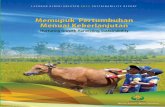

Installed Capacity - semenindonesia.com · United Tractor Semen Gresik 55% PT Swadaya Graha 25% PT...

16

Transcript of Installed Capacity - semenindonesia.com · United Tractor Semen Gresik 55% PT Swadaya Graha 25% PT...

Installed Capacity

Total

108.1 Mio Ton

SMGR market share 2018 was 39.4% despite of only 33.2% capacity share

2018

Semen Indonesia

SBI (ex Holcim Indonesia)

53.17%

26.37%

5.07% 4.09%2.95% 3.12% 2.31% 1.76% 0.93% 0.23%

SMIG(SMGR+ SBI)

INTP Conch Bosowa MerahPutih

Baturaja Jui Shin SiamCement

STAR SemenKupang

Market Share

39.40%

25.50%

15.40%

4.80%3.50% 3.10% 3.10%

1.90% 1.90%1.00% 0.30%

SMGR INTP SBI Conch Bosowa MerahPutih

BaturajaJui Shin SiamCement

STAR SemenKupang

Market Share

SMIG is the market leader in Indonesia with a market share of

39.4% in 2018. The top 3 players dominate 80.3% of domestic

market share. With the acquisition SBI, our market share

increased by 15.40%.

source: Indonesia Cement Association

SMIG

• Established in August 1957

• One of the largest cement players in SE Asia with a design

capacity of 38.2 MTPY of cement and a 40% market share in

Indonesia

• Production facilities in Indonesia’s 3 major islands namely

Java, Sumatera and Sulawesi, and also in Vietnam

• State Owned Enterprise with 51% shares owned by

Government of Indonesia

• Publicly listed in IDX since 1991 with a market capitalization of

$4.8bn

TLCC

70,0%

PT Semen

Indonesia

Aceh

52,28%

SBI

98,4%

PT Semen

Kupang

Indonesia

99,48%

PT Semen

Padang

99,99%

PT

Semen

Tonasa

99,99%

PT Semen

Gresik

99,96%

PT Semen Indonesia Logistic

73,65%

PT Sinergi Mitra Investama

97%

PT Semen Indonesia International

85,00%

PT Sinergi Informatika Semen Indonesia

85,00%

PT Semen Indonesia Beton

99,99%

PT Semen Indonesia Industri Bangunan

99,99%

Industri Kemasan Semen Gresik

60%

United Tractor Semen Gresik

55%

PT Swadaya Graha

25%

PT Krakatau Semen Indonesia

50%

PT Kawasan Industri Gresik

65%

Foreign

individuals

0%

Domestic

institutions

11%

Foreign

institutions

37%Indonesian

Government

51%

Domestic

individuals

1%

*acquired under

SIIB

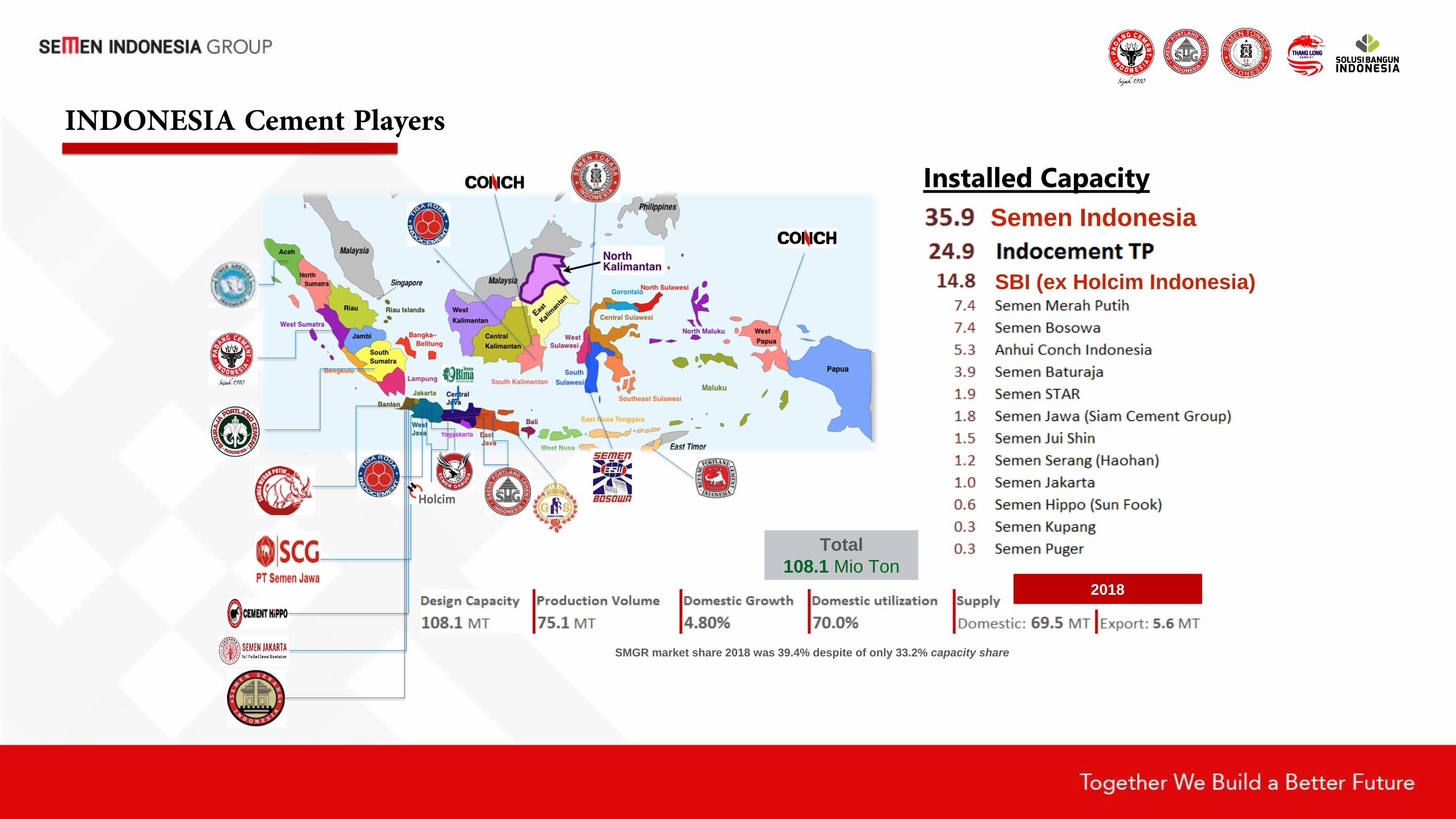

1995 2005 2012 2013

SG became the first SOE that

became a Publicly Listed Company.

SP, ST and SG remained stand-

alone companies.

SG, SP, and ST were consolidated as Semen Gresik Group; where SP

and ST stood under SG

Transformed into a strategic holding

(PT. Semen Indonesia Tbk)

Redesigning Governance.

Restructuring to achieve better synergy results

Acquiring Thang Long Cement

Company (TLCC Vietnam) as a part

of the “Development Growth Plan”

SOE Structure

Timeline

Event

2019

The first SOE to ever acquired a

global corporation, namely LH Indonesia

Strategy1. Company

Growth2. Company Survival 3. Consolidation 4. Regional Leader

5. Centralized Operation & Integrated Functions

7. Strengthening Position as Indonesia’s Market Leader

6. Strategic Holding5. Strategic Holding

2023

4. Functional Holding

3. Functional Holding

2. Operating Holding

1. Operating Company

1991

Through the current structure of Strategic Holding, SMIG has

succeeded in acquiring LHI to strengthen the company's future position without using the State

Budget.

BAG

73%

BULK

27%

32.8 34.239.2

44.1 45.7 46.9 47.5 46.8 49.4 50.8

6.2 6.6

8.8

10.812.2 13 14.5 14.8

16.9 18.830.0%

25.0%

20.0%

15.0%

10.0%

5.0%

0.0%

-5.0%

20

10

0

60

50

40

30

80 40.0%

Bulk Vol

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Bag Vol Growth Bag Growth Bulk Bulk Portion

CAGR Bulk: 13.1%

70 CAGR Bag: 5% 35.0%

Cement demand growth was dominated by the growth of bulk

cement to support infrastructure projects.

86114

146

184 178

290317

388410 415

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019

Infrastructure Budget

18.9 21.5 24.6 25.3 26.2 27.5 28.9 30.5

26.530.3 32.6 33.7 34.5 33.4 37.4 39.0

21.94.6%

17.6%

14.4%

5.5%3.5% 3.5%

28.2-0.6%

7.6%

4.8%

2010 2011 2012 2014 2015 2017 20182013

Outside Java Java

2016

Growth

CAGR:6.6%

source: Indonesia Cement Association

source: Indonesia Cement Association

Bag cement still represent the largest portion of

Indonesia cement consumption

BAG71.71%

BULK28.29%

Bag Bulk

Bulk cement growth is

higher than bag

cement in the last two

years. Bulk demand

growth 2018 was 11%

while demand for bag

was 2.7%.

In Q1’19 bulk demand

growth was at 3%

while bag declined at

-1%.

Government infrastructure

budget is significantly

increasing since 2015 along

with the 5 years National

Strategic Projects.

source: Indonesia Cement Association

source: Indonesia Cement Association

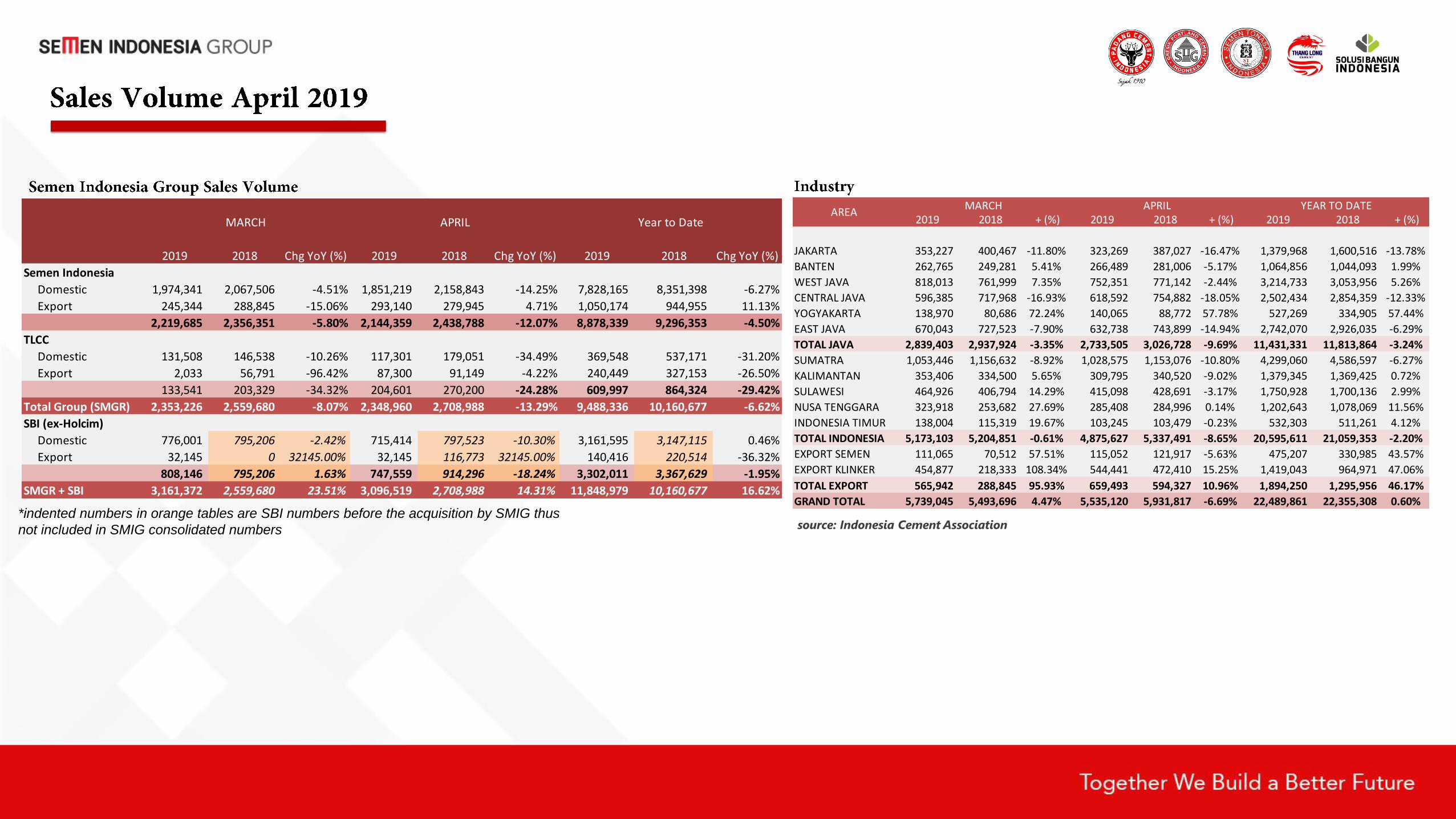

April 2019

2019

source: Indonesia Cement Association*indented numbers in orange tables are SBI numbers before the acquisition by SMIG thus

not included in SMIG consolidated numbers

2019 2018 Chg YoY (%) 2019 2018 Chg YoY (%) 2019 2018 Chg YoY (%)

Semen Indonesia

Domestic 1,974,341 2,067,506 -4.51% 1,851,219 2,158,843 -14.25% 7,828,165 8,351,398 -6.27%

Export 245,344 288,845 -15.06% 293,140 279,945 4.71% 1,050,174 944,955 11.13%

2,219,685 2,356,351 -5.80% 2,144,359 2,438,788 -12.07% 8,878,339 9,296,353 -4.50%

TLCC

Domestic 131,508 146,538 -10.26% 117,301 179,051 -34.49% 369,548 537,171 -31.20%

Export 2,033 56,791 -96.42% 87,300 91,149 -4.22% 240,449 327,153 -26.50%

133,541 203,329 -34.32% 204,601 270,200 -24.28% 609,997 864,324 -29.42%

Total Group (SMGR) 2,353,226 2,559,680 -8.07% 2,348,960 2,708,988 -13.29% 9,488,336 10,160,677 -6.62%

SBI (ex-Holcim)

Domestic 776,001 795,206 -2.42% 715,414 797,523 -10.30% 3,161,595 3,147,115 0.46%

Export 32,145 0 32145.00% 32,145 116,773 32145.00% 140,416 220,514 -36.32%

808,146 795,206 1.63% 747,559 914,296 -18.24% 3,302,011 3,367,629 -1.95%

SMGR + SBI 3,161,372 2,559,680 23.51% 3,096,519 2,708,988 14.31% 11,848,979 10,160,677 16.62%

APRILMARCH Year to Date 2019 2018 + (%) 2019 2018 + (%) 2019 2018 + (%)

JAKARTA 353,227 400,467 -11.80% 323,269 387,027 -16.47% 1,379,968 1,600,516 -13.78%

BANTEN 262,765 249,281 5.41% 266,489 281,006 -5.17% 1,064,856 1,044,093 1.99%

WEST JAVA 818,013 761,999 7.35% 752,351 771,142 -2.44% 3,214,733 3,053,956 5.26%

CENTRAL JAVA 596,385 717,968 -16.93% 618,592 754,882 -18.05% 2,502,434 2,854,359 -12.33%

YOGYAKARTA 138,970 80,686 72.24% 140,065 88,772 57.78% 527,269 334,905 57.44%

EAST JAVA 670,043 727,523 -7.90% 632,738 743,899 -14.94% 2,742,070 2,926,035 -6.29%

TOTAL JAVA 2,839,403 2,937,924 -3.35% 2,733,505 3,026,728 -9.69% 11,431,331 11,813,864 -3.24%

SUMATRA 1,053,446 1,156,632 -8.92% 1,028,575 1,153,076 -10.80% 4,299,060 4,586,597 -6.27%

KALIMANTAN 353,406 334,500 5.65% 309,795 340,520 -9.02% 1,379,345 1,369,425 0.72%

SULAWESI 464,926 406,794 14.29% 415,098 428,691 -3.17% 1,750,928 1,700,136 2.99%

NUSA TENGGARA 323,918 253,682 27.69% 285,408 284,996 0.14% 1,202,643 1,078,069 11.56%

INDONESIA TIMUR 138,004 115,319 19.67% 103,245 103,479 -0.23% 532,303 511,261 4.12%

TOTAL INDONESIA 5,173,103 5,204,851 -0.61% 4,875,627 5,337,491 -8.65% 20,595,611 21,059,353 -2.20%

EXPORT SEMEN 111,065 70,512 57.51% 115,052 121,917 -5.63% 475,207 330,985 43.57%

EXPORT KLINKER 454,877 218,333 108.34% 544,441 472,410 15.25% 1,419,043 964,971 47.06%

TOTAL EXPORT 565,942 288,845 95.93% 659,493 594,327 10.96% 1,894,250 1,295,956 46.17%

GRAND TOTAL 5,739,045 5,493,696 4.47% 5,535,120 5,931,817 -6.69% 22,489,861 22,355,308 0.60%

AREAAPRILMARCH YEAR TO DATE

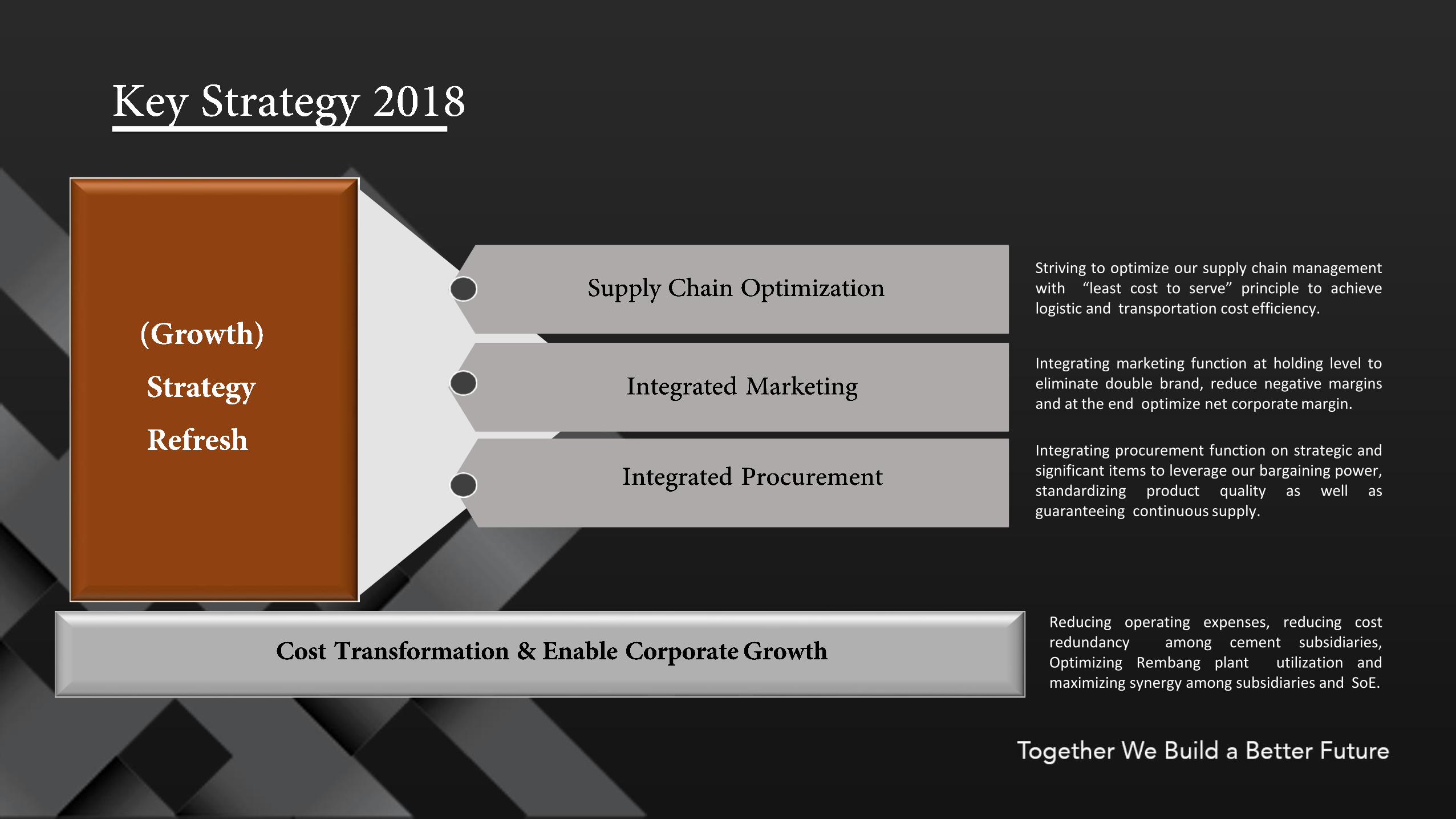

Striving to optimize our supply chain managementwith “least cost to serve” principle to achievelogistic and transportation cost efficiency.

Integrating marketing function at holding level toeliminate double brand, reduce negative marginsand at the end optimize net corporate margin.

Integrating procurement function on strategic andsignificant items to leverage our bargaining power,standardizing product quality as well asguaranteeing continuous supply.

Reducing operating expenses, reducing costredundancy among cement subsidiaries,Optimizing Rembang plant utilization andmaximizing synergy among subsidiaries and SoE.

8

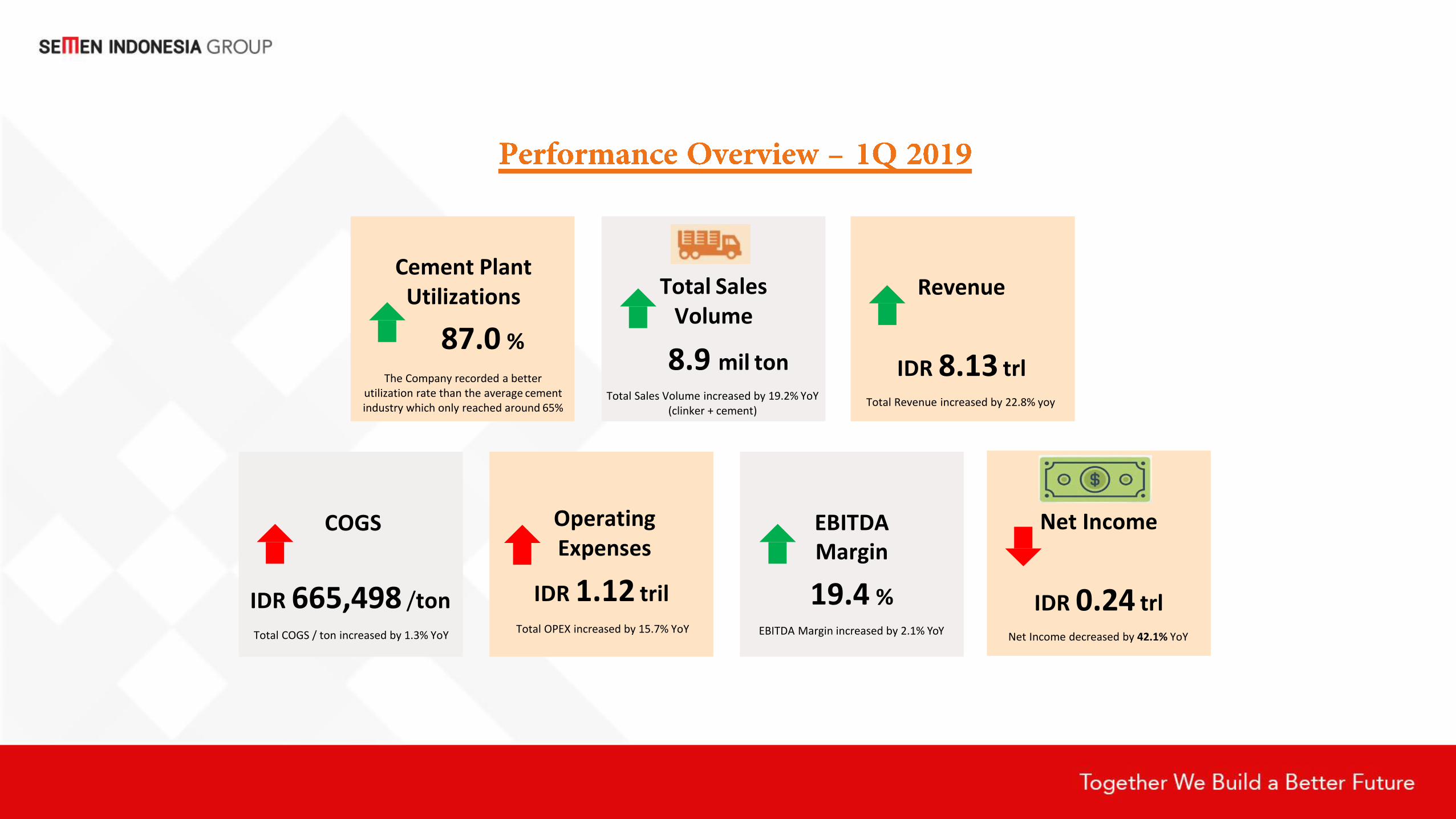

Total Sales Volume

8.9 mil tonTotal Sales Volume increased by 19.2% YoY

(clinker + cement)

Revenue

IDR 8.13 trlTotal Revenue increased by 22.8% yoy

Cement Plant Utilizations

87.0 %

The Company recorded a better utilization rate than the average cement industry which only reached around 65%

Operating Expenses

IDR 1.12 tril

Total OPEX increased by 15.7% YoY

COGS

IDR 665,498 /ton

Total COGS / ton increased by 1.3% YoY

Net Income

IDR 0.24 trlNet Income decreased by 42.1% YoY

EBITDAMargin

19.4 %EBITDA Margin increased by 2.1% YoY

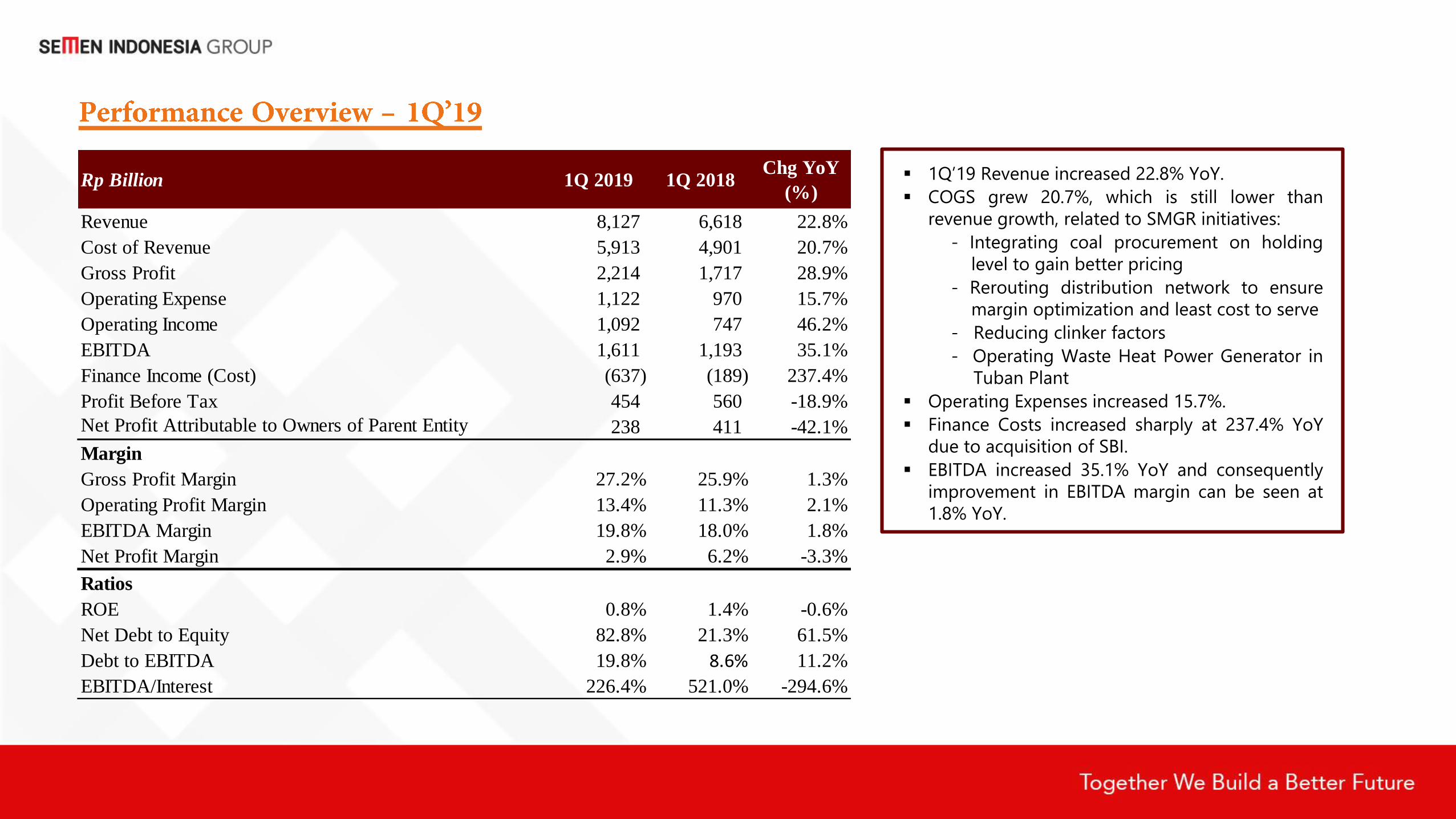

1Q’19 Revenue increased 22.8% YoY.

COGS grew 20.7%, which is still lower than

revenue growth, related to SMGR initiatives:

- Integrating coal procurement on holding

level to gain better pricing

- Rerouting distribution network to ensure

margin optimization and least cost to serve

- Reducing clinker factors

- Operating Waste Heat Power Generator in

Tuban Plant

Operating Expenses increased 15.7%.

Finance Costs increased sharply at 237.4% YoY

due to acquisition of SBI.

EBITDA increased 35.1% YoY and consequently

improvement in EBITDA margin can be seen at

1.8% YoY.

Rp Billion 1Q 2019 1Q 2018Chg YoY

(%)

Revenue 8,127 6,618 22.8%

Cost of Revenue 5,913 4,901 20.7%

Gross Profit 2,214 1,717 28.9%

Operating Expense 1,122 970 15.7%

Operating Income 1,092 747 46.2%

EBITDA 1,611 1,193 35.1%

Finance Income (Cost) (637) (189) 237.4%

Profit Before Tax 454 560 -18.9%

Net Profit Attributable to Owners of Parent Entity 238 411 -42.1%

Margin

Gross Profit Margin 27.2% 25.9% 1.3%

Operating Profit Margin 13.4% 11.3% 2.1%

EBITDA Margin 19.8% 18.0% 1.8%

Net Profit Margin 2.9% 6.2% -3.3%

Ratios

ROE 0.8% 1.4% -0.6%

Net Debt to Equity 82.8% 21.3% 61.5%

Debt to EBITDA 19.8% 8.6% 11.2%

EBITDA/Interest 226.4% 521.0% -294.6%

5,032 3,989

2,847 3,638

5,246 6,049

2014 2015 2016 2017 2018 1Q 2019

Cash Balance (IDRbn)

3,913 3,999 6,260 10,019 9,864

31,929

2014 2015 2016 2017 2018 1Q 2019

Total Interest Bearing Debt (IDRbn)

20.20 19.14

6.48 6.86

2.26

2015 2016 2017 2018 1Q 2019

EBITDA/Interest

0.5 0.5 0.9 2.0 1.5

19.8

2014 2015 2016 2017 2018 1Q 2019

Debt/EBITDA

-0.5%0.0%

11.2%22.8% 20.9%

82.8%

2014 2015 2016 2017 2018 1Q 2019

Net Debt/Equity

15% 20%35% 32%

102%

2015 2016 2017 2018 1Q 2019

Gross Debt/Equity

Source: Internal SMIG

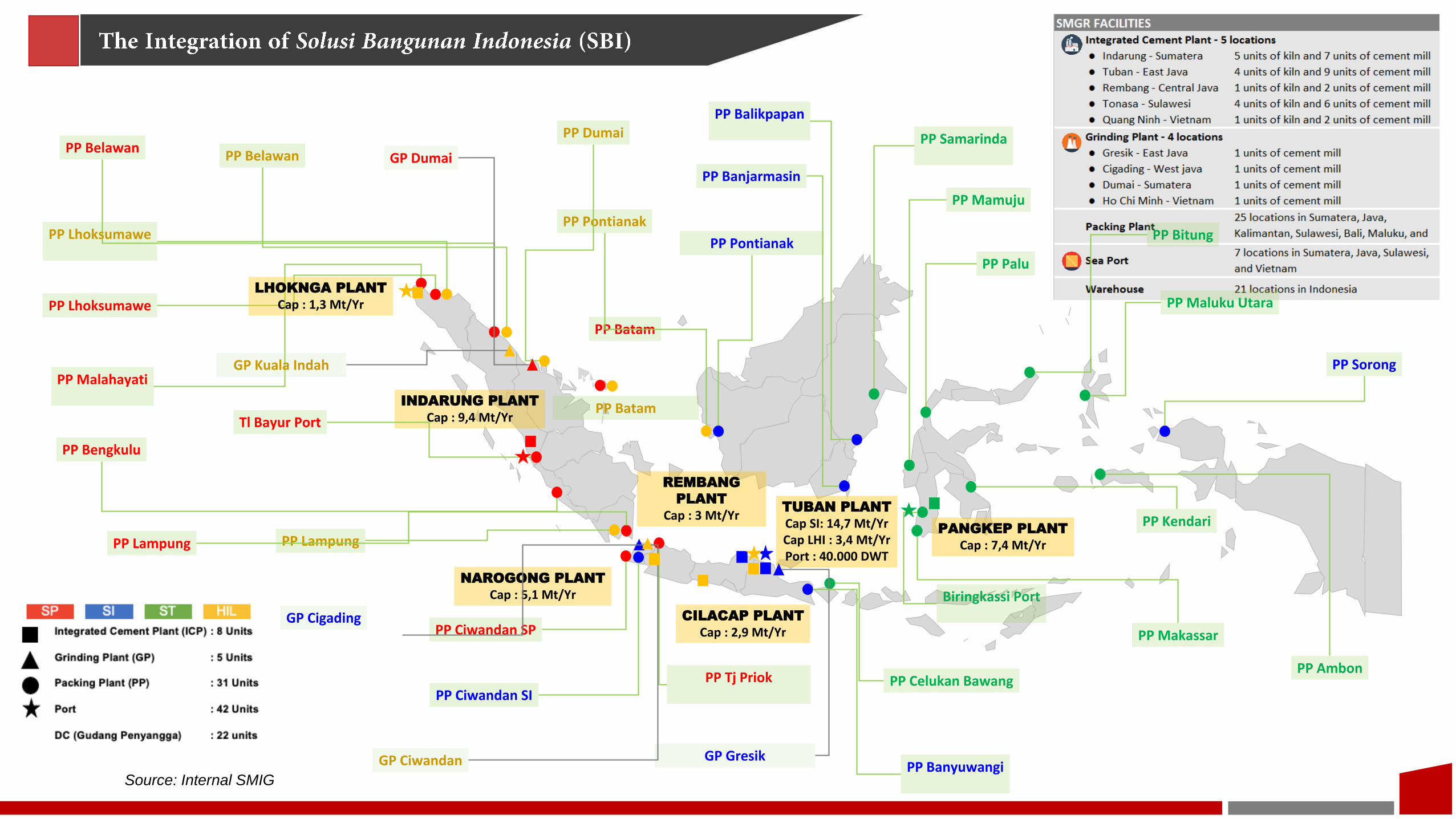

TUBAN PLANT

Cap SI: 14,7 Mt/YrCap LHI : 3,4 Mt/YrPort : 40.000 DWT

INDARUNG PLANT

Cap : 9,4 Mt/Yr

GP Dumai

GP Gresik

PP Lhoksumawe

PP Malahayati

PP Batam

Tl Bayur Port

PP Lampung

PP Pontianak

PP Samarinda

PP Banjarmasin

PP Balikpapan

PP Bitung

PP Palu

PP Mamuju

Biringkassi Port

PP Makassar

PP Kendari

PP Sorong

PP Ambon

PP Banyuwangi

PP Celukan Bawang

PANGKEP PLANT

Cap : 7,4 Mt/Yr

PP Belawan

PP Tj Priok

PP Ciwandan SP

PP Ciwandan SI

PP Maluku Utara

GP Ciwandan

PP Bengkulu

REMBANG

PLANT

Cap : 3 Mt/Yr

LHOKNGA PLANT

Cap : 1,3 Mt/Yr

NAROGONG PLANT

Cap : 5,1 Mt/Yr

CILACAP PLANT

Cap : 2,9 Mt/Yr

PP Lhoksumawe

PP Belawan

PP Pontianak

PP Dumai

PP Batam

GP Kuala Indah

PP Lampung

GP Cigading

IMPORTANT NOTICE

THIS PRESENTATION IS NOT AND DOES NOT CONSTITUTE OR FORM PART OF, AND IS NOT MADE IN CONNECTION WITH, ANY OFFERFOR SALE OR SUBSCRIPTION OF OR SOLICITATION, RECOMMENDATION OR INVITATION OF ANY OFFER TO BUY OR SUBSCRIBE FORANY SECURITIES NOR SHALL IT OR ANY PART OF IT FORM THE BASIS OF OR BE RELIED ON IN CONNECTION WITH ANY CONTRACT,COMMITMENT OR INVESTMENT DECISION WHATSOEVER.

THE SLIDES USED IN THIS PRESENTATION ARE STRICTLY CONFIDENTIAL AND HAVE BEEN PREPARED AS A SUPPORT FOR ORALDISCUSSIONS ONLY. THE INFORMATION CONTAINED IN THIS PRESENTATION IS BEING PRESENTED TO YOU SOLELY FOR YOURINFORMATION AND MAY NOT BE REPRODUCED OR REDISTRIBUTED TO ANY OTHER PERSON, IN WHOLE OR IN PART.

This presentation includes forward-looking statements, which are based on current expectations and forecast about future events. Such statements involve known / unknown risks uncertainties and other factors, which could cause actual results to differ materially from historical results or those

anticipated. Such factors include, among others:

● economic, social and political conditions in Indonesia, and the impact such conditions have on construction and infrastructure spending in

Indonesia;

● the effects of competition;

● the effects of changes in laws, regulations, taxation or accounting standards or practices;

● acquisitions, divestitures and various business opportunities that we may pursue;

● changes or volatility in inflation, interest rates and foreign exchange rates;

● accidents, natural disasters or outbreaks of infectious diseases, such as avian influenza, in our markets;

● labor unrest or other similar situations; and

● the outcome of pending or threatened litigation.

We can give no assurance that our expectations will be attained.

DISCLAIMER

The information contained in this report has been taken from sources which we deem reliable. However, none of PT Semen Indonesia (Persero) Tbk and/or its affiliated companies and/or their respective employees and/or agents make any representation or warranty (express or implied) or

accepts any responsibility or liability as to, or in relation to, the accuracy or completeness of the information and opinions contained in this report or as to any information contained in this report or any other such information or opinions remaining unchanged after the issue thereof.

We expressly disclaim any responsibility or liability (express or implied) of PT Semen Indonesia (Persero) Tbk, its affiliated companies and their respective employees and agents whatsoever and howsoever arising (including, without limitation for any claim, proceedings, action, suits, losses, expenses, damages or costs) which may be brought against or suffered by any person as a result of acting in reliance upon the whole or any part

of the contents of this report and neither PT Semen Indonesia (Persero) Tbk, its affiliated companies or their respective employees or agents accepts liability for any errors, omission or mis-statements, negligent or otherwise, in the report and any liability in respect of the report or any

inaccuracy therein or omission therefrom which might otherwise arise is hereby expresses disclaimed.