Inter Acc 12ed Test.bank

179

IN NTER TE RMED EST B DIAT BANK TEA K12 T CCO H EDT OUNT TION TING N G

-

Upload

sojung-kim -

Category

Documents

-

view

30.194 -

download

40

Transcript of Inter Acc 12ed Test.bank

INNTER

TE

RMED

EST B

DIAT

BANK

TE A

K12TCCOH EDT

OUNT

TION

TING

N

G

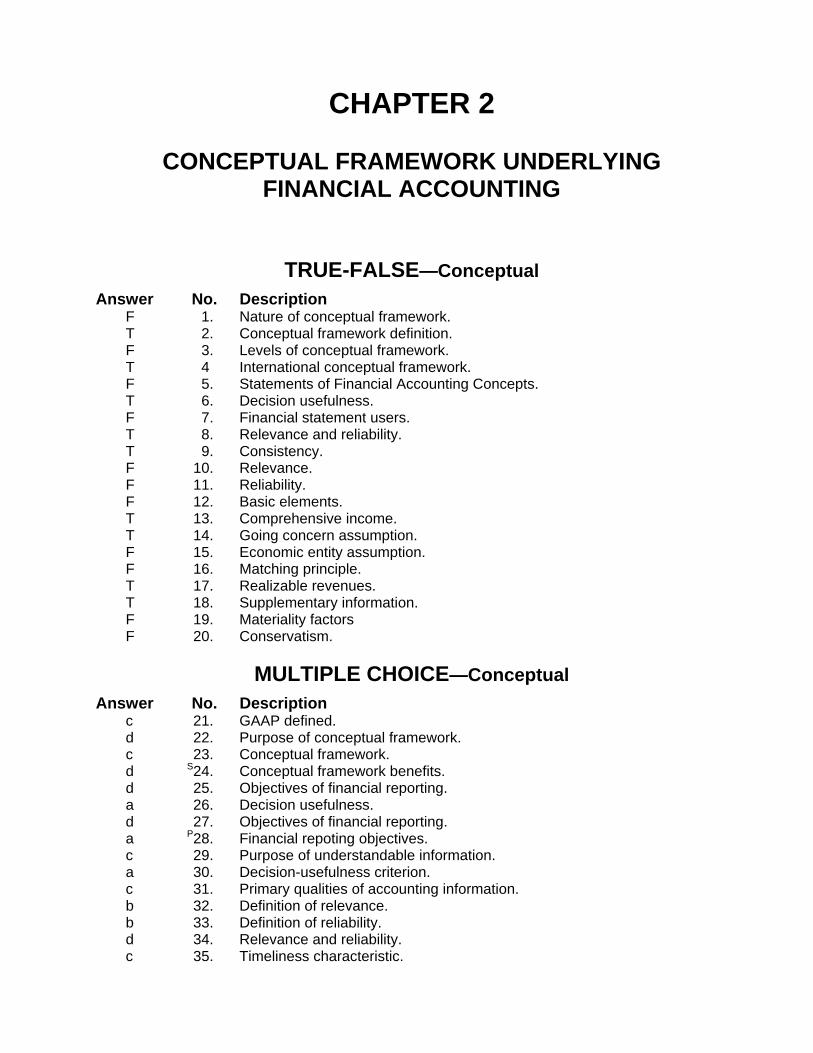

CHAPTER 2

CONCEPTUAL FRAMEWORK UNDERLYING FINANCIAL ACCOUNTING

TRUE-FALSE—Conceptual Answer No. Description F 1. Nature of conceptual framework. T 2. Conceptual framework definition. F 3. Levels of conceptual framework. T 4 International conceptual framework. F 5. Statements of Financial Accounting Concepts. T 6. Decision usefulness. F 7. Financial statement users. T 8. Relevance and reliability. T 9. Consistency. F 10. Relevance. F 11. Reliability. F 12. Basic elements. T 13. Comprehensive income. T 14. Going concern assumption. F 15. Economic entity assumption. F 16. Matching principle. T 17. Realizable revenues. T 18. Supplementary information. F 19. Materiality factors F 20. Conservatism.

MULTIPLE CHOICE—Conceptual Answer No. Description c 21. GAAP defined. d 22. Purpose of conceptual framework. c 23. Conceptual framework. d S24. Conceptual framework benefits. d 25. Objectives of financial reporting. a 26. Decision usefulness. d 27. Objectives of financial reporting. a P28. Financial repoting objectives. c 29. Purpose of understandable information. a 30. Decision-usefulness criterion. c 31. Primary qualities of accounting information. b 32. Definition of relevance. b 33. Definition of reliability. d 34. Relevance and reliability. c 35. Timeliness characteristic.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 2

MULTIPLE CHOICE—Conceptual (cont.) Answer No. Description d 36. Verifiability characteristic. b 37. Neutrality characteristic. d 38. Neutrality characteristic. c 39. Definition of verifiability. a 40. Quality of predictive value. c 41. Quality of representational faithfulness. d 42. Consistency. b 43. Consistency characteristic. b 44. Comparability and consistency. d 45. Comparability. d 46. Elements of financial statements. c 47. Distinction between revenues and gains. c 48. Definition of a loss. d 49. Definition of comprehensive income. b 50. Components of comprehensive income. d P51. Comprehensive income. b S52. Earnings vs. comprehensive income. a S53. Reporting financial statement elements. a S54. Monetary unit assumption. c S55. Periodicity assumption. c 56. Monetary unit assumption. d 57. Economic entity assumption. a 58. Economic entity assumption. b 59. Periodicity assumption. a 60. Going concern assumption. d 61. Going concern assumption. d 62. Implications of going concern assumption. a 63. Historical cost principle. d 64. Historical cost principle. c 65. Revenue recognition principle. d 66. Revenue recognition principle. d 67. Revenue recognition principle. d 68. Timing of revenue recognition. c 69. Realization concept. b 70. Definition of realized. b 71. Matching principle. b 72. Matching principle. b 73. Expense recognition. c 74. Full-disclosure principle. d 75. Constraints to limit the cost of reporting. a 76. Cost-benefit constraint. c 77. Materiality constraint. d 78. Materiality. d 79. Pervasive constraints. a 80. Conservatism constraint. b 81. Conservatism constraint. a 82. Trade-offs between characteristics of accounting information. c 83. Trade-offs between characteristics of accounting information. c P84. Conservatism constraint.

Conceptual Framework Underlying Financial Accounting

2 - 3

MULTIPLE CHOICE—CPA Adapted Answer No. Description a 85. Quality of predictive value. b 86. Consistency characteristic. b 87. Classification of gains and losses. b 88. Earnings concept. a 89. Components of comprehensive income. b 90. Components of comprehensive income. d 91. Components of comprehensive income. d 92. Components of comprehensive income. a 93. Definition of recognition. P Note: these questions also appear in the Problem-Solving Survival Guide. S Note: these questions also appear in the Study Guide.

EXERCISES Item Description E2-94 Examination of the conceptual framework. E2-95 Accounting concepts—identification. E2-96 Accounting concepts—identification. E2-97 Accounting concepts—matching. E2-98 Accounting concepts—fill in the blanks. E2-99 Basic assumptions. E2-100 Revenue recognition. E2-101 Historical cost principle. E2-102 Matching concept.

CHAPTER LEARNING OBJECTIVES 1. Describe the usefulness of a conceptual framework. 2. Describe the FASB’s efforts to construct a conceptual framework. 3. Understand the objectives of financial reporting. 4. Identify the qualitative characteristics of accounting information. 5. Define the basic elements of financial statements. 6. Describe the basic assumptions of accounting. 7. Explain the application of the basic principles of accounting. 8. Describe the impact that constraints have on reporting accounting information.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 4

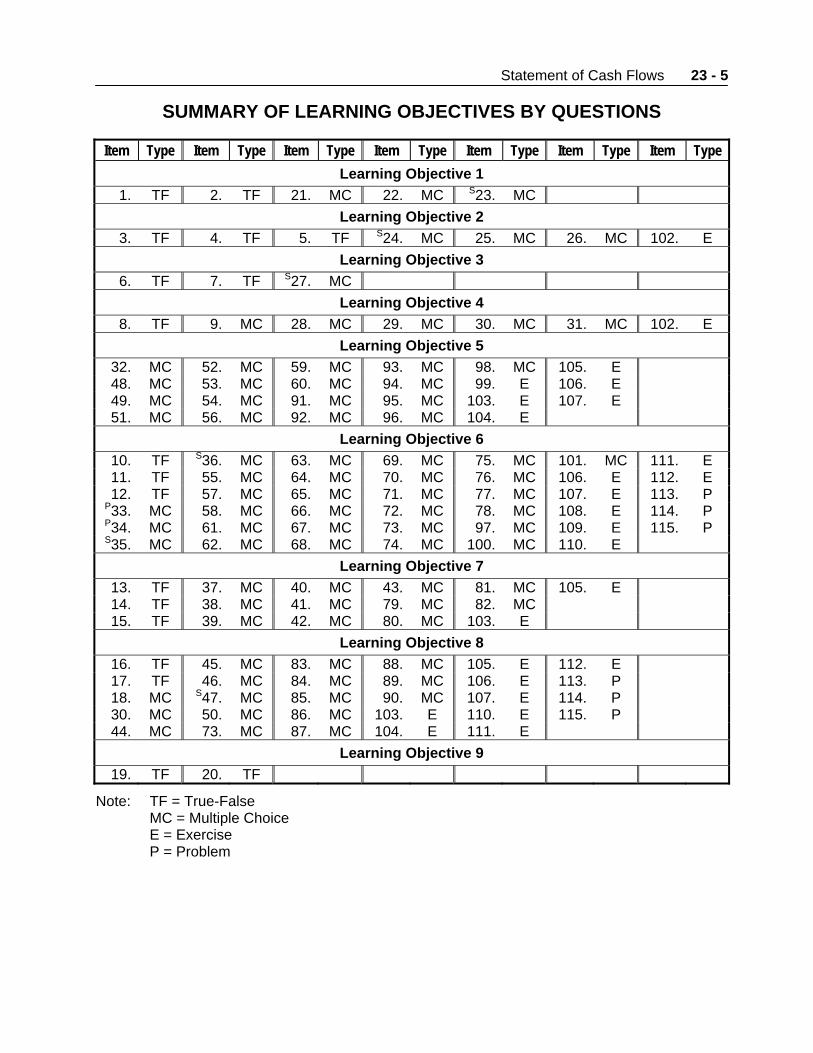

SUMMARY OF LEARNING OBJECTIVES BY QUESTIONS

Item Type Item Type Item Type Item Type Item Type Item Type Item Type Learning Objective 1

1. TF 2. TF 21. MC 22. MC 23. MC S24. MC 94. E Learning Objective 2

3. TF 4. TF 5. TF 25. MC 94. E Learning Objective 3

6. TF 7. TF 26. MC 27. MC P28. MC 94. E Learning Objective 4

8. TF 29. MC 33. MC 37. MC 41. MC 45. MC 96. E 9. TF 30. MC 34. MC 38. MC 42. MC 85. MC 97. E

10. TF 31. MC 35. MC 39. MC 43. MC 86. MC 98. E 11. TF 32. MC 36. MC 40. MC 44. MC 95. E

Learning Objective 5 12. TF 47. MC 50. MC S53. MC 89. MC 92. MC 13. TF 48. MC P51. MC 87. MC 90. MC 46. MC 49. MC S52. MC 88. MC 91. MC

Learning Objective 6 14. TF S55. MC 58. MC 61. MC 98. E 101. E 15. TF 56. MC 59. MC 62. MC 99. E

S54. MC 57. MC 60. MC 95. E 100. E Learning Objective 7

16. TF 64. MC 68. MC 72. MC 95. E 100. E 17. TF 65. MC 69. MC 73. MC 96. E 101. E 18. TF 66. MC 70. MC 74. MC 97. E 102. E 63. MC 67. MC 71. MC 93. MC 98. E

Learning Objective 8 19. TF 75. MC 77. MC 79. MC 81. MC 83. MC 95. E 20. TF 76. MC 78. MC 80. MC 82. MC P84. MC 96. E

Note: TF = True-False MC = Multiple Choice E = Exercise

Conceptual Framework Underlying Financial Accounting

2 - 5

TRUE-FALSE—Conceptual 1. The conceptual framework for accounting has been discovered through empirical research. 2. A conceptual framework is a coherent system of interrelated objectives and fundamentals

that can lead to consistent standards. 3. The first level of the conceptual framework identifies the recognition and measurement

concepts used in establishing accounting standards. 4. The IASB has issued a conceptual framework that is broadly consistent with that of the

United States. 5. Although the FASB intends to develop a conceptual framework, no Statements of Financial

Accounting Concepts have been issued to date. 6. Decision Usefulness is the underlying theme of the conceptual framework. 7. Users of financial statements are assumed to have no knowledge of business and financial

accounting matters by financial statement preparers. 8. Relevance and reliability are the two primary qualities that make accounting information

useful for decision making. 9. The idea of consistency does not mean that companies cannot switch from one accounting

method to another. 10. Timeliness and neutrality are two ingredients of relevance. 11. Verifiability and predictive value are two ingredients of reliability. 12. Revenues, gains, and distributions to owners all increase equity. 13. Comprehensive income includes all changes in equity during a period except those

resulting from investments by owners and distributions to owners. 14. The historical cost principle would be of limited usefulness if not for the going concern

assumption. 15. The economic entity assumption means that economic activity can be identified with a

particular legal entity. 16. The matching principle states that debits must equal credits in each transaction. 17. Revenues are realizable when assets received or held are readily convertible into cash or

claims to cash. 18. Supplementary information may include details or amounts that present a different

perspective from that adopted in the financial statements. 19. Companies consider only quantitative factors in determining whether an item is material.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 6

20. Conservatism in accounting means the accountant should attempt to understate assets and income when possible.

True False Answers—Conceptual

Item Ans. Item Ans. Item Ans. Item Ans. 1. F 6. T 11. F 16. F 2. T 7. F 12. F 17. T 3. F 8. T 13. T 18. T 4. T 9. T 14. T 19. F 5. F 10. F 15. F 20. F

MULTIPLE CHOICE—Conceptual 21. Generally accepted accounting principles

a. are fundamental truths or axioms that can be derived from laws of nature. b. derive their authority from legal court proceedings. c. derive their credibility and authority from general recognition and acceptance by the

accounting profession. d. have been specified in detail in the FASB conceptual framework.

22. A soundly developed conceptual framework of concepts and objectives should

a. increase financial statement users' understanding of and confidence in financial reporting.

b. enhance comparability among companies' financial statements. c. allow new and emerging practical problems to be more quickly soluble. d. all of these.

23. Which of the following (a-c) are not true concerning a conceptual framework in account-

ing? a. It should be a basis for standard-setting. b. It should allow practical problems to be solved more quickly by reference to it. c. It should be based on fundamental truths that are derived from the laws of nature. d. All of the above (a-c) are true.

S24. Which of the following is not a benefit associated with the FASB Conceptual Framework

Project? a. A conceptual framework should increase financial statement users' understanding of

and confidence in financial reporting. b. Practical problems should be more quickly solvable by reference to an existing

conceptual framework. c. A coherent set of accounting standards and rules should result. d. Business entities will need far less assistance from accountants because the financial

reporting process will be quite easy to apply.

Conceptual Framework Underlying Financial Accounting

2 - 7

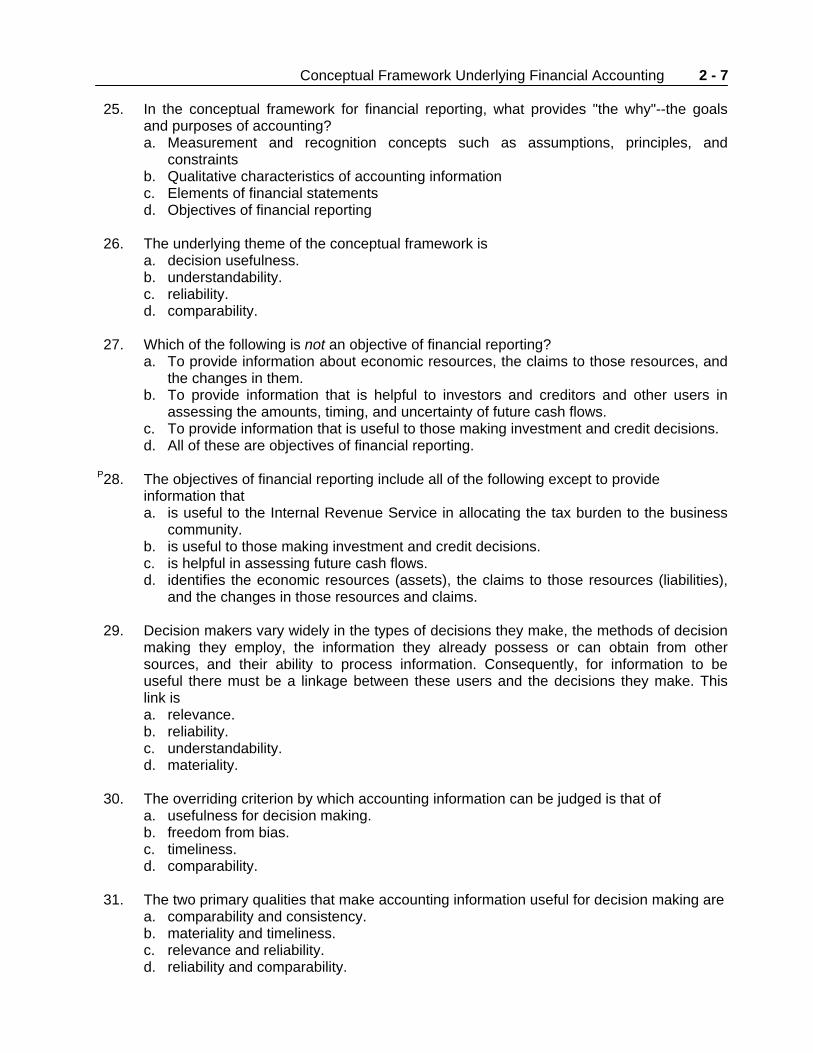

25. In the conceptual framework for financial reporting, what provides "the why"--the goals and purposes of accounting? a. Measurement and recognition concepts such as assumptions, principles, and

constraints b. Qualitative characteristics of accounting information c. Elements of financial statements d. Objectives of financial reporting

26. The underlying theme of the conceptual framework is

a. decision usefulness. b. understandability. c. reliability. d. comparability.

27. Which of the following is not an objective of financial reporting?

a. To provide information about economic resources, the claims to those resources, and the changes in them.

b. To provide information that is helpful to investors and creditors and other users in assessing the amounts, timing, and uncertainty of future cash flows.

c. To provide information that is useful to those making investment and credit decisions. d. All of these are objectives of financial reporting.

P28. The objectives of financial reporting include all of the following except to provide

information that a. is useful to the Internal Revenue Service in allocating the tax burden to the business

community. b. is useful to those making investment and credit decisions. c. is helpful in assessing future cash flows. d. identifies the economic resources (assets), the claims to those resources (liabilities),

and the changes in those resources and claims. 29. Decision makers vary widely in the types of decisions they make, the methods of decision

making they employ, the information they already possess or can obtain from other sources, and their ability to process information. Consequently, for information to be useful there must be a linkage between these users and the decisions they make. This link is a. relevance. b. reliability. c. understandability. d. materiality.

30. The overriding criterion by which accounting information can be judged is that of

a. usefulness for decision making. b. freedom from bias. c. timeliness. d. comparability.

31. The two primary qualities that make accounting information useful for decision making are

a. comparability and consistency. b. materiality and timeliness. c. relevance and reliability. d. reliability and comparability.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 8

32. Accounting information is considered to be relevant when it a. can be depended on to represent the economic conditions and events that it is

intended to represent. b. is capable of making a difference in a decision. c. is understandable by reasonably informed users of accounting information. d. is verifiable and neutral.

33. The quality of information that gives assurance that it is reasonably free of error and bias

and is a faithful representation is a. relevance. b. reliability. c. verifiability. d. neutrality.

34. According to Statement of Financial Accounting Concepts No. 2, which of the following

relates to both relevance and reliability? a. Materiality b. Understandability c. Usefulness d. All of these

35. According to Statement of Financial Accounting Concepts No. 2, timeliness is an

ingredient of the primary quality of Relevance Reliability a. Yes Yes b. No Yes c. Yes No d. No No 36. According to Statement of Financial Accounting Concepts No. 2, verifiability is an

ingredient of the primary quality of Relevance Reliability a. Yes No b. Yes Yes c. No No d. No Yes 37. According to Statement of Financial Accounting Concepts No. 2, neutrality is an ingredient

of the primary quality of Relevance Reliability a. Yes Yes b. No Yes c. Yes No d. No No 38. Information is neutral if it

a. provides benefits which are at least equal to the costs of its preparation. b. can be compared with similar information about an enterprise at other points in time. c. would have no impact on a decision maker. d. is free from bias toward a predetermined result.

Conceptual Framework Underlying Financial Accounting

2 - 9

39. The characteristic that is demonstrated when a high degree of consensus can be secured among independent measurers using the same measurement methods is a. relevance. b. reliability. c. verifiability. d. neutrality.

40. According to Statement of Financial Accounting Concepts No. 2, predictive value is an

ingredient of the primary quality of Relevance Reliability a. Yes No b. Yes Yes c. No No d. No Yes 41. Under Statement of Financial Accounting Concepts No. 2, representational faithfulness is

an ingredient of the primary quality of Reliability Relevance a. Yes Yes b. No Yes c. Yes No d. No No 42. Financial information does not demonstrate consistency when

a. firms in the same industry use different accounting methods to account for the same type of transaction.

b. a company changes its estimate of the salvage value of a fixed asset. c. a company fails to adjust its financial statements for changes in the value of the

measuring unit. d. none of these.

43. Financial information exhibits the characteristic of consistency when

a. expenses are reported as charges against revenue in the period in which they are paid.

b. accounting entities give accountable events the same accounting treatment from period to period.

c. extraordinary gains and losses are not included on the income statement. d. accounting procedures are adopted which give a consistent rate of net income.

44. Information about different entities and about different periods of the same entity can be

prepared and presented in a similar manner. Comparability and consistency are related to which of these objectives?

Comparability Consistency a. Entities Entities b. Entities Periods c. Periods Entities d. Periods Periods

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 10

45. When information about two different enterprises has been prepared and presented in a similar manner, the information exhibits the characteristic of a. relevance. b. reliability. c. consistency. d. none of these.

46. The elements of financial statements include investments by owners. These are increases

in an entity's net assets resulting from owners' a. transfers of assets to the entity. b. rendering services to the entity. c. satisfaction of liabilities of the entity. d. all of these.

47. In classifying the elements of financial statements, the primary distinction between

revenues and gains is a. the materiality of the amounts involved. b. the likelihood that the transactions involved will recur in the future. c. the nature of the activities that gave rise to the transactions involved. d. the costs versus the benefits of the alternative methods of disclosing the transactions

involved. 48. A decrease in net assets arising from peripheral or incidental transactions is called a(n)

a. capital expenditure. b. cost. c. loss. d. expense.

49. One of the elements of financial statements is comprehensive income. As described in

Statement of Financial Accounting Concepts No. 6, "Elements of Financial Statements," comprehensive income is equal to a. revenues minus expenses plus gains minus losses. b. revenues minus expenses plus gains minus losses plus investments by owners minus

distributions to owners. c. revenues minus expenses plus gains minus losses plus investments by owners minus

distributions to owners plus assets minus liabilities. d. none of these.

50. Which of the following elements of financial statements is not a component of compre-

hensive income? a. Revenues b. Distributions to owners c. Losses d. Expenses

P51. Which of the following is false with regard to the element "comprehensive income"?

a. It is more inclusive than the traditional notion of net income. b. It includes net income and all other changes in equity exclusive of owners' invest-

ments and distributions to owners. c. This concept is not yet being applied in practice. d. It excludes prior period adjustments (transactions that relate to previous periods, such

as corrections of errors).

Conceptual Framework Underlying Financial Accounting

2 - 11

S52. According to the FASB conceptual framework, earnings a. are the same as comprehensive income. b. exclude certain gains and losses that are included in comprehensive income. c. include certain gains and losses that are excluded from comprehensive income. d. include certain losses that are excluded from comprehensive income.

S53. According to the FASB Conceptual Framework, the elements⎯assets, liabilities, and

equity⎯describe amounts of resources and claims to resources at/during a

Moment in Time Period of Time a. Yes No b. Yes Yes c. No Yes d. No No S54. Which of the following basic accounting assumptions is threatened by the existence of

severe inflation in the economy? a. Monetary unit assumption. b. Periodicity assumption. c. Going-concern assumption. d. Economic entity assumption.

S55. During the lifetime of an entity accountants produce financial statements at artificial points

in time in accordance with the concept of

Objectivity Periodicity a. No No b. Yes No c. No Yes d. Yes Yes 56. Under current GAAP, inflation is ignored in accounting due to the

a. economic entity assumption. b. going concern assumption. c. monetary unit assumption. d. periodicity assumption.

57. The economic entity assumption

a. is inapplicable to unincorporated businesses. b. recognizes the legal aspects of business organizations. c. requires periodic income measurement. d. is applicable to all forms of business organizations.

58. Preparation of consolidated financial statements when a parent-subsidiary relationship

exists is an example of the a. economic entity assumption. b. relevance characteristic. c. comparability characteristic. d. neutrality characteristic.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 12

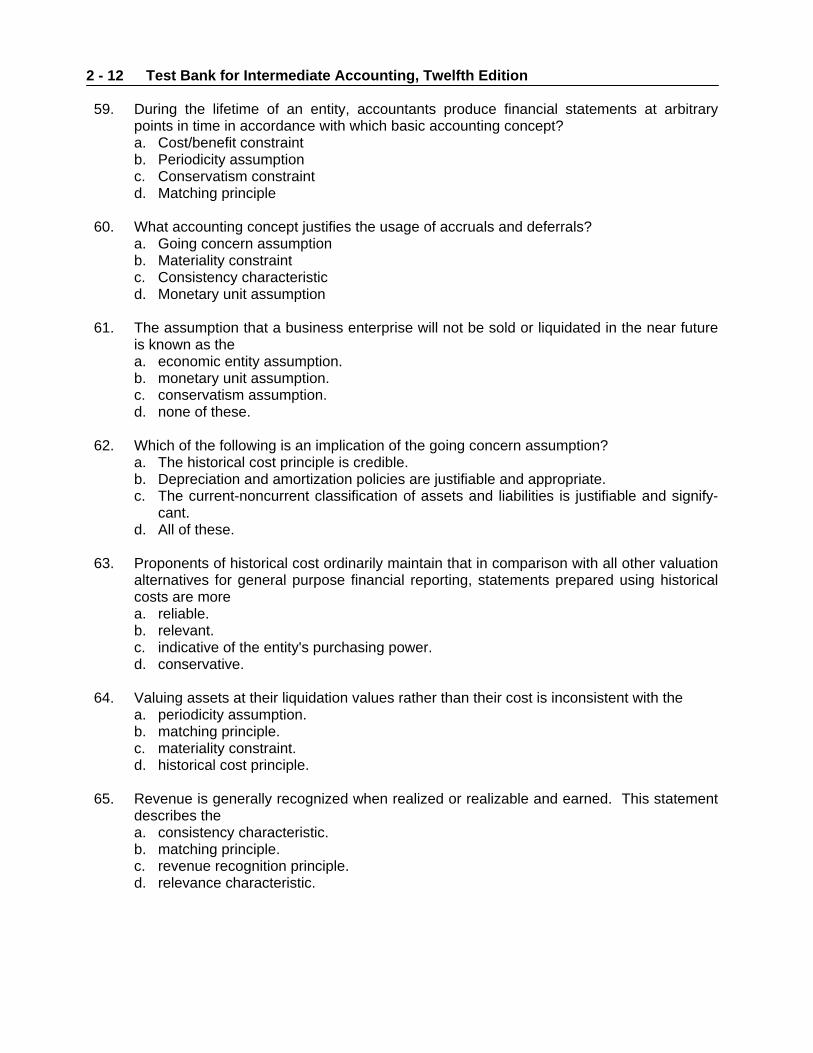

59. During the lifetime of an entity, accountants produce financial statements at arbitrary points in time in accordance with which basic accounting concept? a. Cost/benefit constraint b. Periodicity assumption c. Conservatism constraint d. Matching principle

60. What accounting concept justifies the usage of accruals and deferrals?

a. Going concern assumption b. Materiality constraint c. Consistency characteristic d. Monetary unit assumption

61. The assumption that a business enterprise will not be sold or liquidated in the near future

is known as the a. economic entity assumption. b. monetary unit assumption. c. conservatism assumption. d. none of these.

62. Which of the following is an implication of the going concern assumption?

a. The historical cost principle is credible. b. Depreciation and amortization policies are justifiable and appropriate. c. The current-noncurrent classification of assets and liabilities is justifiable and signify-

cant. d. All of these.

63. Proponents of historical cost ordinarily maintain that in comparison with all other valuation

alternatives for general purpose financial reporting, statements prepared using historical costs are more a. reliable. b. relevant. c. indicative of the entity's purchasing power. d. conservative.

64. Valuing assets at their liquidation values rather than their cost is inconsistent with the

a. periodicity assumption. b. matching principle. c. materiality constraint. d. historical cost principle.

65. Revenue is generally recognized when realized or realizable and earned. This statement

describes the a. consistency characteristic. b. matching principle. c. revenue recognition principle. d. relevance characteristic.

Conceptual Framework Underlying Financial Accounting

2 - 13

66. Generally, revenue from sales should be recognized at a point when a. management decides it is appropriate to do so. b. the product is available for sale to the ultimate consumer. c. the entire amount receivable has been collected from the customer and there remains

no further warranty liability. d. none of these.

67. Revenue generally should be recognized

a. at the end of production. b. at the time of cash collection. c. when realized. d. when realized or realizable and earned.

68. Which of the following is not a time when revenue may be recognized?

a. At time of sale b. At receipt of cash c. During production d. All of these are possible times of revenue recognition.

69. Under Statement of Financial Accounting Concepts No. 5, which of the following, in the

most precise sense, means the process of converting noncash resources and rights into cash or claims to cash? a. Recognition b. Measurement c. Realization d. Allocation

70. "When products (goods or services), merchandise, or other assets are exchanged for

cash or claims to cash" is a definition of a. allocated. b. realized. c. realizable. d. earned.

71. The allowance for doubtful accounts, which appears as a deduction from accounts

receivable on a balance sheet and which is based on an estimate of bad debts, is an application of the a. consistency characteristic. b. matching principle. c. materiality constraint. d. revenue recognition principle.

72. The accounting principle of matching is best demonstrated by

a. not recognizing any expense unless some revenue is realized. b. associating effort (expense) with accomplishment (revenue). c. recognizing prepaid rent received as revenue. d. establishing an Appropriation for Contingencies account.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 14

73. Which of the following serves as the justification for the periodic recording of depreciation expense? a. Association of efforts (expense) with accomplishments (revenue) b. Systematic and rational allocation of cost over the periods benefited c. Immediate recognition of an expense d. Minimization of income tax liability

74. Application of the full disclosure principle

a. is theoretically desirable but not practical because the costs of complete disclosure exceed the benefits.

b. is violated when important financial information is buried in the notes to the financial statements.

c. is demonstrated by the use of supplementary information presenting the effects of changing prices.

d. requires that the financial statements be consistent and comparable. 75. Which of the following statements concerning the cost-benefit relationship is not true?

a. Business reporting should exclude information outside of management's expertise. b. Management should not be required to report information that would significantly harm

the company's competitive position. c. Management should not be required to provide forecasted financial information. d. If needed by financial statement users, management should gather information not

included in the financial statements that would not otherwise be gathered for internal use.

76. Under Statement of Financial Accounting Concepts No. 2, which of the following relates to

both relevance and reliability? a. Cost-benefit constraint b. Predictive value c. Verifiability d. Representational faithfulness

77. Charging off the cost of a wastebasket with an estimated useful life of 10 years as an

expense of the period when purchased is an example of the application of the a. consistency characteristic. b. matching principle. c. materiality constraint. d. historical cost principle.

78. Which of the following statements about materiality is not correct?

a. An item must make a difference or it need not be disclosed. b. Materiality is a matter of relative size or importance. c. An item is material if its inclusion or omission would influence or change the judgment

of a reasonable person. d. All of these are correct statements about materiality.

79. Which of the following are considered pervasive constraints by Statement of Financial

Accounting Concepts No. 2? a. Cost-benefit relationship and conservatism b. Timeliness and feedback value c. Conservatism and verifiability d. Materiality and cost-benefit relationship

Conceptual Framework Underlying Financial Accounting

2 - 15

80. The basic accounting concept that refers to the tendency of accountants to resolve uncertainty in favor of understating assets and revenues and overstating liabilities and expenses is known as the a. conservatism constraint. b. materiality constraint. c. substance over form principle. d. industry practices constraint.

81. Which of the following best illustrates the accounting concept of conservatism?

a. Use of the allowance method to recognize bad debt losses from credit sales b. Use of the lower of cost or market approach in valuing inventories. c. Use of the same accounting method from one period to the next in computing

depreciation expense d. Utilization of a policy of deliberate understatement of asset values in order to present

a conservative net income figure 82. Trade-offs between the characteristics that make information useful may be necessary or

beneficial. Issuance of interim financial statements is an example of a trade-off between a. relevance and reliability. b. reliability and periodicity. c. timeliness and materiality. d. understandability and timeliness.

83. Allowing firms to estimate rather than physically count inventory at interim (quarterly)

periods is an example of a trade-off between a. verifiability and reliability. b. reliability and comparability. c. timeliness and verifiability. d. neutrality and consistency.

P84. In matters of doubt and great uncertainty, accounting issues should be resolved by

choosing the alternative that has the least favorable effect on net income, assets, and owners' equity. This guidance comes from the a. materiality constraint. b. industry practices constraint. c. conservatism constraint. d. full disclosure principle.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 16

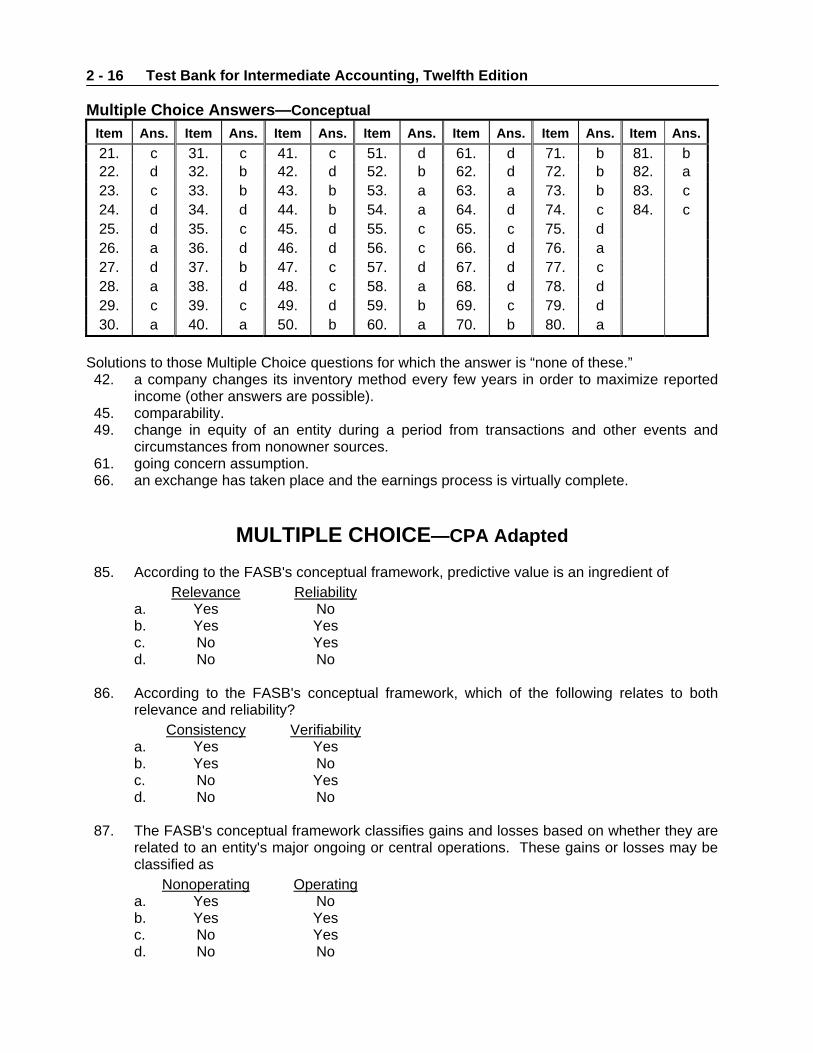

Multiple Choice Answers—Conceptual Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans.21. c 31. c 41. c 51. d 61. d 71. b 81. b 22. d 32. b 42. d 52. b 62. d 72. b 82. a 23. c 33. b 43. b 53. a 63. a 73. b 83. c 24. d 34. d 44. b 54. a 64. d 74. c 84. c 25. d 35. c 45. d 55. c 65. c 75. d 26. a 36. d 46. d 56. c 66. d 76. a 27. d 37. b 47. c 57. d 67. d 77. c 28. a 38. d 48. c 58. a 68. d 78. d 29. c 39. c 49. d 59. b 69. c 79. d 30. a 40. a 50. b 60. a 70. b 80. a

Solutions to those Multiple Choice questions for which the answer is “none of these.” 42. a company changes its inventory method every few years in order to maximize reported

income (other answers are possible). 45. comparability. 49. change in equity of an entity during a period from transactions and other events and

circumstances from nonowner sources. 61. going concern assumption. 66. an exchange has taken place and the earnings process is virtually complete.

MULTIPLE CHOICE—CPA Adapted 85. According to the FASB's conceptual framework, predictive value is an ingredient of

Relevance Reliability a. Yes No b. Yes Yes c. No Yes d. No No

86. According to the FASB's conceptual framework, which of the following relates to both

relevance and reliability? Consistency Verifiability a. Yes Yes b. Yes No c. No Yes d. No No

87. The FASB's conceptual framework classifies gains and losses based on whether they are

related to an entity's major ongoing or central operations. These gains or losses may be classified as Nonoperating Operating a. Yes No b. Yes Yes c. No Yes d. No No

Conceptual Framework Underlying Financial Accounting

2 - 17

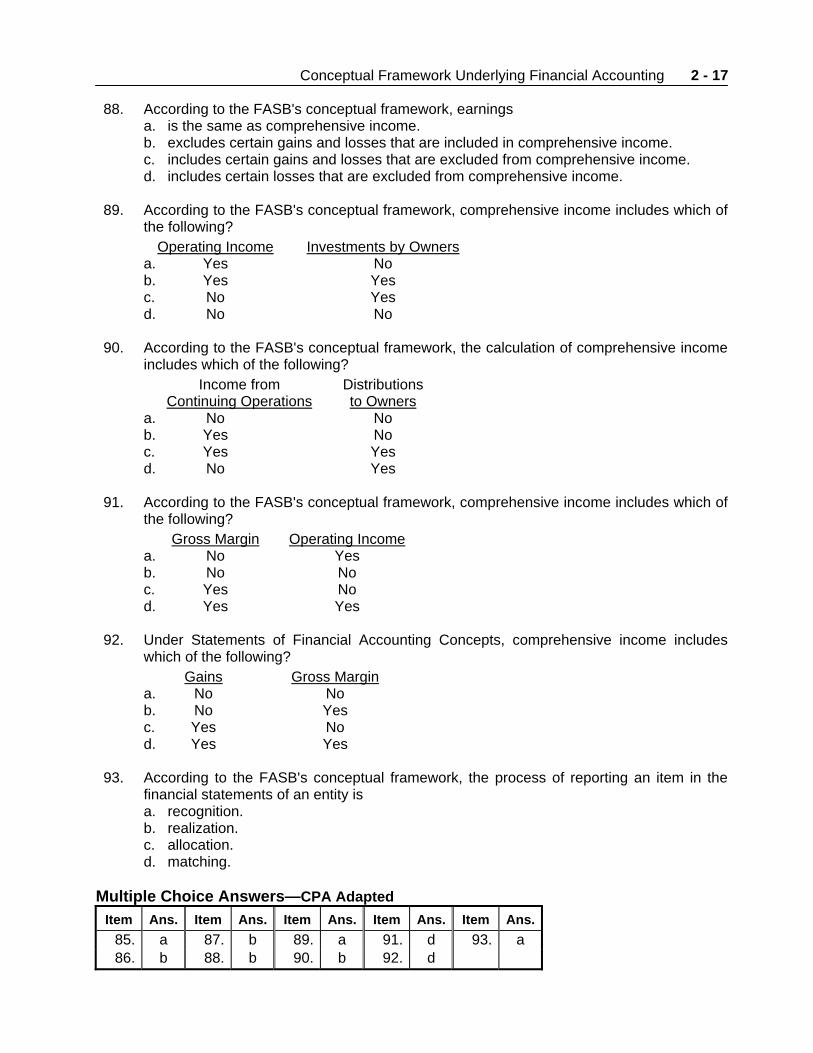

88. According to the FASB's conceptual framework, earnings a. is the same as comprehensive income. b. excludes certain gains and losses that are included in comprehensive income. c. includes certain gains and losses that are excluded from comprehensive income. d. includes certain losses that are excluded from comprehensive income.

89. According to the FASB's conceptual framework, comprehensive income includes which of

the following? Operating Income Investments by Owners a. Yes No b. Yes Yes c. No Yes d. No No

90. According to the FASB's conceptual framework, the calculation of comprehensive income

includes which of the following? Income from Distributions Continuing Operations to Owners a. No No b. Yes No c. Yes Yes d. No Yes

91. According to the FASB's conceptual framework, comprehensive income includes which of

the following? Gross Margin Operating Income a. No Yes b. No No c. Yes No d. Yes Yes

92. Under Statements of Financial Accounting Concepts, comprehensive income includes

which of the following? Gains Gross Margin a. No No b. No Yes c. Yes No d. Yes Yes

93. According to the FASB's conceptual framework, the process of reporting an item in the

financial statements of an entity is a. recognition. b. realization. c. allocation. d. matching.

Multiple Choice Answers—CPA Adapted

Item Ans. Item Ans. Item Ans. Item Ans. Item Ans.85. a 87. b 89. a 91. d 93. a 86. b 88. b 90. b 92. d

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 18

EXERCISES Ex. 2-94—Examination of the conceptual framework.

At an FASB Concept Framework Symposium, a former member of the FASB discussed his views of a conceptual framework. Some excerpts: Standard Setting in the Private Sector A framework of concepts comprises ideas that coordinate to form the fabric of a system: they determine its bounds. In a system like financial reporting that serves a broad public purpose, the first plank in the framework identifies the public role. The decision of the public sector in the 1930s to look at the private sector for the principal thrust to standard setting was sound and extraordinarily enlightened. The credence given financial reporting will determine whether the private sector's role in standard setting will grow or shrink. An operable conceptual framework will go a long way in providing the necessary level of credibility. Without an operable conceptual framework, continuation of standard setting by the private sector would stand in considerable jeopardy. Essence of the Conceptual Framework The conceptual formulation starts with the broad role of financial reporting in society. It: • Identifies its unique competence, that is, its bounds. • States the objectives of the reporting. • Defines the things admissible to financial statements. • Identifies the circumstances triggering admission and qualities to be met for admission to

financial statements. • Selects useful measurements of things admitted. • Furnishes criteria for display. Those are major pieces of the framework. There are others, of course. The various parts are in a hierarchy ranging from highly abstract to reasonably concrete. They lend guidance—they do not provide simple, no-think answers. They leave open a significant range for hard thinking and deliberation about reporting standards. They furnish the reference point for the thinking. Instructions 1. What are the basic concepts of the conceptual framework? 2. What are your views about the success of the conceptual framework? Solution 2-94 1. The basic components of the conceptual framework are:

a. Objectives—present the goals and purposes of accounting. b. Qualitative characteristics—the characteristics that make accounting information useful. c. Elements—provide the definitions of the broad classifications of items found in financial

statements. d. Operational guidelines (recognition and measurement concepts)—recommend concepts

to guide decisions concerning the display and disclosure of information about income, cash flows, and financial position. The operational guidelines are composed of three parts:

Conceptual Framework Underlying Financial Accounting

2 - 19

Solution 2-94 (cont.)

(1) Basic assumptions. (2) Accounting principles. (3) Constraints. 2. In general, the success of the conceptual framework will be determined by its acceptance in

practice. The acceptance in practice will be based in large part upon the FASB's solution of practical problems on a timely basis. It is a matter of opinion and yet to be seen whether or not the conceptual framework will bring about the following benefits. a. The FASB should be able to issue more useful and consistent standards in the future. b. New practice problems should be solved more rapidly by reference to an existing

framework. c. Better understanding of and confidence in the financial reporting process by financial

statement users should result. d. Enhanced comparability among companies' financial statements should result.

Ex. 2-95—Accounting concepts—identification.

State the accounting assumption, principle, information characteristic, or constraint that is most applicable in the following cases.

1. All payments less than $25 are expensed as incurred. (Do not use conservatism.)

2. The company employs the same inventory valuation method from period to period.

3. A patent is capitalized and amortized over the periods benefited.

4. Assuming that dollars today will buy as much as ten years ago.

5. Rent paid in advance is recorded as prepaid rent.

6. Financial statements are prepared each year.

7. All significant post-balance sheet events are reported.

8. Personal transactions of the proprietor are distinguished from business transactions. Solution 2-95 1. Materiality constraint. 2. Consistency characteristic. 3. Matching principle or going concern assumption. 4. Monetary unit assumption. 5. Matching principle or going concern assumption. 6. Periodicity assumption. 7. Full disclosure principle. 8. Economic entity assumption.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 20

Ex. 2-96—Accounting concepts—identification.

Presented below are a number of accounting procedures and practices in Sanchez Corp. For each of these items, list the assumption, principle, information characteristic, or modifying convention that is violated.

1. Because the company's income is low this year, a switch from accelerated depreciation to straight-line depreciation is made this year.

2. The president of Sanchez Corp. believes it is foolish to report financial information on a yearly basis. Instead, the president believes that financial information should be disclosed only when significant new information is available related to the company's operations.

3. Sanchez Corp. decides to establish a large loss and related liability this year because of the possibility that it may lose a pending patent infringement lawsuit. The possibility of loss is considered remote by its attorneys.

4. An officer of Sanchez Corp. purchased a new home computer for personal use with company money, charging miscellaneous expense.

5. A machine, that cost $40,000, is reported at its current market value of $45,000. Solution 2-96 1. Consistency. 2. Periodicity. 3. Matching (also, conservatism). 4. Economic entity. 5. Historical cost (also, revenue recognition)*.

*Reporting the asset at FMV of $45,000 implies the following entry: Machine ..................................................................................... 5,000 Revenue ........................................................................ 5,000 Ex. 2-97—Accounting concepts—matching.

Listed below are several information characteristics and accounting principles and assumptions. Match the letter of each with the appropriate phrase that states its application. (Items a through k may be used more than once or not at all.)

a. Economic entity assumption g. Matching principle b. Going concern assumption h. Full disclosure principle c. Monetary unit assumption i. Relevance characteristic d. Periodicity assumption j. Reliability characteristic e. Historical cost principle k. Consistency characteristic f. Revenue recognition principle

____ 1. Stable-dollar assumption (do not use historical cost principle).

____ 2. Earning process completed and realized or realizable.

____ 3. Presentation of error-free information with representational faithfulness.

____ 4. Yearly financial reports.

____ 5. Accruals and deferrals in adjusting and closing process. (Do not use going concern.)

Conceptual Framework Underlying Financial Accounting

2 - 21

Ex. 2-97 (cont.)

____ 6. Useful standard measuring unit for business transactions.

____ 7. Notes as part of necessary information to a fair presentation.

____ 8. Affairs of the business distinguished from those of its owners.

____ 9. Business enterprise assumed to have a long life.

____ 10. Valuing assets at amounts originally paid for them.

____ 11. Application of the same accounting principles as in the preceding year.

____ 12. Summarizing significant accounting policies.

____ 13. Presentation of timely information with predictive and feedback value. Solution 2-97 1. c 4. d 7. h 10. e 13. i 2. f 5. g 8. a 11. k 3. j 6. c 9. b 12. h Ex. 2-98—Accounting concepts—fill in the blanks.

Fill in the blanks below with the accounting principle, assumption, or related item that best completes the sentence. 1. ________________________ and _______________________ are the two primary

qualities that make accounting information useful for decision making. 2. Information that helps users confirm or correct prior expectations has _________________ ___________________. 3. ________________________ enables users to identify the real similarities and differences

in economic phenomena because the information has been measured and reported in a similar manner for different enterprises.

4. Some costs which give rise to future benefits cannot be directly associated with the

revenues they generate. Such costs are allocated in a __________________ and _________________ manner to the periods expected to benefit from the cost.

5. _______________________ would allow the expensing of all repair tools when purchased,

even though they have an estimated life of 3 years. 6. The ________________________ characteristic requires that the same accounting method

be used from one accounting period to the next, unless it becomes evident that an alternative method will bring about a better description of a firm's financial situation.

7. ____________________ guides accountants to select the accounting treatment that is least

likely to overstate income and assets.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 22

Ex. 2-98 (cont.)

8. Parenthetical balance sheet disclosure of the inventory method utilized by a particular company is an application of the _______________________ principle.

9. Corporations must prepare accounting reports at least yearly due to the _______________

assumption. 10. Recording and reporting inflows at the end of production is an allowable exception to the

_________________ principle. Solution 2-98 1. Relevance; reliability 6. consistency 2. feedback value 7. Conservatism 3. Comparability 8. full disclosure 4. rational; systematic 9. periodicity 5. The materiality convention 10. revenue recognition Ex. 2-99—Basic assumptions. Briefly explain the four basic assumptions that underlie financial accounting. Solution 2-99 1. The economic entity assumption states that economic activity can be identified with a

particular unit of accountability.

2. The going concern assumption assumes that a business enterprise will have a long life.

3. The monetary unit assumption means that money is the common denominator of economic activity and provides an appropriate basis for accounting measurement and analysis. In addition, the monetary unit remains reasonably stable.

4. The periodicity assumption implies that the economic activities of an enterprise can be divided into artificial time periods.

Ex. 2-100—Revenue recognition.

Revenue is generally recognized at the point of sale. There are three exceptions, however. Name the time for each exception, give two qualifications or criteria for the use of each exception, and give an example for each exception. Solution 2-100 1. During production. The revenue is known (contract) or dependably estimable. Total costs are

estimable or other means are available to estimate progress toward completion. Examples are long-term construction contracts and service-type transactions.

Conceptual Framework Underlying Financial Accounting

2 - 23

Solution 2-100 (cont.) 2. At completion. There are quoted prices. Units are interchangeable. There are no significant

distribution costs. Unit costs are not determinable. Examples are precious metals or agricultural products.

3. At collection. There is no reasonable basis for estimating the degree of collectibility. Costs of collection, bad debts, and repossessions are not estimable. Examples are installment sales and cost recovery method.

Ex. 2-101—Historical cost principle.

Cost as a basis of accounting for assets has been severely criticized. What defense can you build for cost as the basis for financial accounting? Solution 2-101 Cost is definite and verifiable and not a matter for conjecture or opinion. Once established, cost is fixed as long as the asset remains the property of the party that incurred the cost. Cost is based on fact; that is, it is the result of an arm's length transaction. Cost is also measurable or determinable. Over the years, accountants have found cost to be the most practical basis for record keeping. Financial statements prepared on a cost basis provide business enterprise information having a common, accepted basis from which each reader can make inferences, comparisons, and analyses. Ex. 2-102—Matching concept.

A concept is a group of related ideas. Matching could be considered a concept because it includes ideas related to both revenue recognition and expense recognition. Briefly explain the ideas in (a) revenue recognition and (b) expense recognition. Solution 2-102 (a) The ideas in revenue recognition include the "three R's" and "earned": 1. Revenues are inflows of net assets from delivering or producing goods or services or

other earning activities that are the major operations of an enterprise during a period. 2. Recognition is recording and reporting in the financial statements. 3. Revenues are realized when goods or services are exchanged for cash or claims to cash. 4. Revenues are earned when the earnings process is complete or virtually complete.

The revenue recognition principle is that revenue is recognized when it is realized and it is earned.

(b) The ideas in expense recognition include "expense" and "matching": 1. Expenses are outflows of net assets during a period from delivering or producing goods or

services or other activities that are the major operations of the entity. 2. Expenses are recognized when the goods or services (efforts) make their contribution to

revenue.

Test Bank for Intermediate Accounting, Twelfth Edition

2 - 24

Solution 2-102 (cont.)

The matching principle is that expenses are matched with revenues. Expenses are matched three ways:

1. When there is an association with revenue, expenses are matched with revenues in the period the revenues are recognized.

2. When no association with revenue is evident, expenses are allocated on some systematic and rational basis.

3. When no association with revenue is evident and no future benefits are expected, expenses are recognized immediately.

CHAPTER 4

INCOME STATEMENT AND RELATED INFORMATION

TRUE-FALSE—Conceptual Answer No. Description T 1. Usefulness of the income statement. F 2. Limitations of the income statement. F 3. Earnings management. T 4. Transaction approach of income measurement. T 5. Single-step income statement. T 6. Revenues and gains. F 7. Multiple-step vs. single-step income statement. F 8. Multiple-step income statement. T 9. Multiple-step vs. single-step income statement. F 10. Current operating performance approach. T 11. Reporting discontinued operations. F 12. Reporting extraordinary items. F 13. Irregular items. T 14. Intraperiod tax allocation. F 15. Reporting earnings per share. F 16. Computation of earnings per share. T 17. Prior period adjustments. F 18. Retained earnings restrictions. F 19. Comprehensive income definition. T 20. Reporting other comprehensive income.

MULTIPLE CHOICE—Conceptual Answer No. Description c 21. Elements of the income statement. d 22. Usefulness of the income statement. b 23. Limitations of the income statement. d S24. Use of an income statement. d S25. Income statement reporting. b 26. Single-step income statement. d 27. Methods of preparing income statements. a 28. Income statement presentation. b 29. Event with no income statement effect. c S30. Net income effect. b P31. Selling expenses. b P32. Reporting merchandise inventory. a 33. Definition of an extraordinary item. d 34. Classification of an extraordinary item. d 35. Identification of an extraordinary item. a 36. Identification of an extraordinary item.

Test Bank for Intermediate Accounting, Twelfth Edition

4 - 2

MULTIPLE CHOICE—Conceptual (cont.) Answer No. Description d 37. Identification of an extraordinary item. a 38. Presentation of unusual or infrequent items. d 39. Identification of a change in accounting principle. d 40. Classification of extraordinary items. c 41. EPS disclosures on income statement. c 42. Reporting discontinued operations. d 43. Intraperiod tax allocation. d 44. Purpose of intraperiod tax allocation. c S45. Reporting unusual or infrequent items. c S46. Earnings per share disclosure. d P47. Reporting correction of an error. c 48. Retained earnings statement. d 49. Prior period adjustment. d 50. Identification of a prior period adjustment. c 51. Comprehensive income items. c 52. Providing information about components of comprehensive income.

MULTIPLE CHOICE—Computational Answer No. Description a 53. Single-step income statement. c 54. Multiple-step income statement. c 55. Multiple-step income statement. c 56. Calculation of net sales. a 57. Presentation of gain on sale of plant assets. a 58. Extraordinary items. a 59. Extraordinary items. a 60. Calculate income before extraordinary items. c 61. Calculate income before taxes and extraordinary items. b 62. Calculate extraordinary loss. a 63. Events affecting income from continuing operations. b 64. Calculation of events affecting net income. c 65. Disposal of a major business component. c 66. Tax effect on irregular items. c 67. Tax effect on irregular items. c 68. Earnings per share. c 69. Earnings per share. a 70. Retained earnings statement. b 71. Retained earnings statement. c 72. Retained earnings statement. d 73. Retained earnings statement. d 74. Calculate balance of retained earnings. d 75. Calculate other comprehensive income. a 76. Calculate comprehensive income. P Note: these questions also appear in the Problem-Solving Survival Guide. S Note: these questions also appear in the Study Guide.

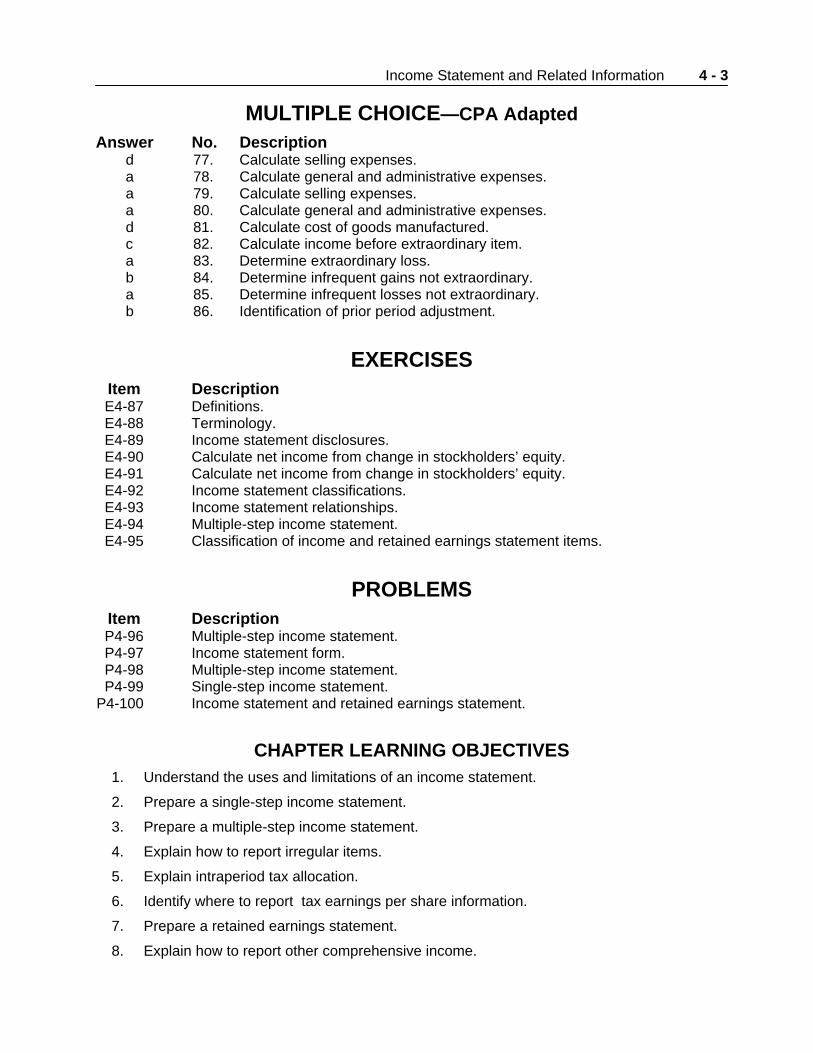

Income Statement and Related Information

4 - 3

MULTIPLE CHOICE—CPA Adapted Answer No. Description d 77. Calculate selling expenses. a 78. Calculate general and administrative expenses. a 79. Calculate selling expenses. a 80. Calculate general and administrative expenses. d 81. Calculate cost of goods manufactured. c 82. Calculate income before extraordinary item. a 83. Determine extraordinary loss. b 84. Determine infrequent gains not extraordinary. a 85. Determine infrequent losses not extraordinary. b 86. Identification of prior period adjustment.

EXERCISES Item Description E4-87 Definitions. E4-88 Terminology. E4-89 Income statement disclosures. E4-90 Calculate net income from change in stockholders’ equity. E4-91 Calculate net income from change in stockholders’ equity. E4-92 Income statement classifications. E4-93 Income statement relationships. E4-94 Multiple-step income statement. E4-95 Classification of income and retained earnings statement items.

PROBLEMS

Item Description P4-96 Multiple-step income statement. P4-97 Income statement form. P4-98 Multiple-step income statement. P4-99 Single-step income statement. P4-100 Income statement and retained earnings statement.

CHAPTER LEARNING OBJECTIVES 1. Understand the uses and limitations of an income statement.

2. Prepare a single-step income statement.

3. Prepare a multiple-step income statement.

4. Explain how to report irregular items.

5. Explain intraperiod tax allocation.

6. Identify where to report tax earnings per share information.

7. Prepare a retained earnings statement.

8. Explain how to report other comprehensive income.

Test Bank for Intermediate Accounting, Twelfth Edition

4 - 4

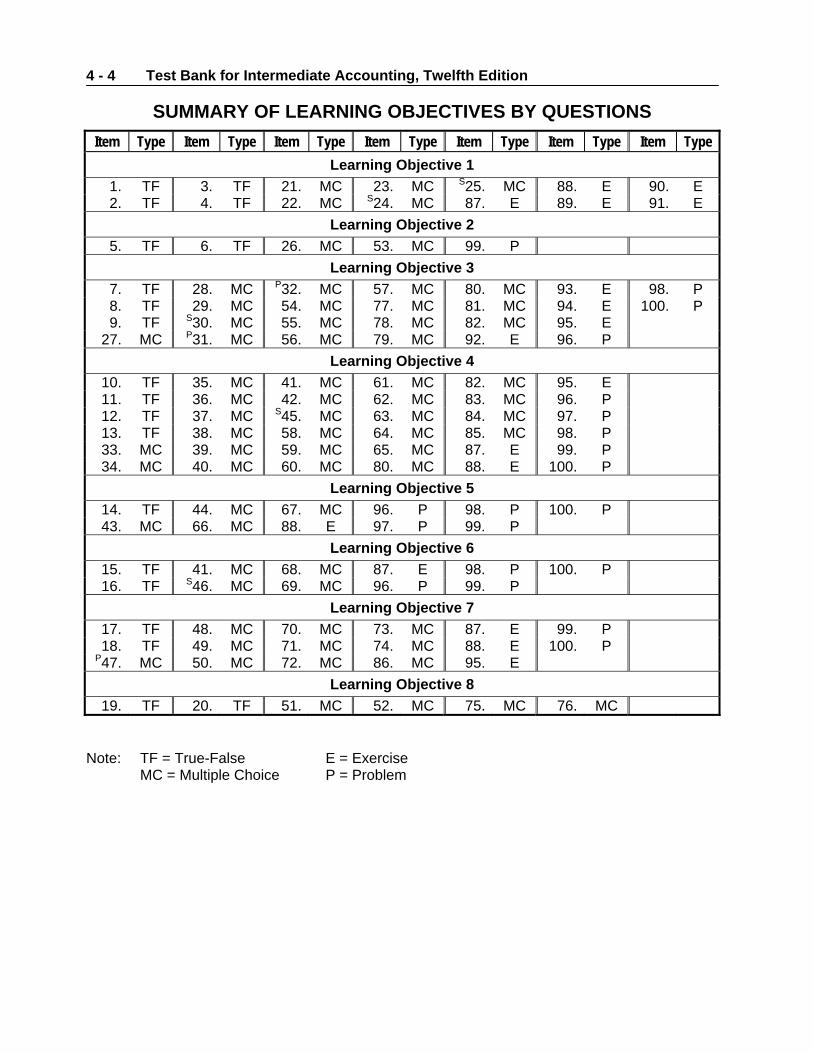

SUMMARY OF LEARNING OBJECTIVES BY QUESTIONS Item Type Item Type Item Type Item Type Item Type Item Type Item Type

Learning Objective 1 1. TF 3. TF 21. MC 23. MC S25. MC 88. E 90. E 2. TF 4. TF 22. MC S24. MC 87. E 89. E 91. E

Learning Objective 2 5. TF 6. TF 26. MC 53. MC 99. P

Learning Objective 3 7. TF 28. MC P32. MC 57. MC 80. MC 93. E 98. P 8. TF 29. MC 54. MC 77. MC 81. MC 94. E 100. P 9. TF S30. MC 55. MC 78. MC 82. MC 95. E

27. MC P31. MC 56. MC 79. MC 92. E 96. P Learning Objective 4

10. TF 35. MC 41. MC 61. MC 82. MC 95. E 11. TF 36. MC 42. MC 62. MC 83. MC 96. P 12. TF 37. MC S45. MC 63. MC 84. MC 97. P 13. TF 38. MC 58. MC 64. MC 85. MC 98. P 33. MC 39. MC 59. MC 65. MC 87. E 99. P 34. MC 40. MC 60. MC 80. MC 88. E 100. P

Learning Objective 5 14. TF 44. MC 67. MC 96. P 98. P 100. P 43. MC 66. MC 88. E 97. P 99. P

Learning Objective 6 15. TF 41. MC 68. MC 87. E 98. P 100. P 16. TF S46. MC 69. MC 96. P 99. P

Learning Objective 7 17. TF 48. MC 70. MC 73. MC 87. E 99. P 18. TF 49. MC 71. MC 74. MC 88. E 100. P

P47. MC 50. MC 72. MC 86. MC 95. E Learning Objective 8

19. TF 20. TF 51. MC 52. MC 75. MC 76. MC Note: TF = True-False E = Exercise MC = Multiple Choice P = Problem

Income Statement and Related Information

4 - 5

TRUE-FALSE—Conceptual 1. The income statement is useful for helping to assess the risk or uncertainty of achieving

future cash flows. 2. A strength of the income statement as compared to the balance sheet is that items that

cannot be measured reliably can be reported in the income statement. 3. Earnings management generally makes income statement information more useful for

predicting future earnings and cash flows. 4. The transaction approach of income measurement focuses on the income-related activities

that have occurred during the period. 5. Companies frequently report income tax expense as the last item before net income on a

single-step income statement. 6. Both revenues and gains increase both net income and owners’ equity. 7. Use of a multiple-step income statement will result in the company reporting a higher net

income than if they used a single-step income statement. 8. The primary advantage of the multiple-step format lies in the simplicity of presentation and

the absence of any implication that one type of revenue or expense item has priority over another.

9. Gross profit and income from operations are reported on a multiple-step but not a single-

step income statement. 10. The accounting profession has adopted a current operating performance approach to

income reporting. 11. Companies report the results of operations of a component of a business that will be

disposed of separately from continuing operations. 12. Gains or losses from exchange or translation of foreign currencies are reported as

extraordinary items. 13. Discontinued operations, extraordinary items, and unusual gains and losses are all reported

net of tax in the income statement. 14. Intraperiod tax allocation relates the income tax expense of the period to the specific items

that give rise to the amount of the tax provision. 15. A company that reports a discontinued operation or an extraordinary item has the option of

reporting per share amounts for these items. 16. Dividends declared on common and preferred stock are subtracted from net income in the

computation of earnings per share.

Test Bank for Intermediate Accounting, Twelfth Edition

4 - 6

17. Prior period adjustments can either be added or subtracted in the Retained Earnings Statement.

18. Companies only restrict retained earnings to comply with contractual requirements or

current necessity. 19. Comprehensive income includes all changes in equity during a period except those

resulting from distributions to owners. 20. The components of other comprehensive income can be reported in a statement of

stockholders’ equity. True False Answers—Conceptual

Item Ans. Item Ans. Item Ans. Item Ans. 1. T 6. T 11. T 16. F 2. F 7. F 12. F 17. T 3. F 8. F 13. F 18. F 4. T 9. T 14. T 19. F 5. T 10. F 15. F 20. T

MULTIPLE CHOICE—Conceptual 21. The major elements of the income statement are

a. revenue, cost of goods sold, selling expenses, and general expense. b. operating section, nonoperating section, discontinued operations, extraordinary items,

and cumulative effect. c. revenues, expenses, gains, and losses. d. all of these.

22. Information in the income statement helps users to

a. evaluate the past performance of the enterprise. b. provide a basis for predicting future performance. c. help assess the risk or uncertainty of achieving future cash flows. d. all of these.

23. Limitations of the income statement include all of the following except

a. items that cannot be measured reliably are not reported. b. only actual amounts are reported in determining net income. c. income measurement involves judgment. d. income numbers are affected by the accounting methods employed.

S24. Which of the following would represent the least likely use of an income statement

prepared for a business enterprise? a. Use by customers to determine a company's ability to provide needed goods and

services. b. Use by labor unions to examine earnings closely as a basis for salary discussions. c. Use by government agencies to formulate tax and economic policy. d. Use by investors interested in the financial position of the entity.

Income Statement and Related Information

4 - 7

S25. The income statement reveals a. resources and equities of a firm at a point in time. b. resources and equities of a firm for a period of time. c. net earnings (net income) of a firm at a point in time. d. net earnings (net income) of a firm for a period of time.

26. The single-step income statement emphasizes

a. the gross profit figure. b. total revenues and total expenses. c. extraordinary items and accounting changes more than these are emphasized in the

multiple-step income statement. d. the various components of income from continuing operations.

27. Which of the following is an acceptable method of presenting the income statement?

a. A single-step income statement b. A multiple-step income statement c. A consolidated statement of income d. All of these

28. Which of the following is not a generally practiced method of presenting the income

statement? a. Including prior period adjustments in determining net income b. The single-step income statement c. The consolidated statement of income d. Including gains and losses from discontinued operations of a component of a business

in determining net income 29. The occurrence which most likely would have no effect on 2007 net income (assuming

that all amounts involved are material) is the a. sale in 2007 of an office building contributed by a stockholder in 1983. b. collection in 2007 of a receivable from a customer whose account was written off in

2006 by a charge to the allowance account. c. settlement based on litigation in 2007 of previously unrecognized damages from a

serious accident which occurred in 2005. d. worthlessness determined in 2007 of stock purchased on a speculative basis in 2003.

S30. The occurrence that most likely would have no effect on 2007 net income is the

a. sale in 2007 of an office building contributed by a stockholder in 1961. b. collection in 2007 of a dividend from an investment. c. correction of an error in the financial statements of a prior period discovered

subsequent to their issuance. d. stock purchased in 1993 deemed worthless in 2007.

P31. Which of the following is not a selling expense?

a. Advertising expense b. Office salaries expense c. Freight-out d. Store supplies consumed

Test Bank for Intermediate Accounting, Twelfth Edition

4 - 8

P32. The accountant for the Orion Sales Company is preparing the income statement for 2007 and the balance sheet at December 31, 2007. The January 1, 2007 merchandise inventory balance will appear a. only as an asset on the balance sheet. b. only in the cost of goods sold section of the income statement. c. as a deduction in the cost of goods sold section of the income statement and as a

current asset on the balance sheet. d. as an addition in the cost of goods sold section of the income statement and as a

current asset on the balance sheet. 33. In order to be classified as an extraordinary item in the income statement, an event or

transaction should be a. unusual in nature, infrequent, and material in amount. b. unusual in nature and infrequent, but it need not be material. c. infrequent and material in amount, but it need not be unusual in nature. d. unusual in nature and material, but it need not be infrequent.

34. Classification as an extraordinary item on the income statement would be appropriate for

the a. gain or loss on disposal of a component of the business. b. substantial write-off of obsolete inventories. c. loss from a strike. d. none of these.

35. Which of these is generally an example of an extraordinary item?

a. Loss incurred because of a strike by employees. b. Write-off of deferred marketing costs believed to have no future benefit. c. Gain resulting from the devaluation of the U.S. dollar. d. Gain resulting from the state exercising its right of eminent domain on a piece of land

used as a parking lot. 36. Under which of the following conditions would material flood damage be considered an

extraordinary item for financial reporting purposes? a. Only if floods in the geographical area are unusual in nature and occur infrequently. b. Only if the flood damage is material in amount and could have been reduced by

prudent management. c. Under any circumstances as an extraordinary item. d. Flood damage should never be classified as an extraordinary item.

37. An item that should be classified as an extraordinary item is

a. write-off of goodwill. b. gains from transactions involving foreign currencies. c. losses from moving a plant to another city. d. gains from a company selling the only investment it has ever owned.

38. How should an unusual event not meeting the criteria for an extraordinary item be

disclosed in the financial statements? a. Shown as a separate item in operating revenues or expenses if material and supple-

mented by a footnote if deemed appropriate. b. Shown in operating revenues or expenses if material but not shown as a separate item. c. Shown net of income tax after ordinary net earnings but before extraordinary items. d. Shown net of income tax after extraordinary items but before net earnings.

Income Statement and Related Information

4 - 9

39. Which of the following is a change in accounting principle? a. A change in the estimated service life of machinery b. A change from FIFO to LIFO c. A change from straight-line to double-declining-balance d. A change from FIFO to LIFO and a change from straight-line to double-declining-

balance 40. Which of the following is never classified as an extraordinary item?

a. Losses from a major casualty. b. Losses from an expropriation of assets. c. Gain on a sale of the only security investment a company has ever owned. d. Losses from exchange or translation of foreign currencies.

41. Which of the following is a required disclosure in the income statement when reporting the

disposal of a component of the business? a. The gain or loss on disposal should be reported as an extraordinary item. b. Results of operations of a discontinued component should be disclosed immediately

below extraordinary items. c. Earnings per share from both continuing operations and net income should be

disclosed on the face of the income statement. d. The gain or loss on disposal should not be segregated, but should be reported together

with the results of continuing operations. 42. When a company discontinues an operation and disposes of the discontinued operation

(component), the transaction should be included in the income statement as a gain or loss on disposal reported as a. a prior period adjustment. b. an extraordinary item. c. an amount after continuing operations and before extraordinary items. d. a bulk sale of plant assets included in income from continuing operations.

43. Income taxes are allocated to

a. extraordinary items. b. discontinued operations. c. prior period adjustments. d. all of these.

44. Which of the following is true about intraperiod tax allocation?

a. It arises because certain revenue and expense items appear in the income statement either before or after they are included in the tax return.

b. It is required for extraordinary items and cumulative effect of accounting changes but not for prior period adjustments.

c. Its purpose is to allocate income tax expense evenly over a number of accounting periods.

d. Its purpose is to relate the income tax expense to the items which affect the amount of tax.

Test Bank for Intermediate Accounting, Twelfth Edition

4 - 10

S45. A material item which is unusual in nature or infrequent in occurrence, but not both should be shown in the income statement

Net of Tax Disclosed Separately a. No No b. Yes Yes c. No Yes d. Yes No

S46. Earnings per share should always be shown separately for

a. net income and gross margin. b. net income and pretax income. c. income before extraordinary items. d. extraordinary items and prior period adjustments.

P47. A correction of an error in prior periods' income will be reported

In the income statement Net of tax a. Yes Yes b. No No c. Yes No d. No Yes

48. Which of the following items will not appear in the retained earnings statement?

a. Net loss b. Prior period adjustment c. Discontinued operations d. Dividends

49. Which one of the following types of losses is excluded from the determination of net

income in income statements? a. Material losses resulting from transactions in the company's investments account. b. Material losses resulting from unusual sales of assets not acquired for resale. c. Material losses resulting from the write-off of intangibles. d. Material losses resulting from correction of errors related to prior periods.

50. Shank Corporation made a very large arithmetical error in the preparation of its year-end

financial statements by improper placement of a decimal point in the calculation of depreciation. The error caused the net income to be reported at almost double the proper amount. Correction of the error when discovered in the next year should be treated as a. an increase in depreciation expense for the year in which the error is discovered. b. a component of income for the year in which the error is discovered, but separately

listed on the income statement and fully explained in a note to the financial statements.

c. an extraordinary item for the year in which the error was made. d. a prior period adjustment.

51. Comprehensive income includes all of the following except

a. dividend revenue. b. losses on disposal of assets. c. investments by owners. d. unrealized holding gains.

Income Statement and Related Information

4 - 11

52. The approach most companies use to provide information related to the components of other comprehensive income is a a. second separate income statement. b. combined income statement of comprehensive income. c. separate column in the statement of changes in stockholders’ equity. d. footnote disclosure.

Multiple Choice Answers—Conceptual

Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans.21. c 26. b 31. b 36. a 41. c 46. c 51. c 22. d 27. d 32. b 37. d 42. c 47. d 52. c 23. d 28. a 33. a 38. a 43. d 48. c 24. d 29. b 34. d 39. d 44. d 49. d 25. d 30. c 35. d 40. d 45. c 50. d

Solution to Multiple Choice question for which the answer is “none of these.” 34. Many answers are possible.

MULTIPLE CHOICE—Computational 53. For Garret Wolfe Company, the following information is available:

Cost of goods sold $ 60,000 Dividend revenue 2,500 Income tax expense 6,000 Operating expenses 23,000 Sales 100,000

In Garret Wolfe’s single-step income statement, gross profit a. should not be reported. b. should be reported at $13,500. c. should be reported at $40,000. d. should be reported at $42,500.

54. For Garret Wolfe Company, the following information is available:

Cost of goods sold $ 60,000 Dividend revenue 2,500 Income tax expense 6,000 Operating expenses 23,000 Sales 100,000

In Garret Wolfe’s multiple-step income statement, gross profit a. should not be reported b. should be reported at $13,500. c. should be reported at $40,000. d. should be reported at $42,500.

Test Bank for Intermediate Accounting, Twelfth Edition

4 - 12

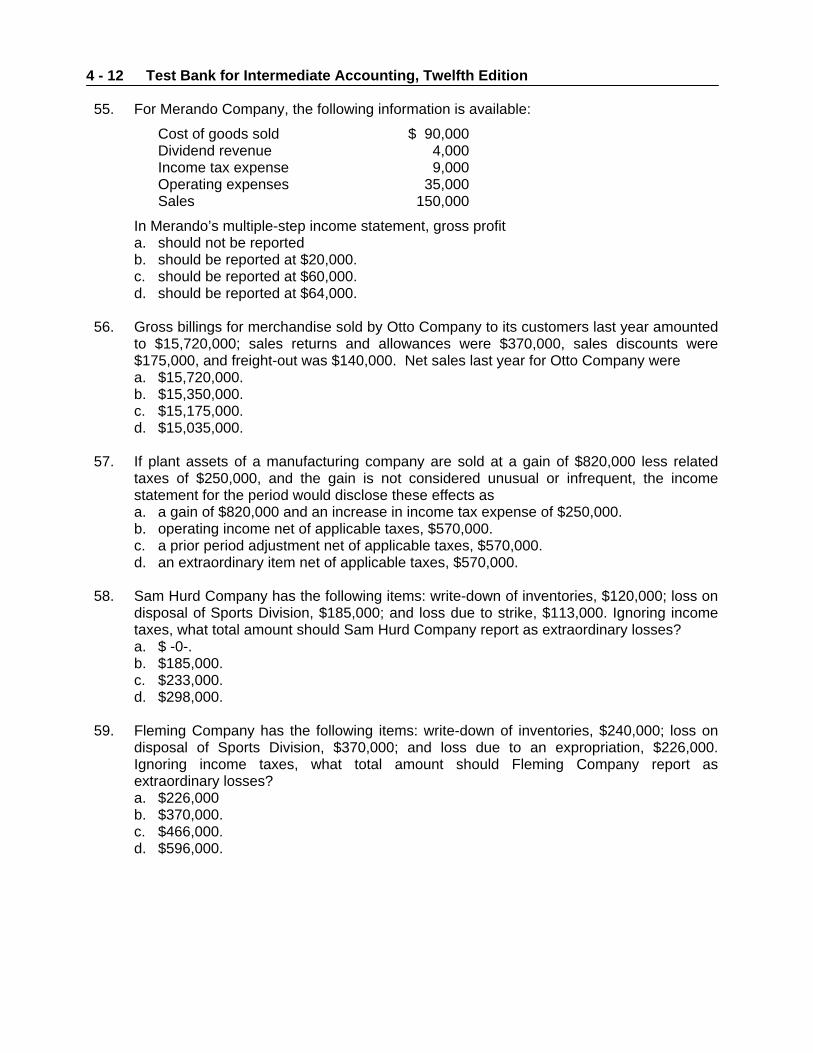

55. For Merando Company, the following information is available:

Cost of goods sold $ 90,000 Dividend revenue 4,000 Income tax expense 9,000 Operating expenses 35,000 Sales 150,000

In Merando’s multiple-step income statement, gross profit a. should not be reported b. should be reported at $20,000. c. should be reported at $60,000. d. should be reported at $64,000.

56. Gross billings for merchandise sold by Otto Company to its customers last year amounted

to $15,720,000; sales returns and allowances were $370,000, sales discounts were $175,000, and freight-out was $140,000. Net sales last year for Otto Company were a. $15,720,000. b. $15,350,000. c. $15,175,000. d. $15,035,000.

57. If plant assets of a manufacturing company are sold at a gain of $820,000 less related

taxes of $250,000, and the gain is not considered unusual or infrequent, the income statement for the period would disclose these effects as a. a gain of $820,000 and an increase in income tax expense of $250,000. b. operating income net of applicable taxes, $570,000. c. a prior period adjustment net of applicable taxes, $570,000. d. an extraordinary item net of applicable taxes, $570,000.

58. Sam Hurd Company has the following items: write-down of inventories, $120,000; loss on

disposal of Sports Division, $185,000; and loss due to strike, $113,000. Ignoring income taxes, what total amount should Sam Hurd Company report as extraordinary losses? a. $ -0-. b. $185,000. c. $233,000. d. $298,000.

59. Fleming Company has the following items: write-down of inventories, $240,000; loss on

disposal of Sports Division, $370,000; and loss due to an expropriation, $226,000. Ignoring income taxes, what total amount should Fleming Company report as extraordinary losses? a. $226,000 b. $370,000. c. $466,000. d. $596,000.

Income Statement and Related Information

4 - 13

60. An income statement shows “income before income taxes and extraordinary items” in the amount of $2,055,000. The income taxes payable for the year are $1,080,000, including $360,000 that is applicable to an extraordinary gain. Thus, the “income before extraordinary items” is a. $1,335,000. b. $615,000. c. $1,395,000. d. $675,000.

61. Cole Company, with an applicable income tax rate of 30%, reported net income of

$210,000. Included in income for the period was an extraordinary loss from flood damage of $30,000 before deducting the related tax effect. The company's income before income taxes and extraordinary items was a. $240,000. b. $300,000. c. $330,000. d. $231,000.

62. A review of the December 31, 2007, financial statements of Baden Corporation revealed

that under the caption "extraordinary losses," Baden reported a total of $515,000. Further analysis revealed that the $515,000 in losses was comprised of the following items:

(1) Baden recorded a loss of $150,000 incurred in the abandonment of equipment formerly used in the business.

(2) In an unusual and infrequent occurrence, a loss of $250,000 was sustained as a result of hurricane damage to a warehouse.

(3) During 2007, several factories were shut down during a major strike by employees, resulting in a loss of $85,000.

(4) Uncollectible accounts receivable of $30,000 were written off as uncollectible.

Ignoring income taxes, what amount of loss should Baden report as extraordinary on its 2007 income statement? a. $150,000. b. $250,000. c. $400,000. d. $515,000.

Use the following information for questions 63 and 64.

At Hall Company, events and transactions during 2007 included the following. The tax rate for all items is 30%.

(1) Depreciation for 2005 was found to be understated by $30,000. (2) A strike by the employees of a supplier resulted in a loss of $25,000. (3) The inventory at December 31, 2005 was overstated by $40,000. (4) A flood destroyed a building that had a book value of $500,000. Floods are very

uncommon in that area. 63. The effect of these events and transactions on 2007 income from continuing operations

net of tax would be a. $17,500. b. $38,500. c. $66,500. d. $416,500.

Test Bank for Intermediate Accounting, Twelfth Edition

4 - 14

64. The effect of these events and transactions on 2007 net income net of tax would be a. $17,500. b. $367,500. c. $388,500. d. $416,500.

65. During 2007, Gomez Corporation disposed of Pine Division, a major component of its

business. Gomez realized a gain of $1,200,000, net of taxes, on the sale of Pine's assets. Pine's operating losses, net of taxes, were $1,400,000 in 2007. How should these facts be reported in Gomez's income statement for 2007? Total Amount to be Included in Income from Results of Continuing Operations Discontinued Operations a. $1,400,000 loss $1,200,000 gain b. 200,000 loss 0 c. 0 200,000 loss d. 1,200,000 gain 1,400,000 loss

66. Dan Nicholson Corporation has an extraordinary loss of $50,000, an unusual gain of

$35,000, and a tax rate of 40%. At what amount should Dan Nicholson report each item? Extraordinary loss Unusual gain a. $(50,000) $35,000 b. (50,000) 21,000 c. (30,000) 35,000 d. (30,000) 21,000

67. Carpino Corporation has an extraordinary loss of $200,000, an unusual gain of $140,000,

and a tax rate of 40%. At what amount should Carpino report each item? Extraordinary loss Unusual gain a. $(200,000) $140,000 b. (200,000) 84,000 c. (120,000) 140,000 d. (120,000) 84,000

68. Craig Rusch Corporation reports the following information:

Net income $500,000 Dividends on common stock 140,000 Dividends on preferred stock 60,000 Weighted average common shares outstanding 100,000

Rusch should report earnings per share of a. $3.00. b. $3.60 c. $4.40. d. $5.00.

Income Statement and Related Information

4 - 15

69. Edmonds Corporation reports the following information:

Net income $500,000 Dividends on common stock 140,000 Dividends on preferred stock 60,000 Weighted average common shares outstanding 200,000

Edmonds should report earnings per share of a. $1.50. b. $1.80 c. $2.20. d. $2.50.

70. Simmons Corporation reports the following information:

Correction of understatement of depreciation expense in prior years, net of tax $ 430,000 Dividends declared 320,000 Net income 1,000,000 Retained earnings, 1/1/07, as reported 2,000,000

Simmons should report retained earnings, 1/1/07, as adjusted at a. $1,570,000. b. $2,000,000. c. $2,430,000. d. $3,110,000.

71. Simmons Corporation reports the following information:

Correction of understatement of depreciation expense in prior years, net of tax $ 430,000 Dividends declared 320,000 Net income 1,000,000 Retained earnings, 1/1/07, as reported 2,000,000

Simmons should report retained earnings, 12/31/07, as adjusted at a. $1,570,000. b. $2,250,000. c. $2,680,000. d. $3,110,000.

72. Joe Novak Corporation reports the following information:

Correction of overstatement of depreciation expense in prior years, net of tax $ 215,000 Dividends declared 160,000 Net income 500,000 Retained earnings, 1/1/07, as reported 1,000,000

Joe Novak should report retained earnings, 1/1/07, as adjusted at a. $785,000. b. $1,000,000. c. $1,215,000. d. $1,555,000.

Test Bank for Intermediate Accounting, Twelfth Edition

4 - 16

73. Joe Novak Corporation reports the following information:

Correction of overstatement of depreciation expense in prior years, net of tax $ 215,000 Dividends declared 160,000 Net income 500,000 Retained earnings, 1/1/07, as reported 1,000,000

Joe Novak should report retained earnings, 12/31/07, at a. $785,000. b. $1,125,000. c. $1,340,000. d. $1,555,000.

74. The following information was extracted from the accounts of Boone Corporation at

December 31, 2007: CR(DR) Total reported income since incorporation $1,700,000 Total cash dividends paid (800,000) Unrealized holding loss (120,000) Total stock dividends distributed (200,000) Prior period adjustment, recorded January 1, 2007 75,000

What should be the balance of retained earnings at December 31, 2007? a. $655,000. b. $700,000. c. $580,000. d. $775,000.

75. Penn Company reported the following information for 2007:

Sales revenue $510,000 Cost of goods sold 350,000 Operating expenses 55,000 Unrealized holding gain on available-for-sale securities 40,000 Cash dividends received on the securities 2,000

For 2007, Penn would report other comprehensive income of a. $137,000. b. $135,000. c. $42,000. d. $40,000.

76. Silas Company reported the following information for 2007:

Sales revenue $500,000 Cost of goods sold 350,000 Operating expenses 55,000 Unrealized holding gain on available-for-sale securities 20,000 Cash dividends received on the securities 2,000

For 2007, Silas would report comprehensive income of a. $117,000. b. $115,000. c. $97,000. d. $20,000.

Income Statement and Related Information

4 - 17

Multiple Choice Answers—Computational Item Ans. Item Ans. Item Ans. Item Ans. Item Ans. Item Ans.

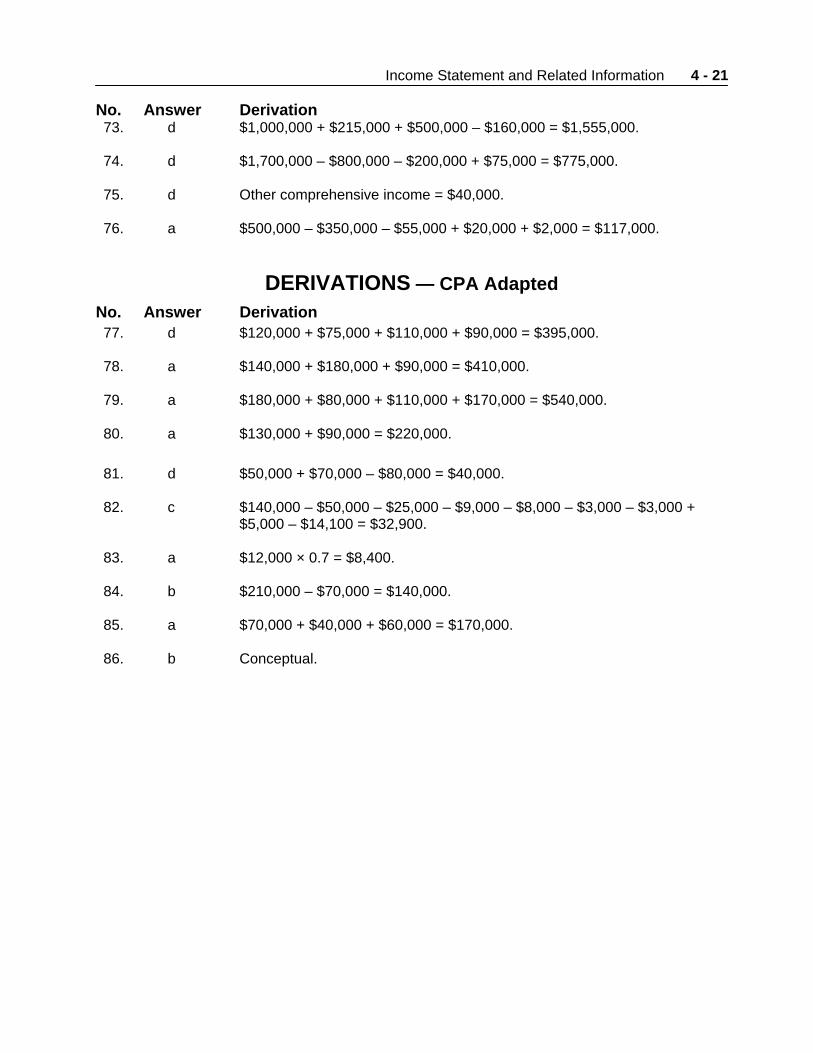

53. a 57. a 61. c 65. c 69. c 73. d 54. c 58. a 62. b 66. c 70. a 74. d 55. c 59. a 63. a 67. c 71. b 75. d 56. c 60. a 64. b 68. c 72. c 76. a

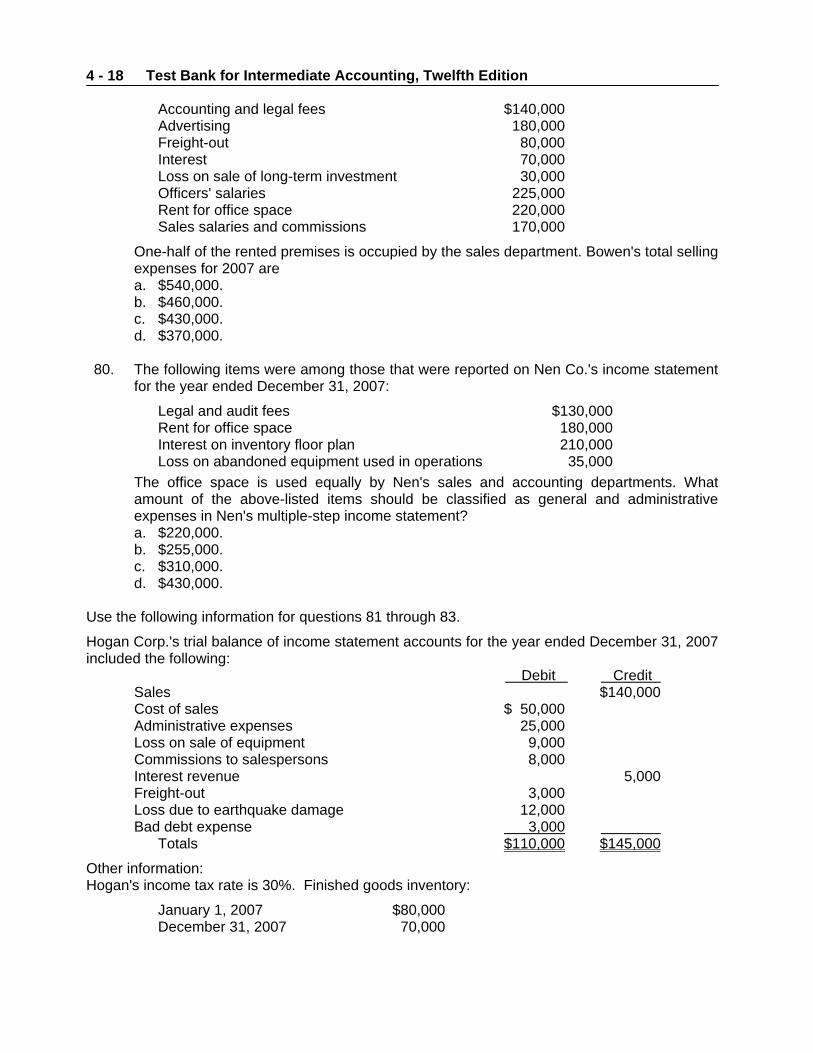

MULTIPLE CHOICE—CPA Adapted Use the following information for questions 77 and 78. Meyer Corp. reports operating expenses in two categories: (1) selling and (2) general and administrative. The adjusted trial balance at December 31, 2007, included the following expense accounts:

Accounting and legal fees $140,000 Advertising 120,000 Freight-out 75,000 Interest 60,000 Loss on sale of long-term investments 30,000 Officers' salaries 180,000 Rent for office space 180,000 Sales salaries and commissions 110,000

One-half of the rented premises is occupied by the sales department. 77. How much of the expenses listed above should be included in Meyer's selling expenses

for 2007? a. $230,000. b. $305,000. c. $320,000. d. $395,000.

78. How much of the expenses listed above should be included in Meyer's general and

administrative expenses for 2007? a. $410,000. b. $440,000. c. $470,000. d. $500,000.

79. Bowen Corp. reports operating expenses in two categories: (1) selling and (2) general and