Institutions and Markets Economics 71a Spring 2005 Gitman/Joehnk Chapter 2 Lecture notes 3.

50

Institutions and Markets Economics 71a Spring 2005 Gitman/Joehnk Chapter 2 Lecture notes 3

-

date post

20-Dec-2015 -

Category

Documents

-

view

217 -

download

0

Transcript of Institutions and Markets Economics 71a Spring 2005 Gitman/Joehnk Chapter 2 Lecture notes 3.

Institutions and Markets

Economics 71a

Spring 2005

Gitman/Joehnk Chapter 2

Lecture notes 3

Goals

Financial institutionsFinancial marketsFinancial transactions

Institutions (the players)

1. Commercial banks

2. Mutual funds

3. Pension funds

4. Securities firms

5. Insurance companies

6. Others

1. Commercial Banks

Consumers Deposits/savings Lending/transactions

Consumer loans Home mortgages Checking accounts Credit cards Debit cards Foreign exchange Brokerage (recent)

1. Commercial Banks

Firms Cash management Lines of credit

Loan of varying magnitude Similar to credit card

Bank loans (term loans)

1. Commercial Banks

Intermediary roles Between lenders and borrowers Repackaging financial products

Regulatory environment Key aspect of monetary policy Federal Deposit Insurance Corporation

(FDIC) Federal Reserve System

2. Mutual Funds

Function Consumer investments -> Firms

Types Stock (invest in stock market portfolios) Money market (short term lending to firms) Bond Real Estate

2. Mutual Funds

Allow consumers to better diversifyGather and process investment

informationMajor industry in Boston

3. Pension Funds

Manage/invest employee savings/pension plans

Similar in spirit to mutual fundsHired by employer

4. Securities Firms

Investment banks/brokerage firms Issue stock and bonds

(IPO: Initial public offering)Facilitate trades in securitiesBanks versus Investment Banks

The repeal of Glass-Steagall (1999)

5. Insurance Companies

Insure individual and corporate risksReceive payments (insurance premia)Payout for losses New issues

Trading insurance policies Derivatives High tech risk management

6. Other Institutions

Savings and loans Savings -> home mortgages

Credit unions Information and software services

Bloomberg Quicken Microsoft

Goals

Financial institutionsFinancial marketsFinancial transactions

Markets

Primary markets New issues (IPO’s, corporate and public

debt)Secondary markets

Trading old stuff In many cases most activity in secondary

Money and Capital Markets

Money markets Short term securities (1 year or less)

Capital markets Longer term

Money Market Securities

Treasury bills U.S. government debt Short term (less than 1 year)

Commercial paper Short term corporate borrowing

Discount pricing Buy for $10, get paid $11 in future No interest payments

Capital Market Securities

Bonds (longer term borrowing) U.S. Treasury Municipal (tax free) Corporate More later

Capital Market Securities

Stocks Common stock Preferred stock International More later

Primary Market

Initial public offering (IPO) Initial sale of stock or bondLate 1990’s boom

IPO Timing

Private firm Negotiations between shareholders and other

initial investors (Venture Capital) Find investment bank to handle IPO

Prospectus filed with Securities and Exchange Commission

Red Herring : Version of prospectus for initial investors

Quiet period: filing to 1 month after IPO Restrictions on public information releases

Investment Banks

Originating investment bank Underwriting syndicate

Insures shares will be purchased Selling group How do people get paid?

Underwriters pay IPO firm ($15/share) Sell to selling group ($16/share) Sell to investors ($17/share) Scandals and IPO prices

Trading and Secondary Markets

Stock marketsBond marketsDerivativesForeign Exchange

U.S. Stock Markets

New York Stock Exchange (NYSE)National Association of Securities

Dealers Automated Quotation (Nasdaq) American Stock Exchange (AMEX)

Continuous Trading

Market types Specialist Electronic dealer Open outcry Over the counter

NASDAQ Upstairs (negotiated) ECN (electronic crossing network)

ECN’s: Electronic Crossing Networks

Internet based trade networks Customers can meet directly (no broker) Used mostly by professional money

managers Advantage: fewer intermediaries Disadvantage: less liquidity

(Fewer people to trade with)

Fastest growing markets

Other Markets

Futures/OptionsForeign Exchange

Spot versus forwardBond

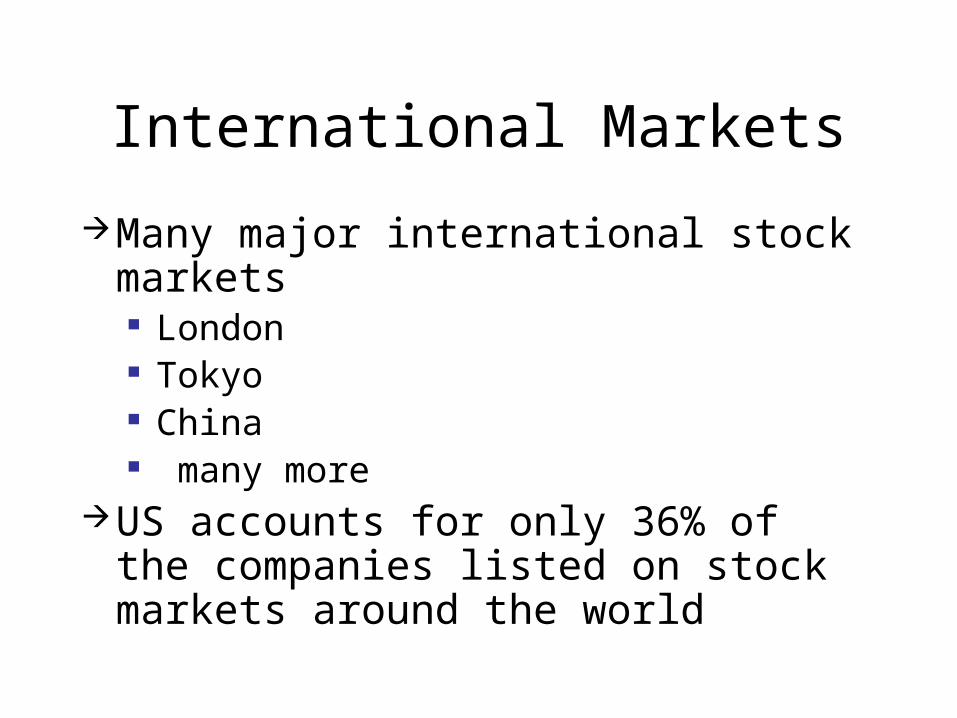

International Markets

Many major international stock markets London Tokyo China many more

US accounts for only 36% of the companies listed on stock markets around the world

Why Should U.S Investors Care?

DiversificationPerformance Industries

How Can U.S. Investors Invest Globally?

Multinational firms Microsoft Ford

Mutual funds Direct purchases

US securities/foreign firms (Yankee Bonds) American deposit receipts (ADR’s) WEBS (World Equity Benchmarks)

International Risks

Macroeconomic risksPolitical risksExchange rate risks

Trading Hours

Most U.S. stock markets 9:30-4:00

Extended hours on electronic trading networks

“After hours trading” International markets (local times) Foreign exchange markets (24 hours) Hours increasing : toward a 24 hour market

Market Regulation

Securities laws protect investors Federal and state laws

Securities and exchange commission (SEC): established in 1934

Important laws Securities act of 1933 (IPO rules) Insider trading and fraud act of 1988 Sarbanes-Oxley act of 2002

Tighter controls on accounting information

Goals

Financial institutionsFinancial marketsFinancial transactions

Long Purchase

Straight purchase of a securitySpeculate that price will increase

Buy at 100 Sell at 110 10% return

Margin Purchase

“Buying on margin”Borrow money to buy stockBuy at 75% margin

75% of money in investment is yours 25% is borrowed from broker or bank

Purchase $100 of stock at 75% margin You put in $75, and you borrow $25

Basic Margin Formula

€

Margin =Total value −Borrowed funds

Total value

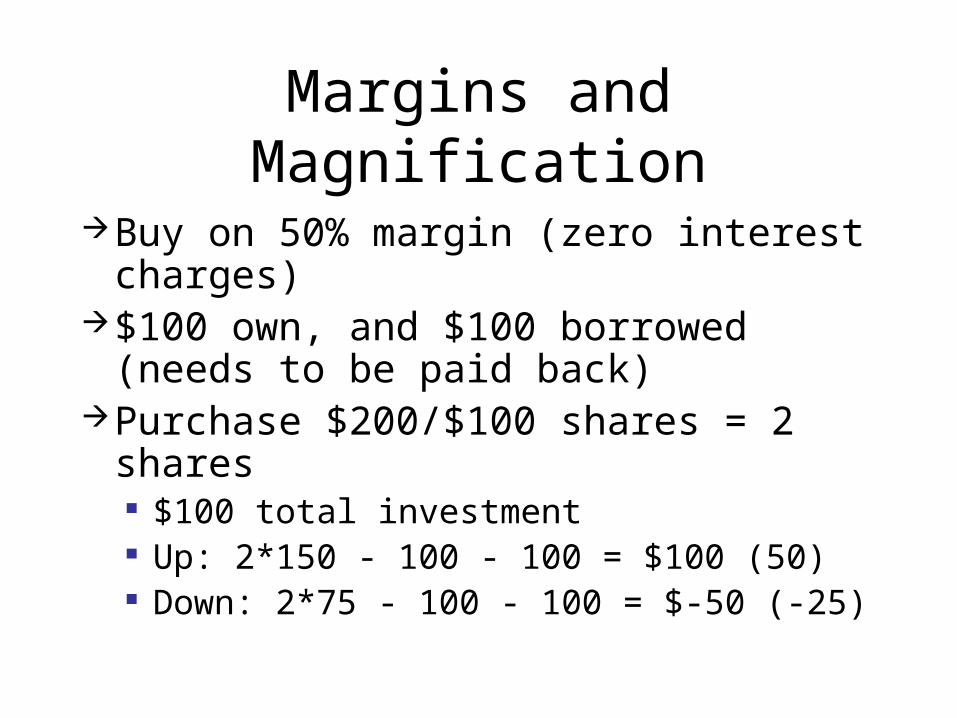

Margins and Magnification

Example stock: Price = $100 Up: Price = $150 Down: Price = $75

If you purchased with your own money $100 total investment Up: + $50 Down: - $25

Margins and Magnification

Buy on 50% margin (zero interest charges)

$100 own, and $100 borrowed (needs to be paid back)

Purchase $200/$100 shares = 2 shares $100 total investment Up: 2*150 - 100 - 100 = $100 (50) Down: 2*75 - 100 - 100 = $-50 (-25)

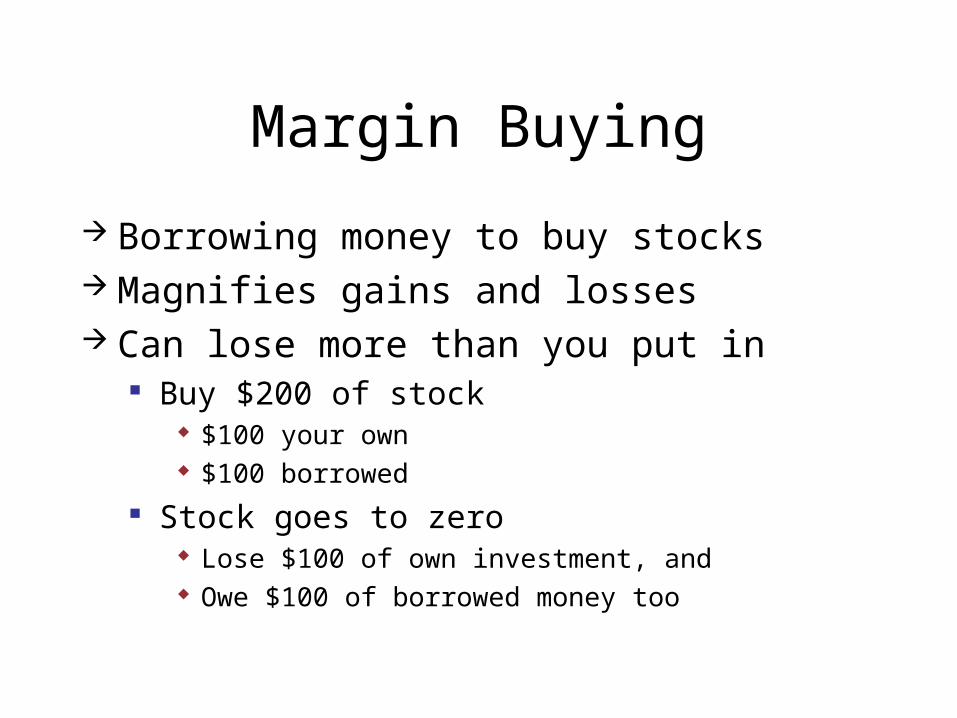

Margin Buying

Borrowing money to buy stocks Magnifies gains and losses Can lose more than you put in

Buy $200 of stock $100 your own $100 borrowed

Stock goes to zero Lose $100 of own investment, and Owe $100 of borrowed money too

Maintenance Margins

Margin required for investor to maintain If margin falls below this level investors

must add more of their own money“Margin call”Common margin call

Prices fall Margin rises Investor needs to come up with more funds

Margin Requirements

Common stock: 50%Bonds: 50%Options: 20% stock valueFutures: 2-10% of the contract value

Short Sales

Holding negative stock Sell stock you don’t have (borrow) Buy it back later Pay dividends yourself in between

Key issue Make money on a price fall Lose money on a rise

Betting against a stock

The Mechanics of a Short

Tell broker you want to sell 100 shares of IBM short (price = $50)

Broker “borrows” shares of 100 shares of IBM owned by another client

Sells it to someone for 50*100=5000, and pays this to you

You must keep this amount on account with broker

When dividends are to be paid, you pay broker, and broker pays the other client

The Mechanics of a Short

IBM goes down to $40 per share You “buy” your 100 shares to take you back to zero,

pay broker 40*100=4000. Broker buys at market, and puts the shares back in

the other person’s account You make 5000-4000 = 1000 (less dividends) Make money when price falls Lose money when price rises

The Mechanics of a Short

IBM goes up to $60 per share You “buy” your 100 shares to take you back to zero,

pay broker 60*100=6000. Broker buys at market, and puts the shares back in

the other person’s account You lose 5000-6000 = -1000 (less dividends)

Margins and Shorts

Broker requires additional funds to cover possible losses

Fraction of additional sale amount Example

Sell $5000 worth of stock at 60% margin Need to keep 0.6*5000 = 3000 on account with the

broker Maintain fraction of value of the stock in this account When the price goes up, need to increase this “Margin call”

Oddities About Shorts

Can lose unbounded amounts of money Normally only lose what you put in With short price can go up forever, and your losses keep

increasing

Also, broker can get in trouble if you default Other customer could lose original shares Often insured for this

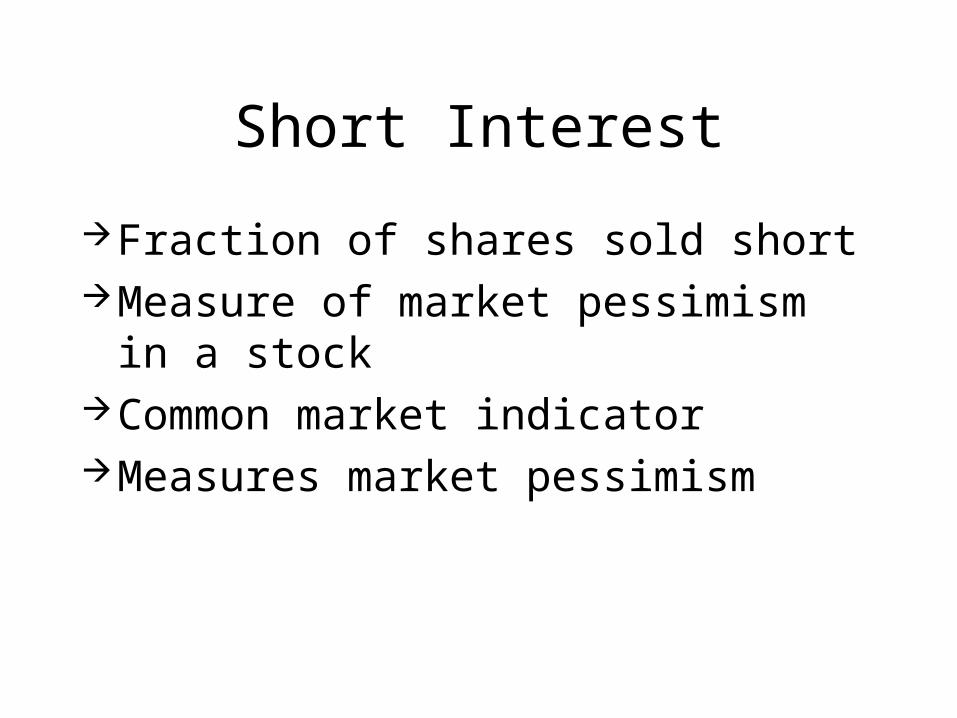

Short Interest

Fraction of shares sold shortMeasure of market pessimism in a

stockCommon market indicatorMeasures market pessimism

Squeeze Play

Assume Microsoft has a large number of short sellers

Price starts to rise Short sellers losing money Get nervous Buy stock to close out their short positions Prices rise more, more buying .. (etc. etc)

Goals

Financial institutionsFinancial marketsFinancial transactions