internship report on UCBL

56

Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited By Ziauddin Chowdhury ID: 0921044 An Internship Report Presented in Partial Fulfillment of the Requirements for the Degree of Bachelor of Business Administration Independent University, Bangladesh December 2012

-

Upload

ziauddin-chowdhury -

Category

Documents

-

view

267 -

download

6

Transcript of internship report on UCBL

Consumer Credit Schemes and Consumer Satisfaction of United

Commercial Bank Limited

By

Ziauddin Chowdhury

ID: 0921044

An Internship Report Presented in Partial Fulfillment of the

Requirements for the Degree of Bachelor of Business Administration

Independent University, Bangladesh

December 2012

Consumer Credit Schemes and Consumer Satisfaction of United

Commercial Bank Limited

By

Ziauddin Chowdhury

ID: 0921044

Has been approved

October, 2012

__________________________

Mr. Abul Bashar

Senior Lecturer, Management

School of Business

Independent University, Bangladesh

November 29, 2012

To

Mr. Abul Bashar

Senior Lecturer, Management

School of Business

Independent University, Bangladesh.

Subject: Submission of Internship Report.

Dear Sir,

With due respect I am very pleased to enclose herewith the internship report on

―Consumer Credit Schemes and Consumer Satisfaction of United Commercial

Bank Limited‖. The last three months has been the most fabulous learning

experience for me. Without your guidance and help this learning experience would

not have been way it has been. I have tried my best to prepare a good report with

providing all of my effort and to cover all aspects regarding the matter. I think that

this report contains the information that you need to get an idea about my research

also. However, because of the confidentially policy of United Commercial Bank

Limited it not been possible to put as many data and information as I would have

liked to.

I, therefore, hope that you would be kind enough to accept my internship report.

Sincerely Yours,

Ziauddin Chowdhury

Id: 0921044

Independent University Bangladesh

Acknowledgement

All praises are due to Almighty Allah who enabled me to complete this report. This report

entitled the Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank

Limited.

The study has been successfully accomplished along with considerate support and continuous

guidance of few people. This is the utmost pleasure of mine to show heartfelt gratitude towards

those individuals.

First and foremost, I would like to express my gratefulness my respected supervisor Mr. Abul

Bashar (Senior Lecturer, Management) School of Business, Independent University, Bangladesh

for his support in every area of this research. He is the person of my inspiration to give best

effort in this study. He was always there as an advisor, monitor and supervisor. Without his

cooperation it would not have been possible to accomplish the research.

My thankfulness also goes to Abu Arafat Latif (Senior Officer) of Bashundhara Branch for his

continuous and cordial support during my internship. He provided me with invaluable insights

about overall Consumer Credit (Retail Banking) system of this bank.

I am grateful to all concerned persons who provided valuable guidance, suggestions and advices

in collecting information, analyzing and preparing the report. I am particularly indebted to them

whose efforts and cordial cooperation made the report possible.

Table of Contents

Executive Summary--------------------------------------------------------------------------------------- 01

Origin of Bank--------------------------------------------------------------------------------------------- 02

United Commercial Bank Limited – At a Glance ---------------------------------------------------- 03

Goals and Objectives ------------------------------------------------------------------------------------- 04

Mission ----------------------------------------------------------------------------------------------------- 04

Vision ------------------------------------------------------------------------------------------------------- 04

UCBL‘s Organizational Structure ---------------------------------------------------------------------- 05

Branch Information --------------------------------------------------------------------------------------- 06

Service booths at UCB- Bashundhara Branch -------------------------------------------------------- 07

Employees at UCBL - Bashundhara Branch ---------------------------------------------------------- 08

Products/ Services offered by the Bank ---------------------------------------------------------------- 09

Consumer Credit ------------------------------------------------------------------------------------------ 10

Consumer Credit Schemes of United Commercial Bank Limited ---------------------------- 11 - 16

Objective of the Customer Credit Scheme ------------------------------------------------------------- 17

Collection Steps of United Commercial Bank Limited ---------------------------------------------- 17

About The Research -------------------------------------------------------------------------------------- 18

Statement of the Problem -------------------------------------------------------------------------------- 19

Purpose of the Study -------------------------------------------------------------------------------------- 19

Review of Literature -------------------------------------------------------------------------------- 20 - 22

Conceptual Framework ----------------------------------------------------------------------------------- 23

Research Questions and Hypothesis -------------------------------------------------------------------- 24

Methodology ----------------------------------------------------------------------------------------- 25 – 26

Data Analysis:

Frequencies analysis ----------------------------------------------------------------------------------- 27

Crosstabs analysis -------------------------------------------------------------------------------------- 28

Correlation analysis ------------------------------------------------------------------------------- 29 - 41

Reliability Analysis ------------------------------------------------------------------------------- 42 - 43

Significance of the Study -------------------------------------------------------------------------------- 44

Recommendation ----------------------------------------------------------------------------------------- 45

Conclusion ------------------------------------------------------------------------------------------------ 46

References ------------------------------------------------------------------------------------------------ 47

Appendix --------------------------------------------------------------------------------------------- 48 - 50

P a g e | 1 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Executive Summary:

Internship report is mandatory in the process to pursue a Bachelor‘s degree from country‘s

leading business school at Independent University. The report is divided into two parts –

Company Background and Research. Company Background discusses about the business

where an intern is appointed to, while the Research portion of the report discusses about an

aspect of the business that was never analyzed before.

The report contains small background information of the bank and the branch where the

internee was placed in. As you would proceed further, a service blueprint of the branch has

been provided. A list of people (with respective designation) who were working at the branch,

while writing this report, has been provided.

A detailed picture of customer satisfaction possessed by the bank with its commercial clients

has been the core of the research. As an internee I visited three branches in Dhaka city and

gathered data from 40 respondents (commercial clients) to conduct analysis on the research

topic.

Major findings include:

i. Front-end employees tend to be doing their job well, in terms of interacting with

customers.

ii. Efficiency and clarity of discussing information is found to be the weak link. Staff

training may improve the situation.

iii. Internal service is perceived to be doing better compared to efficiency and

communication of information.

The most important finding, however, is that if a client has faith in the bank‘s procedures, they

can easily be satisfied through empowerment of which would lead to a lasting commitment to

create pool of loyal customers and source of positive word-of-mouth.

After my research I can say that service quality and employee behavior of UCB is quite

satisfactory. To provide better satisfaction towards customer UCB have to improve their

product line much updated and the charges should be under satisfactory level so that

customers feel happy to being with UCB.

Expert advice on marketing research on this topic could have provided more dimensions to

this research. Having more people for brainstorming and research would have given fresh

perspective. The research could have been much better if there were more variables and

sample size to work on, with adequate resources i.e. time, budget, human, etc.

P a g e | 2 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Origin of Bank:

Originally the word ―BANK‖ we can easily understand the financial institution that deals with

money. But there are different types of banks like; Central Banks, Commercial Banks,

Savings Banks, Investment Banks, Industrial Banks, Co-operative Banks etc. But when we

use the term ―Bank‖ without any prefix, or qualification, it refers to the ‗Commercial banks‘.

Commercial banks are the primary contributors to the economy of a country. So we can say

Commercial banks are a profit-making institution that holds the deposits of individuals &

business in checking & savings accounts and then uses these funds to make loans. For these

people and the government is very much dependent on these banks as the financial

intermediary. As banks are profit -earning concern; they collect deposit at the lowest possible

cost and provide loans and advances at higher cost. The differences between two are the profit

for the bank.

Banking sector is expanding its hand in different financial events every day. At the same time

the banking process is becoming faster, easier and the banking arena is becoming wider. As

the demand for better service increases day by day, they are coming with different innovative

ideas & products. In order to survive in the competitive field of the banking sector, all

banking organizations are looking for better service opportunities to provide their fellow

clients. As a result, it has become essential for every person to have some idea on the bank

and banking procedure.

Internship program is essential for every student, especially for the students of Business

Administration, which helps them to know the real life situation. For this reason a student

takes the internship program at the last stage of the degree, to launch a career with some

practical experiences.

P a g e | 3 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

United Commercial Bank Limited – At a Glance:

In the backdrop of economic liberalization and financial sector reforms, a group of highly

successful local entrepreneurs conceived an idea of floating a commercial bank with a

different outlook. For them it was competence, excellence and consistent delivery of reliable

service with superior value products. Accordingly, United Commercial Bank Limited was

created and commencement of business started on 17th

April 1980.

United Commercial Bank Ltd. is operating as a scheduled bank under the banking license

issued by Bangladesh Bank, the Central Bank of the country on April 17, 1980 through the

opening of its Motijheel Branch at Adamjee Court Annex Building, Motijheel commercial

area, Dhaka-1000. UCBL was actually registered under the Companies Act of 1913 with its

registered office at 5, Rajuk Avenue, Motijheel commercial area, Dhaka-1000 which was later

shifted to Adamjee Court Annex Building, 119-120, Motijheel commercial area, Dhaka-1000.

Since inception, it has committed to provide high quality financial services to the people of

this country to accelerate economic development of the nation. As such, it has been working

for stimulating trade and commerce, accelerating the pace of industrialization, boosting

export, creating employment opportunity, alleviating poverty, raising standard of living of the

people etc and thereby contributing to the sustainable development of the country. The bank is

listed with DSE & CSE as a public quoted company.

As a fully licensed commercial bank, United Commercial Bank Limited has being managed

by highly professional and dedicated team with long experience in banking. They constantly

focus on understanding and anticipating customer needs.

In its 22nd

year of operation in 2012, United Commercial Bank has made substantial headway

in terms of business growth, profitability and establishing its image as one of the leading

private commercial banks. Its march towards reaching greater heights in operation continues

with full vigor and enthusiasm. United Commercial Bank has made significant progress

within a very short period of its existence. The bank has been graded as a top class bank in the

country through internationally accepted CAMEL Rating. The bank has already occupied an

enviable position among its competitors after achieving success in all areas of business

operations.

P a g e | 4 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Goals and Objectives:

To utilize all available resources properly to develop various plan, policies and

procedures in each of the objective and goal areas.

Synchronized and steady growth of the bank.

Utilize team of professional employees.

Search for a total customized solution for by establishing full automation step.

Develop a plan for offering better customer service.

Develop a realistic deposit mobilization plan

Build up appropriate lending risk assessment system

Improve capital plan

Develop a structure to make sound loan and advances

Develop systematic procedures and approaches by improving management efficiency.

Expand scientific MIS to monitor bank‘s activities.

Ensure a sound rate of recovery of all loans & advances and other credit facilities

Build up a low cost fund base

Meet capital adequacy recruitment at all the time.

Mission:

To assist high quality service to customer and to participate in the growth and expansion of

our national economy and to satisfy clients, shareholders and employees.

Vision:

To be the bank of the 1st choice through maximizing value of clients shareholder & employees

and contributing to the national economy with social commitments.

P a g e | 5 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

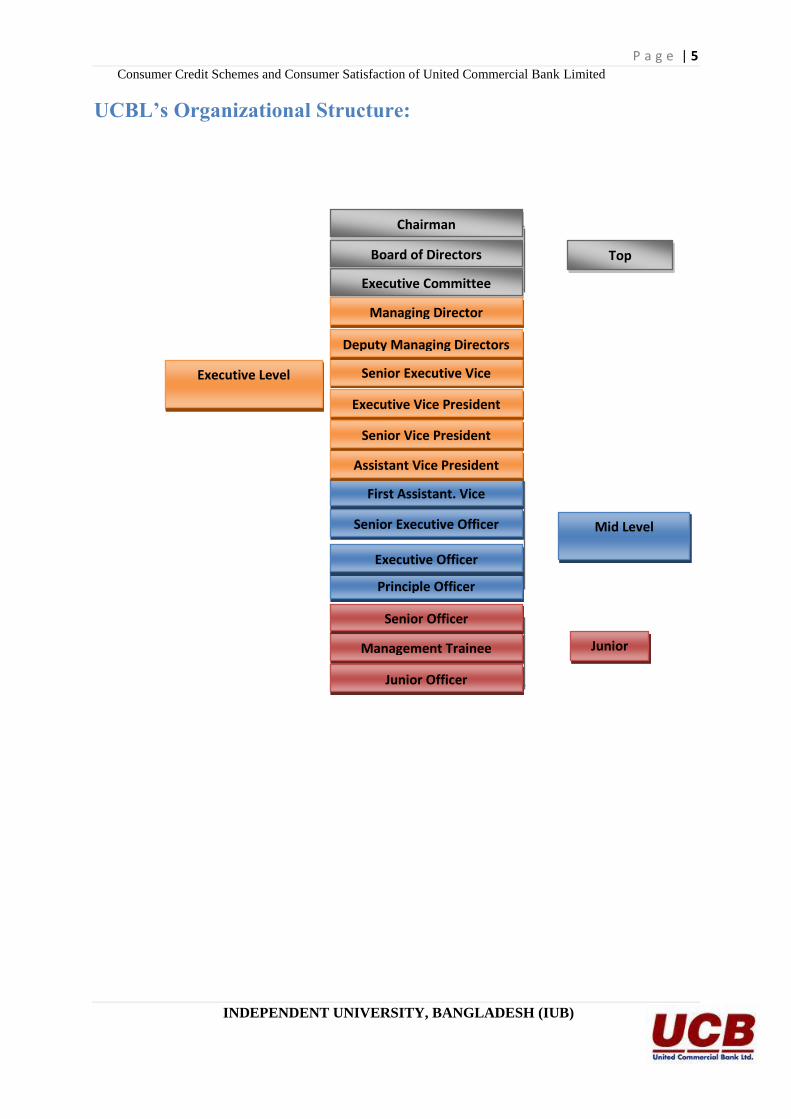

UCBL’s Organizational Structure:

Mid Level

Management

Executive Level

Management

Top

Management

Junior Officer

Management Trainee

Officer

Senior Officer

Principle Officer

Executive Officer

Senior Executive Officer

First Assistant. Vice

President

Assistant Vice President

Senior Vice President

Executive Vice President

Senior Executive Vice

Deputy Managing Directors

Executive Committee

Managing Director

Board of Directors

Chairman

Junior

Level

P a g e | 6 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Branch Information:

UCBL has 125 Branches in Bangladesh

Year 2007 2008 2009 2010 2011 2012

No. of Branches 84 84 84 98 112 125

Total Branch: 56

Total Branch: 38

Total Branch: 07

Total Branch: 01

Total Branch: 02

Total Branch 07

Total Branch: 14

P a g e | 7 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

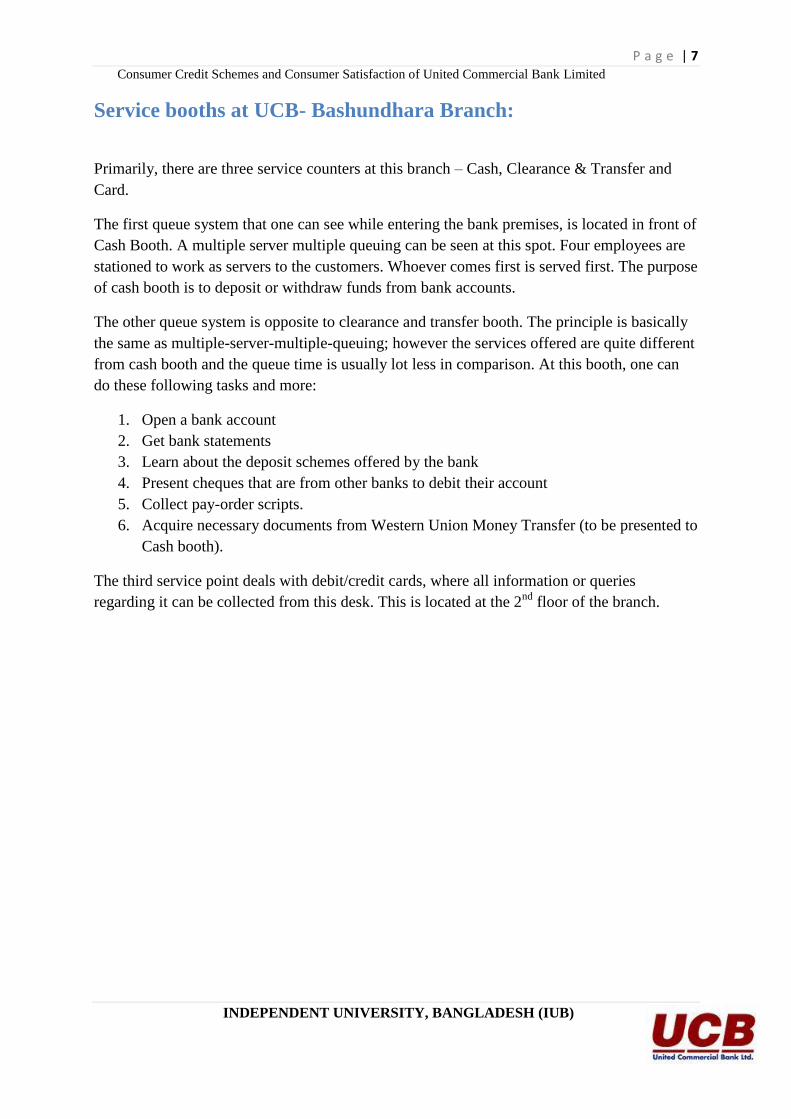

Service booths at UCB- Bashundhara Branch:

Primarily, there are three service counters at this branch – Cash, Clearance & Transfer and

Card.

The first queue system that one can see while entering the bank premises, is located in front of

Cash Booth. A multiple server multiple queuing can be seen at this spot. Four employees are

stationed to work as servers to the customers. Whoever comes first is served first. The purpose

of cash booth is to deposit or withdraw funds from bank accounts.

The other queue system is opposite to clearance and transfer booth. The principle is basically

the same as multiple-server-multiple-queuing; however the services offered are quite different

from cash booth and the queue time is usually lot less in comparison. At this booth, one can

do these following tasks and more:

1. Open a bank account

2. Get bank statements

3. Learn about the deposit schemes offered by the bank

4. Present cheques that are from other banks to debit their account

5. Collect pay-order scripts.

6. Acquire necessary documents from Western Union Money Transfer (to be presented to

Cash booth).

The third service point deals with debit/credit cards, where all information or queries

regarding it can be collected from this desk. This is located at the 2nd

floor of the branch.

P a g e | 8 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Employees at UCBL - Bashundhara Branch:

Designation Name Workstation

Vice-President

& Head of Branch Mr. S.K. Sirajul Kabir

Manager‘s Cabin

(2nd

Floor)

First Assistant

Vice-President

& Operation Manager

Mr. Md Akhter Hossain FAVP‘s Cubicle

(1st Floor)

Senior Executive Officer Mr. Golam Idrees SEO‘s Desk (2nd

Floor)

Senior Officer Mr. Abu Arafat Latif Senior Officer Desk

(2nd

Floor)

Officer Mr. Hafizur Rahman Officer‘s Desk

(2nd

Floor)

Officer – Cash Mr. Shahjahan Chowdhury Cash Booth (1st Floor)

Junior Officer Mrs. Rezwana Khanam Clearance & Transfer

Booth (1st Floor)

Junior Officer Mr. B.M. Borhan Uddin Clearance & Transfer

Booth (1st Floor)

Junior Officer – Probation Mr. Ali Rawshan Ibne Alam Clearance & Transfer

Booth (1st Floor)

Assistant Cash Officer Mrs. Kaniz Fatema Cash Booth (1st Floor)

Assistant Cash Officer Mr. MD. Morshedul Alam Cash Booth (1st Floor)

Assistant Cash Officer –

Probation Mr. MD. Rafiqul Karim Cash Booth (1

st Floor)

Credit Card Service Officer Mr. S.M. Saifullah Card Officers‘ Desk

(2nd

Floor)

Debit Card Service Mr. Ariful Haque Card Officers‘ Desk

(2nd

Floor)

P a g e | 9 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Products/ Services offered by the Bank:

UCB Multi Milionaire

UCB Money Maximizer

UCB Earning Plus

UCB DPS Plan

Western Union Money Transfer

SMS Banking Service

Online Service

Credit Card

One Stop Service

Time Deposit Scheme

Monthly Savings Scheme

Deposit Insurance Scheme

Inward & Outward Remittances

Travelers Cheques

Import Financing

Export Financing

Working Capital Finance

Loan Syndication

Underwriting and Bridge Financing

Trade Finance

Industrial Finance

Foreign Currency Deposit

NFCD (Non Resident Foreign Currency Deposit Account)

All These services can be broken down to Consumer Credit (Retail) Banking; commercial

(includes SME and Corporate) banking; and miscellaneous services.

P a g e | 10 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Consumer Credit:

It is one of the core businesses for United Commercial Bank Limited and has been targeted

for significant further growth. This reflects the potential of consumer credit scheme to

produce high levels of economic profit and perceived demographic trends toward an expanded

middle class and higher income levels.

Asset quality is generally expected to be higher in personal lending than corporate lending due

to variety of factors including:

Diversification of risk

Security

Cultural values

The increasing need for individuals to have access to bank credit for the conduct

of normal daily activities.

United Commercial Bank is a conservative lender in consumer credit as part of its corporate

philosophy. However, conservatism does not mean simply minimizing bad debts, but

incorporates the concept of lending against acceptable risks. The Bank‘s overriding goal is not

only to increase total shareholder return but also to contribute to the socio economy by

improving the life style of the limited income segment of the country and that can be achieved

optimizing profits, rather than just minimizing losses, profit optimization will follow from:

Good-planning and control of approval process

Well-designed products with appropriately focused marketing

The use of statistical techniques and decision support system that permit risks to

be managed predictably

Gathering high quality management information, which is then read and used.

P a g e | 11 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

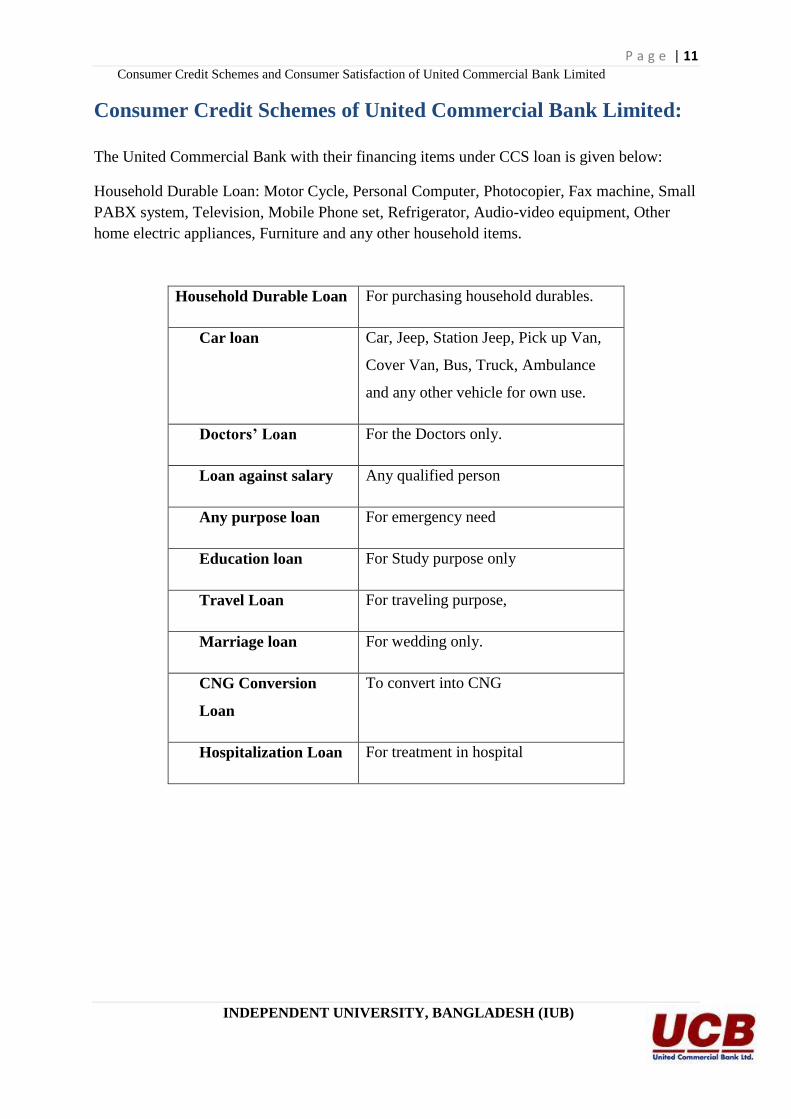

Consumer Credit Schemes of United Commercial Bank Limited:

The United Commercial Bank with their financing items under CCS loan is given below:

Household Durable Loan: Motor Cycle, Personal Computer, Photocopier, Fax machine, Small

PABX system, Television, Mobile Phone set, Refrigerator, Audio-video equipment, Other

home electric appliances, Furniture and any other household items.

Household Durable Loan For purchasing household durables.

Car loan Car, Jeep, Station Jeep, Pick up Van,

Cover Van, Bus, Truck, Ambulance

and any other vehicle for own use.

Doctors’ Loan For the Doctors only.

Loan against salary Any qualified person

Any purpose loan For emergency need

Education loan For Study purpose only

Travel Loan For traveling purpose,

Marriage loan For wedding only.

CNG Conversion

Loan

To convert into CNG

Hospitalization Loan For treatment in hospital

P a g e | 12 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Car loan:

Customer Segment

Any Bangladeshi individual who has the means and capacity to repay the loan. In

specific terms the target customers should cover salaried executives of multinational

companies, middle to large size local corporate, Government officials, Officials

working in Semi-government, Autonomous and reputed Non-Government

Organization, International aid agencies and any tax paying businessmen of repute

and self-employed tax-paying individual having a reliable source of income.

Purpose

Purchase of non-commercial new and reconditioned vehicles for personal use only by

individual.

Doctors’ Loan

Customer Segment

Any Bangladeshi citizen who is a graduate in Medical Science/Dentist/Eye/Allopathic

as self-employed or salaried people has the means and capability to repay the loan.

Purpose

Small scale purchase of different medical equipments, machineries, items to support

professional tools or other relevant needs (e.g. run or set up a

clinic/hospital/dispensary).

Household Durable Loan

Customer Segment

Any Bangladeshi individual who has the means and capacity to repay the loan. In

specific terms the target customers should cover salaried executives of multinational

companies, middle to large size local corporate, Government officials, Officials

working in Semi-government, Autonomous and reputed Non-Government

P a g e | 13 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Organization, International aid agencies and any tax paying businessmen of repute

and self-employed tax-paying individual having a reliable source of income.

Purpose

Purchase of household durables like Television, Refrigerator, Air conditioner,

Washing Machine, Computers, other household furniture etc. for personal use only.

Marriage loan

Customer Segment

Employees of reputed multinational companies and large local corporate

Employees of medium sized or mid-range local corporate such as reputed schools

and colleges, insurance and leasing companies, Non-Government Organization,

reputed trading firms and all other salaried persons.

Any tax paying businessmen of repute and self-employed tax-paying individual

having a reliable source of income.

Purpose

To meet the financial need for marriage purpose.

Any purpose loan

Customer Segment

Employees of reputed multinational companies and large local corporate

Employees of medium sized or mid-range local corporate such as reputed schools and

colleges, insurance and leasing companies, Non-Government Organization,

Government officials, reputed trading firms and all other salaried persons

Purpose

The customer has to declare the purpose of the loan but submission of supporting document is

not mandatory. Purpose may be as follows:

P a g e | 14 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

House renovation

Marriage in a family

Advance retail payment

Hospitalization or other emergency medical needs

Trips abroad

Purchase of Miscellaneous household appliances

Purchase of personal computer

Purchase of electronic items

Purchase of furniture

Education loan:

Customer Segment

Employees of reputed multinational companies and large local corporate

Employees of medium sized or mid-range local corporate such as reputed schools

and colleges, insurance and leasing companies, Non-Government Organization,

reputed trading firms and all other salaried persons.

Any tax paying businessmen of repute and self-employed tax-paying individual

having a reliable source of income.

Purpose

For educational purposes like study in abroad or within the country.

Hospitalization Loan:

Customer Segment

Employees of reputed multinational companies and large local corporate

Employees of medium sized or mid-range local corporate such as reputed schools and

colleges, insurance and leasing companies, Non-Government Organization,

Government officials, reputed trading firms and all other salaried persons

Any tax paying businessmen of repute and self-employed tax-paying individual having

a reliable source of income.

P a g e | 15 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Purpose

To meet the financial need for treatment purposes in the following hospitals/clinics of Dhaka

and Chittagong:

BIRDEM

Holy family Hospital

Central Hospital

Monwara Hospital

Samrita Hospital

Medinova

Bangladesh Medical

Metropolitan Hospital

Sikder Medical

Islami Bank Hospital

Dhaka Renal Centre

Ibne Sina Hospital

Lab Aid Cardiac Hospital

National Heart Foundation

CMH, Dhaka

Apollo Hospital

Health Care, Chittagong

Health Home, Chittagong

Poly Clinic, Chittagong

CMH, Chittagong etc

Loan against salary

Customer Segment

Employees of reputed multinational companies and large local corporate

Employees of medium sized or mid-range local corporate such as reputed schools and

colleges, insurance and leasing companies, Non-Government Organization,

Government officials, reputed trading firms and all other salaried persons

P a g e | 16 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Purpose

To meet the financial need for any acceptable purpose.

Travel Loan

Customer Segment

Employees of reputed multinational companies and large local corporate

Employees of medium sized or mid-range local corporate such as reputed schools

and colleges, insurance and leasing companies, Non-Government Organization,

reputed trading firms and all other salaried persons.

Any tax paying businessmen of repute and self-employed tax-paying individual

having a reliable source of income.

Purpose

To meet the financial need for travel purpose.

CNG Conversion Loan

Customer Segment

Any Bangladeshi individual who has the means and capacity to repay the loan. In

specific terms the target customers should cover salaried executives of multinational

companies, middle to large size local corporate, Government officials, Officials

working in Semi-government, Autonomous and reputed Non-Government

Organization, International aid agencies and any tax paying businessmen of repute and

self-employed tax-paying individual having a reliable source of income

Purpose

For converting vehicles from carbon based fuel to Compressed Natural Gas system.

P a g e | 17 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Objective of the Customer Credit Scheme:

United Commercial Bank Limited started the Consumer Credit Scheme program with a view

to fulfill its benevolent institutional objectives through financing the middle class limited

income group.

To ensure the credit facility to the both middle class Limited income group and upper

class income group.

To improve the living standard of limited income group through financing in

purchasing necessary goods.

To participate in the socio-economic development of the country.

Collection Steps of United Commercial Bank Limited:

Days Past Due Collection Action

1-14 days Letter, Follow up and Persuasion over phone

15-29 days 1st Remainder Letter and first step follows

30-44 days 2nd

Reminder letter

single visit of credit officer

45-59 days 3rd

Reminder letter

Group visit by team members

Follow up over phone

Letter to Guarantor, Employer

Reference all above effort follows

Warning of legal action by next 15 days

60-89 days Call up of loan

Final Reminder and serve legal notice

Legal proceeding begins

Repossession starts

90 and above days Telephone calls

Legal proceeding continues

Collection effort continues by officer & agents

Letter to different Banks and Associations

P a g e | 18 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

About The Research:

Consumer Credit (Retail Banking) is one of the vital functions for any bank. Lion share

revenues of banks comes by meeting the financial requirements of the SMEs and corporates.

Credence product by nature, financing services by banks to commercial institutions are

difficult to measure. While demand for, and supply of funds in the money market intersect at a

point that makes most of the financial service-availing institutions indifferent for selection of

bank. In this scenario a stronger bank has an edge. Simultaneously, banks in recent times have

taken fostering of relationship with present clients with great care, as it is inexpensive and

profitable for the business than attracting new ones and establishing relationship.

United Commercial Bank Ltd. is among the first banks that took relationship banking

seriously through ―Happy Banking‖ campaign, dated back in 2007. The bank offers

innumerable flexible options and benefits to their clients along with emphasizing professional

bonds between bank employees and clientele.

An award winning service research journal on relationship benefits and quality for service-

oriented business authored by Hennig-Thurau, Gwinner and Gremler (2002) has been the

backbone of my research. The journal encompasses a multivariate study that probes several

aspects of relationship between service provider and customers with thorough analysis on this

field of study. With assumption that the structural equation model devised by the author to be

exhaustive, outcomes from processing fieldwork data will lead to the most imperative aspects

the bank needs to focus on for improvement to cater their customers better.

The Credit Department (Retail Banking) policy of UCB is prepared in line with the guidelines

of Bangladesh Bank to handling it in a disciplined way. Credit Department plays a very

important role in bank as they evaluate the risk and take decision about giving loan to the

customers. In this report I have tried to study the literatures instruments about customer

satisfaction process and also the credit operation of United Commercial Bank Limited.

P a g e | 19 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Statement of the Problem:

Credit risk and customer dissatisfaction corresponds to potential financial loss as a result of

customer‘s inability to honor the terms and conditions of credit facility. This report will

mainly focus on managing credit risk by providing proper satisfaction towards the customers

as well as achieving organizations profit.

Purpose of the Study:

The purpose of the internship program is to familiarize students with real market situation and

compare it with bookish concept. The main purpose of the study is to have an assessment

about Consumers Credit Schemes of United Commercial Bank Limited and customer

satisfaction gaining from those credit schemes.

Major purpose of the study are-

To examine customer satisfaction towards UCB credit schemes.

Find out the relationship between service quality, Updated products, charges and

employee behavior about in the context of customer satisfaction.

To find out the real picture of UCB in terms of deposits and other financial products.

Establishing favorable employee attitude to provide better satisfaction towards

customers.

Developing new products and ideas to create brand awareness as well as for proper

customer satisfaction.

P a g e | 20 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Review of Literature:

In this research I have go through some variables which must be needed to create best

customer satisfaction in United Commercial Bank Limited.

Service Quality:

Research has indicated that service quality has been increasingly recognized as a critical

factor in the success of any business (Parasuraman et al., 1988) and the banking sector in this

case is not exceptional. Service quality has been widely used to evaluate the performance of

banking services (Cowling and Newman, 1995). The banks understand that customers will be

loyal if they receive greater value than from competitors (Dawes and Swailes, 1999) and on

the other hand, banks can earn high profits if they are able to position themselves better than

their competitors within a specific market (Davies et al., 1995). Therefore, banks need focus

on service quality as a core competitive strategy (Chaoprasert and Elsey, 2004). Moreover,

banks all over the world offer similar kinds of services, and try to quickly match their

competitors‘ innovations. It can be noted that customers can perceive differences in the

quality of service (Chaoprasert and Elsey, 2004). Moreover, customers evaluate banks‘

performance mainly on the basis of their personal contact and interaction (Gronroos, 1990).

Moreover, many scholars agree that service quality can be decomposed into two major

dimensions (Gronroos, 1984; Lehtinen and Lehtinen, 1982). The first is referred to by

Zeithaml et al. (1985) as ―outcome quality‖ and the second by Gronroos (1984) as ―technical

quality‖. However, the first dimension is concerned with what the service delivers and on the

other hand; the second dimension is concerned with how the service is delivered: the process

that the customer went through to get to the outcome of the service.

The study of McCleary and Weaver (1982) indicated that good service is defined on the basis

of identification of measurement behaviours that are important to customers. The study of

Newman and Cowling (1996) reports that two British banks used the SERVQUAL model and

this model improved quality of service, as well as both banks enjoying substantial increases in

profit. Moreover, Zeithaml (2000) also found evidence about the influences of service quality

on profits and Heskett et al. (1997) argued that a ―direct and strong‖ relationship exists among

service quality, customer satisfaction and profitability.Vimi and Mohd (2008) undertook a

study of the determinants of performance in the Indian retail banking industry based on

perception of customer satisfaction.

The finding of the study reinforces that customer satisfaction is linked with performance of

the banks. Berry (1980) along with Booms and Bitner (1981) argue that, due to intangible

nature of services, customer use elements associated with the physical environment when

evaluating service quality. Levitt (1981) proposes that customers use appearances to make

judgements about realities. Hostage (1975) believes that a service firm‘s contact personnel

comprise the major determinants of service quality, while Lewis and Booms (1983) propose

P a g e | 21 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

that service quality resides in the ability of the service firm to satisfy its customer needs i.e.

customer satisfaction.

Updated Products:

From the beginning of the 1990s until the middle of July 2007, change in the banking industry

was driven by the twin forces of deregulation and technological change. Updated products

refer to the use of information and communication technology by banks to provide services

and manage customer relationship more quickly and most satisfactorily (Charity-Commission,

2003). Burr (1996) describes it as an electronic connection between the bank and the

customer in order to prepare, manage and control financial transactions. Electronic banking

according to Al-Abed (2003) is an umbrella term for the process by which a customer may

perform banking transactions electronically without visiting a brick-and-mortar institution.

Lustsik (2004) describes electronic banking as a variety of the following platforms: Internet

banking, telephone banking, TV-based banking, mobile phone banking, and PC banking.

Banks customers‘ taste and desire have begun to raise the stakes of expectation of exceptional

services. Customers want to transact their banking transactions at any time and location

convenient for their life-style. They want to pay their regular household bills, buy and sell

stocks and shares (Carse, 1999).

Historically, banks have taken the attitude that they will provide customers with the services

and products that they, the banks, wish to provide. In order to survive both from domestic and

the increasing level of global cross-border competition, banks need to change their process of

servicing their customers. Firstly, to capture and retain the most profitable customers and

secondly to redirect unprofitable customers into service channels which can limit the costs and

maximise potential revenues (Mols, 1998).

Charges:

Data from private vendors indicate that average fees for insufficient funds, overdrafts, returns

of deposited items, and stop payment orders have risen by 10 percent or more since 2000,

while others, such as monthly account maintenance fees, have declined. During this period,

the portion of depository institutions income derived from noninterest sources—including fees

on savings and checking accounts—varied but increased overall from 24 percent to 27

percent. Changes in both consumer behavior, such as making more payments electronically,

and practices of depository institutions are likely influencing trends in fees, but their exact

effects are unknown.

Employee Behavior:

Employees are key stakeholders in value delivery and brand/supplier success, and they

frequently represent the difference between positive experiences or negative experiences and

whether customers stay or go. It has been found that employee commitment and advocacy

P a g e | 22 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

behavior have a direct and profound relationship to the loyalty of customers, and also to

corporate sales and profitability.

Work environment influences the way how employees feel about their company, boss, and co-

workers, and they impact the productivity, satisfaction, and intent to turnover of the workers

(Ferris & Kacmar, 1992). Drory and Romm (1988) In fact, the Drory and Romm study found

that employees‟ perception of employee behavior are dependent upon circumstances and that

as circumstances or elements of a situation vary so do perceptions regarding the politics.

Gerald.R.Ferris, Dwight.D.Frink (1996) studied Politics as a potential source of stress in the

work environment.

Customer Satisfaction:

According to the disconfirmation paradigm, customer satisfaction is understood as the

customer‘s emotional or feeling reaction to the perceived difference between performance

appraisal and expectations (e.g., Oliver 1980; Rust, Zahorik, and Keiningham 1996; Yi 1990).

Several studies provide evidence for the significant influence of satisfaction on loyalty and

word-of-mouth communication. However, more recent studies suggest the impact of

satisfaction on customer loyalty is rather complex (e.g., Bloemer and Kasper 1994; Oliva,

Oliver, and MacMillan 1992; Oliver 1999; Reichheld 1993; Stauss and Neuhaus 1997).

In their service profit chain model, Heskett et al. (1994) proposed customer loyalty to be the

result of a complex causal chain. Although satisfaction is modeled as the only immediate

antecedent of loyalty, other key drivers of loyalty include service quality, employee loyalty,

employee satisfaction, and internal service quality. Several (but not all) of the relationships

hypothesized in the service profit chain model have been confirmed empirically by Loveman

(1998).

Relationship quality is generally considered to be composed of satisfaction and commitment.

Drawing on Hennig-Thurau and Klee (1997), we postulate satisfaction to positively influence

commitment. A high level of satisfaction provides the customer with a repeated positive

reinforcement, thus creating commitment-inducing emotional bonds. In addition, satisfaction

is related to the fulfillment of customers‘ social needs, and the repeated fulfillment of these

social needs is likely to lead to bonds of an emotional kind that also constitute commitment

(Hennig-Thurau and Klee 1997).

The relevance of satisfaction in gaining loyal customers and generating positive word-of-

mouth is largely undisputed (e.g., Anderson and Sullivan 1993; Oliver 1996). Indeed, studies

have found satisfaction to be a (and often the) leading factor in determining loyalty (e.g.,

Anderson and Fornell 1994; Rust and Zahorik 1993). Similarly, satisfaction has been

identified as a key driver in the generation of (positive) customer word-of-mouth behavior

(e.g., File, Cermak, and Prince 1994; Yi 1990).

P a g e | 23 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Conceptual Framework:

The framework for the projected study is presented below:

Figure 1: Framework of Research Variable and their Relationships

Service Quality

Updated Products

Charges

Employee Behavior

Customer Satisfaction

Independent Variables

Dependent Variable

P a g e | 24 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Research Questions and Hypothesis:

RESEARCH QUESTIONS

Q1: Does service quality effect customer satisfaction in the context of UCB?

Q2: Does updated products effect customer satisfaction in the context of UCB?

Q3: Does charges effect customer satisfaction in the context of UCB?

Q4: Does employee behavior effect customer satisfaction in the context of UCB?

HYPOTHESIS

H1: Service quality effect customer satisfaction in the context of UCB.

H2: Updated products effect customer satisfaction in the context of UCB.

H3: Charges effect customer satisfaction in the context of UCB.

H4: Employee Behavior effect customer satisfaction in the context of UCB.

P a g e | 25 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Methodology:

Research design:

The projected framework (Figure: 1) represented the outline and arrangement of relationships

among the set of considered variables. The purpose of the study was to measure correlations

among variables. That‘s why it is a causal studies. More specifically it is an ex post facto

study because this study involves after the fact report on what happened to the measured

variables. With the above findings in the literature, this study aims to inspect the possible

relationships among service quality, updated products, charges, employee behavior and

customer satisfaction with organizational performance.

Sampling:

Sample unit:

In this study as a researcher I found some factor really that whether effects on

customer satisfaction or not. To get proper satisfaction idea from customers i targeted the

population who has an experience dealing with UCB. Our sampling technique will be simple

random sampling under the probability sampling method so that we can select randomly from

our existing customers. Cooper and Schindler (2003) stated that in this type of probability

sampling method each population element is known and has an equal chance of selection.

Sample Size:

Sample size relates to how many people to pick for the study. For this kind of study

researcher need to do select a sample size. I picked both male and female from different ages

and professional back ground and the sample size was N=40.The study will be conducted only

in some branches of Dhaka city due to time and budget constraints. Our research is a

Quantitative Research.

Sample Procedure:

Their as a researcher i used probability sampling to collect information. We have used

purposive probability sampling to know the characteristics or experiences, attitudes,

perception of participants. Here i selected participants randomly from UCB and give them the

questionnaire so that we can know about all those characteristics.

P a g e | 26 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Instruments:

Questionnaires will permit us to gather information that cannot be found elsewhere from any

secondary information such as books, newspapers and internet resources. So the questionnaire

survey is the most successful method for this study to collect the data. We used a structured

questionnaire. In a structured questionnaire, quantitative data is required. Because of this

reason, the researcher will use questionnaire. According to interval scale the response choices

will be arranged. There are Five (5) response choices. Five-point of Liker type scales were

used in all measures. This are-

Data Collection, Types of Data and Sources:

There are two types of data collection Primary Data & Secondary Data. Primary Data are

those collected for the first time .Secondary Data are those which have already been collected

and analyzed by someone else. In the context of UCB, as researchers I used primary data to

examine the research problem and verify hypothesis. As a researcher I use questionnaire

method to collect data from the primary sources. Because this research work is exclusively

carry out for Bank. In this study mostly primary data will be used to draw a recommendation.

We will confirm our respondents that all the data collected from them will be kept

confidential and exclusively used for academic purposes and their individual identity would

be kept undisclosed individuals, each taking Twenty Five (25) questionnaires to be filled out

by respondents from the devised sample. While filling out the questionnaires the researchers

assisted the respondents to get a better idea of their actual behaviors to minimize the margin

of error.

1 = Strongly Disagree

2= Disagree

3= Neither Disagree nor Agree

4= Agree

5= Strongly Agree

P a g e | 27 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Data Analysis:

Frequencies analysis:

The sample consists of 32 male and 08 female customers. 80% of male and 20% of female

customers participates in this survey which is shown at below.

Among the responding 08 customers age was between 15-25 years, 12 customers age was

between 26-35 years, 15 customers age was between 36-45 years and 5 customers age was

between 46 and above which is shown below.

There are four income ranges. 15% respondents were in 15000-20000 taka range, 35%

respondent was in the range of 21000-30000 taka, 27.5% respondent was in the range of

31000-40000 and 22.5% respondent was in the range of more than 41000 taka.

P a g e | 28 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Crosstabs Analysis

We survey 40 respondents with different gender, age and income. The resonance rate is 100%.

Table shows that between 15000-20000 income ranges there are 4 male and 2 female. Again

between 21000-30000 income ranges there are 11 male and 3 female. In 31000-40000 income

ranges there are 9male and 2 female. And in the income of above 41000 ranges there are 8

male and 1 female.

P a g e | 29 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Correlation analysis

Correlation analysis was conducted on all variables to explore the relationship between

variables. The bivariate correlation procedure was subject to a two tailed of statistical

significance at two different levels highly significant (p<.01) and significant (p<.05).

According to Nadim Jahangir the classification of correlation coefficient is as follows:

0.0 to 0.2 Very weak, negligible

0.2 to 0.4 Weak, low

0.4 to 0.7 Moderate

0.7 to 0.9 Strong, high, marked

0.9 to 1.0 Very strong, very high

P a g e | 30 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Relationship between Service quality and customer satisfaction:

According to Spearman correlation coefficient between service quality and customer

satisfaction is 0.638 shows positive relationship between two variables. Now we have to test r

for other calculations or comparisons.

We know,

√

= 5.1074

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we cannot accept the null hypothesis as T value don‘t falls in (-

2.021 to +2.021) and accept alternative hypothesis.

So according to Spearman Correlation test there is a relationship between service quality and

customer satisfaction, which means that service quality effect customer satisfaction in context

of UCB.

P a g e | 31 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

According to Pearson correlation coefficient between service quality and customer

satisfaction is 0.656 shows positive relationship between two variables. Now we have to test r

for other calculations or comparisons.

We know,

√

= 5.3741

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we cannot accept the null hypothesis as T value don‘t falls in (-

2.021 to +2.021) and accept alternative hypothesis.

So according to Pearson Correlation test there is a relationship between service quality and

customer satisfaction, which means that service quality effect customer satisfaction in context

of UCB.

P a g e | 32 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

According to Kendall's tau_b correlation coefficient between service quality and customer

satisfaction is 0.504 shows positive relationship between two variables. Now we have to test r

for other calculations or comparisons.

We know,

√

= 3.5971

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we cannot accept the null hypothesis as T value don‘t falls in (-

2.021 to +2.021) and accept alternative hypothesis.

So according to Kendall's tau_b Correlation test there is a relationship between service

quality and customer satisfaction, which means that service quality effect customer

satisfaction in context of UCB.

P a g e | 33 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

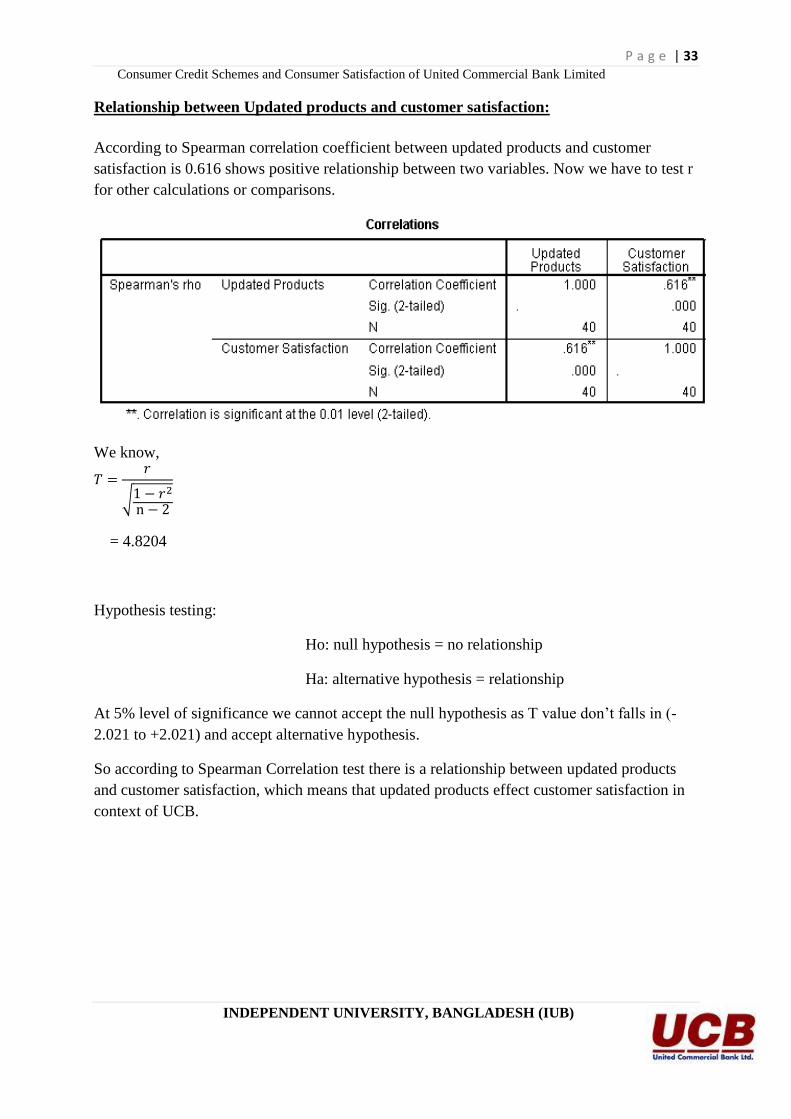

Relationship between Updated products and customer satisfaction:

According to Spearman correlation coefficient between updated products and customer

satisfaction is 0.616 shows positive relationship between two variables. Now we have to test r

for other calculations or comparisons.

We know,

√

= 4.8204

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we cannot accept the null hypothesis as T value don‘t falls in (-

2.021 to +2.021) and accept alternative hypothesis.

So according to Spearman Correlation test there is a relationship between updated products

and customer satisfaction, which means that updated products effect customer satisfaction in

context of UCB.

P a g e | 34 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

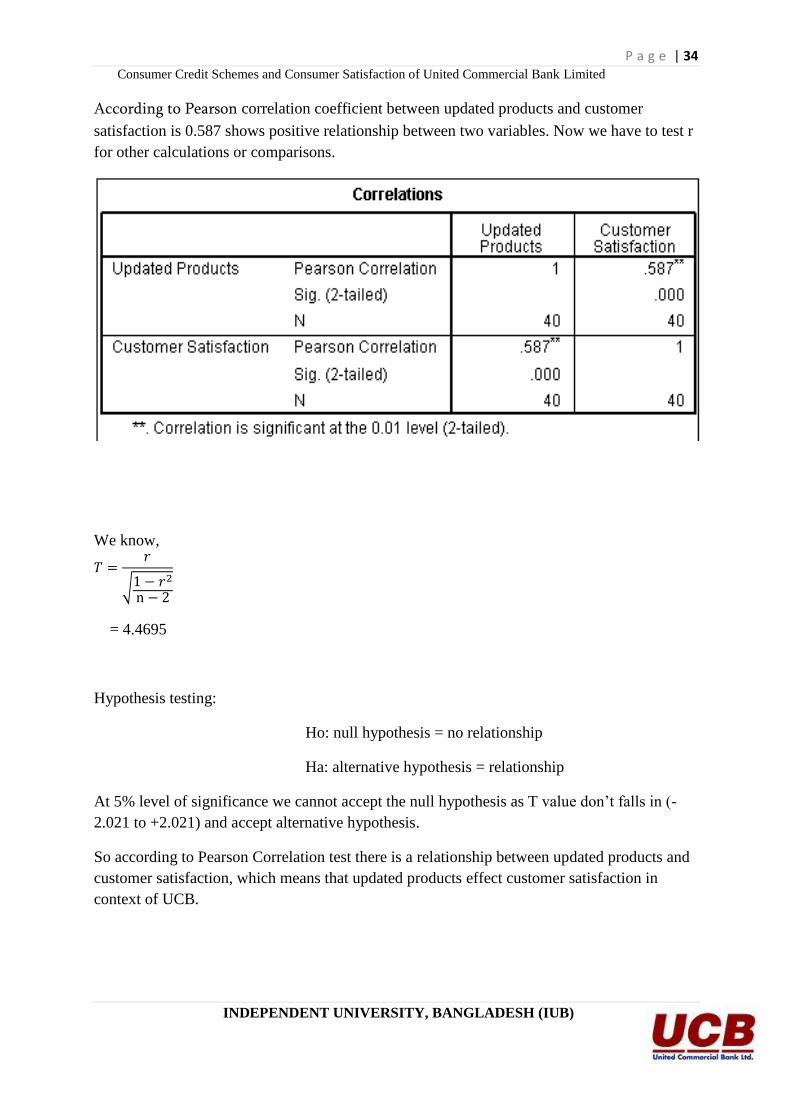

According to Pearson correlation coefficient between updated products and customer

satisfaction is 0.587 shows positive relationship between two variables. Now we have to test r

for other calculations or comparisons.

We know,

√

= 4.4695

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we cannot accept the null hypothesis as T value don‘t falls in (-

2.021 to +2.021) and accept alternative hypothesis.

So according to Pearson Correlation test there is a relationship between updated products and

customer satisfaction, which means that updated products effect customer satisfaction in

context of UCB.

P a g e | 35 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

According to Kendall's tau_b correlation coefficient between updated products and customer

satisfaction is 0.487 shows positive relationship between two variables. Now we have to test r

for other calculations or comparisons.

We know,

√

= 3.4372

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we cannot accept the null hypothesis as T value don‘t falls in (-

2.021 to +2.021) and accept alternative hypothesis.

So according to Kendall's tau_b Correlation test there is a relationship between updated

products and customer satisfaction, which means that updated products effect customer

satisfaction in context of UCB.

P a g e | 36 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Relationship between charges and customer satisfaction:

According to Spearman correlation coefficient between updated products and customer

satisfaction is -0.208 shows negative relationship between two variables. Now we have to test

r for other calculations or comparisons.

We know,

√

= -1.3108

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we can accept the null hypothesis as T value falls in (-2.021 to

+2.021) and reject alternative hypothesis.

So according to Spearman Correlation test there is no relationship between charges and

customer satisfaction, which means that charges is not effect customer satisfaction in context

of UCB which reflect that customers are not satisfied by charges in UCB.

P a g e | 37 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

According to Pearson correlation coefficient between charges and customer satisfaction is -

0.018 shows negative relationship between two variables. Now we have to test r for other

calculations or comparisons.

We know,

√

= -0.1109

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we can accept the null hypothesis as T value falls in (-2.021 to

+2.021) and reject alternative hypothesis.

So according to Pearson Correlation test there is no relationship between charges and

customer satisfaction, which means that charges is not effect customer satisfaction in context

of UCB which reflect that customers are not satisfied by charges in UCB.

P a g e | 38 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

According to Kendall's tau_b correlation coefficient between charges and customer

satisfaction is -0.155 shows positive relationship between two variables. Now we have to test

r for other calculations or comparisons.

We know,

√

= -0.9671

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we can accept the null hypothesis as T value falls in (-2.021 to

+2.021) and reject alternative hypothesis.

So according to Kendall's tau_b Correlation test there is no relationship between charges and

customer satisfaction, which means that charges is not effect customer satisfaction in context

of UCB which reflect that customers are not satisfied by charges in UCB.

P a g e | 39 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Relationship between employee behavior and customer satisfaction:

According to Spearman correlation coefficient between employee behavior and customer

satisfaction is 0.352 shows positive relationship between two variables. Now we have to test r

for other calculations or comparisons.

We know,

√

= 2.3182

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we cannot accept the null hypothesis as T value don‘t falls in (-

2.021 to +2.021) and accept alternative hypothesis.

So according to Spearman Correlation test there is a relationship between employee behavior

and customer satisfaction, which means that updated products effect customer satisfaction in

context of UCB.

P a g e | 40 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

According to Pearson correlation coefficient between employee behavior and customer

satisfaction is 0.549 shows positive relationship between two variables. Now we have to test r

for other calculations or comparisons.

We know,

√

= 4.0490

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we cannot accept the null hypothesis as T value don‘t falls in (-

2.021 to +2.021) and accept alternative hypothesis.

So according to Pearson Correlation test there is a relationship between employee behavior

and customer satisfaction, which means that updated products effect customer satisfaction in

context of UCB.

P a g e | 41 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

According to Kendall's tau_b correlation coefficient between employee behavior and

customer satisfaction is 0.265 shows positive relationship between two variables. Now we

have to test r for other calculations or comparisons.

We know,

√

= 1. 6941

Hypothesis testing:

Ho: null hypothesis = no relationship

Ha: alternative hypothesis = relationship

At 5% level of significance we can accept the null hypothesis as T value falls in (-2.021 to

+2.021) and reject alternative hypothesis.

So according to Kendall's tau_b Correlation test there is no relationship between employee

behavior and customer satisfaction, which means that employee behavior is not effect

customer satisfaction in context of UCB which reflect that customers are not satisfied by

behavior of employees in UCB.

P a g e | 42 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Reliability Analysis:

The reliability of a scale that predicts a variable should be measured in order to see whether it

actually affects the dependent variable. Reliability is the extent to which measurement of

particular measure of particular test are repeatable. If the reliability of scale for any particular

variable is below .5 then it should be deemed unacceptable. The most highly recommended

measure of internal consistency is provided be cronbach‘s Alpha (α) as it provides a good

reliability estimate in most situations. 50-.60 coefficient or cronbach‘s alpha is sufficient. In

this study the coefficient alpha for different constructs were computed using the reliability

procedure in SPSS (version 17.0).

The cronbach‘s alpha of service quality is 0.811 which means it is highly reliable.

Updated products are also fall to the reliability test because cronbach‘s alpha is 0.811. It is

between the standard, so it is reliable.

P a g e | 43 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

The reliability of charges is 0.784 which is between the standard, so it is reliable.

Again the cronbach‘s Alpha (α) of employee behavior is 0.625 which is reliable.

Again the cronbach‘s Alpha (α) of customer satisfaction is 0.800 which is reliable.

P a g e | 44 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Significance of the Study:

Business significance:

Our research hopefully will help various corporations to be concerned about the present

condition of UCB as a bank. Because a trend has been changed over the past few years,

customers‘ attitude toward business products or service also changed. So, sticking with the

obsolete business plan will no longer be effective for making profit. Various law suits has

already been posted against MNC‘s as well as national companies. So it would be really

beneficial for the company s to change their policy and get concerned about the customer

satisfaction rather than making profit .Our study reveals the relationship between the customer

satisfaction with the service quality, updated products, charges and employee behavior

respectively: anyone who will go through these, get crystal clear idea about the significance of

customer satisfaction.

Academic significance:

We know, now a day research is also used for academic purpose. While any student is going

for making any new business plan they are must needed to go for a research. Thus faculties

also need to study and implement those studies (researchers) to their students so that it can

help the students for their study. As my research is based on customer satisfaction this

research may helpful for students who are keen to know about UCB recent position in front of

customers. Students will also get the knowledge about current position of UCB as a private

bank in Bangladesh through this research.

Implication for future research:

As i mention earlier, our research will help various corporations thus far, it could also be

effective and efficient analysis for the future researchers. I analysis various kinds of data that

is given in various journals, newspapers, govt.bureaus and websites so, future researchers

would get the information about the scale that has been used in my study and hypothesis

testing will give them an idea whether there is a relationship between our variables or not and

reliability tests will give an information whether our question adjust with the variable.

P a g e | 45 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Recommendations:

United Commercial bank Limited has an efficient and excellent credit management

team and performing with great expertise and care. There are some limitations that can

be overcome by some measures to make the performance outstanding. There are some

suggestions for United Commercial banks consumer credit management team from my

observation.

Proper consumers‘ credit budget for each branch should be established. A budget is a

record that shows the flow of money in and out of the Branch. Budget is necessary

because it gives customers a clear view of the branch Consumers‘ Credit.

United Commercial Bank training institute should introduce training program on

Consumer Credit of their executives to provide unique solution for their financial

situation.

Strengthening the Marketing ability. The present marketing ability to pursue the

consumers is not so strong. So UCBL should increases the promotion activities as

possible.

UCBL should develop short procedure for taking the consumer credit loan. The

processing time for taking consumer credit scheme should simple as possible.

Introducing the new feature of product may attract the customer to take loan from the

UCBL.

Introducing the appropriate client judgment system: the existing client judgment

system for consumer evaluation is not so rigorous. The system should be developed.

Stopping the diversion of loan: the major portion of the loan goes to the pocket of

those who are wealthy. This means that the targeted people are not getting loan. The

diversion of loan is also prevailing. For example- the consumer taking loan by

showing a quotation of furniture but he is not buying that item. So the monitoring

system should be improved.

Credit officer measures the risk associated with the credit facility. He should not be

liberal in this respect; he should strictly follow the credit evaluation principle followed

by the bank. The analysis should contain information about the borrower, credit

purpose, credit repayment sources, details of collateral security with valuation and

guarantee.

The ATM facility of UCBL is weak than other competitor banks so they should try to

improve this facility as soon as possible.

P a g e | 46 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Conclusion:

As an internee of UCBL. I have truly enjoying my internship from the learning and

experience viewpoint. I am confident that this three months internship program at UCBL will

definitely help me to realize my further carrier in the job market.

As there are lots of local and foreign banks in Bangladesh the UCBL is promising commercial

Bank among them. In this competitive market UCBL has to compete not only the others

commercial banks but also with the public Bank. UCBL is more capable of contributing

towards economic development as compared with other bank. UCBL invested more funds in

export and import business. It is obvious that the right thinking of this bank including

establishing a successful network over the country and increasing resources will be able to

play a considerable role in the portfolio of development. Success in the banking business

largely depends on effective lending. Less the amount of loan losses, the more the income will

be from Credit operations the more will be the profit of the UCBL Limited and here lays the

success of Credit Financing.

During the course of my practical orientation I have tried to learn the practical banking

activities to realize it with my theoretical knowledge, which I have greathearted and going to

acquire from various courses of my BBA program.

P a g e | 47 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

References:

Jahangir, Nadim. (2003). Perceptions of Power: A Cognitive Perspective of

Natinalised Commercial Banks in Bangladesh, Dhaka: SUBARNA.

http://www.ucbl.com

Several Booklets from UCB

Seeral Newsletter from UCB

Credit Operational Manual of UCB

Chowdhury, A.H.M., Nurul Islam and T.A. Chowdhury (1992). ―Financial

liberalization in Bangladesh, Conceptual Issues and Impact on Banking financial

institutions‖ Bank Parikrama, Vol 18, No.3 &4, Sep. & Dec. P.59.

Howard R. Goldsmith, A guide To Growth, Profits and Market share, 2004

Englewood Cliffs, NJ: Prentice-Hall

Bagozzi, R. P., Tybout, A. M., Craig, C. S., & Sternthal, B. (1979). The construct

validity of the tripartite classification of attitude. Journal of Marketing Research, 16,

88 – 95.

Breckler, S. J. (1984). Empirical validation of affect, behaviour and cognition as

distinct attitude Ethical Consumer Research Association: About practice: A review

and recommended two-step approach. Psychological Bulletin, 103, 411 – 423.

Bangladesh Bank. (2010). Schedule Bank Statistics, Various issues. Dhaka,

Bangladesh Bank.

P a g e | 48 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

Appendix

QUESTIONNAIRE

Hello!! We are conducting a survey to find out information regarding ―Consumer Credit

Schemes and Consumers satisfaction of United Commercial Bank Ltd (UCBL).”There is

no right or wrong answer. All information will be used for the purpose of this specific

research. This research is conducted for academic purposes only. So please do not hesitate to

answer. Your information will be kept confidential.

Personal Information

Male Female

Age: 15-25

26-35

36-45

46 and above

Occupation ________________

Income per month:

15000-20000 Taka

21000-30000 Taka

31000-40000 Taka

41000 and above

P a g e | 49 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

1= Strongly Disagree 4= Agree

2= Disagree

3= Neither Disagree nor Agree 5= Strongly Agree

Service quality:

1. UCBL is an excellent bank to have banking services. 1 2 3 4 5

2. The procedure of our services and the transactions are clear to

you.

1 2 3 4 5

3. You feel safe dealing with us. 1 2 3 4 5

4. The service quality should be improved. 1 2 3 4 5

5. UCBL‘s services are up to mark. 1 2 3 4 5

Updated Products:

6. Products are up to date 1 2 3 4 5

7. The installment policy is easy. 1 2 3 4 5

8. External appearance of bank is good. 1 2 3 4 5

9. Availability of ATM in several locations. 1 2 3 4 5

Charges:

10. Compared to our quality, we charges extra. 1 2 3 4 5

11. We do not have any hidden charges. 1 2 3 4 5

12. Sometimes you get services at cheaper price than our listed

rate.

1 2 3 4 5

13. The time limit to repay the payables should be increased. 1 2 3 4 5

14. The interest rate charged on credit scheme is high. 1 2 3 4 5

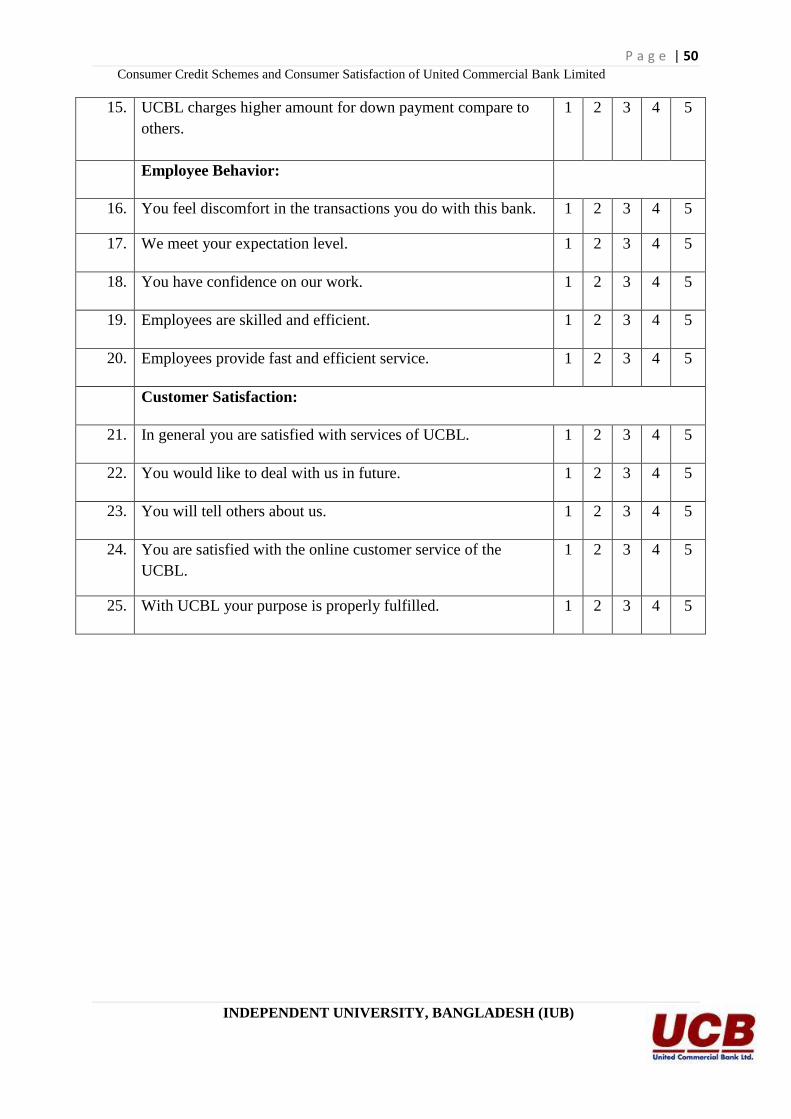

P a g e | 50 Consumer Credit Schemes and Consumer Satisfaction of United Commercial Bank Limited

INDEPENDENT UNIVERSITY, BANGLADESH (IUB)

15. UCBL charges higher amount for down payment compare to

others.

1 2 3 4 5

Employee Behavior:

16. You feel discomfort in the transactions you do with this bank. 1 2 3 4 5

17. We meet your expectation level. 1 2 3 4 5

18. You have confidence on our work. 1 2 3 4 5

19. Employees are skilled and efficient. 1 2 3 4 5

20. Employees provide fast and efficient service. 1 2 3 4 5

Customer Satisfaction:

21. In general you are satisfied with services of UCBL. 1 2 3 4 5

22. You would like to deal with us in future. 1 2 3 4 5

23. You will tell others about us. 1 2 3 4 5

24. You are satisfied with the online customer service of the

UCBL.

1 2 3 4 5

25. With UCBL your purpose is properly fulfilled. 1 2 3 4 5

![[Internship Report] folder... · Web view[Internship Report] [Internship Report] 3 [Internship Report] Prince Mohammed Bin Fahd University College of Computer Engineering and Science](https://static.fdocuments.us/doc/165x107/5adbc5e37f8b9add658e5f6e/internship-report-folderweb-viewinternship-report-internship-report-3-internship.jpg)