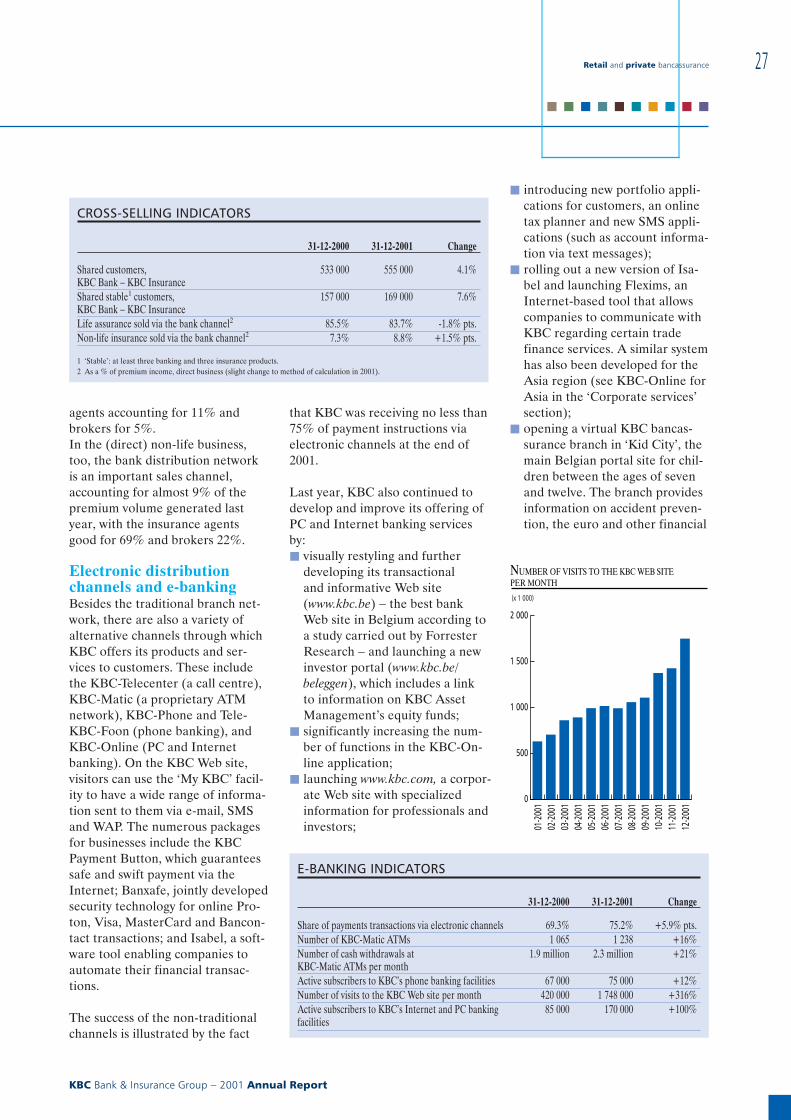

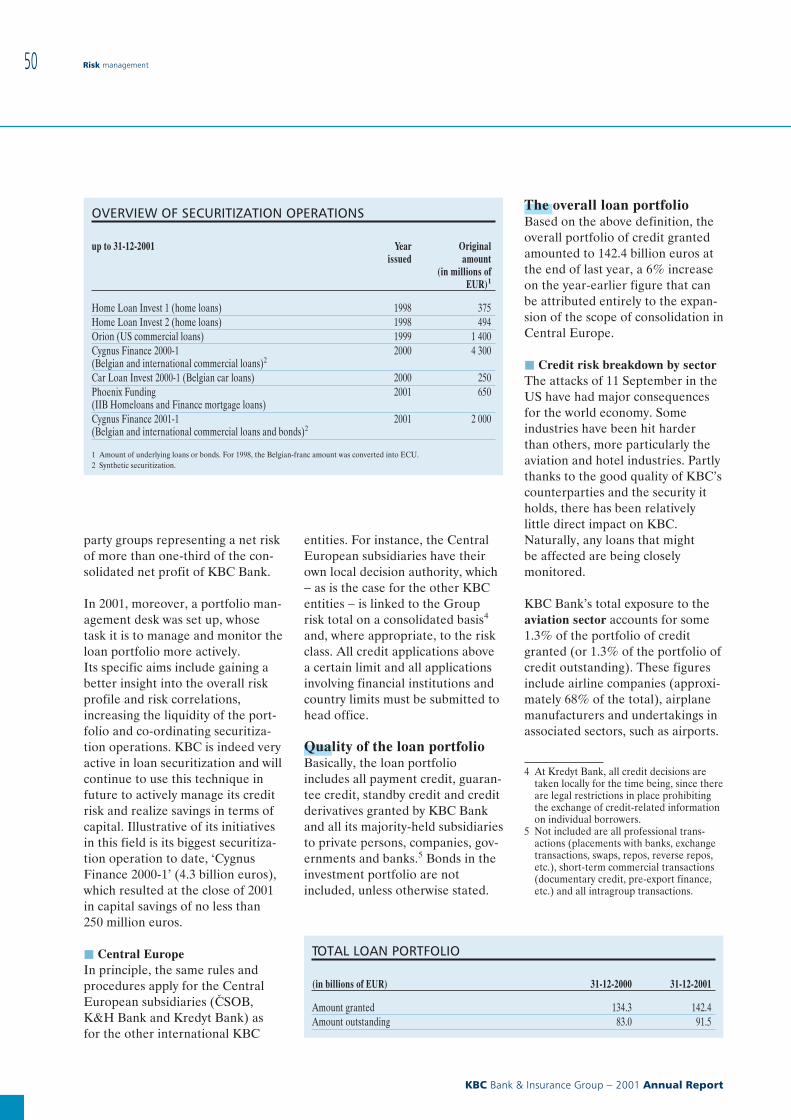

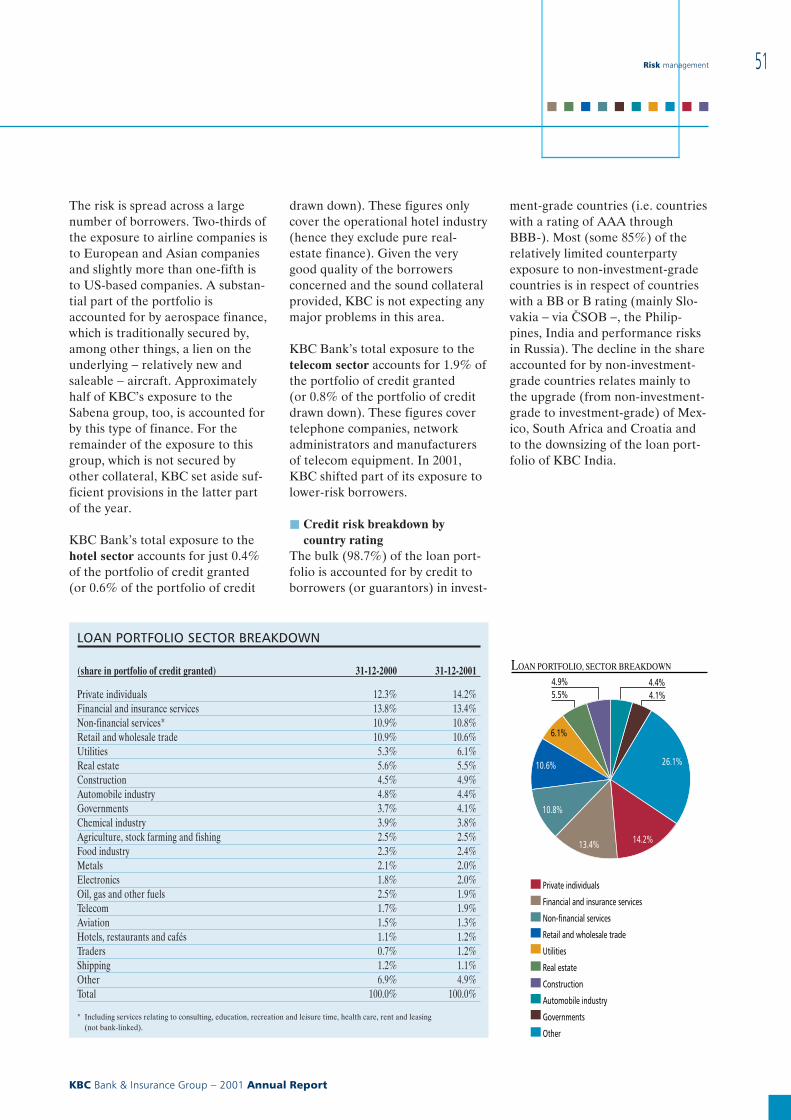

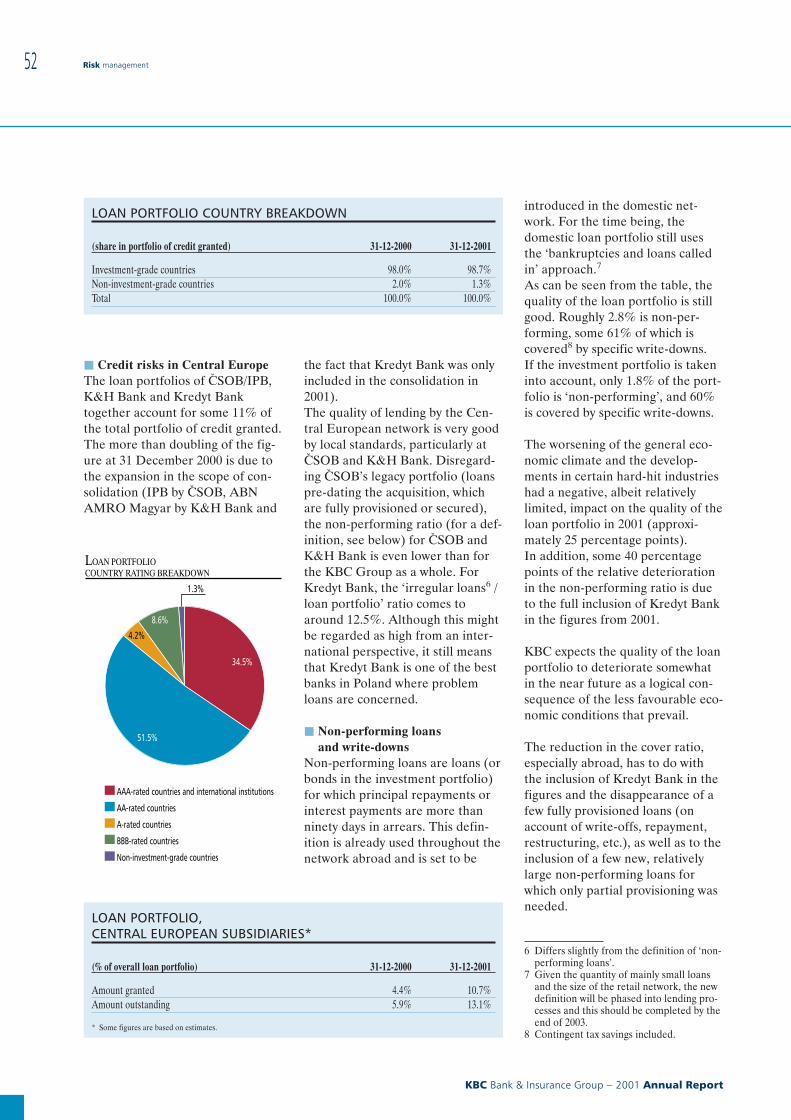

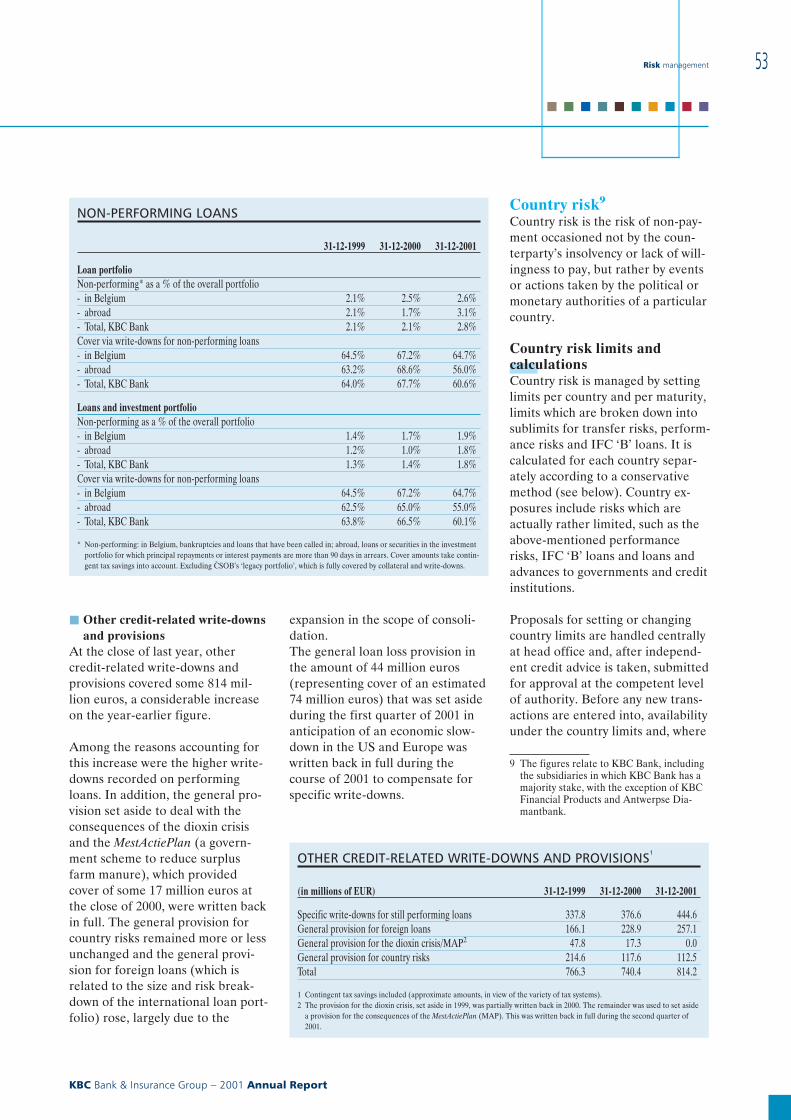

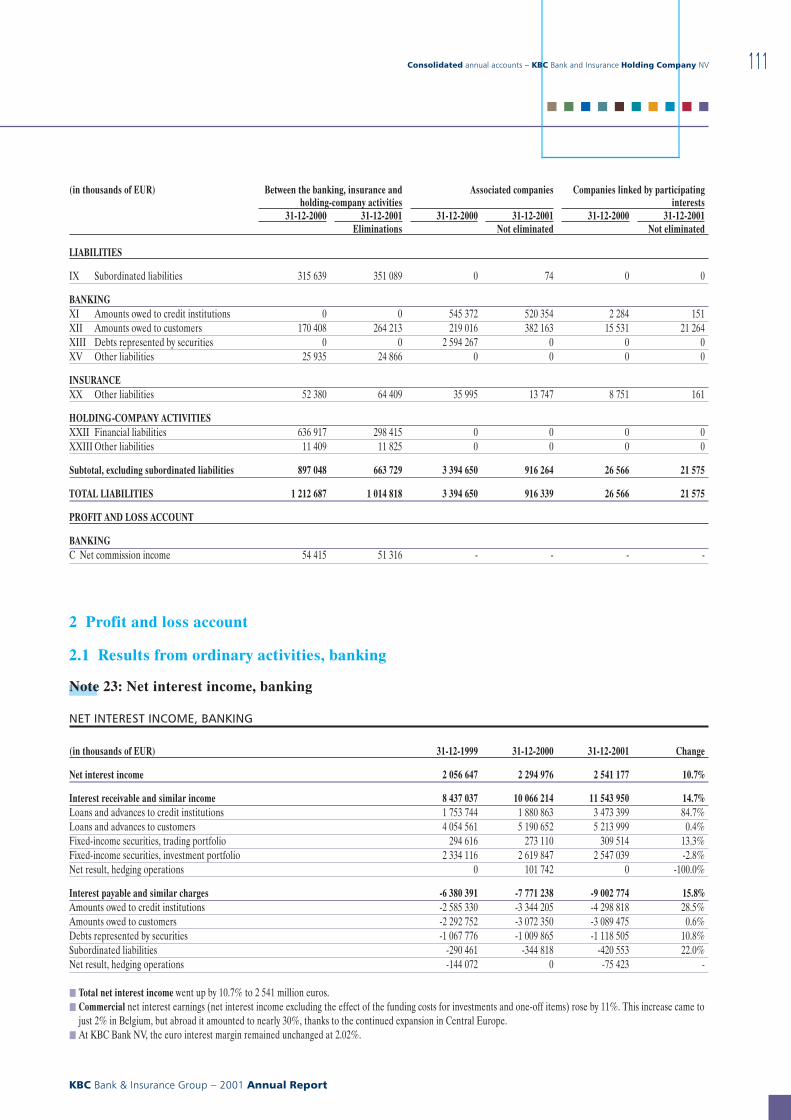

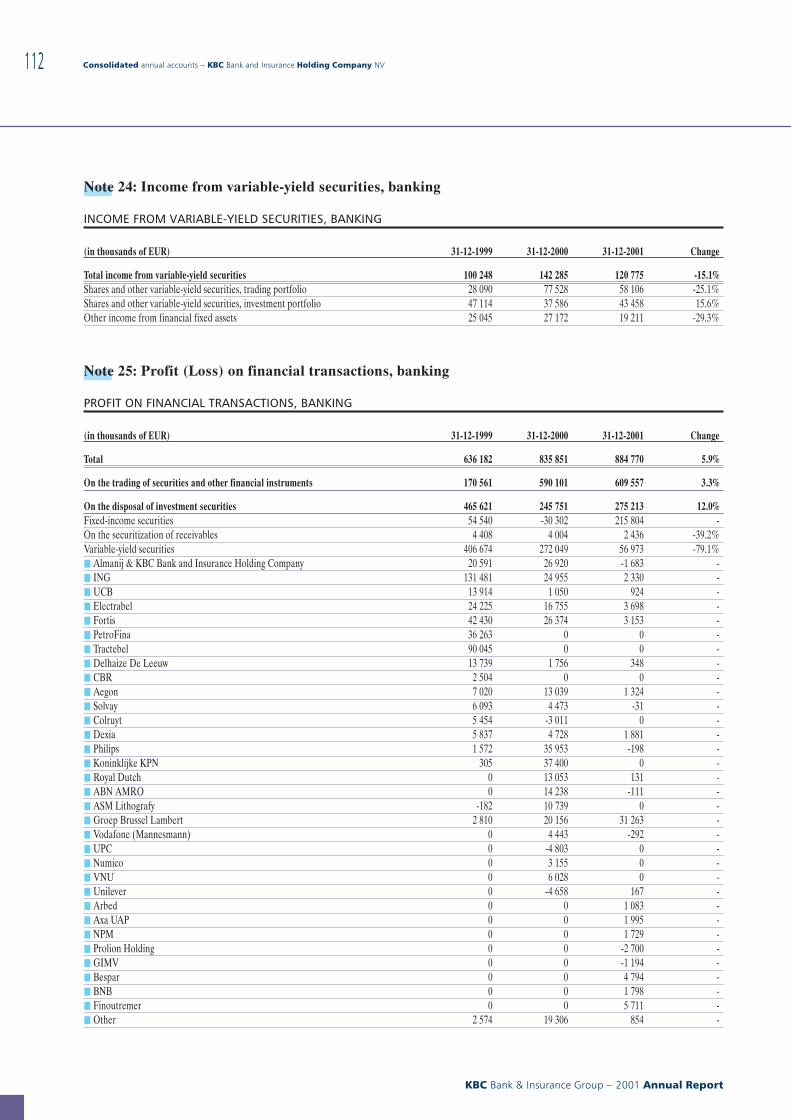

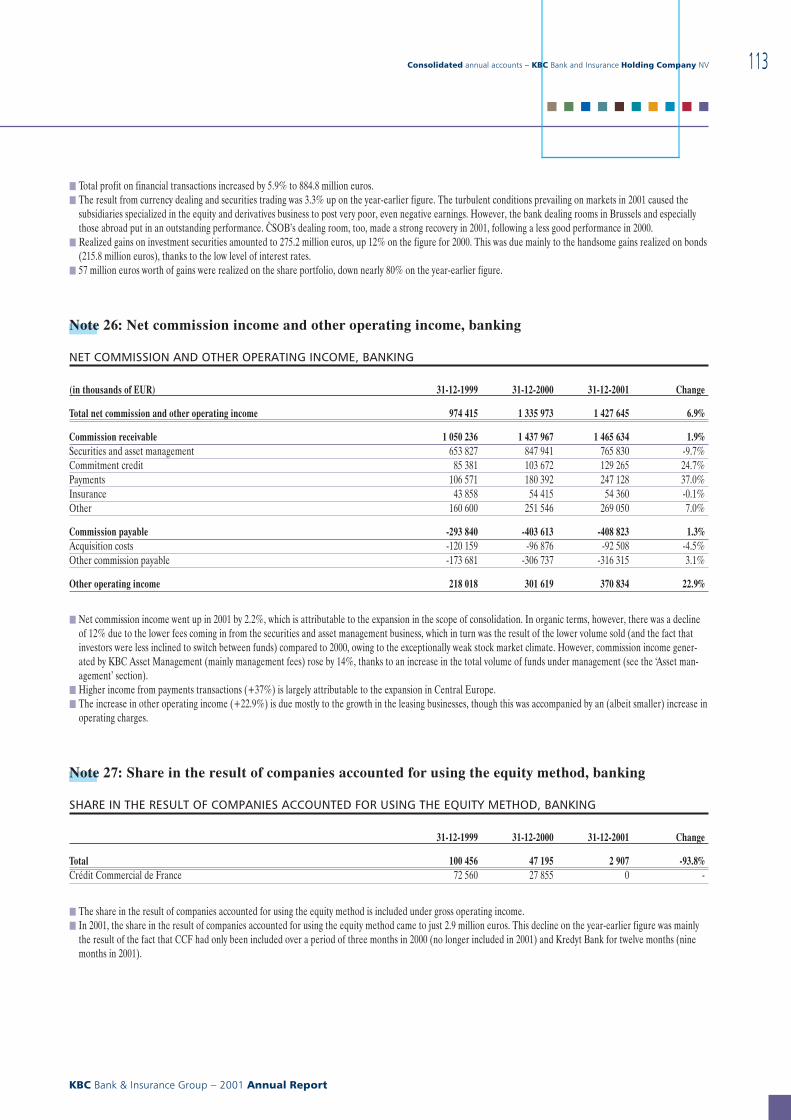

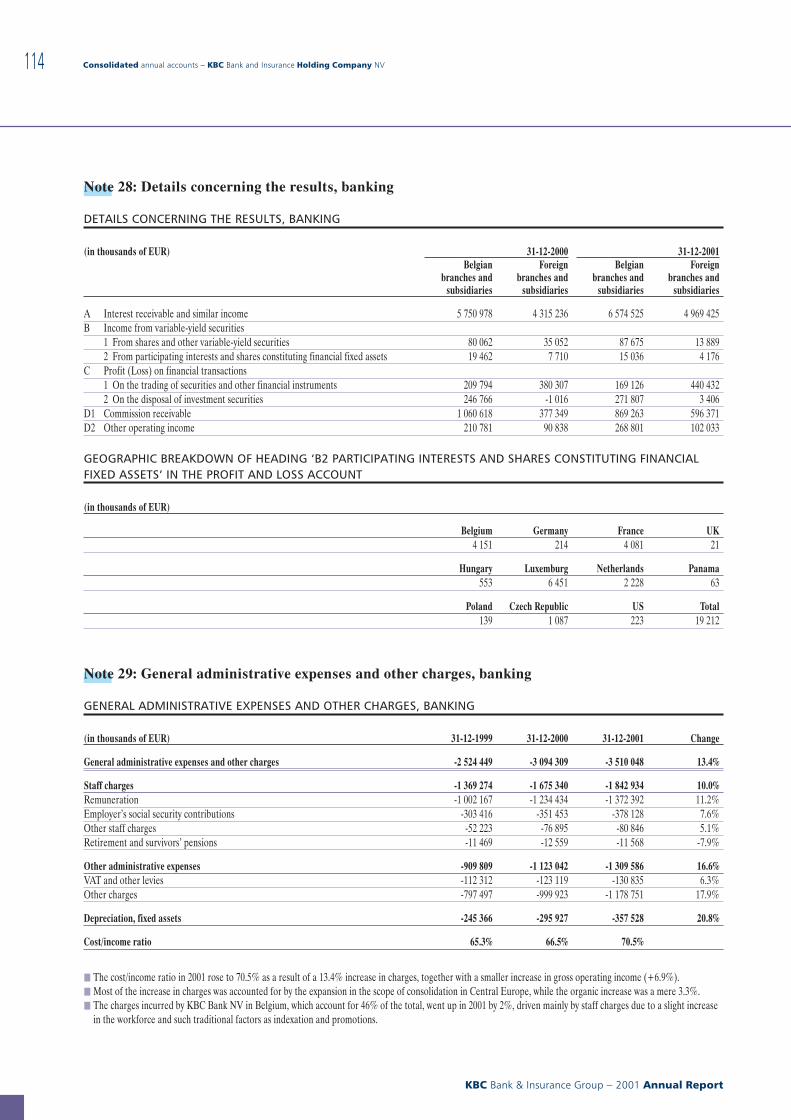

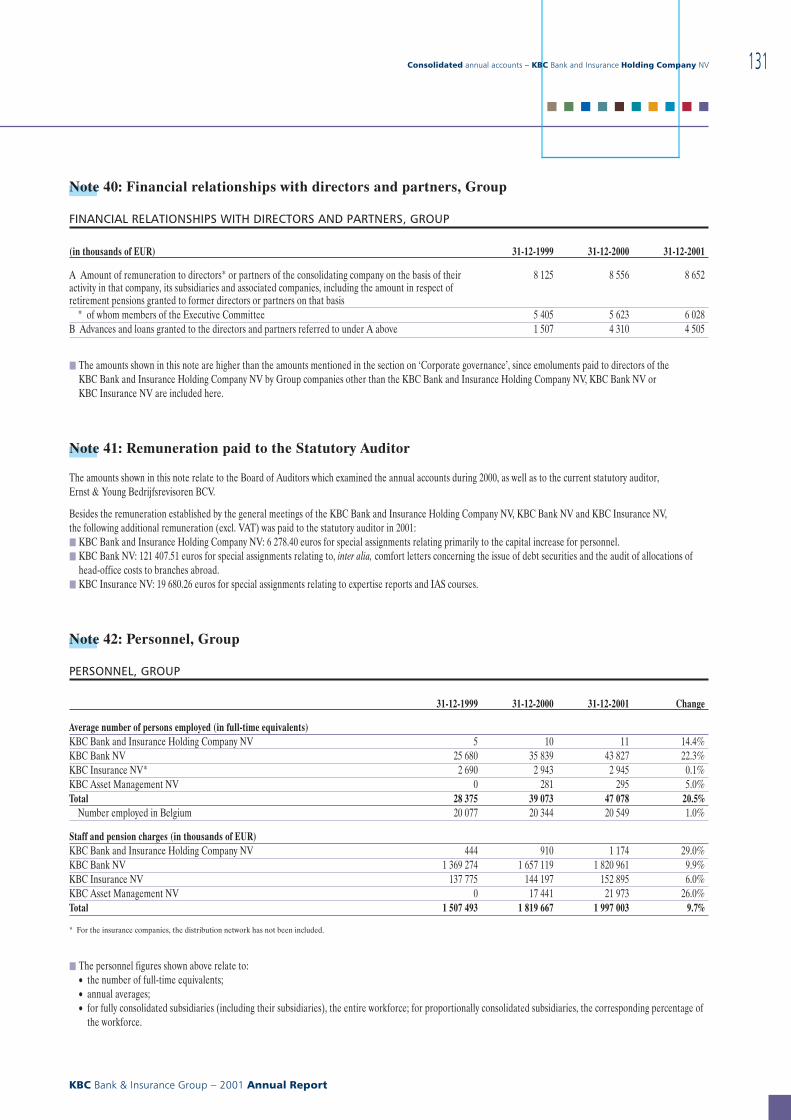

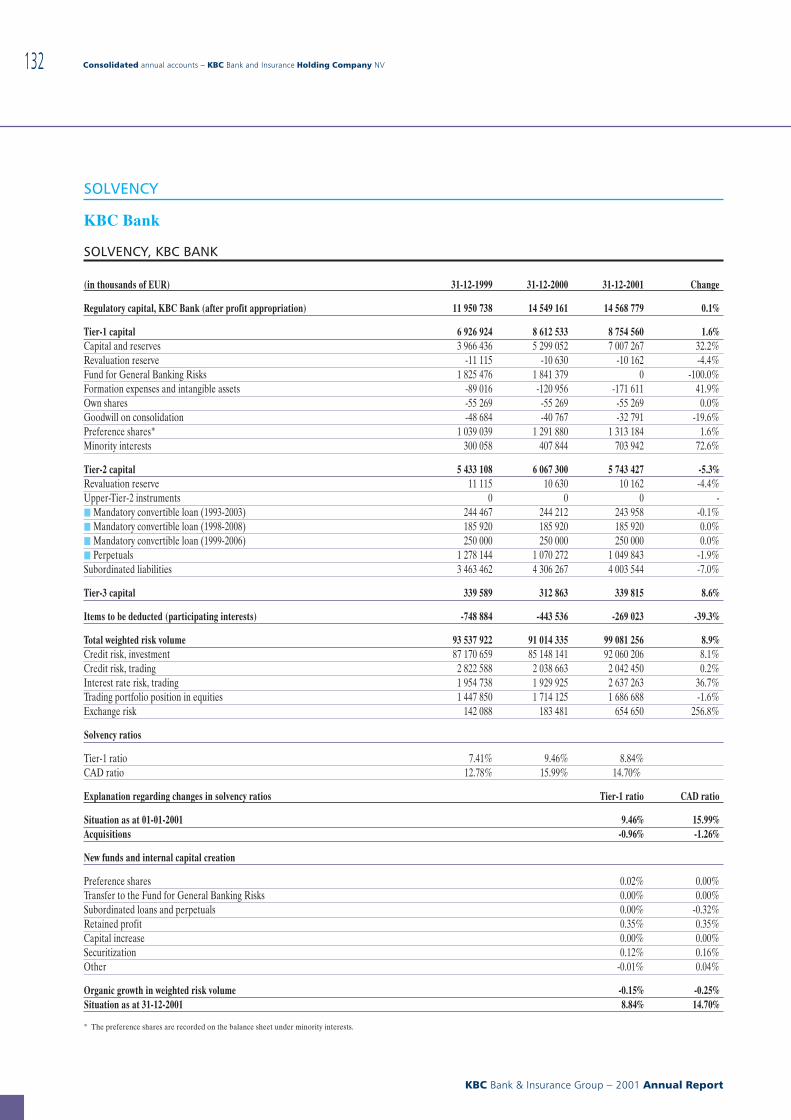

International presence of the KBC Group · International Factors KBC Asset Management KBC Bank KBC...

154

Annual Report 2001

Transcript of International presence of the KBC Group · International Factors KBC Asset Management KBC Bank KBC...

FIRST HOME MARKET:BELGIUM

ADDAlmariskAntwerpse DiamantbankCBC BanqueCentea & KrefimaFideaFin-ForceInternational FactorsKBC Asset ManagementKBC BankKBC Financial Products BrusselsKBC InvestcoKBC LeaseKBC SecuritiesKBC InsuranceSecura

SECOND HOME MARKET: CENTRAL EUROPE*

Agropolisa (Poland)Argosz (Hungary)CSOB (Czech Republic andSlovakia)CSOB Pojist’ovna (Czech Republic)

IPB Pojist’ovna (Czech Republic,since 2000)K&H Bank (Hungary)K&H Life (Hungary)Kredyt Bank (Poland)Patria Finance (Czech Republic)Warta (Poland)

REST OF EUROPE

Assurisk (Luxemburg)Banque Diamantaire Anversoise(Suisse) (Switzerland)FBD (Ireland)IIB Bank (Ireland)KBC Asset Management Limited(Ireland)KBC Bank (representative officesin Italy and Turkey; branches inIreland, the UK, France and theNetherlands; structured financeunits in the UK and Ireland; and a network desk at Banco Urquijoin Spain)KBC Clearing (Netherlands)KBC Bank Deutschland (Germany)KBC Finance Ireland (Ireland)KBC Financial Products (UK, France, Italy)

KBC InternationaleFinancieringsmaatschappij(Netherlands)KBC Lease (UK, Netherlands, France,Luxemburg, Germany)KBC Bank Nederland(Netherlands)KBC Peel Hunt (UK)KBC Securities (France,Netherlands)Lucare (Luxemburg)VITIS Life (Luxemburg)

OUTSIDE EUROPE

KBC Bank (representative officesin Iran and Mexico; a marketingoffice in Malaysia; branches in theUS, Singapore, Hong Kong,Taiwan, the Philippines, thePeople’s Republic of China,Malaysia and India; structuredfinance units in the US, Australiaand Hong Kong)KBC Bank Singapore (Singapore)KBC Financial Products (US, Japan, Hong Kong)KBC Securities (US)

International presence of the KBC Group

Annual Report 2001

2001 An

nu

al R

ep

ort

KBCBa

nk &

Insu

ran

ce

Gro

up

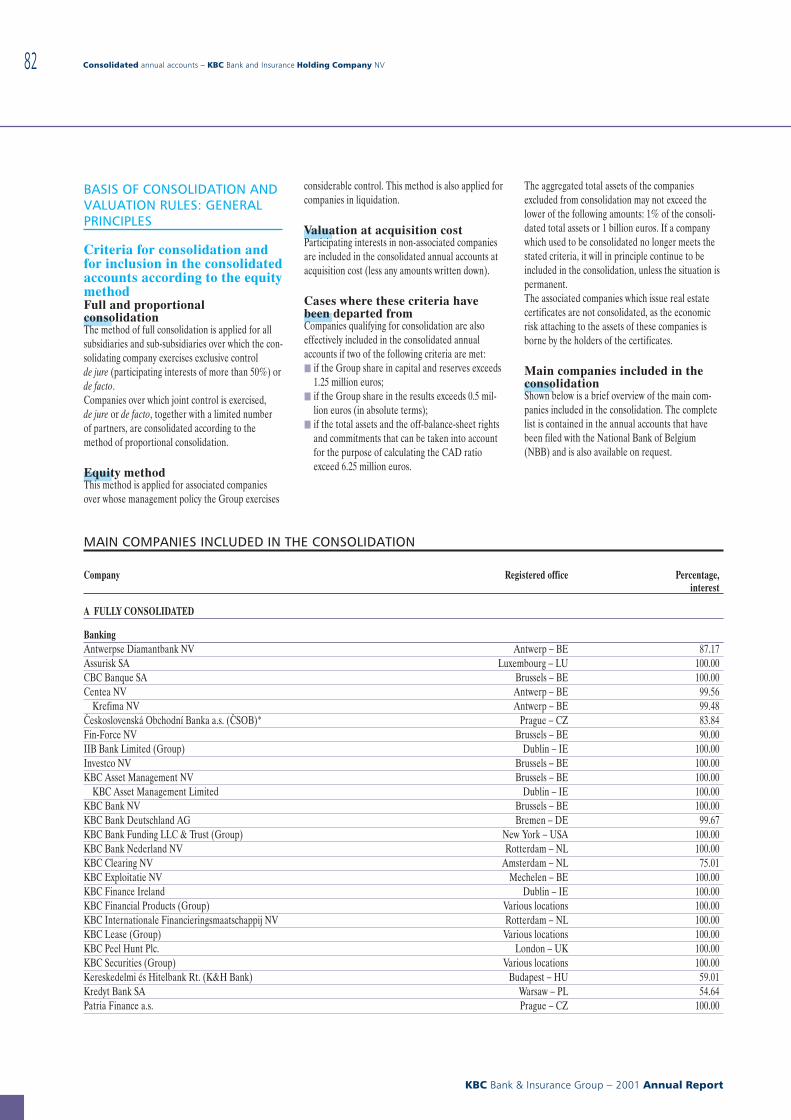

THIS TABLE PROVIDES AN OVERVIEW OF THE INTERNATIONAL NETWORK OF KBC BANK, AS WELL AS

THE MAIN SUBSIDIARIES, SUB-SUBSIDIARIES AND PARTICIPATING INTERESTS OF THE KBC GROUP IN

BELGIUM AND ABROAD.

* Via the representative offices and subsidiaries of CSOB and Kredyt Bank, KBC is also present in Russia, Lithuania and the Ukraine. At the beginning of 2002, the Slovenian government entered into exclusive negotiations with KBC regarding the acquisition of a 34% stake in Nova Ljubljanska banka.However, these negotiations were still ongoing at the time this annual report went to press.

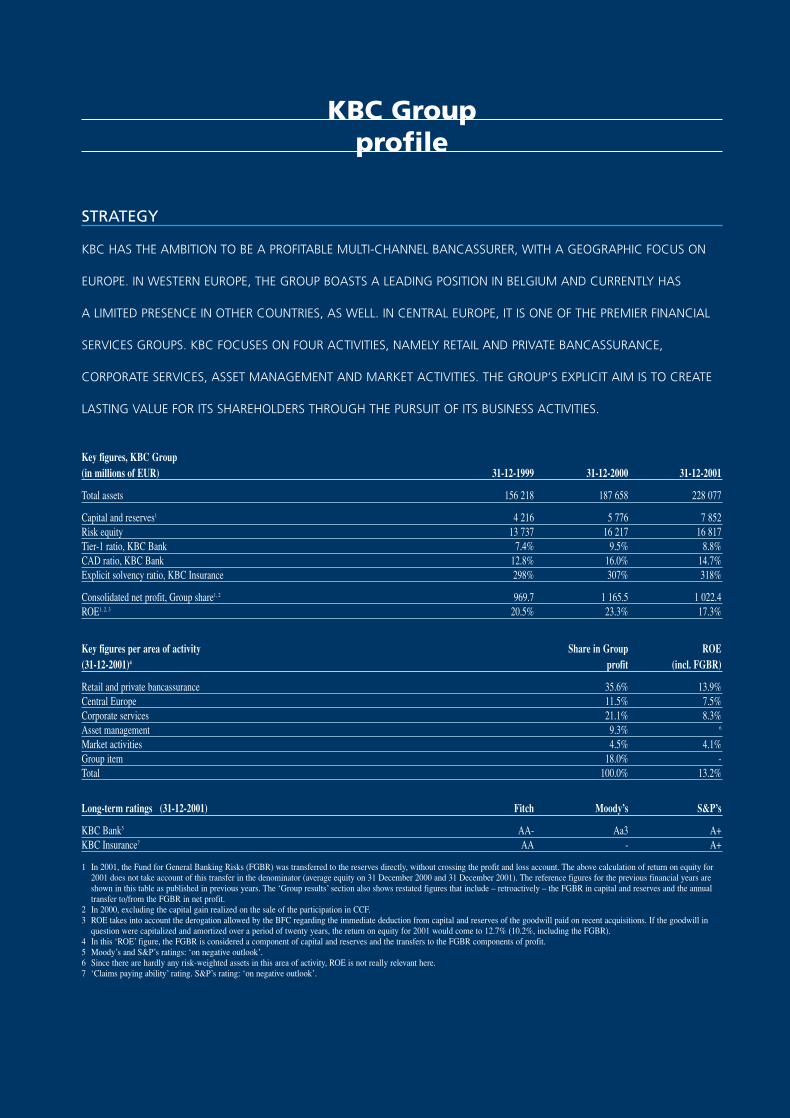

KBC Group profile

STRATEGY

KBC HAS THE AMBITION TO BE A PROFITABLE MULTI-CHANNEL BANCASSURER, WITH A GEOGRAPHIC FOCUS ON

EUROPE. IN WESTERN EUROPE, THE GROUP BOASTS A LEADING POSITION IN BELGIUM AND CURRENTLY HAS

A LIMITED PRESENCE IN OTHER COUNTRIES, AS WELL. IN CENTRAL EUROPE, IT IS ONE OF THE PREMIER FINANCIAL

SERVICES GROUPS. KBC FOCUSES ON FOUR ACTIVITIES, NAMELY RETAIL AND PRIVATE BANCASSURANCE,

CORPORATE SERVICES, ASSET MANAGEMENT AND MARKET ACTIVITIES. THE GROUP’S EXPLICIT AIM IS TO CREATE

LASTING VALUE FOR ITS SHAREHOLDERS THROUGH THE PURSUIT OF ITS BUSINESS ACTIVITIES.

Key figures, KBC Group (in millions of EUR) 31-12-1999 31-12-2000 31-12-2001

Total assets 156 218 187 658 228 077

Capital and reserves1 4 216 5 776 7 852Risk equity 13 737 16 217 16 817Tier-1 ratio, KBC Bank 7.4% 9.5% 8.8%CAD ratio, KBC Bank 12.8% 16.0% 14.7%Explicit solvency ratio, KBC Insurance 298% 307% 318%

Consolidated net profit, Group share1, 2 969.7 1 165.5 1 022.4ROE1, 2, 3 20.5% 23.3% 17.3%

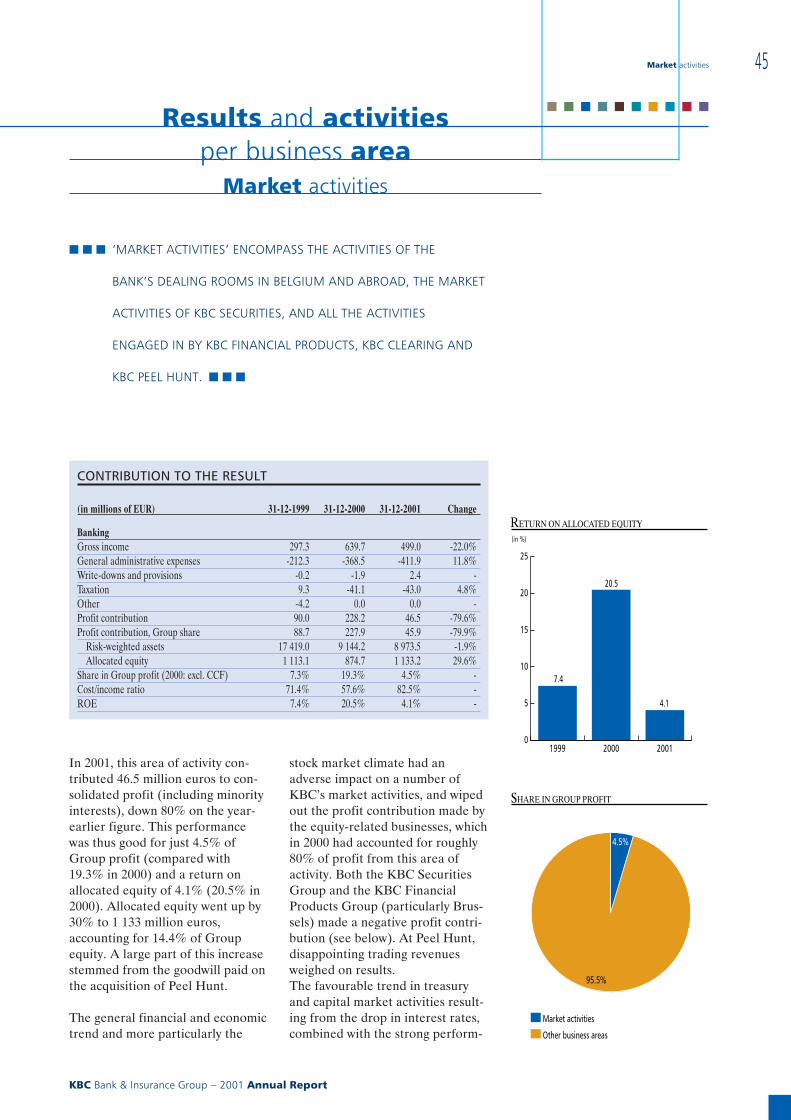

Key figures per area of activity Share in Group ROE(31-12-2001)4 profit (incl. FGBR)

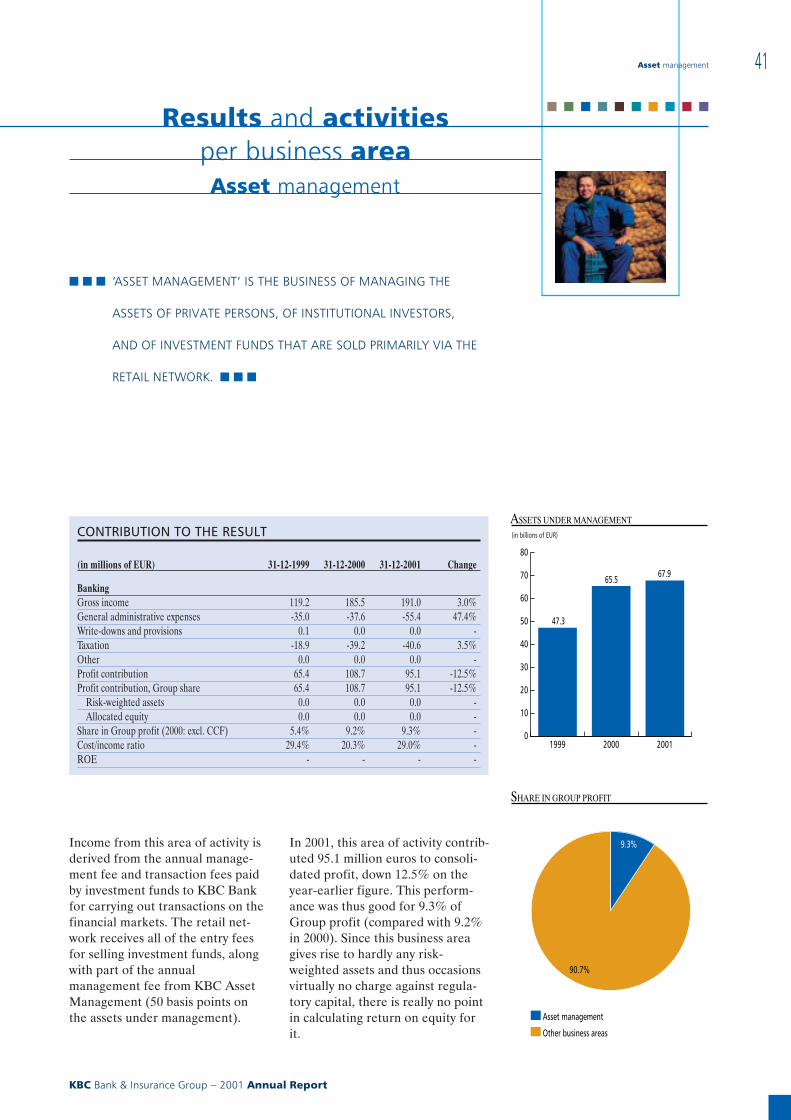

Retail and private bancassurance 35.6% 13.9%Central Europe 11.5% 7.5%Corporate services 21.1% 8.3%Asset management 9.3% 6

Market activities 4.5% 4.1%Group item 18.0% -Total 100.0% 13.2%

Long-term ratings (31-12-2001) Fitch Moody’s S&P’s

KBC Bank5 AA- Aa3 A+KBC Insurance7 AA - A+

1 In 2001, the Fund for General Banking Risks (FGBR) was transferred to the reserves directly, without crossing the profit and loss account. The above calculation of return on equity for2001 does not take account of this transfer in the denominator (average equity on 31 December 2000 and 31 December 2001). The reference figures for the previous financial years areshown in this table as published in previous years. The ‘Group results’ section also shows restated figures that include – retroactively – the FGBR in capital and reserves and the annualtransfer to/from the FGBR in net profit.

2 In 2000, excluding the capital gain realized on the sale of the participation in CCF. 3 ROE takes into account the derogation allowed by the BFC regarding the immediate deduction from capital and reserves of the goodwill paid on recent acquisitions. If the goodwill in

question were capitalized and amortized over a period of twenty years, the return on equity for 2001 would come to 12.7% (10.2%, including the FGBR).4 In this ‘ROE’ figure, the FGBR is considered a component of capital and reserves and the transfers to the FGBR components of profit.5 Moody’s and S&P’s ratings: ‘on negative outlook’.6 Since there are hardly any risk-weighted assets in this area of activity, ROE is not really relevant here.7 ‘Claims paying ability’ rating. S&P’s rating: ‘on negative outlook’.

International presence of the KBC Group

At the beginning of 2002, the Slovenian government entered into exclusive negotiations with KBC regarding the acquisition of a 34% stake in Nova Ljubljanska banka.However, these negotiations were still ongoing at the time this annual report went to press.

USE OF THE ANNUAL REPORTFOR THE PROVISION OF INFORMATION VIA SEPARATE DOCUMENTS

On 27 March 2002, the Belgian Banking and Finance Commission granted the KBC Bank and Insurance Holding Company NV authorization touse the present annual report as a reference document to solicit savings from the public under Title II of Royal Decree No. 185 of 9 July 1935,by means of the procedure for the provision of information via separate documents, and this until such time as the KBC Bank and InsuranceHolding Company NV publishes its next annual report.For the purpose of the above procedure, this annual report must be accompanied by a transaction memorandum in order to constitute a pro-spectus in the sense of Article 29 of the Royal Decree referred to above.This prospectus will be submitted to the Banking and Finance Commission for approval in accordance with Article 29ter, §1, paragraph one,of Royal Decree No. 185 of 9 July 1935.

Annual Report 2001

THE

PIC

TURE

SIN

THIS

AN

NU

AL

REPO

RTW

ERE

USE

DIN

THE

AD

VER

TISI

NG

CA

MPA

IGN

LAU

NC

HED

BYTH

EKB

CBA

NK

&IN

SURA

NC

EG

ROU

PIN

2001

.

P IC

TURE

USE

DIN

THE

2001

KBC

IMA

GE

CAM

PAIG

N.

Report of the Board of Directors to the annual meeting of shareholders

" Statement by the Chairmanof the Board of Directors andthe President of the Executive Committee ............ 4

" Executive Committee .............................................. 7

" Strategy ................................................................... 8

Area of operation and activities ............................ 8Geographic focus .............................................. 8Focus on activities ............................................. 8Focus on clientele ............................................. 8

Financial targets for 2000-2004 ............................. 9Measures taken to meet the merger objectives .... 9

" Shareholder information ..................................... 10

Shareholders ......................................................... 10Annual return ....................................................... 10Ratings .................................................................. 10Key figures per share ............................................ 11Net asset value ...................................................... 11

" Group results ........................................................ 12

Key figures, KBC Group ...................................... 12Transfer of the fund for general banking risksto the reserves ....................................................... 12Consolidated balance sheet, KBC Group ........... 13Consolidated results, KBC Group ....................... 14Comments ............................................................. 15

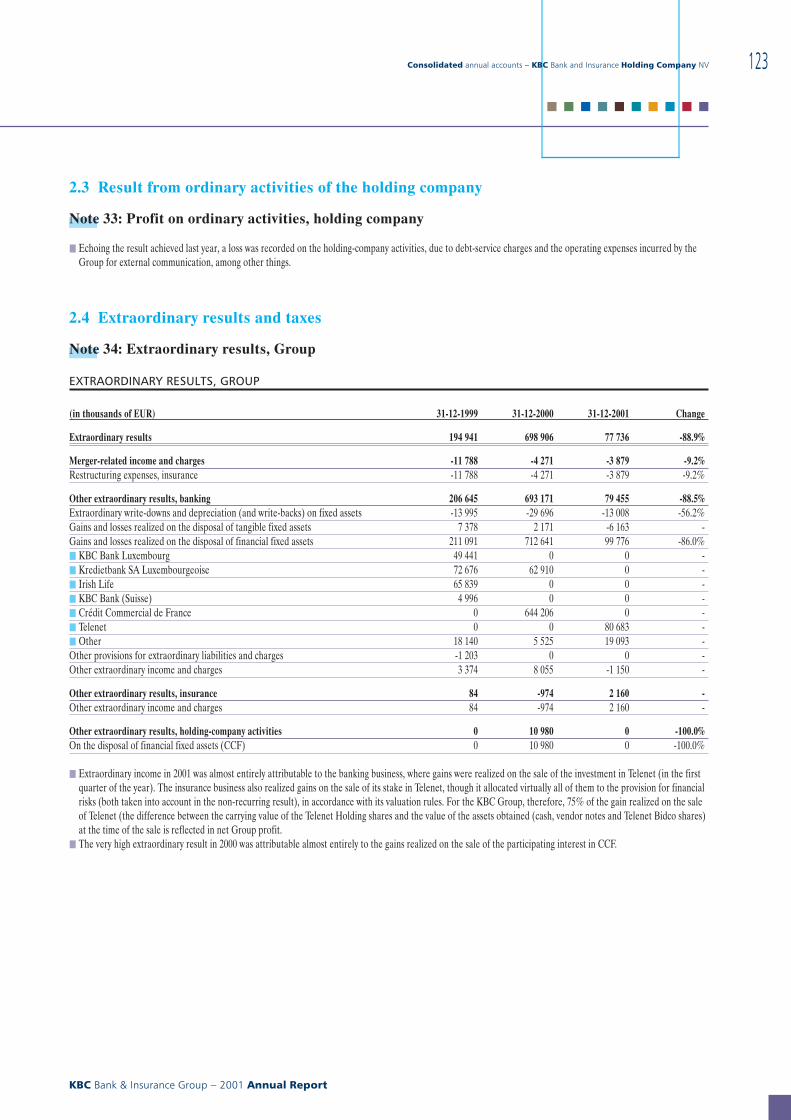

General ............................................................ 15Operating activities − banking ....................... 16Operating activities − insurance .................... 18Holding-company activities ............................ 20Extraordinary result and taxation .................. 21Profit outlook .................................................. 21

Breakdown by area of activity .............................. 21

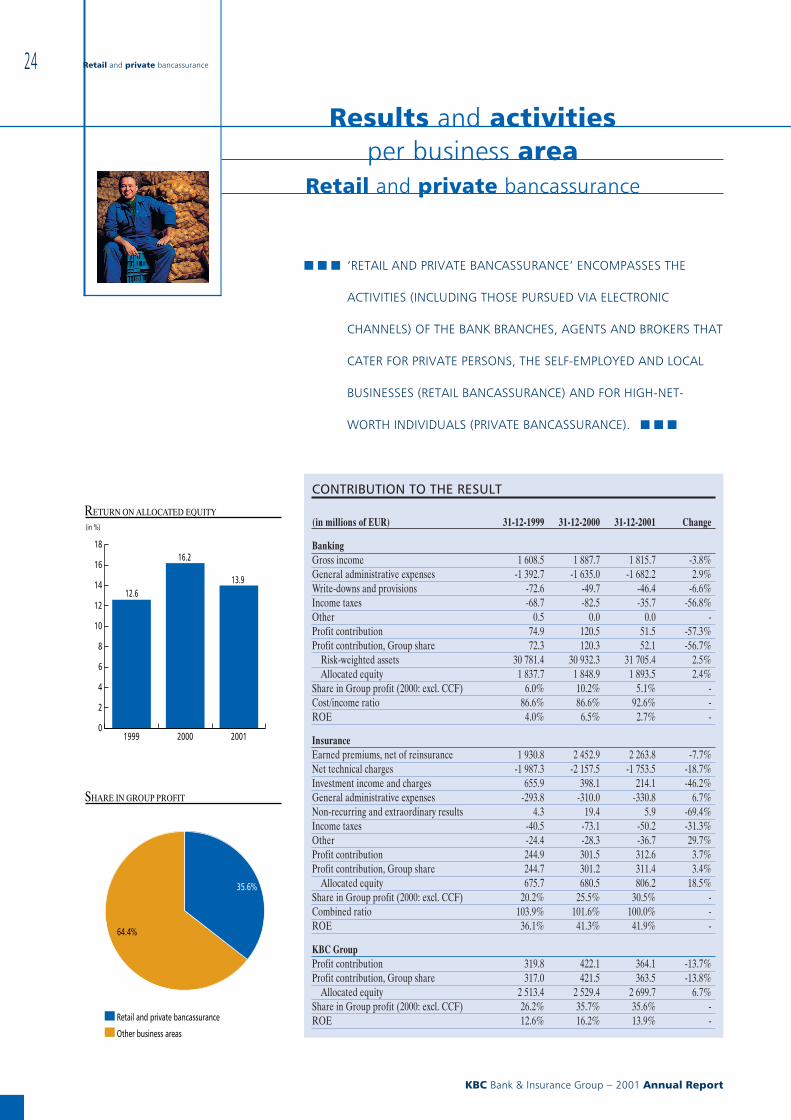

" Results and activities per business area ............. 24

Retail and private bancassurance ........................ 24Contribution to the result .............................. 24Highlights ........................................................ 25Key figures for the main subsidiaries ............ 30

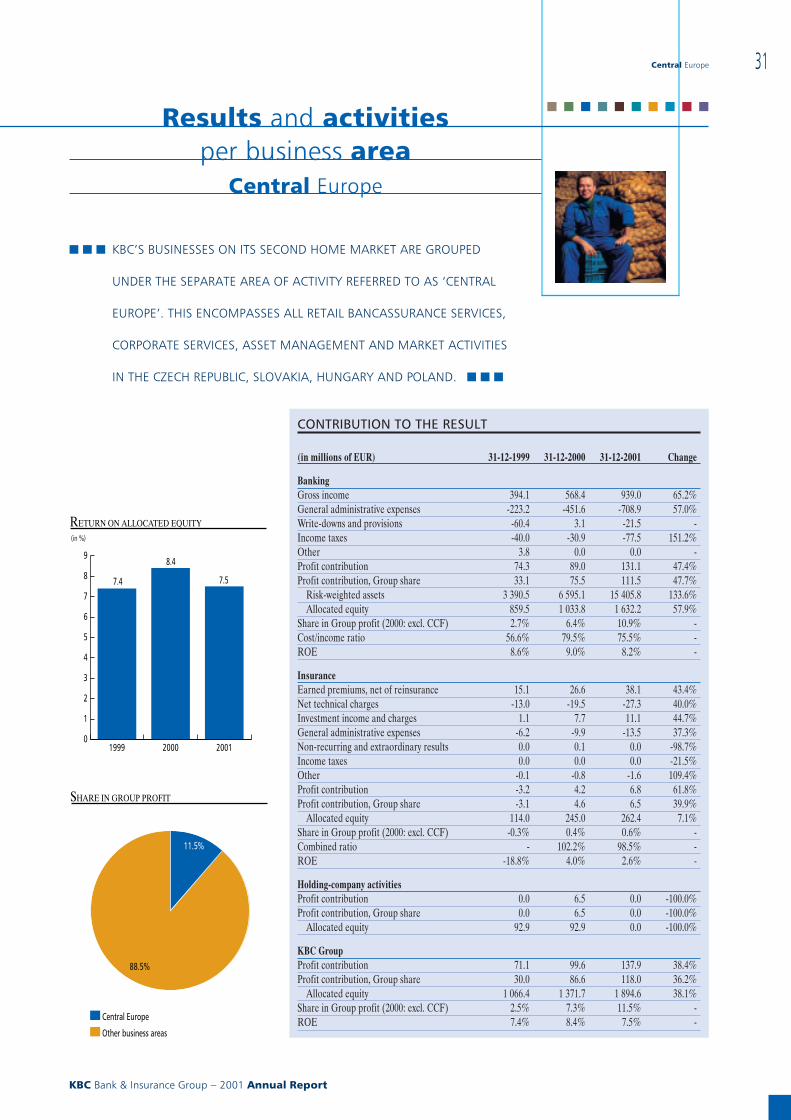

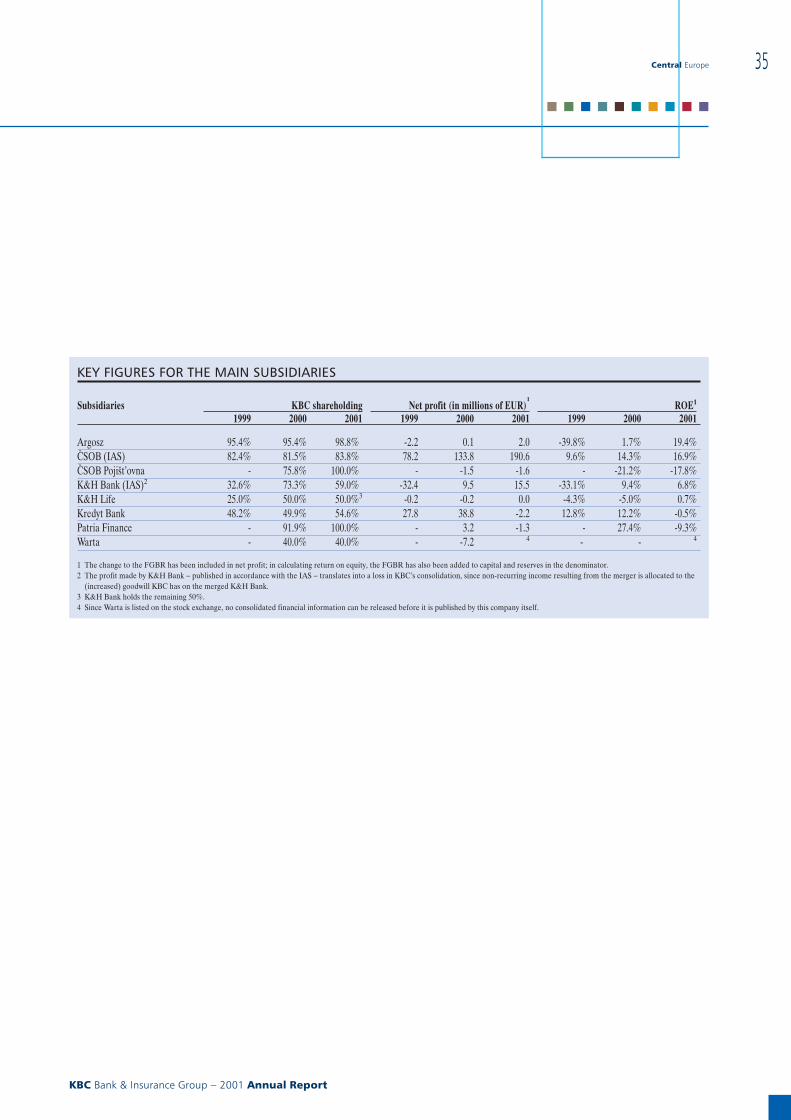

Central Europe ..................................................... 31Contribution to the result .............................. 31Highlights ........................................................ 32Key figures for the main subsidiaries ............ 35

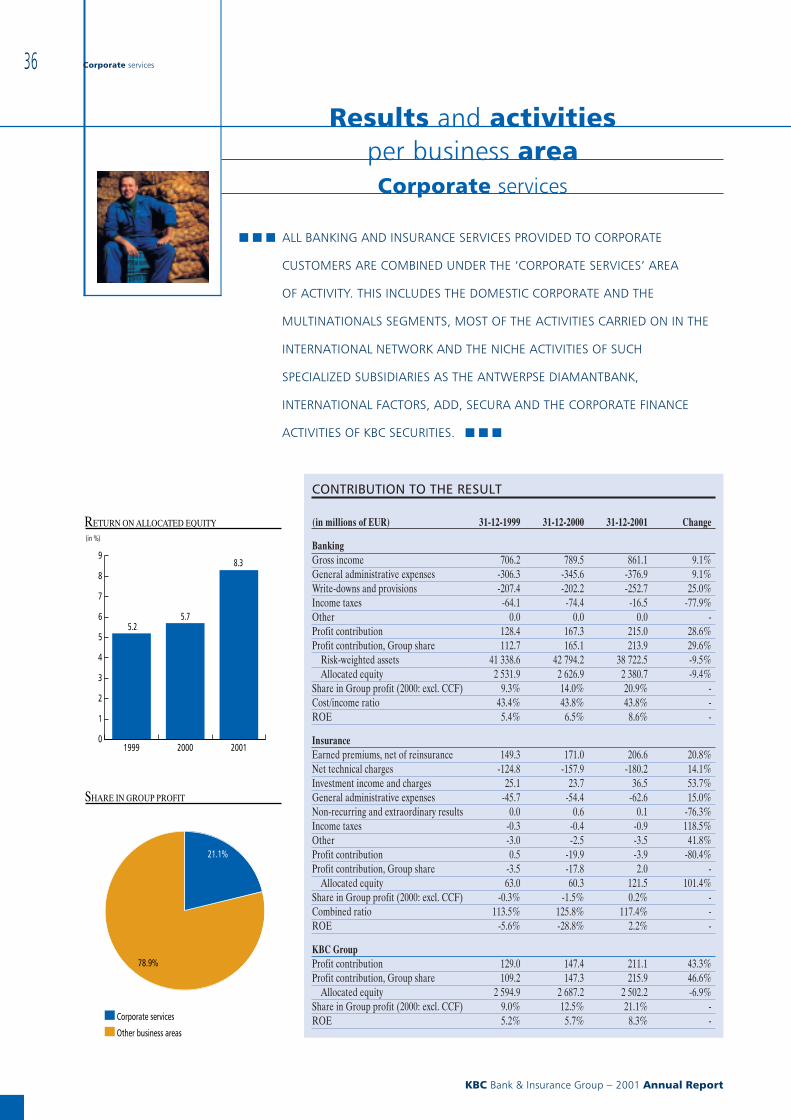

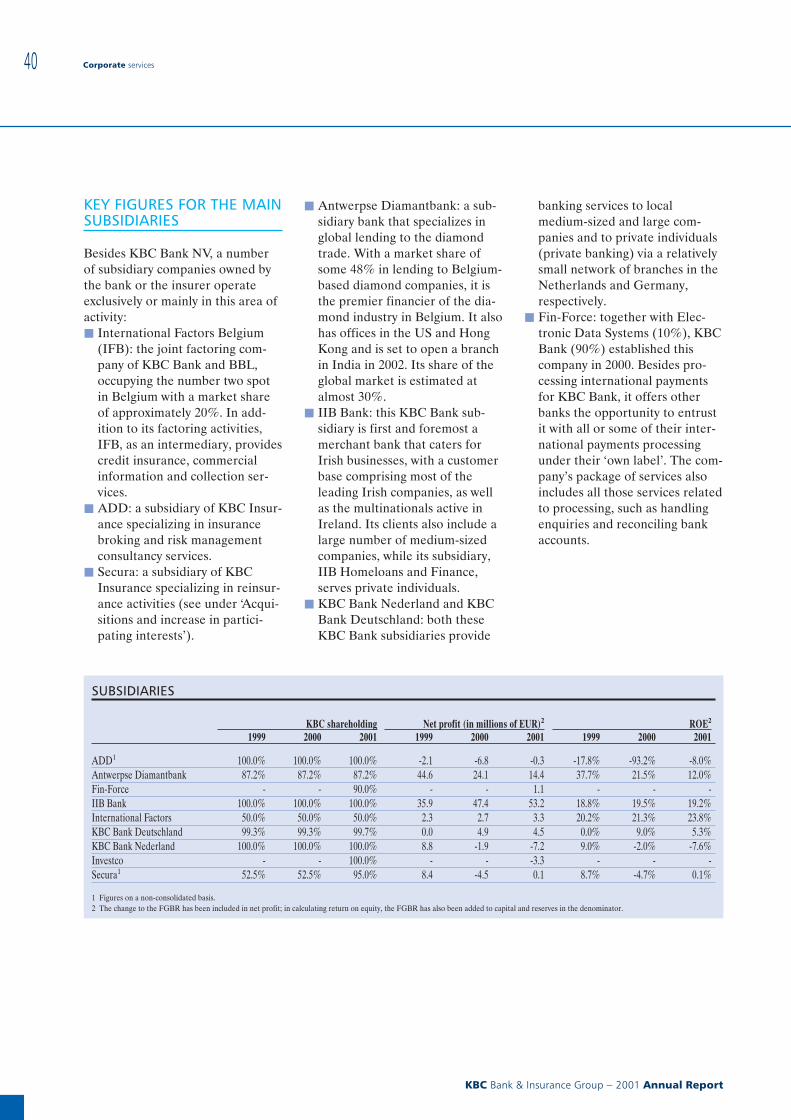

Corporate services ................................................ 36Contribution to the result .............................. 36Highlights ........................................................ 37Key figures for the main subsidiaries ............ 40

Asset management ............................................... 41Contribution to the result .............................. 41Highlights ........................................................ 42Key figures for the main subsidiaries ............ 44

Market activities ................................................... 45Contribution to the result .............................. 45Highlights ........................................................ 46Key figures for the main subsidiaries ............ 47

" Risk management ................................................. 48

Risk management within the Group ................... 48Risk management at KBC Bank .......................... 48

Counterparty risk ............................................ 48Country risk ..................................................... 53Internal credit risk models ............................. 55Market risks .................................................... 56Liquidity risk ................................................... 59

Risk management at KBC Insurance .................. 59Risk governance .............................................. 59Investment risks .............................................. 59Underwriting risks .......................................... 60Value management ......................................... 62

Operational risks .................................................. 62Internal Control Policy Manual ..................... 62Risk identification andmeasurement pilot project ............................. 62Further developments in 2002 ....................... 63

Compliance ........................................................... 63

Report of the Board of Directors to the annual meeting of shareholders

KBC Bank & Insurance Group − 2001 Annual Report

2

Table of contentsAnnual Report 2001

" Personnel .............................................................. 64

Personnel policy .................................................... 64Employee satisfaction ..................................... 64Negotiations with the social partners ............ 64Training ............................................................ 64Measures taken to complete the merger ....... 65

Staffing levels ........................................................ 65

" Group structure and corporate governance ....... 67

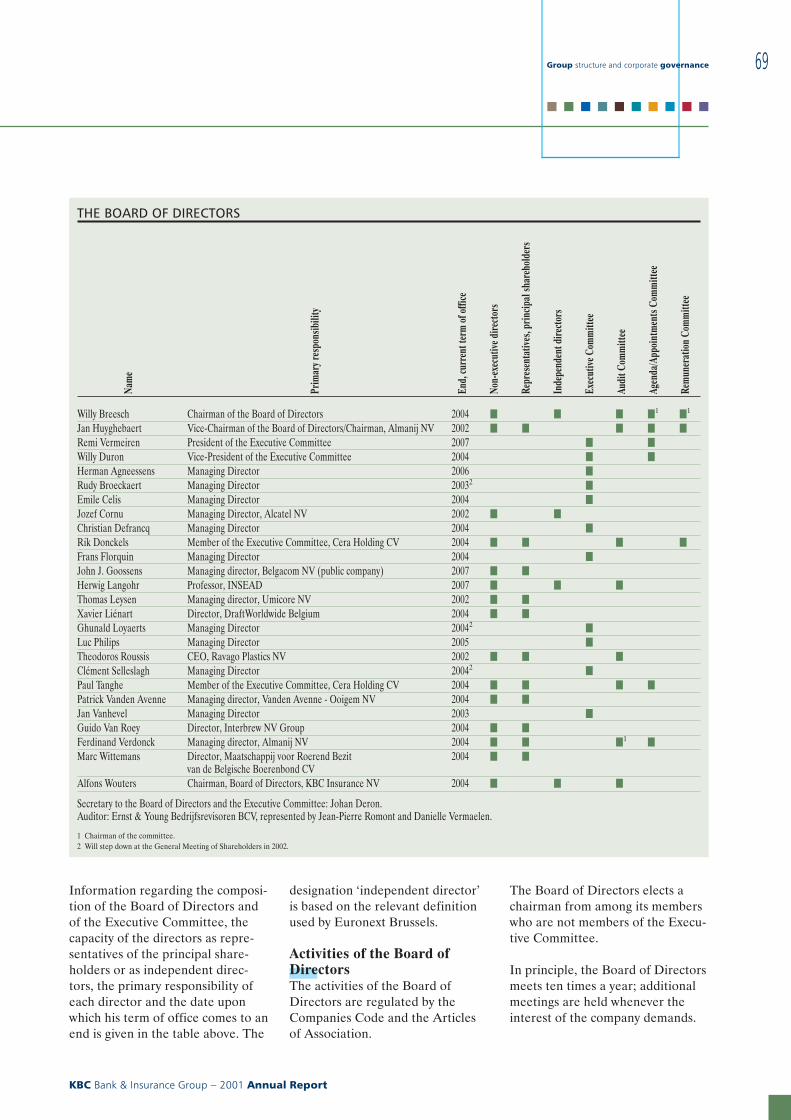

Group structure .................................................... 67Corporate Governance ......................................... 68

1 Management structure ................................ 682 Board of Directors ....................................... 683 Executive Committee .................................. 714 Committees set up by

the Board of Directors ................................. 725 Profit allocation policy ................................ 736 Relations with the principal shareholders .. 737 Appointments ............................................... 738 Prospects for the KBC Bank

and Insurance Holding Company ............... 739 Board of Directors of

KBC Bank and of KBC Insurance .............. 73Open communication with shareholders ............ 74

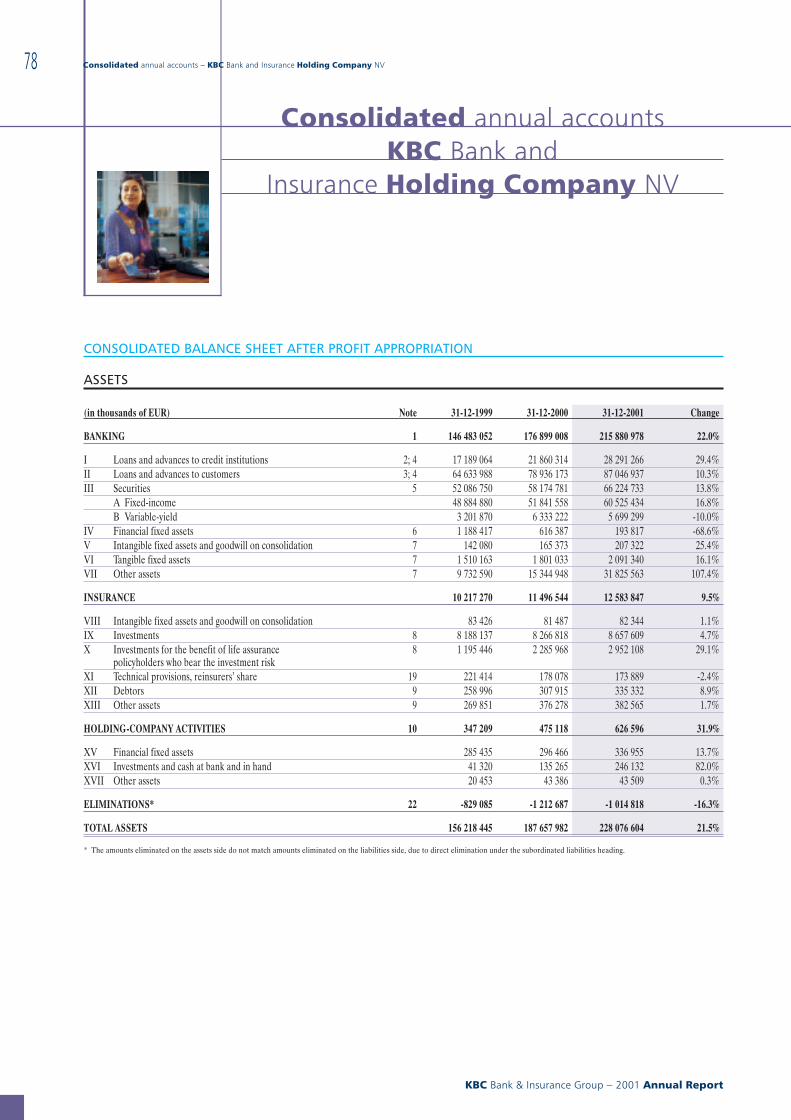

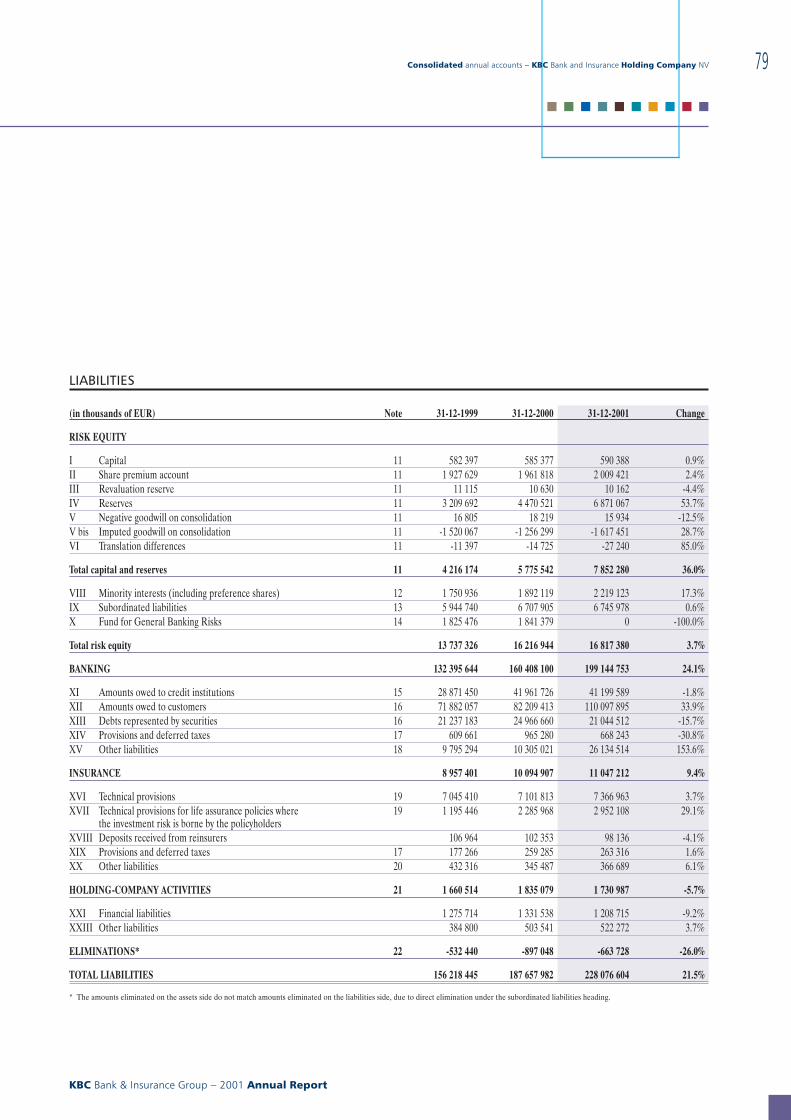

" Consolidated annual accounts − KBC Bank andInsurance Holding Company NV ........................ 78

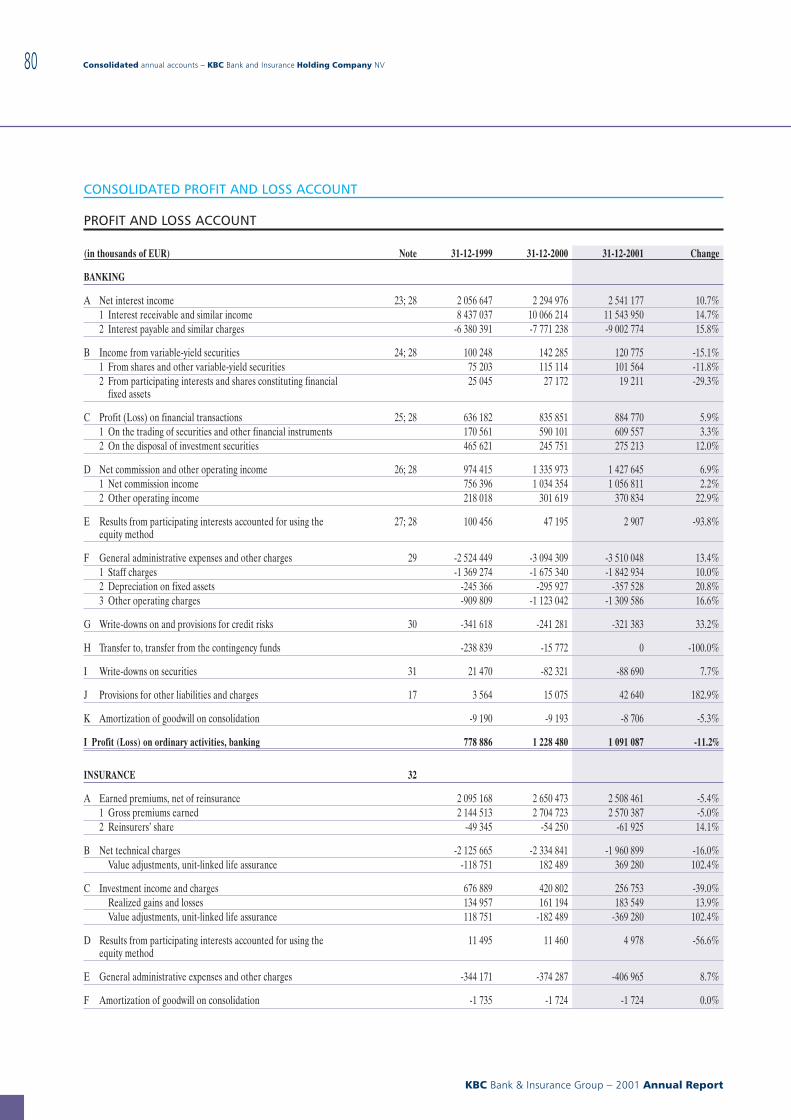

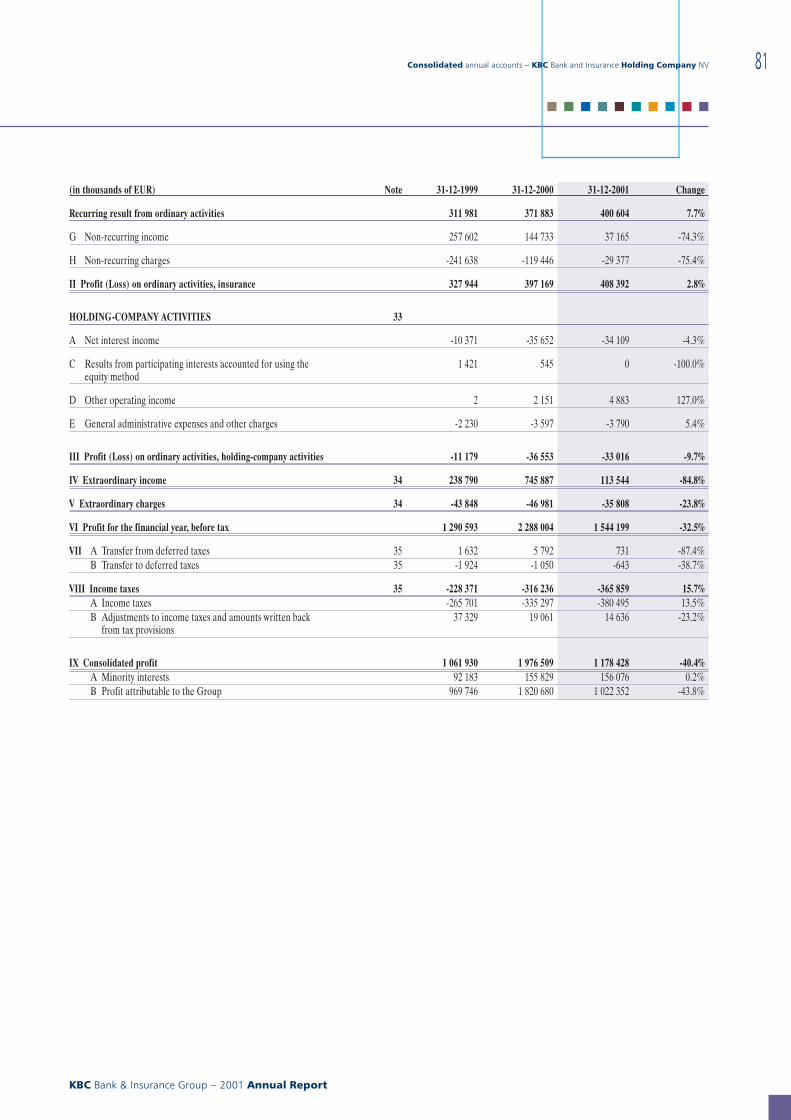

Consolidated balance sheet afterprofit appropriation .............................................. 78Consolidated profit and loss account .................. 80Basis of consolidation and valuation rules:general principles ................................................. 82

Criteria for consolidation and for inclusionin the consolidated accounts according tothe equity method ........................................... 82Accounting principles and valuation rules:general principles ............................................ 85

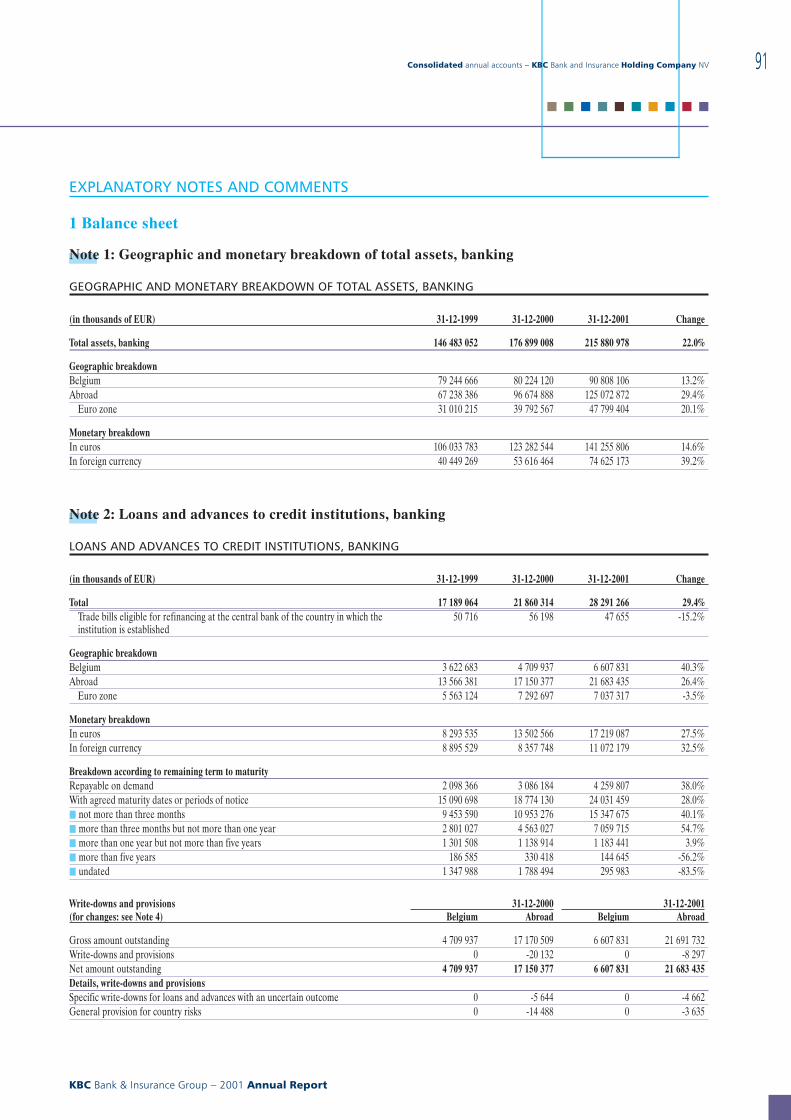

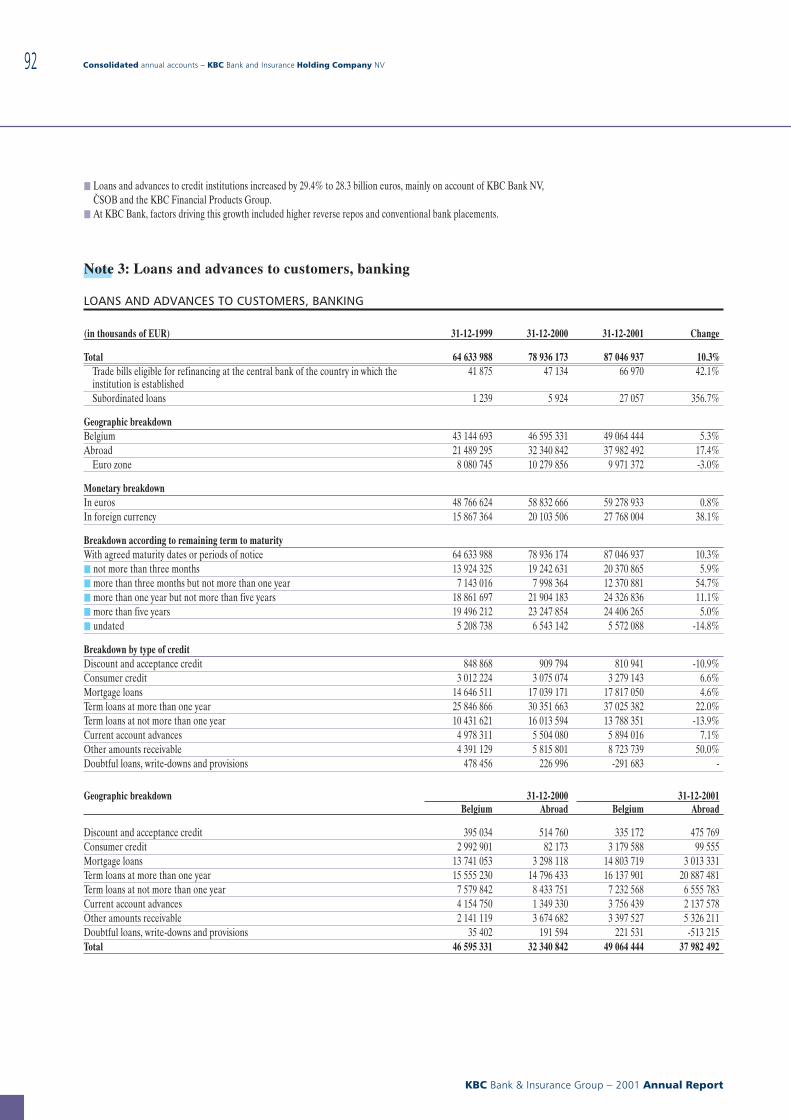

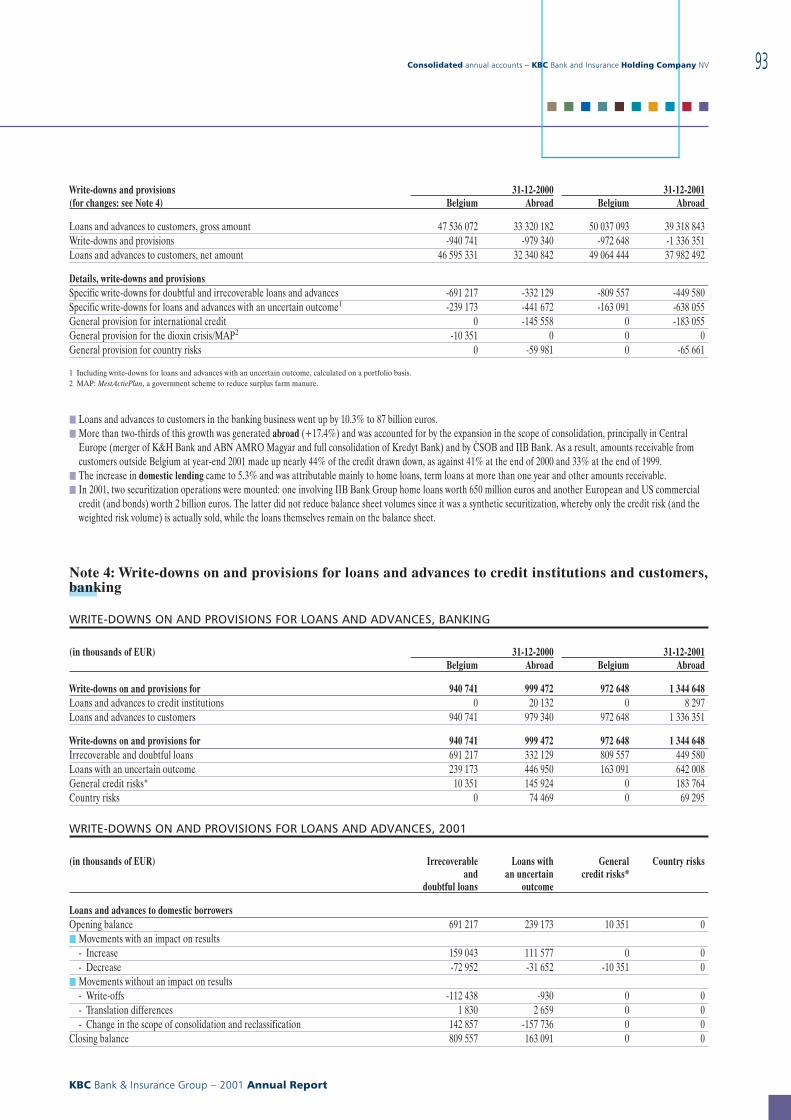

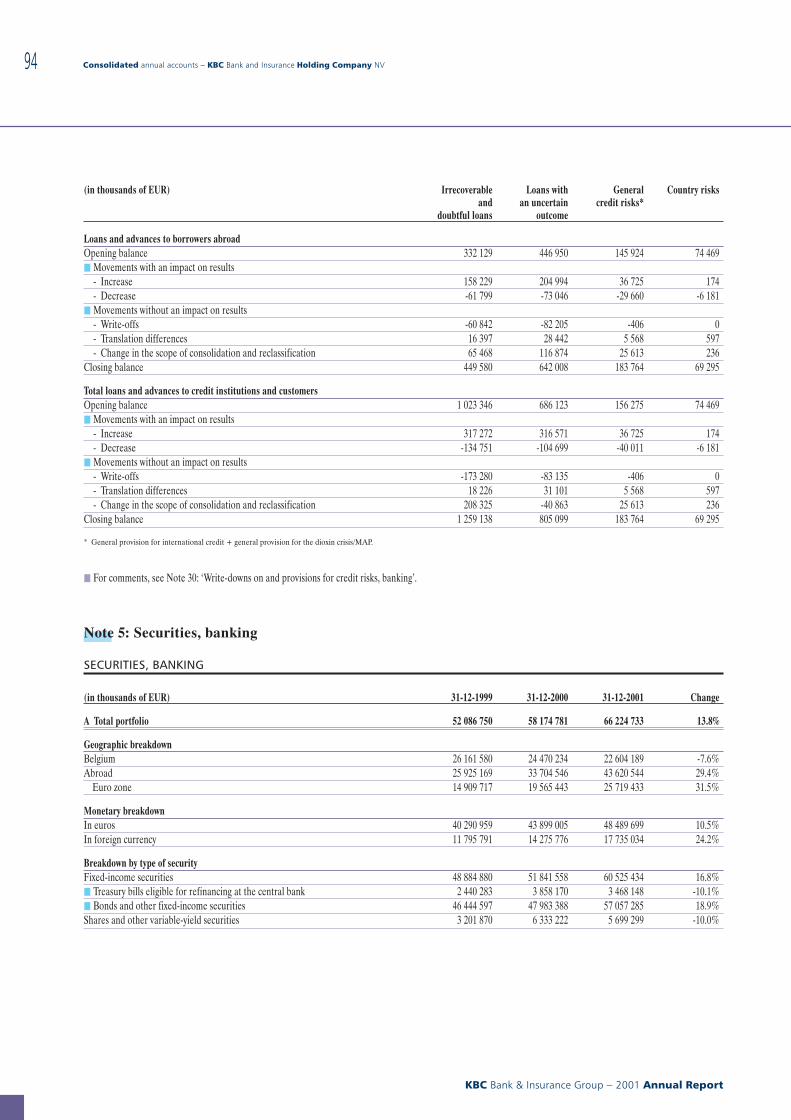

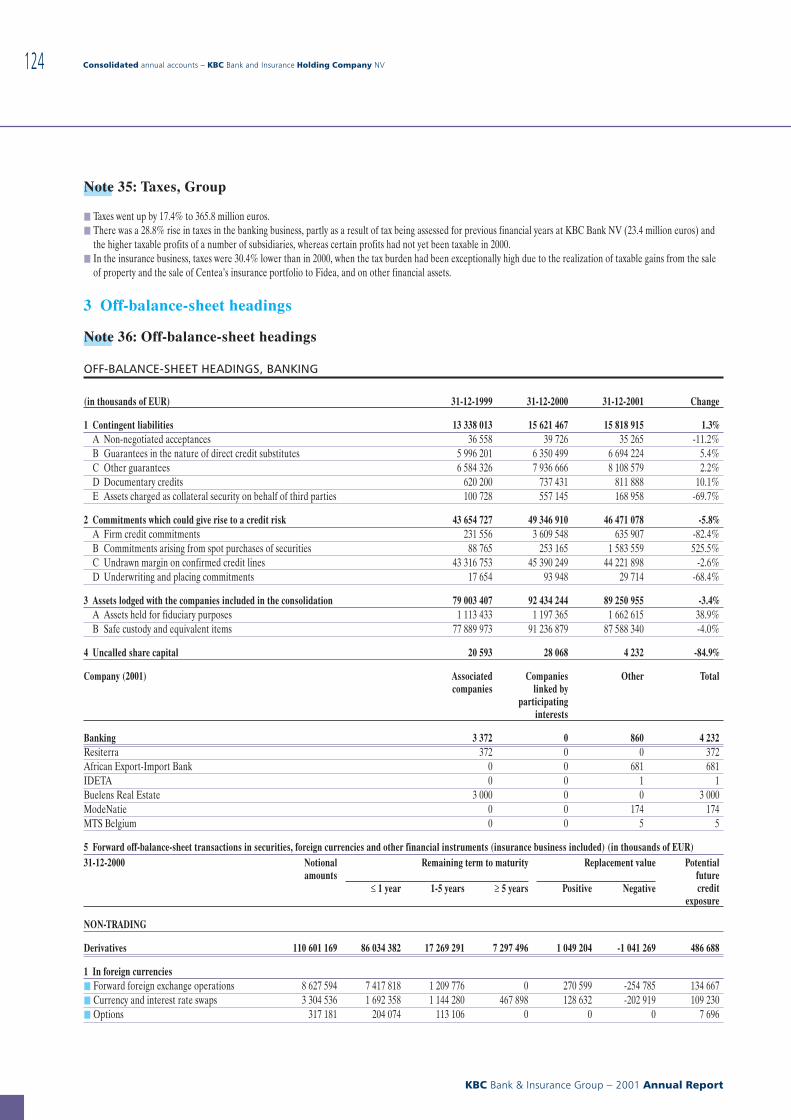

Explanatory notes and comments ........................ 911 Balance sheet ............................................... 912 Profit and loss account .............................. 1113 Off-balance-sheet headings ....................... 1244 Miscellaneous ............................................. 129

Solvency ............................................................... 132KBC Bank ..................................................... 132KBC Insurance .............................................. 134

Statutory auditor’s report on the consolidatedfinancial statements ............................................ 135

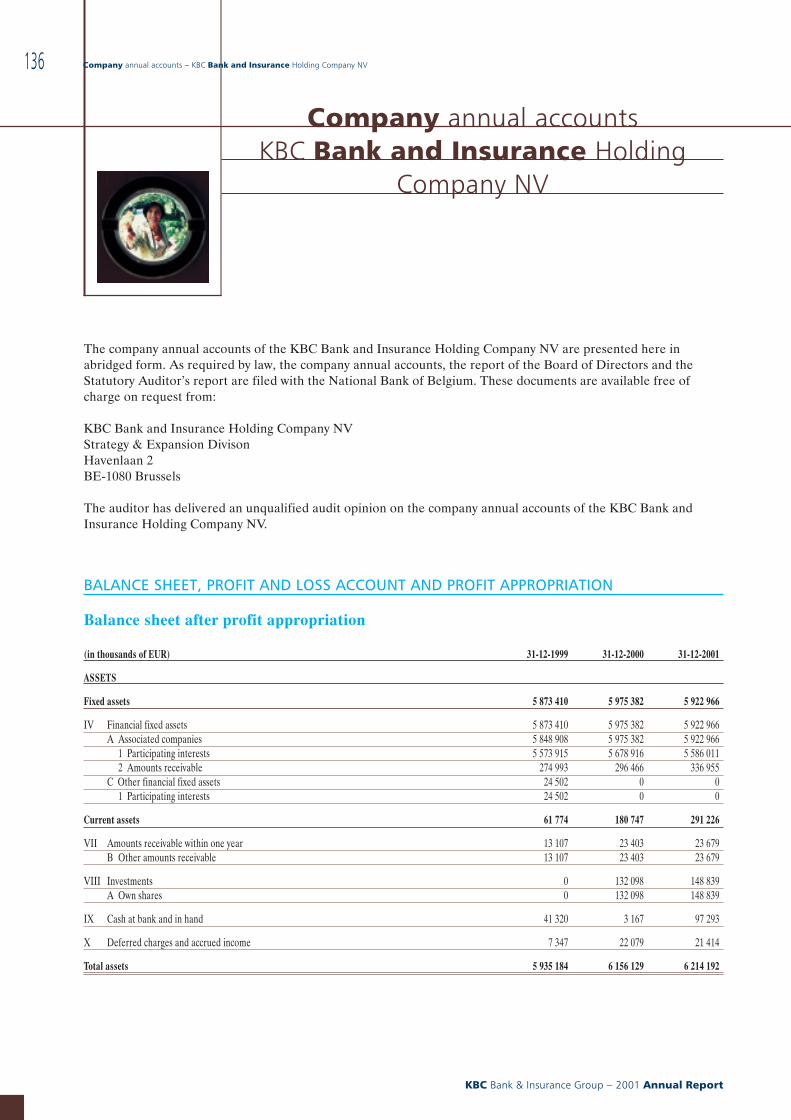

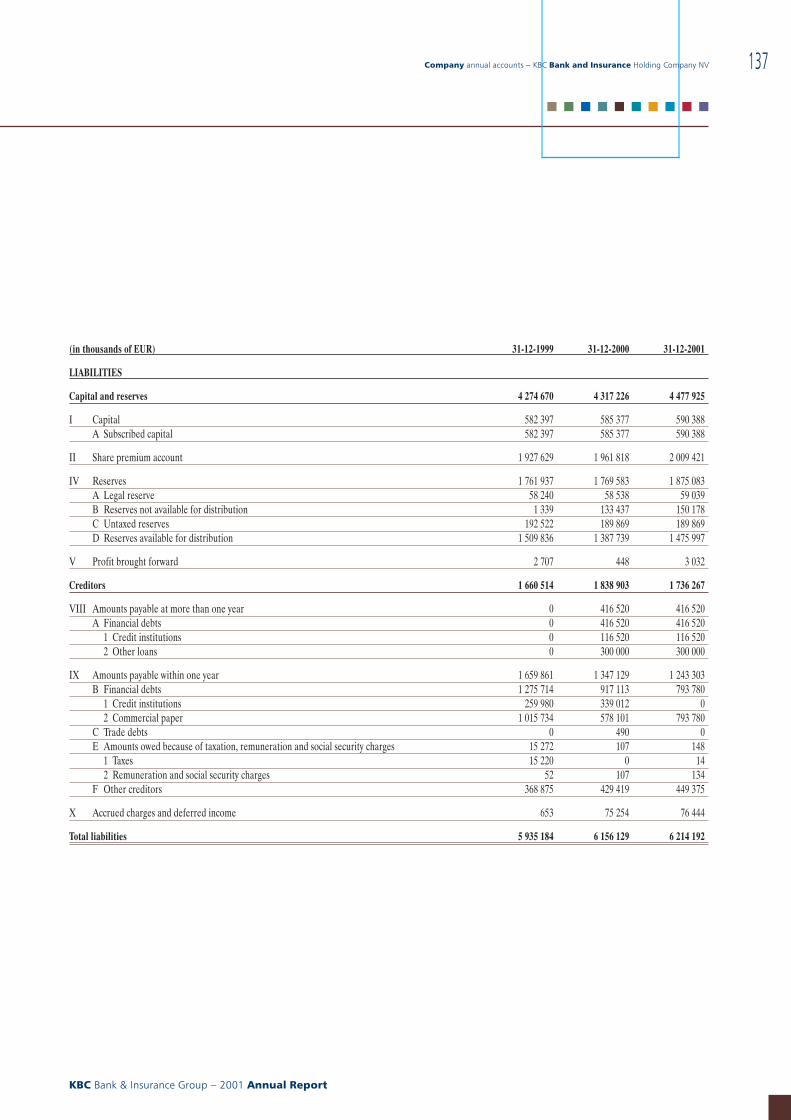

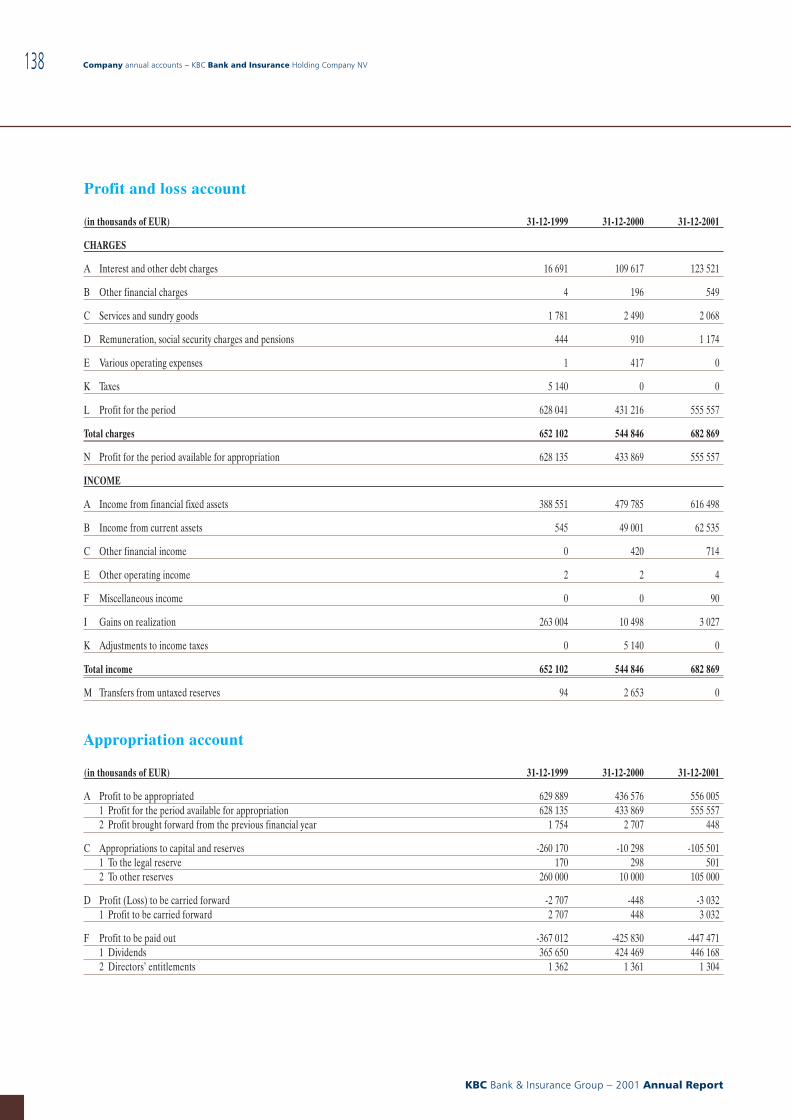

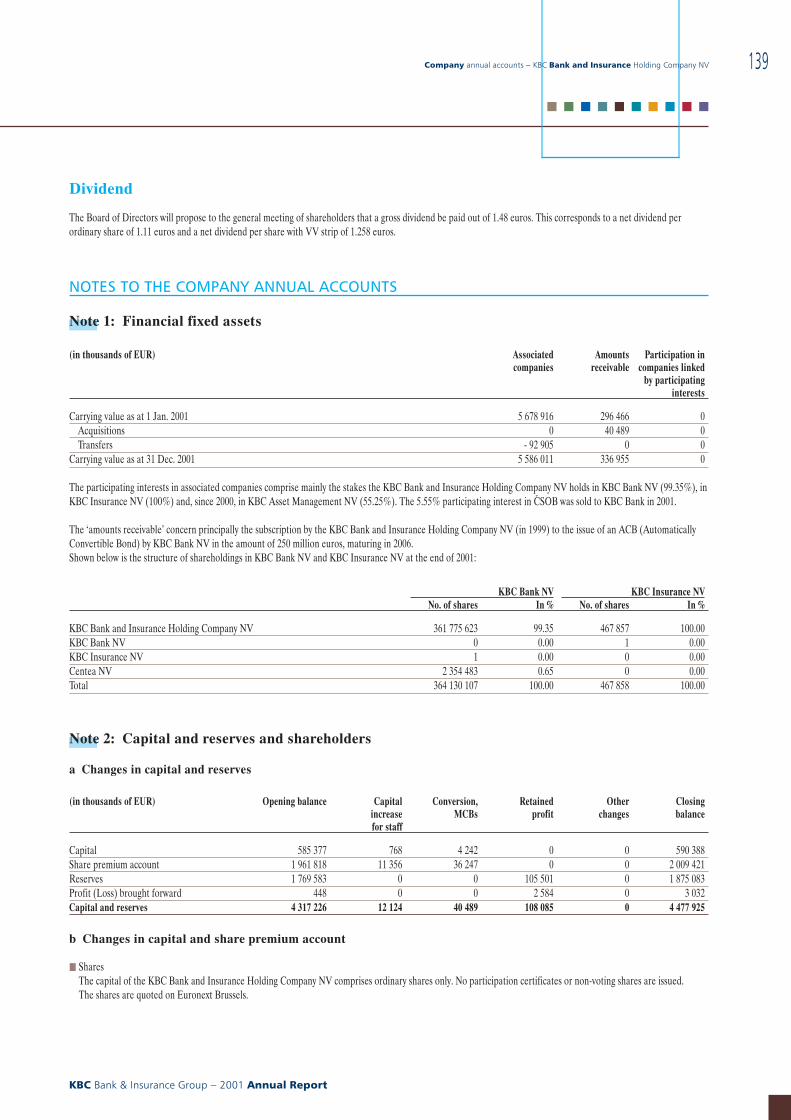

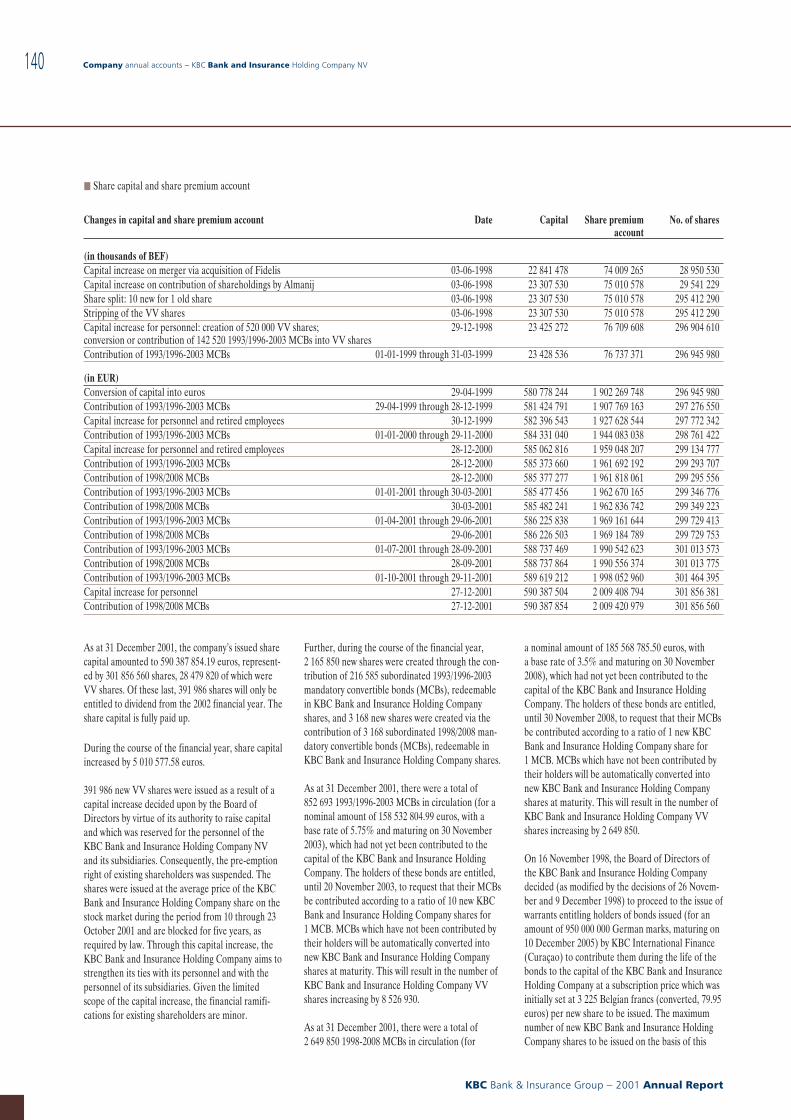

" Company annual accounts − KBC Bank andInsurance Holding Company NV ...................... 136

Balance sheet, profit and loss account and profitappropriation ...................................................... 136Notes to the company annual accounts ............. 139General information ........................................... 142

" Additional information ...................................... 143

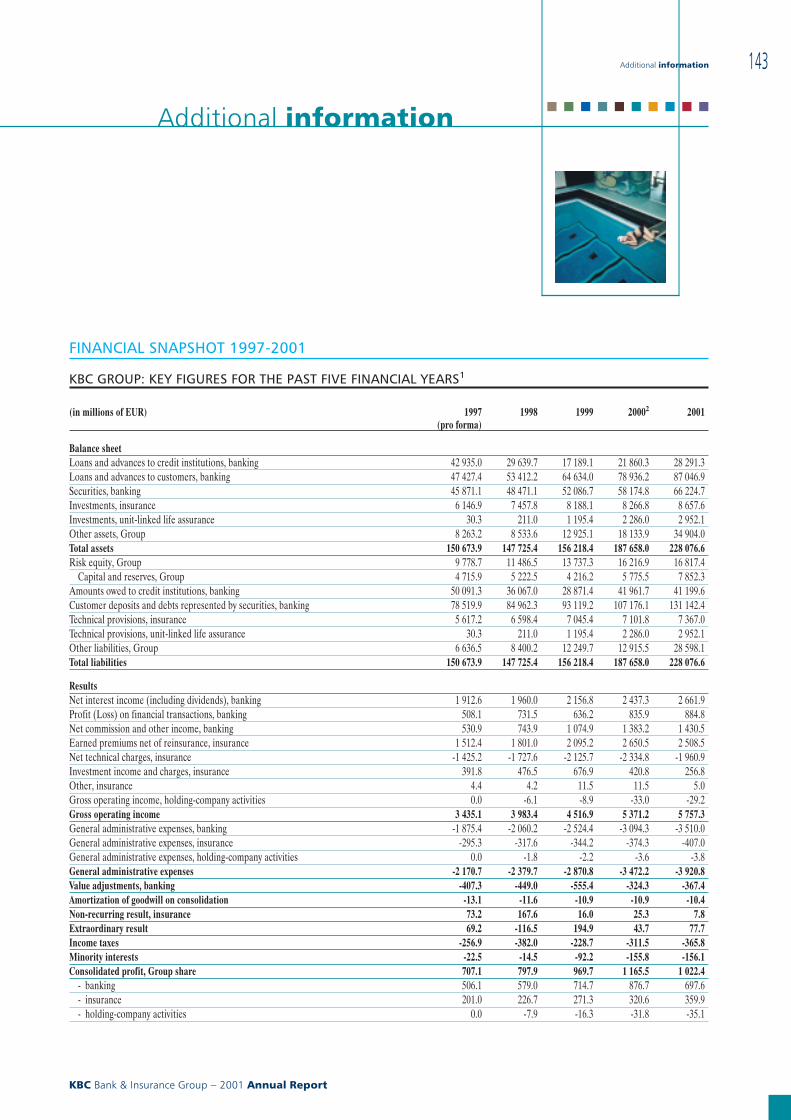

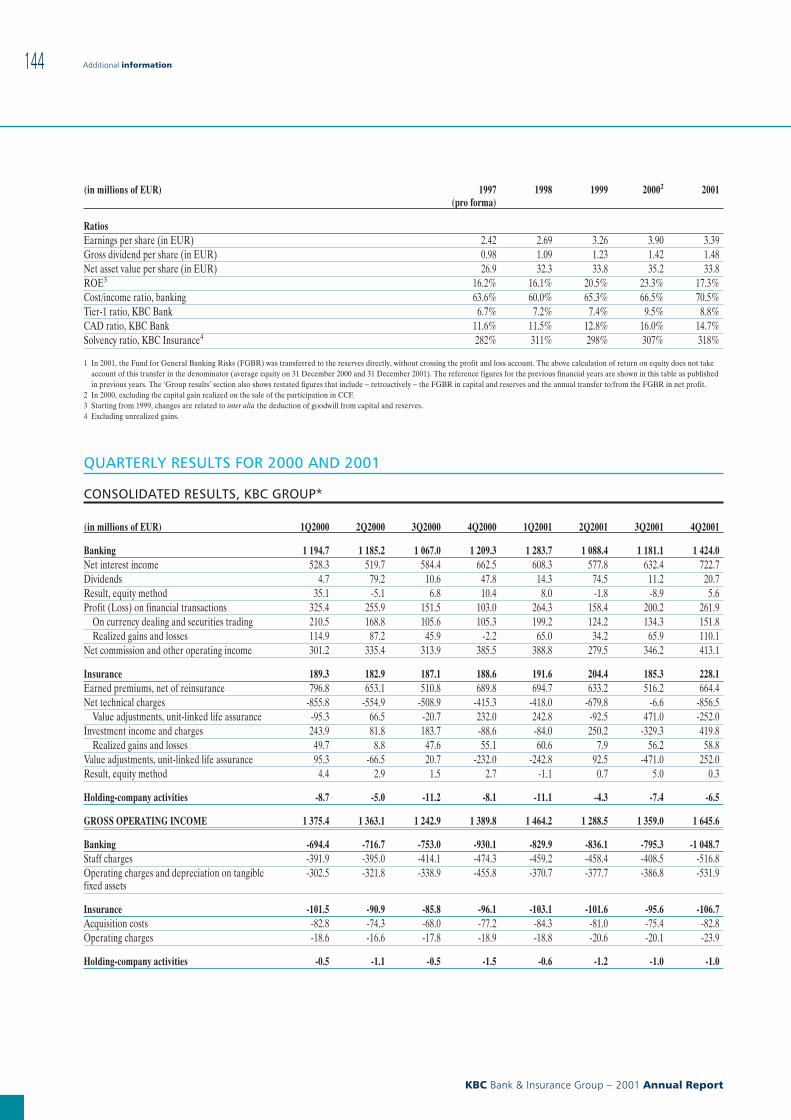

Financial snapshot 1997-2001 ............................ 143Quarterly results for 2000 and 2001 .................. 144Pending litigation ................................................ 145KBC and socially responsible business .............. 146Information for shareholders and the generalpublic ................................................................... 148

Report of the Board of Directors to the annual meeting of shareholders

KBC Bank & Insurance Group − 2001 Annual Report

3

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

Statement by the Chairmanof the Board of Directors and the

President of the Executive Committee

IN MANY RESPECTS, LAST YEAR WAS A DIFFICULT ONE. BESIDES

MINIMAL ECONOMIC GROWTH − WITH SOME COUNTRIES ACTUALLY IN

THE THROES OF RECESSION − AND A CONTINUING UNSTABLE FINANCIAL

CLIMATE CHARACTERIZED BY FALLING INTEREST RATES AND WEAK SHARE

PRICES, A NUMBER OF UNEXPECTED AND INDEED DRAMATIC EVENTS

UNFOLDED. FOREMOST AMONG THEM WERE OF COURSE THE

11 SEPTEMBER ATTACKS ON THE US AND THE FINANCIAL DIFFICULTIES

THAT ONCE-PROMINENT COMPANIES ENCOUNTERED, WHETHER AS A

RESULT OF THESE OR OTHER EVENTS.

All this had an adverse impact onour banking business. The unfavour-able stock market climate de-pressed income from the securitiesbusiness, resulting in our having tobook unrealized losses on ourequity portfolio. The general eco-nomic situation also accounted forhigher write-downs on the loanportfolio in Belgium and the US, aswell as in other countries. Althoughthe increase in costs was able to becontained within reasonablebounds, bank earnings fell by amarked 20.4%.

As to our insurance company, itmade an excellent showing, record-ing earnings growth of 12.2%. Onceagain, this fine performance can beattributed to the quality and astutemanagement of the non-life insur-ance portfolio and to the growth in

the life assurance portfolio, whichstems in part from the progress wehave made in the field of banc-assurance.

After consolidation, the KBCGroup consequently recorded a netprofit of 1 022 million euros,a decline of 12.3% on last year.Changes in the scope of consoli-dation, e.g. the inclusion of PeelHunt after its acquisition at thestart of 2001, the merger of ourK&H Bank with ABN AMROMagyar in Hungary and the fullconsolidation of Kredyt Bank(Poland) in the fourth quarter, hadlittle impact on these results on thewhole.

However, given the low payoutratio in 2000 and particularly givenour confidence in the Group’s

future, the Board of Directors willstill propose to the General Meet-ing of Shareholders that the divi-dend be raised by 4.2% to 1.48euros.

Our confidence in KBC’s continuedexpansion is based in part on theprogress made in the past turbulentyear in growing our businesses.Despite the keen competition thatprevailed, we again succeeded inraising our shares of the bankingmarket in Belgium. All the while,work continued on implementingthe merger, with the number ofKBC Bank and subsidiary CBCBanque branches in Belgium beingreduced even further from 1 454 to1 312. The merged bank’srevamped IT platform also con-tinued to be expanded and, by theend of 2001, it was serving nearly70% of our customers. By the endof this year, we are expecting tohave completed some 80% of allwork relating to the merger. In themeantime, we will continue stead-fastly to develop our specific banc-assurance concept. By the close oflast year, approximately 40% ofKBC Bank customers had pur-chased at least one KBC Insuranceproduct.

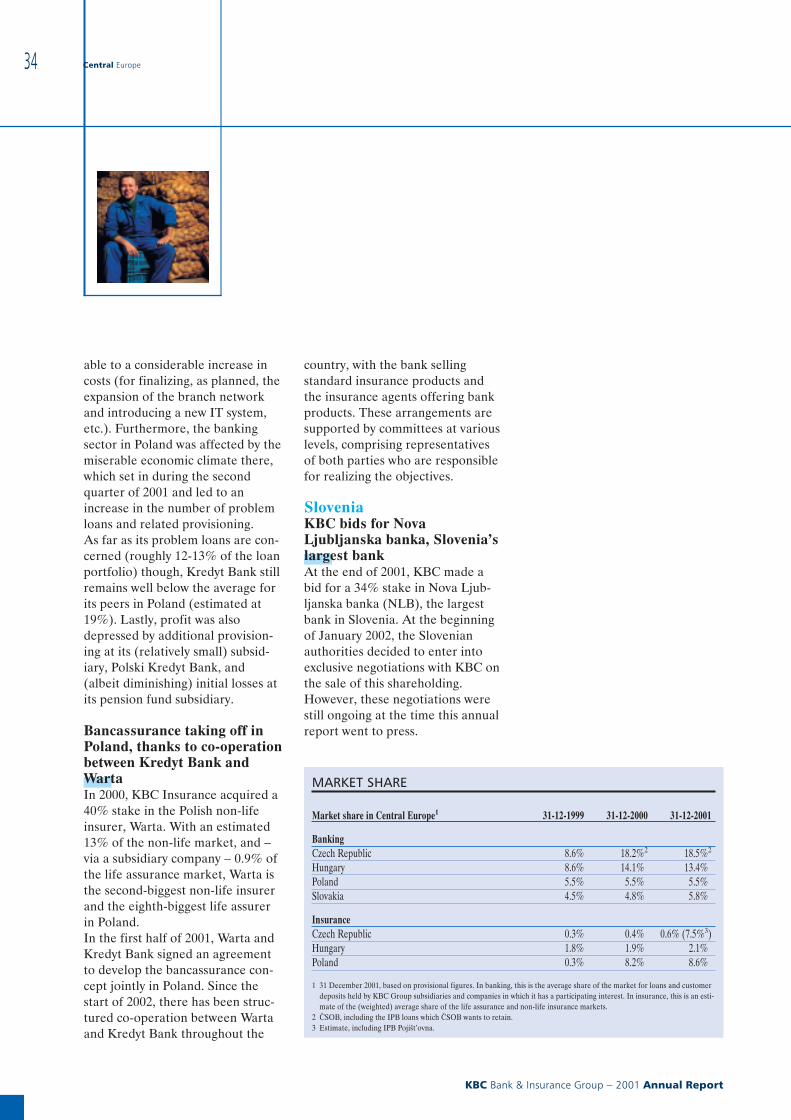

In 2001, we continued to build upour presence in Central Europe,where we are generally regarded asthe premier Western financial insti-tution.Without making any substantialnew investments in the region, wemanaged to significantly strengthenour position in a number of coun-

Statement by the Chairman of the Board of Directors and the President of the Executive Committee

KBC Bank & Insurance Group − 2001 Annual Report

4

REM

IVE

RMEI

REN

tries. In the Czech Republic, ourCzech subsidiary C{SOB became thelargest financial institution afterintegrating IPB, which it hadacquired in mid-2000. In Hungary,our K&H Bank merged with ABNAMRO Magyar to become thesecond largest bank in that country,and is now 59%-owned by KBC.In Poland, we acquired an absolutemajority shareholding in KredytBank, and raised it to 56.6% at thestart of this year following a man-datory public bid. In December2001, we made a bid for a 34%stake in Nova Ljubljanska banka(NLB), the largest bank in Slo-venia. At the beginning of January2002, the Slovenian authoritiesdecided to enter into exclusivenegotiations with KBC on the saleof this shareholding. In those Cen-tral European countries where wehave already established a pres-ence, the bancassurance activitieswill also continue to be developed.Warta, the second largest non-lifeinsurer in Poland (40%-owned byKBC), and Kredyt Bank, forinstance, have entered into a banc-assurance agreement. In Hungary,our non-life insurer Argosz madeits first contribution to profit with afine technical result, while in theCzech Republic, C{SOB Pojist’ovnabecame a wholly-ownedKBC Insurance subsidiary, and thefirst steps were taken in bancassur-ance, mainly through the much big-ger branch network created by theacquisition of IPB.

In 2001, our activities in CentralEurope accounted for 11.5% of

Group profit. Account taken of thestrategic developments describedabove, one of our primary object-ives where Central Europe is con-cerned − namely that it should con-tribute some 15% to total Groupprofit over the next one to twoyears − is within our grasp.

We are well aware of the fact thatimportant challenges lie ahead. Theeconomic environment will remainunstable, with major sectors stillhaving to complete restructuringexercises or cope with earlierexcesses, financial markets subjectto volatility and significant changespossibly occurring in the Europeanbanking and insurance landscape asa result of mergers and alliances.

Given these prospects and based onthe clear insight we have nowgained into the ultimate effects ofthe merger, we have drawn up aplan for reducing the number ofemployees at KBC Bank NV by1 650 full-time equivalents over thenext three years. This will not beaccompanied by outright dismissals,but will be achieved primarily byhaving employees whose job hasbeen made redundant as a result ofthe merger replace those leavingKBC voluntarily or through naturalattrition.This plan has also resulted in thereduction in the ranks of seniormanagement by more than 10%and will lead to the resignation atthe April 2002 General Meeting ofthree of the eight members of theExecutive Committee. During theirlong careers, these individuals

made an enormous contribution toCERA Bank and the Kredietbank,respectively. By their willingness tostep down, they are helping thesebanks to reap the fruits of theirmerger and become an efficient andprosperous institution. We thankthem sincerely for their dedication,their achievements and their loyaltytowards our company.

With a view to enhancing the inte-gration of the bank and the insur-ance company, the ICT, communi-cation and marketing divisions ofthe two have now been combined inorder to improve co-operation andefficiency.

All these measures will serve tosignificantly increase the efficiencyand profitability of KBC Bank.Starting in the year 2004, all elsebeing equal, they should yield costsavings of over 100 million euros ayear, savings which are wholly inline with the merger objectives setin 1998.

As our banking income returns toits traditional pace of growth afterthe slump in 2001, the objective ofachieving a 15% rise in earnings pershare for the 2000-2004 periodremains within reach. Among theforces driving our income growthwill be the continued developmentof our bancassurance concept, ourpresence in Central Europe and thehigh level of profitability of ourasset management activities.

Over the past year, our institutionwas again able to rely fully on its

Statement by the Chairman of the Board of Directors and the President of the Executive Committee

KBC Bank & Insurance Group − 2001 Annual Report

5

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

dedicated employees. In the bank,our people had to deal not onlywith more difficult circumstances inboth the lending and investmentbusinesses, they also had to handleall the work occasioned by themerger, while making the necessarypreparations for the transition toeuro notes and coins. The fact thatthis serious logistical challengewent off without a hitch is duewholly to the dedication of ouremployees, particularly those in thebranch network.Our employees in the insurancebusiness also merit a special wordof thanks for finalizing the mergerof our various insurance activities,while our independent agents aredeserving of our particular grati-tude for their exemplary co-oper-ation with the bank branches, con-sistent with our bancassurance con-cept.

Over the past year, the KBC shareprice fell by some 18%, more orless in line with the trend in the DJEuro Stoxx Banks index. The valueof the KBC share was depressed tosome extent by the reduction of itsweighting in a number of indicesthat are now based mainly on theequity market capitalization of thefree float, rather than on the totalvalue of all shares. Indeed, majorinstitutional investors are attachingever more importance to the freefloat and the liquidity of shares inwhich they invest.

By means of presentations and bycontinually increasing the availabil-ity and transparency of informationon our activities, we are endeavour-ing to inform our shareholders andpotential investors as comprehen-sively as possible. We trust that thisannual report will be a testimony to

our regard for and our gratitude toour shareholders.

Remi VermeirenPresident of theExecutive Committee

Willy BreeschChairman of the Board of Directors

Statement by the Chairman of the Board of Directors and the President of the Executive Committee

KBC Bank & Insurance Group − 2001 Annual Report

6

WIL

LYBR

EESC

H

Executive Committee

THE EXECUTIVE COMMITTEE OF THE KBC BANK AND INSURANCE

HOLDING COMPANY NV CONSISTS OF THE MEMBERS OF THE

EXECUTIVE COMMITTEES OF KBC BANK NV AND KBC INSURANCE NV.

EACH MEMBER OF THE EXECUTIVE COMMITTEE IS RESPONSIBLE FOR

SUPERVISING THE ACTIVITIES OF A NUMBER OF SPECIFIC BUSINESS UNITS.

IN 2001, THE MEMBERS OF THE EXECUTIVE COMMITTEEOF THE KBC BANK AND INSURANCE HOLDINGCOMPANY NV WERE AS FOLLOWS:

Executive Committee

KBC Bank & Insurance Group − 2001 Annual Report

7

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

REMI VERMEIREN(President)

WILLY DURON(Vice-President)

HERMAN AGNEESSENS RUDY BROECKAERT EMILE CELIS

CHRISTIAN DEFRANCQ FRANS FLORQUIN GHUNALD LOYAERTS

LUC PHILIPS CLÉMENT SELLESLAGH JAN VANHEVEL

Messrs. Ghunald Loyaerts, Rudy Broeckaert and Clément Selleslagh,managing directors and members of the Executive Committee ofKBC Bank and the KBC Bank and Insurance Holding Company, will stepdown following the General Meeting of Shareholders in April 2002.

Strategy

■ ■ ■ KBC HAS THE AMBITION TO BE A PROFITABLE MULTI-CHANNEL

BANCASSURER, WITH A GEOGRAPHIC FOCUS ON EUROPE.

IN WESTERN EUROPE, THE GROUP BOASTS A LEADING POSITION IN

BELGIUM AND CURRENTLY HAS A LIMITED PRESENCE IN OTHER

COUNTRIES, AS WELL.

IN CENTRAL EUROPE, IT IS ONE OF THE PREMIER FINANCIAL

SERVICES GROUPS. KBC FOCUSES ON FOUR ACTIVITIES, NAMELY

RETAIL AND PRIVATE BANCASSURANCE, CORPORATE SERVICES,

ASSET MANAGEMENT AND MARKET ACTIVITIES.

THE GROUP’S EXPLICIT AIM IS TO CREATE LASTING VALUE FOR ITS

SHAREHOLDERS THROUGH THE PURSUIT OF ITS BUSINESS

ACTIVITIES. ■ ■ ■

AREA OF OPERATION ANDACTIVITIES

Geographic focusIt is our ambition to be a profitablemulti-channel bancassurer with ageographic focus on Europe.

One of the leading financial groupsin our first home market, Belgium,we are also present in various otherWest European countries throughsubsidiaries, branches and represen-tative offices. We have developeda second home market in CentralEurope, where we have become one

of the premier financial servicesgroups, thanks to a leading positionin the Czech Republic and the sig-nificant presence we have built upin Hungary, Poland and Slovakia.

Through our international networkof representative offices, branchesand subsidiaries, we are currentlypresent in over thirty countriesworldwide.

It is our intention to continue orexpand activities outside Europeonly if they are necessary for theprovision of services to KBC’s core

European customers and/or if theygenerate a higher return on equitythan is generally targeted for theGroup.

Focus on activitiesBancassurance is our core business,and we aim to develop it extensivelyin our two home markets.

In addition, we are also active inthe business of asset management,in various market activities and inthe provision of services to corpor-ations. One of our goals is to grad-ually build up a pan-European plat-form to cater for the needs ofmedium-sized companies in thearea of ‘corporate finance’ (capitalmarket operations, mergers andacquisitions, etc.).

Our focus with regard to activitiesis reflected in their segmentationin 2000 into the following fivebusiness areas: retail and privatebancassurance, Central Europe,corporate services, asset manage-ment and market activities. Eacharea of activity has its own specificmanagement committee, whichplays a preliminary policy-makingand supportive role vis-à-vis theexecutive committees of the bank,the insurer and the holding com-pany. For each of these businessareas, profitability targets havebeen set and equity allocated.

Focus on clienteleWe define our core clientele as pri-vate persons and small andmedium-sized enterprises, to whomwe intend to offer the broadest pos-sible range of financial productsand services via a multi-channelapproach. The product offering tocorporate and institutional cus-tomers has been tailored to meettheir particular needs and is basedon the specific know-how and geo-graphic presence of our Group.

Strategy

KBC Bank & Insurance Group − 2001 Annual Report

8

FINANCIAL TARGETS FOR2000-2004

Along with its strategy, the Group’sfinancial targets were alsoredefined in 2000.

With a view to improving the qual-ity of own funds and in anticipationof the entry into effect of the rele-vant International AccountingStandards (IAS), it was decided in2001 to transfer the Fund for Gen-eral Banking Risks to reserves.1

Given the technical impact of thison the denominator in the ‘returnon equity’ ratio, the target for thisratio was reduced accordingly, from22% to 20%.

The Group also makes use of the‘operational return on equity’ ratioto reflect the profitability of its fiveareas of activity, excluding the‘Group item’ (see the section on‘Group results’ below). The differ-ence between the two profitabilityratios is accounted for primarily byprofit/loss components which arenot allocable to one of the fiveareas of activity (such as capitalgains on shares), by goodwillcharged against capital and reserves(which is dealt with entirely via the‘Group item’) and by leveraging bythe holding company (funding aportion of its subsidiaries’ equitycapital through borrowings).

Consequently, the Group’s financialtargets for 2000-2004 are as shownin the table below.

There are also specific targets forreturn on (allocated) equity foreach area of activity. These will begiven in the specific comments onthe various areas of activity.

MEASURES TAKEN TO MEETTHE MERGER OBJECTIVES

In October 2001, we took a numberof structural measures to ensurethat the merger objectives we hadset ourselves would be met. Theprogress we have made on themerger front by creating a commonIT platform and gradually restruc-turing the branch network to createfewer but larger branches, forinstance, has allowed us to estimateaccurately how the merger willaffect our staffing levels and organ-ization.

Consequently, it was decided tocombine a number of directoratesand shorten various hierarchicallines of authority at head officeand, in the branch network, to sim-plify the provincial and regionalstructures.

These plans, along with the com-pletion of the merger processes bythe end of 2004, will be reflected in:j a reduction in the number of

members on the ExecutiveCommittee of KBC Bank andthe KBC Bank and InsuranceHolding Company by three, toa total of five and eight mem-bers, respectively, following theGeneral Meeting of Sharehold-ers in April 2002;

j an approximately 15% reductionin the ranks of KBC Bank NVsenior management over the nexttwo years;

j the downsizing of the total KBCBank NV workforce by some1 650 employees (full-timeequivalents) by the end of 2004;i.e. 1 100 at head office and 550in the branch network. This willbe achieved through a combin-ation of retirement schemes,approved social plans, ‘timecredit’ arrangements and volun-tary redundancies. As made clearat the start of the merger, therewill be no outright dismissals.

At the various subsidiaries, too,similar exercises are under way tocut costs and/or increase efficiency.

1 Since transferring the entire balance fromthe FGBR via the profit and loss accountwould seriously distort the true picture ofthe trend in Group results, a single transferwas made directly to the reserves.

TARGET

ROE At least 20% at Group level*operational, 17%

Growth in net earnings per share 15% average per annumCost/income ratio Bank: < 55% in 2004

Insurer: combined ratio < 103% in 2004Solvency Bank: tier-1 ratio > 7% and CAD ratio > 11%

Insurer: solvency ratio > 200%

* Account taken of the derogation authorized by the Belgian Banking and Finance Commission regarding the immediatededuction from capital and reserves of goodwill paid on recent acquisitions.

Strategy

KBC Bank & Insurance Group − 2001 Annual Report

9

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

Shareholder information

SHAREHOLDERS

31-12-2001 % No. ofshares

Almanij and Group companies:- Almanij 67.91% 204 984 572- KBC Bank & Insurance Group companies* 3.68% 11 118 319Total 71.59% 216 102 891Free float 28.41% 85 753 669

Total shares issued 100.00% 301 856 560

Mandatory convertible bonds (MCBs),number of shares on conversion

11 176 780

of which: held by Almanij andKBC Bank & Insurance Group companies

1 842 040

* With the exception of shares held by KBC Securities and the KBC Financial Products Group (trading purposes).

ANNUAL RETURN

(price gains and dividends) KBC BEL 20 DJ EuroStoxx Banks

2000-2001 (1 year) -15.2% -4.2% -17.1%1998-2001 (3 years) -15.0% -4.6% 2.3%1996-2001 (5 years) 11.3% 10.8% 17.8%1994-2001 (7 years) 15.3% 13.0% 16.7%

RATINGS*

31-12-2001 Fitch Moody’s Standard & Poor’s

KBC BankLong-term rating AA- Aa3 A+Short-term rating F1+ P1 A-1

KBC InsuranceLong-term rating AA - A+Short-term rating F1+ - -

KBC Holding CompanyLong-term rating A+ - AShort-term rating F1 - A-1

* KBC Bank’s long-term rating has been put on negative outlook by Moody’s. The long-term ratings of KBC Bank, KBC Insurance and theKBC holding company have been placed on negative outlook by S&P’s. The long-term rating accorded KBC Insurance by Fitch has to dowith its ‘claims-paying ability’.

PERFORMANCE OF THE KBC SHARE*

(31-12-1994 = 100 )

0

100

200

300

400

500

600

12-2

001

12-2

000

12-1

999

12-1

998

12-1

997

12-1

996

12-1

995

12-1

994

* Through 31-12-1997: former Kredietbank; the 10-for-1 share split was carried out retroactively.

KBC

DJ Euro Stoxx Banks

NET EARNINGS PER SHARE* AND GROSS DIVIDEND

(in EUR)

* For 2000, excluding the capital gain realized on the sale of participation in CCF.

Net earnings per share

Gross dividend

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

20012000199919981997

2.4

0.98 1.09 1.231.42 1.48

2.7

3.3

3.9

3.4

Shareholder information

KBC Bank & Insurance Group − 2001 Annual Report

10

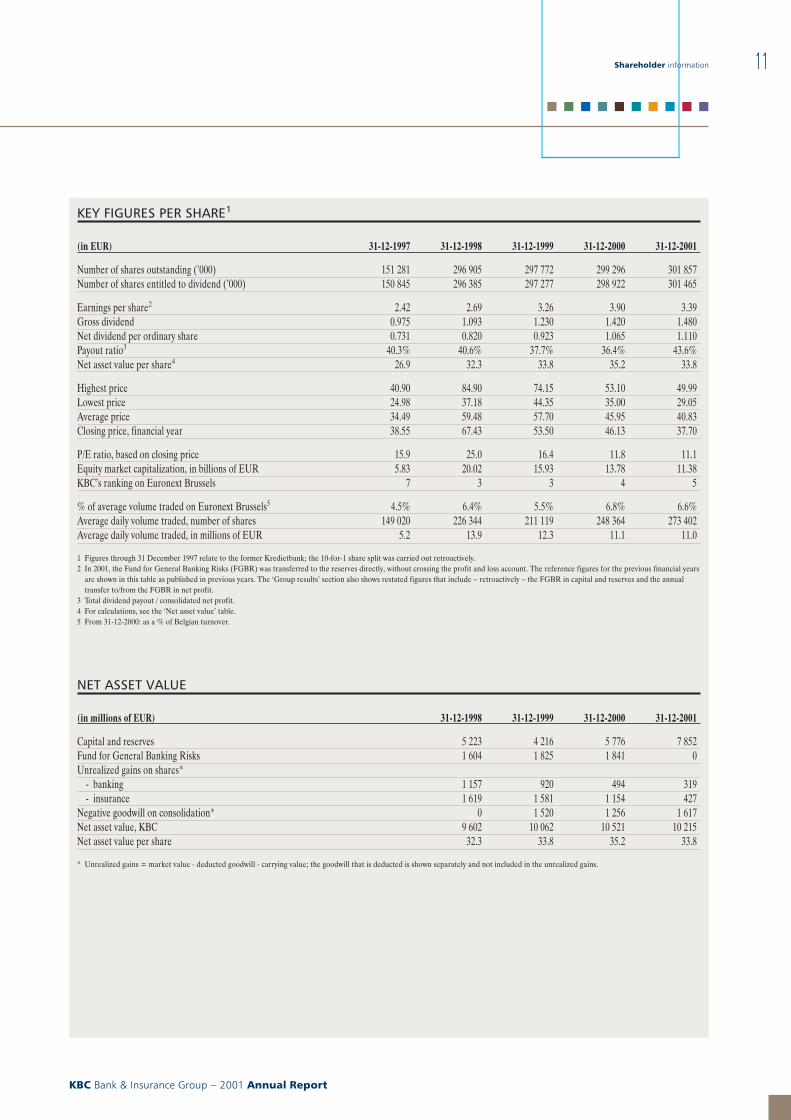

KEY FIGURES PER SHARE1

(in EUR) 31-12-1997 31-12-1998 31-12-1999 31-12-2000 31-12-2001

Number of shares outstanding (’000) 151 281 296 905 297 772 299 296 301 857Number of shares entitled to dividend (’000) 150 845 296 385 297 277 298 922 301 465

Earnings per share2 2.42 2.69 3.26 3.90 3.39Gross dividend 0.975 1.093 1.230 1.420 1.480Net dividend per ordinary share 0.731 0.820 0.923 1.065 1.110Payout ratio3 40.3% 40.6% 37.7% 36.4% 43.6%Net asset value per share4 26.9 32.3 33.8 35.2 33.8

Highest price 40.90 84.90 74.15 53.10 49.99Lowest price 24.98 37.18 44.35 35.00 29.05Average price 34.49 59.48 57.70 45.95 40.83Closing price, financial year 38.55 67.43 53.50 46.13 37.70

P/E ratio, based on closing price 15.9 25.0 16.4 11.8 11.1Equity market capitalization, in billions of EUR 5.83 20.02 15.93 13.78 11.38KBC’s ranking on Euronext Brussels 7 3 3 4 5

% of average volume traded on Euronext Brussels5 4.5% 6.4% 5.5% 6.8% 6.6%Average daily volume traded, number of shares 149 020 226 344 211 119 248 364 273 402Average daily volume traded, in millions of EUR 5.2 13.9 12.3 11.1 11.0

1 Figures through 31 December 1997 relate to the former Kredietbank; the 10-for-1 share split was carried out retroactively.2 In 2001, the Fund for General Banking Risks (FGBR) was transferred to the reserves directly, without crossing the profit and loss account. The reference figures for the previous financial years

are shown in this table as published in previous years. The ‘Group results’ section also shows restated figures that include − retroactively − the FGBR in capital and reserves and the annualtransfer to/from the FGBR in net profit.

3 Total dividend payout / consolidated net profit.4 For calculations, see the ‘Net asset value’ table.5 From 31-12-2000: as a % of Belgian turnover.

NET ASSET VALUE

(in millions of EUR) 31-12-1998 31-12-1999 31-12-2000 31-12-2001

Capital and reserves 5 223 4 216 5 776 7 852Fund for General Banking Risks 1 604 1 825 1 841 0Unrealized gains on shares*

- banking 1 157 920 494 319- insurance 1 619 1 581 1 154 427

Negative goodwill on consolidation* 0 1 520 1 256 1 617Net asset value, KBC 9 602 10 062 10 521 10 215Net asset value per share 32.3 33.8 35.2 33.8

* Unrealized gains = market value - deducted goodwill - carrying value; the goodwill that is deducted is shown separately and not included in the unrealized gains.

Shareholder information

KBC Bank & Insurance Group − 2001 Annual Report

11

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

Group results

TRANSFER OF THE FUNDFOR GENERAL BANKINGRISKS TO THE RESERVES

At the end of 2001, KBC trans-ferred the Fund for General Bank-ing Risks (FGBR) to reserves inanticipation of the introduction ofIAS 30, when the FGBR will nolonger be considered a provision,but part of own funds. The BelgianBanking and Finance Commission(BFC) has allowed KBC a deroga-tion to carry out this non-recurringtransfer directly without having to

go via the profit and loss account;this with a view to assuring a trueand fair picture is given of the trendin results. Shown below is a retro-active restatement of the relevantkey figures, with the FGBR beingadded to capital and reserves andthe annual transfer to/from theFGBR being included in net profitfor each reference year. Unlessotherwise specified, however, thereference figures for previous finan-cial years elsewhere in this annualreport will be given as published inthe relevant annual reports.

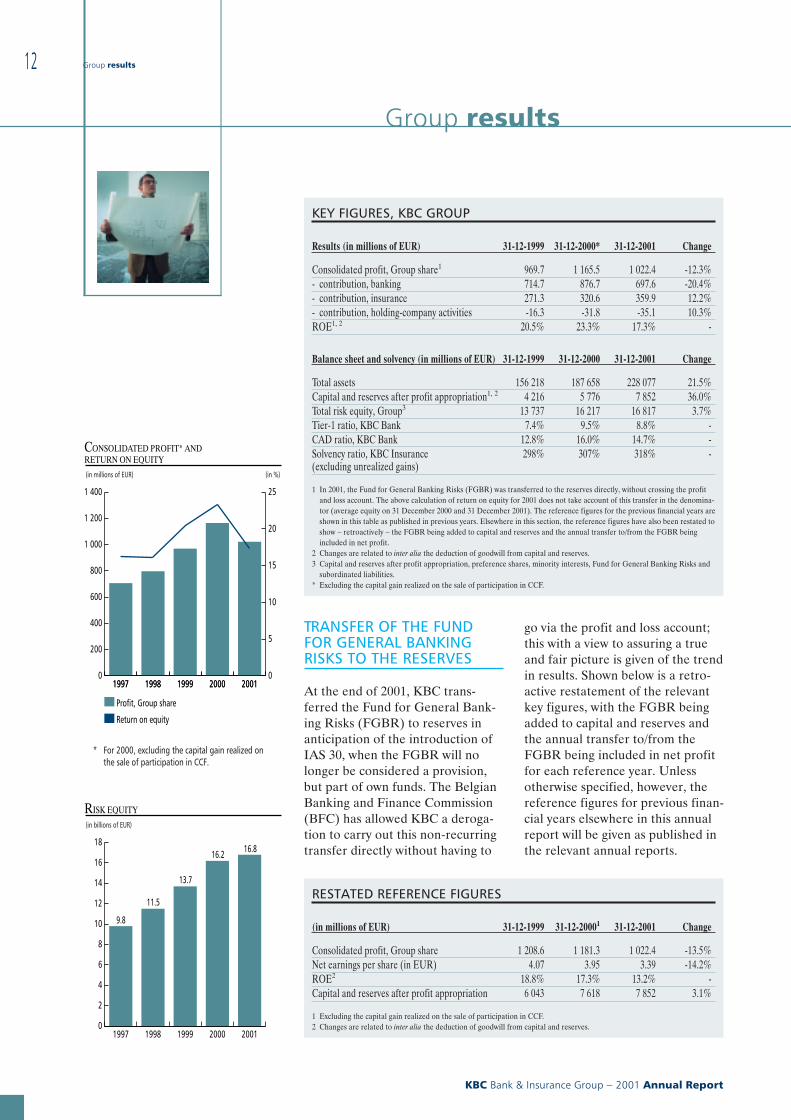

KEY FIGURES, KBC GROUP

Results (in millions of EUR) 31-12-1999 31-12-2000* 31-12-2001 Change

Consolidated profit, Group share1 969.7 1 165.5 1 022.4 -12.3%- contribution, banking 714.7 876.7 697.6 -20.4%- contribution, insurance 271.3 320.6 359.9 12.2%- contribution, holding-company activities -16.3 -31.8 -35.1 10.3%ROE1, 2 20.5% 23.3% 17.3% -

Balance sheet and solvency (in millions of EUR) 31-12-1999 31-12-2000 31-12-2001 Change

Total assets 156 218 187 658 228 077 21.5%Capital and reserves after profit appropriation1, 2 4 216 5 776 7 852 36.0%Total risk equity, Group3 13 737 16 217 16 817 3.7%Tier-1 ratio, KBC Bank 7.4% 9.5% 8.8% -CAD ratio, KBC Bank 12.8% 16.0% 14.7% -Solvency ratio, KBC Insurance(excluding unrealized gains)

298% 307% 318% -

1 In 2001, the Fund for General Banking Risks (FGBR) was transferred to the reserves directly, without crossing the profitand loss account. The above calculation of return on equity for 2001 does not take account of this transfer in the denomina-tor (average equity on 31 December 2000 and 31 December 2001). The reference figures for the previous financial years areshown in this table as published in previous years. Elsewhere in this section, the reference figures have also been restated toshow − retroactively − the FGBR being added to capital and reserves and the annual transfer to/from the FGBR beingincluded in net profit.

2 Changes are related to inter alia the deduction of goodwill from capital and reserves.3 Capital and reserves after profit appropriation, preference shares, minority interests, Fund for General Banking Risks and

subordinated liabilities.* Excluding the capital gain realized on the sale of participation in CCF.

RESTATED REFERENCE FIGURES

(in millions of EUR) 31-12-1999 31-12-20001 31-12-2001 Change

Consolidated profit, Group share 1 208.6 1 181.3 1 022.4 -13.5%Net earnings per share (in EUR) 4.07 3.95 3.39 -14.2%ROE2 18.8% 17.3% 13.2% -Capital and reserves after profit appropriation 6 043 7 618 7 852 3.1%

1 Excluding the capital gain realized on the sale of participation in CCF.2 Changes are related to inter alia the deduction of goodwill from capital and reserves.

0

200

400

600

800

1 000

1 200

1 400

200120001999199819970

5

10

15

20

25

20012000199919981997

CONSOLIDATED PROFIT* AND RETURN ON EQUITY

(in millions of EUR) (in %)

* For 2000, excluding the capital gain realized on the sale of participation in CCF.

Profit, Group share

Return on equity

0

2

4

6

8

10

12

14

16

18

20012000199919981997

RISK EQUITY

(in billions of EUR)

16.816.2

13.7

11.5

9.8

Group results

KBC Bank & Insurance Group − 2001 Annual Report

12

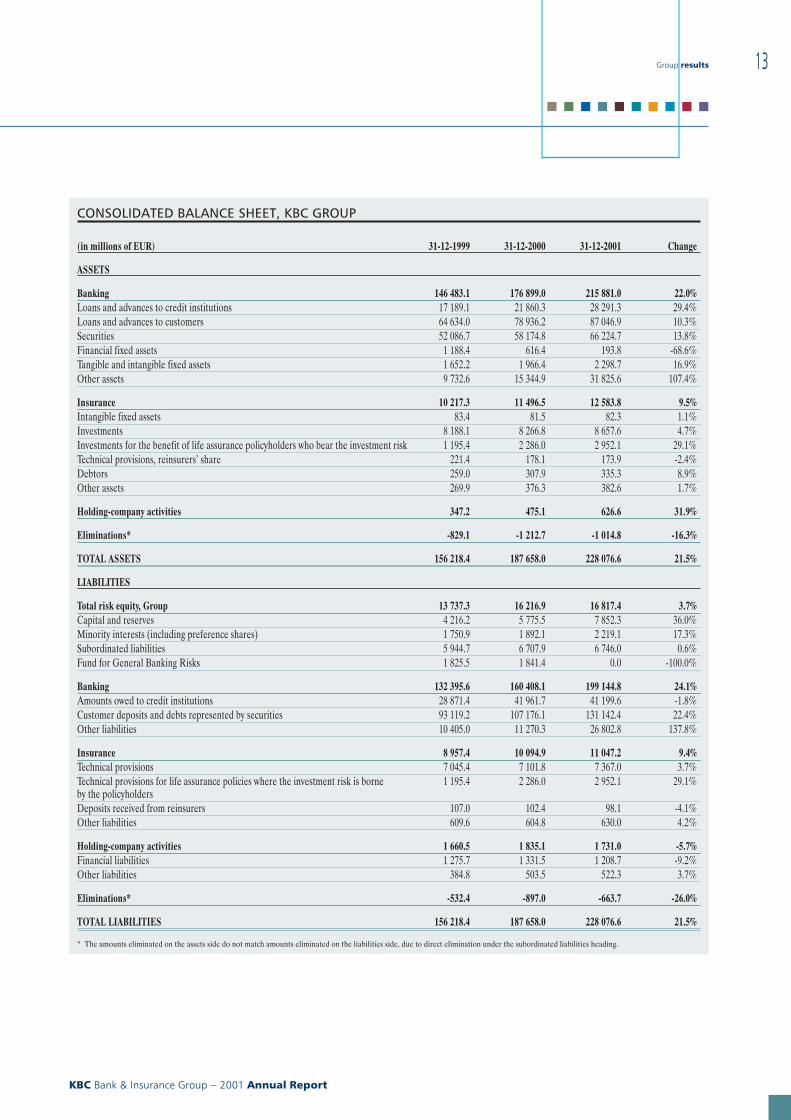

CONSOLIDATED BALANCE SHEET, KBC GROUP

(in millions of EUR) 31-12-1999 31-12-2000 31-12-2001 Change

ASSETS

Banking 146 483.1 176 899.0 215 881.0 22.0%Loans and advances to credit institutions 17 189.1 21 860.3 28 291.3 29.4%Loans and advances to customers 64 634.0 78 936.2 87 046.9 10.3%Securities 52 086.7 58 174.8 66 224.7 13.8%Financial fixed assets 1 188.4 616.4 193.8 -68.6%Tangible and intangible fixed assets 1 652.2 1 966.4 2 298.7 16.9%Other assets 9 732.6 15 344.9 31 825.6 107.4%

Insurance 10 217.3 11 496.5 12 583.8 9.5%Intangible fixed assets 83.4 81.5 82.3 1.1%Investments 8 188.1 8 266.8 8 657.6 4.7%Investments for the benefit of life assurance policyholders who bear the investment risk 1 195.4 2 286.0 2 952.1 29.1%Technical provisions, reinsurers’ share 221.4 178.1 173.9 -2.4%Debtors 259.0 307.9 335.3 8.9%Other assets 269.9 376.3 382.6 1.7%

Holding-company activities 347.2 475.1 626.6 31.9%

Eliminations* -829.1 -1 212.7 -1 014.8 -16.3%

TOTAL ASSETS 156 218.4 187 658.0 228 076.6 21.5%

LIABILITIES

Total risk equity, Group 13 737.3 16 216.9 16 817.4 3.7%Capital and reserves 4 216.2 5 775.5 7 852.3 36.0%Minority interests (including preference shares) 1 750.9 1 892.1 2 219.1 17.3%Subordinated liabilities 5 944.7 6 707.9 6 746.0 0.6%Fund for General Banking Risks 1 825.5 1 841.4 0.0 -100.0%

Banking 132 395.6 160 408.1 199 144.8 24.1%Amounts owed to credit institutions 28 871.4 41 961.7 41 199.6 -1.8%Customer deposits and debts represented by securities 93 119.2 107 176.1 131 142.4 22.4%Other liabilities 10 405.0 11 270.3 26 802.8 137.8%

Insurance 8 957.4 10 094.9 11 047.2 9.4%Technical provisions 7 045.4 7 101.8 7 367.0 3.7%Technical provisions for life assurance policies where the investment risk is borneby the policyholders

1 195.4 2 286.0 2 952.1 29.1%

Deposits received from reinsurers 107.0 102.4 98.1 -4.1%Other liabilities 609.6 604.8 630.0 4.2%

Holding-company activities 1 660.5 1 835.1 1 731.0 -5.7%Financial liabilities 1 275.7 1 331.5 1 208.7 -9.2%Other liabilities 384.8 503.5 522.3 3.7%

Eliminations* -532.4 -897.0 -663.7 -26.0%

TOTAL LIABILITIES 156 218.4 187 658.0 228 076.6 21.5%

* The amounts eliminated on the assets side do not match amounts eliminated on the liabilities side, due to direct elimination under the subordinated liabilities heading.

Group results

KBC Bank & Insurance Group − 2001 Annual Report

13

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

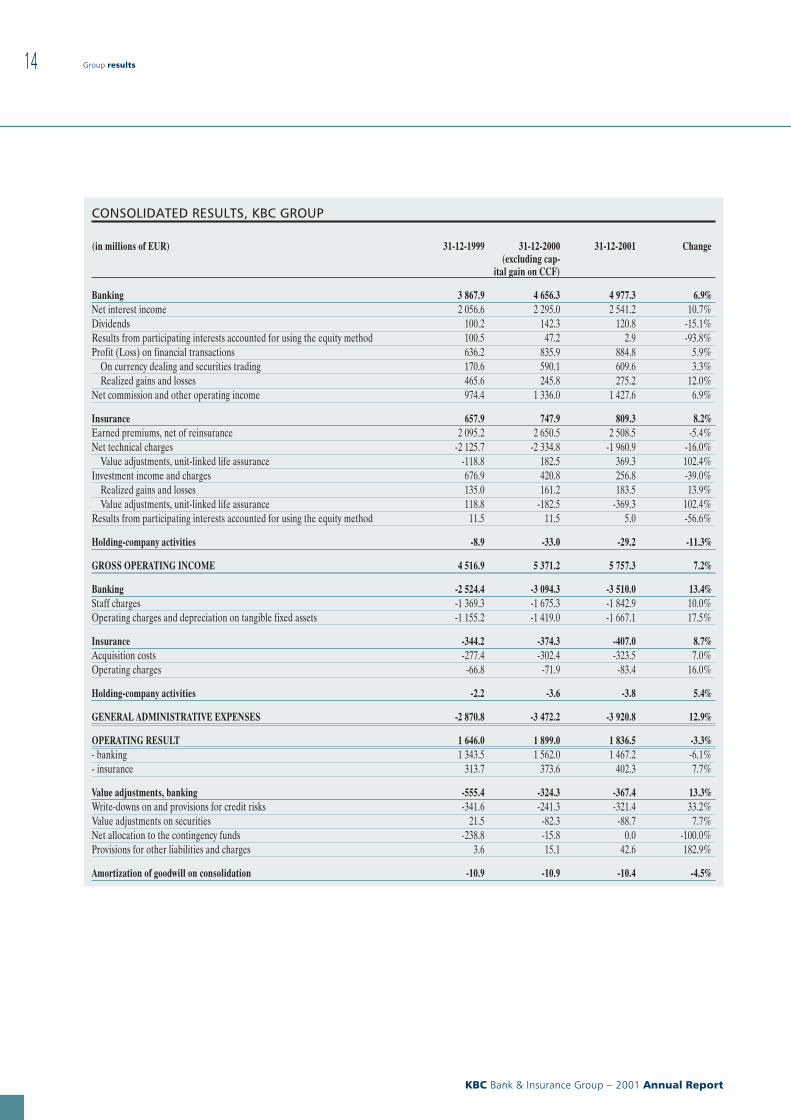

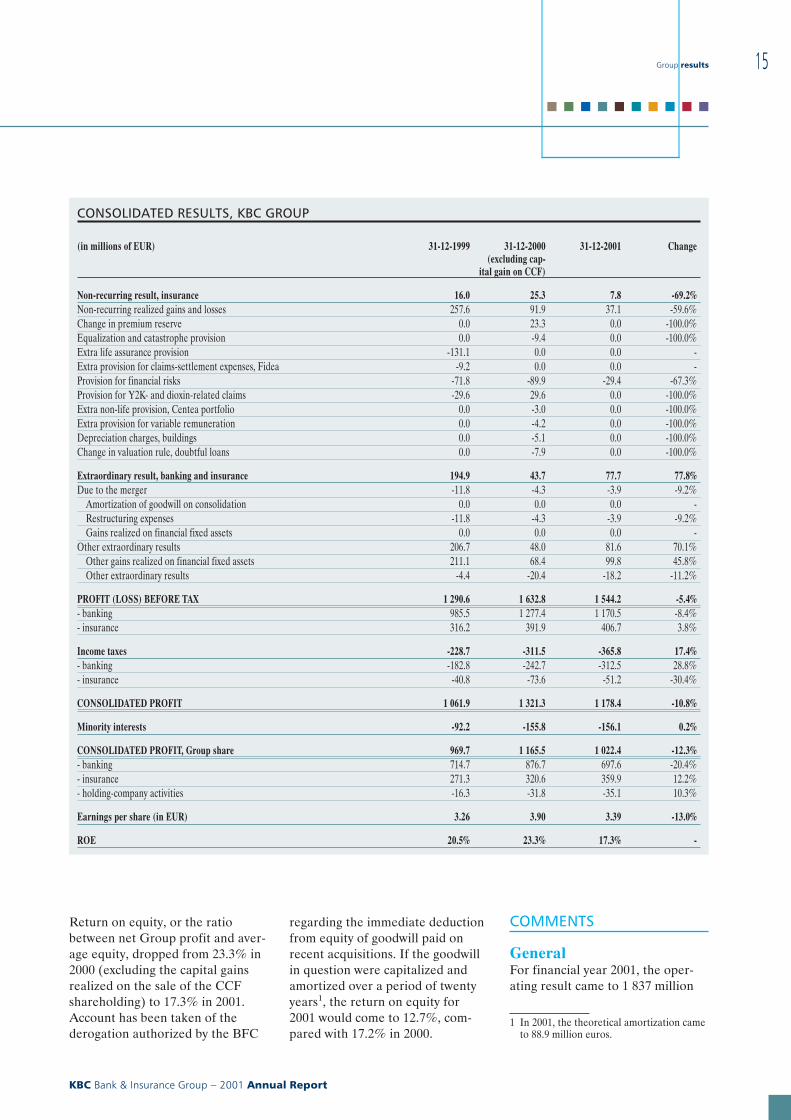

CONSOLIDATED RESULTS, KBC GROUP

(in millions of EUR) 31-12-1999 31-12-2000(excluding cap-

ital gain on CCF)

31-12-2001 Change

Banking 3 867.9 4 656.3 4 977.3 6.9%Net interest income 2 056.6 2 295.0 2 541.2 10.7%Dividends 100.2 142.3 120.8 -15.1%Results from participating interests accounted for using the equity method 100.5 47.2 2.9 -93.8%Profit (Loss) on financial transactions 636.2 835.9 884.8 5.9%

On currency dealing and securities trading 170.6 590.1 609.6 3.3%Realized gains and losses 465.6 245.8 275.2 12.0%

Net commission and other operating income 974.4 1 336.0 1 427.6 6.9%

Insurance 657.9 747.9 809.3 8.2%Earned premiums, net of reinsurance 2 095.2 2 650.5 2 508.5 -5.4%Net technical charges -2 125.7 -2 334.8 -1 960.9 -16.0%

Value adjustments, unit-linked life assurance -118.8 182.5 369.3 102.4%Investment income and charges 676.9 420.8 256.8 -39.0%

Realized gains and losses 135.0 161.2 183.5 13.9%Value adjustments, unit-linked life assurance 118.8 -182.5 -369.3 102.4%

Results from participating interests accounted for using the equity method 11.5 11.5 5.0 -56.6%

Holding-company activities -8.9 -33.0 -29.2 -11.3%

GROSS OPERATING INCOME 4 516.9 5 371.2 5 757.3 7.2%

Banking -2 524.4 -3 094.3 -3 510.0 13.4%Staff charges -1 369.3 -1 675.3 -1 842.9 10.0%Operating charges and depreciation on tangible fixed assets -1 155.2 -1 419.0 -1 667.1 17.5%

Insurance -344.2 -374.3 -407.0 8.7%Acquisition costs -277.4 -302.4 -323.5 7.0%Operating charges -66.8 -71.9 -83.4 16.0%

Holding-company activities -2.2 -3.6 -3.8 5.4%

GENERAL ADMINISTRATIVE EXPENSES -2 870.8 -3 472.2 -3 920.8 12.9%

OPERATING RESULT 1 646.0 1 899.0 1 836.5 -3.3%- banking 1 343.5 1 562.0 1 467.2 -6.1%- insurance 313.7 373.6 402.3 7.7%

Value adjustments, banking -555.4 -324.3 -367.4 13.3%Write-downs on and provisions for credit risks -341.6 -241.3 -321.4 33.2%Value adjustments on securities 21.5 -82.3 -88.7 7.7%Net allocation to the contingency funds -238.8 -15.8 0.0 -100.0%Provisions for other liabilities and charges 3.6 15.1 42.6 182.9%

Amortization of goodwill on consolidation -10.9 -10.9 -10.4 -4.5%

Group results

KBC Bank & Insurance Group − 2001 Annual Report

14

CONSOLIDATED RESULTS, KBC GROUP

(in millions of EUR) 31-12-1999 31-12-2000(excluding cap-

ital gain on CCF)

31-12-2001 Change

Non-recurring result, insurance 16.0 25.3 7.8 -69.2%Non-recurring realized gains and losses 257.6 91.9 37.1 -59.6%Change in premium reserve 0.0 23.3 0.0 -100.0%Equalization and catastrophe provision 0.0 -9.4 0.0 -100.0%Extra life assurance provision -131.1 0.0 0.0 -Extra provision for claims-settlement expenses, Fidea -9.2 0.0 0.0 -Provision for financial risks -71.8 -89.9 -29.4 -67.3%Provision for Y2K- and dioxin-related claims -29.6 29.6 0.0 -100.0%Extra non-life provision, Centea portfolio 0.0 -3.0 0.0 -100.0%Extra provision for variable remuneration 0.0 -4.2 0.0 -100.0%Depreciation charges, buildings 0.0 -5.1 0.0 -100.0%Change in valuation rule, doubtful loans 0.0 -7.9 0.0 -100.0%

Extraordinary result, banking and insurance 194.9 43.7 77.7 77.8%Due to the merger -11.8 -4.3 -3.9 -9.2%

Amortization of goodwill on consolidation 0.0 0.0 0.0 -Restructuring expenses -11.8 -4.3 -3.9 -9.2%Gains realized on financial fixed assets 0.0 0.0 0.0 -

Other extraordinary results 206.7 48.0 81.6 70.1%Other gains realized on financial fixed assets 211.1 68.4 99.8 45.8%Other extraordinary results -4.4 -20.4 -18.2 -11.2%

PROFIT (LOSS) BEFORE TAX 1 290.6 1 632.8 1 544.2 -5.4%- banking 985.5 1 277.4 1 170.5 -8.4%- insurance 316.2 391.9 406.7 3.8%

Income taxes -228.7 -311.5 -365.8 17.4%- banking -182.8 -242.7 -312.5 28.8%- insurance -40.8 -73.6 -51.2 -30.4%

CONSOLIDATED PROFIT 1 061.9 1 321.3 1 178.4 -10.8%

Minority interests -92.2 -155.8 -156.1 0.2%

CONSOLIDATED PROFIT, Group share 969.7 1 165.5 1 022.4 -12.3%- banking 714.7 876.7 697.6 -20.4%- insurance 271.3 320.6 359.9 12.2%- holding-company activities -16.3 -31.8 -35.1 10.3%

Earnings per share (in EUR) 3.26 3.90 3.39 -13.0%

ROE 20.5% 23.3% 17.3% -

Return on equity, or the ratiobetween net Group profit and aver-age equity, dropped from 23.3% in2000 (excluding the capital gainsrealized on the sale of the CCFshareholding) to 17.3% in 2001.Account has been taken of thederogation authorized by the BFC

regarding the immediate deductionfrom equity of goodwill paid onrecent acquisitions. If the goodwillin question were capitalized andamortized over a period of twentyyears1, the return on equity for2001 would come to 12.7%, com-pared with 17.2% in 2000.

COMMENTS

GeneralFor financial year 2001, the oper-ating result came to 1 837 million

1 In 2001, the theoretical amortization cameto 88.9 million euros.

Group results

KBC Bank & Insurance Group − 2001 Annual Report

15

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

euros, 3.3% down on the 2000figure, while net group profit endedat 1 022 million euros, a 12.3%decline on a year earlier. Earningsper share fell 13%.KBC’s performance in 2001 wasquite creditable, having beenachieved during a worldwide eco-nomic slowdown and despite thecontinuing weakness on equitymarkets. The stock market malaisehad an adverse impact especially inthe first nine months of 2001 on theresults of the equity-linked busi-nesses and the subsidiaries special-ized in equity trading and deriva-tives and led to, among otherthings, considerable unrealizedvaluation losses on shares in theinvestment portfolio. As to the eco-nomic slowdown, this made itselffelt particularly in the latter part ofthe year and resulted in consider-able write-downs being made onloans. These less favourable con-ditions, together with the increasein charges, had a negative impactparticularly on bank earnings, withpre-tax profit falling by 8.4%.Higher taxes ultimately pushed netprofit 20.4% lower.The insurance business, on theother hand, turned in a very strongperformance, with profit up 12.2%and another high technical returnbeing posted in the non-life busi-ness. Although sales of unit-linkedlife assurance products were lessbuoyant than in 2000, which hadbeen an exceptional year, they ral-lied again starting in the fourthquarter of 2001. On top of this,sales of traditional fixed-income lifeassurance products went up by7.1%, evidence that the life assur-ance business was holding up welldespite the more difficult con-ditions prevailing on the stockmarket.

Numerous changes were also madein the scope of the KBC Group’sconsolidation in 2001, following on

the merger of K&H Bank withABN AMRO Magyar in Hungary,the increase in the shareholding inKredyt Bank Poland, the inclusionof IPB in the results (the first timefor a full year) and the acquisitionof Peel Hunt, Patria and Investco.However, with the participatinginterest in CCF no longer contrib-uting to profit, the impact of thesechanges on the result was ultimatelylimited, on balance. If the scope ofconsolidation had remainedunchanged, KBC Group profitwould have gone down by 10.5%.

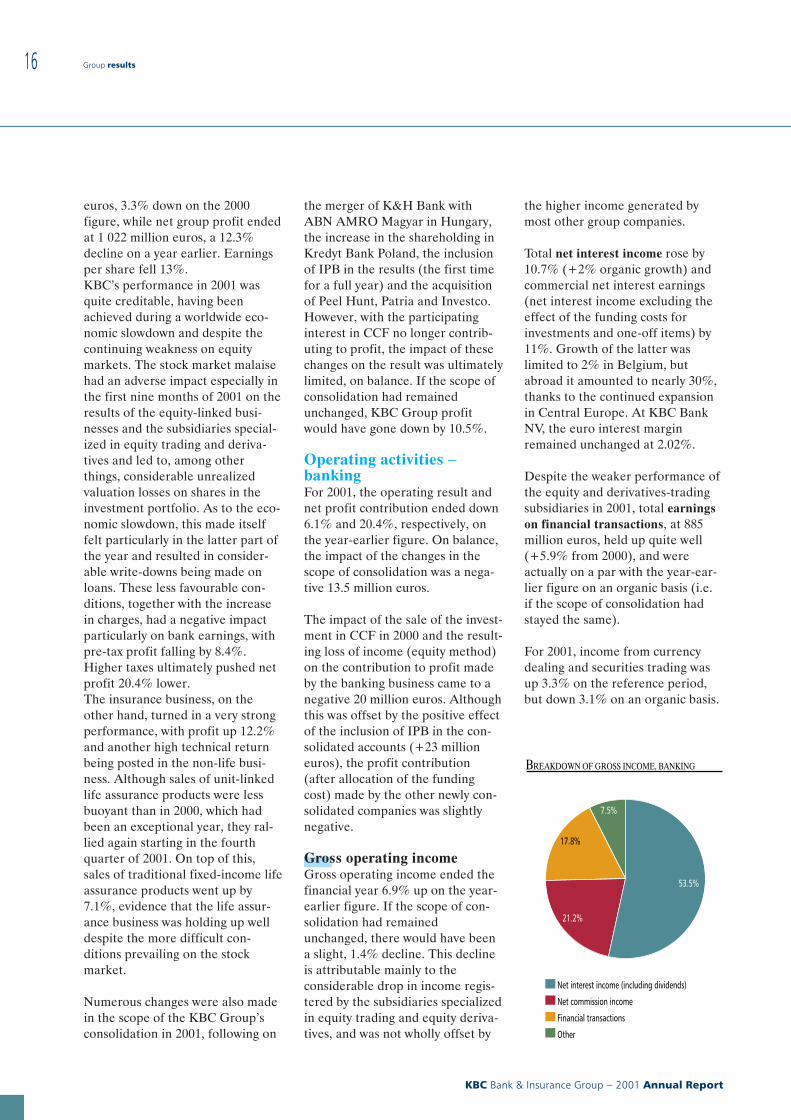

Operating activities −bankingFor 2001, the operating result andnet profit contribution ended down6.1% and 20.4%, respectively, onthe year-earlier figure. On balance,the impact of the changes in thescope of consolidation was a nega-tive 13.5 million euros.

The impact of the sale of the invest-ment in CCF in 2000 and the result-ing loss of income (equity method)on the contribution to profit madeby the banking business came to anegative 20 million euros. Althoughthis was offset by the positive effectof the inclusion of IPB in the con-solidated accounts (+23 millioneuros), the profit contribution(after allocation of the fundingcost) made by the other newly con-solidated companies was slightlynegative.

Gross operating incomeGross operating income ended thefinancial year 6.9% up on the year-earlier figure. If the scope of con-solidation had remainedunchanged, there would have beena slight, 1.4% decline. This declineis attributable mainly to theconsiderable drop in income regis-tered by the subsidiaries specializedin equity trading and equity deriva-tives, and was not wholly offset by

the higher income generated bymost other group companies.

Total net interest income rose by10.7% (+2% organic growth) andcommercial net interest earnings(net interest income excluding theeffect of the funding costs forinvestments and one-off items) by11%. Growth of the latter waslimited to 2% in Belgium, butabroad it amounted to nearly 30%,thanks to the continued expansionin Central Europe. At KBC BankNV, the euro interest marginremained unchanged at 2.02%.

Despite the weaker performance ofthe equity and derivatives-tradingsubsidiaries in 2001, total earningson financial transactions, at 885million euros, held up quite well(+5.9% from 2000), and wereactually on a par with the year-ear-lier figure on an organic basis (i.e.if the scope of consolidation hadstayed the same).

For 2001, income from currencydealing and securities trading wasup 3.3% on the reference period,but down 3.1% on an organic basis.

BREAKDOWN OF GROSS INCOME, BANKING

Net interest income (including dividends)

Net commission income

Financial transactions

Other

7.5%

17.8%

21.2%

53.5%

Group results

KBC Bank & Insurance Group − 2001 Annual Report

16

The turbulent conditions prevailingon markets over the past yearcaused the subsidiaries specializedin the equity and derivatives busi-ness to post very poor, even nega-tive earnings.In contrast, the bank dealing roomsin Brussels and especially thoseabroad put in an outstandingperformance. C{SOB’s dealingroom, too, made a strong recoveryin 2001, following a less goodperformance in 2000.At year-end, realized gains came to275 million euros (+30 millioneuros on 2000), 57 million euros ofthis being realized on shares and218 million euros on fixed-incomesecurities. In 2000, almost all thegains realized were on shares.At the end of December 2001,unrealized (and unbooked) capitalgains came to 317 million euros onshares and 641 million euros onfixed-income securities.

Net commission income went up in2001 by 2.2%, though it fell on anorganic basis by 12%. This was dueentirely to the lower fees coming infrom the securities and asset manage-ment business (-12.6%, organic-ally), especially at KBC Bank Bel-gium. There, a 31% decline wasposted as a result of the lowervolume sold (and the fact thatinvestors were less inclined toswitch between funds) compared to2000, owing to the exceptionallyweak stock market climate. All thesame, the total volume of fundsunder management rose, resultingin a 14% increase in commissionincome generated by KBC AssetManagement (mainly managementfees).The total volume under manage-ment has gone up since the end of2000 by slightly more than 4.5 bil-lion euros. Nonetheless, half of thisincrease has been eaten away by thedrop in the value of the funds sincethe start of the year. KBC Asset

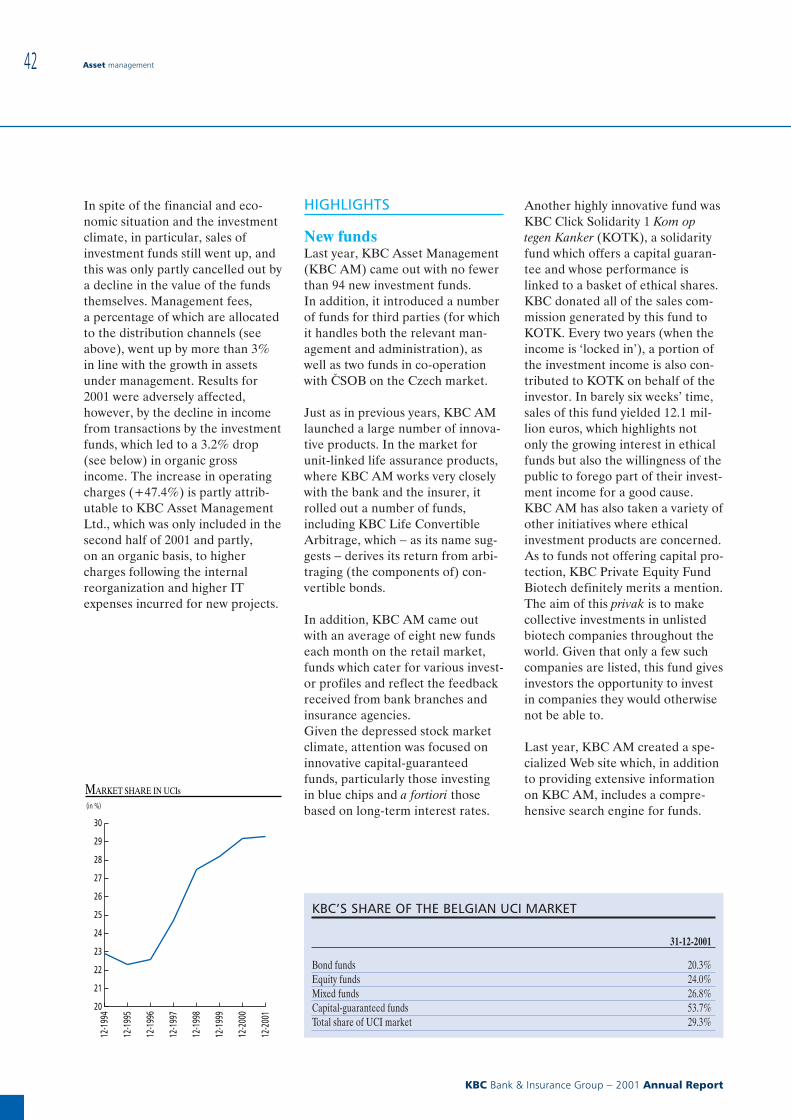

Management still has a very large(i.e. 29.3%) share of the investmentfund market in Belgium.

Higher income from paymentstransactions (+37%) is largelyattributable to the expansion andchanges in the scope of consoli-dation in Central Europe.

In 2001, other operating incomewent up by 22.9% (15%, organic-ally), due practically entirely to thesteady growth in the leasing busi-nesses, though this was accom-panied by an (albeit smaller)increase in operating charges.

General administrativeexpensesThe year 2001 closed with a 13.4%increase in charges. However, if thescope of consolidation had stayedthe same − changes mainly concernCentral Europe − the increase incharges would have come to just3.3%.The charges incurred by KBC BankNV in Belgium, which account for46% of the total, went up in 2001 by2%, driven mainly by staff charges,due to such traditional factors asindexation, promotions and theslight increase in the workforce(+1%) compared to the end of2000.

The belt-tightening measuresannounced at the end of Octoberwith a view to achieving the mergerobjectives will only start makingthemselves felt from 2002.

At the end of 2001, the cost/incomeratio came to 70.5%. Given anunchanged scope of consolidation,it would have come to 69.7%, com-pared with 66.5% at the end of2000. Accounting for the increase isnot only a rise in charges, but espe-cially the less pronounced growth inincome.

Value adjustmentsFor 2001, specific loan loss pro-visions went up by 16% comparedto 2000, and by 2.3% if the impactof Kredyt Bank Poland is not takeninto account.Specific write-downs for Belgianloans were 34% lower than in 2000,when considerable provisions hadto be set aside for a number oflarge individual loans in the textilesand technology sectors.

Disregarding the impact of KredytBank Poland, specific provisions fornon-Belgian loans practically quad-rupled compared with the situationin 2000.Including this bank in the figures,the total non-performing ratio rosefrom 2.1% to 2.8%; excluding it,the non-performing ratio came to2.4%.

Value adjustments on securitieswere in line with those posted in2000, when significant unrealizedvaluation losses had to be bookedespecially in the last quarter onaccount of the stock market climatewhich was already deteriorating atthat time.

Balance sheet and solvencyTotal assets in the banking businessclimbed by 22% from the previous

0

1

2

3

4

5

6

7

8

9

10

20012000199919981997

TIER-1 RATIO, KBC BANK

(in %)

8.89.5

7.47.26.7

Group results

KBC Bank & Insurance Group − 2001 Annual Report

17

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

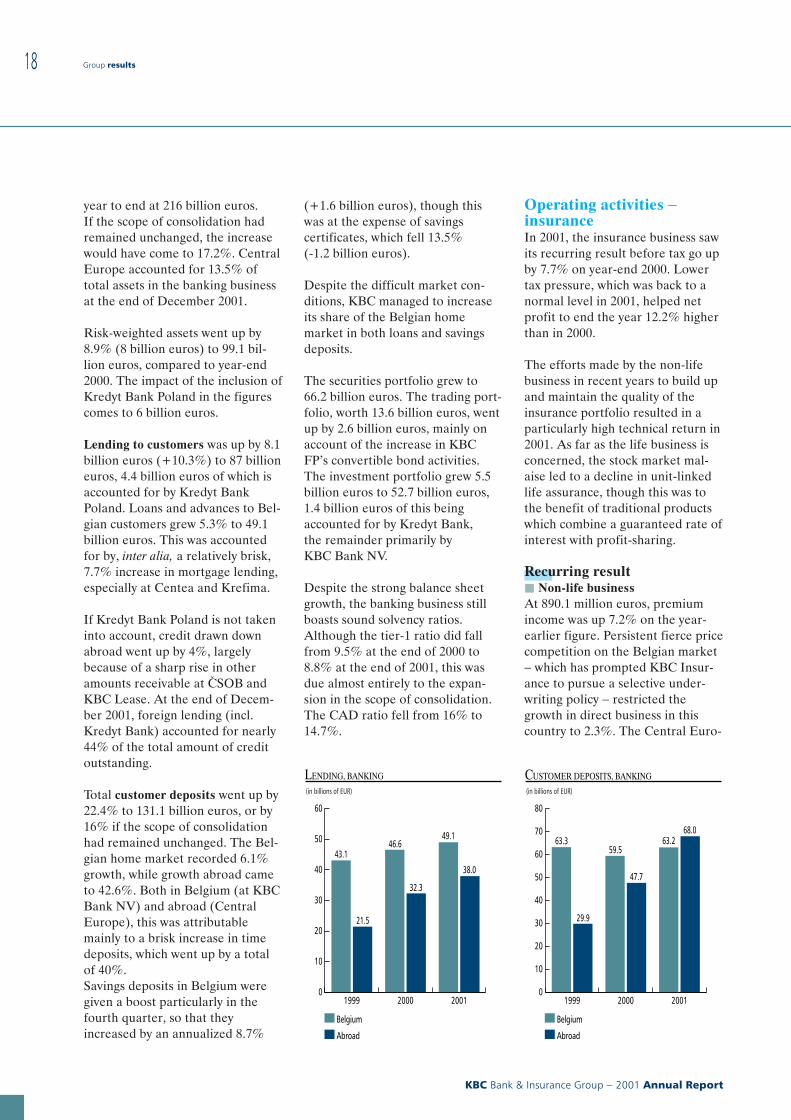

year to end at 216 billion euros.If the scope of consolidation hadremained unchanged, the increasewould have come to 17.2%. CentralEurope accounted for 13.5% oftotal assets in the banking businessat the end of December 2001.

Risk-weighted assets went up by8.9% (8 billion euros) to 99.1 bil-lion euros, compared to year-end2000. The impact of the inclusion ofKredyt Bank Poland in the figurescomes to 6 billion euros.

Lending to customers was up by 8.1billion euros (+10.3%) to 87 billioneuros, 4.4 billion euros of which isaccounted for by Kredyt BankPoland. Loans and advances to Bel-gian customers grew 5.3% to 49.1billion euros. This was accountedfor by, inter alia, a relatively brisk,7.7% increase in mortgage lending,especially at Centea and Krefima.

If Kredyt Bank Poland is not takeninto account, credit drawn downabroad went up by 4%, largelybecause of a sharp rise in otheramounts receivable at C{SOB andKBC Lease. At the end of Decem-ber 2001, foreign lending (incl.Kredyt Bank) accounted for nearly44% of the total amount of creditoutstanding.

Total customer deposits went up by22.4% to 131.1 billion euros, or by16% if the scope of consolidationhad remained unchanged. The Bel-gian home market recorded 6.1%growth, while growth abroad cameto 42.6%. Both in Belgium (at KBCBank NV) and abroad (CentralEurope), this was attributablemainly to a brisk increase in timedeposits, which went up by a totalof 40%.Savings deposits in Belgium weregiven a boost particularly in thefourth quarter, so that theyincreased by an annualized 8.7%

(+1.6 billion euros), though thiswas at the expense of savingscertificates, which fell 13.5%(-1.2 billion euros).

Despite the difficult market con-ditions, KBC managed to increaseits share of the Belgian homemarket in both loans and savingsdeposits.

The securities portfolio grew to66.2 billion euros. The trading port-folio, worth 13.6 billion euros, wentup by 2.6 billion euros, mainly onaccount of the increase in KBCFP’s convertible bond activities.The investment portfolio grew 5.5billion euros to 52.7 billion euros,1.4 billion euros of this beingaccounted for by Kredyt Bank,the remainder primarily byKBC Bank NV.

Despite the strong balance sheetgrowth, the banking business stillboasts sound solvency ratios.Although the tier-1 ratio did fallfrom 9.5% at the end of 2000 to8.8% at the end of 2001, this wasdue almost entirely to the expan-sion in the scope of consolidation.The CAD ratio fell from 16% to14.7%.

Operating activities −insuranceIn 2001, the insurance business sawits recurring result before tax go upby 7.7% on year-end 2000. Lowertax pressure, which was back to anormal level in 2001, helped netprofit to end the year 12.2% higherthan in 2000.

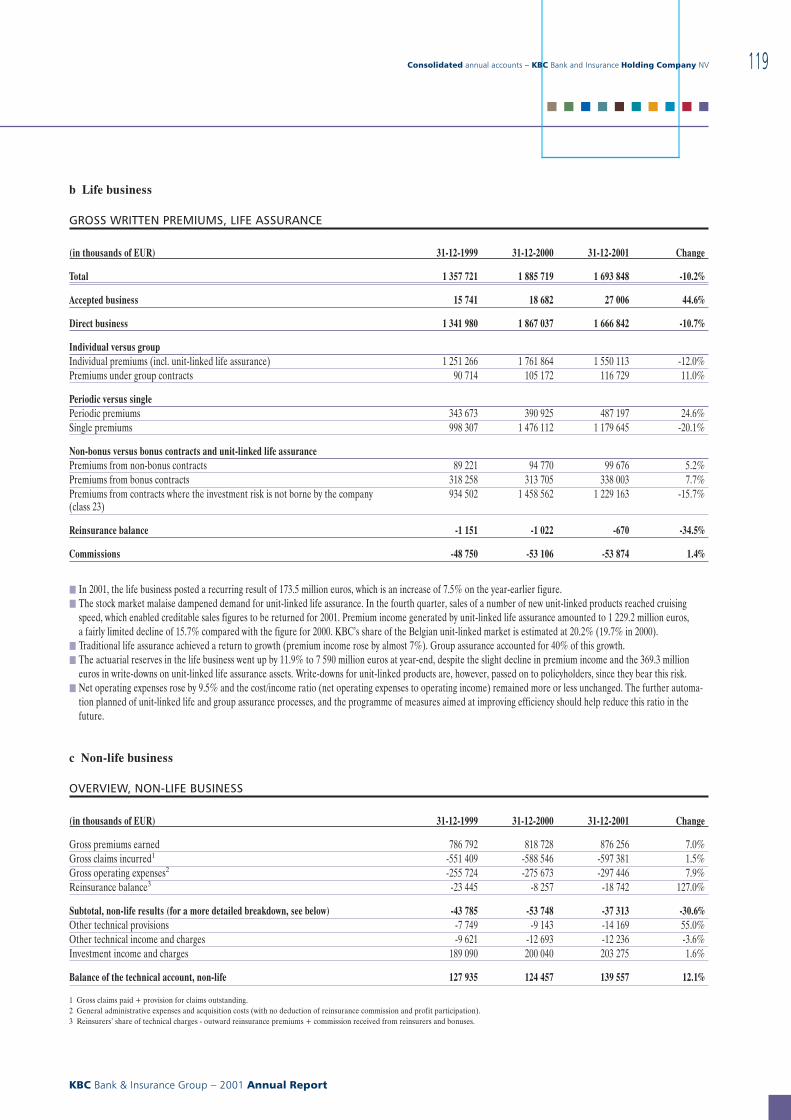

The efforts made by the non-lifebusiness in recent years to build upand maintain the quality of theinsurance portfolio resulted in aparticularly high technical return in2001. As far as the life business isconcerned, the stock market mal-aise led to a decline in unit-linkedlife assurance, though this was tothe benefit of traditional productswhich combine a guaranteed rate ofinterest with profit-sharing.

Recurring resultj Non-life businessAt 890.1 million euros, premiumincome was up 7.2% on the year-earlier figure. Persistent fierce pricecompetition on the Belgian market− which has prompted KBC Insur-ance to pursue a selective under-writing policy − restricted thegrowth in direct business in thiscountry to 2.3%. The Central Euro-

0

10

20

30

40

50

60

200120001999

LENDING, BANKING

(in billions of EUR)

43.1

21.5

46.6

32.3

49.1

38.0

Belgium

Abroad

0

10

20

30

40

50

60

70

80

200120001999

CUSTOMER DEPOSITS, BANKING

(in billions of EUR)

63.3

29.9

59.5

47.7

63.268.0

Belgium

Abroad

Group results

KBC Bank & Insurance Group − 2001 Annual Report

18

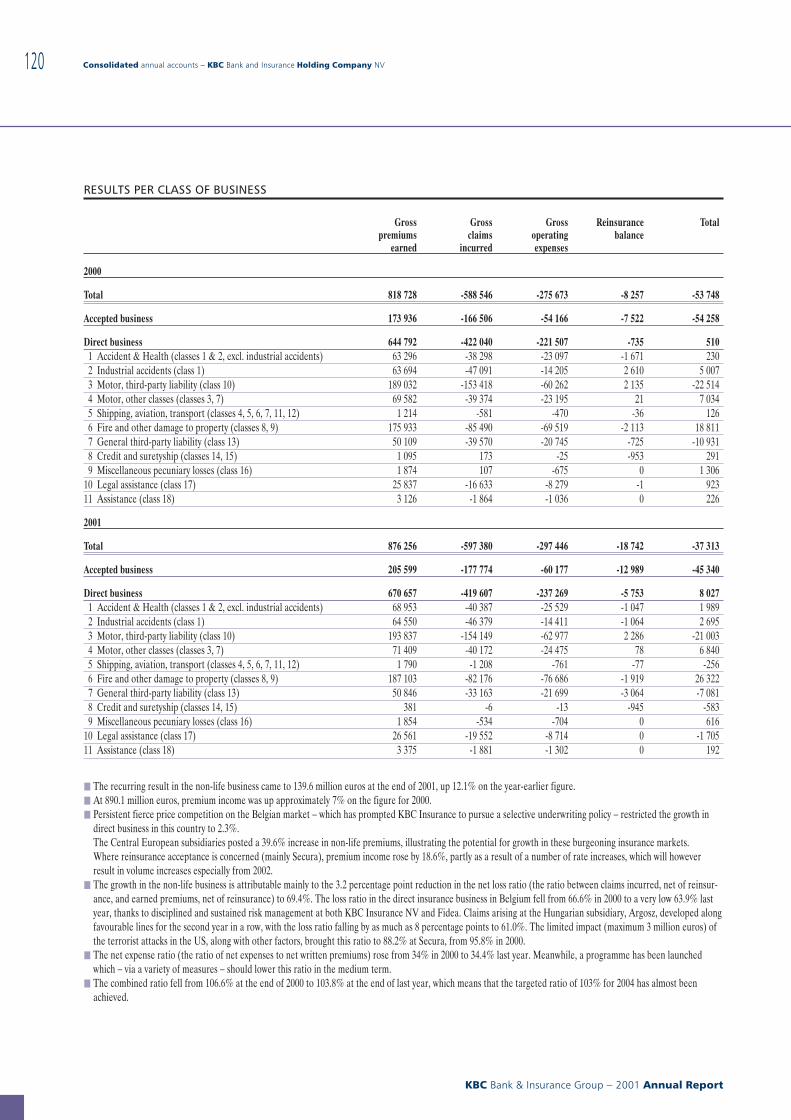

pean subsidiaries posted a 39.6%increase in non-life premiums, illus-trating the potential for growth inthese burgeoning insurancemarkets. Where reinsurance accept-ance is concerned (mainly reinsur-ance subsidiary, Secura), premiumincome rose by 18.6%, partly as aresult of a number of rate increases,which will however result in volumeincreases especially from 2002.

The fine result in the non-life busi-ness is attributable mainly to thereduction in the net loss ratio (theratio between claims incurred, netof reinsurance, and earned pre-miums, net of reinsurance) by3.2 percentage points to 69.4%.The loss ratio in the direct insur-ance business in Belgium fell from66.6% in 2000 to a very low 63.9%last year, thanks to disciplined andsustained risk management at bothKBC Insurance NV and Fidea.Claims arising at the Hungariansubsidiary, Argosz, developed alongfavourable lines for the second yearin a row, with the loss ratio fallingby as much as 8 percentage pointsto 61.0%. The limited impact (max-imum 3 million euros) of the terror-ist attacks in the US, along withother factors, brought this ratio to88.2% at Secura, from 95.8% in2000.

The net expense ratio (the ratio ofnet expenses to net written pre-miums) rose from 34.0% in 2000 to34.4% last year. Meanwhile, a pro-gramme has been launched which −via a variety of measures − shouldlower this ratio in the mediumterm. The combined ratio fell from106.6% at the end of 2000 to103.8% at the end of last year,which means that the targeted ratioof 103% by 2004 has almost beenachieved.

The recurring result in the non-lifebusiness came to 139.6 million

euros at the end of 2001, up 12.1%on the year-earlier figure.

j Life businessThe stock market malaise damp-ened demand for unit-linked lifeassurance, with sales hitting a lowafter 11 September. In the fourthquarter, sales of a number of newunit-linked products reached cruis-ing speed, which enabled very cred-itable sales figures to be returnedfor 2001.

Premium income generated by unit-linked life assurance amounted to1 229.2 million euros, a fairlylimited decline of 15.7% comparedwith the figure for 2000, which hadbeen an excellent year for sales.In spite of this, initial estimatesindicate that KBC Insurance wasable to step up its share of the Bel-gian market from 19.7% in 2000 to20.2% in 2001.

In contrast to the trend for unit-linked products, traditional lifeassurance achieved a return togrowth, with premium income up

7.1% on the figure for 2000. Groupassurance accounted for 40% or12 million euros of this growth.

In 2001, total gross written lifepremiums came to 1 693.8 millioneuros, down by a limited 191.9million euros (-10%) on the year-earlier figure.

The actuarial reserves in the lifebusiness went up by 11.9% to 7 590million euros at year-end, despitethe slight decline in premiumincome and the 369.3 million eurosin write-downs on unit-linked lifeassurance assets. Write-downs forunit-linked products are, however,borne by policyholders.

Net operating expenses rose by9.5% and the cost/income ratio (netoperating expenses to operatingincome) remained more or lessunchanged at 40%. The furtherautomation planned of unit-linkedlife and group assurance processesshould help reduce this ratio in thefuture.

In 2001, the life business posted arecurring result of 173.5 millioneuros, which is an increase of 7.5%on the year-earlier figure.

j Non-technical resultThe non-technical result rose to87.5 million euros, up 1.7% on thefigure for 2000, with investmentincome increasing by 8.0 millioneuros. However, income from par-ticipating interests accounted forusing the equity method fell by 6.5million euros as a result of:j CCF no longer contributing to

profit (good for 2.8 millioneuros), following the sale of theinvestment in 2000;

j the Irish FBD’s profit contri-bution falling in 2001 by 2 mil-lion euros to 7 million euros;

j the 2001 result from the PolishAgropolisa and Warta share-

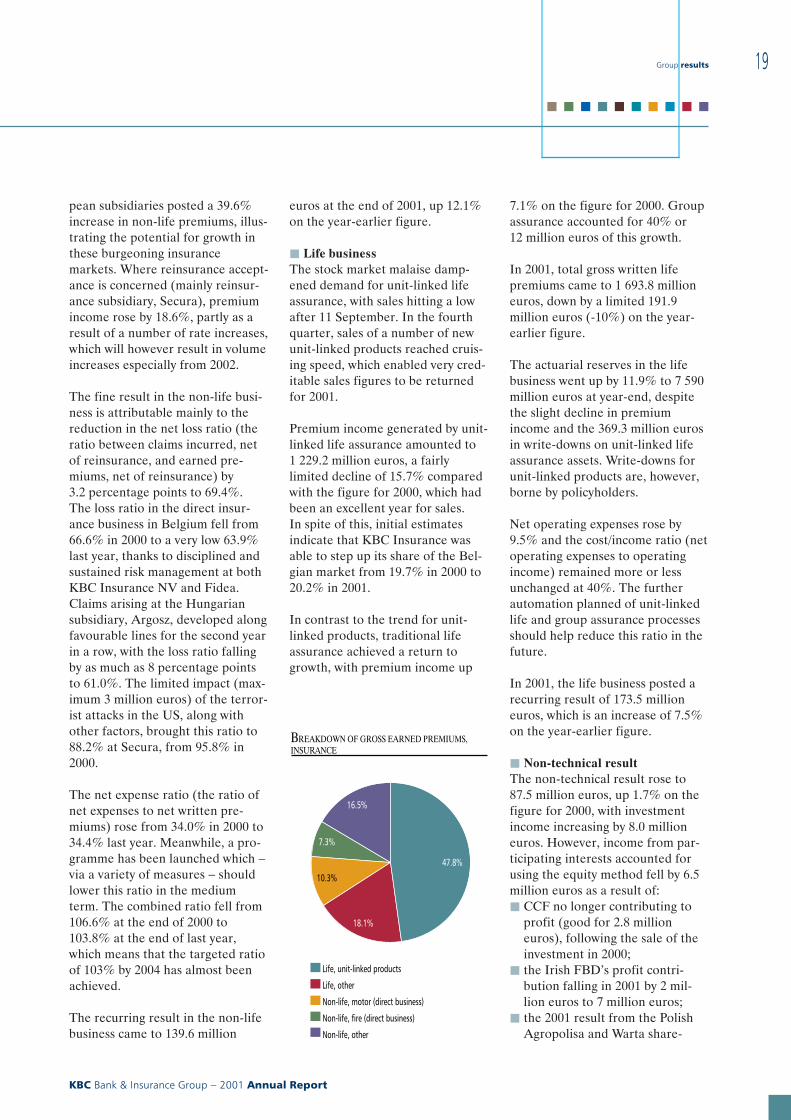

BREAKDOWN OF GROSS EARNED PREMIUMS, INSURANCE

Life, unit-linked products

Life, other

Non-life, motor (direct business)

Non-life, fire (direct business)

Non-life, other

16.5%

7.3%

10.3%

18.1%

47.8%

Group results

KBC Bank & Insurance Group − 2001 Annual Report

19

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

holdings falling by 1.7 millioneuros to -2 million euros.

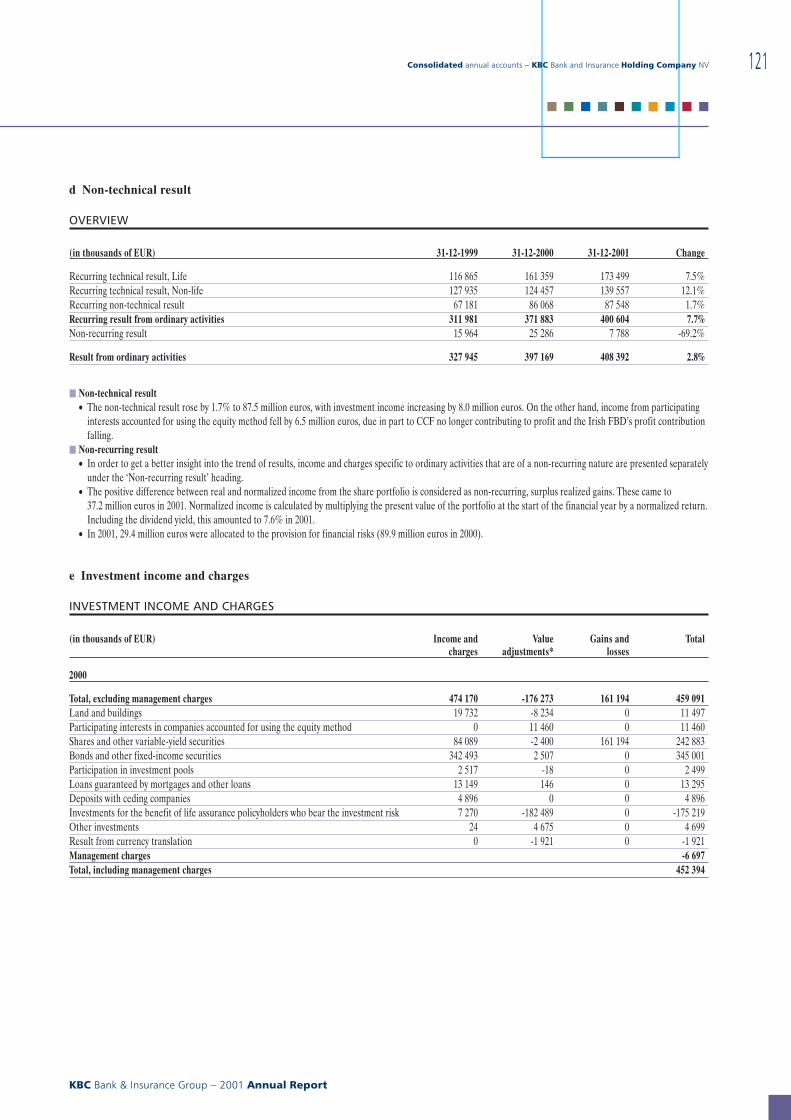

Non-recurring resultThe non-recurring result includesall income and charges specific toordinary activities that are of a non-recurring nature.

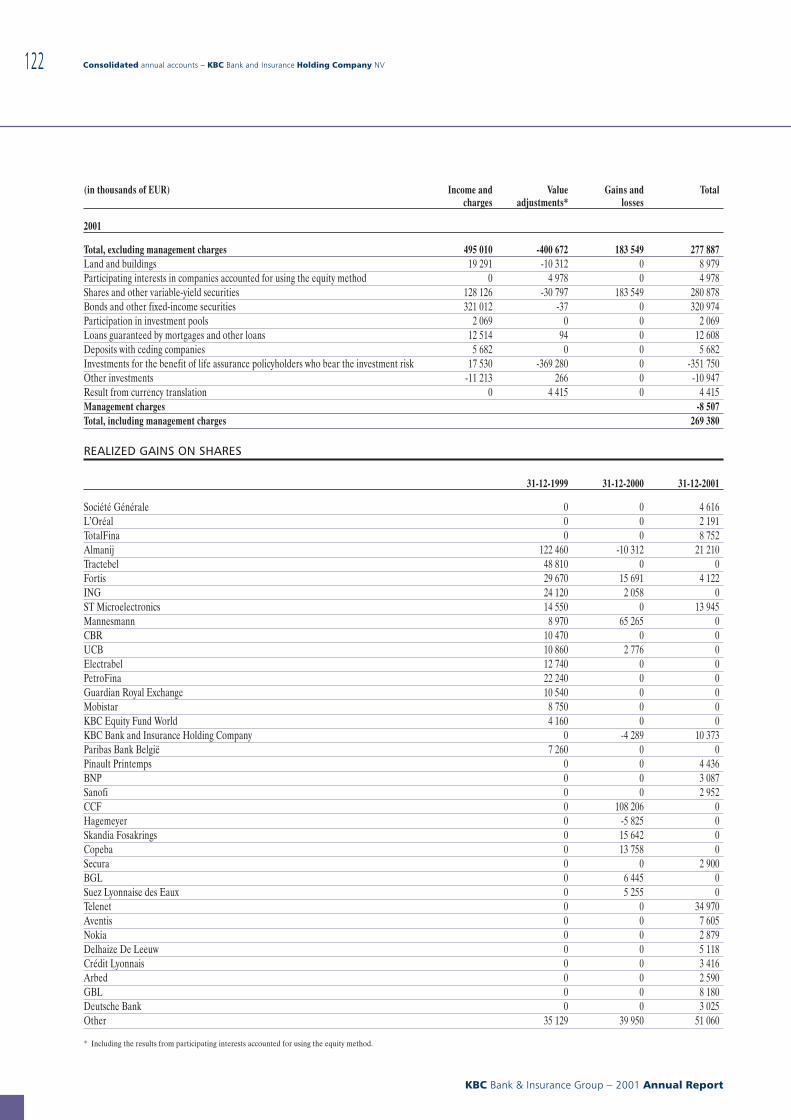

The positive difference betweenreal and normalized income fromthe share portfolio is considered asnon-recurring, surplus realizedgains. These came to 37.2 and 91.9million euros in 2001 and 2000,respectively. Normalized income iscalculated by multiplying thepresent value of the portfolio at thestart of the financial year by a nor-malized return. Including the divi-dend yield, this amounted to 7.6%in 2001, compared to 6.9% in 2000.In 2001, 29.4 million euros wereallocated to the provision for finan-cial risks (89.9 million euros in2000).

Besides the above items, the 2000non-recurring result included theadditional write-back of 23.3 mil-lion euros from the provision forunearned premiums due to thechange to the way in which this pro-vision is calculated, the write-backof the full 29.6 million euros fromthe technical provision for Y2K, aswell as a number of further allo-cations to provisions and valueadjustments, likewise for a total of29.6 million euros.

Balance sheet and solvencyIn 2001, the balance sheet totalgrew by 1 087.3 million euros to12 583.8 million euros, with tech-nical provisions, which increased by931.3 million euros to 10 319.1 mil-lion euros, accounting for 82.0%of liabilities. Technical non-life pro-visions went up by 104.8 millioneuros to 2 567.4 million euros atyear-end 2001. The claims reserveratio, or the average gross provision

for claims outstanding to grossearned premiums, came to 232%,reflecting the prudent provisioningpolicy adhered to in the insurancebusiness. Partly as a result of therecovery in sales of traditional lifeassurance, technical provisions fortraditional life assurance rose by129.4 million euros to 4 769.6 mil-lion euros, which makes it the larg-est liabilities item. Despite the mal-aise on the financial markets, tech-nical provisions for transactionslinked to investment funds climbedby 666.1 million euros to just under3 000 million euros at the end of2001, and this in only a few years ofunit-linked products beinglaunched.

Investments represent 92.3% ofassets. Compared to the year-earlier figure, the carrying value ofparticipating interests accountedfor using the equity methodincreased by 1.7 million euros to104.2 million euros at the end of2001. The market value of the shareportfolio (excluding unit-linkedproducts) fell to 3 213.8 millioneuros, down from 3 532.0 millioneuros a year earlier, with adversedevelopments on the stock marketcausing unrealized gains on this

portfolio to drop to 427 millioneuros. Conversely, the market valueof the portfolio of fixed-incomesecurities climbed by 115.1 millioneuros to 5 442.5 million euros, dueto the interest-rate trend and netpurchases.

As regards the other provisions,those set aside for taxation went upto 71.1 million euros, while the pro-vision for financial risks (156.7 mil-lion euros), the restructuring pro-vision (25.4 million euros) andother provisions (9.1 million euros)remained virtually unchanged.

The changed circumstances on thefinancial markets did not have anadverse effect on solvency.The explicit solvency ratio, i.e. theratio between the solvency capital −excluding unrealized gains −present in the insurance group andthe required solvency capital, wentup by 11 percentage points to318%. The corresponding solvencysurplus climbed from 828.1 millioneuros at the end of 2000 to 921.3million euros in 2001.

Holding-company activitiesThe negative contribution made bythe holding company to Group

0

50

100

150

200

250

300

350

20012000199919981997

SOLVENCY RATIO, KBC INSURANCE

(in %)

318307298311

282

0

2

4

6

8

10

12

14

200120001999

INVESTMENTS INSURANCE

(in billions of EUR)

9.4

1.9

10.6

1.5

11.6

0.8

Carrying value

Unrealized gains

Group results

KBC Bank & Insurance Group − 2001 Annual Report

20

profit increased to -35 million eurosin 2001, from -32 million euros in2000. This is due primarily to thehigher funding costs resulting fromhigher short-term interest rates inthe first half of 2001.

Extraordinary result andtaxationExtraordinary income was almostentirely attributable to the bankingbusiness, where gains of 80.7 mil-lion euros were realized on the saleof the investment in Telenet in thefirst quarter of 2001. It should benoted that the insurance businessalso realized gains of 39 millioneuros on the sale of its stake inTelenet, but that it allocated virtu-ally all of these gains to the pro-vision for financial risks (both takeninto account in the non-recurringresult), in accordance with its valu-ation rules. For the KBC Group,therefore, 75% of the gain2 realizedon the sale of Telenet is reflected innet Group profit.

There was a 28.8% rise in taxes inthe banking business, partly as aresult of tax being assessed forprevious financial years at KBCBank NV (23.4 million euros) andthe higher taxable profits of a num-ber of subsidiaries (certain profitshad not yet been taxable in 2000).In the insurance business, taxeswere 30% lower than in 2000, whenthe tax burden had been exception-ally high due to the realization oftaxable gains from the sale of prop-erty and the sale of Centea’s insur-ance portfolio to Fidea, and toother financial assets.

Profit outlookNow that the difficult year 2001 hascome to a close, KBC expects itsgross income to head up in 2002,powered by higher net interestearnings and better results from itsequity-linked activities, provided of

course that conditions on the finan-cial markets continue to improve.In addition, the belt-tighteningmeasures announced last Octoberwith a view to achieving the mergerobjectives will have a positiveimpact on the cost trend.However, given the uncertaintyregarding economic growth and theinfluence this has on credit volumeand the quality of the loan port-folio, as well as on the financialmarkets, the outlook for financialyear 2002 is itself uncertain andearnings growth difficult to predict.Nevertheless, KBC is convincedthat it is a competitive player, andfaces the year 2002 with confidence.

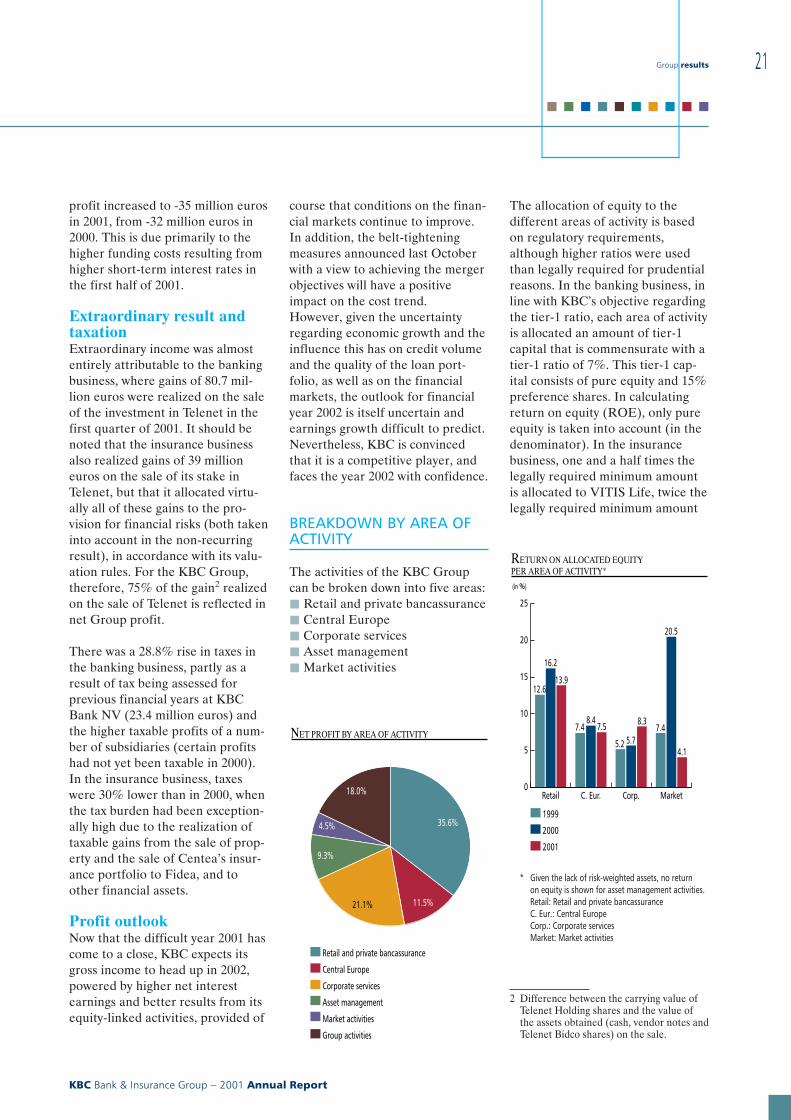

BREAKDOWN BY AREA OFACTIVITY

The activities of the KBC Groupcan be broken down into five areas:j Retail and private bancassurancej Central Europej Corporate servicesj Asset managementj Market activities

The allocation of equity to thedifferent areas of activity is basedon regulatory requirements,although higher ratios were usedthan legally required for prudentialreasons. In the banking business, inline with KBC’s objective regardingthe tier-1 ratio, each area of activityis allocated an amount of tier-1capital that is commensurate with atier-1 ratio of 7%. This tier-1 cap-ital consists of pure equity and 15%preference shares. In calculatingreturn on equity (ROE), only pureequity is taken into account (in thedenominator). In the insurancebusiness, one and a half times thelegally required minimum amountis allocated to VITIS Life, twice thelegally required minimum amount

2 Difference between the carrying value ofTelenet Holding shares and the value ofthe assets obtained (cash, vendor notes andTelenet Bidco shares) on the sale.

NET PROFIT BY AREA OF ACTIVITY

Retail and private bancassurance

Central Europe

Corporate services

Asset management

Market activities

Group activities

18.0%

4.5%

9.3%

21.1% 11.5%

35.6%

Group results

KBC Bank & Insurance Group − 2001 Annual Report

21

■ ■ ■ ■ ■ ■ ■ ■ ■ ■

RETURN ON ALLOCATED EQUITY PER AREA OF ACTIVITY*

(in %)

* Given the lack of risk-weighted assets, no return on equity is shown for asset management activities.Retail: Retail and private bancassuranceC. Eur.: Central EuropeCorp.: Corporate servicesMarket: Market activities

1999

2000

2001

0

5

10

15

20

25

MarketCorp.C. Eur.Retail

12.6

16.2

13.9

7.48.4

7.5

5.2 5.7

8.37.4

20.5

4.1

to the retail businesses and threetimes the legally required minimumamount to corporate services andthe activities in Central Europe.

The ‘Group item’ includes capitalgains in the banking business,adjustments made to the value ofsecurities, income and charges thatcan not, or only arbitrarily, be allo-cated to the specific areas of activ-ity, goodwill that is deducted fromequity, and leveraging (funding ofsubsidiaries’ equity capital with bor-rowings) by the holding company.Consequently, the positive impactof the deduction of goodwill and ofleveraging on ROE is only reflectedin the ROE for the whole Group,but not in the ROE for the differ-ent areas of activity.

Since the previous annual report,a few structural changes − mainlythe introduction of a new profit-centre-based reporting system inthe banking business − andmethodological improvements havebeen made (for 2001 and the refer-ence periods).

These include mainly:j The inclusion of the Fund for

General Banking Risks in netprofit and own funds (and thusalso in the ROE).

j The inclusion of minority inter-ests in net profit (and ROE) forthe various areas of activity(since 100% of the risk-weightedassets are consolidated, allocatedequity also reflects 100% of therisk-weighted assets). Minorityinterests are deducted from netprofit for the ‘Group item’.

j Net profit (and ROE) for theareas of activity being shownbefore the amortization of cap-italized goodwill. The (relativelylimited) amortization of capital-ized goodwill is included underthe ‘Group item’.

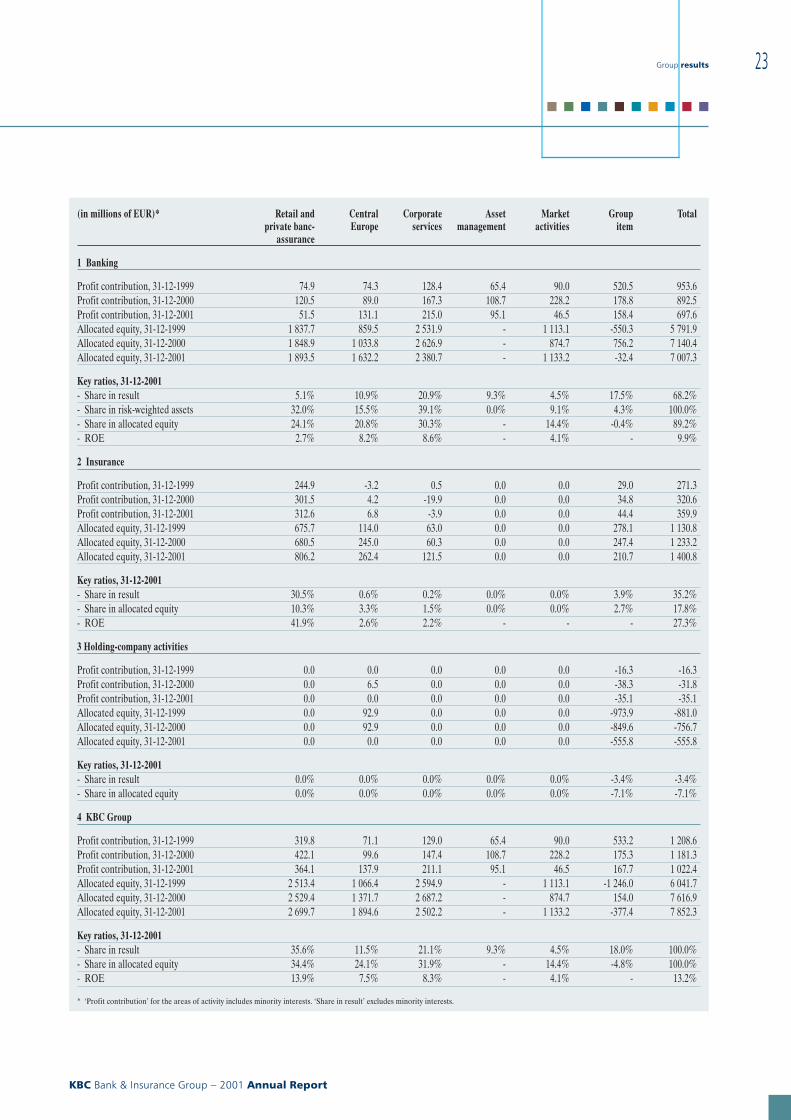

The overview table shows the keyfigures per area of activity. In thenext section, a description, detailedfinancial figures and a brief reporton each area of activity is provided.

Group results

KBC Bank & Insurance Group − 2001 Annual Report

22

(in millions of EUR)* Retail andprivate banc-

assurance

CentralEurope

Corporateservices

Assetmanagement

Marketactivities

Groupitem

Total

1 Banking

Profit contribution, 31-12-1999 74.9 74.3 128.4 65.4 90.0 520.5 953.6Profit contribution, 31-12-2000 120.5 89.0 167.3 108.7 228.2 178.8 892.5Profit contribution, 31-12-2001 51.5 131.1 215.0 95.1 46.5 158.4 697.6Allocated equity, 31-12-1999 1 837.7 859.5 2 531.9 - 1 113.1 -550.3 5 791.9Allocated equity, 31-12-2000 1 848.9 1 033.8 2 626.9 - 874.7 756.2 7 140.4Allocated equity, 31-12-2001 1 893.5 1 632.2 2 380.7 - 1 133.2 -32.4 7 007.3

Key ratios, 31-12-2001- Share in result 5.1% 10.9% 20.9% 9.3% 4.5% 17.5% 68.2%- Share in risk-weighted assets 32.0% 15.5% 39.1% 0.0% 9.1% 4.3% 100.0%- Share in allocated equity 24.1% 20.8% 30.3% - 14.4% -0.4% 89.2%- ROE 2.7% 8.2% 8.6% - 4.1% - 9.9%

2 Insurance

Profit contribution, 31-12-1999 244.9 -3.2 0.5 0.0 0.0 29.0 271.3Profit contribution, 31-12-2000 301.5 4.2 -19.9 0.0 0.0 34.8 320.6Profit contribution, 31-12-2001 312.6 6.8 -3.9 0.0 0.0 44.4 359.9Allocated equity, 31-12-1999 675.7 114.0 63.0 0.0 0.0 278.1 1 130.8Allocated equity, 31-12-2000 680.5 245.0 60.3 0.0 0.0 247.4 1 233.2Allocated equity, 31-12-2001 806.2 262.4 121.5 0.0 0.0 210.7 1 400.8

Key ratios, 31-12-2001- Share in result 30.5% 0.6% 0.2% 0.0% 0.0% 3.9% 35.2%- Share in allocated equity 10.3% 3.3% 1.5% 0.0% 0.0% 2.7% 17.8%- ROE 41.9% 2.6% 2.2% - - - 27.3%

3 Holding-company activities

Profit contribution, 31-12-1999 0.0 0.0 0.0 0.0 0.0 -16.3 -16.3Profit contribution, 31-12-2000 0.0 6.5 0.0 0.0 0.0 -38.3 -31.8Profit contribution, 31-12-2001 0.0 0.0 0.0 0.0 0.0 -35.1 -35.1Allocated equity, 31-12-1999 0.0 92.9 0.0 0.0 0.0 -973.9 -881.0Allocated equity, 31-12-2000 0.0 92.9 0.0 0.0 0.0 -849.6 -756.7Allocated equity, 31-12-2001 0.0 0.0 0.0 0.0 0.0 -555.8 -555.8

Key ratios, 31-12-2001- Share in result 0.0% 0.0% 0.0% 0.0% 0.0% -3.4% -3.4%- Share in allocated equity 0.0% 0.0% 0.0% 0.0% 0.0% -7.1% -7.1%

4 KBC Group

Profit contribution, 31-12-1999 319.8 71.1 129.0 65.4 90.0 533.2 1 208.6Profit contribution, 31-12-2000 422.1 99.6 147.4 108.7 228.2 175.3 1 181.3Profit contribution, 31-12-2001 364.1 137.9 211.1 95.1 46.5 167.7 1 022.4Allocated equity, 31-12-1999 2 513.4 1 066.4 2 594.9 - 1 113.1 -1 246.0 6 041.7Allocated equity, 31-12-2000 2 529.4 1 371.7 2 687.2 - 874.7 154.0 7 616.9Allocated equity, 31-12-2001 2 699.7 1 894.6 2 502.2 - 1 133.2 -377.4 7 852.3