What Are We Protesting About? Martin Luther and the Reformation.

Insight #10

INDUSTRY FOCUSAn insider's guide to project controls

/ Global economy insight/ Middle East markets update/ Commodities price analysis

Insight #10

Insight / June 2016 / Page one

Global

As the global economy continues to struggle for growth, political uncertainties continue to dog prospects for recovery in key markets including the US, EMEA and China. While it is possible that some of those difficulties – such as the US presidential election – will be resolved before the end of 2016, the fall-out may present a further hangover.

The implications of Britain’s referendum vote to leave the European Union will be watched closely for any impact, particularly in Europe. 'Brexit' negotiations may not commence until later in 2016 and the economic impact may depend on whether they can be undertaken smoothly. Issues include future trade agreements, labour movement regulations and whether a UK exit might destabilise the EU. A British exit would take place by 2019.

The sluggishness of the global economy has its roots in the oil price decline that has marked the last two years, and that trend continues to underpin confidence levels in many markets. Oil prices may be comparatively low, but they are clearly gaining some strength, and there remains optimism among oil-producing countries that prices will reach the more comfortable $60 per barrel level before the year's end.

That would improve revenues for economies across the OPEC nations, particularly Russia and the Middle East. If sustained, that development should help to kick-start several massive infrastructure projects – roads, railways, airports and major services – that have slowed down, or even been suspended, amidst public spending restrictions and the private sector’s inevitable response to there being less cash available for contract completion.

Welcome

Welcome to Insight #10. In this edition of Insight we once again analyse the global economy and Middle East markets. Our focus this quarter is project controls.

We also include our commodities price analysis to keep you up to date with the latest prices.

Page one / Global

Page four / Regional

Page seven / Commodities price analysis

Page nine / Focus:

Project controls

Page twelve / Currie & Brown offices

Currie & [email protected]

Source: independent.co.uk

Oil prices are not the only problem facing the world economy, however. Slower growth in the domestic Chinese market means consumer demand is lower there, and that is affecting many exporters. Likewise, the continued slow growth in Europe is having a similar effect on consumer spending, and national economies are still grappling with the euro crisis.

The geo-political situation continues to have a significant braking effect on economies. The welcome ceasefire in Syria, while not holding perfectly, has allowed some opportunity for ongoing peace talks involving most of the factions, and their outcome will be watched closely. However, the refugee situation arising from Syria, but also involving people from Afghanistan and various African states, continues to be a

major international problem.

There is some anecdotal evidence at least that various policy and investment decisions were delayed while the outcome of the June referendum on continued British membership of the European Union was awaited.

These international factors have been reflected in the Gulf region, where they have intertwined with the oil price issue to have a significant impact on capital spending.

The Middle East Capital Projects & Infrastructure Survey (CP&I) for 2016, published recently by international consultants PwC, concludes that the oil price slump has presented new challenges to the sector. Whereas in 2014, respondents were concerned about the sheer scale of projects

and whether the industry had the capacity to cope with them, now 75 per cent of respondents say they have suffered the impact of funding constraints, with a majority expecting more to come during the year ahead.

Broadly, the impact stems from there being less public money available, as this has driven the majority of project spending during the recent relative 'boom'. As governments collect less in oil tax revenues, spending has been cut and projects delayed or even cancelled.

That means more emphasis is being placed on seeking private capital for significant projects in social infrastructure, urban development, transport and energy.

Insight

Insight / June 2016 / Page two

IMPACT OF DECLINING OIL PRICES

Source: PwC Middle East Capital Projects & Infrastructure Survey May 2016

Q. What impact does the declining oil prices have on the industry in which your organisation operates?

One solution may be a form of PPP (public-private partnership), a relatively new concept in the Middle East but one with a longer establishment in western markets such as the UK.

'Market expectations are that the oil price will remain low throughout much of this year, and although there are some forecasts of a recovery towards the end of 2016 or early 2017, it can not be guaranteed,' concludes the PwC report.

'This is going to result in a sustained period where governments will be reassessing spending commitments and priorities around infrastructure. While in some cases this will present opportunities for investment in infrastructure that promotes economic diversification away from the hydrocarbons sector, the overall theme will undoubtedly be on … more efficient spending.'

Optimism remains that spending will stay on schedule for major 'event'-driven projects such as those related to the FIFA World Cup in Qatar (2022) and Dubai Expo (2020). Intriguingly, a growing number of renewable energy-related projects are attracting significant investor attention as the oil-dependent Gulf states focus more intensely on a low hydrocarbon future.

The World Bank has reduced global growth forecasts further for 2016 and 2017. Although low oil prices are theoretically beneficial for importers in Europe and Japan, their impact on producers in regions such as Asia, Latin America and the Middle East is predicted to have a continued stunting effect on business and consumer demand.

All of which means that projects will continue to come under intense scrutiny as governments and the private sector seek greater business efficiencies at every level.

Insight

Insight / June 2016 / Page three

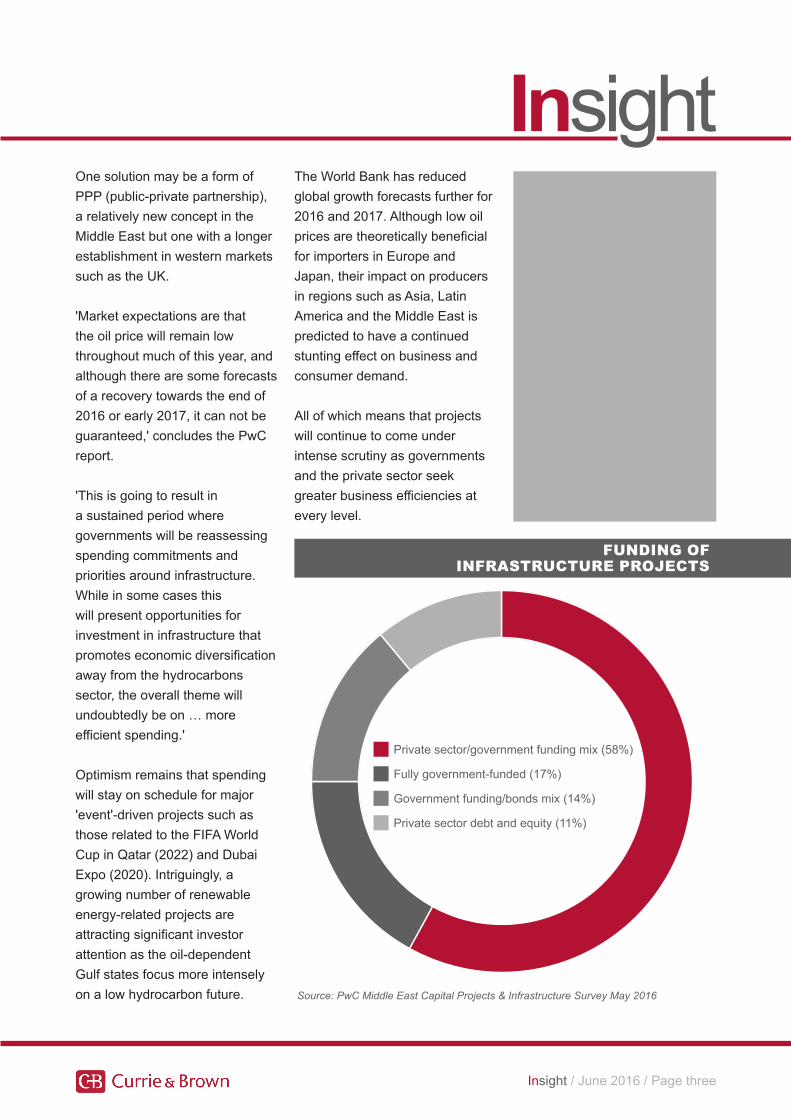

FUNDING OF INFRASTRUCTURE PROJECTS

Private sector/government funding mix (58%)

Fully government-funded (17%)

Government funding/bonds mix (14%)

Private sector debt and equity (11%)

Source: PwC Middle East Capital Projects & Infrastructure Survey May 2016

Insight

Insight / June 2016 / Page four

Regional

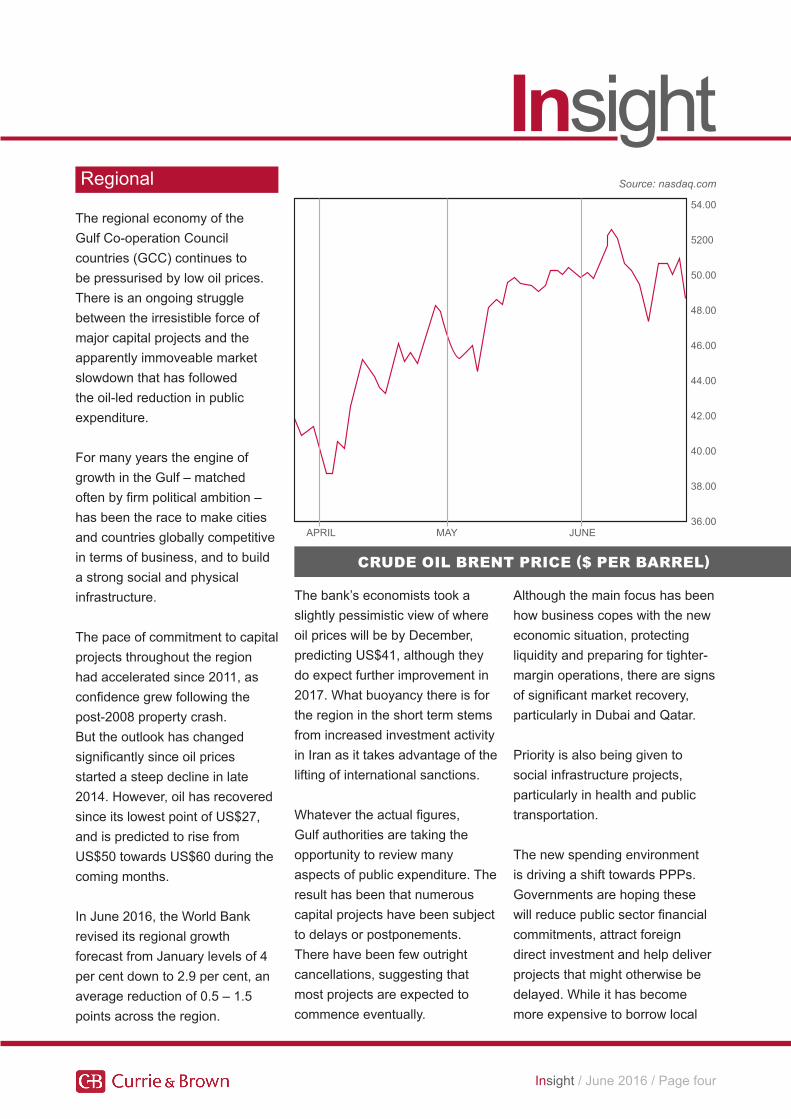

The regional economy of the Gulf Co-operation Council countries (GCC) continues to be pressurised by low oil prices. There is an ongoing struggle between the irresistible force of major capital projects and the apparently immoveable market slowdown that has followed the oil-led reduction in public expenditure.

For many years the engine of growth in the Gulf – matched often by firm political ambition – has been the race to make cities and countries globally competitive in terms of business, and to build a strong social and physical infrastructure.

The pace of commitment to capital projects throughout the region had accelerated since 2011, as confidence grew following the post-2008 property crash.But the outlook has changed significantly since oil prices started a steep decline in late 2014. However, oil has recovered since its lowest point of US$27, and is predicted to rise from US$50 towards US$60 during the coming months.

In June 2016, the World Bank revised its regional growth forecast from January levels of 4 per cent down to 2.9 per cent, an average reduction of 0.5 – 1.5 points across the region.

The bank’s economists took a slightly pessimistic view of where oil prices will be by December, predicting US$41, although they do expect further improvement in 2017. What buoyancy there is for the region in the short term stems from increased investment activity in Iran as it takes advantage of the lifting of international sanctions.

Whatever the actual figures, Gulf authorities are taking the opportunity to review many aspects of public expenditure. The result has been that numerous capital projects have been subject to delays or postponements. There have been few outright cancellations, suggesting that most projects are expected to commence eventually.

Although the main focus has been how business copes with the new economic situation, protecting liquidity and preparing for tighter-margin operations, there are signs of significant market recovery, particularly in Dubai and Qatar.

Priority is also being given to social infrastructure projects, particularly in health and public transportation.

The new spending environment is driving a shift towards PPPs. Governments are hoping these will reduce public sector financial commitments, attract foreign direct investment and help deliver projects that might otherwise be delayed. While it has become more expensive to borrow local

CRUDE OIL BRENT PRICE ($ PER BARREL)

54.00

5200

50.00

48.00

46.00

44.00

42.00

40.00

38.00

36.00APRIL MAY JUNE

Source: nasdaq.com

Insight

Insight / June 2016 / Page five

project finance, investors from outside the Gulf – especially China and Japan – are more liquid and are actively seeking deals. Qatar, Oman and Kuwait are currently involved in significant PPP planning for a range of projects.

Qatar has appointed PPP advisors and is hoping to use the option for some of its World Cup 2022 stadium developments, as well as other infrastructure investment. However, this may require changes to Qatari law, which could take time. World Cup construction to date has relied on conventional finance.

In the UAE, project contracts continue to be tendered and awarded principally in the transportation sector. Various international bidders are chasing

a US$380m contract for major concourse work at Dubai International Airport, where passenger numbers jumped 10.7 per cent to 78 million in 2015. Other construction contracts at Al-Maktoum International Airport are also in hand, such as a recent US$75 million contract for passenger terminal works, and the airport expansion is expected to remain one of the biggest projects of its kind for years to come, with total likely costs currently planned at around US$33 billion.

During the first three months of 2016, contract awards in Dubai topped US$6.6 billion, led in size by the planned Royal Atlantis resort project. Other significant contracts for the Route 2020 metro link and expansion of the Jebel Ali sewage treatment plant are expected to follow, giving the local industry greater cause for optimism.

The oil industry has continued to contract, with 5,000 job cuts at Abu Dhabi National Oil Company (ADNOC) announced in May, adding to 2,000 last January. Together these amount to more than 10 per cent of its workforce. These kind of cuts have been typical across the industry as it adjusts to the realities of lower oil prices.

Similarly, in construction, regional businesses have had to re-align. Recently, for example, Arabtec

shareholders approved a plan to use US$272 million from reserves to wipe out accumulated losses. In Saudi Arabia, the construction giant Saudi Binladen Group endured a cash crisis in the first half of 2016, and announced an asset sale to raise funds to pay protesting workers. The group laid off 70,000 people over several months. Meanwhile, the government in Riyadh introduced measures to prioritise employment for Saudi nationals.

The various major transportation schemes across the GCC – led by rail and metro systems – reflect continued population growth and the congestion caused by a heavy reliance on the automobile.Apart from environmental concerns, traffic congestion causes blight, and can hinder further development. So despite the current financial issues, the commitment of various authorities around the region seems firm, even if project timetables do slip in time.

Another area which seems resistant to downturn is healthcare, where hospitals and other projects continue apace. MEED Projects estimated recently that from 2011-15, total spending on new hospital projects totalled US$25 billion, or US$6.4 billion a year. The biggest investor, with the largest population, has been Saudi Arabia, spending more than US$18 billion over ten years,

Royal Atlantis Resort and Residences

Source: propsearch.ae

Insight

Insight / June 2016 / Page six

while the UAE spent US$8.5 billion and Kuwait US$7.6 billion.Influential factors here include the greater demand for companies to provide healthcare to employees, and also governments increasingly wanting to provide specialist services rather than sending patients abroad for major surgery and other treatments at considerable cost. Many new facilities will focus on specific areas of medicine, rather than general service.

MEED estimated recently that there are US$27 billion worth of hospital and healthcare schemes currently spread across the six states. Saudi Arabia is closely

followed by Kuwait, Qatar and the UAE. Examples include the expansion of King Abdullah Medical City in Makkah, the Kuwait Armed Forces Hospital, Sheikh Khalifa Medical City in the UAE and the Sultan Qaboos Medical City Complex in Oman – each of them costing between US$1.4 and US$1.7 billion.

Professionals with construction interests in the GCC are paying keen attention to developments in Iran, where the lifting of sanctions may be paving the way to more opportunities, as the authorities in Tehran seek to modernise its infrastructure, particularly in transport and water services.

Finally and on a brighter note, 2018 will be an exciting time for young visitors and locals in Abu Dhabi, where Warner Bros has confirmed that Warner Bros World Abu Dhabi will open its first phase that year.

The theme park, which will allow people to experience the work of DC Comics superheroes including Batman, Superman and Wonder Woman as well as cartoons such as Bugs Bunny and Tom and Jerry, will sit alongside Ferrari World and Yas Waterworld, bringing the total annual visitor number to Yas Island to 30 million, said Warner Bros.

A rendering of the theme park on Yas Island. Courtesy Miral

Warner Bros theme park is set to open in Abu Dhabi. Courtesy Miral

WARNER BROS WORLD, ABU DHABI

Source: thenational.ae

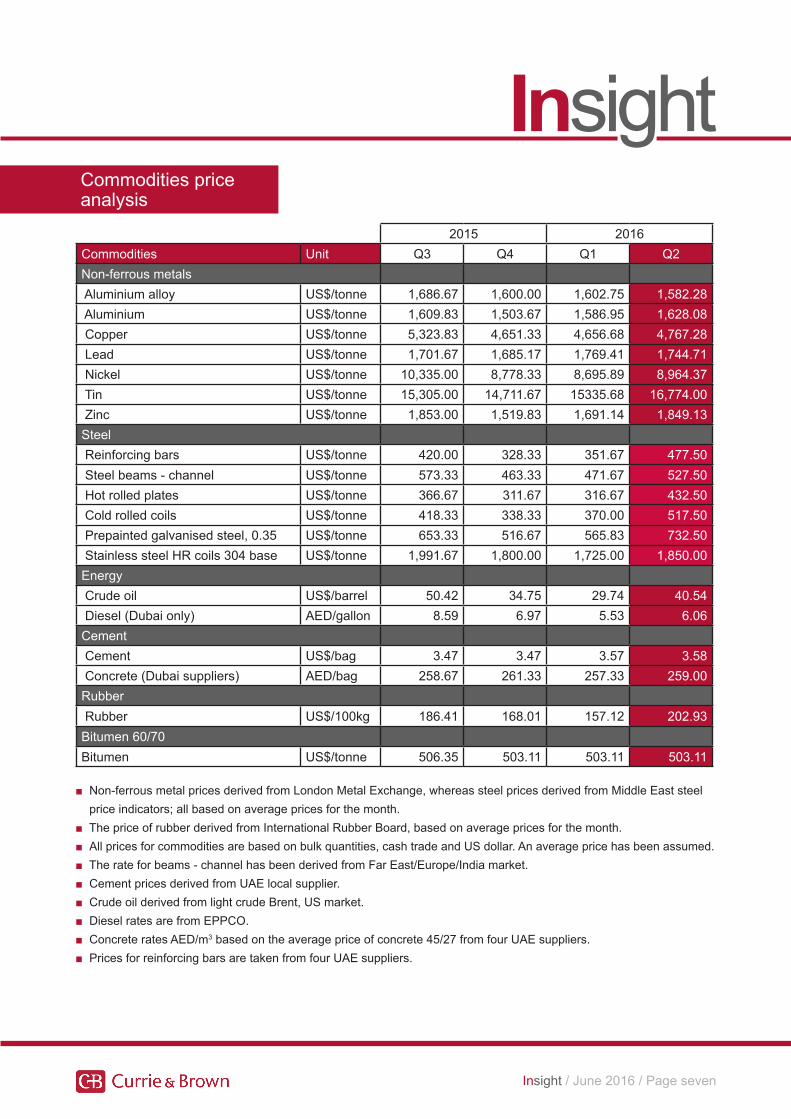

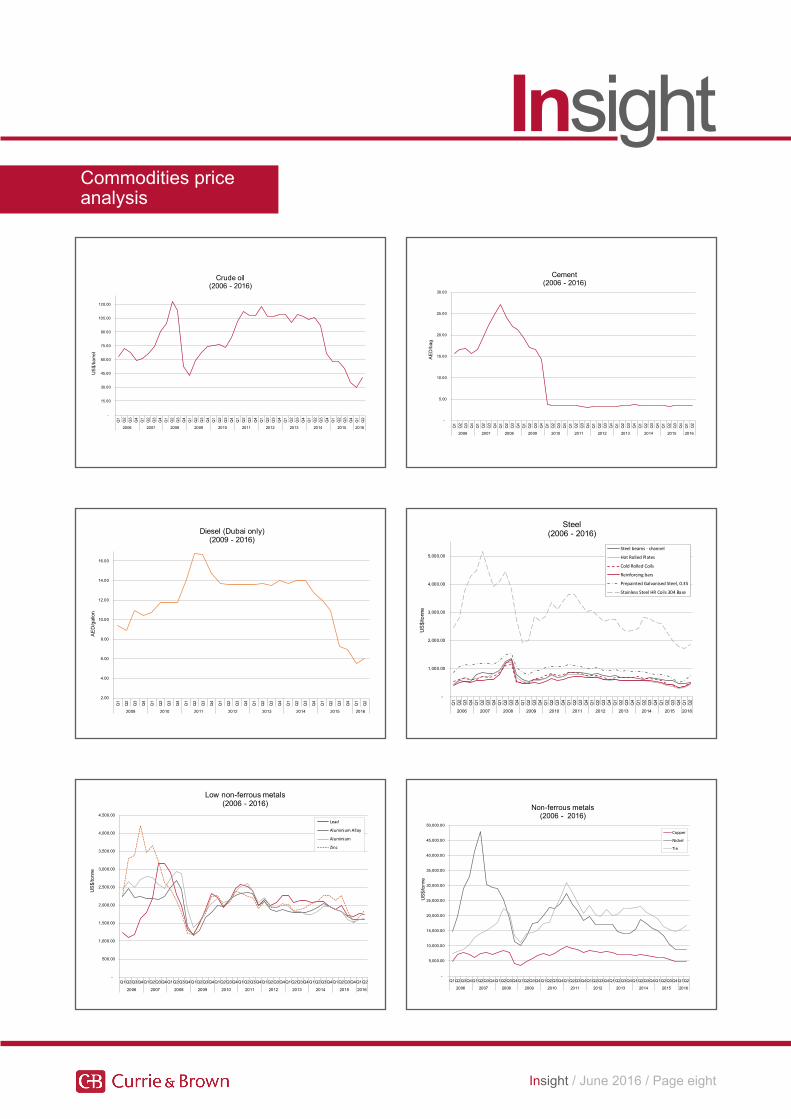

Commodities price analysis

■ Non-ferrous metal prices derived from London Metal Exchange, whereas steel prices derived from Middle East steel price indicators; all based on average prices for the month.

■ The price of rubber derived from International Rubber Board, based on average prices for the month.■ All prices for commodities are based on bulk quantities, cash trade and US dollar. An average price has been assumed.■ The rate for beams - channel has been derived from Far East/Europe/India market.■ Cement prices derived from UAE local supplier.■ Crude oil derived from light crude Brent, US market.■ Diesel rates are from EPPCO.■ Concrete rates AED/m3 based on the average price of concrete 45/27 from four UAE suppliers.■ Prices for reinforcing bars are taken from four UAE suppliers.

Insight

Insight / June 2016 / Page seven

2015 2016Commodities Unit Q3 Q4 Q1 Q2Non-ferrous metals Aluminium alloy US$/tonne 1,686.67 1,600.00 1,602.75 1,582.28 Aluminium US$/tonne 1,609.83 1,503.67 1,586.95 1,628.08 Copper US$/tonne 5,323.83 4,651.33 4,656.68 4,767.28 Lead US$/tonne 1,701.67 1,685.17 1,769.41 1,744.71 Nickel US$/tonne 10,335.00 8,778.33 8,695.89 8,964.37 Tin US$/tonne 15,305.00 14,711.67 15335.68 16,774.00 Zinc US$/tonne 1,853.00 1,519.83 1,691.14 1,849.13Steel Reinforcing bars US$/tonne 420.00 328.33 351.67 477.50 Steel beams - channel US$/tonne 573.33 463.33 471.67 527.50 Hot rolled plates US$/tonne 366.67 311.67 316.67 432.50 Cold rolled coils US$/tonne 418.33 338.33 370.00 517.50 Prepainted galvanised steel, 0.35 US$/tonne 653.33 516.67 565.83 732.50 Stainless steel HR coils 304 base US$/tonne 1,991.67 1,800.00 1,725.00 1,850.00Energy Crude oil US$/barrel 50.42 34.75 29.74 40.54 Diesel (Dubai only) AED/gallon 8.59 6.97 5.53 6.06Cement Cement US$/bag 3.47 3.47 3.57 3.58 Concrete (Dubai suppliers) AED/bag 258.67 261.33 257.33 259.00Rubber Rubber US$/100kg 186.41 168.01 157.12 202.93Bitumen 60/70Bitumen US$/tonne 506.35 503.11 503.11 503.11

Commodities price analysis

Insight

Insight / June 2016 / Page eight

-

5,000.00

10,000.00

15,000.00

20,000.00

25,000.00

30,000.00

35,000.00

40,000.00

45,000.00

50,000.00

Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Copper

Nickel

Tin

Non-ferrous metals(2006 - 2016)

US

$/to

nne

-

15.00

30.00

45.00

60.00

75.00

90.00

105.00

120.00

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Crude oil (2006 - 2016)

US

$/ba

rrel

-

5.00

10.00

15.00

20.00

25.00

30.00

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Cement (2006 - 2016)

AE

D/b

ag

-

1,000.00

2,000.00

3,000.00

4,000.00

5,000.00

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Steel beams - channel

Hot Rolled Plates

Cold Rolled Coils

Reinforcing bars

Prepainted Galvanised Steel, 0.35

Stainless Steel HR Coils 304 Base

Steel (2006 - 2016)

US

$/to

nne

-

500.00

1,000.00

1,500.00

2,000.00

2,500.00

3,000.00

3,500.00

4,000.00

4,500.00

Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2Q3Q4Q1Q2

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Lead

Aluminium Alloy

Aluminium

Zinc

Low non-ferrous metals(2006 - 2016)

US

$/to

nne

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

Q3

Q4

Q1

Q2

2009 2010 2011 2012 2013 2014 2015 2016

AE

D/g

allo

n

Diesel (Dubai only)(2009 - 2016)

SCOPE

COSTTIME

PLANPROJECT

TAKE CORRECTIVE

ACTIONS

MONITORPROGRESS

REPORT VARIANCES

Figure 1 Figure 2

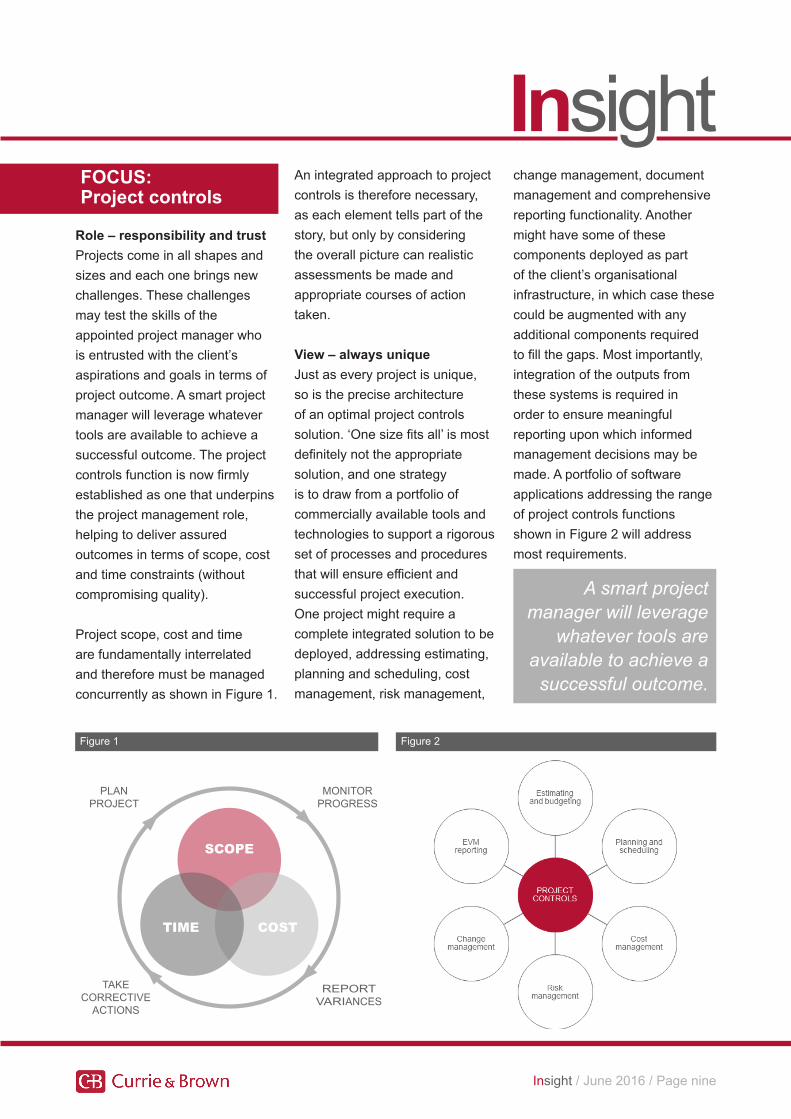

Role – responsibility and trustProjects come in all shapes and sizes and each one brings new challenges. These challenges may test the skills of the appointed project manager who is entrusted with the client’s aspirations and goals in terms of project outcome. A smart project manager will leverage whatever tools are available to achieve a successful outcome. The project controls function is now firmly established as one that underpins the project management role, helping to deliver assured outcomes in terms of scope, cost and time constraints (without compromising quality).

Project scope, cost and time are fundamentally interrelated and therefore must be managed concurrently as shown in Figure 1.

An integrated approach to project controls is therefore necessary, as each element tells part of the story, but only by considering the overall picture can realistic assessments be made and appropriate courses of action taken.

View – always uniqueJust as every project is unique, so is the precise architecture of an optimal project controls solution. ‘One size fits all’ is most definitely not the appropriate solution, and one strategy is to draw from a portfolio of commercially available tools and technologies to support a rigorous set of processes and procedures that will ensure efficient and successful project execution. One project might require a complete integrated solution to be deployed, addressing estimating, planning and scheduling, cost management, risk management,

change management, document management and comprehensive reporting functionality. Another might have some of these components deployed as part of the client’s organisational infrastructure, in which case these could be augmented with any additional components required to fill the gaps. Most importantly, integration of the outputs from these systems is required in order to ensure meaningful reporting upon which informed management decisions may be made. A portfolio of software applications addressing the range of project controls functions shown in Figure 2 will address most requirements.

FOCUS: Project controls

A smart project manager will leverage

whatever tools are available to achieve a

successful outcome.

Insight

Insight / June 2016 / Page nine

Figure 3

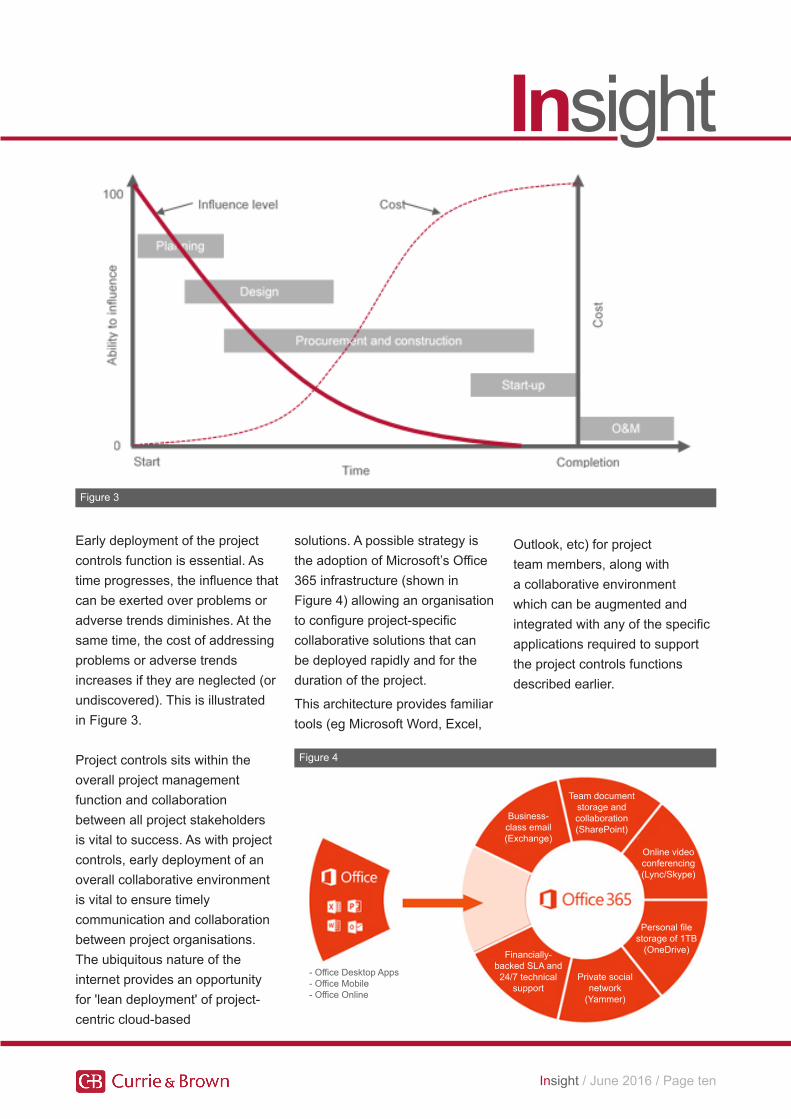

Early deployment of the project controls function is essential. As time progresses, the influence that can be exerted over problems or adverse trends diminishes. At the same time, the cost of addressing problems or adverse trends increases if they are neglected (or undiscovered). This is illustrated in Figure 3.

Project controls sits within the overall project management function and collaboration between all project stakeholders is vital to success. As with project controls, early deployment of an overall collaborative environment is vital to ensure timely communication and collaboration between project organisations. The ubiquitous nature of the internet provides an opportunity for 'lean deployment' of project-centric cloud-based

solutions. A possible strategy is the adoption of Microsoft’s Office 365 infrastructure (shown in Figure 4) allowing an organisation to configure project-specific collaborative solutions that can be deployed rapidly and for the duration of the project.

This architecture provides familiar tools (eg Microsoft Word, Excel,

Outlook, etc) for project team members, along with a collaborative environment which can be augmented and integrated with any of the specific applications required to support the project controls functions described earlier.

Insight

Insight / June 2016 / Page ten

Business-class email(Exchange)

Team document storage and collaboration (SharePoint)

Online video conferencing(Lync/Skype)

Personal file storage of 1TB

(OneDrive)

Private social network

(Yammer)

Financially-backed SLA and

24/7 technical support

- Office Desktop Apps- Office Mobile- Office Online

Figure 4

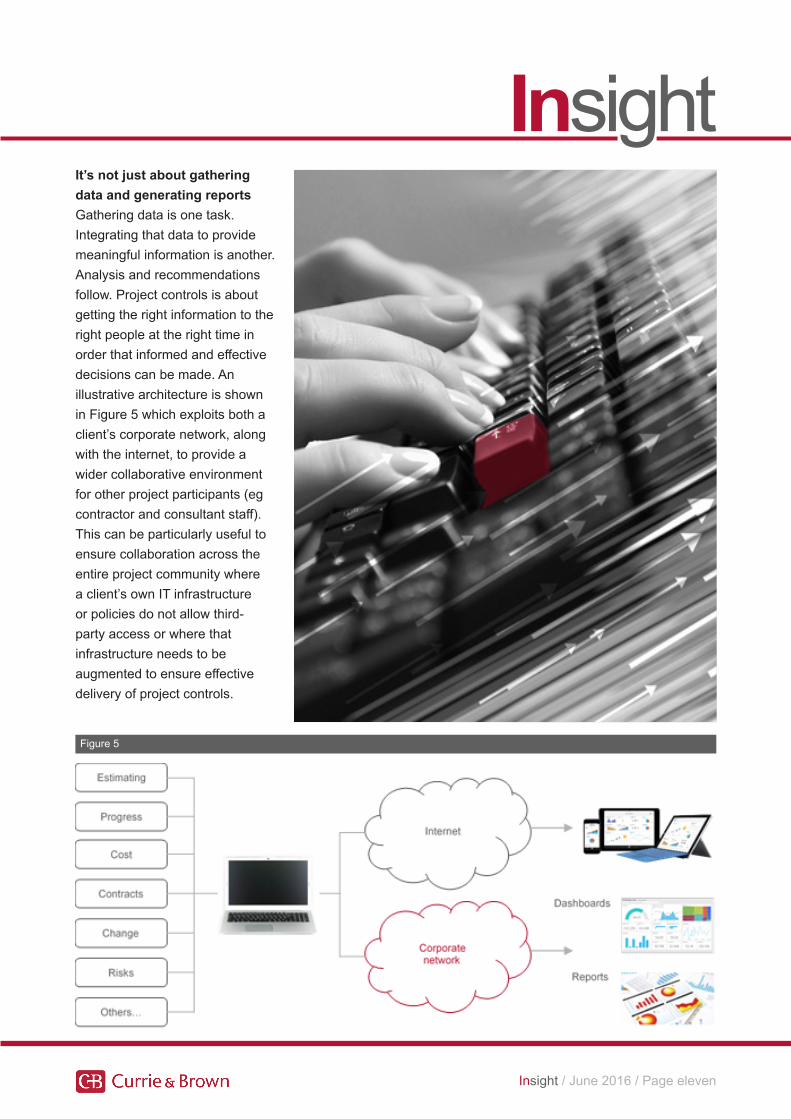

It’s not just about gathering data and generating reportsGathering data is one task. Integrating that data to provide meaningful information is another. Analysis and recommendations follow. Project controls is about getting the right information to the right people at the right time in order that informed and effective decisions can be made. An illustrative architecture is shown in Figure 5 which exploits both a client’s corporate network, along with the internet, to provide a wider collaborative environment for other project participants (eg contractor and consultant staff). This can be particularly useful to ensure collaboration across the entire project community where a client’s own IT infrastructure or policies do not allow third-party access or where that infrastructure needs to be augmented to ensure effective delivery of project controls.

Insight

Insight / June 2016 / Page eleven

Figure 5

AUSTRALIA

Brisbane T +61 7 3835 8555

MelbourneT +61 3 9691 0000

SydneyT +61 2 8220 0800

CHANNEL ISLANDS

JerseyT +44 (0)1534 720 326

CHINA

BeijingT +86 10 6523 1550

ChangshaT +86 731 8281 2560

ChengduT +86 28 8200 8618

ChongqingT +86 23 8672 9088

GuangzhouT +86 20 3877 3990

ShanghaiT +86 21 6426 3883

ShenyangT +86 24 3109 9079

ShenzhenT +86 755 8301 8156

WuhanT +86 27 8580 2996

FRANCE

ParisT +33 (1)55 04 74 10

HONG KONG

Hong KongT +852 2833 1939

INDIA

BangaloreT +91 80 4116 2435

ChennaiT +91 44 4116 2435T +91 44 4393 1300

MumbaiT +91 22 6574 9550

New DelhiT +91 11 2612 4372

JAPAN

TokyoT +81 3 3442 6642

MEXICO

Mexico CityT +52 55 52 81 5588

OMAN

MuscatT +968 244 83417

QATAR

DohaT +974 4434 0048/49

SINGAPORE

SingaporeT +65 6221 7288

TAIWAN

TaipeiT +886 2 2555 5886

THAILAND

BangkokT +66 2 632 6500

UNITED ARAB EMIRATES

Abu DhabiT +971 2 671 6265

DubaiT +971 4 295 5198

UNITED KINGDOM

AberdeenT +44 (0)845 287 8500

CumbriaT +44 (0)845 287 8620

EdinburghT +44 (0)845 287 8500

GlasgowT +44 (0)845 287 8500

Haywards HeathT +44 (0)845 287 8764

LondonT +44 (0)845 287 8800

ManchesterT +44 (0)845 287 8626

Milton KeynesT +44 (0)845 287 8700

PlymouthT +44 (0)845 287 8475

PortsmouthT +44 (0)845 287 8400

UNITED STATES

Phoenix, Arizona T +1 602 748 1470

San Francisco, CaliforniaT +1 415 518 7511

Princeton, New JerseyT +1 609 759 7000

Albuquerque, New MexicoT +1 505 563 5890

Portland, Oregon T +1 503 547 0316

Currie & Brown offices

Insight / June 2016 / Page twelve