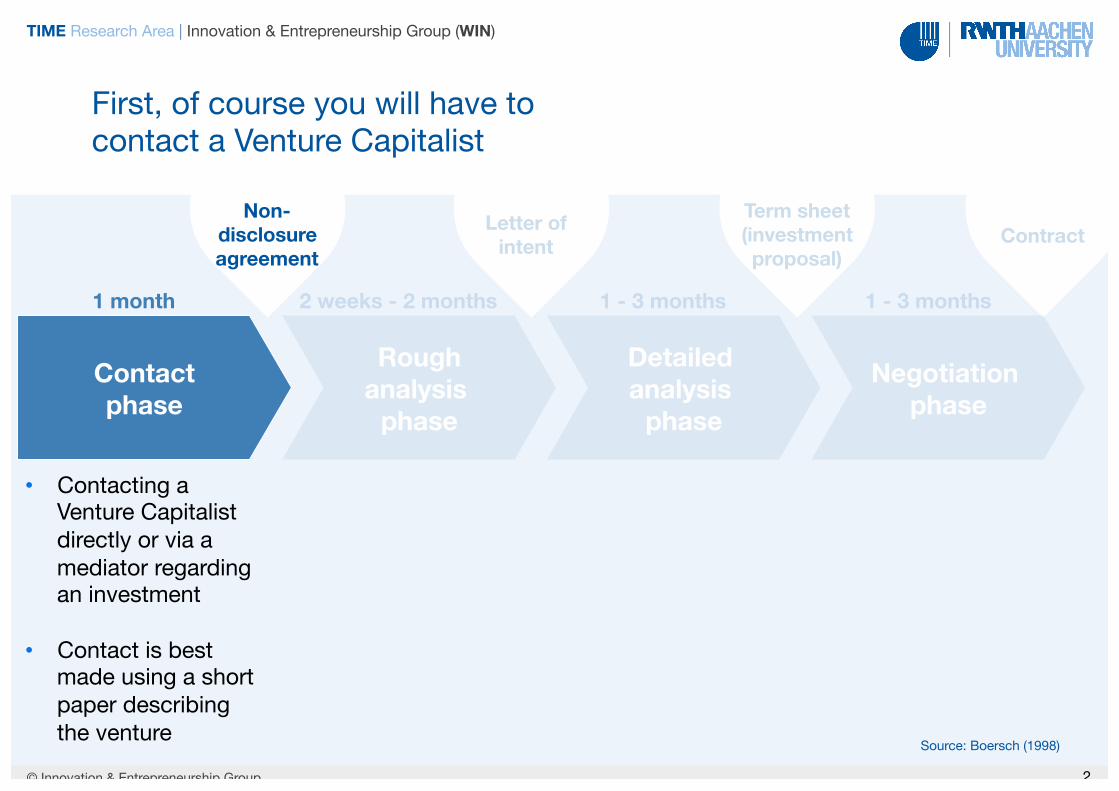

First, of course you will have to contact a Venture Capitalist

Contactphase

Roughanalysis

phase

Detailed analysis

phase Negotiation

phase

1 month 2 weeks - 2 months 1 - 3 months 1 - 3 months

Letter of intent

Term sheet(investment proposal)

Contract Non-

disclosureagreement

• Contacting a Venture Capitalist directly or via a mediator regarding an investment

• Contact is best

made using a short paper describing the venture

Source: Boersch (1998)

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

3 © Innovation & Entrepreneurship Group

Upon your contact, the VC will evaluate whether they will further investigate your proposal

Contactphase

Roughanalysis

phase

Detailed analysis

phase Negotiation

phase

1 month 2 weeks - 2 months 1 - 3 months 1 - 3 months

Letter of intent

Term sheet(investment proposal)

Contract Non-

disclosureagreement

• Contacting a Venture Capitalist directly or via a mediator regarding an investment

• Contact is best made using a short paper describing the venture

• Venture Capitalist makes a preliminary decision on whether to follow up on the contact or not

• Up to 90% of

investment proposals fail at this stage

Source: Boersch (1998)

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

4 © Innovation & Entrepreneurship Group

If you make the cut, the VC will get in contact with you and enter a detailed analysis

Contactphase

Roughanalysis

phase

Detailed analysis

phase Negotiation

phase

1 month 2 weeks - 2 months 1 - 3 months 1 - 3 months

Letter of intent

Term sheet(investment proposal)

Contract Non-

disclosureagreement

• Contacting a Venture Capitalist directly or via a mediator regarding an investment

• Contact is best made using a short paper describing the venture

• Venture Capitalist makes a preliminary decision on whether to follow up on the contact or not

• Up to 90% of investment proposals fail at this stage

• Business plan is checked in detail (due diligence)

• Several meetings

between the Venture Capitalist and the entrepreneurs usually take place in this phase

Source: Boersch (1998)

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

5 © Innovation & Entrepreneurship Group

If all goes well, you might enter the last stage and negotiate a deal with the Venture Capitalist

Contactphase

Roughanalysis

phase

Detailed analysis

phase Negotiation

phase

1 month 2 weeks - 2 months 1 - 3 months 1 - 3 months

Letter of intent

Term sheet(investment proposal)

Contract Non-

disclosureagreement

• Contacting a Venture Capitalist directly or via a mediator regarding an investment

• Contact is best made using a short paper describing the venture

• Venture Capitalist makes a preliminary decision on whether to follow up on the contact or not

• Up to 90% of investment proposals fail at this stage

• Business plan is checked in detail (due diligence)

• Several meetings

between the Venture Capitalist and the entrepreneurs usually take place in this phase

• Final negotiations about all details of the contract

• Negotiations may

take place over a period of several months

Source: Boersch (1998)

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

6 © Innovation & Entrepreneurship Group

In total, you should expect the process to take at least 6 Months until deal closure

Contactphase

Roughanalysis

phase

Detailed analysis

phase Negotiation

phase

1 month 2 weeks - 2 months 1 - 3 months 1 - 3 months

Letter of intent

Term sheet(investment proposal)

Contract Non-

disclosureagreement

• Contacting a Venture Capitalist directly or via a mediator regarding an investment

• Contact is best

made using a short paper describing the venture

• Venture Capitalist makes a preliminary decision on whether to follow up on the contact or not

• Up to 90% of

investment proposals fail at this stage

• Business plan is checked in detail (due diligence)

• Several meetings

between the Venture Capitalist and the entrepreneurs usually take place in this phase

• Final negotiations about all details of the contract

• Negotiations may

take place over a period of several months

Source: Boersch (1998)

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

7 © Innovation & Entrepreneurship Group

Contactphase

Roughanalysis

phase

Detailed analysis

phase Negotiation

phase

1 month 2 weeks - 2 months 1 - 3 months 1 - 3 months

Letter of intent

Term sheet(investment proposal)

Contract Non-

disclosureagreement

This week we will focus on:

Selection of a VC and Tips on getting chosen

by the VC

Source: Boersch (1998), Icons designed by Freepik

• Contacting a Venture Capitalist directly or via a mediator regarding an investment

• Contact is best

made using a short paper describing the venture

• Venture Capitalist makes a preliminary decision on whether to follow up on the contact or not

• Up to 90% of

investment proposals fail at this stage

School of Business and Economics TIME Research Area | Innovation & Entrepreneurship Group (WIN)

Introduction to Venture Capital Week 2 Choosing the (right) VC

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

2 © Innovation & Entrepreneurship Group

First of all, is an institutional Venture Capitalist really the right financing partner for your venture?

Family & Friends

Strategic Investor (e.g. CVC)

Venture Capitalist

Business Angel

Crowdfunding

Who is right for me?

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

3 © Innovation & Entrepreneurship Group

The selection of a potential Venture Capital partner highly depends on the investment phase

Seed Startup Expansion

• Many seed financings are too small and require too much hands-on support from the venture capital firm to make them economically viable as investments

• Contact is best made using a short paper describing the venture

• Venture capitalists makes a preliminary decision on whether to follow up on the contact or not

• Up to 90% of investment

proposals fail at this stage

• Business plan is checked in detail (due diligence)

• Several meetings between

the venture capitalists and the entrepreneurs usually take place in this phase

VC?

Source: IVCA

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

4 © Innovation & Entrepreneurship Group

If your venture is in the right situation to seek institutional VC funding, make up your mind about the following selection criteria

Name and reputation of the Venture Capitalists 1

Development phase of the company 2

Industry sector of firm and Venture Capitalists 3

Required financing volume 4

Location of the Venture Capitalists 5

Venture Capitalists have a different reputation, which reflects on the young company or influences future financing rounds

Different Venture Capitalists finance different development phases of young companies

Venture Capitalists sometimes have a specialization on a certain industry sector

Different Venture Capitalists invest different amounts

Rule of thumb: if the company cannot be reached within two hours, the probability of an investment is not so high

Criterion Relevance

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

5 © Innovation & Entrepreneurship Group

It’s no bad idea to keep these general guidelines in mind when selecting a potential VC

Source: Stanford Business School

Listen to your instinct

Negotiate from a position of strength

Find shared beliefs Pay more attention to the partnership

than the terms

School of Business and Economics TIME Research Area | Innovation & Entrepreneurship Group (WIN)

Introduction to Venture Capital Week 2 Get chosen by the right VC – increase your chances!

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

2 © Innovation & Entrepreneurship Group

Approaching the right Venture Capitalist

Identification and selection of a potential Venture Capital partner depend not only on your current investment phase…

Name and reputation of the venture capitalists

Development phase of the company

Industry sector of firm and venture capitalists

Required financing volume

Location of the venture capitalists

Long-list of potential Venture Capitalist

Sorting of relevant Venture Capitalists

• 3i • Accel Partners • Andreessen Horowitz • Atlas ventures • Greylock Partners • OCA Ventures • Holzbrinck Ventures • Venrock • …

Executive summary of your business idea

1

2

3

4

5

Icons by Freepik

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

3 © Innovation & Entrepreneurship Group

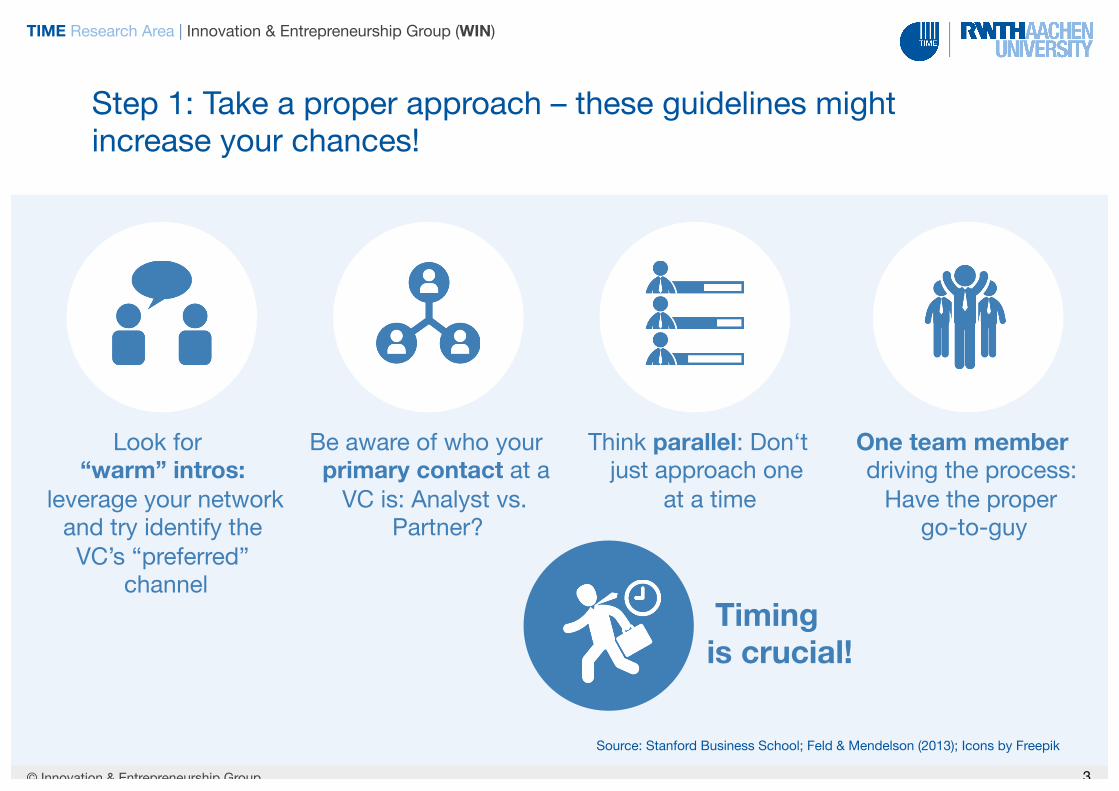

Step 1: Take a proper approach – these guidelines might increase your chances!

Source: Stanford Business School; Feld & Mendelson (2013); Icons by Freepik

Look for “warm” intros:

leverage your network and try identify the VC’s “preferred”

channel

Be aware of who your primary contact at a

VC is: Analyst vs. Partner?

Think parallel: Don‘t just approach one

at a time

One team member driving the process:

Have the proper go-to-guy

Timing is crucial!

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

4 © Innovation & Entrepreneurship Group

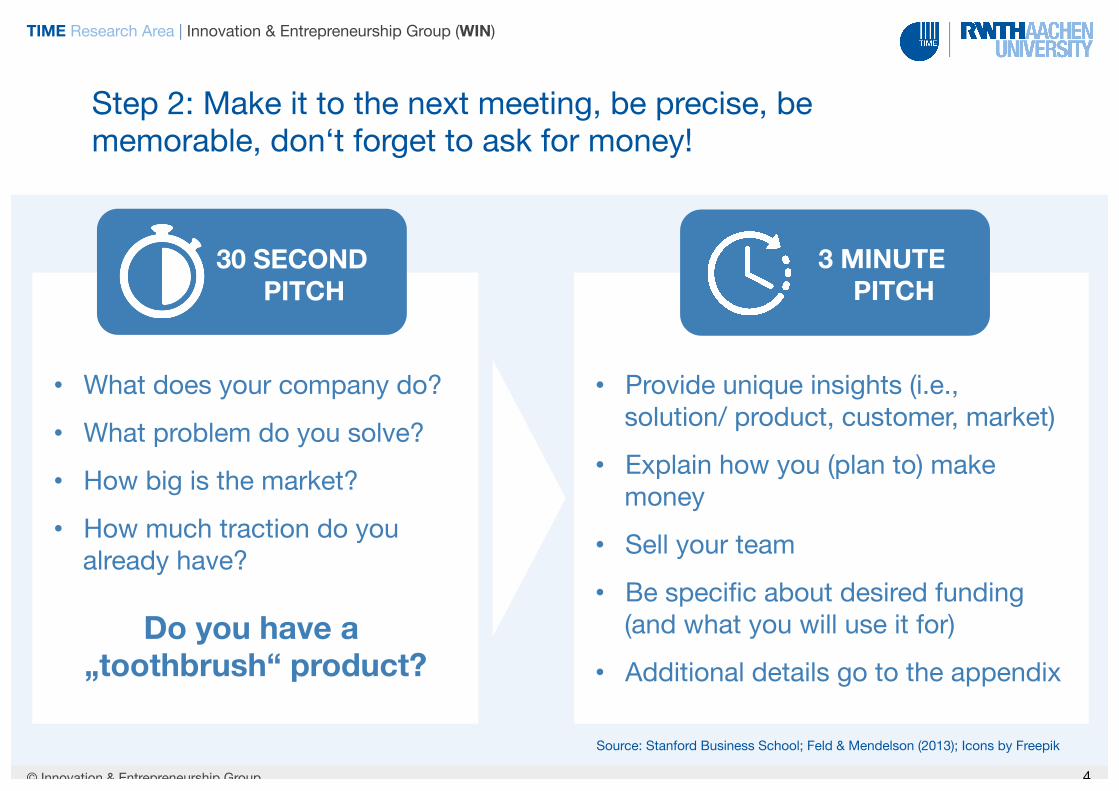

Step 2: Make it to the next meeting, be precise, be memorable, don‘t forget to ask for money!

Source: Stanford Business School; Feld & Mendelson (2013); Icons by Freepik

• What does your company do? • What problem do you solve? • How big is the market? • How much traction do you

already have?

30 SECOND PITCH

3 MINUTE PITCH

Do you have a „toothbrush“ product?

• Provide unique insights (i.e., solution/ product, customer, market)

• Explain how you (plan to) make money

• Sell your team • Be specific about desired funding

(and what you will use it for) • Additional details go to the appendix

TIME Research Area | Innovation & Entrepreneurship Group (WIN)

5 © Innovation & Entrepreneurship Group

Step 3: Avoid mistakes and pay attention to detail – more handy advice coming right up:

Source: Stanford Business School; Feld & Mendelson (2013); Icons by Freepik

INTRODUCTION PROGRESS

MARKET SIZE

Make sure the listener understands what you’re doing

Show it and know your numbers!

Ideally build bottom up analysis (drivers)

INSIGHTS The investor should learn something that is counter-intuitive

TEAM Your team should be uniquely suited for this business

ASKING FOR MONEY Drive the conversation towards a conclusion – but don’t make the claim that you won’t need future funding after this round

INTRODUCTIONS TO OTHER FOUNDERS THEY HAVE BACKED Maybe the best source of information on how the VC will act once they are invested