INTERATIONAL FINANCIAL SYSTEM

55

-

Upload

yshuyam -

Category

Economy & Finance

-

view

152 -

download

0

Transcript of INTERATIONAL FINANCIAL SYSTEM

MEANING OF FINANCIAL SYSTEM

A financial system is a system that allows the transfer of money between

lenders and borrowers . It operates both at national and global levels .

COMPONENTS OF FINANCIAL SYSTEM

Financial system consists of four segments they are :

Financial institutions

Financial markets

Financial instruments

Financial services

FINANCIAL INSTITUTION

A financial institution is an institution that provides financial services for

its clients or members . One of the most important financial services

provided by a financial institution is acting as a financial intermediary .

Most financial institutions are regulated by the government .

TYPES OF FINANCIAL INSTITUTIONS

There are three major types of financial institutions:

Depository institutions

Contractual institutions

Investment institutions

DEPOSITORY INSTITUTIONSDeposit-taking institutions that accept and manage deposits and make loans, including banks, building societies, credit unions, trust companies, and mortgage loan companies .

CONTRACTUAL INSTITUTIONSInsurance companies and pension funds .

INVESTMENT INSTITUTIONSInvestment banks , underwriters and brokerage firms .

FINANCIAL MARKETS

A financial market is a market in which people trade financial securities ,

commodities and other fungible items of value at low transaction costs

and at prices that reflect supply and demand .

Securities include stocks & bonds .

Commodities include precious metals or agricultural products .

ROLE OF FINANCIAL MARKET

The role of financial market are as follows :

Transfer of resources

Growth in income

Productive usage

Capital formation

Price discovery

Sale mechanism

Information availability

TRANSFER OF RESOURCESFinancial markets facilitate the transfer of resources from one person to another .

GROWTH IN INCOMEFinancial markets allow lenders to earn interest/dividend on their surplus investable funds , thus , contributing to the growth in their income .

PRODUCTIVE USAGEFinancial markets allow for the productive use of the funds used in financial system thus enhancing the income and the GNP .

CAPITAL FORMATION Financial markets provide a channel through which new savings flow to aid capital formation of a country .

PRICE DISCOVERY Financial market allows the for determination of the price of the tarded financial asset through the interaction of different set of participants .

SALES MECHANISM

Financial markets provide a mechanism for selling of a financial asset by

an investor so as to offer the benefits of marketability and liquidity of

such assets .

INFORMATION AVAILABILITY

The information generated in financial market is useful to various parties

taking part in financial market .

FUNCTIONS OF FINANCIAL MARKET

The various functions of financial market are as follows :

To facilitate creation and allocation of credit and liquidity .

To serve a intermediary in the process of mobilization of savings in the

economy .

To assist the process of economic development .

To provide financial convenience to the people .

Enabling economic units co exercise their time preference .

Separation , distribution , diversification and reduction of risk .

Efficient payment mechanism .

Providing information about companies .

Providing portfolio management services .

FINANCIAL INSTRUMENTS

A financial instrument is a tradable asset of any kind ; either cash ,

evidence of an ownership interest in an entity , or a contractual right to

receive or deliver cash or another financial instrument .

FEATURES OF FINANCIAL INSTRUMENTS

The features of financial instruments are :

Easy transferability

Ready market

Possess liquidity

Possess security value

Enjoy tax status

Carry risk

Facilitate futures trading

Less handling costs

Risk and return proportionate

Maturity period variations

TYPES OF FINANCIAL INSTRUMENTS

Financial instruments can be classified as :

Cash instruments

Derivative instrument

CASH INSTRUMENTS

They are financial instruments whose value is determined directly by the

markets . They can be securities , which are readily transferable, and

instruments such as loans and deposits , where both borrower and lender

have to agree on a transfer.

DERIVATIVE INSTRUMENTS

They are financial instruments which derive their value from the value

and characteristics of one or more underlying entities such as an asset ,

index , or interest rate. They can be exchange-traded derivatives and

over-the-counter (OTC) derivatives .

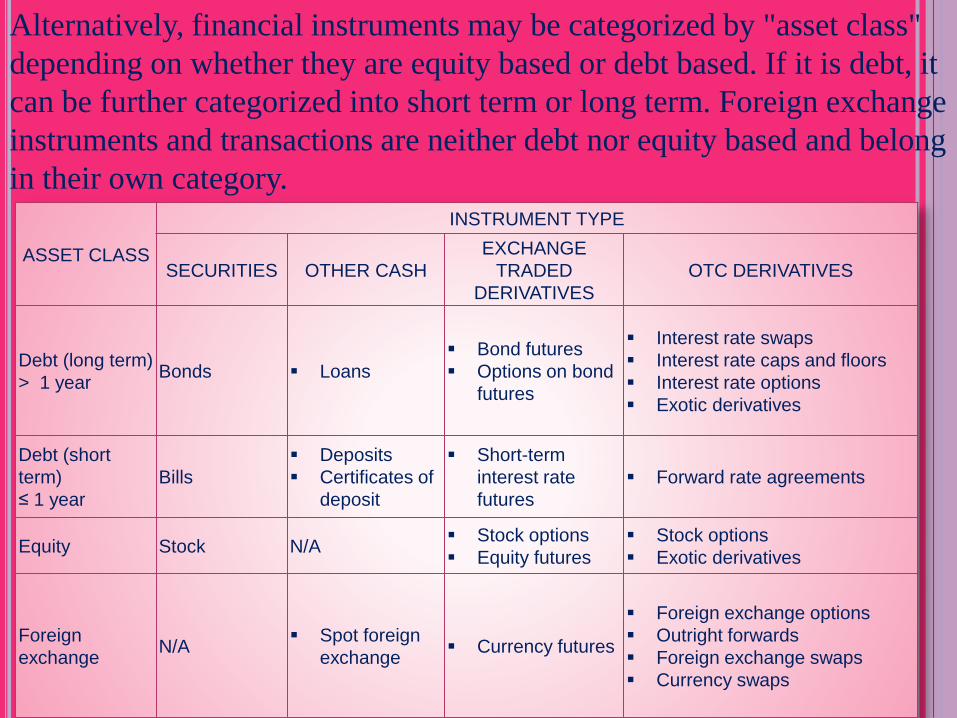

ASSET CLASS

INSTRUMENT TYPE

SECURITIES OTHER CASH

EXCHANGE

TRADED

DERIVATIVES

OTC DERIVATIVES

Debt (long term)

> 1 yearBonds Loans

Bond futures

Options on bond

futures

Interest rate swaps

Interest rate caps and floors

Interest rate options

Exotic derivatives

Debt (short

term)

≤ 1 year

Bills

Deposits

Certificates of

deposit

Short-term

interest rate

futures

Forward rate agreements

Equity Stock N/A Stock options

Equity futures

Stock options

Exotic derivatives

Foreign

exchangeN/A

Spot foreign

exchange Currency futures

Foreign exchange options

Outright forwards

Foreign exchange swaps

Currency swaps

Alternatively, financial instruments may be categorized by "asset class"

depending on whether they are equity based or debt based. If it is debt, it

can be further categorized into short term or long term. Foreign exchange

instruments and transactions are neither debt nor equity based and belong

in their own category.

FINANCIAL SERVICES

Financial services are the economic services provided by the finance

industry, which encompasses a broad range of businesses that manage

money, including credit unions, banks, credit-card companies, insurance

companies, accountancy companies, consumer-finance companies, stock

brokerages , investment funds and some government-sponsored

enterprises .

TYPES OF FINANCIAL SERVICES

The types of financial services are :

Commercial banking services

Investment banking services

Foreign exchange services

Investment services

Insurance services

Other financial services

COMMERCIAL BANKING SERVICES

Keeping money safe while also allowing withdrawals when needed

Issuance of cheque books so that bills can be paid and other kinds of payments can be delivered by post

Provide personal loans, commercial loans, and mortgage loans (typically loans to purchase a home, property or business)

Issuance of credit cards and processing of credit card transactions and billing

Issuance of debit cards for use as a substitute for cheques .

Allow financial transactions at branches or by using Automatic Teller Machines (ATMs)

Provide wire transfers of funds and Electronic fund transfers between banks

Facilitation of standing orders and direct debits, so payments for bills can be made automatically

Provide overdraft agreements for the temporary advancement of the

bank's own money to meet monthly spending commitments of a

customer in their current account.

Provide internet banking system to facilitate the customers to view and

operate their respective accounts through internet.

Provide charge card advances of the bank's own money for customers

wishing to settle credit advances monthly.

Provide a check guaranteed by the bank itself and prepaid by the

customer, such as a cashier's check or certified check .

INVESTMENT BANKING SERVICES

Capital markets services - underwriting debt and equity , assist company deals (advisory services, underwriting, mergers and acquisitions and advisory fees), and restructure debt into structured finance products.

Private banking - Private banks provide banking services exclusively to high-net-worth individuals . Many financial services firms require a person or family to have a certain minimum net worth to qualify for private banking services. Private banks often provide more personal services, such as wealth management and tax planning, than normal retail banks.

Brokerage services - facilitating the buying and selling of financial securities between a buyer and a seller. In today's (2014) stock brokers, brokerages services are offered online to self trading investors throughout the world who have the option of trading with 'tied' online trading platforms offered by a banking institution or with online trading platforms sometimes offered in a group by so-called online trading portals .

FOREIGN EXCHANGE SERVICESForeign exchange services are provided by many banks and specialist foreign exchange

brokers around the world. Foreign exchange services include:

Currency exchange - where clients can purchase and sell foreign currency banknotes.

Wire transfer - where clients can send funds to international banks abroad.

Remittance - where clients that are migrant workers send money back to their home

country.

INVESTMENT SERVICES Investment management - the term usually given to describe companies which run

collective investment funds. Also refers to services provided by others, generally

registered with the Securities and Exchange Commission as Registered Investment

Advisors. Investment banking financial services focus on creating capital through

client investments.

Hedge fund management - Hedge funds often employ the services of "prime

brokerage" divisions at major investment banks to execute their trades.

Custody services - the safe-keeping and processing of the world's securities trades

and servicing the associated portfolios. Assets under custody in the world are

approximately US$100 trillion.

INSURANCE SERVICES Insurance brokerage - Insurance brokers shop for insurance (generally

corporate property and casualty insurance) on behalf of customers. Recently a number of websites have been created to give consumers basic price comparisons for services such as insurance, causing controversy within the industry.

Insurance underwriting - Personal lines insurance underwriters actually underwrite insurance for individuals, a service still offered primarily through agents, insurance brokers, and stock brokers . Underwriters may also offer similar commercial lines of coverage for businesses. Activities include insurance and annuities, life insurance, retirement insurance, health insurance, and property & casualty insurance .

F&I - Finance & Insurance, a service still offered primarily at asset dealerships. The F&I manager encompasses the financing and insuring of the asset which is sold by the dealer. F&I is often called "the second gross" in dealerships who have adopted the model

Reinsurance - Reinsurance is insurance sold to insurers themselves, to protect them from catastrophic losses.

OTHER FINANCIAL SERVICES Bank cards - include both credit cards and debit cards. According to

the Nilson Report, Bank Of America is the largest issuer of bank cards.

Credit card machine services and networks - Companies which provide credit card machine and payment networks call themselves "merchant card providers".

Intermediation or advisory services - These services involve stock brokers (private client services) and discount brokers. Stock brokers assist investors in buying or selling shares. Primarily internet-based companies are often referred to as discount brokerages, although many now have branch offices to assist clients. These brokerages primarily target individual investors. Full service and private client firms primarily assist and execute trades for clients with large amounts of capital to invest, such as large companies, wealthy individuals, and investment management funds.

Private equity - Private equity funds are typically closed-end funds, which usually take controlling equity stakes in businesses that are either private, or taken private once acquired. Private equity funds often use leveraged buyouts (LBOs) to acquire the firms in which they invest. The most successful private equity funds can generate returns significantly higher than provided by the equity markets.

Venture capital is a type of private equity capital typically provided by professional, outside investors to new, high-growth-potential companies in the interest of taking the company to an IPO or trade sale of the business.

Angel investment - An angel investor or angel (known as a business angel or informal investor in Europe), is an affluent individual who provides capital for a business start-up, usually in exchange for convertible debt or ownership equity. A small but increasing number of angel investors organize themselves into angel groups or angel networks to share resources and pool their investment capital.

Conglomerates - A financial services company, such as a universal bank, that is active in more than one sector of the financial services market e.g. life insurance, general insurance, health insurance, asset management, retail banking, wholesale banking, investment banking, etc. A key rationale for the existence of such businesses is the existence of diversification benefits that are present when different types of businesses are aggregated i.e. bad things don't always happen at the same time. As a consequence, economic capital for a conglomerate is usually substantially less than economic capital is for the sum of its parts.

Financial market utilities - Organizations that are part of the

infrastructure of financial services, such as stock exchanges, clearing

houses, derivative and commodity exchanges and payment systems

such as real-time gross settlement systems or interbank networks .

Debt resolution is a consumer service that assists individuals that have

too much debt to pay off as requested, but do not want to file

bankruptcy and wish to pay off their debts owed. This debt can be

accrued in various ways including but not limited to personal loans,

credit cards or in some cases merchant accounts.

PARTICIPANTS OF FINANCIAL SYSTEM

The participants and players of financial system are :

Individuals

Firms or Corporates

Government

Regulators

Market intermediaries

INDIVIDUALS

These are net savers and purchase the securities issued by corporates .

Individuals provide funds by subscribing to these securities or by making

other investments .

FIRMS AND CORPORATES

The corporate are net borrowers . They require funds for different

projects from time to time . They offer different types of securities to suit

the risk preferences of investors . Sometimes , the corporates invest

excess funds , as individuals do . The funds raised by issue of securities

are invested in real assets like plant and machinery . The income

generated by these real assets is distributed as interest or dividends to the

investors who own the securities .

GOVERNMENT

Government may borrow funds to take care of the budget deficit or as a

measure of controlling the liquidity etc., Government may require funds

for long terms or short terms in the money market .

Government makes initial investments in public sector enterprises by

subscribing to the shares , however , these investment (shares) may be

sold to public through the process of disinvestments .

REGULATORS

Financial system is regulated by different government agencies . The

relationships among other participants , the trading mechanism and the

overall flow of funds are managed , supervised and controlled by these

statutory agencies .

In India , two basic agencies regulating the financial market are :

RBI

SEBI

Besides , there is an array of legislations and government departments

also regulate the operations in the financial system .

MARKET INTERMEDIARIES

There are a number of market intermediaries known as financial

intermediaries or merchant bankers , operating in financial system .

These are also known as investment managers or investment bankers .

The objective of these intermediaries is to smoothen the process of

investment and to establish a link between the investors and the users of

funds . Market intermediaries help investors to select investments by

providing investment consultancy , market analysis and credit rating of

investment instruments .

Some of the market intermediaries are clearing corporations , share

brokers , credit rating agencies , underwriters , portfolio managers ,

mutual funds , investment companies .

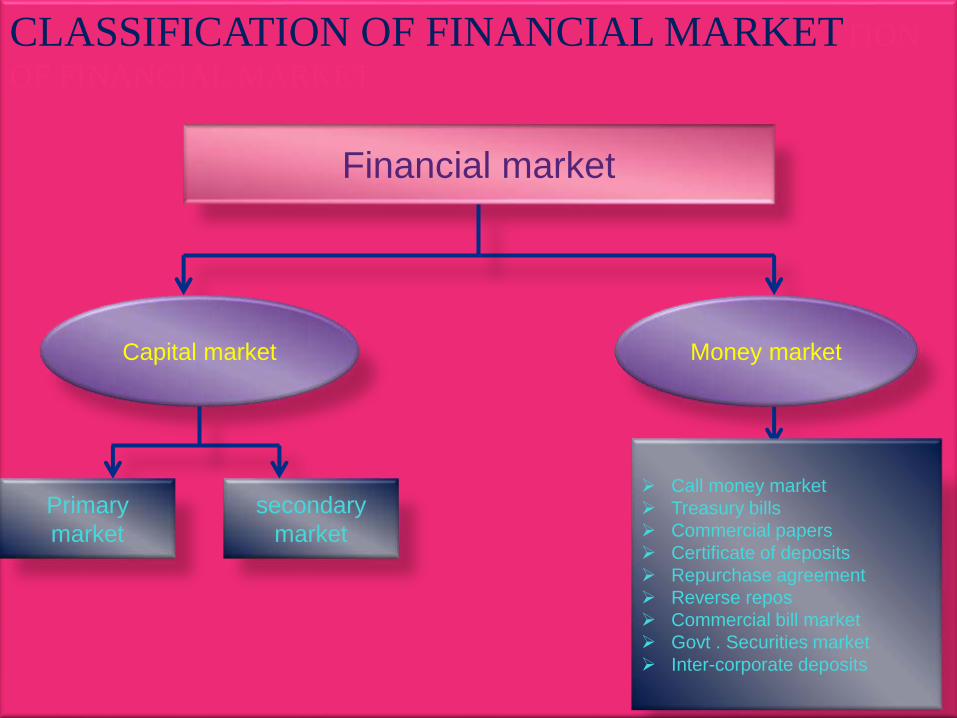

CLASSIFICATION OF FINANCIAL MARKETTION

OF FINANCIAL MARKET

Financial market

Capital market Money market

Primary

market

secondary

market

Call money market

Treasury bills

Commercial papers

Certificate of deposits

Repurchase agreement

Reverse repos

Commercial bill market

Govt . Securities market

Inter-corporate deposits

MEANING OF CAPITAL MARKET

Capital market is a place where the medium-term and long-term financial

needs of business and other undertakings are met by financial institutions

which supply medium and long-term resources to borrowers .

FEATURE OF CAPITAL MARKET

The features of capital market are as follows :

It deals in long and medium term funds .

It acts as a link between savers and investors .

It makes funds available to industrial and commercial undertakings .

It helps in mobilizing the savings on a large scale .

It helps in the capital formation in the country .

It helps in effective distribution of the mobilized funds for balanced

economic development .

TYPES OF CAPITAL MARKET

the types of capital market are :

Primary market

Secondary market

PRIMARY MARKET

The primary market is the part of the capital market that deals with

issuing of new security finance securities. Companies, government or

public sector institutions can obtain funds through the sale of a new stock

or bond issues through primary market.

SECONDARY MARKET

The secondary market is the financial market in which previously issued

financial instruments such as stock or bonds are bought and sold .

MONEY MARKET

Money market refers to the market where money and highly liquid

marketable securities are bought and sold having a maturity period of

one or less than one year .

FEATURE OF MONEY MARKET

The features of money market are :

It is a market purely for short-term funds or financial assets called near

money .

It deals with financial assets having a maturity period of one year .

It provides room for overcoming short-term deficits .

It deals with only those assets which can be converted into cash readily

without loss and with minimum transaction cost .

Transactions have to be conducted without the help of brokers .

It helps in maintaining monetary equilibrium .

INSTRUMENTS OF MONEY MARKET Certificate of deposit – Time deposit, commonly offered to consumers

by banks, thrift institutions, and credit unions.

Repurchase agreements – Short-term loans—normally for less than two weeks and frequently for one day—arranged by selling securities to an investor with an agreement to repurchase them at a fixed price on a fixed date.

Commercial paper – Short term use of promissory notes issued by company at discount to face value and redeemed at face value

Eurodollar deposit – Deposits made in U.S. dollars at a bank or bank branch located outside the United States.

Federal agency short-term securities – In the U.S., short-term securities issued by government sponsored enterprises such as the Farm Credit System , the Federal Home Loan Banks and the Federal National Mortgage Association .

Federal funds – In the U.S., interest-bearing deposits held by banks and other depository institutions at the Federal Reserve ; these are immediately available funds that institutions borrow or lend, usually on an overnight basis. They are lent for the federal funds rate.

Municipal notes – In the U.S., short-term notes issued by

municipalities in anticipation of tax receipts or other revenues.

Treasury bills – Short-term debt obligations of a national government

that are issued to mature in three to twelve months.

Money funds – Pooled short-maturity, high-quality investments which

buy money market securities on behalf of retail or institutional

investors.

Foreign exchange swaps – Exchanging a set of currencies in spot date

and the reversal of the exchange of currencies at a predetermined time

in the future.

Short-lived mortgage- and asset-backed securities

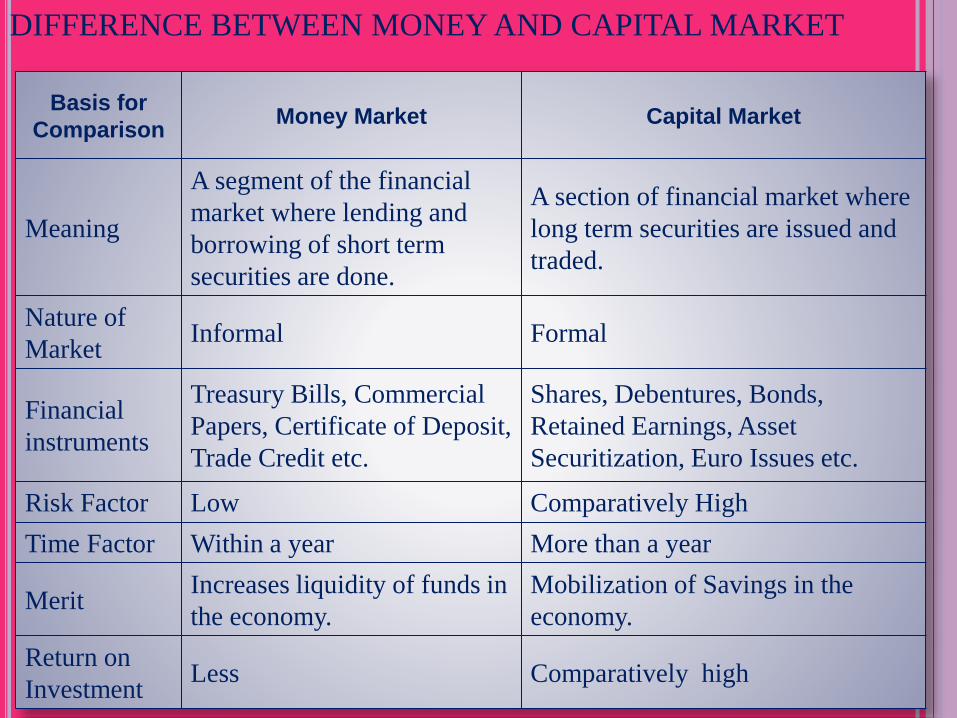

DIFFERENCE BETWEEN MONEY AND CAPITAL MARKET

Basis for

ComparisonMoney Market Capital Market

Meaning

A segment of the financial

market where lending and

borrowing of short term

securities are done.

A section of financial market where

long term securities are issued and

traded.

Nature of

MarketInformal Formal

Financial

instruments

Treasury Bills, Commercial

Papers, Certificate of Deposit,

Trade Credit etc.

Shares, Debentures, Bonds,

Retained Earnings, Asset

Securitization, Euro Issues etc.

Risk Factor Low Comparatively High

Time Factor Within a year More than a year

MeritIncreases liquidity of funds in

the economy.

Mobilization of Savings in the

economy.

Return on

InvestmentLess Comparatively high

FOREX MARKET

The foreign exchange market (forex, FX, or currency market) is a global

decentralized market for the trading of currencies. This includes all

aspects of buying, selling and exchanging currencies at current or

determined prices. In terms of volume of trading, it is by far the largest

market in the world.

EURO CURRENCY MARKET

'Eurocurrency Market' The money market in which Eurocurrency,

currency held in banks outside of the country where it is legal

tender, is borrowed and lent by banks in Europe.

EURO BOND MARKET

A market in which bonds are issued in the capital market of one country

to a non-resident borrower from another country .

Eurobonds are bonds that are sold in countries other than the country of

the currency denominating the bonds .

FORWARD MARKET

The forward market is over-the-counter financial market in contracts for

future delivery .

A forward contract is a non-standardized contract between two parties to

buy or to sell an asset at a specified future time at a price agreed upon

today .

FUTURE MARKET

An agreement to buy or sell a specific amount of a commodity or

financial instrument at a particular price on a stipulated future date ; the

contract can be sold before the settlement date .

IMF

The International Monetary Fund (IMF) is an international organization headquartered in Washington, DC, of "188 countries working to foster global monetary cooperation, secure financial stability, facilitate international trade, promote high employment and sustainable economic growth, and reduce poverty around the world". Formed in 1944 at the Bretton Woods Conference, it came into formal existence in 1945 with 29 member countries and the goal of reconstructing the international payment system. Countries contribute funds to a pool through a quota system from which countries with payment imbalances can borrow. As of 2010, the fund had XDR476.8 billion, about US$755.7 billion at then-current exchange rates.

Through this fund, and other activities such as statistics keeping and analysis, surveillance of its members' economies and the demand for self-correcting policies, the IMF works to improve the economies of its member countries .The organization's objectives stated in the Articles of Agreement are: to promote international economic cooperation, international trade, employment, and exchange-rate stability, including by making financial resources available to member countries to meet balance-of-payments needs.

LOGO

BUILDING OF IMF

Membership: 188 countries

Headquarters: Washington, D.C.

Executive Board: 24 Directors each representing a single country or a

group of countries

Staff: Approximately 2,600 from 147 countries

Total quotas: US$327 billion (as of 3/13/15)

Additional pledged or committed resources: US$ 885 billion

Committed amounts under current lending arrangements (as of

3/13/15): US$163 billion, of which US$137 billion have not been

drawn (see table).

Biggest borrowers (amounts outstanding as of 3/13/15): Portugal,

Greece, Ireland, Ukraine

Biggest precautionary loans (amount agreed as of 3/13/15): Mexico,

Poland, Colombia, Morocco

Surveillance consultations: 122 consultations in 2013 and 129 in 2014

Technical assistance: 274 person years in FY2013 and 285 in FY2014

OBJECTIVES OF IMF

To promote international monetary cooperation.

To facilitate the expansion of international trade.

To ensure stability to foreign exchange rates.

To reduce disequilibrium in the international balance of payments of

member countries.

To promote capital investment in backward and underdevelopment

countries.

To assist in the establishment of a multinational system of payments in

respect of current transactions between the member countries.

To secure multilateral convertibility (i.e., to convert the currency of

any member into the currency of any other member).

To provide short term monetary help to members during emergency.

To achieve balanced economic growth and high level of employment

in member countries.

WORLD BANK

The World Bank is an international financial institution that provides

loans to developing countries for capital programs . It comprises two

institutions: the International Bank for Reconstruction and Development

(IBRD) and the International Development Association (IDA). The

World Bank is a component of the World Bank Group, and a member of

the United Nations Development Group.

The World Bank's official goal is the reduction of poverty. According to

its Articles of Agreement, all its decisions must be guided by a

commitment to the promotion of foreign investment and international

trade and to the facilitation of Capital investment .

MottoWorking for a World Free of

Poverty

FormationJuly 1944; 71 years

ago (1944-07)

TypeMonetary International

Financial Organization

Legal status Treaty

Purpose Crediting

HeadquartersWashington D.C., United

States

Region Worldwide

Membership188 countries (IBRD)

172 countries (IDA)

Parent organization World Bank Group

OBJECTIVES OF WORLD BANK

To provide long-run capital to member countries for economic

reconstruction and development.

To induce long-run capital investment for assuring Balance of

Payments equilibrium and balanced development of international

trade.

To provide guarantee for loans granted to small and large units and

other projects of member countries.

To ensure the implementation of development projects so as to bring

about a smooth transference from a war-time to peace economy.

To promote capital investment in member countries by the following

ways:

To provide guarantee on private loans or capital investment.

If private capital is not available even after providing guarantee, then

IBRD provides loans for productive activities on considerate

conditions.

FUNCTIONS OF WORLD BANK

Granting reconstruction loans to war devastated countries

Granting development loans to developing countries .

To make sure of availability of funds .

Providing loans to governments for agriculture , irrigation , power ,

transport , water supply , education , life and health .

Providing loans to private specified projects .

Promoting foreign investment by guaranteeing loans provided by other

organizations .

Provide technical , monetary , fiscal advice to member countries for

specified projects .

Encouraging industrial development of UDC’s by encouraging

economic reforms .

WTOThe World Trade Organization (WTO) is an intergovernmental organization which regulates international trade. The WTO officially commenced on 1 January 1995 under the Marrakesh Agreement, signed by 123 nations on 15 April 1994, replacing the General Agreement on Tariffs and Trade (GATT), which commenced in 1948.[5] The WTO deals with regulation of trade between participating countries by providing a framework for negotiating trade agreements and a dispute resolution process aimed at enforcing participants' adherence to WTO agreements, which are signed by representatives of member governments[6]:fol.9–10 and ratified by their parliaments. Most of the issues that the WTO focuses on derive from previous trade negotiations, especially from the Uruguay Round (1986–1994).

The WTO is attempting to complete negotiations on the Doha Development Round, which was launched in 2001 with an explicit focus on developing countries. As of June 2012, the future of the Doha Round remained uncertain: the work program lists 21 subjects in which the original deadline of 1 January 2005 was missed, and the round is still incomplete

The conflict between free trade on industrial goods and services

but retention of protectionism on farm subsidies to domestic

agricultural sector (requested by developed countries) and the

substantiation of fair trade on agricultural products (requested by

developing countries) remain the major obstacles. This impasse

has made it impossible to launch new WTO negotiations beyond

the Doha Development Round. As a result, there have been an

increasing number of bilateral free trade agreements between

governments. As of July 2012, there were various negotiation

groups in the WTO system for the current agricultural trade

negotiation which is in the condition of stalemate.

The WTO's current Director-General is Roberto Azevêdo ,who

leads a staff of over 600 people in Geneva, Switzerland. A trade

facilitation agreement known as the Bali Package was reached by

all members on 7 December 2013, the first comprehensive

agreement in the organization's history.

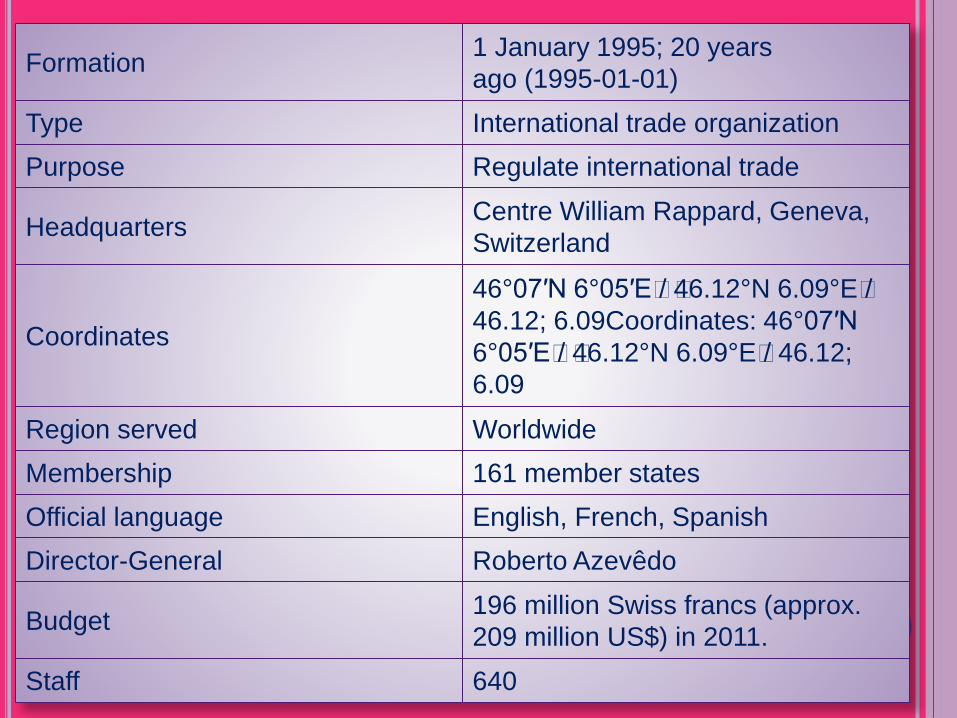

Formation1 January 1995; 20 years

ago (1995-01-01)

Type International trade organization

Purpose Regulate international trade

HeadquartersCentre William Rappard, Geneva,

Switzerland

Coordinates

46°07′N 6°05′E/ 46.12°N 6.09°E/

46.12; 6.09Coordinates: 46°07′N

6°05′E/ 46.12°N 6.09°E/ 46.12;

6.09

Region served Worldwide

Membership 161 member states

Official language English, French, Spanish

Director-General Roberto Azevêdo

Budget196 million Swiss francs (approx.

209 million US$) in 2011.

Staff 640

OBJECTIVES OF WTO

To reduce the restriction on trade and service barrier .

To raise the standard of living .

To promote full employment .

To expand production and trade .

To optimize utilization of world resources .

To sustainable development and environment to gather .

To secure better share of growth and developing countries in the world

trade .

To remove multilateral trade agreements .

FUNCTIONS OF WTO

It promotes welfare of the people .

To improve the quality of life .

To develop region socially , culturally , economically .

It promotes and strengthens collective self-reliance among the

developing countries .

It strengthens co-operation with other developing countries .

It co-operates with international and regional organizations with

similar aims and purposes .

It maintains trade related data base .

It creates and enhances mutual trust , understanding and application of

one another issues .

IFC

The International Finance Corporation (IFC) is an international financial institution that offers investment, advisory, and asset management services to encourage private sector development in developing countries. The IFC is a member of the World Bank Group and is headquartered in Washington, D.C., United States. It was established in 1956 as the private sector arm of the World Bank Group to advance economic development by investing in strictly for-profit and commercial projects that purport to reduce poverty and promote development. The IFC's stated aim is to create opportunities for people to escape poverty and achieve better living standards by mobilizing financial resources for private enterprise, promoting accessible and competitive markets, supporting businesses and other private sector entities, and creating jobs and delivering necessary services to those who are poverty-stricken or otherwise vulnerable. Since 2009, the IFC has focused on a set of development goals that its projects are expected to target. Its goals are to increase sustainable agriculture opportunities, improve health and education, increase access to financing for microfinance and business clients, advance infrastructure, help small businesses grow revenues, and invest in climate health.

The IFC is owned and governed by its member countries, but has its own executive

leadership and staff that conduct its normal business operations. It is a corporation

whose shareholders are member governments that provide paid-in capital and which

have the right to vote on its matters. Originally more financially integrated with the

World Bank Group, the IFC was established separately and eventually became

authorized to operate as a financially autonomous entity and make independent

investment decisions. It offers an array of debt and equity financing services and helps

companies face their risk exposures, while refraining from participating in a

management capacity. The corporation also offers advice to companies on making

decisions, evaluating their impact on the environment and society, and being

responsible. It advises governments on building infrastructure and partnerships to

further support private sector development.

The corporation is assessed by an independent evaluator each year. In 2011, its

evaluation report recognized that its investments performed well and reduced poverty,

but recommended that the corporation define poverty and expected outcomes more

explicitly to better-understand its effectiveness and approach poverty reduction more

strategically. The corporation's total investments in 2011 amounted to $18.66 billion. It

committed $820 million to advisory services for 642 projects in 2011, and held $24.5

billion worth of liquid assets. The IFC is in good financial standing and received the

highest ratings from two independent credit rating agencies in 2010 and 2011.

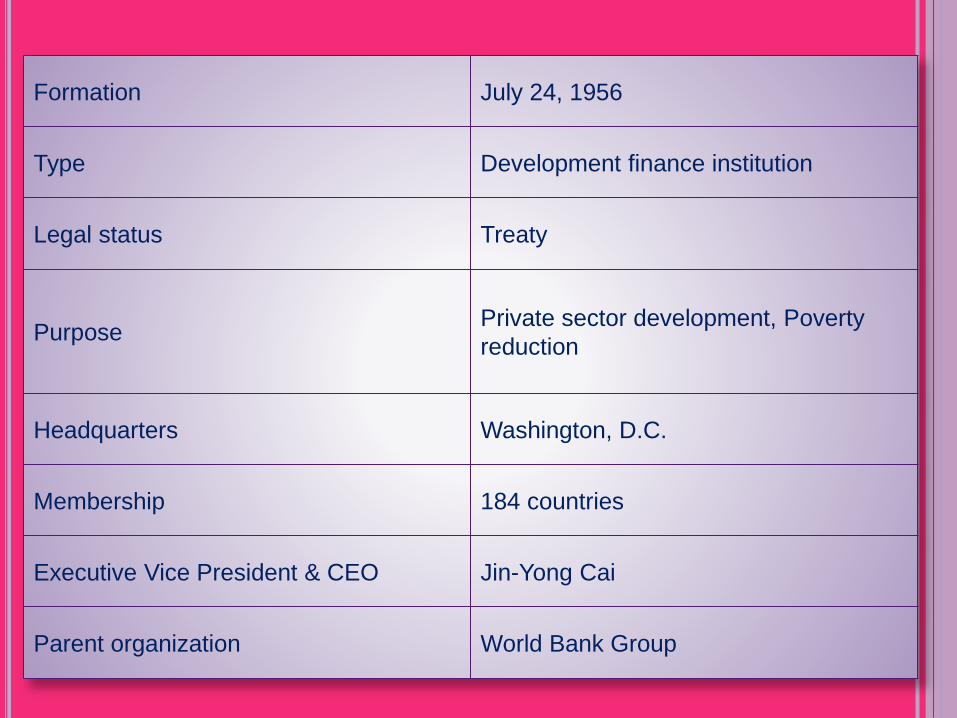

Formation July 24, 1956

Type Development finance institution

Legal status Treaty

PurposePrivate sector development, Poverty

reduction

Headquarters Washington, D.C.

Membership 184 countries

Executive Vice President & CEO Jin-Yong Cai

Parent organization World Bank Group

OBJECTIVES OF IFC

To invest in productive private enterprises, in association with private

investors, and without government guarantee of repayment, in cases

where sufficient private capital is not available on reasonable terms.

To serve as a clearing house to bring together investment

opportunities, private capital (both foreign and domestic) and

experienced management.

To help in stimulating the productive investment of private capital,

both domestic and foreign.