Interactive Investor guide to pension tax relief

24

guide to pension tax relief. 1 2 3 4 5 6 introduction tax benefits of pensions tax relief maximum contributions how to make a pension contribution what next?

-

Upload

james-newman -

Category

Documents

-

view

228 -

download

1

description

Â

Transcript of Interactive Investor guide to pension tax relief

guide to pensiontax relief.

1

2

3

4

5

6

introduction

tax benefits of pensions

tax relief

maximum contributions

how to make a pension contribution

what next?

2

1

2

3

4

5

6

introduction

tax benefits of pensions

tax relief

maximum contributions

how to make a pension contribution

what next?

4 introduction

how to claim your share of the government’s pension tax relief.

Pension tax relief is one of the most generous tax breaks available – you get up to 45% tax relief when you contribute to a pension.

Yet, 4.2 million of us let this valuable tax-saving opportunity go to waste1.

Why is that?It may simply be due to personal circumstances, but there may be other reasons too.

Tax rules are not simple. Even Albert Einstein famously admitted: “The hardest thing to understand in the world is the income tax.” What’s more, help with that complexity is difficult to come by, with many pension providers not providing the clarity needed.

And that’s why we’ve written this guide: to help you make sense of pension tax rules and explain in plain English how different groups of people can benefit when contributing to a private pension.

One very important point, the deadline to make contributions and benefit from pension tax relief on your earnings each tax year is 5 April. Unlike with an ISA, any unused allowance isn’t automatically lost. ‘carry forward’ arrangements apply (see page 17) but are not straightforward. So, if you want to maximise each year’s pension tax relief, make sure you do so before 5 April.

To help you understand some of the inevitable jargon we’ve also published a pensions glossary (see our pension guide).

1

2

3

4

5

61 https://www.unbiased.co.uk/tax-action

important note about this guideThis guide aims to explain in general terms how pension tax relief works. It is a short and simplified summary of a complex subject, so please do not make (or stop making) any decisions based solely on the contents of this guide.

The information is based on our understanding of the current pension and tax rules as at March 2015: these could change in future. The value of tax benefits depends on individual circumstances.

This guide is not personal financial advice. If you are unsure about how pension rules and tax reliefs could affect you and what action, if any, you should take, please seek personal financial advice.

important note about pensionsPlease remember that pensions are a long-term investment for your retirement. Most people can normally only access their money from age 55. Up to 25% can usually be taken as tax-free cash. Subsequent withdrawals are subject to income tax.

Most people can contribute as much as they earn to pensions. A £40,000 annual allowance and a £1.25 million lifetime allowance also apply (2014/15). These limits can be affected by other factors.

SIPPs (Self Invested Personal Pensions) are suitable for investors happy to make their own investment decisions, without financial advice. Of course, you can also work with an adviser then buy and sell investments yourself, based on the advice received. If you do not need the flexibility of a SIPP, you might consider a stakeholder pension. If you have access to an employer’s pension you should always consider that first.

Do bear in mind that investments can fall in value as well as rise so you could get back less than you invest.

6 tax benefits of pensions

the tax benefits of pensions at a glance.

The main reason to invest in a pension is building a nest egg for when you retire. However, you will also enjoy some very valuable tax benefits in the process:

✓ Receive up to 45% tax relief when you pay money in. ✓ Pay no capital gains or further UK income tax when your money grows. ✓ Get up to 25% tax-free cash when you take the money out, usually only possible from age 55 (the rest is taxed like income).

✓ Pass your pension on tax- efficiently or, in some cases, even tax free when you die.

If you are familiar with ISAs, you will notice the benefits are similar but not quite the same. Both ISAs and pensions shelter your money from tax but there are two major differences.

1

2

3

4

5

6

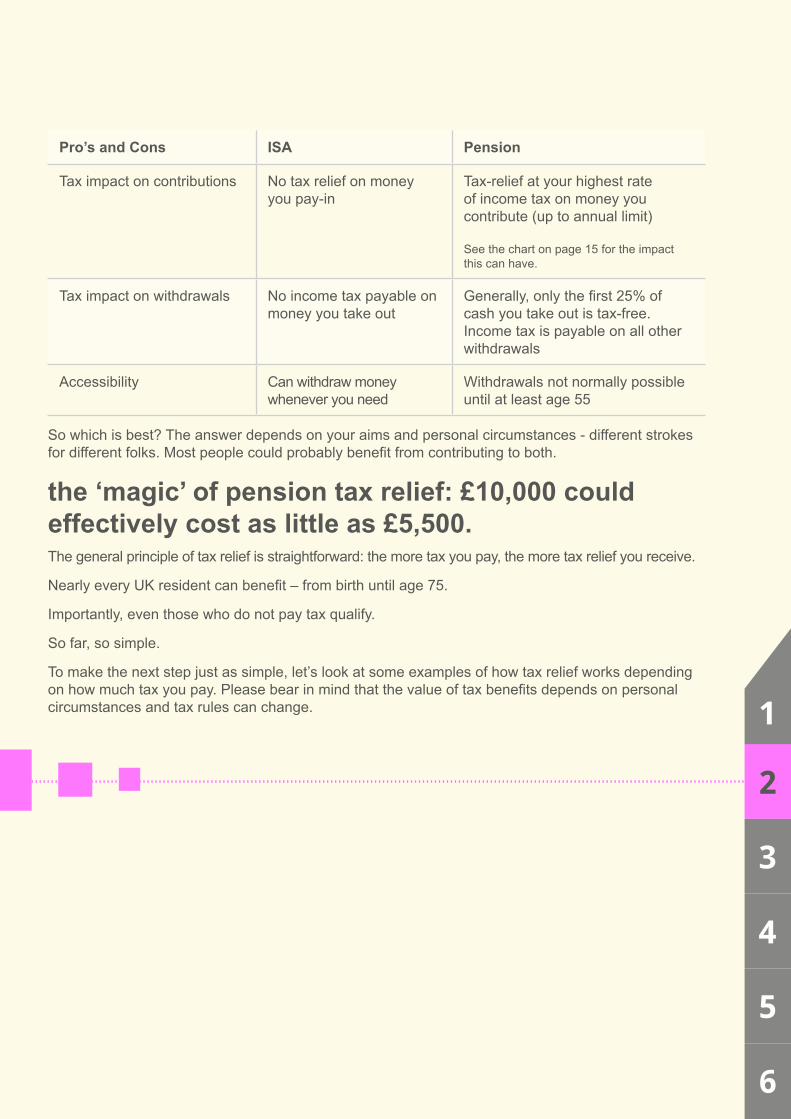

Pro’s and Cons ISA Pension

Tax impact on contributions No tax relief on money you pay-in

Tax-relief at your highest rate of income tax on money you contribute (up to annual limit)

See the chart on page 15 for the impact this can have.

Tax impact on withdrawals No income tax payable on money you take out

Generally, only the first 25% of cash you take out is tax-free. Income tax is payable on all other withdrawals

Accessibility Can withdraw money whenever you need

Withdrawals not normally possible until at least age 55

So which is best? The answer depends on your aims and personal circumstances - different strokes for different folks. Most people could probably benefit from contributing to both.

the ‘magic’ of pension tax relief: £10,000 could effectively cost as little as £5,500.The general principle of tax relief is straightforward: the more tax you pay, the more tax relief you receive.

Nearly every UK resident can benefit – from birth until age 75.

Importantly, even those who do not pay tax qualify.

So far, so simple.

To make the next step just as simple, let’s look at some examples of how tax relief works depending on how much tax you pay. Please bear in mind that the value of tax benefits depends on personal circumstances and tax rules can change.

8 tax benefits of pensions

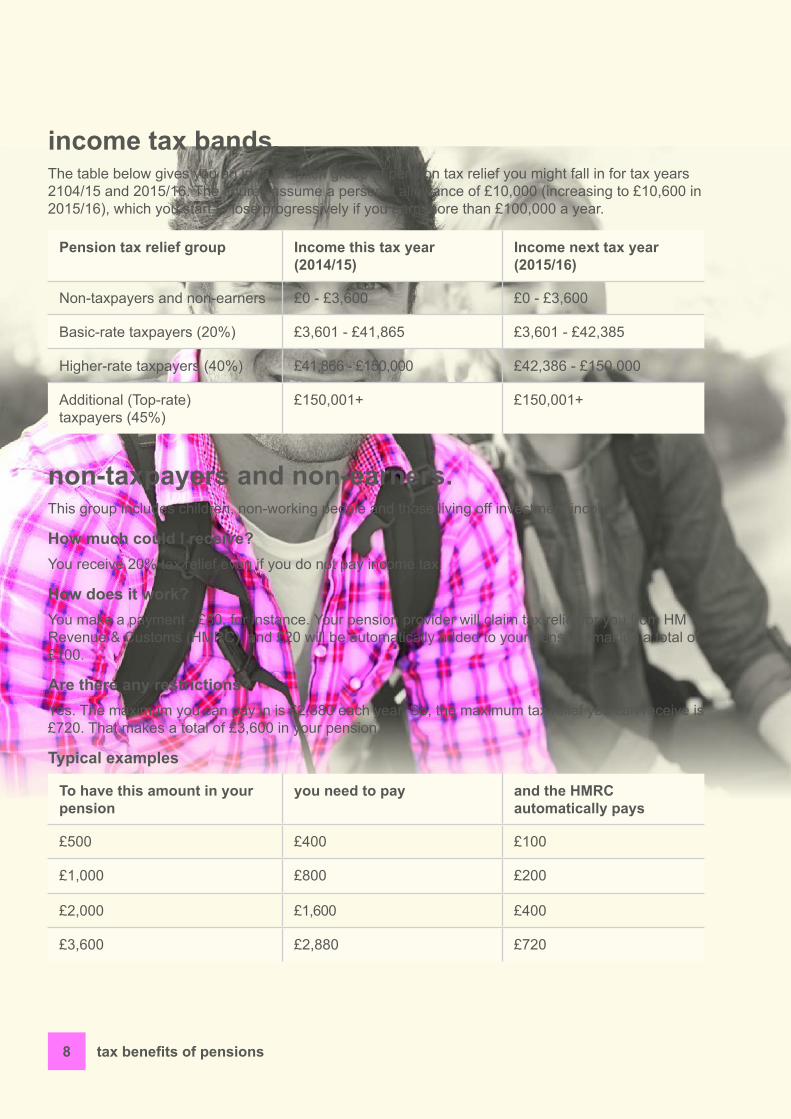

income tax bands.The table below gives you an idea of which group of pension tax relief you might fall in for tax years 2104/15 and 2015/16. The figures assume a personal allowance of £10,000 (increasing to £10,600 in 2015/16), which you start to lose progressively if you earn more than £100,000 a year.

Pension tax relief group Income this tax year (2014/15)

Income next tax year (2015/16)

Non-taxpayers and non-earners £0 - £3,600 £0 - £3,600

Basic-rate taxpayers (20%) £3,601 - £41,865 £3,601 - £42,385

Higher-rate taxpayers (40%) £41,866 - £150,000 £42,386 - £150,000

Additional (Top-rate) taxpayers (45%)

£150,001+ £150,001+

non-taxpayers and non-earners.This group includes children, non-working people and those living off investment income.

How much could I receive?You receive 20% tax relief even if you do not pay income tax.

How does it work?You make a payment - £80, for instance. Your pension provider will claim tax relief for you from HM Revenue & Customs (HMRC), and £20 will be automatically added to your pension, making a total of £100.

Are there any restrictions?Yes. The maximum you can pay in is £2,880 each year. So, the maximum tax relief you can receive is £720. That makes a total of £3,600 in your pension.

Typical examples

To have this amount in your pension

you need to pay and the HMRC automatically pays

£500 £400 £100

£1,000 £800 £200

£2,000 £1,600 £400

£3,600 £2,880 £720

1

2

3

4

5

6

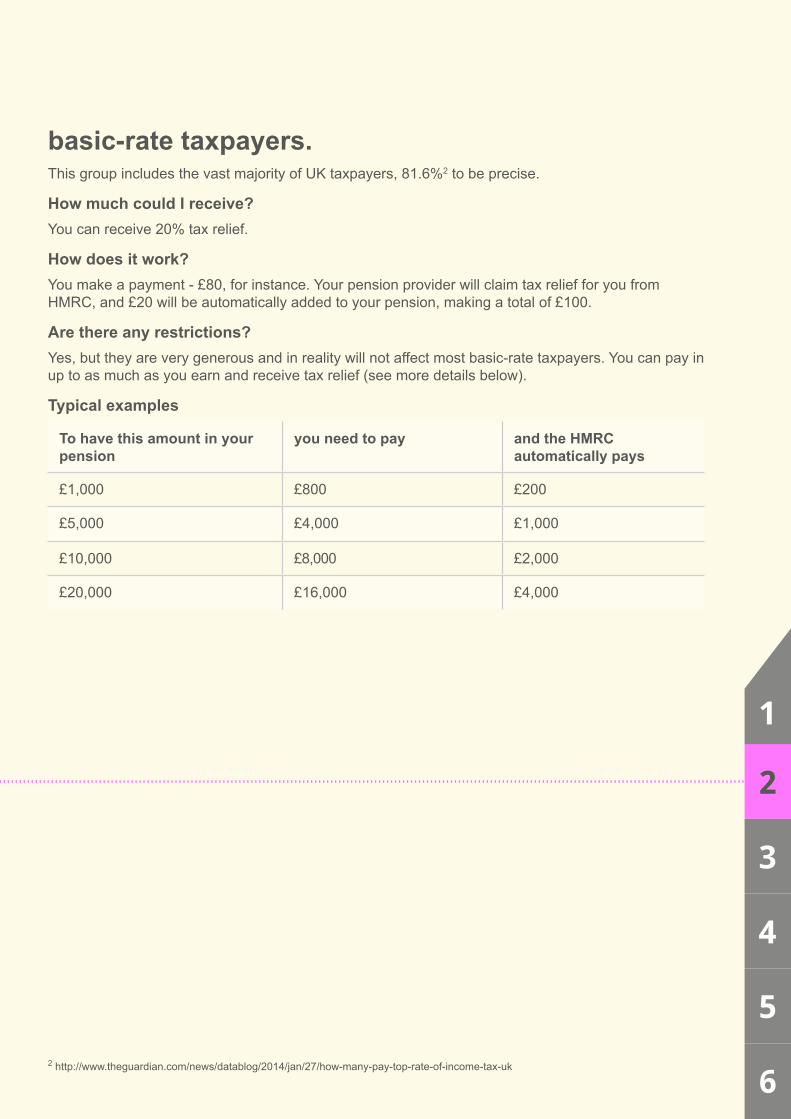

basic-rate taxpayers.This group includes the vast majority of UK taxpayers, 81.6%2 to be precise.

How much could I receive?You can receive 20% tax relief.

How does it work?You make a payment - £80, for instance. Your pension provider will claim tax relief for you from HMRC, and £20 will be automatically added to your pension, making a total of £100.

Are there any restrictions?Yes, but they are very generous and in reality will not affect most basic-rate taxpayers. You can pay in up to as much as you earn and receive tax relief (see more details below).

Typical examples

To have this amount in your pension

you need to pay and the HMRC automatically pays

£1,000 £800 £200

£5,000 £4,000 £1,000

£10,000 £8,000 £2,000

£20,000 £16,000 £4,000

2 http://www.theguardian.com/news/datablog/2014/jan/27/how-many-pay-top-rate-of-income-tax-uk

10 tax benefits of pensions

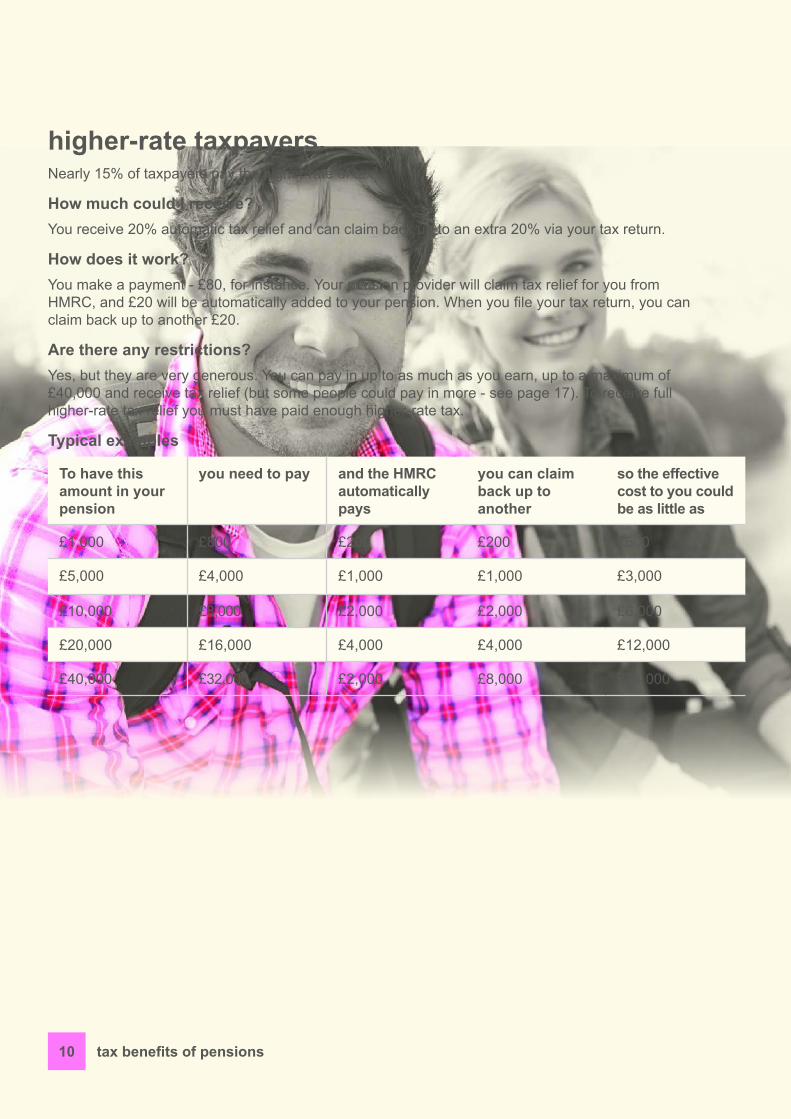

higher-rate taxpayers.Nearly 15% of taxpayers pay the higher rate of tax3.

How much could I receive?You receive 20% automatic tax relief and can claim back up to an extra 20% via your tax return.

How does it work?You make a payment - £80, for instance. Your pension provider will claim tax relief for you from HMRC, and £20 will be automatically added to your pension. When you file your tax return, you can claim back up to another £20.

Are there any restrictions?Yes, but they are very generous. You can pay in up to as much as you earn, up to a maximum of £40,000 and receive tax relief (but some people could pay in more - see page 17). To receive full higher-rate tax relief you must have paid enough higher-rate tax.

Typical examples

To have this amount in your pension

you need to pay and the HMRC automatically pays

you can claim back up to another

so the effective cost to you could be as little as

£1,000 £800 £200 £200 £600

£5,000 £4,000 £1,000 £1,000 £3,000

£10,000 £8,000 £2,000 £2,000 £6,000

£20,000 £16,000 £4,000 £4,000 £12,000

£40,000 £32,000 £2,000 £8,000 £24,000

1

2

3

4

5

6

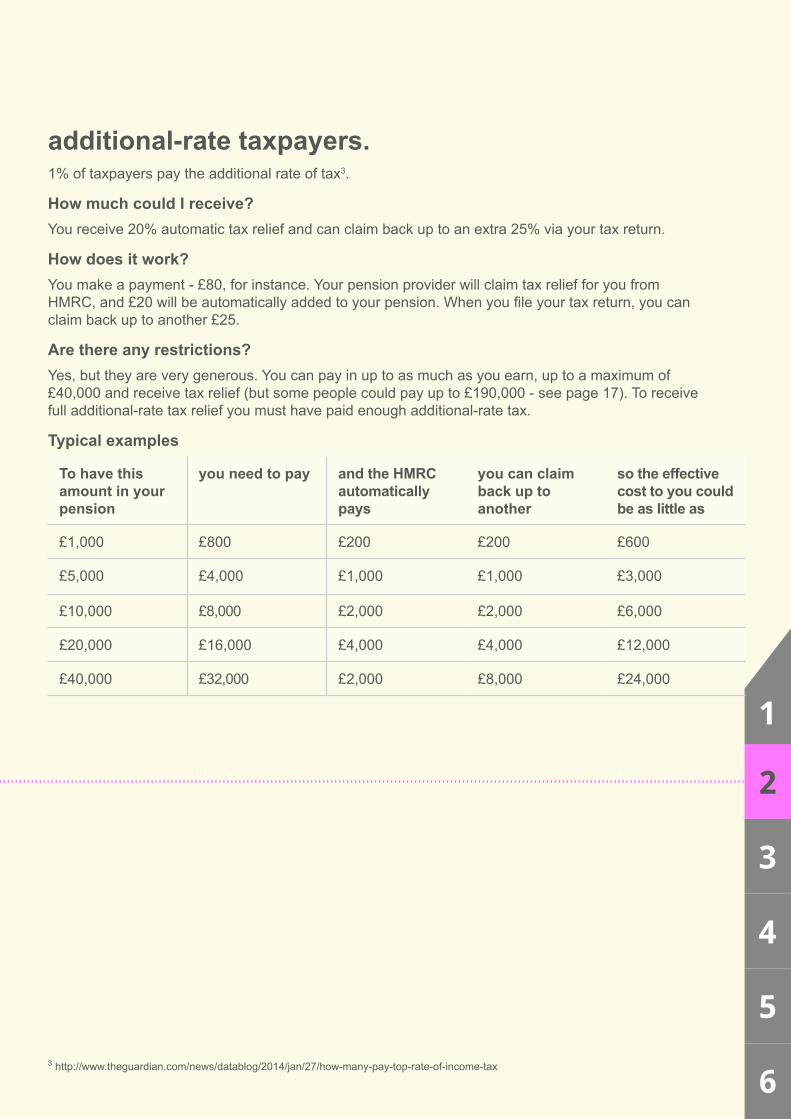

additional-rate taxpayers.1% of taxpayers pay the additional rate of tax3.

How much could I receive?You receive 20% automatic tax relief and can claim back up to an extra 25% via your tax return.

How does it work?You make a payment - £80, for instance. Your pension provider will claim tax relief for you from HMRC, and £20 will be automatically added to your pension. When you file your tax return, you can claim back up to another £25.

Are there any restrictions?Yes, but they are very generous. You can pay in up to as much as you earn, up to a maximum of £40,000 and receive tax relief (but some people could pay up to £190,000 - see page 17). To receive full additional-rate tax relief you must have paid enough additional-rate tax.

Typical examples

To have this amount in your pension

you need to pay and the HMRC automatically pays

you can claim back up to another

so the effective cost to you could be as little as

£1,000 £800 £200 £200 £600

£5,000 £4,000 £1,000 £1,000 £3,000

£10,000 £8,000 £2,000 £2,000 £6,000

£20,000 £16,000 £4,000 £4,000 £12,000

£40,000 £32,000 £2,000 £8,000 £24,000

3 http://www.theguardian.com/news/datablog/2014/jan/27/how-many-pay-top-rate-of-income-tax

12 tax benefits of pensions

what happens if I have a work pension?This guide explains how tax relief works when you contribute to a personal pension. If you are a member of a work pension, the principle of receiving tax relief at your highest marginal rate remains. However, how the tax relief is credited to you will depend on how your scheme has been set up. Your employer should be able to give you more information.

should I top-up my work pension or a personal pension?In some cases it may be better to top-up your work pension than pay into a personal pension. For instance, your employer may offer to match your contribution, or contribute via a salary sacrifice arrangement (see page 13).

Some people, however, prefer to make additional pension contributions to a private pension – perhaps their employer scheme doesn’t give them enough investment choice or flexibility, or perhaps they want to keep their arrangements separate from their employer. Your employer may be willing to make lump sum contributions into a personal pension on your behalf.

1

2

3

4

5

6

salary sacrifice.A popular way for employers to make pension contributions is through something called a ‘salary sacrifice’ arrangement. In effect, in exchange for a reduction in your gross salary, your employer contributes to your pension. Because your salary is reduced, not only do you save income tax, but the amount of National Insurance you pay is also reduced - as is the National Insurance paid by your employer. Some employers even offer to rebate some or all of those savings into your pension.

If you’re going to receive a bonus, they might also enable you to do something called ‘Bonus Sacrifice’ where they substitute part of your bonus for a pension contribution, again with the same National Insurance savings. Generally you would need to arrange this before you know what your bonus is actually going to be. Putting some of your bonus into a personal pension can be done after the event, but without the NI saving.

When using any of these arrangements, the standard annual contribution limits still apply.

If you think you want to make additional pension contributions and you have an employer arrangement in place it’s probably best to check with them first about any of these potential benefits.

14 tax relief

tax relief – the gift that keeps on giving?

Whilst the prospect of receiving tax relief of up to 45% makes pension attractive, the combination of tax relief with compounding makes them almost irresistible.

What is compounding? If you invest £1,000 and your money grows by 5% a year, by the end of the first year you will have added £50. In the second year, even if your money grows at the same 5% rate, you will add a bit more: £52.50 instead of £50 and so on. That is the ‘magnifying’ effect of compounding.

Investment growth always benefits from compounding. However, when you add tax relief to the equation, you’ve the added advantage of starting with a larger sum.

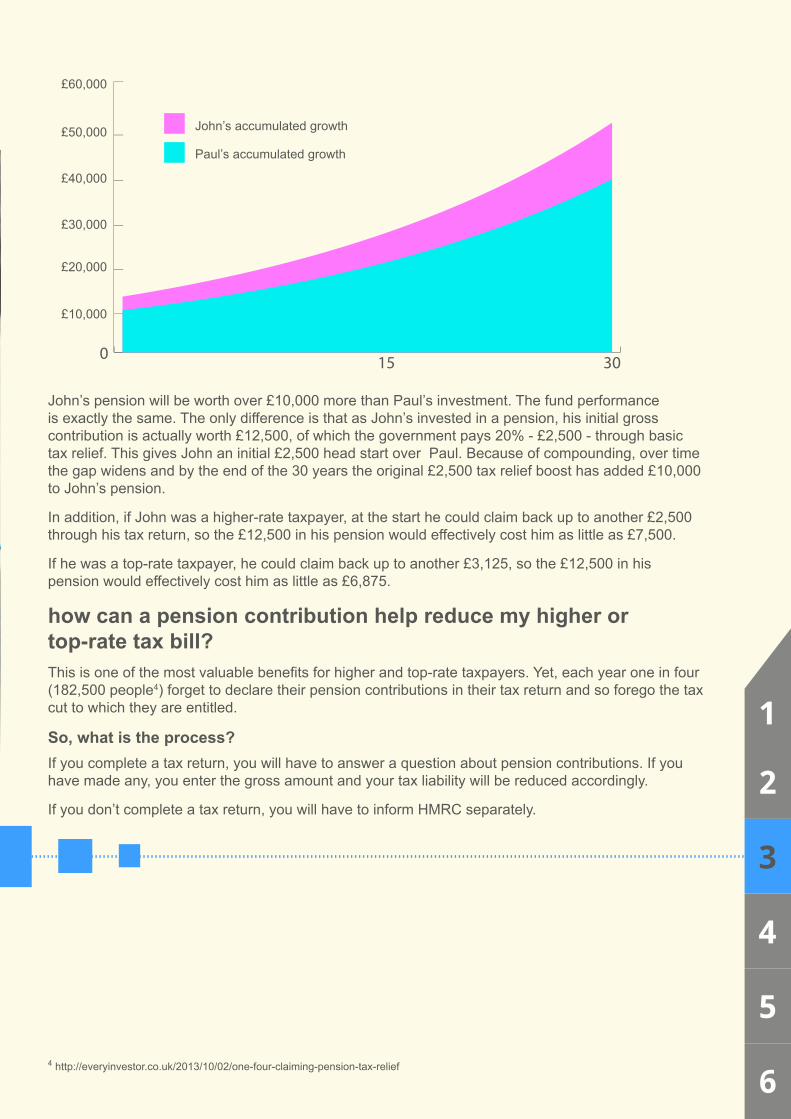

The best way to illustrate this is to look at an example. John and Paul both invest £10,000 in the same fund. John holds it in a pension, whilst Paul holds it in his ISA or share dealing account. If the fund grows at a steady 5% a year, how much will their investment be worth in 30 years?

1

2

3

4

5

6

John’s pension will be worth over £10,000 more than Paul’s investment. The fund performance is exactly the same. The only difference is that as John’s invested in a pension, his initial gross contribution is actually worth £12,500, of which the government pays 20% - £2,500 - through basic tax relief. This gives John an initial £2,500 head start over Paul. Because of compounding, over time the gap widens and by the end of the 30 years the original £2,500 tax relief boost has added £10,000 to John’s pension.

In addition, if John was a higher-rate taxpayer, at the start he could claim back up to another £2,500 through his tax return, so the £12,500 in his pension would effectively cost him as little as £7,500.

If he was a top-rate taxpayer, he could claim back up to another £3,125, so the £12,500 in his pension would effectively cost him as little as £6,875.

how can a pension contribution help reduce my higher or top-rate tax bill?This is one of the most valuable benefits for higher and top-rate taxpayers. Yet, each year one in four (182,500 people4) forget to declare their pension contributions in their tax return and so forego the tax cut to which they are entitled.

So, what is the process? If you complete a tax return, you will have to answer a question about pension contributions. If you have made any, you enter the gross amount and your tax liability will be reduced accordingly.

If you don’t complete a tax return, you will have to inform HMRC separately.

4 http://everyinvestor.co.uk/2013/10/02/one-four-claiming-pension-tax-relief

0 3015

John’s accumulated growth

Paul’s accumulated growth

£10,000

£20,000

£30,000

£40,000

£50,000

£60,000

16 maximum contributions

what is the maximum I can contribute?

For most taxpayers pension contributions rules are simple: you can contribute up to as much as you earn each tax year and receive tax relief. So, if you earn £30,000 in one tax year, the maximum you can contribute that year is £30,000: you pay-in £24,000 and the HMRC adds £6,000.

It’s important to note this is ‘earned income’ and doesn’t include income from savings and investments.

This is all most people need to know.

If you want to make a larger contribution, though, you must be aware of a few more rules.

1

2

3

4

5

6

your annual allowance.First of all, there is a cap called the annual allowance. It is currently £40,000. So during this tax year, the maximum that can be added to all your pensions by yourself and anybody else (including your employer) is £40,000, even if you earn more than £40,000.

But what if you want to contribute more? Perhaps you want to catch up on missed contributions in previous years or have received a windfall.

There is good news. If you qualify, there are two ways to contribute more than £40,000 this tax year without breaking any rules (if you break the rules you may have to pay a tax charge):

1. Carry forward – this allows you to catch up on missed pension contributions. In the simplest terms, you can add up any allowances you have not used in the previous three years and use some, or all of it, in one go. As the annual allowance was £50,000 in the three tax years before 2014/15, that gives a potential maximum contribution of £190,000 this tax year, with up to £85,500 tax relief. However, to make that contribution, you must have sufficient earnings. For instance, to contribute £100,000, you must have earned at least that much in the year in which you’re making the contribution.

2. Employer contributions – this allows you to contribute more than you earn, provided you have enough allowance left. It could be particularly useful to business owners, who might have been paying themselves mostly through dividends rather than salary.

If you think this could apply to you, please read more about the annual allowance, carry forward, and employer contributions. This is only a very brief explanation, and there are other important factors to consider, especially if you and/or your employer have contributed more than one year’s annual allowance across two tax years, or you have been a member of a defined benefit pension.

the lifetime allowance.You should also be aware of the ‘lifetime allowance’. This, currently set at £1.25 million, is the maximum value of pension funds that you can build up without incurring a tax charge. The lifetime allowance applies to the total values of all private and occupational pensions, but it does not include your State pension.

The chancellor’s March 2015 budget statement announced the reduction of the lifetime allowance to £1m from April 2016.

If you’re unsure about your allowances please check the HMRC website or seek personal financial advice.

18 how to make a pension contribution

how to make a pension contribution without investing any new money

1

2

3

4

5

6

Are you thinking you really should make a pension contribution but have no spare cash at the moment?

Not all is lost. If you have any investments outside of a pension, you could use them to make a pension contribution. This is possible only with SIPPs (Self Invested Personal Pensions – a type of personal pension) through a process called ‘Bed & SIPP’. It’s like moving existing investments into an ISA, but in this case, it’s into your SIPP.

Once your investments are in the SIPP, they are subject to pension rules. So, you can enjoy pension tax benefits, but you cannot normally access your money until you are at least age 55.

how does Bed & SIPP work?You effectively have to sell the investments, move the proceeds to your SIPP as a contribution, then buy them back within your SIPP at the market price. In so doing, you could incur trading fees and will be out of the market for a short while.

You will also realise any capital gain or loss on that sale. Most people have an annual capital gains exemption (£11,000 for the 2014/15 tax year). If your gains are below that, there is no capital gains tax charge. If you realise a loss, it may also be possible to carry that forward to offset future capital gains outside your pension.

Once you buy-back the investment in your pension, they can grow practically tax-free. And because of the tax relief boost, the return over time will be greater than if you had kept them in a sharedealing account. To see the difference, just look back at the example of John and Paul on page 15.

20 what next?

I’m thinking of making a pension contribution. What next?

The next natural step is to turn that intention into action.

But this opens the question: “which pension?”

All SIPPs, personal and stakeholder pensions offer the same tax benefits. But they do not all offer the same potential to build a decent nest egg for your retirement.

There are three main factors that determine how much you will have in your pension when you retire:

• How much you put in, and for how long,

• How your investments grow, and

• The charges you pay.

1

2

3

4

5

6

Now, the first of these (how much you pay-in and for how long) is almost entirely up to you. The other two will partly depend upon the pension you choose, and who provides it.

investment choices.How much your pension will grow will partly depend upon the performance of the investments into which you put your money.

The other two will partly depend on the pension you choose.

Some pensions (typically stakeholder and some personal pensions) only allow you to choose your investments from a handful of funds, usually run by insurance companies themselves.

A SIPP, on the other hand, allows you to invest pretty much where you like. You can choose from a very wide range of funds from well-known fund groups to the smaller, more specialist ones; UK and international shares; ETFs; investment trusts, bonds and gilts. If you want to be out of the market at any time, you can hold cash.

A SIPP is very similar to any other investment account you hold, such as a shares ISA or a trading account: you may not want to invest in all these different types of investment, but you have the flexibility to do so.

If you’re unsure which investments to choose, you’ll find plenty of inspiration in the investment ideas section on our website.

You’ll find funds and shares information, news, and analysis. If you need any extra help to get started, or do not have the time to choose your own investments, you could consider our range of model and ready-made portfolios, hand-picked diversified fund selections across different investing themes.

So our SIPP gives you as much investment freedom as you like and the potential for greater returns. As with all investments, though, returns are not guaranteed. Do remember that your SIPP investments could go down as well as up in value so you could end up with less than you invest.

charges.Now consider charges.

The more you pay, the less is left in your pension to grow - so the less you could have at the end.

Some charges are unavoidable – for instance, annual charges applied by the fund manager if you’re investing in funds, or fees for taking an income or reviewing your plan.

However, you do have a choice when it comes to account charges - what you pay to your pension provider (this can also be called a ‘platform’ or ‘administration fee’), and dealing charges.

22 what next?

why give away a share of your pension growth?Many pension and SIPP providers take a percentage of your pension value as a fee. This could be only a few pounds a year when you start building your pension, but can add up to a very significant amount over time as your pension pot hopefully grows.

For instance, if you have a pension worth £100,000, you could easily pay £450 a year just in account charges, based on an account charge of 0.45% a year. If your fund grows, so will the amount you pay. If it grew by 5% a year, over 10 years you would pay nearly £6,500. Over 30 years, nearly £40,000. Over 50 years, that figure would add up to over £86,000.

We think that’s not fair. We firmly believe that you should be the one who benefits from the growth you achieve – after all, keeping it in your pension will help you grow it even further.

That’s why we charge a low, fixed, fee of £80 + VAT p.a. to administer your SIPP and just £80 a year to cover the day to day running costs – and that includes £80 worth of trades too. Of course, when you need to take specific actions such as arranging income drawdown, reviewing those arrangements or purchasing an annuity, there may be costs associated. But you’ll find these set out, fair and square, in our Charges information.

What difference could percentage-based fees make to your investments?

In addition, when you decide to make your pension contribution to the Interactive Investor SIPP, you also benefit from online access, good investment information and great no-nonsense service.

Find out more about our SIPP at www.iii.co.uk/sipp.

1

2

3

4

5

6

what next?Making the most of these new pension options could mean a big difference to your retirement. Planning today will help you make the most of tomorrow. So take a look at your current pension arrangements, make sure you know how those schemes work, what they are currently worth and how they might grow.

If you’re not currently contributing to a pension, now is the time to start. Putting something aside every month – especially if your employer contributes too – is a good discipline and something you’ll thank yourself for later in life. Your current self may thank you too, for the government’s contribution only comes when you pay in … and as we’ve seen that extra boost adds up to a valuable sum over time.

Interactive Investor has a lot more to offer than just pensions. From day-to-day trading accounts to ISAs and SIPPS, we provide a safe, convenient place for investors to hold, monitor and manage their assets. We support an active community of like-minded people in achieving their financial goals – throughout their financial life – and help them create a firm foundation for their children’s future finances.

We look forward to helping you achieve your financial goals.

one final thought: if you read nothing else, read this.11.9 million people are not saving enough for retirement.

If you, too, are worried you may not be saving enough, take action now.

• Look at your current pension arrangements. Are you contributing enough to get you a decent pension when you retire?

• If you have a pension through work, compare the benefits of topping that up and making a contribution to a personal pension.

• Remember: when you contribute to a pension you could receive up to 45% tax relief, it is an extremely valuable benefit.

take careof tomorrow.

Interactive Investor Trading Limited, trading as “Interactive Investor”, is authorised and regulated by the Financial Conduct Authority. Registered Office: Standon House, 21 Mansell Street, London E1 8AA, Tel: 0845 200 3637. Registered in England with Company Registration number 3699618.

iii.co.uk/sipp