Intraday Trading Invariants for Equity-Index Futures · Intraday Trading Invariants for...

29

Intraday Trading Invariants for Equity-Index Futures Torben G. Andersen, Oleg Bondarenko, Albert S. Kyle and Anna Obizhaeva Fields Institute Toronto, Canada January 2015 Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 1/29

Transcript of Intraday Trading Invariants for Equity-Index Futures · Intraday Trading Invariants for...

Intraday Trading Invariantsfor Equity-Index Futures

Torben G. Andersen, Oleg Bondarenko, Albert S. Kyle andAnna Obizhaeva

Fields InstituteToronto, Canada

January 2015

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 1/29

Hypotheses on Trading – Volatility Interactions

Competing Ideas of How Information and Trades Induce Price Changes. . . And How Price Changes Convey News and Induce Trading

One Extreme: All Information Incorporated via Trading

Transactions or Trading Volume Drive VolatilityTransaction Clock (Mandelbrot and Taylor, 1967; Jones, Kaul &Lipson, 1994; Ane & Geman, 2000)Volume Clock (Clark, 1973)

Other Extreme: Information Flow Drives Market Activity

Latent Factor Driving both Trading and VolatilityMixture of Distributions (Tauchen & Pitts, 1983; Andersen, 1996)

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 2/29

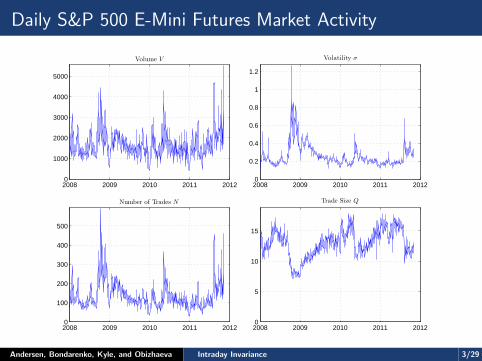

Daily S&P 500 E-Mini Futures Market Activity

2008 2009 2010 2011 20120

1000

2000

3000

4000

5000

Volume V

2008 2009 2010 2011 20120

100

200

300

400

500

Number of Trades N

2008 2009 2010 2011 20120

0.2

0.4

0.6

0.8

1

1.2

Volatility σ

2008 2009 2010 2011 20120

5

10

15

Trade Size Q

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 3/29

Hypotheses on Trading – Volatility Interactions

Focus typically on Observations at Daily Level

Exception: Ane & Geman, 2000; Near Tick-by-Tick

But Nobody has been Able to Confirm their Results

We also Fail to Verify Hypothesis

Use High-Frequency Data to Explore Interactions

Include Market Microstructure “Invariance” in Analysis

Empirical Support for Invariance via Diverse Market Phenomena

Major Expansion in Realm of Features Covered by Invariance

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 4/29

Why High-Frequency Analysis

Fact: Pronounced Intraday Market Activity Patterns

News Incorporated into Prices quickly; Trading Fast

Huge Systematic Variation over 24-Hour Trading Day

Does any Basic Regularity Apply in this Setting?

Macroeconomic Announcements particular Challenge

Large Price Jump on Impact without (much) Trading

Subsequent Price Discovery Process

Sudden Market Turmoil: Crisis, Flash Crash

Do Same or Different Regularities Apply in this Context?

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 5/29

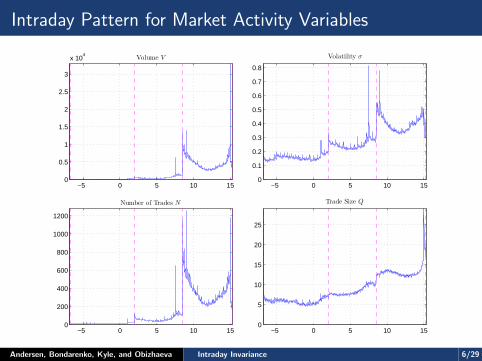

Intraday Pattern for Market Activity Variables

−5 0 5 10 150

0.5

1

1.5

2

2.5

3

x 104

Volume V

−5 0 5 10 150

200

400

600

800

1000

1200

Number of Trades N

−5 0 5 10 150

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

Volatility σ

−5 0 5 10 150

5

10

15

20

25

Trade Size Q

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 6/29

S&P 500 E-Mini Futures Market

Sample: BBO Files from CME Group; Jan 4, 2008 – Nov 2, 2011

Among World’s Most Active Markets – Price Discovery for Equities

Time Stamped to Second; Sequenced in Actual Order

Using Front Month Contract until Week before Expiration (most Liquid)

Three Daily Regimes: Asia, Europe, North America

Sunday – Thursday 17:15 – 2:00; 2:00-8:30; 8:30 – 15:15

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 7/29

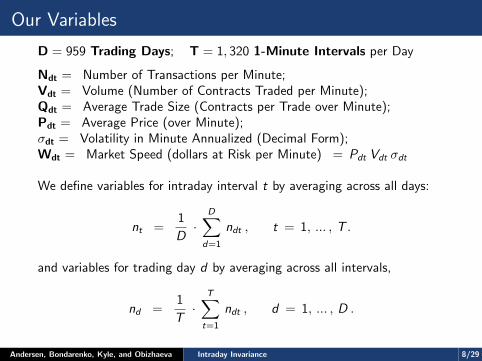

Our Variables

D = 959 Trading Days; T = 1, 320 1-Minute Intervals per Day

Ndt = Number of Transactions per Minute;Vdt = Volume (Number of Contracts Traded per Minute);Qdt = Average Trade Size (Contracts per Trade over Minute);Pdt = Average Price (over Minute);σdt = Volatility in Minute Annualized (Decimal Form);Wdt = Market Speed (dollars at Risk per Minute) = Pdt Vdt σdt

We define variables for intraday interval t by averaging across all days:

nt =1

D·

D∑d=1

ndt , t = 1, ... , T .

and variables for trading day d by averaging across all intervals,

nd =1

T·

T∑t=1

ndt , d = 1, ... , D .

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 8/29

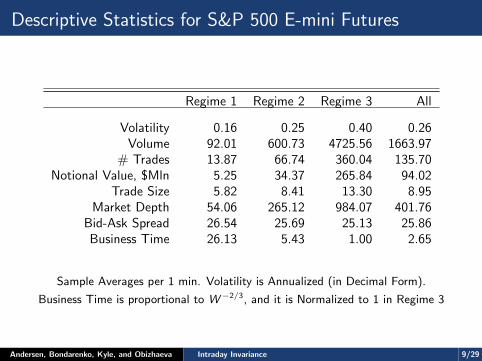

Descriptive Statistics for S&P 500 E-mini Futures

Regime 1 Regime 2 Regime 3 All

Volatility 0.16 0.25 0.40 0.26Volume 92.01 600.73 4725.56 1663.97

# Trades 13.87 66.74 360.04 135.70Notional Value, $Mln 5.25 34.37 265.84 94.02

Trade Size 5.82 8.41 13.30 8.95Market Depth 54.06 265.12 984.07 401.76

Bid-Ask Spread 26.54 25.69 25.13 25.86Business Time 26.13 5.43 1.00 2.65

Sample Averages per 1 min. Volatility is Annualized (in Decimal Form).

Business Time is proportional to W−2/3, and it is Normalized to 1 in Regime 3

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 9/29

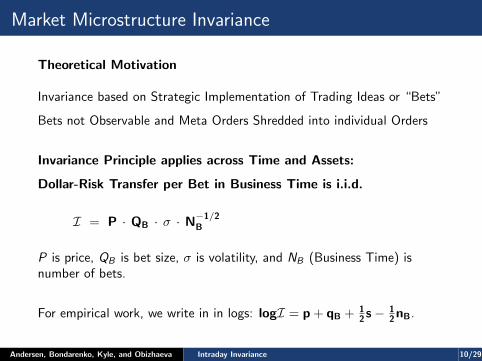

Market Microstructure Invariance

Theoretical Motivation

Invariance based on Strategic Implementation of Trading Ideas or “Bets”

Bets not Observable and Meta Orders Shredded into individual Orders

Invariance Principle applies across Time and Assets:

Dollar-Risk Transfer per Bet in Business Time is i.i.d.

I = P · QB · σ · N−1/2B

P is price, QB is bet size, σ is volatility, and NB (Business Time) isnumber of bets.

For empirical work, we write in in logs: logI = p + qB + 12 s− 1

2 nB.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 10/29

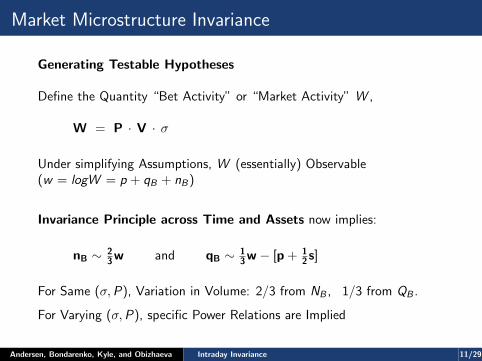

Market Microstructure Invariance

Generating Testable Hypotheses

Define the Quantity “Bet Activity” or “Market Activity” W ,

W = P · V · σ

Under simplifying Assumptions, W (essentially) Observable(w = logW = p + qB + nB)

Invariance Principle across Time and Assets now implies:

nB ∼ 23 w and qB ∼ 1

3 w − [p + 12 s]

For Same (σ,P), Variation in Volume: 2/3 from NB , 1/3 from QB .

For Varying (σ,P), specific Power Relations are Implied

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 11/29

Market Microstructure Invariance

Auxiliary Hypotheses invoked for Testable Hypotheses – still Success

I Kyle and Obizhaeva (2014) find invariance relationships in portfoliotransition orders;

I Kyle, Obizhaeva, and Tuzun (2012) find invariance relationships inprint sizes in TAQ data;

I Kyle, Obizhaeva, Sinha, and Tuzun (2014) find invariancerelationships in number of news articles;

I Bae, Kyle, Lee, and Obizhaeva (2014) find invariance relationshipsin Korean data.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 12/29

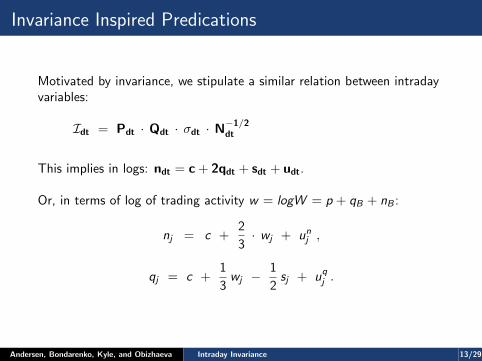

Invariance Inspired Predications

Motivated by invariance, we stipulate a similar relation between intradayvariables:

Idt = Pdt · Qdt · σdt · N−1/2dt

This implies in logs: ndt = c + 2qdt + sdt + udt.

Or, in terms of log of trading activity w = logW = p + qB + nB :

nj = c +2

3· wj + unj ,

qj = c +1

3wj −

1

2sj + uqj .

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 13/29

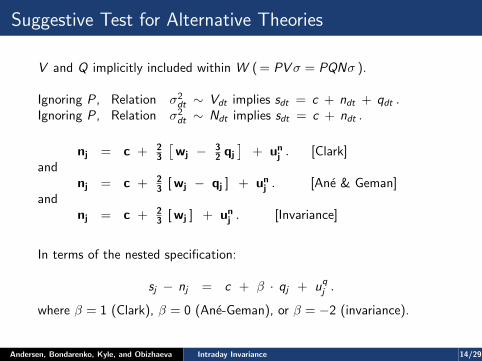

Suggestive Test for Alternative Theories

V and Q implicitly included within W ( = PVσ = PQNσ ).

Ignoring P, Relation σ2dt ∼ Vdt implies sdt = c + ndt + qdt .

Ignoring P, Relation σ2dt ∼ Ndt implies sdt = c + ndt .

nj = c + 23

[wj − 3

2 qj

]+ un

j . [Clark]and

nj = c + 23 [ wj − qj ] + un

j . [Ane & Geman]and

nj = c + 23 [ wj ] + un

j . [Invariance]

In terms of the nested specification:

sj − nj = c + β · qj + uqj .

where β = 1 (Clark), β = 0 (Ane-Geman), or β = −2 (invariance).

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 14/29

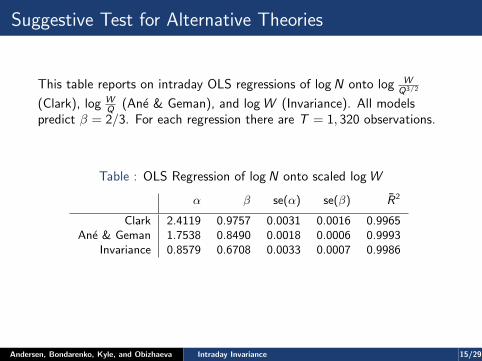

Suggestive Test for Alternative Theories

This table reports on intraday OLS regressions of logN onto log WQ3/2

(Clark), log WQ (Ane & Geman), and logW (Invariance). All models

predict β = 2/3. For each regression there are T = 1, 320 observations.

Table : OLS Regression of logN onto scaled logW

α β se(α) se(β) R2

Clark 2.4119 0.9757 0.0031 0.0016 0.9965Ane & Geman 1.7538 0.8490 0.0018 0.0006 0.9993

Invariance 0.8579 0.6708 0.0033 0.0007 0.9986

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 15/29

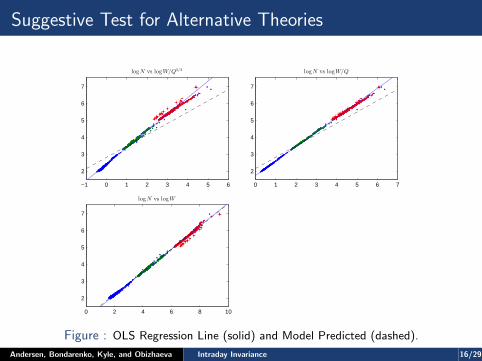

Suggestive Test for Alternative Theories

−1 0 1 2 3 4 5 6

2

3

4

5

6

7

logN vs logW/Q3/2

0 1 2 3 4 5 6 7

2

3

4

5

6

7

logN vs logW/Q

0 2 4 6 8 10

2

3

4

5

6

7

logN vs logW

Figure : OLS Regression Line (solid) and Model Predicted (dashed).

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 16/29

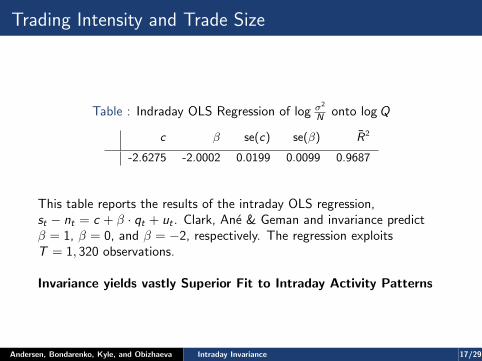

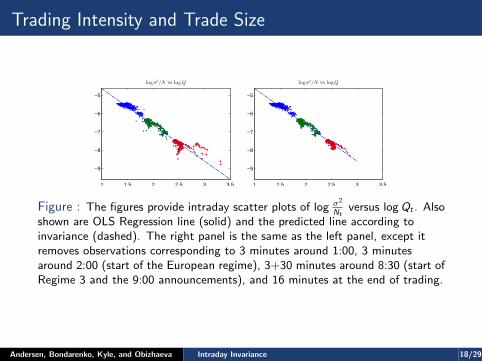

Trading Intensity and Trade Size

Table : Indraday OLS Regression of log σ2

N onto logQ

c β se(c) se(β) R2

-2.6275 -2.0002 0.0199 0.0099 0.9687

This table reports the results of the intraday OLS regression,st − nt = c + β · qt + ut . Clark, Ane & Geman and invariance predictβ = 1, β = 0, and β = −2, respectively. The regression exploitsT = 1, 320 observations.

Invariance yields vastly Superior Fit to Intraday Activity Patterns

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 17/29

Trading Intensity and Trade Size

1 1.5 2 2.5 3 3.5

−9

−8

−7

−6

−5

logσ2/N vs logQ

1 1.5 2 2.5 3 3.5

−9

−8

−7

−6

−5

logσ2/N vs logQ

Figure : The figures provide intraday scatter plots of log σ2

Ntversus logQt . Also

shown are OLS Regression line (solid) and the predicted line according toinvariance (dashed). The right panel is the same as the left panel, except itremoves observations corresponding to 3 minutes around 1:00, 3 minutesaround 2:00 (start of the European regime), 3+30 minutes around 8:30 (start ofRegime 3 and the 9:00 announcements), and 16 minutes at the end of trading.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 18/29

Intraday Invariance and Macro Announcements

Overall Invariance yields vastly Superior Fit to Intraday ActivityPatterns

Extremes? Macro Announcements Involve Dramatic Spikes

7:30 CT: Employment, CPI, PPI, Retail Sales, Housing Starts, . . .

9:00 CT: Home Sales, Confidence Survey, Factory Orders . . .

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 19/29

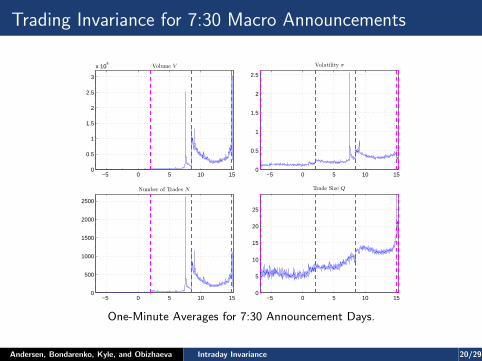

Trading Invariance for 7:30 Macro Announcements

−5 0 5 10 150

0.5

1

1.5

2

2.5

3

x 104

Volume V

−5 0 5 10 150

0.5

1

1.5

2

2.5

Volatility σ

−5 0 5 10 150

500

1000

1500

2000

2500

Number of Trades N

−5 0 5 10 150

5

10

15

20

25

Trade Size Q

One-Minute Averages for 7:30 Announcement Days.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 20/29

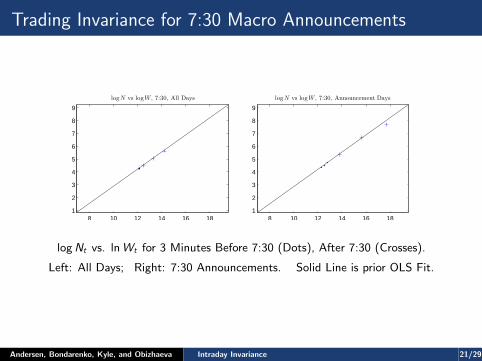

Trading Invariance for 7:30 Macro Announcements

8 10 12 14 16 181

2

3

4

5

6

7

8

9

logN vs logW , 7:30, All Days

8 10 12 14 16 181

2

3

4

5

6

7

8

9

logN vs logW , 7:30, Announcement Days

logNt vs. lnWt for 3 Minutes Before 7:30 (Dots), After 7:30 (Crosses).

Left: All Days; Right: 7:30 Announcements. Solid Line is prior OLS Fit.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 21/29

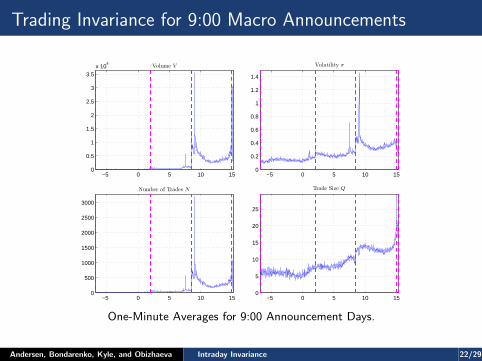

Trading Invariance for 9:00 Macro Announcements

−5 0 5 10 150

0.5

1

1.5

2

2.5

3

3.5x 10

4Volume V

−5 0 5 10 150

0.2

0.4

0.6

0.8

1

1.2

1.4

Volatility σ

−5 0 5 10 150

500

1000

1500

2000

2500

3000

Number of Trades N

−5 0 5 10 150

5

10

15

20

25

Trade Size Q

One-Minute Averages for 9:00 Announcement Days.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 22/29

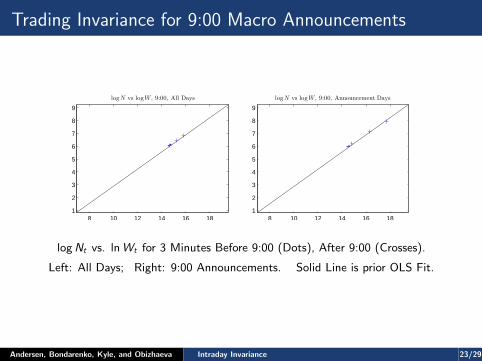

Trading Invariance for 9:00 Macro Announcements

8 10 12 14 16 181

2

3

4

5

6

7

8

9

logN vs logW , 9:00, All Days

8 10 12 14 16 181

2

3

4

5

6

7

8

9

logN vs logW , 9:00, Announcement Days

logNt vs. lnWt for 3 Minutes Before 9:00 (Dots), After 9:00 (Crosses).

Left: All Days; Right: 9:00 Announcements. Solid Line is prior OLS Fit.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 23/29

Subsample Analysis

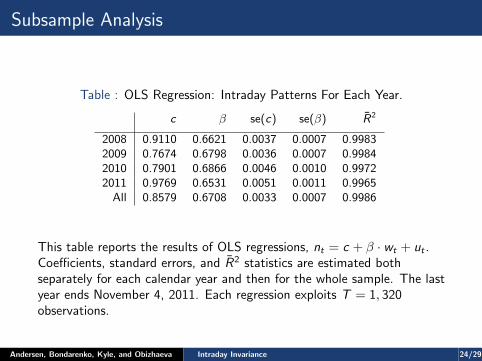

Table : OLS Regression: Intraday Patterns For Each Year.

c β se(c) se(β) R2

2008 0.9110 0.6621 0.0037 0.0007 0.99832009 0.7674 0.6798 0.0036 0.0007 0.99842010 0.7901 0.6866 0.0046 0.0010 0.99722011 0.9769 0.6531 0.0051 0.0011 0.9965

All 0.8579 0.6708 0.0033 0.0007 0.9986

This table reports the results of OLS regressions, nt = c + β · wt + ut .Coefficients, standard errors, and R2 statistics are estimated bothseparately for each calendar year and then for the whole sample. The lastyear ends November 4, 2011. Each regression exploits T = 1, 320observations.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 24/29

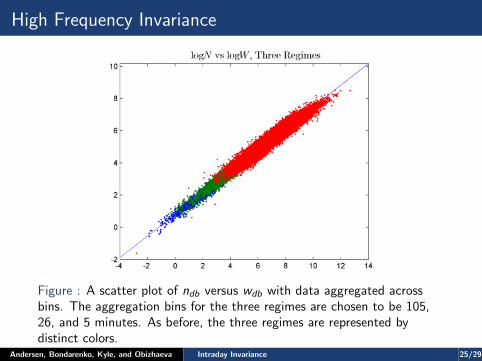

High Frequency Invariance

Figure : A scatter plot of ndb versus wdb with data aggregated acrossbins. The aggregation bins for the three regimes are chosen to be 105,26, and 5 minutes. As before, the three regimes are represented bydistinct colors.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 25/29

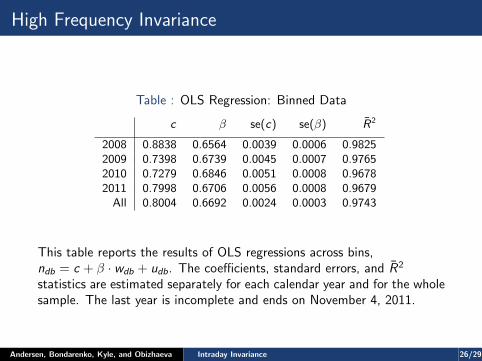

High Frequency Invariance

Table : OLS Regression: Binned Data

c β se(c) se(β) R2

2008 0.8838 0.6564 0.0039 0.0006 0.98252009 0.7398 0.6739 0.0045 0.0007 0.97652010 0.7279 0.6846 0.0051 0.0008 0.96782011 0.7998 0.6706 0.0056 0.0008 0.9679

All 0.8004 0.6692 0.0024 0.0003 0.9743

This table reports the results of OLS regressions across bins,ndb = c + β · wdb + udb. The coefficients, standard errors, and R2

statistics are estimated separately for each calendar year and for the wholesample. The last year is incomplete and ends on November 4, 2011.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 26/29

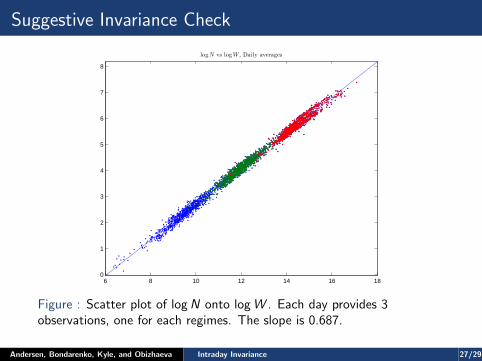

Suggestive Invariance Check

6 8 10 12 14 16 180

1

2

3

4

5

6

7

8

logN vs logW , Daily averages

Figure : Scatter plot of logN onto logW . Each day provides 3observations, one for each regimes. The slope is 0.687.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 27/29

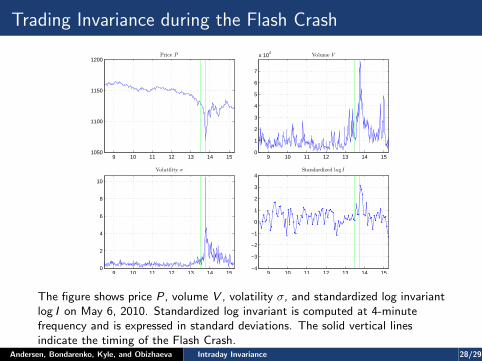

Trading Invariance during the Flash Crash

9 10 11 12 13 14 15−4

−3

−2

−1

0

1

2

3

4Standardized log I

9 10 11 12 13 14 151050

1100

1150

1200Price P

9 10 11 12 13 14 150

1

2

3

4

5

6

7

x 104

Volume V

9 10 11 12 13 14 150

2

4

6

8

10

Volatility σ

The figure shows price P, volume V , volatility σ, and standardized log invariantlog I on May 6, 2010. Standardized log invariant is computed at 4-minutefrequency and is expressed in standard deviations. The solid vertical linesindicate the timing of the Flash Crash.

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 28/29

Conclusions

Intraday Trading Activity Patterns Intimately Related

Traditional Theories: Transactions or Volume Govern Volatility

Invariance (Kyle & Obizhaeva) Motivates Alternative Intraday Relation

Critically, Trade Size Drops in specific Proportion with Volatility

For E-Mini, Tendency Observed by Andersen & Bondarenko RF, VPIN

Qualitative Prediction verified for Diurnal Pattern

Qualitative Prediction verified for Daily Regimes (Time Series)

Theoretical Justification for Invariance in this Context Loom Large

How will Findings Generalize across Market Structures?

Andersen, Bondarenko, Kyle, and Obizhaeva Intraday Invariance 29/29