International Tax Breakfast Briefing Deloitte Tax · PDF fileOpening remarks Lorraine Griffin...

81

International Tax Breakfast Briefing Radisson Golden Lane 26 April 2016 Deloitte Tax

-

Upload

nguyendung -

Category

Documents

-

view

220 -

download

4

Transcript of International Tax Breakfast Briefing Deloitte Tax · PDF fileOpening remarks Lorraine Griffin...

International Tax

Breakfast Briefing

Radisson Golden Lane

26 April 2016

Deloitte Tax

© 2016 Deloitte2

Opening remarks

Lorraine Griffin

Head of Tax

International Tax Issues

Tom Maguire, Tax Partner

26 April 2016

Al Pacino

© 2016 Deloitte 5

© 2016 Deloitte 6

© 2016 Deloitte 7

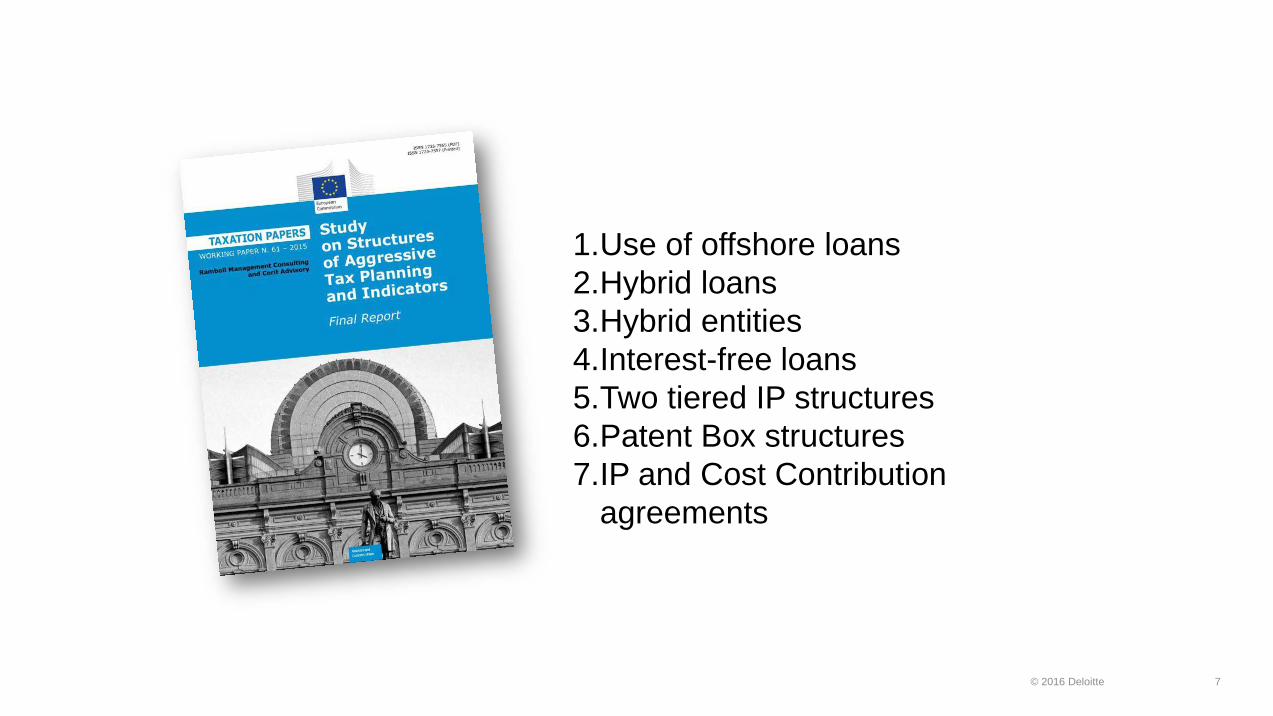

1.Use of offshore loans

2.Hybrid loans

3.Hybrid entities

4.Interest-free loans

5.Two tiered IP structures

6.Patent Box structures

7.IP and Cost Contribution

agreements

© 2016 Deloitte 8

9

16

10

15

98

4

109

7

12

8

1213

109

11

131314

17

1110

11

89

11

8

0

2

4

6

8

10

12

14

16

18

Austr

ia

Belg

ium

Bulg

aria

Cypru

s

Czech

Repu

blic

Germ

any

De

nm

ark

Esto

nia

Gre

ece

Spain

Fin

lan

d

Fra

nce

Cro

atia

Hunga

ry

Irela

nd

Ita

ly

Lith

ua

nia

Lu

xem

bou

rg

La

tvia

Ma

lta

Neth

erl

and

s

Pola

nd

Port

ug

al

Rom

an

ia

Sw

ed

en

Slo

va

kia

Slo

ve

nia

Unite

d K

ing

do

m

© 2016 Deloitte 9

9

16

10

15

98

4

109

7

12

8

1213

109

11

131314

17

1110

11

89

11

8

0

2

4

6

8

10

12

14

16

18

Austr

ia

Belg

ium

Bulg

aria

Cypru

s

Czech

Repu

blic

Germ

any

De

nm

ark

Esto

nia

Gre

ece

Spain

Fin

lan

d

Fra

nce

Cro

atia

Hunga

ry

Irela

nd

Ita

ly

Lith

ua

nia

Lu

xem

bou

rg

La

tvia

Ma

lta

Neth

erl

and

s

Pola

nd

Port

ug

al

Rom

an

ia

Sw

ed

en

Slo

va

kia

Slo

ve

nia

Unite

d K

ing

do

m

© 2016 Deloitte 10

9

16

10

15

98

4

109

7

12

8

1213

109

11

131314

17

1110

11

89

11

8

0

2

4

6

8

10

12

14

16

18

Austr

ia

Belg

ium

Bulg

aria

Cypru

s

Czech

Repu

blic

Germ

any

De

nm

ark

Esto

nia

Gre

ece

Spain

Fin

lan

d

Fra

nce

Cro

atia

Hunga

ry

Irela

nd

Ita

ly

Lith

ua

nia

Lu

xem

bou

rg

La

tvia

Ma

lta

Neth

erl

and

s

Pola

nd

Port

ug

al

Rom

an

ia

Sw

ed

en

Slo

va

kia

Slo

ve

nia

Unite

d K

ing

do

m

EU anti avoidance directive

11

+

EU anti avoidance directive

12

+

Country by Country

Reporting

Interest

Hybrids

Exit taxation

Switchover

GAAR

Public Country by Country

Reporting

EU anti avoidance proposals

13

+

Country by Country

Reporting

Interest

Hybrids

Exit taxation

Switchover

GAAR

Public Country by Country Reporting

© 2016 Deloitte 14

© 2016 Deloitte 15

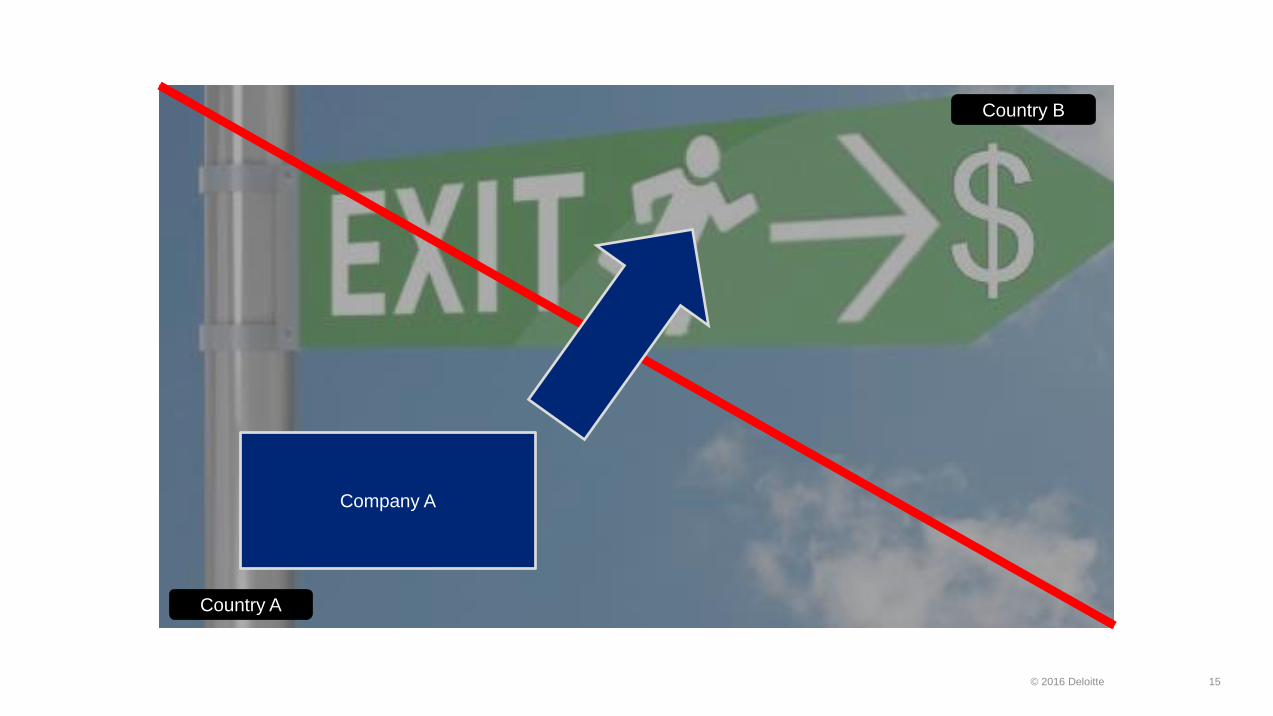

Company A

Country A

Country B

© 2016 Deloitte 16

Company A

Country A

Country B

• Exit tax on specified transfers of

assets or transfer of residence

• Instalment over 5 years or until third

party disposal

• Receiving Member State to provide

a step-up to fair market value.

• Tax should be charged where

assets are transferred from a head

office to a branch.

© 2016 Deloitte 17

Company A

Country A

Country B

“Foreign” country

© 2016 Deloitte 18

Dividends and capital gains from low-taxed

companies

Tax with credit

Statutory tax rate <40% of the tax rate

Ireland a “tax with credit” but s626B

© 2016 Deloitte 19

Public CBCR

© 2016 Deloitte 20

© 2016 Deloitte 21

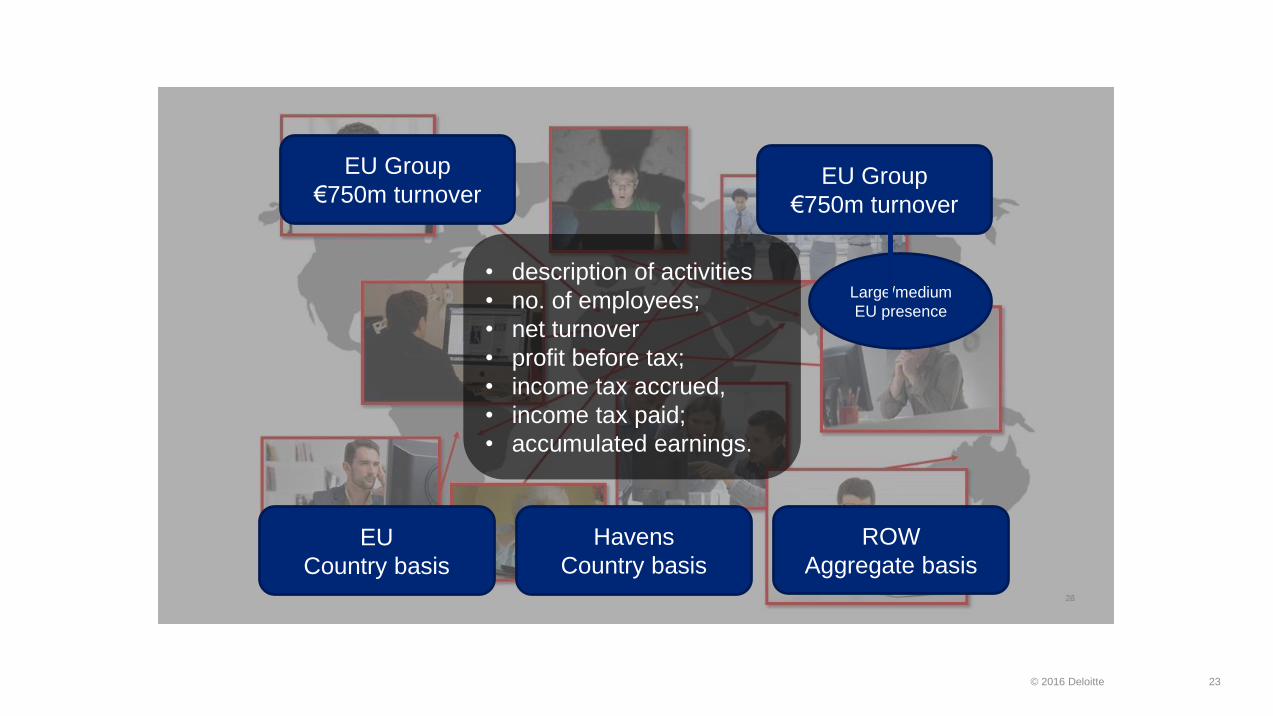

EU Group

€750m turnoverEU Group

€750m turnover

Large/medium

EU presence

© 2016 Deloitte 22

EU Group

€750m turnoverEU Group

€750m turnover

• description of activities

• no. of employees;

• net turnover

• profit before tax;

• income tax accrued,

• income tax paid;

• accumulated earnings.

Large/medium

EU presence

© 2016 Deloitte 23

EU Group

€750m turnoverEU Group

€750m turnover

Large/medium

EU presence

• description of activities

• no. of employees;

• net turnover

• profit before tax;

• income tax accrued,

• income tax paid;

• accumulated earnings.

EU

Country basis

Havens

Country basis

ROW

Aggregate basis

© 2016 Deloitte 24

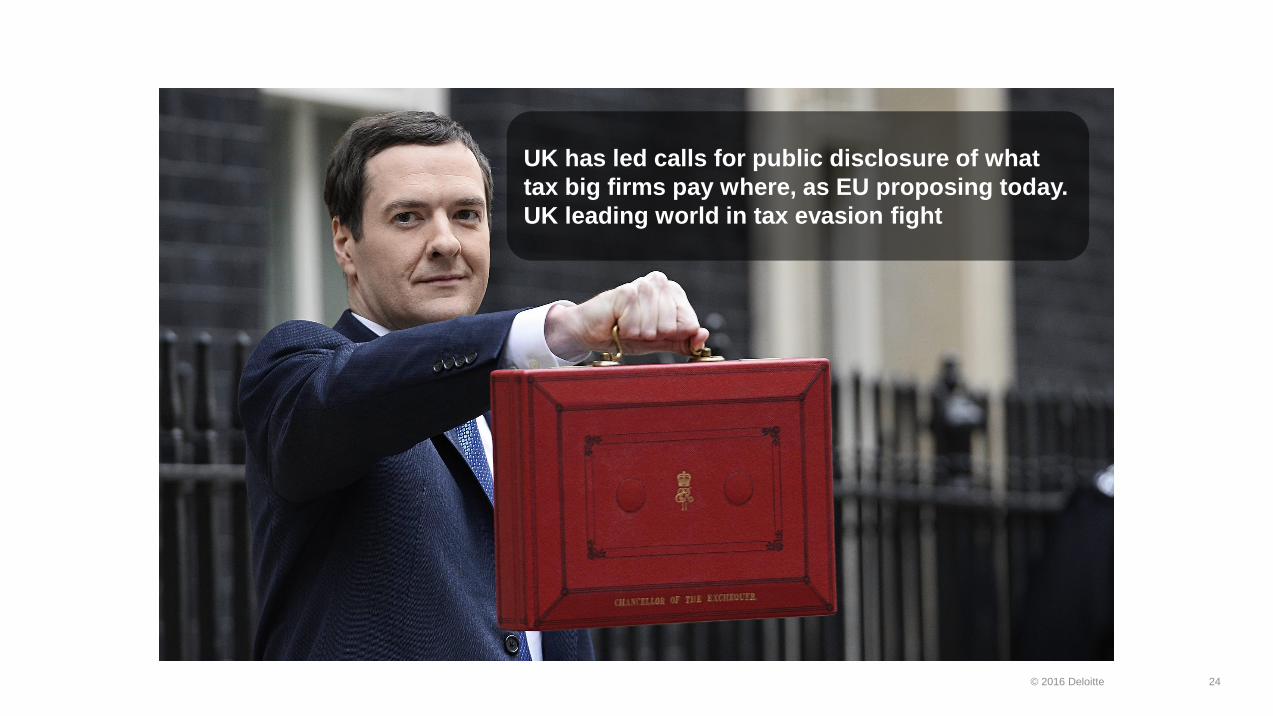

UK has led calls for public disclosure of what

tax big firms pay where, as EU proposing today.

UK leading world in tax evasion fight

© 2016 Deloitte 25

Company’s tax strategy

• Group’s approach to UK tax risk mgt

• Group’s attitude towards tax planning

• The level of UK risk Group prepared to accept

• Group’s approach towards HMRC dealings

© 2016 Deloitte 26

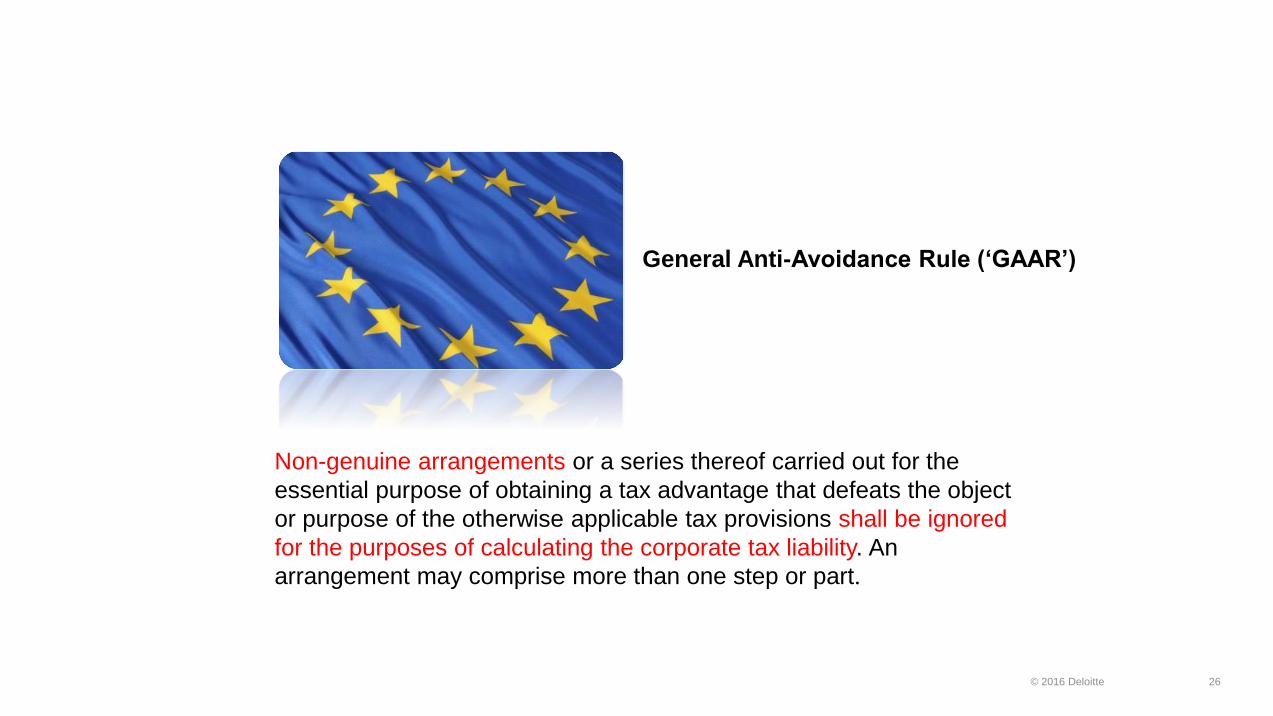

General Anti-Avoidance Rule (‘GAAR’)

Non-genuine arrangements or a series thereof carried out for the

essential purpose of obtaining a tax advantage that defeats the object

or purpose of the otherwise applicable tax provisions shall be ignored

for the purposes of calculating the corporate tax liability. An

arrangement may comprise more than one step or part.

© 2016 Deloitte 27

© 2016 Deloitte 28

© 2016 Deloitte 29

© 2016 Deloitte 30

© 2016 Deloitte 31

to know

to conclude beyond reasonable doubt

to conclude as probable

to reasonably suspect

mere suspicion and belief

© 2016 Deloitte 37

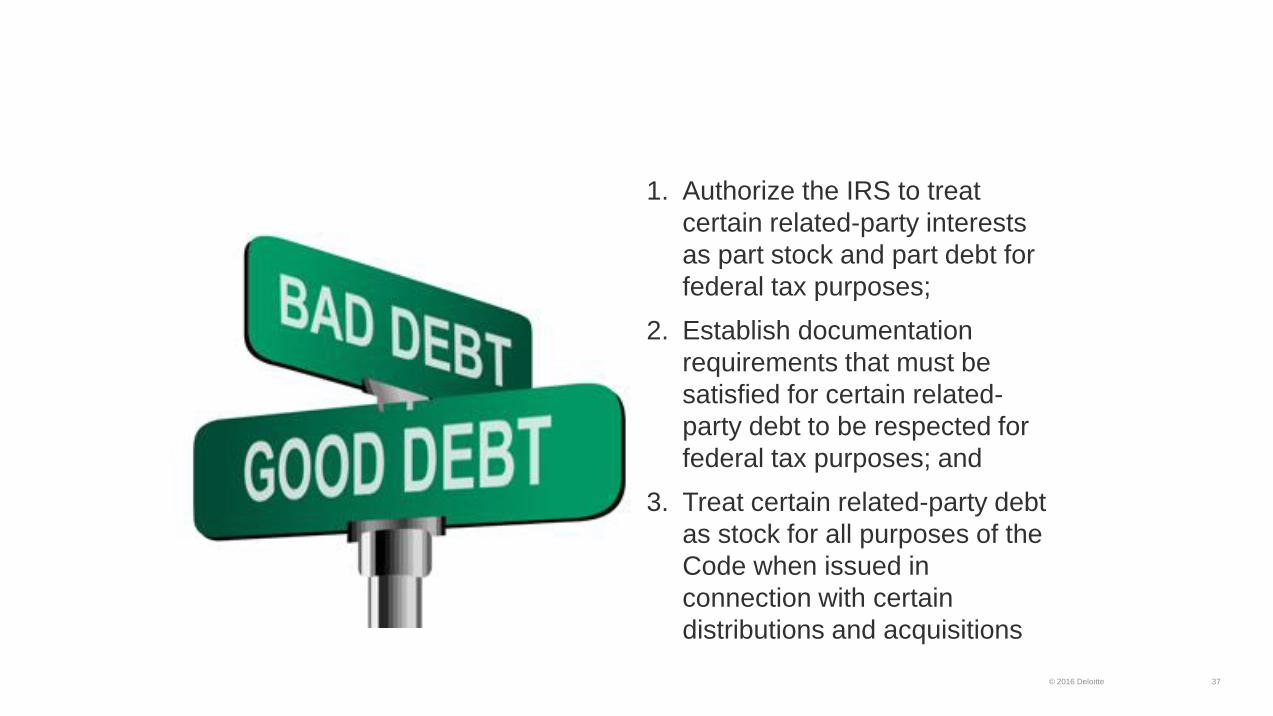

1. Authorize the IRS to treat

certain related-party interests

as part stock and part debt for

federal tax purposes;

2. Establish documentation

requirements that must be

satisfied for certain related-

party debt to be respected for

federal tax purposes; and

3. Treat certain related-party debt

as stock for all purposes of the

Code when issued in

connection with certain

distributions and acquisitions

© 2016 Deloitte 38

Instruments issued between

members of a group that files a

consolidated return.

Cashfunded related-party debt

provided not used for certain

specified distributions or acquisitions

BUT related-party debt issued

• in a distribution;

• in exchange for related party stock;

or

• in certain asset reorganizations

would be treated as “stock”

Refinancing – 36 month pre and post

© 2016 Deloitte 39

1. The issuer has unconditional legally

binding obligation to pay a sum certain

on demand or at fixed dates;

2. The holder has the enforcement rights

of a creditor

3. The issuer’s financial position supports

a reasonable expectation that the issuer

intended to, and would be able to, meet

its obligations under the terms of the

instrument.

Al Pacino

© 2016 Deloitte41

International Tax Environment

Brendan Crowley

Department of Finance

International Tax Environment – 26 April 2016

Department of Finance

Contents

• Policy making context

• EU Tax agenda

• OECD tax agenda

• Other international tax issues

Policy making context

• New Government

• New fiscal rules: preventative arm of Stability and Growth Pact

• 2015 Tax expenditure guidelines

• Evaluations, costings

• Periodic reviews

• Transparency: lobbying legislation, FOI

• Finance Bill/Budget

• Submission before your holidays, not after

• Consultation

• Engagement

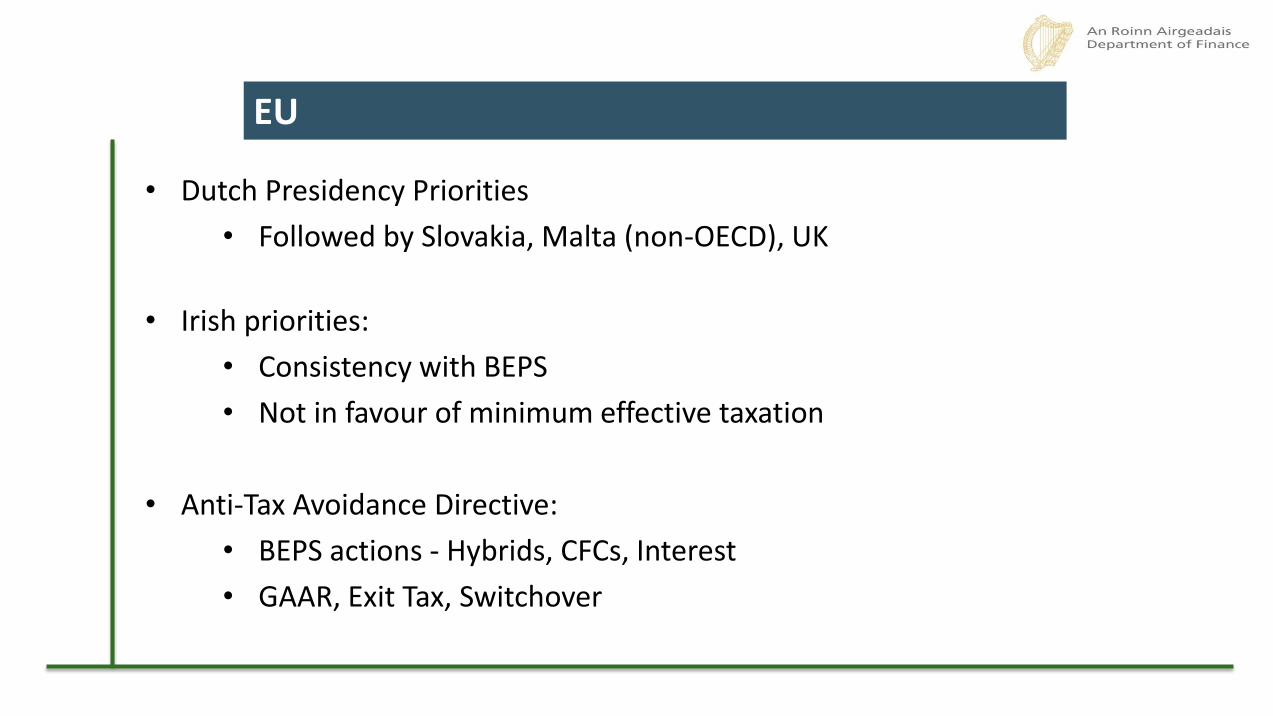

EU

• Dutch Presidency Priorities

• Followed by Slovakia, Malta (non-OECD), UK

• Irish priorities:

• Consistency with BEPS

• Not in favour of minimum effective taxation

• Anti-Tax Avoidance Directive:

• BEPS actions - Hybrids, CFCs, Interest

• GAAR, Exit Tax, Switchover

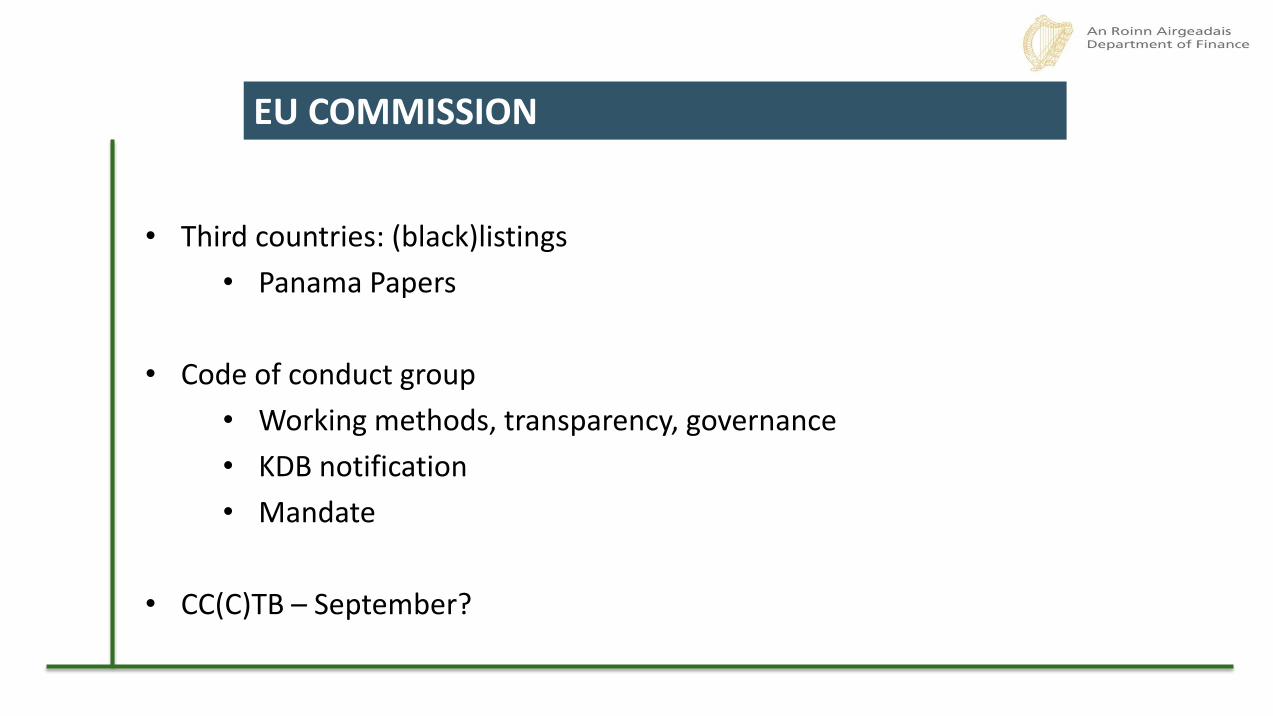

EU COMMISSION

• Third countries: (black)listings

• Panama Papers

• Code of conduct group

• Working methods, transparency, governance

• KDB notification

• Mandate

• CC(C)TB – September?

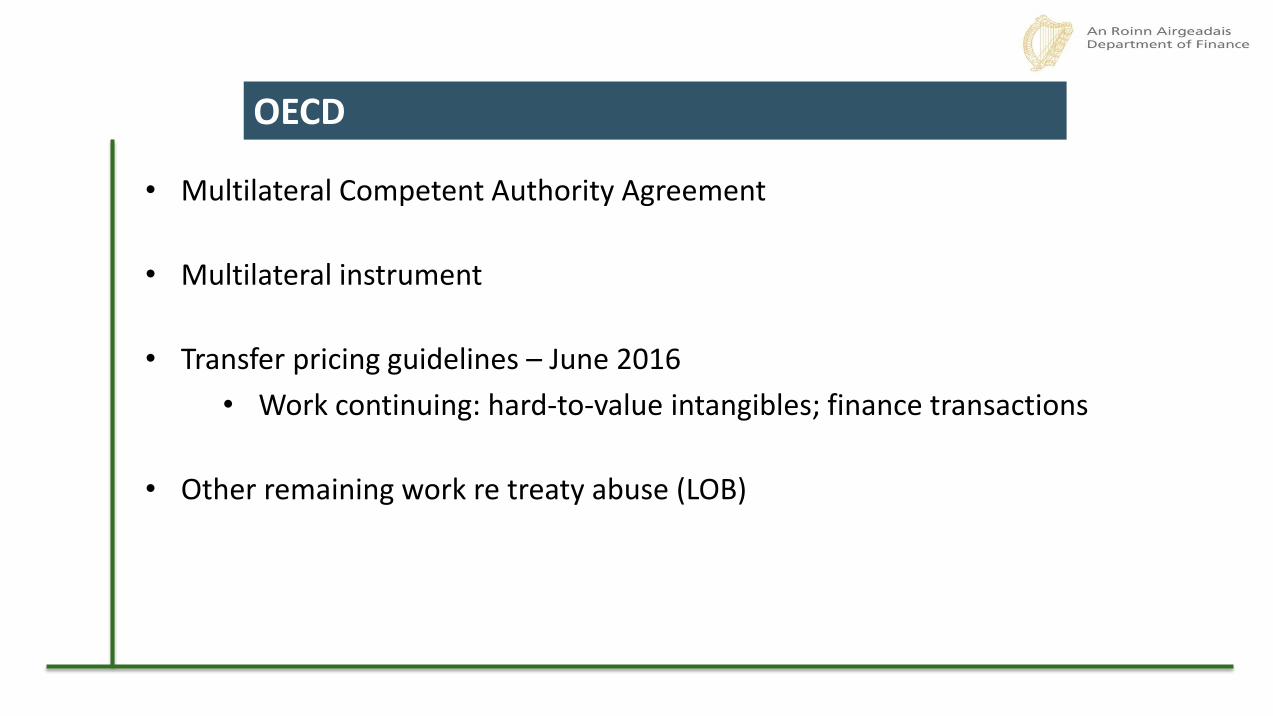

OECD

• Multilateral Competent Authority Agreement

• Multilateral instrument

• Transfer pricing guidelines – June 2016

• Work continuing: hard-to-value intangibles; finance transactions

• Other remaining work re treaty abuse (LOB)

Wider international picture

• Brexit

• CT impact?

• OECD, EU

• Indirect taxes – border issues

• US Reform(?)

• Deemed repatriation

• Inversions

• Panama Papers – Transparency

For more information please go to:

http://www.finance.gov.ie

Copyright 2016 Department of Finance

Disclaimer

This presentation is for informational purposes only.

The Department of Finance does not guarantee the accuracy or completeness of information which is contained in this document and which is statedto have been obtained from or is based upon trade and statistical services or other third party sources. Any data on past performance containedherein is no indication as to future performance.

No representation is made as to the reasonableness of the assumptions made within or the accuracy or completeness of any modelling, scenarioanalysis or back-testing.

All opinions and estimates are given as of the date hereof and are subject to change.

The information in this document is not intended to predict actual results and no assurances are given with respect thereto.

Felix Skala, Partner, Deloitte Legal Germany

26 April 2016

State Aid

State Aid

Introduction

51

State Aid

Introduction

52

“Changing environment”

Why should legal advice on State Aid issues be added to tax services?

• State aid is part of the changing international tax landscape

• Risk assessment

• Analysis of the risk of existing rulings falling within the scope of state aid

• Analysis of the risk of beneficial tax treatment without rulings falling within the

scope of state aid

• Understanding the procedural rights

State Aid

Introduction

53

CJEU: “Although direct taxation falls within the competence of the Member States,

they must exercise that competence consistently with EU law”

Direct taxation

• Tax sovereignty of Member

States

• Free to design national tax

system

• Tax system aims at achieving

revenue and / or policy

objectives

State aid

• Art. 107(1) applies in

relation to the effects of

a State measure

• Hence includes tax

measures

• Policy objectives do not

prevent measure from

being State aid

State Aid

54

Impact on Advance Tax Rulings (ATRs) and APAs

• Tax rulings are not per se unlawful State Aid. However, tax rulings might

constitute unlawful State Aid if they deviate from the normally applicable tax

system by lowering the tax that would otherwise have to be paid.

In the case of tax ruling the focus is on whether such rulings are

“selective”

• In focus of the EU Commission: wide range of unilateral or bilateral cross-border

Rulings and Advanced Pricing Agreements covering TP principles (transactions

between associated enterprises and HQ’s and branches), unilateral downward

adjustments etc.

• State Aid law control reaches back 10 years (even in case of grandfathering

under national law).

State Aid

Concept

55

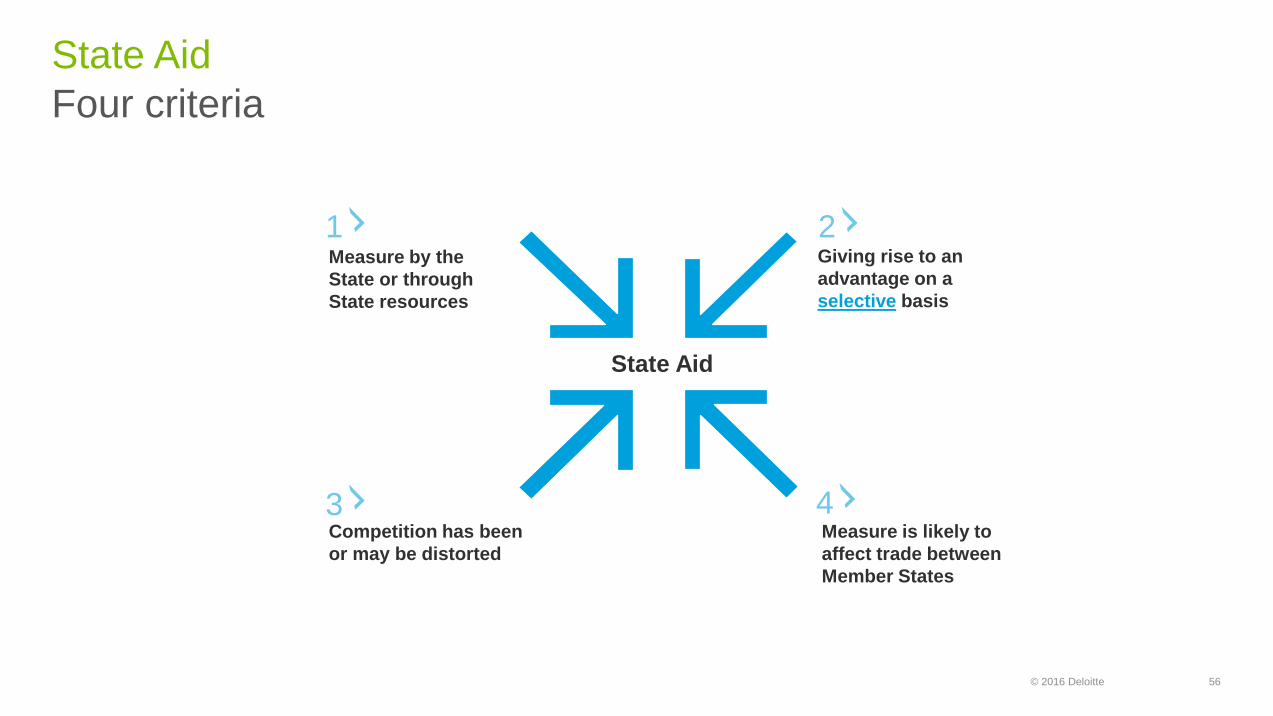

© 2016 Deloitte 56

Measure by the

State or through

State resources

Competition has been

or may be distorted

Measure is likely to

affect trade between

Member States

Giving rise to an

advantage on a

selective basis

1 2

3 4

State Aid

Four criteria

State Aid

© 2016 Deloitte 57

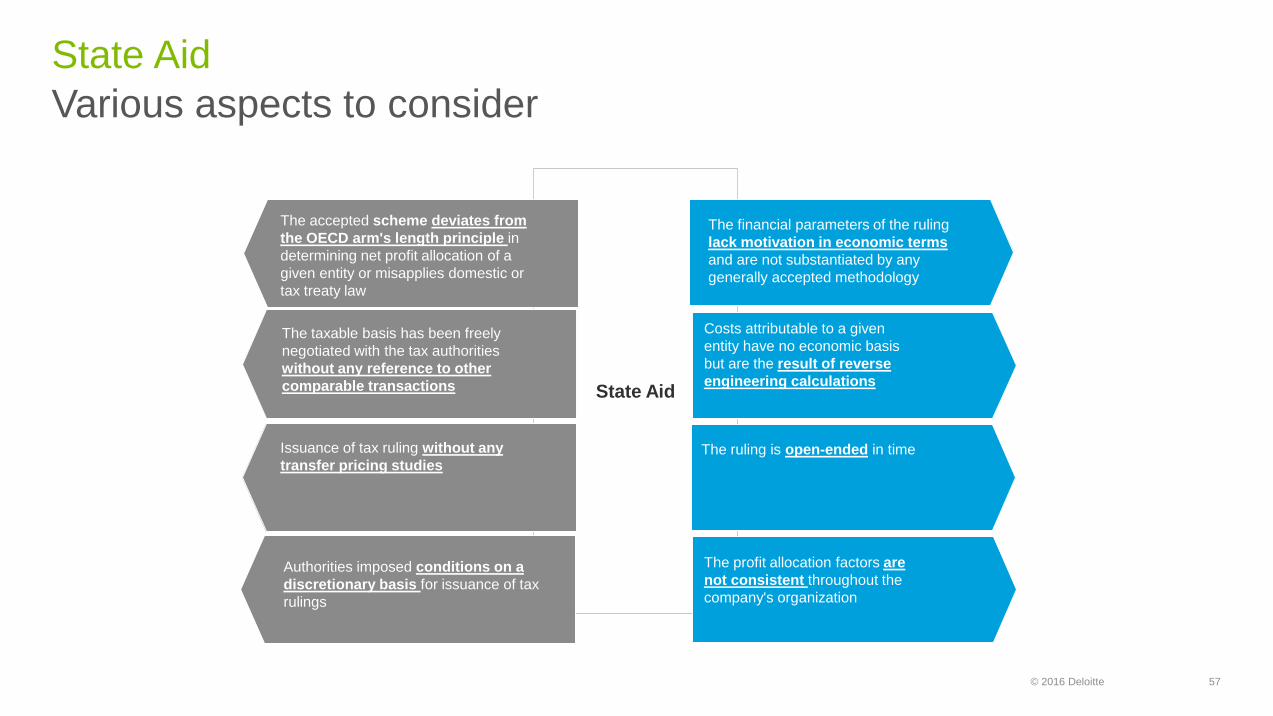

State Aid

The accepted scheme deviates from

the OECD arm's length principle in

determining net profit allocation of a

given entity or misapplies domestic or

tax treaty law

The financial parameters of the ruling

lack motivation in economic terms

and are not substantiated by any

generally accepted methodology

The taxable basis has been freely

negotiated with the tax authorities

without any reference to other

comparable transactions

Issuance of tax ruling without any

transfer pricing studies

Authorities imposed conditions on a

discretionary basis for issuance of tax

rulings

Costs attributable to a given

entity have no economic basis

but are the result of reverse

engineering calculations

The ruling is open-ended in time

The profit allocation factors are

not consistent throughout the

company's organization

Various aspects to consider

State Aid

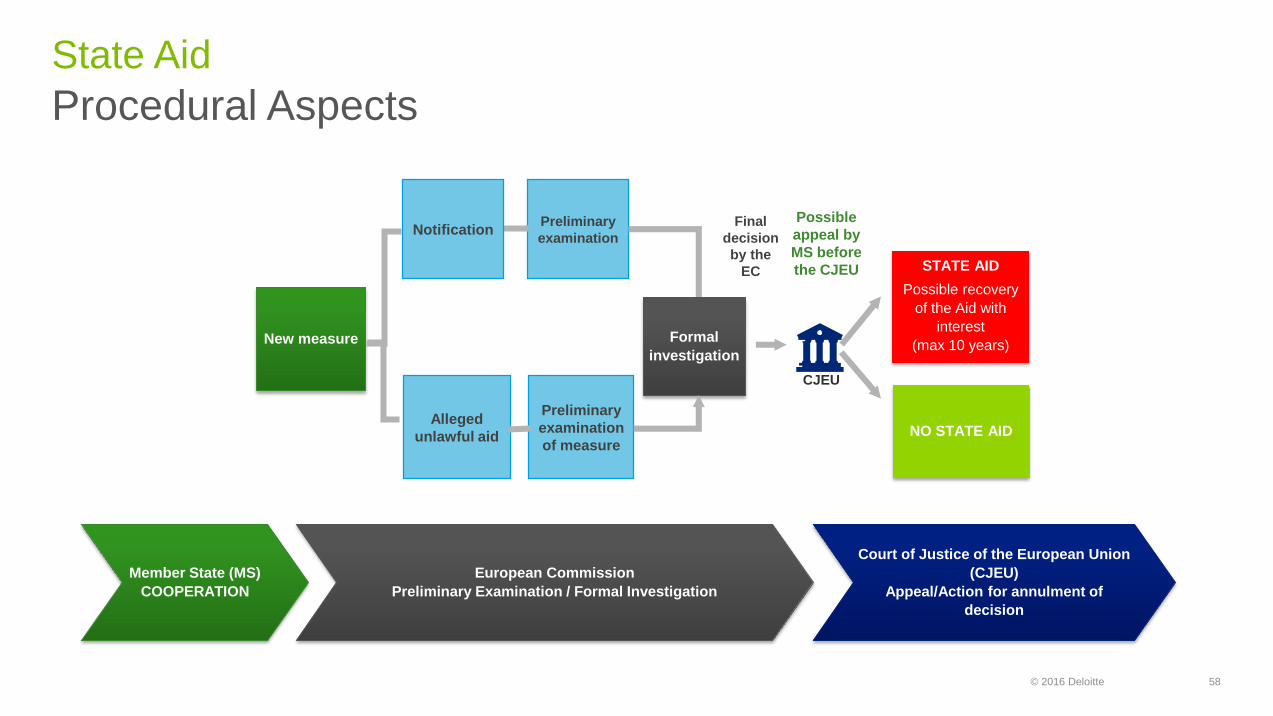

© 2016 Deloitte 58

Member State (MS)

COOPERATION

European Commission

Preliminary Examination / Formal Investigation

Court of Justice of the European Union

(CJEU)

Appeal/Action for annulment of

decision

New measure

Preliminary

examinationNotification

Formal

investigation

STATE AID

Possible recovery

of the Aid with

interest

(max 10 years)

CJEU

Possible

appeal by

MS before

the CJEU

NO STATE AID

Final

decision

by the

EC

Preliminary

examination

of measure

Alleged

unlawful aid

Procedural Aspects

State Aid

© 2016 Deloitte 59

• The beneficiary is not party to the preliminary examination and formal

investigation procedure but may submit comments (generally within one month

after the decision to initiate the formal investigation procedure has been

published in the Official Journal of the EU).

• Final decision of Commission:

Positive decision (= approval, aid but compatible with Common Market)

Conditional decision (= approval with compatibility conditions or obligations of

monitoring)

Negative decision (= prohibition; aid incompatible with State aid rules,

prohibition to put aid into effect)

Recovery decision (= prohibition; Member State has to recover incompatible

aid plus interest)

• After final decision of the Commission the beneficiary can take action for

annulment against the decision under Article 263 TFEU.

• The beneficiary can take action in national court against recovery order.

State Aid

Procedural Aspects

© 2016 Deloitte 60

Rationale

behind the

recovery

10 years

+ interest

In case of an unlawful

State Aid, a recovery of

the aid already paid out

to the beneficiaries plus

interest may be

requested to the

Member State

Beneficiaries

cannot raise

the point of

legitimate

expectation

Recovery

obligation upon the

Member State

concerned

State Aid

Recovery

© 2016 Deloitte 61

A State Aid granted without prior approval of the Commission is illegal.

Member State must recover illegal State Aid.

Amount to be recovered: Granted State Aid plus interest

In case of “Tax State Aid” the amount to be recovered is the difference

between the amount actually paid and the amount which should have

been paid if the generally applicable rule had been applied (plus interest).

National courts are competent for enforcement.

If the Member State does not recover the illegal State Aid, the EU

Commission might launch infringement proceedings before the ECJ.

State Aid

Legal consequences

© 2015. For information, contact Deloitte Touche Tohmatsu Limited. 62

Bios

62

© 2016. For information, contact Deloitte Touche Tohmatsu Limited. 63

Felix Skala, LL.M. is an attorney at law and partner at Deloitte Legal Germany in the Hamburg office. He joined the firm in 2003 and is head of the competition law department of Deloitte Legal Germany as well as the international Deloitte Legal Working Group “Antitrust”.

Felix has 12 years+ experience in advising domestic and international clients in all areas of German and European antitrust and competition law. He has broad experience in all legal matters related to state aid law and government incentives.

Felix received a Master of Laws degree (LL.M.) at Boston University and is also admitted to the New York Bar.

Phone: +49-40-378538-0Email: [email protected]

Speaker bio

Changing Role of Tax

Departments

Karen Frawley

Tax Partner

Managing Evolving

Expectations

Changing role of tax function

© 2016 Deloitte65

How does it influence

your stakeholders’

expectations?

What can you learn

from the experience of

others?

Which activities should

you prioritise?3. Progressing your plan of

action

© 2016 Deloitte66

1. Understanding your changing environment

2. Developing a robust global tax

strategy & management

model

Stakeholder Management

Environmental

pressures

shaping our

world

© 2016 Deloitte67

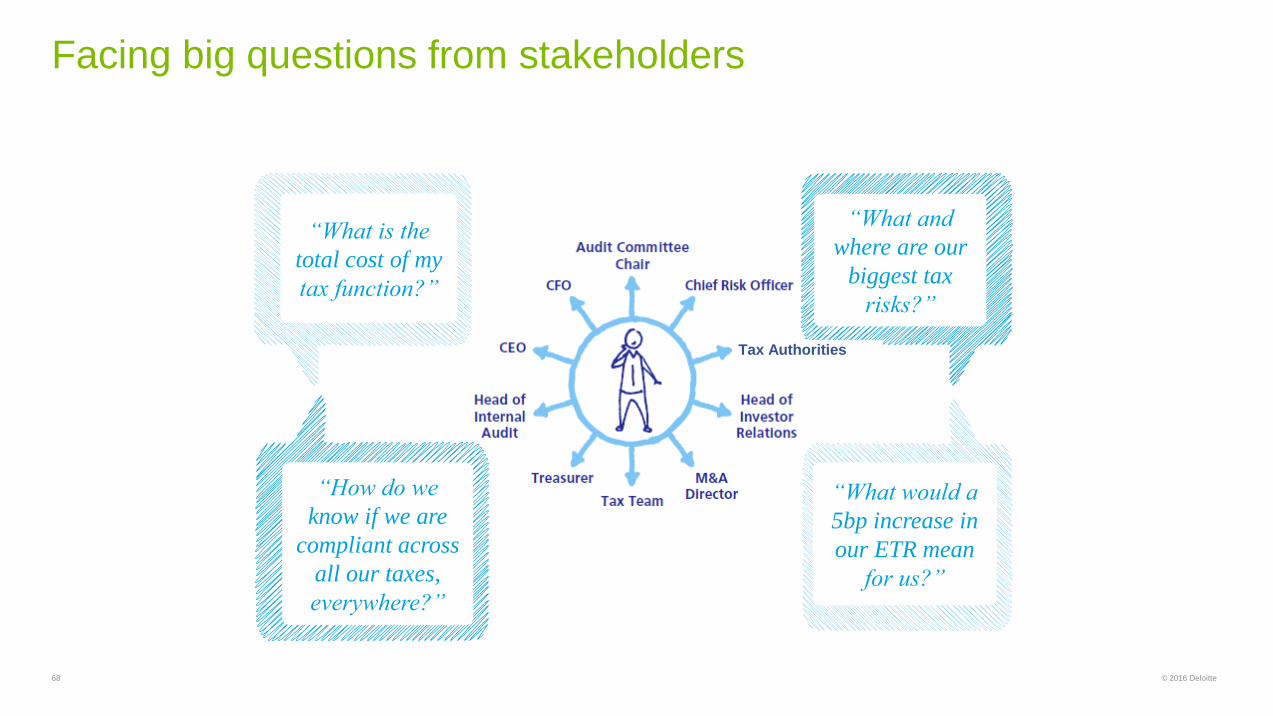

Facing big questions from stakeholders

“What would a

5bp increase in

our ETR mean

for us?”

“How do we

know if we are

compliant across

all our taxes,

everywhere?”

“What and

where are our

biggest tax

risks?”

“What is the

total cost of my

tax function?”

Tax Authorities

© 2016 Deloitte68

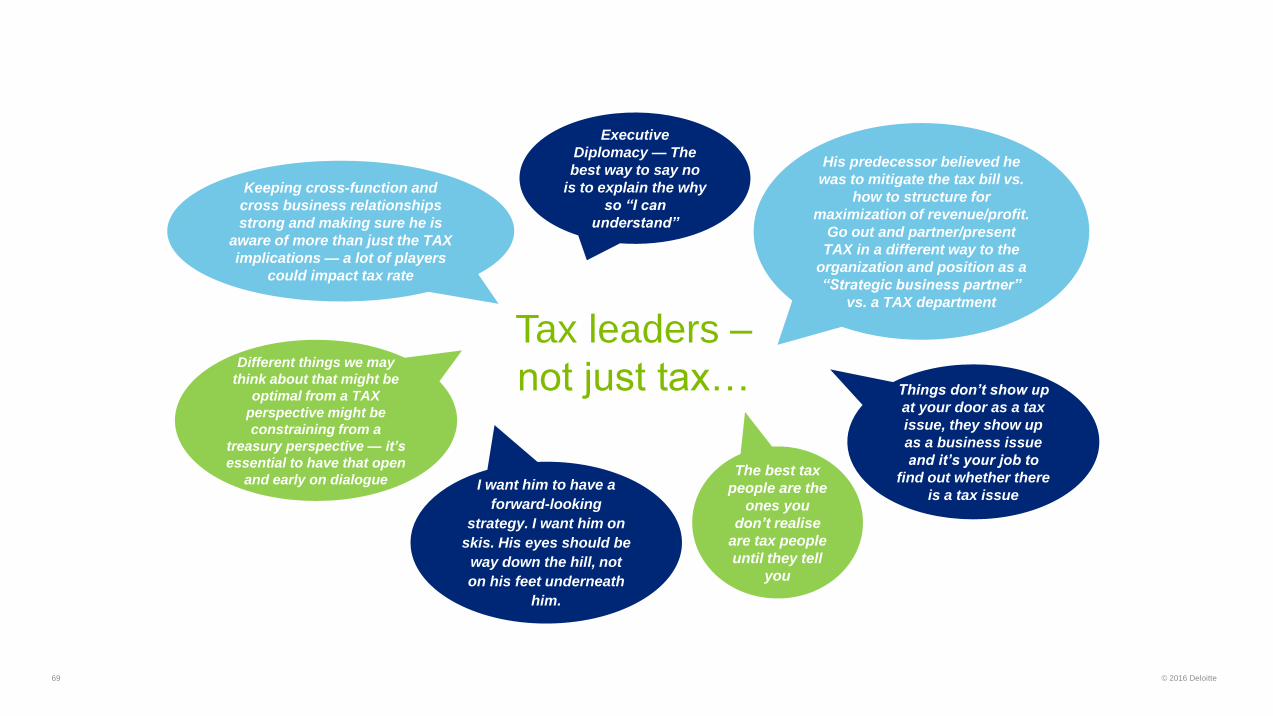

Tax leaders –

not just tax… Things don’t show up

at your door as a tax

issue, they show up

as a business issue

and it’s your job to

find out whether there

is a tax issue

His predecessor believed he

was to mitigate the tax bill vs.

how to structure for

maximization of revenue/profit.

Go out and partner/present

TAX in a different way to the

organization and position as a

“Strategic business partner”

vs. a TAX department

Different things we may

think about that might be

optimal from a TAX

perspective might be

constraining from a

treasury perspective — it’s

essential to have that open

and early on dialogue

Keeping cross-function and

cross business relationships

strong and making sure he is

aware of more than just the TAX

implications — a lot of players

could impact tax rate

Executive

Diplomacy — The

best way to say no

is to explain the why

so “I can

understand”

I want him to have a

forward-looking

strategy. I want him on

skis. His eyes should be

way down the hill, not

on his feet underneath

him.

The best tax

people are the

ones you

don’t realise

are tax people

until they tell

you

© 2016 Deloitte69

Tax risk profile of organisation

70 © 2016 Deloitte

Directors’

compliance

statement

71

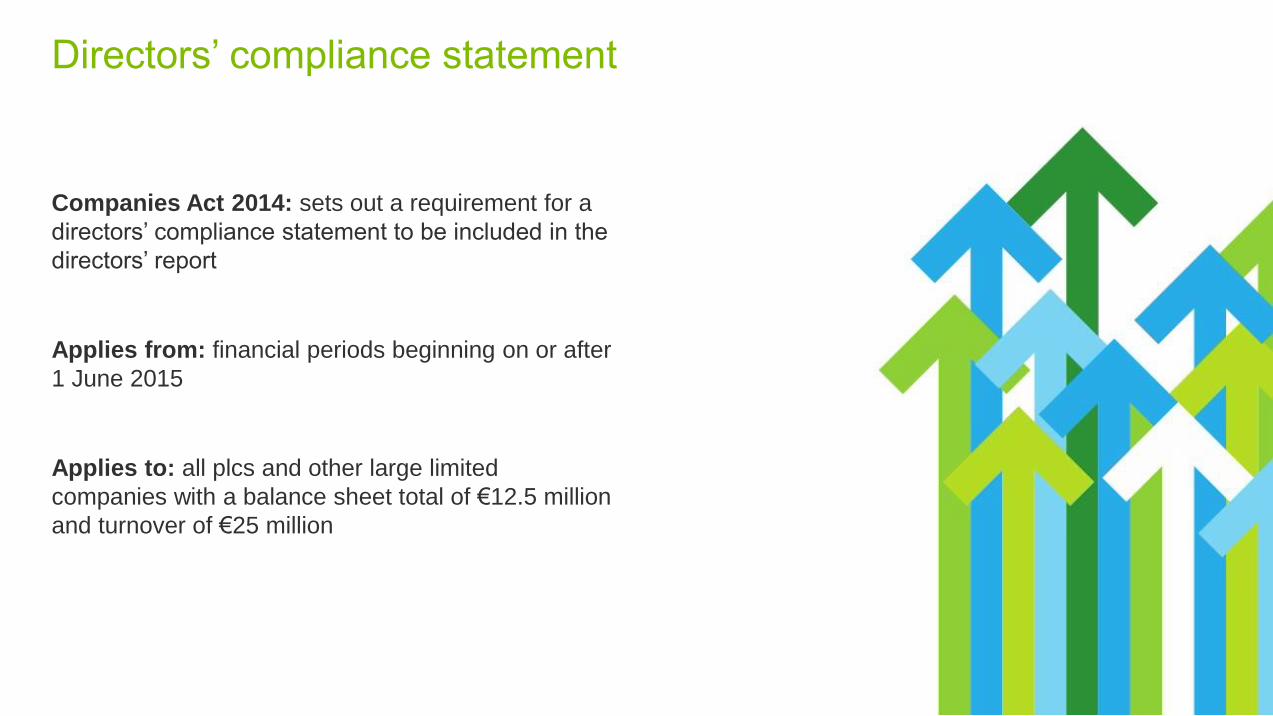

Companies Act 2014: sets out a requirement for a

directors’ compliance statement to be included in the

directors’ report

Applies from: financial periods beginning on or after

1 June 2015

Applies to: all plcs and other large limited

companies with a balance sheet total of €12.5 million

and turnover of €25 million

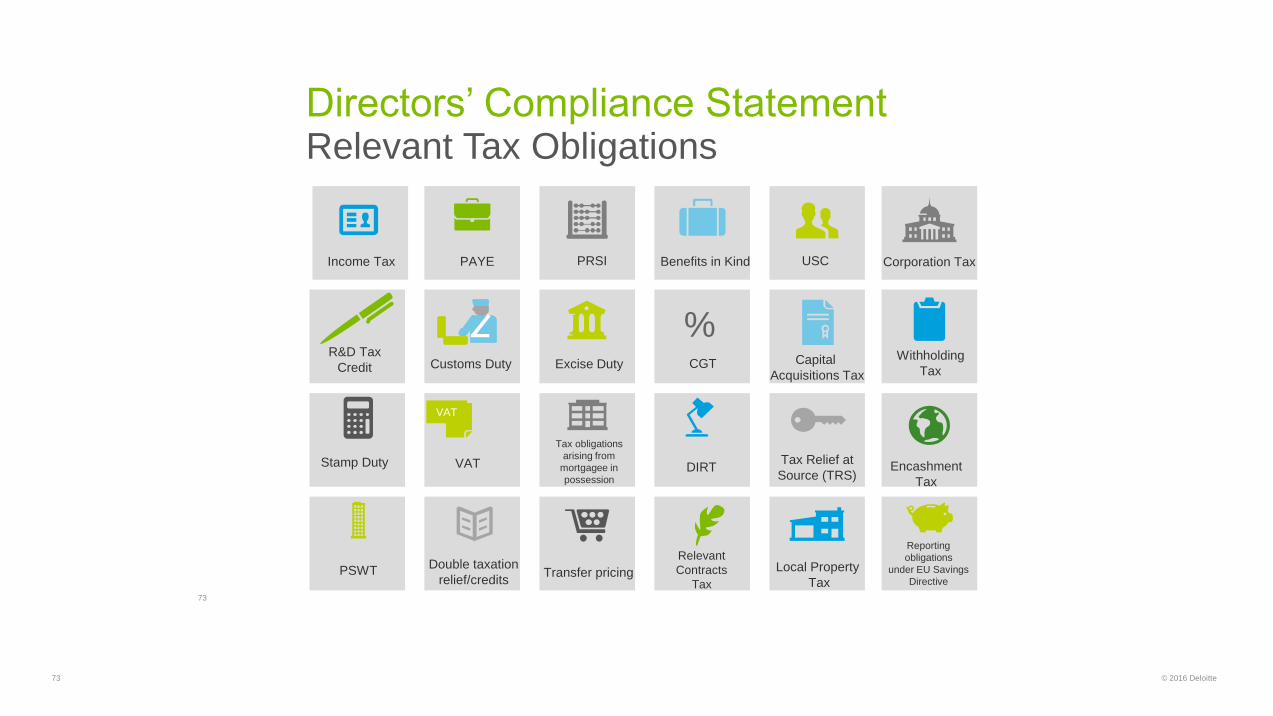

Directors’ compliance statement

Income Tax PAYE PRSI Benefits in Kind USC Corporation Tax

R&D Tax

Credit Customs Duty Excise Duty CGT

%Capital

Acquisitions Tax

Withholding

Tax

Stamp Duty

VAT

VAT

Tax obligations

arising from

mortgagee in

possession DIRT

Tax Relief at

Source (TRS) Encashment

Tax

PSWTDouble taxation

relief/credits Transfer pricing

Relevant

Contracts

Tax

Local Property

Tax

Reporting

obligations

under EU Savings

Directive

Directors’ Compliance StatementRelevant Tax Obligations

73

© 2016 Deloitte73

Developing a robust

global tax management

model

© 2016 Deloitte74

Developing a tax management model

© 2016 Deloitte75

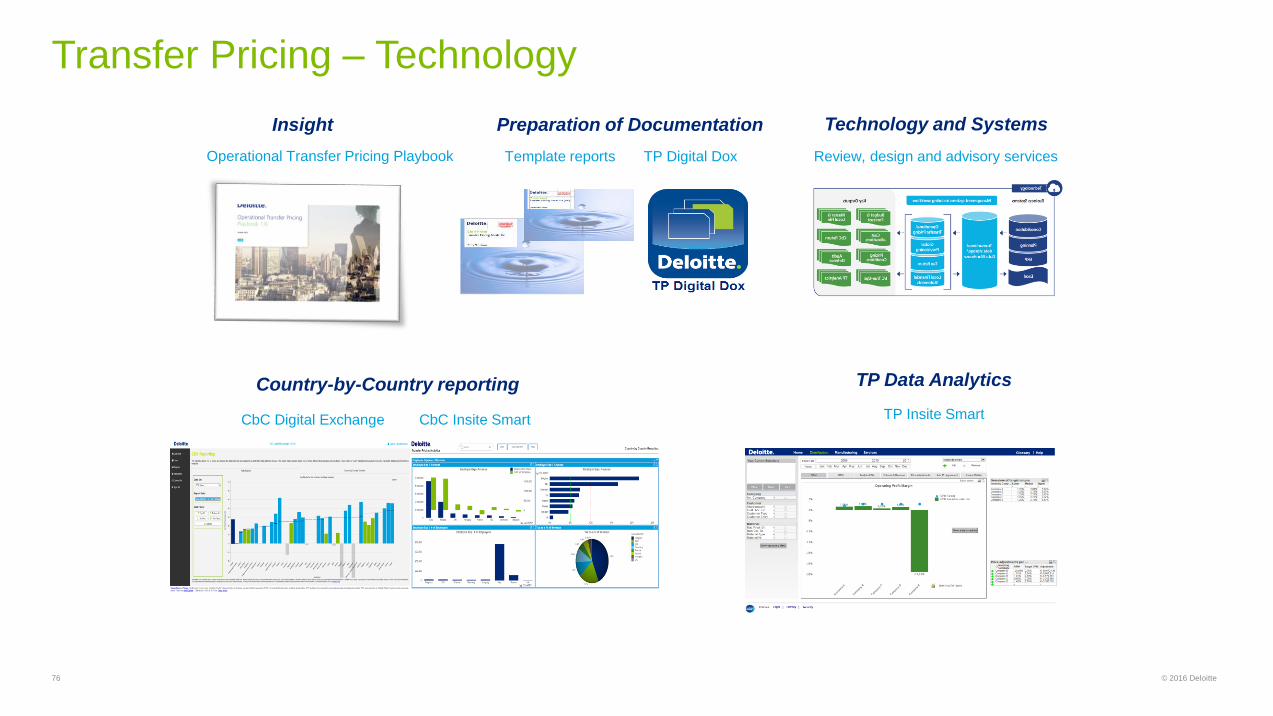

Transfer Pricing – Technology

Operational Transfer Pricing Playbook

Insight Preparation of Documentation

Template reports TP Digital Dox Review, design and advisory services

Technology and Systems

Country-by-Country reporting

CbC Insite SmartCbC Digital Exchange

TP Data Analytics

TP Insite Smart

© 2016 Deloitte76

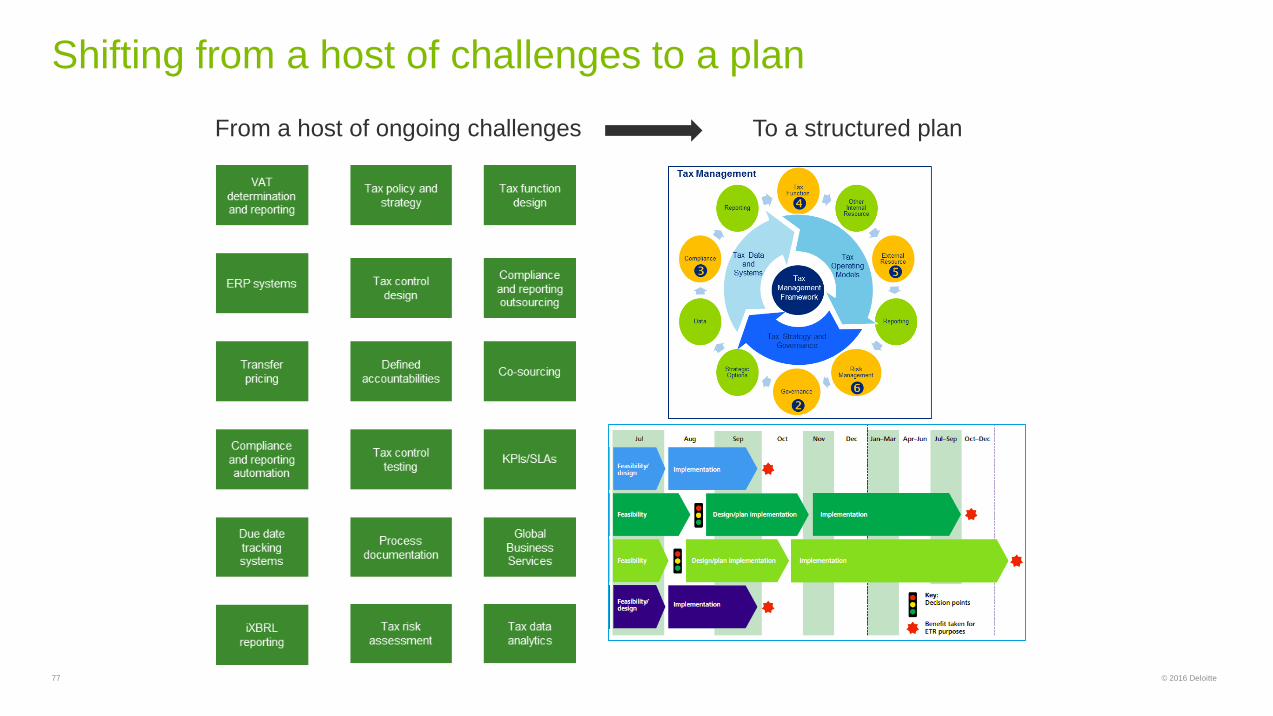

Shifting from a host of challenges to a plan

From a host of ongoing challenges To a structured plan

© 2016 Deloitte77

Strike the right balance

between your

stakeholders’ needs

Consider

governance,

operating models,

resourcing and

technology together

Tactical wins can

form part of a longer,

more strategic

program

3. Progressing your plan of

action

© 2016 Deloitte78

1. Understanding your changing environment

2. Developing a robust global tax

strategy & management

model

Stakeholder Management

Panel Discussion

• Pádraig Cronin, Vice-Chairman of Deloitte Ireland and Tax

Partner

• Joan O’Connor, International Tax Partner

• Karen Frawley, International Tax Partner

• Gerard Feeney, Head of Transfer Pricing

79 © 2016 Deloitte

Closing remarks

Lorraine Griffin

Head of Tax

© 2016 Deloitte80

81

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a private company limited by guarantee, and its network of member firms, each of which is a legally separate

and independent entity. Please see www.deloitte.com/ie/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

With nearly 2,000 people in Ireland, Deloitte provide audit, tax, consulting, and corporate finance to public and private clients spanning multiple industries. With a globally

connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to

address their most complex business challenges. With over 210,000 professionals globally, Deloitte is committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, Deloitte Global Services Limited, Deloitte Global Services Holdings Limited,

the Deloitte Touche Tohmatsu Verein, any of their member firms, or any of the foregoing’s affiliates (collectively the “Deloitte Network”) are, by means of this publication,

rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or

services, nor should it be used as a basis for any decision or action that may affect your finances or your business. Before making any decision or taking any action that may

affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained

by any person who relies on this publication.

© 2016 Deloitte & Touche. All rights reserved