Interim Presentation | 3rd quarter 2018 | 17 October 2018 › cms › 1725 ›...

22

Interim Presentation | 3rd quarter 2018 | 17 October 2018

Transcript of Interim Presentation | 3rd quarter 2018 | 17 October 2018 › cms › 1725 ›...

Interim Presentation | 3rd quarter 2018 | 17 October 2018

2

Profit after tax

624

1,867

3,449

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

Continued growth and improved profitabilityQ3 2018 highlights

Note(*): ROE = 4x profit after t in quarter / average total equity in the quarter

NOK million

Net loans

0.51.7 1.8

3.0

5.77.4

10.1

13.815.5

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

NOK million

Forward flow

Growth driven by geographical expansion

• Net loan balance up 7.4% including NOK 86 million

effect from forward flow agreement

• Loan growth of 24% in Finland vs. Q2,

corresponding to NOK 186 million in loans

• Growth of 5 % vs. Q2 reflects reduced marketing

spending – more conservative approach in Norway

due to regulatory environment

• Net interest income NOK 86.1 million,

up 5 % vs Q2’18 and up 112 % vs. Q3’17

Improved profitability driven by increasing economies of scale

• Net profit after tax up 12% vs. Q2

• Net profit YTD Q3’18 of NOK 39.3 million,

up 372.4% vs YTD Q3’17

• Investments in emerging fintech business reduce

short term company profitability

ROE 11.2%*

3

Financials

4

Key yields and margins

15

23

30

37

45

56

69

82

86

14

22

28

35

41

53

64

75 76

Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18

Net interest income Total income Net profit after tax

14.9 % 14.8 % 14.6 % 14.3 % 14.2 % 14.3 % 14.4 % 14.4 % 14.4 %

12.3 %12.7 % 12.7 % 12.8 % 12.8 % 12.8 %

8.1 %8.8 % 8.7 % 8.7 %

8.0 %7.7 % 7.8 %

8.3 %7.6 %

Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18

Annualized loan yield (Norway) * Annualized loan yield (Finland) *

Annualized NIM ***

Continued high and stable margins

Note(*): yield = weighted average effective annual yield || Note(**): actual end of quarter annual rate || Note(***): NIM = 4x NII in quarter / average total assets in quarter

Income and profit after tax

Per cent (%) NOK (million)

Total income impacted by forward flow agreement and conservative approach in Norway

5

Efficient operations with economies of scale

Note(*): cost / income ratio = operating expenses (incl. or excl. marketing) / total income

Operational expenses

NOK (million)

2.2

6.5 5.5 6.2 6.9 8.0 8.0

12.710.6

3.4

4.3 5.66.3 6.1

8.6 9.6

9.6

7.9

3.6

4.6

8.18.0 7.7

11.3

14.6

12.0

9.9

0.5

0.3

1.11.5 2.0

1.4

2.1

2.4

2.5

9.7

15.8

20.3

21.922.7

29.2

34.2

36.7

30.9

Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 18 Q1 18 Q2 18 Q3 18

Staff costs Other administrative expenses

Marketing expenses Depreciation and amortisation

Cost / Income ratio *

67%73% 72%

64%

55% 55% 53%49%

40%42%

51%

43%40%

36%34%

30%33%

27%

0%

20%

40%

60%

80%

100%

120%

Q2 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 18 Q1 18 Q2 18 Q3 18

Cost / Income Ratio Cost (excl. marketing) / Income Ratio

Temporary dip in administrative costs in the quarter

Per cent (%)

6

Satisfactory loan losses and credit quality

Stabilizing effect from forward flow agreement on NPL and gross loans PD

Note(*): loan loss ratio = LTM loan losses / average LTM net loans / 2) || Note(**): non-performing loan ratio = >PD90 / gross loans || Note(***): provision ratio = total provisions / >PD90

Gross loans past due (# of days) ProvisionsLoan losses

NOK (million)

Total provision ratio ***Loan loss ratio * Non-performing loan ratio **

Per cent (%)

3.2 %

2.9 %

2.2 %

2.2 %2.2 %2.4 %2.6 % 2.7 %

2.9 %

Q316

Q416

Q117

Q217

Q317

Q418

Q118

Q218

Q318

23.5

40.7

58.7

94.7 13

5.7 18

9.1

251.

7

332.

5

356.

6

Q216

Q316

Q416

Q117

Q217

Q317

Q418

Q118

Q218

Q318

31-60 PD 61-90 PD > 90 PD

n.a.n.a. 4.9 %

6.4 %7.1 %

7.9 %8.5 %

10.1 %10.1 %

Q316

Q416

Q117

Q217

Q317

Q418

Q118

Q218

Q318

9.913.5

18.426.3

37.3

50.7

69.5

86.4 91.9

Q316

Q416

Q117

Q217

Q317

Q418

Q118

Q218

Q318

3.1 4.2 3.7 4.9

8.3 10.9

13.8

19.1 18.8

24.5

Q216

Q316

Q416

Q117

Q217

Q317

Q418

Q118

Q218

Q318

n.a.

n.a. 31.4 %27.8 %27.5 %

26.8 %27.6 %

25.9 %25.8 %

Q316

Q416

Q117

Q217

Q317

Q418

Q118

Q218

Q318

NOK (million) NOK (million)

Per cent (%) Per cent (%)

Note(*): loan loss ratio = LTM loan losses / average LTM net loans / 2) || Note(**): non-performing loan ratio = >PD90 / gross loans || Note(***): provision ratio = total provisions / >PD90

7

638 90

3

1,13

8

1,55

6 2,04

3 2,65

2

3,05

7

3,43

4 4,23

9

157

331 33

5

339

345

522

534

548

563

794

1,2351,472

1,895

2,487

3,272

3,689

4,081

4,901

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2017 2018

Deposits by customers Subordinated loan Equity

Easy access to low-cost deposit funding

Note(*): deposit ratio = deposits / net loans

LiquidityFunding

NOK (million)

Key ratios

110

301

220 32

5

489

758

625 68

7

1,22

9

28

51

35

52

64

56

6550

84

138

352

255

377

552

814

691737

1,313

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

Debt securities Loans and advances to banks

NOK (million)

102% 108% 98% 108% 109% 113% 106% 107%123%

159% 168%153% 158% 153%

167% 160% 163%181%

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2017 2018

Deposit ratio * NSFR LCR

8

16.7

%

17.7

%

27.8

%

21.5

%

21.6

%

22.0

% 25.0

%

21.4

%

20.6

%

19.9

%

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

CET1 T1 * T2 *

Regulatory capital structure

Note(*): As of Q3 2018 NOK 46m Tier 1 (1.5% of RWA) and NOK 50m Tier 2 (2.0% of RWA) capital counts towards MONO’s capital adequacy ratios || Note(**): capital requirements (Pillar I) are weighted between Norway and Finland

Risk-weighted assetsRegulatory capital Reported capital adequacy **

CET1 Capital

Req. = 13.5%

Total Capital

Req. = 17.0 %

per cent (%)NOK (million) NOK (million)

139

309 306 302

401

583 592604 615

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2017 2018

CET1 T1 * T2 *

785

1,10

7

1,42

3

1,40

1

1,81

9

2,33

3

2,76

5 2,94

0

3,08

8

Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2016 2017 2018

75% loans 100% loans Other RWA

Note(*): As of Q3 2018 NOK 46m Tier 1 (1.5% of RWA) and NOK 50m Tier 2 (2.0% of RWA) capital counts towards MONO’s capital adequacy ratios || Note(**): capital requirements (Pillar I) are weighted between Norway and Finland

9

Strategy and

operations

10

Building a digital bank focused on consumer loans independently from scratch

*optional

Unsecured consumer loans || Deposit & saving accounts

Credit cards

Banking-as-a-service*

SAVING ACCOUNTS NORWAY AND

EUROPE

1

2

3

UNSECURED CONSUMER LOANS

NORWAY AND FINLANDCREDIT CARDS

BUSINESS SOLUTIONS

• Fee based business solution with banks

• Cooperation with partners

P2P AND POS SOLUTIONS

PHASE 1

LOAN PLATFORM

2015-2017

APP DEVELOPMENT

Diverse product portfolio in three phases

PHASE 2

CREDIT CARD

PLATFORM

2018

PHASE 3

“BANKING-AS-A

SERVICE”

2019 -

11

A scalable business model enabling both geographical and product expansion

Core

banking platform

New “fintech” products

within consumer credit

24/7 customer

experience platform

Consumer credit and

deposit accountsCredit cards

150 000

12

Combining people, technology and systems to deliver superior performance

LEAN

Only 46 full-time employees

and 5 part-time employees

SCALABLE

Organization scaled for considerable

growth in the Nordic markets

COMPETENT

Experienced staff with long track-

record within the financial sector,

technology and analytics

DILLIGENT

Organization with efficient and

hands-on execution approach

Bent H. Gjendem

CEO

Head of Customers

Product Consultant + 4 employees

Customer Support

+ 13 employees

IT Architect

IT Architect

IT Architect

Controller Head of Compliance

Head of Marketing (NO)

Head of Analytics

Head of Sales

Treasury

Head of Marketing (FI) Product Consultant

IT Architect

COO CTO CFO CRO

Head of Credit (FI)

Senior Analyst/Data Scientist

CPO

Performance Specialist

Office manager Creditcard

Product Consultant

IT Architect

IT Architect

IT Architect

Controller

On leave

Kitchen Operations consultant

Accountant

Legal Counsel

Product manager Creditcard

13

Our ambition is to deliver the best customer experience in our segment

Monobank

digital consumer banking

platform

Consumer financial

services needs

Consumer loans Credit cardpayment

Purchaseinsurance

Consumer everyday

life and goalsUtilities

Shopping

Entertainment

Travel Health

Wedding

Car

Home

Deposit

14

Consumers increasingly expect simplicity and flexibility

Source: Brett King with adjustments

The best customer

experience on core

banking services

Free and instant

person-to-person

payments

Instant access to

all your funds in a

mobile app

Instant access to

customer service

when you need it

15

Established position in digital consumer banking

-

500

1,000

1,500

2,000

2,500

3,000

3,500

Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18

Norway Finland

624

0

5,000

10,000

15,000

20,000

25,000

30,000

Q3 16 Q4 16 Q1 17 Q2 17 Q3 17 Q4 17 Q1 18 Q2 18 Q3 18

Deposit customers, NorwayLoan customers, NorwayLoan customers, FinlandDeposits customers, EuroCredit card customers, Norway

24 781

3 671

Net loans Number of customers

NOK (million) Number

* Net of NOK 86 million transferred in a forward flow agreement

3 449*

Ambition of NOK 10 bn in net loans within 3-4 years

16

Monobank’s strategy is to develop tomorrow’s solutions

Plastic cards Hybrid solutions Only digital solutions

Yesterday Today Tomorrow

17

Future growth fuelled by innovative solutions and strategic partnershipsWiderøe first partner roll-out

Gradual launch

• Monobank Mono Pay credit

card combined platform

• Widerøe branded front-end

• Launch towards employees

in September

• Campaigns in Widerøe’s owned

channels starting Q4 2018

18

Outlook and StrategyKey highlights

Profitable

organic growth

Multi-country

operation

Mono Pay / Monocard

Credit card

platform

Point-of-sale

solutions

• Attractive margins in Norway and Finland enables high organic growth

• Efficient and scalable operation

• Diligent credit risk management

= CONTINUED PROFITABLE GROWTH

No official guiding as of now. Profitable

growth will be given priority over dividend

payouts in short / medium term

KEY LONG-TERM FINANCIAL RATIOS

Dividends

Net loans of ~ NOK 3.7-3.8 bn and

Profit after tax of ~NOK 55-60m

within year-end 2018

Net loans of NOK 10 bn in 3-4 years

Net loans & Profit after tax

No official guiding as of now.

Investments in growth will impact

ROE short / medium term

Return on Equity

No official guiding as of now. SREP

initiated by the NFSA with estimated

completion by year-end 2018

Regulatory capital adequacy

• Operationalize and fine-tune the Finnish consumer loan portfolio

• Expand EUR funding through Raisin further

• Launch consumer loan business in Sweden in Q1 2019

• Innovative and flexible solution with technological edge

• Launch of joint credit card with Widerøe and Eurobonus in Q3 2018

• Monobank will continuously seek to establish new agreements with third-party partners

• Operational partner for other financial institutions

• Represents an asset light source of “other income” providing diversification

• Monobank will continuously seek to establish new agreements with third-party

partners

• Provide easy to use point-of-sale solutions online and in-store

• In discussions with Widerøe

• Monobank will continuously seek to establish new agreements with third-party partners

19

Appendix

20

Customer segmentationContinuous development and tuning of scorecards to navigate the portfolio

3%

31%

66%

Primary school

Secondary school

Higher education

25%

28%29%

14%3%

<= 34 years 35-44 years

45-54 years 55-64 years

>= 65 years

69%

31%

Home owner

Tenant

43 years4%

22%

35%

39%

NOK 250k-349k

NOK 350k-499k

NOK 500k-749k

>= NOK 750k

Age Income Education Housing Average customer

No

rway

Fin

lan

d

NOK 638k

Higher education

Home owner

43 years

NOK 454k

Higher education

Home owner

23%

30%29%

15%3%

<= 34 years 35-44 years

45-54 years 55-64 years

>= 65 years

25%

33%

28%

14%

NOK 250k-349k

NOK 350k-499k

NOK 500k-749k

>= NOK 750k

12%

8%

80%

Primary school

Secondary school

Higher education

71%

29%

Home owner

Tenant

21

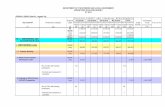

Detailed financial figuresQuarterly income statement and balance sheet

Balance SheetIncome Statement

NOK thousand2018 2017

Q3 Q2 Q1 Q4 Q3 Q2 Q1

Interest income 105,680 98,055 84,702 70,275 53,535 43,218 34,174

Interest expenses 19,549 16,358 15,940 14,365 8,953 6,110 4,305

Net interest income 86,131 81,697 68,762 55,910 44,581 37,108 29,869

Income comissions and fees 6,975 6,255 6,485 5,209 4,076 2,931 2,641

Expenses comissions and fees 16,706 12,888 19,988 7,898 7,201 5,533 4,350

Net comissions and fees -9,731 -6,633 -13,503 -2,689 -3,125 -2,603 -1,709

Total income 76,400 75,064 64,259 53,220 41,457 34,505 28,160

Income / (loss) from trading activities -348 -1,182.00 2,136.00 -459.00 -279 -246 -472

Staff costs 10,602 12,675 7,793 7,965 6,862 6,162 5,514

Other administrative expenses 7,795 21,663 24,234 19,882 13,806 14,284 13,736

- of which marketing expenses 9,958 12,018 14,598 11,311 7,705 7,992 8,133

Depreciation and amortisation 2,513 2,364 2,131 379 1,999 1,500 1,079

Total operating costs 30,868 36,702 34,158 28,226 22,666 21,946 20,329

Profit / (Loss) before impairment losses 45,184 37,181 32,237 23,536 18,511 12,313 7,359

Impairment (losses) / releases -24,524 -18,825 -19,057 -13,834 -10,946 -8,277 -4,919

Operating profit / (loss) before tax 20,660 18,356 13,180 9,702 7,565 4,036 2,440

Tax charge -5,168 -4,563 -3,122 -2,306 -1,857 -1,009 -611

Profit / (Loss) for the year 15,492 13,793 10,058 7,396 5,708 3,027 1,829

NOK thousand2018 2017

Q3 Q2 Q1 Q4 Q3 Q2 Q1

ASSETS

Loans and advances to banks 83,630 49,906 65,439 56,000 63,559 52,081 34,536

Debt securities 1,228,593 686,825 652,089 757,910 488,535 324,510 220,474

Loans and advances to customers 3,540,868 3,298,138 2,945,025 2,402,869 1,904,116 1,472,644 1,180,590

Provision for impairment losses 91,882 86,419 69,470 50,681 37,278 26,340 18,439

Net loans and advances to customers 3,448,985 3,211,719 2,875,555 2,352,188 1,866,839 1,446,304 1,162,150

Deferred tax asset - 907 5,470 8,592 8,902 10,760 11,769

Other intangible assets 62,119 55,669 47,157 39,349 31,606 27,042 19,133

Property, plant and equipment 2,104 2,072 2,094 1,755 1,675 1,513 433

Prepayments, accrued income & other

assets120,552 113,827 103,108 85,095 65,980 52,525 43,360

- of which accrued commission to agents 113,837 107,773 97,586 80,817 62,677 49,677 40,504

Other assets 1,499,150 172,475 157,829 134,791 108,163 91,841 74,695

Total assets 4,948,135 4,120,925 3,723,911 3,300,888 2,527,096 1,914,735 1,491,856

LIABILITIES & EQUITY

Deposits by customers 4,238,973 3,433,627 3,057,120 3,651,861 2,042,687 1,556,326 1,137,690

Provisions, acrruals and other liabilities 47,415 41,128 34,503 28,797 40,370 19,512 19,458

Subordinated loan 98,654 98,568 98,483 98,399 98,811 - -

Total liabilities 4,385,042 3,573,323 3,190,106 3,779,057 2,181,868 1,575,838 1,157,148

Share capital 249,196 249,196 249,196 248,318 200,746 200,746 200,461

Surplus capital 313,897 298,406 284,609 273,129 143,475 137,767 133,862

Not registered capital - - - - 622 - -

Other equity - - - 384 384 384 384

Total equity 563,093 547,602 533,805 521,831 345,228 338,897 334,708

Total liabilities and equity 4,948,135 4,120,925 3,723,911 4,300,888 2,527,096 1,914,735 1,491,856

22

Important InformationDisclaimer

22

This presentation (the “Presentation”) has been produced by Monobank ASA (the “Company”, the “Bank”, “Monobank” or “MONO”), solely for use at the presentation to investors and is strictly

confidential and may not be reproduced or redistributed, in whole or in part, to any other person. To the best of the knowledge of the Company and its board of directors, the information contained in

this Presentation is in all material respect in accordance with the facts as of the date hereof, and contains no material omissions likely to affect its import.

This Presentation contains information obtained from third parties. Such information has been accurately reproduced and, as far as the Company is aware and able to ascertain from the information

published by that third party, no facts have been omitted that would render the reproduced information to be inaccurate or misleading. This Presentation contains certain forward-looking statements

relating to the business, financial performance and results of the Company and/or the industry in which it operates. Forward-looking statements concern future circumstances and results and other

statements that are not historical facts, sometimes identified by the words “believes”, expects”, “predicts”, “intends”, “projects”, “plans”, “estimates”, “aims”, “foresees”, “anticipates”, “targets”, and

similar expressions. The forward-looking statements contained in this Presentation, including assumptions, opinions and views of the Company or cited from third party sources are solely opinions

and forecasts which are subject to risks, uncertainties and other factors that may cause actual events to differ materially from any anticipated development. None of the Company or any of their parent

or subsidiary undertakings or any such person’s officers or employees provides any assurance that the assumptions underlying such forward-looking statements are free from errors nor does any of

them accept any responsibility for the future accuracy of the opinions expressed in this Presentation or the actual occurrence of the forecasted developments. The Company assumes no obligation,

except as required by law, to update any forward-looking statements or to conform these forward-looking statements to our actual results.

AN INVESTMENT IN THE COMPANY INVOLVES RISK, AND SEVERAL FACTORS COULD CAUSE THE ACTUAL RESULTS, PERFORMANCE OR ACHIEVEMENTS OF THE COMPANY TO BE

MATERIALLY DIFFERENT FROM ANY FUTURE RESULTS, PERFORMANCE OR ACHIEVEMENTS THAT MAY BE EXPRESSED OR IMPLIED BY STATEMENTS AND INFORMATION IN THIS

PRESENTATION, INCLUDING, AMONG OTHERS, RISKS OR UNCERTAINTIES ASSOCIATED WITH THE COMPANY’S BUSINESS, SEGMENTS, DEVELOPMENT, GROWTH MANAGEMENT,

FINANCING, MARKET ACCEPTANCE AND RELATIONS WITH CUSTOMERS, AND, MORE GENERALLY, GENERAL ECONOMIC AND BUSINESS CONDITIONS, CHANGES IN DOMESTIC

AND FOREIGN LAWSAND REGULATIONS, TAXES, CHANGES IN COMPETITION AND PRICING ENVIRONMENTS, FLUCTUATIONS IN CURRENCY EXCHANGE RATES AND INTEREST

RATES AND OTHER FACTORS. SHOULD ONE OR MORE OF THESE RISKS OR UNCERTAINTIES MATERIALISE, OR SHOULD UNDERLYING ASSUMPTIONS PROVE INCORRECT,

ACTUAL RESULTS MAY VARY MATERIALLY FROM THOSE DESCRIBED IN THIS PRESENTATION. THE COMPANY DOES NOT INTEND, AND DOES NOT ASSUME ANY OBLIGATION, TO

UPDATE OR CORRECT THE INFORMATION INCLUDED IN THIS PRESENTATION.

No representation or warranty (express or implied) is made as to, and no reliance should be placed on, any information, including projections, estimates, targets and opinions, contained herein, and

no liability whatsoever is accepted as to any errors, omissions or misstatements contained herein, and, accordingly, none of the Company or any of their parent or subsidiary undertakings or any such

person’s officers or employees accepts any liability whatsoever arising directly or indirectly from the use of this document. By attending or receiving this Presentation you acknowledge that you will be

solely responsible for your own assessment of the market and the market position of the Company and that you will conduct your own analysis and be solely responsible for forming your own view of

the potential future performance of the Company’s business.

This Presentation speaks as of 17 October 2018. Neither the delivery of this Presentation nor any further discussions of the Company with any of the recipients shall, under any circumstances, create

any implication that there has been no change in the affairs of the Company since such date.