Institutional Presentation 1H10 - RI Mobileir.bmfbovespa.com.br/enu/3502/Institutional Presentation...

40

Institutional Presentation First Half of 2010 Institutional Presentation

Transcript of Institutional Presentation 1H10 - RI Mobileir.bmfbovespa.com.br/enu/3502/Institutional Presentation...

Institutional Presentation

First Half of 2010

Institutional Presentation

1. CETIP’s Investment Highlights

2. New Initiatives

3. CETIP’s Financial Highlights

Index

2

3. CETIP’s Financial Highlights

4. Appendix

1. CETIP’s Investment Highlights

3

Dominant position in a rapidly expanding market

Diversified and vertically integrated model

CETIP is the largest registration, depository and trading platform of fixed income and

OTC derivatives in Latin America

CETIP’s Highlights

Strong

Position

Business

4

Diversified and vertically integrated model

Superior growth profile

Experienced management team and high standards of governance

Resilient and predictable cash generative business with low execution risk

Business

Model

Growth

Profile

Management

Resilience

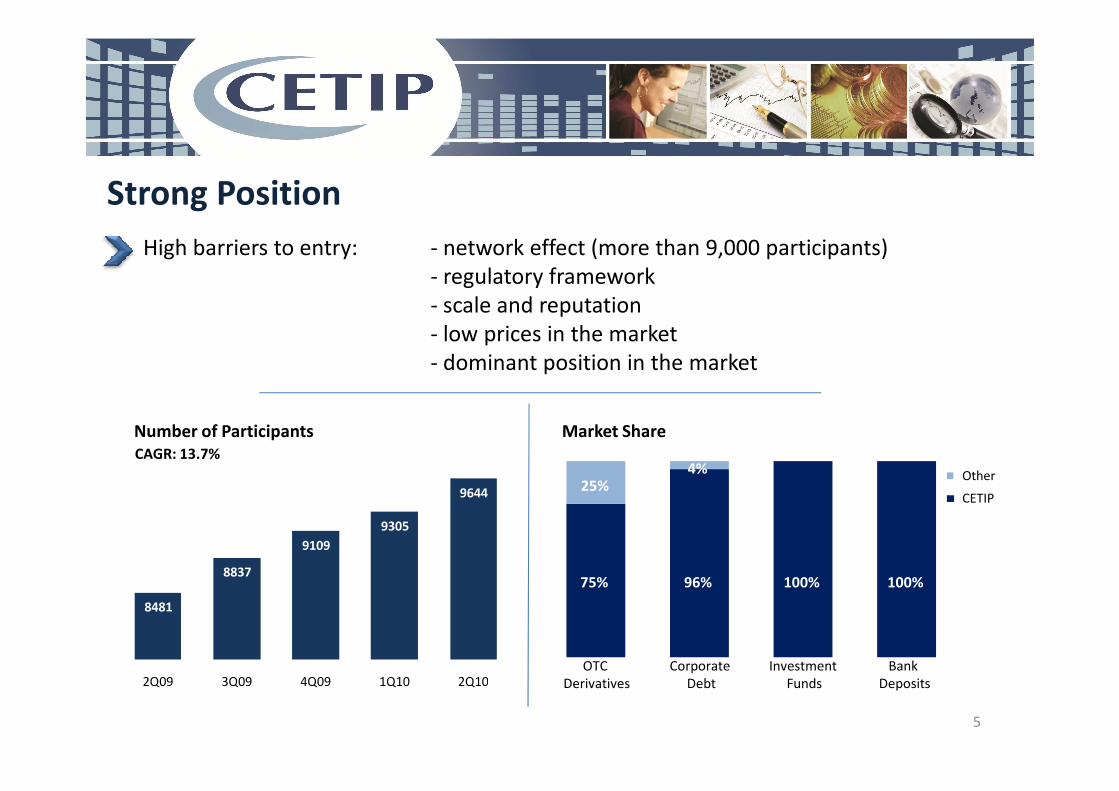

High barriers to entry: - network effect (more than 9,000 participants)

- regulatory framework

- scale and reputation

- low prices in the market

- dominant position in the market

Strong Position

8481

8837

9109

9305

9644

2Q09 3Q09 4Q09 1Q10 2Q10

5

Number of Participants

CAGR: 13.7%

75% 96% 100% 100%

25%4%

OTC

Derivatives

Corporate

Debt

Investment

Funds

Bank

Deposits

CETIP

Other

Market Share

Registration - Fixed income instruments

Financial Institutions

- CDs, IDs, others

- Loans participants (CCBs)

- Real estate financing (CCI, LCI, others)

- Agribusiness financing (LCA, CCA, others)

- Export financing

- Others

Corporations

- Corporate Bonds, Debentures, Commercial

Custody Transactions

Business ModelWe derive our revenues from acting as a registration,

custodian/depository and settlement agent for all securities under our

care, with over 50 asset classes, primarily in fixed income, such as

interbank and time deposits, corporate bonds, some specialty

government bonds, mutual funds, and finally over the counter

derivatives.

6

- Corporate Bonds, Debentures, Commercial

Papers

- OTC DerivativesCustody- Debentures

- Quota of Funds

- Other assets held in custody

Transactions (custody services)- Management of Corporate

Events

Monthly

Utilization- Connectivity Fee26%*

22%* 14%*25%*

(*) % of revenue (2Q10)

Others- CIP services

13%*

Vertically Integrated Model

Business ModelDiversified Revenue Drivers

Registration

Fixed Income Volume %/volume R$

OTC Derivatives Quantity R$/contract

Custody

Debentures Average Volume %/volume R$

Quota of Funds Average Volume %/volume R$

Registration

Matching

Confirmation

Risk ManagementElectronic

7

Vertical integration driven by regulatory zeal

Rest of the world heading this way

Quota of Funds Average Volume %/volume R$

End Users Quantity R$/customer

Transactions Quantity R$/transaction

Monthly Utilization Quantity R$/customer/scale

Others Quantity R$/fund transfer

Risk Management

Collateral

Management

SettlementDepository/

Custody

Electronic

Trading

CETIPNet

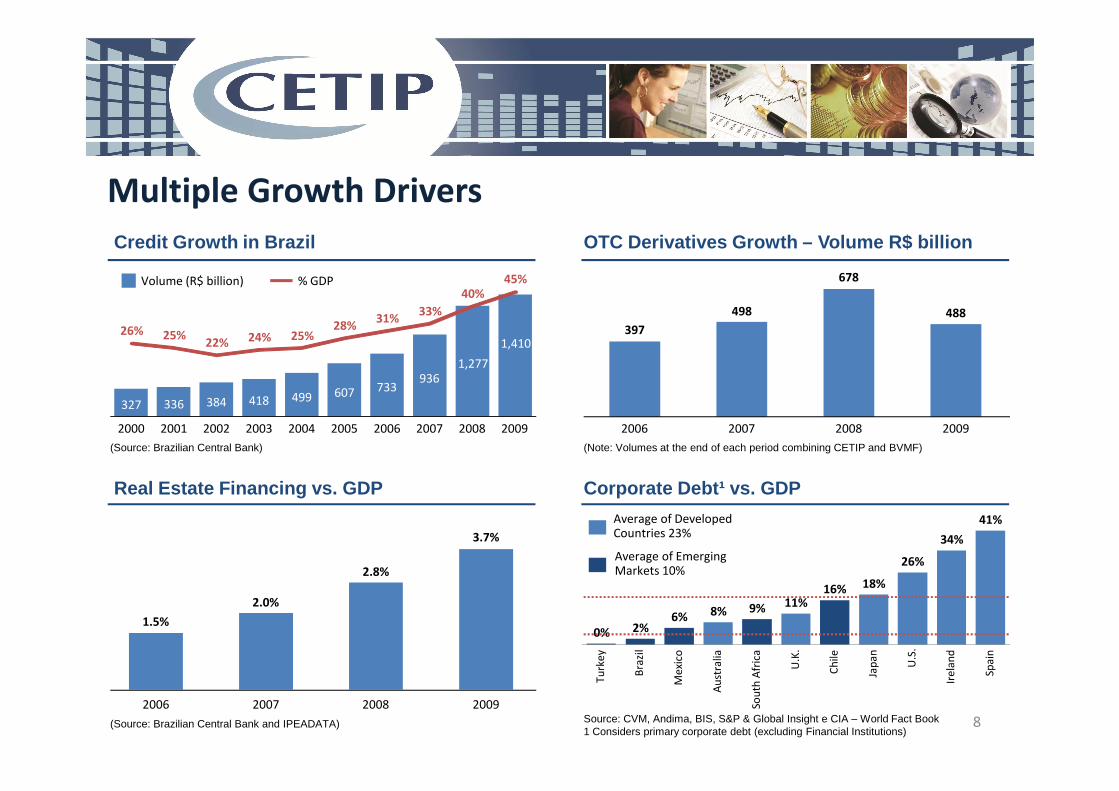

384 418 499 607 733936

1,277

1,41026% 25%

22% 24% 25%28%

31%33%

40%45%

Multiple Growth Drivers

Credit Growth in Brazil OTC Derivatives Growth – Volume R$ billion

397

498

678

488

Volume (R$ billion) % GDP

327 336 384 418 499 607

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

(Note: Volumes at the end of each period combining CETIP and BVMF)(Source: Brazilian Central Bank)

(Source: Brazilian Central Bank and IPEADATA)

Average of Developed Countries 23%

Average of Emerging Markets 10%

Source: CVM, Andima, BIS, S&P & Global Insight e CIA – World Fact Book1 Considers primary corporate debt (excluding Financial Institutions)

8

Real Estate Financing vs. GDP Corporate Debt¹ vs. GDP

2006 2007 2008 2009

1.5%

2.0%

2.8%

3.7%

2006 2007 2008 2009

0% 2%6% 8% 9% 11%

16% 18%

26%

34%

41%

Tu

rke

y

Bra

zil

Me

xico

Au

stra

lia

Sou

th A

fric

a

U.K

.

Ch

ile

Jap

an

U.S

.

Ire

lan

d

Spa

in

18.3

45.1

Growth DriversAnnual Volume of OTC DerivativesTrading per Country ¹

Benefits from Multiple Growth Drivers – OTC Derivatives

• Increased usage of fixed rate debt

• Lengthening of tenors

Multiple of Country’s GDP

9

0.4

2.81.6

4.15.1

7.0

13.2 13.6 14.0

18.3

Bra

zil'

07

Bra

zil '

12

Tur

key

Mex

ico

Spa

in

Italy

Ger

man

y

Japa

n

S.A

fric

a

US

A

Aus

tral

ia

• Lengthening of tenors

• Progressive regulatory environment

• Increased variety of underlying assets and sophistication of managers and investors

• Development of collaterization and tools for fair value calculation

Source: BIS, Global Insight, Oliver Wyman analysis1 Volumes for other countries in 2007

Emerging markets average 5x

Developed countries average 17x

Volume CAGR

07-12E: 60%

Raising demand for Real Estate Sector Funding

35

53

83

117

25

38

62

3553

83

117

150

188

215

254

Net Savings vs. Real Estate Sector Funding Savings Balance vs. Real Estate Sector Funding(Source: Brazilian Central Bank and ABECIP)(In R$ billion)

Real estate sector funding Net savings Real estate sector funding Savings balance

(Source: Brazilian Central Bank and ABECIP)(In R$ billion)

10

-2

Dec/06 Dec/07 Dec/08 Dec/09

35

Dec/06 Dec/07 Dec/08 Dec/09

2.22.9

7.2

10.6

2.012.64

8.29

12.7

Dec/06 Dec/07 Dec/08 Dec/09

CRI CCI

Dec/06 Dec/07 Dec/08 Dec/09

Savings Accounts LCI/LH CRI

CRI & CCI Volumes Sources of Funding Real Estate Sector(Source: CETIP. Volumes at the end of each period)(In R$ billion)

(Source: Brazilian Central Bank , ABECIP and CETIP )(In R$ billion)

CRI CCI

Real Estate sector is funded, essentially, by savings accounts. Net amount of funds outstanding in

savings accounts is growing less than the Real Estate funding demand.

In 2009 CETIP committed to the highest corporate governance standards with the Novo

Mercado listing

CETIP is created

as a non-for-

profit

Agreement with

ANDIMA to

Advent becomes

a shareholder

with 32% stake

Novo Mercado

Listing

One class of shares

with voting rights

Experience and Corporate Governance

11

CETIP starts its

operations

profit

organization

1984 1986

ANDIMA to

operate SND

1988

Demutualization

process, creating

CETIP SA

2008

with 32% stake

2009 2009

with voting rights

CTIP3

Corporate GovernanceMain ExecutivesYears in Financial

Industry

Francisco Carlos Gomes (CFO)

Former CFO of Bovespa, created CBLC+ 33 years

Luiz Fernando Vendramini Fleury (CEO)

Former CEO of IBI / Redecard+ 19 years

-

Boards

Shareholders

Self Regulation

BoardBoard of Directors

Experience and Corporate Governance

12

Management

CommitteePricing Committee

Self Regulation

OfficerCEO

Former CFO of Bovespa, created CBLC

Carlos Eduardo Ratto Pereira (Commercial Director

and Product Development Director)

Formerly at BankBoston, Bank of America, Banco

Itaú and HSBC Bank

+ 17 years

Maurício Rebouças dos Santos (CTO)

Formerly at Mercabolsa (Portugal), ANDIMA (Selic

manager)

+ 24 years

Wagner Anacleto (COO)

Formerly at BM&FBovespa and CBLC+ 29 years

-

Committees

Executive

Bodies

BoardBoard of Directors

Compensation

Committee

Nominations

Committee

CFO and

Investor

Relations

Commercial and

Product

Development

Chief

Operations

Officer

Chief

Technology

Officer

Carlos Menezes (Self regulation Director)

Formerly at Unibanco and BPN Brasil Bank+ 27 years

2. New Initiatives

13

New Products Implemented

2003 - 2004 2005 - 2006 2007 - 2010

► CCI - real estate securities

► Bank deposits - multiple index

► NCE - export credit note

► CCE - export credit securities

► Export notes

► Agribusiness securities

► FIDIC - mutual funds for securitizations

► Cash flow swaps

► Collateralized interbank deposits

► Resetable swaps

► Collateral management for derivatives

► New modalities bank deposits

Continued Innovation to Sustain Our Advantage

► CCE - export credit securities

► Credit default swap

► Box contracts

► New modalities interbank deposits

► Flexible options – currencies

► CetipNet - request for quote functionality

► CetipNet - government bonds functionality

► CetipNet - auction functionality

► Non deliverable forward

► Cash flow swaps

► Portfolio netting

► Mutual funds primary distribution system

► New modalities interbank deposits

► CCB / CCCB - bank credit securities - new

system

► End user identification system

► CetipNet - single dealer functionality

► CetipNet - agribusiness securities

functionality

► Collateralized bank deposits

► Trading monitoring system

► New modalities bank deposits

► Real estate securities - new system

► Non deliverable commodities

► CetipNet - auction new functionalities

► CetipNet - new government securities

functionalities

► Standardized derivatives

► Back-office automation

► Business information

► Derivatives Carried out Abroad – DCE/ DCE-DP

► Credit Derivatives – DVE

► Letras Financeiras

► Collateral Management

► Time Deposits with Special Guarantee – DPGE

► Leasing Bills – LAM

14

2011e

... Q2 Q3 Q4 Q1 ...

Off-shore Derivatives

Equity Derivatives

2010e

Registration of Derivatives Carried out Abroad

2010e New Products

Equity Derivatives

Collateral Management

Bank Assets

Agreement with Clearstream to jointly

develop, promote and distribute collateral

management service for OTC Derivatives

Improvement of the Stock Options registration

procedure and implementation of Stock

Contracts without physical delivery

Implementation of registration module to

Certificados de Operações Estruturadas (COE)

15

(Pending on Brazilian Central Bank regulation)

Collateral Management

CETIP plans to develop a comprehensive collateral

New Initiatives

16

CETIP plans to develop a comprehensive collateral

management functionality to support OTC Derivatives as well

as to help Brazilian banks reduce their capital requirements

and improve process efficiency.

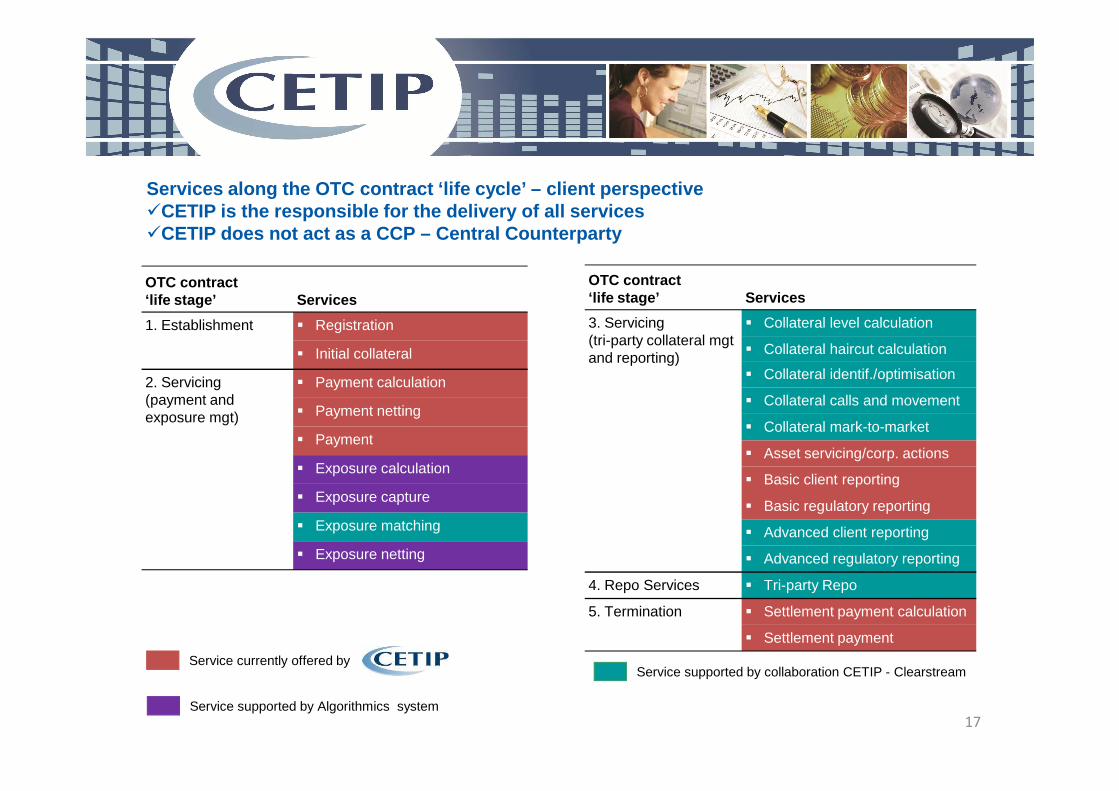

OTC contract‘life stage’ Services

1. Establishment � Registration

� Initial collateral

2. Servicing(payment and

� Payment calculation

OTC contract‘life stage’ Services

3. Servicing(tri-party collateral mgt and reporting)

� Collateral level calculation

� Collateral haircut calculation

� Collateral identif./optimisation

� Collateral calls and movement

Services along the OTC contract ‘life cycle’ – clien t perspective�CETIP is the responsible for the delivery of all se rvices�CETIP does not act as a CCP – Central Counterparty

17

Service currently offered by

(payment and exposure mgt) � Payment netting

� Payment

� Exposure calculation

� Exposure capture

� Exposure matching

� Exposure netting

� Collateral calls and movement

� Collateral mark-to-market

� Asset servicing/corp. actions

� Basic client reporting

� Basic regulatory reporting

� Advanced client reporting

� Advanced regulatory reporting

4. Repo Services � Tri-party Repo

5. Termination � Settlement payment calculation

� Settlement payment

Service supported by Algorithmics system

Service supported by collaboration CETIP - Clearstream

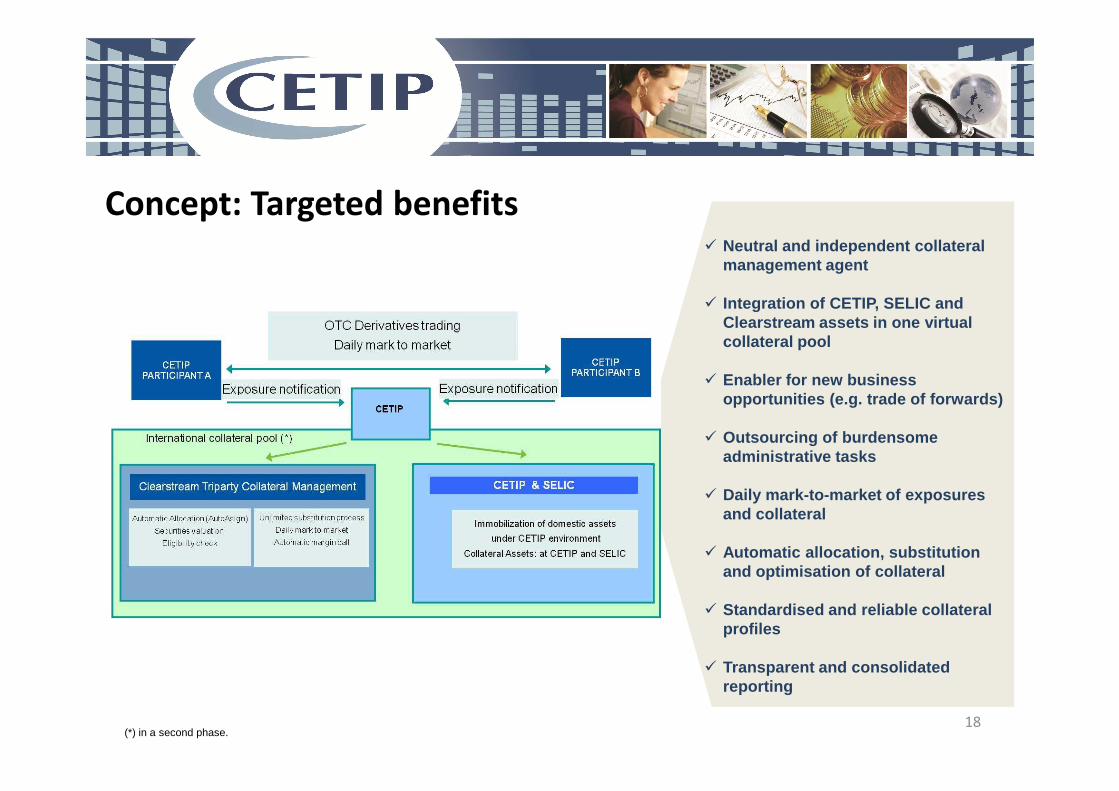

� Neutral and independent collateral management agent

� Integration of CETIP, SELIC and Clearstream assets in one virtual collateral pool

� Enabler for new business opportunities (e.g. trade of forwards)

Concept: Targeted benefits

18

opportunities (e.g. trade of forwards)

� Outsourcing of burdensome administrative tasks

� Daily mark-to-market of exposures and collateral

� Automatic allocation, substitution and optimisation of collateral

� Standardised and reliable collateral profiles

� Transparent and consolidated reporting

(*) in a second phase.

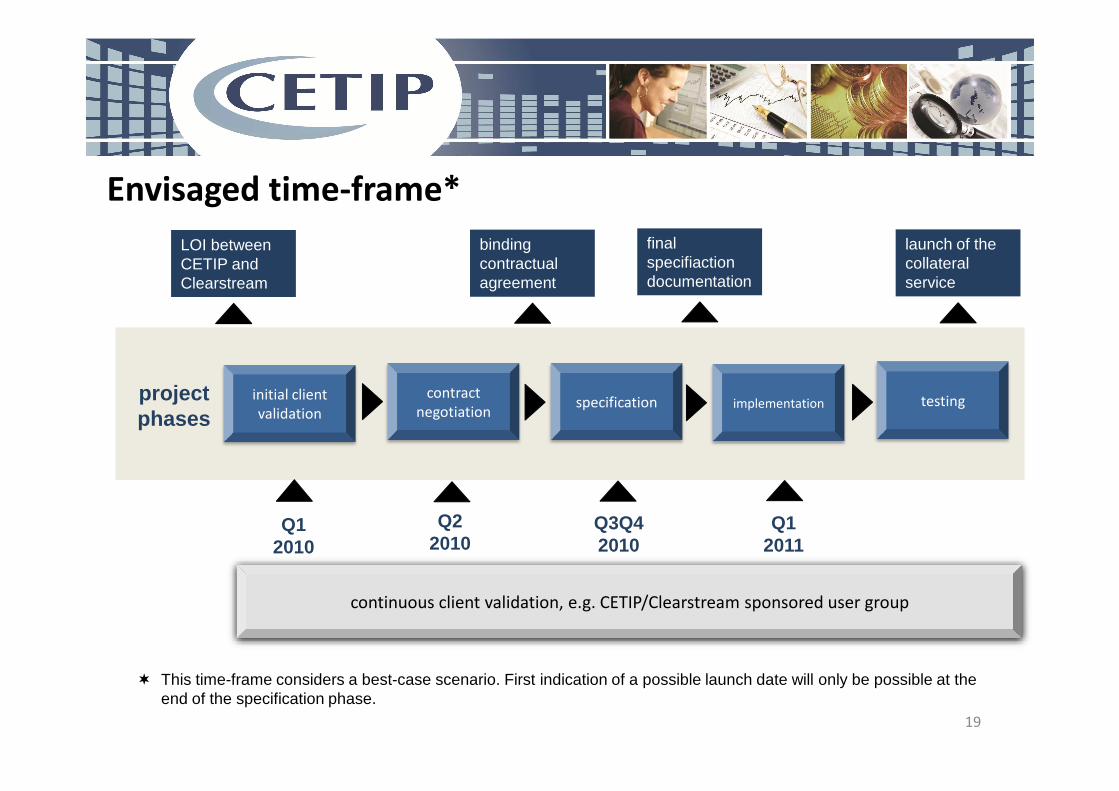

Envisaged time-frame*

project initial client

LOI between CETIP and Clearstream

contractspecification implementation testing

binding contractual agreement

final specifiactiondocumentation

launch of the collateral service

19

project phases

initial client

validation

Q1 2010

contract

negotiationspecification implementation testing

continuous client validation, e.g. CETIP/Clearstream sponsored user group

Q2 2010

Q3Q4 2010

Q12011

� This time-frame considers a best-case scenario. First indication of a possible launch date will only be possible at the end of the specification phase.

550

500

450

400

350

Peak over € 500 bn

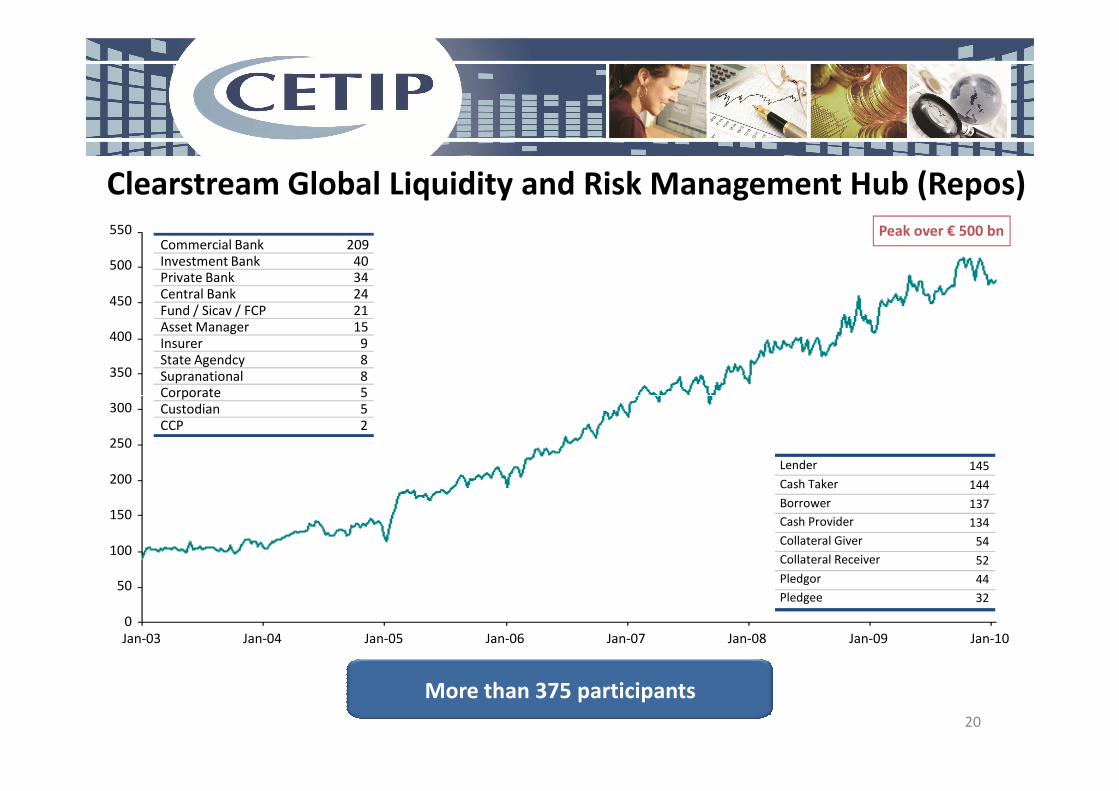

Clearstream Global Liquidity and Risk Management Hub (Repos)

Commercial Bank 209Investment Bank 40Private Bank 34Central Bank 24Fund / Sicav / FCP 21Asset Manager 15Insurer 9State Agendcy 8Supranational 8Corporate 5

300

250

200

150

100

50

0

Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09 Jan-10

20

More than 375 participants

Corporate 5Custodian 5CCP 2

Lender 145

Cash Taker 144

Borrower 137

Cash Provider 134

Collateral Giver 54

Collateral Receiver 52

Pledgor 44

Pledgee 32

3. CETIP’s Financial Highlights

21

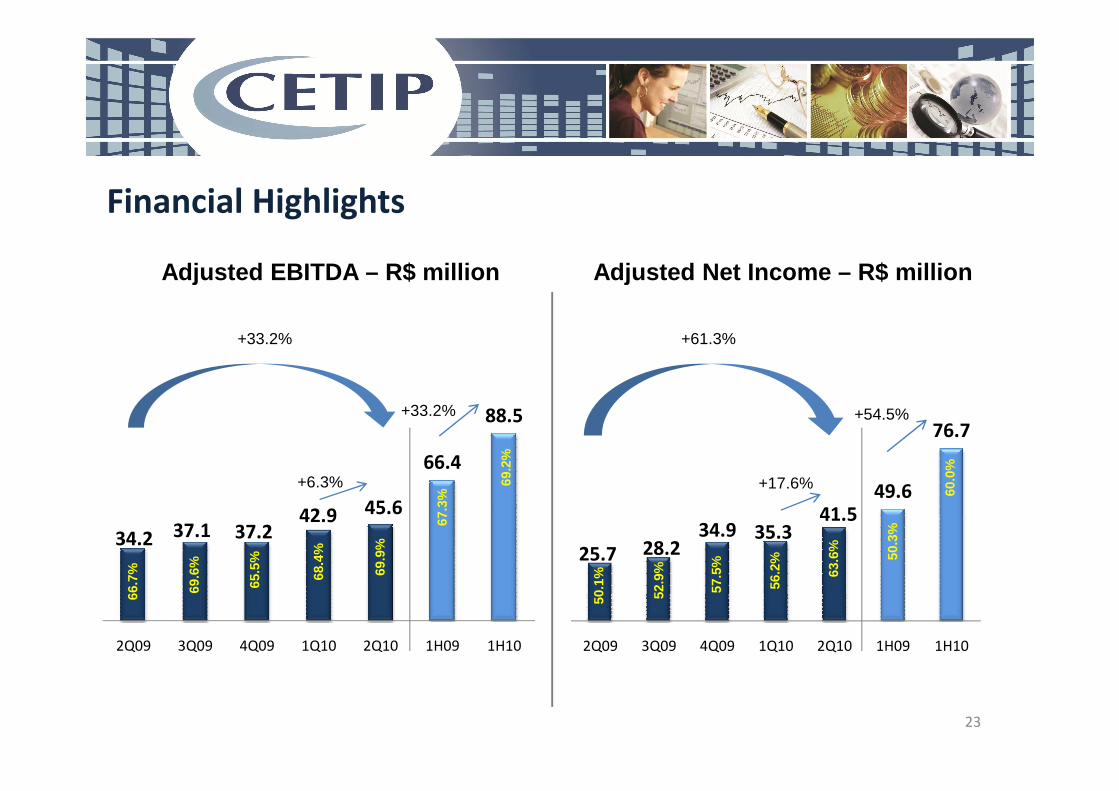

Financial Highlights

Net Revenues – R$ million Adjusted Operating Expenses – R$ million

127.9

+27.1% +6.9%

+29.6% +12.9%

22

65.251.3 53.4 56.8 62.7

98.7

127.9

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

21.119.8 19.0 22.3 21.4

37.742.5

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

+4.0% -1.2%

+29.6% +12.9%

Financial Highlights

Adjusted EBITDA – R$ million Adjusted Net Income – R$ million

+33.2% +61.3%

23

41.5

25.7 28.234.9 35.3

49.6

76.7

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

45.6

34.2 37.1 37.2 42.9

66.4

88.5

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

+6.3%

69.9

%

68.4

%

66.7

%

65.5

%

69.6

%

+17.6%

56.2

%

50.1

%

57.5

%

52.9

% 63.6

%

69.2

%

67.3

%

+33.2% +54.5%

50.3

%

60.0

%

Revenue Breakdown by Type (%) – R$ million

+3.6%

+26.6%

+29.6%

24

12% 13% 14% 12% 13% 12% 13%

29% 29% 27% 25% 25% 28% 25%

15% 15% 15%13% 14% 13% 13%

21% 22% 22%22% 22% 20% 22%

23% 21% 22%28% 26% 27% 27%

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

Other revenues

Monthly Utilization

Transactions

Custody

Registration

75.659.7 61.9 66.1 72.9 114.5 148.5

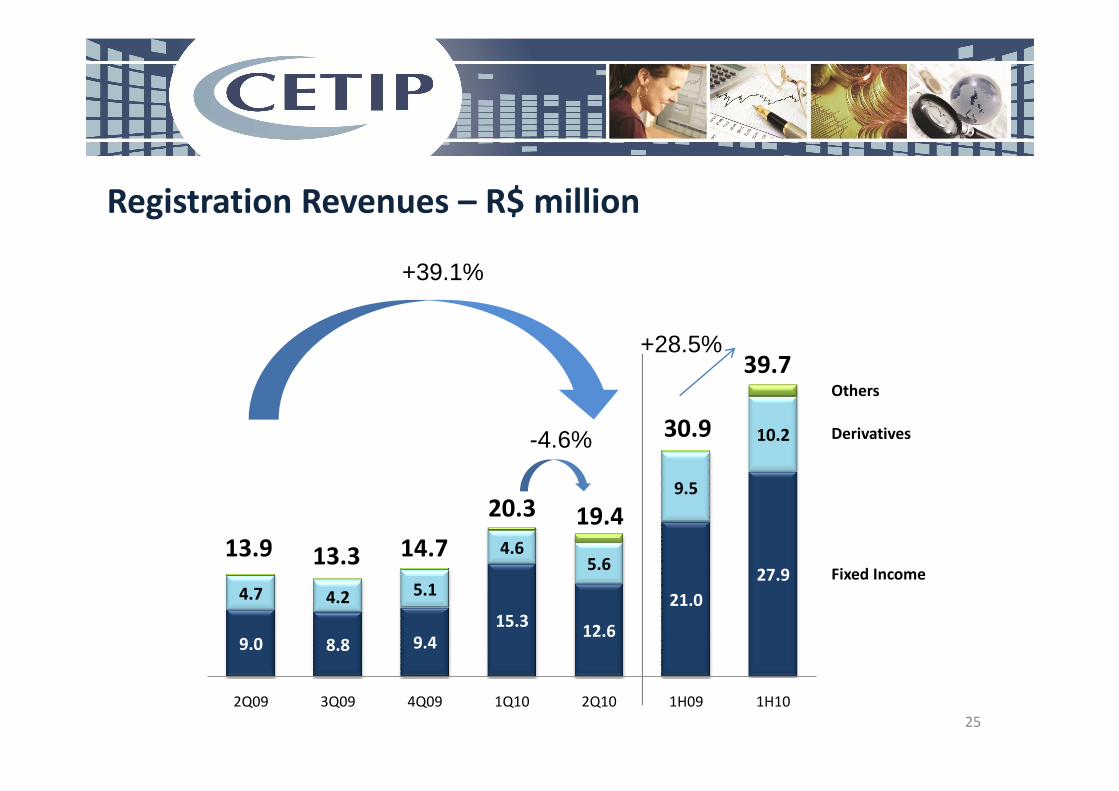

Registration Revenues – R$ million

Others

+39.1%

39.7+28.5%

25

Fixed Income

Derivatives

Others

9.0 8.8 9.4

15.312.6

21.0

27.94.7 4.2 5.1

4.65.6

9.5

10.2

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

19.4

13.9 13.3 14.7

20.3

-4.6% 30.9

Custody Revenues – R$ million

23.0

32.5

+7.3%

+33.9%

+41.4%

26

16.8

12.6 13.6 14.6 15.7

23.0

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

+7.3%

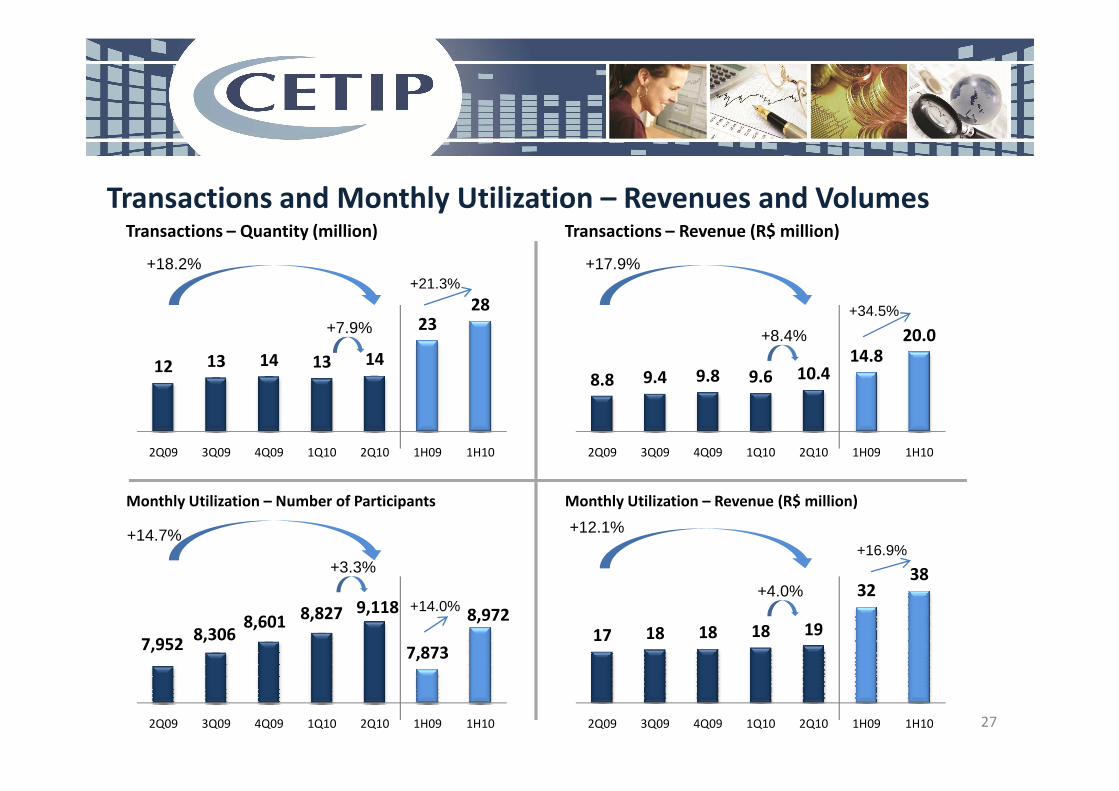

Transactions and Monthly Utilization – Revenues and Volumes

12 13 14 13 14

2328

Transactions – Quantity (million)

+18.2%

+7.9%

8.8 9.4 9.8 9.6 10.414.8

20.0

Transactions – Revenue (R$ million)

+17.9%

+8.4%

+21.3%

+34.5%

27

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10 2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

9,118

7,9528,306

8,601 8,827

7,873

8,972

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

Monthly Utilization – Number of Participants

+14.7%

+3.3%

17 18 18 18 19

3238

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

Monthly Utilization – Revenue (R$ million)

+12.1%

+4.0%+14.0%

+16.9%

CAPEX - % of Net Revenues

% NR 3.4% 5.0% 5.2% 5.0% 14.8%

16%

11%

6%

5% 15%6%

3%

26%7% 20%

10%4% 5% 8%

1%

3.4% 10.0%

R$ mm 1.7 2.7 2.9 3.1 9.6 3.3 12.8

28

21%

5%12%

63%

10%17%

23%

30% 59%

61%

22%

59%

26%

50%

34%

17% 4%

42%

6%

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

Product Development

Technology

Office Settlement

Platform Migration

Others

Other Highlights

0.3421

Adjusted Earnings per Share – R$

+59.8%

+53.2%

Shareholder Remuneration

Remuneration Deliberation Amount (R$mm)Gross amount per

Payment

29

Note: As provided in the bylaws, dividend and/or ISE payment policy corresponds to at least 25% of adjusted net income in accordance with Brazilian law.

0.1849

0.1157 0.12660.1560 0.1577

0.2233

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

+59.8%+17.3%

Remuneration Deliberation Amount (R$mm)Gross amount per

share (R$)Payment

1H09 ISE Board Meeting 08/26/09 6.88 0.030939 09/15/09

2H09 ISE Board Meeting 12/21/09 8.95 0.040025 01/13/10

2009 Dividend Board Meeting 03/10/10 50.78 0.226862 05/17/10

1H10 ISE Board Meeting 06/18/10 9.24 0.041207 07/12/10

Shareholder Base As of September 30, 2010

TOTAL SHARES: 226,014,250*

18% Advent

30

Outstanding options 5,704,659 shares

Potential future grants 3,970,807 shares

(*) Considers the capital increases in the period.

FEMCO: Federated Management Company; parent Company for Federated Kauffman Fund.

13% FEMCO

10% Itaú Unibanco

1% Santander

4% Bradesco

1% Board

Free Float 53%

12,45

16.35

25

30

35

14

16

18

Stock Performance

CTIP3 (R$) vs. Volume (R$ mm)(Oct 27, 2009 – Sep 17, 2010)

CTIP3 vs. IBOV vs. BVMF(Oct 27, 2009 – Sep 17, 2010)

26%

20%

130

140

12,45

0

5

10

15

20

25

0

2

4

6

8

10

12

29-Oct 14-Dec 1-Feb 17-Mar 30-Apr 14-Jun 27-Jul 8-Sep

Volume - R$ mm Price-R$

Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10

31Note: Financial volume in the first trading session amounted to R$260 million and in the second trading session, R$80 million.

6%

20%

80

90

100

110

120

IBOV CTIP3 BMFB

Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10

4. Appendix

32

DIs and CDBs - Volumes and Revenues

870 885701 814 756

1,992

1,569

DI – Volume (R$ billion)

7.75.3 4.8 4.9

11.413.5

19.1

DI – Revenue (R$ million)

-13.1%

-32.0%

+45.6%

-7.1%

-21.2% +41.8%

33

290 316 362 339398

618737

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10 2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

+17.2%

CDB – Volume (R$ billion)

+37.3%

3.22.4 2.5 2.9 2.7

5.25.9

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

CDB – Revenue (R$ million)+32.4%

+17.0%

+19.3%+13.1%

Swaps - Volume and Revenue

168-36.6%

SWAPS – Quantity (thousand)

5.1

7.0

SWAPS – Revenue (R$ million)

+19.7%

+22.2%

+37.4%-42.9%

34

7867 67

47 49

96

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

+5.8% 3.83.1 2.9

4.2

3.2

5.1

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

+19.7%

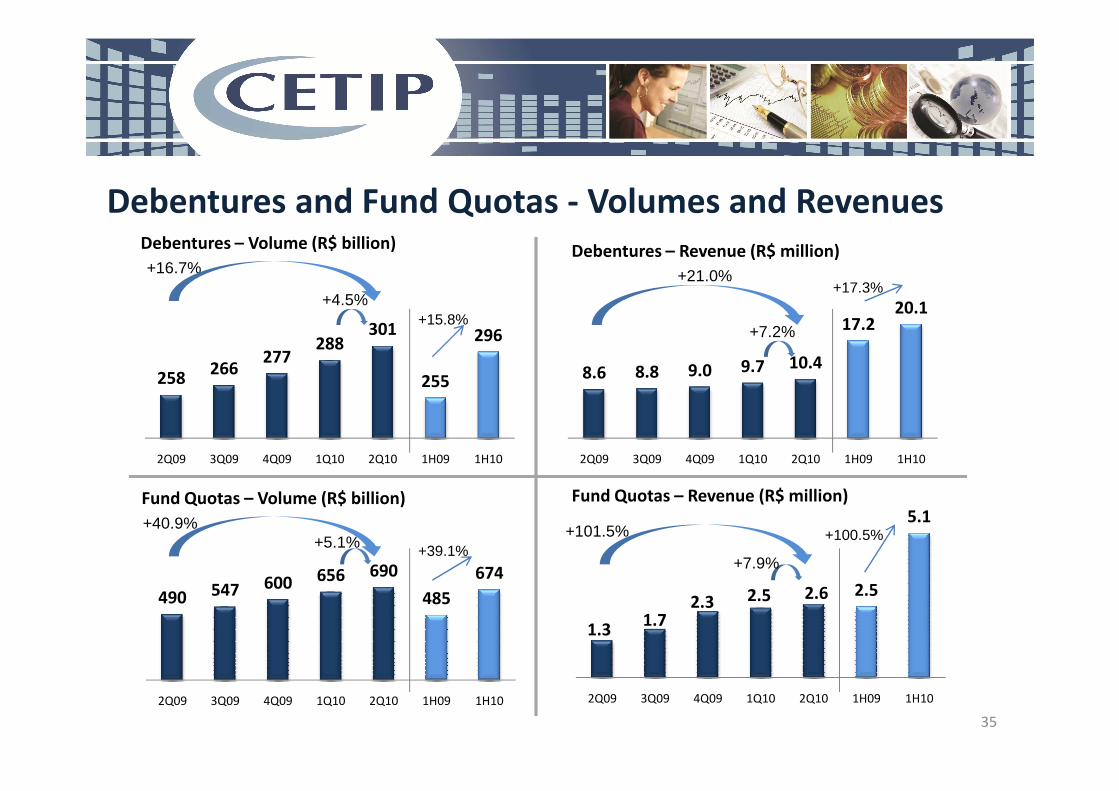

Debentures and Fund Quotas - Volumes and Revenues

258266

277288

301

255

296

Debentures – Volume (R$ billion)

+16.7%

+4.5%

8.6 8.8 9.0 9.7 10.4

17.220.1

Debentures – Revenue (R$ million)

+21.0%

+7.2%

+17.3%

+15.8%

35

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10 2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

490 547 600 656 690

485

674

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

Fund Quotas – Volume (R$ billion)

+40.9%+5.1%

2.6

1.31.7

2.3 2.5 2.5

5.1

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

Fund Quotas – Revenue (R$ million)

+101.5%

+7.9%

+100.5%+39.1%

CIP – Revenue and Volume

12.0 12.8

CIP – Revenue (R$ million)

-1.7%

Processed EFTs

38.3

323300293268274

+19.8%

+21.5%+7.2%

258 311

Note: Revenue refers only to services of SITRAF – Transfer Funds System.36

6.26.3 6.6 6.6 6.6

12.0 12.8

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

-6.9%

Processed EFTs(Quantity – MM)

Processed EFTs/day(Quantity - thousand)

16.7 17.4 18.4 18.3 20.0

31.538.3

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

+19.8%+9,5%

Adjusted Operating Expenses Breakdown – % and R$ million

21.119.8 19.0 22.3 21.4

-1.2%

+6.9%

• Depreciation and Amortization: -3.4%

• Personnel: -3.0%

37.7 42.5

+12.9%

37

Personnel

Outsourced services

Depreciation and amortization

General

Equipments and systems rental

Others expenses/revenues & taxes and fees1% 3% 1% 0% 1% 1%5% 4% 1% 1% 1% 5%

1%

9% 11%8% 9% 11%

9%10%

14% 14%12%

7% 7%

14%

7%

14%15%

15%16% 16%

13%

16%

58% 55%62% 66% 65%

58%65%

2Q09 3Q09 4Q09 1Q10 2Q10 1H09 1H10

21.119.8 19.0 22.3 21.4 37.7 42.5

Note: Personnel expenses include board members’ compensation.

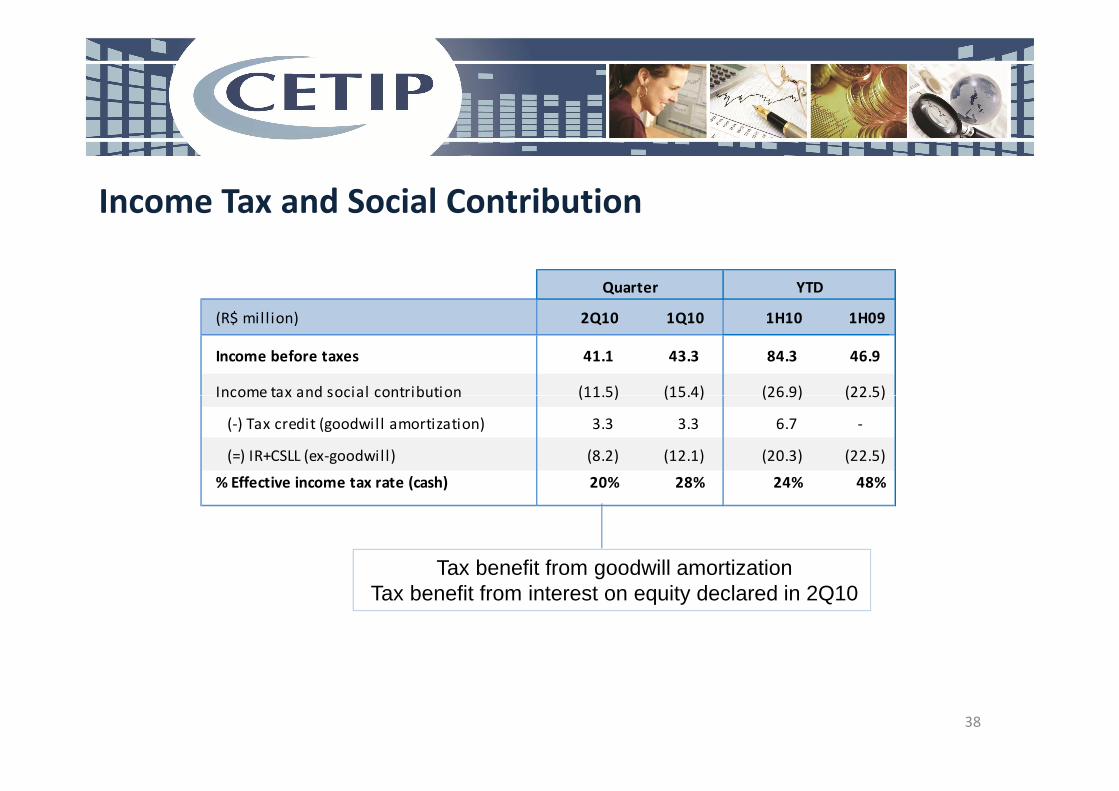

Income Tax and Social Contribution

(R$ mill ion) 2Q10 1Q10 1H10 1H09

Income before taxes 41.1 43.3 84.3 46.9

Income tax and social contribution (11.5) (15.4) (26.9) (22.5)

Quarter YTD

38

Tax benefit from goodwill amortizationTax benefit from interest on equity declared in 2Q10

Income tax and social contribution (11.5) (15.4) (26.9) (22.5)

(-) Tax credit (goodwill amortization) 3.3 3.3 6.7 -

(=) IR+CSLL (ex-goodwill) (8.2) (12.1) (20.3) (22.5)

% Effective income tax rate (cash) 20% 28% 24% 48%

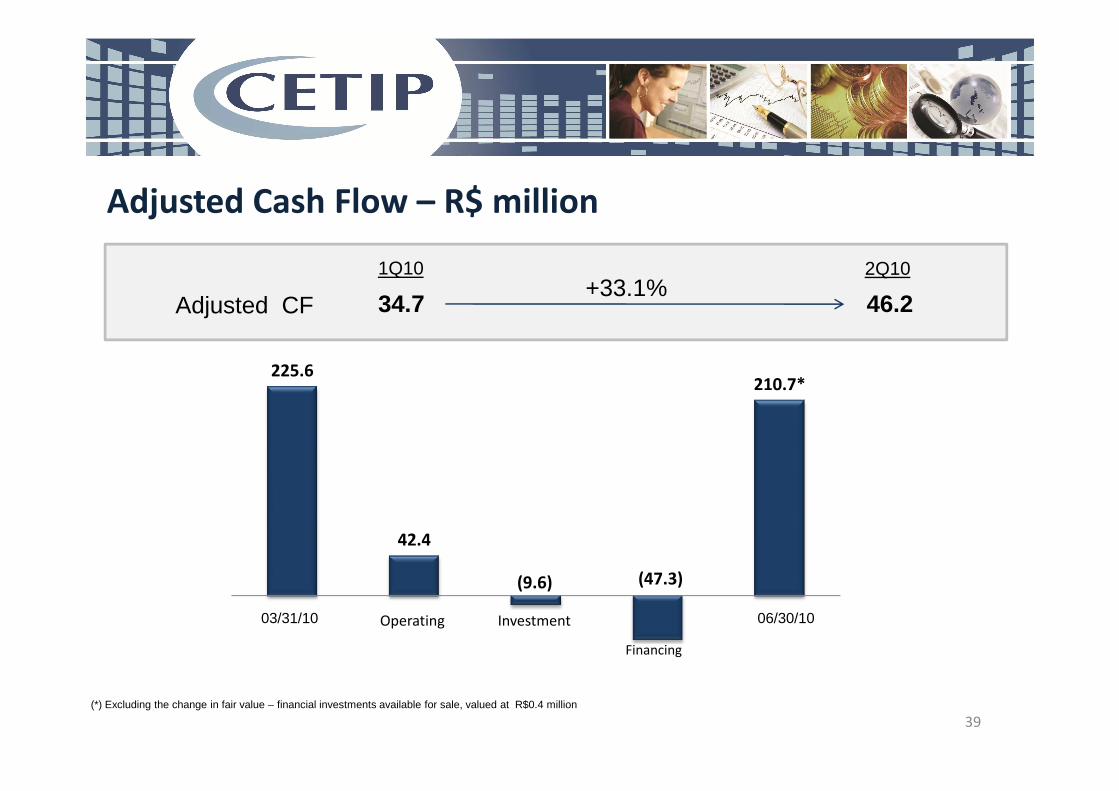

Adjusted Cash Flow – R$ million

34.7 46.2Adjusted CF+33.1%

1Q10 2Q10

225.6210.7*

39

(*) Excluding the change in fair value – financial investments available for sale, valued at R$0.4 million

42.4

(9.6) (47.3)

1Q10 Operating Investment 2Q10

Financing

03/31/10 06/30/10

Investor Relations

40

Legal Disclaimer

The forward-looking statements contained in this document relating to business prospects, projections of

operating and financial results, and those related to the growth prospects of CETIP are merely estimates and

as such are based exclusively on the Management’s expectations about the future of the business. These

forward-looking statements depend substantially on the approvals and licenses necessary for the projects,

market conditions, and performance of the Brazilian economy, the sector and international markets and

hence are subject to change without prior notice. This performance report includes accounting data and non-

accounting data such as operating, pro forma financial data and projections based on the Management’s

expectations. Non-accounting data has not been reviewed by the Company’s independent auditors.