INTRODUCTION TO CORPORATE FINANCE Laurence Booth W. Sean Cleary Chapter 2 – Business (Corporate)...

44

INTRODUCTION TO INTRODUCTION TO CORPORATE FINANCE CORPORATE FINANCE Laurence Booth Laurence Booth • • W. Sean W. Sean Cleary Cleary Chapter 2 – Business Chapter 2 – Business (Corporate) Finance (Corporate) Finance Prepared by Prepared by Ken Hartviksen Ken Hartviksen

-

date post

18-Dec-2015 -

Category

Documents

-

view

264 -

download

9

Transcript of INTRODUCTION TO CORPORATE FINANCE Laurence Booth W. Sean Cleary Chapter 2 – Business (Corporate)...

INTRODUCTION TOINTRODUCTION TO CORPORATE FINANCECORPORATE FINANCELaurence Booth Laurence Booth •• W. Sean Cleary W. Sean Cleary

Chapter 2 – Business (Corporate) FinanceChapter 2 – Business (Corporate) Finance

Prepared byPrepared by

Ken HartviksenKen Hartviksen

CHAPTER 2CHAPTER 2 Business (Corporate) Business (Corporate)

FinanceFinance

CHAPTER 2 – Business (Corporate) Finance 2 - 3

Lecture AgendaLecture Agenda

• Learning ObjectivesLearning Objectives• Important TermsImportant Terms• Types of Business OrganizationsTypes of Business Organizations• Goals of the CorporationGoals of the Corporation• Role of Management and Agency IssuesRole of Management and Agency Issues• Corporate FinanceCorporate Finance• Finance Careers Finance Careers • Organization of the Finance FunctionOrganization of the Finance Function• Sample ProblemsSample Problems

CHAPTER 2 – Business (Corporate) Finance 2 - 4

Learning ObjectivesLearning Objectives

1.1. The advantages of disadvantages of four different ways to The advantages of disadvantages of four different ways to organize a businessorganize a business

2.2. Some of the pressures exerted on corporations by various Some of the pressures exerted on corporations by various stakeholdersstakeholders

3.3. What the ultimate objective of a firm is and why this is a What the ultimate objective of a firm is and why this is a logical objectivelogical objective

4.4. Why agency costs arise and how they can reduce Why agency costs arise and how they can reduce shareholder wealthshareholder wealth

5.5. The main types of decisions made by corporations The main types of decisions made by corporations regarding the financial management of their real and regarding the financial management of their real and financial assets, as well as the associated corporate financial assets, as well as the associated corporate financing decisionsfinancing decisions

6.6. Some of the major types of finance jobs available with Some of the major types of finance jobs available with financial and non-financial companiesfinancial and non-financial companies

CHAPTER 2 – Business (Corporate) Finance 2 - 5

Important Chapter TermsImportant Chapter Terms

• Account managersAccount managers• Agency costsAgency costs• Agency problemsAgency problems• Agency relationshipsAgency relationships• AnalystsAnalysts• AssociatesAssociates• Banking associatesBanking associates• Capital budgetingCapital budgeting• Chief financial officerChief financial officer• ControllerController• Corporate financeCorporate finance• Corporate finance associatesCorporate finance associates• Corporate financingCorporate financing• CorporationsCorporations• Financial and investment Financial and investment

analystsanalysts

• Financial managementFinancial management• Fixed income or equity tradersFixed income or equity traders• Income and royalty trustsIncome and royalty trusts• Limited liabilityLimited liability• ManagersManagers• PartnershipPartnership• Portfolio managersPortfolio managers• Private bankersPrivate bankers• Retail brokersRetail brokers• Sales and trading peopleSales and trading people• Security analystsSecurity analysts• Senior vice-president of financeSenior vice-president of finance• Sole proprietorshipSole proprietorship• TreasurerTreasurer• TrustTrust• Unlimited liabilityUnlimited liability

CHAPTER 2 – Business (Corporate) Finance 2 - 6

Types of Business OrganizationsTypes of Business Organizations

• Sole proprietorshipsSole proprietorships• PartnershipsPartnerships• TrustsTrusts• CorporationsCorporations

CHAPTER 2 – Business (Corporate) Finance 2 - 7

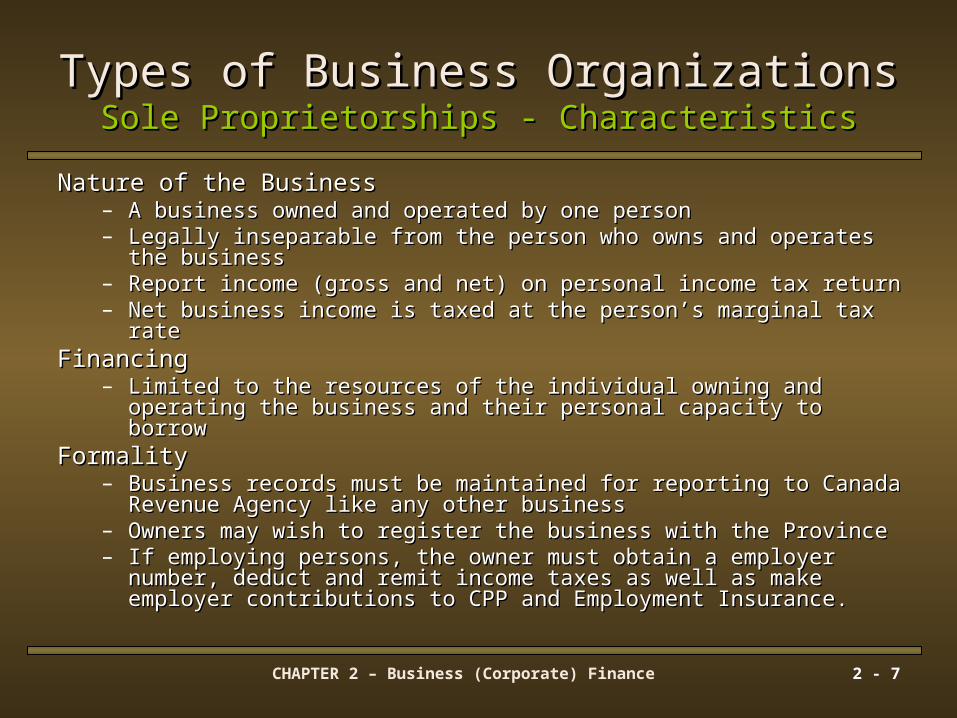

Types of Business OrganizationsTypes of Business OrganizationsSole Proprietorships - CharacteristicsSole Proprietorships - Characteristics

Nature of the BusinessNature of the Business– A business owned and operated by one personA business owned and operated by one person– Legally inseparable from the person who owns and operates the Legally inseparable from the person who owns and operates the

businessbusiness– Report income (gross and net) on personal income tax returnReport income (gross and net) on personal income tax return– Net business income is taxed at the person’s marginal tax rateNet business income is taxed at the person’s marginal tax rate

FinancingFinancing– Limited to the resources of the individual owning and operating the Limited to the resources of the individual owning and operating the

business and their personal capacity to borrowbusiness and their personal capacity to borrowFormalityFormality

– Business records must be maintained for reporting to Canada Revenue Business records must be maintained for reporting to Canada Revenue Agency like any other businessAgency like any other business

– Owners may wish to register the business with the ProvinceOwners may wish to register the business with the Province– If employing persons, the owner must obtain a employer number, If employing persons, the owner must obtain a employer number,

deduct and remit income taxes as well as make employer contributions deduct and remit income taxes as well as make employer contributions to CPP and Employment Insurance.to CPP and Employment Insurance.

CHAPTER 2 – Business (Corporate) Finance 2 - 8

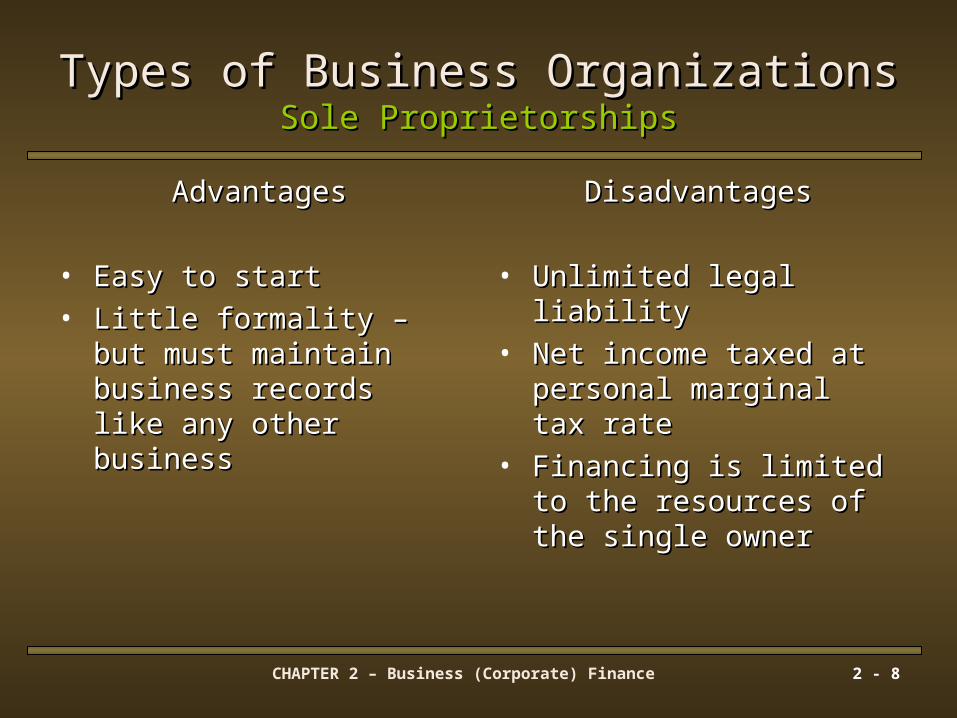

Types of Business OrganizationsTypes of Business OrganizationsSole ProprietorshipsSole Proprietorships

AdvantagesAdvantages

• Easy to startEasy to start• Little formality – but Little formality – but

must maintain business must maintain business records like any other records like any other businessbusiness

DisadvantagesDisadvantages

• Unlimited legal liabilityUnlimited legal liability• Net income taxed at Net income taxed at

personal marginal tax personal marginal tax raterate

• Financing is limited to Financing is limited to the resources of the the resources of the single ownersingle owner

CHAPTER 2 – Business (Corporate) Finance 2 - 9

Types of Business OrganizationsTypes of Business OrganizationsPartnership CharacteristicsPartnership Characteristics

Nature of the BusinessNature of the Business– Involves two or more partnersInvolves two or more partners– Must have at least one general partner who holds unlimited legal Must have at least one general partner who holds unlimited legal

liability for the activities of the business liability for the activities of the business

FinancingFinancing– A function of the combined resources of the partnersA function of the combined resources of the partners– Can attract additional resources through limited partner Can attract additional resources through limited partner

contributionscontributions

FormalityFormality– Must be registered under provincial partnership legislationMust be registered under provincial partnership legislation– Should be formalized through a partnership agreementShould be formalized through a partnership agreement outlining outlining

partner responsibilities, how partners enter and cash out of the partner responsibilities, how partners enter and cash out of the business, and division of net business incomebusiness, and division of net business income

CHAPTER 2 – Business (Corporate) Finance 2 - 10

Types of Business OrganizationsTypes of Business OrganizationsLimited Liability Partnerships (LLP)Limited Liability Partnerships (LLP)

• New form of organization for professional New form of organization for professional firmsfirms

• Partners have limited legal liability Partners have limited legal liability • Partner’s income included as ordinary income Partner’s income included as ordinary income

and filed using an individual tax return.and filed using an individual tax return.• This form of business organization is used by This form of business organization is used by

Canadian legal and accounting firmsCanadian legal and accounting firms

CHAPTER 2 – Business (Corporate) Finance 2 - 11

Types of Business OrganizationsTypes of Business OrganizationsExamples of LLPs in CanadaExamples of LLPs in Canada

Law Firms Employees Lawyers PartnersMcCarthy Tetrault LLP 1,250 712 379Gowling Lafleur Henderson LLP 1,181 698 353Borden Ladner Gervais LLP 1,290 679 395Fasken Martineau DuMoulin LLP 936 583 348

Accounting Firms

Sales ($ million)

Partners Professional Staff

Deloitte & Touche LLP 1,024 512 4,603KPMG LLP 729 433 3,163PricewaterhouseCoopers LLP 698 430 2,640Ernst & Young LLP 556 266 2,081Grant Thornton LLP 315 349 2,166

Source: Financial P ost , FP 500, 2004.

Table 2-1 Canadian Law and Accounting Firms, 2004

CHAPTER 2 – Business (Corporate) Finance 2 - 12

Types of Business OrganizationsTypes of Business OrganizationsLimited and General PartnershipsLimited and General Partnerships

Used for tax purposesUsed for tax purposes– Limited partners are often able to use unused non-cash Limited partners are often able to use unused non-cash

deductions such as ‘depreciation’ and/or business losses to deductions such as ‘depreciation’ and/or business losses to offset personal tax liabilities.offset personal tax liabilities.

General PartnerGeneral Partner– There must be one general partner (responsible for operating There must be one general partner (responsible for operating

the business)the business)– Unlimited legal liabilityUnlimited legal liability– Often the general partner is a corporationOften the general partner is a corporation

Limited PartnersLimited Partners– Passive investorsPassive investors– Contribute money only to the business, and share in the profits Contribute money only to the business, and share in the profits

CHAPTER 2 – Business (Corporate) Finance 2 - 13

Types of Business OrganizationsTypes of Business OrganizationsGeneral PartnershipsGeneral Partnerships

AdvantagesAdvantages

• Harnesses the combined Harnesses the combined talents and energies of all the talents and energies of all the partnerspartners

• Potentially taps the greater Potentially taps the greater combined financial resources combined financial resources of the partnersof the partners

• Spreads liability across the Spreads liability across the partners (jointly and partners (jointly and severally)severally)

DisadvantagesDisadvantages

• Income is taxed at the Income is taxed at the individual’s marginal tax rateindividual’s marginal tax rate

• Governed by provincial Governed by provincial partnership legislation – so partnership legislation – so some formality does exist – some formality does exist – and probably should exist and probably should exist through a formal partnership through a formal partnership agreementagreement

• Unlimited legal liabilityUnlimited legal liability• Under law, non-partnership Under law, non-partnership

business arrangements can business arrangements can be deemed a partnership be deemed a partnership under the lawunder the law

• It can be legally challenging It can be legally challenging to disassociate ones’ self from to disassociate ones’ self from and/or dissolve a partnership and/or dissolve a partnership arrangementarrangement

CHAPTER 2 – Business (Corporate) Finance 2 - 14

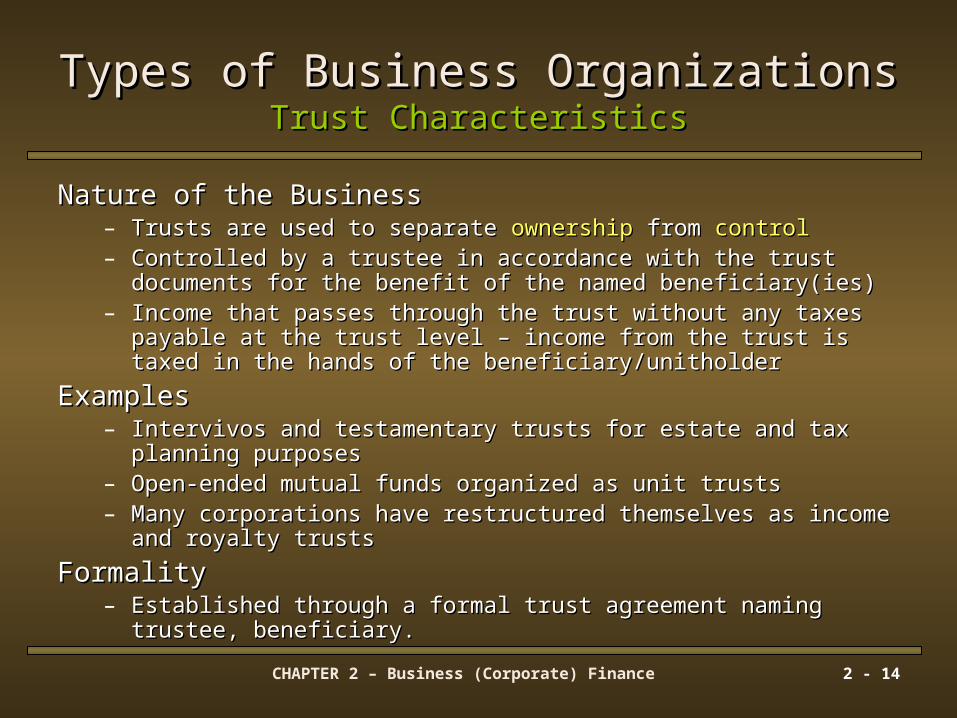

Types of Business OrganizationsTypes of Business OrganizationsTrust CharacteristicsTrust Characteristics

Nature of the BusinessNature of the Business– Trusts are used to separate Trusts are used to separate ownershipownership from from controlcontrol– Controlled by a trustee in accordance with the trust documents for the Controlled by a trustee in accordance with the trust documents for the

benefit of the named beneficiary(ies)benefit of the named beneficiary(ies)– Income that passes through the trust without any taxes payable at the Income that passes through the trust without any taxes payable at the

trust level – income from the trust is taxed in the hands of the trust level – income from the trust is taxed in the hands of the beneficiary/unitholderbeneficiary/unitholder

ExamplesExamples– Intervivos and testamentary trusts for estate and tax planning purposesIntervivos and testamentary trusts for estate and tax planning purposes– Open-ended mutual funds organized as unit trustsOpen-ended mutual funds organized as unit trusts– Many corporations have restructured themselves as income and royalty Many corporations have restructured themselves as income and royalty

truststrusts

FormalityFormality– Established through a formal trust agreement naming trustee, Established through a formal trust agreement naming trustee,

beneficiary.beneficiary.

CHAPTER 2 – Business (Corporate) Finance 2 - 15

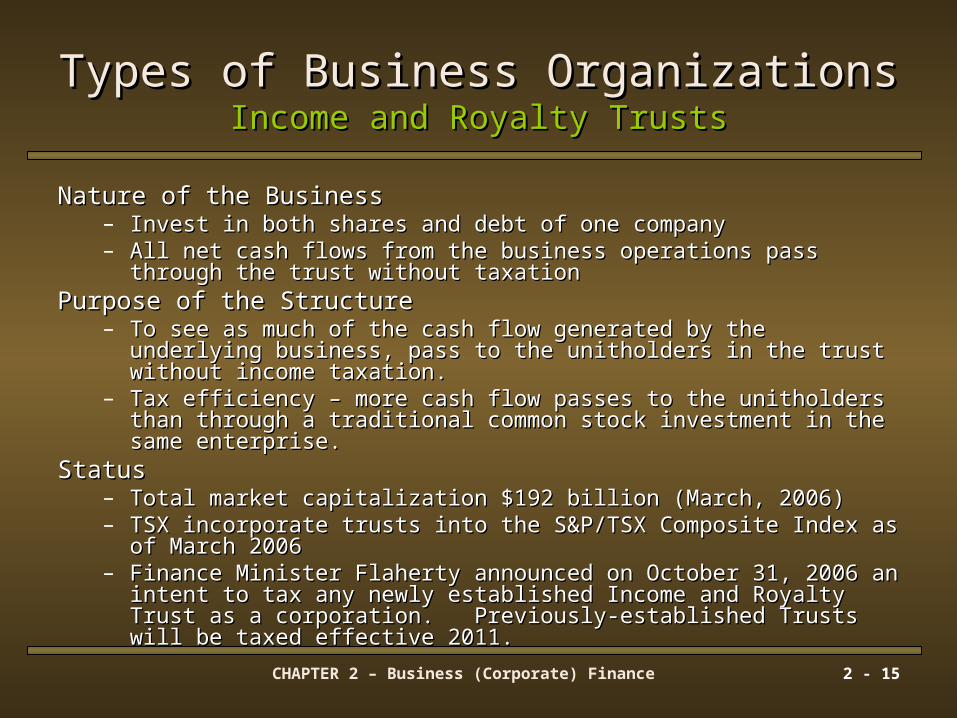

Types of Business OrganizationsTypes of Business OrganizationsIncome and Royalty TrustsIncome and Royalty Trusts

Nature of the BusinessNature of the Business– Invest in both shares and debt of one companyInvest in both shares and debt of one company– All net cash flows from the business operations pass through the trust All net cash flows from the business operations pass through the trust

without taxationwithout taxationPurpose of the StructurePurpose of the Structure

– To see as much of the cash flow generated by the underlying business, To see as much of the cash flow generated by the underlying business, pass to the unitholders in the trust without income taxation.pass to the unitholders in the trust without income taxation.

– Tax efficiency – more cash flow passes to the unitholders than through Tax efficiency – more cash flow passes to the unitholders than through a traditional common stock investment in the same enterprise.a traditional common stock investment in the same enterprise.

StatusStatus– Total market capitalization $192 billion (March, 2006)Total market capitalization $192 billion (March, 2006)– TSX incorporate trusts into the S&P/TSX Composite Index as of March TSX incorporate trusts into the S&P/TSX Composite Index as of March

20062006– Finance Minister Flaherty announced on October 31, 2006 an intent to Finance Minister Flaherty announced on October 31, 2006 an intent to

tax any newly established Income and Royalty Trust as a corporation. tax any newly established Income and Royalty Trust as a corporation. Previously-established Trusts will be taxed effective 2011.Previously-established Trusts will be taxed effective 2011.

CHAPTER 2 – Business (Corporate) Finance 2 - 16

Types of Business OrganizationsTypes of Business OrganizationsTrustsTrusts

AdvantagesAdvantages

• No taxation of funds No taxation of funds flowing through the trustflowing through the trust

• Separates ownership Separates ownership and controland control

DisadvantagesDisadvantages

• Governance structure Governance structure may only be appropriate may only be appropriate for well established firms for well established firms with little further capital with little further capital investment needsinvestment needs

CHAPTER 2 – Business (Corporate) Finance 2 - 17

Types of Business OrganizationsTypes of Business OrganizationsCorporation CharacteristicsCorporation Characteristics

Nature of the BusinessNature of the Business– A separate legal entity (person) under the law A separate legal entity (person) under the law

• Incorporated either federally or provinciallyIncorporated either federally or provincially– Governed by the Board of Directors, managed by professional Governed by the Board of Directors, managed by professional

managers and owned by shareholdersmanagers and owned by shareholders

FinancingFinancing– Highly flexible and long term including issuing stocks, bonds and Highly flexible and long term including issuing stocks, bonds and

other hybrid securities to raise capital for research and other hybrid securities to raise capital for research and development and overall corporate growthdevelopment and overall corporate growth

FormalityFormality– Articles of Incorporation, bylaws, practices are governed by Articles of Incorporation, bylaws, practices are governed by

corporate and securities lawcorporate and securities law

CHAPTER 2 – Business (Corporate) Finance 2 - 18

Types of Business OrganizationsTypes of Business OrganizationsCorporationsCorporations

AdvantagesAdvantages

• Immortal – issue securities Immortal – issue securities with very long terms to with very long terms to maturitymaturity

• Potential to attract great Potential to attract great amounts of financing by amounts of financing by expanding the base of expanding the base of shareholdersshareholders

• Potential to attract and use Potential to attract and use expertise of its board of expertise of its board of directorsdirectors

• Potential to hire Potential to hire professional managers to professional managers to build valuebuild value

DisadvantagesDisadvantages

• Formality and structure Formality and structure may slow the speed of may slow the speed of response of the response of the organizationorganization

• Corporate taxation means Corporate taxation means that shareholder income that shareholder income (dividends) are paid out (dividends) are paid out after-tax and then are after-tax and then are taxed in the hands of taxed in the hands of shareholders when shareholders when received.received.

CHAPTER 2 – Business (Corporate) Finance 2 - 19

Governance of the CorporationGovernance of the CorporationCorporationsCorporations

• Shareholders are the owners of the corporationShareholders are the owners of the corporation– Residual claims to profits and assetsResidual claims to profits and assets

– Rights to vote to:Rights to vote to:• Elect the board of directorsElect the board of directors• Adopt the financial statementsAdopt the financial statements• Approve the auditors for the coming yearApprove the auditors for the coming year

• Board of Directors and Managers are Board of Directors and Managers are responsible for day-to-day operation of the responsible for day-to-day operation of the corporation in accordance with standards set corporation in accordance with standards set out in the corporations act.out in the corporations act.

CHAPTER 2 – Business (Corporate) Finance 2 - 20

Governance of the CorporationGovernance of the CorporationDirector and Officer ResponsibilitiesDirector and Officer Responsibilities

Canada Business Corporations Act (CBCA Canada Business Corporations Act (CBCA S122.1)S122.1)Every director and officer of a corporation in exercising Every director and officer of a corporation in exercising

their powers and discharging their duties shall:their powers and discharging their duties shall:a)a) Act honestly and in good faith with a view to the best Act honestly and in good faith with a view to the best

interests of the corporation, andinterests of the corporation, and

b)b) Exercise the care, diligence and skill that a reasonably Exercise the care, diligence and skill that a reasonably prudent person would exercise in comparable prudent person would exercise in comparable circumstances.circumstances.

CHAPTER 2 – Business (Corporate) Finance 2 - 21

Governance of the CorporationGovernance of the CorporationSeparation of Ownership and ManagementSeparation of Ownership and Management

• In the modern publicly-traded corporation, professional In the modern publicly-traded corporation, professional managers and directors manage the corporation; they are managers and directors manage the corporation; they are agents of the shareholders who are the principal ownersagents of the shareholders who are the principal owners

• It is possible for agents (management) to pursue their It is possible for agents (management) to pursue their own goals at the expense of the principal (shareholder).own goals at the expense of the principal (shareholder).

• The fact that owners (shareholders) have limited access The fact that owners (shareholders) have limited access to information about the company they own, and to information about the company they own, and managers and the board hold superior information, managers and the board hold superior information, creates further potential for conflict.creates further potential for conflict.

• Corporate law anticipates the potential for principal/agent Corporate law anticipates the potential for principal/agent conflict and imposes responsibilities and reporting conflict and imposes responsibilities and reporting controls on management to reduce the probability of such controls on management to reduce the probability of such conflicts.conflicts.

CHAPTER 2 – Business (Corporate) Finance 2 - 22

Governance of the CorporationGovernance of the CorporationInformation AsymmetryInformation Asymmetry

The fact that owners (shareholders) have limited access to The fact that owners (shareholders) have limited access to information about the company they own, and managers information about the company they own, and managers and the board hold superior information, creates the and the board hold superior information, creates the potential for abuse of position by management.potential for abuse of position by management.

To reduce the potential for conflict arising out of To reduce the potential for conflict arising out of information asymmetry corporate and securities law information asymmetry corporate and securities law requires regular release of information about corporate requires regular release of information about corporate performance and the right to require approval from performance and the right to require approval from shareholders for major changes in the corporation shareholders for major changes in the corporation including:including:

• Annual shareholders meetings required by proper noticeAnnual shareholders meetings required by proper notice• Audited financial statementsAudited financial statements• Approval of auditors for the coming yearApproval of auditors for the coming year• Shareholder approval for changes to bylaws and articles of Shareholder approval for changes to bylaws and articles of

incorporation incorporation

CHAPTER 2 – Business (Corporate) Finance 2 - 23

The Goals of the CorporationThe Goals of the CorporationSeparation of Ownership and Management in the CorporationSeparation of Ownership and Management in the Corporation

Shareholders - PrincipalShareholders - Principal

Board of Directors

Chief Executive Officer

Chief Financial Officer

Vice President Operations

Vice President Marketing

The Board of Directors and Management are

Agents of the Shareholders

Shareholders Elect the Board

There is a separation between

ownership and management

CHAPTER 2 – Business (Corporate) Finance 2 - 24

The Goals of the CorporationThe Goals of the CorporationProfit MaximizationProfit Maximization

Profit maximization is an inadequate goal to Profit maximization is an inadequate goal to guide officers and directors of the guide officers and directors of the corporation.corporation.

– It fails to consider the risks undertaken by the firm in It fails to consider the risks undertaken by the firm in pursuit of profitpursuit of profit

– Its focus is on accounting profitIts focus is on accounting profit– Its focus is on one year’s accounting profit, Its focus is on one year’s accounting profit,

potentially at the expense of longer-term interests of potentially at the expense of longer-term interests of the shareholderthe shareholder

CHAPTER 2 – Business (Corporate) Finance 2 - 25

The Goals of the CorporationThe Goals of the CorporationPressures on ManagementPressures on Management

Professional managers of corporations face Professional managers of corporations face pressures and have responsibilities to many pressures and have responsibilities to many different ‘stakeholders’ different ‘stakeholders’

(See Figure 2-1 on the following slide.) (See Figure 2-1 on the following slide.)

CHAPTER 2 – Business (Corporate) Finance 2 - 26

The Goals of the CorporationThe Goals of the CorporationThe Firm As an Input-Output FunctionThe Firm As an Input-Output Function

FIGURE 2-2

MANAGERSMANAGERS

GOVERNMENTS

FREE GOODS

PRODUCT/ CONSUMERS

SOCIAL PRESSURESLABOUR

SUPPLIERS

CAPITAL

FREE GOODS

CHAPTER 2 – Business (Corporate) Finance 2 - 27

The Goals of the CorporationThe Goals of the CorporationShareholder Wealth MaximizationShareholder Wealth Maximization

Shareholder wealth maximization is Shareholder wealth maximization is considered the most appropriate goal to considered the most appropriate goal to guide officers and directors of the guide officers and directors of the corporation.corporation.

– Its focus is on genuine economic profitIts focus is on genuine economic profit– It reflects the value of all economic profits of the It reflects the value of all economic profits of the

corporation now and into the future.corporation now and into the future.

CHAPTER 2 – Business (Corporate) Finance 2 - 28

The Goals of the CorporationThe Goals of the CorporationShareholder Wealth Maximization and Negative ExternalitiesShareholder Wealth Maximization and Negative Externalities

Despite the attention given to major Despite the attention given to major corporations because of negative corporations because of negative externalities, the agents of the corporation externalities, the agents of the corporation must:must:– Operate legally and in compliance with contractual Operate legally and in compliance with contractual

responsibilities,responsibilities,– In the interests of its owners by creating value for In the interests of its owners by creating value for

them.them.

CHAPTER 2 – Business (Corporate) Finance 2 - 29

Role of Management and Agency IssuesRole of Management and Agency IssuesDefinitionsDefinitions

• Agency RelationshipAgency Relationship– Managers work on behalf of the shareholdersManagers work on behalf of the shareholders

• Agency ProblemsAgency Problems– Problems that arise due to potential divergence of Problems that arise due to potential divergence of

interest between managers, shareholders and interest between managers, shareholders and creditorscreditors

• Agency CostsAgency Costs– The costs associated with agency problemsThe costs associated with agency problems

CHAPTER 2 – Business (Corporate) Finance 2 - 30

Agency CostsAgency CostsDirect CostsDirect Costs

• Direct Agency CostsDirect Agency Costs– Arise because suboptimal decisions are made by Arise because suboptimal decisions are made by

managers when the act in a manner that is not in the managers when the act in a manner that is not in the best interests of shareholdersbest interests of shareholders

– Examples:Examples:• Managers avoiding high risk projects because they have an Managers avoiding high risk projects because they have an

undiversified stake in the health of the corporation (they undiversified stake in the health of the corporation (they could lose their job if the outcome is negative)could lose their job if the outcome is negative)

• Managers spending corporate resources on luxurious offices, Managers spending corporate resources on luxurious offices, executive aircraft, pension plans and poison pills that favour executive aircraft, pension plans and poison pills that favour their own self interest at the expense of shareholderstheir own self interest at the expense of shareholders

CHAPTER 2 – Business (Corporate) Finance 2 - 31

Agency CostsAgency CostsIndirect CostsIndirect Costs

• Indirect Agency CostsIndirect Agency Costs– Are incurred by the corporation in the attempt to avoid direct Are incurred by the corporation in the attempt to avoid direct

agency costsagency costs– Examples:Examples:

• Shareholder approval required before management can change the Shareholder approval required before management can change the articles of incorporate or bylaws or make major changes in share articles of incorporate or bylaws or make major changes in share capitalcapital

• Reporting requirements placed on management including, annual Reporting requirements placed on management including, annual report, audited financial statements, requirements for notice of report, audited financial statements, requirements for notice of annual and special shareholders meetingsannual and special shareholders meetings

• Elaborate compensation schemes including use of stock options Elaborate compensation schemes including use of stock options used to try to align the interests of managers with shareholders.used to try to align the interests of managers with shareholders.

CHAPTER 2 – Business (Corporate) Finance 2 - 32

Agency CostsAgency CostsAreas of For Potential DisagreementAreas of For Potential Disagreement

• Managers and shareholders may have Managers and shareholders may have differing goals, attitudes toward risk, and differing goals, attitudes toward risk, and differential access to information.differential access to information.– This can lead to areas of disagreementThis can lead to areas of disagreement

See Table 2-2 on the following slide. See Table 2-2 on the following slide.

CHAPTER 2 – Business (Corporate) Finance 2 - 33

Role of Management and Agency IssuesRole of Management and Agency IssuesAreas of Disagreement between Shareholders and ManagersAreas of Disagreement between Shareholders and Managers

Managers Shareholders

Performance Appraisal Accounting

ROI/cash Market Prices

Investment Analysis IRR of best division WACC external

Financing Retentions DebtDebt RetentionsNew Equity New equity

Risk Preservation of firm Portfolio

Table 2-2 Areas of Disagreement

CHAPTER 2 – Business (Corporate) Finance 2 - 34

Agency CostsAgency CostsExecutive CompensationExecutive Compensation

• In an attempt to align managements interests with In an attempt to align managements interests with shareholders, Boards of Directors have tried to tie shareholders, Boards of Directors have tried to tie compensation to performance measures.compensation to performance measures.

• These compensation schemes are not always effective These compensation schemes are not always effective in achieving their goal and have lead to concerns in achieving their goal and have lead to concerns about excessive management compensation.about excessive management compensation.

See Table 2-3 on the following slide. See Table 2-3 on the following slide.

CHAPTER 2 – Business (Corporate) Finance 2 - 35

Role of Management and Agency Issues Role of Management and Agency Issues Compensation Arrangements for CEOsCompensation Arrangements for CEOs

CEO Company Salary

($million)

Bonus

($million)

Shares/

Options

($million)

Other

($million)

Total

($million)

Hank Swartout Precision Drilling Trust 0.84 3.36 55.03 15.59 74.82

Hunter Harrison Canadian National Railway Co. 1.67 4.67 48.18 1.71 56.22Mike Zafirovski Nortel Networks Corp. 0.31 0.00 8.42 28.70 37.43

John Hunkin CIBC 0.75 0.00 28.72 0.00 29.47

James Buckee Talisman Energy Inc. 1.10 1.99 20.09 0.15 23.33

William Doyle Potash Corp. of Saskatchewan Inc. 1.15 1.28 19.53 0.16 22.13

Donald Walker Magna International Inc. 0.20 6.06 13.26 0.04 19.56

Andre Desmarais Power Corp. of Canada 0.91 0.70 16.69 0.55 18.84

Gwyn Morgan EnCana Corp. 1.48 2.66 13.87 0.16 18.16Richard Waugh Bank of Nova Scotia 1.00 1.50 14.40 0.28 17.18

Source: "Executive Compensation 2005." Report on Business w ebsite: <w w w .globeandmail.com>.

Table 2-3 Canadian Executive Compensation, 2005

CHAPTER 2 – Business (Corporate) Finance 2 - 36

What Is Corporate Finance? What Is Corporate Finance?

• The financial management of assets and The financial management of assets and corporate financing decisionscorporate financing decisions

(See Table 2-4 on the following slide for a (See Table 2-4 on the following slide for a

snapshot of the Canadian Corporate Balance Sheet) snapshot of the Canadian Corporate Balance Sheet)

CHAPTER 2 – Business (Corporate) Finance 2 - 37

Corporate Finance Corporate Finance Corporate Balance SheetCorporate Balance Sheet

($ billion) Liabilities ($billion)

Real AssetsBuildings 815Machinery and Equipment 362

Inventories 191

Land 281 Payables 203

Financial Assets Loans 321

Deposits 259 Paper 53

Receivables 249 Mortgages 114

Paper 29 Bonds 321

Debt 22 Claims 296

Claims 509 Shares 1659

Other 294 Other 44

Table 2-4 Non-Financial Corporate Canada Balance Sheet, 2005

Source: Statistics Canada. National Balance Sheet Accounts, Quarterly Estimates, Fourth Quarter 2005.

Ottaw a: Minister of Industry, 2006 (Catalogue No. 13-214-XIE).

Assets

CHAPTER 2 – Business (Corporate) Finance 2 - 38

Corporate Finance Corporate Finance What Senior Managers DoWhat Senior Managers Do

• Financial Management of AssetsFinancial Management of Assets– Capital budgeting decisionsCapital budgeting decisions

• Analysis and decision making with respect to asset Analysis and decision making with respect to asset investment, acquisition, and replacementinvestment, acquisition, and replacement

– Credit decisions, cash management, investment Credit decisions, cash management, investment decisionsdecisions

• Corporate Financing DecisionsCorporate Financing Decisions– Ratio of debt and equity, raising equity capital through Ratio of debt and equity, raising equity capital through

profit retention or new share issues, dividend policy, profit retention or new share issues, dividend policy, borrowing decisions, liability managementborrowing decisions, liability management

CHAPTER 2 – Business (Corporate) Finance 2 - 39

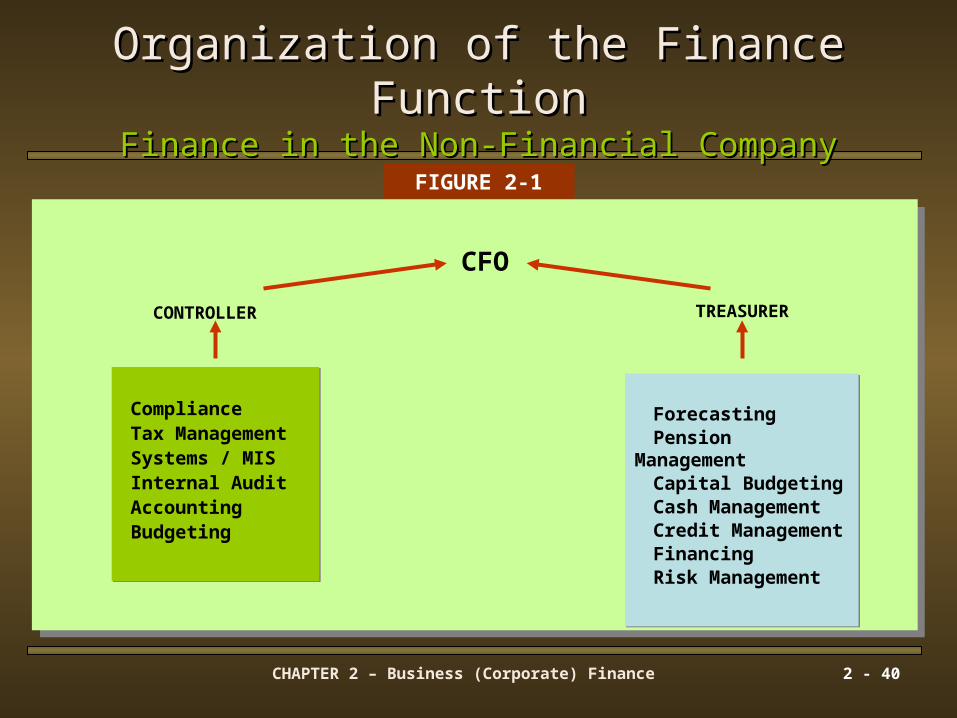

Finance Careers Finance Careers In Non-Financial FirmsIn Non-Financial Firms

• Chief Financial Officer (CFO)/Senior vice-Chief Financial Officer (CFO)/Senior vice-president of financepresident of finance

• Treasurer (pure finance)Treasurer (pure finance)– Forecasting, pension management, capital budgeting, Forecasting, pension management, capital budgeting,

cash management, credit management, financing, cash management, credit management, financing, risk managementrisk management

• Controller (finance and accounting)Controller (finance and accounting)– Compliance, tax management, systems, internal Compliance, tax management, systems, internal

audit, accounting, budgetingaudit, accounting, budgeting(See Figure 2-2 on the following slide)(See Figure 2-2 on the following slide)

CHAPTER 2 – Business (Corporate) Finance 2 - 40

Organization of the Finance FunctionOrganization of the Finance FunctionFinance in the Non-Financial CompanyFinance in the Non-Financial Company

ComplianceTax ManagementSystems / MISInternal AuditAccountingBudgeting

ComplianceTax ManagementSystems / MISInternal AuditAccountingBudgeting

TREASURER

CFO

CONTROLLER

ForecastingPension ManagementCapital BudgetingCash ManagementCredit ManagementFinancingRisk Management

ForecastingPension ManagementCapital BudgetingCash ManagementCredit ManagementFinancingRisk Management

FIGURE 2-1

CHAPTER 2 – Business (Corporate) Finance 2 - 41

Finance Careers Finance Careers In Financial InstitutionsIn Financial Institutions

• AnalystsAnalysts• AssociatesAssociates• ManagersManagers• Account ManagersAccount Managers• Banking AssociatesBanking Associates• Security AnalystsSecurity Analysts• Sales and Trading Sales and Trading

peoplepeople• Private BankersPrivate Bankers• Retail BrokersRetail Brokers

• Financial and Financial and Investment AnalystsInvestment Analysts

• Portfolio ManagersPortfolio Managers• Fixed income or equity Fixed income or equity

traderstraders• Corporate finance Corporate finance

associates and associates and consultantsconsultants

CHAPTER 2 – Business (Corporate) Finance 2 - 42

Internet LinksInternet Links

• TSX – TSX – http://www.tsx.comhttp://www.tsx.com• Report on BusinessReport on Business website – website – http://www.globeandmail.comhttp://www.globeandmail.com• Statistics Canada - Statistics Canada - http://www.statcan.ca/http://www.statcan.ca/• Small Business Canada – incorporating a company - Small Business Canada – incorporating a company - http://http://

sbinfocanada.about.com/od/incorporation/index_r.htmsbinfocanada.about.com/od/incorporation/index_r.htm• Industry Canada - Corporations Canada Site - Industry Canada - Corporations Canada Site -

http://strategis.ic.gc.ca/epic/site/cd-dgc.nsf/en/home?OpenDocumenthttp://strategis.ic.gc.ca/epic/site/cd-dgc.nsf/en/home?OpenDocument• Department of Finance Canada - Department of Finance Canada - http://www.fin.gc.ca/http://www.fin.gc.ca/

CHAPTER 2 – Business (Corporate) Finance 2 - 43

SummarySummary

• In this chapter you have learned:In this chapter you have learned:– About alternative ways to organize business enterprisesAbout alternative ways to organize business enterprises– About the pressures on corporations to create shareholder About the pressures on corporations to create shareholder

valuevalue– That agency relationships pose unique challenges on That agency relationships pose unique challenges on

corporations that result in additional costs to be borne by the corporations that result in additional costs to be borne by the firmfirm

– About the major decisions facing financial managers, andAbout the major decisions facing financial managers, and– About the major types of finance jobs in financial and non-About the major types of finance jobs in financial and non-

financial companies.financial companies.

CHAPTER 2 – Business (Corporate) Finance 2 - 44

CopyrightCopyright

Copyright © 2007 John Wiley & Sons Canada, Ltd. All rights Copyright © 2007 John Wiley & Sons Canada, Ltd. All rights reserved. Reproduction or translation of this work beyond that reserved. Reproduction or translation of this work beyond that permitted by Access Copyright (the Canadian copyright licensing permitted by Access Copyright (the Canadian copyright licensing agency) is unlawful. Requests for further information should be agency) is unlawful. Requests for further information should be addressed to the Permissions Department, John Wiley & Sons addressed to the Permissions Department, John Wiley & Sons Canada, Ltd.Canada, Ltd. The purchaser may make back-up copies for his or The purchaser may make back-up copies for his or her own use only and not for distribution or resale.her own use only and not for distribution or resale. The author The author and the publisher assume no responsibility for errors, omissions, and the publisher assume no responsibility for errors, omissions, or damages caused by the use of these files or programs or from or damages caused by the use of these files or programs or from the use of the information contained herein.the use of the information contained herein.

![[PPT]Introduction to Corporate Finance - John Wiley & Sons · Web viewINTRODUCTION TO CORPORATE FINANCE Laurence Booth • W. Sean Cleary Prepared by Ken Hartviksen Lecture Agenda](https://static.fdocuments.us/doc/165x107/5ac332217f8b9a12608b9edb/pptintroduction-to-corporate-finance-john-wiley-sons-viewintroduction-to-corporate.jpg)