Insurance Lead Management

87

MEMOIRE DE RECHERCHE 2012/2013 NOM et PRENOM de l’auteur : Dhankhar, Avikar Singh SUJET DU MEMOIRE How online leads in insurance could be converted to customers by combining online distribution channels and physical sales force through lead management? Presentation and analysis of AXA Group‘s recommendations - NOM DU DIRECTEUR DE RECHERCHE: Prof. Dr. Thierry Boudès CONFIDENTIEL Non La diffusion de ce recueil est strictement réservée à ESCP Europe.

-

Upload

avikar-singh-dhankhar -

Category

Marketing

-

view

241 -

download

0

Transcript of Insurance Lead Management

MEMOIRE DE RECHERCHE

2012/2013

NOM et PRENOM de l’auteur : Dhankhar, Avikar Singh

SUJET DU

MEMOIRE

How online leads in insurance could be converted to customers by combining online

distribution channels and physical sales force through lead management?

Presentation and analysis of AXA Group‘s recommendations

- NOM DU DIRECTEUR DE RECHERCHE: Prof. Dr. Thierry Boudès

CONFIDENTIEL Non

La diffusion de ce recueil est

strictement réservée à

ESCP Europe.

ESCP Europe

Strategy, Organizational Behavior, and Human Resources Department

European Research Project

How online leads in insurance could be converted to customers by combining online

distribution channels and physical sales force through lead management?

Presentation and analysis of AXA Group‘s recommendations

Director of Research: Prof. Dr. Thierry Boudès

Student: Avikar Singh Dhankhar

Master in Management Grande Ecole student

Student number: e113038

11 May 2013

Key Words

Digital – Multi-access – Internet – Lead– Lead management – Lead generation – Lead

prioritization – Lead allocation – Lead nurturing – Lead conversion

Abstract of the paper

This research paper explains and analyses the recommendations given by AXA Group

regarding how to do lead management. First lead management is introduced and existing

literature on lead management and its various processes are reviewed. Then why lead

management is important in today‘s digitalized world is explained before explaining AXA

Group‘s recommendations on how to do it. For better explaining the recommendations

practical examples from AXA Group entities and external benchmarks have been provided.

Then AXA Group‘s recommendations are compared with existing literature to find gaps.

Gaps have been found in AXA‘s recommendations and also it has been found that existing

literature is not exhaustive and there is scope of further research on lead management. Also, in

the end, AXA Group‘s recommendations are tested on the lead management model of one of

AXA entities and it has been found that all the recommendations are not applicable to every

entity. Entities need to test and learn to find the right set of recommendations applicable to

their lead management process.

Résumé du mémoire

Ce mémoire de recherche explique et analyse les recommandations du Groupe AXA en ce qui

concerne la façon de faire le Lead management. Tout d‘abord, le Lead management est

présenté et la littérature existante sur le Lead management et sur ses divers processus est

examinée. Deuxièmement, la raison pour laquelle le Lead management est important dans le

monde digital est expliquée avant passer aux recommandations du Groupe AXA sur la façon

de le faire. Afin de mieux expliquer les recommandations, des exemples pratiques tirés des

entités du Groupe AXA et de références externes sont fournis. Ensuite, les recommandations

du Groupe AXA sont comparées avec la littérature existante pour trouver des écarts. Des

écarts sont trouvés dans les recommandations du Groupe AXA et on constate aussi que la

littérature existante n'est pas exhaustive et qu‘il est possible de poursuivre les recherches sur

le Lead management. Finalement, les recommandations du Groupe AXA sont testées sur le

modèle du Lead management de l'une de ses entités et il en résulte que toutes les

recommandations ne sont pas applicables à chaque entité. Les entités ont besoin de tester et

apprendre à trouver les recommandations applicables à leur processus de Lead management.

Contents

1. Lead Management – Introduction .......................................................................................... 1

1.1. Definition of lead ................................................................................................................ 1

1.2. Scope of thesis ..................................................................................................................... 1

1.3. Type of leads - Hot/Cold leads ............................................................................................ 1

1.4. Definition of lead management process .............................................................................. 1

1.5. Lead management objectives .............................................................................................. 2

2. Review of related literature ................................................................................................... 2

2.1. General literature relating to lead management overall ...................................................... 2

2.1.1. Summary of general literature relating to lead management overall ......................... 4

2.2. Literature review related to lead generation ........................................................................ 4

2.2.1. Summary of literature relating to lead generation ..................................................... 7

2.3. Literature review related to lead prioritization and allocation ............................................ 7

2.3.1. Summary of literature relating to lead prioritization and allocation ........................ 10

2.4. Literature review related to lead nurturing/conversion ..................................................... 10

2.4.1. Summary of literature relating to lead nurturing/conversion .................................. 12

2.5. Summary and insights from the literature review ............................................................. 13

2.6. Literature review and research question of the paper ....................................................... 13

2.7. Methodology and data collection ...................................................................................... 14

3. Insurance and lead management .......................................................................................... 15

3.1. Types of insurance and lead management ........................................................................ 15

3.1.1. Life and savings (L&S) ........................................................................................... 15

3.1.2. Property and causality (P&C) – focus of lead management .................................... 15

3.2. Distribution channels under scope of lead management at AXA ..................................... 15

4. Effect of digital and multi-access on insurance business .................................................... 17

4.1. Effect on customer behavior and expectations .................................................................. 17

4.1.1. Information gathering .............................................................................................. 18

4.1.2. Buying online ........................................................................................................... 19

4.1.3. Freedom of interaction ............................................................................................. 19

4.1.4. Customers‘ willingness to use mobile devices to decrease insurance premiums .... 20

4.2. Effect on Insurance Business Operations .......................................................................... 21

4.2.1. Transformation of value chain ................................................................................. 21

4.2.2. Changes in competitive dynamics ........................................................................... 22

5. AXA‘s digital and multi-access transformation levers and lead management .................... 23

5.1. Objectives 23

5.2. Transformation levers ....................................................................................................... 24

6. How to do lead management: AXA Group recommendations ............................................ 25

6.1. Lead generation ................................................................................................................. 25

6.1.1. Define scope ............................................................................................................ 25

6.1.2. Sources 25

6.1.3. Managing marketing campaigns – Preparation ....................................................... 26

6.1.4. Managing marketing campaigns - Execution .......................................................... 27

6.1.5. Measure and improve marketing campaign performance........................................ 28

6.1.6. Best practice for lead generation from existing customers: an example of ING ..... 28

6.2. Prioritize and allocate leads .............................................................................................. 30

6.2.1. Prioritize leads ......................................................................................................... 30

6.2.2. Allocate leads ........................................................................................................... 31

6.3. Nurture and convert leads ................................................................................................. 34

6.3.1. Conversion and nurturing of web-based leads ......................................................... 35

6.3.2. Increasing lead conversion through KPIs ................................................................ 38

6.3.3. Increasing lead conversion through engaging agents .............................................. 42

6.3.4. Increasing conversion through good governance of lead management process ...... 44

7. Lead Management Gap Analysis: AXA Group‘s Recommendations and Existing

Literature/Sources ................................................................................................................ 46

7.1. Gaps in lead generation ..................................................................................................... 46

7.1.1. Scope of improvements in AXA Group‘s recommendations .................................. 47

7.1.2. Scope of future research in lead generation ............................................................. 47

7.2. Prioritize and allocate leads .............................................................................................. 47

7.2.1. Gaps in lead prioritization ....................................................................................... 47

7.2.2. Gaps in lead allocation ............................................................................................. 49

7.2.3. Nurture and convert ................................................................................................. 50

8. Value proposition of lead management and practical implications of recommendations ... 52

8.1. Basic financial approaches of sending leads to sales ........................................................ 53

8.1.1. Billing leads ............................................................................................................. 54

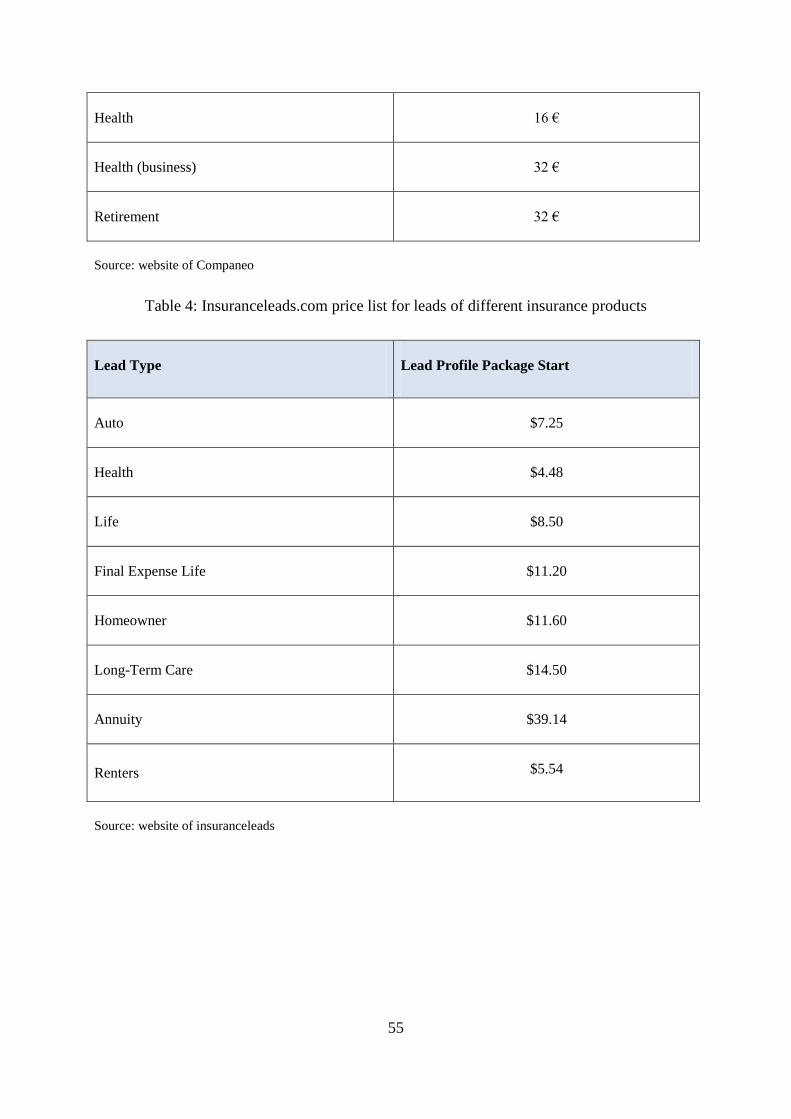

8.1.2. Price charged by lead generating and distributing companies ................................. 54

8.2. Business case of lead management ................................................................................... 56

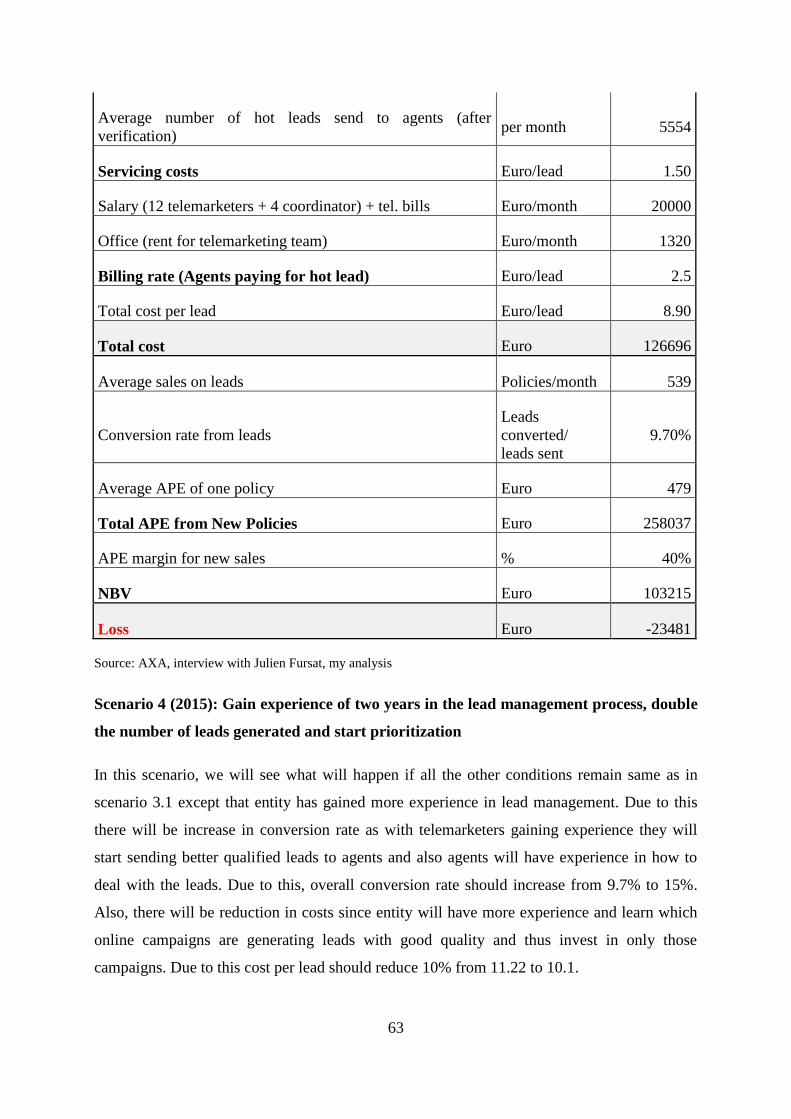

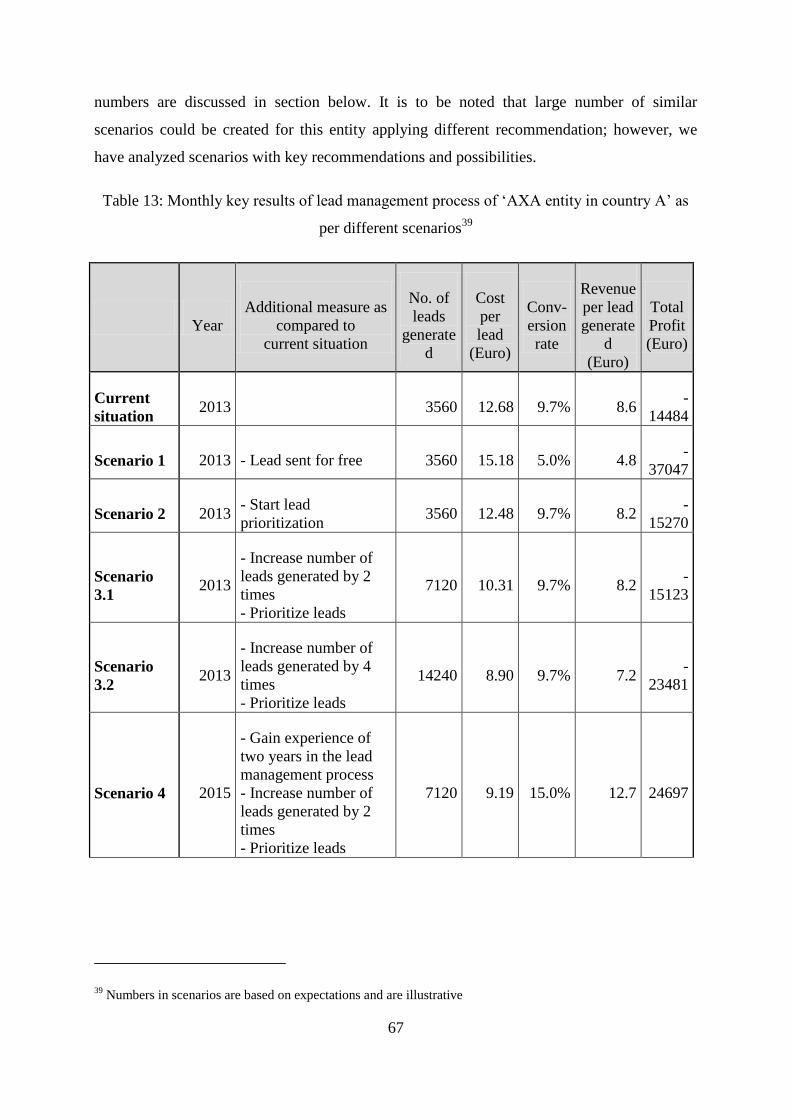

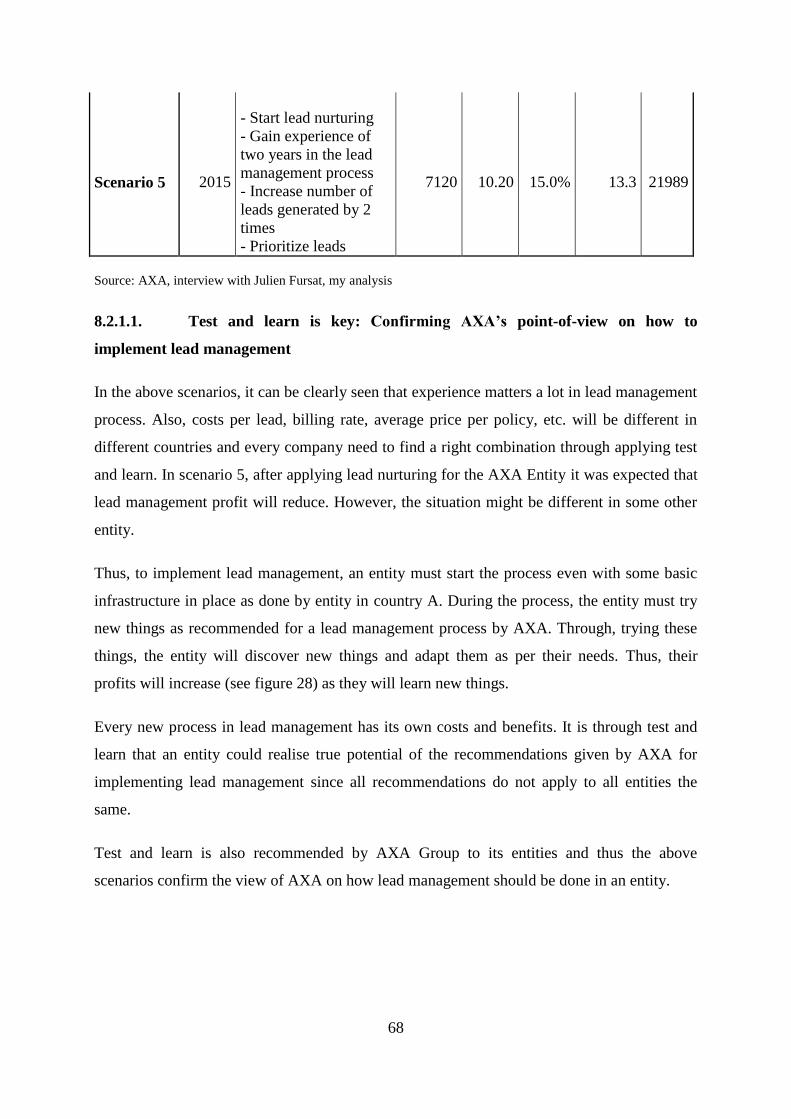

8.2.1. Key learning from the 5 different scenarios ............................................................ 66

8.3. Lead management‘s profit calculation: Upsell/cross-sell/retain ....................................... 70

9. Conclusion ........................................................................................................................... 71

9.1. Recommendations for future research .............................................................................. 72

Appendices…………………………………………………………………………............... 73

Bibliography…………………………………………………………………………………. 76

Declaration of

honor/Affidavit………………………………………………………………………..............79

List of tables

Table 1: Different distribution networks at AXA .................................................................... 16

Table 2: People considering buying auto insurance online, US ............................................... 19

Table 3: Companeo's price list ................................................................................................. 54

Table 4: Insuranceleads.com price list for leads of different insurance products .................... 55

Table 5: Insuranceleads.com price list of auto insurance leads ............................................... 56

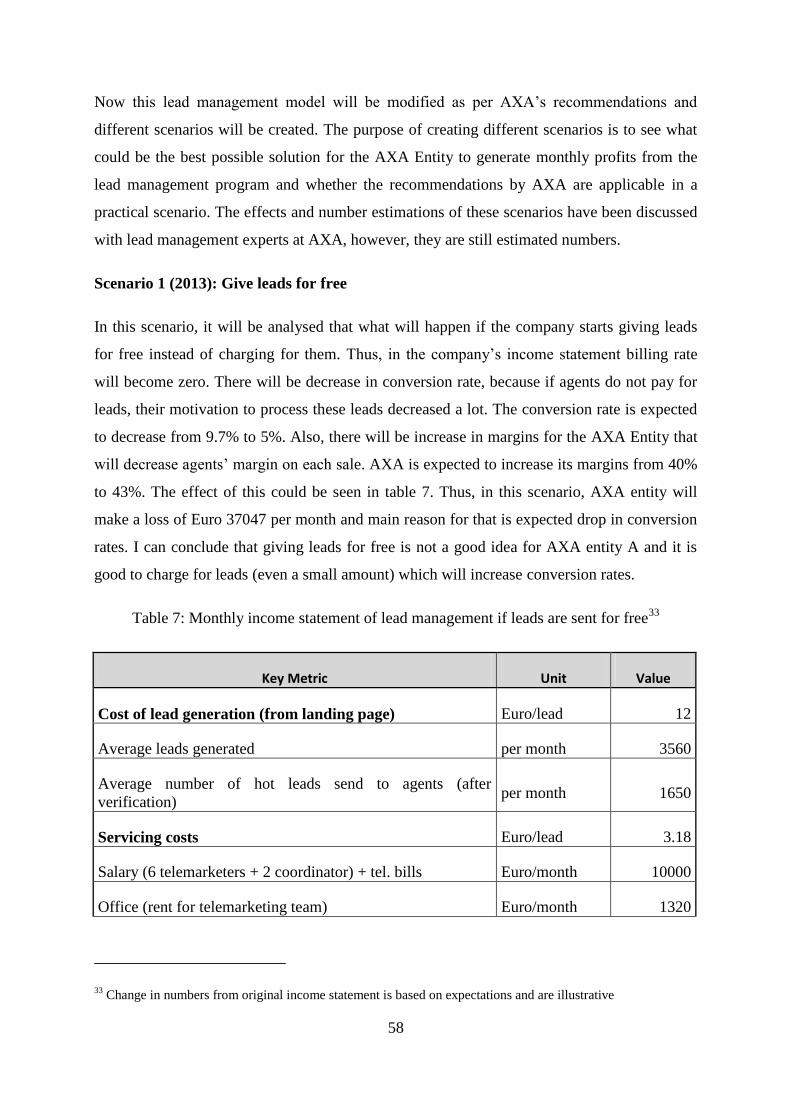

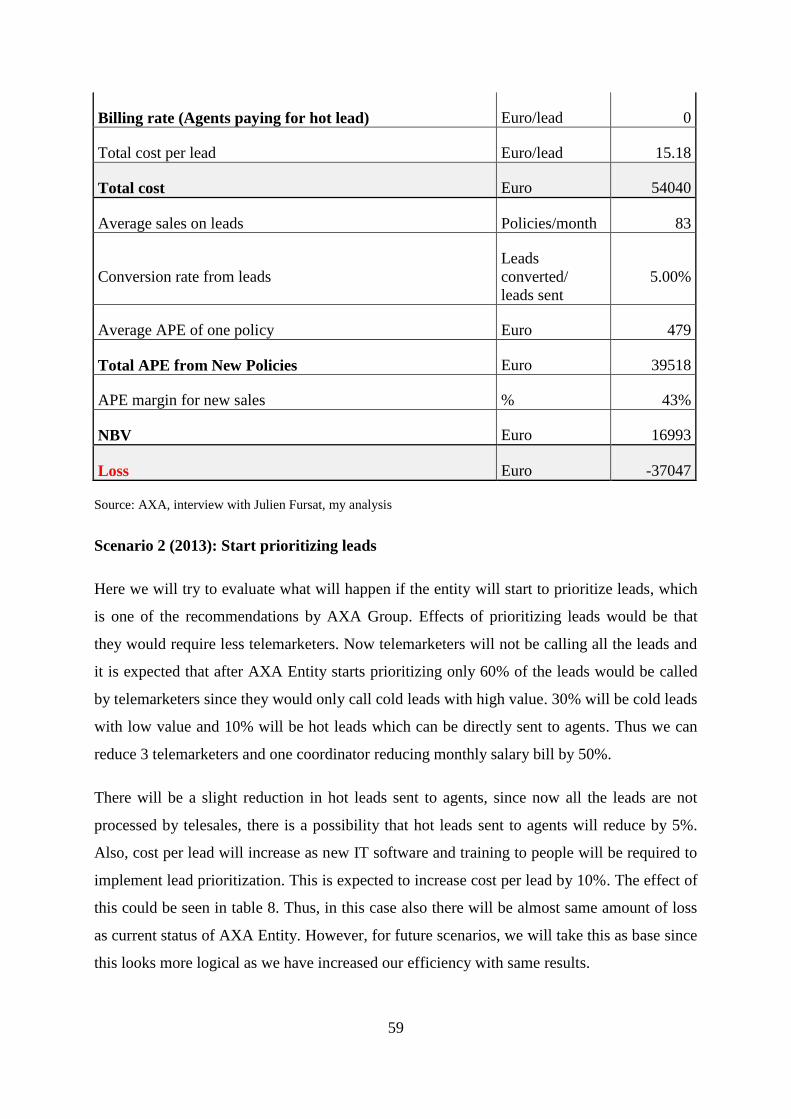

Table 6: Monthly income statement of lead management ....................................................... 57

Table 7: Monthly income statement of lead management if leads are sent for free................. 58

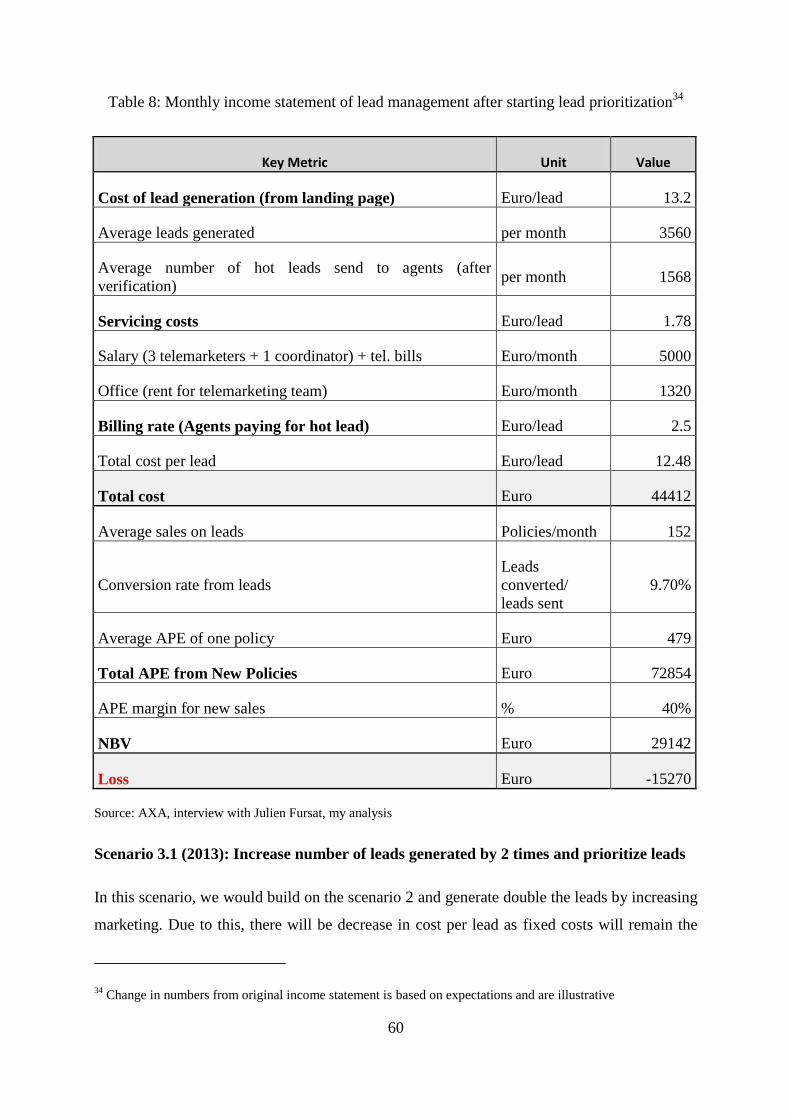

Table 8: Monthly income statement of lead management after starting lead prioritization..... 60

Table 9: Monthly income statement of lead management after lead prioritization and

increasing the number of leads generated by twice .................................................................. 61

Table 10: Monthly income statement of lead management after starting lead prioritization and

increasing the number of leads generated by four times .......................................................... 62

Table 11: Monthly income statement of lead management after gaining 2 years of experience,

starting lead prioritization and increasing the number of leads generated by two times ......... 64

Table 12: Monthly income statement of lead management after starting lead nurturing,

gaining 2 years of experience, starting lead prioritization and increasing the number of leads

generated by two times ............................................................................................................. 65

Table 13: Monthly key results of lead management process of ‗AXA entity in country A‘ as

per different scenarios .............................................................................................................. 67

List of figures

Figure 1: Main steps of lead management ................................................................................. 2

Figure 2: Lead Source Metric Comparison ................................................................................ 6

Figure 3: Initial dials to leads that become contacted by hours ................................................. 9

Figure 4: Initial dials to leads that become qualified by hours .................................................. 9

Figure 5: Leads contacted/qualified by 5 minute interval ........................................................ 10

Figure 6: Importance of social media feedback in selecting insurance provider ..................... 18

Figure 7: % of very likely and somewhat likely people who would switch to other companies

if their company would not provide a multi-access communication channel .......................... 20

Figure 8: Number of people willing to accept using mobile to reduce their insurance premium

.................................................................................................................................................. 20

Figure 9: Market share of traditional and direct insurance players in the US .......................... 23

Figure 10: AXA's transformation levers and lead management .............................................. 24

Figure 11: Google search result of keyword ―assurance auto‖ in France and AXA‘s

positioning ................................................................................................................................ 26

Figure 12: Outbound and inbound marketing campaign management .................................... 29

Figure 13: Private client website of ING ................................................................................. 30

Figure 14: Lead management portal of AXA Equitable fully integrated with CRM ............... 32

Figure 15: Lead file sent by insuranceleads.com to sales ........................................................ 33

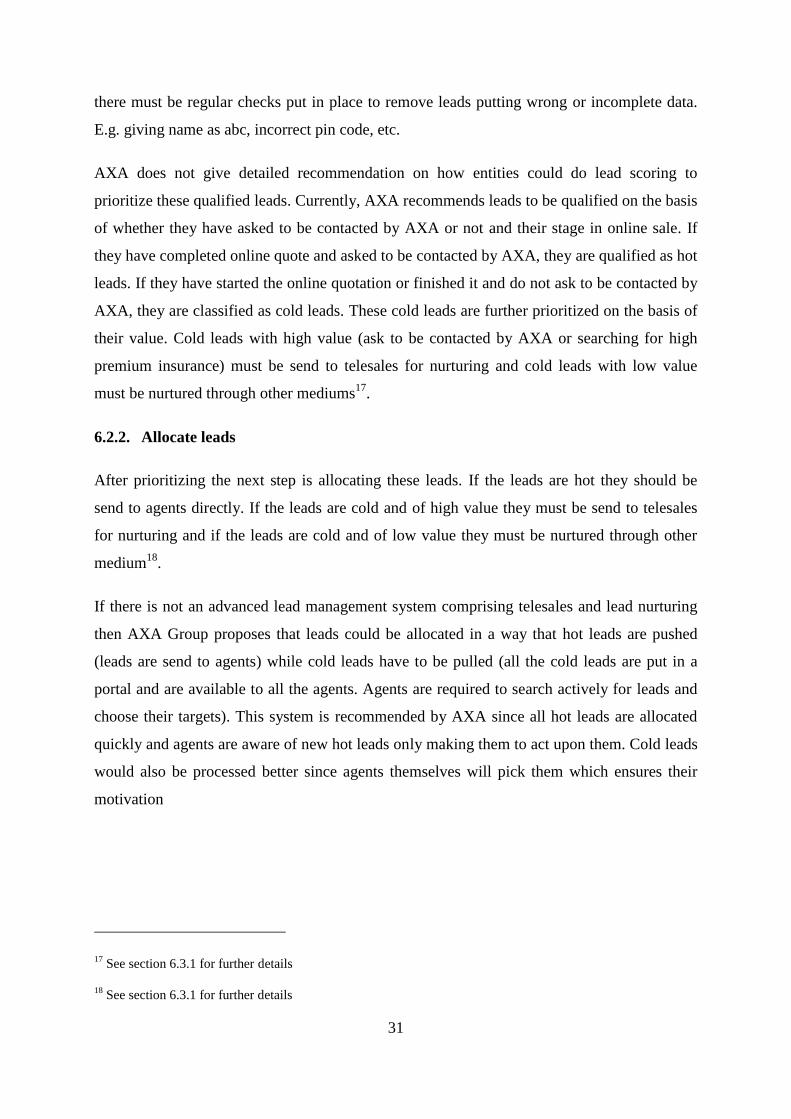

Figure 16: Different categories of web-based leads ................................................................. 36

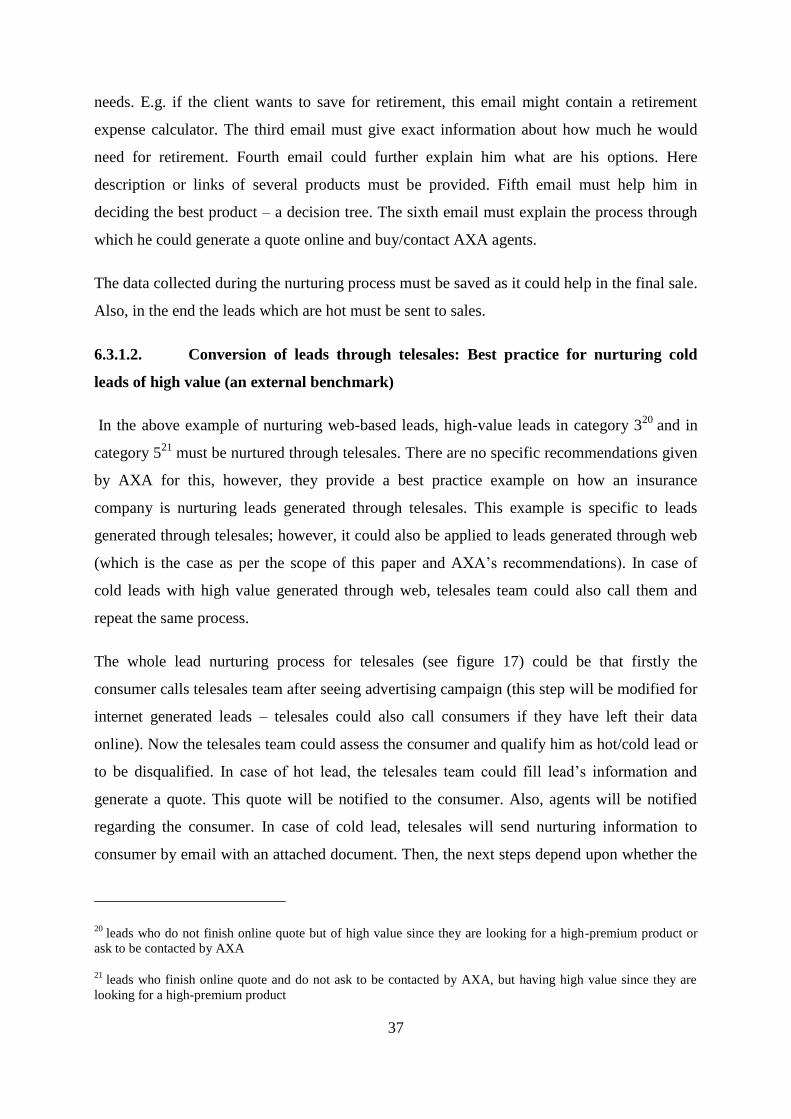

Figure 17: Flowchart of lead nurturing through telesales ........................................................ 38

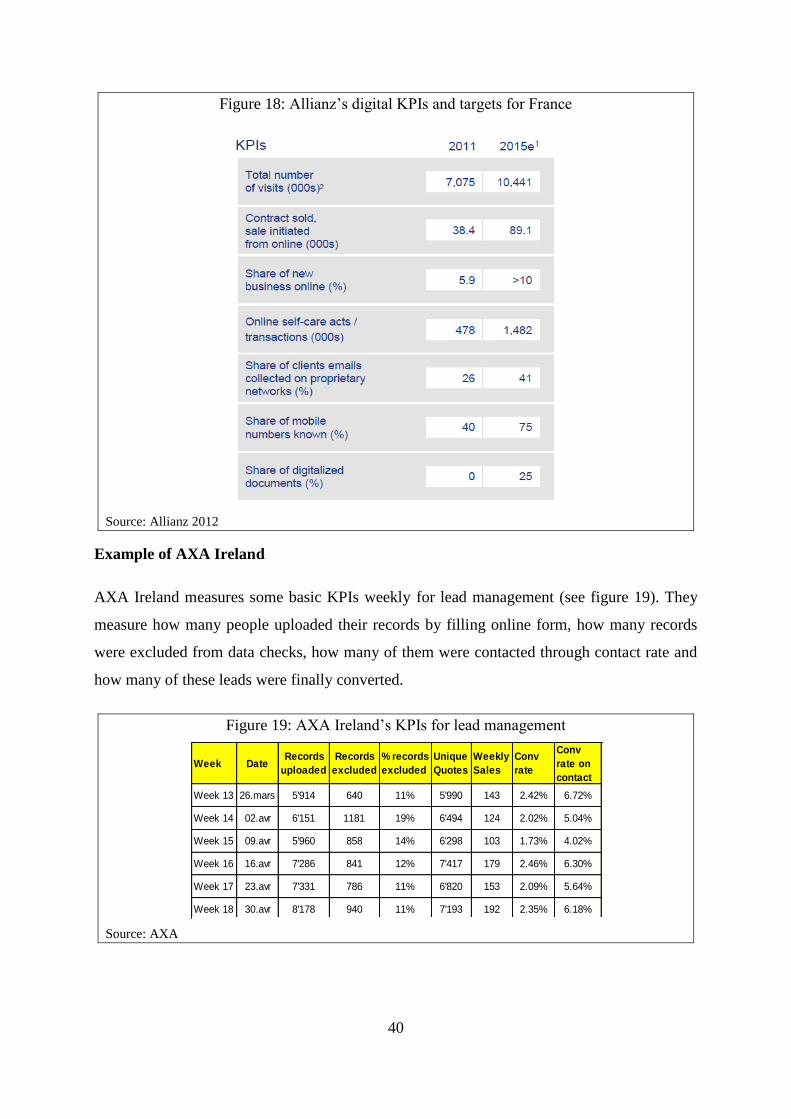

Figure 18: Allianz‘s digital KPIs and targets for France ......................................................... 40

Figure 19: AXA Ireland‘s KPIs for lead management ............................................................. 40

Figure 20: Performance monitoring of a US based insurance company .................................. 41

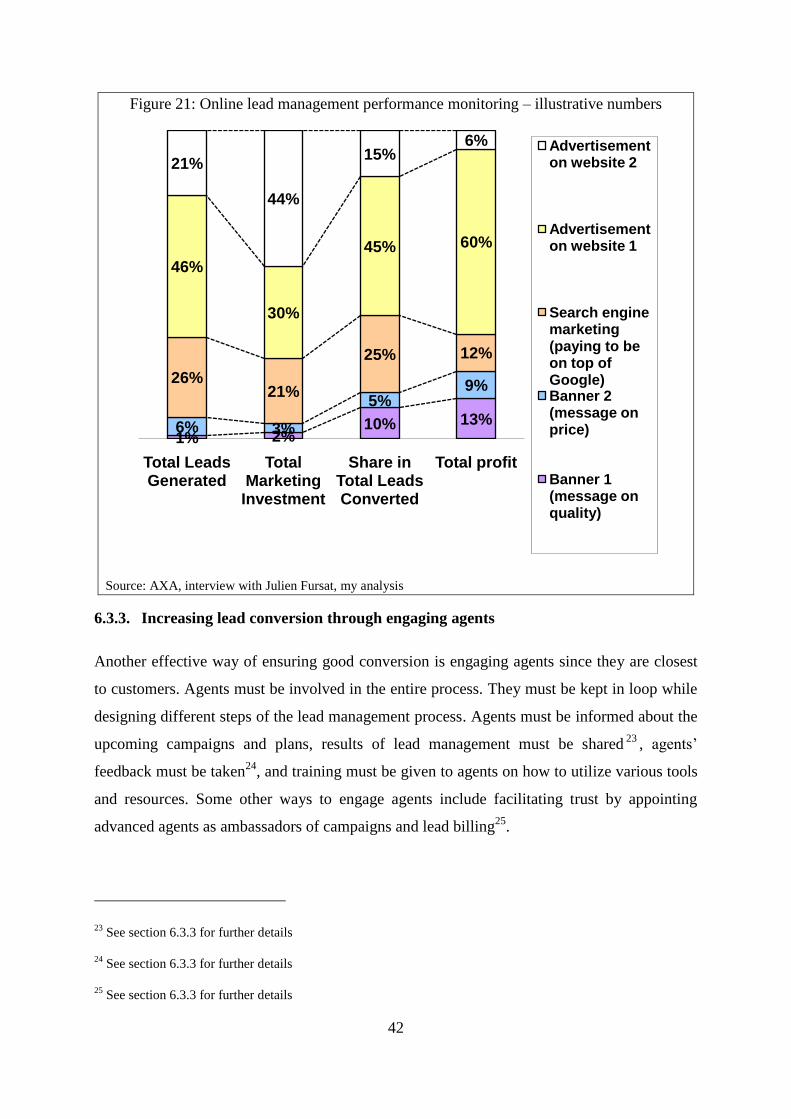

Figure 21: Online lead management performance monitoring – illustrative numbers ............. 42

Figure 22: Conversion rate of health products‘ leads in AXA Germany ................................. 44

Figure 23: Gap analysis of AXA Group‘s Recommendation and existing literature on lead

generation ................................................................................................................................. 46

Figure 24: Gap analysis of AXA Group‘s Recommendation and existing literature on lead

prioritization ............................................................................................................................. 48

Figure 25: Gap analysis of AXA Group‘s Recommendation and existing literature on lead

allocation .................................................................................................................................. 50

Figure 26: Gap analysis of AXA Group‘s Recommendation and existing literature on lead

nurturing ................................................................................................................................... 51

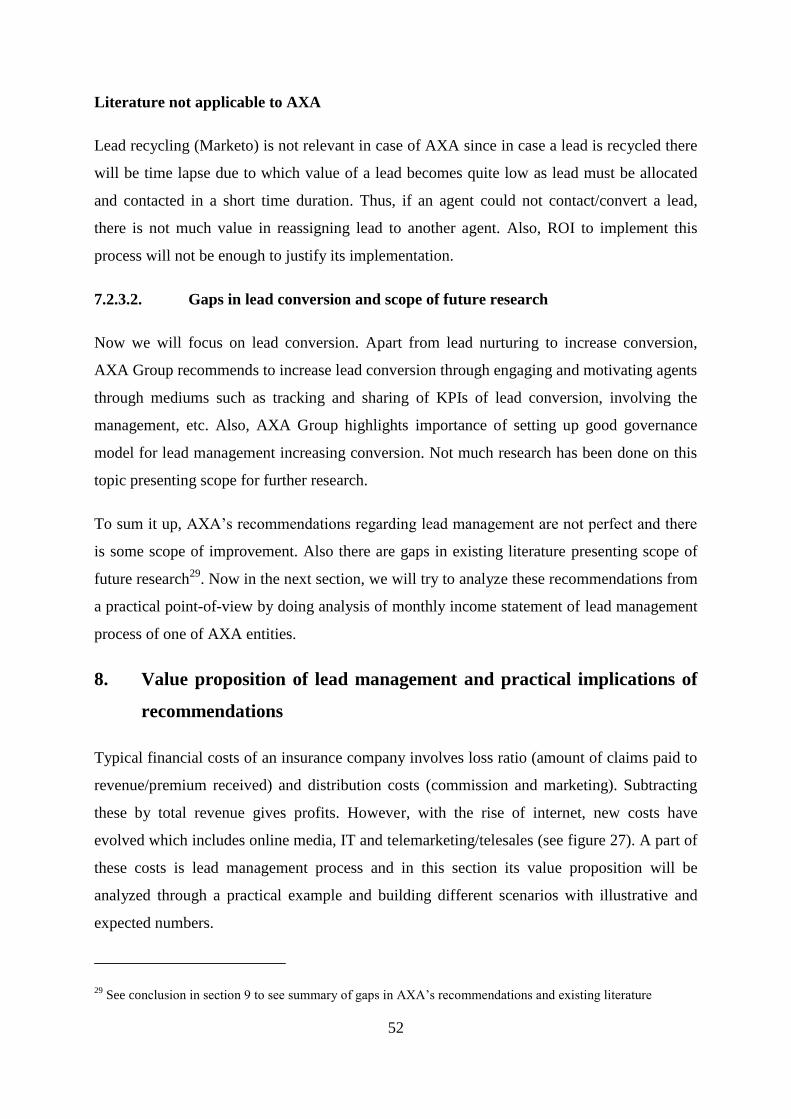

Figure 27: Key costs associated with revenue of 100 Euro in Insurance ................................. 53

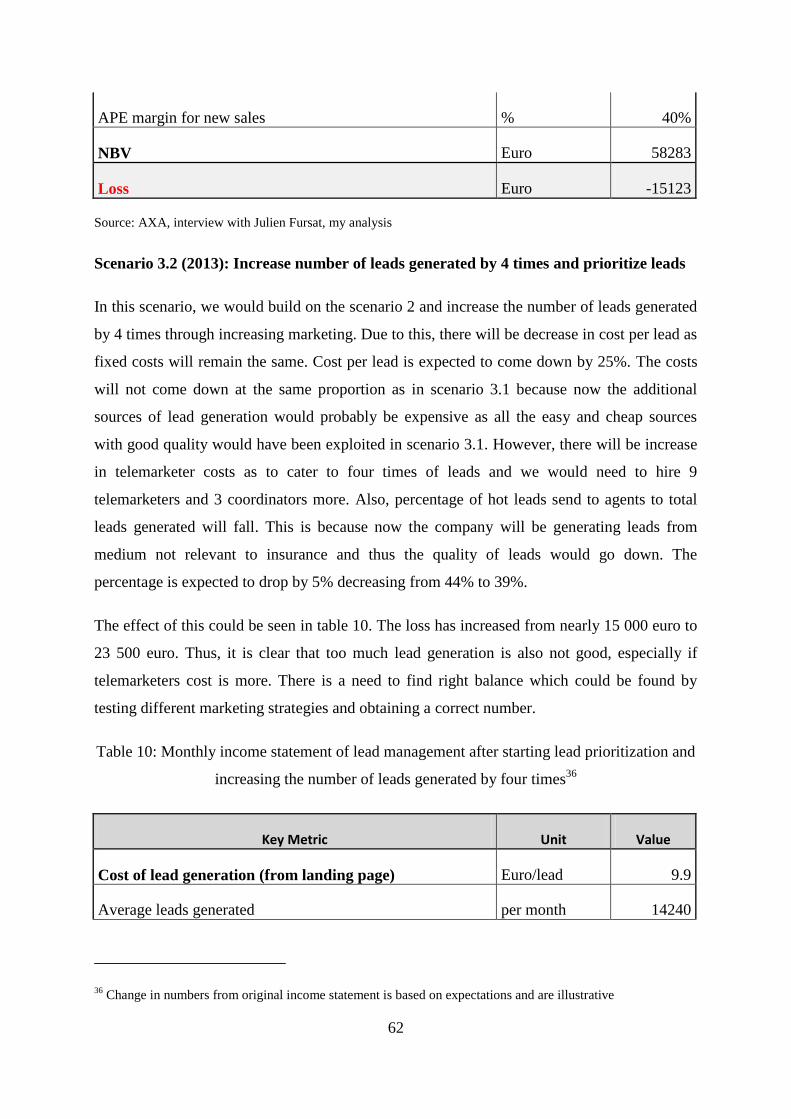

Figure 28: Per year profit from a typical lead management process ........................................ 69

Figure 29: Importance of optimum number of lead generation in lead management .............. 70

1

1. Lead Management – Introduction

1.1. Definition of lead

As per AXA, a lead is a customer or a prospect who corresponds to AXA‘s target segments,

who contacts AXA (inbound contact) through one channel (phone, website, mail, point-of-

sale, e-mail, etc.) or who is qualified to be contacted through a direct marketing campaign

(outbound contact).

In simple terms, lead could be defined as a person who would be potentially interested in an

AXA product and for whom, AXA have at least one contact detail.

1.2. Scope of thesis

This thesis will focus mainly on online leads generated from the company‘s website or other

online sources.

1.3. Type of leads - Hot/Cold leads

As per AXA, leads could be classified as hot or cold leads. Hot leads are people who

complete the online quotation and ask to be contacted by AXA. Cold leads are people who

start or complete the online quotation but do not ask to be contacted by AXA.

1.4. Definition of lead management process

It is a process through which insurance companies improve conversion of leads generated

through web/telephone. This is important, since, still the conversion on pure online selling is

low and lead management represents a strong value-creation lever in AXA‘s Digital and

Multi-access model1.

As per AXA, overall lead management is a very transversal process involving three main

steps (see figure 1): generation of leads, ‗prioritization and allocation‘ of leads, and ‗nurturing

and conversion‘ of leads.

1 See section 5 for further details

2

Figure 1: Main steps of lead management

Source: AXA

1.5. Lead management objectives

The main objective of lead management is acquisition of new customers. Through lead

management a company could acquire new customers since the process will help it in

generating qualified leads and sending them to agents for conversion. Also, through sending

only qualified leads to agents, it enables agents to concentrate their efforts on leads which are

most likely to get converted.

Other objectives of lead management are to increase sales to existing customers (through

cross/upsell) or increase their retention.

2. Review of related literature

First, the general literature relating to lead management will be reviewed. Then, the literature

focusing on specific parts of lead management including lead generation, lead prioritization

and allocation, and lead nurturing/conversion will be discussed. Also, it is to be noted that the

literature review of lead management has not been limited to insurance sector, since in

insurance this is a relatively new term and not much research has been done.

2.1. General literature relating to lead management overall

Gebert H., Geib M., Kolbe L., and Brenner W. (2003) described lead management as one of

the six main customer relationship management processes. The other five processes

mentioned include campaign management, offer management, contract management,

complaint management and service management. Further they defined lead management as a

―consolidation, qualification, and prioritization of contacts with prospective customers”. In

their combined model of knowledge management and customer relationship management

called customer knowledge management, they placed lead management as a process to be

governed by both marketing and sales.

3

Dous M., Salomann H., Kolbe L., and Brenner W., (2005) surveyed 1000 CRM executives to

gather data on various CRM processes used by them. In the survey, they categorized the

processes under four themes: Service processes, Support processes, Analysis processes, and

Management processes. Customer scoring and lead management was placed under Analysis

processes. In terms of degree of implementation customer scoring and lead management

process received 12.9% (fully implemented), 20% (mostly implemented), 25.9% (partly

implemented), 22.4% (hardly implemented) and 18.8% (not implemented).

Rechtin M. (2012) described his interview with George Borst CEO, Toyota Financial Services.

During the interview, George Borst described Enterprise Lead Management program

launched by Toyota Financial recently. In the program, Toyota Financial calls customers six

months before the lease of their car is due to expire. After gathering information about the

customer‘s future needs, this information is provided to dealers through an automatic CRM

tool. George Borst said that 94% of the leads are contacted by dealers within three hours and

then they try to close the deal.

Cordo J. (2012) explained how lead management is the main area of misalignment between

sales and marketing. The major issue he described is how to transform the data marketing

department has on customer intelligence in to sales intelligence to increase efficiency of both

marketing and sales. He further described 5 ways to transform data.

Croft S. (2002) identified various important steps to manage leads. However, the context is a

B2B lead generation process, thus all the concepts are not relevant to this thesis. Some of the

things that might apply to B2C lead management include identifying your buyers, conducting

research and building relationship with buyers.

Blake T. (1999) explains how house renting agencies can gather and store data on their

customers or potential customers easily using a computer. Also, he explained various lead

management software companies could buy. This computerized tracking could also help

companies in increasing their marketing ROI, he explained.

4

Marketo2 has described what companies need to do to sell products to leads that are not sales

ready (as per a survey done by RainToday, of the total leads generated 25% are disqualified,

25% are sales ready and the rest of 50% needs to be handled appropriately to convert them).

Some of the steps explained include lead nurturing, lead scoring to identify strong leads,

giving all necessary information about leads to sales, tracking marketing campaigns, tracking

anonymous visitors to the website, and continuously learning about needs of customers.

SmartLead3 explained benefits of a lead management system and how companies should do it.

As per them, lead management is a six step process the first step is to capture the inquiries

received. Then, it is important to qualify these leads and rank them. After this, the leads must

be nurtured and distributed. The final important step is to track the journey of a lead

throughout the process to measure effectiveness of various steps.

2.1.1. Summary of general literature relating to lead management overall

Most of the early studies put lead management as a part of customer relationship management.

There has not been any significant study on insurance; however there have been studies on

house renting and automobile sectors.

The main sources are practitioners such as Marketo and SmartLead. Marketo has published an

extensive range of white papers which describe essentials of lead management. These include

qualifying leads, lead scoring and lead nurturing, giving detailed information to sales and

following-up with them, tracking all marketing programs and segregating them to see which

are more effective, and tracking anonymous visitors on the website.

2.2. Literature review related to lead generation

Aquino J. (2012) quoted the survey on 1200 US SMBs conducted by a research company

Techaisle to highlight importance of marketing automation. Some of the marketing

automation components used by SMBs include email marketing, message personalization and

campaign management. Lead capture was included in the components SMBs plan to explore.

Also, nearly half of the survey respondents highlighted importance of marketing automation

2 Marketing software providing firm

3 Lead management company

5

to enhanced management of sales leads: 46% observing better demand generation and 42%

better marketing ROI through marketing automation.

Shea P. (2012) described lead management as ―acquisition and maintenance of prospective

leads”. He conducted various interviews to investigate lead management in property market.

He interviewed Israel Carunungan, director of property marketing at Greystar. Carunungan

highlighted the advancement of their lead tracking platform, through which, they are able to

allocate 100% of leads to their sources. This helps Greystar to optimize their marketing ROI.

Also Carunungan described how through this lead tracking platform, they are able to identify

the trend of more leads being generated through online sources. Eric Broughton, president and

COO of RentSentinel, described importance of keeping various marketing channels and also

gave importance of each channel with online as primary channel. Kim Atkinson, director of

marketing and public relations at Mark-Taylor Residential, indicated the importance of their

company website in generating leads with nearly 50% of their walk-ins, emails and phone

calls generated through their website. Also, Atkinson described how rise of social media is

affecting online lead generation with Facebook bringing more prospects to their website than

search engines such as Bing and Yahoo.

Hosford C. (2012) described how we might be entering a great time for lead generation with

the ability to create personalized emails, rise of social media and new data analytical abilities.

Also, he highlighted how various sales channels coupled together will be more effective. He

quoted Yuchun Lee, VP-general manager of IBM's Enterprise Marketing Management Group

saying that augmenting the sales channel through lead generation by digital channel might be

―the most fruitful next step in lead generation”.

Marketo4 explained in detail how to bring more people to companies‘ website and then how to

convert those leads. For lead generation, they explained the importance of being in first few

Google search pages. In terms of how to allocate leads they explained about allocating leads‘

pipeline revenue to marketing programs as per first touch (allocation to the marketing

program that originally generated lead e.g. only Google) and multi touch (allocation to the

marketing programs involved in the entire process of lead conversion e.g. Google+website).

This helps to optimize advertising revenue.

4 Marketing software providing firm

6

Marketo explained that it is important to use all the channels including social. For social they

have provided extensive list of recommendation explaining how to effectively use social e.g.

what kind of status updated, how to measure your effectiveness, type of cove photo, etc.

SmartLead5 has given some best practices to generate leads by using referral programs with

the current customers or leads, in the current difficult scenario. As per them, for the referral

program to be a success the reward given must be good enough to motivate the customer or

lead to give referrals. This reward must not be based on luck and must be of appropriate

amount. Also, if the company has no money to allocate to rewards, a simple process of adding

a link ―refer a friend‖ in the thank you email could also help.

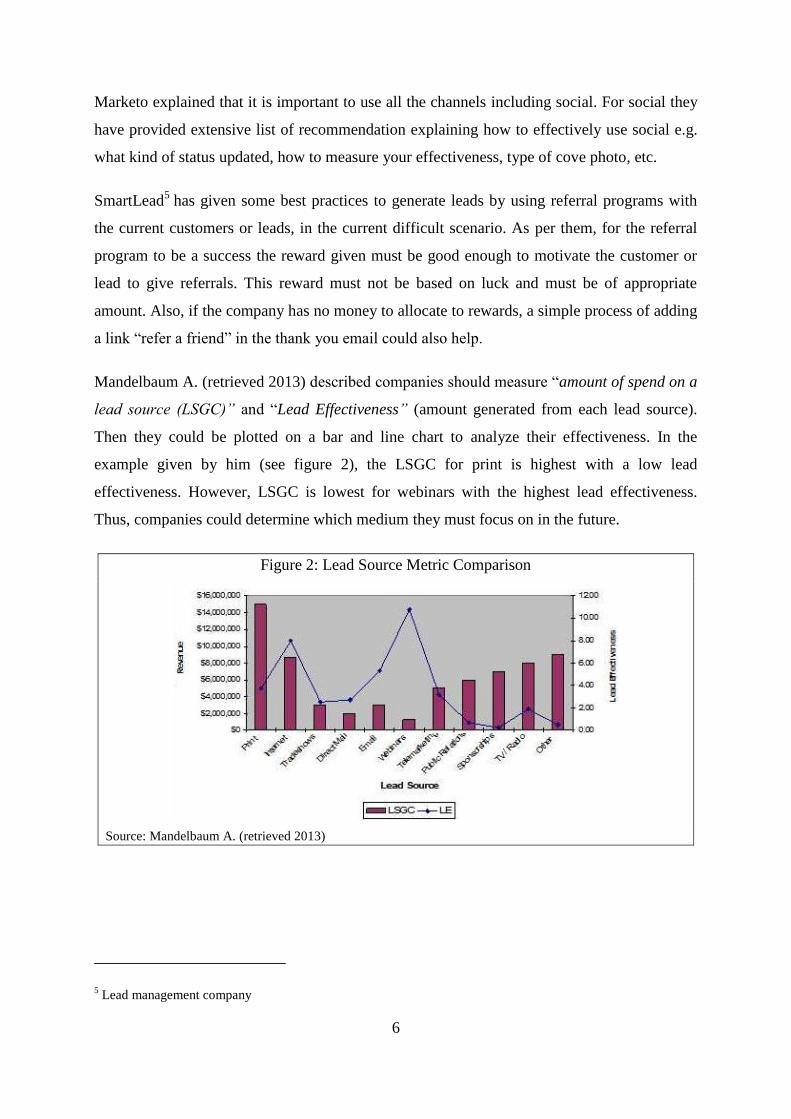

Mandelbaum A. (retrieved 2013) described companies should measure ―amount of spend on a

lead source (LSGC)” and ―Lead Effectiveness” (amount generated from each lead source).

Then they could be plotted on a bar and line chart to analyze their effectiveness. In the

example given by him (see figure 2), the LSGC for print is highest with a low lead

effectiveness. However, LSGC is lowest for webinars with the highest lead effectiveness.

Thus, companies could determine which medium they must focus on in the future.

Figure 2: Lead Source Metric Comparison

Source: Mandelbaum A. (retrieved 2013)

5 Lead management company

7

2.2.1. Summary of literature relating to lead generation

Lead generation has both academics and practitioners as authors. However, academics‘

research is also based on interviews with practitioners in industries such as technology (IBM)

and residential mortgages/renting. Literature highlighted the importance of lead generation

and lead-tracking.

Some of the key findings from the literature on how lead generation should be done are to

include various marketing channels (including social media), allocating resources to different

channels as per their importance or lead generating capacity and tracking leads. Marketing

automation is important to generate high ROI and also it is important to track sources of

different leads and thus measuring effectiveness of leads coming from different marketing

campaigns. Other important suggestions include being in the first few Google search pages

and using referrals from existing customers to generate leads.

2.3. Literature review related to lead prioritization and allocation

Hosford C. (2012) through an interview with Ken Fredman, head-digital programs &

operations, at J.P. Morgan Asset Management described how J.P. Morgan Asset Management

generates leads online and then confirm them through their or third party databases. Only then,

these leads are sent to telesales teams. The result is that these leads have a better conversion

rate.

Croft S. (2002) identified the three most important aspects of lead management as qualifying

leads, developing right sales strategy and knowing when to walk away. She further described

each of the individual aspects in detail. To qualify and rate leads from 1 to 5, she identified 17

factors to be taken in to account such as lead‘s financial status, whether or not our

product/service mix matches with lead‘s needs and lead‘s potential to introduce to new leads.

For developing sales strategy they described to make a good pitch team and keep in mind the

budget. She further gave 6 conditions when to walk away from lead.

Marketo6 has given a complete guide on lead scoring. They explained that lead scoring is

required because on an average 75% of sales leads generated online are not ready to be sent to

6 Marketing software providing firm

8

sales teams. They further explained scoring could be done on basis of fit of lead (someone

you are interested in and someone interested in you) and interest or behavior (e.g. going to the

prices page, opening emails, watching demo videos). Fit could be done through explicit

functions such as demographics, BANT (Budget, Authority, Need, Timing) and

Firmographics (details about their company, more for B2B) and implicit functions such as ISP

and data quality. Also, they explained the necessity of integrating social media scoring. Then

they explained 3 advanced scoring techniques that could be applied: score degradation

(reducing scores over a period of time in-case of inactivity), product scoring (score interest on

specific products) and account scoring (score all leads from a company, more for B2B). After

deciding scores and variables, they signified importance of deciding what is the threshold (e.g.

in case of 100 score it is a hot lead). They explained the matrix methodology to identify

qualified leads, which is an advanced method to only putting threshold on total scores. Then

after identification of good lead, they said it is important to set targets for sales people

receiving those leads (contact within 24 hours and process within 7 days).

Also, one another interesting concept Marketo explains is lead lifecycle. After sending leads

to sales and they are contacted, it is important to further score them. If they are not interested

at all, the reason for that must be noted and the fit/behavioral scores must be reduced, this will

help in lead nurturing process also. Further, if lead says that they will not buy now but after 3

months, it must be recorded and that lead must be put back in the system after 3 months. They

further explained how to show these leads to sales agents, and for that they took their example

and mentioned how they do it through number of stars and flames with stars showing quality

of lead and number of flames showing urgency of lead. Also, sales reps must have access to

leads‘ behavioral history. As per them, to do lead scoring practically the first step in to start

small and learn. Then, it is important to continuously review the scoring data.

Marketo7 has identified importance of effectively handing over leads to sales channels. They

highlight the importance of sending leads with information to sales thus increasing their

chances of converting them. Also, they advise to take regular feedback from sales to improve

the overall process.

7 Marketing software providing firm

9

SmartLead8 gave advantages of distributing only hot leads to sales force. The advantages

include sending all leads have a negative impact on the value given by sales reps to all the

leads, it is costly to process all leads, and the time taken to reach hot leads increases which

increases the chances of them going to the competition.

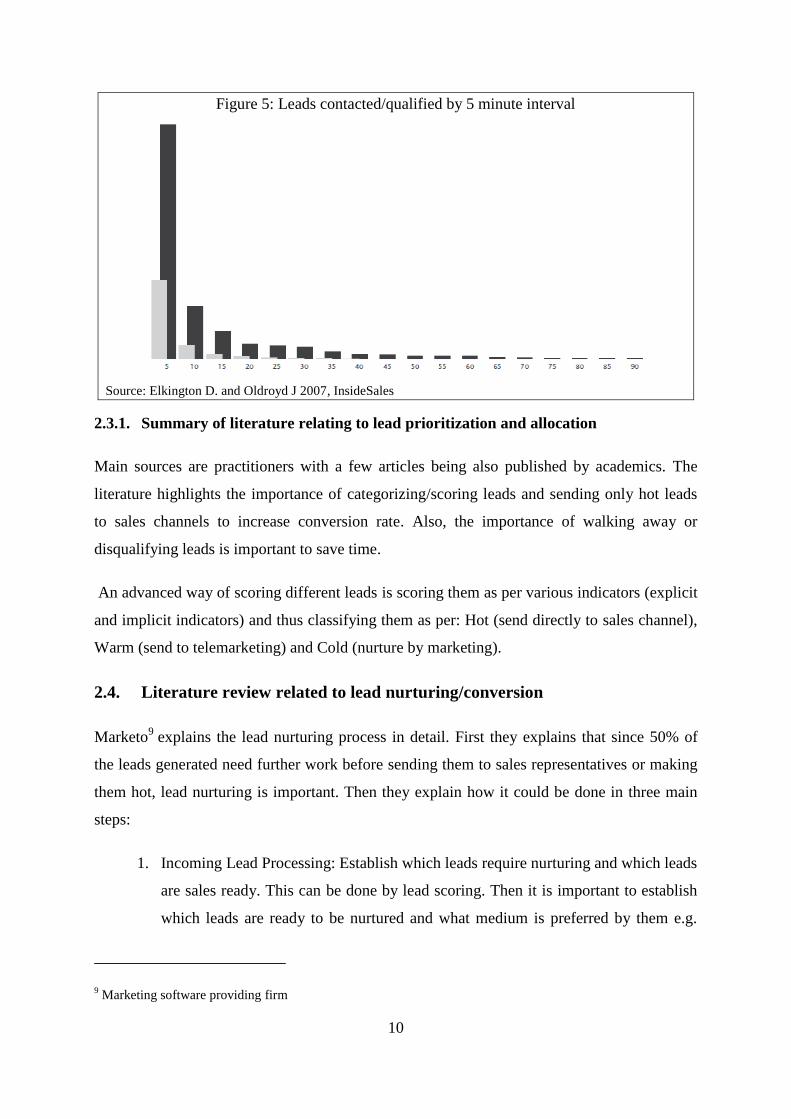

Elkington D. and Oldroyd J. (2007) conducted research to determine the best day and time to

contact leads. Their research showed that the chances of contacting and qualifying a lead drop

significantly with time. After one hour, chances of contacting a lead ―drop over ten times‖

(see figure 3) and chances of qualifying (being able to collect relevant data) reduces by six

times (see figure 4). Also, “The odds of contacting a lead if called within five minutes versus

30 minutes are 100 times greater” and the odds of qualifying are 21 times greater (see figure

5)

Figure 3: Initial dials to leads that become contacted by hours

Source: Elkington D. and Oldroyd J 2007, InsideSales

Figure 4: Initial dials to leads that become qualified by hours

Source: Elkington D. and Oldroyd J 2007, InsideSales

8 Lead management company

10

Figure 5: Leads contacted/qualified by 5 minute interval

Source: Elkington D. and Oldroyd J 2007, InsideSales

2.3.1. Summary of literature relating to lead prioritization and allocation

Main sources are practitioners with a few articles being also published by academics. The

literature highlights the importance of categorizing/scoring leads and sending only hot leads

to sales channels to increase conversion rate. Also, the importance of walking away or

disqualifying leads is important to save time.

An advanced way of scoring different leads is scoring them as per various indicators (explicit

and implicit indicators) and thus classifying them as per: Hot (send directly to sales channel),

Warm (send to telemarketing) and Cold (nurture by marketing).

2.4. Literature review related to lead nurturing/conversion

Marketo9 explains the lead nurturing process in detail. First they explains that since 50% of

the leads generated need further work before sending them to sales representatives or making

them hot, lead nurturing is important. Then they explain how it could be done in three main

steps:

1. Incoming Lead Processing: Establish which leads require nurturing and which leads

are sales ready. This can be done by lead scoring. Then it is important to establish

which leads are ready to be nurtured and what medium is preferred by them e.g.

9 Marketing software providing firm

11

call, email. Also, it is important to make an option available to prospects to opt-out

when they want.

2. Stay in touch: Key is to keep yourself in the leads‘ mind and make them to contact

you when they want to buy. For this, leads must be categorized in three categories

early stage (just learning), middle stage (evaluating possible solutions) and last

stage (making buying decision). Different content must be send to these leads to

maintain their interest in the company. Also, if possible, leads could be categorized

as per industry, their role, geography; and material must be send accordingly. The

frequency to send this content needs to be customized and this could be asked from

the lead, how many tomes per month they want the content.

3. Lead recycling: It is the process of tracking and reassigning leads that are not or

could not be contacted by sales representatives. Sometimes the leads are not

contacted and sometimes they are contacted by sales recycle the leads back since

they are not ready now. The marketing department should keep these leads and

must send them back to sales whenever the timeframe mentioned by sales is over.

However, at the same time, marketing department of Marketo maintains a

scoresheet and if their score goes above threshold, leads are anyways sent back to

sales. But key is, to make sure sales representative are sure that the lead will come

back when they recycle a lead to marketing.

Marketo, in collaboration with Spear Marketing Group, explained how companies can

increase efficiency and get started in lead nurturing. The paper is more focused on B2B. In the

paper they tackled issues of how to set-up a goal for lead nurturing program, how to analyze

the current lead nurturing process, how much effort to be put in and gives the 80/20 rule of

lead nurturing, how to be innovative in the content you send to nurture (use of blogs), how to

generate better response from the lead nurturing emails (keeping it relevant), how to respond

to email inquiries, how to start (test and start small).

Tangwall D., Cecil J., Soucie W. (2011) explained the advantages of using social media for

lead nurturing. Social media enables prospects to select the company instead of company

selecting them. This is particularly possible since everyone can see and share the social media

content. Social media through its media groups and other filtering options allow companies to

post relevant and customized information to their prospects. Social media has the capacity to

12

influence people. People share content and their passion on social media and seeing them,

many other people start trusting the products and start following. Also, it is easy to interact

through social media and it has the capacity to build long-term relationships.

ActiveConversion10

described how companies should prepare their lead nurturing content.

They explained lead nurturing content must have a “consultative tone” which would help to

increase company‘s reputation. Then, it is important to send content relevant to your customer

– which could be done by segmenting customers. Finally, prospects must also be segmented

on the basis of their stage of buying a company‘s product.

Brownell A. (2010) gave the 4‖P‖s of lead nurturing. The first P is Permission Marketing

according to which companies should take permission from prospects the way they would like

to be communicated. Next P is Preferences which signifies importance of knowing what kind

of material prospects would like to have for nurturing. The third P is Personal according to

which it is also important to have people calling prospects apart from email messages. A

personal contact would help companies understand what is really required to nurture that

specific lead. The final P is Pulling which is about getting to know prospects in greater detail

and then offering them relevant nurturing content.

2.4.1. Summary of literature relating to lead nurturing/conversion

Practitioners are the main sources of literature relating to lead nurturing. The key highlights

from the literature are that it is important to involve leads in the lead nurturing by asking their

permission, preferred medium of contact and frequency of material they want to obtain. Also

for nurturing it is important to establish the stage of cold lead in the lead nurturing and thus

sending them customized lead nurturing content. Social media is also highlighted as an

important medium to nurture leads.

For lead conversion, it is advised to include sales in the lead management process by taking

their feedback and leads must be sent to sales with additional information. Also, the literature

highlights that even after allocation of leads to sales channel they must be tracked and their

scores must be revised so that the leads not converted or contacted could be recycled thus

10 Marketing measurement company

13

increasing conversion rate. These leads must be send back to agents in the timeframe selected

by them or when their score goes above threshold.

2.5. Summary and insights from the literature review

The review of relevant literature has provided insights regarding what different practitioners

and academics think about lead management and also about the three main topics of this

research paper, lead generation, lead prioritization and allocation, and lead

nurturing/conversion. Main sources of literature are practitioners such as Marketo and

SmartLead. The literature is more general without focusing on one particular industry.

However, there is not much of literature regarding lead management highlighting it is a new

topic.

General literature relating to lead management overall gives a good understanding of various

necessary processes in lead management. Literature relating to lead generation highlights the

importance of effectively generating leads and how it should be done with various sources to

include and importance of measurement. Literature relating to lead prioritization and

allocation gave insights about the importance of lead prioritization and how leads could be

allocated after being prioritized. This is a critical step to increase the efficiency of lead

management process, since if right leads are sent to right sales force, the chances of their

conversion is good. Finally the literature relating to lead nurturing/conversion gives insight on

how we can gain the maximum out of every lead being generated ensuring maximum

conversion rate.

2.6. Literature review and research question of the paper

Literature review has helped to increase understanding of how lead management could be

done and various processes associated with lead management. Now, this will be used to assess

the lead management process recommended by AXA Group to its various entities. After

understanding and analyzing AXA Group‘s recommendations, a gap analysis will be done

between AXA Group‘s recommendations and existing literature11

. Through this gap analysis,

we will be able to see how different the AXA Group‘s recommended process is as compared

11 See section 7 for further details

14

to the literature and if there is any scope of improvement to AXA Group‘s recommendations.

Also, we will observe if there are some existing literature‘s recommendations which could not

be applied to AXA or there is scope for further research. Thus, this literature review will be

critical to the analysis of AXA Group‘s recommendations.

2.7. Methodology and data collection

In order to fully understand AXA Group‘s lead management recommendations I used my

experience in the Group‘s marketing and distribution team as an intern from May to

December 2012. During my internship, I attended various workshops and seminars conducted

by AXA Group to share its recommendations and best practices related to lead management

with AXA entities. Thus, I was able to gain a good insight of the topic and also understood

the concerns of AXA entities from a practical point of view.

Apart from my experience at AXA, I also had access to the lead management documents

prepared by AXA Group. These documents have been prepared by doing extensive internal

and external benchmarks of lead management and best practices from these benchmarks are

recommended by AXA Group to its entities. To further insure that I am staying up to date

with the recommendations proposed and not limiting myself to my knowledge and AXA

Group‘s documents, I interviewed people at AXA Group. Through these interviews I tested

my hypothesis and scenarios to ensure that this paper is very close to what is being done

practically at AXA.

Also, I carried out extensive search on the internet and research databases to explore existing

literature and find some best practices by companies in lead management and other relevant

information to support and validate my opinions in this paper.

Before analyzing the lead management recommendations of AXA Group, in the next few

sections the importance of lead management in insurance and at AXA will be highlighted, and

why it has become a focus now.

15

3. Insurance and lead management

3.1. Types of insurance and lead management

3.1.1. Life and savings (L&S)

These are complex insurance products which are sold once and then the buyer gives premium

after a certain time period depending on the initial contract. Since these are complex, it is not

easy to sell them online and thus lead management is not focusing on these products. This is

highlighted by direct channels having a small share in L&S distribution12

.

3.1.2. Property and causality (P&C) – focus of lead management

Property and causality could have both complex and simple products. The simple products

under P&C are sold online and thus lead management is focused on these simple products.

This is highlighted by direct channels having a large share in P&C distribution11

. Some of

these simple products include motor insurance, health insurance, and property insurance.

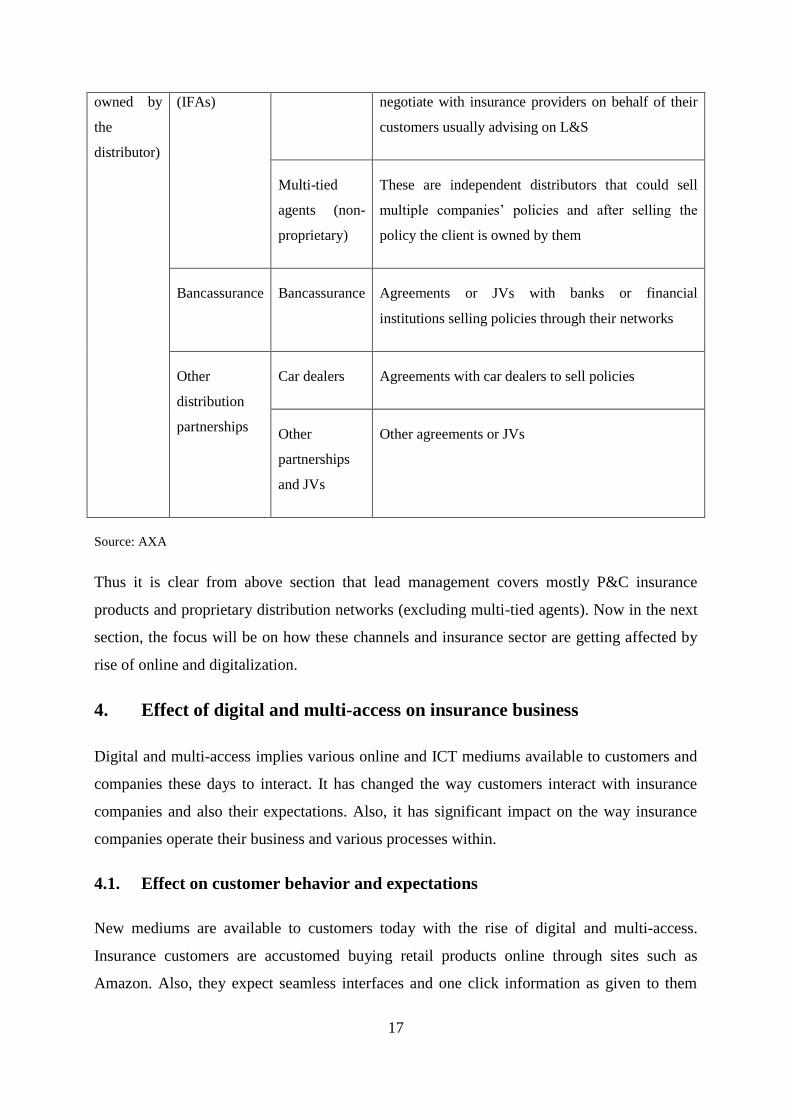

3.2. Distribution channels under scope of lead management at AXA

The distribution channels in insurance could be broadly categorized into proprietary and non-

proprietary networks. Proprietary channels are the distribution networks owned by insurance

companies. Non-proprietary networks are not owned by insurance companies and usually sell

multiple insurance policies. As per AXA, these could be further subdivided as in table 1. It is

to be noted that lead management covers only proprietary distribution networks at AXA. The

distribution channels in scope of lead management are direct, salaried sales force, exclusive

agents generalists and exclusive agents specialists. Non-proprietary networks are not included

in lead management since they could sell policies of multiple companies to customers and

thus AXA could not make sure that to a lead send by AXA they only sell policy of AXA to

that lead.

12 See Appendix 1

16

Table 1: Different distribution networks at AXA

Type of

network

Intermediate

consolidation

Name of

channel

Definition

Proprietary

networks

(client base

owned by

AXA)

Direct Direct There is no involvement of sales person or

intermediary and sales are done directly through

internet, telephone, etc.

Salaried Sales

Force

Salaried Sales

Force

This include AXA employees selling insurance

policies to retail / SMEs, large account managers

selling to corporate business, and also the insurance

policies of AXA employees taken without a

distributor

Agents

Exclusive

Agents

Generalists

These are independent distributors (not on the payroll

of AXA). As generalists, they sell both L&S and

P&C insurance

Exclusive

Agents

Specialized

These are independent distributors but specialized in

certain category E.g. selling only motor in P&C

Multi-tied

agents

(proprietary)

These are independent distributors that could sell

multiple companies‘ policies. However, after they sell

the policy, the client is owned by AXA and not them.

Non-

proprietary

networks

(Client

base

Brokers/

Independent

Financial

Advisors

Brokers

General

These are independent insurance intermediaries who

negotiate with insurance providers on behalf of their

customers selling L&S and P&C

IFAs These are independent financial intermediaries who

17

owned by

the

distributor)

(IFAs) negotiate with insurance providers on behalf of their

customers usually advising on L&S

Multi-tied

agents (non-

proprietary)

These are independent distributors that could sell

multiple companies‘ policies and after selling the

policy the client is owned by them

Bancassurance Bancassurance Agreements or JVs with banks or financial

institutions selling policies through their networks

Other

distribution

partnerships

Car dealers Agreements with car dealers to sell policies

Other

partnerships

and JVs

Other agreements or JVs

Source: AXA

Thus it is clear from above section that lead management covers mostly P&C insurance

products and proprietary distribution networks (excluding multi-tied agents). Now in the next

section, the focus will be on how these channels and insurance sector are getting affected by

rise of online and digitalization.

4. Effect of digital and multi-access on insurance business

Digital and multi-access implies various online and ICT mediums available to customers and

companies these days to interact. It has changed the way customers interact with insurance

companies and also their expectations. Also, it has significant impact on the way insurance

companies operate their business and various processes within.

4.1. Effect on customer behavior and expectations

New mediums are available to customers today with the rise of digital and multi-access.

Insurance customers are accustomed buying retail products online through sites such as

Amazon. Also, they expect seamless interfaces and one click information as given to them

18

through products such as Apple store. This has considerably changed their expectations and

way to interact with insurance companies. As per a insurance study done by Accenture on

7000 consumers in 13 countries, around 60% of people13

use mobile devices to get

information on insurance products, do operations related to insurance and subscribe an

insurance service or product. The number is expected to increase to nearly 70% in next 2

years.

4.1.1. Information gathering

With the rise of digital and multi-access consumers are changing their buying behavior.

Consumers are spending more time online to learn about the insurance products. ―72 percent

of consumers use the Internet to learn about auto insurance” (Accenture 2011). ―Fiftyone

percent of consumers search the Internet before making a high-value in-store purchase”

(Accenture 2011). Thus now, customers have more transparency regarding insurance prices

with rise of aggregators (online websites giving combined information of products of various

insurance companies) and other online channels. Also, social media is changing the way

customers gather information regarding insurance products. As per Accenture survey in 2011,

30% of the people said that they took in account of feedback of other customers on social

media. This percentage is even higher among people in lower age group (see figure 6).

Figure 6: Importance of social media feedback in selecting insurance provider

Source: Accenture 2011

13 60% in each category separately

19

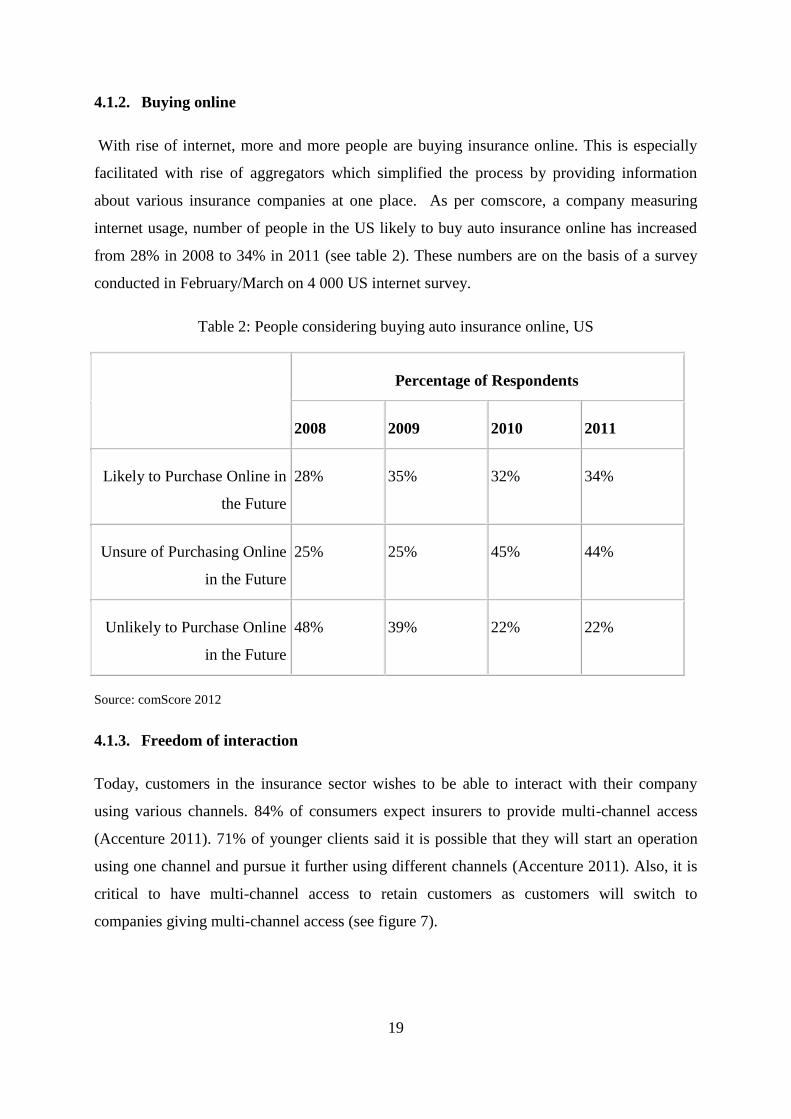

4.1.2. Buying online

With rise of internet, more and more people are buying insurance online. This is especially

facilitated with rise of aggregators which simplified the process by providing information

about various insurance companies at one place. As per comscore, a company measuring

internet usage, number of people in the US likely to buy auto insurance online has increased

from 28% in 2008 to 34% in 2011 (see table 2). These numbers are on the basis of a survey

conducted in February/March on 4 000 US internet survey.

Table 2: People considering buying auto insurance online, US

Percentage of Respondents

2008 2009 2010 2011

Likely to Purchase Online in

the Future

28% 35% 32% 34%

Unsure of Purchasing Online

in the Future

25% 25% 45% 44%

Unlikely to Purchase Online

in the Future

48% 39% 22% 22%

Source: comScore 2012

4.1.3. Freedom of interaction

Today, customers in the insurance sector wishes to be able to interact with their company

using various channels. 84% of consumers expect insurers to provide multi-channel access

(Accenture 2011). 71% of younger clients said it is possible that they will start an operation

using one channel and pursue it further using different channels (Accenture 2011). Also, it is

critical to have multi-channel access to retain customers as customers will switch to

companies giving multi-channel access (see figure 7).

20

Figure 7: % of very likely and somewhat likely people who would switch to other

companies if their company would not provide a multi-access communication channel

Source: Accenture 2011

4.1.4. Customers’ willingness to use mobile devices to decrease insurance premiums

Significant amount of customers are willing to use mobile devices to lower their insurance

premiums. This gives a good opportunity to insurance companies and also makes a strong

case for them to offer such products. As per the Accenture survey, 60% of the people buying

P&C products and 45% of the people buying L&S products are very or somewhat interested

in using mobile to reduce their insurance premiums. Some of the applications of mobile

devices to reduce insurance premiums include recording how a customer is driving through

their mobile device, life insurance premiums depending on the daily activity level, etc. (see

figure 8).

Figure 8: Number of people willing to accept using mobile to reduce their insurance

premium

Source: Accenture 2011

21

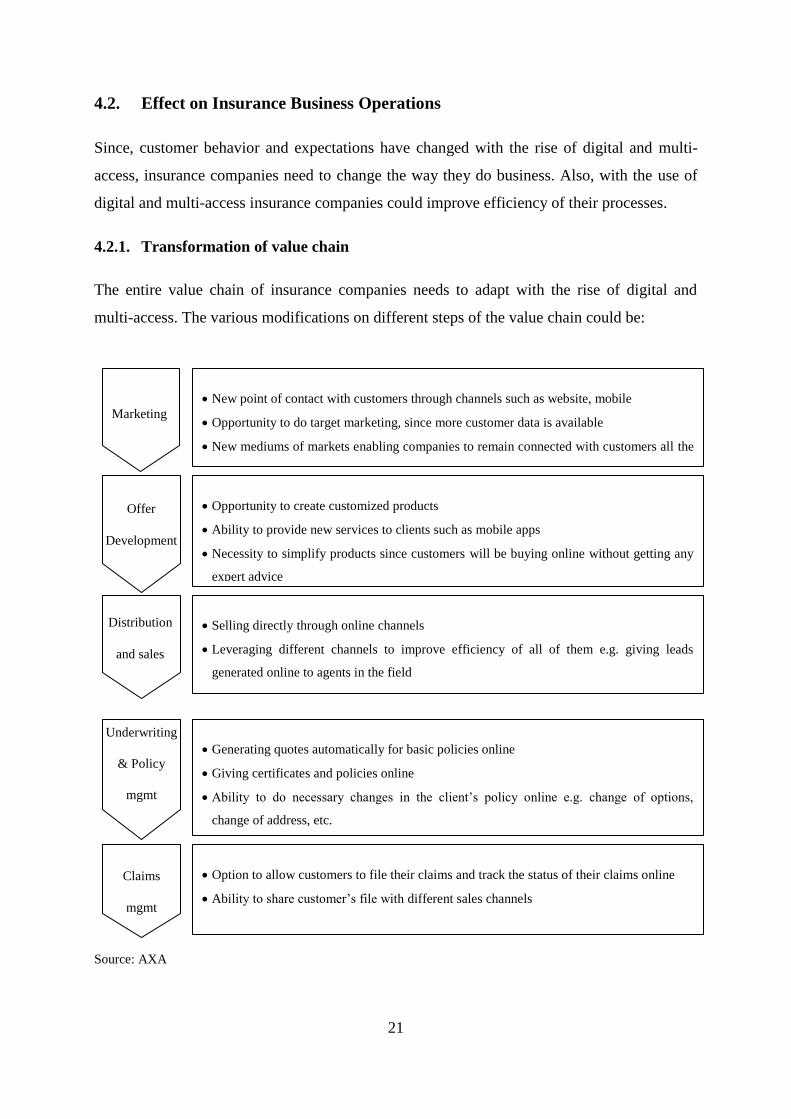

4.2. Effect on Insurance Business Operations

Since, customer behavior and expectations have changed with the rise of digital and multi-

access, insurance companies need to change the way they do business. Also, with the use of

digital and multi-access insurance companies could improve efficiency of their processes.

4.2.1. Transformation of value chain

The entire value chain of insurance companies needs to adapt with the rise of digital and

multi-access. The various modifications on different steps of the value chain could be:

Source: AXA

New point of contact with customers through channels such as website, mobile

Opportunity to do target marketing, since more customer data is available

New mediums of markets enabling companies to remain connected with customers all the

time such as Facebook and twitter

Opportunity to create customized products

Ability to provide new services to clients such as mobile apps

Necessity to simplify products since customers will be buying online without getting any

expert advice

Selling directly through online channels

Leveraging different channels to improve efficiency of all of them e.g. giving leads

generated online to agents in the field

Rise of aggregators

Generating quotes automatically for basic policies online

Giving certificates and policies online

Ability to do necessary changes in the client‘s policy online e.g. change of options,

change of address, etc.

Option to allow customers to file their claims and track the status of their claims online

Ability to share customer‘s file with different sales channels

Marketing

Offer

Development

Distribution

and sales

Claims

mgmt

Underwriting

& Policy

mgmt

22

4.2.1.1. Transformation of distribution network

Among the changes in value chain, transformation of distribution is one of the key challenges

and also the focus of this paper. In the new environment the way to access the client has

changed with new marketing channels. Also, the number of people going to traditional

insurance agents is reducing with more people buying online. This will have an impact on

value sharing agreements between insurance companies and agents e.g. change in

commissions. Also, there is possibility that insurance companies might need to reduce their

distribution footprint, which might led to greater political and economical issues. Also, with

the rise of digitalization insurance companies need to find ways to link all their different

channels, ensuring that instead of different channels competing against themselves, they assist

each other in achieving better results e.g. lead management process.

4.2.2. Changes in competitive dynamics

Apart from internal changes in value chain, external environment has also changed

considerably and especially the competitive environment. Insurance industry has become

more competitive due to rise of digital and multi-access. With the rise of digital, the entry

barriers for new entrants have reduced significantly since now they do not necessarily need to

have large scale agent network on the field. Also, digitalization has enabled customers to

collect information about different insurance products in the market easily. Clients have

become more demanding regarding services and speed online. This increases the chances of

customers switching to competitors and has decreased client royalty.

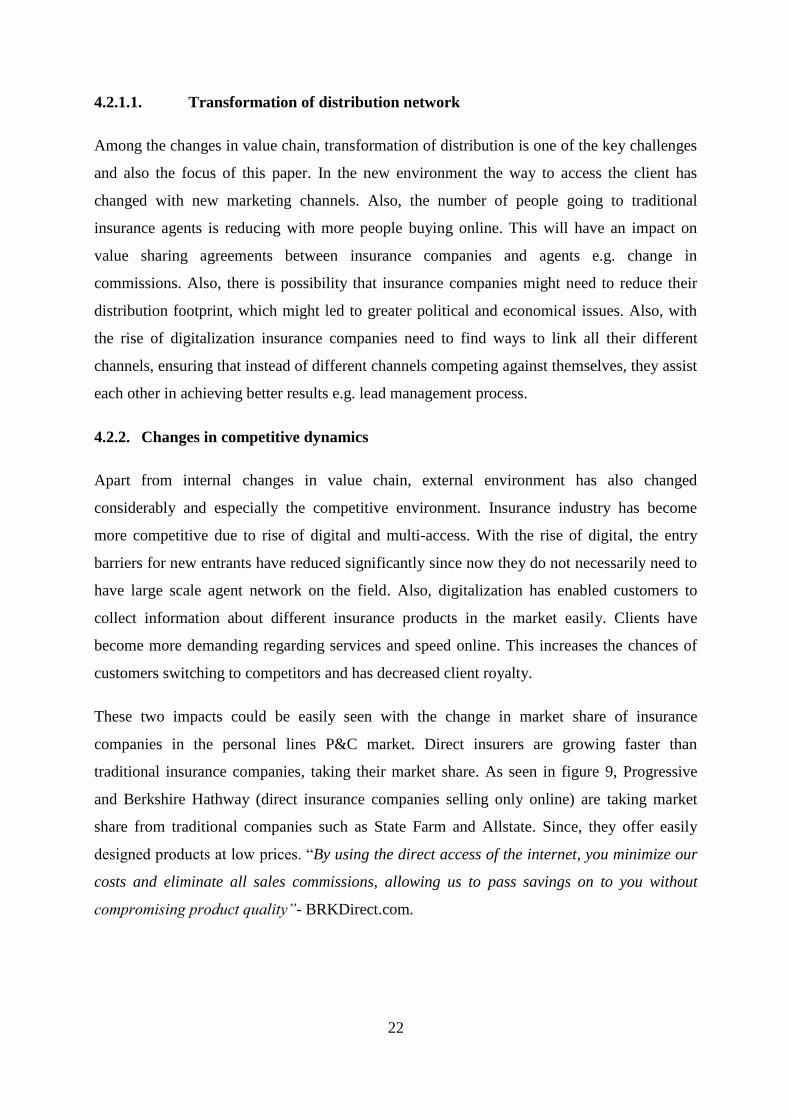

These two impacts could be easily seen with the change in market share of insurance

companies in the personal lines P&C market. Direct insurers are growing faster than

traditional insurance companies, taking their market share. As seen in figure 9, Progressive

and Berkshire Hathway (direct insurance companies selling only online) are taking market

share from traditional companies such as State Farm and Allstate. Since, they offer easily

designed products at low prices. ―By using the direct access of the internet, you minimize our

costs and eliminate all sales commissions, allowing us to pass savings on to you without

compromising product quality”- BRKDirect.com.

23

Figure 9: Market share of traditional and direct insurance players in the US

Source: PwC, SNL data, website of Progressive, website of Berkshire Hathway

Thus it is quite clear that digital and multi-access has transformed the way insurance

companies used to conduct their business. Their customers are researching on the internet

before buying and also buying on the internet. Customers‘ expectations have changed as they

expect to interact with their companies using various digital channels and not only the

traditional physical channels. Customers are even willing to share their data through mobiles

to reduce their premium. Also, the industry has become more competitive with reduced entry

barriers.

Due to this change in customer behavior and competitive environment insurance companies

are adapting their business model. In the next section, how AXA is adapting its business

model as per this new environment through transformation levers will be explained. Also how

lead management fits in this new model will be highlighted.

5. AXA’s digital and multi-access transformation levers and lead

management

5.1. Objectives

Considering the impacts digital and multi-access have on insurers and their customers, AXA

has decided to build a multi-access model focused on building a differentiated customer

experience by providing public & private digital services on all devices (web, mobile,

touchpad) and new digital tools and processes for distributors (paperless, e-signature). Also,

24

AXA aims to develop businesses originated from distant channels (online/telesales) through

developing simplified and adaptive offers, and providing choice to buy through full distant

channels or agents and increasing cross-selling to the existing customer base.

Another objective is to achieve a cultural shift towards experimentation through focusing on

increasing tests on innovative offers or relationship models, leveraging new technologies and

new media. Also, to switch towards a test and learn approach

5.2. Transformation levers

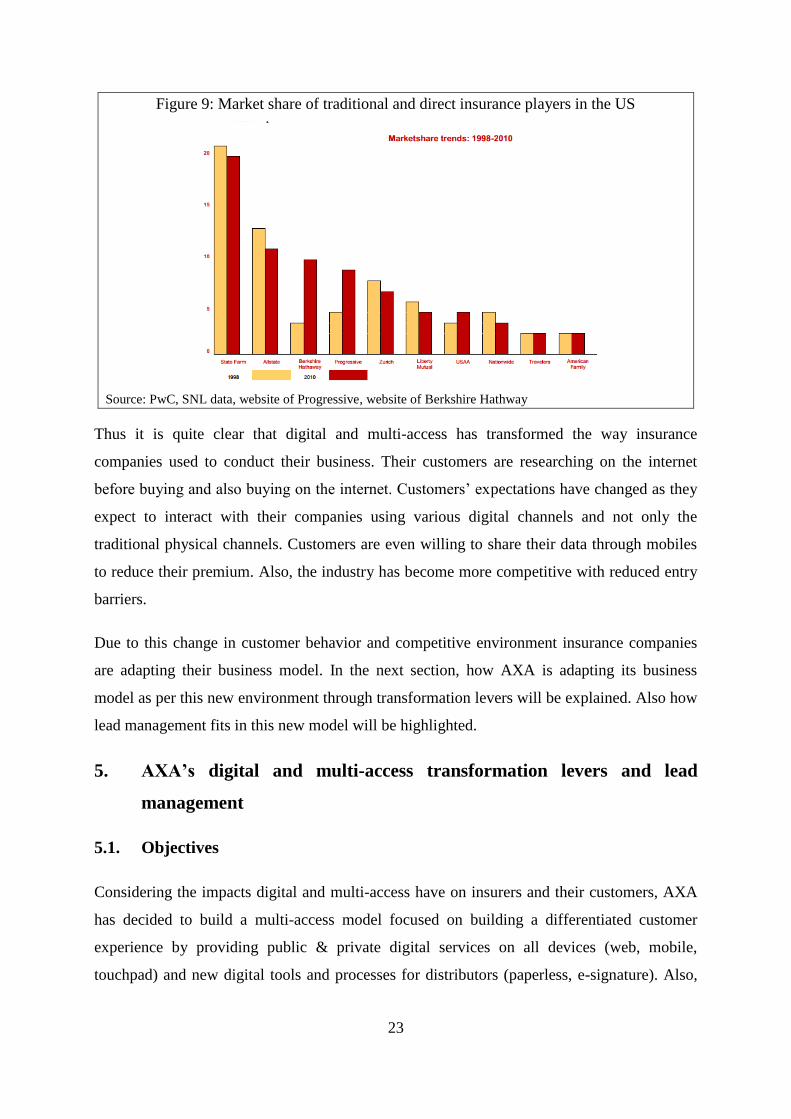

To achieve these objectives, AXA identified nine levers. Four of the levers have specific

focus with others being more transversal. Two of the nine levers are specifically related to

Lead Management (which is the main focus of this paper):

4. Multi-Channel Purchase funnel/CRM

7. Distribution Transformation

Figure 10: AXA's transformation levers and lead management

Source: AXA

Thus in AXA, lead management is a very important process in fully achieving the distribution

transformation necessary with the rise of digital and multi-access. To ensure that all the AXA

entities could perform lead management, AXA Group did an internal and external

benchmarking study to identify best practices and thus give recommendations on how to do

lead management. The results of this study, combined with my own research through my

internship, internet and interviews is presented in the next section describing AXA‘s

recommendation on how to do lead management.

Lead Management

identified as number #1

priority

25

6. How to do lead management: AXA Group recommendations

AXA Group gives recommendation to entities on how to implement different phases of lead

management process. In this section, these recommendations for three operational processes

of lead management: generate leads, ‗prioritize and allocate‘ leads and ‗nurture and convert‘

leads will be presented. Also, some best practice examples have been included to further

elaborate how it could be done in real world.

6.1. Lead generation

Lead generation is the first step of the lead management process. This is where insurance

companies find contacts of potential future clients. The recommendations by AXA include

following:

6.1.1. Define scope

The first step of lead management process is defining its scope. This includes some of the key

decisions including the product to be sold, the type of lead to target and whether the objective

is to acquire new customers or to cross-sell/upsell/retain existing customers.

The product must be decided in advance and the product should be a non-complex product

such as motor or health insurance so that leads could be generated online14

.

6.1.2. Sources

The leads must be collected through all the different channels available. The possible

channels to generate online leads include mail, email, aggregators (third parties) and website.

Also, it is important to be on top of Google search results. There can be two ways to be on top

of Google search results: Search Engine Marketing (SEM) and Search Engine Optimization

(SEO). SEM is a way to be on top of search results by paying the search engine. SEO is a way

to be on top of search results through optimizing website and other methods on which search

engine selects and prioritize results. AXA recommends its entities to use SEM and pay for

being on top of Google search results, since it is quite hard to be on top through SEO due to

14 See appendix 1

26

lack of knowledge of how Google sorts its data. This can be seen in the screenshot of Google

search result of assurance auto (see figure 11). www.axa.fr is the second link on the

advertisement related to auto assurance (SEM). Also, it is second in the list generated by

Google through its prioritization methodology.

The third recommendation by AXA Group is that the data collected at different sources must

be same. The data collected must enable the entity to be able to identify and contact leads.

Also, it must have qualification data, enabling the entity to classify lead as hot/cold. E.g. one

qualifying data could be their behaviour on the AXA website. Which page they visit (main

page, buying page, products page), whether they complete the form or not, how far they go in

the buying process (generate quote or not).

The final recommendation for sources is that online channels must have necessary resources

to collect data. To do this online quotations must be provided to visitors on the website and

online forms and questions must include data which will help to classify leads in hot/cold and

enabling the entity to send them directly to agents/telesales.

Figure 11: Google search result of keyword ―assurance auto‖ in France and AXA‘s

positioning

Source: Google.fr

6.1.3. Managing marketing campaigns – Preparation

After deciding the scope and sources next step is preparation of marketing campaigns. The

marketing campaign must be designed keeping in mind the objective (sell, cross-sell, up-sell,

retain, etc.) and the target population (segment, demography, etc.). Further to prepare a good

27

marketing campaign, it is important to keep agents in the loop and ensure that the campaign

fits their needs.

Another key aspect of preparation of marketing campaigns is to select the right combination

of marketing actions. An appropriate action or a mix of actions must be selected based on

objective, resources and target population. There could be four main types of marketing

actions possible: ―advertising‖, ―push direct marketing‖, ―online lead generation‖ and

―experience based lead generation‖ which is a part of online lead generation. Advertising

involves campaigns run in TV, print, etc. They target both existing and new customers.

However, their cost is high and the quality of leads generated is not good. Push direct

marketing includes campaigns directly addressing consumers through medium such as mails

by post or emails. They also target both existing and new customers. Their costs are high but

generate good leads. However, it is difficult to acquire new customers through them since the

company would need to acquire customer data from a 3rd

party database.

Online lead generation include online campaigns which aim at bringing consumers to AXA

website or to a third party website from where AXA collect leads. They also target both

existing and new customers. They are less costly and if banner ads/message is done correctly

could get good quality leads. Another way of generating online leads is through experience

based lead generation. These campaigns mostly target existing clients through inbound

contact by private websites and generate excellent quality leads15

.

6.1.4. Managing marketing campaigns - Execution

For effectively executing the marketing campaigns first it is necessary to select a good source

for getting target files (people you would like to target). For existing customers an entity

could use CRM database and buy list from third-party for prospects and former customers.

After getting the target files they must be checked and additional data must be added. For

prospects it is important to check duplication. Then the entity must choose the marketing

media. Direct marketing media to use for each targeted prospect could be defined based on

previous campaigns response history

15 See section 6.1.6 for further details

28

Also, it is important to handle relationship with agents since AXA does not always own

agents. It is important to keep them in the loop since they are the end-contact to prospects.

Their role in the marketing campaign must be clearly defined. Also, agents must be allowed to

define the scope of campaigns and must have the option to add or exclude customers from

targets. E.g. AXA France informs agents of all marketing campaigns via a single tool (KIWI)

and allows agents to manage and control their participation to marketing campaigns via a

unique interface (NETAGENTS)

6.1.5. Measure and improve marketing campaign performance

After preparing and executing marketing campaigns, next important step is measuring their

performance. Key metrics must be defined to measure lead generation performance. Some of

these metrics per campaign could be lead generation rate (number of generated leads / number

of targeted consumers), cost per generated lead (marketing campaign budget / number of

generated leads). The results must also be split by tracking sources of incoming leads, per

products, per segments, customers and prospects, etc.16

.

6.1.6. Best practice for lead generation from existing customers: an example of ING

After doing the initial steps and establishing a web-based lead generation system, the next

advanced step for insurance companies could be using inbound marketing to generate

personalised offers to clients. These offers could be presented/pushed through customer

private websites to generate highly qualified ―cross-sell leads‖ at minimal marketing cost.

This has been done by ING Direct (Hesse A., 2009).

In late 2000s ING switched from traditional outbound campaign management to inbound

campaign management (see figure 12). In outbound campaign, first an offer is build and then

ING used to market this offer to best group of people. This led to similar offers being

marketed to every selected client. In inbound campaign, first data of a customer is analyzed

and then matched with various offers available. This enabled ING to provide customized

solutions to customers. Through providing these customized solutions ING expected to

increase the response rate by as much as 60% and an additional earning of Euro 20 million per

year. Also, ING expected to cut its direct marketing costs by 35% per year.

16 See section 6.3.2 for further details

29

For selecting the type of product suited for a particular customer, first at least one product

most suited for the customer is selected from different product groups e.g. one product from

savings, one from payments and two from mortgages. Now the net present value of all these

products is calculated and the products most profitable to bank are proposed to the customer.

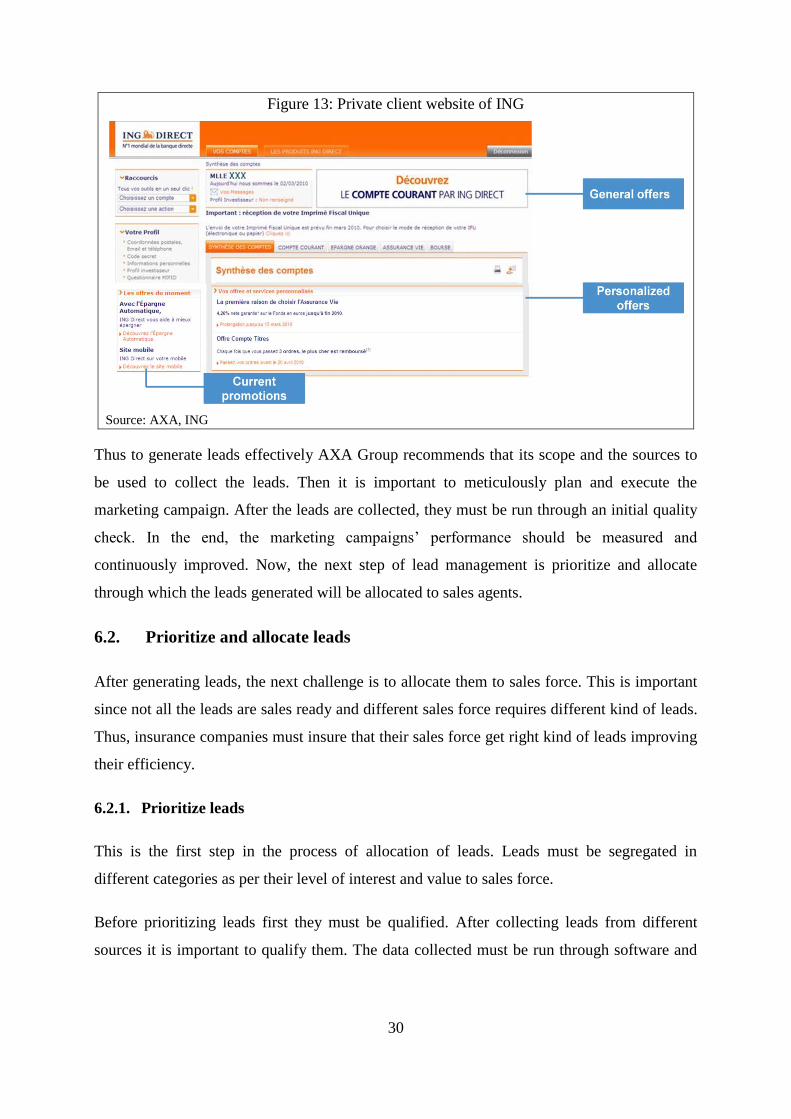

These customized solutions are presented to client through a private website (see figure 13).

In ING Direct, customers can see best offers for them on their private websites. When

customers login to their page, they could see customized as well as general offers and

promotions of ING Direct. To provide these customized solutions, ING Direct gathers

additional information about customers through online forms. Insurance companies could

launch similar private websites generating high-quality leads at minimal costs.

Figure 12: Outbound and inbound marketing campaign management

Source: Hesse A. 2009

30

Figure 13: Private client website of ING

Source: AXA, ING

Thus to generate leads effectively AXA Group recommends that its scope and the sources to

be used to collect the leads. Then it is important to meticulously plan and execute the

marketing campaign. After the leads are collected, they must be run through an initial quality

check. In the end, the marketing campaigns‘ performance should be measured and

continuously improved. Now, the next step of lead management is prioritize and allocate

through which the leads generated will be allocated to sales agents.

6.2. Prioritize and allocate leads

After generating leads, the next challenge is to allocate them to sales force. This is important

since not all the leads are sales ready and different sales force requires different kind of leads.

Thus, insurance companies must insure that their sales force get right kind of leads improving

their efficiency.

6.2.1. Prioritize leads

This is the first step in the process of allocation of leads. Leads must be segregated in

different categories as per their level of interest and value to sales force.

Before prioritizing leads first they must be qualified. After collecting leads from different

sources it is important to qualify them. The data collected must be run through software and

31

there must be regular checks put in place to remove leads putting wrong or incomplete data.

E.g. giving name as abc, incorrect pin code, etc.

AXA does not give detailed recommendation on how entities could do lead scoring to

prioritize these qualified leads. Currently, AXA recommends leads to be qualified on the basis

of whether they have asked to be contacted by AXA or not and their stage in online sale. If

they have completed online quote and asked to be contacted by AXA, they are qualified as hot

leads. If they have started the online quotation or finished it and do not ask to be contacted by

AXA, they are classified as cold leads. These cold leads are further prioritized on the basis of

their value. Cold leads with high value (ask to be contacted by AXA or searching for high

premium insurance) must be send to telesales for nurturing and cold leads with low value

must be nurtured through other mediums17

.

6.2.2. Allocate leads

After prioritizing the next step is allocating these leads. If the leads are hot they should be

send to agents directly. If the leads are cold and of high value they must be send to telesales

for nurturing and if the leads are cold and of low value they must be nurtured through other

medium18

.

If there is not an advanced lead management system comprising telesales and lead nurturing

then AXA Group proposes that leads could be allocated in a way that hot leads are pushed