INTRODUCTION - Tech.eu€¦ · The Latvian startup ecosystem 19 Top industries in Lithuania 41...

68

1

Transcript of INTRODUCTION - Tech.eu€¦ · The Latvian startup ecosystem 19 Top industries in Lithuania 41...

1

INTRODUCTIONSince we started, one of the key aims of the team at Tech.eu has been to track all of the funding rounds and exits in Europe, providing the most comprehensive and accurate records and analysis of the European technology scene.

We do this by meticulously monitoring hundreds of sources, across multiple languages and regions.

However, many Baltic rounds were off our radar. They hadn’t been reported on by the press, even less by the English press. Much of the data came from founders or investors. This highlights the need for Baltic states to have a more comprehensive reporting system for deals, so that we can be sure to have accurate data.

We want to thank organisations from each country’s ecosystem, such as the Latvian Startup Association and Estonia’s Garage84, whose crowdsourced spreadsheets helped us to complete our data set. Also, thanks to Infogr.am, a Latvian startup we found while doing this analysis, which we used to create many of our charts.

Some of the biggest scale-ups emerging from these countries have moved the majority of their operations abroad, such as Skype, Latvia’s Bitfury, and Lithuania’s YPlan, and have been excluded from the analysis. The removal of these successful scale-ups certainly affected the total funding figures for each country. We also excluded TransferWise’s huge $280 million round in Q4 2017, because our analysis only includes data through Q3 2017.

This report focuses on the ecosystems and funding raised by the Baltic states of Latvia, Lithuania, and Estonia, between 2014 – Q3 2017.

In this report we take an in-depth look at the funding in the Baltics over the analysed period, highlight some of the most important investors and startups from each country, and give background on the growing ecosystems of these European countries, who are at the forefront of building some of the most startup friendly governments and ecosystems in Europe despite their small size. These countries have made great progress by investing in ICT infrastructure and implementing laws that encourage entrepreneurship.

There were less than 10 exits per country in the analysed period, so instead of doing an analysis, we highlighted a few of the major exits.

We’ve worked to make this report as comprehensive and valuable as possible. Please refer to the end of this report for methodology and disclaimers. For any questions or comments regarding the report we invite you to email [email protected].

This report was written by:

• Mary Loritz, data analyst at Tech.eu• Robin Wauters, founding editor of Tech.eu

2

INDEXIntroduction 2 Top rounds in Latvia by year 26-27 Interview with Kadi-Ingrid Lilles 50-51

Index 3 Top investors in Latvia 28 Interview with Ragnaar Sass 52-53

Key takeaways 4 Notable Latvian startups 29-30 Estonian funding analysis 54

Key trends 5 Notable Latvian exits 31 Average and median deal size in Estonia

55

Baltic funding analysis 6 The Lithuanian startup ecosystem 32-34 Top industries in Estonia 56

Funding by quarter and year 7 Interview with Arvydas Bloyze 35-36 Top rounds by year 57-58

Funding in the Baltics and other European countries

8 Interview with Ilja Laurs 37-38 Top investors in Estonia 59

Tech investment in the Baltics and Europe per capita

9-14 Lithuanian funding analysis 39 Notable Estonian startups 60-62

Average and median round size in the Baltics 15 Average and median deal size in Lithuania 40 Notable Estonian exits 63-64

The Latvian startup ecosystem 19 Top industries in Lithuania 41 Conclusions 65

Interview with Jeckaterina Novicka 20 Top rounds in Lithuania by year 42-43 Methodology and disclaimers 66-67

Interview with Olga Barreto Goncalves 22 Top investors in Lithuania 44

Latvian funding analysis 23 Notable startups in Lithuania 45-46

Average and median deal size: Latvia 24 Notable exits in Lithuania 47

Top industries in Latvia 25 The Estonian startup ecosystem 48-49

3

THE BALTICS: KEY TAKEAWAYS, 2014 – Q3 2017

4

KEY TRENDSDeveloping strong infrastructures to become startup havens

The Baltics – Latvia, Lithuania, and Estonia, are countries that have seen a lot of success in the past 10 years. Each country’s government has made efforts to invest in ICT infrastructure, fast internet, funding for accelerators, IT education beginning in primary school, and laws to encourage entrepreneurship. Each country now has its own Startup Visa programme to attract foreigners to start their business in the Baltics.

No big VCs mean low funding rounds

The Baltics are so small – with populations ranging from 1.3 to 3 million people – that they can’t support big VCs that would help startups to scale. That means that most startups with funding from Baltic investors receive early stage or seed funding from accelerators and angel investors, and the majority of rounds in the Baltics are worth €200,000 or less. Larger rounds are usually backed by foreign investors.

Scale-ups tend to move abroad

When startups do scale – raising €5 million or more, usually from a foreign investor – they tend to move their headquarters abroad to cities like London, San Francisco, and New York. However, this isn’t necessarily a bad thing. According to Jeckaterina Novicka from the Latvian Startup Association, scale-ups change headquarters so they can be near other major companies as well as VCs to make new contacts and partnerships,

but many keep their back offices and the majority of their staff in their home countries, and pay taxes in the Baltics. The founders are also able to contribute back to the local ecosystem by sharing their experiences in other markets.

Low overall investment volume, high funding levels per capita

Though investment volume seems low in the Baltics compared to larger European countries, when taking into account their small populations, they have much higher investment volume per capita than their counterparts. Estonia ranks above Germany, France, and the Netherlands in per capita funding. Latvia ranks above Spain, and Lithuania ranks above Italy and Eastern European countries.

The Skype effect

Estonia dominates the region in terms of total funding and number of deals. The country has raised 3x that of Latvia or Lithuania, with €283 million in the analysed period. This success can be attributed in part to Estonia’s early adoption of e-Governance initiatives, which, among other things, allow Estonians to start a business in just 15 minutes. But the success of Skype was key in kickstarting the startup ecosystem, encouraging many to follow its path. Many former employees and founders of Skype have gone on to launch other startups (they even have their own organisation, “Skype Mafia”), and it has had an effect on the other Baltic states in inspiring entrepreneurship and investments in technology.

5

BALTIC FUNDING ANALYSIS

6

2014 – Q3 2017

Latvia, Lithuania, and Estonia

ANALYSIS

• For Europe as a whole, tech funding has been steadily increasing since 2014 – tripling from Q1 2014 to Q3 2017. Yet the Baltic states of Latvia, Lithuania, and Estonia show no such steady growth trends, as quarters tend to fluctuate over the analysed period. In most quarters, between €20 and €50 million has been raised. There is no clear correlation between number of deals and amount raised, suggesting that most rounds are small, with occasional exceptions.

• The average amount raised per quarter across all three Baltic states is €32 million.

• Baltic states had an outstanding year in 2015, raising €189 million. This was due to large rounds for TransferWise (€53 million), Vinted(€25 million) and Adcash (€20 million). Over €100 million was raised in 2014 and 2016, but only €64 million has been raised in so far in 2017. This excludes TransferWise’s $280 million round in Q4 2017. If this round had been included, total funding for 2017 would be brought to over €300 million, making it by far the best year in the analysed period.

• The number of deals per year stayed steady throughout 2014-2016, but dropped off in 2017, with only one quarter left to raise 60 rounds and keep it on par with other years.

7

Funding in the Baltics by quarter and year, 2014 – Q3 2017

ANALYSIS

• Investment volume in Baltic nations is clearly lower than the majority of its European counterparts, with Baltic states collecting a total of €465 million over the analysed period, compared to €15 billion for the UK, €10.2 billion for Germany, and €7.4 billion for France.

• Estonia has the highest overall investment volume of the Baltic states, raising €283 million in the analysed period, followed by Latvia with €93 million, and Lithuania with €89 million.

• Yet, is this a fair comparison? Does this necessarily correspond to lower activity? The UK is home to 65 million people, Germany 81 million, and France 67 million. Meanwhile, Estonia is home to a only 1.3 million people, Lithuania 3 million, and Latvia 2 million.

• Correspondingly, the Baltics also had fewer deals than their counterparts - Estonia with 169, Latvia with 146, and Lithuania with just 70.

Total funding in different European countries, 2014 – Q3 2017

8

• Deal sizes tend to be smaller in the Baltics than more populous nations, as these countries are too small to attract big VCs, and most deals are early stage or angel rounds.

• If we take into account the small populations of Baltic nations, we can see that their investment activity actually exceeds that of many other European nations.

9

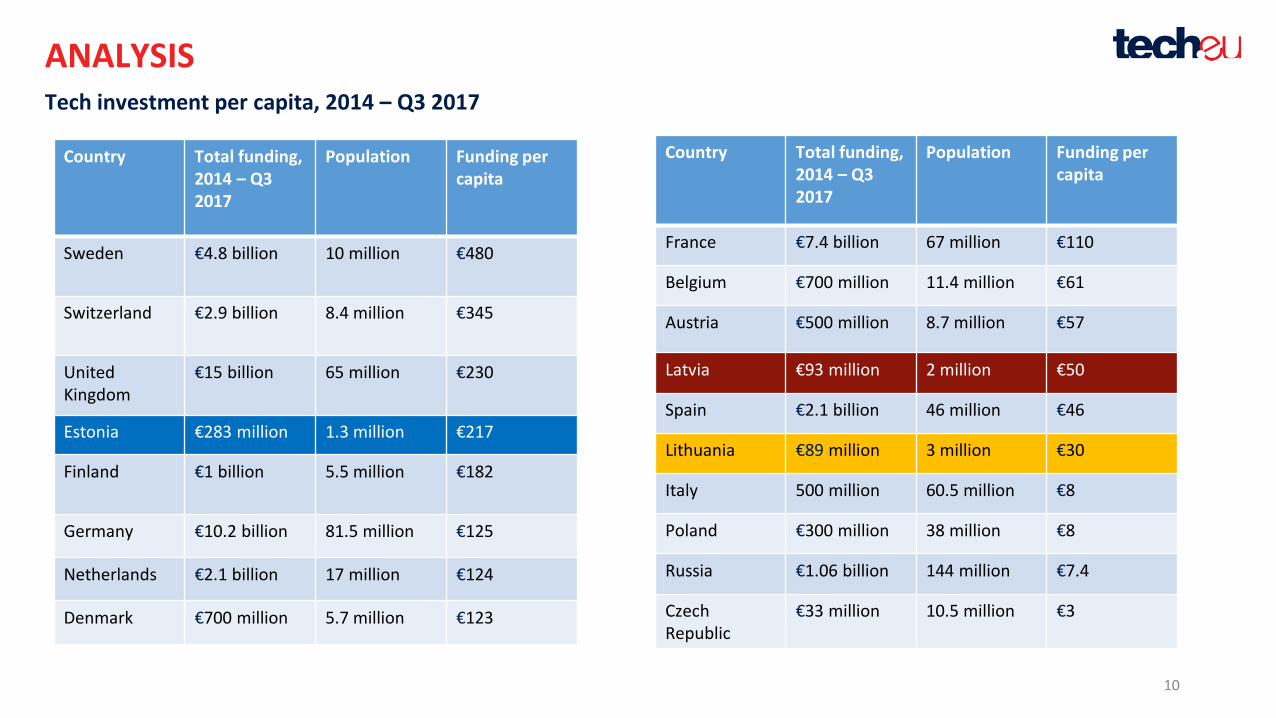

• When taking population into account and looking at tech investment on a per capita basis, a much different picture appears. Sweden leads with €480 in funding per capital in the analysed period, followed by the wealthy nation of Switzerland with €345, and the UK with €230, though it leads Europe in total investment volume.

• Estonia ranks very high, neck and neck with the UK, raising €217 per capita, with more activity than wealthier counterparts such as Finland, Germany, the Netherlands, Denmark, and France. If TransferWise’s Q4 round were included, Estonia’s per capita would rise to €399, above Switzerland and the UK.

• Latvia ranks above Spain, Russia, Italy, and Poland, with €50 per capita, making it competitive with Belgium, which has raised €61 per capita, and Austria, with €58 per capita.

• Lithuania’s per capita funding remains low compared to other European and Baltic countries with €30 per capita, but is above Italy and other Eastern European countries like Poland, Russia, and the Czech Republic.

ANALYSISTech investment per capita in Europe and the Baltics, 2014 – Q3 2017

00

10

Country Total funding, 2014 – Q3 2017

Population Funding per capita

Sweden €4.8 billion 10 million €480

Switzerland €2.9 billion 8.4 million €345

United Kingdom

€15 billion 65 million €230

Estonia €283 million 1.3 million €217

Finland €1 billion 5.5 million €182

Germany €10.2 billion 81.5 million €125

Netherlands €2.1 billion 17 million €124

Denmark €700 million 5.7 million €123

Country Total funding, 2014 – Q3 2017

Population Funding per capita

France €7.4 billion 67 million €110

Belgium €700 million 11.4 million €61

Austria €500 million 8.7 million €57

Latvia €93 million 2 million €50

Spain €2.1 billion 46 million €46

Lithuania €89 million 3 million €30

Italy 500 million 60.5 million €8

Poland €300 million 38 million €8

Russia €1.06 billion 144 million €7.4

Czech Republic

€33 million 10.5 million €3

ANALYSISTech investment per capita, 2014 – Q3 2017

11

How do Baltic states compare to other countries of a similar size or in Eastern Europe?

ANALYSIS

• Poland raised the most funding overall, with €293 million across 70 deals.

• Estonia had the second highest investment volume, at €283 million, followed by Turkey, Iceland and Luxembourg.

• Latvia and Lithuania follow, each raising around €90 million.

• While there is generally a correlation between funding and number of deals, Latvia diverges drastically, with a higher number of deals compared to funding, indicating smaller rounds. • There are few countries with a smaller

population than Baltic nations - Iceland, Luxembourg, and Malta.

• We can see that Eastern European countries with higher populations (though perhaps less GDP per capita) raise less capital, including Croatia, Romania, Greece, Hungary, Slovenia, and Bulgaria.

12

Per capita funding: the Baltics compared to smaller and Eastern European countries

ANALYSIS

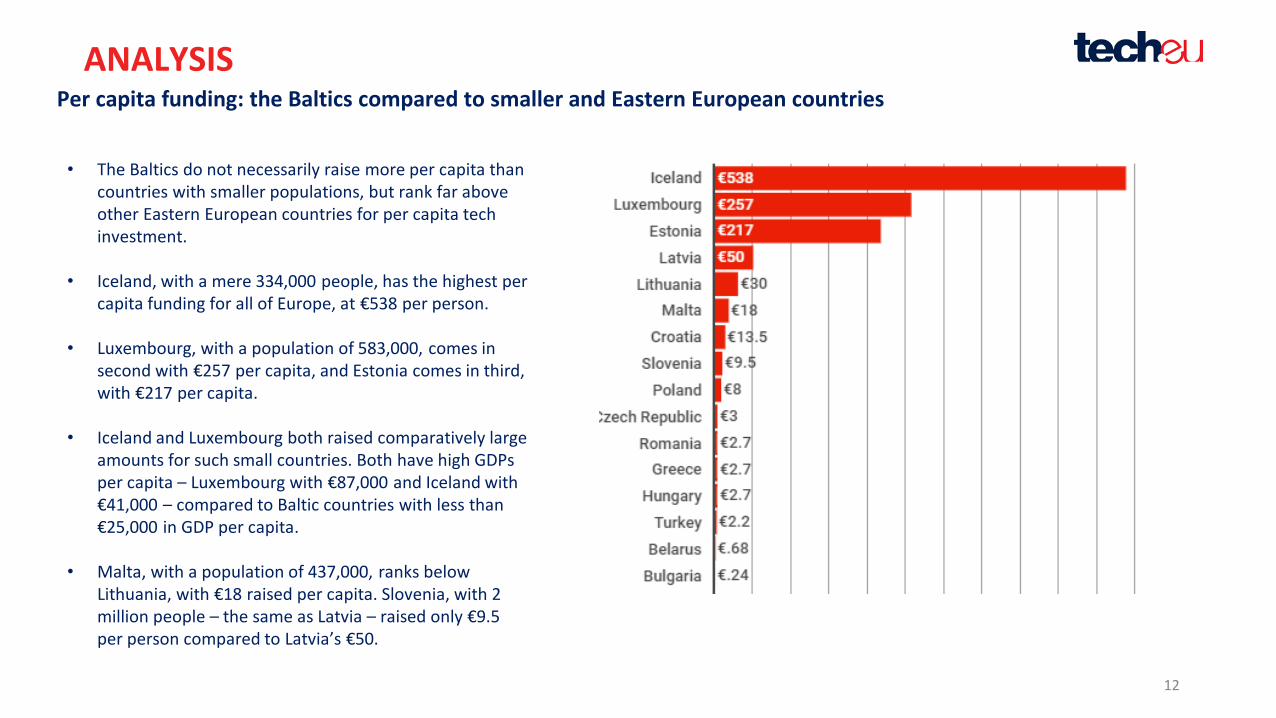

• The Baltics do not necessarily raise more per capita than countries with smaller populations, but rank far above other Eastern European countries for per capita tech investment.

• Iceland, with a mere 334,000 people, has the highest per capita funding for all of Europe, at €538 per person.

• Luxembourg, with a population of 583,000, comes in second with €257 per capita, and Estonia comes in third, with €217 per capita.

• Iceland and Luxembourg both raised comparatively large amounts for such small countries. Both have high GDPs per capita – Luxembourg with €87,000 and Iceland with €41,000 – compared to Baltic countries with less than €25,000 in GDP per capita.

• Malta, with a population of 437,000, ranks below Lithuania, with €18 raised per capita. Slovenia, with 2 million people – the same as Latvia – raised only €9.5 per person compared to Latvia’s €50.

13

Country Total funding, 2014 – Q3 2017

Population Funding per capita

Iceland €180 million 334,000 €538

Luxembourg €150 million 583,000 €257

Estonia €283 million 1.3 million €217

Latvia €93 million 2 million €50

Lithuania €89 million 3 million €30

Malta €8 million 437,000 €18

Croatia €54 million 4 million €13.5

Country Total funding, 2014 – Q3 2017

Population Funding per capita

Slovenia €19 million 2 million €9.5

Poland €300 million 38 million €8

Czech Republic €33 million 10.5 million €3

Greece €30 million 11 million €2.7

Hungary €27 million 10 million €2.7

Romania €54 million 20 million €2.7

Turkey €180 million 79.5 million €2.2

Bulgaria €1.7 million 7 million €.24

ANALYSISTech investment per capita in small and Eastern European countries, 2014 – Q3 2017

14

ANALYSISTech investment per capita in Europe and the Baltics, 2014 – Q3 2017

• This map shows investment volume per capita in each country during the analysed period, 2014 – Q3 2017.

• The countries with the most per capita funding are in red – Iceland and Sweden. Next comes Switzerland in mauve raising €345 per capita, the UK with €230, and Estonia with €217 (which would be €399 if the TransferWise deal from Q4 was included) with other high ranking countries in purple.

• Countries raising €100 or less appear in blue, with some Eastern European countries raising less than €1 per capita (Albania, Bulgaria, Belarus, and Slovakia). Because these countries don’t tend to have strong ecosystems, it is possible that they don’t have websites or organisations systematically reporting deals, and that many go unrecorded.

• We had little or no data for countries missing from the map, including Ukraine, Bosnia, Moldova, and Georgia.

15

ANALYSIS

• The average round size in Europe grew substantially in Q2 and Q3 2017, doubling the average round size in previous quarters. Average round size for Europe as a whole across the analysed period is €5.2 million.

• The average round size in the Baltics varies greatly from quarter to quarter, and is uncorrelated with the median round size, pointing to the influence of a few large deals.

• Median round size in Europe shows a steady growth pattern, going from €550,000 in Q1 2014 to a high of €1.6 million in Q2 2017, so overall deal size is rising.

• Median round size for the Baltics shows no growth pattern, with median deal size per quarter about 20% of the median deal size for Europe as a whole. The majority of rounds are worth less than €200,000 in most quarters.

Average and median round sizes in Europe vs. the Baltics

16

• Estonia’s average deal size hovers around €1 million, while Latvia has a much smaller average deal size at €500,000 in 2014, 2015, and 2016, though it soared to €2.9 million in 2017 due to few rounds and the €21 million deal for Creamfinance.

• Estonia has a higher median round size than other Baltic states, with an average median round size of €314,000.

• Lithuania has an average median round size of €188,000, higher than Latvia. However Lithuania has far fewer deals overall – only 70 in the analysed period, versus 146 for Latvia.

ANALYSISAverage and median round size in the Baltics by year

A CLOSER LOOK AT COUNTRY-SPECIFIC FUNDING AND EXIT

ACTIVITY

17

18

Latvia

The Latvian startup ecosystem

19

Latvia is the only country in the analysis that shows a year over year growth pattern in investment volume – though it has still raised less overall than its neighbors.

However, this can be understood as it has a smaller population than Lithuania, and doesn’t have the legacy of Skype or e-Governance in Estonia, which strengthened its ecosystem early on.

We’ve also taken Latvia’s most successful startup, BitFury, out of the analysis, because it moved the majority of its operations to Poland. The startup raised €81 million in the analysed period. Had the startup kept their operations in Latvia, the country’s total funding in the analysed period would be €174 million instead of €93 million.

The country is making progress, however. The government, through its state development financing institution, Altum, launched Labs of Latvia, which tracks startup news in English and Latvian. Altum provides state funds for acceleration (€15 million), seed and growth stage startups (€60 million), and for social entrepreneurship (€12 million).

The Latvian Startup Association has been moving quickly, working with the government to pass a new startup law that reduces taxes on employees salaries for startups in Latvia, and is being amended to apply to more startups. The startup law allows for a flat tax on employee salaries, co-financing of highly qualified labor, and waives personal and corporate income tax.

20

Interview with Jekaterina NovickaChairwoman of theLatvian Startup Association

Can you provide a brief background of the Latvian startupecosystem, and how it has changed in recent years?

The ecosystem has changed a lot in the past five to six years. Five years ago, you might have heard the word startup in the media once a month, if that, and now you hear the word startup every day. There has certainly been a growth in the number of startups in Latvia, even if they haven’t received big amount of funding yet.

The government has begun to acknowledge the importance of startups to the economy, and provide more support. For example, the government launched the portal Labs of Latvia three years ago, a website that provides news and aggregates all the important information about the Latvian startupecosystem.

The Latvian Startup Association was formed in the beginning of 2016 to bring together different players in the Latvian ecosystem including startupfounders and employees, coworking spaces, incubators, accelerators, individual and corporate supporters, and investors. The association has been working with the Latvian government to pass the new startup law and Startup Visa.

We also became a member of Startup Nations and the European StartupNetwork and have established a cooperation with international corporations such as Accenture, as we want to increase recognition of Latvia as a tech-oriented country.

Over the past few years we have seen more startup events, and host some of the largest conferences in the Baltics, like the Digital Freedom Festival and TechChill. We are seeing growing interest from corporations and banks, both Latvian and international, who want to get involved in the ecosystem, by coming to events, supporting them, or creating partnerships with some of our startups.

Can you tell us about Latvia’s new startup law and how it has affected the ecosystem?

We worked with the Latvian government to pass the new startup law in 2016. The main advantage it provides to startups is a significant reduction in taxes for employee salaries. Unfortunately, the law has not yet had the impact we would like, because it currently only applies to startups that have received VC funding - not startups backed by accelerators, business angels, or startups with no funding. However we are working with the government to make changes to the law by the end of this year to make it more inclusive, and these changes should go into effect in the beginning of 2018. We hope these changes will make the law accessible to many more startups, and attract people from other countries to launch their startups in Latvia, or even for more mature startups to relocate and maintain a back-office here.

21

Why haven’t we seen a strong trend of increasing deals and investment if the Latvian ecosystem is growing?

The number of startups has grown, but they haven’t necessarily received big funding. There haven’t been many available funds the past couple of years, because funding provided from the EU to invest in Latvian startups, administered by government-backed funds Imprimatur Capital, ZGI Capital and FlyCap, ran out in 2016 and Latvia has only few private VCs. So that has affected investment in Latvian startups, as these were the most active funds in the country.

However, Latvia expects to receive €60 million in EU funding next year, to be distributed by different funds and 3 accelerators that are already in the launch process. New private smart money VCs like Change Ventures or Buran Venture Capital have also recently launched in Latvia. So we expect there to be an influx of funding very soon.

Some of the more successful startups that are receiving large rounds and scaling-up, such as BitFury, have moved their headquarters to other countries. Why do these startups change their headquarters once they start growing?

Well, this is something that affects all Baltic states, I think. Scale-upschange headquarters when they grow because they want to be closer to

grow as well as have access to major VC funds. The clear trend we see thatthose scale-ups still keep their back-offices in Latvia where majority of staff is located and therefore there is an effect of contributing back to the society by these people and sharing experience to the local startupcommunity. Also, our Ministry of Economics is happy as large amounts of the taxes paid by these scaleups is still paid in Latvia.

Despite lower investment in Latvia than in other European countries, because the country is so small it has more investment in startups per capita than Spain, Italy, and other Eastern European countries.

So, for such a small country, Latvia is doing quite well. What do you think accounts for its success?

That’s a good point, we are a very small country. In Latvia I would say almost all business people speak three languages, Latvian, English and Russian, often even more. Latvia has a great airport that makes it accessible internationally, the internet is the 10th fastest in the world, and startup costs and the cost of living are low compared to other European countries.

And because Latvia is such a small market, from day one startups here realize that they need to be designed to reach an international market. I also like to think that our success is accelerated by the supportive and very active startup community we have locally.

Interview with Jekaterina Novicka cont’d

22

How has Latvia's ecosystem changed in recent years?

There has been a big shift in mentality: in Soviet times, there was little room for innovation, creativity and entrepreneurship. The economy was planned, supply shaped demand, and young people were interested in stable well-paid jobs.

Once the Soviet Union collapsed and the crazy chaotic 1990’s had passed, a painful but necessary transition took place towards embracing innovation. This has been an interesting journey and we are only at the beginning of it!

Government support is unprecedently high, with a range of support programmes are being offered to startups. The Latvian startup market is far from saturation point: the money-to-startup ratio (money = startupfinancing) is much higher than in other countries (e.g. in Silicon Valley it is extremely low, a lot more startups compete for the same $1 than here in Latvia).

This means that a lot of change needs to happen to the “startup” part of that ratio – we need to increase the number of startups. This is one of the dilemmas our government is trying to solve: how do we increase the number of startups, while keeping the quality high?

To address this, the government has launched a series of interventions which range from helping would-be entrepreneurs who do not even have an idea yet but who would like to try something of their own, to solid startups who already have a well defined product and would like to conquer new markets – and everything in between. It is a good ecosystem for launching and testing/piloting your product. We hope that foreigners will also appreciate that and more and more startup founders will come here.

If you have any questions for the LIAA, you can send them an email at [email protected].

Interview with Olga Barreto Goncalves, Chief StartupInstigator at Investment and Development Agency of Latvia

What do you think is important for others to know about the Latvian ecosystem?

The ecosystem has been developing and growing rapidly. In the ecosystem at the moment everyone is doing something by themselves, but we are gradually moving towards more open and frequent communication. It is clear that all sectors – public, private, academia need to work together.

23

• For four-fifths of the quarters in the analysed period, investment volume stayed below €10 million in Latvia, and less than €5 million was raised in over half of the quarters on record. Periodic high volume quarters were due to one or two large deals in those quarters.

• Latvia had its best quarter in Q1 2017, due to a large round for the fintech startup Creamfinance (€21 million).

• Q3 2015 was another high quarter, with a large round for Eco Baltia (€10 million), a waste management and recycling startup serving over 45,000 clients.

• Q3 2016 had the most rounds, 32, despite raising only €8 million. All other quarters had 13 deals or less.

• Despite raising less than Estonia, Latvia is the only Baltic state that shows a consistent upward trend in investment volume year over year since 2014. Already in 2017 Latvia’s investment volume has doubled since 2014, though only 11 deals have been recorded this quarter versus 50 in 2016, pointing to the significant effect of Creamfinance’s round.

ANALYSIS: LATVIAInvestment volume and number of deals by quarter and year

24

ANALYSIS: LATVIA

• The average round size in Latvia was below €100 million in 11 out of 15 quarters. Q4 2016 – Q3 2017 have seen an increase in average deal size, there were fewer deals in these quarter than in most – between 3 and 6 – and some large rounds including €7.7 million for Twinoin Q4 2016, €21 million for Creamfinance in Q1 2017, and €7 million for Atlas Dynamics in Q3 2017.

• The average round size in Latvia is around €500,000 in most quarters, with a few recent outliers, while for the Baltics, the majority of quarters were above €1 million. • The median round size for the Baltics stayed

below €300,000 for all quarters, except for a Q1 2015, which saw a median of €433,000.

• While Latvia had medians of below €200,000 in most quarters, there were outliers in which the median deal size was €375,000, €500,000, or €1.4 million. All things considered, median round size in Latvia and the Baltics as a whole is more or less comparable.

Average and median round size by quarter in the Baltics and Latvia, 2014 – Q3 2017

25

ANALYSIS: LATVIA

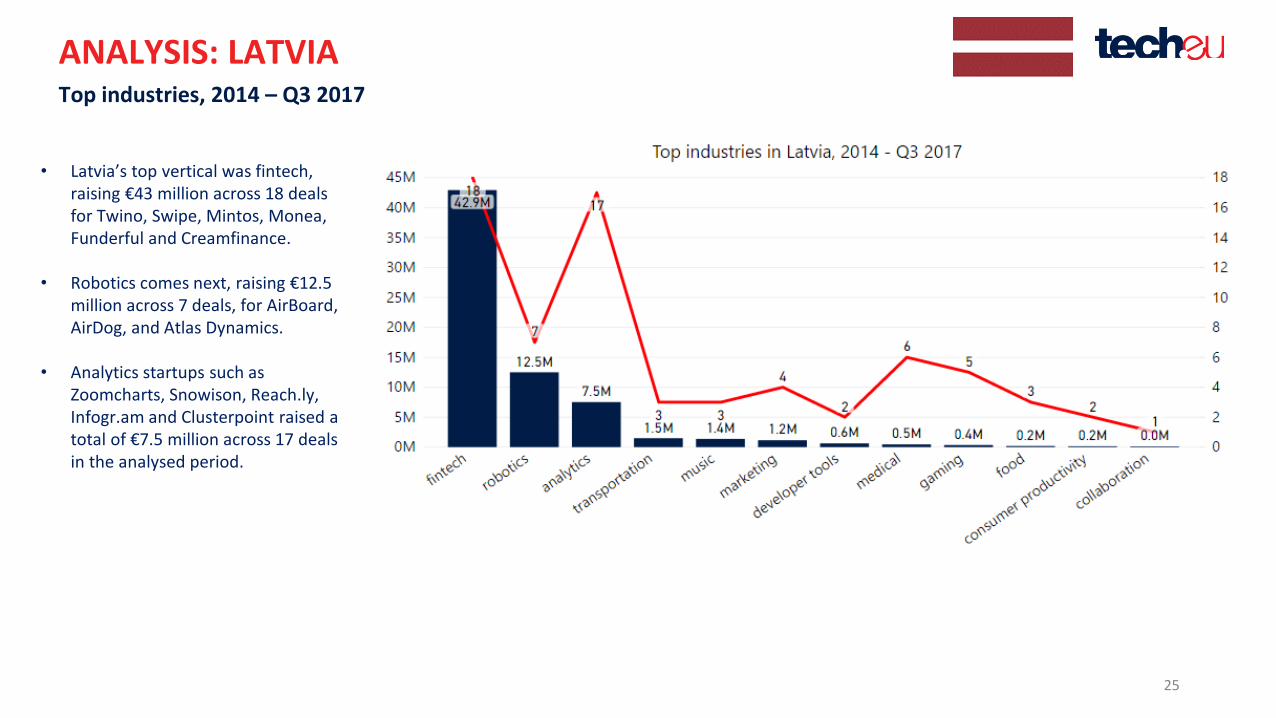

• Latvia’s top vertical was fintech, raising €43 million across 18 deals for Twino, Swipe, Mintos, Monea, Funderful and Creamfinance.

• Robotics comes next, raising €12.5 million across 7 deals, for AirBoard, AirDog, and Atlas Dynamics.

• Analytics startups such as Zoomcharts, Snowison, Reach.ly, Infogr.am and Clusterpoint raised a total of €7.5 million across 17 deals in the analysed period.

Top industries, 2014 – Q3 2017

26

• Latvia’s largest round was for the fintech startup Creamfinance, which raised €21 million Series B from South African Capitec Bank in Q1 2017.

• 2017 also saw a large round for Atlas Dynamics, which creates drones and operating systems that can be used in a variety of industries, such as security, agriculture, inspections, and emergency response.

• The top round for 2016 was for the fintech TWINO, an investment marketplace that provides consumer loans. The company operates in 7 countries and has issued over €280 million in loans since it launched.

• Mintos, another fintech that offers peer-to-peer lending, raised €2 million from Skillion Ventures in Q1 2016.

• AirDog, a producer of drones that are intended to follow their owners and create videos of action sports, raised €3 million from FlyCap and Altum in Q2 2016.

Top rounds in Latvia, 2017

Top rounds in Latvia, 2016

ANALYSIS: LATVIATop rounds in Latvia

27

• Latvia’s top round for 2015 was for Eco Baltia, a cleantech startup that provides waste management and recycling services. The company raised €10 million in Q3.

• Clusterpoint, a software startup that develops special databases that can be used by business and governments alike, raised €3 million across 2 different rounds in Q1 and Q3 2015. Investors included BaltCapand Imprimatur Capital. The company is now developing network forensics cybersecurity solutions.

• The top round for 2014 was for Creamfinance, raising €5.6 million in Q4 from Flint Capital.

• Infogr.am, a platform for easily creating infographics and data visualizations such as maps, charts, and graphs, raised €2 million from Point Nine Capital and Connect Ventures in Q1 2014. In May 2017, the Latvian startup was acquired by the US-based interactive presentation platform Prezi.

Top rounds in Latvia, 2015

Top rounds in Latvia, 2014

ANALYSIS: LATVIATop rounds in Latvia

28

• Latvia’s two top investors were Imprimatur Capital and FlyCap. These investors, along with ZGI Capital, received money from the government and the EU for their investments, and these funds have dried up since 2016, accounting for the small number of deals in 2017, though there is supposed to be an influx of EU funding coming in 2018.

• Imprimatur Capital is a London-based fund that backs science and technology startups. Out of the 69 deals Imprimatur Capital has backed in the analysed period, 46 were in 2014 and 2015, and 64 were between 2014 – 2016. The fund apparently has had little left to invest in 2017.

• FlyCap is a Latvian-based fund which invests a maximum of €1.5 million per startup, with first investments ranging from €50,000 – €200,000. It has invested in RCG Lighthouse, PolyLabs, Mailigen, TapCore, and AirDog. All of FlyCap’s 16 deals in the analysed period were between 2014 – 2016.

Top investors, 2014 – Q3 2017

29

Sellfy is an e-commerce marketplace for self-publishers of digital content, allowing them to open their own online shop through the platform to sell their digital products. E-books, music, video, photos, other digital products can be sold by the content’s creators. Sellers can easily customise their online storefront to be consistent with their brands. Sellfy provides a range of services to these digital sellers including product hosting, payments, product delivery, and allows users to easily integrate their products into other sites such as Facebook, YouTube, or their own website. The platform also offers marketing features, such as SEO optimisation, discount codes, and email marketing, and tracks the online shop’s analytics. The startuptakes a mere 5% cut from each purchase made through the platform.

Sellfy was founded in 2011 in Riga by Maris Dagis and Kristaps Alks. The startup raised an undisclosed seed round in 2011 from StartupHighway, followed by another undisclosed round in 2012 by angel investors Sten Tamkivi and Toivo Annus.

LightSpace Technologies has been developing its volumetric real time 3D display technology since 1996. The company has created technology for 3D image guided surgery to help surgeons conduct precise and minimally invasive procedures. It has also applied its technology to create solutions for 3D luggage screening, and can be used for many more applications. It has recently produced a 3D visualization toolbox for MATLAB.

LightSpace Technologies raised €800,000 from Imprimatur Capital and HansaMatrix in Q2 2017, and a small round in 2014 of €150,000. The company just opened its first office in Silicon Valley in 2017 to market its technology in the US market.

Notable Latvian startups

30

BranchTrack has created a platform to train employees through digital simulations. The platform is especially tailored to customer service and sales, but can be used in any sector to improve learning and outcomes for employees. Using BranchTrack, companies can create digital simulations of situations in which employees may find themselves, allowing them to role-play with different responses. Companies can add characters, materials, videos, and voiceovers to the platform to customise the training.

The startup has also gamified its service, so learners can accumulate points by completing simulations, compete with coworkers on mobile devices, and engage in competitive digital roleplays. The company raised a €250,000 seed round in Q1 2016 from Imprimatur Capital and an angel investor. BranchTrack has already partnered with 1,500 clients, including major companies such as Johnson & Johnson, Mary Kay, and Slack.

Notable Latvian startups

Nordigen is a B2B fintech and data analytics startup. The company uses machine learning and AI to analyse customer transaction data in order to more accurately evaluate credit scores. Banks typically reject 30-90% of all loan applications, however Nordigen claims that the riskiness of rejected applicants is often overrated.

“A lot of resources are spent to acquire information necessary for making a credit decision – loan applicant’s salary, liabilities, late payments, household expenses, etc. Luckily, all this information is already available to you in client bank transactions, including payment behaviour, payday loans, gambling and 200 more categories,” according to the company.

Nordigen allows banks to reduce the number of rejected loan applications by providing better data, thereby increasing revenue for banks, and providing more loans to those who need them. The startup, founded in 2008, works with more than 20 banks and alternative lenders in 5 countries.

31

Infogram is an online platform to create data visualizations and graphics. Users can create charts, infographics, maps, and entire reports.

Infogram was founded in 2012 in Riga by Oldis Leiterts, Raimonds Kaze, and Alise Semjonova. It initially raised a €250,000 seed round in 2012, and raised €2 million in Q1 2014 from Point Nine Capital and Connect Ventures.

In May 2017, Prezi, a San Francisco-based platform that allows users to create interactive, cloud-based presentations, acquired Infogramfor an undisclosed amount.

Notable Latvian exits

Founded in 2015, Setupad, a Latvian adtech and marketing startup, helps companies and publishers better target their advertising, and helps publishers gain incremental revenues ranging from 50% to 70%. Setupad provides a yield management service and allows publishers to get back to their job of content creation.

Setupad was acquired by the Swedish Signia Group in May 2017. The Signia Group is a digital media company whose customers include major media conglomerates and niche publishers. It helps content creators, publishers, and brands to increase their customer engagement. Signia provides services and tools for workflow management, business intelligence, reporting, ad delivery and monetization.

32

Lithuania

33

The Lithuanian startup ecosystem

Lithuania has been busy transforming itself into a business friendly country in the past decade. The country may not have seen a steady rise in investment volume over the past three years, but the number of startups has grown from around 80 five years ago to over 300 today.

Between 2006 - 2013, Lithuania spent €411 million to develop R&D infrastructure and science valleys, and is investing another €679 million between 2014 – 2020 to further develop R&D capacity.

The country has been ranked the 16th

most business friendly country in the world for 2018 by the World Bank. According to Lithuania’s Centre of Registers, it only takes three days to start a new business. The country ranks 1st in the CEE for collaboration between

universities and industry for R&D, and Vilnius was also listed as one of the top ten “smart cities” by CNN.

The country has some of the lowest taxes in Europe. Meanwhile, the cost of living is quite low, with Vilnius ranked among the 5 least expensive cities in Europe.

Infrastructure, low taxes, the ease of starting a business, and low costs are not the only reasons to startup in Lithuania. The country boasts a highly-skilled workforce, where nearly 100% of young professionals speak English, and many speak additional languages. Students begin to learn computer science and robotics in primary school. What’s more, labor costs here are 4x less than the European average.

Top startups

Investment volume Number of deals

Because of the ease of obtaining a banking license, which only takes 3 months in Lithuania, about 12 Israeli fintech startups have recently moved operations there. And the UK-based fintech Revolut, a money transfer app, has just established a presence in Lithuania in order to apply for a European banking license.

The country’s low tax rate and low costs have also attracted several Russian startups to relocate in the country and establish a presence in the EU.

Lithuania introduced several reforms in 2016 and 2017 to make the country more business friendly, including strengthening minority investor protections by increasing corporate transparency, and introducing an electronic system for filing and paying value added tax, corporate income tax and social security contributions.

The country’s Startup Visa programme was also implemented in 2016. It is designed for startupfounders who want to establish their business in Lithuania or attract foreign talent. It allows entrepreneurs to quickly gain temporary residency status based on their business plan, bypassing other requirements like capital or employment.

Lithuania’s startup ecosystem hosts over 100 tech and startup events every year, providing forums for networking, building partnerships, and exchanging ideas.

New facilities provide space for startups to work and for hosting events. The Vilnius Tech Park opened in 2016 and includes offices for established startups, a large coworking space, 31 meeting rooms, 3 event spaces, and a conference room that seats 250 people.

34

The Lithuanian startup ecosystem

35

Interview with Arvydas BlozeCEO at Startup.lt, and investment manager at early stage VC fund Practica Capital

How has the Lithuanian startup ecosystem changed in recent years?

The ecosystem is clearly maturing, there are over 320 active startups in Lithuania, employing about 1,500 people. It’s truly impressive, considering that five years ago “startup” was just a concept. Today Lithuania is enjoying its first startup success stories, like the Oberlo and TrackDuck exits, startups raising Series A,B,C, and heavyweight bootstrapped startups like Bored Panda and Pixelmator.

The country is pioneering in fintech regulation in the EU and front running in ICO fundraising. There is fairly visible success in the Lithuanian diaspora (startups that have gone abroad): AimBrain, Genus AI, and Medigo to name a few. We have close to one million Lithuanians living abroad, including solid professional networks in London, Stockholm, Berlin, New York and Silicon Valley.

The Lithuanian government is firmly taking the baton from the European Investment Fund, if you will, in using EU structural and local funds in instruments to facilitate entrepreneurship. Such measures include €120 million in public funds for accelerators, co-investment, VC and PE funds that have launched or will be launched in 2017-18, investing from pre-seed to growth stages. These funds will in turn attract at least 40% of private money, creating a multiplier effect. I have no doubt that Lithuania will become a point of gravity in the regional tech scene.

In 2017, the government also took a major interest in startup policy and investment conditions. We had a lot of changes in legislation to facilitate VC and PE infrastructure, with the government working closely with Lithuanian private and venture capital associations. Currently the government is working on a startup package to further facilitate the ease of kickstarting from Lithuania. When the StartupVisa programme was launched, it picked up interest from Belarussian, Ukrainian, Russian, Turkish and US teams. The Lithuanian Startup association was also formed in 2017, to give voice to startups’ interests in policy making.

What are some of the challenges you see in Lithuania’s startup ecosystem?

The talent pool. Lithuania is a small, export-driveneconomy, dominated by traditional sectors. Firstly,and very naturally, it implies a limitedunderstanding on how global market works in neweconomic sectors, where the real inefficiencies are,how exactly to resegment the market, etc.

Secondly, we have a young ecosystem and a firsttime founder generation that yet has to acquireexperience. Gladly, we are on a fast-track in doingso.

Thirdly, our talent pool is limited as competition ison a global market. The talent pool for startups isaffected by braindrain to Western countries andservice centres of big corporations (Barclays,Booking.com, etc) opening in Lithuania. I believe itis short-term problem, as on a long-term basis wewill see (and actually are already observing) peoplecome back to Lithuania with experience oracquiring it working in a big corporation locally.

Overall, we want to stress execution, and turningideas into business requires true grit from localfounders.

Funding levels haven’t increased in the past two years, why do you think this is?

The bigger numbers are Series A or B rounds,facilitated by foreign investors. The number of pre-seed and seed rounds is pretty stable year overyear and is provided by local capital. In 2016 weraised €5 million, as there was a gap in A and Brounds for several reasons. While in 2017 we have€10 million raised and counting, and an exceptional€100 million if ICOs are taken into account.

Local VC capital has to bring startups to a level where broader focus funds can pick them up. This means we have to seed, bridge, participate in Series A, and be patient. Very importantly, there are a whole bunch of startups in Lithuania that did not receive any funding but have had success –such as Bored Panda, Pixelmator, Omnisend, Tesonet, Nordcurrent, to name a few.

Interview with Arvydas Bloze cont’d…

“We have a young ecosystem and a first

time founder generation that yet has to acquire experience.

Gladly, we are on a fast-track in doing so.”

37

Interview with IljaLaurs, Founder of GetJar and Founder and CEO ofNextury Ventures

You have a lot of experience early on in the Lithuanian startup ecosystem, having launched GetJar in 2002. What was it like then and what is it like now?

In 2002 there was no ecosystem whatsoever. You either had a profitable business or you didn’t exist. In a way, this mentality helped us learn how to be strong. We have a strong community now, and multiple success stories. We now collaborate with fairly well known international VCs, such as Accel Ventures, and have several local VCs and government initiatives to support startups.

I think the ecosystem is going to grow 10x in terms of people and number of startups in the next 10 years.

Why do you expect it to grow so much?

Lithuania is a hungry country, because we have so little. There is a lot of incentive to work., and a really good attitude towards work here. People are also strongly educated.

How so?

The government started implementing IT education in schools in the early 2000s, and so everyone knows how to code, install Windows, and use photoshop.

What also helped was a strong a black market for software in Lithuania from 1995 to 2010, so every kid had access to any software they could want for a couple of dollars.

“I think the ecosystem is going to grow 10x in terms of people and number of

startups in the next 10 years.”

38

If you had complete control, and could do anything to improve or change the Lithuanian startup ecosystem, what would you do?

I have a lot of ideas – and I’m involved with many initiatives to make changes.

Firstly, we need to change our education system. Intellectual property created by students now belongs to the university. This needs to be changed. Millions of hours are spent creating ideas and programmes, which just turn into research papers, and universities own the patents - the students don’t have access to them. We need to make changes so that students can have access to their own intellectual property.

Universities have a lot of resources. They can more easily acquire a lot of EU funding, because they’re non-profit, to do research – this means bonuses, more jobs, creating more labs – but it doesn’t actually create anything except research papers.

We also must choose our priorities as an ecosystem, and focus on specific verticals, especially in fintech, or some other vertical, and focus on those – that is critical.

And in general, we need an institution devoted to innovation.

Also, our angel funding ecosystem is not functional. The UK has a great example for how tax incentives can encourage angel funding. Copying the UK model would be a big kick for the Lithuanian startup ecosystem.

Why have the Baltic states been so much more successful in creating startups than other Eastern European countries?

I think Skype had a big effect on Lithuania. Skype’s success has really changed people’s mentality, and made people think, “I can do this”.

Interview with Ilja Laurs, cont’d

“We need to make changes so that students can have

access to their own intellectual property.”

“Skype had a big effect on Lithuania. Skype’s success has

really changed people’s mentality, and made people

think, ‘I can do this’.”

39

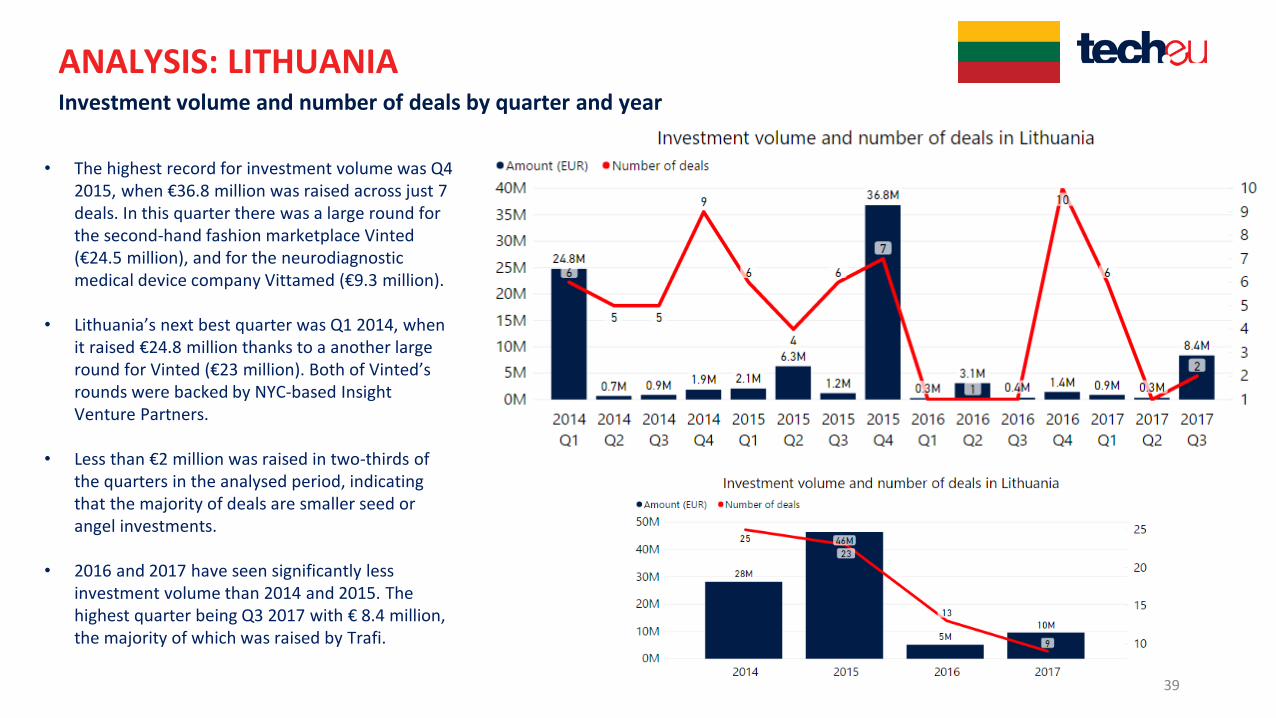

• The highest record for investment volume was Q4 2015, when €36.8 million was raised across just 7 deals. In this quarter there was a large round for the second-hand fashion marketplace Vinted(€24.5 million), and for the neurodiagnosticmedical device company Vittamed (€9.3 million).

• Lithuania’s next best quarter was Q1 2014, when it raised €24.8 million thanks to a another large round for Vinted (€23 million). Both of Vinted’srounds were backed by NYC-based Insight Venture Partners.

• Less than €2 million was raised in two-thirds of the quarters in the analysed period, indicating that the majority of deals are smaller seed or angel investments.

• 2016 and 2017 have seen significantly less investment volume than 2014 and 2015. The highest quarter being Q3 2017 with € 8.4 million, the majority of which was raised by Trafi.

ANALYSIS: LITHUANIAInvestment volume and number of deals by quarter and year

40

• In Lithuania the average round size was between €100,000 – 400,000 in two-thirds of the quarters, with a few outliers. The average round in Q1 2014 was almost €5 million, influenced heavily by the €23 million round for Vinted. Q2 2017 had an average of more than €5 million per round thanks to another round for Vinted, and two other large rounds for Vittamed and Trafi.

• The average round size in Lithuania is generally much lower than it is for the Baltics as a whole, which has an average of €1 million or more in most quarters.

• The median round size stayed below €360,000 for all quarters except for Q2 2016 and Q3 2017, which only had 1 or 2 deals. Most quarters had a median deal size of €200,000 or less, and is on par with the median quarter for the Baltics as a whole.

ANALYSIS: LITHUANIAAverage and median round sizes, 2014 – Q3 2017

41

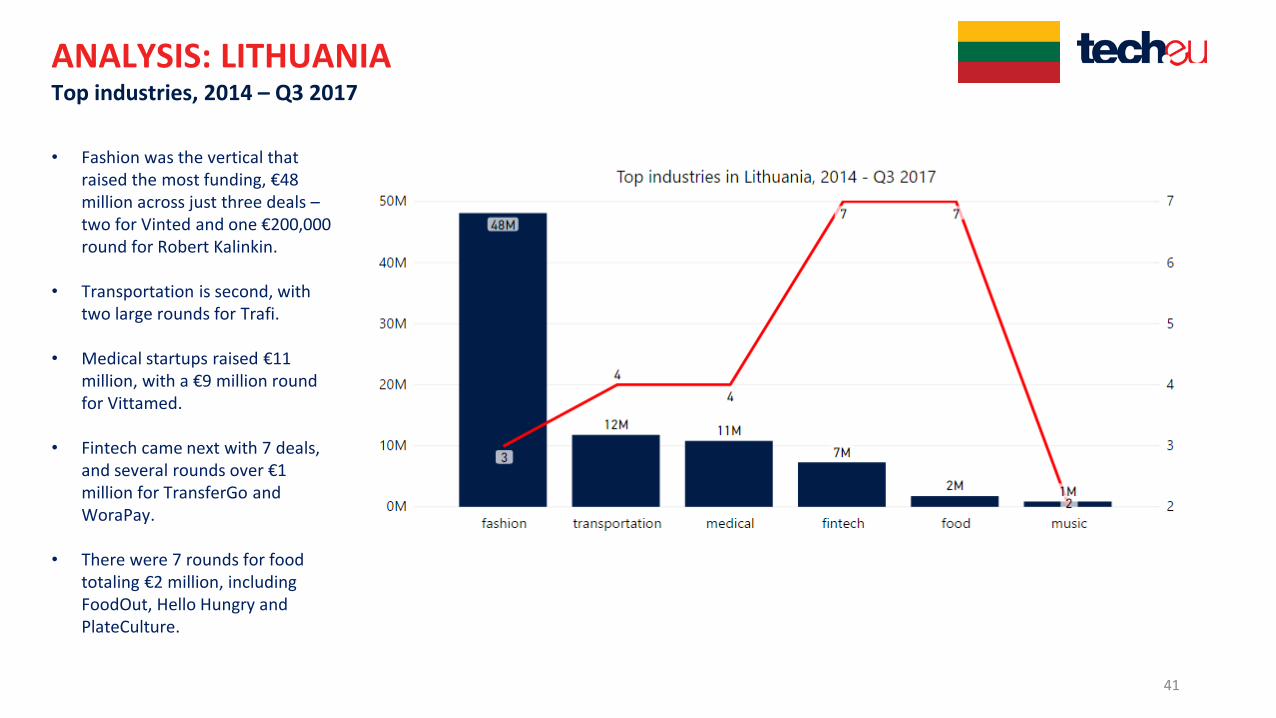

Top industries, 2014 – Q3 2017

ANALYSIS: LITHUANIA

• Fashion was the vertical that raised the most funding, €48 million across just three deals –two for Vinted and one €200,000 round for Robert Kalinkin.

• Transportation is second, with two large rounds for Trafi.

• Medical startups raised €11 million, with a €9 million round for Vittamed.

• Fintech came next with 7 deals, and several rounds over €1 million for TransferGo and WoraPay.

• There were 7 rounds for food totaling €2 million, including FoodOut, Hello Hungry and PlateCulture.

42

• The top deal by far for Lithuania in 2017 was for Trafi, a mobility app that connects different transportation options throughout a city, so users can better navigate their routes. Trafi raised €6 million in Q2 2017 in a Series B round from Octopus Ventures and the European Bank for Reconstruction and Development.

• The top round for 2016 was for TransferGo, which raised €3.1 milion from Vostok Emerging Finance (VEF). Next was RubedoSistemos, a robotics company, which raised €500,000.

• The next highest round in Lithuania was for Interactio, which provides real time audio broadcasting solutions, and raised €330,000. TutoTOONS, which creates mobile games for kids to foster imagination and creativity, raised €200,000.

• PlateCulture, a marketplace for homemade meals, raised €350,000.

• Top rounds were much smaller in Lithuania in 2017 and 2016 than in 2015 and 2014, with only two rounds of more than 1 million. No scale-ups such as Vinted or Integrated Optics raised major rounds of €20 million or more as they did in previous years.

ANALYSIS: LITHUANIATop rounds in Lithuania

Top rounds in Lithuania, 2017

Top rounds in Lithuania, 2016

43

• Lithuania’s top deals in 2015 and 2014 were for Vinted, a second-hand fashion marketplace. This scale-up raised €24.5 million from Accel Partners and Insight Venture Partners in Q4 2015 in a Series C round, and €23 million in Q1 2014 in a Series B round from the same investors.

• Vittamed, a neurodiagnostic medical company that develops ultrasound-based devices, raised €9 million Series A from Xeraya Capital in 2015.

• WoraPay, a fintech that allows retail customers to order and pay through their mobiles, thereby avoiding queues, raised €2 million in 2014.

• Integrated Optics, which develops lasers and sensors for spectroscopy and LiDAR technologies used for the manufacturing of highly integrated optical and electro-optical devices, raised €1.2 million in 2014.

Top rounds in Lithuania

Top rounds in Lithuania, 2015

Top rounds in Lithuania, 2014

ANALYSIS: LITHUANIA

44

• Lithuania’s top investor is Practica Capital, which has backed 23 deals in the country since 2014. The fund invests in early-stage startups, providing €3,000 to €2 million in capital per deal, though most of its investments are worth €200,000 or less. Startups backed by the fund include Trafi, TrackDuck, Interactio, Hello Hungry, Robert Kalinkin, Xylo, and TableAir.

• Lithuania-based Nextury Ventures was started by Ilja Laurs, the founder of one of country’s earliest startups, GetJar. Nextury has backed 4 startups in the analysed period: Baltic Arrow, Ekspertas.lt, Toyze, and Feedpresso. The VC was founded in 2013 and invests in early-stage startups.

• BaltCap is a private equity and venture capital investor in the Baltic states of Estonia, Latvia and Lithuania focusing investment on the growth of SMEs.

• Insight Venture Partners is the only non-European investor that made the top five. Based in New York since 1995, it has raised nine funds and invested in over 300 companies. Its investments are typically much larger than those of Baltic investors. In Lithuania, it has two rounds for Vinted.

Top investors in Lithuania, 2014 – Q3 2017

• Paris-based Kima Ventures is an active early-stage investor, making 2-3 investments per week. It has invested in over 400 companies in the past five years.

ANALYSIS: LITHUANIA

45

Notable Lithuanian startups

Vinted is a fashion tech startup launched in 2008 in Vilnius. It’s basically an online thrift shop - a marketplace and app where users can sell, buy, and swap secondhand clothing and accessories. It lets people get rid of clothing they used to love, or that just doesn’t fit anymore, and find good homes with people who will love the clothing just as much. The startup is one of the most successful in Lithuania, having raised over €50 million. It raised €20 million Series B in 2014 from Insight Venture Partners, and €23 million Series C from Burda Principal Investments.

“Vinted’s business model is perfectly scalable and will work in practically any country,” said Martin Weiss, Burda Media’s managing director. “We think Vinted can benefit from Burda’s focus on digital media and the international media market.”

The company says that 11 million girls and young women use the site every day, and spend about 45 minutes shopping and chatting with sellers. Vinted says it has made over $150 million in sales since it launched.

Trafi claims to be the “world’s most accurate public transport app”. It uses machine learning, crowdsourced data, and self-learning algorithms to help users plan their journeys and navigate through a city. The app combines information on all public transportation options - buses, trains, and trams - and has recently partnered with Uber to include ridesharing options. The app also locates your closest transportation hub, and provides schedules and arrival times.

Trafi raised $7 million from Octopus Investments and the European Bank for Reconstruction and Development in 2017, following a $6.5 million Series A round in 2015, also backed by Octopus Ventures. Unfortunately, the app is only available in a few countries – Brazil, Estonia, Latvia, Lithuania, Turkey, Taiwan, and Indonesia.

According to the company, it already has 250,000 users, and hopefully that number will grow as they expand to other countries with their new funding rounds.

46

Notable Lithuanian startups

TransferGo is a global money transfer company launched by Justinas Lasevičius, Daumantas Dvilinskas, Arnas Lukoševičiusand Edvinas Šeršniovas in 2012. The company provides low-cost international money transfers, especially targeting migrant workers sending money to their family, but also for other types of transactions, such as businesses paying international suppliers.

The company bypasses bank fees using a digital account-to-account business model, so money transfers do not have to leave the country as funds are paid in and out locally. It charges a low, fixed fee for transferring money and a 0.6% to 1.5% fee for the currency conversion per transaction. TransferGo now operates in 45 countries, handles over 1 million transactions per year and has transferred over 559 million to date. Since it removes the costs of international transfers,

Bored Panda is one of the most popular Lithuanian startups –though it has raised no funding. It’s a webzine full of creative articles, art, and photography. Its submission platform helps artists and writers turn their stories into viral content. It offers content related to art, photography, design, animals, travel, illustrations, DIYs, food art, architecture, parenting, and more. The platform was launched in 2009 by Tom Banišauskas, who was at the time a business management student at Vilnius University .

According to the startup, it has about 38 million readers, and a recent report by NewsWhip states that Bored Panda is one of the most popular sites on Facebook, ranking above CNN, the BBC, and the New York Times.

The company has an office in Vilnius Technology Park Vilnius Tech Park and employs 36 people, according to Wikipedia.

47

Notable Lithuanian exits

Oberlo is a marketplace that allows entrepreneurs to search for products to sell online. It allows online stores to easily run their business through dropshipping.

Oberlo connects merchants with suppliers, who send products directly to customers. Oberlo merchants have sold over 85 million products to customers around the world since it launched in September 2015.

In May 2017, the Oberlo was acquired by Canadian Shopify for $15 million, shortly after raising an undisclosed seed round.

TrackDuck simplifies collaboration on web development projects, by allowing users to easily give both visual and content feedback on live websites. TrackDuck can be integrated with other project management platforms. To give feedback on a website, a user can simply select an for improvement and leave a comment, which immediately goes to other management tools or web developers.

In May 2017, TrackDuck was acquired by InVision, a collaborative product design platform based in New York. The terms of the deal were undisclosed.

In January 2015, Lithuanian app development consultancy Lemon Labs was acquired by Wahanda, a UK-based online health and beauty marketplace, as part of their strategy to go mobile.

“We have been working with the Lemon Labs team for the past six months in building our consumer and business apps, and the results speak for themselves,” said Lopo Champalimaud, CEO and founder of Wahanda, as reported by Scratch Magazine. “Last week we broke through the 150,000 downloads mark, and that number is growing 20% month on month.”

Wahanda itself was acquired soon after in June 2015 by Recruit Co., an advertising, publication, and human resources company based in Tokyo.

48

Estonia

49

The Estonian startup ecosystem

Estonia has been called the “most advanced digital society in the world”.

As early as 1997, Estonia established e-Governance, allowing citizens to access many public services online, saving time and paperwork. In 2000, the country declared access to the internet a basic human right. In 2001 it created the Digital Identity Card, which all citizens use to access everything from transportation to their medical records. In 2005, the government started allowing citizens to vote online, the first country in the world to do so.

In 2014 Estonia launched e-Residency, letting anyone in the world apply to be an Estonian e-resident. The programmeme does not grant the right to live and work in Estonia, but allows e-residents to establish a business there from abroad and access certain e-services. However the new Startup Visa programmeme, implemented in early 2017, allows startup founders and employees to relocate to Estonia physically.

According to Startup Estonia, it takes only 15 minutes to set up a business in Estonia, and just 3 minutes to do the taxes.

Moreover, the corporate tax in Estonia is 0%, though dividends are taxed at 20%.

Estonia has been ranked #1 by the OECD for Tax Competitiveness, #1 from the World Economic Forum for Entrepreneurship, #1 for Barclays 2018 Digital Development Index, and #12 in the World Bank’s Global Ease of Doing Business ranking.

This background of a high-tech, digital society with low tax rates has made Estonia the Silicon Valley of Eastern Europe. Though funding levels trail behind many Western European countries, this is due to Estonia’s very small population of only 1.3 million people. When looking at investment volume on a per capita basis, Estonia ranks above the UK, Germany, and France.

In the next slides, Tech.eu interviews Kadi-Ingrid Lilles from Startup Estonia and Ragnar Saas, co-founder of Pipedrive, to share their thoughts on the Estonian startup ecosystem.

Top startups

50

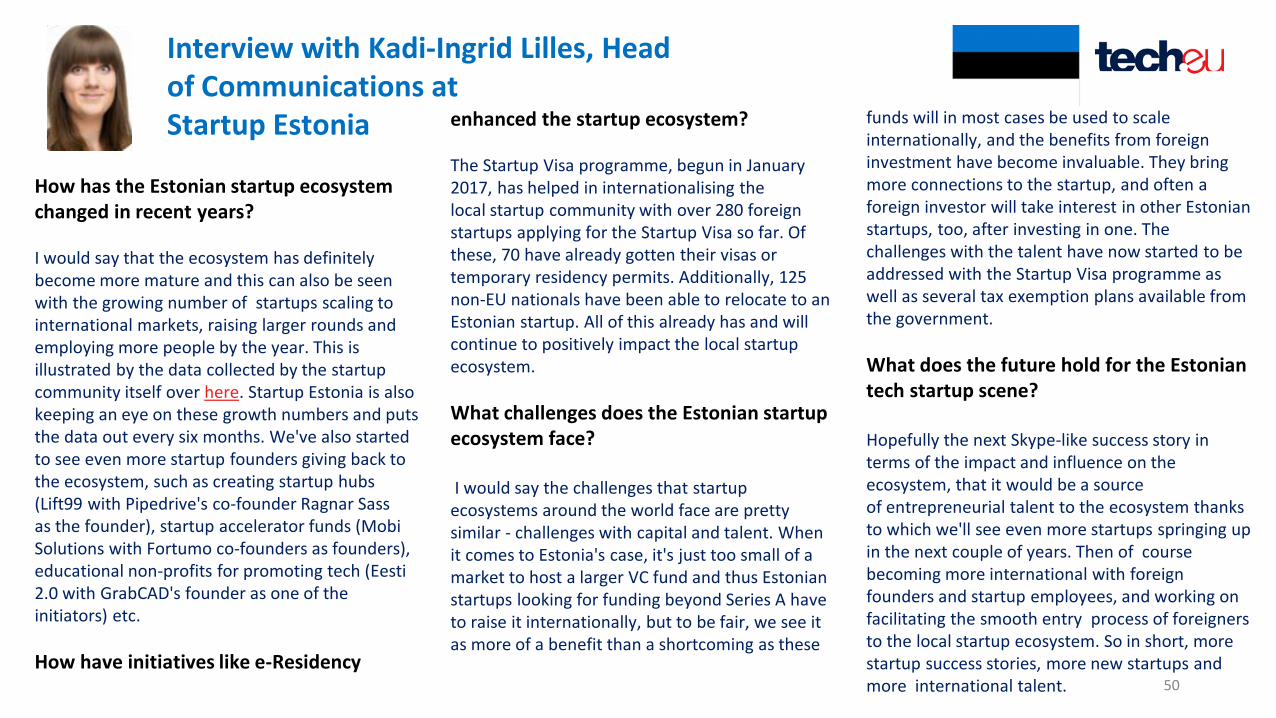

How has the Estonian startup ecosystem changed in recent years?

I would say that the ecosystem has definitely become more mature and this can also be seen with the growing number of startups scaling to international markets, raising larger rounds and employing more people by the year. This is illustrated by the data collected by the startupcommunity itself over here. Startup Estonia is also keeping an eye on these growth numbers and puts the data out every six months. We've also started to see even more startup founders giving back to the ecosystem, such as creating startup hubs (Lift99 with Pipedrive's co-founder Ragnar Sass as the founder), startup accelerator funds (MobiSolutions with Fortumo co-founders as founders), educational non-profits for promoting tech (Eesti2.0 with GrabCAD's founder as one of the initiators) etc.

How have initiatives like e-Residency

enhanced the startup ecosystem?

The Startup Visa programme, begun in January 2017, has helped in internationalising the local startup community with over 280 foreign startups applying for the Startup Visa so far. Of these, 70 have already gotten their visas or temporary residency permits. Additionally, 125 non-EU nationals have been able to relocate to an Estonian startup. All of this already has and will continue to positively impact the local startupecosystem.

What challenges does the Estonian startupecosystem face?

I would say the challenges that startupecosystems around the world face are pretty similar - challenges with capital and talent. When it comes to Estonia's case, it's just too small of a market to host a larger VC fund and thus Estonian startups looking for funding beyond Series A have to raise it internationally, but to be fair, we see it as more of a benefit than a shortcoming as these

funds will in most cases be used to scale internationally, and the benefits from foreign investment have become invaluable. They bring more connections to the startup, and often a foreign investor will take interest in other Estonian startups, too, after investing in one. The challenges with the talent have now started to be addressed with the Startup Visa programme as well as several tax exemption plans available from the government.

What does the future hold for the Estonian tech startup scene?

Hopefully the next Skype-like success story in terms of the impact and influence on the ecosystem, that it would be a source of entrepreneurial talent to the ecosystem thanks to which we'll see even more startups springing up in the next couple of years. Then of course becoming more international with foreign founders and startup employees, and working on facilitating the smooth entry process of foreigners to the local startup ecosystem. So in short, more startup success stories, more new startups and more international talent.

Interview with Kadi-Ingrid Lilles, Head of Communications atStartup Estonia

51

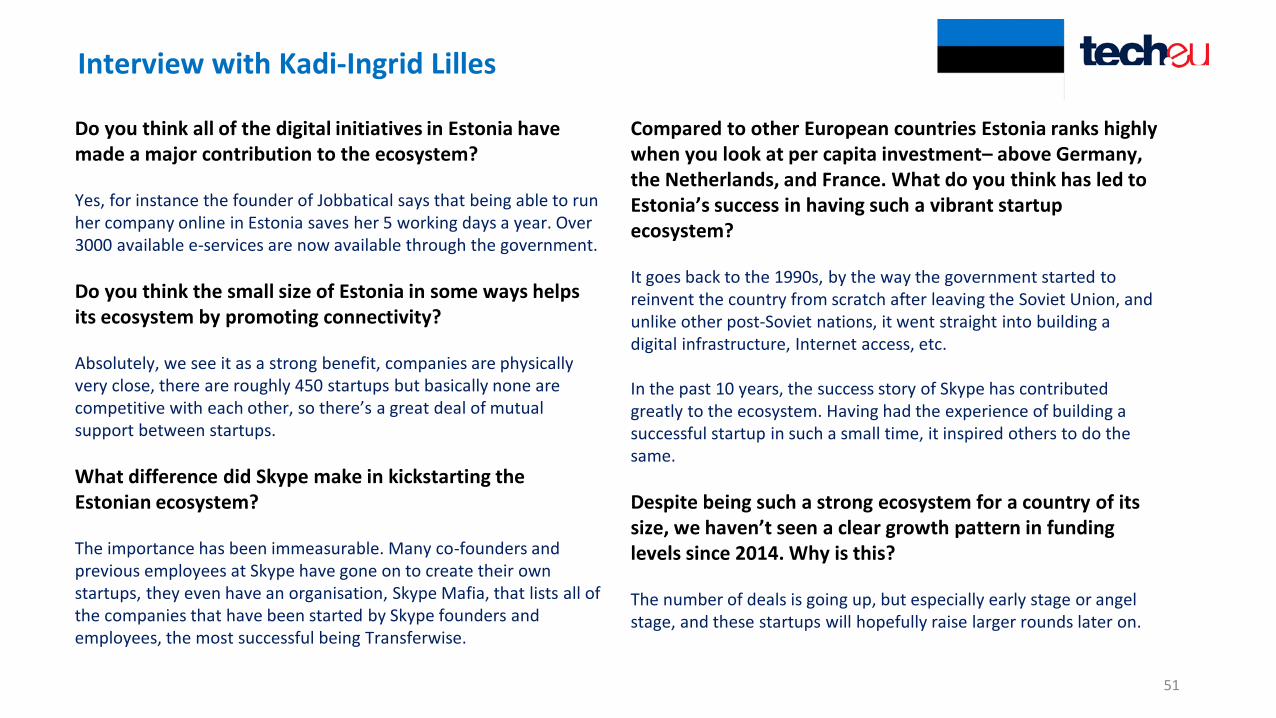

Do you think all of the digital initiatives in Estonia have made a major contribution to the ecosystem?

Yes, for instance the founder of Jobbatical says that being able to run her company online in Estonia saves her 5 working days a year. Over 3000 available e-services are now available through the government.

Do you think the small size of Estonia in some ways helps its ecosystem by promoting connectivity?

Absolutely, we see it as a strong benefit, companies are physically very close, there are roughly 450 startups but basically none are competitive with each other, so there’s a great deal of mutual support between startups.

What difference did Skype make in kickstarting the Estonian ecosystem?

The importance has been immeasurable. Many co-founders and previous employees at Skype have gone on to create their own startups, they even have an organisation, Skype Mafia, that lists all of the companies that have been started by Skype founders and employees, the most successful being Transferwise.

Compared to other European countries Estonia ranks highly when you look at per capita investment– above Germany, the Netherlands, and France. What do you think has led to Estonia’s success in having such a vibrant startup ecosystem?

It goes back to the 1990s, by the way the government started to reinvent the country from scratch after leaving the Soviet Union, and unlike other post-Soviet nations, it went straight into building a digital infrastructure, Internet access, etc.

In the past 10 years, the success story of Skype has contributed greatly to the ecosystem. Having had the experience of building a successful startup in such a small time, it inspired others to do the same.

Despite being such a strong ecosystem for a country of its size, we haven’t seen a clear growth pattern in funding levels since 2014. Why is this?

The number of deals is going up, but especially early stage or angel stage, and these startups will hopefully raise larger rounds later on.

Interview with Kadi-Ingrid Lilles

52

What is your experience in the Estonian ecosystem?

My first startup began in 2007, it was called United Dogs, which is like Facebook but for dog and cat owners. Later I became of the founders of Pipedrive, which has been named the best B2B startup from Europe by TechCrunch. We already have 50,000 customers, and Pipedrive was named the best employer in Estonia in 2016. In 2010 I started Garage48 Foundation with 4 other startup entrepreneurs , which organizes hackathons in Eastern Europe and developing countries. We have held more then 80 hackathons and our most successful alumni is MSQRD, what was sold to Facebook 3 months later with more then $100 million.

The main objective of a hackathon is to bring together professionals and engineers. The idea is for participants to get the sense of what it would feel like to start your own company, and to learn about startups.

Last year we moved this to the next level, I founded Lift99, a startupfounders community, coworking and event space.

Our aim is to help this movement, to connect experienced founders with talented people, who have a lot of drive to startup new companies. If we connect experience and young energy - miracles will start to happen.

Estonia is different because Estonian founders strive to give back to the community. This is something I haven’t found in other countries.

How have you seen Estonia’s startup ecosystem change over the years?

We are such a small country that the government has been doing things to help us. They are looking at who we should give a Startup Visa to and who we should not. Over a thousand companies have been opened because of e-Residency. You can do everything online and it really helps the ecosystem.

As I mentioned, there is also a lot of giving back to the ecosystem. For example, one successful entrepreneur started a nonprofit in Boston that is now giving 3D printers to Estonian schools.

I think startups are becoming more popular, you used to only hear about Skype, but now many more as we’ve seen much more of a variety of ideas, we’ve seen that Taxify can be competitive with Uber. We look at how much tax startups have been paying in Estonia, and it goes up every year 50-60%, I’m sure that in the next few years we will see 3 or 4 new unicorns from Estonia.

Interview with Ragnar Sass, Co-founder of Pipedrive and Garage48, Founder of Lift99

53

I’ve heard that Estonia is too small to support large VCs, and the majority of Estonian startups are dependent on accelerators or angel funding, or have to look for foreign investment. Do you think this will change?

If you look at the statistics 90% of funding is from outside of Estonia. We have to understand that we need foreign funding, and because we depend on foreign customers it is important for us to be thinking internationally from the beginning. I have seen more and more foreign VCs taking interest in Estonia. We have to go pitch to investors in Berlin, London, New York. What has changed totally in the past 10 years is that we see a lot more experienced angels.

Looking at the data on funding per quarter in Estonia, there’s no real trend as quarters seem to fluctuate, and there’s no correlation between the number of deals and investment volume. Why do you think this is?

The numbers we have in Estonia depend on a few outliers, so we have to look at the numbers on an annual basis.

How did the government help when you were building Pipedrive?

I don’t think the government can do much, I think it’s entrepreneurs who help each other and build an ecosystem.

What government can do is support entrepreneurship. I would encourage people to check out foreign accelerators like YCombinator. Pipedrive was successful because we became active in accelerators in Silicon Valley.

I spoke to one man whose parents were working in IT in the 80s… so in a way you could say the Soviet Union actually helped Estonia evolve digitally, because they had made some technological advancements.

What do you see for the future of the Estonian startupecosystem?

I think because of the Startup Visa and e-residency we will see many more startups coming from foreigners. The amount of people who have experience with successful companies is doubling, and they can help new startups. We have been attracting people from neighbouring countries like Russia, Belarus, and Ukraine, where they can have access to the EU.

Interview with Ragnar Sass, cont’d…

54

• Estonia showed much higher investment volume per quarter than Latvia or Lithuania. Estonia’s average quarter over the analysed period is €18.8 million.

• The data shows no clear growth pattern in the analysed period. Investment volume and number of deals do not correlate, and fluctuate greatly from quarter to quarter. For example, €80 million was raised in Q2 2015 across just 9 deals, but only €2.3 million was raised in Q2 2017 across 21 deals, the highest number of any quarter in our analysis.

• As in the Baltics as a whole, high volume quarters tend to depend on one or two large deals, while the majority of deals are worth €500,000 or less.

ANALYSIS: ESTONIA

55

• Both the average and median round sizes for Estonia tend to be larger than the Baltics as a whole, suggesting that Estonian startups raise bigger rounds than Latvia and Lithuania.

• Median round sizes for Estonia were of 500,000 or less, with one outlier of 770,000.

• In 8 of the quarters, the median was at or above 350,000, while in 7 of the 15 quarters more than half of the rounds were worth less than 200,000. • However, average round size in

Estonia is less than half of the average round size for Europe as a whole of 5.2 million. Median round size as well is less than half of the median round size for Europe.

• Average and median round size in Estonia show no growth trend in the analysed period, meaning that deal size is not rising.

56

Top industries, 2014 – Q3 2017

ANALYSIS: ESTONIA

• The top vertical in Estonia was by far fintech, with €114 million raised across 23 deals. Estonian fintechs include Bondoroa, Funderbeam, Investly, LeapIn, Paytailor, and TransferWise.

• Marketing startups brought in €20 million across 8 deals, including startups like Adcash, Clipman, SorryasaService, and Promo Republic.

• €16 million was raised for robotics by Starship Technologies.

• Developer tools raised €12 million for ZeroTurnaround and High Mobility.

• Analytics raised €9 million across 24 deals – the most of any vertical. Estonian analytics startups include Nordic Automation Systems, Planet OS, Spectx, and TeamScope.

57

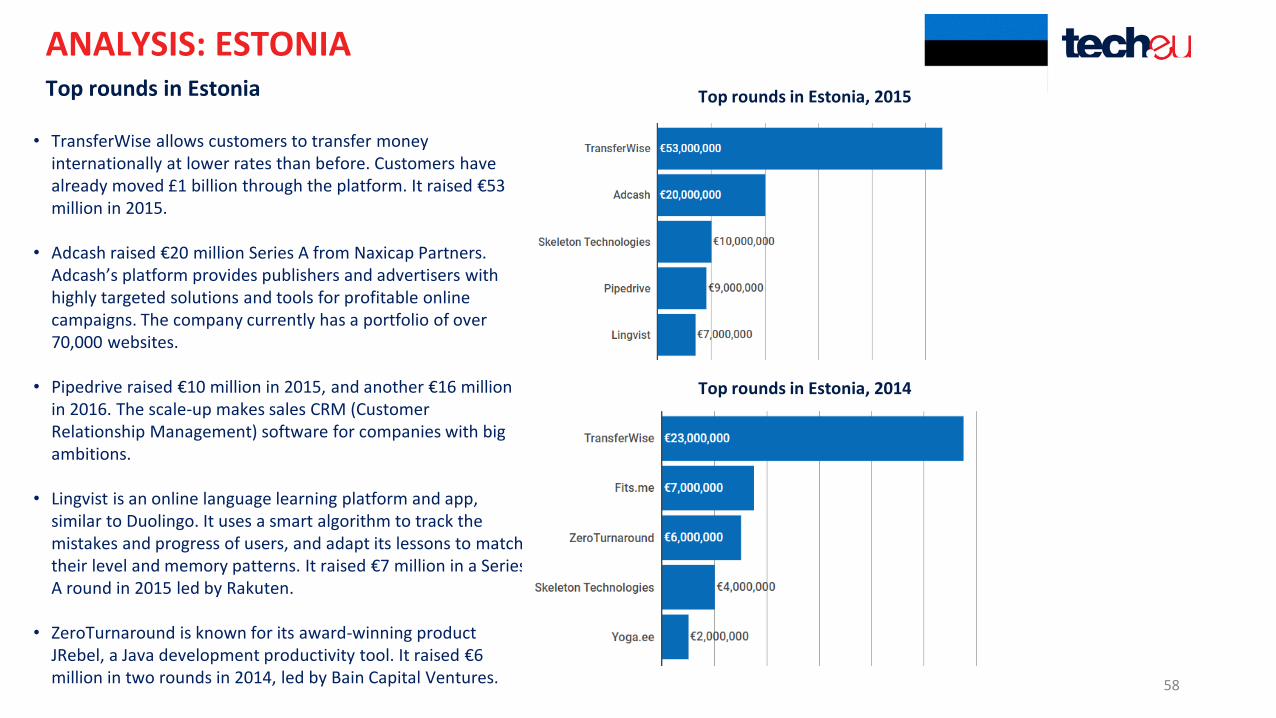

Top rounds in Estonia, 2017

Top rounds in Estonia, 2016

• Starship Technologies raised the highest round in Estonia in 2017, raising €16 million in a seed round led by Daimler. Starship is building a fleet of self-driving delivery robots that can deliver food and other goods locally within 30 minutes and potentially upend the delivery market.

• Jobbatical is platform for job recruitment and job seekers, especially those looking to relocate to new countries. It has recently moved into scale-up territory, raising €3 million in 2016 in two different seed rounds, and another €3.4 million Series A in 2017 from Mistletoe.

• TransferWise has already reached European unicorn status, with a valuation of €1.6 billion. The company just raised $280 million in Series E funding from numerous investors in Q4 2017 – which, unfortunately, is left out of our analysis. However it also led Estonia in 2016, 2015, and 2014 – though their deals in these quarters don’t approach the $280 million raised in its Q4 2017 round.

• Skeleton Technologies creates ultracapacitors and energy-storage systems to deliver high energy, reliable and long-life storage solutions across industries. It raised €17 million across two rounds in 2016, after raising €10 million in 2015. The company works with global engineering companies including the European Space Agencies and car manufacturers.

ANALYSIS: ESTONIATop rounds in Estonia

58

Top rounds in Estonia, 2015

Top rounds in Estonia, 2014

• TransferWise allows customers to transfer money internationally at lower rates than before. Customers have already moved £1 billion through the platform. It raised €53 million in 2015.

• Adcash raised €20 million Series A from Naxicap Partners. Adcash’s platform provides publishers and advertisers with highly targeted solutions and tools for profitable online campaigns. The company currently has a portfolio of over 70,000 websites.

• Pipedrive raised €10 million in 2015, and another €16 million in 2016. The scale-up makes sales CRM (Customer Relationship Management) software for companies with big ambitions.

• Lingvist is an online language learning platform and app, similar to Duolingo. It uses a smart algorithm to track the mistakes and progress of users, and adapt its lessons to match their level and memory patterns. It raised €7 million in a Series A round in 2015 led by Rakuten.

• ZeroTurnaround is known for its award-winning product JRebel, a Java development productivity tool. It raised €6 million in two rounds in 2014, led by Bain Capital Ventures.

ANALYSIS: ESTONIATop rounds in Estonia

59

• Startup Wise Guys, an accelerator based in Tallinn, has backed the most rounds in Estonia since 2014. Startup Wise Guys typically provides seed investments of €20,000. It also offers mentoring and office space to new startups.

• The next most active Estonian investor is Jaan Tallinn, a programmemer and physicist who co-founded Skype in 2002, and has funded 11 Estonian startups since 2014, including Fleep, Shipitwise, and Plumbr.

• SmartCap is a government held fund of funds supporting the development of the Estonian economy, that manages the early stage venture capital fund Early Fund II. It has €40 million in assets under management. SmartCap has decided on a strategy to make new investments into early stage venture capital funds, or accelerators. It has invested in Jobbatical, Vitalfields, Fits.me, Lingvist, and the accelerator Startup Wise Guys.

ANALYSIS: ESTONIA

60

Notable Estonian startups

Testlio helps companies to improve their products and their customers’ experiences by testing products for quality assurance before they go to market. It has a growing customer base and already has some major clients including Microsoft. Testlio tests iOS, Android, web, and desktop applications.

According to the company’s website, it’s mission is to “Connect enterprises with the best testers in the world to provide amazing customer experiences.”

The company was founded in 2012 by the tester couple Kristel and Mark Kruustük. It raised €6 million Series A led by Vertex Ventures in 2016, after a €900,000 seed round in 2015.

Taxify was launched in 2013 in Tallinn, and is one of the fastest growing companies in Europe and Africa with over 3 million customers in more than 20 countries. Taxify was founded in Estonia in 2013 as a market-leading platform connecting riders to private drivers or licensed taxis.

Taxify has steadily grown its Uber-like service across Europe and in Africa, fuelled by €2 million in funding and a recent undisclosed financing boost from Didi Chuxing, the Chinese ride-sharing giant.

61

Deekit is a virtual whiteboard, which allows real-time collaboration between remote teams or individuals to work together on projects. The whiteboard can also be used in meetings to show and discuss ideas with stakeholders. Users can add various forms of content, including drawing, text, and images.

The platform provides templates for specific uses such as marketing or business plans. was the winner of “Estonia’s Best Early Stage Startup” in 2016. Deekit has been enjoying international success ever since. Besides the winning investment, the company has raised an additional €468,940 investment, received international recognition and was named the finalist at the StartupEurope Awards.

Sprayprinter is a smart spray can technology which prints pictures from smartphones to different surfaces. For that, users need a SprayPrinter, the smartphone app and spray cans. The phone tracks movements of the printer and tells it when to release paint and when not.

SprayPrinter was founded in 2015 and is based in Tartu. The young company did a successful global crowdfunding campaign on Indiegogo which resulted with over 200 pre-orders and massive amount of inquiries from retailers, promoters and strategic partners.

Notable Estonian startups

62