Interest rate management

22

Professor Robert B.H. Hauswald Kogod School of Business, AU FIN 683 Financial Institutions Management Measuring and Managing Interest-Rate Risk Cash-Flow Based Interest-Rate Risk Measurement • Market-value based models for assessing and managing interest rate risk: beats accounting! – Duration – Computation of duration – Economic interpretation • Immunization using duration: balance-sheet management for financial institutions – Problems in applying duration 9/18/2012 2 Duration and Immunization © Robert B.H. Hauswald

description

ALM

Transcript of Interest rate management

Professor Robert B.H. HauswaldKogod School of Business, AU

FIN 683Financial Institutions Management

Measuring and Managing Interest-Rate Risk

Cash-Flow Based Interest-Rate Risk Measurement

• Market-value based models for assessing and managing interest rate risk: beats accounting!– Duration

– Computation of duration

– Economic interpretation

• Immunization using duration: balance-sheet management for financial institutions– Problems in applying duration

9/18/2012 2Duration and Immunization © Robert B.H. Hauswald

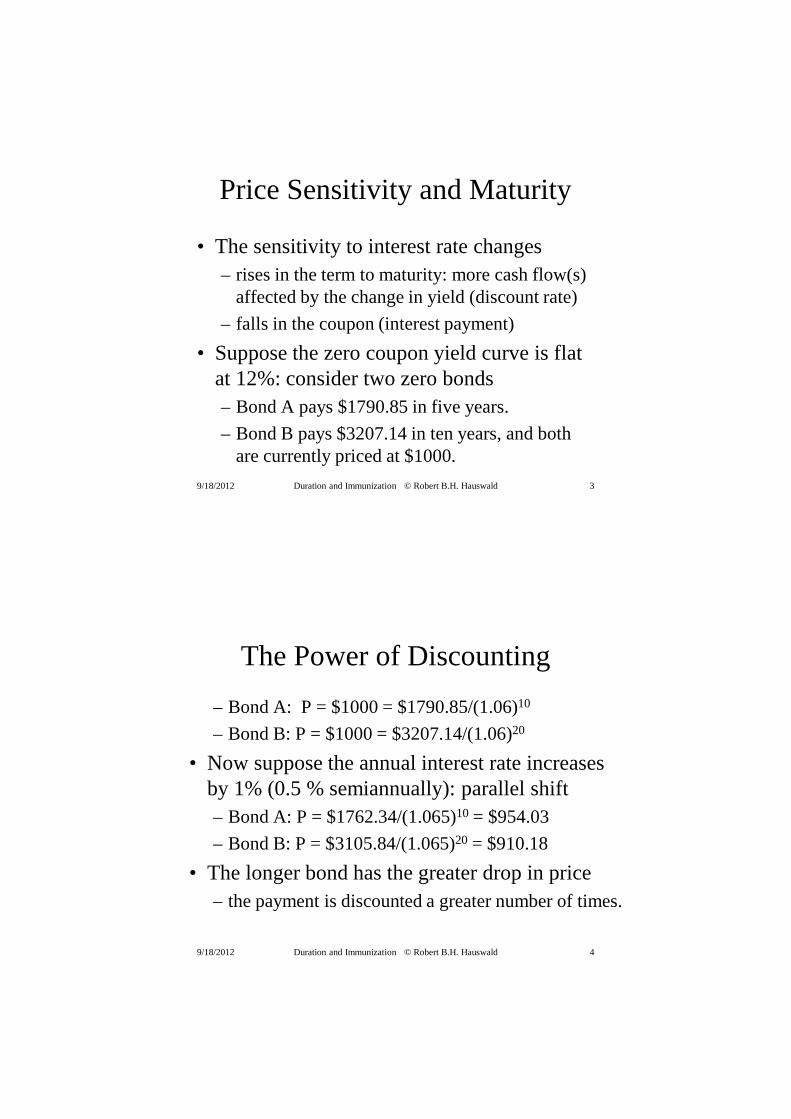

Price Sensitivity and Maturity

• The sensitivity to interest rate changes– rises in the term to maturity: more cash flow(s)

affected by the change in yield (discount rate)

– falls in the coupon (interest payment)

• Suppose the zero coupon yield curve is flat at 12%: consider two zero bonds – Bond A pays $1790.85 in five years.

– Bond B pays $3207.14 in ten years, and both are currently priced at $1000.

9/18/2012 3Duration and Immunization © Robert B.H. Hauswald

The Power of Discounting

– Bond A: P = $1000 = $1790.85/(1.06)10

– Bond B: P = $1000 = $3207.14/(1.06)20

• Now suppose the annual interest rate increases by 1% (0.5 % semiannually): parallel shift – Bond A: P = $1762.34/(1.065)10 = $954.03

– Bond B: P = $3105.84/(1.065)20 = $910.18

• The longer bond has the greater drop in price – the payment is discounted a greater number of times.

9/18/2012 4Duration and Immunization © Robert B.H. Hauswald

Coupon Effect

• Different coupons, same maturity– Bonds with identical maturities respond differently

to interest rate changes when the coupons differ.

• Notice that any coupon bond simply consists of a bundle of “zero-coupon” bonds. – With higher coupons, more of the bond’s value is

generated by earlier cash flows

– Consequently, it is less sensitive to changes in R

– again: the power of discounting

9/18/2012 5Duration and Immunization © Robert B.H. Hauswald

Fixed-Income Instruments

• In general, longer maturity bonds experience greater price changes in response to any change in the discount rate

• The range of prices is greater when the coupon is lower– A 6% bond will have a larger change in price in

response to a 2% change than an 8% bond

– The 6% bond has greater interest rate risk

9/18/2012 6Duration and Immunization © Robert B.H. Hauswald

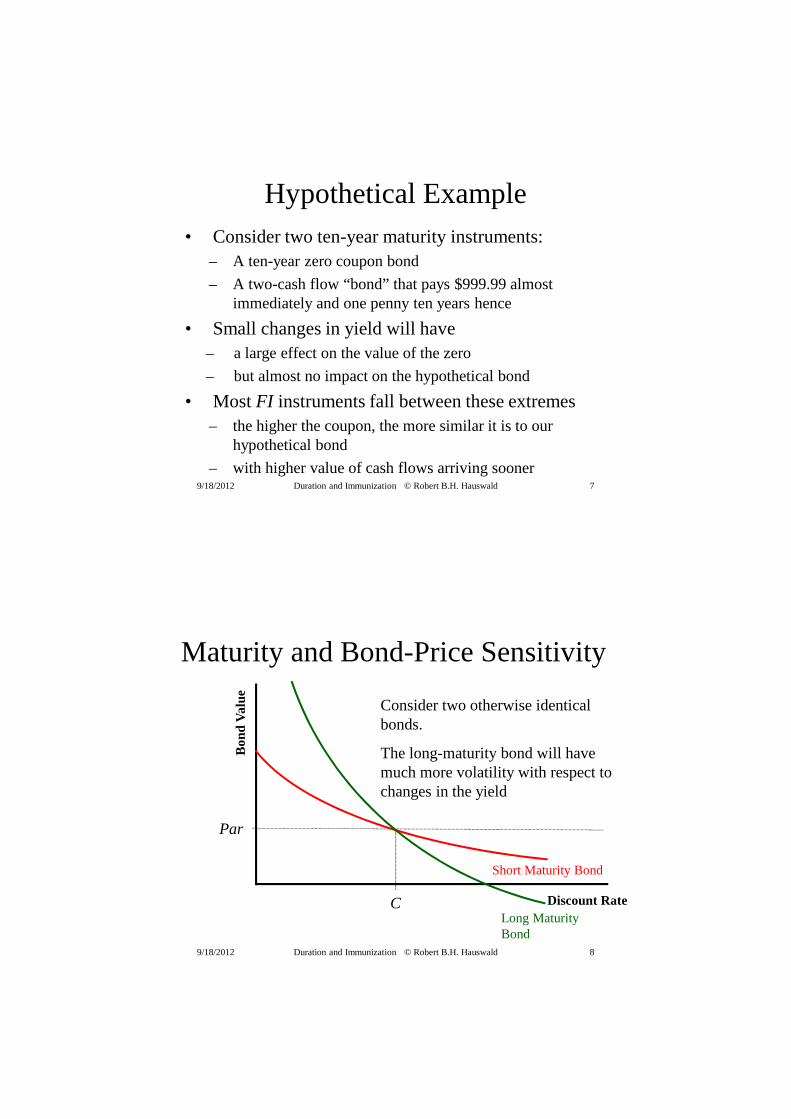

Hypothetical Example• Consider two ten-year maturity instruments:

– A ten-year zero coupon bond

– A two-cash flow “bond” that pays $999.99 almost immediately and one penny ten years hence

• Small changes in yield will have – a large effect on the value of the zero

– but almost no impact on the hypothetical bond

• Most FI instruments fall between these extremes– the higher the coupon, the more similar it is to our

hypothetical bond

– with higher value of cash flows arriving sooner9/18/2012 7Duration and Immunization © Robert B.H. Hauswald

9/18/2012 Duration and Immunization © Robert B.H. Hauswald 8

Maturity and Bond-Price Sensitivity

C

Consider two otherwise identical bonds.

The long-maturity bond will have much more volatility with respect to changes in the yield

Discount Rate

Bon

d V

alue

Par

Short Maturity Bond

Long Maturity Bond

Duration

• Weighted average time to maturity using the relative present values of cash flows as weights– takes into account the effects of differences in both

coupon rates and differences in maturity

• Based on elasticity of bond price with respect to interest rate: derivative scaled by bond price– simple differentiation of price function wrt yield

• The units of duration are years: cash-flow adjusted maturity

9/18/2012 9Duration and Immunization © Robert B.H. Hauswald

9-10

Macaulay Duration

• Formula

WhereD = Macaulay duration (in years)

t = number of periods in the future

CFt = cash flow to be delivered in t periods

N = time-to-maturity

DFt = discount factor 9/18/2012 Duration and Immunization © Robert B.H. Hauswald

Duration

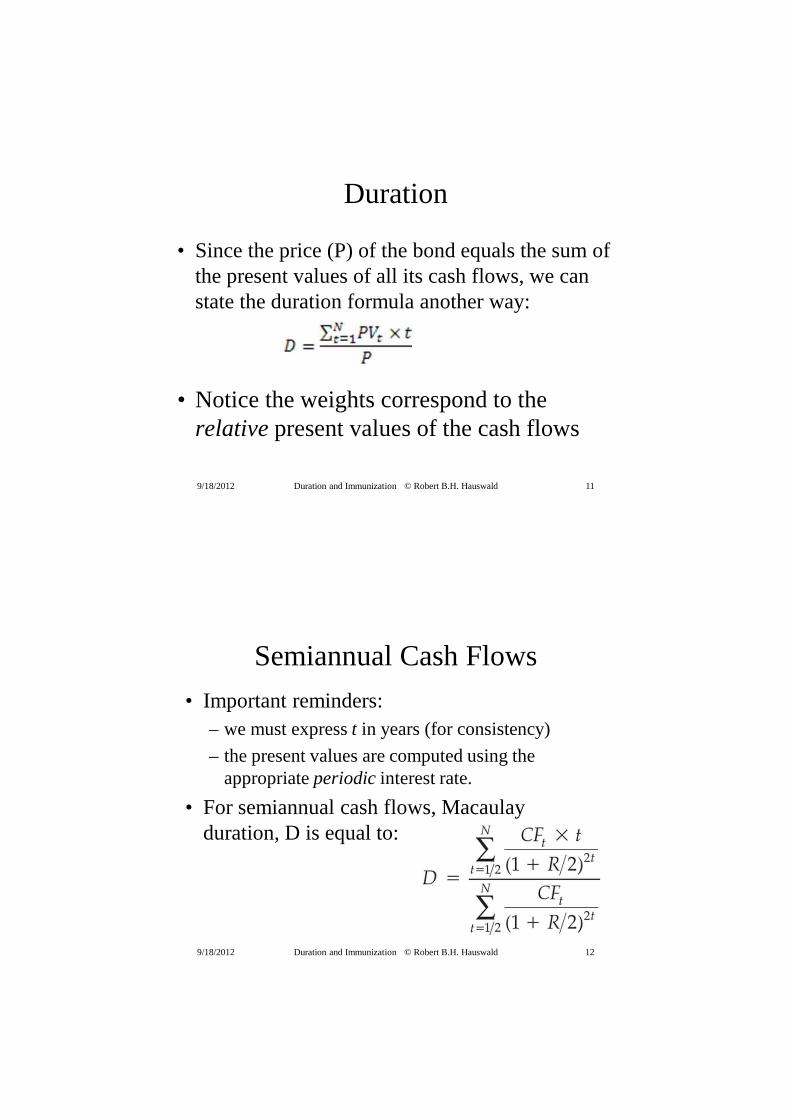

• Since the price (P) of the bond equals the sum of the present values of all its cash flows, we can state the duration formula another way:

• Notice the weights correspond to the relative present values of the cash flows

9/18/2012 11Duration and Immunization © Robert B.H. Hauswald

Semiannual Cash Flows

• Important reminders: – we must express t in years (for consistency)

– the present values are computed using the appropriate periodic interest rate.

• For semiannual cash flows, Macaulay duration, D is equal to:

9/18/2012 12Duration and Immunization © Robert B.H. Hauswald

Duration of Zero = Its Maturity

• For a zero-coupon bond, Macaulay duration equals maturity – 100% of its present value is generated by the

payment of the face value, at maturity

• For all other bonds, duration < maturity– can you see why?

9/18/2012 13Duration and Immunization © Robert B.H. Hauswald

9/18/2012 Duration and Immunization © Robert B.H. Hauswald 14

Duration and IR Sensitivity

Example

• Consider a 2-year, 8% coupon bond face – value of $1,000 and yield-to-maturity of 12%

– coupons are paid semi-annually: how many periods?

• Therefore, each coupon payment is $40 and the per period YTM is (1/2) × 12% = 6%– yield already adjusted for semi-annual compounding

• Present value of each cash flow equals CFt ÷(1+ 0.06)t where t is the period number

9/18/2012 15Duration and Immunization © Robert B.H. Hauswald

Duration of 2-Year, 8% Bond: Face Value = $1,000, YTM = 12%

t years CFt PV(CFt) Weight (W)

W × years

1 0.5 40 37.736 0.041 0.020

2 1.0 40 35.600 0.038 0.038

3 1.5 40 33.585 0.036 0.054

4 2.0 1,040 823.777 0.885 1.770

P = 930.698 1.000 D=1.883 (years)

9/18/2012 16Duration and Immunization © Robert B.H. Hauswald

Duration: Special Cases

• Consols (“perps” in the jargon): perpetual bonds issued by governments, e.g., UK – if c and y are the coupon and yield: its price?

– Maturity of a consol: M = ∞.

– Duration of a consol: D = 1 + 1/R

• Floating rate note or any other variable-interest fixed-income instrument– duration = length of reset period

– inverse floater: tricky and surprising…9/18/2012 17Duration and Immunization © Robert B.H. Hauswald

Properties of Duration

• Duration and maturity– D increases with M, but at a decreasing rate

• Duration and yield-to-maturity– D decreases as yield increases

• Duration and coupon interest– D decreases as coupon increases

• Duration is additive: how fortunate!

9/18/2012 18Duration and Immunization © Robert B.H. Hauswald

Economic Interpretation

• Duration is a measure of interest rate sensitivity or elasticity of a liability or asset:

[∆P/P] ÷ [∆R/(1+R)] = -D

• Or equivalently,

∆P/P = -D[∆R/(1+R)] = -MD ×∆R

where MD is modified duration

9/18/2012 19Duration and Immunization © Robert B.H. Hauswald

9/18/2012 Duration and Immunization © Robert B.H. Hauswald 20

Duration and Yield Sensitivity

y

$

DurationModifiedPdy

dP ⋅−=

Duration is related to the rate of change in a bonds price as its yield changes: linear (first-order) approximation of price changes in yield - let’s see what the problem is…

9/18/2012 Duration and Immunization © Robert B.H. Hauswald 21

Predicting Price Changes

1. Find Macaulay duration of bond

2. Find modified duration of bond

3. When interest rates change, the change in a bond’s price is related to the change in yield according to

– Find percentage price change of bond

– Find predicted dollar price change in bond

– Add predicted dollar price change to original price of bond

⇒ Predicted new price of bond (…or use XLS)

∆P

P×100= −Dm

* × ∆y ×100

Predicting Price Changes

• To estimate the change in price, we can express the previous equation as:

∆P = -D[∆R/(1+R)]P = -(MD) × (∆R) × (P)

• Note the direct linear relationship between ∆P and -D : what does this imply?

9/18/2012 22Duration and Immunization © Robert B.H. Hauswald

Dollar Duration

• Dollar duration equals modified duration times price– Dollar duration = MD × Price

• Using dollar duration, we can compute the change in price as

∆P = -Dollar duration ×∆R

• Allows us to compute the direct price impact of yield or interest-rate changes

9/18/2012 23Duration and Immunization © Robert B.H. Hauswald

Semi-annual Coupon Payments

• With semi-annual coupon payments the percentage change in price is given by

∆P/P = -D[∆R/(1+(R/2)]

• As always, for more frequent compounding we need to adjust– yield

– number of (time) periods

9/18/2012 24Duration and Immunization © Robert B.H. Hauswald

Managing Interest-Rate Risk

• Measuring interest-rate exposure– duration:

– potential problems?

• Managing interest-rate exposure:– principle:

– implementation?

• Overall objective:

9/18/2012 Duration and Immunization © Robert B.H. Hauswald 25

Immunization

• Matching the maturity of an asset investment with a future payout responsibility – does not necessarily eliminate interest rate risk

– but introduces fundamental principle: match assets and liabilities along risk sensitivity

• Matching durations will immunize against changes in interest rates– why?

9/18/2012 26Duration and Immunization © Robert B.H. Hauswald

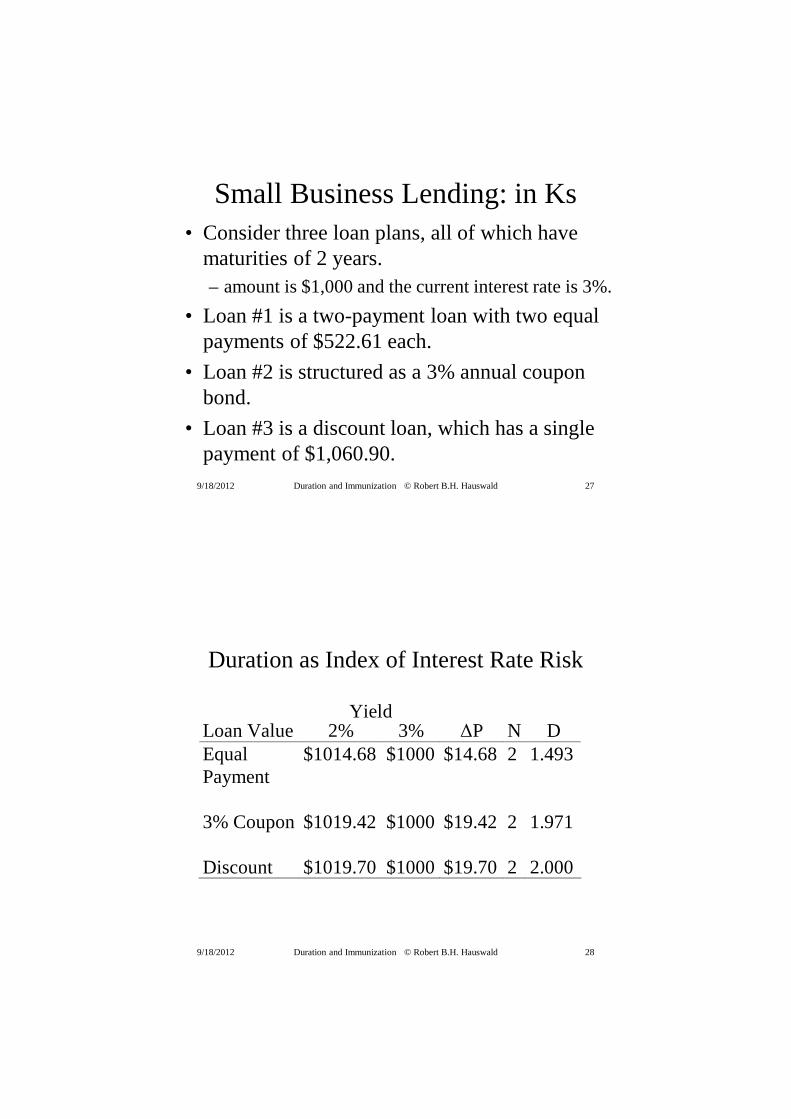

Small Business Lending: in Ks• Consider three loan plans, all of which have

maturities of 2 years. – amount is $1,000 and the current interest rate is 3%.

• Loan #1 is a two-payment loan with two equal payments of $522.61 each.

• Loan #2 is structured as a 3% annual coupon bond.

• Loan #3 is a discount loan, which has a single payment of $1,060.90.

9/18/2012 27Duration and Immunization © Robert B.H. Hauswald

Duration as Index of Interest Rate Risk

Yield Loan Value 2% 3% ∆P N D Equal Payment

$1014.68 $1000 $14.68 2 1.493

3% Coupon $1019.42 $1000 $19.42 2 1.971

Discount $1019.70 $1000 $19.70 2 2.000

9/18/2012 28Duration and Immunization © Robert B.H. Hauswald

Balance-Sheet Immunization

• Duration is a measure of the interest rate risk exposure for an FI

• If the durations of liabilities and assets are not matched, then there is a risk that – adverse changes in the interest rate will

increase the present value of the liabilities

– more than the present value of assets is increased

• Result?9/18/2012 29Duration and Immunization © Robert B.H. Hauswald

Duration Gap

• A simple FI balance sheet:– a 2-year coupon bond is the only loan asset (A)

– a 2-year certificate of deposit itsonly liability (L)

• If the duration of the bond is 1.8 years, then:

Maturity gap: MA - ML = 2 -2 = 0, but

Duration Gap: DA - DL = 1.8 - 2.0 = -0.2– Deposit has greater interest rate sensitivity than

the bond, so DGAP is negative

– FI exposed to rising interest rates9/18/2012 30Duration and Immunization © Robert B.H. Hauswald

9-31

Immunizing the Balance Sheet

• Duration Gap: the DGAP– From the balance sheet, E = A – L; therefore,

∆E = ∆A – ∆L

– reflects what management priority?

• Like for changes in bond prices, we can find the change in value of equity using duration.

∆E = [-DAA + DLL] ∆R/(1+R), or

∆E = −[DA - DLk]A(∆R/(1+R))

9/18/2012 Duration and Immunization © Robert B.H. Hauswald

Duration and Immunizing

• The formula shows 3 effects:– Leverage adjusted D-Gap

– The size of the FI

– The size of the interest rate shock

• How does each factor affect the value of a financial institution?– leverage:

– size:

– interest-rate shock:9/18/2012 32Duration and Immunization © Robert B.H. Hauswald

An Example

• Suppose DA = 5 years, DL = 3 years and rates are expected to rise from 10% to 11%. – Rates change by 1%

– balance sheet: A = 100, L = 90 and E = 10..

• Find change in E ∆Ε = −[DA - DLk]A[ ∆R/(1+R)]

= -[5 - 3(90/100)]100[.01/1.1] = - $2.09.

• Methods of immunizing balance sheet– simply adjust DA , DL or k: what is least expensive?

9/18/2012 33Duration and Immunization © Robert B.H. Hauswald

Immunization and Regulation

• Regulators set target ratios for an FI’s capital (net worth): immunize capital ratio– Capital (Net worth) ratio = E/A

• If target is to set ∆(E/A) = 0: DA = DL

– accept without proof

• But, to set ∆E = 0:– DA = kDL

• Who should managers make happy?– shows what?

9/18/2012 34Duration and Immunization © Robert B.H. Hauswald

Limitations of Duration

• Immunizing the entire balance sheet need not be costly: why not that expensive for FIs?

• Duration can be employed in combination with hedge positions to immunize

• Immunization is a dynamic process since duration depends on instantaneous R

• Large interest rate changes not accurately captured– Convexity

• More complex if nonparallel shift in yield curve– stylized facts on term structure of interest rates (TSIR)?

9/18/2012 35Duration and Immunization © Robert B.H. Hauswald

Convexity

• The duration measure is a linear approximation of a non-linear function. – If there are large changes in R, the

approximation is much less accurate.

– All fixed-income securities are convex.

• Convexity is desirable, but – greater convexity causes larger errors in the

duration-based estimate of price changes.

9/18/2012 36Duration and Immunization © Robert B.H. Hauswald

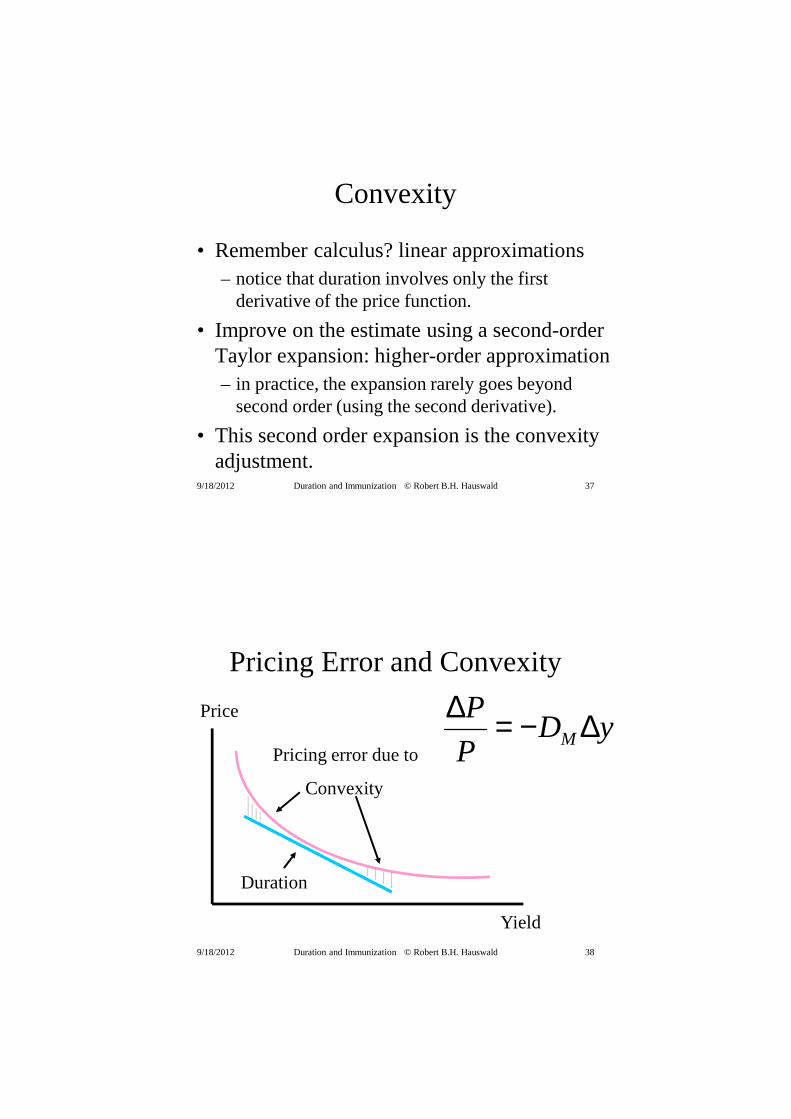

Convexity

• Remember calculus? linear approximations– notice that duration involves only the first

derivative of the price function.

• Improve on the estimate using a second-order Taylor expansion: higher-order approximation– in practice, the expansion rarely goes beyond

second order (using the second derivative).

• This second order expansion is the convexity adjustment.

9/18/2012 37Duration and Immunization © Robert B.H. Hauswald

Pricing Error and Convexity

Price

Yield

Duration

Pricing error due to

Convexity

9/18/2012 Duration and Immunization © Robert B.H. Hauswald

yDP

PM ∆−=∆

38

Modified Duration & Convexity

• Second-order approximation using convexity:

∆P/P = -D[∆R/(1+R)] + (1/2) CX (∆R)2 or ∆P/P = -MD ∆R + (1/2) CX (∆R)2

– where MD is modified duration and CX is a measure of the curvature effect.

– CX = Scaling factor × [capital loss from 1bp rise in yield + capital gain from 1bp fall in yield]

• Commonly used scaling factor is 108

9/18/2012 39Duration and Immunization © Robert B.H. Hauswald

Calculation of CX

• Convexity of a 8% coupon, 8% yield, six-year maturity Eurobond priced at $1,000 (why??)

CX = 108[∆P-/P + ∆P+/P]

= 108[(999.53785-1,000)/1,000 + (1,000.46243-1,000)/1,000)]

= 28

9/18/2012 40Duration and Immunization © Robert B.H. Hauswald

Duration Measure: Other Issues

• Default risk

• Floating-rate loans and bonds

• Duration of demand deposits and passbook savings

• Mortgage-backed securities and mortgages– Duration relationship affected by call or

prepayment provisions

9/18/2012 41Duration and Immunization © Robert B.H. Hauswald

Contingent Claims

• Interest rate changes also affect value of off-balance sheet claims

• Duration gap hedging strategy must include the effects on off-balance sheet items such as – futures, options, swaps, caps, and other

contingent claims

• In fact: derivatives widely used to adjust duration, i.e., interest-rate exposure

9/18/2012 42Duration and Immunization © Robert B.H. Hauswald

Summary

• Duration and convexity are market-value DCF based measures of interest exposure– basis for FIs’ risk and balance-sheet management

• Adjusting duration gap:– derivatives

– product pricing: how to shorten duration?

• Tension between shareholders’ and regulators’ objective: apparent conflict of interest– but do shareholders really want to be immunized?

9/18/2012 Duration and Immunization © Robert B.H. Hauswald 43

Pertinent Websites

Bank for International

Settlements

Securities Exchange

Commission

The Wall Street Journal

www.bis.org

www.sec.gov

www.wsj.com

9/18/2012 44Duration and Immunization © Robert B.H. Hauswald