Introduction of Chinese Debt Capital Market From...

23

Introduction of Chinese Debt Capital Market From Private Sector Perspective December 2009 Presented To: ABMI Conference CITIC Securities Corporation Limited

Transcript of Introduction of Chinese Debt Capital Market From...

Introduction of Chinese Debt Capital Market From Private Sector Perspective

December 2009

Presented To: ABMI Conference

CITIC Securities Corporation Limited

Contents

Part 1 OVERVIEW OF DEBT MARKET

Part 2 BOND INSTRUMENTS AND MAJOR BREAKTHOUGH IN CHINA

Part 3 CHINESE MARKET PLAYERS

Part 4DESIRABLE DEVELOPMET IN THE FRUTURE

- FROM PRIVATE SECTOR PERSPECTIVE

Table of Contents

PART 1

OVERVIEW OF DEBT MARKET

1.1 Overview

1.2 History

1.3 List of Debt Financing Instruments

1.4 Market Statistics

3

China debt capital market has been experiencing fast development for the past decade

The total volume of innovation for debt instruments has hit a record high

Encouraged by dynamic innovation of Chinese regulators, the private sector has been fervently devoted to producing new instruments while expanding existing business.

Comparison of Issuance Volume of Major Debt Instruments

1.1 Overview

Source: Chinabond

0

100

200

300

400

500

600

700

800

900

1000

RM

B B

illio

n

2006 2007 2008 Jan-Oct2009

MTN&CP Corporate Bond Listed Company Corporate Bond

4

1.2 History of Opening Debt Market

2007

2005

2003

1982 The first issuance of International Bond by China’s financial institution in the international

capital market.

1985 The first bond issuance by commercial banks in China.

1987 The first issuance of domestic bond issued by Chinese corporate.

The first issuance of US Dollar bond by China Development Bank in China.

The first issuance of Commercial Paper in China.

Panda bonds issued by approved supranational organizations in China

China's first introduction of QFII¹ into the inter-bank bond market.

China‘s first introduction of ABS & MBS.

The first issuance of Listed Corporate Bond in China.

Recent China-US strategic economic dialogues announced permission for foreign banks to issue

bonds in RMB in China.

1. QFII: Qualified Foreign Institutional Investors5

1.2 History of Opening Debt Market (Continued)

April 2009

Dec 2008 The first issuance of Medium Term Note by 7 corporations in China.

The ‚30-point proposal‛ by State Council promised to study the feasibility of allowing foreign

institutions and enterprises to issue RMB bonds.

The State Council’s document on building Shanghai into international financial center also

declares boosting foreign entities to issue bonds.

The first issuance of Medium Term Note in US Dollar in China.

The successful RMB bonds issuance by HSBC China and BEA China in Hong Kong on 25th

and 30th of June heralds the policy to allow RMB bonds by foreign banks in mainland China.

May 2009

June 2009

6

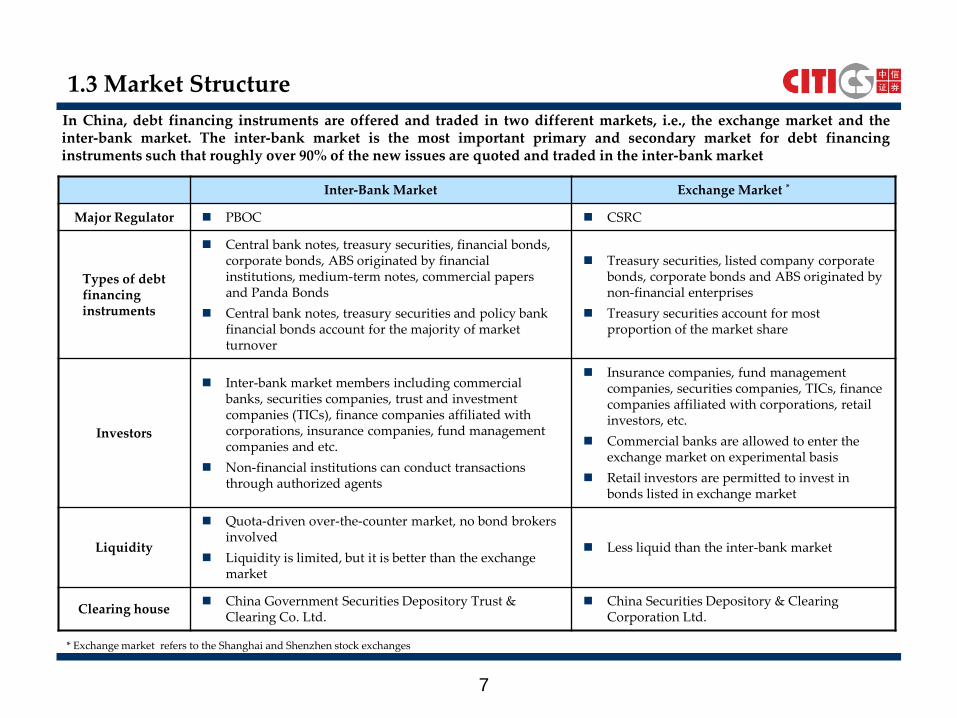

1.3 Market Structure

In China, debt financing instruments are offered and traded in two different markets, i.e., the exchange market and theinter-bank market. The inter-bank market is the most important primary and secondary market for debt financinginstruments such that roughly over 90% of the new issues are quoted and traded in the inter-bank market

Inter-Bank Market Exchange Market *

Major Regulator PBOC CSRC

Types of debt financing instruments

Central bank notes, treasury securities, financial bonds, corporate bonds, ABS originated by financial institutions, medium-term notes, commercial papers and Panda Bonds

Central bank notes, treasury securities and policy bank financial bonds account for the majority of market turnover

Treasury securities, listed company corporate bonds, corporate bonds and ABS originated by non-financial enterprises

Treasury securities account for most proportion of the market share

Investors

Inter-bank market members including commercial banks, securities companies, trust and investment companies (TICs), finance companies affiliated with corporations, insurance companies, fund management companies and etc.

Non-financial institutions can conduct transactions through authorized agents

Insurance companies, fund management companies, securities companies, TICs, finance companies affiliated with corporations, retail investors, etc.

Commercial banks are allowed to enter the exchange market on experimental basis

Retail investors are permitted to invest in bonds listed in exchange market

Liquidity

Quota-driven over-the-counter market, no bond brokers involved

Liquidity is limited, but it is better than the exchange market

Less liquid than the inter-bank market

Clearing house China Government Securities Depository Trust &

Clearing Co. Ltd. China Securities Depository & Clearing

Corporation Ltd.

* Exchange market refers to the Shanghai and Shenzhen stock exchanges

7

1.4 Market Statistics

The bond market developed fast in 2007 and 2008

The issuance of central bank notes and treasuries in 2008 declined since the government withdrew less money

through open-market transaction in economic downturn

Active fiscal policy and loosen monetary policy will keep the supply aloft levels of previous years

Coupling with macro economic rebound and the expectation of inflation, yield curve therefore is expected to

rise and become flatter

Commercial banks will still be the primary investor, despite demand has somewhat dropped as regulators

begin to concern about excessive liquidity and potential inflation

Source: Chinabond

New Bond Issuance in 2007, 2008 and 2009 Jan-Oct

2007 2008 2009 Jan-Oct

Class TermsVolume

(billion yuan)Terms

Volume(billion yuan)

TermsVolume

(billion yuan)

Central Bank Note 143 4,072 122 4,296 63 3,257

Treasury Securities 30 2,188 29 725 105 1,375

Financial Bond 95 1,191 85 1,178 83 1,155

Corporate Bond 89 172 71 237 153 311

Commercial Paper 263 335 269 434 211 368

Asset Backed Securities 16 18 26 30 0 0

MTN -- -- 41 174 141 572

Total 636 7,976 643 7,074 756 7,038

8

PART 2

BOND INSTRUMENTS AND MAJOR BREAKTHOUGH IN CHINA

2.1 Traditional Debt Instruments

2.2 Major Breakthrough

9

2.1 Traditional Debt Instruments

10

TypesApplicable

Regulator(s)Eligible Issuers Launch Date

Amount Issued Since Introduction(Up to end of October 2009)(RMB Billion)

Central Bank Note PBOC PBOC January 2007 3,664.5

Treasury Securities(1)

PBOC, CSRC (for Exchange Market issuance), MOF

MOF August 1998 12,301.39

Policy Bank Financial Bonds

PBOC Policy banks December 1999 4,457.15

Financial Bond

(including policy bank financial bonds)

PBOC

Commercial banks(2),

financial companies affiliated with corporations,

other financial institutions

December 2001 628.85

Corporate BondNDRC, PBOC, and CSRC

PRC enterprises July 2000 1,267.65

Listed Company Corporate Bond

CSRC Listed companies September 2007 91.3

Asset-Backed Securities

PBOC, CBRC, CSRC

Originators: financial institutions supervised by CBRC, non-financial institutions supervised by CSRC

December 2005 60.98

(1) Treasury securities can be issued on either the Exchange Market or the Inter-bank Market or in both. The two markets used to have two different underwriting groups. Starting in late 2004, most treasury securities are issued in both markets concurrently.

(2) In theory, commercial banks include the PRC incorporated subsidiaries and branches of foreign banks.

2.2 Major Breakthrough – Commercial Paper

11

Regulator/SRO

Market Data

Issuer

Governing Law

PBOC, NAFMII

Legal registered non-financial institutions which are NAFMII corporate members

Until the end of October, 2009, there were 233 Commercial Paper issued in the market with a total size of RMB 418.71 billion

Commercial paper program was launched in 2005 by PBOC The introduction of commercial paper in Chinese capital market inaugurated a new channel of debt financing forenterprises NAFMII, a self disciplined non-profit association of institutional investors in the financial industry was founded in2007 and is under the direct control of the PBOC. The NAFMII takes over the responsibilities of regulatingcommercial paperNAFMII is considered as a very open-minded regulatory SRO and is devoted to market innovations

By PBOC:- Commercial Paper Management Regulation (PBOC Order No.2, 2005)- Regulation On Debt Financing Instruments for Non-financial Institutions in the Inter-bank Debt Market (PBOC Order No.1, 2008)

By NAFMII- Commercial Paper Guidelines- Information Disclosure Rules- Self-Discipline Guidelines for Intermediaries - Due Diligence Guidelines- Prospectus Guidelines- Membership Registration Guidelines

2.2 Major Breakthrough – MTN

12

Regulator/SRO

Market Data

Issuer

Governing Law

By PBOC:- Regulation on Debt Financing Instruments for Non-financial Institutions in the Inter-bank Debt Market (PBOC Order No.1, 2008)- Rules on the Registration of Debt Financing Instrument

By NAFMII- Medium Term Note Guidelines - Information Disclosure Rules- Self-Discipline Guidelines for Intermediaries - Due Diligence Guidelines- Prospectus Guidelines- Membership Registration Guidelines

PBOC, NAFMII

Legal registered non-financial institutions which are NAFMII corporate members

Since its introduction, 183 MTNs with a total amount of RMB 747.1 billion have been issued in the market up to the end of October 2009

On 15th April, 2008, Regulation on Debt Financing Instruments for Non-financial Institutions in the Inter-bankDebt Market (PBOC Order No.1, 2008) was issued. On the same day, Medium Term Note Guidelines and other sixself-disciplined rules was released by NAFMIIAt the end of June, MTN was suspended, until which there were 75.5 billion MTNs issued by 15 institutions. Starting from Oct. 6th, NAFMII, as allowed by PBOC, resumed accepting registration applications of non-financialcorporations for issuing MTN

2.2 Major Breakthrough – Collective Note

13

Regulator/SRO

Market Data

Issuer

Governing Law

PBOC, NAFMII

Small and medium legally registered non-financial institutions The collective issuer shall compose at least two companies and no more than 10 companies

Since its introduction, three collective notes with a total amount of RMB 1.265 billion have been successfully issued in the market

Collective note was introduced to Chinese market in November 2009 by NAFMII

So far, three pilot collective notes have got the registration approval of NAFMII

The launch of collective note program explored a new funding channel for SMEs

By PBOC:- Regulation on Debt Financing Instruments for Non-financial Institutions in the Inter-bank Debt Market (PBOC Order No.1, 2008)- Rules on the Registration of Debt Financing Instrument

By NAFMII- Collective Note Guidelines - Information Disclosure Rules- Self-Discipline Guidelines for Intermediaries - Due Diligence Guidelines- Prospectus Guidelines- Membership Registration Guidelines

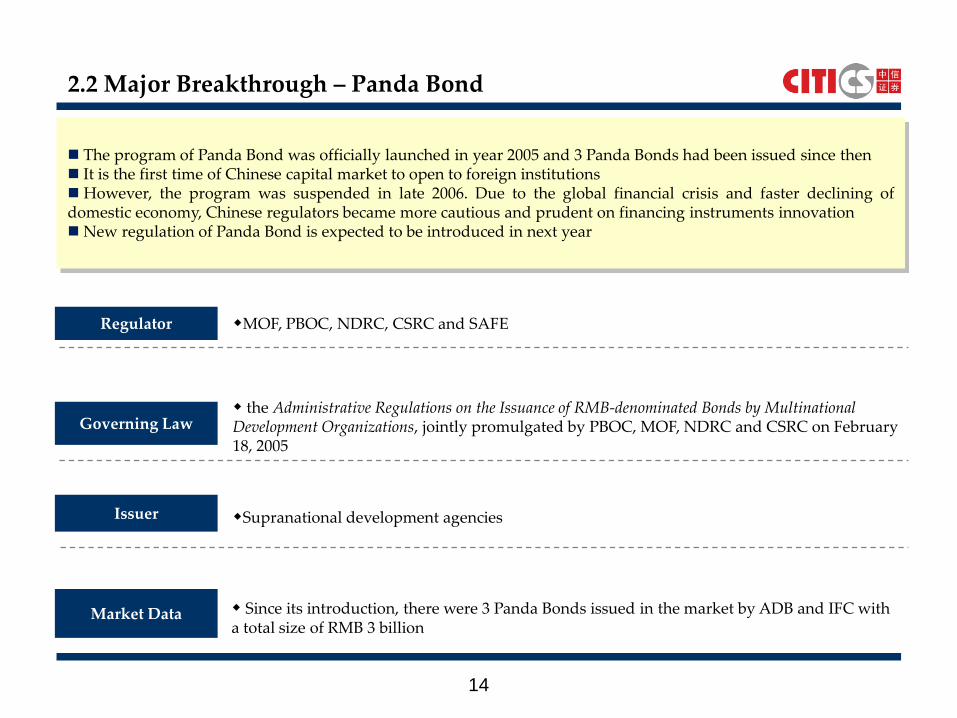

2.2 Major Breakthrough – Panda Bond

14

Regulator

Market Data

Issuer

Governing Law the Administrative Regulations on the Issuance of RMB-denominated Bonds by Multinational Development Organizations, jointly promulgated by PBOC, MOF, NDRC and CSRC on February 18, 2005

MOF, PBOC, NDRC, CSRC and SAFE

Supranational development agencies

Since its introduction, there were 3 Panda Bonds issued in the market by ADB and IFC with a total size of RMB 3 billion

The program of Panda Bond was officially launched in year 2005 and 3 Panda Bonds had been issued since then It is the first time of Chinese capital market to open to foreign institutions However, the program was suspended in late 2006. Due to the global financial crisis and faster declining ofdomestic economy, Chinese regulators became more cautious and prudent on financing instruments innovationNew regulation of Panda Bond is expected to be introduced in next year

2.2 Major Breakthrough – Offshore RMB Bond

15

Regulator

Market Data

Issuer

Governing Law Regulation on RMB Bond Issuance of Domestic Financial Institutions in Hong Kong SAR, jointly promulgated by PBOC and NDRC on June 8, 2007

Hong Kong: FSCMainland China: PBOC, NDRC, SAFE

Domestic Financial Institution

Since June 2007, a total 11 terms of offshore RMB bonds were issued in Hong Kong and raised RMB 31 billion The RMB bonds in Hong Kong were issued by two policy banks (which are China Development Bank and the EXIM Bank) , three state-owned commercial banks (which are Bank of China, China Construction Bank and Bank of Communications) and two locally incorporated foreign banks (which are HSBC Bank China and BEA China)

The offshore RMB bond was introduced in 2007 and the first offshore RMB bond by China Development Bank wasissued in Hong Kong Both policy banks and big state-owned banks have successfully issued RMB bonds in Hong Kong In 2009, HSBC Bank (China) issued an offshore RMB bond in Hong Kong. It was the first time for a locallyincorporated foreign commercial bank to issue RMB bond in offshore market The RMB Bond issued in Hong Kong by HSBC Bank (China) is a landmark deal with its contribution to theopening of Chinese debt market and the establishment of the synergy between Chinese capital market and HongKong market

PART 3

CHINESE MARKET PLAYERS

3.1 Underwriters

3.2 Investors

16

3.1 Underwriters

17

Central Bank Notes

Treasury Securities

Financial Bond(including

policy bank financial bonds)

Corporate Bond(1)

Listed Corporate

BondMTN/CP(2) ABS

Panda Bond

Securities Houses

Commercial Banks

Policy Banks

Trust and Investment Companies

(1) Only securities houses and China Development Bank are eligible to underwrite corporate bond(2) 24 commercial banks and 2 securities houses (CITICS and CICC) approved by NAFMII are eligible to underwrite MTN/CP

In China, securities houses are the most important underwriters in bond market Commercial banks, some policy bank and trust and investment companies are also eligible for specific bondsunderwriting given regulatory approval

3.2 Investors

18

As of the end of October, 2009, the total bond depository balance in the inter-bank market was RMB 16,690.247billion, while the number was only RMB 278.867 billion in the exchange market Commercial banks are major bond investors and holding more than half of the bonds in the market. However,commercial banks are not allowed to enter exchange market by current regulation

Inter-Bank Market Exchange Market

Investors Base

Commercial banks, insurance companies, securities companies, fund management companies, trust and investment companies, finance companies affiliated with corporations

Insurance companies, securities companies, fund management companies, trust and investment companies, finance companies affiliated with corporations, retail investors

(RMB 100 Million) Bond Holding Balance as of 31/10/2009 Percentage

Total 166,902.48 100.00%

Special Members 17,209.15 10.31%

Commercial Banks 117,416.03 70.35%

Credit Cooperative Banks 4,625.15 2.77%

Non-bank Financial Institutions 801.60 0.48%

Securities Companies 814.05 0.49%

Insurance Institutions 14,575.23 8.73%

Mutual Funds 7,189.72 4.31%

Non-financial Institutions 258.67 0.15%

Retail Investors 1,212.64 0.73%

Others 2,800.24 1.68%

PART 4

DESIRABLE DEVELOPMET IN THE FRUTURE - FROM PRIVATE SECTOR PERSPECTIVE

4.1 Domestic Market-Wishes of Private Sector

4.2 Market Globalization and International Cooperation

19

4.1 Domestic Market-Wishes of Private Sector

20

Regulation

Diversify issuer base Private sector will be able to serve the funding purpose of companies of different calibres

Innovation

Organization Cooperation

More liquid and dynamic secondary market to accommodate the sharply rising debt funding Private sector will be better poised to innovate in the market

CITICS Better interactions between government, SRO and private sector SRO with Chinese features may play stronger role in bridging over the market demand and government regulation

Stronger cooperation between market players Competition and cooperation may coexist in private sector, and stronger association among market players will achieve synergy and win-win scenario in a fast-growing market

4.2 Market Opening and International Cooperation

21

Invigorate the market by bringing in diversified issuers and investors Better meet the funding demand of companies and provide them with better-tailored funding solution, such as currency, tenor, etc. Boost the growth of intermediaries of each country in the region by greater exposure to international business and standards Lower down the funding risks of company and business risks of financial service sector by enabling them to putting eggs in different baskets

Necessity of Market Opening- Perspective of Private Sector

Political agenda and regional initiatives Strong communications between government regulators Unique role can be played by SROs in the region Supranational organization is an important driving force International collaboration and exchange between private market players are crucial to demonstrate what market demands and what is viable in the market

Driving Forces for Market Opening and International Cooperation

If you have further questions, please contact us:

Wan Tailei, Vice President, Debt Underwriting, Investment Banking Commission

Email: [email protected] Mobile: 86-13910836894 Phone: 86-10-84683760

Thank You!

Contact

Disclaimer

This presentation is not directed at, or intended for distribution to or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject CITIC Securities Co., Ltd. and its subsidiaries and affiliates (collectively ‚CITICS‛) to any registration or licensing requirement within such jurisdictions. All material presented in this presentation, unless specifically indicated otherwise, is under copyright to CITICS. None of the material, nor its contents, nor any copy of it, may be altered in any way, transmitted to, copied or distributed to any other party, without the prior express authorization in written of CITICS. All trademarks, service marks and logos of CITICS used herein are copyrighted.

The information, tools and material presented in this presentation are provided for your reference only and are not to be used or considered as an offer or the solicitation of an offer to sell or to buy or subscribe for securities or other financial instruments. CITICS have not taken any steps to ensure that the securities referred to herein are suitable for any particular investor. The contents herein do not constitute investment advice to any person and CITICS will not deem recipients as its customers by virtue of their receiving the presentation.

Information and opinions presented herein have been obtained or derived from sources believed by CITICS to be reliable, but CITICS makes no representation as to their accuracy or completeness and CITICS assumes no liability for any losses or damages arising from the use of the material presented herein unless such liability arises under specific statutes or regulations. This report is not to be relied upon in substitution for the exercise of independent judgment. CITICS may have issued other reports inconsistent with, and reaching conclusions different from, the information presented herein. Those reports reflect the different assumptions, views and analytical methods of the analysts who prepared them. To avoid any doubt, the opinions herein do not represent the standpoints of CITIC Securities Co., Ltd. or any of its subsidiaries or affiliates.

CITICS may, to the extent permitted by law, participate or invest in financial transactions with the issuer(s) of the securities referred to herein, perform services for or solicit business from such issuers, and/or have a position or effect transactions in the securities or options thereon. CITICS may, to the extent permitted by law, act upon or use the information or opinions presented herein, or the research or analysis on which they are based, before the material is published.

CITICS may have, within the last three years, served as manager or co-manager of a public offering of securities for, or currently may make a primary market in issues of, any or all of the companies mentioned herein. Additional information is available on request.

Past performance shall be no indication and guarantee of the future performance. Information, opinions and estimates contained herein reflect a judgment at the date of its original publication by CITICS and are subject to change. The prices, values and incomes of the securities or financial notes referred to herein may decline or increase.

This presentation is to be distributed to clients only. Those recipients who are not the market professionals and institutional investment clients of CITICS shall consult independent financial advisers prior to making any investment decisions based on this presentation or requesting any interpretations hereon.

CITIC Securities Co., Ltd. and Subsidiaries and Affiliates 2009 copyright. All rights reserved.