Instructure 3.3.16 v final pdf

33

-

Upload

instructure -

Category

Investor Relations

-

view

757 -

download

5

Transcript of Instructure 3.3.16 v final pdf

FORWARDING LOOKING STATEMENTS & NON-GAAP MEASURES This presentation and the accompanying oral commentary contain “forward-looking” statements that are based on our beliefs and assumptions and on information currently available to us. Forward-looking statements include information concerning our possible or assumed future results of operations and financial performance, business strategies, potential growth opportunities and the effects of competition. Forward-looking statements include all statements that are not historical facts and can be identified by terms such as “believe,” “will,” “may,” “estimate,” “continue,” “anticipate,” “intend,” “should,” “plan,” “might,” approximately,” “expect,” “predict,” “could,” “potentially” or the negative of these terms or other similar expressions. Forward-looking statements involve known and unknown risks, uncertainties, assumptions and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Important risk factors are described more fully in the final prospectus for our initial public offering, which was filed with the Securities and Exchange Commission (the “SEC”) on November 13, 2015 and other documents filed with the SEC and could cause actual results to vary from expectations. Forward-looking statements represent our management’s beliefs and assumptions only as of the date of this presentation. Except as required by law, we assume no obligation to update these forward-looking statements publicly, or to update the reasons why actual results could differ materially from those anticipated in the forward-looking statements, even if new information becomes available in the future. This presentation includes certain non-GAAP financial measures as defined by the SEC rules. These non-GAAP financial measures are in addition to, and not as a substitute for or superior to measures of financial performance prepared in accordance with U.S. GAAP. There are a number of limitations related to the use of these non-GAAP financial measures versus their nearest GAAP equivalents. For example, other companies may calculate non-GAAP financial measures differently or may use other measures to evaluate their performance, all of which could reduce the usefulness of our non-GAAP financial measures as tools for comparison. As required by Regulation G, we have provided a reconciliation of those measures to the most directly comparable GAAP measures, which is available in the appendix.

2

SOFTWARE PEOPLE SMARTER

that makes

3

PRODUCT OVERVIEW

4

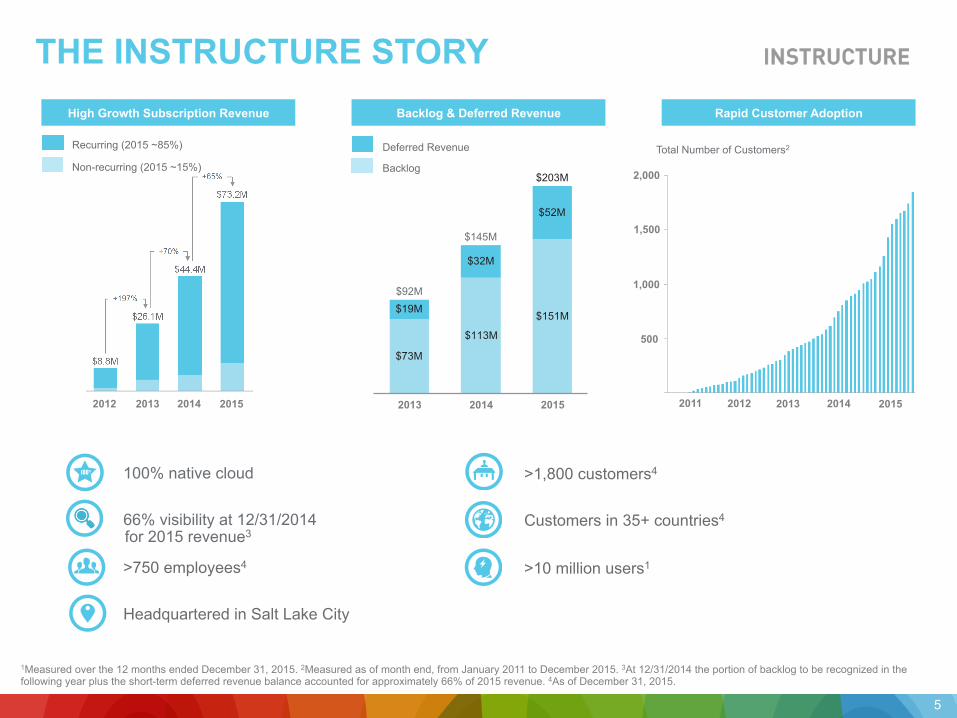

100% native cloud

66% visibility at 12/31/2014

>750 employees4

Headquartered in Salt Lake City

1Measured over the 12 months ended December 31, 2015. 2Measured as of month end, from January 2011 to December 2015. 3At 12/31/2014 the portion of backlog to be recognized in the following year plus the short-term deferred revenue balance accounted for approximately 66% of 2015 revenue. 4As of December 31, 2015.

for 2015 revenue3

THE INSTRUCTURE STORY High Growth Subscription Revenue

>1,800 customers4

Customers in 35+ countries4

>10 million users1

Recurring (2015 ~85%)

Non-recurring (2015 ~15%)

2014 2013 2012 2015

5

100%

Deferred Revenue

Backlog

Backlog & Deferred Revenue Rapid Customer Adoption

$73M

$113M

$151M$19M

$32M

$52M

$203M

$145M

$92M

2014 2013 2015

500

1,000

1,500

2,000

2014 2013 2012 2015 2011

Total Number of Customers2

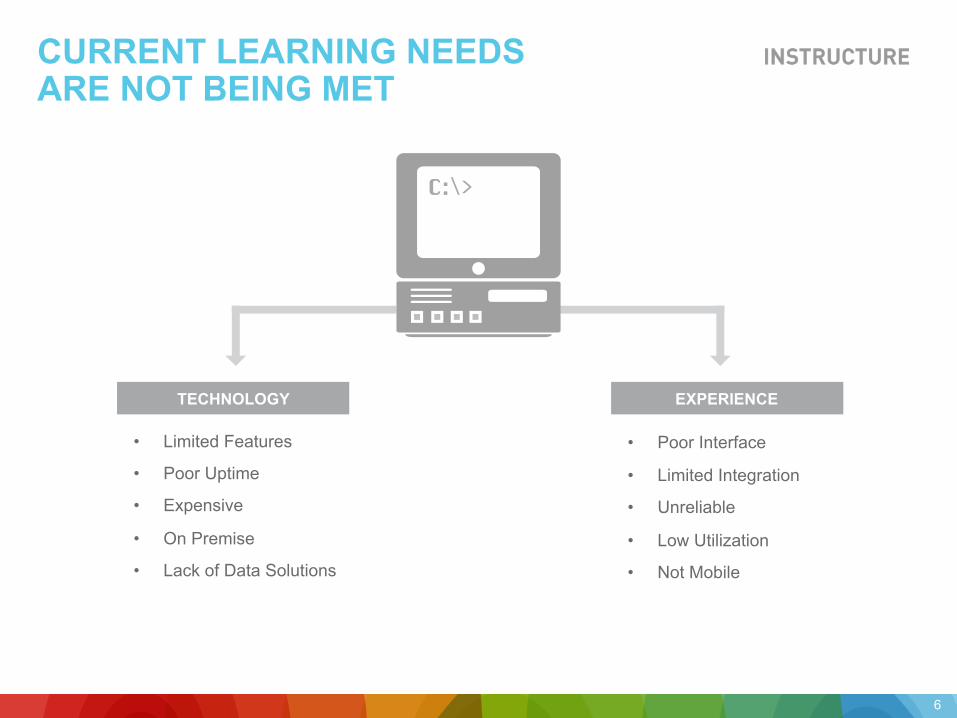

CURRENT LEARNING NEEDS ARE NOT BEING MET

• Limited Features

• Poor Uptime

• Expensive

• On Premise

• Lack of Data Solutions

• Poor Interface

• Limited Integration

• Unreliable

• Low Utilization

• Not Mobile

TECHNOLOGY EXPERIENCE

C:\>C:\>

6

INDUSTRY FORCES ARE CHANGING HOW PEOPLE WANT TO LEARN

Consumerized Collaborative

Mobile Engaging

7

OUR WINNING SOLUTION

Collaborative 99.9% Uptime Guarantee

Data Driven

Customer Support

Native Cloud Ease of Use

8

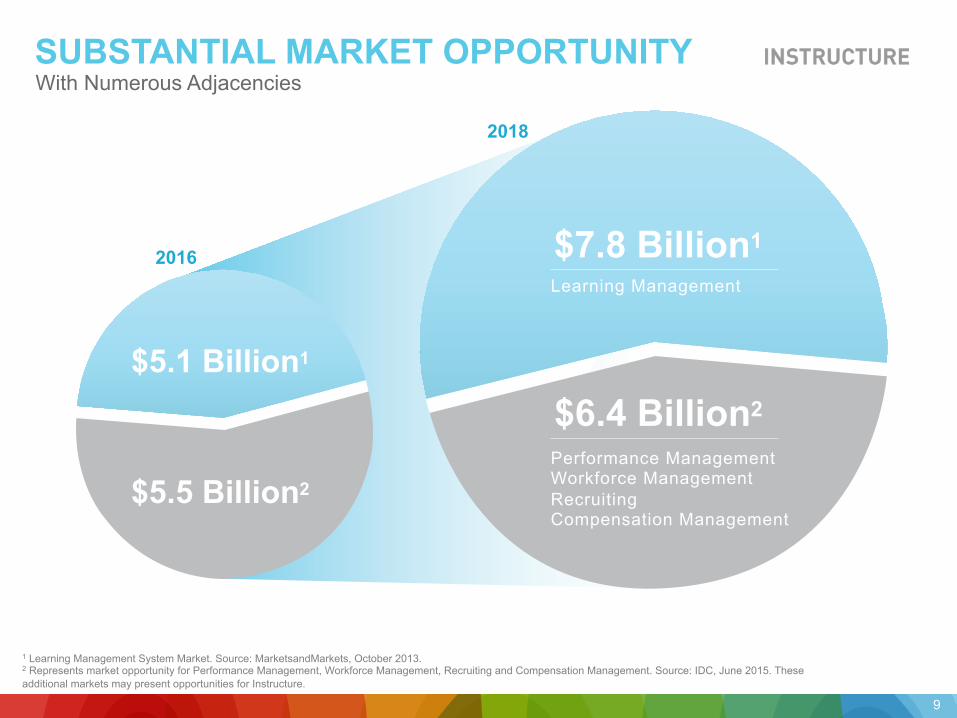

SUBSTANTIAL MARKET OPPORTUNITY With Numerous Adjacencies

2016

2018

Learning Management

Performance Management Workforce Management Recruiting Compensation Management

$7.8 Billion1

$6.4 Billion2

$5.1 Billion1

$5.5 Billion2

1 Learning Management System Market. Source: MarketsandMarkets, October 2013. 2 Represents market opportunity for Performance Management, Workforce Management, Recruiting and Compensation Management. Source: IDC, June 2015. These additional markets may present opportunities for Instructure.

9

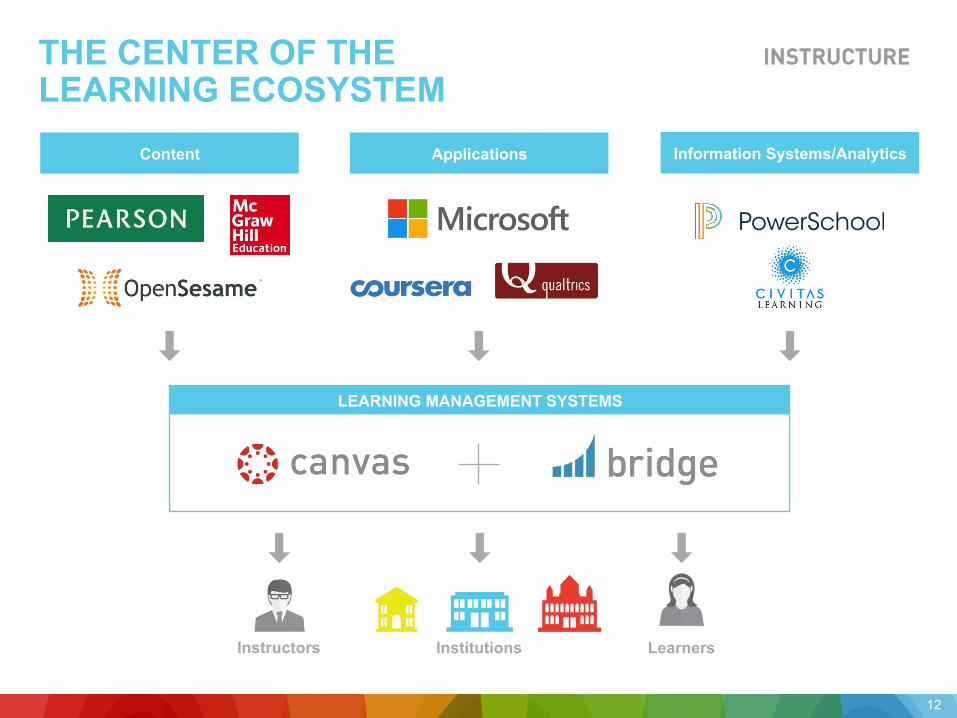

THE CENTER OF THE LEARNING ECOSYSTEM

Institutions

Information Systems/Analytics Content Applications

LEARNING MANAGEMENT SYSTEMS

Instructors Learners

12

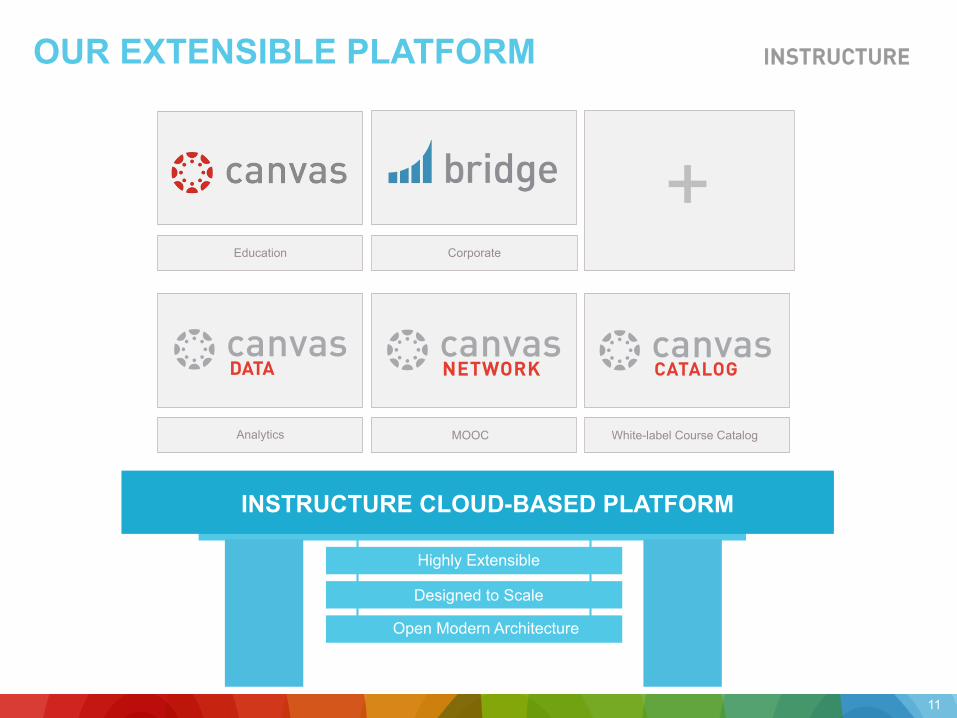

OUR EXTENSIBLE PLATFORM

Education Corporate

White-label Course Catalog MOOC Analytics

+

Highly Extensible

Designed to Scale

Open Modern Architecture

INSTRUCTURE CLOUD-BASED PLATFORM

11

OVER 1,800 CUSTOMERS ACROSS CATEGORIES

Hig

her E

d K

– 1

2 In

tern

atio

nal

Cor

pora

te

City University of Hong Kong

Used by 7 Ivy League

Schools

Used by K-12 Schools in 48 States

Serving 35+

Countries

Used by Businesses

and Academia

1As of December 31, 2015.

12

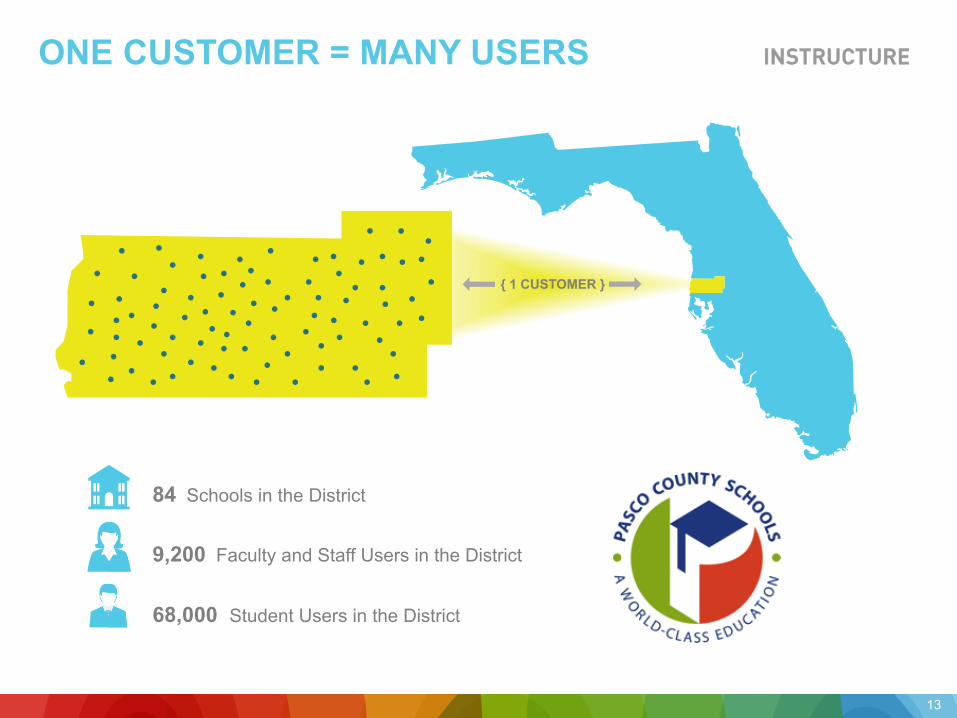

ONE CUSTOMER = MANY USERS

84 Schools in the District

9,200 Faculty and Staff Users in the District

68,000 Student Users in the District

{ 1 CUSTOMER }

13

LMS

LMS

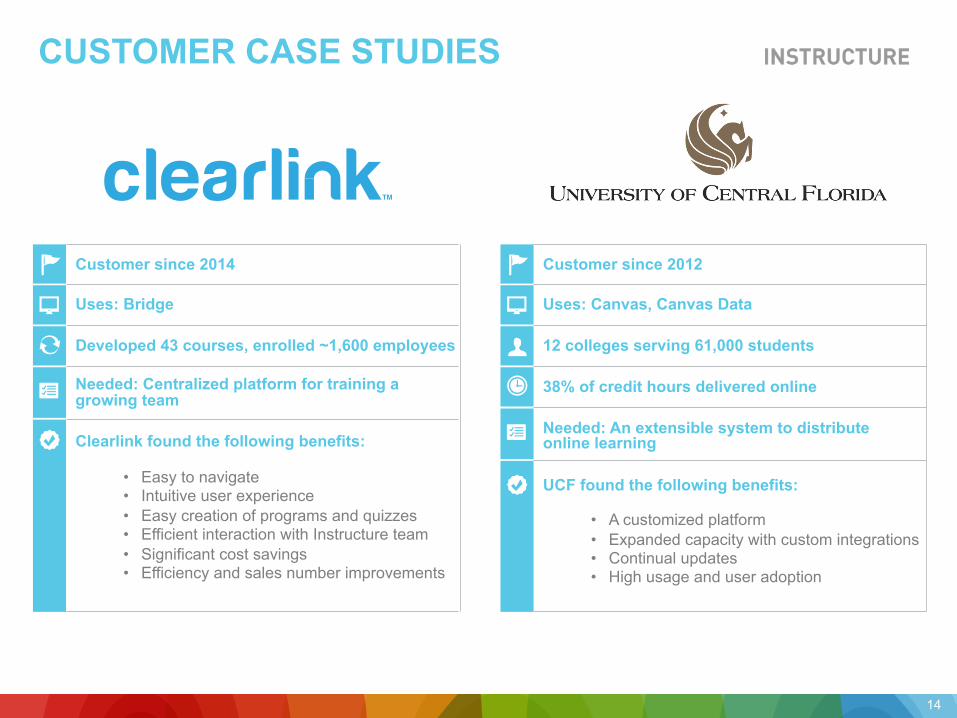

CUSTOMER CASE STUDIES

EDU

K12

CORP

LMS

Customer since 2014

Uses: Bridge

Developed 43 courses, enrolled ~1,600 employees

Needed: Centralized platform for training a growing team

Clearlink found the following benefits:

• Easy to navigate • Intuitive user experience • Easy creation of programs and quizzes • Efficient interaction with Instructure team • Significant cost savings • Efficiency and sales number improvements

Customer since 2012

Uses: Canvas, Canvas Data

12 colleges serving 61,000 students

38% of credit hours delivered online Needed: An extensible system to distribute online learning

UCF found the following benefits:

• A customized platform • Expanded capacity with custom integrations • Continual updates • High usage and user adoption

14

OUR USER’S EXPERIENCE

15

OUR GROWTH STRATEGY

Grow US Customer Base

Expand with Existing Customers New Offerings International

Expansion

16

INSIDE INSTRUCTURE

POWERFUL MISSION OPEN CULTURE CUTTING EDGE TECH

17

CUSTOMER CONFERENCE

INNOVATIVE MANAGEMENT

Josh Coates EMC Corp • Mozy.com • Scale Eight CEO

Steve Kaminsky Radisphere • TriZetto • Ernst & Young • McDonald’s Corporation

CFO

SVP People and Places Jeff Weber

Ancestry • The Russell Group • Shell Oil Company

FamilySearch • Microsoft

David Burggraaf SVP Engineering

Vmware • InfoTrax Systems • GE

Mitch Macfarlane SVP Product & Customer Experience

Marc Maloy HireRight • Certico EVP Worldwide Sales

Misty Frost Datamark • Critical Mass • Sumus Interactive• Dahlin Smith White

SVP Marketing

SVP/General Counsel and Secretary

18

Matt Kaminer Collective • Epocrates • MediMedia USA • WebMD

SVP General Counsel and Secretary

FINANCIAL HIGHLIGHTS

Solid Revenue Growth

Net Revenue Retention Greater than 100%1 100%

Investing for Continued Growth

Attractive Long Range Model

Strong Unit Economics $

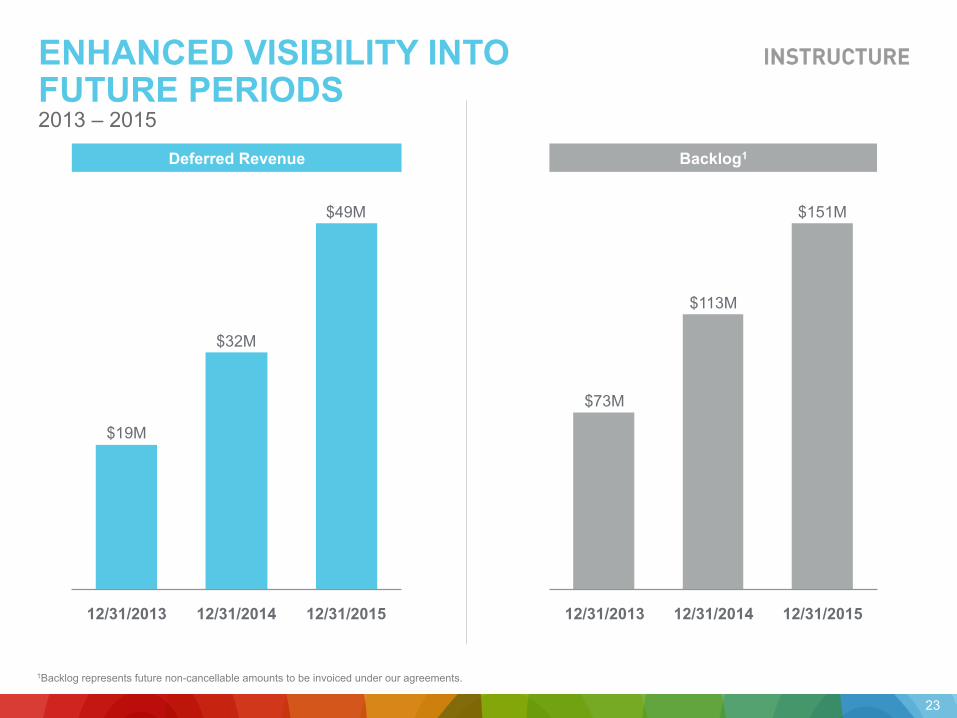

Enhanced Visibility Through Multi-Year Contracts

1 Net revenue retention rate is calculated by dividing the total revenue obtained from a particular customer in a given month by the total revenue from that customer from the same month in the immediately preceding year.

19

Non-GAAP Operating Loss as a % of Revenue2 Revenue Growth

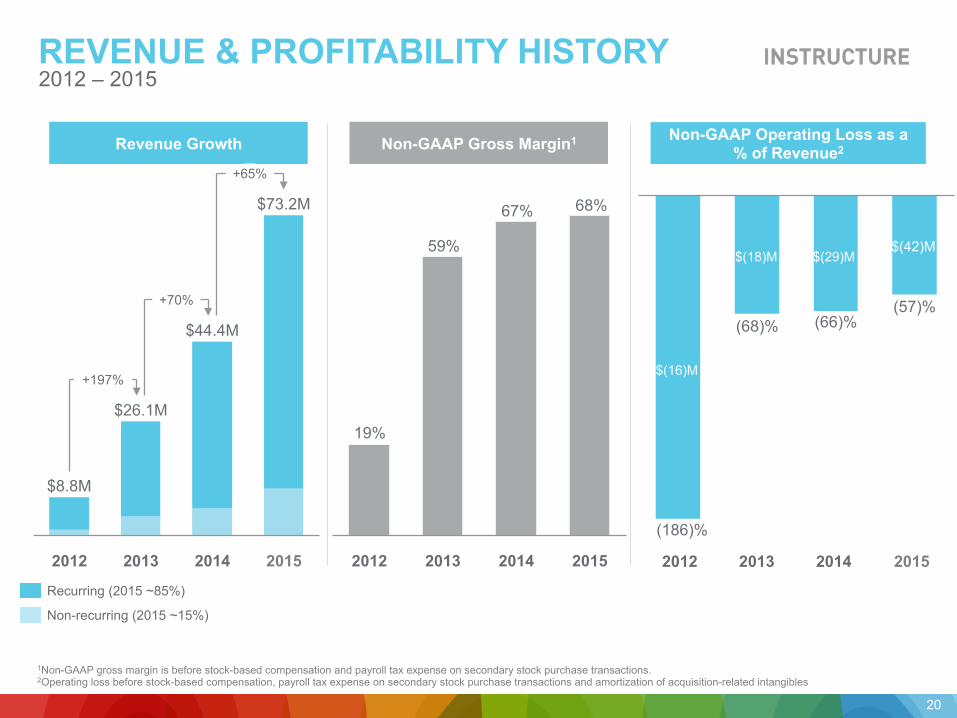

REVENUE & PROFITABILITY HISTORY 2012 – 2015

1Non-GAAP gross margin is before stock-based compensation and payroll tax expense on secondary stock purchase transactions. 2Operating loss before stock-based compensation, payroll tax expense on secondary stock purchase transactions and amortization of acquisition-related intangibles

Non-GAAP Gross Margin1

2015 2014 2013 2012 2012 2015 2014 2013

$(16)M

$(18)M $(29)M

+65%

2014

$44.4M

2013

$26.1M

+70%

2015

+197%

$73.2M

$8.8M

2012

$(42)M

20

19%

59%

67% 68%

(68)%

(186)%

(66)% (57)%

Recurring (2015 ~85%)

Non-recurring (2015 ~15%)

Non-GAAP General and Administration1

(% of Revenue) Non-GAAP Sales and Marketing1

(% of Revenue)

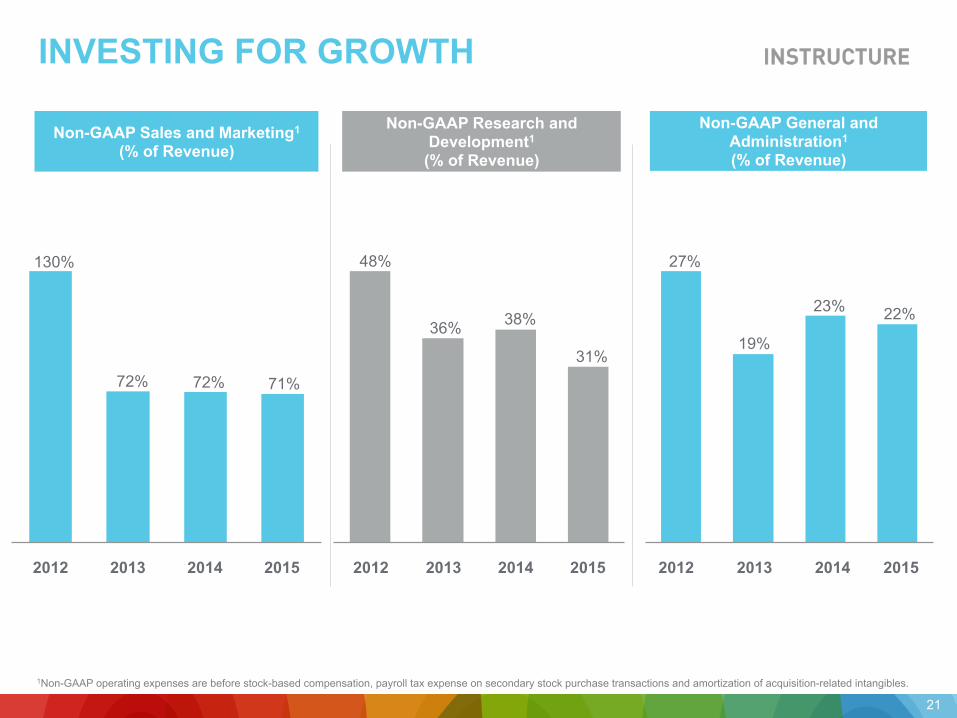

INVESTING FOR GROWTH

1Non-GAAP operating expenses are before stock-based compensation, payroll tax expense on secondary stock purchase transactions and amortization of acquisition-related intangibles.

Non-GAAP Research and Development1

(% of Revenue)

2015 2013 2014 2012 2015 2014 2013 2012 2014 2013 2012 2015

21

130%

72% 71%

48%

36% 38%

27%

31% 19%

23% 22%

72%

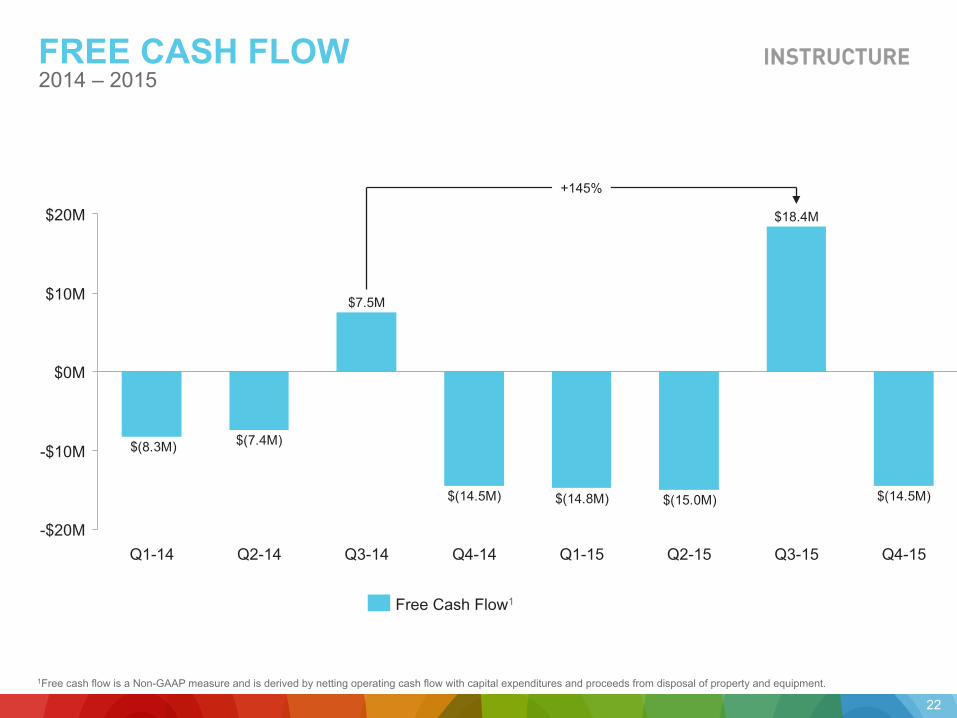

FREE CASH FLOW

Non-GAAP Gross Margin2 %

2014 – 2015

1Free cash flow is a Non-GAAP measure and is derived by netting operating cash flow with capital expenditures and proceeds from disposal of property and equipment.

$(14.5M)$(15.0M)$(14.8M)$(14.5M)

$(7.4M)$(8.3M)

$20M

$10M

$0M

-$10M

-$20M Q4-15 Q3-15

$18.4M

Q2-15 Q1-15 Q4-14 Q3-14

$7.5M

Q2-14 Q1-14

+145%

Free Cash Flow1

22

ENHANCED VISIBILITY INTO FUTURE PERIODS 2013 – 2015 Backlog1 Deferred Revenue

12/31/2015

$151M

12/31/2014

$113M

$73M

12/31/2013 12/31/2013 12/31/2015

$32M

12/31/2014

$49M

$19M

1Backlog represents future non-cancellable amounts to be invoiced under our agreements.

23

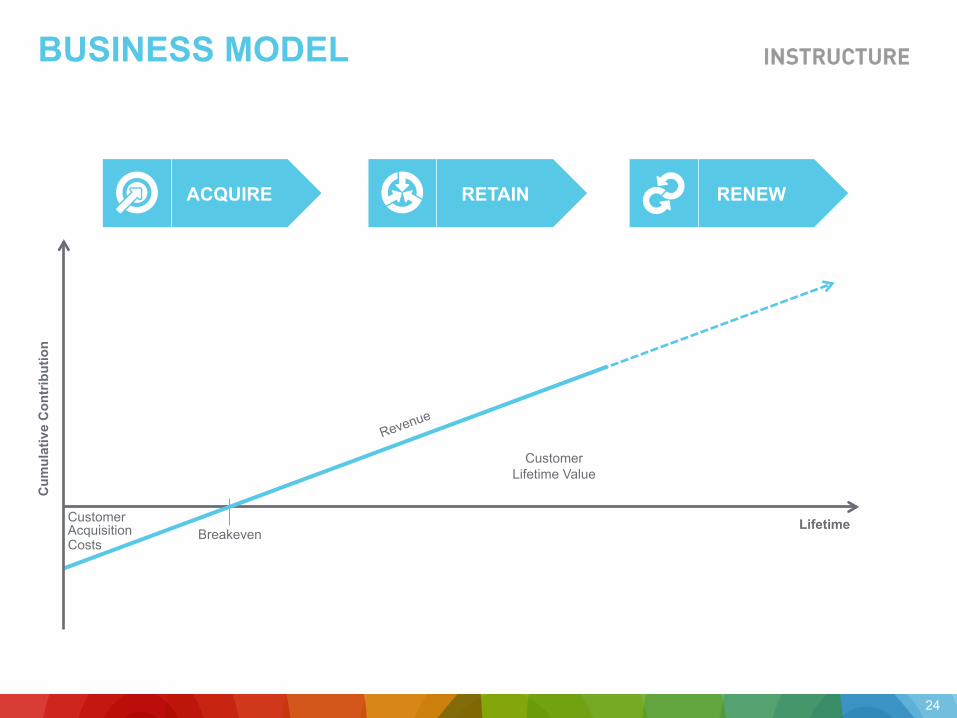

BUSINESS MODEL

Cum

ulat

ive

Con

trib

utio

n

24

Lifetime Customer Acquisition Costs

Breakeven

Customer Lifetime Value

ACQUIRE RETAIN RENEW

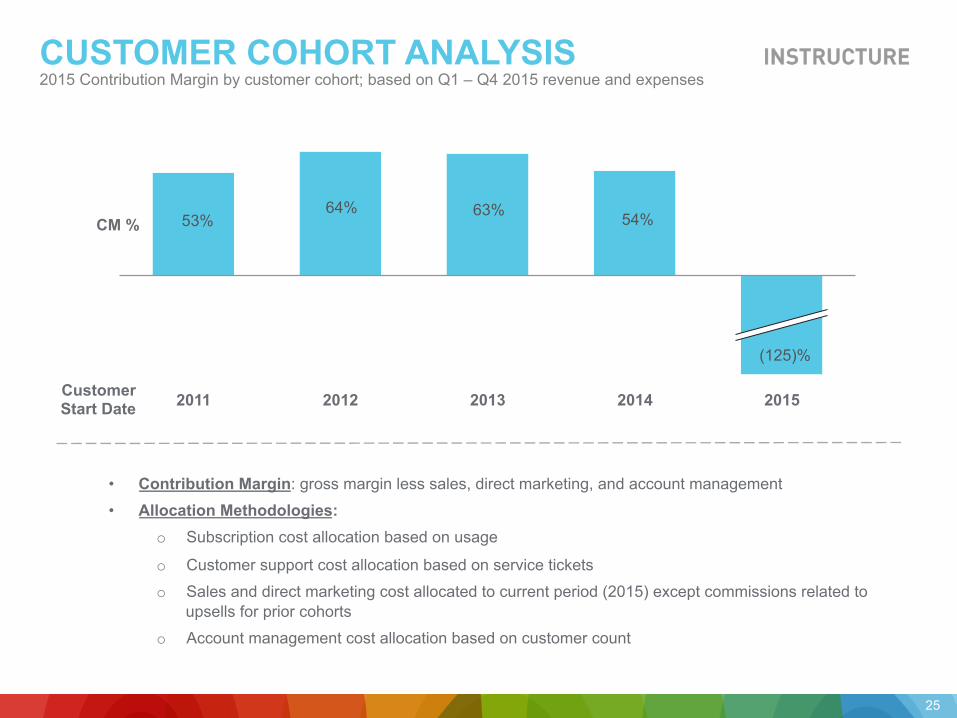

• Contribution Margin: gross margin less sales, direct marketing, and account management

• Allocation Methodologies: o Subscription cost allocation based on usage

o Customer support cost allocation based on service tickets

o Sales and direct marketing cost allocated to current period (2015) except commissions related to upsells for prior cohorts

o Account management cost allocation based on customer count

CUSTOMER COHORT ANALYSIS 2015 Contribution Margin by customer cohort; based on Q1 – Q4 2015 revenue and expenses

CM %

2015 2014 2013 2012 2011 Customer Start Date

25

53% 64% 63% 54%

(125)%

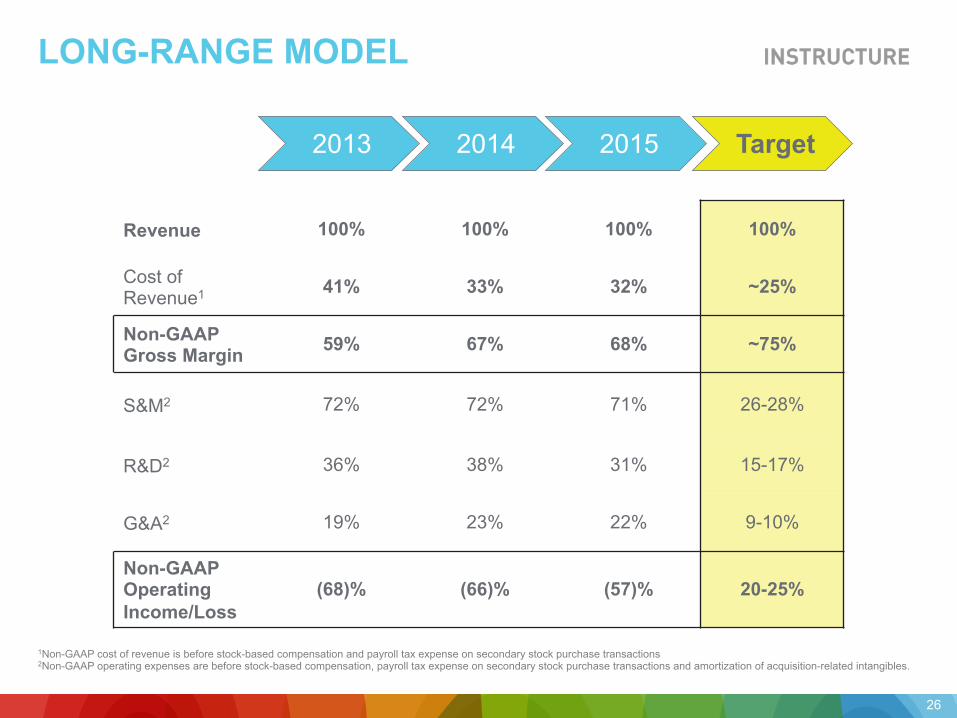

LONG-RANGE MODEL

Revenue 100% 100% 100% 100%

Cost of Revenue1 41% 33% 32% ~25%

Non-GAAP Gross Margin 59% 67% 68% ~75%

S&M2 72% 72% 71% 26-28%

R&D2 36% 38% 31% 15-17%

G&A2 19% 23% 22% 9-10%

Non-GAAP Operating Income/Loss

(68)% (66)% (57)% 20-25%

2013 2014 2015 Target

1Non-GAAP cost of revenue is before stock-based compensation and payroll tax expense on secondary stock purchase transactions 2Non-GAAP operating expenses are before stock-based compensation, payroll tax expense on secondary stock purchase transactions and amortization of acquisition-related intangibles.

26

INVESTMENT HIGHLIGHTS

Market Ripe for Disruption

Rapid and Widespread Customer Adoption

Substantial Market Opportunity

Native, Cloud-Based Platform

Focused on User-Experience and Simplicity

Solid Revenue Growth

Enhanced Visibility Through Multi-Year Contracts

27

APPENDIX

29

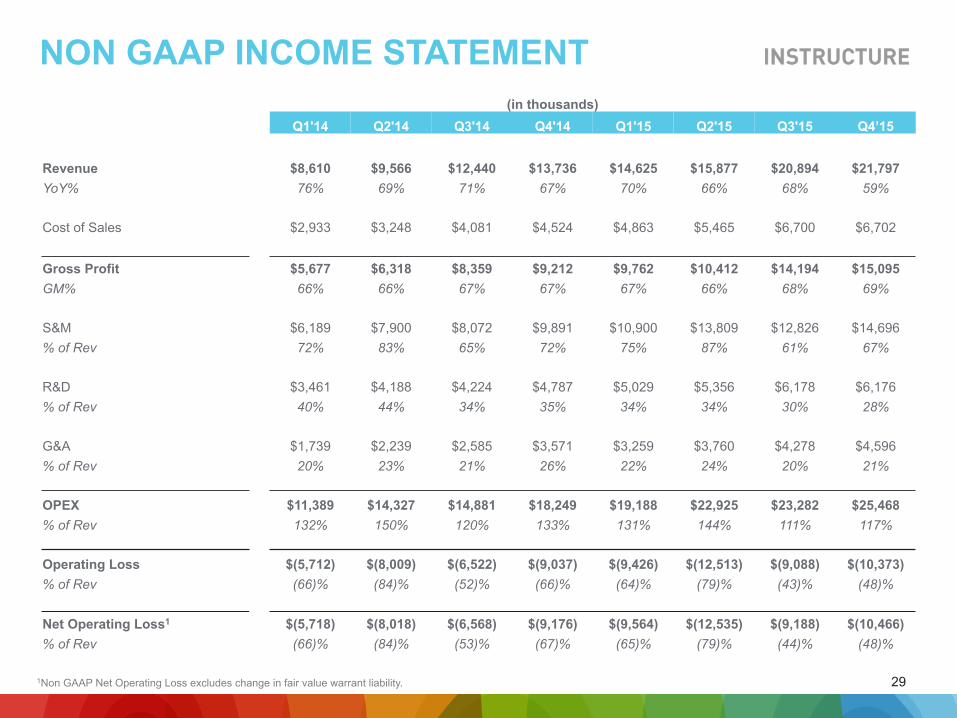

(in thousands) Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4’15

Revenue $8,610 $9,566 $12,440 $13,736 $14,625 $15,877 $20,894 $21,797 YoY% 76% 69% 71% 67% 70% 66% 68% 59%

Cost of Sales $2,933 $3,248 $4,081 $4,524 $4,863 $5,465 $6,700 $6,702

Gross Profit $5,677 $6,318 $8,359 $9,212 $9,762 $10,412 $14,194 $15,095 GM% 66% 66% 67% 67% 67% 66% 68% 69%

S&M $6,189 $7,900 $8,072 $9,891 $10,900 $13,809 $12,826 $14,696 % of Rev 72% 83% 65% 72% 75% 87% 61% 67%

R&D $3,461 $4,188 $4,224 $4,787 $5,029 $5,356 $6,178 $6,176 % of Rev 40% 44% 34% 35% 34% 34% 30% 28%

G&A $1,739 $2,239 $2,585 $3,571 $3,259 $3,760 $4,278 $4,596 % of Rev 20% 23% 21% 26% 22% 24% 20% 21%

OPEX $11,389 $14,327 $14,881 $18,249 $19,188 $22,925 $23,282 $25,468 % of Rev 132% 150% 120% 133% 131% 144% 111% 117%

Operating Loss $(5,712) $(8,009) $(6,522) $(9,037) $(9,426) $(12,513) $(9,088) $(10,373) % of Rev (66)% (84)% (52)% (66)% (64)% (79)% (43)% (48)%

Net Operating Loss1 $(5,718) $(8,018) $(6,568) $(9,176) $(9,564) $(12,535) $(9,188) $(10,466) % of Rev (66)% (84)% (53)% (67)% (65)% (79)% (44)% (48)%

NON GAAP INCOME STATEMENT

1Non GAAP Net Operating Loss excludes change in fair value warrant liability.

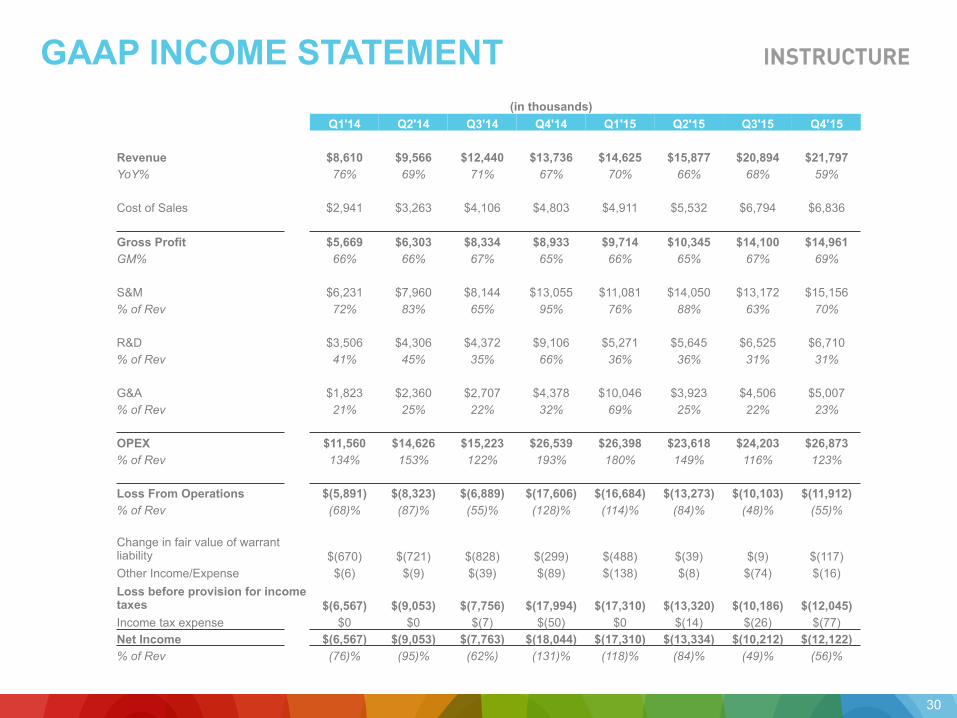

GAAP INCOME STATEMENT

(in thousands) Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3'15 Q4’15

Revenue $8,610 $9,566 $12,440 $13,736 $14,625 $15,877 $20,894 $21,797 YoY% 76% 69% 71% 67% 70% 66% 68% 59%

Cost of Sales $2,941 $3,263 $4,106 $4,803 $4,911 $5,532 $6,794 $6,836

Gross Profit $5,669 $6,303 $8,334 $8,933 $9,714 $10,345 $14,100 $14,961 GM% 66% 66% 67% 65% 66% 65% 67% 69%

S&M $6,231 $7,960 $8,144 $13,055 $11,081 $14,050 $13,172 $15,156 % of Rev 72% 83% 65% 95% 76% 88% 63% 70%

R&D $3,506 $4,306 $4,372 $9,106 $5,271 $5,645 $6,525 $6,710 % of Rev 41% 45% 35% 66% 36% 36% 31% 31%

G&A $1,823 $2,360 $2,707 $4,378 $10,046 $3,923 $4,506 $5,007 % of Rev 21% 25% 22% 32% 69% 25% 22% 23%

OPEX $11,560 $14,626 $15,223 $26,539 $26,398 $23,618 $24,203 $26,873 % of Rev 134% 153% 122% 193% 180% 149% 116% 123%

Loss From Operations $(5,891) $(8,323) $(6,889) $(17,606) $(16,684) $(13,273) $(10,103) $(11,912) % of Rev (68)% (87)% (55)% (128)% (114)% (84)% (48)% (55)%

Change in fair value of warrant liability $(670) $(721) $(828) $(299) $(488) $(39) $(9) $(117) Other Income/Expense $(6) $(9) $(39) $(89) $(138) $(8) $(74) $(16) Loss before provision for income taxes $(6,567) $(9,053) $(7,756) $(17,994) $(17,310) $(13,320) $(10,186) $(12,045) Income tax expense $0 $0 $(7) $(50) $0 $(14) $(26) $(77) Net Income $(6,567) $(9,053) $(7,763) $(18,044) $(17,310) $(13,334) $(10,212) $(12,122) % of Rev (76)% (95)% (62%) (131)% (118)% (84)% (49)% (56)%

30

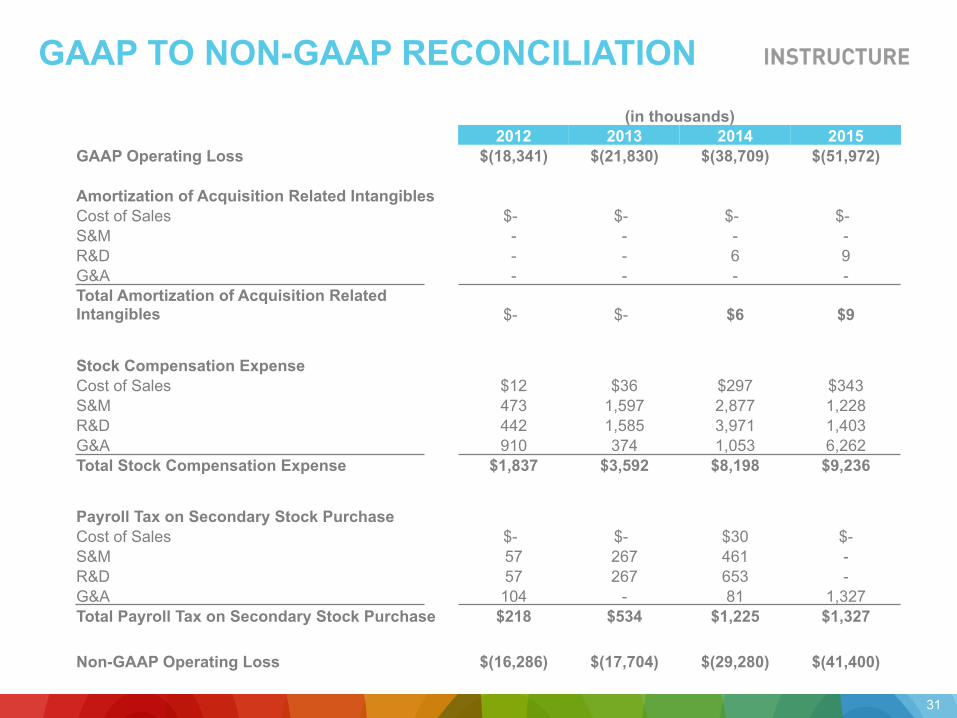

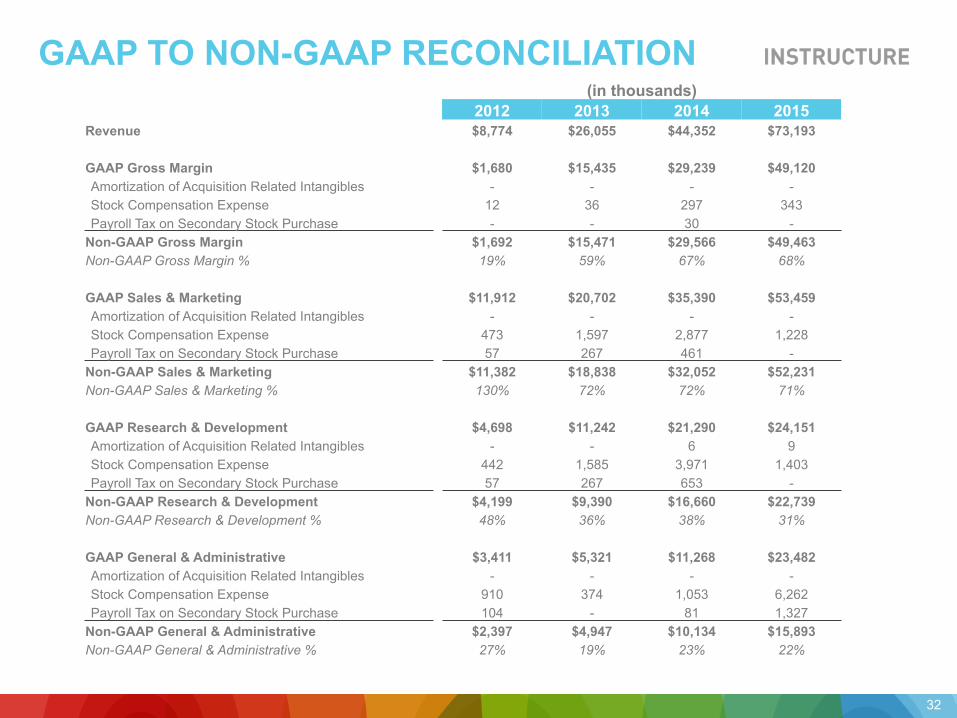

GAAP TO NON-GAAP RECONCILIATION (in thousands)

2012 2013 2014 2015

GAAP Operating Loss $(18,341) $(21,830) $(38,709) $(51,972)

Amortization of Acquisition Related Intangibles Cost of Sales $- $- $- $- S&M - - - - R&D - - 6 9 G&A - - - - Total Amortization of Acquisition Related Intangibles $- $- $6 $9

Stock Compensation Expense Cost of Sales $12 $36 $297 $343 S&M 473 1,597 2,877 1,228 R&D 442 1,585 3,971 1,403 G&A 910 374 1,053 6,262 Total Stock Compensation Expense $1,837 $3,592 $8,198 $9,236

Payroll Tax on Secondary Stock Purchase Cost of Sales $- $- $30 $- S&M 57 267 461 - R&D 57 267 653 - G&A 104 - 81 1,327 Total Payroll Tax on Secondary Stock Purchase $218 $534 $1,225 $1,327

Non-GAAP Operating Loss $(16,286) $(17,704) $(29,280) $(41,400)

31

GAAP TO NON-GAAP RECONCILIATION (in thousands)

2012 2013 2014 2015

Revenue $8,774 $26,055 $44,352 $73,193

GAAP Gross Margin $1,680 $15,435 $29,239 $49,120 Amortization of Acquisition Related Intangibles - - - - Stock Compensation Expense 12 36 297 343 Payroll Tax on Secondary Stock Purchase - - 30 -

Non-GAAP Gross Margin $1,692 $15,471 $29,566 $49,463 Non-GAAP Gross Margin % 19% 59% 67% 68%

GAAP Sales & Marketing $11,912 $20,702 $35,390 $53,459 Amortization of Acquisition Related Intangibles - - - - Stock Compensation Expense 473 1,597 2,877 1,228 Payroll Tax on Secondary Stock Purchase 57 267 461 -

Non-GAAP Sales & Marketing $11,382 $18,838 $32,052 $52,231 Non-GAAP Sales & Marketing % 130% 72% 72% 71%

GAAP Research & Development $4,698 $11,242 $21,290 $24,151 Amortization of Acquisition Related Intangibles - - 6 9 Stock Compensation Expense 442 1,585 3,971 1,403 Payroll Tax on Secondary Stock Purchase 57 267 653 -

Non-GAAP Research & Development $4,199 $9,390 $16,660 $22,739 Non-GAAP Research & Development % 48% 36% 38% 31%

GAAP General & Administrative $3,411 $5,321 $11,268 $23,482 Amortization of Acquisition Related Intangibles - - - - Stock Compensation Expense 910 374 1,053 6,262 Payroll Tax on Secondary Stock Purchase 104 - 81 1,327

Non-GAAP General & Administrative $2,397 $4,947 $10,134 $15,893 Non-GAAP General & Administrative % 27% 19% 23% 22%

32

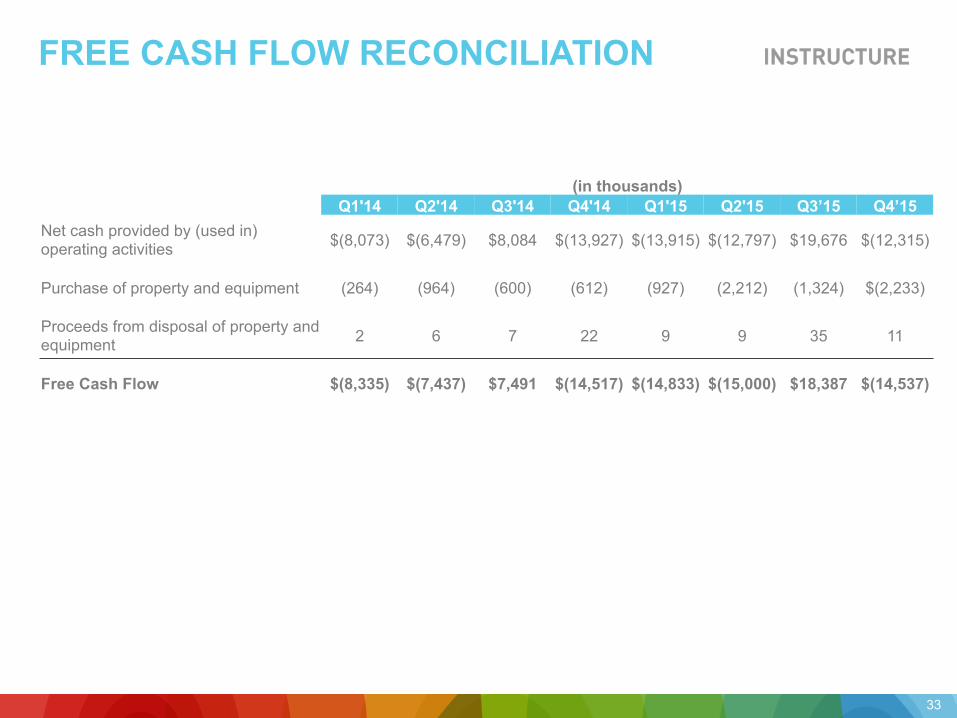

FREE CASH FLOW RECONCILIATION

33

(in thousands) Q1'14 Q2'14 Q3'14 Q4'14 Q1'15 Q2'15 Q3’15 Q4’15

Net cash provided by (used in) operating activities $(8,073) $(6,479) $8,084 $(13,927) $(13,915) $(12,797) $19,676 $(12,315)

Purchase of property and equipment (264) (964) (600) (612) (927) (2,212) (1,324) $(2,233)

Proceeds from disposal of property and equipment 2 6 7 22 9 9 35 11

Free Cash Flow $(8,335) $(7,437) $7,491 $(14,517) $(14,833) $(15,000) $18,387 $(14,537)