Inox Leisure Limitedcdn.inoxmovies.com/Downloads/8cc0393e-b4e1-4e1f-84a6-45...INOX –a diversified...

23

Inox Leisure Limited Investor Presentation – Q4 and FY14 June 2014

Transcript of Inox Leisure Limitedcdn.inoxmovies.com/Downloads/8cc0393e-b4e1-4e1f-84a6-45...INOX –a diversified...

Inox Leisure LimitedInvestor Presentation – Q4 and FY14

June 2014

INOX – a diversified business group with market leadership

2

Privately held

India’s largest cryogenic

engineering company,

amongst the world’s

largest

Manufacturing facilities

in India, US, Canada,

Brazil and China

Listed on BSE and NSE

49% subsidiary of GFL

India’s largest

integrated multiplex

chain

Currently operates 79

properties in 43 cities

comprising of 310

screens and 83,809

seats

Listed on BSE and NSE

India’s largest

manufacturer of

refrigerants,

chloromethanes &

PTFE

Carbon credit revenues

utilized to build strong

businesses

Subsidiaries in 3

countries, JVs in 2

80 year track record of ethical business growth

Diversified, professionally managed business group

22 companies (including two listed, 7 international subsidiaries, and 5 joint ventures – of which 3 international)

10 different businesses

Gross block over Rs 7,000 crores, Gross revenues over Rs 5,000 crores

More than 100 business units across India, employing more than 10,000 people

50:50 joint venture with

Air Products and

Chemicals Inc(USA), a

Fortune 500 Company

India’s largest industrial

gas manufacturer –

around 40 plants across

the country

75% subsidiary of GFL

Fully integrated wind

turbine manufacturer

with state of the art

facilities for nacelles,

blades, towers, and

hubs

India’s fastest growing

and amongst largest

wind farm solutions

provider

100% subsidiary of GFL

Wind farm operator with

around 200 MW of

operational wind farms,

with another 100 MW

under construction,

across 4 different

States

Market leadership across almost all businesses

Indian Movie Exhibition Business

3

Immense opportunity for large, organized players

Organized Retail

on Overdrive

Organized retail is expected to grow at a rapid rate of 19-20% CAGR over the next 5 years

o As of 2013, only 7.5% of the $520 bn retail market in India was organized

o Organized retail expected to be 10% share of total retail by 2018.

o Favorable regulatory environment – 51% FDI permitted in multi brand retail

o Real Estate sector more organized – huge development in malls and commercial properties

Large Malls need anchor tenants – strong preference for Multiplexes

Vibrant

Domestic Box

Office

Domestic theatrical accounts for 75% of total film industry revenues in 2013

Box Office collections estimated to grow at 11.4% CAGR from Rs 93 bn in 2013 to Rs 160 bn in 2018

Multiple drivers for box office growth –

o Digital Cinema enabled wide releases Larger box office collections Film Distributors

enjoying large profits Larger investments Quality content pipeline

o Younger demographics and increasing discretionary spends especially on entertainment

o Limited alternative entertainment options

o Movie going is a social activity

Underpenetrated

multiplex market

India is a severely under-served market with low screen density (8 screens / mn vs. 117 in US)

Multiplex screens account for just 25% of total screens

Latent demand in several markets for quality movie going experience

Large Movie

Industry

~ 1000 movies released per annum

~ 5 billion tickets sold annually

Quality content across genres and languages

Source: FICCI KPMG Report 2014; Pulse of Indian Retail Market - EY Report 2014; Research Reports

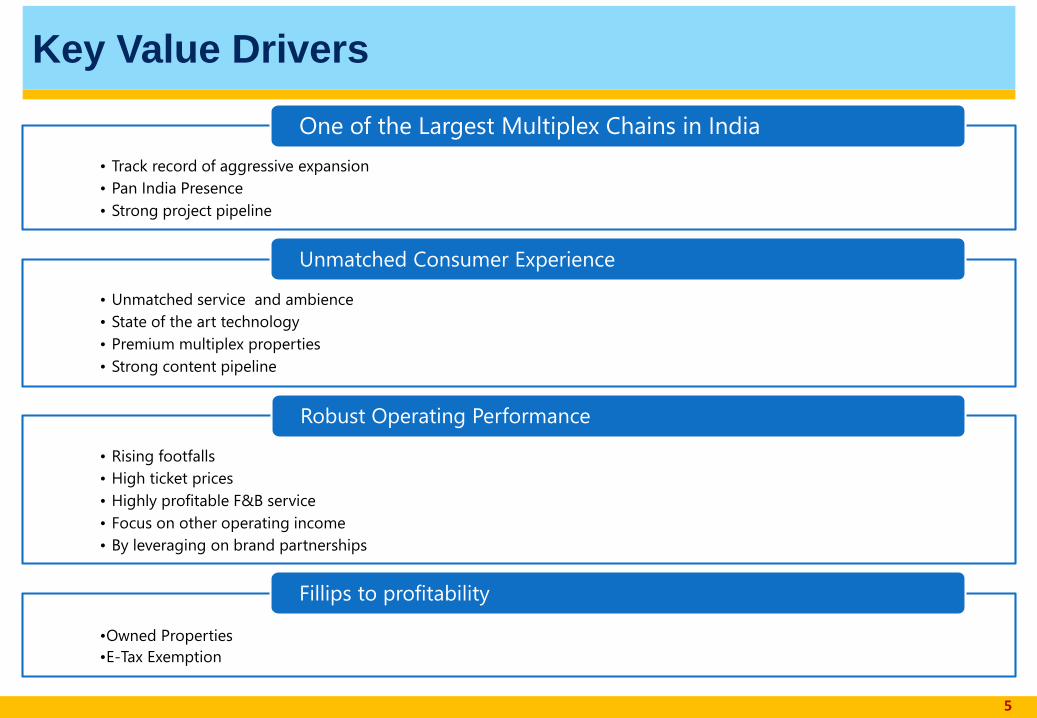

One of the Largest Multiplex Chains in India

4

14 States43 Cities

79 Multiplexes310 Screens83809 Seats

40 million patrons *

TAMILNADU3 Properties | 14 Screens

KARNATAKA 9 Properties | 34 Screens

GOA 1 Properties | 4 Screens

ANDHRA PRADESH 7 Properties | 31 Screens

MAHARASTRA 19 Properties |76 Screens

GUJARAT

6 Properties |25 Screens

RAJASTHAN

7 Properties |22 Screens

HARYANA 3 Properties | 10 Screens S

MADHYA PRADESH 3 Properties | 11 Screens

UTTAR PRADESH 3 Properties | 13 Screens

JHARKHAND 1 Properties | 4 Screens

WEST BENGAL 14 Properties |55 Screens

CHHATTISGARH 2 Properties | 8 Screens

ORISSA 1 Properties |3 Screens

* FY14 including Management Properties

• Track record of aggressive expansion

• Pan India Presence

• Strong project pipeline

One of the Largest Multiplex Chains in India

• Unmatched service and ambience

• State of the art technology

• Premium multiplex properties

• Strong content pipeline

Unmatched Consumer Experience

• Rising footfalls

• High ticket prices

• Highly profitable F&B service

• Focus on other operating income

• By leveraging on brand partnerships

Robust Operating Performance

•Owned Properties

•E-Tax Exemption

Fillips to profitability

Key Value Drivers

5

FY03 FY04 FY05 FY06 FY07 FY08 FY09 FY10 FY11 FY12 FY13 FY14

Track Record of Aggressive Expansion

6

On average, added two properties every quarter over the last decade

2 Prop.

8 Screens

3 Prop.

12 Screens

6 Prop.

25 Screens

9 Prop.

35 Screens

14 Prop.

51 Screens

22 Prop.

76 Screens

26 Prop.

91 Screens

32 Prop.

119 Screens

63 Prop.

239 Screens

68 Prop.

257 Screens

74 Prop.

285 Screens

79 Prop.

310 Screens

SURAT

VIZIANAGARAM

KALKA

RAIPUR

JAIPUR

MADURAI

GREATER NOIDA

KOLKATA

MANIPAL

HYDERABAD

NAVI MUMBAI

PUNE

(Amanora)

BHUBANESWAR

UDAIPUR

BHOPAL

LILUAH

SILIGURI

(CC)

Vijaywada

(LEPL)

------------

2 FAME

Properties

VIZAG (CMR)

BANGALORE

(Mantri Sq)

BELGAUM

JAIPUR

(Raja Park)

KANPUR

BANGALORE

(J.P.Nagar)

--------------------

25 FAME Properties

HYDERABAD

SILIGURI

KOLKATA

(Rajarhat)

INDORE

(Central Mall)

THANE

VIZAG

(Beach Road)

FARIDABAD

NAGPUR

(Jaswant Tuli)

BANGALORE

(Swagath)

BURDWAN

BHARUCH

DURGAPUR

JAIPUR

(Crystal Palm)

LUCKNOW

RAIPUR

KOLKATA

(Swabhumi)

VIJAYWADA

DARJEELING

KOTA

NAGPUR

(Wardhaman Nagar)

CHENNAI

JAIPUR

(Bani Park)

KOLKATA

(Salt Lake)

GOA

MUMBAI

(Nariman Point)

KOLKATA

(Elgin Road)

PUNE

VODADARA

BANGALORE

(Magrath Road)

JAIPUR

(Vaishali Ngr)

INDORE

(Sapna Sangeeta)

IPO

Acquisition

of 89

Cinemas

Acquisition

of Fame

India

Includes 6 Managed Properties with 20 screens

Pan India Presence

7

Cities Properties

Well distributed mix of properties

Screens Seats

East, 9West, 16

South, 9

North, 9

East, 18 West, 29

South, 19North, 13

East, 70 West, 116

South, 79

North, 45

East, 18631 West, 33817

South, 19320

North, 12041

Strong Project Pipeline

8

FY14

FY15

Sl No City No of screens Launch Date

1 Surat 8 11th Jul 2013

2 Vizianagaram 3 29th Jul 2013

3 *Kalka 3 17th Sep 2013

4 *Raipur 4 5th Oct 2013

5 Jaipur 3 23rd Dec 2013

6 Madurai 5 24th Dec 2013

7 Greater Noida 5 14th Feb 2014

8 Kolkatta 6 7th Mar 2014

9 Manipal 3 31st Mar 2014

Total screens 40

Sl No City No of screens Est. Launch

1 Vizag 5 Q1 FY15

2 Jamnagar 5 Q1 FY15

3 Jalgoan 4 Q1 FY15

4 Gurgaon 3 Q1 FY15

5 Faridabad 3 Q2 FY15

6 Lucknow 4 Q2 FY15

7 Ajmer 3 Q3 FY15

8 Kurnool 3 Q3 FY15

9 Pune 6 Q3 FY15

10 *Bhiwadi 3 Q3 FY15

11 Jaipur 4 Q3 FY15

12 Vijayawada 3 Q4 FY15

13 Thrissur 6 Q4 FY15

14 Kota 4 Q4 FY15

15 Jammu 3 Q4 FY15

16 Bangalore 5 Q4 FY15

17 Goa 4 Q4 FY15

18 Mangalore 8 Q4 FY15

19 Cuttack 4 Q4 FY15

20 Vadodara 3 Q4 FY15

Total Screens 83

*Management properties

Unmatched Service and Ambience

9

Ambience World class ambience

Emphasis on safety, comfort and convenience

Video Quality

Setup own high quality DCI Compliant 2K Digital Projection Systems across

locations to ensure world class cinematic experience

High definition picture quality

3D enabled

High frame rate (HFR) ready (can go up to 60 fps)

Audio Quality Early adopters of Dolby ATMOS sound technology

Excellent acoustic systems

Distortion free sound

Programming

Experienced Programming Team

Wide variety of movies catering to different genres and tastes

Theatre management system installed in every unit allows flexibility in

programming

State of the Art Technology

10

First multiplex chain in the country to co-develop an Integrated ERP software

Focus on ensuring transparency to all business partners (regulatory agencies and distributors)

End of day data availability allows for performance analysis and better management control

Automated DCR (Daily Collection Reports) sent to regulatory agencies and distributors - no

manual intervention for report generation and hence no room for errors, complete transparency

Setup NOC in Mumbai that enables management team to continuously monitor, control and

report information on digital systems across the country

Real time programming changes

Dynamic on screen ad scheduling from NOC

Premium Multiplex Properties

11

PUNE AMANORA KOLKATA QUEST GREATER NOIDA

BHOPAL MUMBAI INORBIT SURAT

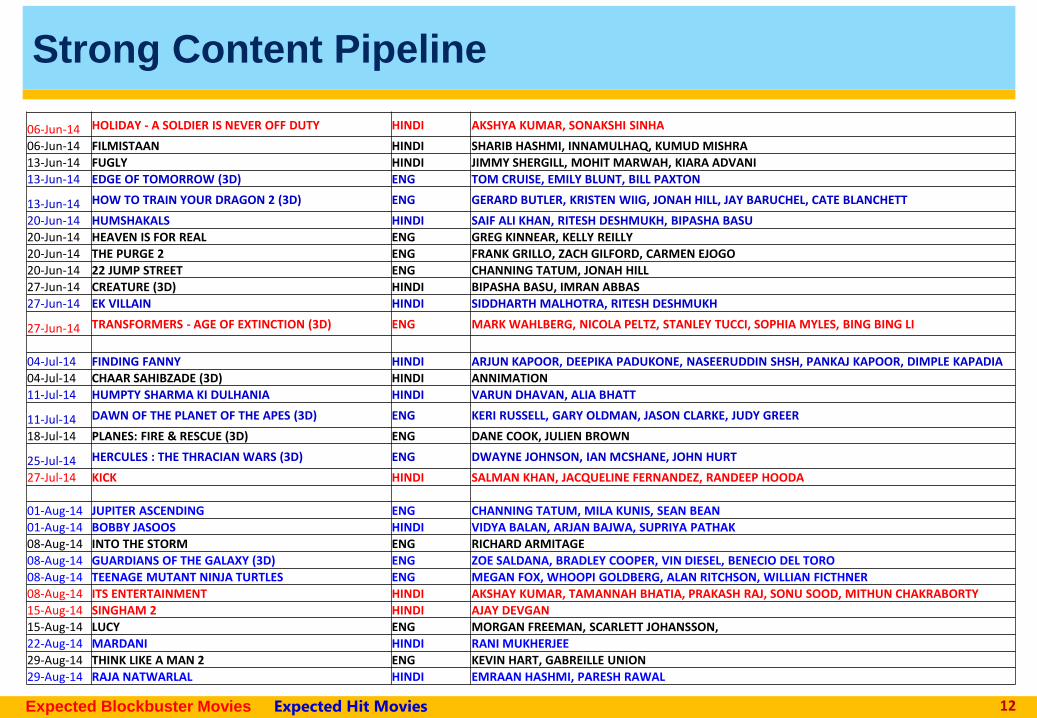

Strong Content Pipeline

12Expected Blockbuster Movies Expected Hit Movies

06-Jun-14 HOLIDAY - A SOLDIER IS NEVER OFF DUTY HINDI AKSHYA KUMAR, SONAKSHI SINHA

06-Jun-14 FILMISTAAN HINDI SHARIB HASHMI, INNAMULHAQ, KUMUD MISHRA

13-Jun-14 FUGLY HINDI JIMMY SHERGILL, MOHIT MARWAH, KIARA ADVANI

13-Jun-14 EDGE OF TOMORROW (3D) ENG TOM CRUISE, EMILY BLUNT, BILL PAXTON

13-Jun-14 HOW TO TRAIN YOUR DRAGON 2 (3D) ENG GERARD BUTLER, KRISTEN WIIG, JONAH HILL, JAY BARUCHEL, CATE BLANCHETT

20-Jun-14 HUMSHAKALS HINDI SAIF ALI KHAN, RITESH DESHMUKH, BIPASHA BASU

20-Jun-14 HEAVEN IS FOR REAL ENG GREG KINNEAR, KELLY REILLY

20-Jun-14 THE PURGE 2 ENG FRANK GRILLO, ZACH GILFORD, CARMEN EJOGO

20-Jun-14 22 JUMP STREET ENG CHANNING TATUM, JONAH HILL

27-Jun-14 CREATURE (3D) HINDI BIPASHA BASU, IMRAN ABBAS

27-Jun-14 EK VILLAIN HINDI SIDDHARTH MALHOTRA, RITESH DESHMUKH

27-Jun-14 TRANSFORMERS - AGE OF EXTINCTION (3D) ENG MARK WAHLBERG, NICOLA PELTZ, STANLEY TUCCI, SOPHIA MYLES, BING BING LI

04-Jul-14 FINDING FANNY HINDI ARJUN KAPOOR, DEEPIKA PADUKONE, NASEERUDDIN SHSH, PANKAJ KAPOOR, DIMPLE KAPADIA

04-Jul-14 CHAAR SAHIBZADE (3D) HINDI ANNIMATION

11-Jul-14 HUMPTY SHARMA KI DULHANIA HINDI VARUN DHAVAN, ALIA BHATT

11-Jul-14 DAWN OF THE PLANET OF THE APES (3D) ENG KERI RUSSELL, GARY OLDMAN, JASON CLARKE, JUDY GREER

18-Jul-14 PLANES: FIRE & RESCUE (3D) ENG DANE COOK, JULIEN BROWN

25-Jul-14 HERCULES : THE THRACIAN WARS (3D) ENG DWAYNE JOHNSON, IAN MCSHANE, JOHN HURT

27-Jul-14 KICK HINDI SALMAN KHAN, JACQUELINE FERNANDEZ, RANDEEP HOODA

01-Aug-14 JUPITER ASCENDING ENG CHANNING TATUM, MILA KUNIS, SEAN BEAN

01-Aug-14 BOBBY JASOOS HINDI VIDYA BALAN, ARJAN BAJWA, SUPRIYA PATHAK

08-Aug-14 INTO THE STORM ENG RICHARD ARMITAGE

08-Aug-14 GUARDIANS OF THE GALAXY (3D) ENG ZOE SALDANA, BRADLEY COOPER, VIN DIESEL, BENECIO DEL TORO

08-Aug-14 TEENAGE MUTANT NINJA TURTLES ENG MEGAN FOX, WHOOPI GOLDBERG, ALAN RITCHSON, WILLIAN FICTHNER

08-Aug-14 ITS ENTERTAINMENT HINDI AKSHAY KUMAR, TAMANNAH BHATIA, PRAKASH RAJ, SONU SOOD, MITHUN CHAKRABORTY

15-Aug-14 SINGHAM 2 HINDI AJAY DEVGAN

15-Aug-14 LUCY ENG MORGAN FREEMAN, SCARLETT JOHANSSON,

22-Aug-14 MARDANI HINDI RANI MUKHERJEE

29-Aug-14 THINK LIKE A MAN 2 ENG KEVIN HART, GABREILLE UNION

29-Aug-14 RAJA NATWARLAL HINDI EMRAAN HASHMI, PARESH RAWAL

23%25%

28%32% 33%

27%

23%

28%

Rising Footfalls

13

Quality content driving Occupancy rates Expansion driving total footfalls

(millions)

o Convenient locations / Good catchment areas

o Good mix of Hollywood, Bollywood and Regional movies

o“Virtuous cycle” in movie business

Quality content leading to strong box office collections

There were 6 movies over Rs.100 crs.(NBOC) and 2 movies over Rs.200 crs.(NBOC) in 2013

Higher profitability enabling large investments by film producers / distributors

Note: Excludes Managed properties

25.730.7

35.3

10.7 10.8 8.8 8.2

38.6

152

156

160

153

156

163

153

156

High Ticket Prices (ATP)

14

ATP Trend

o Inox brand enjoys a premium positioning amongst urban consumers

o Prime locations provide strong pricing power

o Increasing contribution of 3D movies – 3D tickets are priced at a premium of 15-20 % over 2D tickets

Note: Excludes Managed properties

32% 31% 30%27% 27%

25% 24%26%

41 44 47 49 48 51 49 49

Highly Profitable F&B Service

15

SPH Growth – overall

o Multiple initiatives on increasing the highly profitable F&B revenues (74% Gross margins)

Unique variety of food with choice of International, Indian and City-Centric special flavors

No menu fatigue - Variety in menu for week days and week ends

Season specific food festivals

Investment in quality machines to serve best pop corn

o Contribution of F&B revenues to net revenues increased from 18% to 21% over last 4 years

Note: Excludes Managed properties

F&B Cost (% of F&B revenues)

172 292 32478 110 146 161

495167

299 323

143 136 190 135

604

Ad Revenue Other Operating Revenue

Focus on Other Operating Income

16

Other operating revenues

Significant scope for enhancement of high margin other

operating revenues

Pan India Reach

Premium positioning

Good locations

Several initiatives have been taken up to focus on better monetization

Ad Revenues

Hiked Ad rates

Focus on high value / long term deals

Sales to Leading corporates

DAVP / Government Segment

Off-screen advertising

Other Revenues

Virtual Print Fee

Online booking revenues

Conducting Fee

(Rs million)

By Leveraging Brand Partnerships

17

Owned Properties

18

City / Property State Screens Seats Total Area (sft)

Multiplex Area

(sft)

Pune Maharashtra 4 1316 140,229 53,189

Vadodara Gujarat 4 1318 109,452 48,622

Nariman Point, Mumbai Maharashtra 5 1323 40,131 40,131

Jaipur Rajasthan 2 787 26,392 26,392

Swabhumi , Kolkatta West Bengal 4 1022 46,204 46,204

Anand Gujarat 3 624 27,871 27,871

Corporate Office Maharashtra - - 16,000 -

o Owned properties in prime locations enable savings in lease expense, thereby boosting EBITDA

E-Tax Exemption

19

E-Tax No. of prop Screens Seats

Average Residual

Period

Full Tax 55 225 59,953

Exempted 11 43 12,039 2 years

Zero Tax 7 22 6,148

• Tax incentives such as e-tax exemptions enable faster recovery of capital cost and

reduced exhibition cost

• E-tax exemption treated as capital receipt – no income tax on the amount

Annexure I - Key Management Personnel

20

Mr. Pavan Jain

Mr. Vivek Jain

Mr. Deepak Asher

Mr. Siddharth Jain

Mr. Haigreve

Khaitan

Mr. Amit Jatia

Mr. Kishore Biyani

Board of Directors Key Management Personnel

Mr. Alok Tandon

(CEO)

Mr. Muralikrishna

(CPO)

Mr. Rajender Singh

(VP – Programming)

Mr. Upen Shah

(CFO)

Mr. Harshavardhan

Gangurde

(VP-Marketing)

Mr. Uday Sakharkar

(VP – Projects)

Mr. Jitender Verma

(CTO)

Ms. Daizy Lal

(COO)

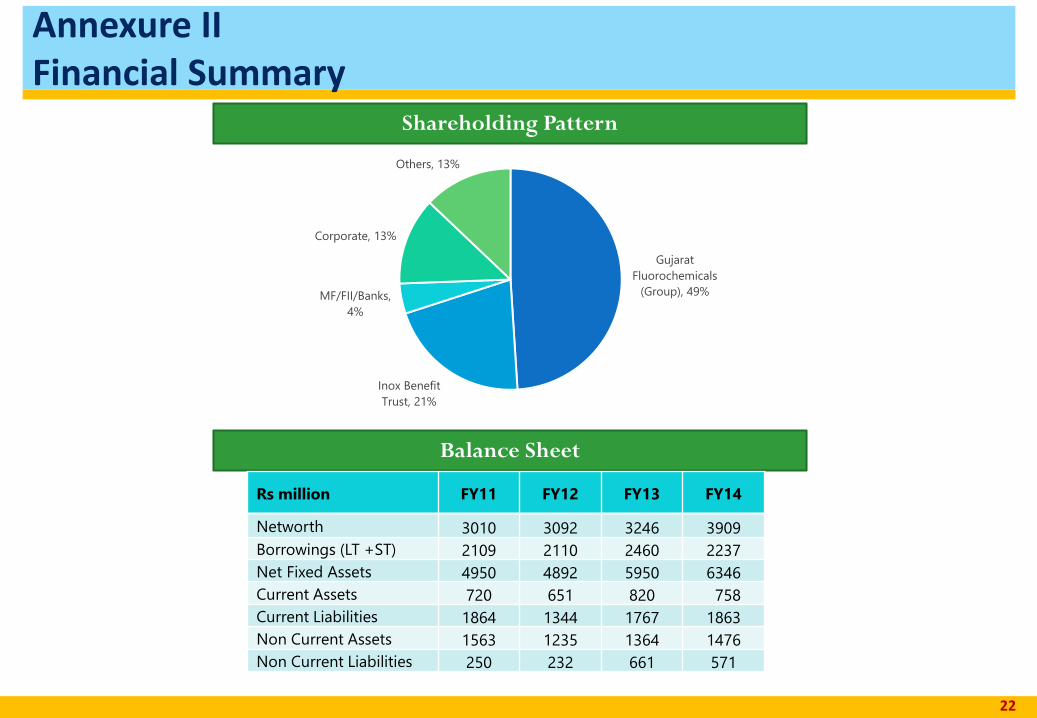

Annexure II Financial Summary

21

Profit and Loss Statement

Rs million FY11 FY12 FY13 Q1 FY14 Q2 FY14 Q3 FY14 Q4 FY14 FY14

Net Box Office 2269 3889 4567 1332 1378 1171 1024 4905

F&B Revenues 602 1139 1418 451 447 383 342 1623

Ad Revenues172 292 324 78 110 146 161 495

Other Revenues224 380 359 151 141 205 197 694

Total Revenues3,267 5,700 6,668 2,012 2,076 1905 1724 7717

Distributor Share1029 1803 2099 604 622 545 464 2235

F&B Cost195 349 426 135 132 107 92 466

Payroll Cost 261 394 427 116 117 139 123 495

Other Expenses1417 2344 2700 765 796 830 821 3212

Total Expenses2,902 4,890 5,652 1,620 1,667 1621 1500 6408

EBITDA365 810 1016 392 409 285 224 1309

EBITDA Margin (%)11.17% 14.21% 15.24% 19.48% 19.70% 14.93% 12.97% 16.96%

Depreciation229 375 430 121 128 130 128 507

Interest162 243 267 73 74 66 63 276

Exceptional Items -56 180 25 4 4

Tax-1 27 109 55 59 24 15 153

Minority share in loss 19 57 0

PAT50 42 185 143 148 65 14 369

Annexure IIFinancial Summary

22

Shareholding Pattern

Balance Sheet

Rs million FY11 FY12 FY13 FY14

Networth 3010 3092 3246 3909

Borrowings (LT +ST) 2109 2110 2460 2237

Net Fixed Assets 4950 4892 5950 6346

Current Assets 720 651 820 758

Current Liabilities 1864 1344 1767 1863

Non Current Assets 1563 1235 1364 1476

Non Current Liabilities 250 232 661 571

Gujarat

Fluorochemicals

(Group), 49%

Inox Benefit

Trust, 21%

MF/FII/Banks,

4%

Corporate, 13%

Others, 13%

THANK YOU

Inox Leisure Limited

ABS Towers, Old Padra Road,

Vadodara, Gujarat – 390 007

![Inox Leisure Limitedcdn.inoxmovies.com/Downloads/Investor Presentation... · ^dZ] presentation includes forward-looking statements which deal with future events, including those relating](https://static.fdocuments.us/doc/165x107/5ae28bb77f8b9a5b348c60b7/inox-leisure-presentationdz-presentation-includes-forward-looking-statements.jpg)