Assessment of impact of air pollution among school children in selected schools of Dhaka city.

Upload

truongnguyetCategory

view

229download

0

Miami-Dade County Public Schools

Internal Audit Report Selected Schools/Centers

The Financial Statements Were Fairly Stated

For All 45 Schools/Centers In This Report.

At Two Schools/Centers,

Controls Over The Safeguarding Of Collections

Need Improvement.

Property Inventory Results Were Satisfactory

For All Schools/Centers Reported Herein.

September 2017

THE SCHOOL BOARD OF MIAMI-DADE COUNTY, FLORIDA Dr. Lawrence S. Feldman, Chair

Dr. Marta Pérez, Vice Chair Dr. Dorothy Bendross-Mindingall

Ms. Susie V. Castillo Dr. Steve Gallon III

Ms. Perla Tabares Hantman Dr. Martin Karp

Ms. Lubby Navarro Ms. Mari Tere Rojas

Mr. Alberto M. Carvalho

Superintendent of Schools

Mr. Jose F. Montes de Oca, CPA Chief Auditor

Office of Management and Compliance Audits

Contributors To This Report: School Audits Performed by:

Ms. Yvonne M. Barrios Ms. Pamela L. Davis

Mr. Harry Demosthenes Mr. Hugo Garcia, CFE

Ms. Maite Jimenez Mr. Reginald Lafontant

Ms. Sandra Lainez Ms. Wanda M. Ramirez

Mr. Elliott Satz Ms. Glendys Y. Serra

Ms. Patricia A. Tumelty Ms. Jana E. Wright, CFE

School Audits Supervised and Reviewed by:

Ms. Maria T. Gonzalez, CPA Ms. Tamara Wain, CPA

Ms. Mariela Jimenez-Linaje

Property Audit Supervised and Performed by: Mr. Rolando Gonzalez and Property Audits Staff

School Audits Division Assisted by:

Mr. Daniel J. Garo

School Audit Report Prepared by: Ms. Maria T. Gonzalez, CPA

Office of Management and Compliance Audits School Board Administration Building • 1450 N.E. 2nd Ave. • Suite 415 • Miami, FL 33132

305-995-1436 • 305-995-1331 (FAX) • http://mca.dadeschools.net

Chief Auditor Jose F. Montes de Oca, CPA

September 28, 2017

The Honorable Chair and Members of The School Board of Miami-Dade County, Florida Members of The School Board Audit and Budget Advisory Committee Mr. Alberto M. Carvalho, Superintendent of Schools Ladies and Gentlemen: This report includes the audit results of 45 schools/centers currently reporting to the North Region Office, the Central Region Office, the South Region Office or the Office of Adult/Vocational, Alternative and Community Education within School Operations. The audit period of 34 of the 45 schools/centers is two fiscal years ended June 30, 2017, while the audit period of the remaining 11 schools/centers is one fiscal year ended June 30, 2017. At 17 schools/centers, there was a change of Principal since the prior audit. The main objectives of these audits were to express an opinion on the financial statements of the schools/centers, evaluate compliance with District policies and procedures, and ensure that assets were properly safeguarded. The audits included a review of internal funds at all 45 schools/centers. On a selected basis, we reviewed Title I Program procedures and Full-Time Equivalent (FTE) reporting and student records. Generally as part of audit follow-ups, we reviewed payroll, the Purchasing Card program, and certain aspects of school site data security. The audits also included the results of property inventories of all schools/centers reported herein. Audit results proved satisfactory at 43 of the 45 schools/centers reported herein, and property inventory results for all schools/centers were satisfactory. Notwithstanding the individual school findings included in this report, the financial statements of all 45 schools/centers reported herein were fairly stated. At two schools/centers, we found improper controls over the receipting and depositing of funds and the safeguarding of deposits. These issues resulted in monetary losses at both schools. We discussed the audit findings with school, region and district administrations, and their responses are included in this report. In closing, we would like to thank the schools/centers’ staff and administration for the cooperation and consideration provided to the audit staff during the performance of these audits. Sincerely,

Jose F. Montes de Oca, CPA Chief Auditor Office of Management and Compliance Audits

JFM:mtg

i

TABLE OF CONTENTS

Page Number

EXECUTIVE SUMMARY ........................................................................................... 1 CONDENSED ANNUAL FINANCIAL REPORTS .................................................... 10 INTERNAL CONTROLS RATING ........................................................................... 20 SUMMARY SCHEDULE OF AUDIT FINDINGS ...................................................... 24 LIST OF SCHOOL PRINCIPALS/ADMINISTRATORS ........................................... 28 ACCOUNTING SYSTEM CONVERSION SCHEDULE ............................................ 34 PROPERTY SCHEDULE ......................................................................................... 38 FINDINGS AND RECOMMENDATIONS 1. Inadequate Controls

Over The Collecting, Receipting, And Safeguarding Of Collections Led To Monetary Losses Madie Ives Elementary School ................................................................... 42

2. Deposits Not Property Safeguarded Resulted In Monetary Losses Ada Merritt K-8 Center ................................................................................ 48

OBJECTIVES, SCOPE AND METHODOLOGY ...................................................... 52 BACKGROUND ....................................................................................................... 54 ORGANIZATIONAL CHART (SCHOOLS/CENTERS) ............................................ 61

ii

TABLE OF CONTENTS (CONTINUED)

Page Number

APPENDIX—MANAGEMENT’S RESPONSES PRINCIPALS: North Region Office School/Center: Madie Ives Elementary School .............................................................. 62 Central Region Office School/Center Ada Merritt K-8 Center ........................................................................... 64 REGION ADMINISTRATION: North Region Office ............................................................................... 66 Central Region Office ............................................................................ 68 DISTRICT ADMINISTRATION: School Operations ................................................................................. 69

1 Internal Audit Report Selected Schools/Centers

EXECUTIVE SUMMARY The Office of Management and Compliance Audits has completed the audits of 45 schools/centers. These include 25 that report to the North Region Office, ten that report to the Central Region Office, seven that report to the South Region Office; and one adult education center and two alternative education centers that report to the Office of Adult/Vocational, Alternative and Community Education within School Operations. For 34 of the 45 schools/centers reported herein, the scope of the audit was two fiscal years ended June 30, 2017. For the remaining 11 schools/centers, the scope of the audit was one fiscal year ended June 30, 2017. At 17 schools/centers, there was a change of Principal since the prior audit. The audits disclosed that 43 of the 45 schools/centers reported herein maintained their records in good order and in accordance with prescribed policies and procedures. The two schools/centers with audit findings and the affected areas are as follows:

Work Loc. No.

Name Of School/Center Principal’s Tenure

Region Office

Audit Scope

Change

Of Principal

Since Prior Audit

Prior Audit

Findings At

School/ Center

Current Audit Total

Findings Per

School/ Center

Findings Per Category

Internal Funds Receipting and

Depositing/ Safeguarding of

Collections

2581 1. Madie Ives Elementary1 Same Principal as in prior audit-no change. Finding under current (same) Principal. Audit requested by the Principal.

North 2015-2016 2016-2017 No No 1 1

(2016-2017)

3191 2. Ada Merritt K-8 Center Same Principal as in prior audit-no change. Finding under current (same) Principal.

Central 2015-2016 2016-2017 No No 1 1

(2016-2017)

TOTAL 2 2

As depicted in the table above, we noted certain deficiencies in the controls over the receipting, depositing and safeguarding of collections/deposits. The table also illustrates whether a change of Principal since the prior audit occurred; the tenure of the school administration under which the finding was assessed; the audit period (scope); whether the audit was the result of a request from the school administration; and whether findings were recurrent/consecutive. More specific details regarding prior/current findings, names of Principals and timeframes of their administrative assignments are provided on pages 24-33 of this report. A Summary Schedule of Audit Findings listing audit results of current and prior audit periods for all schools/centers in this report is presented on pages 24-27. Responses are included following the recommendations in the Findings and Recommendations section of this report (Pages 42-51); and in the Appendix Section in memorandum format (Pages 62-69).

1 Madie Ives Elementary became a K-8 Center effective for the 2017-2018 fiscal year. It was an elementary school during the audit period (2015-2016 and 2016-2017) reported herein.

2 Internal Audit Report Selected Schools/Centers

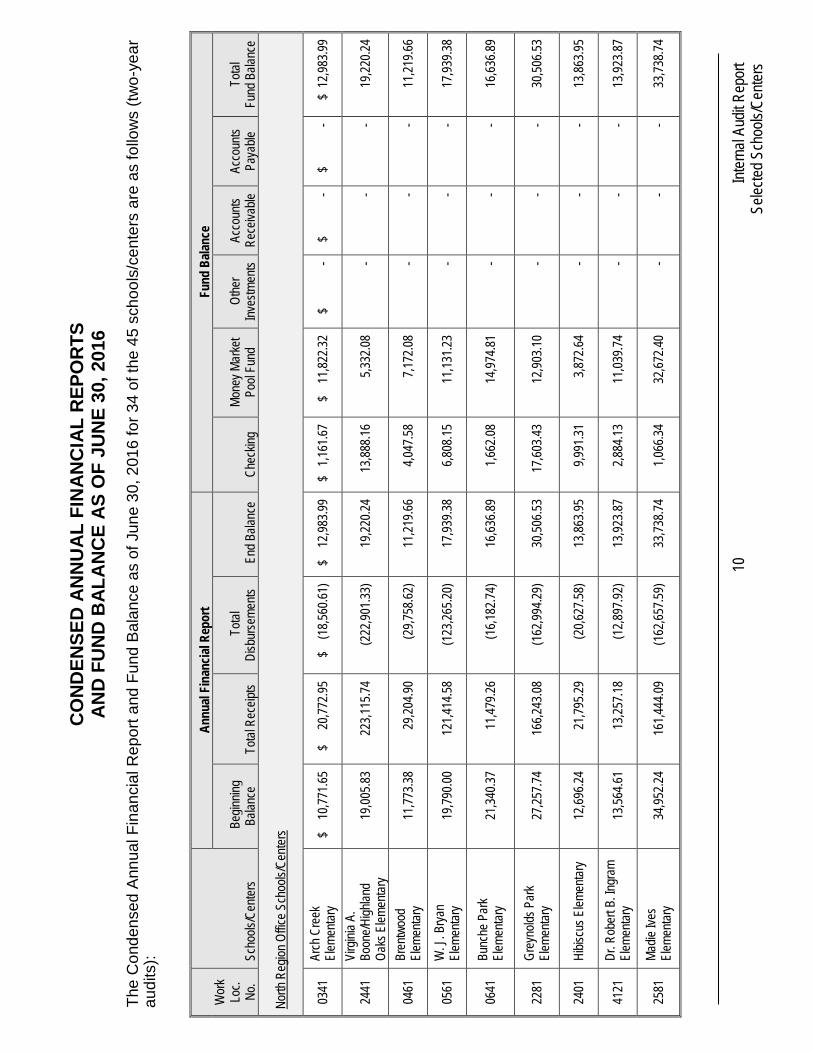

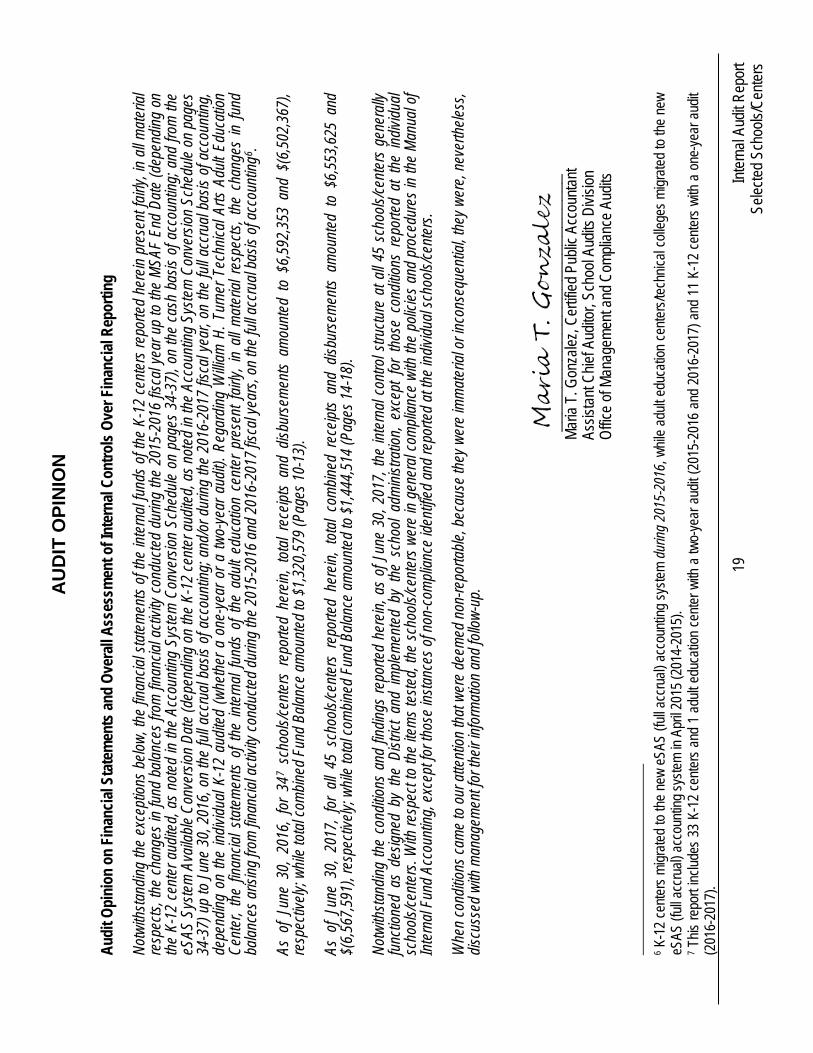

Notwithstanding the exceptions below, the financial statements of the internal funds of the K-12 centers reported herein present fairly, in all material respects, the changes in fund balances from financial activity conducted during the 2015-2016 fiscal year up to the MSAF End Date (depending on the K-12 center audited, as noted in the Accounting System Conversion Schedule on pages 34-37), on the cash basis of accounting; and from the eSAS System Available Conversion Date (depending on the K-12 center audited, as noted in the Accounting System Conversion Schedule on pages 34-37) up to June 30, 2016, on the full accrual basis of accounting; and/or during the 2016-2017 fiscal year, on the full accrual basis of accounting, depending on the individual K-12 audited (whether a one-year or a two-year audit). Regarding William H. Turner Technical Arts Adult Education Center, the financial statements of the internal funds of the adult education center present fairly, in all material respects, the changes in fund balances arising from financial activity conducted during the 2015-2016 and 2016-2017 fiscal years, on the full accrual basis of accounting2. As of June 30, 2016, for 343 schools/centers reported herein, total receipts and disbursements amounted to $6,592,353 and $(6,502,367), respectively; while total combined Fund Balance amounted to $1,320,579 (Pages 10-13). As of June 30, 2017, for all 45 schools/centers reported herein, total combined receipts and disbursements amounted to $6,553,625 and $(6,567,591), respectively; while total combined Fund Balance amounted to $1,444,514 (Pages 14-18). Notwithstanding the conditions and findings reported herein, as of June 30, 2017, the internal control structure at all 45 schools/centers generally functioned as designed by the District and implemented by the school administration, except for those conditions reported at the individual schools/centers. With respect to the items tested, the schools/centers were in general compliance with the policies and procedures in the Manual of Internal Fund Accounting, except for those instances of non-compliance identified and reported at the individual schools/centers. When conditions came to our attention that were deemed non-reportable, because they were immaterial or inconsequential, they were, nevertheless, discussed with management for their information and follow-up.

2 K-12 centers migrated to the new eSAS (full accrual) accounting system during 2015-2016, while adult education centers/technical colleges migrated to the new eSAS (full accrual) accounting system in April 2015 (2014-2015). 3 This report includes 33 K-12 centers and 1 adult education center with a two-year audit (2015-2016 and 2016-2017) and 11 K-12 centers with a one-year audit (2016-2017).

3 Internal Audit Report Selected Schools/Centers

INTERNAL FUNDS Implementation Of New Accounting System At K-12 Centers In March 2016, the District migrated the bookkeeping of the internal funds of all K-12 centers from a legacy bookkeeping system (referred to as the MSAF system) to a web-based full accrual accounting system. The new system is named the Electronic Student Accounting System by the District (otherwise referred to as the eSAS system)4. The deployment to the new system was accomplished in tiers, where K-12 schools/centers were segregated into four different groups (the first being the pilot group followed by three cohorts). Each group migrated into the new bookkeeping system according to the following schedule under the direction and guidance of various district departments (i.e., Accounting, Treasury Management, Information Technology Services (ITS)), and with technical assistance from the software vendor. Regarding 33 of the 34 schools/centers in this report with two-year audits, the summarized group configuration and overall deployment schedule was as follows:

Group Designation

MSAF (Legacy)

System End Date

eSAS System Available For Conversion

No. Of K-12 Centers In This Report Phasing Into

eSAS During 2015-2016 Pilot 9/29/2015 10/1/2015 0

Cohort 1 11/24/2015 12/1/2015 6 Cohort 2 1/27/2016 2/1/2016 17 Cohort 3 2/24/2016 3/1/2016 10

Total K-12 Centers 33 Consequently, the schools in this report converted from the cash basis system of accounting to the new full accrual system on different dates, and these dates are reflected in the Opinion to the financial statements during the year of conversion (2015-2016). Please, refer to Accounting System Conversion Schedule on pages 34-37 for dates specific to each K-12 center reported herein. Implementation Of New Accounting System At Adult Ed. Centers/Technical Colleges The internal funds of adult and community education centers/technical colleges were accounted for on the cash basis of accounting until March 31, 2015. In early April 2015, the District migrated the bookkeeping of the internal funds of these centers from a legacy (bookkeeping) system to a web-based full accrual accounting system. Consequently, the legacy accounting system at William H. Turner Technical Arts Adult Education Center (the only adult education center included in this report) was phased out towards the end of 2014-2015. Therefore, the financials corresponding to the two-fiscal year audit reported herein ended June 30, 2017 are fully accounted for under the new eSAS accounting system. 4 Please, refer to Background Section on pages 54-56 for additional details.

4 Internal Audit Report Selected Schools/Centers

Internal Funds-Summary Of Audit Results Internal funds records and procedures were reviewed at all 45 schools/centers. At 43 of the 45 schools/centers, we determined there was general compliance with the procedures established in the Manual of Internal Fund Accounting. At the following two schools/centers we found that: • During April 2017, the Principal of Madie Ives Elementary contacted our office

regarding cash collections that were missing from the Treasurer’s Office and requested an audit of the school records. The funds in question represented student collections for an upcoming field trip. Although our audit confirmed a monetary shortfall of approximately $1,000, it could not identify the party responsible for the misappropriation of funds because of the conditions surrounding the collection and custody of these funds, and the lack of documentary evidence over these collections. However, the audit concluded that the former Treasurer was negligent not only in the performance of her duties, but also in the improper handling/safeguarding of these funds, which led to their loss. We reported the results of our review to M-DCPS School Police and the Office of Professional Standards for their consideration. The former Treasurer is on board-approved leave since the time of the incident and the case is ongoing pending her return to the District. A new Treasurer has been hired at this school (Pages 42-47).

• During November 2016, the Principal of Ada Merritt K-8 Center reported an incident

of missing funds that was initially investigated by M-DCPS School Police. According to the allegation, the Treasurer left several deposit bags on her desk while stepping out of the school for lunch; and one of the bags said to contain approximately $1,770 cash was discovered missing upon her return. We conducted an audit subsequent to the MDCPS Police investigation. Neither the police investigation nor our audit could identify the individual(s) responsible for the misappropriation; however, both concluded that the Treasurer failed to exercise due diligence in the safeguarding of collections. Consequent to the substantiation of the allegation in the incident report, the School Board approved the District’s recommended disciplinary action to suspend the employee for two days’ work without pay. In addition, the employee is in the process of restituting the funds (Pages 48-51).

5 Internal Audit Report Selected Schools/Centers

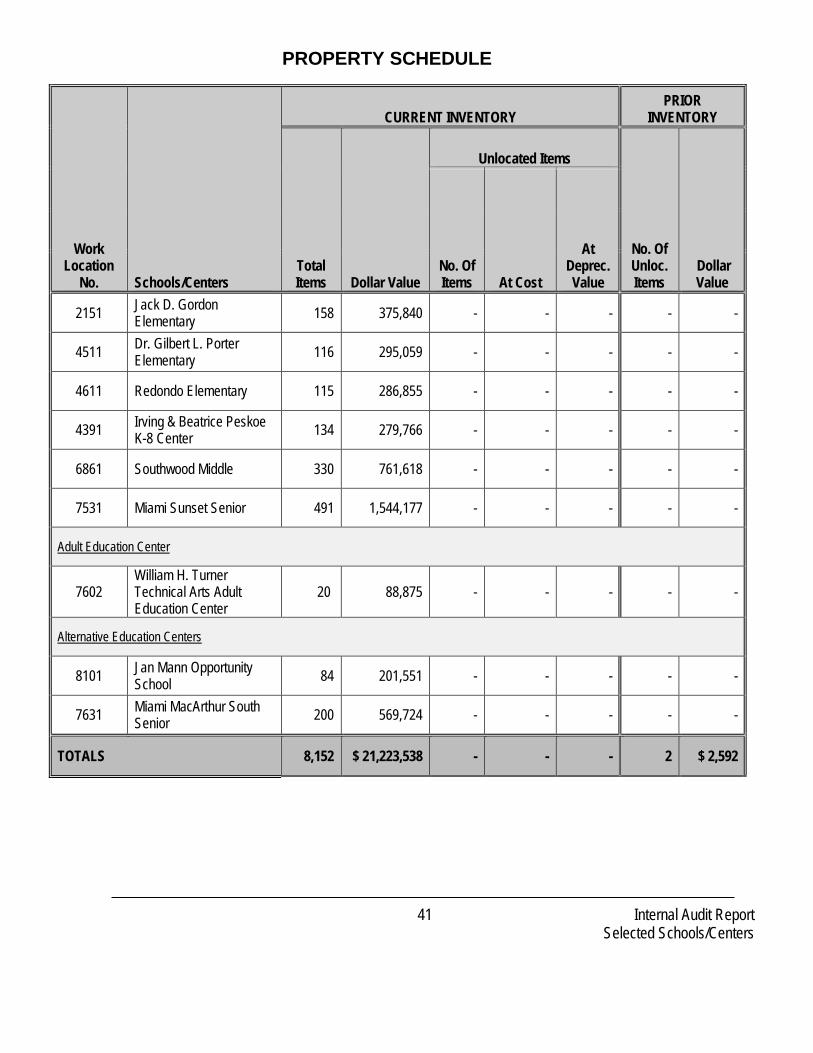

PROPERTY The results of physical inventories of property items with an individual cost of $1,000 or more are reported for all 45 schools/centers reported herein. At these 45 schools/centers, Property Audits staff inventoried approximately 8,200 equipment items with a total approximate cost of $21.2 million. All inventories proved satisfactory. Property inventories also include the review of property losses reported by the schools/centers through the Plant Security Report process. However, none of the schools/centers reported any losses through Plant Security Reports (Pages 38-41). PAYROLL We reviewed payroll records and procedures at the following four schools/centers. The payroll audit at Madie Ives Elementary was performed due to a concern raised by the school administration during the audit visit. The audits at Brentwood, Miami Sunset Senior and Peskoe K-8 were corollary to the audits of Title I Program funds. In addition, at Peskoe K-8, we followed up on prior audit findings in the payroll area. The scope of the payroll audits varied, depending on the conditions being reviewed/followed up, as previously noted.

Work Location

No.

Schools/Centers

Region

Pay Periods Reviewed

Corresponding To

0461 Brentwood Elementary North 2015-2016

2581 Madie Ives Elementary North 2016-2017

4391 Irving & Beatrice Peskoe K-8 Center South 2015-2016 and 2016-2017

7531 Miami Sunset Senior South 2015-2016 We found that at all four schools/centers, there was general compliance with the Payroll Processing Procedures Manual.

6 Internal Audit Report Selected Schools/Centers

PURCHASING CREDIT CARD (P-CARD) PROGRAM We reviewed the P-Card Program’s procedures and records at the following two schools/centers. At Madie Ives Elementary, our review resulted from a concern shared by the Principal during the audit. At Miami Norland Senior, we performed the review as a follow-up to a prior audit finding. The scope of the P-Card audits covered P-Card monthly reconciliations from the 2016-2017 fiscal year.

Work Location

No.

Schools/Centers

Region

P-Card Reconciliations Reviewed

Corresponding To

2581 Madie Ives Elementary North 2016-2017

7381 Miami Norland Senior North 2016-2017

Both schools/centers reviewed were generally compliant with the procedures and guidelines established in the Purchasing Card Program Policies and Procedures Manual. TITLE I PROGRAM EXPENDITURES AND PROCEDURES A review of Title I Program expenditures and procedures corresponding to the 2015-2016 fiscal year was conducted at three schools/centers. The following table summarizes the schools/centers reviewed:

Work Location

No. Schools/Centers Region Audit Period Total

Expenditures

0461 Brentwood Elementary North 2015-2016 $ 762,951

4391 Irving & Beatrice Peskoe K-8 Center South 2015-2016 211,410

7531 Miami Sunset Senior South 2015-2016 182,529

Total Title I Program Expenditures $ 1,156,890

At these three schools/centers, aggregate expenditures incurred under various Title I programs amounted to approximately $1.2 million. All three schools/centers reviewed were generally compliant with the procedures and guidelines established in the Title I Administration Handbook.

7 Internal Audit Report Selected Schools/Centers

FULL TIME-EQUIVALENT (FTE) FUNDING The following 11 schools/centers were selected for these audits:

Work Location

No. Schools/Centers Region Survey Period

(SP) FTE Funding

0341 Arch Creek Elementary North 2016-2017 SP 3 $ 1,549,639

0561 W. J. Bryan Elementary North 2016-2017 SP 3 1,900,912

2281 Greynolds Park Elementary North 2016-2017 SP 3 2,043,905

3661 Natural Bridge Elementary North 2016-2017 SP 3 1,849,315

4281 Palm Springs North Elementary North 2016-2017 SP 3 2,832,406

3281 Miami Lakes K-8 Center North 2016-2017 SP 3 3,685,081

5141 Hubert O. Sibley K-8 Academy North 2016-2017 SP 3 2,095,687

6751 Hialeah Gardens Middle North 2016-2017 SP 3 4,287,998

7381 Miami Norland Senior North 2016-2017 SP 3 4,559,130

3191 Ada Merritt K-8 Center Central 2016-2017 SP 3 2,140,497

7531 Miami Sunset Senior South 2016-2017 SP 3 3,814,640

Total FTE Funding $ 30,759,210

The total FTE funding amounted to approximately $30.8 million for the 11 schools/centers combined. FTE records reviewed corresponded to the 2016-2017 Survey Period 3 (February 2017) as noted in the table above. Our FTE reviews disclosed that all 11 schools/centers were generally compliant with District policy and FTE records reviewed were in good order.

8 Internal Audit Report Selected Schools/Centers

DATA SECURITY We reviewed the report titled “Authorized Applications for Employees by Locations Report” at the following two schools/centers. At Miami Norland Senior, our review was the result of an audit follow-up to conditions cited in the prior audit of the individual school/center. At Brentwood Elementary, our review of the report was corollary to the Title I Program audit conducted at the school.

Work Location

No. Schools/Centers Region

Data Security Reports Reviewed

Corresponding To

0461 Brentwood Elementary North 2016-2017

7381 Miami Norland Senior North 2017-2018

Our review disclosed that both schools/centers generally complied with the review of the report and with the requirements for granting staff’s access to system applications. At both schools, minor issues regarding staff members’ access to certain system applications were discussed with the school administration for their information and corrective follow-up.

9 Internal Audit Report Selected Schools/Centers

AUDIT OPINION The following tables summarize total receipts, disbursements and Fund Balance as of June 30, 2016 and/or June 30, 2017, for the 45 schools/centers included herein, depending on the year(s) audited for each individual school/center5. It also provides the audit opinion regarding the schools/centers’ financial statements:

5 This report includes a total of 45 schools/centers, of which 34 underwent a two-year audit ended June 30, 2017, and 11 underwent a one-year audit ended June 30, 2017.

CO

ND

ENSE

D A

NN

UAL

FIN

ANC

IAL

REP

OR

TS

AND

FU

ND

BAL

AN

CE

AS O

F JU

NE

30, 2

016

10

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

The

Con

dens

ed A

nnua

l Fin

anci

al R

epor

t and

Fun

d Ba

lanc

e as

of J

une

30, 2

016

for 3

4 of

the

45 s

choo

ls/c

ente

rs a

re a

s fo

llow

s (tw

o-ye

ar

audi

ts):

Wor

k Lo

c. No

. Sc

hools

/Cen

ters

Annu

al Fi

nanc

ial R

epor

t Fu

nd B

alanc

e

Beg

inning

Ba

lance

To

tal R

eceip

ts

Tota

l Di

sbur

seme

nts

End

Bala

nce

Ch

eckin

g Mo

ney M

arke

t Po

ol Fu

nd

Othe

r Inv

estm

ents

Acco

unts

Rece

ivable

Ac

coun

ts Pa

yable

To

tal

Fund

Bala

nce

North

Reg

ion O

ffice

Scho

ols/C

enter

s

0341

Ar

ch C

reek

El

emen

tary

$ 1

0,771

.65

$

20,77

2.95

$ (

18,56

0.61)

$

12,9

83.99

$

1,16

1.67

$ 1

1,822

.32

$

-

$

-

$

-

$ 12

,983.9

9

2441

Vi

rgini

a A.

Boon

e/High

land

Oaks

Elem

entar

y 1

9,005

.83

223

,115.7

4 (2

22,90

1.33)

19

,220.2

4

13,88

8.16

5,332

.08

-

-

-

1

9,220

.24

0461

Br

entw

ood

Elem

entar

y 1

1,773

.38

29

,204.9

0 (

29,75

8.62)

11,2

19.66

4,04

7.58

7,172

.08

-

-

-

1

1,219

.66

0561

W

. J. B

ryan

Elem

entar

y 1

9,790

.00

121

,414.5

8 (1

23,26

5.20)

17,9

39.38

6,80

8.15

1

1,131

.23

-

-

-

1

7,939

.38

0641

Bu

nche

Par

k El

emen

tary

21,3

40.37

11,47

9.26

(16

,182.7

4)

1

6,636

.89

1

,662.0

8

14,9

74.81

-

-

-

16,6

36.89

2281

Gr

eyno

lds P

ark

Elem

entar

y 2

7,257

.74

166

,243.0

8 (1

62,99

4.29)

30,5

06.53

17,60

3.43

1

2,903

.10

-

-

-

3

0,506

.53

2401

Hi

biscu

s Elem

entar

y 1

2,696

.24

21

,795.2

9 (

20,62

7.58)

13,8

63.95

9,99

1.31

3,872

.64

-

-

-

1

3,863

.95

4121

Dr

. Rob

ert B

. Ingr

am

Elem

entar

y 1

3,564

.61

13

,257.1

8 (

12,89

7.92)

13,9

23.87

2,88

4.13

1

1,039

.74

-

-

-

1

3,923

.87

2581

Ma

die Iv

es

Elem

entar

y 3

4,952

.24

161

,444.0

9 (1

62,65

7.59)

33,7

38.74

1,06

6.34

3

2,672

.40

-

-

-

3

3,738

.74

CO

ND

ENSE

D A

NN

UAL

FIN

ANC

IAL

REP

OR

TS

AND

FU

ND

BAL

AN

CE

AS O

F JU

NE

30, 2

016

11

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

Wor

k Lo

c. No

. Sc

hools

/Cen

ters

Annu

al Fi

nanc

ial R

epor

t Fu

nd B

alanc

e

Beg

inning

Ba

lance

To

tal R

eceip

ts

Tota

l Di

sbur

seme

nts

End

Bala

nce

Ch

eckin

g Mo

ney M

arke

t Po

ol Fu

nd

Othe

r Inv

estm

ents

Acco

unts

Rece

ivable

Ac

coun

ts Pa

yable

To

tal

Fund

Bala

nce

3661

Na

tural

Bridg

e El

emen

tary

11,0

17.19

38,38

2.65

(35

,453.8

5)

1

3,945

.99

12

,044.2

6

1,9

01.73

-

-

-

1

3,945

.99

5131

No

rth D

ade C

enter

Fo

r Mod

ern

Lang

uage

s El

emen

tary

26,7

14.75

45,37

0.33

(53

,178.5

3)

1

8,906

.55

9

,977.3

8

8,9

29.17

-

-

-

18,9

06.55

4021

Oa

k Gro

ve

Elem

entar

y

9,17

6.51

61

,037.1

1 (

61,06

2.54)

9,

151.0

8

9,15

1.08

-

-

-

-

9,151

.08

4261

Pa

lm S

pring

s El

emen

tary

17,7

16.10

37,40

6.24

(35

,789.6

5)

1

9,332

.69

15

,106.4

5

4,2

26.24

-

-

-

19,3

32.69

4281

Pa

lm S

pring

s Nor

th El

emen

tary

35,4

07.74

4

63,69

8.79

(463

,929.4

4)

3

5,177

.09

12

,696.1

0

22,4

80.99

-

-

-

35,1

77.09

4341

Pa

rkway

Elem

entar

y

4,03

3.19

20

,705.5

6 (

20,32

5.78)

4,

412.9

7

3,27

6.33

1,136

.64

-

-

-

4,412

.97

4541

Ra

inbow

Par

k El

emen

tary

9,

549.0

1

38,23

1.73

(39

,111.2

4)

8,66

9.50

5

,691.2

7

2,9

78.23

-

-

-

8,6

69.50

2371

W

est H

ialea

h Ga

rden

s Elem

entar

y 2

5,857

.22

432

,621.0

4 (4

31,08

2.63)

27,3

95.63

25,85

3.14

1,542

.49

-

-

-

2

7,395

.63

0091

Bo

b Gra

ham

Educ

ation

Cen

ter

29,5

09.07

5

90,65

6.11

(588

,855.3

8)

3

1,309

.80

22

,057.3

8

9,2

52.42

-

-

-

31,3

09.80

3281

Mi

ami L

akes

K-8

Ce

nter

26,9

96.60

1

61,99

2.81

(172

,526.3

0)

1

6,463

.11

12

,916.1

6

3,5

46.95

-

-

-

16,4

63.11

5141

Hu

bert

O. S

ibley

K-8

Ac

adem

y 1

2,735

.84

48

,558.4

3 (

47,44

5.55)

13,8

48.72

3,99

7.36

9,851

.36

-

-

-

1

3,848

.72

6023

An

dove

r Midd

le 2

5,253

.28

72

,385.9

6 (

72,16

6.08)

25,4

73.16

10,75

6.92

1

4,716

.24

-

-

-

2

5,473

.16

CO

ND

ENSE

D A

NN

UAL

FIN

ANC

IAL

REP

OR

TS

AND

FU

ND

BAL

AN

CE

AS O

F JU

NE

30, 2

016

12

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

Wor

k Lo

c. No

. Sc

hools

/Cen

ters

Annu

al Fi

nanc

ial R

epor

t Fu

nd B

alanc

e

Beg

inning

Ba

lance

To

tal R

eceip

ts

Tota

l Di

sbur

seme

nts

End

Bala

nce

Ch

eckin

g Mo

ney M

arke

t Po

ol Fu

nd

Othe

r Inv

estm

ents

Acco

unts

Rece

ivable

Ac

coun

ts Pa

yable

To

tal

Fund

Bala

nce

6751

Hi

aleah

Gar

dens

Mi

ddle

37,6

63.55

2

21,49

6.09

(221

,190.7

4)

3

7,968

.90

7

,304.5

1

30,6

64.39

-

-

-

37,9

68.90

7381

Mi

ami N

orlan

d Sen

ior

98,4

95.79

3

72,71

1.24

(364

,032.9

7)

10

7,174

.06

9

,491.1

9

97,6

82.87

-

-

-

107,1

74.06

Centr

al Re

gion O

ffice

Scho

ols/C

enter

s

0122

Dr

. Rola

ndo

Espin

osa

K-8 C

enter

5

6,239

.54

437

,917.0

5 (4

41,53

3.78)

52,6

22.81

26,08

9.21

2

6,533

.60

-

-

-

52,6

22.81

3191

Ad

a Mer

ritt K

-8

Cente

r 3

6,658

.80

467

,456.1

2 (4

65,45

8.66)

38,6

56.26

26,52

1.93

1

2,134

.33

-

-

-

38,6

56.26

7601

W

illiam

H. T

urne

r Te

chnic

al Ar

ts Hi

gh

Scho

ol 11

4,018

.25

354

,520.5

4 (3

49,53

6.35)

119,0

02.44

70,73

9.84

4

8,262

.60

-

-

-

119,0

02.44

South

Reg

ion O

ffice S

choo

ls/Ce

nter

s

0211

Dr

. Man

uel C

. Ba

rreiro

Elem

entar

y 1

6,033

.42

277

,467.3

6 (2

72,51

2.36)

20,9

88.42

19,94

5.78

1,042

.64

-

-

-

2

0,988

.42

2151

Ja

ck D

. Gor

don

Elem

entar

y 2

4,920

.75

501

,763.4

7 (4

72,16

7.89)

54,5

16.33

2

9,471

.88

2

5,044

.45

-

-

-

54,5

16.33

4511

Dr

. Gilb

ert L

. Por

ter

Elem

entar

y

9,28

7.98

295

,830.0

1 (2

84,00

0.52)

21,1

17.47

1

4,429

.98

6,687

.49

-

-

-

2

1,117

.47

4391

Irv

ing &

Bea

trice

Pesk

oe K

-8 C

enter

1

1,240

.90

22

,477.9

1 (

19,99

1.31)

13,7

27.50

8,71

1.79

5,015

.71

-

-

-

1

3,727

.50

6861

So

uthwo

od M

iddle

118,5

23.26

2

25,29

0.70

(245

,462.3

6)

9

8,351

.60

7

,141.8

3

91,2

09.77

-

-

-

98,3

51.60

7531

Mi

ami S

unse

t Sen

ior

188,6

16.75

4

26,75

2.94

(409

,295.3

4)

20

6,074

.35

21

,401.7

1

184,6

72.64

-

-

-

206,0

74.35

CO

ND

ENSE

D A

NN

UAL

FIN

ANC

IAL

REP

OR

TS

AND

FU

ND

BAL

AN

CE

AS O

F JU

NE

30, 2

016

13

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

Wor

k Lo

c. No

. Sc

hools

/Cen

ters

Annu

al Fi

nanc

ial R

epor

t Fu

nd B

alanc

e

Beg

inning

Ba

lance

To

tal R

eceip

ts

Tota

l Di

sbur

seme

nts

End

Bala

nce

Ch

eckin

g Mo

ney M

arke

t Po

ol Fu

nd

Othe

r Inv

estm

ents

Acco

unts

Rece

ivable

Ac

coun

ts Pa

yable

To

tal

Fund

Bala

nce

Adult

Edu

catio

n Cen

ter

7602

W

illiam

H. T

urne

r Te

chnic

al Ar

ts Ad

ult

Educ

ation

Cen

ter

94,5

00.64

2

05,07

7.08

(159

,410.6

8)

14

0,167

.04

69

,583.3

9

23,5

02.53

-

4

7,081

.12

-

14

0,167

.04

Alter

nativ

e Edu

catio

n Cen

ter

8101

Ja

n Man

n Op

portu

nity S

choo

l 1

9,274

.75

3

,818.7

5

(7,00

1.20)

16,0

92.30

14,07

3.97

2,018

.33

-

-

-

16,0

92.30

TOTA

LS

$1,23

0,592

.94

$6,59

2,353

.09

$(6,5

02,36

7.01)

$1

,320,5

79.02

$5

27,54

3.69

$745

,954.2

1 $

-

$47,0

81.12

$

-

$1,32

0,579

.02

CO

ND

ENSE

D A

NN

UAL

FIN

ANC

IAL

REP

OR

TS

AND

FU

ND

BAL

AN

CE

AS O

F JU

NE

30, 2

017

14

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

The

Con

dens

ed A

nnua

l Fin

anci

al R

epor

ts a

nd F

und

Bala

nce

as o

f Jun

e 30

, 201

7 fo

r the

45

scho

ols/

cent

ers

repo

rted

here

in a

re a

s fo

llow

s (3

4 tw

o-ye

ar a

udits

and

11

one-

year

aud

its):

Wor

k Lo

c. No

. Sc

hools

/Cen

ters

Annu

al Fi

nanc

ial R

epor

t Fu

nd B

alanc

e

Beg

inning

Ba

lance

To

tal R

eceip

ts

Tota

l Di

sbur

seme

nts

End

Bala

nce

Ch

eckin

g Mo

ney M

arke

t Po

ol Fu

nd

Othe

r Inv

estm

ents

Acco

unts

Rece

ivable

Ac

coun

ts Pa

yable

To

tal

Fund

Bala

nce

North

Reg

ion O

ffice

Scho

ols/C

enter

s

0341

Ar

ch C

reek

El

emen

tary

$ 1

2,983

.99

$ 1

6,331

.05

$

(15,0

98.57

) $

14,2

16.47

$

4,80

7.68

$

9,408

.79

-

-

$

-

$

14,2

16.47

2441

Vi

rgini

a A.

Boon

e/High

land

Oaks

Elem

entar

y 1

9,220

.24

222

,324.6

6

(22

7,326

.84)

14

,218.0

6

8,83

3.43

5,

384.6

3 -

-

-

14,2

18.06

0461

Br

entw

ood

Elem

entar

y 1

1,219

.66

25

,339.8

1

(2

3,183

.07)

13

,376.4

0

6,13

3.62

7,

242.7

8 -

-

-

13,3

76.40

0561

W

. J. B

ryan

Elem

entar

y 1

7,939

.38

123

,416.0

1

(12

4,287

.48)

17

,067.9

1

5,82

6.95

11,2

40.96

-

-

-

17,0

67.91

0641

Bu

nche

Par

k El

emen

tary

16,6

36.89

8,05

8.86

(9,3

06.37

)

15,38

9.38

4,

300.1

4 1

1,089

.24

-

-

-

1

5,389

.38

2281

Gr

eyno

lds P

ark

Elem

entar

y 3

0,506

.53

150

,441.2

5

(15

5,567

.09)

25

,380.6

9 1

2,350

.40

13,0

30.29

-

-

-

25,3

80.69

2401

Hi

biscu

s Elem

entar

y 1

3,863

.95

30

,126.6

0

(3

1,070

.38)

12

,920.1

7

9,00

6.91

3,

913.2

6 -

-

-

12,9

20.17

4121

Dr

. Rob

ert B

. Ingr

am

Elem

entar

y 1

3,923

.87

9

,707.3

5

(1

0,733

.09)

12

,898.1

3

1,76

0.62

11,1

37.51

-

-

-

12,8

98.13

2581

Ma

die Iv

es

Elem

entar

y 3

3,738

.74

199

,288.6

2

(20

3,025

.00)

30

,002.3

6

3,02

4.80

26,9

77.56

-

-

-

30,0

02.36

CO

ND

ENSE

D A

NN

UAL

FIN

ANC

IAL

REP

OR

TS

AND

FU

ND

BAL

AN

CE

AS O

F JU

NE

30, 2

017

15

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

Wor

k Lo

c. No

. Sc

hools

/Cen

ters

Annu

al Fi

nanc

ial R

epor

t Fu

nd B

alanc

e

Beg

inning

Ba

lance

To

tal R

eceip

ts

Tota

l Di

sbur

seme

nts

End

Bala

nce

Ch

eckin

g Mo

ney M

arke

t Po

ol Fu

nd

Othe

r Inv

estm

ents

Acco

unts

Rece

ivable

Ac

coun

ts Pa

yable

To

tal

Fund

Bala

nce

3661

Na

tural

Bridg

e El

emen

tary

13,9

45.99

32,92

2.47

(28,4

16.28

)

18,45

2.18

16,5

31.70

1,92

0.48

-

-

-

1

8,452

.18

5131

No

rth D

ade C

enter

Fo

r Mod

ern

Lang

uage

s El

emen

tary

18,9

06.55

32,15

1.32

(36,1

53.39

)

14,90

4.48

5,

887.3

0

9,01

7.18

-

-

-

1

4,904

.48

3901

No

rth H

ialea

h El

emen

tary

13,5

26.34

26,19

6.91

(25,9

74.84

)

13,74

8.41

7,

898.9

0

5,84

9.51

-

-

-

1

3,748

.41

4021

Oa

k Gro

ve

Elem

entar

y

9,15

1.08

56

,829.9

3

(5

5,711

.78)

10

,269.2

3 1

0,269

.23

- -

-

-

10,2

69.23

4261

Pa

lm S

pring

s El

emen

tary

19,3

32.69

41,85

4.18

(42,3

53.23

)

18,83

3.64

14,5

65.75

4,26

7.89

-

-

-

1

8,833

.64

4281

Pa

lm S

pring

s Nor

th El

emen

tary

35,1

77.09

4

67,25

6.19

(

461,4

09.00

)

41,02

4.28

18,3

21.70

2

2,702

.58

-

-

-

4

1,024

.28

4341

Pa

rkway

Elem

entar

y

4,41

2.97

26

,027.2

7

(2

5,760

.31)

4

,679.9

3

3,53

2.08

1,

147.8

5 -

-

-

4,

679.9

3

4541

Ra

inbow

Par

k El

emen

tary

8,

669.5

0

19,32

6.70

(20,6

55.06

)

7,34

1.14

4,

333.5

5

3,00

7.59

-

-

-

7,34

1.14

2371

W

est H

ialea

h Ga

rden

s Elem

entar

y 2

7,395

.63

409

,989.1

3

(40

8,067

.09)

29

,317.6

7 2

4,759

.98

4,

557.6

9 -

-

-

29,3

17.67

0091

Bo

b Gra

ham

Educ

ation

Cen

ter

31,3

09.80

5

67,07

4.50

(

565,5

97.71

)

32,78

6.59

23,4

42.99

9,34

3.60

-

-

-

3

2,786

.59

3281

Mi

ami L

akes

K-8

Ce

nter

16,4

63.11

1

69,11

3.87

(

159,2

89.21

)

26,28

7.77

22,7

05.86

3,58

1.91

-

-

-

2

6,287

.77

5141

Hu

bert

O. S

ibley

K-8

Ac

adem

y 1

3,848

.72

35

,581.2

5

(3

4,275

.87)

15

,154.1

0

5,22

8.22

9,

925.8

8 -

-

-

15,1

54.10

CO

ND

ENSE

D A

NN

UAL

FIN

ANC

IAL

REP

OR

TS

AND

FU

ND

BAL

AN

CE

AS O

F JU

NE

30, 2

017

16

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

Wor

k Lo

c. No

. Sc

hools

/Cen

ters

Annu

al Fi

nanc

ial R

epor

t Fu

nd B

alanc

e

Beg

inning

Ba

lance

To

tal R

eceip

ts

Tota

l Di

sbur

seme

nts

End

Bala

nce

Ch

eckin

g Mo

ney M

arke

t Po

ol Fu

nd

Othe

r Inv

estm

ents

Acco

unts

Rece

ivable

Ac

coun

ts Pa

yable

To

tal

Fund

Bala

nce

6023

An

dove

r Midd

le 2

5,473

.16

66

,788.2

6

(5

8,243

.83)

34

,017.5

9 1

9,156

.29

14,8

61.30

-

-

-

34,0

17.59

6751

Hi

aleah

Gar

dens

Mi

ddle

37,9

68.90

1

91,28

8.34

(

188,9

16.50

)

40,34

0.74

9,

374.1

0 3

0,966

.64

-

-

-

4

0,340

.74

7381

Mi

ami N

orlan

d Sen

ior

107,1

74.06

3

01,27

0.46

(

294,3

82.93

) 1

14,06

1.59

15,2

70.72

9

8,790

.87

-

-

-

11

4,061

.59

8151

Ro

bert

Renic

k Ed

ucati

onal

Cente

r 1

3,775

.95

3

,964.7

4

(

4,117

.94)

13

,622.7

5

6,70

8.92

6,

913.8

3 -

-

-

13,6

22.75

Centr

al Re

gion O

ffice

Scho

ols/C

enter

s

0401

Va

n E. B

lanton

El

emen

tary

15,9

52.17

11,56

5.42

(12,5

54.01

)

14,96

3.58

1,

191.9

1 1

3,771

.67

-

-

-

1

4,963

.58

0721

Ge

orge

Was

hingto

n Ca

rver E

lemen

tary

21,8

04.44

78,86

0.30

(78,7

33.75

)

21,93

0.99

5,

476.2

2 1

6,454

.77

-

-

-

2

1,930

.99

1641

Em

erso

n Elem

entar

y 1

2,262

.94

148

,219.1

6

(14

7,890

.19)

12

,591.9

1

5,31

2.36

7,

279.5

5 -

-

-

12,5

91.91

2981

Lib

erty

City

Elem

entar

y

5,86

6.47

20

,294.5

3

(1

5,538

.90)

10

,622.1

0

8,68

8.67

1,

933.4

3 -

-

-

10,6

22.10

4841

Sa

nta C

lara

Elem

entar

y

5,78

0.33

8

,592.7

9

(

8,231

.93)

6

,141.1

9

1,81

7.09

4,

324.1

0 -

-

-

6,

141.1

9

1441

Pa

ul La

uren

ce

Dunb

ar K

-8 C

enter

1

3,233

.80

11

,215.8

4

(1

1,567

.93)

12

,881.7

1

3,36

4.76

9,

516.9

5 -

-

-

12,8

81.71

0122

Dr

. Rola

ndo

Espin

osa

K-8 C

enter

5

2,622

.81

298

,843.0

9

(30

5,752

.41)

45

,713.4

9 1

8,901

.60

26,8

11.89

-

-

-

45,7

13.49

3191

Ad

a Mer

ritt K

-8

Cente

r 3

8,656

.26

510

,277.1

9

(50

5,727

.41)

43

,206.0

4 3

0,947

.00

12,2

59.04

-

-

-

43,2

06.04

CO

ND

ENSE

D A

NN

UAL

FIN

ANC

IAL

REP

OR

TS

AND

FU

ND

BAL

AN

CE

AS O

F JU

NE

30, 2

017

17

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

Wor

k Lo

c. No

. Sc

hools

/Cen

ters

Annu

al Fi

nanc

ial R

epor

t Fu

nd B

alanc

e

Beg

inning

Ba

lance

To

tal R

eceip

ts

Tota

l Di

sbur

seme

nts

End

Bala

nce

Ch

eckin

g Mo

ney M

arke

t Po

ol Fu

nd

Othe

r Inv

estm

ents

Acco

unts

Rece

ivable

Ac

coun

ts Pa

yable

To

tal

Fund

Bala

nce

7005

iTe

ch @

Tho

mas A

. Ed

ison

Educ

ation

al Ce

nter

9,

177.4

5

10,21

0.44

(9,3

57.88

)

10,03

0.01

5,

984.7

5

4,04

5.26

-

-

-

1

0,030

.01

7601

W

illiam

H. T

urne

r Te

chnic

al Ar

ts Hi

gh

Scho

ol 11

9,002

.44

403

,991.8

6

(41

1,745

.93)

111

,248.3

7 6

2,510

.03

48,7

38.34

-

-

-

111,2

48.37

South

Reg

ion O

ffice S

choo

ls/Ce

nter

s

0211

Dr

. Man

uel C

. Ba

rreiro

Elem

entar

y 2

0,988

.42

212

,670.7

0

(21

3,204

.08)

20

,455.0

4 1

9,402

.13

1,

052.9

1 -

-

-

20,4

55.04

2151

Ja

ck D

. Gor

don

Elem

entar

y 5

4,516

.33

409

,096.5

8

(43

1,641

.56)

31

,971.3

5

6,68

0.04

25,2

91.31

-

-

-

31,9

71.35

4511

Dr

. Gilb

ert L

. Por

ter

Elem

entar

y 2

1,117

.47

263

,316.7

8

(26

6,787

.74)

17

,646.5

1 1

0,893

.11

6,

753.4

0 -

-

-

17,6

46.51

4611

Re

dond

o Elem

entar

y 1

5,055

.08

43

,347.5

3

(4

3,073

.93)

15

,328.6

8

3,80

0.47

11,5

28.21

-

-

-

15,3

28.68

4391

Irv

ing &

Bea

trice

Pesk

oe K

-8 C

enter

1

3,727

.50

21

,209.4

8

(1

7,128

.09)

17

,808.8

9 1

2,743

.73

5,

065.1

6 -

-

-

17,8

08.89

6861

So

uthwo

od M

iddle

98,3

51.60

2

59,80

4.48

(

264,0

26.37

)

94,12

9.71

2,

020.8

7 9

2,108

.84

-

-

-

9

4,129

.71

7531

Mi

ami S

unse

t Sen

ior

206,0

74.35

4

20,01

7.53

(

398,0

96.34

) 2

27,99

5.54

41,4

24.74

186,5

70.80

-

-

-

227,9

95.54

Adult

Edu

catio

n Cen

ter

7602

W

illiam

H. T

urne

r Te

chnic

al Ar

ts Ad

ult

Educ

ation

Cen

ter

140,1

67.04

1

74,72

5.94

(

201,6

42.51

) 1

13,25

0.47

63,1

63.99

23,7

34.19

-

26

,352.2

9

-

113,2

50.47

CO

ND

ENSE

D A

NN

UAL

FIN

ANC

IAL

REP

OR

TS

AND

FU

ND

BAL

AN

CE

AS O

F JU

NE

30, 2

017

18

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

Wor

k Lo

c. No

. Sc

hools

/Cen

ters

Annu

al Fi

nanc

ial R

epor

t Fu

nd B

alanc

e

Beg

inning

Ba

lance

To

tal R

eceip

ts

Tota

l Di

sbur

seme

nts

End

Bala

nce

Ch

eckin

g Mo

ney M

arke

t Po

ol Fu

nd

Othe

r Inv

estm

ents

Acco

unts

Rece

ivable

Ac

coun

ts Pa

yable

To

tal

Fund

Bala

nce

Alter

nativ

e Edu

catio

n Cen

ters

8101

Ja

n Man

n Op

portu

nity S

choo

l 1

6,092

.30

3

,721.7

0

(

4,176

.15)

15

,637.8

5 1

3,670

.63

2,03

8.22

-

-

(71

.00)

1

5,637

.85

7631

Mi

ami M

acAr

thur

South

Sen

ior

11,4

65.50

10,97

4.37

(11,7

90.77

)

10,64

9.10

3,

284.9

7

7,

364.1

3 -

-

-

10,6

49.10

TOTA

LS

$1,45

8,479

.49

$6,55

3,625

.44

$(6,5

67,59

0.74)

$1

,444,5

14.19

$5

85,31

0.91

$ 83

2,921

.99

$

-

$2

6,352

.29

$ (

71.00

) $1

,444,5

14.19

AUD

IT O

PIN

ION

19

Inter

nal A

udit R

epor

t

Se

lected

Sch

ools/

Cente

rs

Au

dit O

pini

on o

n Fi

nanc

ial S

tate

men

ts an

d Ov

erall

Ass

essm

ent o

f Int

erna

l Con

trols

Over

Fin

ancia

l Rep

ortin

g No

twith

stand

ing th

e ex

cept

ions b

elow,

the

finan

cial s

tate

men

ts of

the

inter

nal fu

nds o

f the

K-1

2 ce

nter

s rep

orte

d he

rein

pres

ent f

airly,

in a

ll mat

erial

re

spec

ts, th

e ch

ange

s in

fund

balan

ces f

rom

fina

ncial

acti

vity

cond

ucte

d du

ring

the

2015

-201

6 fis

cal y

ear u

p to

the

MSA

F En

d Da

te (d

epen

ding

on

the

K-12

cen

ter a

udite

d, a

s no

ted

in th

e Ac

coun

ting

Syste

m C

onve

rsion

Sch

edule

on

page

s 34

-37)

, on

the

cash

bas

is of

acc

ount

ing; a

nd fr

om th

e eS

AS S

yste

m A

vaila

ble C

onve

rsion

Dat

e (d

epen

ding

on th

e K-

12 ce

nter

aud

ited,

as n

oted

in th

e Ac

coun

ting

Syste

m C

onve

rsion

Sch

edule

on

page

s 34

-37)

up

to J

une

30, 2

016,

on

the

full a

ccru

al ba

sis o

f acc

ount

ing; a

nd/o

r dur

ing th

e 20

16-2

017

fisca

l yea

r, on

the

full a

ccru

al ba

sis o

f acc

ount

ing,

depe

nding

on

the

indivi

dual

K-12

aud

ited

(whe

ther

a o

ne-y

ear o

r a tw

o-ye

ar a

udit)

. Reg

ardin

g W

illiam

H. T

urne

r Tec

hnica

l Arts

Adu

lt Ed

ucat

ion

Cent

er, t

he fi

nanc

ial s

tatem

ents

of th

e int

erna

l fun

ds o

f the

adu

lt ed

ucat

ion c

ente

r pre

sent

fairly

, in

all m

ater

ial re

spec

ts, th

e ch

ange

s in

fund

ba

lance

s aris

ing fr

om fin

ancia

l acti

vity c

ondu

cted

durin

g th

e 20

15-2

016

and

2016

-201

7 fis

cal y

ears

, on

the

full a

ccru

al ba

sis o

f acc

ount

ing6 .

As

of

June

30,

201

6, f

or 3

47 sc

hools

/cent

ers

repo

rted

here

in, to

tal r

eceip

ts an

d dis

burs

emen

ts am

ount

ed t

o $6

,592

,353

and

$(6

,502

,367

), re

spec

tively

; whil

e to

tal c

ombin

ed F

und

Balan

ce a

mou

nted

to $

1,32

0,57

9 (P

ages

10-

13).

As

of

June

30,

201

7, f

or a

ll 45

sch

ools/

cent

ers

repo

rted

here

in, t

otal

com

bined

rec

eipts

and

disbu

rsem

ents

amou

nted

to

$6,5

53,6

25 a

nd

$(6,

567,

591)

, res

pecti

vely;

whil

e to

tal c

ombin

ed F

und

Balan

ce a

mou

nted

to $

1,44

4,51

4 (P

ages

14-

18).

No

twith

stand

ing th

e co

nditio

ns a

nd fi

nding

s re

porte

d he

rein,

as

of J

une

30, 2

017,

the

inter

nal c

ontro

l stru

cture

at a

ll 45

scho

ols/ce

nter

s ge

nera

lly

func

tione

d as

des

igned

by

the

Distr

ict a

nd im

pleme

nted

by

the

scho

ol ad

mini

strat

ion, e

xcep

t for

thos

e co

nditio

ns r

epor

ted

at th

e ind

ividu

al sc

hools

/cent

ers.

With

resp

ect t

o th

e ite

ms t

este

d, th

e sc

hools

/cent

ers w

ere

in ge

nera

l com

plian

ce w

ith th

e po

licies

and

pro

cedu

res i

n th

e M

anua

l of

Inte

rnal

Fund

Acc

ount

ing, e

xcep

t for

thos

e ins

tanc

es o

f non

-com

plian

ce id

entifi

ed an

d re

porte

d at

the

indivi

dual

scho

ols/ce

nter

s. W

hen

cond

itions

came

to o

ur a

ttent

ion th

at w

ere

deem

ed n

on-re

porta

ble, b

ecau

se th

ey w

ere

imm

ater

ial o

r inc

onse

quen

tial, t

hey w

ere,

nev

erth

eless

, dis

cuss

ed w

ith m

anag

emen

t for

their

info

rmat

ion a

nd fo

llow-

up.

_

____

____

____

____

____

____

____

Ma

ria T

. Gon

zalez

, Cer

tified

Pub

lic A

ccou

ntant

Assis

tant C

hief A

udito

r, Sc

hool

Audit

s Divi

sion

Offic

e of M

anag

emen

t and

Com

plian

ce A

udits

6 K

-12

cente

rs mi

grate

d to

the ne

w eS

AS (f

ull ac

crual)

acco

untin

g sys

tem du

ring

2015

-201

6, wh

ile ad

ult e

duca

tion

cente

rs/tec

hnica

l coll

eges

migr

ated

to the

new

eS

AS (f

ull ac

crual)

acco

untin

g sys

tem in

Apr

il 201

5 (20

14-2

015)

. 7 T

his re

port

includ

es 3

3 K-

12 ce

nters

and

1 ad

ult e

duca

tion

cente

r with

a tw

o-ye

ar a

udit (

2015

-201

6 an

d 20

16-2

017)

and

11

K-12

cente

rs wi

th a

one-

year

aud

it (2

016-

2017

).

INTERNAL CONTROLS RATING

20 Internal Audit Report Selected Schools/Centers

The internal control ratings for the two schools/centers reported herein with audit exceptions are depicted as follows:

SCHOOLS/CENTERS

PROCESS & IT CONTROLS POLICY & PROCEDURES COMPLIANCE

EFFECT

SATISFACTORY NEEDS

IMPROVEMENT

INADEQUATE

SATISFACTORY NEEDS

IMPROVEMENT

INADEQUATE

North Region Office School/Center

Madie Ives Elementary Likely to impact.

Central Region Office School/Center

Ada Merritt K-8 Center Likely to impact.

INTERNAL CONTROLS RATING

21 Internal Audit Report Selected Schools/Centers

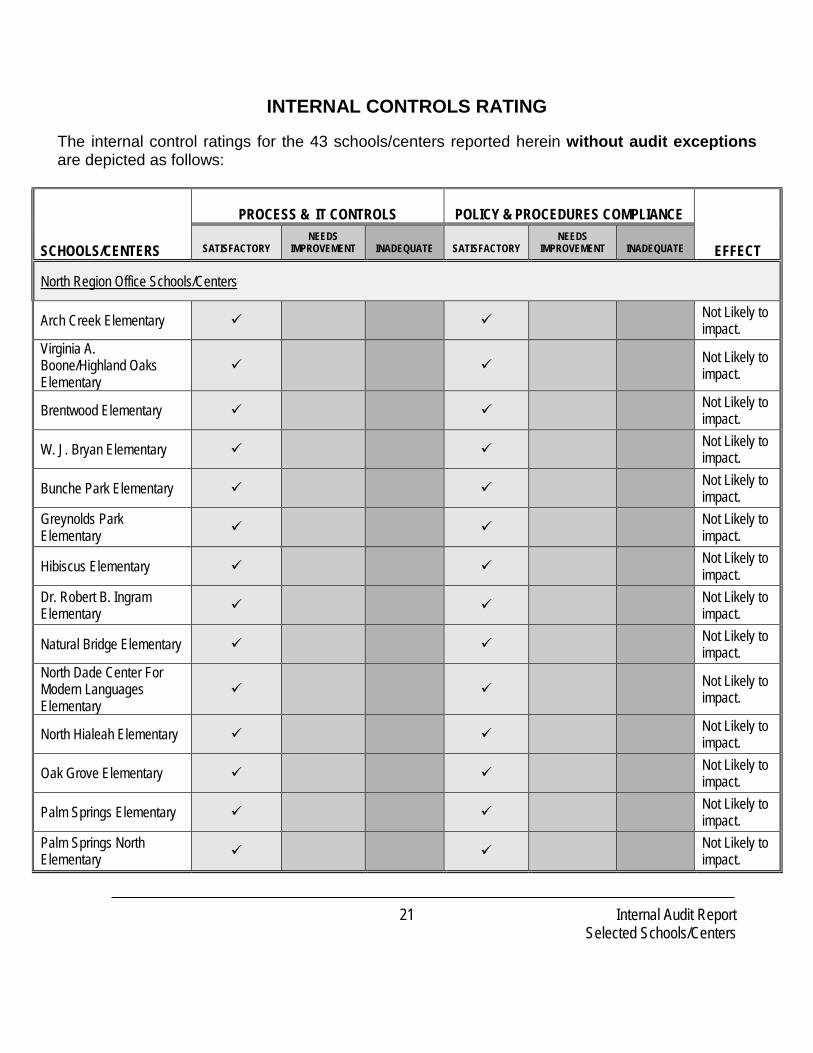

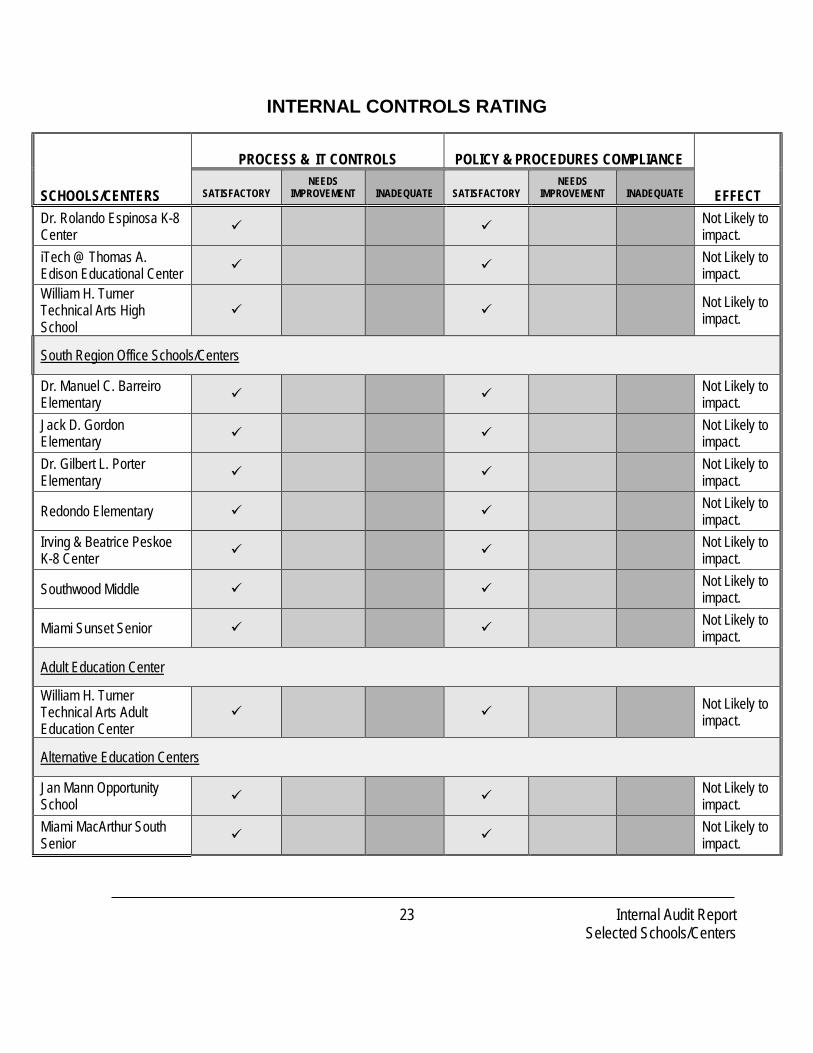

The internal control ratings for the 43 schools/centers reported herein without audit exceptions are depicted as follows:

SCHOOLS/CENTERS

PROCESS & IT CONTROLS POLICY & PROCEDURES COMPLIANCE

EFFECT

SATISFACTORY NEEDS

IMPROVEMENT

INADEQUATE

SATISFACTORY NEEDS

IMPROVEMENT

INADEQUATE

North Region Office Schools/Centers

Arch Creek Elementary Not Likely to impact.

Virginia A. Boone/Highland Oaks Elementary

Not Likely to impact.

Brentwood Elementary Not Likely to impact.

W. J. Bryan Elementary Not Likely to impact.

Bunche Park Elementary Not Likely to impact.

Greynolds Park Elementary Not Likely to

impact.

Hibiscus Elementary Not Likely to impact.

Dr. Robert B. Ingram Elementary Not Likely to

impact.

Natural Bridge Elementary Not Likely to impact.

North Dade Center For Modern Languages Elementary

Not Likely to impact.

North Hialeah Elementary Not Likely to impact.

Oak Grove Elementary Not Likely to impact.

Palm Springs Elementary Not Likely to impact.

Palm Springs North Elementary Not Likely to

impact.

INTERNAL CONTROLS RATING

22 Internal Audit Report Selected Schools/Centers

SCHOOLS/CENTERS

PROCESS & IT CONTROLS POLICY & PROCEDURES COMPLIANCE

EFFECT

SATISFACTORY NEEDS

IMPROVEMENT

INADEQUATE

SATISFACTORY NEEDS

IMPROVEMENT

INADEQUATE

Parkway Elementary Not Likely to impact.

Rainbow Park Elementary Not Likely to impact.

West Hialeah Gardens Elementary Not Likely to

impact. Bob Graham Education Center Not Likely to

impact.

Miami Lakes K-8 Center Not Likely to impact.

Hubert O. Sibley K-8 Academy Not Likely to

impact.

Andover Middle Not Likely to impact.

Hialeah Gardens Middle Not Likely to impact.

Miami Norland Senior Not Likely to impact.

Robert Renick Educational Center Not Likely to

impact.

Central Region Office Schools/Centers

Van E. Blanton Elementary Not Likely to

impact. George Washington Carver Elementary Not Likely to

impact.

Emerson Elementary Not Likely to impact.

Liberty City Elementary Not Likely to impact.

Santa Clara Elementary Not Likely to impact.

Paul Laurence Dunbar K-8 Center Not Likely to

impact.

INTERNAL CONTROLS RATING

23 Internal Audit Report Selected Schools/Centers

SCHOOLS/CENTERS

PROCESS & IT CONTROLS POLICY & PROCEDURES COMPLIANCE

EFFECT

SATISFACTORY NEEDS

IMPROVEMENT

INADEQUATE

SATISFACTORY NEEDS

IMPROVEMENT

INADEQUATE

Dr. Rolando Espinosa K-8 Center Not Likely to

impact. iTech @ Thomas A. Edison Educational Center Not Likely to

impact. William H. Turner Technical Arts High School

Not Likely to impact.

South Region Office Schools/Centers

Dr. Manuel C. Barreiro Elementary Not Likely to

impact. Jack D. Gordon Elementary Not Likely to

impact. Dr. Gilbert L. Porter Elementary Not Likely to

impact.

Redondo Elementary Not Likely to impact.

Irving & Beatrice Peskoe K-8 Center Not Likely to

impact.

Southwood Middle Not Likely to impact.

Miami Sunset Senior Not Likely to impact.

Adult Education Center

William H. Turner Technical Arts Adult Education Center

Not Likely to impact.

Alternative Education Centers

Jan Mann Opportunity School Not Likely to

impact. Miami MacArthur South Senior Not Likely to

impact.

SUMMARY SCHEDULE OF AUDIT FINDINGS CURRENT AND PRIOR AUDIT PERIODS

24 Internal Audit Report Selected Schools/Centers

Summary of findings of the two schools/centers reported herein with audit exceptions are as follows:

WORK LOC. NO.

SCHOOLS/CENTERS

AUDIT PERIOD

CURRENT AUDIT PERIOD

FINDINGS

PRIOR AUDIT PERIOD

FINDINGS Fiscal

Year(s)/ FTE Survey

Total Per

Center

Area Of

Findings

Total Per

Center

Area Of

Findings North Region Office School/Center

2581 Madie Ives Elementary(a) 2015-2016 2016-2017 1

• Receipting and Depositing/Safeguarding of Collections

None

Central Region Office School/Center

3191 Ada Merrit K-8 Center(a) 2015-2016 2016-2017 2016-17 SP3

1 • Safeguarding of Deposits None

TOTAL 2 None

Note: (a) No change in school administration since prior audit.

SUMMARY SCHEDULE OF AUDIT FINDINGS CURRENT AND PRIOR AUDIT PERIODS

25 Internal Audit Report Selected Schools/Centers

Summary of findings of the 43 schools/centers reported herein without audit exceptions are as follows:

WORK LOC. NO.

SCHOOLS/CENTERS

AUDIT PERIOD

CURRENT AUDIT PERIOD

FINDINGS

PRIOR AUDIT PERIOD

FINDINGS Fiscal

Year(s)/ FTE Survey

Total Per Center

Area Of

Findings Total

Per Center

Area Of

Findings

North Region Office Schools/Centers

0341 Arch Creek Elementary 2015-2016 2016-2017 2016-17 SP3

None None

2441 Virginia A. Boone/Highland Oaks Elementary

2015-2016 2016-2017 None None

0461 Brentwood Elementary 2015-2016 2016-2017 None None

0561 W. J. Bryan Elementary 2015-2016 2016-2017 2016-17 SP3

None None

0641 Bunche Park Elementary 2015-2016 2016-2017 None None

2281 Greynolds Park Elementary 2015-2016 2016-2017 2016-17 SP3

None None

2401 Hibiscus Elementary 2015-2016 2016-2017 None None

4121 Dr. Robert B. Ingram Elementary

2015-2016 2016-2017 None None

3661 Natural Bridge Elementary 2015-2016 2016-2017 2016-17 SP3

None None

5131 North Dade Center For Modern Languages Elementary

2015-2016 2016-2017 None None

3901 North Hialeah Elementary 2016-2017 None None

4021 Oak Grove Elementary 2015-2016 2016-2017 None None

4261 Palm Springs Elementary 2015-2016 2016-2017 None None

4281 Palm Springs North Elementary

2015-2016 2016-2017 2016-17 SP3

None None

SUMMARY SCHEDULE OF AUDIT FINDINGS CURRENT AND PRIOR AUDIT PERIODS

26 Internal Audit Report Selected Schools/Centers

WORK LOC. NO.

SCHOOLS/CENTERS

AUDIT PERIOD

CURRENT AUDIT PERIOD

FINDINGS

PRIOR AUDIT PERIOD

FINDINGS Fiscal

Year(s)/ FTE Survey

Total Per Center

Area Of

Findings Total

Per Center

Area Of

Findings

4341 Parkway Elementary 2015-2016 2016-2017 None 1 • Bookkeeping

4541 Rainbow Park Elementary 2015-2016 2016-2017 None None

2371 West Hialeah Gardens Elementary

2015-2016 2016-2017 None None

0091 Bob Graham Education Center

2015-2016 2016-2017 None None

3281 Miami Lakes K-8 Center 2015-2016 2016-2017 2016-17 SP3

None None

5141 Hubert O. Sibley K-8 Academy

2015-2016 2016-2017 2016-17 SP3

None None

6023 Andover Middle 2015-2016 2016-2017 None None

6751 Hialeah Gardens Middle 2015-2016 2016-2017 2016-17 SP3

None None

7381 Miami Norland Senior 2015-2016 2016-2017 2016-17 SP3

None 2 • Disb. (Int. Funds

& P-Card) • Data Security

8151 Robert Renick Educational Center 2016-2017 None 2 • Bookkeeping

• Disbursements

Central Region Office Schools/Centers

0401 Van E. Blanton Elementary 2016-2017 None None

0721 George Washington Carver Elementary 2016-2017 None None

1641 Emerson Elementary 2016-2017 None None

2981 Liberty City Elementary 2016-2017 None None

4841 Santa Clara Elementary 2016-2017 None None

1441 Paul Laurence Dunbar K-8 Center 2016-2017 None None

SUMMARY SCHEDULE OF AUDIT FINDINGS CURRENT AND PRIOR AUDIT PERIODS

27 Internal Audit Report Selected Schools/Centers

WORK LOC. NO.

SCHOOLS/CENTERS

AUDIT PERIOD

CURRENT AUDIT PERIOD

FINDINGS

PRIOR AUDIT PERIOD

FINDINGS Fiscal

Year(s)/ FTE Survey

Total Per Center

Area Of

Findings Total

Per Center

Area Of

Findings

0122 Dr. Rolando Espinosa K-8 Center

2015-2016 2016-2017 None None

7005 iTech @ Thomas A. Edison Educational Center 2016-2017 None None

7601 William H. Turner Technical Arts High School

2015-2016 2016-2017 None None

South Region Office Schools/Centers

0211 Dr. Manuel C. Barreiro Elementary

2015-2016 2016-2017 None None

2151 Jack D. Gordon Elementary 2015-2016 2016-2017 None 1 • FTE-ELL

4511 Dr. Gilbert L. Porter Elementary

2015-2016 2016-2017 None None

4611 Redondo Elementary 2016-2017 None None

4391 Irving & Beatrice Peskoe K-8 Center

2015-2016 2016-2017 None 1 • Payroll

6861 Southwood Middle 2015-2016 2016-2017 None None

7531 Miami Sunset Senior 2015-2016 2016-2017 2016-17 SP3

None None

Adult Education Center

7602 William H. Turner Technical Arts Adult Education Center

2015-2016 2016-2017 None None

Alternative Education Centers

8101 Jan Mann Opportunity School

2015-2016 2016-2017 None None

7631 Miami MacArthur South Senior 2016-2017 None None

TOTAL None 7

LIST OF SCHOOL PRINCIPALS/ADMINISTRATORS

28 Internal Audit Report Selected Schools/Centers