Interim Results Six months to 30 September 2015 -...

43

Interim Results Six months to 30 September 2015 11 November 2015

Transcript of Interim Results Six months to 30 September 2015 -...

Interim Results

Six months to 30 September 2015

11 November 2015

Disclaimer

2

This presentation, which has been prepared by ICAP plc ("ICAP"), is strictly confidential and is being provided to you solely for your information and comprises the written materials/slides for a

presentation concerning the proposed disposal of ICAP's global hybrid voice broking business to Tullett Prebon plc ("Tullett Prebon") (the "Proposed Transaction"). Where used in this document,

"Presentation" shall mean and include the slides that follow, the oral presentation of the slides by the ICAP's officers on behalf of ICAP, any question and answer session that follows the oral

presentation, hard copies of this Presentation and any materials distributed at, or in connection with, this Presentation.

Neither this Presentation nor any part of it, nor the fact of its distribution, shall form the basis of, or be relied on in connection with, any contract or commitment or investment decision in relation

thereto, nor does it constitute a recommendation regarding the shares of ICAP, Tullett Prebon, the combined company ("Enlarged Tullett Prebon") or the new holding company of the ICAP group

("NewCo"). Any decision to purchase must be made solely on the basis of the information gained from the recipients' own investigations and analysis of ICAP, NewCo, Tullett Prebon or Enlarged

Tullett Prebon. None of ICAP, its advisers, or any other party is under any duty to update or inform you of any change to such information. Shareholders should not base any voting decision in

connection with resolutions to authorise the Proposed Transaction except on the basis of information in any circular and/or prospectus (and any supplement(s) thereto) published in connection with

the Proposed Transaction, which information will supersede the information contained in this Presentation.

No reliance must be placed for any purpose whatsoever on the information contained in this Presentation, or any other information discussed verbally, or in its completeness (including, without

limitation, on the fairness, accuracy, completeness or correctness of the information or opinions contained herein) and it does not purport to contain all information that may be required to evaluate

ICAP or its business. No representation or warranty, express or implied, is or will be made as to, or in relation to, and no responsibility or liability is or will be accepted by or on behalf of ICAP or any

member of the ICAP's group (the "Group"), Evercore Partners International LLP, J.P. Morgan Limited or by any of their respective directors, officers, employees, agents, affiliates and advisers, or any

other person as to or in relation to the accuracy, fairness, correctness, sufficiency or completeness of the information or opinions contained in this Presentation (or any part hereof) or any other written

or oral information made available to, or publicly available to, any interested party or its advisers. Each of ICAP, Evercore Partners International LLP and J.P. Morgan Limited and each of their

respective directors, officers, employees, agents, affiliates and advisers accordingly disclaims to the fullest extent permitted by law all and any liability whatsoever, whether arising in tort, contract or

otherwise which it might otherwise have in respect of any statements or other information contained in this Presentation.

This Presentation contains certain statements which are, or may be deemed to be, "forward-looking statements" relating to the business, financial performance and results of ICAP, Tullett Prebon or

Enlarged Tullett Prebon and/or the industry in which they operate. These forward-looking statements involve substantial risks and uncertainties and actual results, levels of activity, performance,

achievements, developments and events may differ materially from those expressed or implied by these statements and depend on a variety of factors. By their nature, forward-looking statements

involve risk and uncertainty because they relate to future events and circumstances. The forward-looking statements concern future circumstances and results and other statements that are not

historical facts, sometimes identified by the words 'believes', 'expects', 'predicts', 'intends', 'projects', 'plans', 'estimates', 'aims', 'foresees', 'anticipates', 'targets', 'goals', 'due', 'could', 'may', 'should',

and similar expressions. These forward-looking statements include, without limitation, statements regarding future financial position, income growth, impairment charges, business strategy, projected

levels of growth in the relevant markets, projected costs, estimates of capital expenditures, and plans and objectives for future operations of ICAP, Tullett Prebon or Enlarged Tullett Prebon. Past

performance should not be taken as an indication or guarantee of future results, and no representation or warranty, express or implied, is made regarding future performance. No assurance can be

given that the forward-looking statements in this Presentation will be realised and these forward-looking statements speak only as at the date of this Presentation. ICAP or its directors, officers,

employees, agents, affiliates and advisers, or any other party undertakes no obligation publicly to release the results of any revisions or updates to any forward-looking statements in this Presentation

that may occur due to any change in its expectations or to reflect events or circumstances after the date of this Presentation (except to the extent required by applicable law or regulation or any

appropriate regulatory authority). As a result of these risks, uncertainties and assumptions, recipients should not place undue reliance on these forward-looking statements as a prediction of actual

results or otherwise. No statement in this Presentation is intended to be nor may be construed as a profit forecast.

The forward-looking statements, including assumptions, opinions and views of ICAP or cited from third party sources, contained in the half year results slides are solely opinions and forecasts which

are uncertain and subject to risks. Although ICAP believes that the expectations reflected in these forward-looking statements are reasonable, it can give no assurance that these expectations will

prove to be correct. Actual results may differ materially from those expressed or implied by these forward-looking statements. A number of factors could cause actual events to differ significantly.

These factors include, but are not limited to: volatility and changing conditions in financial markets; significant unexpected movements in interest and exchange rates; risk of disruption to existing client

relationships; adverse regulatory conditions being imposed on the transaction or significant delay in regulatory approval; difficulties in separating and integrating the respective businesses; unexpected

and greater costs arising out of the transaction.

Most of these factors are difficult to predict accurately and are generally beyond the control of ICAP. Any forward-looking statements made by, or on behalf of ICAP, speak only as of the date they

are made.

Evercore Partners International LLP, which is authorised and regulated in the United Kingdom by the Financial Conduct Authority, and J.P. Morgan Limited, which is authorised and regulated in the

United Kingdom by the Financial Conduct Authority, are acting exclusively for ICAP and NewCo and no one else in connection with the Proposed Transaction and will not regard any other person as a

client in relation to the Proposed Transaction and will not be responsible to anyone other than ICAP and NewCo for providing the protections afforded to their respective clients, nor for providing

advice, in relation to the Proposed Transaction or any other matter referred to in this Presentation.

Michael Spencer

Group Chief Executive Officer

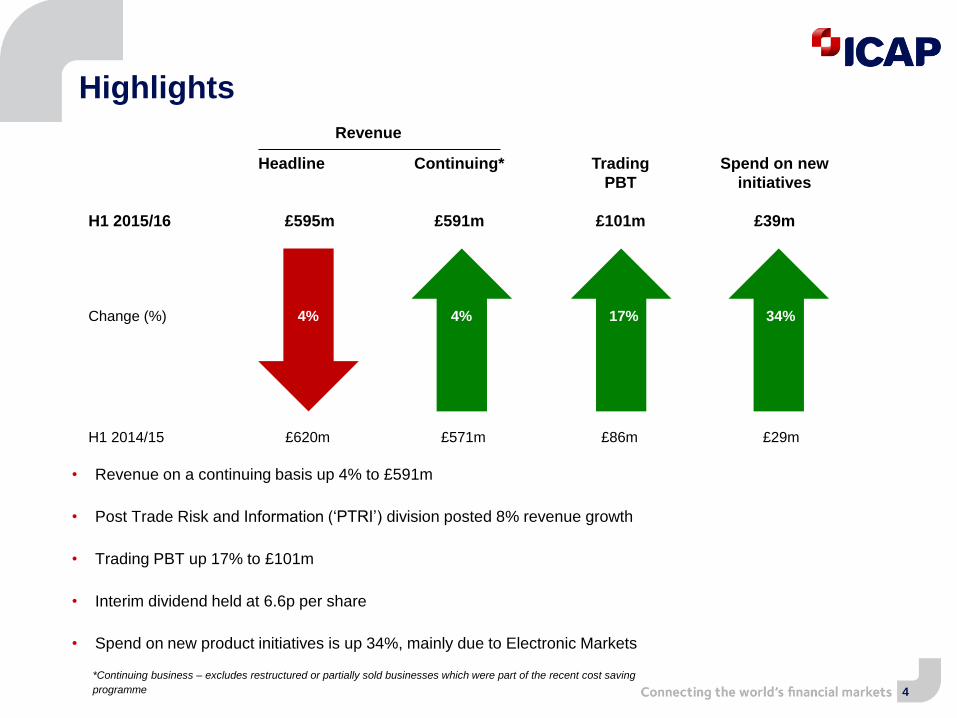

Revenue

H1 2015/16

Headline

£595m

Continuing*

£591m

Trading

PBT

£101m

Spend on new

initiatives

£39m

Change (%) 4% 4% 17% 34%

H1 2014/15 £620m £571m £86m £29m

• Revenue on a continuing basis up 4% to £591m

• Post Trade Risk and Information (‘PTRI’) division posted 8% revenue growth

• Trading PBT up 17% to £101m

• Interim dividend held at 6.6p per share

• Spend on new product initiatives is up 34%, mainly due to Electronic Markets

*Continuing business – excludes restructured or partially sold businesses which were part of the recent cost saving

programme

Highlights

4

Stuart Bridges

Group Finance Director

Group income statement

Headline results

6

Highlights

• Revenue down 4%, up 4% on a continuing

basis (up 1% on continuing/constant currency

basis)

• Expenses down 7%, up 1% on a continuing

basis (down 1% on continuing/constant

currency basis), as lower Global Broking

broadly offset by investment in Electronic

Markets / PTRI

• Trading PBT up 17% to £101m

• Despite significant new investment, margin up

3ppt

H1 H1 %

2015/16 2014/15 change

£m £m

Revenue 595 620 (4)

Net operating expense (485) (520) 7

Trading operating

profit110 100 10

Net finance charge (13) (18) 28

Associates & JV's 4 4 -

Trading Profit before tax 101 86 17

Trading operating

profit margin 19% 16% 3ppt

Interim dividend 6.6p 6.6p -

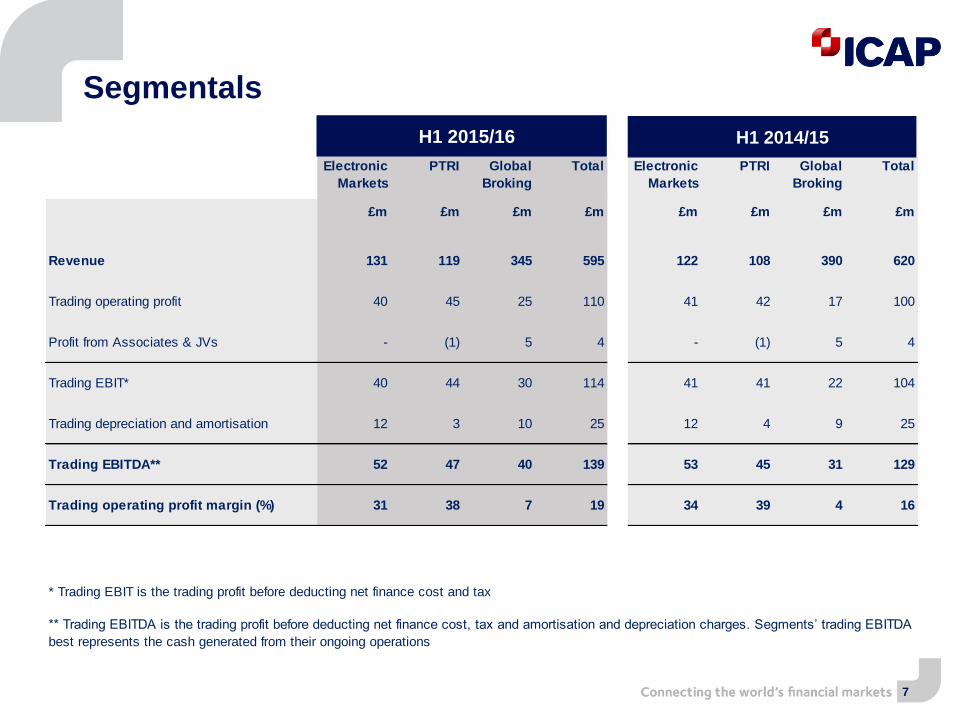

Electronic

Markets

PTRI Global

Broking

Total Electronic

Markets

PTRI Global

Broking

Total

£m £m £m £m £m £m £m £m

Revenue 131 119 345 595 122 108 390 620

Trading operating profit 40 45 25 110 41 42 17 100

Profit from Associates & JVs - (1) 5 4 - (1) 5 4

Trading EBIT* 40 44 30 114 41 41 22 104

Trading depreciation and amortisation 12 3 10 25 12 4 9 25

Trading EBITDA** 52 47 40 139 53 45 31 129

Trading operating profit margin (%) 31 38 7 19 34 39 4 16

* Trading EBIT is the trading profit before deducting net finance cost and tax

** Trading EBITDA is the trading profit before deducting net finance cost, tax and amortisation and depreciation charges. Segments’ trading EBITDA

best represents the cash generated from their ongoing operations

Segmentals

7

H1 2015/16 H1 2014/15

3

6

1

2

2

2

2

-

0 2 4 6 8 10 12

H12014/15

H12015/16

Electronic Markets Traiana TriOptima SEF

9

24

4

3

2

2

6

-

0 5 10 15 20 25 30 35

H12014/15

H12015/16

2%

4%6%

9%11%

3%

4%

6%

9%

12%

0%

5%

10%

15%

20%

25%

FY 201 1/12 FY 201 2/13 FY 201 3/14 FY 201 4/15 H1 2015/16

ElectronicMarkets

PTRI

Investment in major new initiatives

£39m spent on new product initiatives

Income statement% of Electronic Markets / PTRI revenue from new

products / customers

23%

18%

12%

8%

5%

All new products/customers since FY2010/11

Capex

£29m

£21m

£10m

£8m

8

£m

£m

18%

18%

19%

20%

22%

12%

14%

15%

18%

20%

70%

68%

66%

62%

58%

0% 25% 50% 75% 100%

2011/12 FY

2012/13 FY

2013/14 FY

2014/15 FY

2015/16 H1

Electronic Markets PTRI Global Broking

34%

37%

37%

37%

36%

24%

29%

33%

38%

41%

42%

34%

30%

25%

23%

0% 25% 50% 75% 100%

2011/12 FY

2012/13 FY

2013/14 FY

2014/15 FY

2015/16 H1

Electronic Markets PTRI Global Broking

ICAP’s business mix

Revenue split

Trading operating profit margin by business

9

Operating profit split

• Electronic Markets / PTRI operating profit split up 19ppt to 77% from 58% 2011/12 FY

• Margins impacted by continued investment, £29mnew product initiative spend in Electronic Markets (£24m) / PTRI (£5m)

• Electronic Markets / PTRI revenue split up 12ppt to 42% from 30% 2011/12 FY

42% 42%40%

36%34%

31%

44% 43%45%

43%

39% 38%

13%11% 10%

8%4%

7%

0%

10%

20%

30%

40%

2011/12 FY 2012/13 FY 2013/14 FY 2014/15 FY 2014/15 H1 2015/16 H1

Electronic Markets PTRI Global Broking

FY H1

0%

5%

10%

15%

20%

25%

FY 2011/12 FY 2012/13 FY 2013/14 FY 2014/15 H1 2015/16

H1 H1 %

2015/16 2014/15 change£m £m

Revenue 131 122 7

Constant currency 130 1

Trading operating

profit40 41 (2)

Trading operating

profit margin 31% 34% (3ppt)

£64m£64m

£3m

£56m

£62m

£4m

EBS

BrokerTec

Other

Electronic Markets

Headline

10

H1 2014/15 H1 2015/16

£122m £131m

Revenue mix% of Electronic Markets revenue from new customers /

products

• Revenue up 1% on a constant currency basis, EBS up 7%, and BrokerTec down 3%

• Significantly increased FX volume in Asian currencies partially offset by cyclical pressures

• Margins down 3ppt owing to new product initiative spend of £24m investment in EBS Direct, forwards and swaps and BrokerTec Direct

Highlights

21%

17%

10%

8%

4%

All new products/customers since FY2010/11

0%

5%

10%

15%

20%

25%

FY 2011/12 FY 2012/13 FY 2013/14 FY 2014/15 H1 2015/16

29

35

34

40

25

26

20

18

0 20 40 60 80 100 120 140

H1 2014/15

H1 2015/16

TriOptima Information Traiana Reset/ReMatch

H1 H1 %

2015/16 2014/15 change

£m £m

Revenue 119 108 10

Constant currency 110 8

Trading operating

profit45 42 7

Trading operating

profit margin38% 39% (1ppt)

Post Trade Risk & Information

Headline Highlights

Revenue by product

11

• Revenue up 8% on a constant currency basis,

underpinned by TriOptima growth due to increased

demand for compression and reconciliation

• Reset affected by market headwinds from low volatility

• Margins slightly lower, new product initiative spend £5m

• Transaction v Subscription split 35% / 65%

% of PTRI revenue from new customers / products

25%

20%

13%

10%

6%

All new products/customers since FY2010/11

18% 10%21% 4%

£m

16 20 25 3016 16

2839 28

3012

13 1816

19

11

1127

27

23

18

68

84

37

37

1412

0

50

100

150

200

H1 2016 H1 2015 H1 2016 H1 2015 H1 2016 H1 2015

EMEA Americas Asiapac

Emerging markets Commodities Credit FX&MM Equities Rates

59%58% 58%

56%

50%

44%

46%

48%

50%

52%

54%

56%

58%

60%

H1 2011/12 H1 2012/13 H1 2013/14 H1 2014/15 H1 2015/16

Global Broking

Headline

12

Highlights

• Revenue on a continuing basis flat despite adverse

market conditions

• Broker compensation 50%

• Margin up 3ppt driven by cost savings

• Growth in Asia-Pacific region and Equities

Revenue by region

50

144

128

202

167

44

Broker Compensation

H1 H1 %

2015/16 2014/15 change

£m £m

Revenue 345 390 (12)

Constant currency 400 (14)

Trading operating

profit25 17 47

Trading operating

profit margin7% 4% 3ppt

Broker compensation 50% 56% (6ppt)

£m

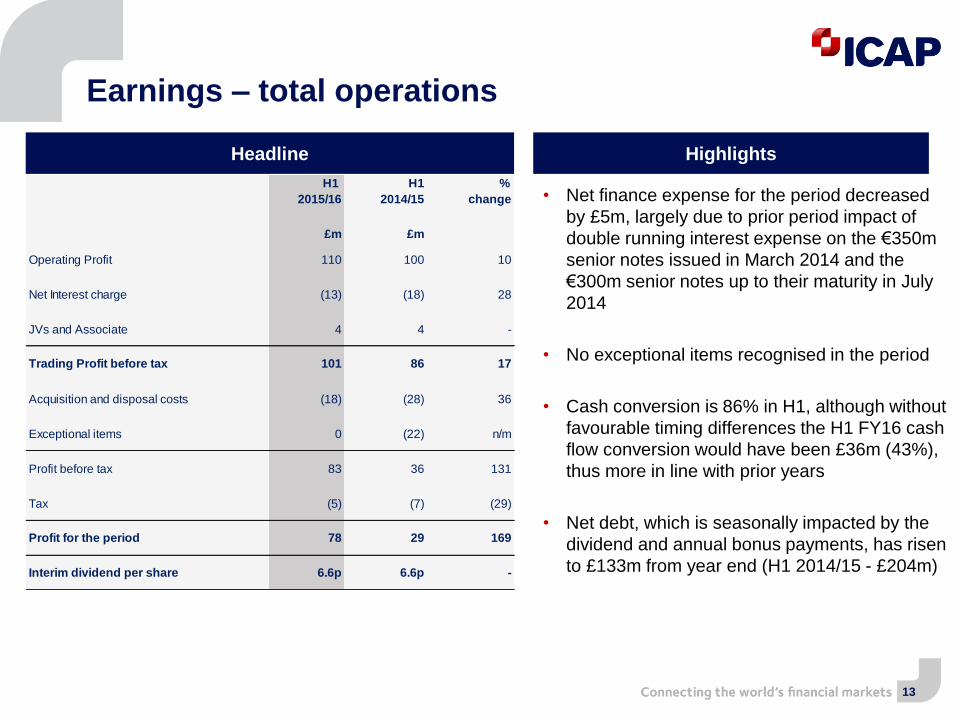

Earnings – total operations

Headline Highlights

• Net finance expense for the period decreased

by £5m, largely due to prior period impact of

double running interest expense on the €350m

senior notes issued in March 2014 and the

€300m senior notes up to their maturity in July

2014

• No exceptional items recognised in the period

• Cash conversion is 86% in H1, although without

favourable timing differences the H1 FY16 cash

flow conversion would have been £36m (43%),

thus more in line with prior years

• Net debt, which is seasonally impacted by the

dividend and annual bonus payments, has risen

to £133m from year end (H1 2014/15 - £204m)

13

H1 H1 %

2015/16 2014/15 change

£m £m

Operating Profit 110 100 10

Net Interest charge (13) (18) 28

JVs and Associate 4 4 -

Trading Profit before tax 101 86 17

Acquisition and disposal costs (18) (28) 36

Exceptional items 0 (22) n/m

Profit before tax 83 36 131

Tax (5) (7) (29)

Profit for the period 78 29 169

Interim dividend per share 6.6p 6.6p -

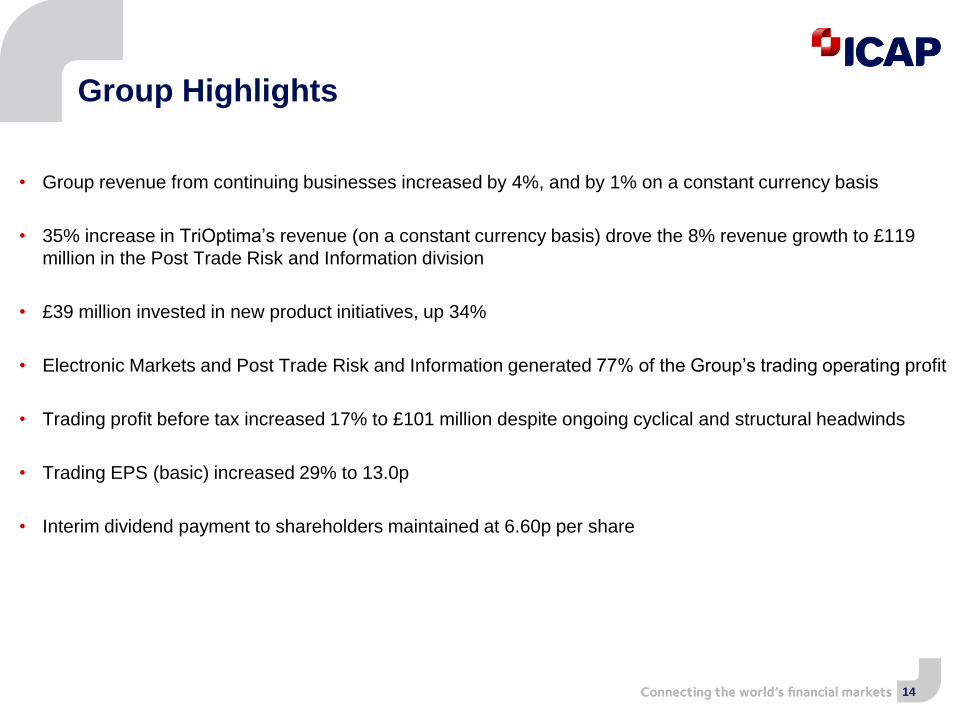

Group Highlights

• Group revenue from continuing businesses increased by 4%, and by 1% on a constant currency basis

• 35% increase in TriOptima’s revenue (on a constant currency basis) drove the 8% revenue growth to £119

million in the Post Trade Risk and Information division

• £39 million invested in new product initiatives, up 34%

• Electronic Markets and Post Trade Risk and Information generated 77% of the Group’s trading operating profit

• Trading profit before tax increased 17% to £101 million despite ongoing cyclical and structural headwinds

• Trading EPS (basic) increased 29% to 13.0p

• Interim dividend payment to shareholders maintained at 6.60p per share

14

Transaction Overview

Michael Spencer

Group Chief Executive Officer

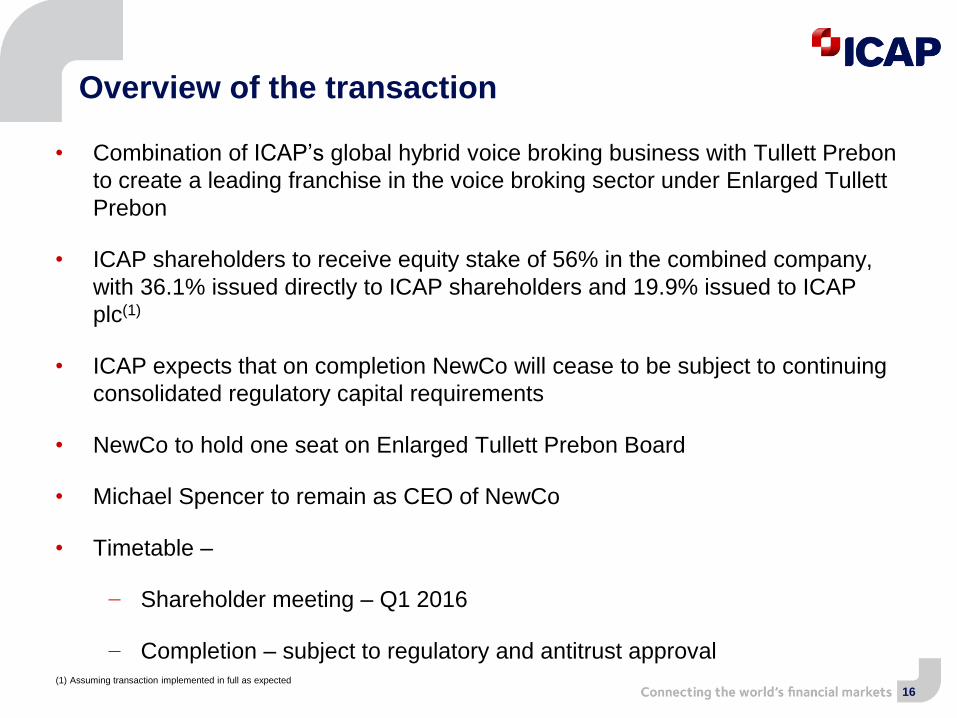

Overview of the transaction

16

• Combination of ICAP’s global hybrid voice broking business with Tullett Prebon

to create a leading franchise in the voice broking sector under Enlarged Tullett

Prebon

• ICAP shareholders to receive equity stake of 56% in the combined company,

with 36.1% issued directly to ICAP shareholders and 19.9% issued to ICAP

plc(1)

• ICAP expects that on completion NewCo will cease to be subject to continuing

consolidated regulatory capital requirements

• NewCo to hold one seat on Enlarged Tullett Prebon Board

• Michael Spencer to remain as CEO of NewCo

• Timetable –

− Shareholder meeting – Q1 2016

− Completion – subject to regulatory and antitrust approval(1) Assuming transaction implemented in full as expected

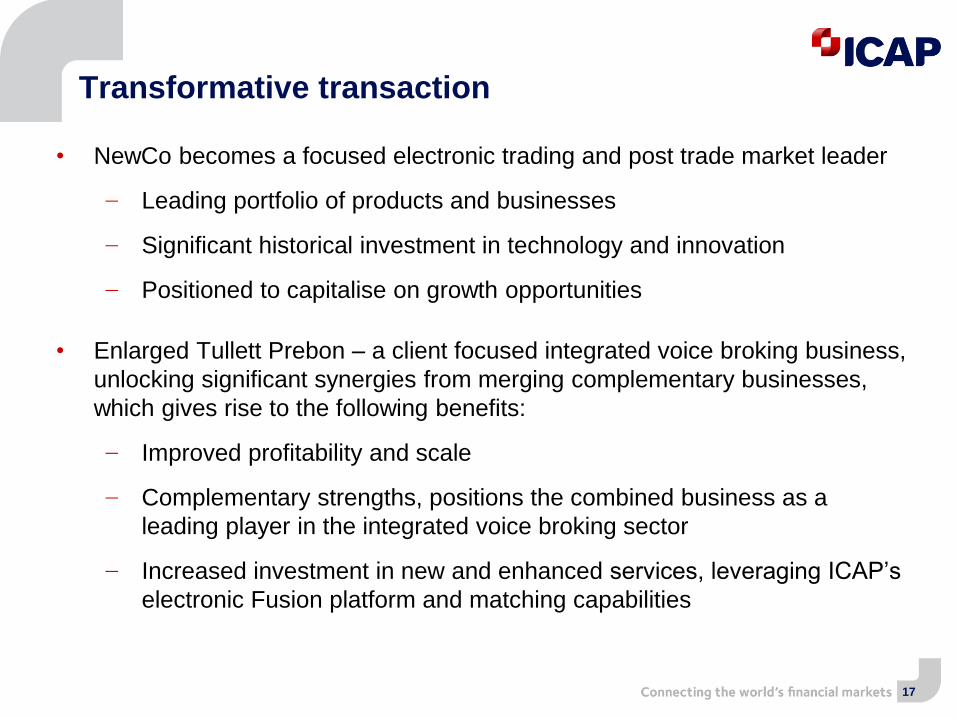

Transformative transaction

17

• NewCo becomes a focused electronic trading and post trade market leader

− Leading portfolio of products and businesses

− Significant historical investment in technology and innovation

− Positioned to capitalise on growth opportunities

• Enlarged Tullett Prebon – a client focused integrated voice broking business,

unlocking significant synergies from merging complementary businesses,

which gives rise to the following benefits:

− Improved profitability and scale

− Complementary strengths, positions the combined business as a

leading player in the integrated voice broking sector

− Increased investment in new and enhanced services, leveraging ICAP’s

electronic Fusion platform and matching capabilities

18

• 56% ownership stake represents attractive valuation of

ICAP’s global hybrid voice broking business, reflecting

its strong market position and prospects

Drivers of ICAP value creation

Attractive

transaction

terms for ICAP

shareholders

Synergies

Capital benefits

• Approximately £60m+ in annual synergies to Enlarged

Tullett Prebon shareholders

• 67-75% of expense savings realisable within two years

of transaction closing

• NewCo is expected to operate with a more capital-light

business model

• ICAP expects that on completion NewCo will cease to be

subject to continuing consolidated regulatory capital

requirements

NewCo – A focused

electronic and post

trade services group

20

• Leading portfolio at the heart of financial market infrastructure

• Drive expansion of addressable market through continuing product

development and broadening of geographic reach and customer base

• Offers solutions that are integrated into the workflow of our customers

• Increasing level of recurring subscription revenue

• Benefiting from regulatory-driven increased demand for post trade / risk

mitigation solutions and electronic trading infrastructure

• Management has strong track record of innovation

NewCo – A focused electronic and post trade services group

Post trade FX processing

21

Leading portfolio at the heart of financial market infrastructure

Derivatives portfolio compression and portfolio reconciliation franchises

Electronic trading platform in US Treasuries and repos

Electronic spot FX trading platform in EUR/USD, USD/JPY, Asian

NDFs and CNH

Basis risk management

Leading

position

Leading portfolio of early stage fin tech assets

22

Ac

qu

isit

ion

sP

rod

uct

lau

nch

es

Gro

wth

d

rive

rs(1

)

BTEC / EBS growth in algorithmic

trading / non-bank customers

Growth of FX

prime brokerage

underpins growth

of Traiana

Basel III / SLR

drives increased

demand for

compression

EMIR requirements

for portfolio

reconciliation

underpins triResolve

Market share gains /

migration from voice

drives growth of EM

currencies on EBS

20022004

20052006

20072008

20092010

20112012

2013

2014

2015

2016

Launch of

triResolve

Launch

of EBS

Direct

TriOptima

launches

bilateral

compression

TriOptima

launches CCP

compression

Launch of

Traiana

CreditLink

LimitHub Launch

of EBS

eFix

Launch of

EBS Select

TriOptima

expands

compression

to CME, JSCC

& FX forwards

EBS Direct

for FX

forwards /

corporates

2003

30%

stake in

TriOptima

BrokerTec –

£180m

EBS – £465m,

Reset – 25% stake

Traiana –

£120m

Remaining stake

in TriOptima –

£95m, stake in

AcadiaSoftMyTreasury

Remainder of Reset

in 3 tranches –

£143m

Investment

in Duco

Investment in

OpenGamma

Investments

in Enso

Further investment

in AcadiaSoft,

investment in

Abide Financial

Banks invest in

Traiana with implied

valuation of £185m

Strong track record of innovation

Launch of

BrokerTec

Direct

£1bn on acquisitions which now generate ~£170m of trading operating profit(1) Ranges are an approximation for the estimated start of each respective trend

23

Post Trade Risk Information

NewCo

• FY ‘15 revenue: £254m

• FY ‘15 trading operating profit: £102m

Michael SpencerGroup CEO

Electronic Markets

Gil MandelzisCEO

Jenny KnottCEO

• FY ‘15 revenue: £187m

• FY ‘15 trading operating profit: £70m

Charles GregsonNon-executive Chairman

Stuart BridgesGroup CFO

NewCo organisational chart

Steve GibsonCEO

Euclid Opportunities

Non-executive Directors

• John Sievwright

• Diane Schueneman

• Robert Standing

• Ivan Ritossa

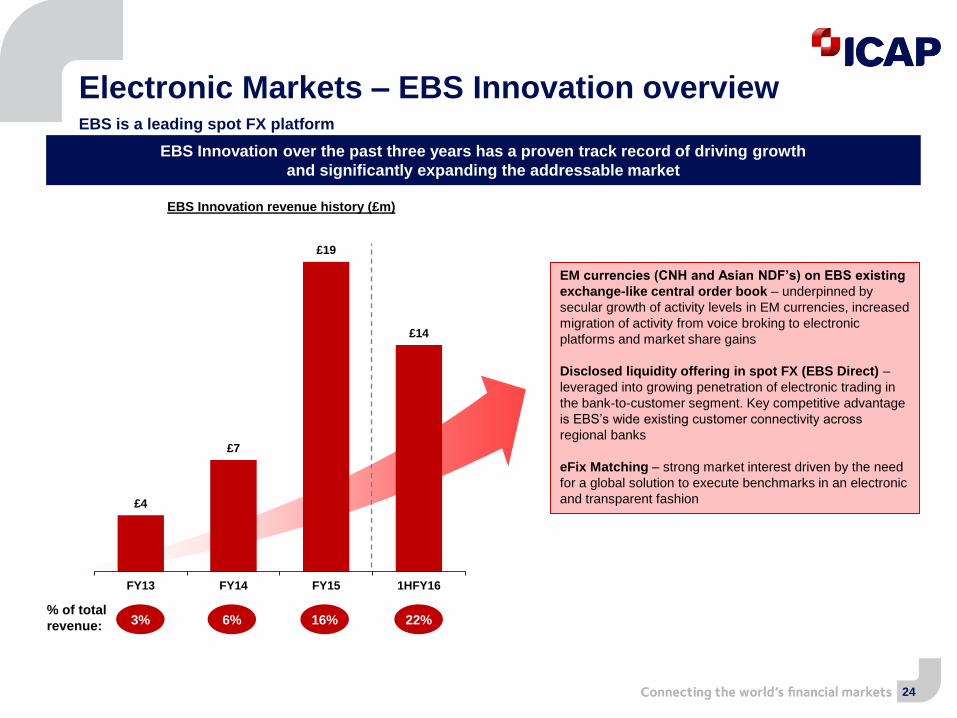

3% 6% 16% 22%

£4

£7

£19

£14

FY13 FY14 FY15 1HFY16

EBS Innovation revenue history (£m)

Electronic Markets – EBS Innovation overviewEBS is a leading spot FX platform

24

EBS Innovation over the past three years has a proven track record of driving growth

and significantly expanding the addressable market

% of total

revenue:

EM currencies (CNH and Asian NDF’s) on EBS existing

exchange-like central order book – underpinned by

secular growth of activity levels in EM currencies, increased

migration of activity from voice broking to electronic

platforms and market share gains

Disclosed liquidity offering in spot FX (EBS Direct) –

leveraged into growing penetration of electronic trading in

the bank-to-customer segment. Key competitive advantage

is EBS’s wide existing customer connectivity across

regional banks

eFix Matching – strong market interest driven by the need

for a global solution to execute benchmarks in an electronic

and transparent fashion

60

70

80

90

100

110

120

130

140

150

160

EBS Total EBS Market G3 Reuters Hotspot CME

Spot FX market

$5.3tn$5.3tn

Total FX market Total FX market

Voice

Electronic

Undistributed

$87bn $18bn

EBS Market EBS Direct

Electronic Markets – The EBS growth opportunity

Source: BIS Triannual Survey and company filings / websites

Note: Total FX market ADV for CY2013 period, and EBS ADV for LTM September 2015 (ICAP latest trading results)

25

EBS has a strong position in the spot FX IDB market…

By product By execution method

Spot

Forwards

FX Swaps

Other

$2.0tn

EBS Market /

Direct have a

sizable opportunity

in the Spot FX

market

This opportunity

expands as EBS

adds additional

products

Opportunity overview

(Average Daily Volume)

EBS vs Competitors Monthly ADV – Indexed• Building from EBS’s proven track record in

innovation, EBS has a significant opportunity to

expand its strong position in the broader FX market

− FX forwards / swaps – to be launched on EBS

Direct this year

− Corporates – currently in customer trials,

leveraging MyTreasury corporate relationships

− Asset managers – recent Molten Markets

acquisition will deepen relationships with asset

managers

… with substantial room to expand in the broader FX market

$170bn

$500bn

BrokerTec US Treasury Total US Treasury market

Electronic Markets – BrokerTec highlightsElectronic trading platform in Govt bonds and repos

Source: SIFMA and company filings / websites

Note: US Treasury ADV for CY 2014 period, and BrokerTec ADV for LTM September 2015 (ICAP latest trading results)

26

BrokerTec has a leading position in US Treasury…

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Ou

tsta

nd

ing

($

bn

)

Ve

loc

ity (

AD

V /

Ou

tsta

nd

ing

%)

… which is trading at a historic low level of velocity

BrokerTec competitive positioning / opportunity

• BrokerTec has a strong position in interbank US

Treasury, US Repo, and European Repo products

• Meaningful opportunities exist for expansion into other

fixed income instruments

• BrokerTec Direct is expected to significantly expand

customer base (asset managers, regional banks, etc.)

Benefits of combining with EBS

• BrokerTec’s recent merger with EBS provides an

opportunity to leverage EBS’s experience in

innovation and driving growth across both businesses

• Operational synergies associated with this

combination:

− Sales – EBS sales force trained to sell BrokerTec

products

− Technology – BrokerTec Direct leverages

footprint of BrokerTec Market and platform

architecture of EBS Direct

− Engineering / other – operational cost savings

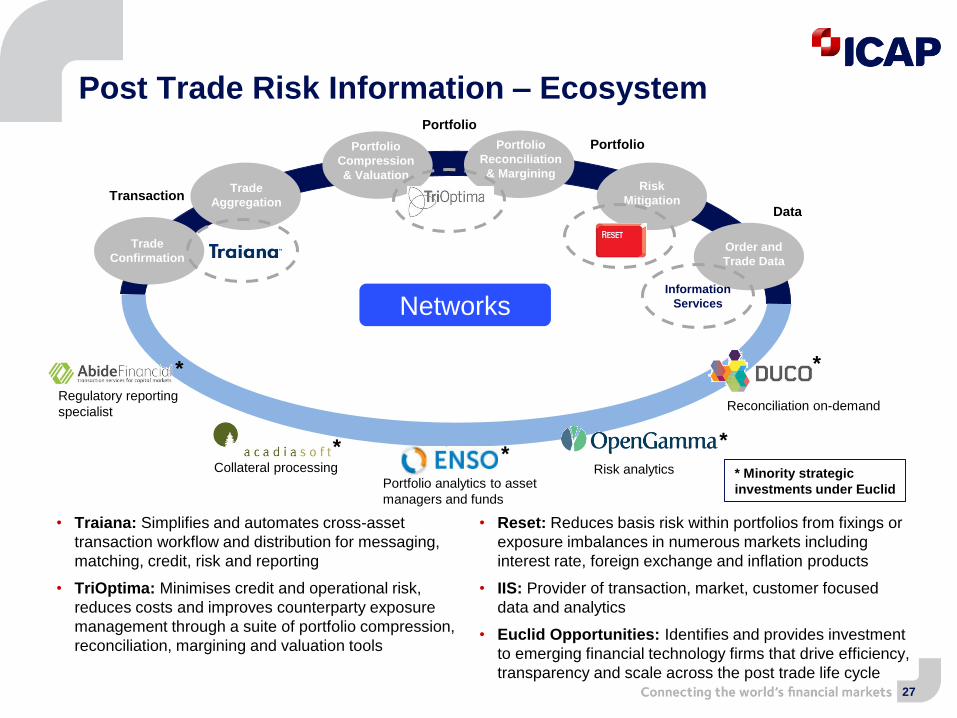

Post Trade Risk Information – Ecosystem

27

Networks

Trade

Confirmation

Trade

Aggregation

Portfolio

Compression

& Valuation

Portfolio

Reconciliation

& MarginingRisk

Mitigation

Order and

Trade Data

Transaction

Portfolio

Portfolio

Data

Information

Services

Reconciliation on-demand

Risk analyticsPortfolio analytics to asset

managers and funds

Collateral processing

Regulatory reporting

specialist

• Traiana: Simplifies and automates cross-asset

transaction workflow and distribution for messaging,

matching, credit, risk and reporting

• TriOptima: Minimises credit and operational risk,

reduces costs and improves counterparty exposure

management through a suite of portfolio compression,

reconciliation, margining and valuation tools

• Reset: Reduces basis risk within portfolios from fixings or

exposure imbalances in numerous markets including

interest rate, foreign exchange and inflation products

• IIS: Provider of transaction, market, customer focused

data and analytics

• Euclid Opportunities: Identifies and provides investment

to emerging financial technology firms that drive efficiency,

transparency and scale across the post trade life cycle

*

* **

*

* Minority strategic

investments under Euclid

Post Trade Risk Information – Performance drivers

TriOptima – revenue mix (£m)Headlines

• TriOptima: triReduce benefited from increased

portfolio compression cycles across multiple clearing

houses. triResolve recorded strong demand from

portfolio and repository reconciliations

• Traiana volumes from non-FX asset classes

continued to grow reflecting diversification in

revenues and client type

• Reset continued to face challenging conditions from

low Eurozone interest rate volatility but saw improved

demand in US and EM products at the end of the

period

Reset – volatility(1)Traiana – revenue mix (£m)

-0.2%

0.0%

0.2%

0.4%

0.6%

0.8%

1.0%

1.2%

1.4%

1.6%

1.8%

A J A O D F A J A O D F A J A O D F A J A O D F A J A

FY12 FY13 FY14 FY15 FY16

£43m £47m

£53m

£25m £26m

£0

£20

£40

£60

£80

H1 H1

FY13 FY14 FY15 FY15 FY16

FX Non-FX

Non-FX

Non-FX

£43m £44m

£54m

£67m

£29m £35m

£0

£20

£40

£60

£80

£100

H1 H1

FY12 FY13 FY14 FY15 FY15 FY16

triReduce triResolve

28

(1) 3m Euribor rate – monthly average

0%

20%

40%

60%

80%

100%

120%

140%

H1 H1

FY13 FY14 FY15 FY15 FY16

FX Non-FX

47m 41m 44m45m39m

Post Trade Risk Information – Positioned for growth

29

TriOptimaHeadlines

300

800

1,300

1,800

2,300

2,800

-

20

40

60

80

100

120

140

160

H1 H1

FY12 FY13 FY14 FY15 FY15 FY16

(nu

mb

er

of

us

ers

)

($tn

)

triReduce - compressions triResolve - active users

Traiana – average monthly transactions

• Well positioned to take advantage of key industry

trends:

− Regulation – Electronification - Standardisation

of Products and Services

• Expanding asset classes and client offering:

− Connecting triReduce to new clearing houses

− Increasing non-FX transactions in Traiana

• Growing client base:

− triResolve more than doubled number of

clients in last 2 years to 1,500+

− Traiana reported double digit growth in client

activity across all assets

• Focus on new products and services:

− Bilateral margining product – bilateral OTC

swaps regulatory requirement for margining

− triCalculate valuation product – assist banks to

measure counterparty risk

− Comprehensive Regulatory Reporting

Solutions

• Euclid will continue to focus on identifying and

nurturing emerging opportunities that compliment

the Post Trade offering

30

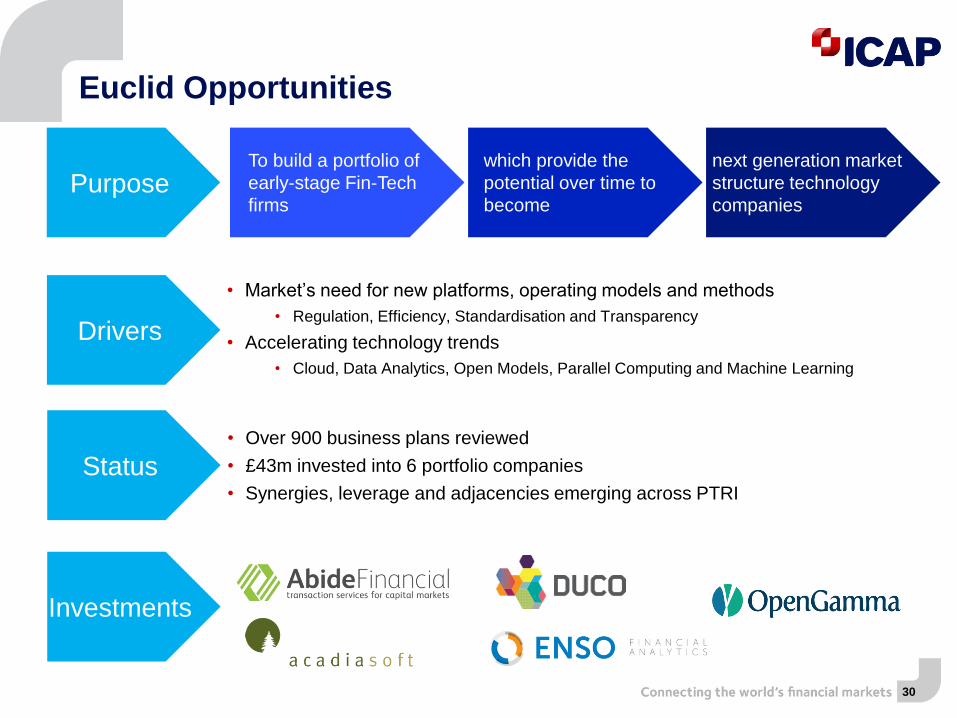

Euclid Opportunities

PurposeTo build a portfolio of

early-stage Fin-Tech

firms

which provide the

potential over time to

become

next generation market

structure technology

companies

Drivers

• Market’s need for new platforms, operating models and methods

• Regulation, Efficiency, Standardisation and Transparency

• Accelerating technology trends

• Cloud, Data Analytics, Open Models, Parallel Computing and Machine Learning

Status• Over 900 business plans reviewed

• £43m invested into 6 portfolio companies

• Synergies, leverage and adjacencies emerging across PTRI

Investments

Financial impact of the transaction

Stuart Bridges

Group Finance Director

Key financial strengths of NewCo

32

Historical revenue (£m)Financial highlights

% of revenue from new products and new customers(1)

• New products and new customers added since

FY2011 now account for over 20% of total

revenue

• Electronic markets revenues well diversified

− 29% of revenues are recurring in nature

− 36% of revenues from non-bank

customers

• Post trade risk mitigation revenues

− 50% of revenues are recurring in nature

− 5% organic revenue growth over the past

four years

• Well capitalised giving flexibility to take

advantage of growth opportunities

£98

£186 £243 £245 £246

£293 £289 £261 £257 £254 £4

£31

£51 £96 £113

£151 £172 £171 £174 £187

£102

£217

£294

£341 £359

£444 £461

£432 £431 £441

FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14 FY15

Electronic Post trade

1%

4%

8%

11%

17%

22%

FY11 FY12 FY13 FY14 FY15 1H16

(1) Based on launched / relaunched products since FY11

Electronic Markets

FY13

£m

FY14

£m

FY15

£m

% CAGR

(FY13 to

FY15)

Revenue 261 257 254 (1%)

Constant currency 254 254 (0%)

Trading operating

profit115 111 102 (6%)

Constant currency 112 110 (5%)

Trading operating

profit margin44% 43% 40%

33

Financial highlightsTrading results

Revenue by business (£m) P&L / cash investment in new products (£m)

£124 £122 £139

£128 £133 £121

£2 £2 £1 £254 £257 £261

FY15FY14FY13

EBS BrokerTec ISDX

£23 £22

£3

£16

£13 £13

FY15 FY14 FY13

Total cash spend Income statement

• This business has faced cyclical headwinds over the

past few years due to a depressed trading

environment in foreign exchange and fixed income

• Despite these headwinds, a significant level of

investment has been made in new and existing

products to drive the future growth of the business

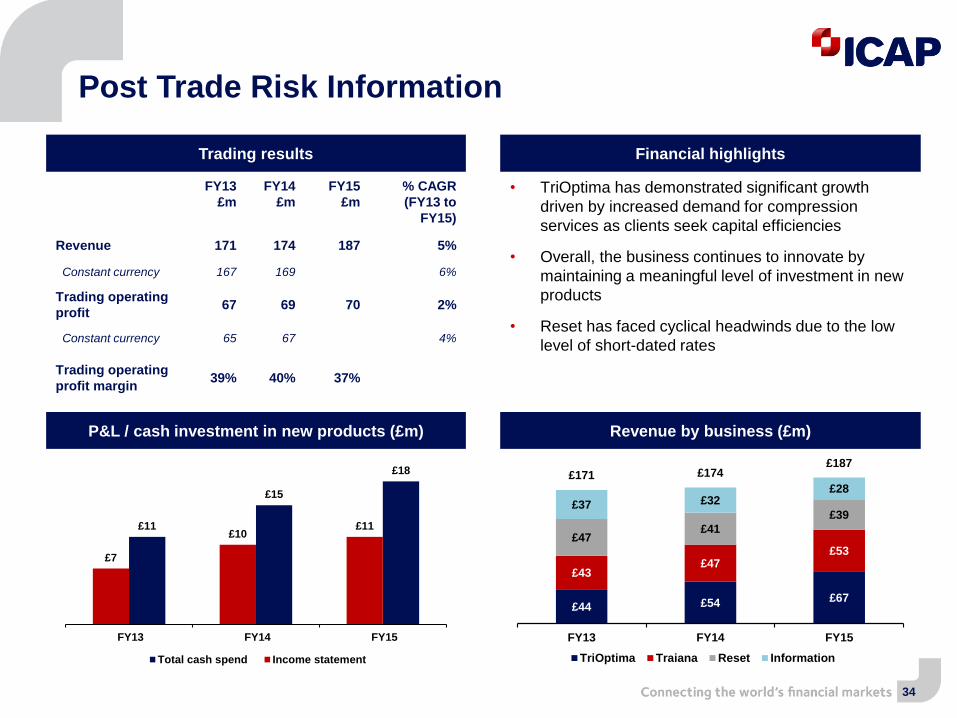

FY13

£m

FY14

£m

FY15

£m

% CAGR

(FY13 to

FY15)

Revenue 171 174 187 5%

Constant currency 167 169 6%

Trading operating

profit67 69 70 2%

Constant currency 65 67 4%

Trading operating

profit margin39% 40% 37%

Post Trade Risk Information

34

£67 £54 £44

£53 £47

£43

£39

£41 £47

£28 £32 £37

£187 £174 £171

FY15FY14FY13

TriOptima Traiana Reset Information

Financial highlightsTrading results

Revenue by business (£m) P&L / cash investment in new products (£m)

£18

£15

£11 £11 £10

£7

FY15 FY14 FY13

Total cash spend Income statement

• TriOptima has demonstrated significant growth

driven by increased demand for compression

services as clients seek capital efficiencies

• Overall, the business continues to innovate by

maintaining a meaningful level of investment in new

products

• Reset has faced cyclical headwinds due to the low

level of short-dated rates

• Balance sheet – NewCo is expected to operate with a more capital-light

business model. On completion NewCo will cease to be subject to

continuing consolidated regulatory capital requirements

• Dividend policy – Our policy is to maintain a progressive dividend in line

with our view of the underlying earnings and cash flow of NewCo

• Capex – To be in line with historical levels for the Electronic and Post

Trade businesses

35

NewCo key financials

Summary

Michael Spencer

Group Chief Executive Officer

37

Summary

• Strong investment track record – acquired NewCo businesses for

£1bn which now generate ~£170m of trading operating profit

• A portfolio of leading financial market infrastructure – major

businesses are all leading providers in respective segments

• Management team with strong track record of innovation – 20%+ of

revenues come from new products / customers in the last five years

Q&A

Appendix

Financial bridge (FY15)

40

Post Trade Risk Information (£m)Electronic Markets (£m)

£259

(£5)

£254

Current(Per ICAP)

iSwap adjustment Pro Forma

£93 £9 £102

Current(Per ICAP)

iSwap adjustment Pro Forma

£228

(£41)

£187

Current(Per ICAP)

Global Broking Dataadjustment

Pro Forma

£97

(£27)

£70

Current(Per ICAP)

Global Broking Dataadjustment

Pro Forma

Revenue bridge Revenue bridge

Trading operating profit bridge Trading operating profit bridge

41

A leading portfolio

• BrokerTec - a global electronic platform for the trading of US Treasuries, US Repos, and

European Repos. BrokerTec facilitates trading for institutions, banks and non-bank professional

trading firms.

• EBS - an electronic FX business, which is a reliable and trusted source of orderly, executable and

genuine liquidity across major and emerging market currencies. It supports multiple execution

methods and multiple ways of trading through a common distribution network.

• TriOptima - through triReduce and triResolve, is a leader in risk mitigation solutions for OTC

derivatives, primarily through the elimination and reconciliation of outstanding transactions.

• Information Services delivers independent data solutions to financial market participants,

generating subscription-based fees from a suite of products and services.

• Traiana - the leading market infrastructure for pre and post trade risk management and post trade

processing across multiple asset classes. Its robust and proven product suite automates trade

processing across the life cycle for FX, cash equities, equity swaps, futures, OTC derivatives and

fixed income.

• Reset - a provider of services that reduce the basis risk within portfolios from fixings in the interest

rate, FX and inflation derivatives and bonds markets. Basis risk results from the structure of the

instruments traded and unintended mismatches of exposure over time.

110

139129

101

72

4 25

36

4

(46) (28)

(33)

0

20

40

60

80

100

120

140

Trading

operating

profit

JVs & Associates Depreciation

&

amortisation

EBITDA Movement in

working

capital

Timing

differences

Cash from

trading

operations

Interest

&

tax

Cash from

trading operating

activities

Capex Dividends

from

associates &

invesments

Trading

free cash

flow

47

227

12

139

14

120

72

0

25

50

75

100

125

150

175

200

225

250

H1 2012/13 H2 2012/13 H1 2013/14 H2 2013/14 H1 2014/15 H2 2014/15 H1 2015/16

H1 2015/16 H2 2014/15 H1 2014/15

£m £m £m

Long term facilities (816) (811) (832)

Short term facilities and loans (55) (130) (175)

Overdrafts (7) (33) (23)

Less: undraw n 252 425 410

Gross debt (626) (549) (620)

Trading cash 453 441 413

Central cash 40 40 3

Gross cash 493 481 416

Net debt (133) (68) (204)

Restricted funds 34 43 47

** Includes net impact of unsettled items and changes in restricted funds

Free cash flow & borrowings – ICAP plc only

42

£m

Impact of trading activities on free cash flow

Historic cash conversion

**

Application of free cash flow

£m

Cash and debt

152%

22%

129%

47%

203%

12%

86%

ICAP plc

2 Broadgate, London EC2M 7UR

+44 (0) 20 7000 5000

www.icap.com

Investor Relations:Alex Dee+44 (0) 20 7050 [email protected]