institutional investors: latest trends and impacts for ... · Breakout Session 2 Risk transparency...

25

Breakout Session 2 Risk transparency reporting for investment funds’ institutional investors: latest trends and impacts for risk managers Adela Baho, Senior Risk Manager AIF, Credit Suisse, Multiconcept Fund Management S.A. Michael Derwael, Risk Manager, Lombard Odier Funds (Europe) S.A. Xavier Zaegel, Partner, Deloitte

Transcript of institutional investors: latest trends and impacts for ... · Breakout Session 2 Risk transparency...

Breakout Session 2

Risk transparency reporting for investment funds’

institutional investors: latest trends and impacts for

risk managers

Adela Baho, Senior Risk Manager AIF, Credit Suisse, Multiconcept

Fund Management S.A.

Michael Derwael, Risk Manager, Lombard Odier Funds (Europe)

S.A.

Xavier Zaegel, Partner, Deloitte

sponsors

media partners

Risk transparency reporting

for institutional investors

19 May 2015

Latest trends and impacts

for risk managers

Xavier Zaegel

Adela Baho

Michael Derwael

General context 03

SCR & Solvency II Reports for investment funds

• What is Solvency II 05

• Implementation timeline 06

• Solvency II reporting for investment funds 07

• Impact for risk management functions 08

Beyond Solvency II and regulatory requirements

• The new norm 11

• Practical cases 13

Transparency: Why does it matter? 16

Agenda

4

EU sovereign debt

CHF

Subprimes

Banking

crisis

Russia crisis

5

RegulatorsFinancial

Markets

The new norm - DisclosureDisclosure is ingrained in the regulatory regime as one of its three

pillars

Investors and market

operators

Management

Companies

1765

1776

1787

1798

1809

1820

1831

1842

1853

1864

1875

1886

1897

1908

1919

1930

1941

1952

1963

1974

1985

1996

2007

History of financial crises

A broad range of regulations trigger transparency

reporting needs for your institutional investors

6

Solvency I (VAG)

Solvency II:

Club-Ampère / BVI / IMA

SCR Market reporting

QRT as per D1/S.06.02.f and D4/S.06.03.a

Client bespoke templates

Insurers

RWA (Solva, SolvV)

CVA-risk & ECD

Large Exposures (GroMiKV)

LCR & NSFR

Credit Institutions

Transparency reporting (QMV, FTK)

Risk measurement (FTK)

Pension Funds

Retail26%

Insurance Companies29%

Pension Funds24%

Banks 2%

Other Institutionals19%

Institutional74%

European Asset Management industryClient portfolio breakdown

Source: EFAMA, April 2015

7

Solvency II: disclosures and

reporting impacts on asset

managers

SOLVENCY II

Assets & liabilities

valuation

Technical

provisions

Own fundsSolvency capital

requirements

Minimum capital

requirementInvestment rules

Governance

system

Supervisory

review

Groups control

Supervisory

reporting

Public

information

Impacts for Assets

Managers / Services

What is Solvency II?

PILLAR I

Capital requirements

PILLAR II

Governance & supervision

PILLAR III

Disclosures

Two thresholds:

Solvency capital requirements (SCR)

Minimum capital requirements (MCR)

Harmonised standards for:

Valuation of assets and liabilities

Eligibility criteria of own funds

Effective risk management system

Own risks and solvency assessment

(ORSA)

Supervisory review & intervention

Insurers are required to publish

details on risks, capital adequacy and

risk management

Transparency and open information

are intended to assess market forces

in imposing greater discipline to the

industry

Our focus of today

Full implementation is approaching

Solvency II reporting for investment funds

9

Preparatory phase Solvency II

FY 2014 FY 2015 FY 2016

FY 2014 Solo

reporting (22 weeks)

Q3 2015 Solo

reporting (8 weeks)

22 8 7 7 7# Weeks

Risk management

closing deadlines

3 6

Quarter report

Annual report

Solvency II deadlines have been set as follows:

• The preparatory measures will start as from January 2015 on FY 31 December 2014 figures.

• The full scope reporting will start as from January 2016 on FY December 2015 figures.

• Insurers will need risk transparency data on their investment funds holdings on a quarterly basis

starting from January 2016

• Transparency could be requested earlier during the preparatory phase

28%

42%0%

30%

10%6%

0%-14%

100%

0%

20%

40%

60%

80%

100%

120%

140%

Interest rate Equity Property Spread Currency Concentration IlliquidityPremium

Diversification Market risk

SCR Market

Solvency II reporting for investment funds

10

Market risk for the European insurance industry

• Market risk is the largest component (56%) of the standard SCR formula for the European industry

• Insurers will require from asset managers transparency data (Club Ampère / BVI template) or

sub-SCR Market calculations

• The equity, currency, spread and interest rate components are usually the largest elements for

investment funds

Source: illustrative calculation

Challenges for risk management functions

Solvency II reporting for investment funds

11

• Contact / Organization

• Collection, enrichment, and

preparation of data

• Scarcity and complexity of data

• Look-through on investment

vehicles

Data

Management

SCR

Calculation

Regulatory

Context

Reporting

Frequency &

Reporting

• Mark-to-Market valuations

• Pricing of complex derivatives and

structured products

• Shocks & risk mitigation techniques

• Sensitivities

• Ressourcing

• Frequency

• EIOPA Guidelines

• Entry in force of Solvency II

in March 2016

• Regulatory watch

12

Beyond Solvency II and

regulatory requirements

1929 1973 1981 1987 1989 1991 1992 1994 1997 1998 2000 2001 2002 2008 2009 2010 2014 2015

Wa

ll S

tre

et cra

sh

&

Gre

at D

ep

ressio

n

Crisis…

The new norm:

13

• Market events the new transparency

norm

• Shocks require a short reaction time

to avoid crisis escalation

Financial Markets

1765

1776

1787

1798

1809

1820

1831

1842

1853

1864

1875

1886

1897

1908

1919

1930

1941

1952

1963

1974

1985

1996

2007

History of financial crises

Oil

cri

sis

La

tam

de

bt cri

sis

Bla

ck M

on

da

y

US

Sa

vin

gs &

Lo

an

s c

risis

Sca

nd

ies b

an

k

cri

sis

Bla

ck W

ed

ne

sd

ay +

att

acks o

n E

RM

Me

xic

o d

eb

t cri

sis

&

de

fau

lt

Asia

n c

risis

Russia

n d

efa

ult

Tu

rke

y c

risis

Dotc

om

bu

bb

le +

9/1

1

Arg

en

tin

a d

efa

ult

Le

hm

an

de

fau

lt &

Glo

ba

l cri

sis

Ice

lan

d c

risis

EU

so

ve

reig

n d

eb

t

cri

sis

Russia

cri

sis

Sw

iss F

ran

c d

ep

eg

Complexity…

The new norm:

1609

Equities

1685

Futures

1750

Bonds

1970

MBS

1973

Listed options

1981

IRS & ExoticsOptions

1982

Cap, floors & Swaptions

1987

CDO

1993

ETF

1995

Variance Swaps, VolatilityFutures

1997

CDS

2004

CDS index

2004 - present

Synthetic, structured multi-layer securitizations

Broad variety of structured products (single asset class and hybrids, Cocos, etc.)

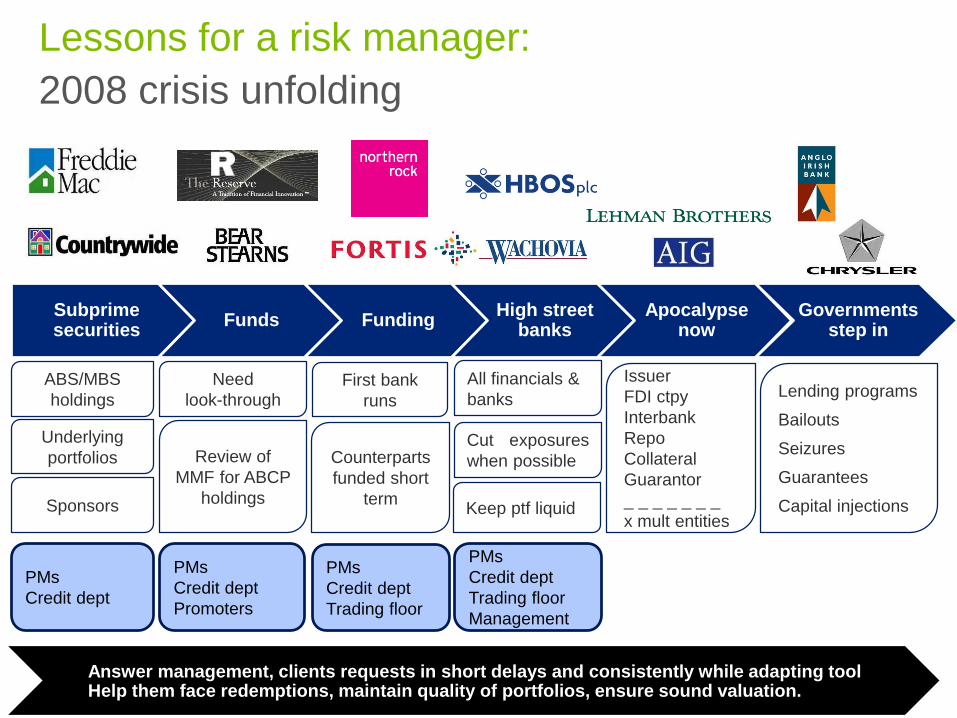

Lessons for a risk manager:

15

Subprime securities

Funds FundingHigh street

banksApocalypse

nowGovernments

step in

ABS/MBS

holdings

Underlying

portfolios

Sponsors

Need

look-through

Review of

MMF for ABCP

holdings

Counterparts

funded short

term

All financials &

banks

Cut exposures

when possible

Keep ptf liquid

Issuer

FDI ctpy

Interbank

Repo

Collateral

Guarantor

_ _ _ _ _ _ _

x mult entities

First bank

runsLending programs

Bailouts

Seizures

Guarantees

Capital injections

PMs

Credit dept

Promoters

PMs

Credit dept

Trading floor

PMs

Credit dept

Trading floor

Management

Answer management, clients requests in short delays and consistently while adapting toolHelp them face redemptions, maintain quality of portfolios, ensure sound valuation.

PMs

Credit dept

2008 crisis unfolding

How a market event can reshape risk

management and disclosures

16

Event

• January 2015, unexpected decision from SNB to switch back to free-floating CHF

• Investors requesting information about exposures and impact of a forthcoming quantitative easing

Illustrative context

• Multi-Asset “Fund” : 20% net short exposure to CHF with multi hedged and unhedged share

classes

Risk management response

• Adjust the shock at 20% (and not 10%) on CHF in stress tests

• Stress other similar currencies, such as RMB (dirty-floating)

• Stress variables strongly correlated to CHF or similar (spillover effects)

• Hedge ratio and efficiency per share class

• Analysis per share class

• Detailed currency exposures

Risk disclosures

Target funds held by funds: transparency and the

look-through approach

17

Context

• Lack of market data for underlying funds

• Lower visibility on underlying exposures and risks

• Difficulty to assess and measure risks ex-ante

Possible approaches

• Qualitative selection of publicly traded proxies: indices, model portfolio, asset mix

• Quantitative methods: Dimension reduction -Parametric assumptions- Stress Tests

• Partial / Full look-through

Risk management challenge

• Historical volatility can be a bad proxy of historical or current risks

• Misconception of low volatility and high returns

• Overestimation of diversification benefits

From a necessity to an opportunity

Transparency: why does it matter?

18

• More accuracy in assessing risks inherent in the portfolios

• More efficient monitoring and risk-based decision making

Understanding of risks

A focus on transparency will create added value for all market participants

Evolution of the Risk Management function

• Unique entry point for multiple communication channels

• Driver for evolution of information systems incl. standardization & drill-down

capabilities

• Pairing of products with client risk profile

19

Q&A

Appendix

20

A broad range of regulations triggering

transparency reporting needs

21

• Alternative Investment Fund Managers Directive (AIFMD)

• Banking Union (CRD IV / CRR / BRRD / DGSD / SSM / SRM)

• European Market and Infrastructure Regulation (EMIR)

• Key Investor Information Documents for Packaged Retail and Insurance-based Investment

Products (PRIIPs)

• Markets in Financial Instruments Directive and Regulation (MiFID II / MiFIR)

• UCITS V & CSSF Circular 14/587 (UCITS V)

• European Long Term Investment Funds (ELTIFs)

• Insurance Mediation Directive (IMD II)

• Money Market Funds (MMFs)

• Solvency II and Omnibus II

Top 2015 regulatory priorities

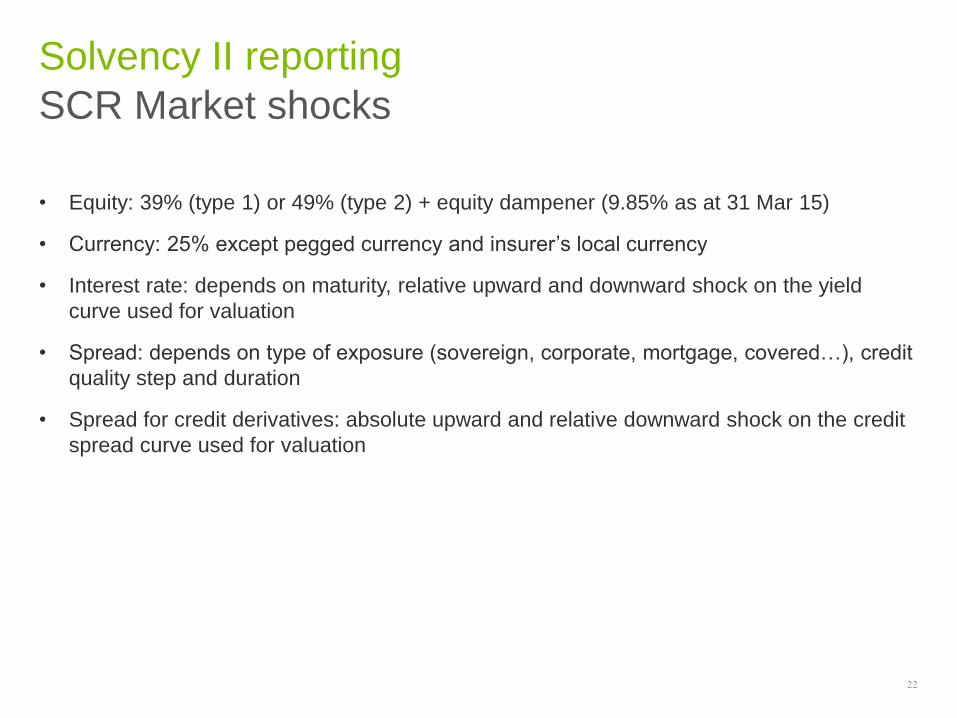

SCR Market shocks

Solvency II reporting

• Equity: 39% (type 1) or 49% (type 2) + equity dampener (9.85% as at 31 Mar 15)

• Currency: 25% except pegged currency and insurer’s local currency

• Interest rate: depends on maturity, relative upward and downward shock on the yield

curve used for valuation

• Spread: depends on type of exposure (sovereign, corporate, mortgage, covered…), credit

quality step and duration

• Spread for credit derivatives: absolute upward and relative downward shock on the credit

spread curve used for valuation

22

Data essentials and sample Solvency II report

Appendix

23

Counterparty/Issuer/Broker Name;

Counterparty/Issuer/Broker Credit Rating; Hedging/Not

Hedging1 for derivatives; Hedging1 type

Instrument unique ID allowing matching of both leg of

each instrument; Currency Class Hedging purpose Y/N

Underlying ISIN/Ticker; Underlying Description; Buy/Sell

information for Credit Default Swaps; Running spread (or

fixed coupon) for Credit derivatives; Trade dates;

Instrument unique ID allowing matching of both leg of

each instrument

Underlying ISIN/Ticker; Underlying Description;

Underlying price; Contract Size; Strike; Delta; Call/Put

Information; Distinction OTC/ Listed

Security description; Security type; ISIN /ticker; currency;

FX Rates; Notional/Quantity; Dirty Market Value; Maturity

Date; Modified Duration; Rating

All Investment lines

NAV Date; Fund Name; Fund ISIN; Fund TNA; Fund

Currency; Hedged class (Y/N)

Fund and Target Funds

Treasury & all derivatives

FX Forwards

Swaps

Options

sponsors

media partners

Thank you

for attending!