Introduction to International Finance International Finance (MB 74)

Upload

stolen-heartCategory

view

219download

0

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 1/22

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 2/22

How do buyers and sellers in different countries dobusiness when they all use different currencies?Means that if someone in the US wants to buy something from someone in, say,India, she must first exchange her local currency dollars for the currencyaccepted in India Rupee.

This currency conversion occurs at an exchange rate .

The exchange rate the price of one nation's currency in termsof another nation's is a central concept in InternationalFinance .

Efficient market exists when the exchange rate reflects all availablepublic and private information.

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 3/22

` Hedging decisions

` Investment of short-term fundsEg : An international co, when having surplus cash makes

short-term investment in different currency. It will prefercurrencies where future spot rate is expected to rise thanforward rate.

` Long-term investments of fundsEg : An international co., wishes to set up an office in foreigncountry.

` Financing decisions

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 4/22

1 . Technical forecasting

2. Fundamental forecasting

3. Market-based forecasting

4. Mixed forecasting

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 5/22

` Is based on movements of historical rates, asthis gives clear indication about movements infuture.

` Various charting types are used such as linechart, bar chart, candle-stick chart, etc.

` Is generally used for short-term forecasts.

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 6/22

` H ere the future rates are estimated on the basis of changesin the economic variable like Inflation.

Inflation is a rise in the general level of prices

of goods and services in an economy over aperiod of time.

Eg : Inflation rate in Country A higher than inCountry B by 5%, the value of A¶s currency vis-àvis B¶s currency will decline by that %.

³H igher the Inflation, lower will be the currency rate´

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 7/22

` T he estimates of future rates depends on theexpected trend in the market.

Eg : 1$ - Rs.40But due to some economic pressures it isexpected to rise to Rs.41, then speculator willbuy $ and sell in future ± thus making a profit.

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 8/22

It is a weighted average of technical,fundamental and market-based forecasts.

Forecasting Error !!!!

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 9/22

` By a controlled exchange rate regime, we mean apegged, yet adjustable exchange rate.

` T he exchange rate is fixed and administered, yetthe monetary authorities change the value of currency when fundamental disequilibrium in theBOP occurs.

` When this occurs the forecaster reviews theinformation reg. price level, money supply, foreigntrade, international reserves, etc.

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 10/22

` H igher rate of inflation

` Shrinkage in international reserve

` Coverage of imports by export earnings

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 11/22

In a floating exchange rate regime, the value of currency changes frequently.

Eg : Firm A is a MNCDue to change in value of currency, the co¶svalue of assets and liabilities change whichindirectly impact the cash flows.

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 12/22

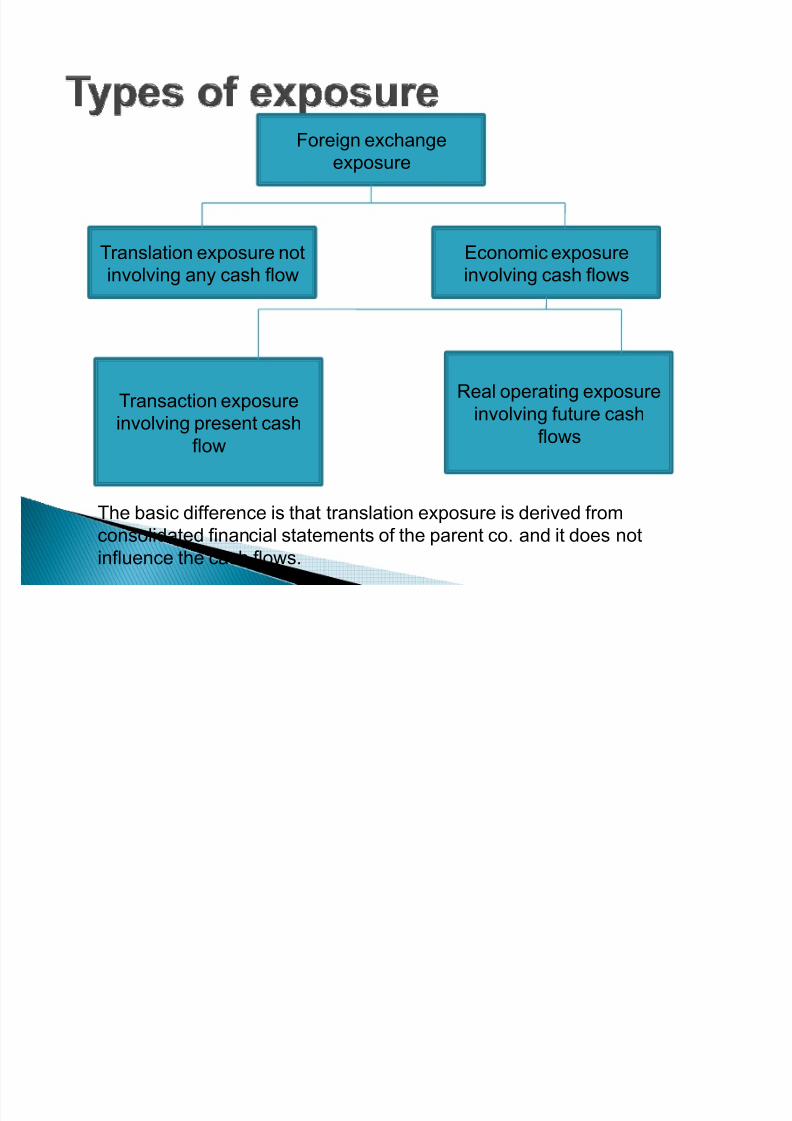

Foreign exchangeexposure

T ranslation exposure not

involving any cash flow

Economic exposure

involving cash flows

T ransaction exposureinvolving present cash

flow

Real operating exposure

involving future cashflows

T he basic difference is that translation exposure is derived fromconsolidated financial statements of the parent co. and it does notinfluence the cash flows.

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 13/22

T here is one view that any talk of exchangerate exposure is irrelevant.

T his argument is based on PPP theory .

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 14/22

`

States that the movement in exchange rate is matched by movement inprice and so, the financial performance of the firm is not affected.Eg : Inflation India s higher than USA Value of rupee is lower than $` Co. A imports components from USA` Face cost escalation on account of higherimport bill.

` Its competitive power would erode via-a-vis the domestic firm producingthe same products.` But if the exchange rate has occurred due to rise in inflation, then the

domestic firms too will escalate.

Therefore, there will be no change in the competitive position btw. Theimporting firm and domestic firm even after changes in the exchange rates.

Hence PPP theory says that exchange rate exposure is irrelevant.

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 15/22

` Some other view that exchange rate is relevant,because PPP is not applicable in short-run.

` Even in long-run, it may not be useful.` H ence, there are various hedging tools that are

used to protect themselves from foreign exchangeexposure.

H edging means making an investment toreduce the risk of adverse price movements inan asset.

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 16/22

` Is concerned with the impact of changes inexchange rate on present cash flows.

` Emerges mainly on account of:

Export & import of commodity on open accountx Eg :Borrowing & lending in foreign currencyx Eg :Intra-firm flows in international co.x Eg :

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 17/22

` It arises when the changes in the exchange rate, together withrate of inflation, alter the amount and risk element of acompanies future revenue and cost stream.

` If inflation is forecasted correctly, the real operating exposure can

be estimated.` Eg : Rupee decline by 10%Exports ± competitiveImports ± costlier T hus affecting the cash flows

Inflation increases by 10%, then the ultimate result iszero real operating exposure.

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 18/22

` It is also known as accounting exposure.` It emerges on account of consolidation of financial

statements of different units of a MNC.

Eg :

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 19/22

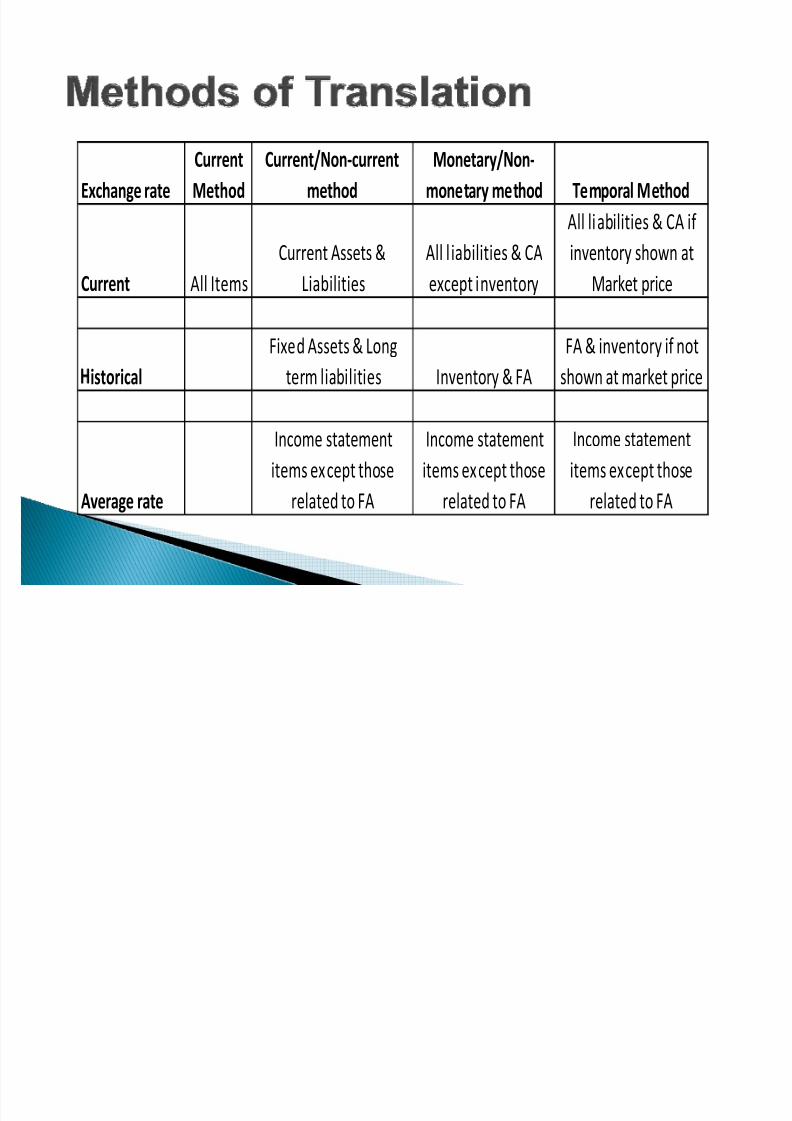

` Current rate method

` Current/non-current method

` Monetary/non-monetary method

` Temporal Method

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 20/22

Exchange rateCurrentMethod

Current/Non-currentmethod

Monetary/Non-monetary method Temporal Method

Current All Items

Current Assets &

Liabilities

All liabilities & CA

except inventory

All liabilities & CA if inventory shown at

Market price

istoricalFixed Assets & Long

term liabilities Inventory & FAFA & inventory if not

shown at market price

Average rate

Income statementitems except those

related to FA

Income statementitems except those

related to FA

Income statementitems except those

related to FA

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 21/22

8/8/2019 International Finance - Part 1

http://slidepdf.com/reader/full/international-finance-part-1 22/22

` H edging

` Need for hedging

` H edging techniques

![Department for International Trade and UK Export Finance ... · Department for International Trade and UK Export Finance: Key events to date Part [01] – Developing an export strategy](https://static.fdocuments.us/doc/165x107/5f0b343d7e708231d42f5c40/department-for-international-trade-and-uk-export-finance-department-for-international.jpg)