From cost to profit centre...Title From cost to profit centre Keywords ()

Upload

frederica-fergusonCategory

view

229download

1

Introduction to revenue, cost and

profit terms

Variable and fixed costs, cost-volume-profit analysis

Pia Nylinder

Organization of the presentation

• Variable cost

• Fixed cost

• Cost volume profit (CVP) analysis

• Decision-making

• Opportunity costs

• Sunk costs

Variable and fixed costs

Principles of cost divisionCost terms and concepts

Activity level Variable and fixed costs

Cost assignment Direct and indirect costs

Decision making Relevant and irrelevant costs

Variable and fixed cost can be used in different situations

Cost volume profit analysis

Budgeting

Product costing

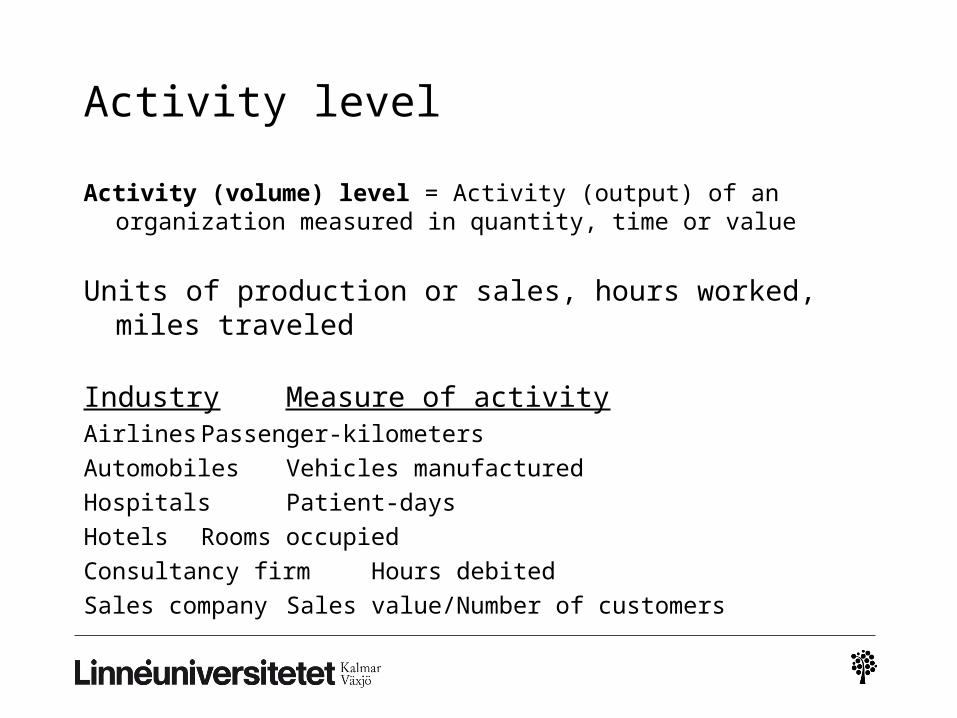

Activity level

Activity (volume) level = Activity (output) of an organization measured in quantity, time or value

Units of production or sales, hours worked, miles traveled

Industry Measure of activityAirlines Passenger-kilometers

Automobiles Vehicles manufactured

Hospitals Patient-days

Hotels Rooms occupied

Consultancy firm Hours debited

Sales company Sales value/Number of customers

Variable costs

Variable Cost = A cost that varies in total when the volume of activity changes

Linearity of variable costs

Nonlinearity of variable costs (two types of nonlinierity)

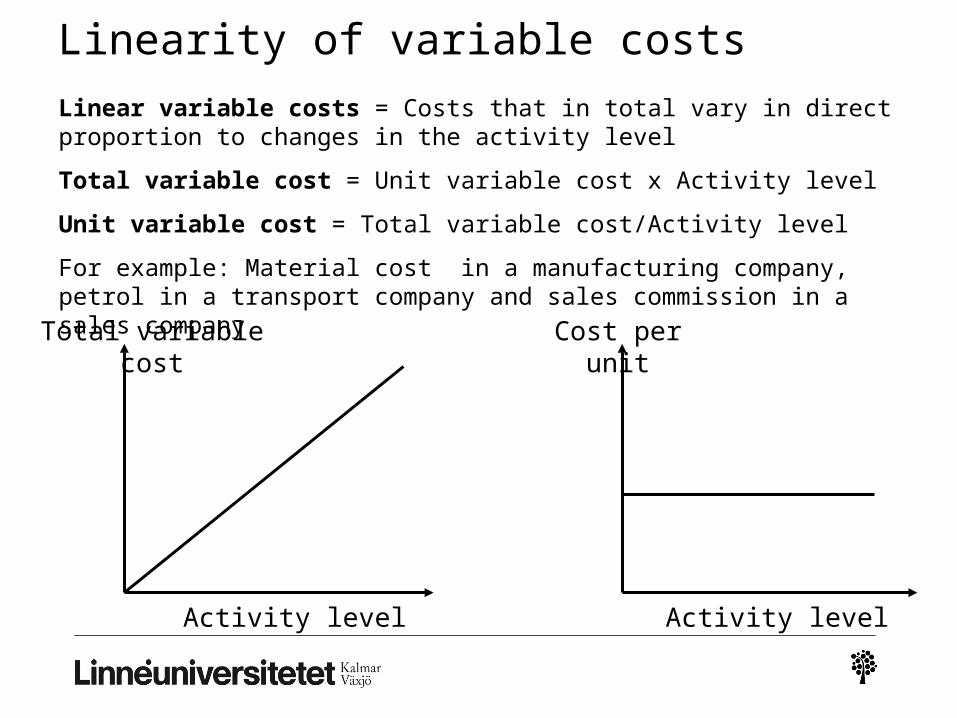

Linearity of variable costs

Cost per unit

Activity level Activity level

Linear variable costs = Costs that in total vary in direct proportion to changes in the activity level

Total variable cost = Unit variable cost x Activity level

Unit variable cost = Total variable cost/Activity level

For example: Material cost in a manufacturing company, petrol in a transport company and sales commission in a sales company

Total variable cost

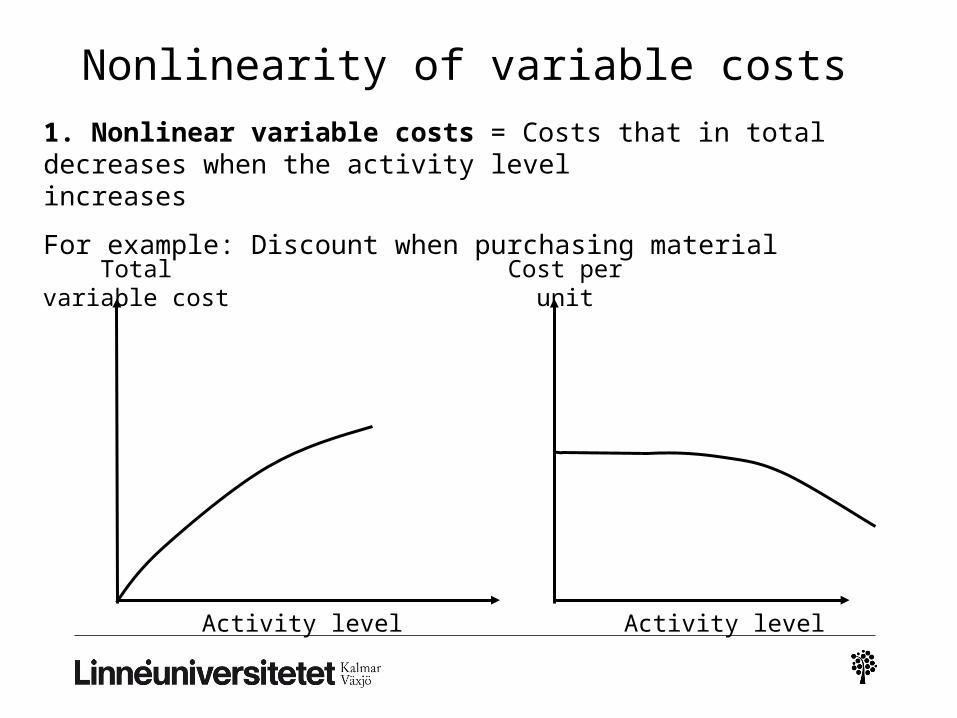

Nonlinearity of variable costs

Cost per unit

Activity level Activity level

1. Nonlinear variable costs = Costs that in total decreases when the activity level increases

For example: Discount when purchasing material

Total variable cost

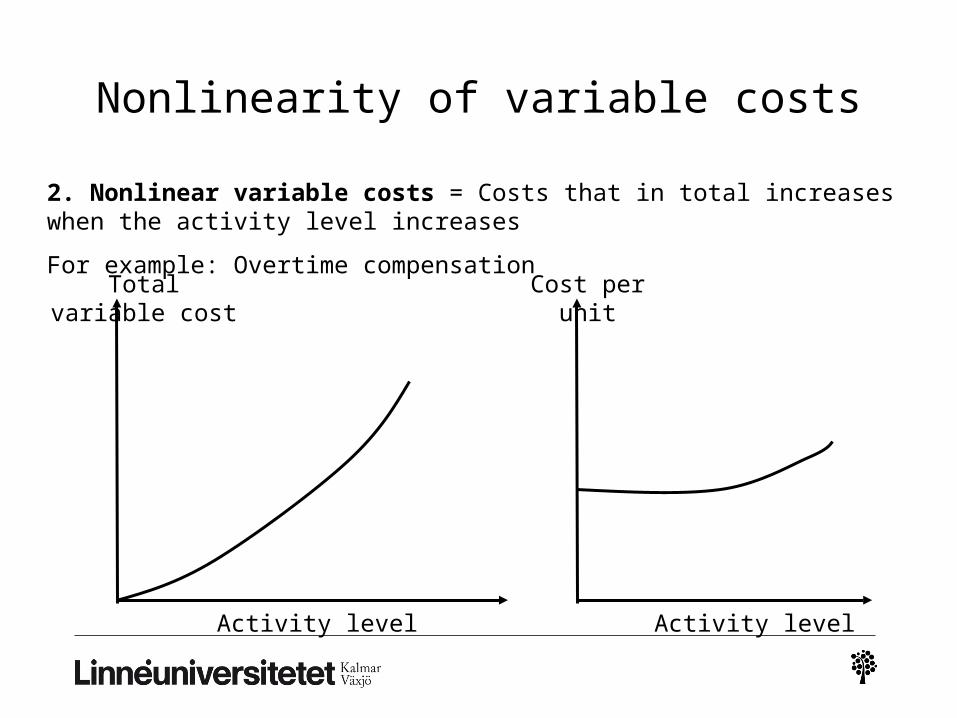

Nonlinearity of variable costs

Total variable cost Cost per unit

Activity level Activity level

2. Nonlinear variable costs = Costs that in total increases when the activity level increases

For example: Overtime compensation

Fixed costs

Fixed costs

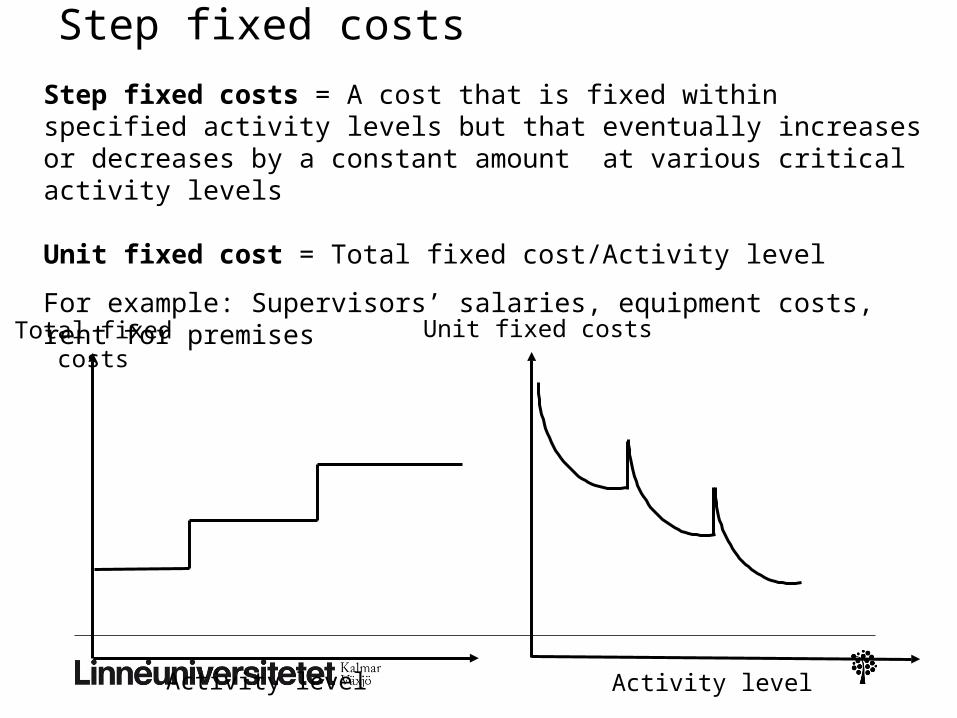

Step fixed costs (Semi-fixed)

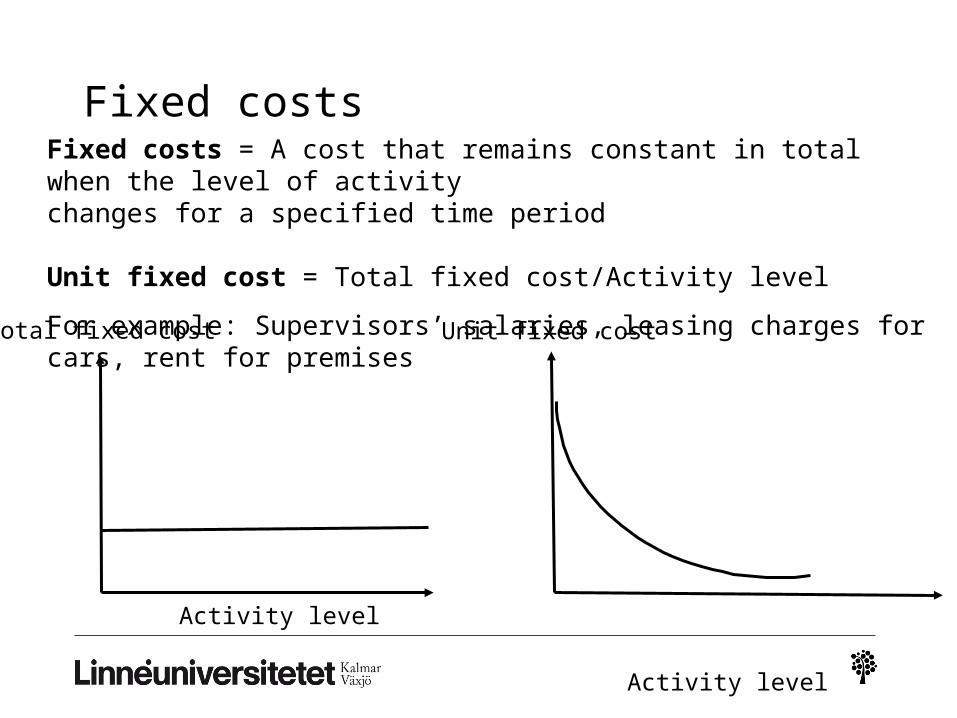

Fixed costs

Total fixed cost

Unit fixed cost

Activity level

Activity level

Fixed costs = A cost that remains constant in total when the level of activity changes for a specified time period

Unit fixed cost = Total fixed cost/Activity level

For example: Supervisors’ salaries, leasing charges for cars, rent for premises

Fixed costs

Two important assumptions

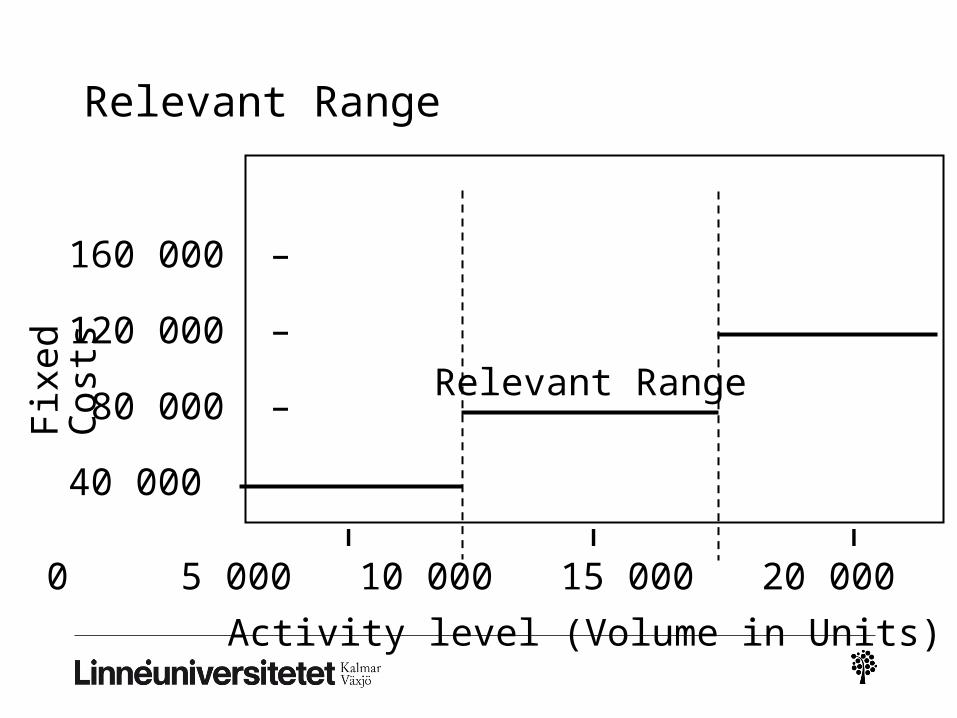

Relevant rangeAn output range of activity level that the firm expects to be operating

within period of time

Time spanA cost is only fixed for a short period of time, for instance a month or a

year

Relevant Range

Fix

ed

Cos

ts

Activity level (Volume in Units)

160 000 –

120 000 –

80 000 –

40 000

0 5 000 10 000 15 000 20 000 25 000

– – –

Relevant Range

Step fixed costs

Total fixed costs

Activity level

Unit fixed costs

Activity level

Step fixed costs = A cost that is fixed within specified activity levels but that eventually increases or decreases by a constant amount at various critical activity levels

Unit fixed cost = Total fixed cost/Activity level

For example: Supervisors’ salaries, equipment costs, rent for premises

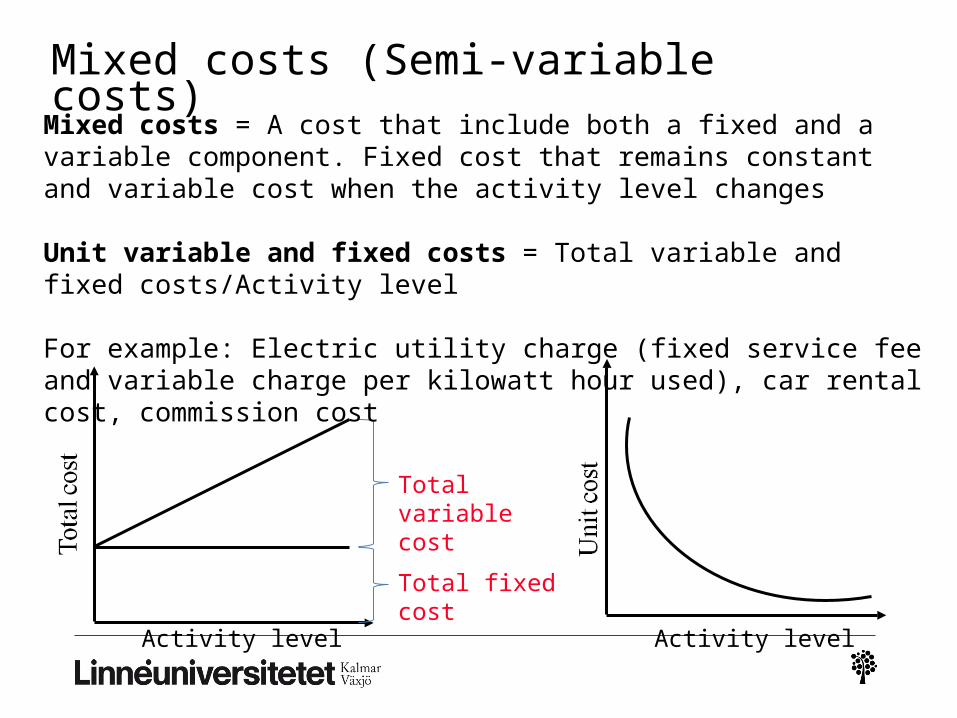

Mixed costs (Semi-variable costs)

Activity level Activity level

Total fixed cost

Total variable cost

Mixed costs = A cost that include both a fixed and a variable component. Fixed cost that remains constant and variable cost when the activity level changes

Unit variable and fixed costs = Total variable and fixed costs/Activity level

For example: Electric utility charge (fixed service fee and variable charge per kilowatt hour used), car rental cost, commission cost

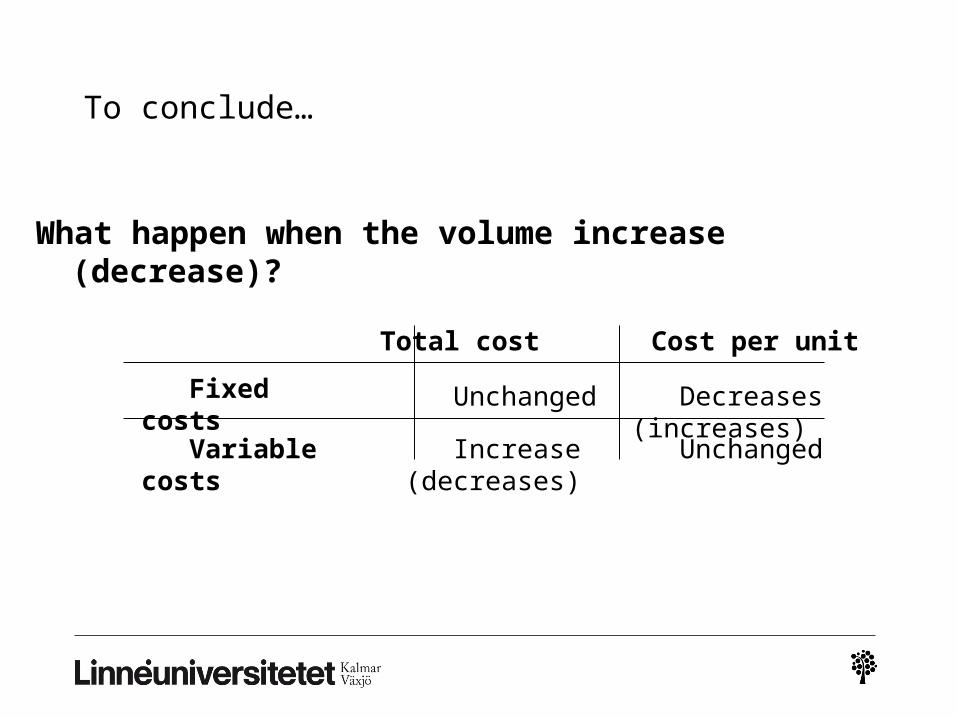

To conclude…

What happen when the volume increase (decrease)?

Total cost Cost per unit

Fixed costs

Variable costs

Unchanged Decreases (increases)

Increase (decreases)

Unchanged

Cost volume profit (CVP) relationship

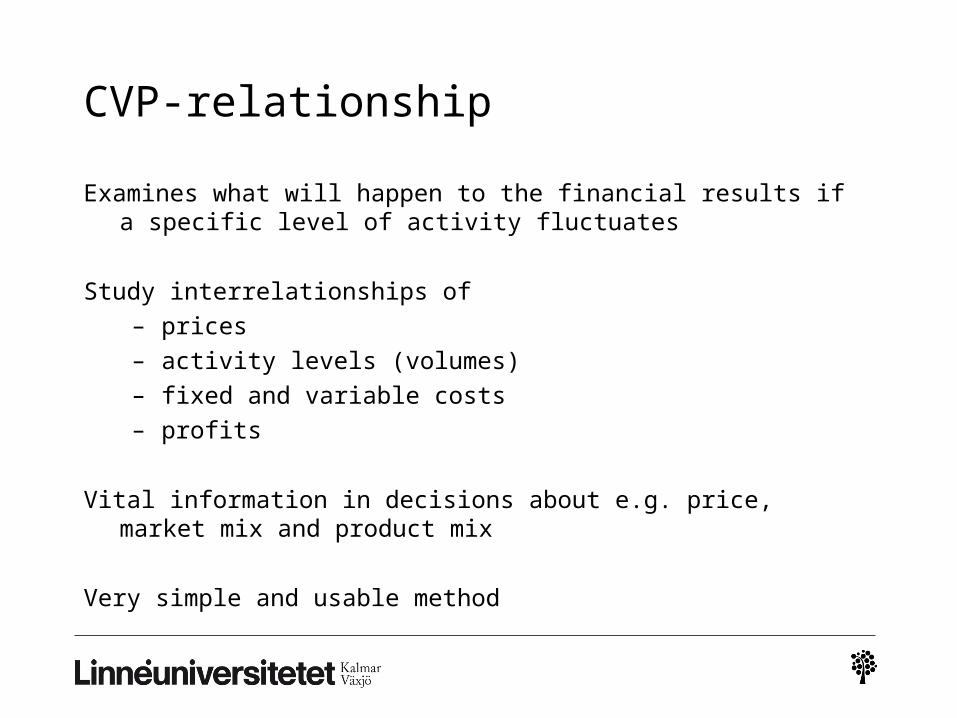

CVP-relationship

Examines what will happen to the financial results if a specific level of activity fluctuates

Study interrelationships of

– prices

– activity levels (volumes)

– fixed and variable costs

– profits

Vital information in decisions about e.g. price, market mix and product mix

Very simple and usable method

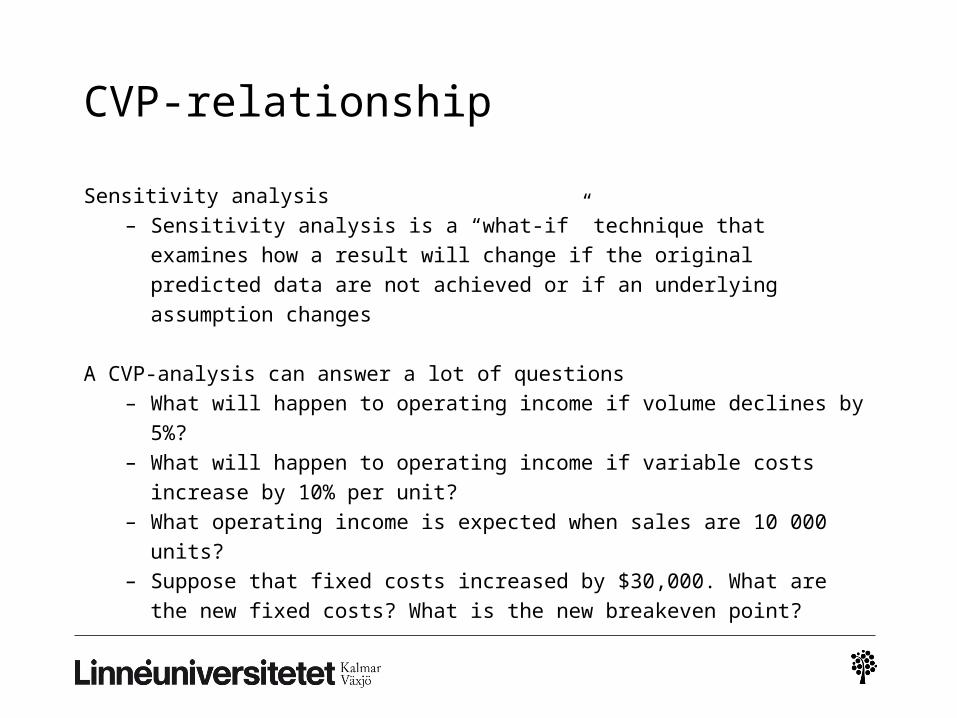

CVP-relationship

Sensitivity analysis

– Sensitivity analysis is a “what-if” technique that examines how a result

will change if the original predicted data are not achieved or if an

underlying assumption changes

A CVP-analysis can answer a lot of questions

– What will happen to operating income if volume declines by 5%?

– What will happen to operating income if variable costs increase by 10%

per unit?

– What operating income is expected when sales are 10 000 units?

– Suppose that fixed costs increased by $30,000. What are the new fixed

costs? What is the new breakeven point?

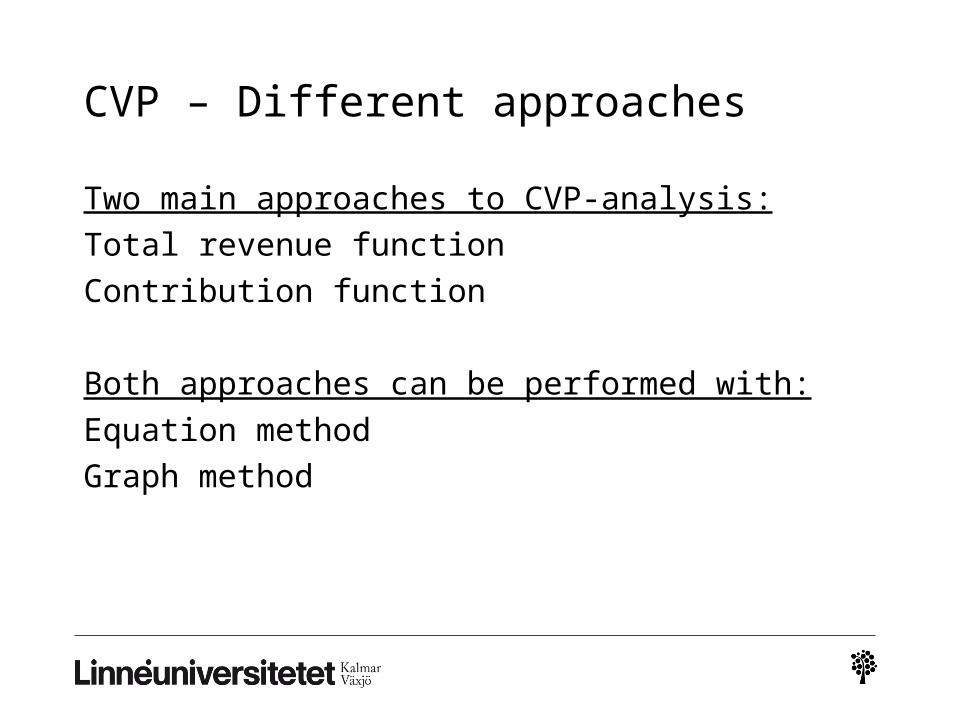

CVP – Different approaches

Two main approaches to CVP-analysis:

Total revenue function

Contribution function

Both approaches can be performed with:

Equation method

Graph method

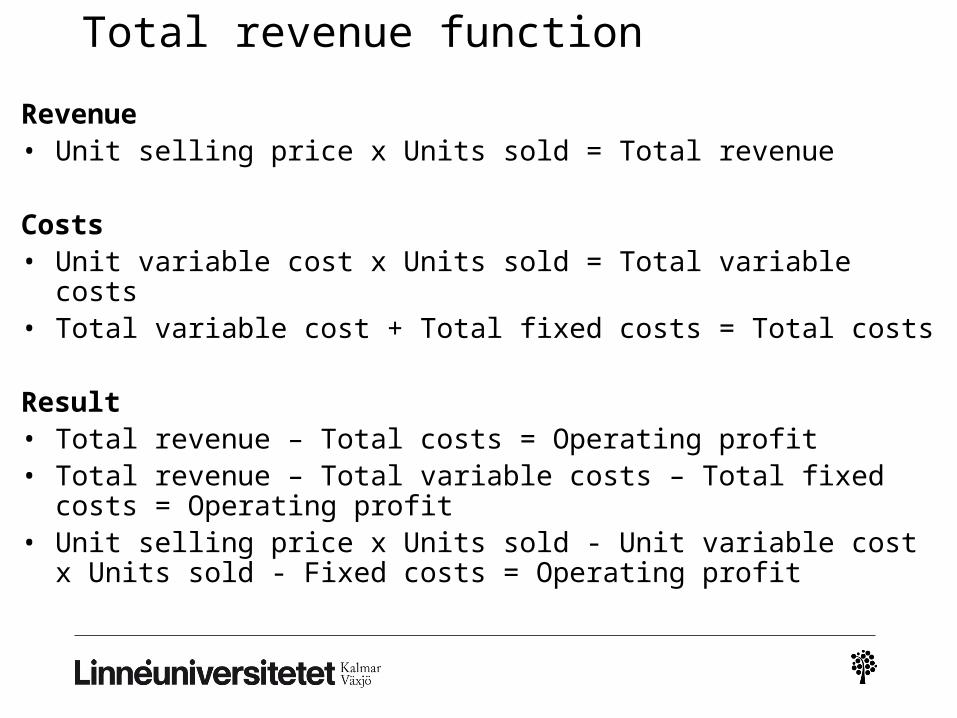

Total revenue function

Revenue• Unit selling price x Units sold = Total revenue

Costs• Unit variable cost x Units sold = Total variable costs• Total variable cost + Total fixed costs = Total costs

Result• Total revenue – Total costs = Operating profit• Total revenue – Total variable costs – Total fixed costs =

Operating profit• Unit selling price x Units sold - Unit variable cost x Units

sold - Fixed costs = Operating profit

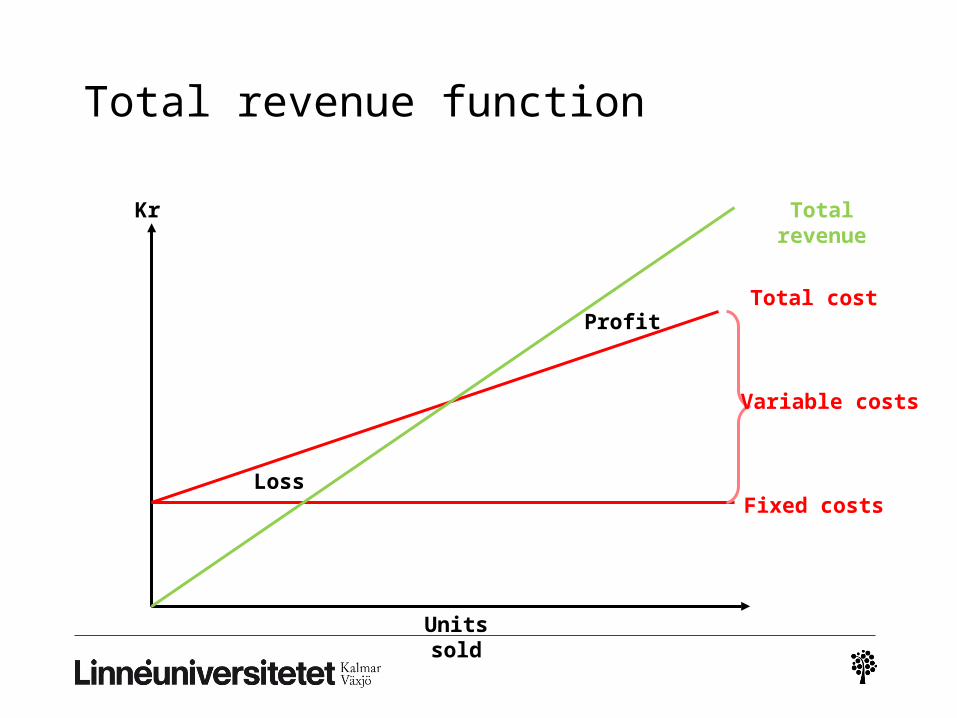

Total revenue function

Kr

Units sold

Fixed costs

Variable costs

Total cost

Total revenue

Loss

Profit

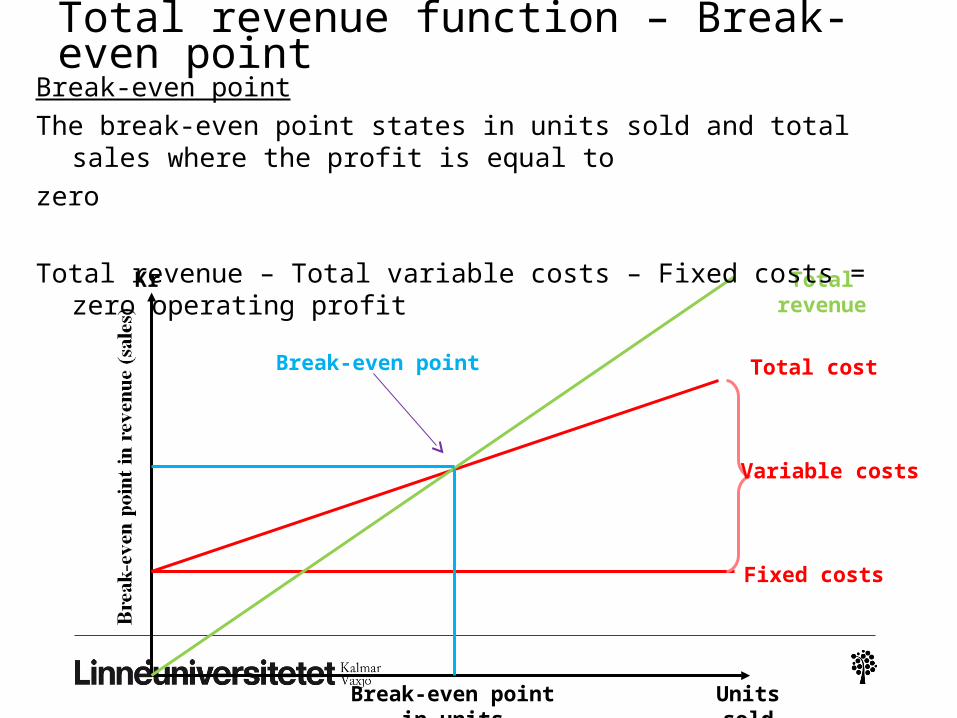

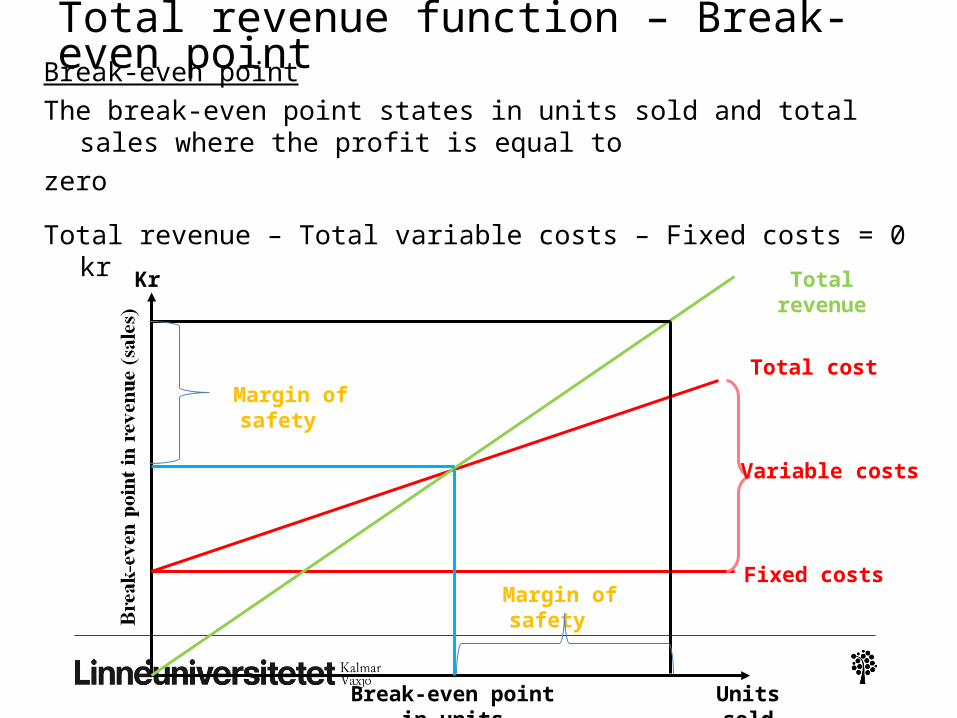

Total revenue function – Break- even point

Kr

Units sold

Fixed costs

Variable costs

Total cost

Total revenue

Break-even point in units

Break-even point

Break-even point

The break-even point states in units sold and total sales where the profit is equal to

zero

Total revenue – Total variable costs – Fixed costs = zero operating profit

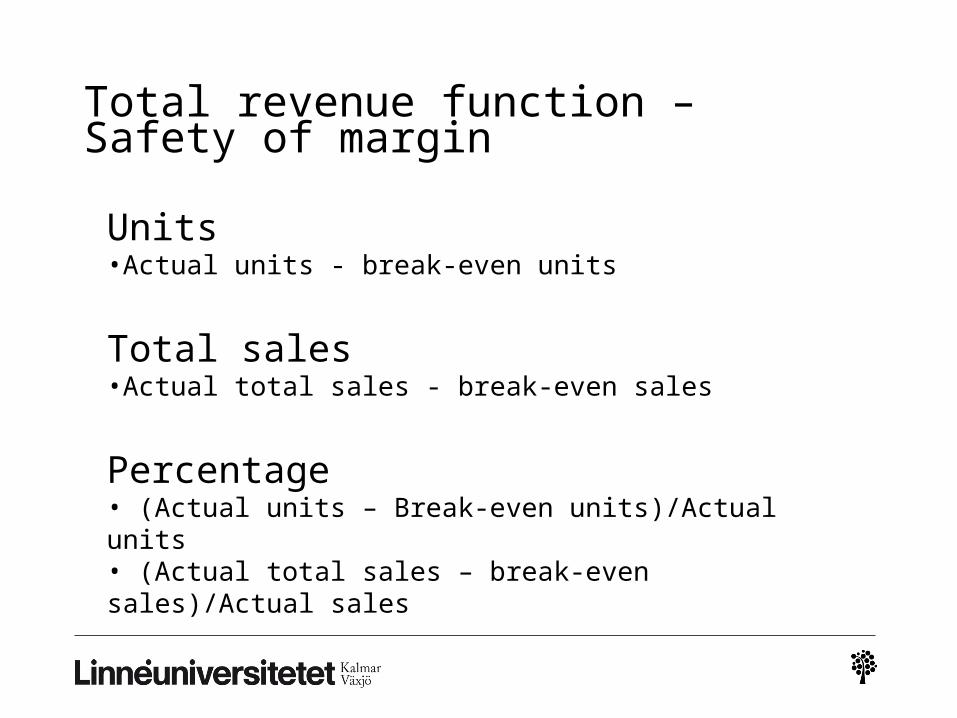

Total revenue function – Safety of margin

Safety of margin

• Indicates by how much sales may decrease before a loss occurs

• Can be expressed in actual units and actual sales

• Margin of safety percentage

Total revenue function – Break- even point

Kr

Units sold

Fixed costs

Variable costs

Total cost

Total revenue

Break-even point in units

Break-even point

The break-even point states in units sold and total sales where the profit is equal to

zero

Total revenue – Total variable costs – Fixed costs = 0 kr

Margin of safety

Margin of safety

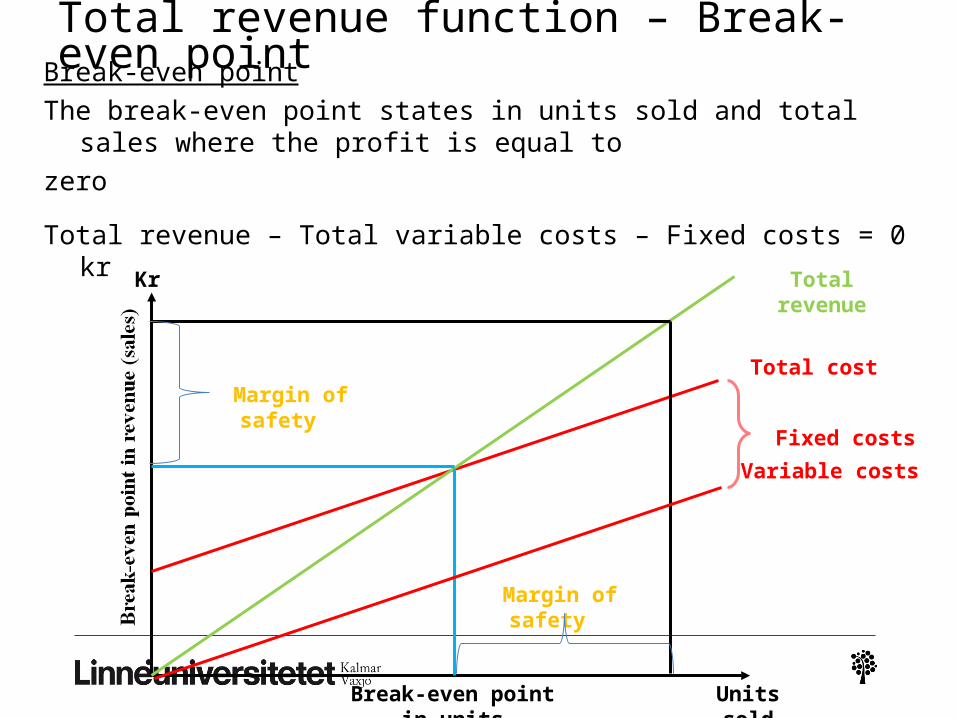

Total revenue function – Break- even point

Kr

Units sold

Fixed costs

Variable costs

Total cost

Total revenue

Break-even point in units

Break-even point

The break-even point states in units sold and total sales where the profit is equal to

zero

Total revenue – Total variable costs – Fixed costs = 0 kr

Margin of safety

Margin of safety

Total revenue function – Safety of margin

Units •Actual units - break-even units

Total sales •Actual total sales - break-even sales

Percentage• (Actual units – Break-even units)/Actual units• (Actual total sales – break-even sales)/Actual sales

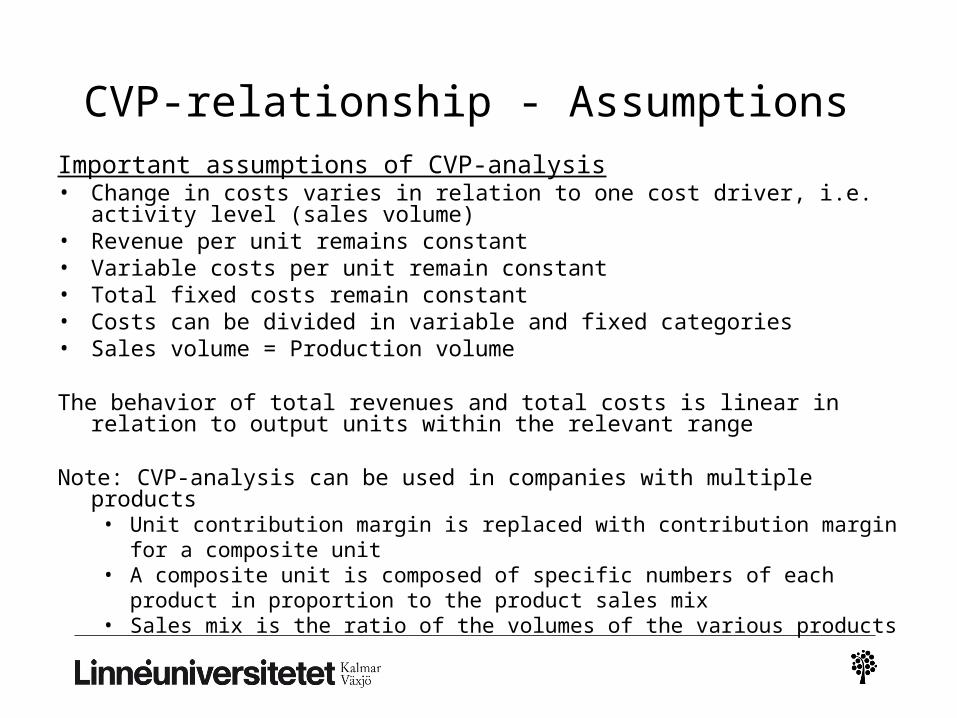

CVP-relationship - AssumptionsImportant assumptions of CVP-analysis• Change in costs varies in relation to one cost driver, i.e. activity level (sales

volume) • Revenue per unit remains constant• Variable costs per unit remain constant• Total fixed costs remain constant• Costs can be divided in variable and fixed categories• Sales volume = Production volume

The behavior of total revenues and total costs is linear in relation to output units within the relevant range

Note: CVP-analysis can be used in companies with multiple products• Unit contribution margin is replaced with contribution margin for a composite unit• A composite unit is composed of specific numbers of each product in proportion to

the product sales mix• Sales mix is the ratio of the volumes of the various products

Cost volume profit analysis – Example

A company has recently developed a new product. The new product is a book about management accounting and it will revolutionize the area. It contains new terms and concepts. The company is particularly interested in adopting the cost volume profit approach to decision-making. The accountant at the company has prepared the following information about price, costs and volume for one year:

Price per unit $40Variable cost per unit $20Fixed costs $600 000Sales volume 40 000 units

Cost volume profit analysis – Example

• What will the operating profit be if 40 000 units are sold?

• What will the operating profit be if the company spends an additional $100 000 on a marketing campaign. They assume that the campaign will increase the sales volume with 10 000 units.

• If the company desire a profit of $300 000, how many units would have to be sold?

• Determine the annual break-even point in units.

• Suppose that the variable cost increases by 10 %. Compute the new break-even point.

• Determine the margin of safety in units at a sales volume of 40 000 units.

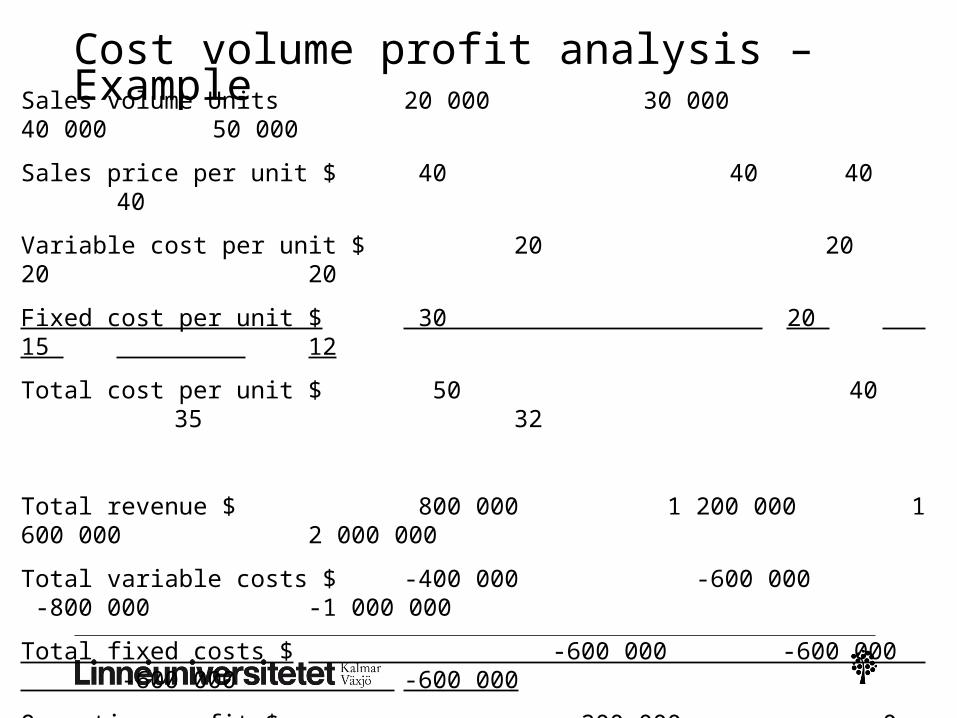

Cost volume profit analysis – Example Sales volume Units 20 000 30 000 40 000 50 000

Sales price per unit $ 40 40 40 40

Variable cost per unit $ 20 20 20 20

Fixed cost per unit $ 30 20 15 12

Total cost per unit $ 50 40 35 32

Total revenue $ 800 000 1 200 000 1 600 000 2 000 000

Total variable costs $ -400 000 -600 000 -800 000 -1 000 000

Total fixed costs $ -600 000 -600 000 -600 000 -600 000

Operating profit $ -200 000 0 200 000 400 000

(Total costs 1 000 000 1 200 000 1 400 000 1 600 000)

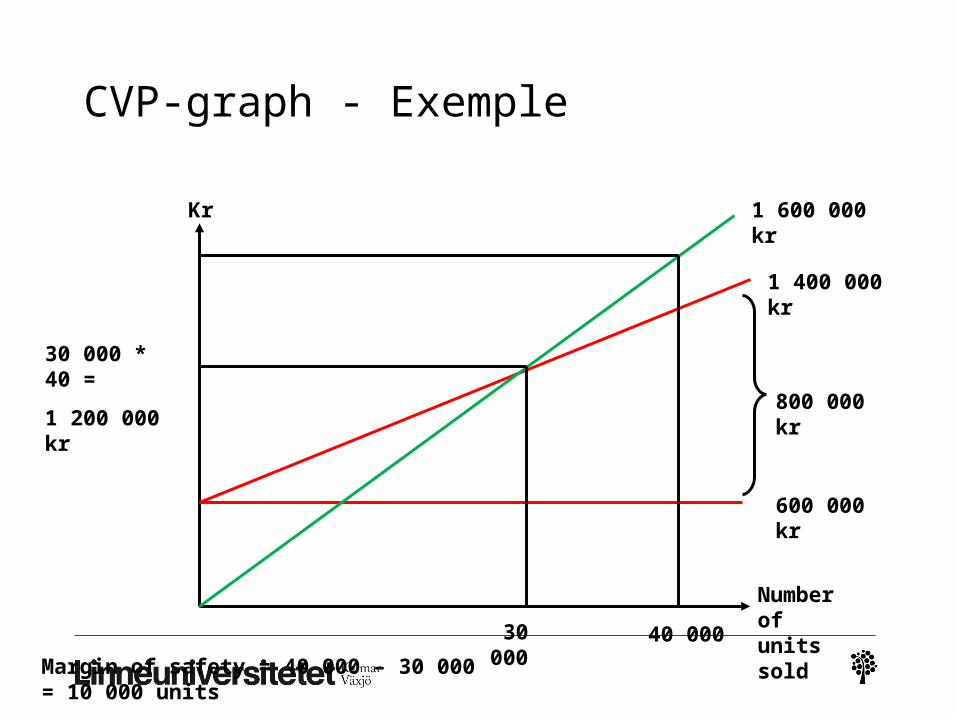

CVP-graph - Exemple

Kr

Number of units sold

600 000 kr

800 000 kr

1 400 000 kr

1 600 000 kr

30 000

30 000 * 40 =

1 200 000 kr

40 000 Margin of safety = 40 000 – 30 000 = 10 000 units

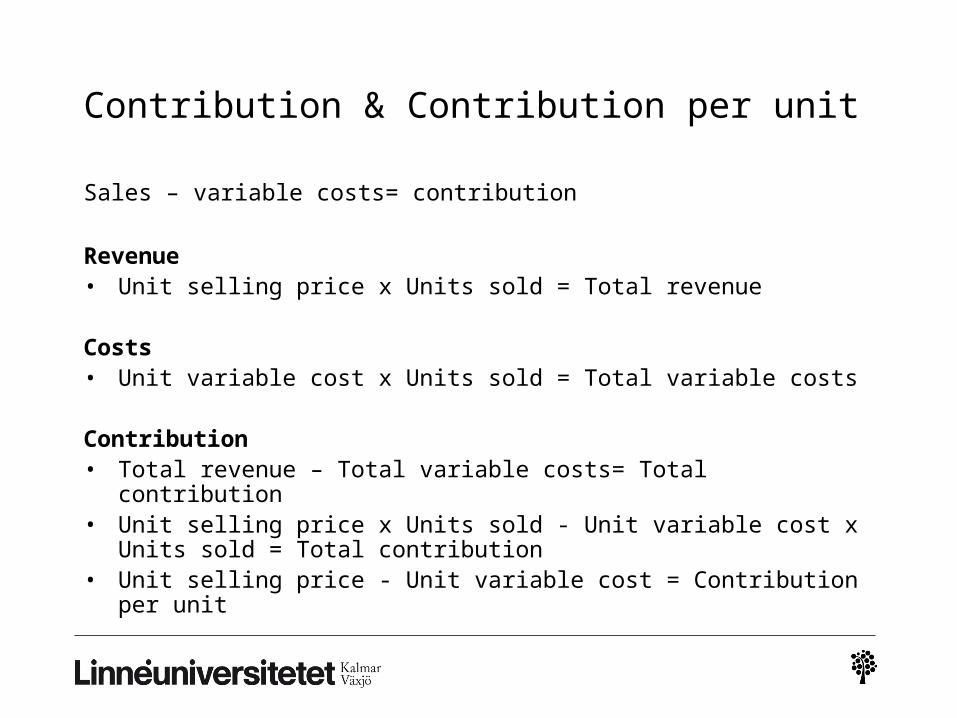

Contribution & Contribution per unit

Sales – variable costs= contribution

Revenue• Unit selling price x Units sold = Total revenue

Costs• Unit variable cost x Units sold = Total variable costs

Contribution• Total revenue – Total variable costs= Total contribution• Unit selling price x Units sold - Unit variable cost x Units

sold = Total contribution• Unit selling price - Unit variable cost = Contribution per unit

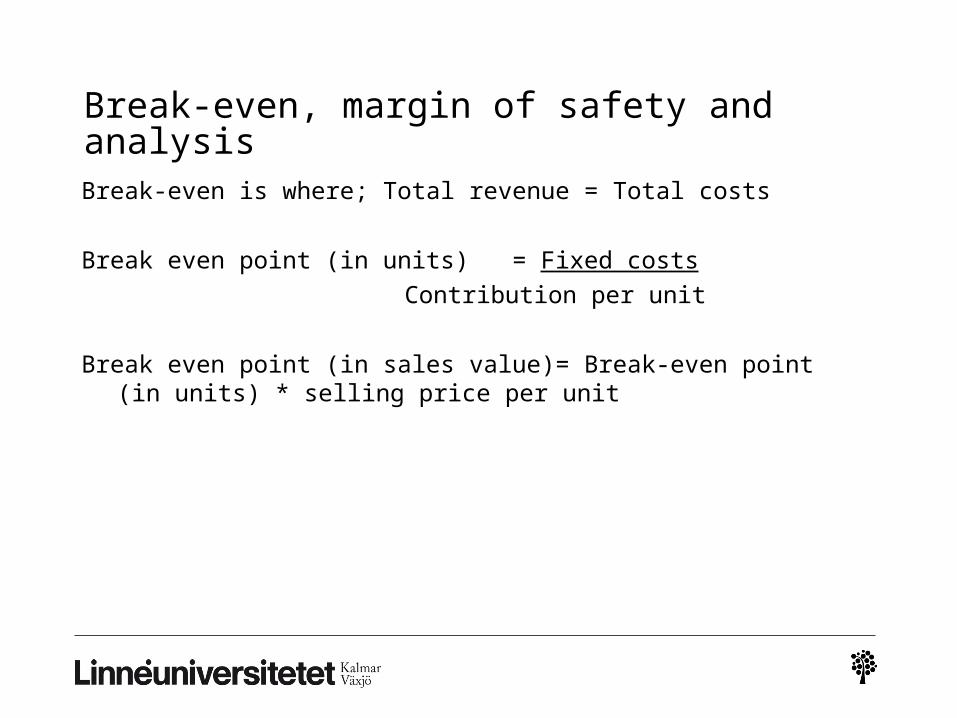

Break-even, margin of safety and analysis

Break-even is where; Total revenue = Total costs

Break even point (in units) = Fixed costs

Contribution per unit

Break even point (in sales value)= Break-even point (in units) * selling price per unit

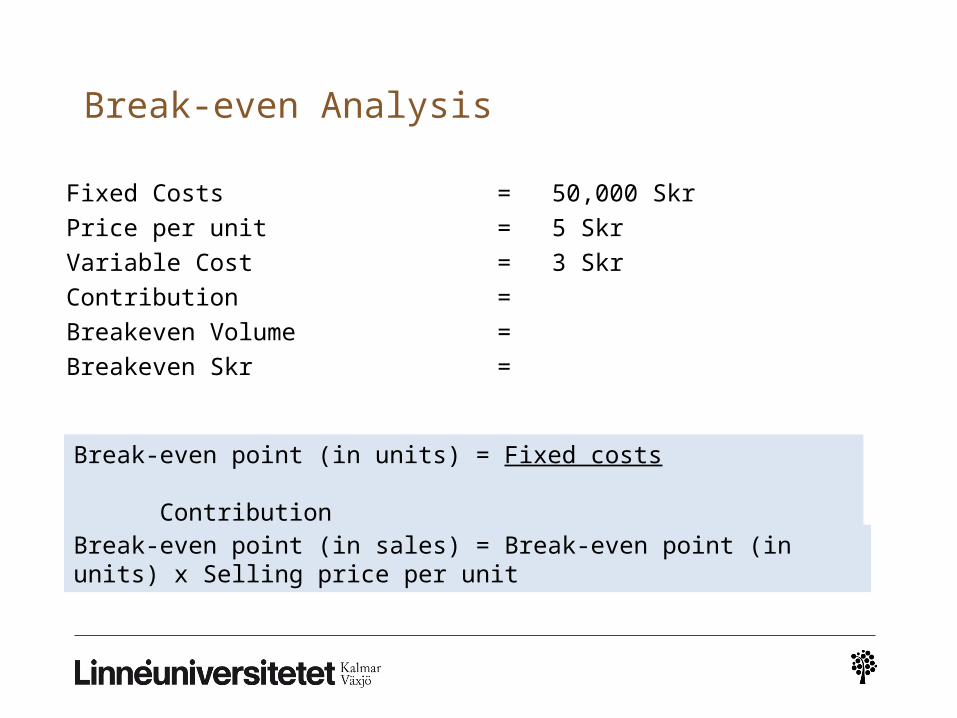

Break-even Analysis

Fixed Costs = 50,000 Skr

Price per unit = 5 Skr

Variable Cost = 3 Skr

Contribution =

Breakeven Volume =

Breakeven Skr =

Break-even point (in units) = Fixed costs Contribution

Break-even point (in sales) = Break-even point (in units) x Selling price per unit

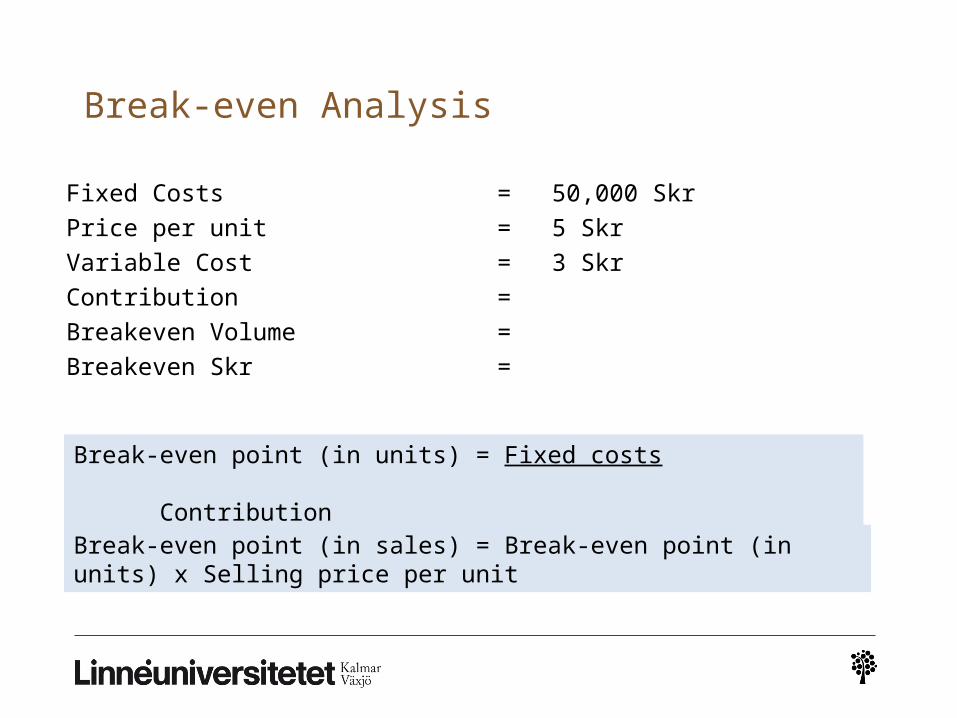

Break-even Analysis

Fixed Costs = 50,000 Skr

Price per unit = 5 Skr

Variable Cost = 3 Skr

Contribution =

Breakeven Volume =

Breakeven Skr =

Break-even point (in units) = Fixed costs Contribution

Break-even point (in sales) = Break-even point (in units) x Selling price per unit

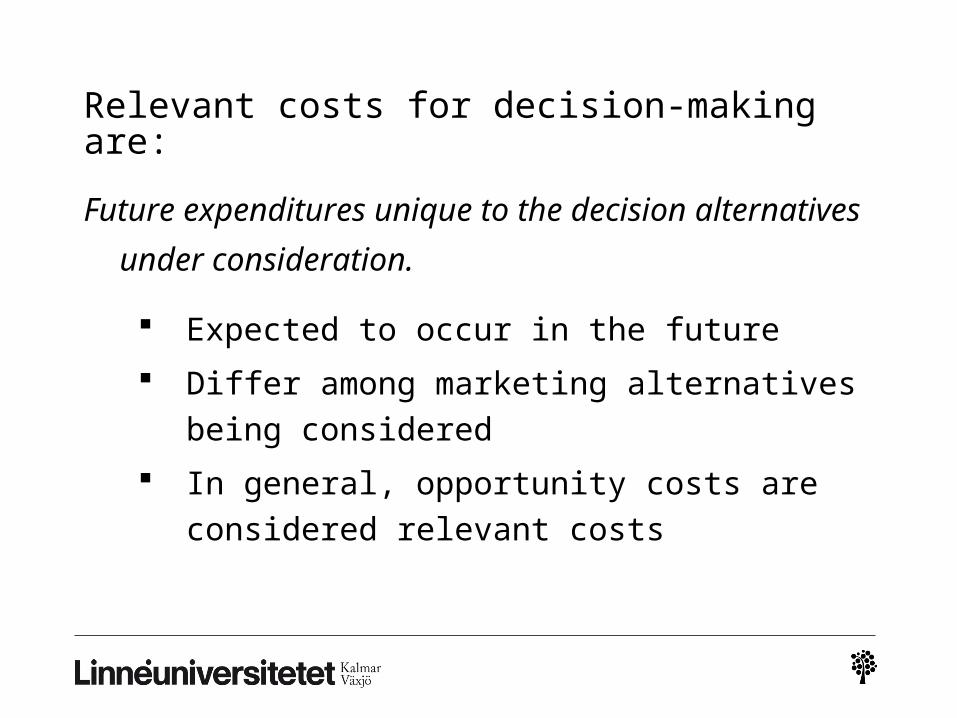

Relevant costs for decision-making are:

Future expenditures unique to the decision alternatives under

consideration.

Expected to occur in the future

Differ among marketing alternatives being considered

In general, opportunity costs are considered relevant

costs

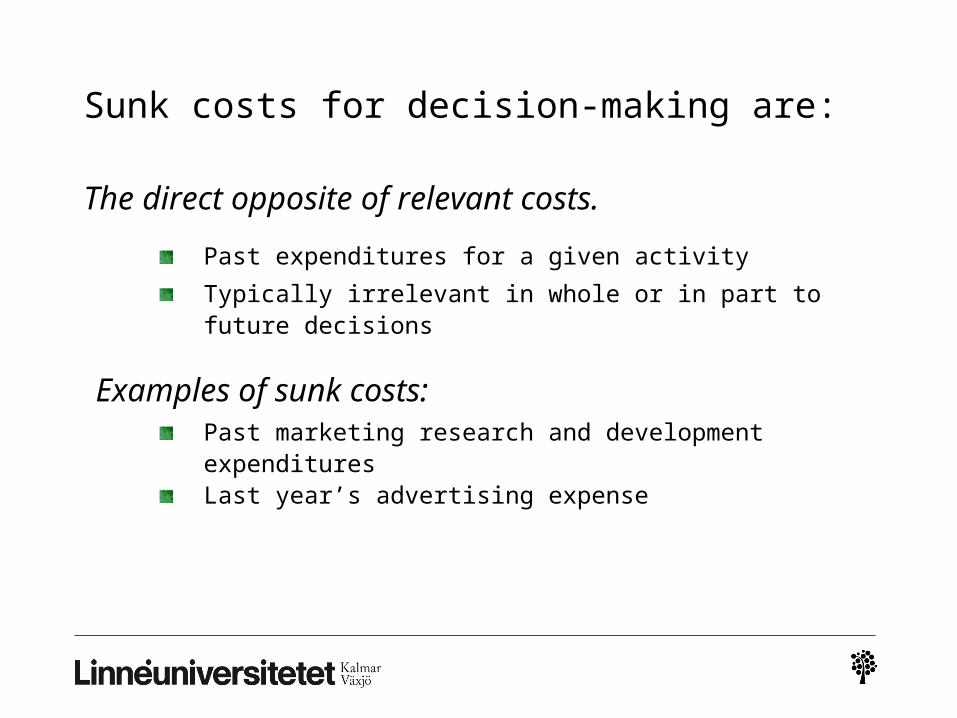

Sunk costs for decision-making are:

The direct opposite of relevant costs.

Past expenditures for a given activity

Typically irrelevant in whole or in part to future decisions

Examples of sunk costs:Past marketing research and development expendituresLast year’s advertising expense

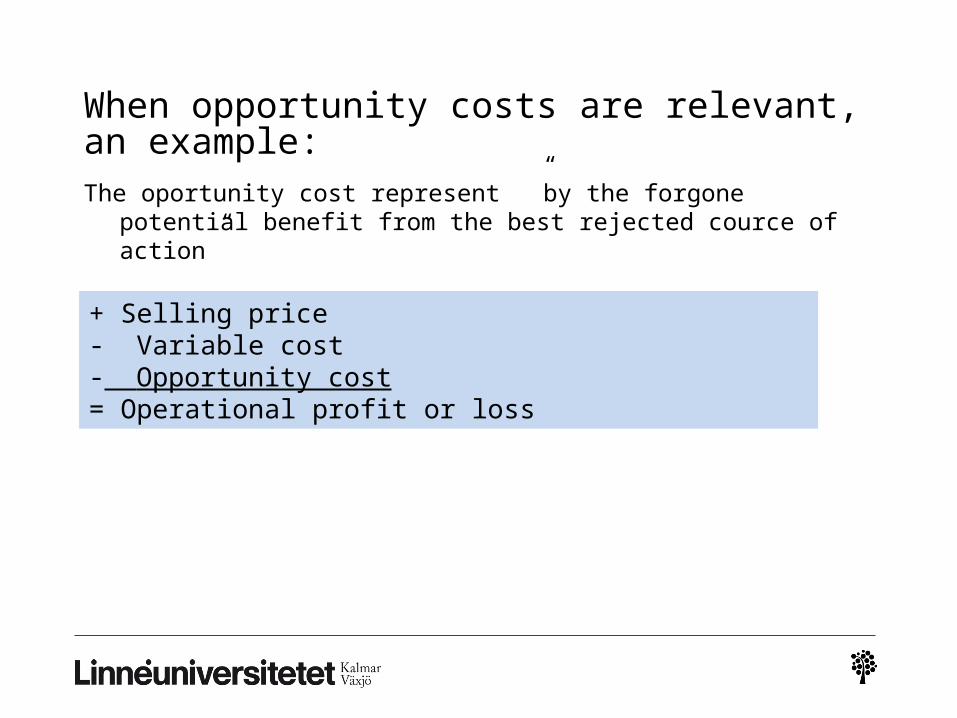

When opportunity costs are relevant, an example:

The oportunity cost represent ”by the forgone potential benefit from the best rejected cource of action”

Sid 178

+ Selling price- Variable cost- Opportunity cost= Operational profit or loss

Limiting factors

Avalable capacity

Limited capacity

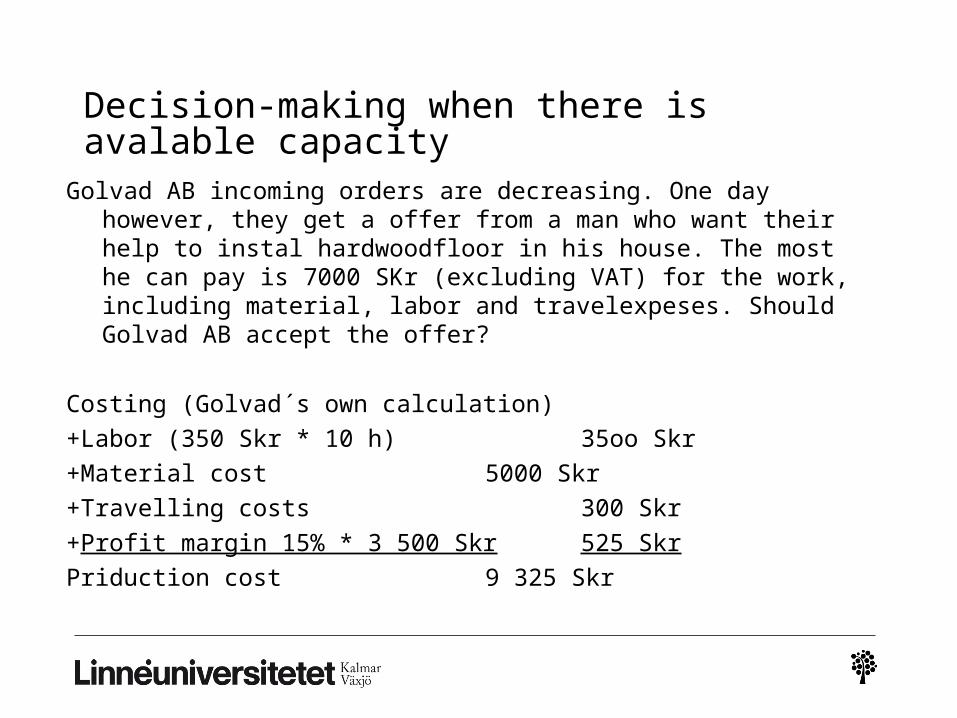

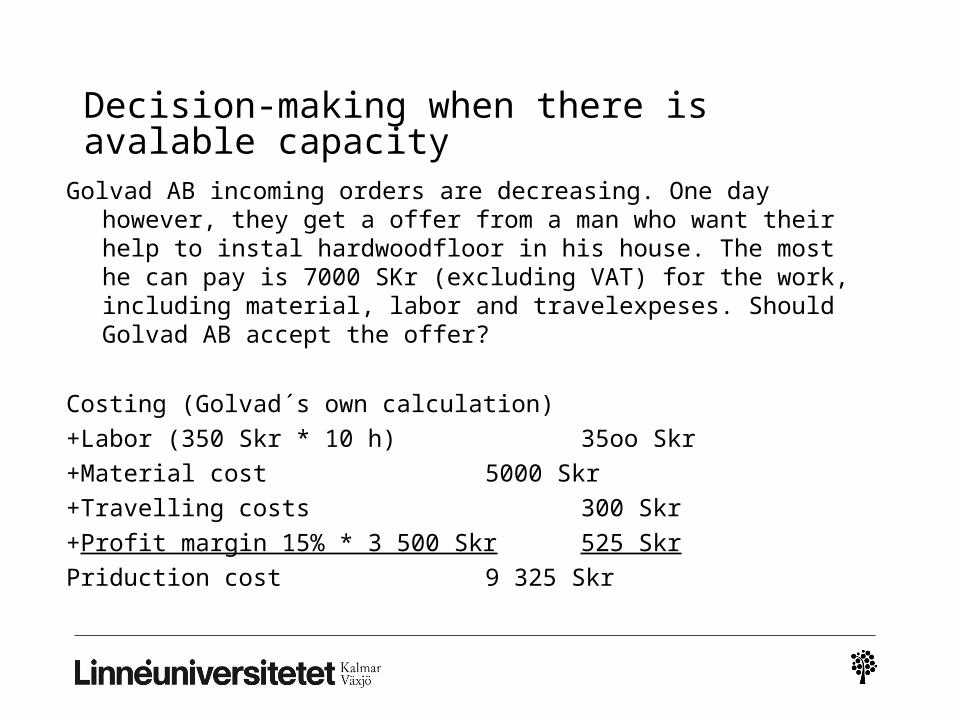

Decision-making when there is avalable capacity

Golvad AB incoming orders are decreasing. One day however, they get a offer from a man who want their help to instal hardwoodfloor in his house. The most he can pay is 7000 SKr (excluding VAT) for the work, including material, labor and travelexpeses. Should Golvad AB accept the offer?

Costing (Golvad´s own calculation)

+Labor (350 Skr * 10 h) 35oo Skr

+Material cost 5000 Skr

+Travelling costs 300 Skr

+Profit margin 15% * 3 500 Skr 525 Skr

Priduction cost 9 325 Skr

Decision-making when there is avalable capacity

Golvad AB incoming orders are decreasing. One day however, they get a offer from a man who want their help to instal hardwoodfloor in his house. The most he can pay is 7000 SKr (excluding VAT) for the work, including material, labor and travelexpeses. Should Golvad AB accept the offer?

Costing (Golvad´s own calculation)

+Labor (350 Skr * 10 h) 35oo Skr

+Material cost 5000 Skr

+Travelling costs 300 Skr

+Profit margin 15% * 3 500 Skr 525 Skr

Priduction cost 9 325 Skr

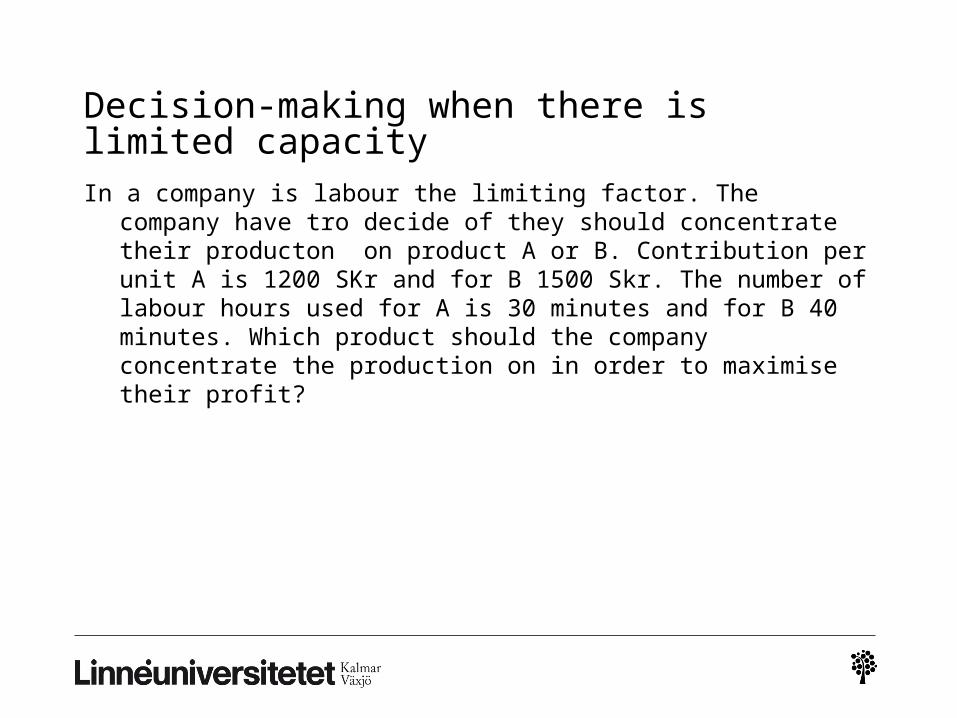

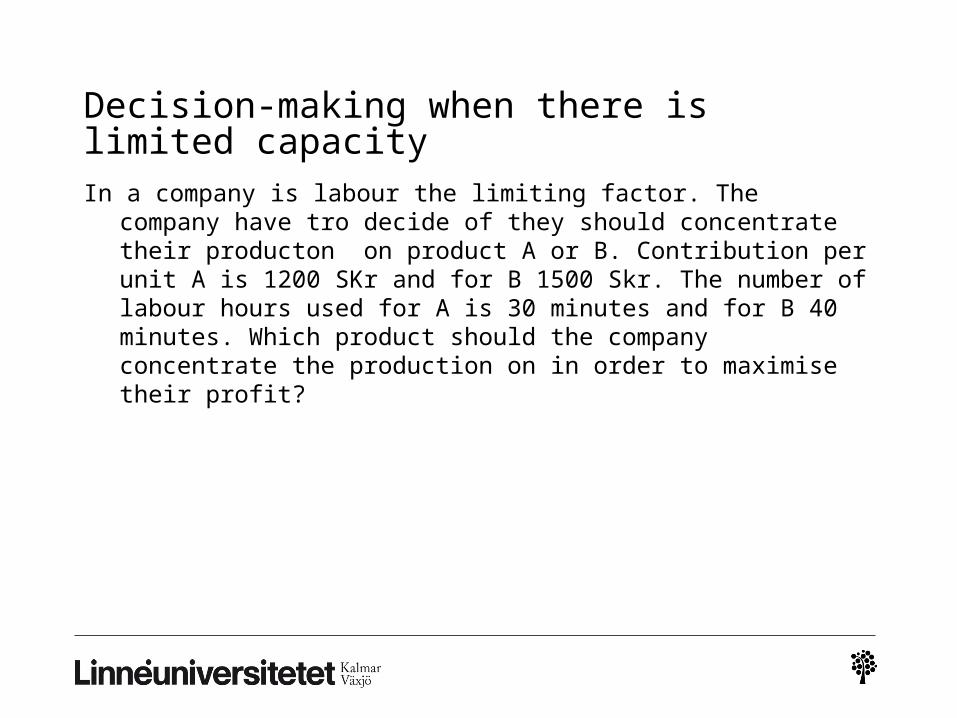

Decision-making when there is limited capacity

In a company is labour the limiting factor. The company have tro decide of they should concentrate their producton on product A or B. Contribution per unit A is 1200 SKr and for B 1500 Skr. The number of labour hours used for A is 30 minutes and for B 40 minutes. Which product should the company concentrate the production on in order to maximise their profit?

Decision-making when there is limited capacity

In a company is labour the limiting factor. The company have tro decide of they should concentrate their producton on product A or B. Contribution per unit A is 1200 SKr and for B 1500 Skr. The number of labour hours used for A is 30 minutes and for B 40 minutes. Which product should the company concentrate the production on in order to maximise their profit?

Decision-making when there is limited capacity

In a company is labour the limiting factor. The company have tro decide of they should concentrate their producton on product A or B. Contribution per unit A is 1200 SKr and for B 1500 Skr. The number of labour hours used for A is 30 minutes and for B 40 minutes. Which product should the company concentrate the production on in order to maximise their profit?

Product A Product B

The company should choose to procuce A. The contribution comes out ahead because it produces the highes contribution per scarce labour resourses.

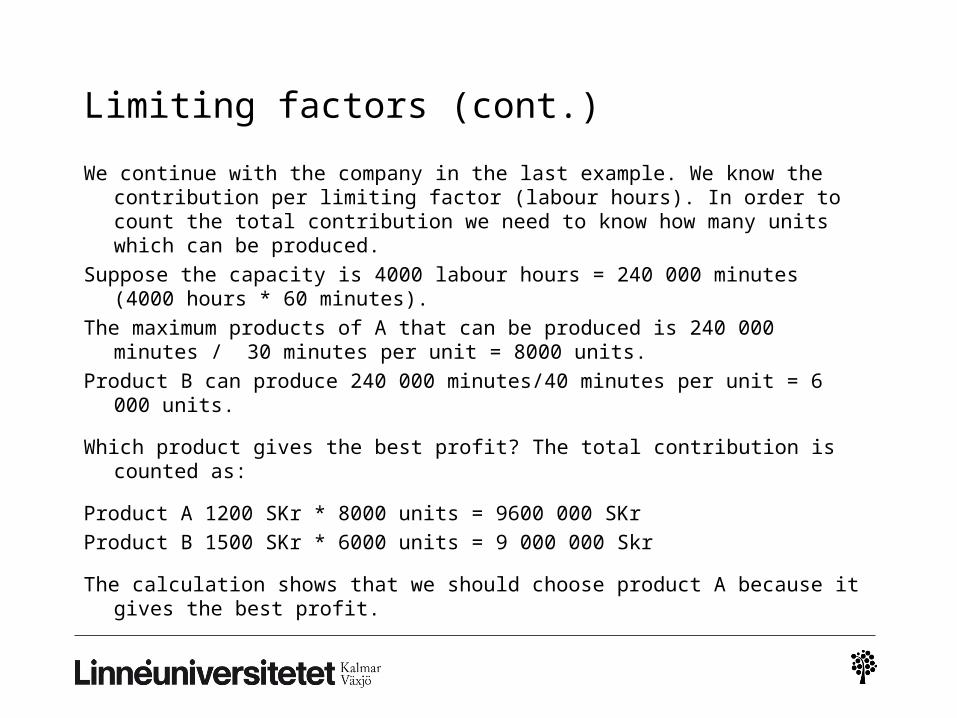

Limiting factors (cont.)

We continue with the company in the last example. We know the contribution per limiting factor (labour hours). In order to count the total contribution we need to know how many units which can be produced.

Suppose the capacity is 4000 labour hours = 240 000 minutes (4000 hours * 60 minutes).

The maximum products of A that can be produced is 240 000 minutes / 30 minutes per unit = 8000 units.

Product B can produce 240 000 minutes/40 minutes per unit = 6 000 units.

Which product gives the best profit? The total contribution is counted as:

Product A 1200 SKr * 8000 units = 9600 000 SKr

Product B 1500 SKr * 6000 units = 9 000 000 Skr

The calculation shows that we should choose product A because it gives the best profit.