International Tax Law I - UniBg

82

International Tax Law I (2019 – 2020) Università degli studi di Bergamo & Eötvös Loránd Budapest [email protected] Prof. em. KU Leuven

Transcript of International Tax Law I - UniBg

International Tax Law I (2019 – 2020)

Università degli studi di Bergamo &

Eötvös Loránd Budapest

Prof. em. KU Leuven

Content International Taxation

• International tax rules for income and capital &

double and multiple taxation

• Unilateral measures to relieve double taxation

• DOUBLE TAX CONVENTIONS (OECD & UN)

Content Double Tax Conventions (DTC)

• History

• Integration of DTC’s into national law, Objectives

& interpretation of DTC’s,

• Scope of application of DTC’s (persons & taxes)

• Distributive rules of taxing power

• Mechanisms of relief of double taxation

• Non-discrimination

• Mutual agreement procedure

• Exchange of information

• New art. 29: anti-avoidance (BEPS)

Content International Taxation

• 2015 BEPS action plan, 2017 Multilateral

Convention: a fundamnetal change of paradigm in

international taxation.

• Basic concepts of international taxation for sales,

turn-over & VAT: principles of origin & destination,

elimination of cross-border taxation and export

subsidies.

• Customs duties

• WTO principles to eliminate trade and tax barriers

International tax rules & double taxation

• In order to be able to tax a state needs a nexus

(link or connection) to apprehend the person of

the taxpayer or the matter of taxation (tax base).

• To be subject to a tax jurisdiction a taxpayer

needs a nexus with a state, either in person, or

through one of the sources of the matter of

taxation. If there is no nexus, there is neither an

obligation, nor a practical way to contribute (or to

collect) to the public finances of a state.

International tax rules & double taxation

Basic tax pattern: residence as nexus for person

• Most developed countries tax on the basis of

residence, i.e. individuals and entities established

in their jurisdiction. Taxation of residents is their

worldwide income regardless where the source

of that income is being situated. This is in

accordance with the ability to pay principle.

• A few countries tax residents on a strict territorial

basis: foreign source income is not taxed.

International tax rules & double taxation

Basic tax pattern: source as nexus for income

• Countries also tax specific categories of income

that have their source in their territory. Taxation at

source is effectuated on the limited basis of that

specific category of income. Tax is often on a

gross basis, regardless of where the beneficiary of

such income is established, whether he is taxed

on this income and regardless whether the

beneficiary has other income elsewhere.

International tax rules & double taxation

Nexus for the person of the taxpayer

• Individuals: domicile, residence, habitual abode,

address, centre of social & economic interest,

nationality or citizenship.

• Legal entities: law of incorporation, registered

office, place of central or effective management

(POEM).

• Regardless of where income is sourced.

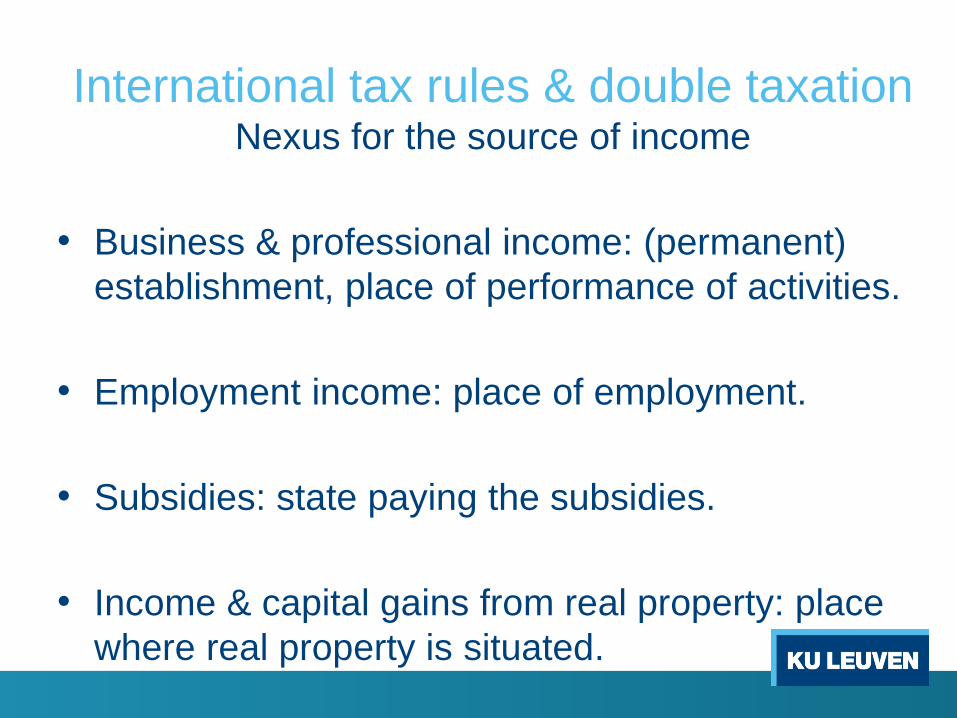

International tax rules & double taxationNexus for the source of income

• Business & professional income: (permanent)

establishment, place of performance of activities.

• Employment income: place of employment.

• Subsidies: state paying the subsidies.

• Income & capital gains from real property: place

where real property is situated.

International tax rules & double taxationNexus for the source of income

• Dividends, interests & royalties: place where the

debtor or payor is located.

• Capital gains from personal property: place where

assets are being held.

• New source?: for services income and royalties

for intangibles: the market where services are

performed or intangibles are used.

International tax rules & double taxation

Double taxation

• Combination of the two different rules of personal

nexus in one jurisdiction and source nexus in

another jurisdiction result into double taxation.

• There are two forms of double taxation: double

juridical taxation and double economic taxation.

International tax rules & double taxation

Double juridical taxation

• Double juridical taxation means that the same or a

similar tax is imposed twice (by two different

states) on the same taxpayer, on the same basis

(income).

International tax rules & double taxation

Causes of double juridical taxation

• The combination of full and unlimited tax

liability of the taxpayer in his country of

residence and a limited tax liability on part of

the same income in the country of source.

International tax rules & double taxation

Causes of double juridical taxation

• Dual residence, i.e. overlapping concepts of

residence on the nexus for full and unlimited tax

liability: residence, domicile, nationality, POEM.

International tax rules & double taxation

Causes of double juridical taxation

• Dual source, i.e. conflicts on limited tax liability

because of conflicts on the concept of source of,

when income of the same taxpayer is sourced

in several states: shareholder in France receives

dividend from co. incorporated and registered in

NL and with POEM in Belgium. WHT in NL and B.

International tax rules & double taxation

Causes of double juridical taxation

• Different interpretation of identical facts, resulting in the

application of different allocation rules:

• Ex.: remuneration is qualified as employment income in

one state and pension income in another. In tax treaties

employment income taxed in the work state and pension

income in the residence state.

• Ex.: premium paid at redemption of a bond is qualified as

interest in one state and as capital gain in the other. In

tax treaties interest is taxable in the source state and

capital gains in the residence state.

International tax rules & double taxation

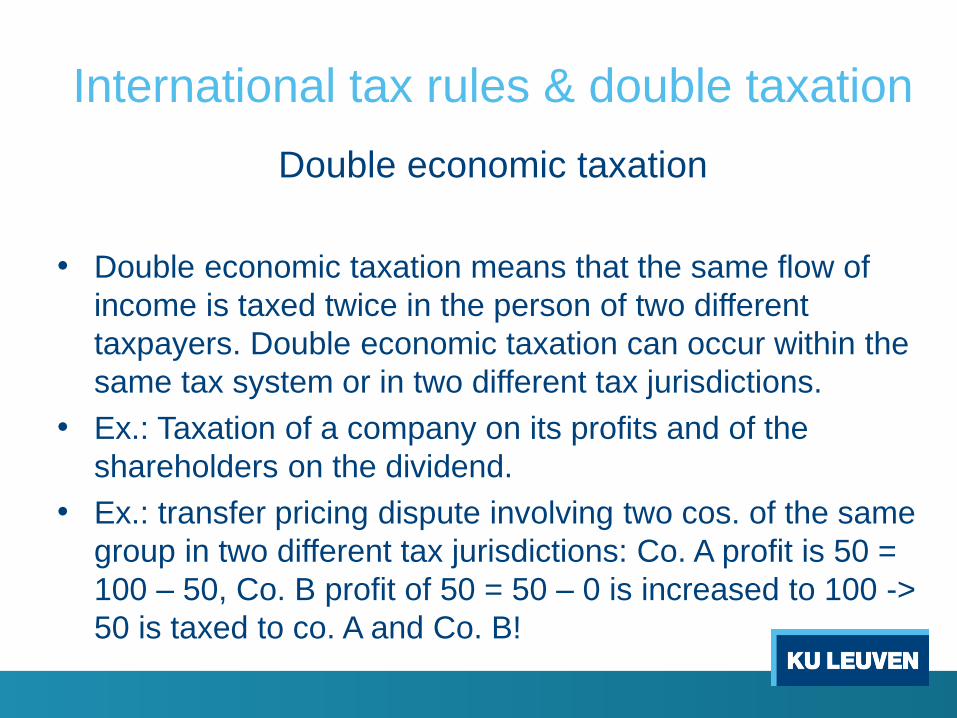

Double economic taxation

• Double economic taxation means that the same flow of

income is taxed twice in the person of two different

taxpayers. Double economic taxation can occur within the

same tax system or in two different tax jurisdictions.

• Ex.: Taxation of a company on its profits and of the

shareholders on the dividend.

• Ex.: transfer pricing dispute involving two cos. of the same

group in two different tax jurisdictions: Co. A profit is 50 =

100 – 50, Co. B profit of 50 = 50 – 0 is increased to 100 ->

50 is taxed to co. A and Co. B!

International tax rules & double taxation

International double taxation

• The core problem is not so much double taxation,

but double taxation resulting in excessive taxation

& the competitive disadvantage of double taxation

compared to single taxation.

• Historically double taxation has been challenged

(before WWII) before excessive taxation.

• There is no world standard for excessive taxation

cfr. Tax havens <-> high tax countries.

International tax rules & double taxation

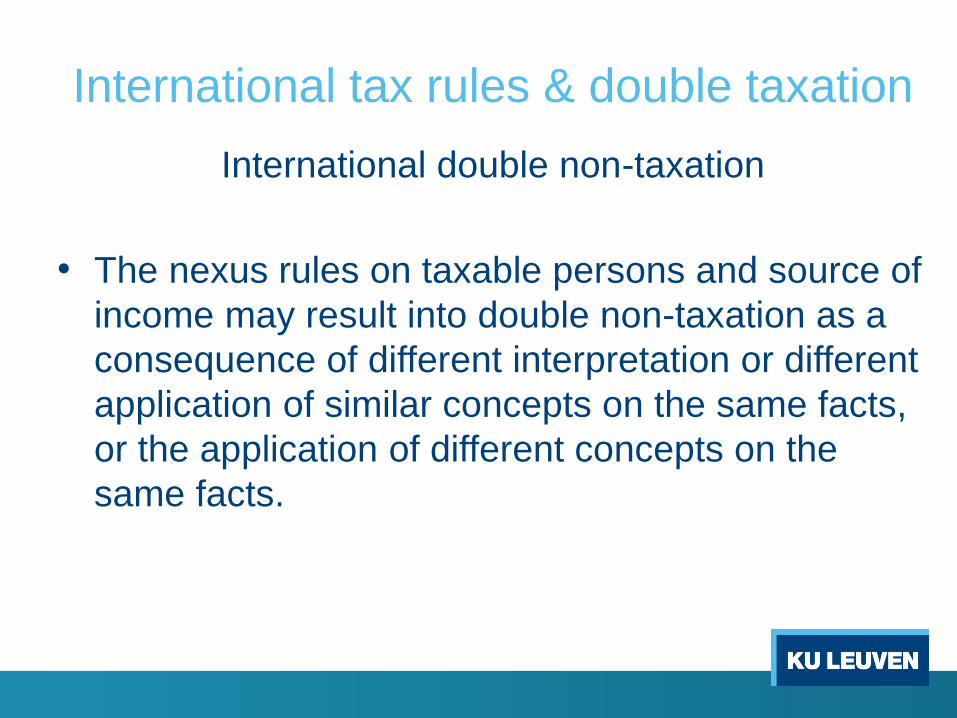

International double non-taxation

• The nexus rules on taxable persons and source of

income may result into double non-taxation as a

consequence of different interpretation or different

application of similar concepts on the same facts,

or the application of different concepts on the

same facts.

International tax rules & double taxation

International double non-taxation

• Ex.: Business income is taxable in state A, if PE >

12 months, while in B a PE is > 6 months.

Business income of PE of 9 months in A owned by

co. resident in B is not taxed in A and exempt in B.

• Ex.: severance pay is qualified as pension by

state of employment (taxable in residence state),

while it is qualified as employment income

(taxable in state employment) in state of

residence, i.e. no taxed in either state.

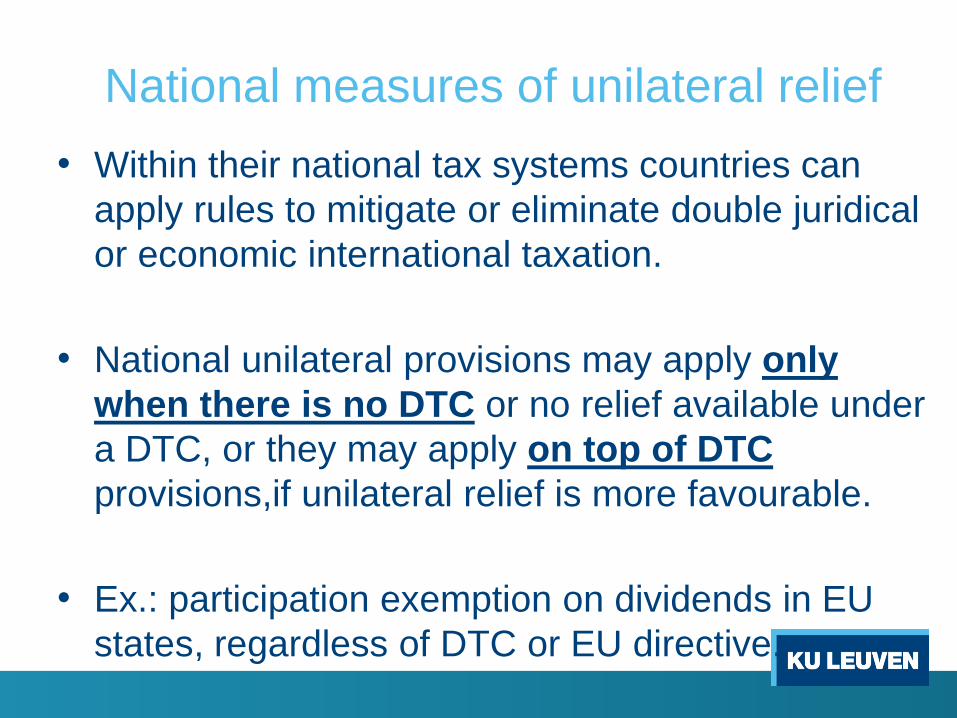

National measures of unilateral relief

• Within their national tax systems countries can

apply rules to mitigate or eliminate double juridical

or economic international taxation.

• National unilateral provisions may apply only

when there is no DTC or no relief available under

a DTC, or they may apply on top of DTC

provisions,if unilateral relief is more favourable.

• Ex.: participation exemption on dividends in EU

states, regardless of DTC or EU directive.

National measures of unilateral relief

• Territorial tax system: taxes only income sourced

within the tax jurisdiction.

• Strictly territorial tax system may still result in

double taxation: different transfer price between

associated cos. in two territorial juridictions.

• Deduction as an expense of the amount of foreign

tax paid from the tax base.

• Ex.: Foreign net profit 100, domestic net profit

500, foreign tax on 100 = 30. Domestic tax base

100-30 = 70 + 500. Double tax on 70.

National measures of unilateral relief

• Foreign tax credit: deduction of the amount of

foreign tax paid from the amount of domestic tax

due on foreign source income.

• Ex.: Foreign profit 100, tax 30% = 30. Domestic

profit 500, tax 40% = 200. Total taxable income in

residence state 600 x 0,4 = 240 – 30 = 210.

• Exemption of foreign source income.

• Ex.: Foreign profit 100, taks 30% = 30. Domestic

profit 500, tax 40% = 200. Total taxable income in

residence state 500, exempt 100.

Double tax conventions

History

• Historically tax rules can be found in treaties of

friendship, commerce and navigation (19 century)

with tax exemptions and equal treatment for non-

nationals. (US – Brunei 1850, US - Argentina

1853, Kanawaga convention 1854 between US -

Japan).

Double tax conventions

History

• The objective of these treaties was to end the old

tradition (Jewish quarters, Decima), whereby

foreigners were granted only limited access and

limited protection in a country to do business.

• The objective was not avoidance of double

taxation, but equal treatment of foreigners living in

the country compared to treatment of nationals for

business purposes. Cfr. non-discrimination

provision based on nationality in OECDMC.

Double tax conventions

History

• 19th. Century tax treaties in the Nord-Deutsche

Bund as part of the integration and unification

process in Germany. Treaty between Prussia and

Saxony (1869), Austria – Germany (1899) and

Austria-Hungary (1909).

• Objective is avoidance of double taxation based

on the place of real estate or the situs of business

activity and on residence (farming).

Double tax conventions

History

• After WWI the League of Nations was established

with a fiscal committee drafting a tax convention

on the basis of a report of 15.04.1923 by Bruins

(Rotterdam), Einaudi (Torino), Seligman

(Columbia) and Stamp (UK).

Double tax conventions

History

• Heated discussion on priority of residence or

source states for income tax. League of Nations

report 1925 with compromise: priority for

residence for personal income tax (business

income) and source for non-personal income tax.

• Studies in the History of Taxation, John Tiley ed. Vol. 6, chap. 1,

John Avery Jones, Sir Josiah Stamp and Double Income Tax.

Taxtreatieshistory.org

• Michael Graetz & Michael O’Hear, The “original intent” of US

International Taxation, Duke Law Journal, Vol. 46, 1021 (1997).

Double tax conventions

History

• League of Nations Fiscal Committee London &

Mexico, Draft Model Tax Convention 01.11.1946.

• In 1963 OECD Model Tax Convention, revised in

1977 and 1992 and many times thereafter.

Double tax conventions

History

• In 1966 Model Tax Convention of Inheritance

Taxes, revised in 1982.

• In 1980 UN Model Tax Convention, revised in

2001 and 2011. Largely follows OECD model, but

puts more emphasis on taxation in source

jurisdiction.

• Commentaries on OECD and UN model:

explanation of MC without binding legal force,

value of informed expert opinion.

Double tax conventions

History

• Multilateral tax conventions: 1983 Nordic

Multilateral Tax Convention, 1988 Convention on

Mutual Administrative Assistance in Tax Matters.

• 2002 TIEA’s: OECD Agreement on Exchange of

Information on Tax Matters

• 2012 IGA’s: intergovernmental agreements on

automatic Exchange of Information.

• National model conventions: US, UK,NL.

OECD model convention

Objectives

• In the 1963/1977 OECD “MC on income and

capital for the avoidance of double taxation” the

reduction or elimination of double taxation was

the major if not the only aim of the MC.

OECD model convention

Objectives change in BEPS action 6

• To the title of the MC for the elimination of double

taxation is added: “the prevention of tax

avoidance and evasion”.

OECD model convention

Objectives change in BEPS action 6

• New preamble: “Intending to conclude Convention

for the elimination of double taxation … without

creating opportunities for non-taxation or

reduced taxation through tax evasion or

avoidance (including treaty shopping … aimed at

obtaining benefits for residents of third states.)

• The title and the preamble form part of the

context of the Convention and as such play a role

in the interpretation of the convention.

OECD model convention

Structure

• Persons covered (1)

• Taxes covered (2)

• Definitions (3-5)

• Allocation rules for different types of income (6-22)

- Income from immovable property (6)

- Business profits (7)

- International shipping and air transport (8)

- Arm’s length principle (9)

OECD model convention

Structure

• Allocation rules for different types of income

- Dividends (10)

- Interests (11)

- Royalties (12)

- Capital gains (13)

- Independent personal services (14 deleted)

- Employment income (15)

- Director’s fees (16)

OECD model convention

Structure

• Allocation rules for different types of income

- Artistes and sportsmen (17)

- Pensions (18)

- Government service (19)

- Students (20)

- Other income (21)

- Taxation of capital (22)

OECD model convention

Structure

• Methods elimination double juridical taxation (23)

• Non-discrimination rules (24)

• Mutual agreement procedure (25)

• Exchange of information (26)

• Assistance in collection of taxes (27)

• Tax status of diplomats (28)

• New anti-abuse provision, PP test (29)

• Extension, entry into force, termination (30-32)

OECD model convention

Integration of DTC in national law

• Integration of international treaties (including tax

treaties) in national law is a constitutional issue.

• There are monist and dualist states.

OECD model convention

Integration of DTC in national law

• In monist states the approval of the treaty has

direct effect.

• In dualist states the treaty has to be integrated in

the national legal system, by a national

legislative act. As long as it is not integrated it

has no effect: non-integration may delay

application of DTC.

OECD model convention

Integration of DTC in national law

• The question of integration of a DTC in national

law is different from the question of priority

between treaties and national law.

• Ratification in federal states may require approval

of all regional governments. Ex.: Belgium:

Brussels region has to ratify tax treaties.

OECD model convention

Priority of DTC over national tax law

• Constitution determines whether DTC integrated

in national law has priority on national tax law.

• In the US statutory law and treaties are of equal

status: lex posterior derogat priori.

• Most other countries accept that a treaty that has

been integrated into national law has in principle

priority over national statutory provisions: Ex.:

Canada explicit priority in implementing act.

Exception: Anti-avoidance rule in Australia.

OECD model convention

Priority of DTC over national tax law

• If international treaties, including DTC’s, have to

make any sense treaties must have priority over

national statutory tax law.

• Priority of DTC is grounded on its nature as lex

specialis in relation to domestic tax law. The DTC

determines whether the application of the national

tax law will be authorised in relation to competing

tax claims of other tax jurisdictions.

OECD model convention

Priority of DTC over national tax law

• Treaty has the same rank as constitutional rule

which remains valid even to posterior national law.

• Problem of the lex posterior: tax statutes change

frequently, while DTC’s are difficult to renegotiate

and remain valid for a long period of time. The

impact of a lex posterior is a question of

interpretation of treaties. If interpretation leads

to application in which domestic law prevails over

DTC -> infringement of international law.

OECD model convention

Priority of DTC over national tax law

• Priority of DTC cannot mean that a state is

prohibited from adapting its tax law for example to

protect its tax base and to prevent tax avoidance

or tax evasion.

• Ex.: Switch from exemption to credit in DE

Aussensteuergesetz, against tax avoidance: C-

298/05, Columbus Container.

OECD model convention

Priority of DTC ove national tax law

• If there is an interpretative provision in later

domestic law that specifically derogates from DTC

-> treaty override and DTC has priority.

• Ex. Abolition in domestic law of foreign tax credit

for individuals that was agreed in treaty: C-540/11,

Daniël Levvy, Carine Sebbag v Belgium,

19.09.2012.

OECD model convention

Priority of DTC over national tax law

• Later tax reforms should take into account

obligations under DTC’s and the scope of the

concept of tax avoidance is very important.

• If the national interpretation of treaties holds that

later domestic law, which derogates from DTC,

has priority on DTC -> treaty override.

OECD model conventionEffects of DTC

DTC does not create taxing rights

• States exercise full tax sovereignty and levy tax under their

national law on any person or source that is connected to

that State.

• States freely accept to limit the exercise of this tax

sovereignty in DTC.

• DTC only allocates taxing rights to states that have

effectively exercised these rights, it does not create

taxing rights.

OECD model convention

Effects of DTC

DTC does not create taxing rights

• If a DTC allocates the taxing power on income to one CS,

and that state does not tax that income according to its

national law, the DTC neither creates taxing rights for that

state, nor does it create taxing rights for the other C.S.

OECD model convention

Effects of DTC

DTC does not create taxing rights

• A DTC does not provide an independent legal basis for

taxing if there is no legal basis in its national law.

• The traditional rule is that if a CS does not exercise its

taxing right, the DTC does not fully apply and the other CS

can only exercise its taxing rights, when it has claimed a

specific reservation to that effect in the DTC.

OECD model convention

Effects of DTC

DTC does not create taxing rights

• For a domestic tax claim to exist under international law, a

state must fulfil an additional condition of having tax

jurisdiction under the DTC allocation rules.

• For an international tax liability to exist DTC rules of

allocation act as a condition on top of national rules. The

DTC acts as a stencil slid over the mould of domestic law,

covering and thereby excluding part of it.

OECD model convention

Effects of DTC

DTC does not create taxing rights

• However BEPS & the new draft of the 2017 OECDMC now

promotes the objective of prohibition of double non

taxation, justifying a state to retake its taxing rights when

the other state to which those rights have been allocated

does not tax. Ex. Anti-hybrids rule.

• This results in a reversal of tax jurisdiction and

automatic taxation in the other C.S., if the latter claims

taxing rights under its domestic law.

OECD model convention

Effects of DTC

DTC does not create taxing rights

• However, although some DTC’s in force contain a specific

reversal rule, the reversal rule and the preamble on non-

double-taxation are not articles of the OECDMC.

• The new art. 29 and the ML convention contain a rule

denying the benefit of the convention to taxpayers who are

not “qualified residents” or covered by a “principal purpose

test”, potentially resulting in a reversal of tax jurisidiction.

• That reversal can only result into effective taxtion if the

arrangement is subject to tax in the other CS.

OECD model convention

Effects of DTC

Interpretation of DTC in national law

• Where to start DTC or domestic law?

• DTC refers to domestic tax concepts, if the concepts are

not defined in the DTC I.e. domestic concepts are the

starting position.

• Domestic law establishes the national tax claim.

• When there is no domestic tax claim there is no problem

and the DTC does not need to be consulted.

• But DTC may still limit taxing rights in the other CS, except

for the rule of avoiding double non-taxation.

OECD model convention

Effects of DTC

Allocation of taxing rights & mitigation of double

taxation

• Full taxation: DTC allocates taxing power to the two C.S.:

source state and residence state. Double juridical taxation

is eliminated or mitigated by limiting the tax rates in the

source state and obliging the residence state to apply

exemption or tax credit.

• Double taxation is eliminated when foreign source income

is exempt, or when foreign tax can be fully credited against

tax in residence state.

OECD model convention

Effects of DTC

Allocation of taxing rights & mitigation of double

taxation

• Incomplete taxation: allowing limited source taxation in

combination with full exemption in residence state.

• Double juridical taxation is fully eliminated by allocating

exclusive taxing rights to one of the two CS. This results

sometimes in incomplete (reduced) or limited single

taxation in the source state and exemption in residence

state.

OECD model convention

Interpretation of tax treaties

• Principles of interpretation of all treaties including DTCs

are in the Vienna Convention on the Law of Treaties

(VCLT)(signed in 1969, effective as of 1980).

• 124 countries have signed and ratified this convention,

with the major exceptions of France and the US.

OECD model convention

Interpretation of tax treaties

Interpretation principles of VCLT

• Art. 31(1): treaty must be interpreted in “good faith within

ordinary meaning to be given to the terms of the treaty in

their context and in the light of its object and purpose”.

Pacta sunt servanda.

• The context includes the text, its preambles, annexes &

any agreement or instrument made by one of the parties in

connection with the treaty and accepted by the other

parties.

OECD model convention

Interpretation of tax treaties

Interpretation principles of VCLT

• Art. 31(3): subsequent agreement on the interpretation of

a provision of the treaty or subsequent practice when

established in agreement between contracting parties can

also be taken into account and change the way in which

the treaty is applied. However this can never change the

clear wording of a treaty.

• Quid: prohibition of double non-taxation? Only when CS

agree that MLConvention covers existing DTC’s prohibition

of double non-taxation applies.

OECD model convention

Interpretation of tax treaties

Interpretation principles of VCLT

• Ex.: Taxpayer is frontier worker and exempt in country of

employment if he returns home every day to his state of

residence under F/DE DTC. Mutual agreement between

F&DE that he does not lose his status as frontier worker if

he does not return < 45 days per calendar year.

• Taxpayer relied on mutual agreement. DE federal tax

court: MA cannot amend provisions of domestic law after

incorporation of DTC in domestic law. DE BFH 10.12.2001,

IB 94/01

OECD model convention

Interpretation of tax treaties

Interpretation principles of VCLT

• All methods of interpretation are allowed without

hierarchy: grammatical, systematic, teleological and

historical interpretation are allowed.

• Art. 31(4): special meaning to be given to a treaty term

must be observed, “if it is established that the parties so

intended”.

• OECD rule: concepts are defined by national law, unless

clearly defined in DTC.

OECD model convention

Interpretation of tax treaties

Is OECD Commentary part of the context?

• The Commentary is not the context in the sense of the

preamble or the annex of a DTC, neither its preparatory

work, nor the circumstances of its conclusion.

• If the C.S. adopt “ne varietur” the literal text of the OECD

MC, it can be argued that the Commentary is part of the

historical interpretation material, giving a special

meaning to treaty terms.

OECD model convention

Interpretation of tax treaties

Interpretation principles of VCLT

• Sometimes concepts are losely, or incompletely defined in

the DTC. What is the role of OECD MC & Commentary?

• Belgian resident receives severance pay from DE co. DE

tax administration claims taxing rights under OECD

wording: salaries, wages and other remuneration with

respect to employment. DE court decided that DE law

requires close connection between payment and work

performance and rejected OECD Commentary. BEH

02.09.2009, IR 111/08

OECD model convention

Interpretation of tax treaties

Is OECD Commentary part of the context?

• Some tax autorities take the position that the Commentary

should also be used for DTC’s that do not follow the OECD

MC.

• But if the C.S. did not take the OECD MC as the guideline

for their negotiations, the Commentary cannot be used as

a guideline for the interpretation of a DTC.

OECD model convention

Interpretation of tax treaties

Is OECD Commentary part of the context?

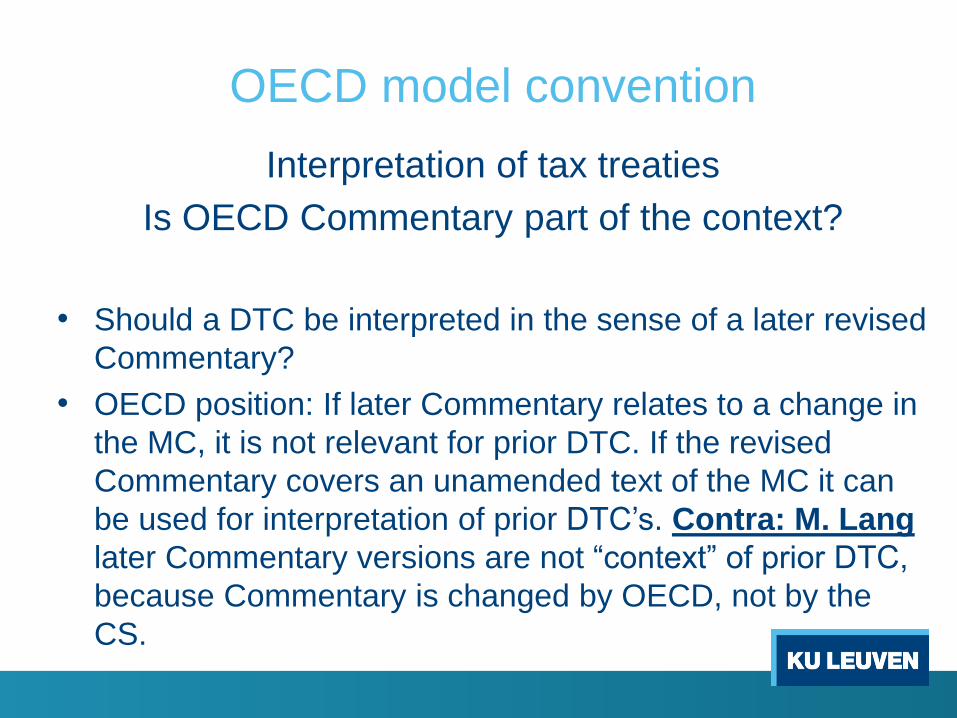

• Should a DTC be interpreted in the sense of a later revised

Commentary?

• OECD position: If later Commentary relates to a change in

the MC, it is not relevant for prior DTC. If the revised

Commentary covers an unamended text of the MC it can

be used for interpretation of prior DTC’s. Contra: M. Lang

later Commentary versions are not “context” of prior DTC,

because Commentary is changed by OECD, not by the

CS.

OECD model convention

Interpretation of tax treaties

Is OECD Commentary part of the context?

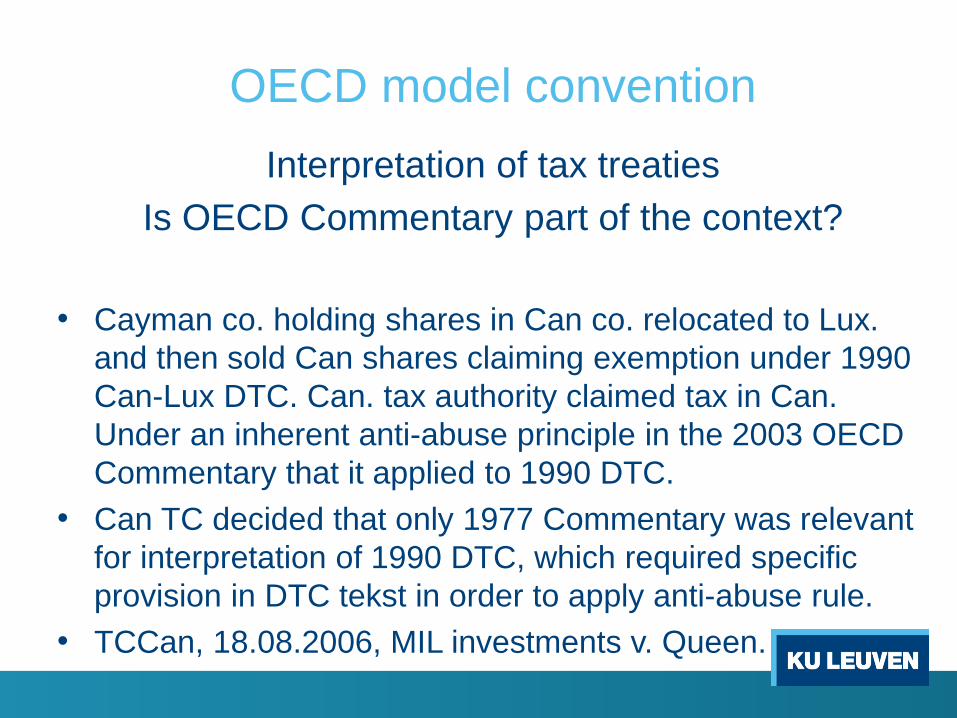

• Cayman co. holding shares in Can co. relocated to Lux.

and then sold Can shares claiming exemption under 1990

Can-Lux DTC. Can. tax authority claimed tax in Can.

Under an inherent anti-abuse principle in the 2003 OECD

Commentary that it applied to 1990 DTC.

• Can TC decided that only 1977 Commentary was relevant

for interpretation of 1990 DTC, which required specific

provision in DTC tekst in order to apply anti-abuse rule.

• TCCan, 18.08.2006, MIL investments v. Queen.

OECD model convention

Interpretation of tax treaties

Is OECD Commentary part of the context?

• Some recent DTC’s contain a specific rule of interpretation

that later Commentaries should be taken into account (AT,

BE, NL). Such a rule makes the use of later Commentaries

for interpretation mandatory.

• Commentaries are often changed even before the text of

the MC is amended: it is not clear which recent

Commentary should then be used.

OECD model convention

Interpretation of tax treaties

Other instruments of interpetation

• When the text of a DTC is not clear, or when there are new

legal, technical or factual developments any reasonable

support for interpretation can be used: new

Commentaries, expert opinions and foreign court

decisions.

• However the use of those instruments is not binding.

Courts often stick to the text of a DTC, because of principle

of legality.

OECD model convention

Interpretation of tax treaties

Object and purpose of OECD MC

• Art. 31(1): DTC must be interpreted “in the light of its

object and purpose”. The main objective of the MC/DTC’s

is avoidance of double taxation, as reflected in its

original title (1963 and 1977).

• However this objective can only be achieved within the

text and scope of the MC. It does not allow to eliminate

double taxation outside the scope of the MC.

OECD model convention

Interpretation of tax treaties

Object and purpose of OECD MC

• Title of the OECDMC was amended adding: “the

prevention of tax avoidance and evasion”.

• The preamble mentions as objective preventing the

reduction of tax burdens through treaty shopping for

residents of third states.

• The UNMC of 2011 does not mention the avoidance of

double taxation in its title.

OECD model convention

Interpretation of tax treaties

Object and purpose of OECD MC

• BEPS action plan 6 proposes to introduce prohibition of

double non-taxation or reduced taxation as an objective

of the MC at the same level as avoidance of double

taxation.

• But the text of the MC contains only rules to avoid double

taxation, but its objective is also to avoid double non-

taxation. However a new art. 29 has been introduced in the

2017 text of the MC and is part of the MLC

OECD model convention

Interpretation of tax treaties

Priority of DTC definitions

• Art. 3 (2): “any term not defined shall, unless the context

otherwise requires, have the meaning that it has at that

time under the law of the State for the purposes of the

taxes to which the DTC applies”.

• However terms defined in the DTC have priority over the

definitions in domestic law.

• Ex.: PE, residence, national, interest, royalty etc.

• Undefined: dividends

OECD model convention

Interpretation of tax treaties

Priority of DTC definitions

• Art. 3 OECDMC contains a number of “definitions” that are

not complete, full meaning is to be completed by national

law. Ex.: Enterprise: “carrying on any business”.

• Business: includes performance of services and any other

independent activity.

• Taxation of business requires PE, quid of services without

PE, can we apply new concept of services PE?

OECD model convention

Interpretation of tax treaties

Priority of DTC definitions

• Lang finds reference to domestic law controversial,

becasue that reference is limited by “unless the context

requires otherwise”.

• Reference to domestic law often does not resolve the

conflict between C.S. and can only be applied if all

possible interpretation methods under DTC have been

exhausted and failed. The question then is: which

domestic law has priority?

OECD model convention

Interpretation of tax treaties

Static & dynamic method

• Two methods of interpretation of DTC over time:

static & ambulatory or dynamic method of

interpretation.

OECD model convention

Interpretation of tax treaties

Static & dynamic method

• The static method maintains that concepts and rules of a

treaty should be applied in accordance with their meaning

at the time that the treaty was signed (ratified?).

• The ambulatory method maintains that the concepts and

rules of a treaty should be applied in accordance with their

meaning at the time that the treaty is being applied.

Compare to constitutional interpretation of national law.

OECD model convention

Interpretation of tax treaties

Static & dynamic method

• The dynamic method results in a situation where,

depending on developments in law, technology

and business, identical treaty texts lead to

different outcomes.

• The static method freezes a treaty situation and

makes it difficult to adapt to changing

circumstances.

OECD model convention

Interpretation of tax treaties

Static & dynamic method

• In this respect it is important whether a concept is

defined or not defined in the DTC. In case of

explicit reference to domestic law, changes in

domestic law should be taken into account.

• In case of concepts defined in the DTC, changes

in domestic law and later Commentaries are not

relevant. The DTC text is controlling.

OECD model convention

Interpretation of tax treaties

Static & dynamic method

• In 1995 the MC Commentary inlcuded a

recommendation to use the dynamic method

across the board.

• However M. Lang maintains an exception for the

use of later Commentaries for concepts that are

clearly and autonomously defined in earlier DTC’s.

OECD model convention

Interpretation of tax treaties

Static & dynamic method

• The interpretation of DTC’s in accordance with

dynamic method, including later OECD

Commentaries results into tensions with the

principles of legality and legal certainty that taxes

can only be levied by national law and DTC’s

approved in parliament, because of retroactive

application of new rules.

OECD model convention

Interpretation of tax treaties

Multilateral Instrument MLC

• BEPS action 15 contains a proposal for a “Multilateral

Instrument” (MI) open for signature as of 1 January 2017.

Has MI priority on national law?

• New rules are to be included in MLC. Is signature of MLC

equivalent to signing protocol amending existing treaties?

No. MLC should be approved by national parliament. (See

CETA).

OECD model convention

Interpretation of tax treaties

Multilateral Convention MLC

• Signature of MLC is not equivalent to protocol

because a protocol is always signed by two C.S.

and the purpose is the application of some

specific DTC provisions.

• The MLC contains new rules with lots of options.

There are still many decisions to be made on how

to amend the rules after the signature of the MLC,

which need to be approved by parliament.